Abstract

Land value capture is an underutilized and sometimes misunderstood component of urban policy. In this article, we develop a conceptual framework to compare four approaches to land value capture—land and property taxes, real estate transfer taxes, betterment levies, and development charges. Given that urban land values arise from collective action, local governments should tax this wealth to fund public infrastructure. However, local governments confront technical and political challenges in properly applying different land value capture mechanisms, which also vary substantially in equity and efficiency. Using Mexico City as a case study, we propose a conceptual framework to assess the technical and political challenges of the design components of land value capture mechanisms, as well as their impacts on equity and efficiency. We find that technical challenges to land value capture appraisals have substantially diminished and are surmountable, yet political challenges remain. The proposed conceptual framework facilitates a comparative approach to guide planners and policymakers toward more equitable and less distortionary land value capture strategies. We argue that land value capture mechanisms should not be dismissed as viable solutions due to the shortcomings of past implementations. Instead, scholars can use the proposed framework to identify a mechanism's limitations and propose better policy.

Introduction

Cities concentrate economic opportunities, cultural activities, and public services, creating social and economic value for urban land. However, much of this created value accrues to property owners and does not circulate back into the society that creates it. This has led many scholars to argue that local governments should capture rising land values to fund services and infrastructure, especially when the value results from public and collective action (Bird and Slack 2007; Smolka 2013). Yet land value capture mechanisms are technically and politically challenging to implement. The way local governments calculate their tax base, collect, administer, and use funds influences both the effectiveness of these mechanisms and the challenges that arise in implementation.

In this paper, we examine the four most prevalent land value capture mechanisms: (a) property and land taxes, (b) real estate transfer taxes, (c) betterment levies, and (d) development charges. 1 We propose a conceptual framework with seven design features to describe the mechanisms. The framework allows us to identify distinct technical and political challenges for each mechanism, contrast their equity and efficiency, and assess the degree to which they align with Henry George and John Stuart Mill's vision of land-based strategies that tax the “unearned increment” of land value (Mill 1848; George 1895, 359). 2 We apply the framework to four mechanisms in Mexico City.

We select Mexico City as our case study for four primary reasons. First, the city employs a diverse array of mechanisms to tax land and property, both directly and indirectly. Nonetheless, like most cities, Mexico City has not taken full advantage of the mechanisms at its disposal to leverage its substantial property wealth for public benefit. Third, Mexico City is the capital of a centralized country, and thus is the site of significant economic activity representing 15% of the national GDP (INEGI 2023). The high demand to live in the city has resulted in a consistent increase in property prices, leading to the out-migration of lower-income residents to peripheral municipalities (INEGI 2020). 3 Finally, Mexico City has a long history of social mobilization for public service provision and claims-making for reduced tax burdens (Moctezuma 1984; Davis 1994).

Through our analysis of Mexico City, we argue that the underutilization of land value capture is less of a technical problem than a political one. We also show how our conceptual framework can be used to analyze and diagnose the application of land value capture mechanisms. The proposed framework can be used in future scholarship to compare different land value capture mechanisms in the same city or the same mechanism across different cities.

Literature Review: Principles of Land Value Capture and Its Challenges

Local governments around the globe draw on land value capture mechanisms to strengthen local revenues and fund projects (Smolka and Amborski 2000; Ingram and Hong 2007; Medda 2012). The premise is that unlike agricultural land, which derives its value from inherent agricultural potential and location, the value of urban land comes from the collective efforts of a city's residents, public investment, and market conditions. 4 Indeed, land value is the principal driver of the global rise in housing prices (Knoll, Schularick, and Steger 2017). Thus the capture of land value by individual landowners, rather than a city government, exacerbates social inequalities by further concentrating wealth among the property-owning class.

Nineteenth-century political economist Henry George advocated for a “single tax” on land as the most effective and equitable way to address growing inequality in the United States. His proposal is rooted in the philosophical principle of redistributing the benefits of land ownership back to the community that creates its value. Despite critiques of being too reformist or not sufficiently challenging existing property institutions (Wolf-Powers 2024), land taxes capture the positive externalities of property ownership within a community, without penalizing the actions (i.e., development on that land) that benefit society. If land value depends on social action as well as its scarcity, land taxes will not distort behavior in the use of land or its supply, and even promote socially beneficial uses (Stiglitz 2015; Schwerhoff, Edenhofer, and Fleurbaey 2022). These attributes support the broad consensus that land value taxes are efficient, equitable, and superior to alternative fiscal instruments (Arnott and Stiglitz 1979; Garza and Lizeri 2016; Bonnet et al. 2021).

Local governments implement land value capture mechanisms in distinct forms and designs. Alterman (2012) classifies land value capture mechanisms into three categories: direct, indirect, and macro. Direct value capture tools refer to those that intentionally seek to capture the unearned increment of land value. Indirect value capture tools arise from practical motives, such as collecting revenue for government services, but unintentionally capture some of that untapped value. According to this definition, a single mechanism can be either direct or indirect depending on its design. Betterment levies can be a direct value capture mechanism if they are calculated based on projected land value increases, but an indirect mechanism if they are calculated based on the cost of projected impacts or infrastructure costs. An example is the 2012 Mayoral Community Infrastructure Levy that London introduced to fund the Elizabeth Line. The city applied this levy to planning permissions for new developments and the rate varied depending on the proximity to the new rail line. In its design, this tax represents an indirect land value capture tool. Finally, Alterman's macro instruments are those embedded in broader land governance systems such as land banking and readjustment.

The design of land value mechanisms impacts not only whether they collect value directly or indirectly, but also the technical and political challenges they face when implemented. Inadequate design of land value capture mechanisms by local governments can reduce their efficiency, as well as their positive impacts on equity. For example, the implementation of tax increment financing in the United States has been criticized for giving too many concessions and benefits to private developers at the expense of taxpayers, as well as increasing intermunicipal inequality (Fisher, Leite, and Weber 2023; Mason and Thomas 2010). 5 Jaramillo (2001) also questions the potential of Colombia's betterment levy in capturing land value increases. He argues that measures implemented to mitigate property owner opposition, such as caps on charges, and formal channels of complaint have decreased the revenue-generating potential of the mechanism and increased the costs to use it.

The most critiqued design component is the way the tax base is calculated. Appraising land and property value is the first task for local governments aiming to tax it. The amount of revenue collected from land and property taxes is a result of the tax rate applied, but also, and perhaps more importantly, the value of the tax base and the degree to which the government's assessment matches market values (Youngman and Malme 1994; Slack and Bird 2014). Depending on what is being taxed (land alone or land and structures on it), the tax rate applied, and when the appraisal occurs, different types of valuation systems may be required. To effectively estimate a property tax, for example, local governments require periodic information about the market value of structures and land. Other mechanisms that directly capture land value, such as betterment levies, require property value appraisals before and after a public work to measure the increase in value (Jaramillo 2001).

The sale value of a property is the most accurate estimation of its market value (Berrens and McKee 2004; Ma and Swinton 2012). Since this is only available for recently sold properties, appraisals are estimates based on the sales of similar properties (Kokinis-Graves 2006). This approach is commonly used when sales information and property characteristics are readily available so they can be extrapolated to similar properties using a statistical model. This comparable pricing model is widely used to estimate appraised values internationally, including in some Latin American cities (Lozano-Gracia and Anselin 2012). A second, less common approach to appraisal relies on the cost of construction for new properties and applies depreciation to the structure in question. A third approach uses an estimate of the potential rental income that a property can generate, and then applies a capitalization rate to arrive at the value (Baum, Mackmin, and Nunnington 2017). This latter approach is more commonly used for commercial property, which is more likely to have an income stream.

Many cities intentionally keep cadaster assessments below market values, a practice referred to as fractional assessment (Sirmans, Gatzlaff, and Macpherson 2008; Hultquist and Petras 2012; Curto, Fregonara, and Semeraro 2017). For example, the city of Mérida, Mexico, applies an assessment rate of 80% to appraised values. In Bogotá, assessment rates range from 60% to 100% (Article 24 of Law 1450, Colombia). Fractional assessments can introduce unnecessary complexity to the tax calculation and undermine tax uniformity (Youngman 2016). Keeping cadaster values in line with market values ensures that the tax base closely reflects reality, which can reduce resistance from property owners. Basing cadastral values on accurate appraised values also makes property taxes more equitable by ensuring that taxes reflect the true value of each property (Peña-Medina 2016; Berry 2021).

The technical challenges to implementing precise and effective land value capture mechanisms have rapidly decreased because of information technology. However, the implementation and management of land value mechanisms depends on local politics, which often limit their effective implementation. Each mechanism and form of implementation involves a different constellation of actors and stakeholders with diverse interests and views (Wang 2022; Canelas and Noring 2022). Wang, van Noorlos, and Spit (2020) develop a conceptual framework to map out the power relations of different stakeholders in the implementation of land sales in countries with public and private legal frameworks. Their analysis works through the abstraction of land value capture by focusing on land sales and the role of local government, as well as land buyers and sellers. This approach is helpful in obtaining a conceptual understanding of the conflicts and interests in land transactions, but it omits the role of local politics.

Political science research demonstrates that powerful interest groups, such as wealthy landowners, use their influence to limit the capacity of land value capture mechanisms. For example, Sánchez-Talanquer (2020) demonstrates that in Colombia, powerful landowners have historically used their political influence to keep cadaster values artificially low to reduce their property tax burden. Electoral incentives also influence local government decisions of how to capture land values (Christensen and Garfias 2021). Incumbent local government officials wary of potential political costs are less likely to update cadaster bases than officials not seeking re-election (Christensen and Garfias 2021). Local bureaucrats, such as directors of planning offices, cadaster offices, and local revenue offices, may support, and benefit from, increasing revenue collection, but lack political power.

Powerful interests that keep property taxes low face little opposition from the general population, who often view any tax increase as a threat, even when they are not directly affected or could benefit from improved services and infrastructure (Musgrave 1979; Slack 2012). Additionally, even if only a small percentage of property owners would be negatively affected by an increase, they may make use of media campaigns to extend their impact and block any potential implementation of land value capture mechanisms or tax increases. Probably the most studied case of property tax resistance is the 1978 California tax revolts in which White, high-income property owners mobilized to pass a proposal that would benefit them, a minority, and negatively impact renters, new property owners, and low-income individuals that relied on public services, a majority (Sears and Citrin 1982, 220). City officials could reduce the opposition from local populations by better communicating how funds are used and making clear who would ultimately pay the charges imposed. Despite the centrality of politics in the management and implementation of land value capture mechanisms, it is often neglected in planning scholarship.

Conceptual Framework: Equitable and Effective Value Capture

We propose a conceptual framework with two objectives. The first is to analyze how the design of a land value capture mechanism introduces technical and political implementation challenges. The second is to identify the equity and efficiency impacts of each feature of the mechanism. This conceptual framework is a useful tool for analyzing and comparing different land value capture mechanisms, identifying their limitations, and making decisions about their trade-offs. Through this framework, we emphasize the multidimensional character of taxes and show how variation in design creates opportunities and challenges. Future scholarship can adopt this framework to assess the barriers that land value capture mechanisms and other taxes encounter to improve policy.

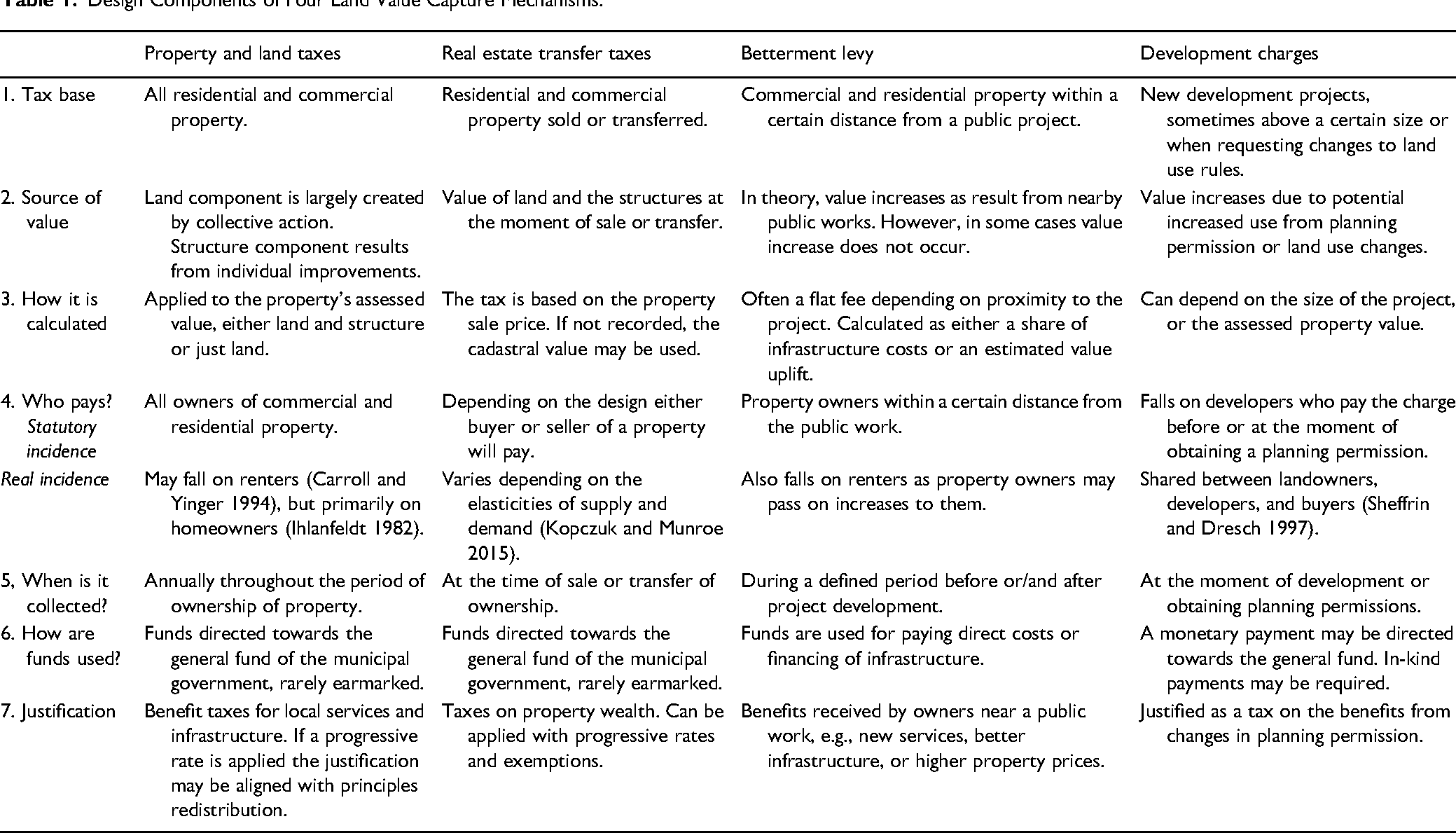

Our analysis is organized around a two-axis matrix. One axis delineates the seven design features of the mechanisms: the tax base, the source of value, the method of tax calculation, who pays the tax (both statutory and real incidence), the timing of tax collection, the use for the collected funds, and the rationale for the tax. We define these features based on how governments determine the collection and allocation of revenue. Table 1 presents the design features for the four land value capture mechanisms.

Design Components of Four Land Value Capture Mechanisms.

The horizontal axis of our conceptual framework covers the political and technical implementation challenges, as well as the impacts on equity, and efficiency of each design feature. In Table 1 in Appendix 1 in the supplemental material, we apply our conceptual framework to the four land value capture mechanisms.

The first dimension is the tax base-which properties are taxed and on what basis. Property taxes have the broadest and largest base since they generally apply to all individual property owners irrespective of the services they may receive from the government. This broad application mitigates political challenges in part, because the government does not select specific properties for taxation, unlike with betterment levies, which confront challenges in assessing who benefits and therefore who pays. If the benefits of a project extend beyond the immediate property owners, justifying taxation may be a challenge. Conversely, mechanisms like development charges are popular as they specifically target developers. However, they disrupt comprehensive planning practices if used as a bargaining tool for land use changes (Monkkonen and Manville 2019; Kim 2020).

The second dimension is the source of the value that is taxed. An ideal and efficient land value capture mechanism directly targets the unearned increment in land value. However, many mechanisms do this only indirectly. For instance, proponents of development charges argue that these charges indirectly tax land by reducing pre-development land values (see Sheffrin and Dresch 1997 for a discussion). However, in urban areas with low elasticity of supply and demand, owners of properties with established uses will likely resist accepting lower prices for properties. Thus, local governments will collect less tax than expected due to reduced development and buyers will bear a larger share of the tax burden.

The incidence of the development charge, that is, whether it is paid by developers, future buyers, or landowners depends on elasticities of supply and demand. Nonetheless, because development charges tax land that is being put to a new use, they do not apply to the vast majority of landowners, thus generate limited revenue and can lead to unproductive land uses and insufficient housing development (Manville 2021; Monkkonen 2023).

The focus on land and property as the primary source of value raises equity concerns. Some scholars contend that relying on land values for revenue might lead local governments to view land and property as commodities for monetization (Wolf-Powers 2024). This could incentivize governments to deliberately maintain or increase property values. Atuahene (2018) suggests that the overvaluation of property in Detroit by local authorities has led to widespread property tax foreclosures due to low-income residents’ unfamiliarity with appeal processes (1503). Similarly, LaPoint (2023) points out that property tax foreclosures driven by the D.C. local government have facilitated the transfer of property from low-income, Black and Latino residents to large-scale property developers. However, most property tax systems do not foreclose on owners who cannot pay, using a lien on the future sale of the property instead.

The third dimension is the method used to calculate the tax, with a focus on valuation techniques. Ideally, governments should calculate betterment levies by assessing the property's value before and after the implementation of a nearby public work. However, measuring the exact value uplift that resulted from a public work is an imprecise practice because of the difficulties in quantitatively assessing the true impact of a project on property values (Jaramillo 2001, 80). Thus many cities resort to using the actual cost of the public work or cadaster values at the end of project implementation as the base for calculating betterment levies. In Mexico City, for example, government calculates betterment levies based on both the total cost of the public work, the distance of a property from the public work, and the cadaster value of the property. Lack of clarity in the connection between value uplift and charges applied can create backlash from those being taxed as they can argue unfair treatment. Development charges can also be calculated through consistent formulas or negotiation agreements, the latter can facilitate corruption as local elected officials can seek to monetize their decision-making power (Finnegan 2022).

The fourth dimension is both the statutory (literally who pays) and real incidence (where the burden falls). No matter who pays a real estate transfer tax its real incidence falls on both buyers and sellers, as the tax affects the price a buyer pays and what the seller receives. How the incidence is split depends on the relative elasticities of supply and demand and therefore varies across markets (Kopczuk and Munroe 2015). The incidence of development charges is difficult to measure. Proponents argue that it falls on landowners, as it reduces land prices. However, the extent to which developers pass the charge to landowners, reduce their own profits, or pass it to future homebuyers or renters depends on market conditions such as changes in demand, the landowners’ ability to hold out, and competition in the building industry (Sheffrin and Dresch 1997). Property taxes also raise questions about the distribution of the tax burden. Property taxes don’t only impact homeowners, but also renters who pay a portion of property taxes directly through their rent (Carroll and Yinger 1994).

Determining who pays and who doesn’t introduces political and technical challenges that affect both equity and efficiency. For instance, determining the geographic zone of impact for a betterment levy, and therefore who is charged, does not have a straight-forward formula. The positive impacts of a public work may extend to properties outside of the zone of impact. This makes the government's definition of the “impact zone” consequential and can jeopardize project feasibility. What may seem like a technical matter could spark political opposition.

The next dimension is the time during which the government applies and collects the tax. It can be continuously (annually), at the time of development approval, or at sale. The timing also introduces technical and political challenges. For instance, real estate transfer taxes encounter less technical challenges because they are applied at the time of a property transaction when it is technically easier to obtain accurate sale values and politically easier because taxpayers have increased liquidity, and the tax can be factored into the transaction price.

In contrast, the annual character of property taxes prompts political and technical challenges. Property owners may find the constant increase in their assessed value as unjustified, thus creating political resistance. Tax increases driven by rising housing prices, inflation, or long periods between assessments can provoke push-back from property owners, a group that tend to be politically active (Yoder 2020). Protests for unfair property tax assessments are common throughout Latin America (Zapata, Lucia and Agudelo Cano 2019). For example, in 2024, property owners in the Metropolitan Area of Bogotá blockaded major city streets to protest what they perceived as unjustified increases to their cadaster assessments. (Espinoza Mejia 2024). In extreme cases, increasing property taxes may force owners to sell if the local government doesn’t implement mitigation measures, such as deferred payments or limits on annual increases (Martin and Beck 2018). Technically, the challenge lies in the need for governments to manage increases in property assessments to prevent abrupt jumps in tax bills.

The sixth dimension is how local governments utilize tax revenue collected. For instance, development charges may be levied to create a public benefit from upzoning, but payments collected may not reflect this objective. For example, developers in Mexico are often required to donate a share of project's land to the municipality. Even though in theory these donations are supposed to be used to provide green areas and infrastructure, they often end up as vacant lots throughout the city (Pérez-Medina and López-Falfán 2015). Moreover, communities neighboring development projects may not be involved in the decision-making on the use of funds collected from development charges. Involving local residents in decisions about fund allocation may mitigate resistance (Robinson and Edwards 2013).

The final dimension considers how the local government justifies the imposition of each mechanism, a critical factor influencing political opposition. For instance, property taxes are often framed as a fee collected for service and infrastructure benefits owners receive, but the calculation includes the physical characteristics of a property (such as materials, lighting fixtures, etc.). As a result, owners may argue that they are being penalized for improving their property and adding value to the neighborhood. Similarly, real estate transfer taxes might face political hurdles due to their ambiguous justification (Oldman et al. 1967). In most cases, these taxes aren't tied to specific benefits but rather to the act of transferring property.

Applying this framework to compare four different land value capture mechanisms presents four insights. The degree of political resistance faced by each mechanism varies and is largely influenced by the clarity of the link between payments and benefits. A weak connection often prompts opposition from property owners and creates inefficiencies. Additionally, political challenges can affect the technical precision of these taxes. For instance, electoral considerations might influence how governments define tax bases, reducing the fairness and effectiveness of these mechanisms by making the taxes more regressive.

Land value capture mechanisms also encounter technical challenges depending on how the government defines the source of value (Youngman 1998). Mechanisms that directly tax land face greater technical hurdles, as distinguishing land values from structure values is cumbersome. This difficulty may lead to a simpler value calculation method, which could introduce further inefficiencies. The challenge of delineating values generated by the market, the government, and individual property owners may also fuel opposition to the implementation of these taxes if not adequately addressed.

Furthermore, these taxes could be more equitable if combined with avenues for participation. This problem is particularly pronounced with one-time, project-specific fees such as betterment levies and development charges. Property taxes may also deepen inequities if revenue generated from this source is allocated in a hyper-local manner without mechanisms for redistribution.

Mexico City Background

A surge of recent international and national media stories has drawn global attention to Mexico City's high housing prices (Vaquero Simancas 2024; Hernandez 2023; Shortell and Cegarra 2022). These recent news stories center on growing gentrification and the influence of foreign, remote workers on increasing housing prices in central city areas, many now unaffordable to local residents. However, Mexico City's property market has been characterized by high demand and insufficient housing production for decades. From 2006 to 2015 alone, housing prices increased over 100% in all the city's boroughs. Figure 1 in Appendix 3 in the supplemental material demonstrates housing price increase trends for each of the city's boroughs. Housing prices have steadily increased throughout the city from 2006 to 2015, with the highest value increases in the center and west of the city. Interestingly, the percentage of total property value attributed to land in the city increased from a median of 46% to 54% from 2005 to 2015, demonstrating that an increasing share of property prices results from social, rather than individual, action. 6

As property values continue to increase and demand for central city areas grows, the local government can leverage value-capture mechanisms to redistribute property wealth and lower property prices. Mechanisms like the property tax, which is collected and centralized at the city-wide level, rather than the Alcaldia, or borough level, can reduce inequality between neighborhoods if properly applied. Particularly, these funds could be used to bring the infrastructure and green spaces—factors that contribute to high land values in central areas—to peripheral zones.

The technical challenges to value capture have diminished substantially in Mexico City. In Appendix 2 in the supplemental material, we detail three strategies for obtaining appraisal values in the city and compare these to cadaster values. Political challenges, however, are substantial.

Mexico City is unique in that its constitution recognizes the social function of land and property at the local level, something included at the national level in Brazil and Colombia (Article 16, C). 7 Yet, like other large, historic cities, Mexico City, is a politically contested territory in which political and citizen groups often push back on and block policy reforms (Becker and Müller 2013; Gonzalez Malagon 2019). Additionally, the omission of well-integrated public consultations and participatory practices, as well as opacity in the management of planning mechanisms in the past has left the public wary of the use of new strategies for financing urban development and public works (Gonzalez Malagon 2019; Leipziger 2021).

The 2016 draft of Mexico City's new constitution considered a legal framework to facilitate direct capture of land value growth, which encountered significant opposition. Early drafts included a clause stating that any increase in land value resulting from public actions—such as planning permissions or nearby public works—was considered part of the city's public wealth. The clause's vagueness facilitated the media's ability to reinterpret its meaning, swaying public opinion against it. In the backlash, opponents claimed it constituted government overreach of private property (Azuela 2019). The public outcry contributed to the decision to omit any mention of value capture from the final version of the city's constitution, despite national legislation supporting the local implementation of these mechanisms. 8

This event revealed a general lack of understanding of the potential for land value capture mechanisms to fund urban services and infrastructure. Furthermore, it demonstrates a complete absence of communication strategies from the government on this topic. The experience captures some of the challenges that arise in attempts to introduce new, or modify existing, fiscal mechanisms based on land value and property.

Application of Conceptual Framework: Value Capture

The case of Mexico City highlights how in their implementation, the four mechanisms can differ from the philosophical principles of redistributing land wealth. Our conceptual framework can identify gaps in effectively capturing land value. In this section, we apply the conceptual framework to each of the city's four mechanisms to demonstrate how their design prompts technical and political challenges and impacts equity and efficiency.

Property and Land Taxes

Over recent decades, property taxes in Mexico City have evolved in response to political opposition from property owners and elected government officials. The tax base has received the most pushback. For example, from 1929 to 2008 rental properties were charged property taxes based on rental value, Base Renta (Oldman et al. 1967). In the early 2000s, property owners of rental properties argued that this tax base represented unequal treatment and was therefore unconstitutional. Based on this claim, they used a kind of legal protection called an amparo to justify nonpayment. From 2001 to 2004, property tax collection decreased by 8.5% as a result of these legal protections (Ciudad de Mexico 2008). The debate over the constitutionality of this tax base prompted the city to eliminate it in 2008.

The elimination of rental value as a tax base pushed local officials to modernize the city's cadaster and reassess property values. Spearheaded by Mayor Marcelo Ebrard and supported by the Spanish firm Corte Inglés, the city allocated $425 million pesos towards this initiative. The revised cadaster aimed to align more closely with market property values in order to make assessment fairer. However, the sudden increase in property taxes, particularly in affluent neighborhoods, sparked coordinated protests by property owners. Many objected to the perceived excessive hike, especially since the new tax system increased property values in some zones more than others. Property owners also voiced concerns about the lack of transparency in how the tax was calculated (Gómez and González 2008).

Past attempts to increase property taxes also faced opposition from political actors. In 2017, Mexico City's legislative assembly approved a reform to discount rates from a possible reduction of 1% per year of a property's antiquity to 0.8% a year, as well as to increase the cadastral value of properties above a certain value. 9 However, politicians from opposition parties challenged the constitutionality of these actions and raised the issue to the Supreme Court (Diario Oficial de la Federación 2022). Opponents argued that the changes would result in disproportional increases for certain properties, particularly older ones. The Supreme Court ultimately upheld the reform's constitutionality and cadaster value increases, yet this case illustrates the political frictions that surround making changes to cadaster base values, which should be an entirely technical exercise.

The question of who pays also creates challenges for property tax collection in the city. Tax compliance varies dramatically throughout the city and low tax compliance reduces total property tax revenue. 10 In 2022, wealthier boroughs such as Benito Juarez and Miguel Hidalgo reported the highest compliance rates at 77% and 76%, respectively. In contrast, lower-income boroughs like Milpa Alta and Tlahuac had compliance rates of 29% and 48%, respectively. 11 These are also among the boroughs with the highest levels of informality in the city. About 18%–21% of properties in Mexico City do not have property titles, but all property owners and even informal occupants of property are required to pay property taxes in Mexico (ENVI 2020; ENIGH 2022). It is therefore common for property owners without property titles to pay property taxes. According to 2022 survey data on household expenditures (ENIGH), 40% of property owners without formal titles reported to have paid their property tax, which is slightly below the rate of property owners with property titles (60%).

Brockmeyer et al. (2021) suggest that due to the high incidence of non-compliance in the city's poorest areas, strategies to boost property tax revenue should prioritize adjusting tax rates and assessments over increasing compliance. Low compliance rates in lower-income boroughs are likely the result of lower incomes and liquidity constraints.

Concerns for who pays are also evident in the subsidies and discounts on property taxes that the city offers to low-income populations. For example, properties valued below $1.3 million pesos (about $62,000 USD) are taxed at a fixed bi-monthly rate ranging from $63 to $102 pesos (2024). Meanwhile, properties valued between $1.3 million and $2.7 million pesos receive discounts ranging from 50% to 25%. Mexico City also offers discounts for seniors or individuals in vulnerable situations, such as single mothers with a dependent who has a disability. In 2021, the city gave nearly $684 million pesos in property tax subsidies (about 4% of collected property tax revenue). While these subsidies mitigate potential adverse effects on lower-income populations, their effectiveness is compromised by the widespread undervaluation of properties, which diminishes both the efficiency of the tax and its revenue-generating potential.

Mexico City calculates property taxes using highly progressive tax rates, reducing the need for subsidies. To give a concrete illustration, we applied the property tax rates of three different large Latin American cities—Bogotá, Colombia; Lima, Peru, and São Paulo, Brazil—to residential properties worth US$50,000, US$150,000, and US$700,000. We converted the value of tax paid to USD to facilitate comparison across different currencies and used the tax rates for 2022 or 2023. 12 From this analysis, detailed in Table 1 in Appendix 3 in the supplemental material, we find that the rates applied in Mexico City are slightly more progressive than those in other large Latin American cities. Mexico City does not apply a differential property tax rates to vacant lots or housing, which could increase revenue and promote more compact urban development.

Mexico City also manages property tax revenue differently than other cities across Mexico. The city is comprised of 16 boroughs which function like municipalities with a certain degree of autonomy. However, while in the rest of the country municipalities spend their collected property tax revenue within their territorial boundaries, Mexico City centralizes and redistributes this revenue across all boroughs. As a result, boroughs do not receive the revenue collected within their boundaries. Rather, distribution is based on a formula which considers total and floating population, poverty levels, urban area, and the extent of conservation area.

This centralized system redistributes wealth from boroughs with higher property values to those with lower values. Mayors of wealthier boroughs, such as Miguel Hidalgo, have disputed this system of redistribution, claiming that the wealthier borough is a “gold mine” for the city without seeing any of the benefits (Díaz 2023). The scale in which funds are collected and spent in Mexico City fuels political tensions that surround this tax and can contribute to low tax morale in high-income areas. Nonetheless, the centralization of funds in Mexico City enhances the tax's redistributive character, making it an important tool for reducing spatial inequalities in the city.

A significant weakness Mexico City's property tax system is the absence of explicit justification for property tax charges. In 2024, Mexico City's government carried out a publicity campaign which sought to promote property tax payments by highlighting how payments contribute to supporting the provision of important services like the metro (Figure 3 in Appendix 3 in the supplemental material). Additionally, tax receipts featured images of street paving and an accompanying message connecting property tax contributions to the continuous improvement of the city (Figure 3 in Appendix 3 in the supplemental material). Despite the importance of the campaign, its duration was short-lived and not continued for the 2025 collection cycle.

Applying our conceptual framework to property taxes in Mexico City shows that many of the implementation challenges stem from political, rather than technical factors. The city grapples with political hurdles in defining characteristics of the tax that, in theory, should be entirely defined through technical processes. Mexico City's government prioritizes equity in the tax system by providing discounts and subsidies to lower-income and vulnerable populations, however, undervaluation of properties diminishes the efficiency of these measures and reduces the city's revenue. Finally, due to their design, property taxes in Mexico City hold significant redistributive potential and can mitigate spatial inequalities throughout the city if applied properly.

Real Estate Transfer Taxes

Mexico City taxes the acquisition of a property through a real estate transfer tax known as the Impuesto sobre la adquisición de inmuebles (ISAI), which is generally paid by the buyer at the moment of purchasing or inheriting a property above a certain value (about US$400,000). As the base for this tax, the government uses the highest of three values: (1) value of acquisition, (2) cadastral value, or (3) assessment value given by the fiscal authority. Because the value is defined by the seller and both buyers and sellers have full knowledge of the value, this tax does not encounter political or technical challenges in defining its base.

Currently, the city calculates the ISAI using a semi-progressive rate that ranges from 0.4% to above 7.5% depending on the tax base. The tax rates defined for 2024 are slightly regressive when moving between brackets. This technical oversight could result in the loss of revenue if affected individuals claim the unconstitutionality of this tax rate based on the proportionality principle (Article 31). With few exceptions related to the changes between tax brackets, the ISAI is progressive overall. The tax is largely equitable, both in terms of how it is calculated, who pays, and how it is spent. More valuable properties have a higher burden and higher-income individuals with more property, as well as property developers, are more likely to engage in property transactions and more likely to pay this tax. This is beneficial at the city-wide level since the revenue from this tax is shared across all boroughs, redistributing the property wealth from higher to lower-valued neighborhoods.

The justification of the ISAI tax presents challenges in implementation. Unlike other taxes such as property tax or betterment levy, which are justified by the benefits provided by the city or the accrued property wealth, or like the income tax on capital gains paid to the federal government by sellers upon property sale, the ISAI lacks a clear direct benefit rationale. Many perceive this transfer tax, paid by the buyer at the time of property purchase, as a fee for property titling. This perception affects the tax's efficiency in Mexico City, as some individuals may opt to avoid it by not formally registering the sale and relying solely on a private contract (Aguilar 2024). Collecting this tax at the time of a property transaction eliminates liquidity constraints. However, the timing also means it is a relatively small and unstable source of revenue. For example, in 2023 it made up 3% of all revenue, compared to 8% for property taxes. An additional drawback is that revenue fluctuates with market conditions. During periods of economic downturn, fewer property sales results in lower revenues. For example, it dropped to 3% in 2020, a percentage point reduction from 2018.

Our conceptual framework reveals that the definition of the tax base and source of value does not present technical or political challenges. The greatest challenge of this tax is in its calculation, which violates principles of proportionality and equal application of the tax. Its collection at the time of property sales also makes it vulnerable to macroeconomic fluctuations. The weak justification of the tax also makes it vulnerable to political opposition and may have unintended effects.

Betterment Levy

Mexico City has used multiple mechanisms to capture value resulting from public works since the 1940s (Title IX and Title X, Treasury Law 1941). The city's 1941 treasury law established two main mechanisms, a value uplift tax (Impuesto de Plusvalia) and a contribution for public works (Cooperación por obra publica). The first mechanism calculated payments based on land value increases resulting from public works at the city-wide or block level and the latter mechanism calculated payments based on project costs at the street level. Both tools played a large role in financing the expansion of the city's road network during the 14-year mandate of Mayor Ernesto Uruchurtu in the 1950s and 1960s (Zenteno 2021; Perlo Cohen 2023). However, the government's inability to adequately distinguish between direct benefits to the taxed property owners and benefits to the broader community eventually challenged their implementation (Oldman et al. 1967). In some cases, property owners argued that their properties were negatively affected by the public work, or that the charges placed an excessive burden on lower-income individuals who struggled to make payments (Zenteno 2021).

The two mechanisms were precedents for the current contribución por mejoras, or contribution for improvement. This mechanism is akin to a betterment levy as it permits the government to collect a contribution from property owners that directly benefit from public projects like road improvements, sewage or drainage networks, street lighting, or transportation interventions.

In 2014, Mexico City's government sparked a controversy when it sought to use this mechanism for the renovation of Masaryk Avenue in the affluent neighborhood of Polanco. The government proposed to use the contribución de mejoras to finance half the project costs, which is the maximum allowable amount. To calculate costs, the government disaggregates nearby properties into three potential levels of contributions depending on their proximity to the project and their land use. 13 This disaggregation by level of benefit and contribution is an attempt to make the use of this mechanism more equitable. Property owners then have a period of 48 months to pay the full amount charged to them after being notified by authorities. In return, the government must be fully transparent about the costs of the public work. If the mayor determines that the benefits of the project extend beyond nearby property owners or involve low-income residents, the charge can be partially or fully waived.

Affected property owners opposed the Masaryk Avenue project for several reasons including its novelty within the city's recent history and the perceived lack of connections between payments and benefits (Aguayo Ayala 2021). The intended use of this mechanism for the renovation of a high-end commercial street presented an important limitation to its successful implementation. Residential property owners voiced concerns that the project would favor high-end commerce at their expense. Many residents also felt excluded from the decision-making stage and found it unfair that they would be expected to bear the financial burden for a project that they did not support (Ramírez 2015). Property owners ultimately argued that because of the notoriety of the street, the project had city-wide benefits, making this ultra-localized tax unjustified (González 2014). Due to the pushback, the city and borough governments ultimately covered 60% of the project costs while commercial property owners and a public trust paid the remainder, leaving residential property owners fully absolved of this charge (Llanos and Gómez 2014).

Applying our conceptual framework here reveals that the main political challenges were the result of who would pay for the tax, how the tax was justified, and how funds would be used. The project was going to be supported by the residential and commercial property owners near a public work but many of the owners felt that the tax was not justified by the purported benefits of the street remodeling and the potential increase in property value. Furthermore, many believed the project did not benefit them directly and felt excluded from the project definition process. The lack of adequate procedures and local resident involvement in defining the project and its financing rendered the tax less equitable and heightened tensions, ultimately leading to its devolution (Montes 2014).

Development Charges

Mexico City's government uses two mechanisms that grant development permissions outside land use plans in exchange for an in-kind or monetary charge (1); development charges that apply to developments above a certain size, and (2) the city's place-based planning programs called polígonos de actuación and the Sistemas de Actuación por Contribución, which we describe below.

Both mechanisms focus on changes in land use plans or for developments exceeding a certain size. They differ from impact fees, which the city charges all residential and commercial developments for impacts on the environment, road infrastructure, and water infrastructure. 14

Large developments in Mexico City that require land use changes incur charges for planning permissions. According to the operational rules (Article 80) of the city's urban development law (Article 64), all commercial, residential, and office developments that require an impact evaluation or that solicit a license for the subdivision of lots in an area equal to or larger than 5,000 square meters must transfer to the city the equivalent of 10% of the project area as territorial reserve to be used for housing. These donations can be paid in form or the monetary equivalent. From August 2021 to July 2022, the city collected a total amount of $165 pesos, or nearly $10 million USD (.07% of total revenue) from six different projects under these rules. Five out of six of these donations were made in cash, as opposed to land or public works. On the whole, from August 2019 to July 2022, 29 different projects made these donations (Ciudad de México-SEDUVI 2022). These funds are harder for citizens to track and are not specifically spent on improvements linked to development.

The city also permits modifications to land use plans within defined zones called polígonos de actuación, determined by Mexico City's Ministry of Urban Development and Housing (SEDUVI). This mechanism allows developers to assemble lots for large projects, but they must pay 0.4% of the market value of the property to register a poligono de actuación (Article 242 Fiscal Code). From 2016 to 2022, Mexico City's government approved 301 out of 477 requests for poligonos de actuación (Ciudad de México- SEDUVI 2022).

These planning tools work through obscure operational rules, which promote exceptions to the comprehensive planning system and enable corruption (Gonzalez Malagon 2020). For example, for the years 2017 and 2018, 48 of the 174 poligonos de actuación approved contained irregularities (SEDUVI 2019). Mexico City Mayor, Claudia Sheinbaum stated at the beginning of her mandate (2018–2023) that she would not authorize new poligonos de actuación because they undermined urban development programs (Sosa 2019). However, from 2019 to 2024, Mexico City's government approved 115 requests for new poligonos de actuación (Ciudad de México-SEDUVI 2024).

The Mexico City government also uses a neighborhood-based financing mechanism, initially intended to facilitate infill development in exchange for the provision of public infrastructure and services. The city's 2010 Urban Development Law (Article 81) approved the Sistema de Actuación por Cooperación (SAC), which gives private developers permission to deviate from standard land use plans for large projects in exchange for payments destined towards public infrastructure projects in the neighborhood (Leipziger 2021). With this model, funds remain in the polygon in which they are collected and go towards projects that will in theory increase the value of properties in that neighborhood. Currently, there are five up-to-date SACs in the city, but not all remain active. 15

This mechanism has received push-back due to its opacity in the management of funds, which are managed in a private trust governed by private and public stakeholders. A 2019 audit by Mexico City's Supreme Audit Institution (Auditoría Suprema de la Ciudad de México) found legal irregularities in the application of SAC's and opacity in the use of funds. Additionally, they were unable confirm that revenue collected through this mechanism was directed towards urban development initiatives (ASCM/4/18). This mechanism has also been critiqued for making too many concessions to the private sector, as well as for prioritizing political interests (Gomez Peltier 2021). Local residents adjacent to SAC developments bear the impacts of new development, without receiving the necessary infrastructure and service improvements. 16

The most significant challenges that development charges face in Mexico City are related to how the government ultimately uses the collected funds. Negotiation-based development charges and fees also facilitate corruption in a sector where large sums of money are frequently exchanged. Additionally, development charges may increase the cost of development and may make developing housing prohibitively expensive, reducing necessary housing production in Mexico City. Additionally, limited citizen involvement in approving planning exceptions and using funds collected make this mechanism widely unpopular in practice.

Discussion

Capturing land value is a theoretical simple idea, returning the value created through the collective efforts of a city back to the city's residents. Yet its application requires a careful balance of technical and political maneuvering. Our conceptual framework facilitates a comparative approach across the four mechanisms to identify the limitations and strengths of each. Our analysis of Mexico City offers guidance to planners and policymakers on where the city should focus its efforts to increase land value capture, while the proposes framework is broadly applicable across other urban contexts.

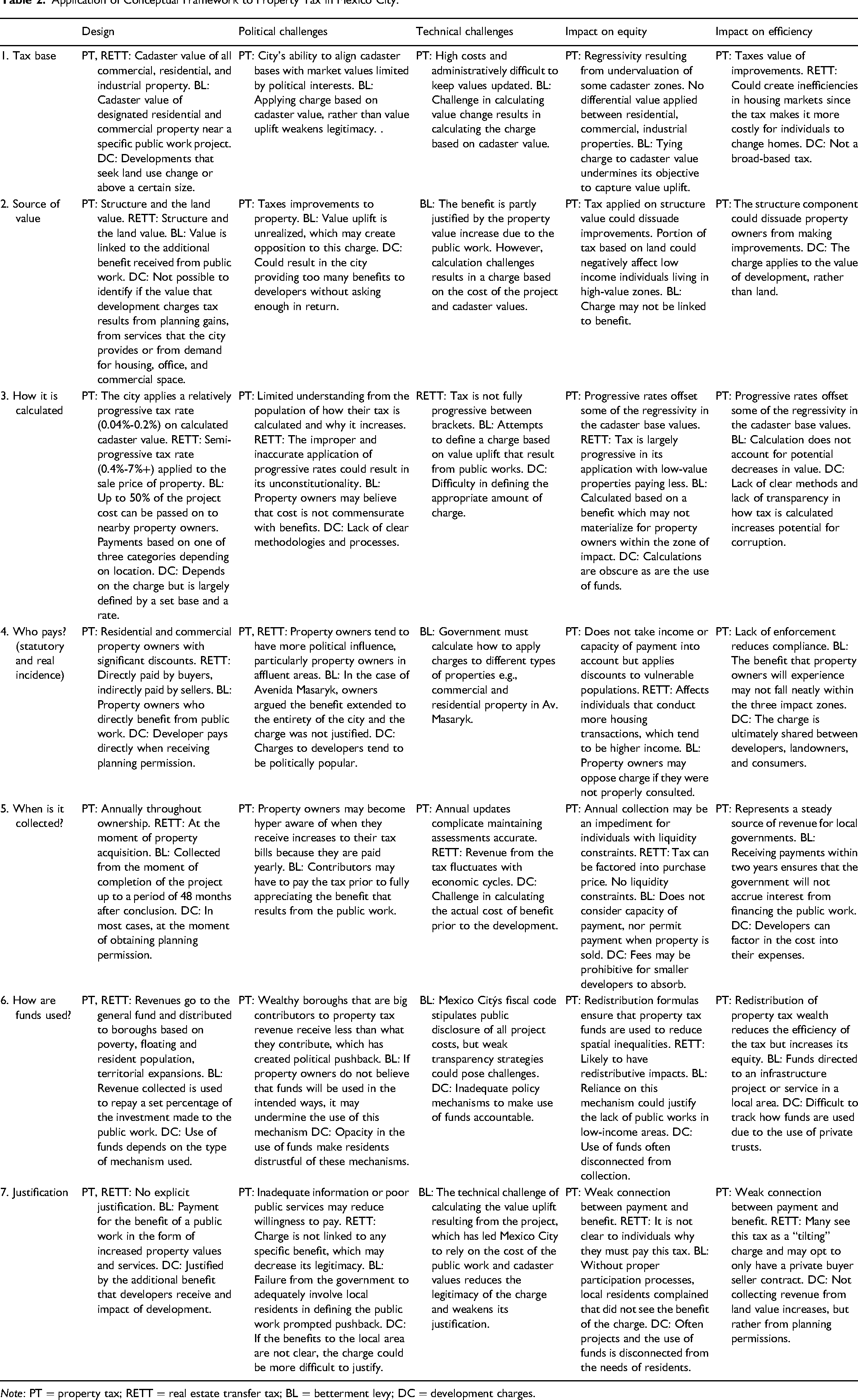

We apply the conceptual framework to the four selected mechanisms with the objective of identifying which land value capture mechanism encounters the fewest implementation barriers and has the most positive impacts on equity and efficiency. In Table 2, we summarize the application of the conceptual framework to the four mechanisms we analyze in the case of Mexico City. The applied framework offers an overview of how the technical and political challenges that arise from the way that Mexico City's government applies each mechanism. Additionally, we highlight impacts on equity and efficiency.

Application of Conceptual Framework to Property Tax in Mexico City.

Note: PT = property tax; RETT = real estate transfer tax; BL = betterment levy; DC = development charges.

Development charges are fairly straightforward to calculate because they are collected at the moment of permitting and can be based on market values and predefined formulas. Although making changes to development plans may result in beneficial projects, giving local bureaucrats and government officials the power to make exceptions to land use plans creates opportunities for corruption. This is evident in the widespread irregularities identified in the use of the poligonos de actuacion mechanism. Additionally, these exceptions have generated confusion about urban development rules and have fueled uncertainty about potential illegalities in large urban development projects (Mexicanos contra la Corrupción y la Impunidad 2018, 2). Development charges capture value from land indirectly by charging for permission to use land in a newly profitable way but exempt nearly all landowners who profit off land in its existing use. Development charges face significant political barriers to the proper use of funds and have the most negative impacts on equity and efficiency out of all four mechanisms.

The betterment levy is another land value capture mechanism used in Mexico City. This mechanism attempts to capture some of the benefits from public works, such as improved infrastructure and attendant property value increases. Through tapping into some of the value increase produced by improved infrastructure, the betterment levy has some of the characteristics of an ideal land value capture mechanism. However, in the case of Mexico City, the charge is not directly linked to the resulting value increase, but rather cost of the infrastructure proportional to cadaster values. Mexico City could eliminate the need for betterment levies by maintaining accurate, regular property assessments, allowing land value increases from public actions to be directly captured through annual property taxes.

In contrast to property taxes and betterment levies, the real estate transfer tax has a technical advantage insofar as its tax base is the sale value of properties. Moreover, since this tax is applied only when a property transaction occurs, it faces less political opposition and places a smaller burden on taxpayers with liquidity constraints. This tax is also equitable in the sense that it is a direct tax on property wealth and follows a relatively progressive structure. However, this tax can be volatile, does not represent a significant source of revenue for the local government, and does not raise revenue from most property owners.

Property taxes in Mexico City, with their progressive rates, most closely resemble an ideal land value capture mechanism. This mechanism directly collects a portion of land value determined by socially created factors such as location value, infrastructure, and service provision. However, outdated cadasters values, fueled by political concerns, limits the efficiency of the tax and makes the tax regressive at points. Additionally, the portion of the tax that falls on improvements limits its efficiency.

Our analysis reveals that the effective implementation of the four land value capture mechanisms faces far more political than technical barriers. Whereas property taxes, real estate taxes, and development charges confront predominantly political barriers, betterment levies face both political and technical challenges due to the complexity of calculating the charge and defining who should pay. Moreover, the implementation of betterment levies and development charges in Mexico City have had an overwhelmingly negative impact on equity as a result of their obscure processes and lack of citizen participation. Meanwhile, real estate transfer taxes achieve a positive impact on equity but have important inefficiencies due to their volatility and limited tax base. Property taxes are the most equitable and efficient mechanism at present. However, this mechanism still possesses important limitations. Strategic improvements to the tax base and the source of value—such as ensuring that cadaster assessments are closer to market values and thus capture land value increases—can significantly increase their efficiency and equity. Our proposed framework enables policy-makers to punctually identify the potential areas of improvement for existing land value capture mechanisms and facilitates the comparison of these mechanisms both within and across cities.

Conclusion

Increased data availability and computing power has substantially diminished the technical challenges of accurately implementing land value capture mechanisms in recent decades (IVSC 2022; Behr et al. 2023). While these technical advancements should make land value capture mechanisms more equitable and efficient, substantial political hurdles prevent widely employing accurate assessments. Mexico City illustrates these political challenges to land value capture clearly. Previous attempts to update assessment values or implement land value capture schemes have resulted in political defiance from opposition parties and wealthy property owners. Indeed, owners of more expensive and appreciating properties tend to be more politically influential than renters or owners of less expensive properties. These more influential owners often resist changes to taxation and property reassessment (Martin 2013).

Mexico City can and should take more advantage of the broad-based mechanism already at its disposal, the property tax, despite its political unpopularity. Policy-makers must take advantage of equity and efficiency strengths of this mechanism and diminish its weaknesses by making strategic improvements to its design. They should also work towards designing communication strategies that increase the confidence of taxpayers in the use of funds to increase support and reduce political barriers. In this way, they would not need to undertake the strenuous process of implementing new mechanisms and would avoid the potential for corruption and loss of credibility from development charges. Instead, it should ensure that the mechanisms that it has in place are working for the benefit of the city.

Supplemental Material

sj-docx-1-uar-10.1177_10780874251323896 - Supplemental material for Challenges to Equitable and Effective Land Value Capture: Lessons from Mexico City

Supplemental material, sj-docx-1-uar-10.1177_10780874251323896 for Challenges to Equitable and Effective Land Value Capture: Lessons from Mexico City by Aurora Echavarria and Paavo Monkkonen in Urban Affairs Review

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the UCLA Ciudades Latin American Cities Initiative, Based on a project funded by the Lincoln Institute of Land Policy.

Supplemental Material

Supplemental material for this article is available online.

Notes

Authors Biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.