Abstract

Recent disasters across the United States highlight the devastating effect of climate-change on individuals and households. The effects of these disasters on access to housing and housing stability are pressing issues of social equity and urban policy. How, if at all, do disasters affect rents? We find that severe floods are associated with significant increases in rents for households renting units priced at the bottom of the rent distribution, but not the middle or the top. Second, is there a relationship between federal rental assistance to affected households and any price changes in the market? We find that disaster rental assistance is not associated with changes in rents after flooding disasters. These findings raise important questions about how policy should support low-income renters after disasters, including those not directly displaced by the disaster who are facing increased rents after a disaster but unable to access federal post-disaster rental assistance.

Introduction

Recent hurricanes, floods, and wildfires across the United States highlight the devastating effect of climate change on individuals and households. These disasters manifest long-term social and political processes that generate inequality and vulnerability, and the effects of these disasters on access to housing and housing stability are pressing issues of social equity and urban politics and policy. Research has found that renters and households with low-incomes are disproportionately exposed to and harmed by these disasters (Fothergill and Peek 2004; Lee and Van Zandt, 2019). While scholars have explored the long-term effects of disasters on crucial outcomes such as health (Raker et al. 2019; Zacher et al. 2021), migration (Boustan et al. 2020), and employment (Deryugina, Kawano and Levitt 2018), comparatively little is known about how climate related disasters systematically affect renters and their rents in the near term.

This paper seeks to understand, first, what effect, if any, disasters have on rents in the years immediately following the disaster. How disasters affect rents is not immediately obvious. On the one hand, research suggests that disasters generally lead to net outmigration (Boustan et al. 2020), which would be expected to reduce demand for housing and, in theory, lead to lower rents. On the other hand, disasters generally damage housing units, rendering some unusable (Vigdor 2008; Bates and Green 2009), which would be expected to reduce the supply of housing and, in theory, lead to higher rents. Any relationship between disasters and rents may also vary by housing market segment (Jacobus 2019), given differences by neighborhood income in housing units’ exposure to disaster risks (Morrow 1999; Lee and Van Zandt 2019) and the pace of rebuilding (Zhang and Peacock 2010), as well as differences by household income in household mobility (Smith et al. 2022).

This paper then analyzes, second, whether levels of FEMA rental assistance are associated with the changes in rents after disasters. After severe disasters, some homeowners and renters whose homes are rendered uninhabitable are able to access temporary rental assistance from the Federal Emergency Management Agency. There is the possibility that that the influx in federal rental assistance could drive up rents broadly or that landlords could exploit that aid to charge higher than market rents, as some evidence suggests may take place in other federal rental assistance programs (e.g., Desmond and Perkins, 2016).

We assemble a panel dataset on rents, disasters, the social and built environment, and federal disaster assistance across the country at the level of Census’ Public Use Microdata Areas (PUMAs, or Areas) level from 2012 to 2018. To overcome the stickiness inherent in the rents of leased-up units, we use household level records and isolate the dynamics of the post-disaster market by comparing rents for households that moved in the past year to households that did not move that year (mover and non-mover households). We specify a difference-in-differences model to estimate the effect of disasters and of federal disaster aid on rents. We exploit the exogenous timing of disasters to interpret our results causally.

We find that disasters are associated with significant increases in rents for households renting units priced in the bottom decile of the rent distribution in the year following a severe flood (defined by the value of damage caused by the disaster), but that disasters do not have a statistically significant effect on rents paid at the middle or top of the distribution. In other words, rents after disasters increase most for those who can least afford it. This spike translates to an estimated average 5 percent increase in rent for households renting at the bottom of the distribution—a substantial burden for low-income households, especially after a disaster. We also find that increased values of rental assistance to renter households from FEMA are not associated with higher rents, indicating that this assistance does not appear to exert significant upward pressure on the market.

Background

Disasters are not individual environmental events, but long-term social processes in which exposure to hazards and the ability to recover from disasters are shaped through political processes of social and physical investment and disinvestment (Benner and Pastor 2013; Rumbach and Makarewicz, 2016; Lee and Van Zandt 2019; Arcaya et al. 2020). Race, socioeconomic status, gender, and age all powerfully shape both physical and social vulnerability to the effects of disasters (Peacock 1997; Bolin and Kurtz 2007; Arcaya et al. 2020; Rivera and Knox 2022). As Lee and Van Zandt (2019) emphasize, housing tenure lies at the intersection of physical and social dimensions of vulnerability, given the correlations between tenure and unit characteristics, income, race or ethnicity, age, likelihood of insurance coverage, and housing stability.

In the past three decades, coastal and river flooding and other climate-related disasters stemming from hurricanes, storms, and sea level rise have increased in severity (Barthel and Neumayer 2012; Kunkel et al. 2013; Smith and Katz 2013). At the same time, the percent of household budgets spent on housing have risen while homeownership rates have declined, particularly for low-income households. These intersecting trends make understanding the relationship between disasters and rental markets increasingly important.

Median gross rents have increased on average faster than median household incomes since the 1970s. In 2021, nearly one out of four renter households in the United States paid more than half of their gross income toward housing costs, and nearly one out of every four renter households with incomes below $25,000 were behind on their rent (U.S. Census Bureau, 2021b; Joint Center for Housing Studies 2022). The Census Bureau's Rental Housing Finance Survey (2021d) has documented an increase over the past several decades in the share of rental properties owned by corporate entities and real estate investment trusts as well as the share of homes purchased by investors, including single family homes, for rent. The increasing financialization of housing (Gotham 2006; Newman 2009; Fields 2015) has coincided with rising housing costs relative to income and declining homeownership rates in the United States. The number of renter households increased by roughly 340,000 between 2011 and 2021 while the number of vacant housing units declined by nearly three million (U.S. Census Bureau, 2021a, 2021). The vacancy rate for both rental and homeowner housing was at its lowest level in more than 35 years in 2020 (U.S. Census Bureau, 2021c).

At the same time as demand for rental housing has been increasing, hurricanes, wildfires, flooding, and other disasters have been damaging or destroying rental homes. In 2021, nearly 15 million homes, or one out of ten, were affected by severe disasters, causing $57 billion in property damage (CoreLogic 2022). The risks in the future are greater—roughly 40 percent of occupied rental housing across the United States is at moderate or high risk from flooding, drought, earthquakes, and hurricanes (Joint Center for Housing Studies 2022). The risks to subsidized housing are higher still, with 39 percent of the 3.1 million rental homes supported by the Low-Income Housing Tax Credit program and 30 percent of the 2.3 million rental homes supported by HUD's project-based vouchers located in what FEMA categorizes as high-risk locations (Joint Center for Housing Studies 2022).

Understanding the effects of disasters on renters, and especially low-income renters, is essential to understanding how disasters affect inequality (Fothergill and Peek 2004; Brennan 2024; Howell and Elliott, 2018; Lee and Van Zandt 2019). Early research in the field noted the disproportionate damage to rental units relative to homeowner units in the Northridge and Loma Prieta earthquakes and the discrepancy between the comparatively generous assistance to owner occupied units relative to rental units (Comerio 1997). Subsequent research identified evidence that high-income households displaced by the disasters “take over such surplus housing as may be available” but noted that “the relationship of that to the pre-impact stock is unclear” (Quarantelli 1982, 77). Renters are more vulnerable to housing loss than homeowners after a disaster (Fussell and Harris 2014) and recent research has found that disasters cause a significant increase in evictions in the year of a disaster and the two years following the disaster (Brennan et al. 2022). Changes in rents may play an important role in both of these vulnerabilities.

To understand how disasters might affect rents, it is relevant to examine what has been identified about the effects of disasters on local population size. Much of the existing research focuses on extreme individual disasters, such as Hurricane Andrew (Smith and McCarty 1996; Hallstrom and Smith 2005) or Hurricane Katrina (Sastry and Gregory 2014; Bleemer and Van der Klaauw 2017), finding that these disasters were followed by large out-migrations. Several papers look across multiple disasters, including Boustan et al. (2017) who examine more than 10,000 disasters between 1920 and 2010, finding that severe disasters increase out-migration rates at the county level by 1.5 percentage points and lower housing prices and rents by 2.5–5.0 percent over the decade of the disaster. Narrowing in on the effects of hurricanes and tropical storms between 1980 and 2012, Fussell et al. (2017) find that they only decrease population growth in counties with growing, high-density populations, presumably where housing costs are highest. The increasing prevalence of home insurance generally over the past century, the creation of federal disaster assistance, the initiation of the National Flood Insurance Program in 1968, and the creation of FEMA in 1979 all may have contributed to mitigating disaster effects that in previous decades drove population declines. 1 Investments in rebuilding may generate a “recovery machine” that even attracts new residents (Pais and Elliott 2008). This recovery machine often exacerbates inequality, however, benefitting residents in the upper half of the income distribution who can afford private insurance coverage while doing little to alter the number of residents living in poverty (Schultz and Elliott 2017). Socioeconomic status substantially affects the trajectory of households after disasters, with low-income households frequently moving into housing in heavily damaged areas, while middle-income households move away to avoid risk, and high-income households, for whom insurance was most affordable, remain in place (Smith et al. 2022). These findings highlight how the experiences of renters likely differ across the income distribution.

Another relevant factor is the effect of disasters on the housing stock. Even if population declines after a disaster, where the relative loss of housing units, particularly rental housing units, is larger than relative loss of population home prices and rents would be expected to increase, at least in the short term. For instance, Vigor (2008) finds that from the year before to the year after Hurricane Katrina, New Orleans witnessed a 48 percent increase in rents. The experiences of renters again may differ by housing segment. Looking at nationwide data, severe floods reduce the number of publicly subsidized housing units in a disaster affected county by up to 5 percent in the year following the disaster and prolong the average waiting time for units (Davlasheridze and Miao 2021). Private sector landlords in low-income neighborhoods may also be reluctant to repair or replace damaged buildings in low-income, low-rent neighborhoods if they can gain higher profits elsewhere, further contributing to the scarcity of affordable rental units (Comerio et al., 1994; Bolin and Stanford 1998; Pais and Elliott 2008; Zhang and Peacock 2010).

The existing literature highlights the salience of understanding the effects of disasters on rents and suggests that these effects may differ across the income spectrum. Aside from some studies of individual disasters (e.g., Vigdor 2008), however, scholars have not yet identified systematic effects of disasters on rents by income. While findings regarding declining population size and home values might suggest a decline in rents after a disaster, the findings regarding damaged units, and an influx of recovery funding and workers might lead one to expect increasing rents in a tight market. Because rental assistance from FEMA to affected rental households is currently the main policy mechanism to stabilize housing outcomes in the short-term, investigating the relationship between disasters, rent, and aid is also central to understanding the recovery dynamics for city residents.

Methods and Data

Data

To explore these questions, we merge rent, disaster, and demographic and housing covariate datasets by U.S. Census Public Use Microdata Area-year, which we subsequently refer to as Area-year. We create a panel dataset for 2012 through 2018 of 281 Areas. This panel consists of Areas that have experienced a severe flood at least once during the course of the seven-year period. These 281 Areas are exposed to a severe flood disaster in that timeframe or, in other words, are treated. We choose to focus on the Public Use Microdata Area because it is an appropriate scale to measure the effects of disasters on different segments of regional housing markets, more granular than a Metropolitan Statistical Area (a geography so large it may mask local housing market effects) but larger than a Census Tract (a geography so small that yearly changes in rents for moving households might be hard to detect and at which such precise household level data is not publicly available). Populations within each Area average 134,921 residents, and occupied rental units within each Area average 16,967. Several recent studies have used these PUMA Areas instead of metropolitan statistical areas or more granular zip codes to investigate urban phenomena such as schooling, commuting, or employment (Pastor 2001; Saporito, Yancey and Louis 2001; Xu 2020). In particular, there is an expanding housing policy literature using household data identified at the Area-level to investigate housing market and policy dynamics (Collinson and Ganong 2018; Glaeser and Luttmer 2003; Grady 2019; Hanratty 2017; Quigley and Raphael 2005; Richard et al. 2022). 2

The dependent variables in our analysis are two points on the distribution of monthly gross rents paid by households. We focus on the bottom-decile and mean gross rents on the rent distribution for Areas in a given year, giving us insight into two crucial segments of the rental market from a policy perspective. We work with household records from IPUMS USA dataset, previously the Integrated Public Use Microdata Series (IPUMS) dataset (Ruggles et al. 2024). 3 In total we work with 301 million (weighted) renter households sampled from 2012 to 2018, which is derived from 2.5 million unweighted survey records. Because IPUMS does not track households over time, we build our longitudinal panel at the Area, instead of household, level.

We construct the dependent variable as a difference in differences in gross rent paid between mover and non-mover households at time t and t-1 in Area i. This construction overcomes two common barriers, discussed below, to working with rent data and forms the basis of our identification strategy.

First, we compare moving to non-moving households. 4 Market frictions and social norms can lead the rents of new tenants to increase more rapidly than the rents of current tenants (Clark and Heskin 1982; Eubank and Sirmans 1979; Rose et al. 1983; Robinson and Steil, 2021). Furthermore, shocks may have uneven effects on prices for different renter groups or unit types (Saiz 2003). By separating mover from non-mover households’ rents, we look past the sticky, average behavior of rents in an Area to more clearly identify the impact of a disaster, the effect of which is likely concentrated among mover households.

Second, we compare the year-to-year difference in rents, following the general approach of Saiz (2003) and more broadly that of Card and Krueger (1994). In taking the difference of rents within each Area with respect to time, we adjust our initial difference in mover households compared to non-mover households, to be able to exploit the exogeneity of when disasters occur to identify their effect. The difference in difference is described in equation (1):

Drawing from U.S. Census Bureau data, we construct a panel of economic, housing, and demographic covariates. 8 We use reports from the Census Bureau American Community Survey (ACS) 1-year estimates to obtain yearly estimates from 2012 to 2018 for share of population with a bachelor's degree or higher, share of households in poverty, median household income, rental vacancy rate, multi-family housing units (> 4 units), share of renter-occupied units, median home value, monthly gross rent, and shares of Hispanic, non-Hispanic White, non-Hispanic Black, and non-Hispanic Asian populations.

Finally, our analysis examines the effect of FEMA assistance on rents. We use the total numbers of renters’ registrations, and values of rental assistance delivered to renters by Area for 2012 to 2018. 9 The panel has 424 Area-years in which FEMA assistance to rent temporary housing was delivered to renters (and 525 Area-years in which any renters registered with FEMA). This open FEMA data forms the basis of several recent investigations about the relationship between aid and its outcomes, including inequality (Howell and Elliott 2019).

Identification and Estimation

We identify the effect of severe flood disasters on changes in bottom-decile and mean rent using these panel data. The timing of disasters is exogenous to rent trends and Area or state level characteristics, allowing for causal estimation of the effects of disasters on residential rental prices. As discussed above, we employ a difference-in-differences strategy. We estimate a random effects model across the panel of 281 Areas and seven years to quantify the effect of severe flood disasters on the rent distribution, focusing on the bottom-decile and mean rent. A difference-in-differences specification is an approach to causal inference that can be used in the context of housing markets to exploit an exogenous shock to compare its effect on prices over treated and untreated geographies, household groups, and periods (Boes and Nüesch 2011; Diamond, McQuade and Qian 2019; Freemark 2020; Koster, van Ommeren and Volkhausen 2021).

To examine the impact of a disaster on rental prices, we compare the evolution of rents in disaster-affected Areas with that of rents in other Areas nationwide that experience a severe flood over the course of the panel. The identification strategy is built on two comparisons intended to capture the size and slope of rent trends attributable to economic conditions within each Area: differences in rents between mover households and non-mover households, and between subsequent years. 10

We estimate a random effects model to test whether a severe flood disaster in one year has an effect on the difference in differences of rents in the following year. We include time-variant and salient Area-level characteristics, including measures of socio-economic conditions and housing markets.

The model is described in equation (2):

Testing for the effect of FEMA aid to renters on market prices, we add the following interaction to the specification in Eq. (2):

Results

Descriptive Analysis

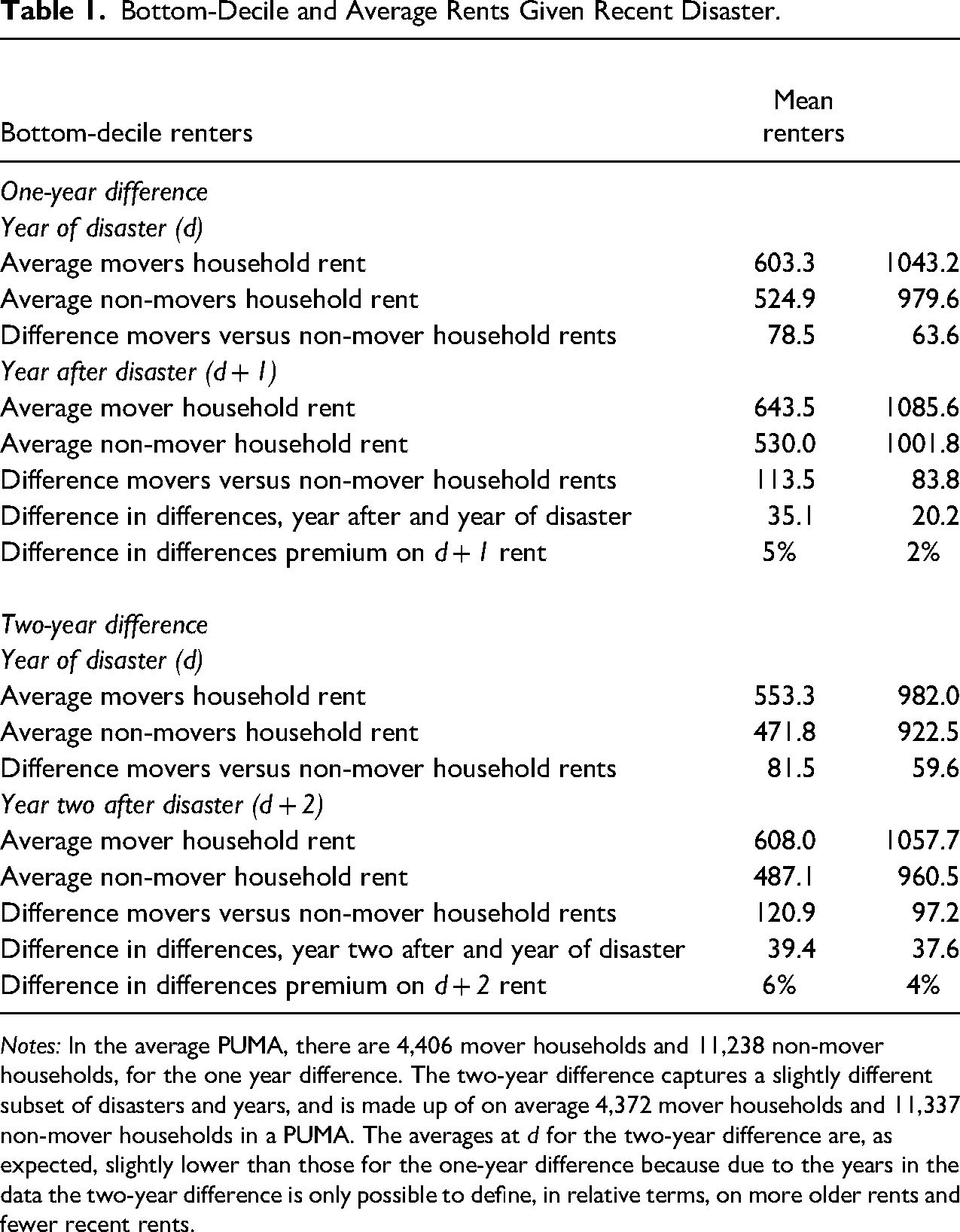

Bottom-Decile and Average Rents Given Recent Disaster.

Notes: In the average PUMA, there are 4,406 mover households and 11,238 non-mover households, for the one year difference. The two-year difference captures a slightly different subset of disasters and years, and is made up of on average 4,372 mover households and 11,337 non-mover households in a PUMA. The averages at d for the two-year difference are, as expected, slightly lower than those for the one-year difference because due to the years in the data the two-year difference is only possible to define, in relative terms, on more older rents and fewer recent rents.

On average across Areas, the difference between mover and non-mover households’ rents at the bottom decile of the rent distribution was $79 in the year the disaster occurred and $114 the year after. The average difference between movers and non-mover households’ rents at the mean was $64 in the year of a disaster and $84 the year after. Looking at the difference in differences for movers and non-mover households at the bottom decile of the rent distribution, we see that at on average, mover households pay $35 more the year after a disaster, after netting out rent paid by non-mover households in that year and the difference between mover and non-mover households in the year of the disaster. In relative terms, this effect indicates mover households renting units at the bottom decile of the rent distribution face a 5 percent premium in the year after a disaster. For mover households at the mean of the rent distribution, the difference in differences is a 2 percent premium.

Two years after a disaster, the difference in differences is slightly larger than in the first year, at a 6 percent premium for renters in the bottom decile. This means that rent for renters in the bottom decile jumped $35 the year after the disaster, relative to other movers, and then increased a further $5 the following year. Again, the additional rent paid by renters in the bottom decile two years after the disaster is larger than the rent premium paid by renters at the mean (4 percent). While the rent increase for renters at the mean is close in absolute terms to renters at the bottom decile at this point, it is substantially lower as a share of their rent paid.

The effects of these post-disaster increases in rent fall disproportionately on households of color. While nationally roughly 75 percent of households that own a home are white and 25 percent are households of color, roughly half of renter households are households of color (AHS 2017 Renters profile). Consistent with the national composition of renters, the renters in the sample here who are renting in the bottom decile are a majority of households of color. Unfortunately even though the sample size overall in this analysis is large, the samples of renters who moved in a given year by race are too small to analyze the impact broken out by race with any confidence. As seen in the

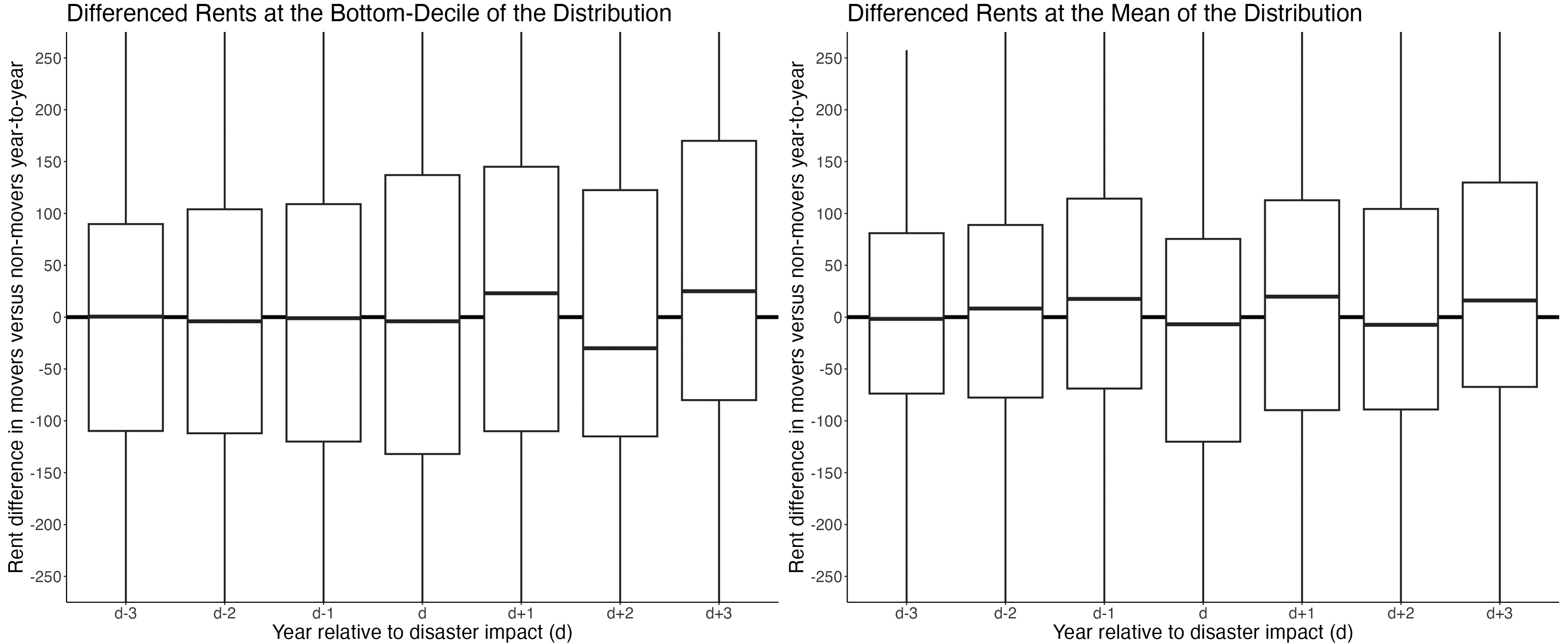

This pattern for all renters is represented visually year-by-year before and after a disaster in

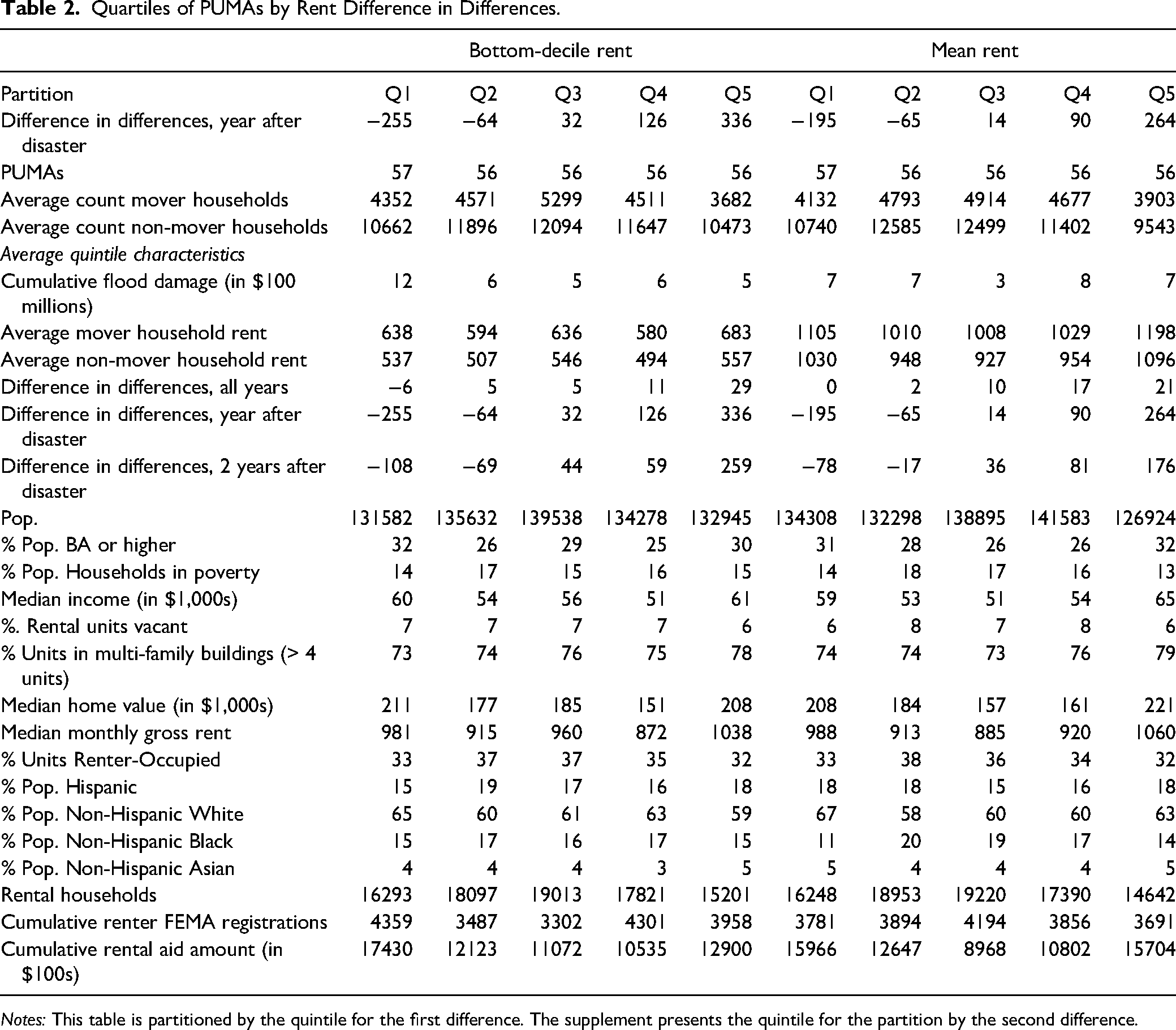

In

Quartiles of PUMAs by Rent Difference in Differences.

Notes: This table is partitioned by the quintile for the first difference. The supplement presents the quintile for the partition by the second difference.

In the year following a disaster, some Areas actually experience decreases in rents. The Areas with the largest decreases in rents in the bottom decile are those with the most severe disasters, understood as the highest levels of damage; consistent with the increased severity of these disasters, these Areas also have more FEMA registrations and larger rental aid per registrant than other Areas in the panel. Most Areas, however, experience increases in rents the year after a disaster. The Areas with the largest increases in rental prices are those where rents and median household incomes are already highest and where there is the largest share of residents of color. This suggests a tentative pattern where the most severe disasters actually drive down rents, even as a majority of disasters lead to increasing rents. Disasters in the most expensive rental markets are associated with the largest increases in rents for low-income renters.

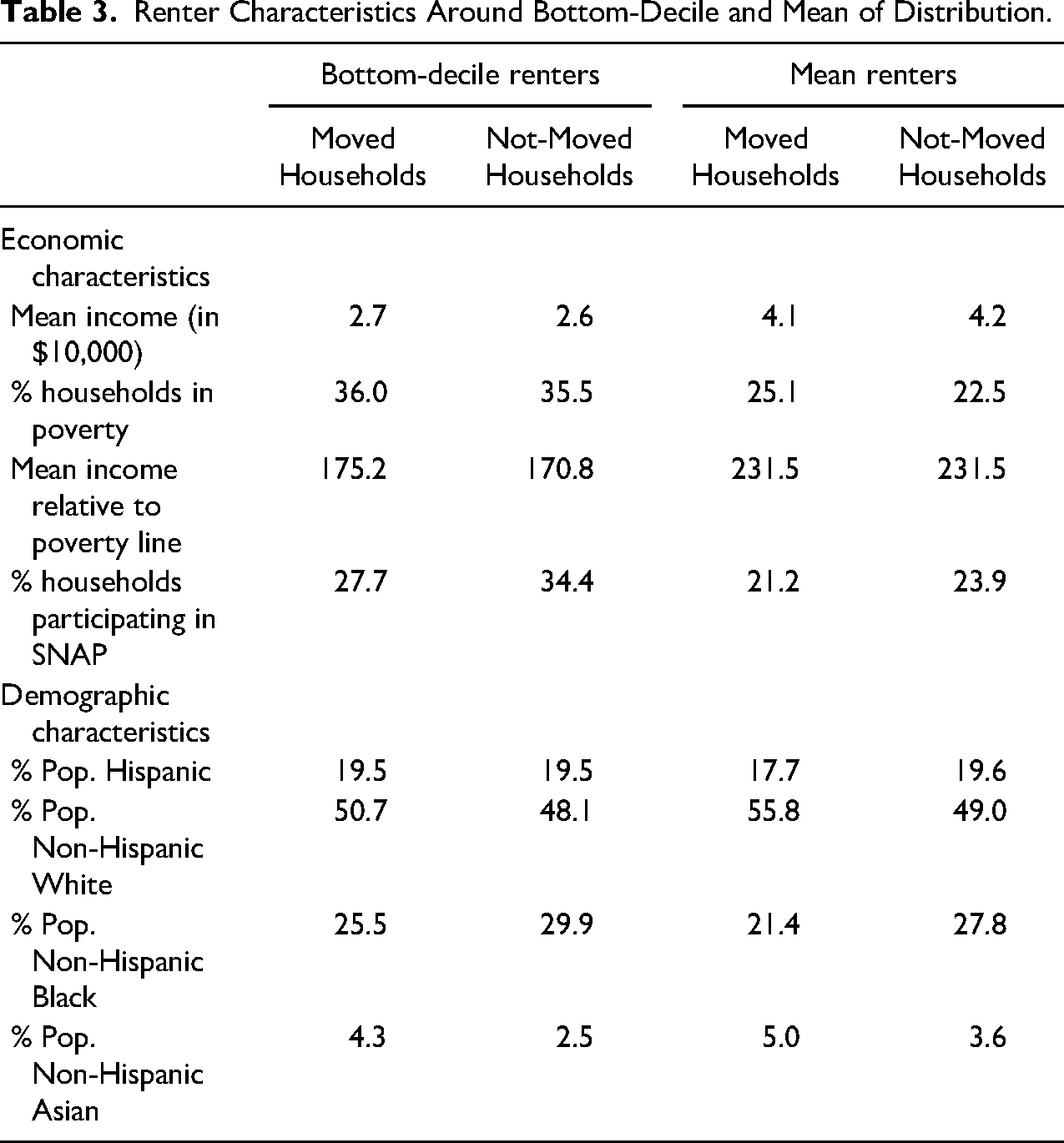

Table 3 reports the household characteristics for those renting in the bottom-decile of rent and around the mean rent (defined by households in the ventiles along the rent distribution just below, at, and just above those points). Renters who move and secure units priced at the bottom-decile and at the mean are slightly wealthier and whiter than renters who do not move. These moving households are also less likely to be using food assistance (i.e., SNAP) compared to non-moving households; this is especially true of moving households at the bottom decile of the rent distribution.

Renter Characteristics Around Bottom-Decile and Mean of Distribution.

Causal Analysis

To estimate the effect of a severe flood disaster on rents, we specify a difference in differences approach and estimate the model using a panel regression model following

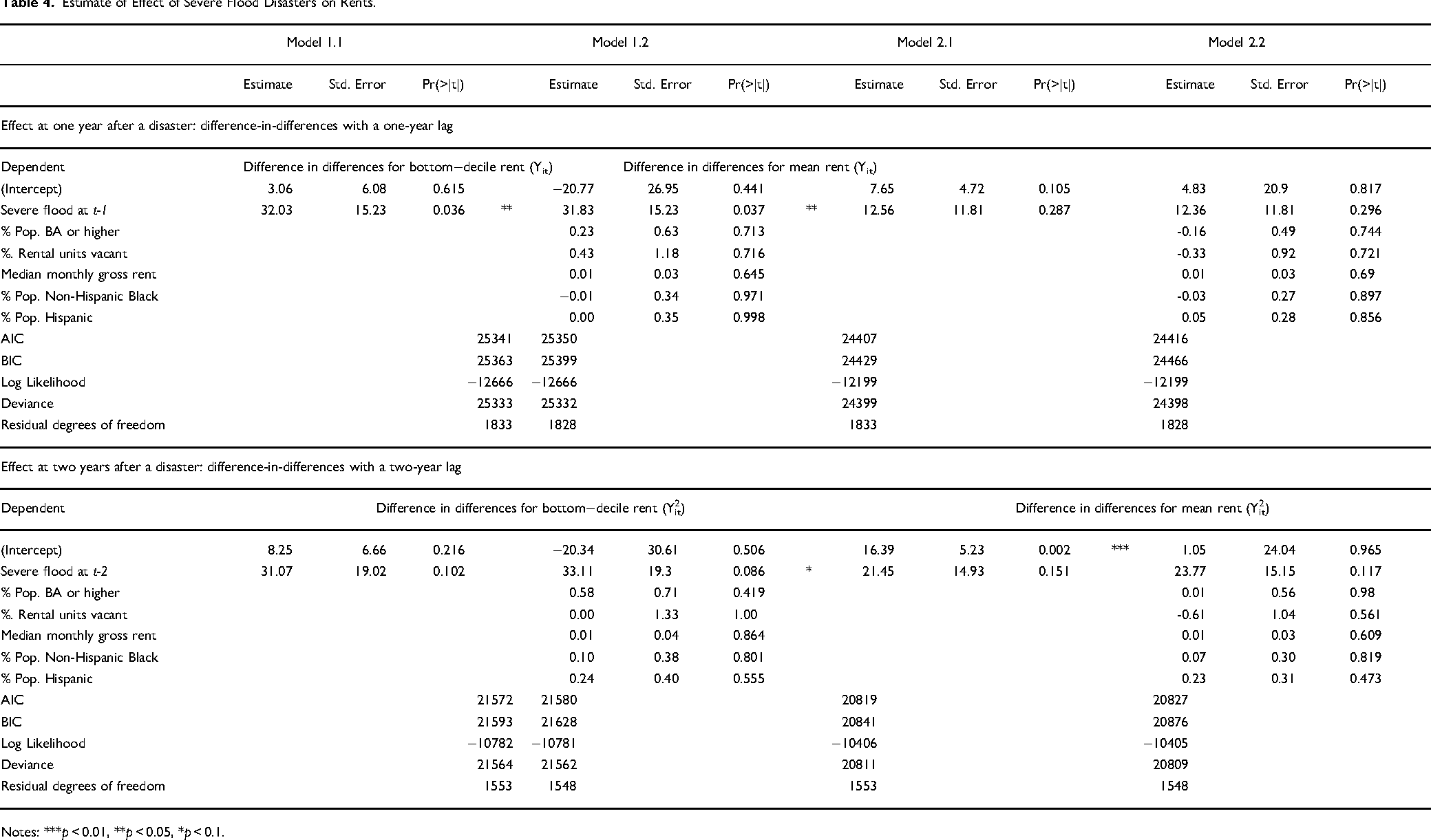

Estimate of Effect of Severe Flood Disasters on Rents.

Notes: ***p < 0.01, **p < 0.05, *p < 0.1.

This effect at the bottom decile of the rental distribution endures through the second year after a severe flood disaster, though weakening statistically. Model 1.1 estimates the change in difference for moving versus not-moving renters at the bottom decile between the year of the disaster and two years after the severe flood disaster, registering a not-statistically-significant average $31 increase in an Area. This result holds for Model 2.2, gaining modest significance with the addition of covariates. In contrast, Model 2.1 estimates a not-statistically-significant $21 increase in difference in differences for rents at the mean in an Area two years after a severe flood. This result is directionally and in size consistent with what

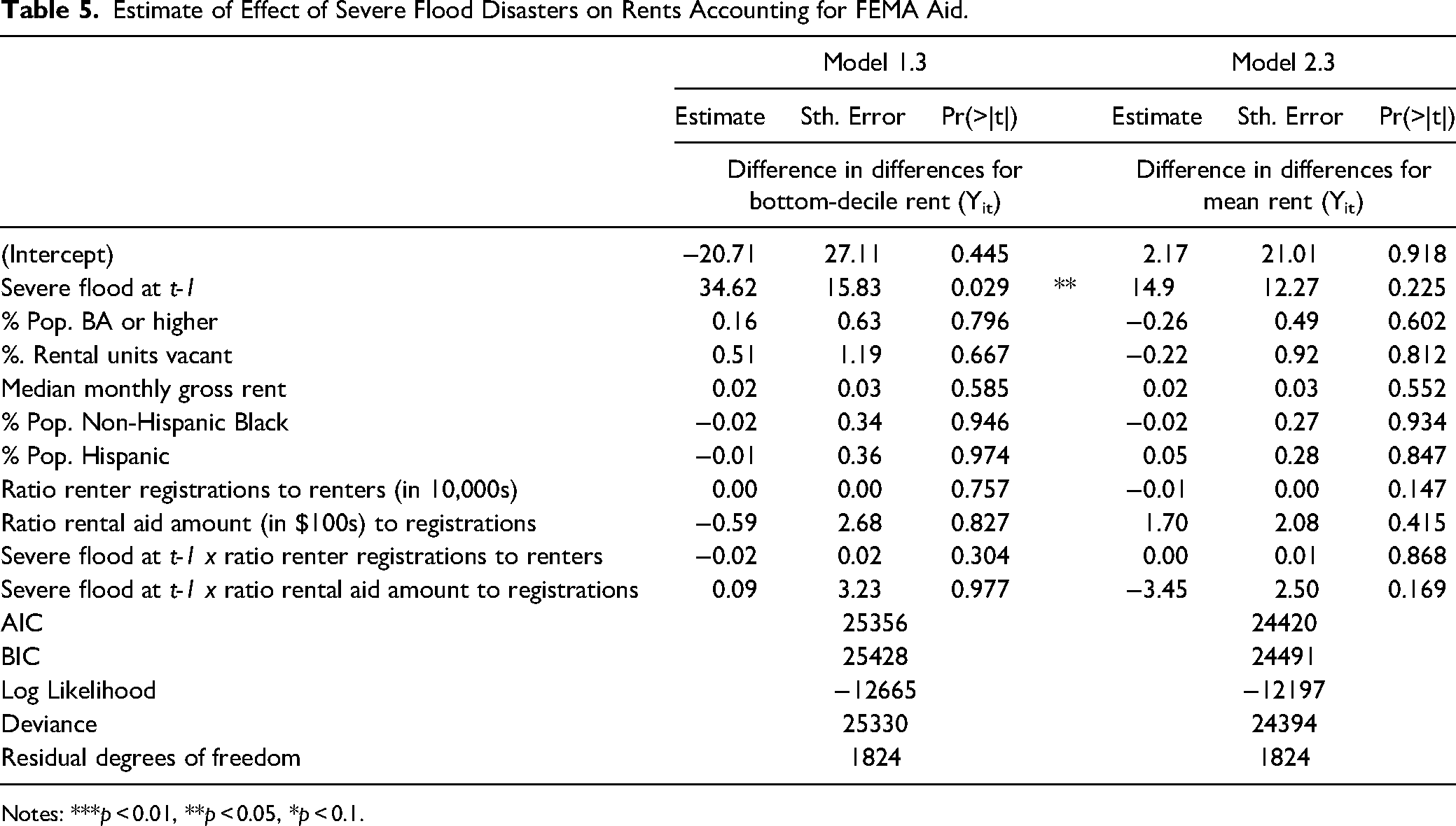

The results in Model 1.3 and Model 2.3 explore what effect, if any, federal rental aid to renters has on change in the rent difference in differences. For rents at the bottom-decile and mean, we observe no significant effect of the interaction between severe floods in the preceding year and the amount of rental assistance delivered to renters. In short, FEMA aid is providing some assistance to renters without having a significant effect on market rents. This may be partially because renters are taking assistance and moving somewhere out of the affected Area, or because displaced renters previously renting at the bottom decile (in t-1, where Model 1.2 indicates the market may be the tightest after a flood) benefit from the ‘market-rate’ aid and start to rent at prices closer to the mean of the distribution without significantly driving up those rents (in t), or because the share of renters receiving rental assistance is not large enough to have a broad effect on all low-income renters, among possible reasons.

Sensitivity

To evaluate the robustness of these models, we conduct several additional tests, presented in the appendix. We evaluate the stability of results using alternative constructions of the model presented above and of the independent variable.

First, we validate our specification. We estimate an OLS model, with idiosyncratic error ζi,t. Cross-sectional dependence is challenging in panel data with high time dimension (20–30 years), but is often less problematic in panel data with few years and high individual dimension, which is true of our data. It does not produce results substantively different from ours. This is available in

Discussion

All households affected by a disaster face challenges. For renters leasing at the bottom of the rent distribution, the structural barriers faced in procuring and remaining in stable housing are exacerbated after disasters. While low-income renters must navigate an already-insufficient stock of affordable homes before disasters, the 5 percent additional increase in the monthly price of housing attributable to the disaster further constricts their housing choices. The findings suggest that federal rental assistance programs do not aggravate these price increases.

In

Estimate of Effect of Severe Flood Disasters on Rents Accounting for FEMA Aid.

Notes: ***p < 0.01, **p < 0.05, *p < 0.1.

These findings raise important questions for future research analyzing the social, economic, and legal processes leading to rental price increases after disasters and contribute to two lines of scholarship on the politics of disaster recovery. First is the question of how market actors treat vulnerable groups, such as low-income households, affected by societal shocks, and how public programs intervene in turn (e.g., Bitler, Hoynes and Kuka 2017; Klerman and Danielson 2011). Since the beginning of the twenty-first century, economic recessions, floods and fires, and the COVID-19 pandemic have disproportionately negatively affected low- and moderate-income households, renters, and people of color, making more salient the question of to what extent social supports effectively support these populations after a crisis. By revealing the extent to which rents at the bottom of the rental distribution increase after environmental disasters while rents at other levels of the rent distribution remain largely stable, we provide important evidence of how those least able to withstand economic shocks suffer the greatest relative economic harms.

Second, continuing debate over the funding and structure of disaster assistance and the uneven distribution of disaster assistance between renters and homeowners raise important questions about the effects of disaster rental assistance. Given the finding that disasters increase rents at the bottom of the distribution, some might ask whether federal aid could actually be the cause of that increase. We find no evidence that rental prices are related to federal rental assistance. While federal rental assistance may thus aid households displaced by disasters who qualify for this financial support without the assistance raising costs for others, we note that it does not reach low-income renters whose homes are not damaged and thus who are not eligible for assistance but who still face increased housing costs as a result of the disaster. This result may contribute to explaining some portion of the finding that disasters widen wealth gaps between renters and homeowners (Elliot and Howell 2016) and increase evictions (Brennan et al. 2022).

Given existing research on the need for affordable housing in the US far outpacing its availability, the finding that disasters are associated with increases in rental prices at the bottom decile of the rent distribution suggests that policymakers should consider interventions that might interrupt the relationship between disasters and housing unaffordability, especially for those households with the lowest incomes.

How public programs enable successful recovery, especially for low-income communities and renters in them, is highly context dependent. Creating opportunities for meaningful public participation and involving relevant stakeholders often affects how successful policy interventions are (Williams and Jacobs 2021). Potential state and local interventions include reconceiving and extending price-gouging laws limiting the ability of landlords to rent to new tenants at prices significantly larger than pre-disaster prices, even if some price controls might in ways slightly slow recovery (Kim, Shahandashti and Yasar 2023); providing landlords with grants or loans for repairs conditioned upon maintaining stable rent prices so that the value of repairs are not passed on to new renters; directing affordable housing construction subsidies towards disaster affected areas, which for one federal program has led to (re)building mainly out of the floodplain (Brennan, Mehta and Steil 2022); thinking more carefully about how recovery workers rent in disaster-affected places to balance convenient access to affected areas with efforts to protect the affordability of those locations; and prioritizing repairs to damaged or vacant affordable housing stock, a recovery mechanism that is already authorized in federal law.

The potential impact of federal policy action in this space is significant, as today, FEMA averages $250 million in annual aid to renters (Drakes et al. 2021). As just one example, increasing the utilization of the federal Multi-Family Lease and Repair Program, which authorizes FEMA to repair unused multifamily residential buildings to temporarily house displaced households, could result in those units being leased-up by renters living in units priced at the bottom of the rent distribution. Compared to the financial programs that deliver rental assistance, repair-based aid is underutilized, but could have a significant impact on the quality and availability of units for low-income renters after disasters.

Beyond FEMA's temporary assistance, states often use Community Development Block Grant Recovery funding appropriated by Congress. These resources, however, generally disproportionately benefit homeowners relative to the harms they experienced compared to renters and those experiencing homelessness (GAO 2010). Greater oversight from HUD to ensure that that long-term assistance goes to low-income renters and rental housing at levels at least proportionate to the damage those households experienced could help ensure that aid goes to those who most need it, not primarily to those who are most politically powerful. The findings here are relevant to disaster preparedness and response efforts outside of frequent flood zones as well, as the frequency and severity of disasters increases and they strike in previously unexpected locations.

The disaster safety net is a consequential and growing branch of the American welfare state in terms of relevance, scope, and scale. From special food stamp disbursements (‘D-SNAP’), to rental assistance, to home-repair financing, federal disaster programs rest on markets, mirroring the privatized logic of the broader social safety net. Over the past half-century, disaster assistance has proven somewhat resistant to the regressive “roll-back” of welfare reform, and more representative of the “roll-out” of privatization of public services (Pick and Tickell 2002). This may reflect the historical mobilization of support for those seen as “deserving” beneficiaries (Skocpol 1992; Fox 2010). 12 Consistent with this construction of deservingness, most disaster housing aid, though not means tested, is limited to directly displaced households.

The findings here highlight the uneven, indirect effects of disasters. The price increases identified for rental housing in the bottom decile of the market will be shouldered by both renters directly displaced by a disaster as well those indirectly displaced and still needing to move, such as by disaster-related job loss or landlords refusing to renew a lease in order to find a higher paying tenant. Thus, for many households only indirectly affected by the disaster, rental assistance is retrenched: those who would benefit from aid cannot access it because by design and in administration, it is unavailable to them. This also adds one partial explanation for how disasters widen wealth inequality (Howell and Elliott 2019). While homeowners largely benefit from any increase in home prices, renters directly lose from increases in rents – widening gaps by tenure and relatedly by income. Further, within renter households, effects of disasters on rents for the mean renter are not significant but low-income renters, who can least afford to pay more, face a significant increase.

As housing prices continue to rise relative to wages and as the frequency and severity of climate-related disasters increase, the disproportionate effects of both of these ongoing crises on low-income renters will only exacerbate socioeconomic inequality. Climate related disasters are notable additionally for frequently accelerating inequality in places where housing had previously remained comparatively affordable. The findings here reveal another form in which the inequality generating effects of these crises reach far beyond those directly affected by disasters. They raise again the question of what point these crises or systemic shocks become so disruptive that they will force systemic change.

Although the descriptive statistics presented here suggest that these post-disaster rent increases disproportionately affect renters of color, a substantial limitation of the research is its inability given sample sizes of mover households at the PUMA level by race to directly estimate the effects of these post-disaster rent increases on racial inequality. Future research using other administrative or industry data could help better pinpoint the effects of disasters on racial inequality for renters. The quantitative approach used here reveals that severe flooding disasters increase rents for the households at the bottom of the rent distribution who can least afford it. Future qualitative research could help identify how households with low-incomes respond to these rent increases and reveal in more detail the mechanisms through which flooding disasters lead to increases in rents. Future research could also explore connections between these rent increases and evictions and household mobility as well effects on renters socio-economic and health outcomes that space limitations prevent engaging with here.

Conclusion

Recent disasters in the United States have devastated individuals and communities and highlighted the importance of supporting survivors’ housing needs. We find that severe floods are associated with significant increases in rents for households renting units priced at the bottom of the rent distribution, but not at the middle or the top. Higher levels of assistance to renter households from the Federal Emergency Management Agency (FEMA) is not associated with higher rents. These results address an important empirical question in urban policy analysis about how market actors treat vulnerable groups affected by societal shocks, and a related theoretical question after decades of privatization about how to ensure that all households, but especially those with the lowest incomes who are most vulnerable to climate disasters, have the support they need to recover and to thrive after these events.

Supplemental Material

sj-docx-1-uar-10.1177_10780874241243355 - Supplemental material for High and Dry: Rental Markets After Flooding Disasters

Supplemental material, sj-docx-1-uar-10.1177_10780874241243355 for High and Dry: Rental Markets After Flooding Disasters by Mark Brennan, Tanaya Srini and Justin Steil in Urban Affairs Review

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Supplemental Material

Supplemental material for this article is available online.

Notes

Author Biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.