Abstract

This study explores firm responses to stakeholder-initiated involuntary disclosures, which are disclosures made by stakeholders about an organization but are against the will of managers, and subsequent stakeholder reactions. We analyzed 134,977 firm Twitter replies from seven companies to identify their responses to involuntary corporate social responsibility (CSR) disclosures and find that companies demonstrate different attitudes toward engagement in the exchange about involuntary disclosures. Whereas some companies communicate with stakeholders, others are almost silent. When a company engages in communication with its stakeholders, the communication is mostly one-way, and mortification or dissent is the likely response strategy. We also find that while stakeholders generally do not continue to engage with corporate communications, they are likely to respond when companies deny the information revealed by involuntary disclosure. Our results suggest that involuntary disclosures on social media are not able to improve communication between stakeholders and companies.

Introduction

Traditionally, a company communicates corporate social responsibility (CSR) information through official documents, such as annual reports, CSR reports or press releases, and sections of its official corporate website dedicated to nonfinancial issues. CSR has been defined in different ways but generally relates to the responsibilities of an organization beyond its benefits and profits (Carroll, 1999; Waddock, 2004). At a minimum, CSR focuses on how companies manage their economic, social, and environmental impacts and their relationships and negotiations with different stakeholder groups and society at large (Ihlen et al., 2011). The development of internet technologies and the spread of social media (SM) platforms—such as social networks, blogs, microblogs, and other internet platforms—have the potential to transform how companies communicate with stakeholders.

SM can also foster stakeholder engagement because it offers stakeholders a platform upon which they can interact with each other and with companies. Stakeholders may use SM to engage with a company—they can praise, criticize, and question its decisions and actions and even call for action such as banning. A body of research exists that investigates both how firms use SM to interact with stakeholders (Bellucci & Manetti, 2017; Castelló et al., 2013; Gómez-Carrasco & Michelon, 2017; Manetti et al., 2021; Okazaki et al., 2020; Saxton et al., 2019; Saxton et al., 2021; Whelan et al., 2013) and vice versa (Gómez-Carrasco & Michelon, 2017; Okazaki et al., 2020; Saxton et al., 2019).

SM allows stakeholders to express their views and expectations of a company (Bellucci et al., 2019)—not only as a reaction to corporate communications but also as a source of independent information about a company. Dumay and Guthrie (2017) define this type of information as involuntary disclosure, as through this type of disclosure, information is involuntarily revealed against the will of managers. Involuntary disclosures could be used, for instance, to highlight or denounce some facts related to the social or environmental activities of a company. Stakeholders may want to disclose such information in this way because they otherwise have limited abilities to influence firms. A well-known example of an involuntary disclosure was one made by a whistleblower inside the Volkswagen Group. As a result, in September 2015 the U.S. Environmental Protection Agency accused Volkswagen of installing illegal “defeat device” software that dramatically reduced emissions. The involuntary disclosure resulted in a share price decrease of more than 30% and led to significant reputational damage (Dumay & Guthrie, 2017). Michael Horn, head of Volkswagen America, admitted “We’ve totally screwed up,” while the group’s CEO, Martin Winterkorn, admitted that the company had “broken the trust of our customers and the public” (Hotten, 2015).

The objective of our study is to examine stakeholder-initiated communication dynamics after involuntary information is disclosed on SM by analyzing firms’ attempts to manage such communication and stakeholder reactions to these efforts. Specifically, we investigate how firms use rhetorical strategies and the types of language they use in their replies to involuntary disclosures. We then analyze stakeholders’ subsequent reactions to firm responses to involuntary disclosures. We focus our attention on Twitter, as this microblogging and social networking service seems to be the most popular for business communication (Okazaki et al., 2020).

In our empirical analysis, we focus on a data set of 134,977 Twitter replies made by seven large companies (Dell Technologies, H&M Group, Intel Corporation, Nestlé, Danone, Hewlett–Packard [HP], and General Electric [GE]) that engage in corporate communication on Twitter and are well known for their CSR programs. We first identified 4,644 firm replies in response to stakeholders’ involuntary disclosures. We then coded and analyzed the types of rhetorical strategies and language used in these replies. Finally, we analyzed stakeholders’ reactions to the strategies employed by the firms to address involuntary CSR disclosures.

Our article contributes to the existing literature in two distinct ways. First, it brings to light a specific disclosure type made by stakeholders—involuntary disclosures—which may be considered a potential mechanism leading to sustainable changes within the firm (Dumay & Guthrie, 2017). To date, most of the literature has focused mainly on voluntary corporate disclosures that may (or may not) lead to real changes in firm behavior (see Michelon et al., 2022, for a summary review). Despite the general tendency to emphasize positive information in voluntary sustainability reporting, prior research has also documented that self-disclosing information on negative aspects related to sustainability by a company might be regarded as a positive signal and a risk mitigation tool (Reimsbach & Hahn, 2015), and companies develop communicative legitimation strategies to report the negative aspects of sustainability disclosures (Hahn & Lülfs, 2014). Prior research has also suggested that third-party disclosures on negative aspects of CSR might lead to negative evaluative judgments (Reimsbach & Hahn, 2015). In the case of SM, when negative information about a company spreads quickly and widely, negative judgments may jeopardize corporate reputation (Etter et al., 2019) and firms need to develop ways to manage social disapproval (Wang et al., 2021).

This article builds on and contributes to the prior literature by providing some insights into how companies manage involuntary disclosures on SM. We provide evidence that companies are generally not eager to respond to involuntary disclosures made by stakeholders—but, if they decide to do so, the most frequently used communication strategy is mortification. However, companies may also dispute involuntary disclosures by choosing denial or evasion of responsibility as their response strategy. Overall, with some exceptions, involuntary disclosures are unlikely to be a mechanism through which meaningful communications can develop between companies and stakeholders and real sustainable changes in corporate behavior can be achieved.

Second, our article contributes to the literature on communication between stakeholders and companies. Prior research documents that, despite the advantages of SM in terms of easily engaging in more meaningful two-way communication, companies still focus on one-way communication by simply managing communication with stakeholders (Bellucci & Manetti, 2017; Gómez-Carrasco et al., 2021; Okazaki et al., 2020). Gómez-Carrasco et al. (2021) even suggest that two distinct worlds of communication exist—one belonging to companies and another belonging to stakeholders. This article adds to these findings evidence that neither companies nor stakeholders can engage in persuasive conversations about stakeholder-initiated involuntary disclosures. Our empirical evidence suggests that stakeholders do not symmetrically engage with most firms’ rhetorical strategies. Only when denial is used as a response strategy to involuntary disclosures are stakeholders likely to become more involved by replying to corporate communications. However, in such cases, further exchanges and communications may be hindered or even blocked by the firm’s denial. Overall, communication between stakeholders and companies around involuntary disclosures seems to be limited and predominantly one-way on both sides.

The remainder of the article is structured as follows. In “Literature Review” section, we present the literature review and discuss our research framework. “Research Method” section discusses the method, whereas “Findings” section presents our sample and descriptive statistics and discusses the results. “Discussion and Conclusion” section provides a discussion and concluding remarks.

Literature Review

Firm CSR Communication and the Role of SM

Morsing and Schultz (2006) build on Gruning and Hunt’s public information model (Gruning & Hunt, 1984) and discuss three types of stakeholder relations in terms of how firms strategically engage in CSR communication with stakeholders. These include stakeholder information, response, and involvement strategies. A stakeholder information strategy is always a one-way communication through which information flows from the organization to its stakeholders. The purpose of an information strategy is to disseminate information—not necessarily with a persuasive intent but rather to inform the public as objectively as possible about CSR outcomes. Therefore, this strategy is more about telling than it is about listening. In contrast, the stakeholder response and involvement strategies are, at first glance, two-way communication strategies. The main difference between these two strategies is the extent of their engagement with stakeholders. In the stakeholder response strategy, communication is about obtaining feedback on what stakeholders accept or think. In the stakeholder response strategy, stakeholders passively respond to corporate communication. Given that such communication is inherently asymmetric, the stakeholder response strategy can still be considered a one-sided communication. In contrast, the stakeholder involvement strategy assumes symmetric communication, proactive involvement, and dialogue with stakeholders. It is described by Brennan et al. (2013) as “a process of reciprocal influence between organizations and their audiences” (p. 666). Both the company and its stakeholders are equally and reciprocally involved in the communication process; thus, persuasion comes from both. The stakeholder involvement strategy invites concurrent negotiations with a company’s stakeholders to explore their concerns while accepting necessary changes. As a result, the purpose of a stakeholder involvement strategy is to reach mutual understanding, rational agreement, and consent (Morsing & Schultz, 2006).

The development of new communication technologies has had a profound impact on how organizations disclose information and communicate with stakeholders (Dumay, 2016). SM can be defined as “a group of Internet-based applications that build on the ideological and technological foundations of Web 2.0, and that allow the creation and exchange of user generated content” (Kaplan & Haenlein, 2010, p. 61). The increase in the use of SM leads to more information production, which is diffused more quickly, and new ways to access, evaluate, and use such information (Dumay & Guthrie, 2017). SM changes the dynamics of traditionally corporate-centric communication to gain legitimacy (Schultz et al., 2013). Higher connectivity, speed, and pluralization allow for more diverse voices on CSR. However, more importantly, organizations are often confronted with stakeholders’ alternative views on organizations’ alignment with societal and environmental norms and expectations, and stakeholders put moral pressures on them (Castelló et al., 2013). Not surprisingly, Castelló et al. (2013) call for an exploration of CSR as a polyphonic concept, in which “several voices are combined into a complex concept in which the individual voices can remain independent identities instead of being dominated by another homophonic voice” (p. 688). Along the same lines, Whelan et al. (2013) discuss and distinguish between corporate and public citizenship arenas in the SM age. In the former, corporations construct digital spaces (e.g., YouTube channels) within which individual citizens can discuss, debate, and organize CSR issues relevant to the company that created the space. As a result, more citizens gain the ability to voice their concerns and issues about firm CSR practices, but this ability does not necessarily lead to substantial changes in CSR because the company maintains control over the communication medium. In contrast, an individual citizen can influence CSR issues within the public arena of citizenship by creating and disseminating media content in public arenas—such as Facebook, Twitter, Instagram, and other SM platforms—potentially increasing stakeholder participatory capacities.

Undoubtedly, the emergence of SM provides companies with new alternative communication modes that may bring benefits but also risks. As Bellucci and Manetti (2017) argue, SM is particularly well suited for stakeholder engagement because it allows companies to interact with a large group of people, especially external stakeholders. SM can help organizations engage with stakeholders because it allows one party (the organization) to interact with another (the stakeholder) in communication in which both parties learn from the interactions, thereby allowing them to revise their expectations and preconceptions. SM also makes it possible for stakeholders to “initiate and discuss any issue of their interest and engage in dialog about and with the company, in a media characterized by almost immediate and worldwide diffusion” (Gómez-Carrasco & Michelon, 2017, p. 855).

The use of SM in corporate stakeholder communication has been investigated in prior research from the perspective of both financial (Bilinski, 2019; Elliott et al., 2018) and nonfinancial reporting (Gómez-Carrasco et al., 2021; Manetti & Bellucci, 2016; Okazaki et al., 2020). Manetti and Bellucci (2016) show that a small number of organizations use SM to engage stakeholders and that the level of interaction is generally low. Bellucci and Manetti (2017) investigate Facebook as a dialogic accounting tool and explore its use by large nongovernmental organizations (NGOs). They found that, with some exceptions, NGOs use SM simply to legitimize their activities rather than to interact with stakeholders. In the context of CSR reporting on Twitter, Okazaki et al. (2020) suggested that SM communication remains a mostly one-way process. Given the still relatively low engagement on Twitter, Saxton et al. (2021) investigate the determinants of a company’s responses to stakeholders. In general, companies do not respond to stakeholders’ tweets, with some exceptions in the case of the high connecting power of stakeholders and their urgency. Gómez-Carrasco et al. (2021) point out that significant differences exist between the information interests of companies and stakeholders and suggest that a “parallel” occurs in relation to CSR information on SM.

Involuntary Disclosures and Possible Corporate Responses

Dumay and Guthrie (2017) define involuntary disclosures as “what stakeholders and stake seekers disclose about an organization” (p. 30). 1 Not all information revealed by stakeholders is classified as involuntary. Involuntary disclosures are initiated by third parties against the will of managers. They are not subject to any guidelines or regulations. Hence, the reliability of such information may be questionable as it might be based on rumors or insinuations and misinterpreted as being truthful. Rumors, however, like any other disclosed information, can be negative or positive. Therefore, involuntary disclosures pose opportunities and threats to firms, bringing new risks that affect their reputations and need to be managed effectively (Dumay & Guthrie, 2017).

Organizations can undertake various strategies to manage information produced by stakeholders outside their boundaries and control, but each involves using communication processes. One of the perspectives allowing for the conceptualization of firm responses to involuntary disclosures is impression management. Merkl-Davies and Brennan (2011) developed a conceptual framework of impression management, suggesting that the concept is multifaceted and complex and aims to shape the perceptions of a wide range of outside parties. Impression management may be explained from four perspectives: (a) economic, (b) psychologic/behavioral, (c) sociological, and (d) critical. Each is based on different assumptions regarding the rationale underlying the behavior of managers and organizational audiences and the motivation for providing disclosures (Merkl-Davies & Brennan, 2011). The sociological perspective may be particularly suitable for analyzing the motivation for companies to respond to involuntary disclosures. The sociological perspective sees corporate narrative-reporting as determined by structural constraints exerted by stakeholders (Merkl-Davies & Brennan, 2011) as well as by public pressure and media attention (Hooghiemstra, 2000). Companies may engage in symbolic management to provide the impression that their activities are congruent with societal norms and values. In a situation in which a company faces an event that jeopardizes its image as a legitimate organization, it may become involved in strategic restructuring and/or providing normalizing accounts (Suchman, 1995). Normalizing accounts are verbal remedial strategies, such as justifications, excuses, and apologies (Hooghiemstra, 2000; Merkl-Davies & Brennan, 2011). In contrast, strategic restructuring is aimed at symbolically distancing the company from a negative event by, for instance, disassociation (Suchman, 1995).

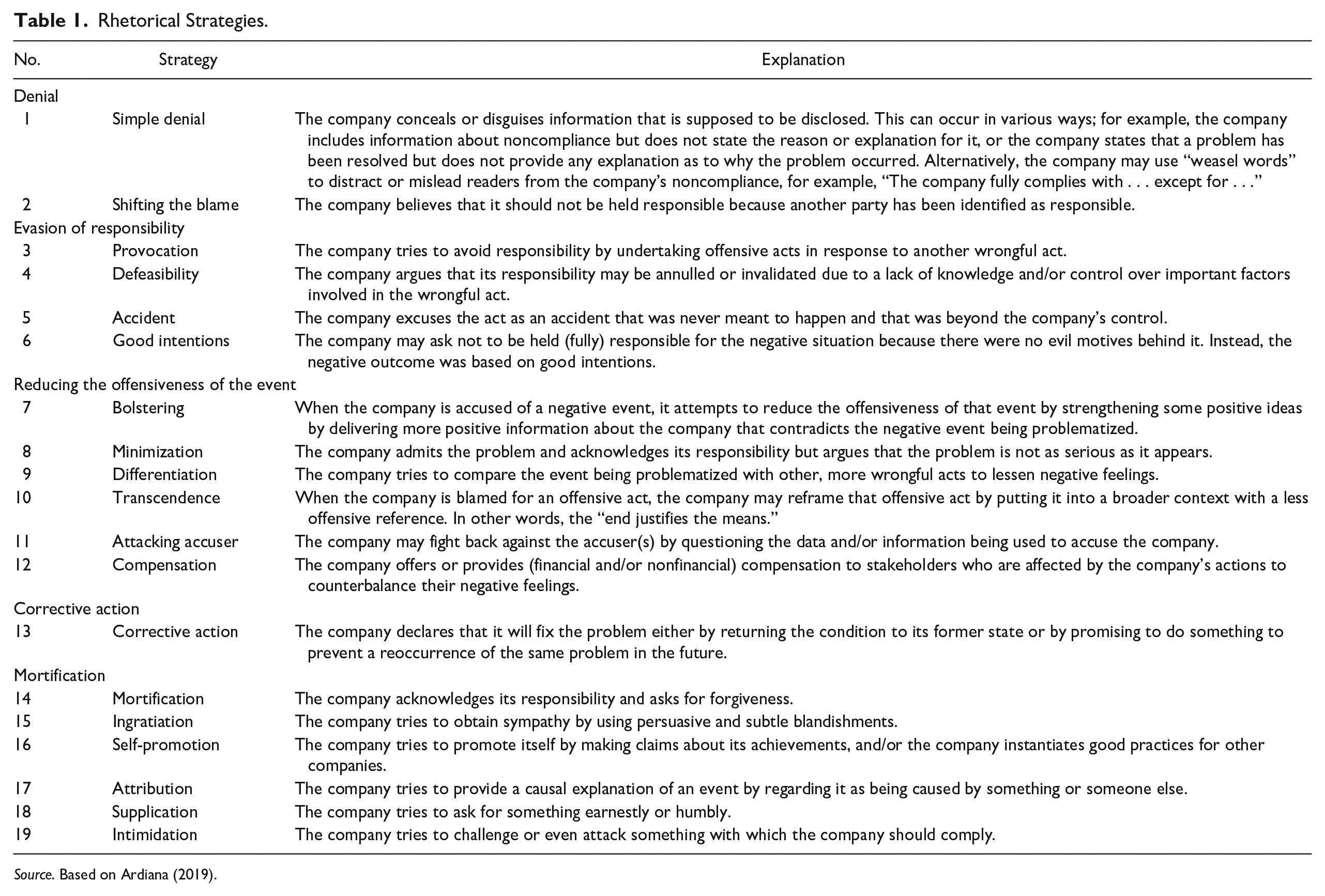

Possible corporate reactions to involuntary disclosures may also be analyzed from the perspective of reputation risk management. Reputation can be viewed as an asset but also as the outcome of the company’s shared, socially constructed impressions (Bebbington et al., 2008). Drawing on the corporate communication literature, Bebbington et al. (2008) analyze how CSR disclosures can be used for reputation risk management. Reputation risk management involves, among others, possible discourses (image-restoration strategies) in the face of the need for image restoration. Benoit (1995) suggests that reputation discourse is a function of two factors: (a) an audience of concern perceives the fact or the perception of a commitment of a “reprehensible act,” and (b) a relevant audience demands that the actor “be held responsible for the occurrence of that reprehensible act.” Image-restoration strategies may be addressed to the accuser alone or to the accuser and other audiences. Benoit (1995) presents a typology of 14 image-restoration strategies that can be classified into five groups: (a) denial, (b) evasion of responsibility, (c) reduction of the offensiveness of the event, (d) corrective action, and (e) mortification. Shrives and Brennan (2017) extend the framework for analyzing communication strategies in reputation risk management by combining Benoit’s (1995) image-restoration strategies with Bolino and Turnley’s (2003) impression management profiles and offer a more complex typology. Table 1 provides a summary of the strategies and a list of the subcategories.

Rhetorical Strategies.

Source. Based on Ardiana (2019).

Ardiana (2019) uses an extended typology to analyze the rhetorical strategies used in sustainability disclosures for reputation risk management. Because involuntary disclosures can be perceived as a part of reputation risk, this typology may be suitable for the analysis of rhetorical strategies in response to involuntary disclosures.

Theoretical Framework

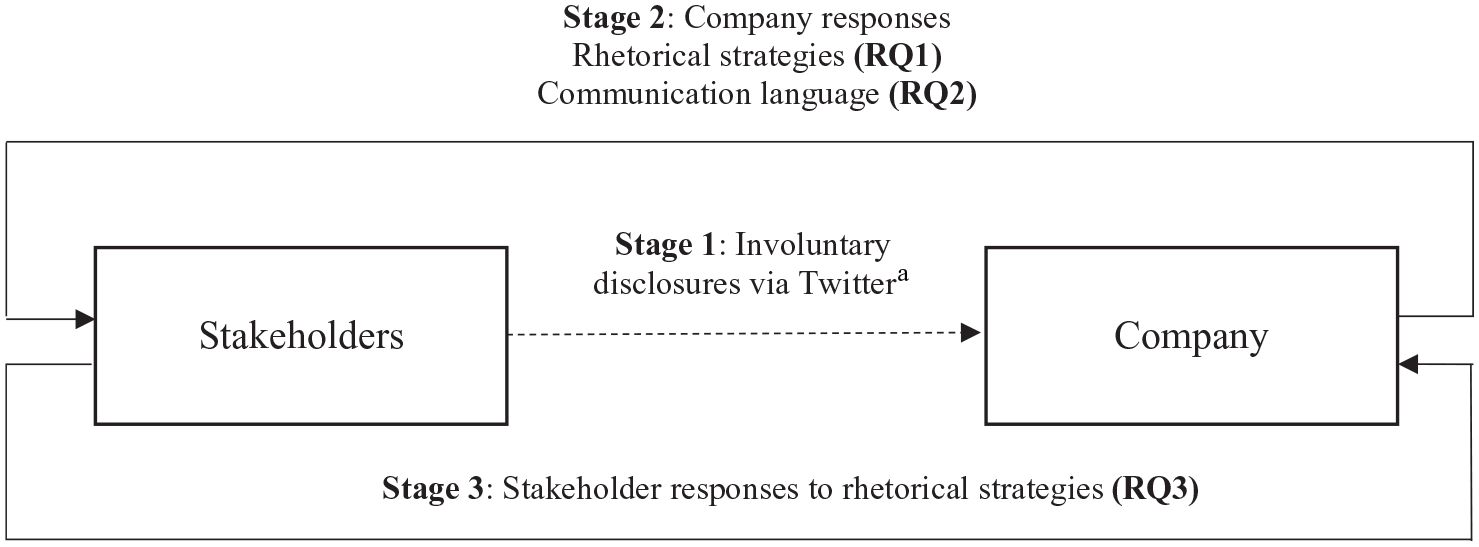

We build on the concepts of involuntary disclosures and stakeholder–company communications to frame our research in the context of SM. Our research framework is presented in Figure 1.

Research Framework.

We focus on firm responses to stakeholder-initiated communication with a particular interest in understanding how firms address stakeholder-initiated involuntary disclosures. Initially, stakeholders disclose involuntary information (Stage 1 in Figure 1); then, the company may choose to ignore or respond to such disclosures (Stage 2 in Figure 1). In turn, stakeholders may discontinue the communication or engage in additional discussion (Stage 3 in Figure 1). The communication may continue in the subsequent cycles. The main point of interest in this study is to examine the interactions between firms and stakeholders at Stages 2 and 3 in Figure 1. Mainly, we investigate both the rhetorical strategies and the language used by companies in their responses to stakeholder-initiated communication when involuntary information is disclosed (Stage 2 in Figure 1). Next, we focus our attention on the stakeholder responses and the reactions to firm communications (Stage 3 in Figure 1). As such, we pose the following research questions:

Because stakeholder-initiated communication may provide opportunities and threats not only in terms of firm reputation but also in terms of share value, companies might want to respond to these communication types. However, companies may adopt different approaches in responding to involuntary disclosures and use different rhetorical strategies to respond to stakeholder-initiated/sustained communications. We build on Shrives and Brennan (2017) and Ardiana (2019) to propose the rhetorical strategies of (a) denial, (b) evasion of responsibility, (c) reduction of the offensiveness of the event, (d) corrective action, and (e) mortification.

Research Method

Sample, Data Collection, and Coding

We observed the Twitter accounts of the top 30 companies from the Salterbaxter (SB) Influencers 100 Index 2 (Salterbaxter, 2019) in 2019. While we acknowledge that stakeholders may use alternative SM channels to disseminate involuntary disclosures, 3 we believe that Twitter is the best platform for our analyses for three main reasons: (a) Compared with alternative SM platforms—such as Facebook, YouTube, and Instagram—Twitter is known for information dissemination, and firms generally prefer to adopt Twitter rather than Facebook as their first choice of an SM platform (Zhou et al., 2015); moreover, the “@” function allows stakeholders to directly establish dialog with the firm and the firm’s responses to individual stakeholder tweets can be traced via Tweet ID and mentioned usernames; (b) unlike Facebook, where firms may delete stakeholder comments without responding, Twitter users do not face any restrictions from the firm when posting messages, making Twitter a more appropriate platform for identifying involuntary disclosures; and (c) Twitter data are more easily accessible than other SM platforms; for example, Facebook restricted its API licenses in 2018, making it more difficult for the public to retrieve firm messages and stakeholder comments.

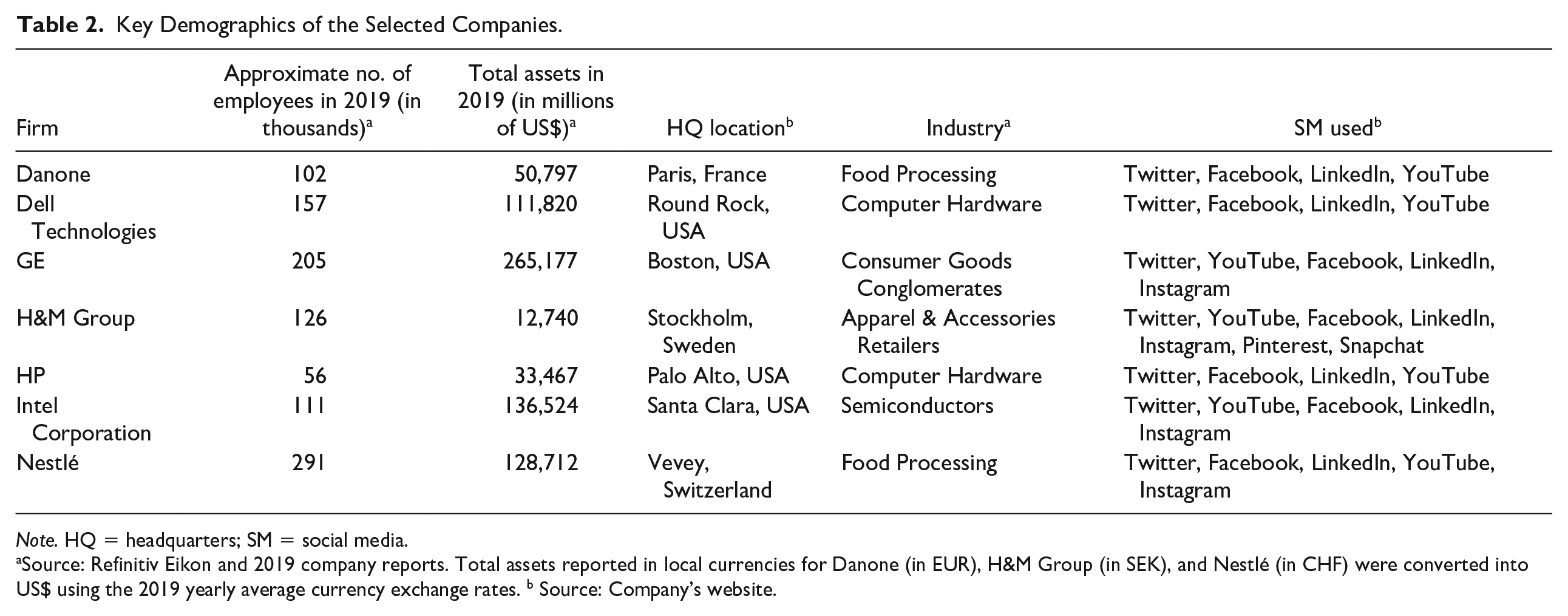

We initially selected five firms from the top 30 companies listed on the SB Influencers 100 Index (Salterbaxter, 2019) that have the highest number of followers and the highest number of tweets issued (Dell Technologies, Intel Corporation, Nestlé, HP, and GE). These companies have the highest interaction rates with CSR-/sustainability-related posts. We therefore considered them as the most active and engaged in building a sustainability agenda on Twitter. We assumed that such an approach would provide rich material for analysis. As all of these companies—apart from Nestlé—are from the United States, we added two European-based firms to our sample: H&M and Danone. Both are ranked highly on the SB Influencers 100 Index (Salterbaxter, 2019). Moreover, H&M is the highest ranked company on the SB Influencers 100 Index representing the apparel and “fast fashion” industry, which is subject to criticism for payments to workers in the supply chain below the living-wage level (Schrage & Gilbert, 2021) and enormous waste production (see Brennan et al., 2013; Greenpeace, 2011).

In summary, our sample consists of seven well-known and leading international brands (Dell Technologies, H&M Group, Intel Corporation, Nestlé, Danone, HP, and GE) based on their high Twitter activity, respective of their industry and their reputation for their CSR programs according to leading industry reports (Forbes, 2021; Newsweek, 2021; Salterbaxter, 2019). Similar to the approach used in Okazaki et al. (2020), they represent various industries. Table 2 presents the key demographics of the selected companies.

Key Demographics of the Selected Companies.

Note. HQ = headquarters; SM = social media.

Source: Refinitiv Eikon and 2019 company reports. Total assets reported in local currencies for Danone (in EUR), H&M Group (in SEK), and Nestlé (in CHF) were converted into US$ using the 2019 yearly average currency exchange rates. b Source: Company’s website.

To examine how firms employ rhetorical strategies and linguistic features to respond to involuntary disclosures, we focused on firm replies that explicitly address stakeholders’ communication, revealing information against managers’ will. We adopted this approach to ensure (a) that we could crossmatch the firm replies with the stakeholder-initiated involuntary disclosures that refer to the firm and (b) that the information communicated by stakeholders meets the definition of involuntary disclosures. 4

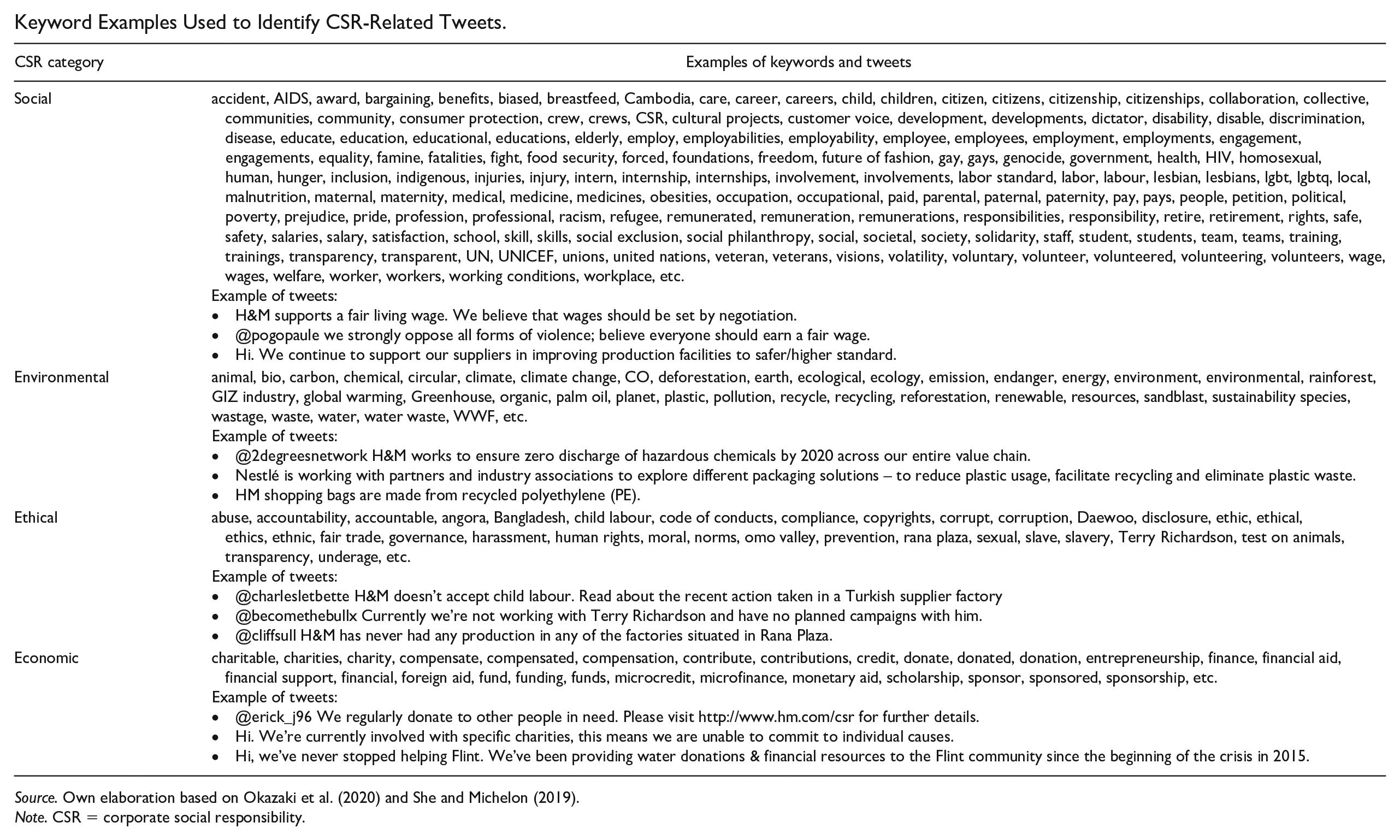

Using a scraping algorithm, 206,801 firm-initiated tweets were initially extracted from Twitter. 5 The firm-initiated tweets included tweets from brands’ corporate handles or news published up to May 20, 2020, and tweets that mentioned or directly replied to these tweets. Non-English tweets were excluded from the sample. Following other Twitter content analysis research (e.g., Adams & McCorkindale, 2013; Lovejoy & Saxton, 2012; Okazaki et al., 2020; Waters & Jamal, 2011), a coding booklet was developed to guide coders to sort tweets into specific coding categories. The booklet instructed two independent researchers on how to code the collected data. First, the coders identified the character of all extracted tweets by assessing the subject matter of the tweets’ messages, and then classified them into the categories of CSR and other general information. For this purpose, CSR-related keywords were used based on the literature review of economic, environmental, ethical, and social issues (see Okazaki et al., 2020; She & Michelon, 2019; and Appendix 1 for the keywords used and examples of tweets from each category).

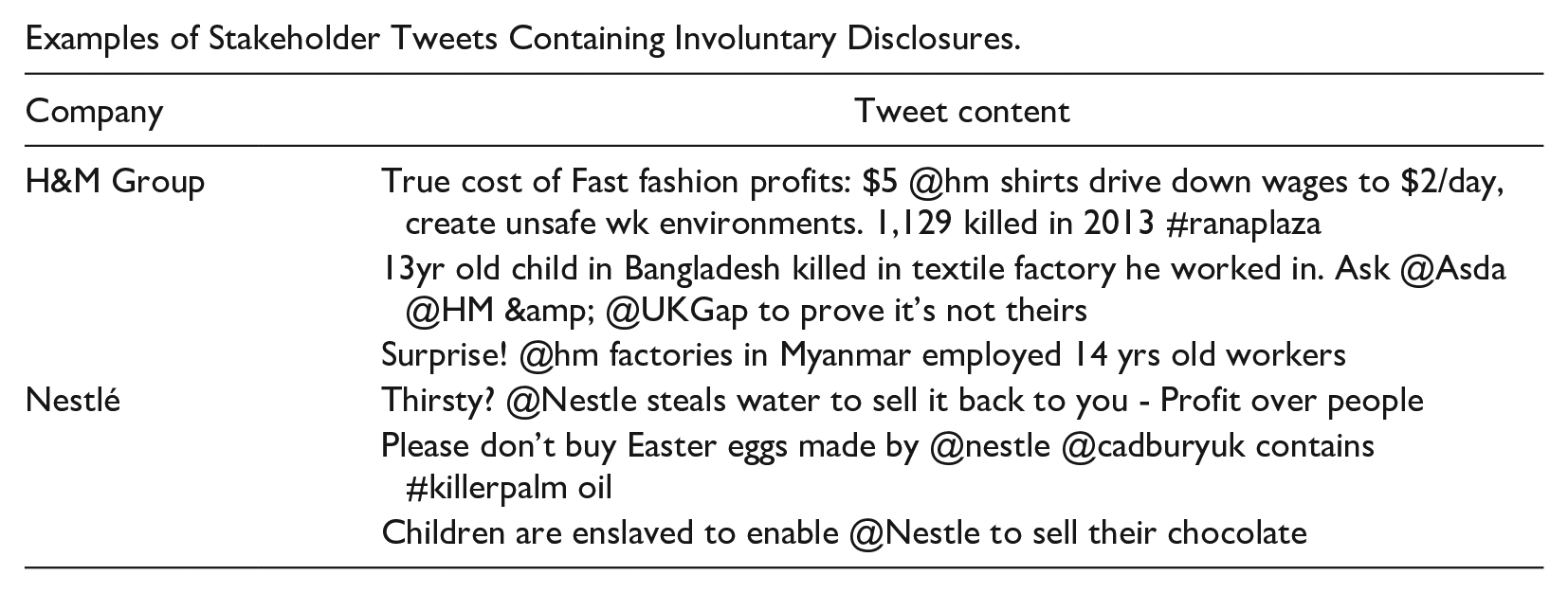

Next, the tweets that contained firm replies to stakeholders were identified and manually classified by two independent coders into replies to involuntary disclosures related to CSR and other replies. 6 We found 134,977 total replies to stakeholders, of which 4,644 tweets were replies to involuntary disclosures related to CSR. To ensure the accurate identification of firm responses to involuntary disclosures, we analyzed not only the company’s reply but also the stakeholder’s original tweet containing the involuntary disclosure. In this case, we analyzed both the information released by the stakeholder against the company’s will (see Appendix 2 for examples of involuntary disclosures) and the content of the hyperlinks added to the tweet to ensure that the information met the definition of an involuntary disclosure.

Finally, all replies to involuntary disclosures were examined by the coders following the coding booklet to determine the rhetorical strategies used by the company. 7 Examples of the coding of the rhetorical strategies can be found in Appendix 3. The coding took more than 9 months (from June 2020 to February 2021) because the content of all companies’ replies to stakeholders’ tweets (134,977) was analyzed by two independent coders to identify the replies to involuntary disclosures and rhetorical strategies. Moreover, the process required the investigation of the original stakeholders’ tweets and other provided information. The independent coders had an intercoder reliability of 95%, which was deemed acceptable (Rust & Cooil, 1994). However, all coding discrepancies between the coders were reconciled and discussed to ensure consistency and reliability.

Empirical Model and Variable Measurement—Main Analyses

We relied on 4,644 firm replies to involuntary disclosures and their associated descriptive statistics to address RQ1 and RQ2, exploring the types of rhetorical strategies and language used by the firms. We first identified the extent of firm replies to involuntary disclosures vis-à-vis other replies. This analysis provided a general indication of the firms’ willingness to engage in involuntary disclosures. We then examined the extent of the firm replies that employed each of the five rhetorical strategies (i.e., denial, evasion of responsibility, reduction of the offensiveness of the event, corrective action, and mortification). Finally, we identified the linguistic characteristics of the firm replies by examining the number of replies that were positive or negative in tone. We use the Valence Aware Dictionary for Sentiment Reasoning (VADER) net sentiment score to measure the tone of the firm replies. The VADER net sentiment score ranges from −1 to +1 and a higher score indicates a more positive tone (Gilbert & Hutto, 2014). The VADER is particularly suitable for an SM context because it considers terms and phrases used in an online setting (Gilbert & Hutto, 2014; She & Michelon, 2019). 8 We coded a firm reply as positive (negative) in tone if the VADER net sentiment score was above (below) zero. Firm replies were considered neutral if the net sentiment score was equal to zero.

To investigate the subsequent stakeholder reactions to the firm replies that addressed involuntary disclosures (RQ4), we first focused on all the firm replies (N = 139,477) made to the stakeholder-initiated tweets. We included all firm replies in this model to examine whether stakeholders reacted differently to the firm replies that addressed involuntary disclosures vis-à-vis other replies. Following prior studies (e.g., Saxton et al., 2019), we estimated the following logit model to determine the likelihood of stakeholders responding to a firm’s reply to an involuntary disclosure:

where subscript ij denotes message i posted by firm j.

In Model (1), Stakeholder_Reaction is the likelihood of a stakeholder reacting to a firm’s reply. We used three alternatives to capture stakeholder reaction: favorites (Favorite), retweets (Retweet), and comments (Reply). Favorite (Favorite) captures stakeholders’ acknowledgment of the reply and represents positive stakeholder sentiment (Saxton & Waters, 2014; She & Michelon, 2019). Retweet (Retweet) shows that the message resonates with stakeholders, as a high level of retweeting increases message visibility (Saxton et al., 2019). Retweet also indicates the message credibility, as stakeholders are more likely to share credible messages with their followers (Cade, 2018). Comment (Reply) represents the level of discussion and debate between stakeholders and the firm (She & Michelon, 2019). Each of the three measures is a dummy variable equal to one if at least one stakeholder reacted to a firm reply using the relevant response and zero otherwise. FirmReply_InvDisc is a dummy variable equal to one if a firm replied to an involuntary disclosure and zero otherwise. We included several variables to control for other message characteristics. Following prior studies, we included the sentiment of the firm reply as measured by the VADER net sentiment score (Sentiment), as prior studies have shown that firms may strategically frame CSR information in a positive tone to manage stakeholder perceptions (Bozzolan et al., 2015; Cho et al., 2010). We controlled for text readability (Readability) using the Flesch–Kincaid score, as prior studies have found that firms may reduce text readability to hide poor CSR performance (Muslu et al., 2019). We also controlled for the presence of hyperlinks (Hyperlink), the mention of any Twitter account (MentionAcc), and hashtags (Hashtag), as these SM message features affect stakeholder responses (Saxton et al., 2019; Saxton & Waters, 2014; She & Michelon, 2019). We included firm fixed effects to control for unobservable, time-invariant firm characteristics and year fixed effects to control for any unobservable events that may have occurred during the sample period.

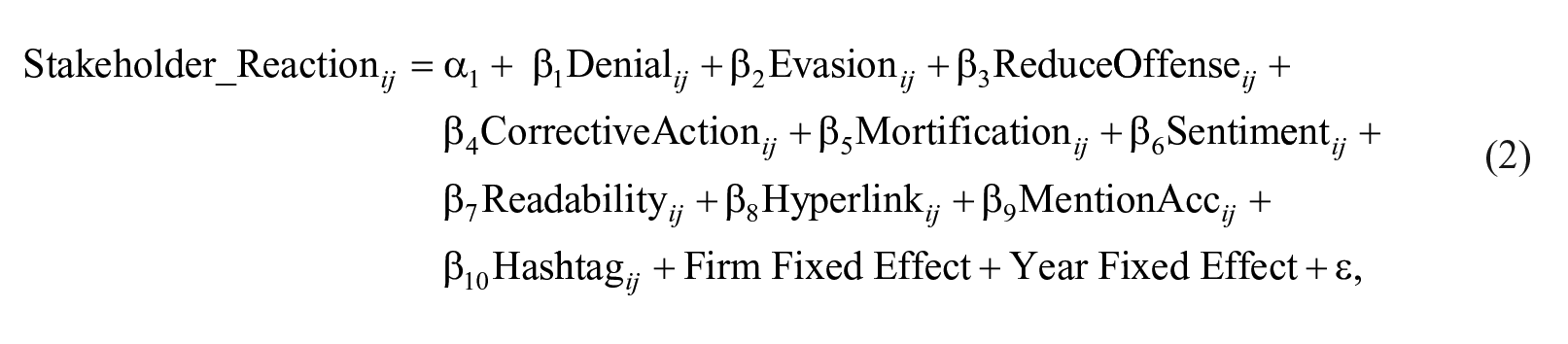

Next, we further explored the subsequent stakeholder reactions to the rhetorical strategies and types of language used in the firm replies that addressed involuntary disclosures. In this model, we focused on firm replies that addressed involuntary disclosures (N = 4,644). We used the following logit model to examine the likelihood of stakeholders’ continuing dialogue with the firm after seeing the rhetorical strategies and linguistic characteristics:

where subscript ij denotes message i posted by firm j.

In Model (2), Denial, Evasion, ReduceOffense, CorrectiveAction, and Mortification are dummy variables equal to one if the firm employed a denial, evasion of responsibility, reduction of the offensiveness of the event, corrective action, or mortification strategy, respectively, in the reply and zero otherwise. The use of rhetorical strategies in a firm reply is neither requisite nor mutually exclusive. A firm may not employ any strategy or it may employ more than one strategy in response to an involuntary disclosure.

Empirical Model and Variable Measurement—Additional Analysis

To further explore the variations in firm strategies employed to respond to involuntary disclosures, we examined whether firms may strategically select rhetorical strategies depending on the CSR issue exposed by stakeholders. To answer this additional research question, we focused on the firm replies that addressed involuntary disclosures (N = 4,644). We manually coded the involuntary disclosures that the firms replied to into economic, environmental, ethical, and social issues (Okazaki et al., 2020; She & Michelon, 2019). We used the following logit model to explain the variance in the firms’ use of rhetorical strategies when responding to different CSR topics:

where subscript ij denotes message i posted by firm j.

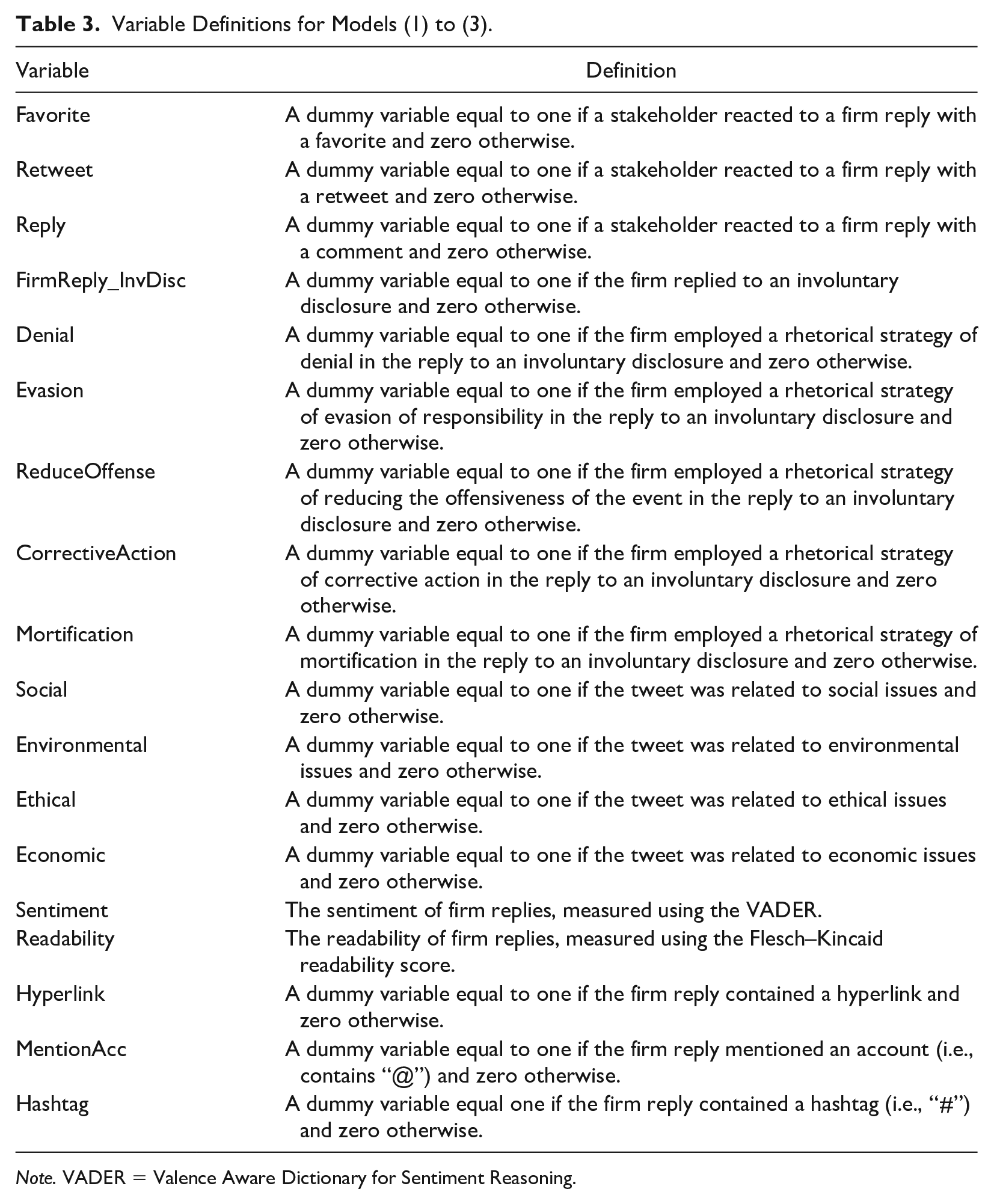

Rhetoric_Strategy is the likelihood of using a selected rhetorical strategy by a firm when replying to an involuntary disclosure and includes the denial (Denial), evasion of responsibility (Evasion), reduction of the offensiveness of the event (ReduceOffense), corrective action (CorrectiveAction), and mortification (Mortification) strategies. Social, Environmental, Ethical, and Economic are dummy variables equal to one if the tweet is related to social, environmental, ethical, and economic issues, respectively, and zero otherwise. All other variables are identical to those in Models (1) and (2). The definitions of all variables used for Models (1) to (3) can be found in Table 3.

Variable Definitions for Models (1) to (3).

Note. VADER = Valence Aware Dictionary for Sentiment Reasoning.

Findings

Descriptive Statistics for RQ1 and RQ2

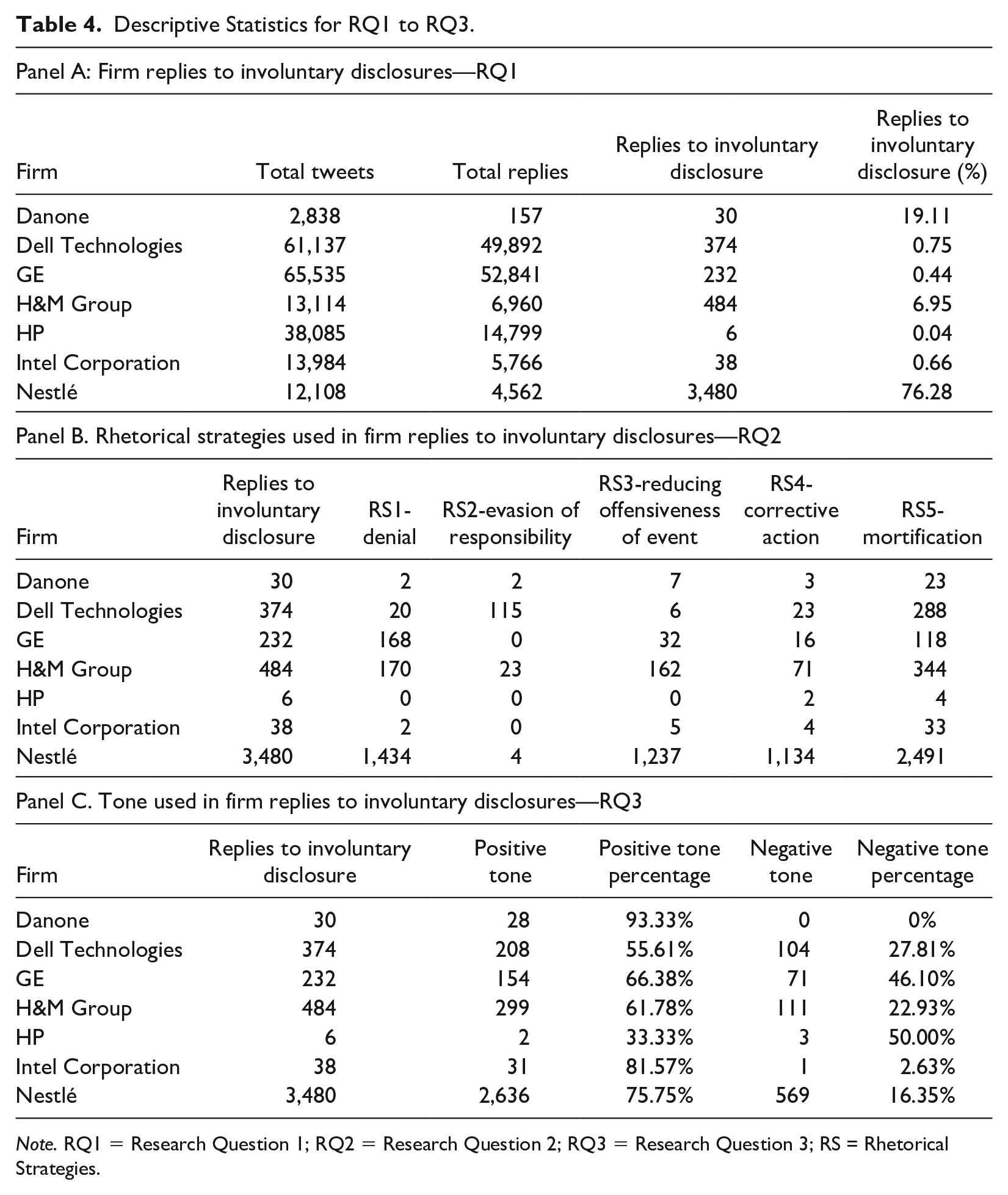

Table 4 presents the descriptive statistics and provides answers to RQ1 and RQ2, which aim to explore the types of rhetorical strategies and language used by companies when replying to involuntary disclosures.

Descriptive Statistics for RQ1 to RQ3.

Note. RQ1 = Research Question 1; RQ2 = Research Question 2; RQ3 = Research Question 3; RS = Rhetorical Strategies.

Panel A presents the total number of firm replies to stakeholders’ tweets and to involuntary disclosures made by stakeholders. Of the 206,801 extracted firm tweets, 134,977 represented the firms’ replies to stakeholders’ tweets, whereas less than an average of 4% of those tweets (N = 4,644) were the firms’ replies to involuntary disclosures (Table 4, Panel A). This percentage varied significantly across firms; for example, in the case of Nestlé, more than 76% of all replies were related to involuntary disclosures, whereas they represented merely 0.04% of all replies for HP. Three of the analyzed companies—Nestlé, Danone and H&M Group—actively engaged in communication initiated by stakeholders through involuntary disclosures. 9 The tweets replying to involuntary disclosures represented only 2% of all of the companies’ tweets. This result indicates that, in most cases, companies responded to involuntary disclosures, but engagement remained relatively low, as only a small percentage of firm replies addressed involuntary disclosures. The only exception was Nestlé, whose replies to involuntary disclosures represented almost one third of all of the firm tweets, which means that they were visible to the public. 10

Panel B presents the number of firm replies employing rhetorical strategies. For almost all companies, the most frequently used rhetorical strategy was mortification. Only GE preferred to use denial to a higher degree than the other companies. Interestingly, H&M Group mostly used the mortification strategy, but denial and reducing offensiveness were also widely used. Similar to H&M Group, Nestlé used a combination of these three strategies but added the corrective action strategy to their replies. Evasion of responsibility was rarely used. Dell Technologies used this strategy more frequently than did the other sample firms.

Panel C presents the number of firm replies with positive and negative tones. 11 Generally, the tone used in firm replies to involuntary disclosures was positive (over 70% of companies’ replies). In particular, the tone of Danone’s and Nestlé’s tweets was mostly positive (93% and over 75% of their tweets, respectively). Interestingly, for two companies (GE and HP), almost half of the replies had a negative tone. Moreover, the language used in 9% of the tweets can be described as neutral. The information technology companies (Dell Technologies, HP, and Intel Corporation) were more prone to using a neutral tone than were the other companies.

Descriptive Statistics for Stakeholder Reactions to Firm Responses (RQ3)

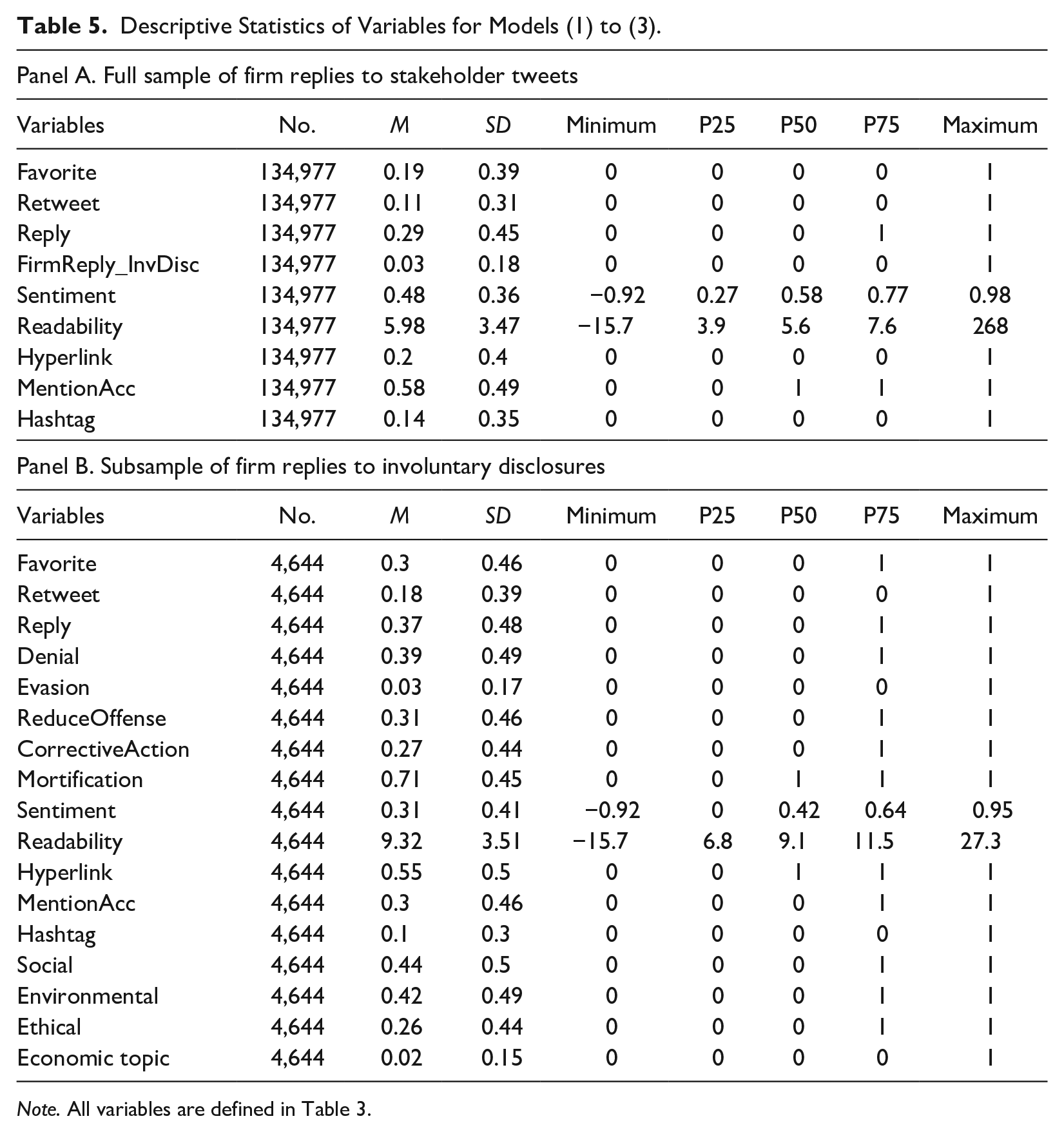

Table 5 presents the descriptive statistics for the variables used to analyze the stakeholders’ subsequent reactions to the firm replies to involuntary disclosures.

Descriptive Statistics of Variables for Models (1) to (3).

Note. All variables are defined in Table 3.

Panel A presents the descriptive statistics for the full sample (N = 134,977) of firm replies to stakeholder tweets (including replies to both involuntary disclosures and other tweets). Panel B presents the descriptive statistics when focusing on firm replies to involuntary disclosures (N = 4,644).

Interestingly, the replies to involuntary disclosures achieved greater public resonance and encouraged stakeholders to continue engagement with the companies more so than did the general firm replies. This phenomenon was clearly visible in the higher percentage of reactions to the retweets (18%), comments (37%), and favorites (30%) to the replies to involuntary disclosures than to all of the firm replies (11%, 29%, and 19%, respectively). More than 3% of all firm replies were to involuntary disclosures.

The mean values of the Flesch–Kincaid readability index equaled 5.98 for all replies and 9.32 for replies to involuntary disclosures, suggesting that the content of the tweeted replies was generally difficult to understand. Regarding the sentiment of the tweets, it was on average neutral (0.48 for all replies and 0.31 for replies to involuntary disclosures). However, the sentiment index for tweets with the most negative sentiments equaled −0.92, whereas the same index for tweets with the most positive sentiments equaled 0.98 (0.95 for replies to involuntary disclosures), suggesting a large variation in the tone of the replies.

Twenty percent of the replies contained a hyperlink to an external webpage. Interestingly, such hyperlinks were included in 55% of replies to involuntary disclosures, which means that companies want to provide stakeholders with additional information to make them more informed or convince them about their activities. We also observe that only 14% of the tweets contained a hashtag. The user-targeted tweets represented 58% of all tweets, whereas only 30% of tweets replied to involuntary disclosures. Moreover, a denial strategy was used in 39% of replies to involuntary disclosures; evasion of responsibility, in 3%; reduction of the offensiveness of the event, in 31%; corrective action, in 27%; and mortification, in 71%. Firms replied to involuntary disclosures related to social issues in 44% of the replies to involuntary disclosures, to environmental issues in 42%, and to ethical topics in 26%. The replies to economic involuntary disclosures were in the minority at 2%. 12

Regression Analyses for Stakeholder Reactions to Firm Responses (RQ3)

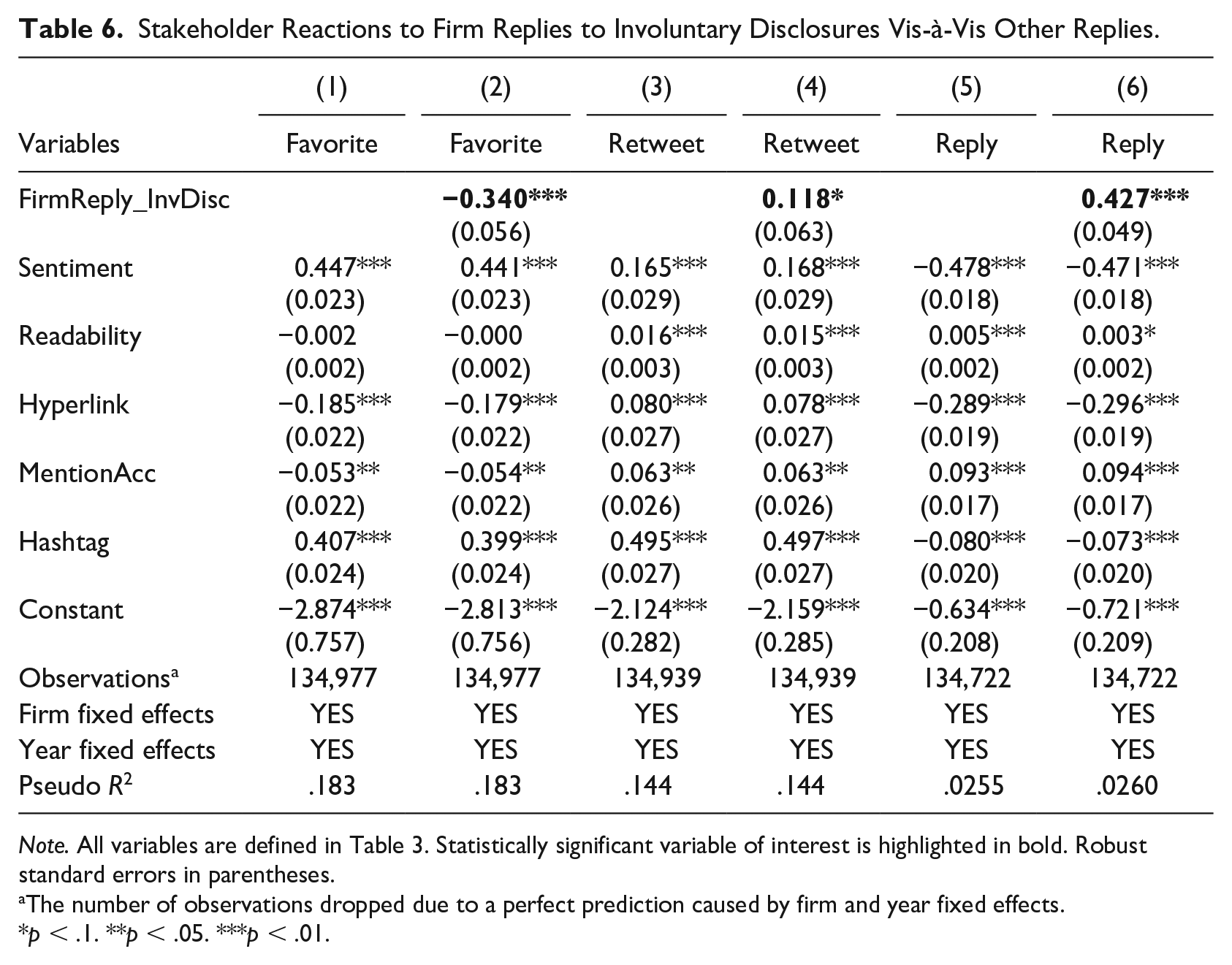

Table 6 presents the logit regression results of stakeholder reactions to firm replies to involuntary disclosures. Specifications 1, 3, and 5 present the effect of the control variables on stakeholder reactions using the favorite, retweet, and reply buttons, respectively. In Specifications 2, 4, and 6, we added our variable of interest, FirmReply_InvDisc, to the regression model and examined how stakeholders might react differently to firm replies to involuntary disclosures vis-à-vis other replies using the favorite, retweet, and reply buttons, respectively. FirmReply_InvDisc is a dummy variable equal to one if a firm replies to an involuntary disclosure made earlier by a stakeholder and zero otherwise.

Stakeholder Reactions to Firm Replies to Involuntary Disclosures Vis-à-Vis Other Replies.

Note. All variables are defined in Table 3. Statistically significant variable of interest is highlighted in bold. Robust standard errors in parentheses.

The number of observations dropped due to a perfect prediction caused by firm and year fixed effects.

p < .1. **p < .05. ***p < .01.

As shown in Table 6, firm replies to involuntary disclosures (FirmReply_InvDisc) were significantly and positively related to stakeholder reactions through retweets and comments. However, for reactions through favorites, FirmReply_InvDisc was negative and significant. These results suggest that stakeholders engage in dialogue with companies on involuntary disclosures and are willing to make comments and continue communication. However, stakeholders are less likely to react through favorites because they might not like what firms are doing and may be critical of firm actions. These results suggest that stakeholders are willing to establish two-way communication with firms regarding exposed involuntary disclosures instead of merely acknowledging or appreciating everything that firms say.

Regarding the control variables, tweets with positive sentiments (Sentiment) received more stakeholder reactions through favorites and retweets, whereas those with negative sentiments are more likely to attract stakeholder comments. This finding is in line with those suggesting that negative messages receive more attention from users than do positive messages (Coleman & Wu, 2010; Ferrara & Yang, 2015; Saxton et al., 2021). For stakeholder reactions through favorites, the Flesch–Kincaid index (Readability) was negative but not statistically significant. In contrast, the consistent and positive effect of Readability on Reply and Retweet suggests that stakeholders may prefer to retweet and reply to less complicated tweets. Inclusions of URLs (Hyperlink) negatively affected reactions through likes and comments on the message, which may suggest that stakeholders are less likely to question firm responses when stakeholders are provided with additional information. Similarly, the use of the user mention convention in replies (MentionAcc) was not appreciated by Twitter users, but it increased the likelihood of retweeting and commenting by stakeholders. Finally, tweets with hashtags (Hashtag) were more likely to attract positive reactions from stakeholders and to be retweeted but were less likely to receive comments.

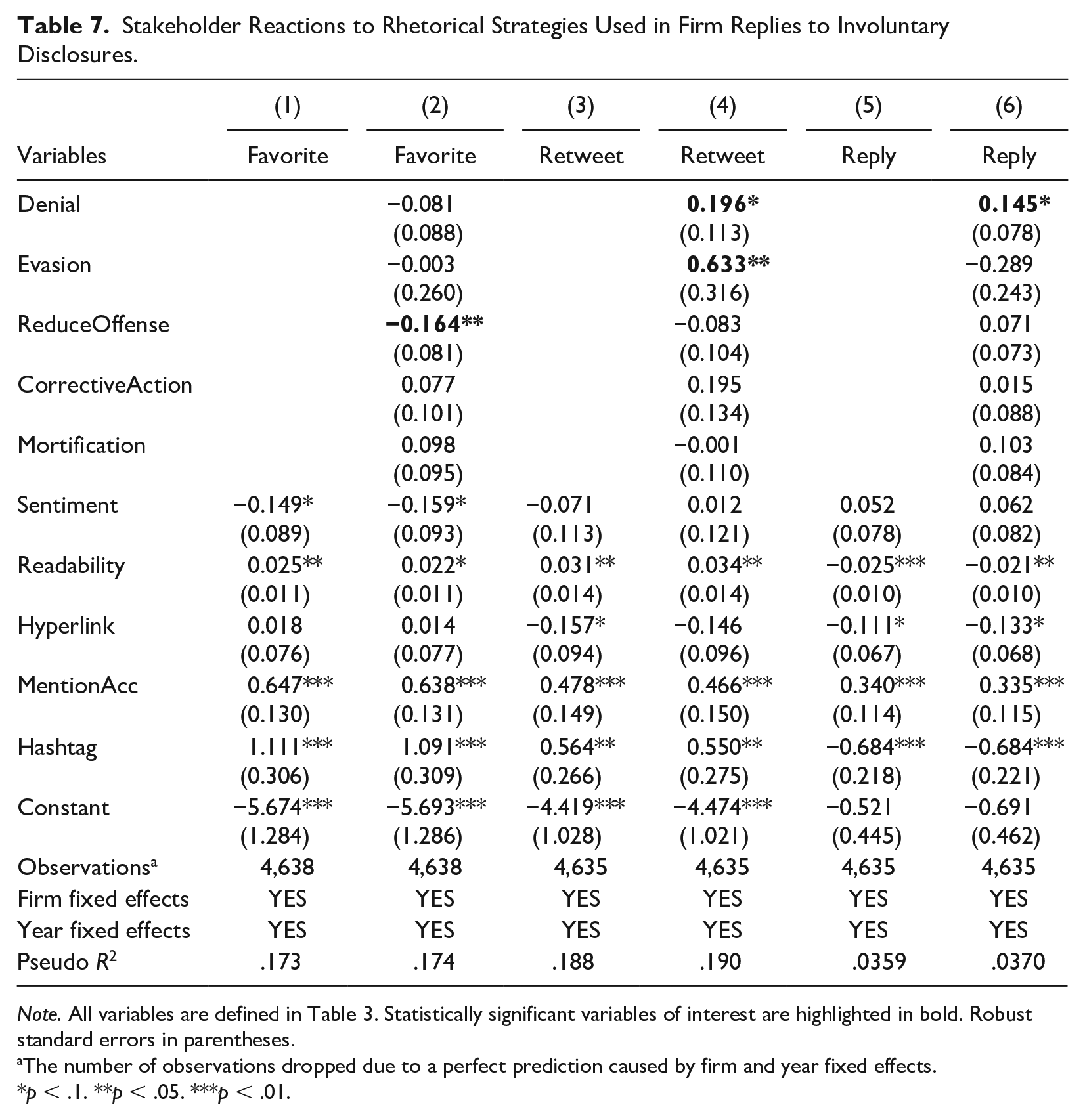

Table 7 presents the logit regression results of stakeholder reactions to the rhetorical strategies used in firm replies to involuntary disclosures. In this model, we focused only on firm replies to involuntary disclosure (N = 4,644). Specifications 1, 3, and 5 present the regression results using only the control variables. In Specifications 2, 4, and 6, we added our variables of interest—the rhetorical strategies—to the regression and examined their effects on stakeholder reactions with a favorite, retweet, and reply button, respectively.

Stakeholder Reactions to Rhetorical Strategies Used in Firm Replies to Involuntary Disclosures.

Note. All variables are defined in Table 3. Statistically significant variables of interest are highlighted in bold. Robust standard errors in parentheses.

The number of observations dropped due to a perfect prediction caused by firm and year fixed effects.

p < .1. **p < .05. ***p < .01.

The results show that ReduceOffense was significantly and negatively related to stakeholder reactions through the favorite button. These results suggest that stakeholders are not impressed by firms using the tactic of reducing the offensiveness of the event in their replies to involuntary disclosures. In contrast, Specification 4 shows that disclosure strategies Denial and Evasion were positively associated with stakeholder retweets, and the use of denial and evasion of responsibility disclosure strategies was more likely to result in a retweet. Finally, the likelihood of receiving a comment to the reply (Specification 3) was positively associated with Denial, indicating that stakeholders engaged in discussions of firms’ denial. Overall, these findings indicate that while stakeholders do not engage with most rhetorical strategies used by firms in response to involuntary disclosures, they are more willing to engage in subsequent discussions about firms’ use of denial and evasion strategies. Therefore, the mere use of denial, evasion, and reduction of the offensiveness of the event strategies does not satisfy stakeholder information needs and firms need to communicate more concrete actions regarding their sustainability practices.

Regarding the control variables, interestingly, tweets with negative sentiments (Sentiment) received more favorites (Specification 1) than did those with positive sentiments. This finding suggests that stakeholders are more likely to react with a favorite button when firms deliver bad news and/or acknowledge their wrongdoings. For stakeholder reactions with favorites and retweets, the Flesch–Kincaid index (Readability) was positive (Specifications 1 and 2), whereas the negative effect of Readability on Reply (Specification 3) might suggest that stakeholders prefer to reply to less complicated tweets. This result suggests that stakeholders may know a firm’s strategy of avoiding public scrutiny by providing obfuscating information. Hyperlink was negative and statistically significant only for commented tweets (Specification 3), suggesting that stakeholders are less likely to question firm responses when being provided with additional information. Firm replies mentioning an account (MentionAcc) are appreciated by Twitter users and increase the likelihood of retweets and comments by stakeholders (Specifications 1, 2, and 3). Furthermore, firm replies to involuntary disclosures with hashtags (Hashtag) were more likely to attract positive reactions from stakeholders and be retweeted (Specifications 1 and 2) but were less likely to receive comments (Specification 3).

Exploring Firm Selective Responses to Involuntary Disclosure—Additional Analysis

In “Descriptive Statistics for RQ1 and RQ2” subsection, we noted a substantial variation in firm replies to involuntary disclosures (see Table 4, Panels A and B). This subsection obtains further insights and explores possible differences in firm replies to different types of involuntary disclosures. In doing so, we examined how each CSR topic (social, environmental, ethical, and economic) is associated with each rhetorical strategy that companies might selectively use to respond to involuntary disclosure.

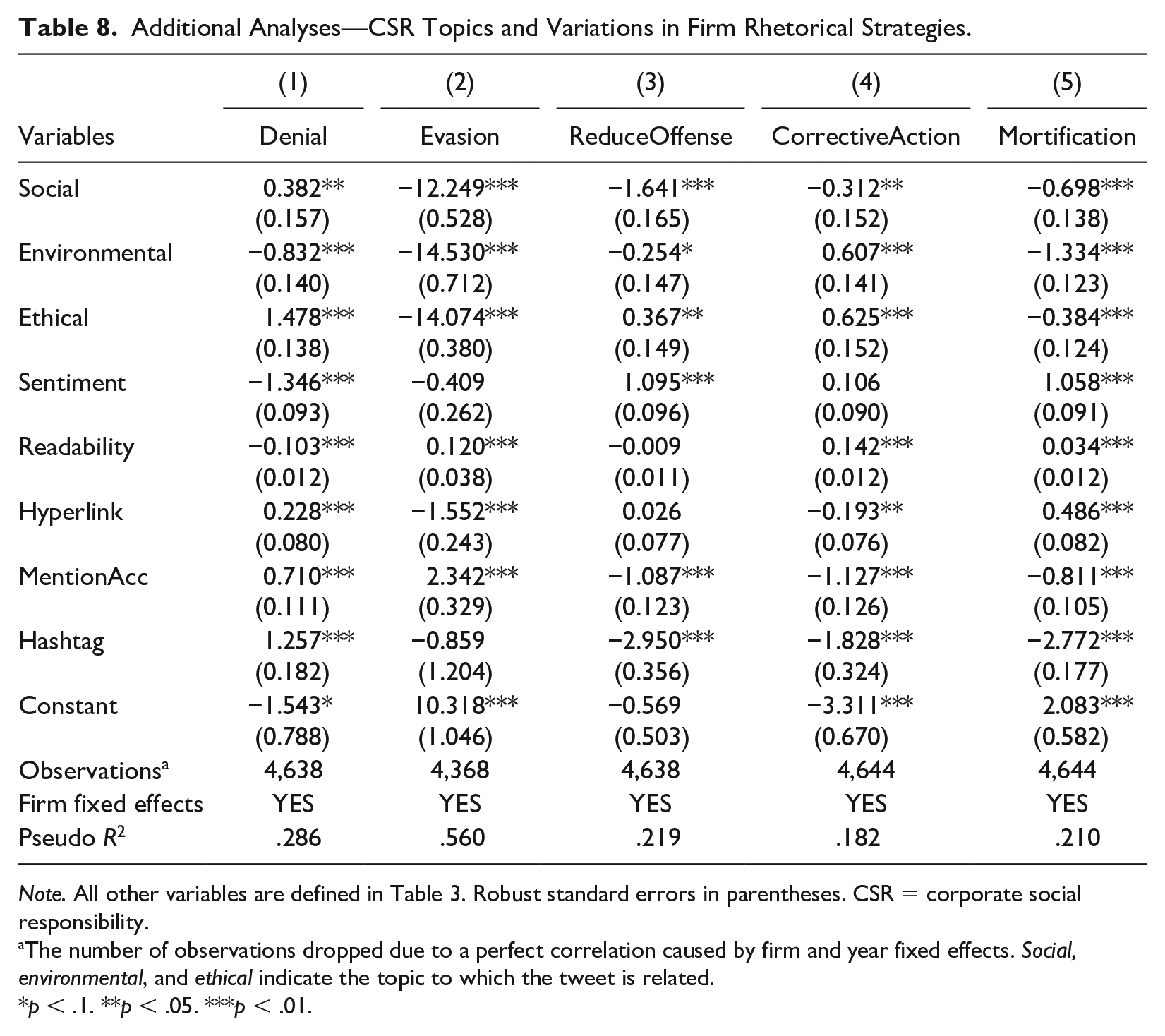

Table 8 presents the logit regression results used to examine the likelihood that each CSR topic is related to each rhetorical strategy with the economic topic as a baseline. In this model, we focused only on firm replies to involuntary disclosures (N = 4,644). We used only firm fixed effects, as firms’ choices in choosing a strategy when responding to involuntary disclosures tended to be consistent over the years; therefore, we do not expect companies to suddenly change strategies in a particular year.

Additional Analyses—CSR Topics and Variations in Firm Rhetorical Strategies.

Note. All other variables are defined in Table 3. Robust standard errors in parentheses. CSR = corporate social responsibility.

The number of observations dropped due to a perfect correlation caused by firm and year fixed effects. Social, environmental, and ethical indicate the topic to which the tweet is related.

p < .1. **p < .05. ***p < .01.

As shown in Specification 1, the likelihood of using a denial strategy when replying to environmentally related involuntary disclosures was lower than it was for involuntary disclosures related to economic issues, whereas the responses to involuntary disclosures related to social and ethical topics had a higher likelihood than did economic involuntary disclosures. The likelihoods of an evasion (Specification 2) or a mortification strategy (Specification 5) were lower for social, environmental, and ethical involuntary disclosures than they were for economic tweets. According to the result of Specification 3, for the social and environmental involuntary disclosures, the likelihood of the reducing offensiveness strategy was lower than it was for the economic tweets. Moreover, the likelihood of using a corrective action strategy (Specification 4) when responding to involuntary disclosures related to environmental and ethical topics was higher than it was for economic topics.

In sum, the results indicate that companies are more likely to use a denial strategy for social topics and less likely to use other rhetorical strategies in their responses to involuntary disclosures than they are in their responses to economic topics. For environmental topics, companies are more likely to use a corrective action strategy than they are to use other strategies. Finally, for ethical topics, companies are more likely to reduce the offensiveness of the event or to use a corrective action strategy than they are for economic topics, but they are less likely to use denial, evasion of responsibility, and mortification as their rhetorical strategies in response to involuntary disclosures. Overall, the results indicate that companies are likely to choose different communication strategies in their responses to involuntary disclosures related to various CSR topics.

Discussion and Conclusion

In this study, we examine the communication dynamics of company–stakeholder interactions after involuntary disclosures are made on SM. We first investigated how firms respond to involuntary disclosures made on SM by analyzing the rhetorical strategies and language tone used in corporate replies. Our findings show that companies are generally more reluctant (with some exceptions) to engage in persuasive conversation with stakeholders. When a company responds to involuntary disclosures, it is likely to use a mortification communication strategy, followed by the denial and reduction of the offensiveness of the event strategies. Combining the latter two strategies as a form of dissent to involuntary disclosures, companies are more likely to disagree with than to propose corrective action to the disclosures. Regarding tone, our results show that firm replies were mostly positive, supporting the view that companies are more likely to downplay the seriousness of involuntary disclosures through positive messages (Cho et al., 2010). These results indicate that, for involuntary disclosures made on SM, companies prefer either to acknowledge an issue and ask stakeholders for “forgiveness” or to dispute the revealed information (by denying or reducing its offensiveness). The use of the mortification strategy suggests that companies may see involuntary disclosures as potentially crisis-generating (Muralidharan et al., 2011); thus, they prefer to de-escalate the claim rather than to engage in further dialogues with stakeholders. Our empirical evidence also shows almost equal chances of a company reacting to involuntary disclosures by denying or reducing offensiveness. In contrast, proposing corrective action is one of the least used responses. These findings suggest that companies have little intention of considering involuntary disclosures seriously and making a real change after they are made.

Next, we examined how stakeholders react to firm replies to involuntary disclosures. We find that in general, firm responses to involuntary disclosures are likely to resonate with the public, as stakeholders were likely to continue to engage by replying to or retweeting a message, but they were less likely to simply press the “like” button. Stakeholders did not engage with companies’ responses if mortification was chosen as a rhetorical strategy to an involuntary disclosure. At the same time, stakeholders were more likely to respond to firm communication by replying to the company’s tweet when denial was the company’s communication strategy to an involuntary disclosure. When the denial strategy was used, stakeholders were also likely to share the firm response with their Twitter network. This finding does not necessarily mean that stakeholders appreciate how companies respond to involuntary disclosures. The reply may be generated because stakeholders disagree or think greenwashing is taking place. Stakeholders were also likely to share, but not reply to, corporate tweets when evasion of responsibility was the strategy chosen by the company in reaction to an involuntary disclosure. At the same time, stakeholders were less likely to press the “like” button when reduction of the offensiveness of the event was the rhetorical strategy used for the initial involuntary disclosure. Overall, the above results suggest that two streams of communication exist on SM—one belonging to companies and another belonging to stakeholders (Gómez-Carrasco et al., 2021; Manetti & Bellucci, 2016).

While firms’ choices regarding their responses do not seem to support real engagement in two-way communication, stakeholders also fail to follow up on firm communication to exert pressure for real change—even though they are not reluctant to make involuntary disclosures. This finding is intriguing, as stakeholders seem more likely to make involuntary disclosures for the sake of information only, without much expectation regarding the reaction of the company. As a result, they miss the opportunities provided by SM, which offers a convenient and relatively fast communication medium for both senders and receivers to initiate sustainable changes within firms. Therefore, we argue that both parties (i.e., companies and stakeholders) should play a role in materializing involuntary disclosures into sustainability-related outcomes (Hahn et al., 2020). While we cannot ascertain why stakeholders failed to take follow-up actions, future studies may investigate stakeholders’ motives behind involuntary disclosures on SM through experiments, interviews, or analyzing their tweets using the classification scheme proposed in Saxton and Waters (2014).

In addition, we examined the involuntary disclosure types by dividing them into different CSR themes (social, environmental, ethical, and economic), as different types of involuntary disclosures may have different behavioral outcomes in regard to enhancing sustainability (Hahn et al., 2020). Our results indicate that companies are more likely to use the mortification and evasion of responsibility strategies in the case of involuntary disclosures related to economic issues than they are for other disclosure types. At the same time, companies are more likely to use denial as a response strategy for social disclosures than they are in response to economic disclosures and to reduce the offensiveness of the event in response to ethical issues raised in involuntary disclosures. Hence, our findings suggest that companies have certain preferences regarding the use of rhetorical strategies in responding to different types of CSR issues raised. Companies may consider social and ethical issues to be more important than economic issues when building and/or maintaining their reputation. Thus, our findings support the view that companies are less willing to take a dialogic approach in forging a democratic consensus on how to address specific sustainability issues (Manetti & Bellucci, 2016). Instead, SM is mainly used by companies to legitimize their presence in society and maintain the status quo on sustainability outcomes (Cho et al., 2010). Therefore, future research may explore how firm behaviors may differ when stakeholders strategically choose involuntary disclosure topics that firms consider material.

Our findings also bring an interesting debate as to whether involuntary disclosures on SM can become an effective mechanism for initiating sustainable change within firms. SM changes how evaluations about organizations in the public domain are organized, supplementing the traditional vertical, top-down and one-to-many diffusion by horizontal, bottom-up coproduction (Etter et al., 2019). Indeed, prior studies document that SM has emerged as a public arena of citizenship where corporate sustainability issues can be reported, discussed, and debated by stakeholders (Whelan et al., 2013). Undoubtedly, involuntary disclosures made by stakeholders on SM can be a powerful tool to expose possible irresponsible corporate activities, empowering stakeholders to influence share prices (Gómez-Carrasco & Michelon, 2017) and organizing campaigns targeting corporate behaviors (She, 2022). Given the potential ability of stakeholders to undermine corporate greenwashing, SM is expected to make companies sincerely commit to sustainability (Lyon & Montgomery, 2013). On the contrary, some studies question the ability of SM to advance sustainability as companies continue to engage in one-way dialog with stakeholders (Bellucci & Manetti, 2017; Gómez-Carrasco et al., 2021; Okazaki et al., 2020), while stakeholder voices on SM do not seem to serve as an impulse for positive social change (Neu et al., 2020). While our findings are largely aligned with the latter view that involuntary disclosures on SM may have limitations in initiating sustainable changes within firms, some of our results also seem to provide evidence that some firms are more willing to respond in a persuasive way to stakeholders than others. For example, Nestlé is far more active in responding than HP. This may be due to the possibility that Nestlé may respond to messages they consider urgent in terms of being time-sensitive and critical and may perceive a message as a threat to their value or legitimacy. Saxton et al. (2021) refer to this phenomenon as “stakeholder urgency,” in which stakeholder power and firm connecting power can influence (although in opposite directions) firm responses to stakeholder messages. While companies sometimes may not take individual stakeholders’ disclosures seriously, the mobilization of a large number of involuntary disclosures via SM may also create collective power to draw companies’ and potentially other stakeholders’ attention (She, 2022), thus resulting in different behavioral outcomes. While our study provides evidence on whether involuntary disclosures may influence firm behavioral outcomes as reflected in the use of rhetorical strategies, future research may shed more light on this issue by investigating the conditions under which involuntary disclosures may result in different firm behaviors and whether involuntary disclosures can indeed generate real impacts on firm sustainability outcomes.

Our article also offers some practical implications about how to shape communication strategies after involuntary disclosures are made. We support Saxton et al.’s (2019) suggestion that managers should be careful in determining how they draft their communication strategies on SM. Among the many rhetorical strategies used by managers, denial attracts shareholders’ reactions the most.

Like all empirical studies, ours is not without limitations. First, we analyzed communication in relation to involuntary disclosures only on Twitter. The use of other SM platforms may require different communication-management strategies; thus, the interaction patterns between companies and stakeholders may be different. We also examined corporate tweets for seven companies. While we aimed to select the most active companies on Twitter with the highest interaction levels with sustainability-related posts, we acknowledge the possibility of a biased sample given that this choice was arbitrary, which precludes the generalization of the results. Finally, we analyzed involuntary disclosure as a homogeneous group of disclosures without distinguishing between presenting facts or fake news, such as rumors or insinuation.

Given these limitations, further research could investigate stakeholder–company communications in relation to involuntary disclosures conducted on other SM platforms (such as LinkedIn or Facebook) and a different sample. As we focused only on firm replies to involuntary disclosures and stakeholder subsequent reactions to these replies, future studies may employ a larger data set and more sophisticated machine-learning algorithms to identify potential involuntary disclosures and track the subsequent multistep communications to obtain more insights into what information is being disclosed, the communication dynamics, and stakeholders’ motivations in disseminating such information. Further studies may also deepen our understanding of the differences in the rhetorical strategies used by companies in the case of shareholders disclosing facts or fake news as well as for different topics of involuntary disclosures. Finally, researchers could employ alternative methods, such as in-depth case studies, to explore the challenges companies face when managing involuntary disclosures on SM. Given that SM has become an integral part of everyday life, the role it plays in communication between companies and their stakeholders and how it enhances public engagement are certainly worthy topics of further scientific inquiry.

Footnotes

Appendix 1

Keyword Examples Used to Identify CSR-Related Tweets.

| CSR category | Examples of keywords and tweets |

|---|---|

| Social | accident, AIDS, award, bargaining, benefits, biased, breastfeed, Cambodia, care, career, careers, child, children, citizen, citizens, citizenship, citizenships, collaboration, collective, communities, community, consumer protection, crew, crews, CSR, cultural projects, customer voice, development, developments, dictator, disability, disable, discrimination, disease, educate, education, educational, educations, elderly, employ, employabilities, employability, employee, employees, employment, employments, engagement, engagements, equality, famine, fatalities, fight, food security, forced, foundations, freedom, future of fashion, gay, gays, genocide, government, health, HIV, homosexual, human, hunger, inclusion, indigenous, injuries, injury, intern, internship, internships, involvement, involvements, labor standard, labor, labour, lesbian, lesbians, lgbt, lgbtq, local, malnutrition, maternal, maternity, medical, medicine, medicines, obesities, occupation, occupational, paid, parental, paternal, paternity, pay, pays, people, petition, political, poverty, prejudice, pride, profession, professional, racism, refugee, remunerated, remuneration, remunerations, responsibilities, responsibility, retire, retirement, rights, safe, safety, salaries, salary, satisfaction, school, skill, skills, social exclusion, social philanthropy, social, societal, society, solidarity, staff, student, students, team, teams, training, trainings, transparency, transparent, UN, UNICEF, unions, united nations, veteran, veterans, visions, volatility, voluntary, volunteer, volunteered, volunteering, volunteers, wage, wages, welfare, worker, workers, working conditions, workplace, etc. Example of tweets: • H&M supports a fair living wage. We believe that wages should be set by negotiation. • @pogopaule we strongly oppose all forms of violence; believe everyone should earn a fair wage. • Hi. We continue to support our suppliers in improving production facilities to safer/higher standard. |

| Environmental | animal, bio, carbon, chemical, circular, climate, climate change, CO, deforestation, earth, ecological, ecology, emission, endanger, energy, environment, environmental, rainforest, GIZ industry, global warming, Greenhouse, organic, palm oil, planet, plastic, pollution, recycle, recycling, reforestation, renewable, resources, sandblast, sustainability species, wastage, waste, water, water waste, WWF, etc. Example of tweets: • @2degreesnetwork H&M works to ensure zero discharge of hazardous chemicals by 2020 across our entire value chain. • Nestlé is working with partners and industry associations to explore different packaging solutions – to reduce plastic usage, facilitate recycling and eliminate plastic waste. • HM shopping bags are made from recycled polyethylene (PE). |

| Ethical | abuse, accountability, accountable, angora, Bangladesh, child labour, code of conducts, compliance, copyrights, corrupt, corruption, Daewoo, disclosure, ethic, ethical, ethics, ethnic, fair trade, governance, harassment, human rights, moral, norms, omo valley, prevention, rana plaza, sexual, slave, slavery, Terry Richardson, test on animals, transparency, underage, etc. Example of tweets: • @charlesletbette H&M doesn’t accept child labour. Read about the recent action taken in a Turkish supplier factory • @becomethebullx Currently we’re not working with Terry Richardson and have no planned campaigns with him. • @cliffsull H&M has never had any production in any of the factories situated in Rana Plaza. |

| Economic | charitable, charities, charity, compensate, compensated, compensation, contribute, contributions, credit, donate, donated, donation, entrepreneurship, finance, financial aid, financial support, financial, foreign aid, fund, funding, funds, microcredit, microfinance, monetary aid, scholarship, sponsor, sponsored, sponsorship, etc. Example of tweets: • @erick_j96 We regularly donate to other people in need. Please visit http://www.hm.com/csr for further details. • Hi. We’re currently involved with specific charities, this means we are unable to commit to individual causes. • Hi, we’ve never stopped helping Flint. We’ve been providing water donations & financial resources to the Flint community since the beginning of the crisis in 2015. |

Source. Own elaboration based on Okazaki et al. (2020) and She and Michelon (2019).

Note. CSR = corporate social responsibility.

Appendix 2

Examples of Stakeholder Tweets Containing Involuntary Disclosures.

| Company | Tweet content |

|---|---|

| H&M Group | True cost of Fast fashion profits: $5 @hm shirts drive down wages to $2/day, create unsafe wk environments. 1,129 killed in 2013 #ranaplaza |

| 13yr old child in Bangladesh killed in textile factory he worked in. Ask @Asda @HM & @UKGap to prove it’s not theirs | |

| Surprise! @hm factories in Myanmar employed 14 yrs old workers | |

| Nestlé | Thirsty? @Nestle steals water to sell it back to you - Profit over people |

| Please don’t buy Easter eggs made by @nestle @cadburyuk contains #killerpalm oil | |

| Children are enslaved to enable @Nestle to sell their chocolate |

Appendix 3

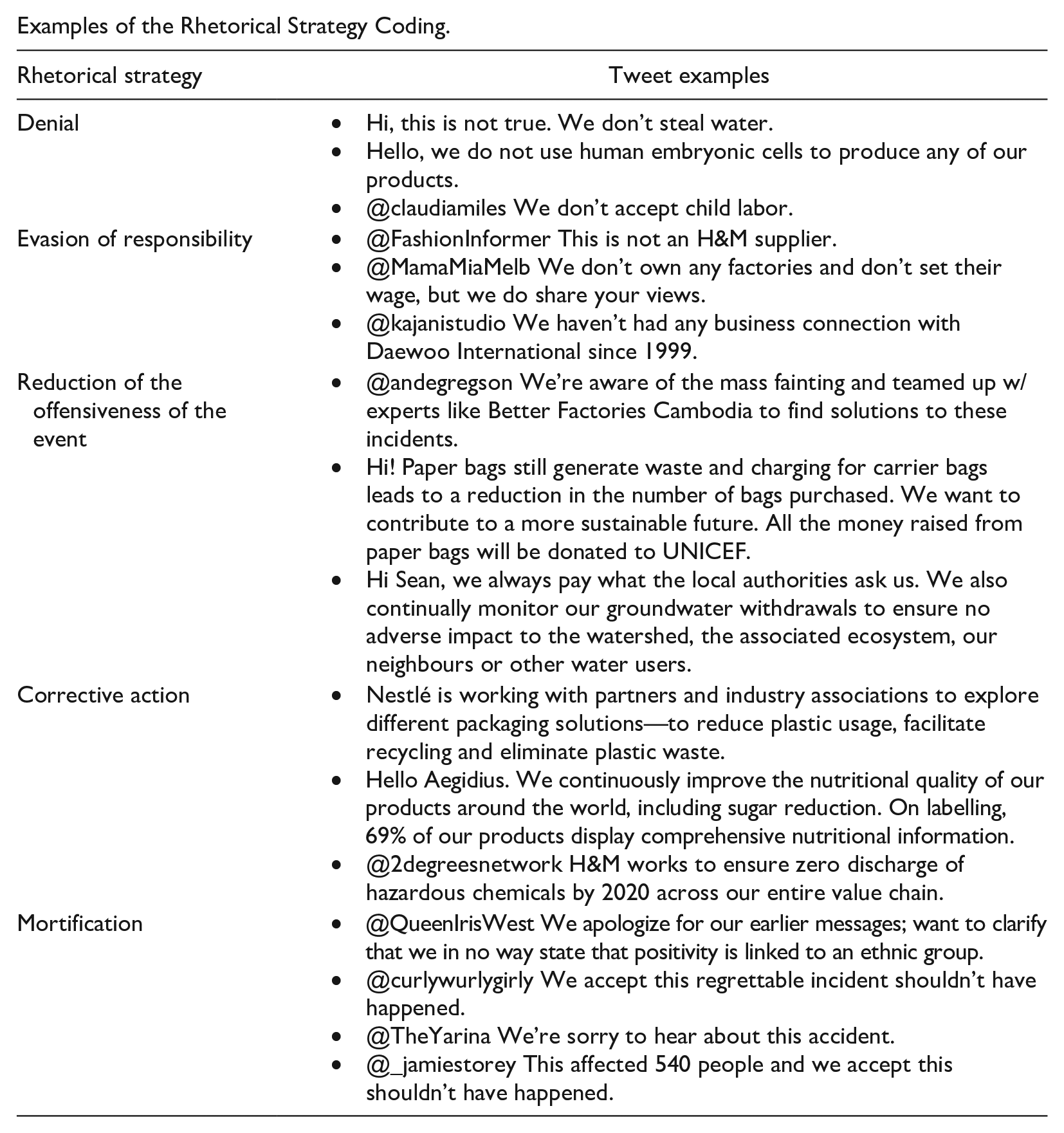

Examples of the Rhetorical Strategy Coding.

| Rhetorical strategy | Tweet examples |

|---|---|

| Denial | • Hi, this is not true. We don’t steal water. • Hello, we do not use human embryonic cells to produce any of our products. • @claudiamiles We don’t accept child labor. |

| Evasion of responsibility | • @FashionInformer This is not an H&M supplier. • @MamaMiaMelb We don’t own any factories and don’t set their wage, but we do share your views. • @kajanistudio We haven’t had any business connection with Daewoo International since 1999. |

| Reduction of the offensiveness of the event | • @andegregson We’re aware of the mass fainting and teamed up w/ experts like Better Factories Cambodia to find solutions to these incidents. • Hi! Paper bags still generate waste and charging for carrier bags leads to a reduction in the number of bags purchased. We want to contribute to a more sustainable future. All the money raised from paper bags will be donated to UNICEF. • Hi Sean, we always pay what the local authorities ask us. We also continually monitor our groundwater withdrawals to ensure no adverse impact to the watershed, the associated ecosystem, our neighbours or other water users. |

| Corrective action | • Nestlé is working with partners and industry associations to explore different packaging solutions—to reduce plastic usage, facilitate recycling and eliminate plastic waste. • Hello Aegidius. We continuously improve the nutritional quality of our products around the world, including sugar reduction. On labelling, 69% of our products display comprehensive nutritional information. • @2degreesnetwork H&M works to ensure zero discharge of hazardous chemicals by 2020 across our entire value chain. |

| Mortification | • @QueenIrisWest We apologize for our earlier messages; want to clarify that we in no way state that positivity is linked to an ethnic group. • @curlywurlygirly We accept this regrettable incident shouldn’t have happened. • @TheYarina We’re sorry to hear about this accident. • @_jamiestorey This affected 540 people and we accept this shouldn’t have happened. |

Acknowledgements

The authors wish to thank the guest editors, two anonymous reviewers, Elisavet Mantzari, Claudio Columbano, and participants of the IAAER-ACCA Paper Development Workshop hosted by the Bucharest University of Economic Studies the 2021 Alternative Accounts Europe Conference held at Queen Mary University of London’s School of Business and Management, and the (virtual) Paper Development Workshop (PDW) for the Special Issue for their helpful feedback, comments and suggestions.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The authors would like to acknowledge the financial support provided by the National Science Centre, Poland (Grant No. 2019/33/B/HS4/00998). C.H.C. also acknowledges the financial support provided by the Erivan K. Haub Chair in Business & Sustainability at the Schulich School of Business.