Abstract

This article examines how home and land tenure shapes manufactured home (MH) residents’ access to financing and consumer protections. Three tenure categories are explored: homeowners who own both home and land (own–own), homeowners who do not own land – often paying to rent it (own–rent) and home renters who also rent their land (rent–rent). A new nationally representative US survey sheds light on the characteristics of these residents, with a focus on metropolitan compared with non-metropolitan locations, landownership, house titling, the type of home financing used by borrowers and financial stability. This survey provides detail previously unavailable in other data. Results show that US MH buyers are much less likely to use mortgages compared with site-built home buyers. Instead, MH owners who currently have a loan for their home are more likely to use home-only (‘personal property’ or ‘chattel’ loans) or contract financing arrangements such as rent-to-own, seller financing or contract for deed. Mortgages have the strongest consumer protections, so use of these alternatives leaves buyers more at risk of eviction, foreclosure and financial instability. Challenges with access to mortgage financing and robust consumer protections are especially acute for MH owners in metropolitan areas because they are more likely to rent their land. However, local-, state- and federal-level policy updates can improve access to safe and affordable homeownership, and for renters, policymakers can mandate formal lease agreements to improve housing stability.

Introduction

Manufactured homes (MHs) are currently one of the only ways that smaller, lower-cost homes are made in the United States – filling an especially important supply gap (Kaul and Pang, 2022; Freddie Mac, n.d.). In addition, MHs – which are the modern version of mobile homes but built to the updated US Housing and Urban Development (HUD) code federal standards (US Department of Housing and Urban Development, n.d.) – have been shown to save a buyer around US$50,000 to US$100,000 compared with similarly sized ‘site-built’ homes (Herbert et al., 2023), and are more affordable even in rural areas (Mimura et al., 2015).

MH quality has improved quite a lot over the last five decades since the HUD code came into existence. These homes can now be constructed to be virtually indistinguishable from other single-family homes (with pitched roofs, high-end finishes, porches and garages) but outdated exclusionary zoning in many metropolitan areas continues to prevent their use in many places that could benefit from lower-cost single-family homes (Herbert et al., 2024).

Currently, MHs in metropolitan areas are largely relegated to parks and communities, often sited in industrial or commercial areas, on leased land (Pierce et al., 2018). In these cases – due to state laws in almost all states – owned homes on leased land can only be titled as personal property, like an automobile. As a result, these homeowners often slip through the cracks of both homeowner and home rental protections. Homeowners who rent their land can be evicted for lack of land payment but, even more challenging, they can be evicted en masse simply because a community is sold or redeveloped, putting homeowners at risk of loss of their home through no fault of their own (I’m HOME [Innovations in Manufactured Homes], 2014; Sullivan, 2017).

However, metropolitan places could better leverage MHs to supply much-needed safe, affordable, stable homeownership by allowing them to be installed and affixed to foundations on land that the homebuyer owns (as infill in neighbourhoods or new developments) and titled as real estate. This would allow MHs to be used to their full advantage – providing a lower-cost housing option with all the benefits of homeownership without the nagging disadvantages that homeowners on rented land experience. There is some indication that this has started, with a few new non-profit and for-profit companies in metropolitan regions around the United States beginning to use MHs in developments where homes are sold with land and financed with a mortgage (Herbert et al., 2024).

This article’s analysis is based on an original survey of 1252 adult MH residents. The survey introduces the many ways that MHs and the land they are on are owned or rented, how titling impacts access to credit, the use of largely unregulated contract financing and the challenges with housing stability especially for land renters. These components can be difficult to study using available administrative or census data, as a homeowner is often assumed to also own their land and there is no way to discern if the home is owned as real estate or personal property. In addition, less traditional loan types (like rent-to-own, contract for deed and seller financing) are not included in administrative data. The remainder of the article discusses the relevant literature, covers the survey design, presents descriptive findings on MH topics and demographics and then concludes with reflections and conclusions for future research.

Understanding home and land tenure in manufactured housing

Homeowners in the United States almost always also own the land beneath their home (though there are some who live in condominiums, in cooperatives or on land trusts where this is not the case). Other homes are automatically titled as real estate and it is often taken for granted that the home and land are owned by the same person. In contrast, MH residents can own both their home and land (own–own), which is most like the ownership structure of other single-family homes though usually not automatically titled as real estate; own the home but rent the land (own-rent); or rent both the home and the land (rent–rent). There were three respondents who reported that they rent their home and own their land. These respondents are included in the analysis but not as a breakout category. Most landowners are on private land but 8% are in resident-owned communities or cooperatives. In addition, though most owner–renters report that they rent their land from a business (54%) or person that they aren’t related to (28%), 9% are on family land and another 1% are on tribal or nonprofit-owned land. Both the own–own model and the rent–rent model are quite like usual models of homeowning or home renting. However, the own–rent model is unique to MHs in the US context. Because MHs are the modern version of mobile homes, and before that trailers could be pulled behind a vehicle, they are treated by default more like automobiles than homes in state law – typically titled as personal property until the homeowner can show that the structures have met the required criteria to treat them like a home (Fannie Mae, 2020). Yet MHs are not particularly mobile – the majority are moved just once from the factory to their permanent location. Moving a home after installation is extremely costly and finding a new site can be onerous (Wallender and Tynan, 2024).

Homeowners: MH can be owned and financed like site-built homes

Despite the stereotypes, about half of all MH residents also own their land (own–own) – just like site-built homeowners (Park, 2022). Landownership is even more common among those who purchase their home with a mortgage or personal property ‘chattel’ loan secured by the home-only. These loans are reported in Home Mortgage Disclosure Act data, and 64% of these borrowers in 2019 owned or were purchasing land. Among own–own residents who get financing, most use a real estate mortgage. However, even among this group, 17% use a home-only personal property ‘chattel’ loan (Consumer Financial Protection Bureau [CFPB], 2021).

The own–own model is most common in non-metropolitan areas, likely due to exclusionary zoning in metropolitan places rather than demand, since at least half of these homes are in metropolitan areas (Durst and Sullivan, 2019). MHs on owned land could easily be used wherever a site-built single-family home is appropriate, yet in many metropolitan locations MHs are excluded from use or require onerous permitting processes or zoning variances. However, this use pattern could be changed. MHs could be used as a more affordable and quickly constructed source of housing for new developments or infill housing and sold with the land as real estate. There are a few new examples of developers using them in just this way starting up around the United States (Peters, 2024).

Renters: MHs can be rented along with their land just like site-built homes

Nearly a quarter of MH residents rent both their home and their land (rent–rent) (Park, 2022). However, little is written about the role that MHs do or could play in the rental market when both the home and land are rented. These residents tend to be very low income and the homes they rent are more likely than owned units to have been made before 1976 – when the national HUD code came into force to improve housing quality (Apgar et al., 2002).

Homeowners who don’t own land: Challenges accessing safe and affordable financing and renter instability

For those who rent land in a community, there can be several risks. MHs in such settings are either financed or purchased in a lump sum in cash, yet because the land is rented the homeowner can still be evicted from the land. Evictions can come about due to nonpayment of lot rent. However, residents can also be evicted due to some infraction of community rules or because the land is sold for redevelopment. In most places, land rents can go up unexpectedly, becoming untenable for the homeowner. Because it can be hard to find a new location and moving a home is expensive, people who cannot stay on their rented land may lose their homes or be forced to sell (Legal Services Corporation, 2023). These own–rent scenarios can bring a concerning mix of the responsibilities of homeownership (e.g. insurance, maintenance) without the corresponding consumer protections (e.g. foreclosure protections, homeowner disaster recovery and relief).

In addition, homeowners who do not own their land cannot title their home as real estate in most states, and so cannot obtain mortgage financing. 1 Real estate titling is required in order to get a mortgage, which has the lowest interest rates, longest terms and strongest consumer protections compared with home-only personal property loans and what is known about contract financing such as lease-purchase and instalment sales contracts (CFPB, 2021; Pew Charitable Trusts, 2025). This restriction is not just for those who pay to rent their land. Most homeowners who live in a cooperative where homeowners collectively own the land are similarly excluded from real estate titling in most states. This is also true for homeowners on tribal or family land even if they have long-term leases and the borrower and home meet all other criteria. Though there are some states in which a homeowner who does not own land could title an MH as real estate when they have a long-term lease, getting a mortgage when land is not owned by the same person who owns the home remains challenging and often impossible (Fannie Mae, 2023). However, federal policymakers at Fannie Mae and Freddie Mac are starting to pilot methods to better serve homeowners with long-term leases or on tribal land (Fannie Mae, n.d.; Freddie Mac, n.d.).

Gaps in the literature

It has been documented that most MHs in metropolitan areas are on rented land and in non-metropolitan areas the majority are on owned land (Durst and Sullivan, 2019). Yet there is a gap in the literature regarding how landownership and informal homeownership impact access to financing and consumer protections. In fact, Lamb et al. (2023) note a broader lack of attention to MHs in the academic and practitioner literature. In particular, though mortgage and home-only financing are easy to study using publicly available Home Mortgage Disclosure Act data, little research has investigated the prevalence of largely unregulated forms of contract financing (rent-to-own, contract for deed and instalment sales contracts), or how often homes are purchased in cash. In addition, for renters little is known about who owns the land. Moreover, determinants of financial stability for MH residents are not thoroughly studied. This survey and article aim to fill these gaps by examining the following research questions:

What is the prevalence of US MHs by tenure and how does this vary between metro and non-metro areas?

How does financing access for MH residents vary by tenure or metro/non-metro location?

Do tenure or metro/non-metro location affect MH residents’ financial stability?

Methods and data

To better understand these relationships, Pew commissioned a survey from Ipsos Public Affairs’ (Ipsos) KnowledgePanel probability-based web panel 2 (Pew Charitable Trusts, 2025). Ipsos’ KnowledgePanel is designed to be nationally representative of the United States. This Pew 2022 MH survey was fielded from 23 November to 26 December 2022 among 42,984 US residents aged 18 or above who spoke either English or Spanish who constituted the panel. Seventy-one per cent completed the qualification questions: whether they made financial decisions for the household, and whether they lived in an MH as their primary residence. Most of these did not qualify for the survey. Ipsos KnowledgePanel response rates among those who qualify averages 60%. 3 Ultimately, 4% or 1252 completed the full survey in English or Spanish. For reference, MHs represent around 6% of the US housing stock (Fannie Mae, 2020) and our survey was limited to individuals who were 18 years or older, living in a mobile or MH as their primary residence and who said that they make financial decisions for their household. Therefore 4% qualifying for the survey was reasonable given the survey screening. We present weighted percentages up to the national population of US adult households based on survey weights provided by Ipsos, which are weighted based on the following characteristics: sex, age, race/ethnicity, education, census region, household income, homeownership status, metropolitan designation and Hispanic origin.

The next section first provides survey-based descriptive analysis of US MHs by tenure and metro/non-metro areas and compares them to site-built homes where relevant comparison data exists (CPS or ACS). Next, a descriptive analysis of how MHs are titled, bought and financed follows. Then, we examine the financial stability of MH residents using regression analysis. We transformed four survey questions into binary financial stability measures:

(1) Behind on payments: are you currently caught up on land and home payments? (Yes/no).

(2) Forced to leave home: how likely is it that your household will have to leave this home within the next two months because of eviction, foreclosure or repossession? (Somewhat/very likely vs. not very likely/not likely at all).

(3) Forgo expenses: in the last 12 months, how many months did your household reduce or not pay expenses for basic household necessities, such as medicine or food, in order to pay an energy bill or housing costs? (One or more months vs. never).

(4) Unsafe temperature: in the last 12 months, how many months did your household keep your home at a temperature that you felt was unsafe or unhealthy? (One or more months vs. never).

We estimate these binary measures using logit regressions weighted by survey weights, with the following explanatory variables: housing tenure, metro/non-metro, location in an MH community, race/ethnicity, income, sex, age, marital status, household size, presence of children, educational attainment, employment, veteran status, disability status and census region.

Results

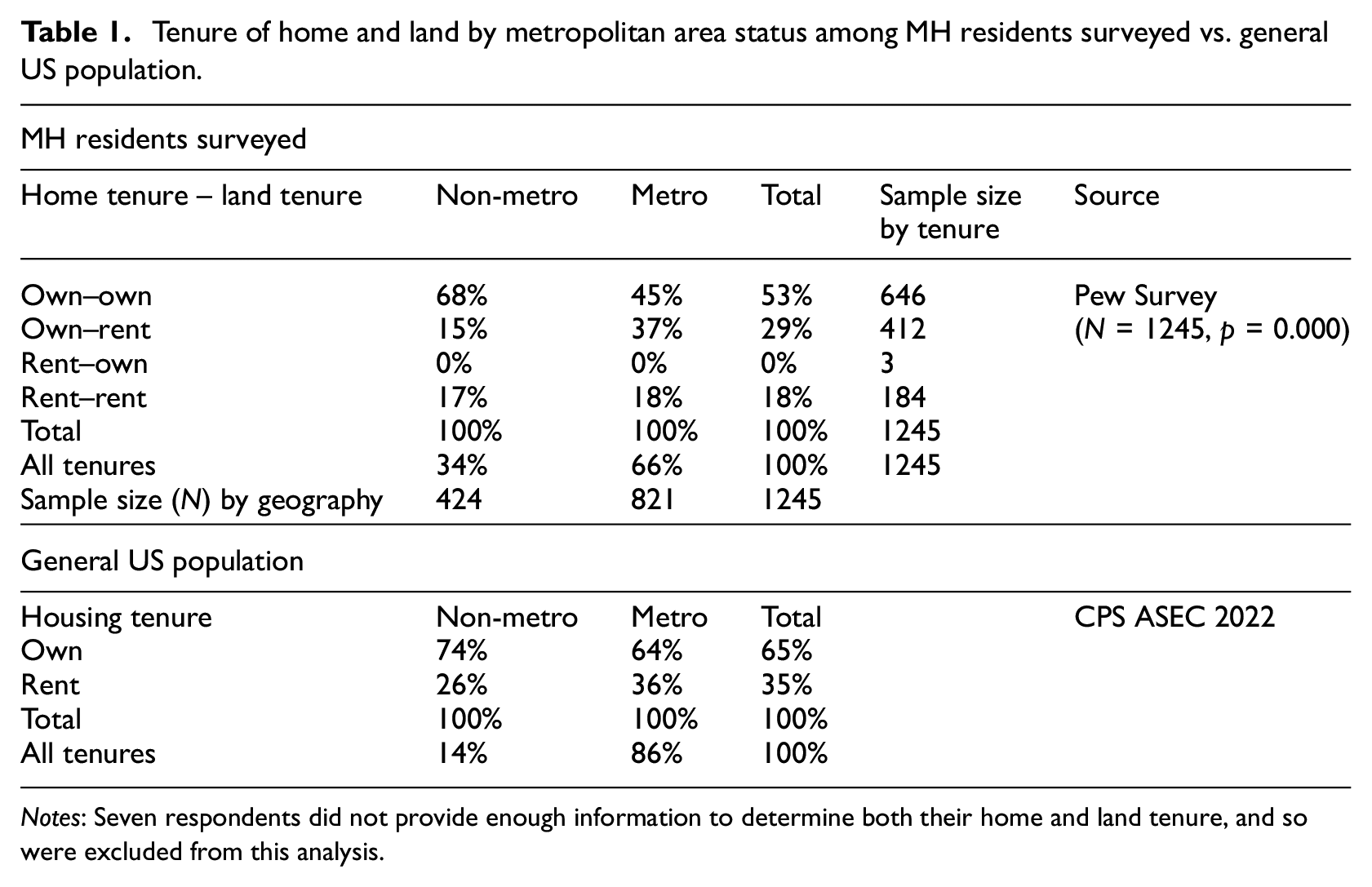

The Pew Survey found that 66% of respondents live inside a metropolitan area – in a densely populated urban place or surrounding less densely populated places (Table 1). Other research has found that about half of MHs are in metropolitan areas (Durst and Sullivan, 2019). Yet, the general US population is much more likely to be in metropolitan areas (85%; Table 1).

Tenure of home and land by metropolitan area status among MH residents surveyed vs. general US population.

Notes: Seven respondents did not provide enough information to determine both their home and land tenure, and so were excluded from this analysis.

There are multiple reasons for these differences. First, MHs tend to be more prevalent in rural areas (Choi and Goodman, 2020; Durst and Sullivan, 2019). Second, though Ipsos tries to reach more rural places and provides internet-enabled tablets to participants who do not have internet access, it is also possible that some MH residents in non-metropolitan areas are underrepresented. MH residents, especially those living in rural locations in the United States, can be hard-to-reach populations as they have relatively lower income, educational attainment and broadband access, and thus lower participation in and response rate to Ipsos’ national panel. Where relevant, we highlight differences by metro and non-metro areas. However, many other factors such as home and land ownership, use of mortgage and home-only financing and titling practices align with other datasets such as HMDA and AHS.

Those who own both land and home (own–own) make up 53% of MH resident respondents to our survey (Table 1). An additional 29% own their homes but rent land (own–rent) and the remaining 18% rent both (rent–rent). The rent–rent share is about the same for metro and non-metro areas. Own–own is especially common in non-metro areas (68%) and less usual in metro areas. In contrast, own-rent is just 15% of MHs in non-metro areas yet makes up 37% in metro places. Own–own rates are below the general US population homeownership rate, but if own–own and own–rent are added together, MHs have a higher house ownership rate.

We report additional demographics for MH residents with comparisons to the general population in Appendix 1.

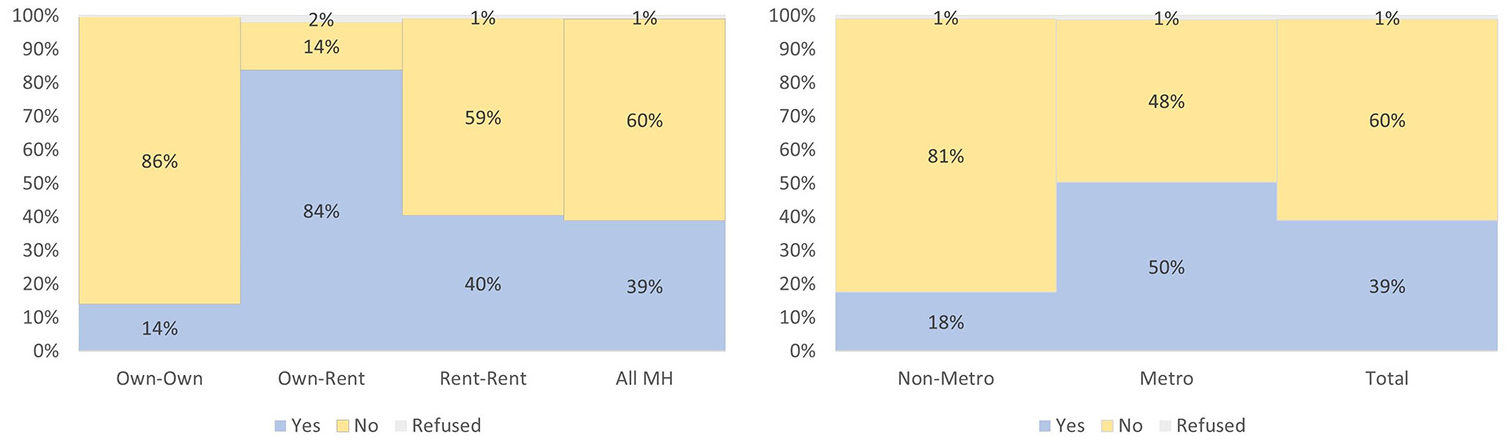

Manufactured home communities

Overall, 39% of MH residents live in manufactured home communities (MHCs) (Figure 1). The share of rent–rent residents living in MHCs is 40%. However, own–rent residents are predominantly in MHCs (84%), while just 14% of own–own residents are in MHCs. Own–own residents in MHCs are akin to homeowners in site-built subdivisions or may be in cooperative resident-owned communities. Communities are much more prevalent in metro areas, with 50% of MH residents reporting living in one regardless of home/land tenure. In non-metro areas, just 18% are in communities. Other research has found that California and Los Angeles County, for example, have 75% of MH residents in MHCs (Pierce et al., 2018).

MH residents by whether they live in a community by home and land tenure and metro/non-metro.

Financing and titling

Difficulty obtaining financing is a key challenge for aspiring or existing MH owners (Kouhirostami et al., 2023), even for those in communities (Kear et al., 2023). Though own–owners could get a mortgage, some still use home-only loan or contract financing. This can be due to differences in titling, appraisal, state laws, etc. Home-only loans are also generally not purchased in the secondary market (West, 2006), meaning that lenders hold them on portfolio, without a ready market to sell them, making them usually more expensive and less beneficial for the borrower than a mortgage. Home-only loans were also not included in Great Recession-era mortgage buy-downs and market reforms (Burkhart, 2009). Home-only loan markets are understudied; information on titling is hard to obtain from administrative sources. This section uses the Pew Survey to better understand the relationship between financing, titling, home and land tenure and metropolitan designation.

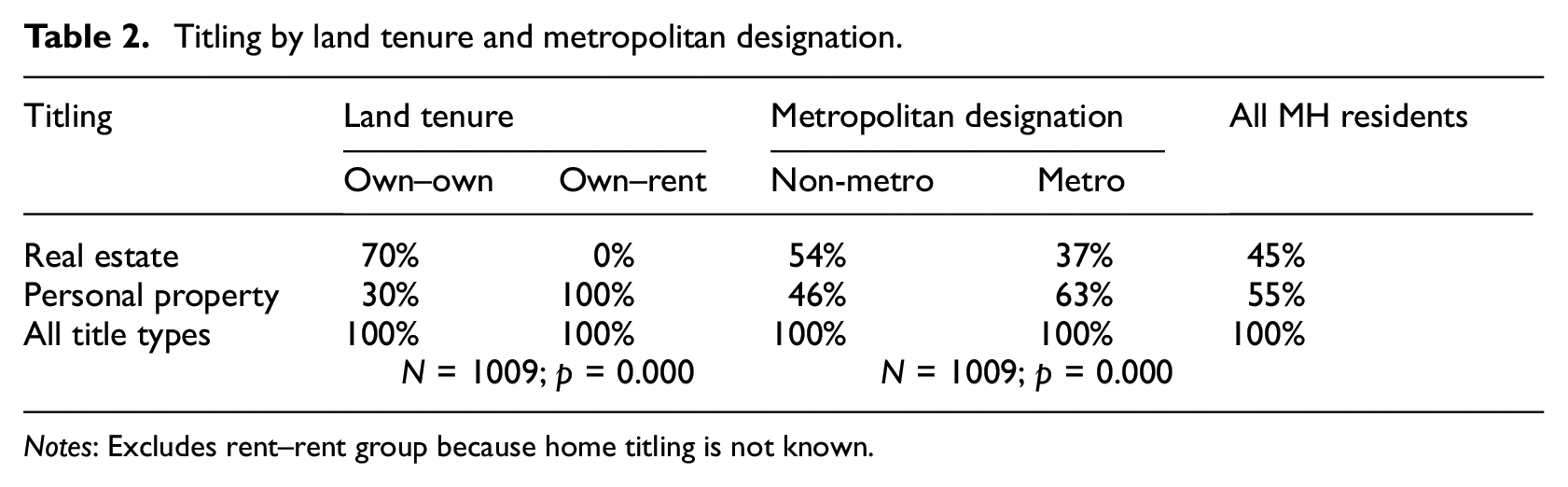

Own–rent residents almost always title their homes as personal property, since land ownership is usually necessary for titling as real estate (Table 2). 4 MH owners who live in metropolitan areas are more likely to own their home as personal property. This difference likely reflects the larger share of residents who own–rent in metro areas versus non-metro areas. Among those who own both home and land, 30% still title their homes as personal property rather than real estate.

Titling by land tenure and metropolitan designation.

Notes: Excludes rent–rent group because home titling is not known.

Titling is rarely changed. Survey responses show that only 22% of own–own residents who bought their home titled as personal property converted their home from personal property to real estate after they purchased it, 14% did not know whether they had converted and 62% kept it as personal property. When asked if they could convert title to real estate, 38% said yes, 16% said no and nearly half said they did not know. The most common reasons for not converting from personal property to real estate titling included not seeing the benefit of retitling, a lower tax rate for personal rather than real property and only wanting to place the home and not the land on the loan (likely to avoid the risk of losing the land if the borrower falls behind on payments). However, research on the tax rates in different states for MHs depending on the titling classification showed that in general taxation was similar to that for site-built homes (Burkhart, 2013). However, additional research could be done to investigate whether MHs titled as personal property tend to be valued less by assessors (and taxed on that lower value) than ones titled as real estate with the land. That said, it is unclear how much homeowners know about the level of taxation if they convert their home to real estate.

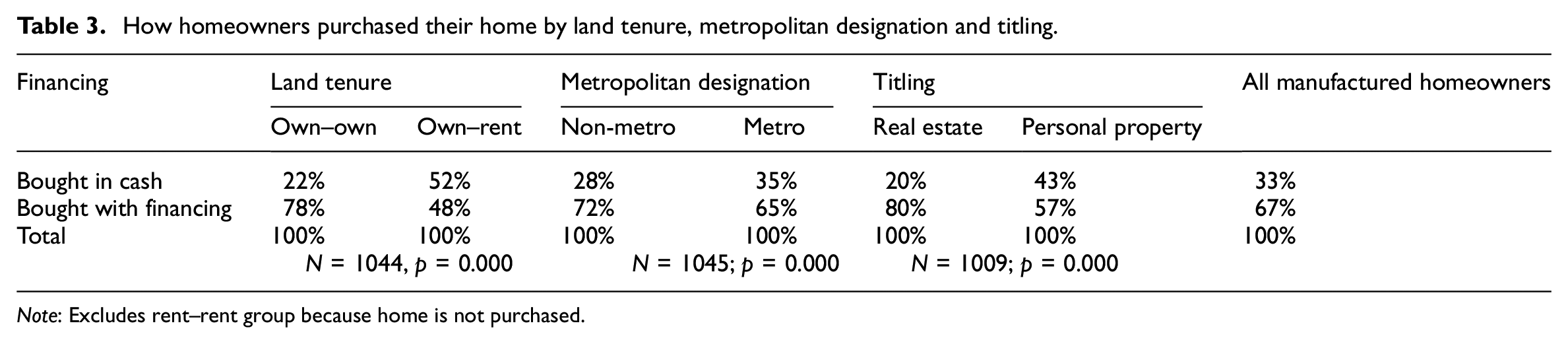

One-third of MHs in our sample were bought in cash (Table 3), approximately in line with the overall US housing market (Anderson, 2023; Lautz, 2024). The cash buyer share was over 50% for own–rent residents, but only 22% for own–own. While many cash transactions in the overall US housing market are for vacation homes or investment properties (Lautz, 2024), our survey focused on individuals and primary residences, suggesting that these factors do not explain the high cash purchase rate for own–rent. Cash purchases were also more likely to be titled as personal property, likely reflecting the high own–rent share of homes titled this way.

How homeowners purchased their home by land tenure, metropolitan designation and titling.

Note: Excludes rent–rent group because home is not purchased.

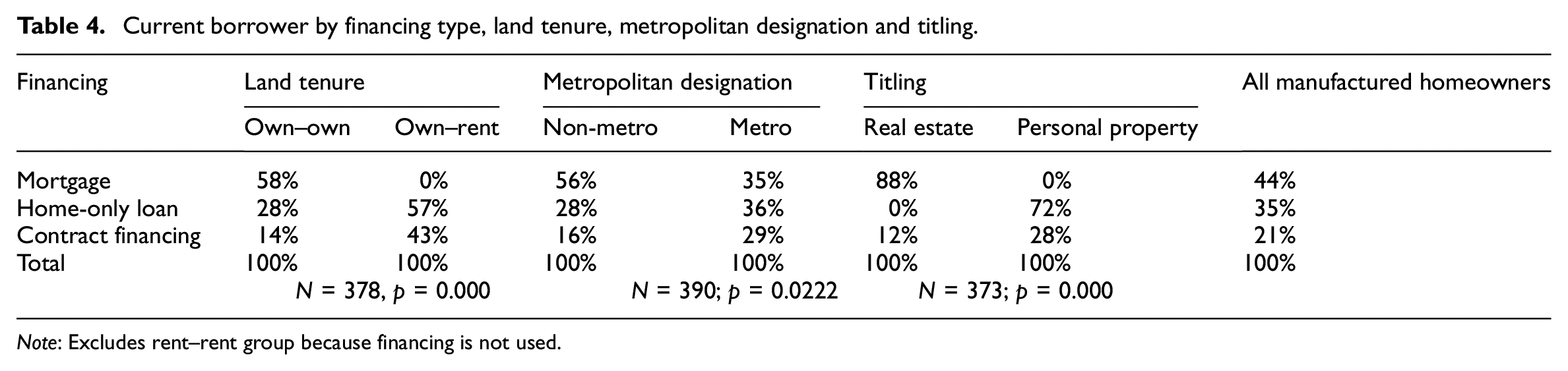

Current borrowers (those still actively repaying their loan) use a wide array of arrangements: 44% of borrowers used mortgages, 35% used home-only loans and 21% used contract financing (such as contract for deed, lease-purchase, seller financing, etc.; Table 4). Recall that an owner–owner can use a mortgage only if their home is also titled as real estate. As a result, 28% of own–own borrowers report using a home-only loan. Contract financing may have the highest borrower costs (though little is known about the details of these contracts due to a lack of standardised recording and the significant informality of these agreements) and the fewest borrower protections (Pew Charitable Trusts, 2022a). While contract financing is used in other parts of the housing market, it is more common for MHs (Pew Charitable Trusts, 2022b). Contract financing was most common for own–rent (43%), for those titling as personal property (28%) and for MHs in metro areas (29%). Home-only loans made up the remainder of own–rent resident borrowing (57%). The bulk of those titling as personal property (65%) used home-only loans. Fifty-eight percent of own–own residents used mortgages, as did 56% of non-metro MH owners. Among those titling as real estate, 12% used contract financing.

Current borrower by financing type, land tenure, metropolitan designation and titling.

Note: Excludes rent–rent group because financing is not used.

Financial stability

The purported financial instability of MH residents is often portrayed as a reason to restricting MH siting, to increase financing costs for MH borrowers and to not buy pools of MH mortgages or personal property loans. However, research on these residents’ financial stability is scant, and differences by tenure, metro/non-metro and demographic characteristics have been understudied.

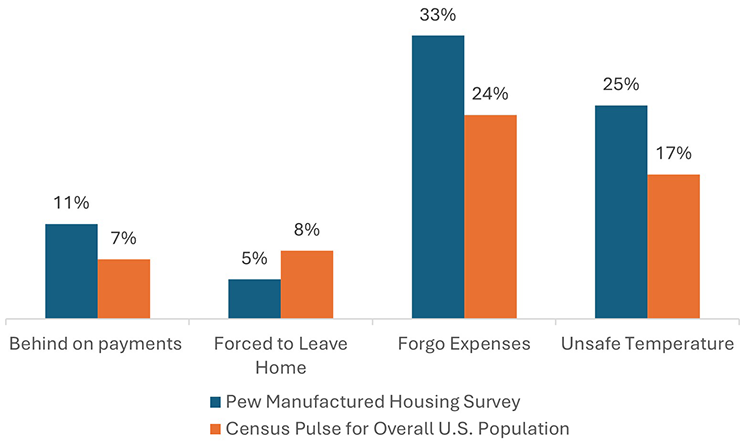

Figure 2 shows our survey’s estimates of financial stability measures compared with Census Pulse results for residents of all other types of homes in the same period (US Census Bureau, 2022). Eleven percent of MH residents surveyed were behind on their home and/or land payment. Differences between the financial stability of metro and non-metro MH residents were not statistically significant, and neither were differences between home and land tenure. In comparison, 7% of Pulse mortgage borrowers were behind on payments. A better comparison (due to the demographics of MH residents) may be Federal Housing Administration (FHA) borrowers, who showed the same delinquency rate as MH mortgage borrowers and a 1% higher rate than non-MH mortgage borrowers (Federal Housing Administration [FHA], 2022).

Manufactured housing resident financial stability.

Figure 2 paints a mixed picture: while housing costs are generally covered and forced displacement is rare, residents nevertheless struggle with utilities and other expenses. Five percent of MH residents in Pew’s survey report forced displacement, which is lower than Pulse (8%). However, a higher percentage of MH residents reported that they had to forgo expenses (33%) and have kept their home at unsafe temperatures (25%) compared with non-MH residents (24% and 17% respectively).

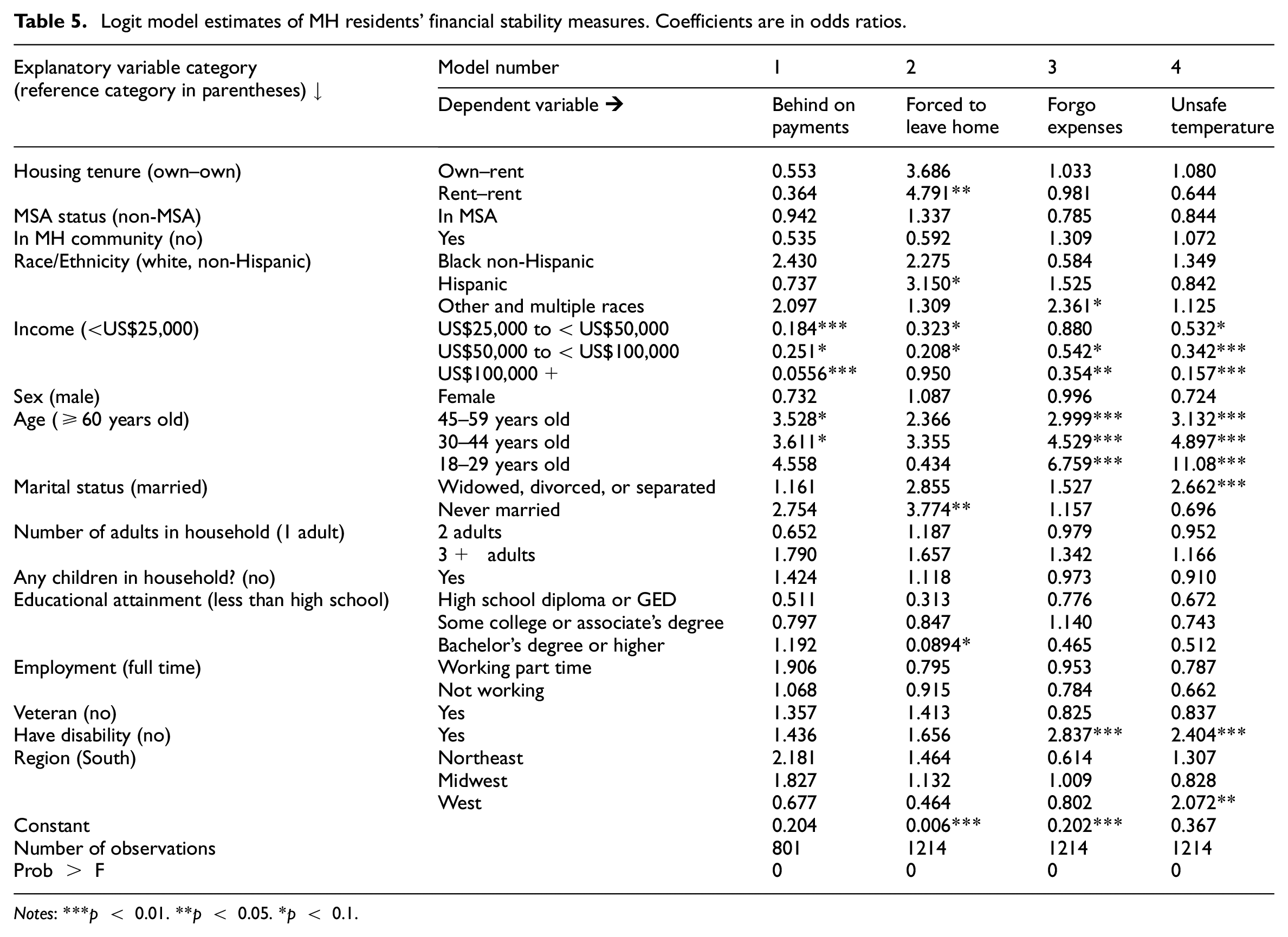

Our regression analysis helps to shed further light on the correlates of financial stability among MH residents (Table 5). Housing tenure is not highly predictive of instability, except for renter–renters who had nearly five times the odds of being forced to leave home compared to owner–owners. Residents with incomes above US$25,000 had much lower odds of being behind on payments, of forgoing expenses or of keeping homes at unsafe temperatures. Younger and middle-aged residents had higher odds of forgoing expenses and keeping homes at unsafe temperatures than those above 60 years old. Those aged between 30 and 60 years also had higher odds of being behind on payments. Never-married residents had higher odds of forced moves, while widowed/divorced/separated residents had higher odds of keeping unsafe temperatures. MH residents with a bachelor’s degree or higher had much lower odds of a forced move. Residents who reported a disability had higher odds of forgoing expenses or keeping unsafe temperatures. Residents in the West region had twice the odds of keeping unsafe temperatures compared to those in the South region.

Logit model estimates of MH residents’ financial stability measures. Coefficients are in odds ratios.

Notes: ***p < 0.01. **p < 0.05. *p < 0.1.

Metro/non-metro, MHC location, sex, employment, household size, presence of children and veteran status yielded no statistically significant differences on financial stability measures.

Discussion

The MH is a key component of the US housing market and has been poised to grow in importance for decades as one of the remaining bastions of affordable homeownership and a cost-effective way to deliver new affordable home supply. However, it has fallen short of its promise, as this sector’s structural and regulatory peculiarities make it challenging to obtain financing to buy a home or to site a home on owned land in many metropolitan areas. Finally, the sector remains understudied, especially for those who rent either their MH or the land under it. This article uses a novel survey to shed light on these issues.

Key takeaways

There are three key takeaways from this survey research:

Own–own is much more common in non-metro areas and own–rent is less common in metro areas. For those who do not own their land, this distinction drives a multitude of gaps in access to mortgage financing, exposure to unexpected increases in home expenses and housing instability, often in part due to lack of land lease.

Homeowners who keep their home titled as personal property face steep challenges in obtaining financing. This survey shows that 28% of borrowers with personal property titling turn to largely unregulated contract financing.

Troublingly, about half of MH residents who rent (own–rent and rent–rent residents) do not have a formal lease. Another 18% of own–rent residents and 25% of rent–rent residents do not know about their lease term. This lack of formal lease arrangements can expose residents to unexpected changes in land costs or even losing their homes.

This research reinforces that homeownership that includes land comes with much stronger consumer protections and housing stability than when a home is owned but the land is rented. However, titling as real estate is key to ensure that own–own residents retain all the benefits of this ownership model. These benefits include consumer protections common for homeowners and access to mortgage financing which carries both lower interest rates and stronger consumer protections – especially if the borrower falls behind.

Though MH residents in metro areas are more likely to have own–rent arrangements, the own–own model could be better leveraged in metro areas to improve access to lower-cost housing that has the same access to mortgage financing and the same consumer protections and avoids the risks and instability of rented land. To accomplish this, MHs cannot be zoned out of metropolitan areas but rather must be allowed for both infill and new developments wherever single-family homes would be appropriate. In addition, to the extent that own–rent models in metropolitan places already exist and play a vital role in access to unsubsidised affordable housing, more could be done to ensure that residents can collectively purchase their communities (e.g. right of first refusal) and that renters enjoy the stability benefits of leases and reasonable consumer protections.

Policy discussion

Based on our research findings, there are three key policy areas that could help improve outcomes for MH owners:

Modernising state titling laws to expand access to mortgages

Updating federal financing policies

Bolstering consumer protections for land renters.

Titling

More work is needed to identify ways to reduce hurdles for MH buyers to title their homes as real estate and finance with a mortgage. Right now, New Hampshire is the only state that automatically titles an MH as real estate. However, Vermont and Oregon also have titling that could allow for real estate among land renters. But in others, usually several additional steps must be taken to convert to real estate (Fannie Mae, 2023). One possible approach is to automatically title a home that will be installed on owned land as real estate unless the purchaser takes steps to title as personal property. Since the majority of owner–owners do end up with real estate titling, this would streamline the process and allow the homebuyer the flexibility to choose personal property titling if needed. In addition, expanding the number of homeowners and buyers who can title their home as real estate could improve access to mortgage financing – improving both the affordability of the loan and applicable consumer protections.

Updates to federal financing programmes

Fannie Mae and Freddie Mac currently purchase MH mortgages, and both have started to explore purchasing mortgages even when the borrower doesn’t own land – such as when the home is in a cooperative, has a long lease or is on tribal land. However, real estate titling is required, so modernisation of state titling laws is necessary in most states for borrowers to gain mortgage access (Fannie Mae, 2025; Freddie Mac Single-Family, 2025).

Home-only loans for MHs are the next best option if a mortgage isn’t possible. However, due to a lack of federal programmes to insure, guarantee or purchase a loan, the sector is extremely uncompetitive. Just five private lenders provide over 75% of the loans, two-thirds of loan applications are denied and interest rates are often double mortgage rates (Liang et al., 2022). To address these challenges, FHA and Ginnie Mae made some updates to their defunct Title I programme in 2024 which mirror their thriving Title II programme for mortgages. Specifically, FHA updated their loan limits and set a standard so that loan limits would be increased based on the market yearly. Ginnie Mae amended lender net worth requirements to be more like those for mortgage companies (US Department of Housing and Urban Development, 2024). However, further modernisation (such as allowing automated underwriting) could help improve access to credit and reduce barriers to entry for new lenders. Fannie Mae and Freddie Mac also have the explicit ability to start home-only loan programmes but have yet to do so.

Bolstering consumer protections for land renters

There are several ways to bolster land renter stability. Fannie Mae and Freddie Mac require tenant protections in any community that they help finance so that residents have leases of at least one year and other consumer protections to improve their stability (Freddie Mac Multifamily, 2019). In addition, states and localities can consider putting more consumer protections in place (such as renewable leases and eviction only for good cause).

Conclusion

The current housing supply needs in the United States are severe, with a shortage of between 4 and 7 million homes. This has resulted in rising housing prices and skyrocketing homelessness. MHs used to make up a much larger proportion of overall housing but have never fully recovered from the Great Recession due to outdated zoning regulations and financing policies. However, there are great opportunities to remedy these problems. Federal-level programmes are especially well placed, and FHA has taken important first steps to improve access to credit for MH buyers. States and localities have an opportunity to expand where these lower-cost homes can be placed and to lower barriers to allow them to be used where single-family homes or accessory dwelling units are permitted. And lastly, metropolitan areas should consider how to best preserve their lower-cost MH communities while also ensuring housing stability for the residence. Right now, homeowners in communities tend to be especially vulnerable to unexpected changes due to a lack of land leases, short land terms and lack of financing options, yet well-placed policies could drastically reduce these risks. Overall, the MH needs to be treated as what it is – a home (not a vehicle) – and to be allowed to be used as such.

While this article shines additional light on MH resident experiences, more work remains to be done. The survey, while valuable, can only provide high-level understanding about important topics like contract financing, financial stability or resident-owned communities, because of small sample sizes. Manufactured housing is not a monolithic category, and future surveys should attempt to oversample in difficult-to-weight categories, such as own–rent, contract financing users or resident-owned community residents. Future work should also focus on understanding the determinants of financing and titling among MH residents. Qualitative vignettes could be a useful follow-up to provide context on the different home and land tenure and titling arrangements.

Footnotes

Appendix 1

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Disclaimer

The views in this article are of the authors and do not necessarily reflect the views of The Pew Charitable Trusts.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: We gratefully acknowledge use of the Manufactured Housing Survey 2022 funded by the Pew Charitable Trusts.