Abstract

Value capture (VC) is widely cited as a method for local authorities to provide urban public goods to their cities in the face of fiscal stress. Its application in practice however remains limited. In this article, we aim to explain the implementation process of VC as a strategy to fund public transportation infrastructure through case studies in London, New York, and Copenhagen. Adopting a theory of gradual institutional change, we argue that the implementation of VC depends on the capacity to change distributional institutions that are inherently contested. Particularly relevant is the role of the beneficiary, whose support of VC is necessary but not likely. Our results show that a strategic urban development project can act as a driver to overcome this barrier, but that this driver can, simultaneously, also hinder the institutionalization potential of a VC strategy. We therefore suggest that, for VC strategies to become more commonplace, sharing value uplifts among beneficiaries must become more commonplace too.

Keywords

Introduction

Cities around the world are facing major spatial challenges, such as meeting the growing demand for affordable housing, managing the risks associated with climate change, and improving polluting and congested transportation systems. Crucial to addressing those challenges is the provision of sustainable urban infrastructure, such as light rail transit, smart grid heating, and climate adaptation measures. While it is clearly in the collective interest to invest in such urban infrastructure, urban stakeholders are mostly dependent on public authorities to provide the necessary funding even though local authorities in many countries are finding it increasingly difficult to do so (Ingram and Hong 2012). Public resources are under pressure as local authorities face fiscal constraints, some of which have been worsened due to the COVID-19 pandemic (Love et al. 2021; United Cities & Local Governments, 2016).

Faced with their spatial challenges and responsibilities, many local authorities are considering new, innovative funding strategies. More often than not, these considerations involve the application of value capture (VC), a concept or tool by which the value uplift generated by a public investment is used to fund that investment (Chapman 2017; Ingram and Hong 2012; Medda 2012). The theoretical advantages of VC are widely accepted, including its efficient economic logic, capability to generate significant revenue, financial justice and ability to concentrate development (Batt 2001; Mathur and Smith 2012; Peterson 2008; Suzuki et al. 2015). In practice, however, the use of VC to fund sustainable urban infrastructure remains limited. Although numerous countries do use an indirect form of VC by shifting infrastructure costs to private developers (Cervero and Murakami 2009; Muñoz Gielen and Tasan-Kok 2010), only a few countries such as Israel and Poland apply funding instruments based on the idea that property owners should relinquish part of the value uplift caused by public investments (Alterman 2012; Yoshino, Helble and Abidhadjaev 2018).

Despite extensive evidence of value uplift caused by new urban infrastructure (see Gupta, Van Nieuwerburgh and Kontokosta 2022; Peng and Knaap 2023 for recent studies), city authorities attempting to implement new VC strategies typically encounter a variety of barriers (Salon, Sclar and Barone 2019; Suzuki et al. 2015). A greater understanding of the process of VC implementation is needed. Indeed, there is a large body of work on VC, but few studies focus on the implementation process of a new VC strategy (Li et al. 2022; Mathur and Smith 2013; Smith and Gihring 2006) while even fewer attempt to explain the inner workings of such an implementation process (Aveline-Dubach and Blandeau 2019).

In this article, we therefore aim to construct a better understanding of the implementation process of VC as a strategy to fund public transportation infrastructure. In search of a useful way to understand this phenomenon, we propose to interpret this process as an effort of institutional change, which we analyze using Mahoney and Thelen's (2010) power-distributional perspective on such change. By adopting this perspective, we will show that the implementation of VC is not only an instrumental process, but also depends on the modification of contested distributional institutions. Our focus on transportation infrastructure is based on the dominance of this type of infrastructure in VC literature as well as the availability of cases, but we assume that our insights will provide starting points for understanding the implementation of VC strategies in funding urban infrastructures more broadly.

Combining intensive desk research and semi-structured interviews with key decision-makers and local experts, we investigated the processes for implementing VC for three major urban infrastructure projects: Crossrail 1 in London, the extension of the No. 7 Line combined with the redevelopment of Hudson Yards in New York, and the development of the first two metro lines combined with the development of the Ørestad district in Copenhagen.

We continue by reviewing the literature on VC, highlighting the role of the beneficiary as a key actor. We then build our theoretical perspective based on novel insights of gradual institutional change. After discussing the methodology of our empirical study, we use this perspective to present our findings on the implementation of VC in our three cases. We then discuss how the support for a strategic urban development project enabled a one-time application of VC in all three cases, but at the same time impeded the institutionalization of VC in two of them. We conclude the paper by discussing the interplay between institutional change and urban infrastructure funding strategies and provide recommendations for further research on VC.

Variants of VC

VC is based on the idea that public investments create financial value, and that this value can in turn be captured to fund those investments. The main idea behind it is that the beneficiaries of public, local investments are not only their direct users but also adjacent property owners and property developers who benefit from enhanced locational advantages (Zhao and Levinson 2012). Through VC, these actors are asked to contribute as well.

Much of the VC literature focuses specifically on land VC, which focuses exclusively on capturing the increments in land value. This focus is based on the economic assumption that all value added will be capitalized in land prices (e.g., Ingram and Hong 2012; Levinson and Istrate 2011; Medda 2012). In practice, however, we also see the use of various VC instruments that are not directly linked to land value, but rather capture other value uplifts such as those in property values or property taxes. Therefore, following Muñoz Gielen and Lenferink (2018), we use the more generic concept of public VC, which includes “all instruments that capture all possible increases of the value of land and buildings” (p. 795). This corresponds to the concept of location VC (Salon, Sclar and Barone 2019).

Because of our interest in the implementation process of VC, we classify VC variants according to the type of beneficiary, i.e., types of actors who receive some form of economic value caused by a public infrastructure investment. The choice of beneficiary may formally seem an instrumental choice: who benefits from an infrastructure investment and through which instrument can the economic value uplift be captured? However, there are clearly also political and legal dimensions to consider. The implementation of VC requires the beneficiary to make a financial contribution that it did not have to make before, either voluntarily or compulsory. This makes the choice of the beneficiary politically relevant, and legally significant for the implementation process.

Following Zhao and Levinson (2012, p. 1), we distinguish three types of beneficiaries that are relevant for the implementation of VC. In the first category, local authorities capture value through land development. There are multiple ways to do this. If local authorities own the land themselves, they can capture the value uplift through land lease or sale. If private actors own land and develop it themselves, local authorities can apply funding instruments such as air rights or development impact fees (Li et al. 2022; Mathur and Smith 2012; Zhao and Levinson 2012). Other examples of VC strategies based on new development include joint development (Zhao, Das and Larson 2012) and active land policy (Muñoz Gielen 2010).

The second category concerns owners of existing real estate (RE), who often see an increase in the value of their properties when public transportation investments increase the accessibility of these properties (Lari et al. 2009; Smith and Gihring 2006; Suzuki et al. 2015). Local authorities can capture (part of) this value uplift through instruments such as a betterment tax, betterment levy or benefit assessment (Medda 2012). The term “betterment” however has a diverging meaning in the VC literature. Alterman (2012) for instance distinguishes two types of betterment levies: the development-rights type, where the value uplift is due to a planning or development control decision, and the infrastructure-based type, where the value uplift is due to the approval to develop a particular public infrastructure project. Within the taxonomy of this article, only infrastructure-based levies fall under the second category. We consider betterment levies based on development-rights as part of the first category. 1

The final category of beneficiary is the local tax-collecting authority. A transportation investment can generate value uplift in an area by increasing the value of existing RE and enabling the development of new RE—both of which increase property taxes. Local tax-collecting authorities, such as municipalities, can capture this value uplift by earmarking the expected increase in tax revenues within a specific area. This is also referred to as an accessibility increment contribution (Medda 2012). A well-documented example of this is tax increment financing (TIF) (Squires and Lord 2012, p. 818). 2

However, applying a VC instrument in a city, region, or country where it has not been applied before can be a major challenge. An institutional perspective can help explain why this is so challenging.

Institutions and VC Implementation

In this article, we argue that the implementation of VC is not just a matter of applying a novel policy instrument, but that it should rather be understood as a process of institutional change. Adopting an institutional perspective can be especially useful in understanding the politics of implementing VC. Following Elinor Ostrom (2005, p. 3), we define institutions as the rules and prescriptions shaping and influencing the behavior of individuals and their decisions. These institutions can be both formal and informal (North 1990).

Provision of public goods always involves formal institutions (Pierson 2004) that have to be adapted if a new VC instrument is to be implemented. In case of a large group of beneficiaries, for instance, the problem of free-riding arises (Hardin 1982), which can be countered with rules that set the requirements for mandatory contributions. If local authorities decide to use their own value uplift to fund public infrastructure, this is often accompanied by institutional changes such as the creation of a regulatory body to administer and execute tax collections or the establishment of a legal entity to manage the land and/or property development process.

Such formal institutions and governance arrangements are typically embedded in informal institutions, such as local norms or customs (Williamson 2000). To secure successful VC implementation, these informal institutions might have to change as well. The feasibility of a betterment tax can, for instance, depend on the willingness of citizens to accept new taxes, thus challenging dominant views on private property protection and government taxation. The decision to apply TIF, on the other hand, can challenge prevailing levels of nation-state control, or customs that dictate what government tier picks up the tab (Alterman 2012; Salon, Sclar and Barone 2019; Squires and Lord 2012). The implementation of a new instrument to fund public infrastructure can thus challenge many written and unwritten rules and procedures, thereby requiring a process of small or elaborate institutional modification.

Changing Institutions

Institutional change can be viewed as either a spontaneous, evolutionary process or as the outcome of a deliberate design. Given our interest in the deliberate implementation of VC, we are primarily interested in the latter. This view is also referred to as endogenous institutional change (Greif and Laitin 2004; Kingston and Caballero 2009).

Changing institutions however is no simple task. Institutions can be purposefully difficult to alter, because actors like to rely on them (Pierson 2004). In effect, over time, institutions become increasingly difficult or costly to change, which causes what can be referred to as path dependency (Mahoney and Schensul 2006). The longer actors operate in a status quo, the less attractive a shift to an alternative becomes, leading to a “lock-in” created by path-dependent institutions (Arthur 1989).

How then can institutions change? For a long time, institutions were understood to arise and change primarily through critical junctures, i.e., transformative moments of major change, often in response to exogenous shocks, such as natural disasters or defeat in war. According to these theories, institutions are understood to change less or much more slowly in between critical junctures (Capoccia and Kelemen 2007; R. B. Collier and Collier 1991; Sorensen 2017).

A growing body of work, however, focuses on the gradual institutional change irrespective of critical junctures (Mahoney and Thelen 2010; Streeck and Thelen 2005; Thelen 2009). Streeck and Thelen (2005) argue that much of the institutional change in the political economies of today's advanced capitalist societies unfolds primarily incrementally, without dramatic disruptions. Therefore, scholars are increasingly focused on understanding incremental institutional change, which is endogenous rather than induced by some exogenous shift or shock (Lowndes and Roberts 2013; Mahoney and Thelen 2010). As we will show, our cases demonstrate that this perspective of gradual institutional change is particularly relevant in explaining the implementation process of VC.

Characteristics of Gradual Change

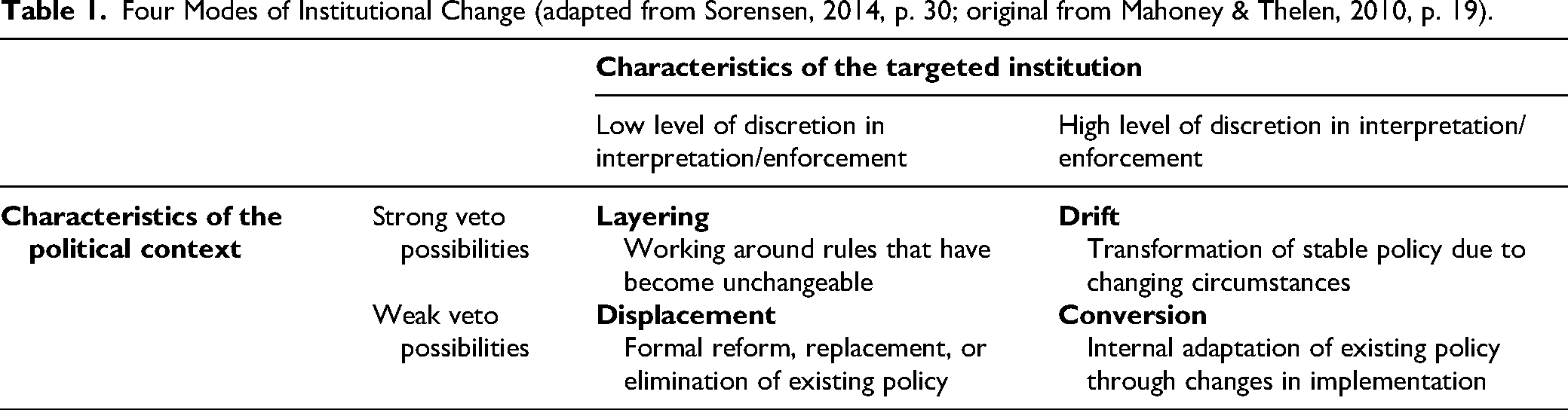

How then can we conceptualize and theorize gradual institutional change? Streeck and Thelen (2005) discern four broad modes of gradual institutional change, of which the attributes have been elaborated by Mahoney and Thelen (2010). They argue that the characteristics of an institution and its political context together drive the type of institutional change one can expect.

As Table 1 shows, it first matters whether the targeted institution provides actors opportunities for exercising discretion in the interpretation or enforcement of the change. If this is not the case, institutional change is most likely to occur through the modes Displacement or Layering. Between these two, it matters whether the political context affords defenders of the status quo strong or weak veto possibilities. Mahoney and Thelen suggest Displacement in case of weak veto possibilities, entailing abolition of a former institutional arrangement and displacement with a new one. In case of strong veto possibilities, on the other hand, reformers learn to work around the elements of an institution that have become unchangeable. Rather than replacing it, new policy is created alongside the old, which often provokes less countermobilization by defenders of the status quo (Streeck and Thelen 2005, p. 23).

Four Modes of Institutional Change (adapted from Sorensen, 2014, p. 30; original from Mahoney & Thelen, 2010, p. 19).

In case of high levels of discretion in the interpretation or enforcement of institutions on the other hand, the modes of Drift and Conversion are most likely. Institutional change through these modes can occur even without formal revision of the rules. Mahoney and Thelen describe Drift as the changed impact of existing rules due to shifts in the environment. With Conversion on the other hand, rules remain formally the same as well, but are interpreted and enacted in new ways (Thelen 2003). Existing institutions in this mode are redirected to new goals, functions, or purposes.

The literature on institutional change also theorizes on the expected associated behavior of actors. For deliberate institutional change, it is first relevant who the main agent is behind the change: who takes the initiative? From a distributional perspective on institutional change, one would expect that “losers” of existing institutions drive institutional change while “winners” try to block it (Kingston and Caballero 2009). This would logically imply that beneficiaries are against the implementation of VC. However, Mahoney and Thelen (2010, 22–23) advocate thinking beyond the dichotomy between winners and losers, because short-term behaviors do not always match long-term strategies, and institutional change does not necessarily emerge from actors with transformational motives.

The concept of “vested interests path dependency” explains why cooperation of the beneficiary can be a major barrier for implementation of VC. Institutions often have significant distributional effects (Lowndes 2009; Mahoney 2010). Because of this, the impact of an institutional change often varies among different actors (Knight 1992). The concept of vested interests path dependency takes into consideration this heterogeneity of actors (Mahoney 2000). It occurs in situations where the costs and benefits of an institutional change are unequally distributed, with actors who prefer change being relatively weak, whereas the actors who favor the status quo are powerful enough to determine political outcomes (Alexander 2001). Because of this, as Mahoney (2000, 521) explains, an institution can persist “even when most individuals or groups prefer to change it, provided that an elite that benefits from the existing arrangement has sufficient strength to promote its reproduction”.

This view of institutions as “contested distributional instruments” with persistent vested interests path dependency is especially relevant when studying the implementation of VC in urban environments. The value of RE depends to a large degree on the prevailing institutions within a jurisdiction (Alterman 2011). The introduction of a VC strategy changes these institutions. It involves a contribution to infrastructure that a beneficiary is not used to, at least not to that extent, which can lead to serious resistance. Support from beneficiaries is therefore vital for the introduction of VC, but also unlikely.

In theory, it is also possible to make beneficiaries such as RE owners contribute without their support. A beneficiary could have weak veto possibilities, leading to institutional change through displacement. However, in practice, ownership of valuable RE often goes hand in hand with significant political access and influence, either through voting or through lobbying power. Introduction of VC without any resistance by disadvantaged actors is therefore not likely.

Finally, deliberate institutional change commonly involves coalition building. Change agents must often work together with other actors to successfully transform institutions. This is also acknowledged by Elinor Ostrom (2005), who argues that to change operational rules, actors must shift into another realm of decision-making, which she calls the collective-choice arena. Within these arenas, change agents must seek alliances with other institutional challengers, who have their own reasons for opposing existing arrangements. As Mahoney and Thelen (2010, 30) explain, “the success of various kinds of agents in effecting change typically depends crucially on the coalitions they are able to deliberately forge or that emerge unexpectedly in the course of distributional struggle.” All actors within such a coalition must be willing to face the risks and costs that accompany institutional change.

Methodology

To investigate the governance process of VC implementation, we conducted qualitative comparative research through three in-depth case studies. We selected three large public transportation infrastructure projects for which at least a significant part of the funding was raised through a VC instrument that had not previously been used by the responsible authorities. To take into account the wide variety of VC strategies and to improve the external validity of our findings, we selected three cases that together cover the three VC variants mentioned above—i.e., land development, contributions from owners of the existing RE, and earmarking future tax revenues. . In addition, we selected cases in which the implementation of VC was apparently deliberate and successful, e.g., selection on the dependent variable, a strategy we chose because little is known about the process leading to this outcome (D. Collier and Mahoney 1996). Finally, we also applied some other, more practical selection criteria: an implementation process recent enough so that (a) key decisions makers could be interviewed, and (b) that the adequate availability of scholarly as well as archival sources on the cases could be expected.

Our criteria led us to the following case selection: (1) Crossrail 1 in London, in the United Kingdom, a significant portion of which is paid for by commercial property owners in several business districts throughout the city; (2) the first two metro lines in Copenhagen, Denmark, which are funded through land development in the new district Ørestad; and (3) the extension of the No. 7 Line in New York City, United States, which is consciously connected to the development zone known as Hudson Yards and is funded in large part by earmarking future tax revenues within this zone.

As Sellers (2005), Pierre (2005) and Denters and Mossberger (2006) argued in this journal, comparative, cross-national urban political research holds great potential to unravel the drivers between change at the urban level. Moreover, the application of the institutional perspective allowed for consideration of the national-level variations.

We investigated the funding strategy through which each of the projects were funded, thereby focusing on the implementation process of VC. In line with the literature on the topic, we define a funding strategy as a series of actions carried out (or deliberately omitted) by the parties involved to secure funding for a project. A funding strategy can therefore include (changes to) several institutions as well as both regular and novel funding instruments that are put together and/or adjusted over a certain period. A funding instrument is a tool or arrangement, usually of a policy, legal and/or financial-economic nature, that allows or enables an organization to fund a project. Where each project may involve the application of multiple new VC instruments, the focus in this article is on the implementation of the instrument that represents the greatest deviation from the “status quo” and is responsible for the largest portion of funding.

We started our data collection through extensive desk research, combining scientific literature as well as grey literature to trace the process of the funding strategy. Next, we conducted a series of face-to-face interviews within each of the cities of our cases. We spoke to 35 people in 29 in-person semi-structured interviews 3 of approximately 1–1.5 hours. Interviews were typically audio-recorded, transcribed in interview reports, and then manually coded. Interviewees involved key actors within the governance processes of our cases from the public, private and civic spheres, as well as experts from science and practice to gain more understanding of the local context. Most interviewees were selected through the desk analysis, supplemented through snowballing.

In the following paragraphs, we first systematically unravel the “thick” narrative of each case (Flyvbjerg 2006) to allow for within-case analysis using holistic case-level data (Ragin and Byrne 2009). We briefly explain for each of the three cases (a) what transportation infrastructure had to be funded, (b) why using traditional funding methods was not an option and what VC strategy was implemented, (c) the corresponding implementation process, (d) the usage of VC in subsequent projects and (e) the characteristics of the institutional change. Next, we assess the similarities and differences between our cases and discuss what these imply for understanding the implementation process of VC and other urban governance innovations.

Implementing Value Capture in London, New York, and Copenhagen

London's Business Rate Supplement

The infrastructure project Crossrail 1 resulted in the Elizabeth line show in Figure 1, a new subway line that runs east-west across London and connects several suburbs, the city center, the two main central business districts (CBDs) and the city's main airport. With a total length of 119 km, it is claimed to provide a 10% increase in London's rail transport capacity (Haylen 2019b). Approximately 28% of the project will be funded by existing commercial property owners.

Route map of Crossrail 1 (Daamen and van Zoest 2021, 17).

VC Strategy

Prior to Crossrail 1, large infrastructure projects in the United Kingdom were typically funded almost entirely by the national government. However, while the state was supportive of the project itself, it did not want to pay its full sum. This was partly due to the enormous investment required, estimated at just under £16 billion in 2007 (Haylen 2019b). Paying such a sum was particularly difficult to justify to politicians from outside London. The Treasury also had bad memories of funding previous major infrastructure projects in London, notably the Jubilee Line Extension, which went way over budget and over schedule (see East and Mitchell 1999).

Simultaneously, the state had been thinking for some time about reducing infrastructure spending and getting local beneficiaries to contribute (Harrison 2006). Previous attempts to make beneficiaries pay have been accompanied by much debate and controversy (Nadin and Cullingworth 2001), but they do fit into a long history of experimentation with betterment instruments (Alterman 2012; Booth 2012). The local and the national government thus agreed that London needed a new public transport line, but it also became clear that traditional funding was not an option, both politically and financially.

The local authorities expected a significant value uplift among beneficiaries, particularly among existing commercial property owners. The new subway line runs through the entire city, connecting the two CBDs with Heathrow International Airport. The project was therefore expected to add value to many of the city's existing commercial properties by significantly improving accessibility and facilitating economic growth.

Beneficiaries fund £4.1 billion of the £14.8 billion investment (2010 estimate) through deployment of the Business Rate Supplement (BRS) (Mayor of London, 2010). The Business Rate itself is a tax on the use of property other than residential. The BRS is a supplement of up to 2% on this existing levy. 4 In 2009, local governments across the United Kingdom were given the power to levy this supplement and use it to invest in “additional projects aimed at promoting the economic development of their local area” (H. M. Treasury, 2010, 3).

The Mayor of London immediately applied the BRS with a term of 24–31 years to the entire Greater London Area. There is however a relatively high threshold below which the supplement need not to be paid, so most of the properties taxed are large properties located in the business centers around Crossrail stations. All of the revenues will be used to fund Crossrail 1 (Buck 2017).

Implementation Process

The introduction of the BRS meant that, for the first time in the United Kingdom, a large group of companies was obliged to contribute directly to a specific infrastructure project. This had financial implications for the beneficiaries and posed a political risk for the local authorities. Our results show that the anticipated impact of Crossrail 1 on economic growth motivated both actors to pursue the implementation of this VC instrument.

Businesses saw Crossrail early on as an essential project to compete with other global cities (Mboumoua 2017; Schabas 2005). Not insignificant to this support was Crossrail's route, which was extended to include Canary Wharf, the second business district, and Heathrow, the main international airport, after plans for a shorter version were denounced by London's business leaders (Lundrigan 2016, 181). Shortly thereafter, a government study found that London businesses were willing to contribute significantly to the project, in the order of £2 billion to perhaps £3 billion in net present value (Montague 2004, 2).

Achieving such sums, however, required more than just voluntary agreements. Most companies were positive about contributing to better public transport. However, another proportion of companies was less enthusiastic. Local authorities in London began organizing workshops with the business community to sample sentiment and gain as much support as possible. Using detailed transportation models, the local authorities were able to demonstrate that the private sector would benefit greatly from the project in terms of accessibility and financial value uplift (Buck 2017).

Simultaneously, it was made clear to the London business community that the project would not be realized without a significant contribution from the local beneficiaries. This changed their options; it was no longer perceived as “project with or without a levy,” but rather as “project with a levy or no project at all.” One of the property owners who expected to benefit most from Crossrail 1 even went so far as to lobby for VC legislation, thereby acting as a change agent. Executives from this company explained in an interview that they did so because such legislation would ensure a contribution not only from them, but also from all their local competitors.

This business support put pressure on the local and national government to enable and implement new VC legislation for the delivery of Crossrail 1. Meanwhile, these government tiers had their own motivations for doing so. At the local level, the mayor had recently gotten direct power and responsibility for both London's economic development and public transport (Salon, Sclar and Barone 2019; Sweeting 2002). Crossrail 1 represented a major opportunity to improve both. Together with the business community, it lobbied for VC legislation at the national level. As one local senior transport official explained: “It wasn’t just a mayor of London and his transport organization saying this was a project that London needed. It was also the mayor of London or a very left-wing mayor of London, Ken Livingstone, and the London Business community, saying that this was a project that London needed, and that the business community would be prepared to pay additional taxes for a proportion of it. And that joint lobbying effort that was highly effective.”

Subsequent Projects

In theory, the BRS can also be used for other projects in the United Kingdom, as this new VC instrument is implemented as part of national legislation. Local authorities are considering the continuation of the BRS in London for Crossrail 2, a proposed north-south line across the London metropolitan area (Haylen 2019a; PWC, 2014).

However, shortly after the BRS was implemented for Crossrail 1, companies were given stronger veto power over the application of the BRS to subsequent projects in the form of a ballot-requirement for all new applications (MHCLG, 2011, 1). This is an obstacle to a BRS for Crossrail 2. Stakeholders in our interviews indicated that business support for Crossrail 2 is significantly lower, due to its lack of connection to business districts. The BRS has not yet been applied elsewhere in the United Kingdom either.

Institutional Change

The implementation of the BRS instrument can best be characterized as a form of displacement, as it was made possible by the creation of new formal rules rather than changes in the interpretation or enforcement of the existing rules, i.e., drift or conversion. Nor can it be characterized as a typical form of layering, which typically does not undermine existing institutions and therefore does not provoke countermobilization by defenders of the status quo (Streeck and Thelen 2005, 23). After all, the BRS had significant financial consequences for the beneficiaries, and it is doubtful if it could have been introduced if all these beneficiaries opposed its application.

The change agents of this institutional change were the local authorities and a selection of London-based companies. For both parties, however, the institutional change was primarily a means to an end: the Crossrail 1 project. The veto power of the business sector, combined with the fact that its support has so far been limited to a single project, means that for the time being the usage of the BRS remains a one-off deviation from the institutions rather than their modification. This may change, however, if a BRS is supported for more projects and thus becomes commonplace.

New York's PILOTs

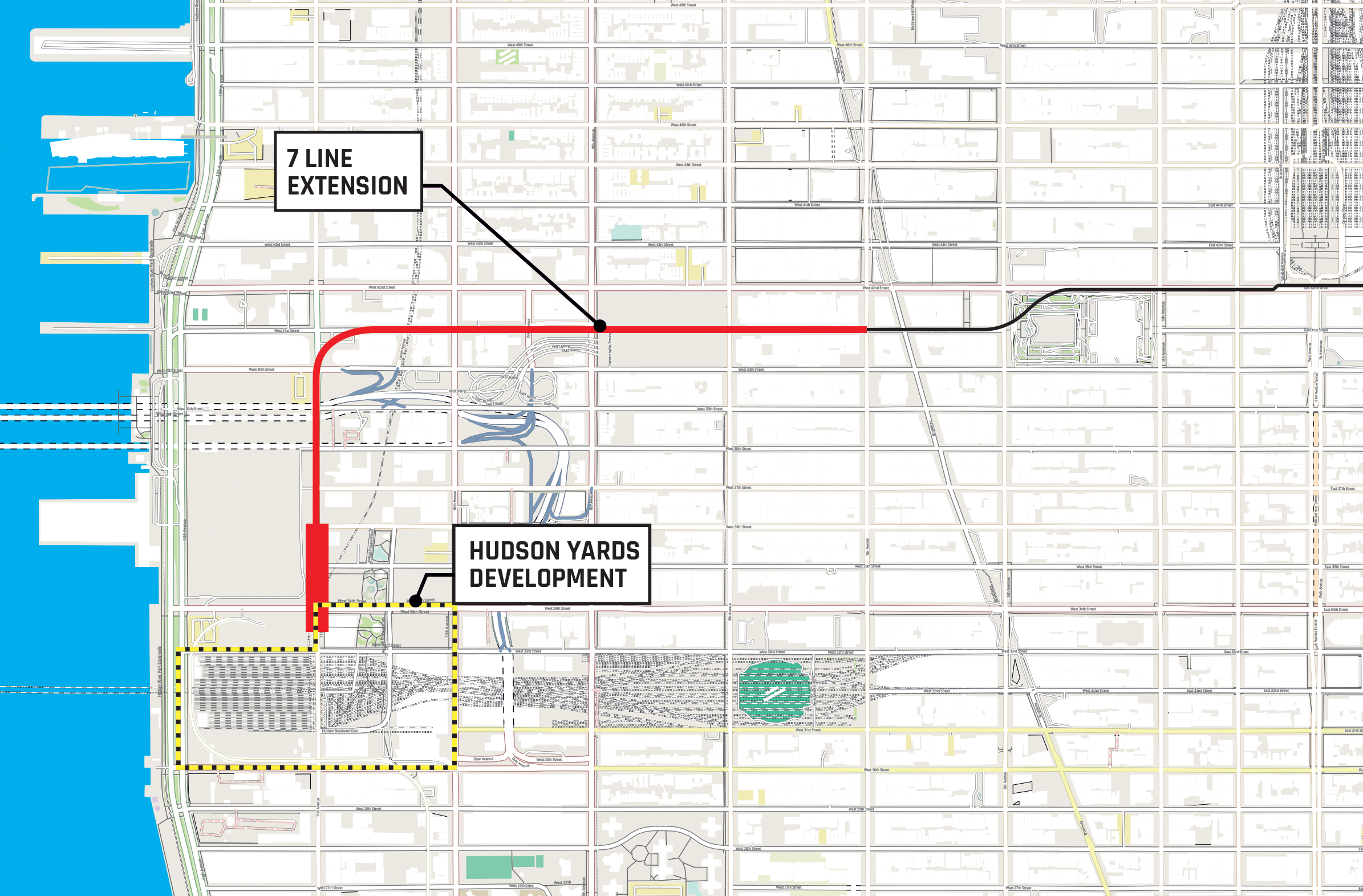

Compared to Crossrail, the New York case involves a smaller transportation infrastructure project; a 2.4 km extension of the No. 7 subway line on the west side of Manhattan shown in Figure 2 (Van der Veen 2009). The entire project is funded by earmarking future property tax income.

No. 7 line extension (bold line) and the Hudson Yards Development area (Daamen and van Zoest 2021, p. 19).

VC Strategy

Such public transportation projects in New York City are typically funded primarily by the Metropolitan Transportation Authority (MTA)—which is owned by the State of New York—and to a lesser extent by the federal government. However, neither the federal government nor the state considered this $2.1 billion (2007 estimate) extension as a priority (NYC Bar Association, 2007). This in contrast to the local government. As a former senior official in the Department of City Planning put it in an interview, “the only way it was going to happen was if the city paid for it”.

The New York City (NYC) administration did not have sufficient funds available to pay for the 7-line extension. However, it expected a significant value uplift due to the RE development program that the project would enable. The primary objective of the subway extension was making the Far West Side accessible by public transportation. This area was one of the last places in Manhattan that was underdeveloped while being adjacent to Midtown, one of New York's major business districts. Although the area was partly being used as an MTA rail yard, NYC envisioned development opportunities through the construction of a platform. The subway extension, along with a zoning change that allowed for very high density, allowed for the development of a new high-rise area of approximately 1.1 million square feet, now called Hudson Yards.

NYC captures part of the value uplift in Hudson Yards by allocating its growing property tax revenues. The city defined a financing district that includes the Hudson Yards district and decided that, for a period of 20 up to possibly 64 years, all property taxes in that area will not go to the city's general budget, but will be used specifically to fund the subway extension and some related public works (Van der Veen 2009). This novel funding instrument is similar to TIF, but was adapted to maximize revenues and fit within existing New York legislation (Cerciello 2005; McSpiritt 2015).

Implementation Process

Whereas in London the local authorities had to secure the support of a large and diverse group of companies, the local authorities themselves were the beneficiaries of the funding strategy in the New York case. Nevertheless, by allocating its own property taxes, NYC deviated significantly from the custom that the State of New York provides most of the funding for major infrastructure projects. Our results show that, as in the other two cases, the pursuit of one specific urban development project was the main driver behind this decision.

In 2001, NYC released an influential report arguing that the government should support the construction of office buildings to maintain the economic growth and status of the city in general, and Manhattan in particular (Deutsch 2001). This endeavor aligned with then-mayor Bloomberg's strategy of attracting global investment power (Brash 2012). In consultation with a coalition of parties, Bloomberg designated a large number of waterfront areas for urban development in 2007 (see New York City, 2007). The development of the Far West Side was a very important one, because it was intended to provide a major boost to Manhattan's office stock—and to accommodate the job growth that was projected to come with it. Although alternatives had been discussed in previous years, the Bloomberg coalition saw subway access to the site as a critical condition for its development.

The MTA owned the rail yards and the land beneath them and was willing to allow development on top of it, but only for the right price. While financial contributions from developers to the city are common, NYC could not ask for too much because the developer had to build an expensive platform on the rail yards. Meanwhile, its high degree of local tax freedom allowed NYC to earmark its future property taxes to the development. The city felt it had no choice but to use the expected value uplift in the Hudson Yards area to realize the subway extension.

Subsequent Projects

While the State-owned MTA is eager to apply VC strategies like the one in Hudson Yards more often, NYC is more hesitant. In 2018, the governor of New York released a proposal that would give the MTA the freedom to apply VC by allocating the city's property taxes when and where it chooses (Rubinstein 2018). However, as a former senior NYC official explained in an interview, “the city has strongly objected to this, on the grounds that it will agree, which I support, that the city will, might enter into VC agreements on a case-by-case basis, but would never support legislation that would give the state the ability, or the MTA on its own, to simply invoke VC, to divert city RE taxes.”

Institutional Change

For the extension of the No. 7 subway line, the traditional funding method (i.e., state subsidy) was displaced by a local VC-based funding instrument. The change agent in this case was clearly the New York City administration. However, as in London, it did not take on the role of the change agent because it wanted the institutional change itself, but rather because it saw VC as a means to an end. New York State, by contrast, became a supporter for the institutional change itself. However, due to NYC's veto power, for now it remains a one-time deviation from existing institutions.

Land Transfer in Copenhagen

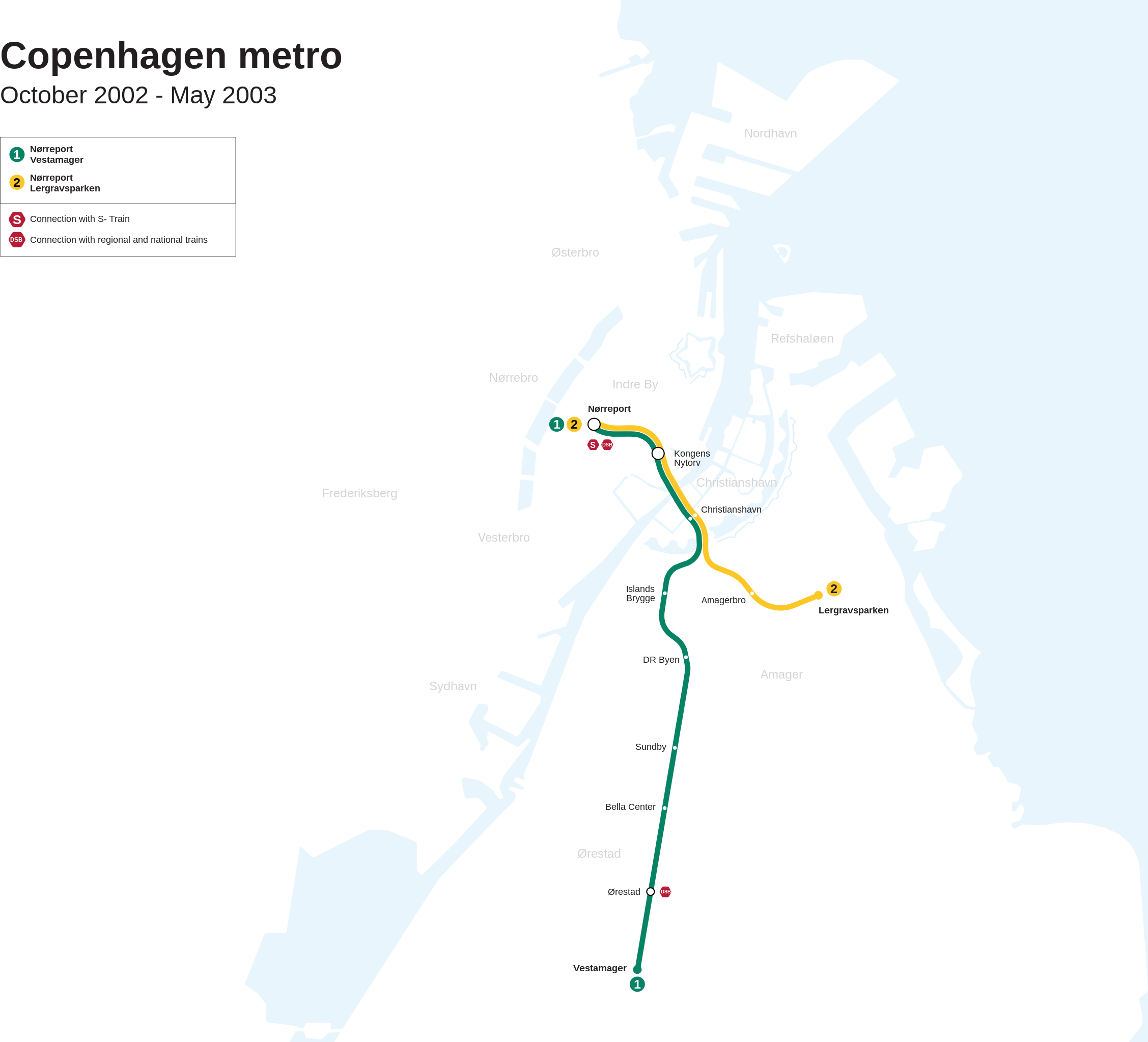

Construction of Copenhagen's first two metro lines began in 1996. As shown on Figure 3, they run from the west side of the city, through the city center, to the airport and a new district called Ørestad. Together, the metro lines are 20.4 km long and represent an investment of 1.64 billion euros (2005 estimate 5 ). Both metro lines have been funded through land development.

First two metro lines of Copenhagen. Source. Created by Tomtom24, distributed under a CC BY-SA 4.0 license.

VC Strategy

Prior to the development of this project, virtually all major infrastructure projects were funded and financed by the national government (Jørgensen, Kjaersdam and Nielsen 1997). Investing in the Copenhagen region however was politically very sensitive at the time. Financially, Denmark has a strong redistributive culture. Administrators from other regions always wanted to see the investments in Copenhagen reflected in their own regions, and there was not enough money to do so. In addition, both the Danish government and the municipality of Copenhagen were in a very poor financial position (Majoor and Jørgensen 2006). There was only one conclusion to be drawn: an alternative way of funding public transport construction had to be found (Jørgensen, Kjaersdam and Nielsen 1997).

An area of about 310 hectares west of the city center of Copenhagen provided a solution to this funding problem. The site was jointly owned by the state and the municipality and was no longer in use. The two government tiers saw an opportunity for a large-scale area development, which would generate sufficient revenue to fund the two metro lines.

To stimulate and capitalize on this value development, the state and the municipality jointly established a new public development company, which, after some changes, was named By & Havn (Katz and Noring 2017). Both governments transferred their land to By & Havn at no cost, after which the municipality changed the zoning to allow RE development on the land. Using government loans, By & Havn first began building the two subway lines and then prepared the land for construction. As a result of the construction of the public transport system, the change in the zoning plan and the development of the land, the value of the land has risen sharply. Finally, By & Havn repays its government loans with the proceeds from the land issue.

Implementation Process

Although it was not necessary to gain the support of a broad group of beneficiaries, this new strategy still implied a major departure from the existing funding arrangements. The two government tiers, which were not on good terms at the time, had to work closely together, transfer their land free of charge to provide sufficient potential for value development, and adopt a more entrepreneurial and risky strategy than before to realize and capture the value uplift. What made them do this?

In the 1980s, the city of Copenhagen was in very bad shape. The municipality was nearly bankrupt and the quality of life in the city was rapidly deteriorating. Like many other Western (capital) cities at the time, much of the industry and population had moved out of the city, leaving the economy in a state of collapse. The predominantly social democratic municipality wanted to respond by investing in the city but lacked the resources to do so. The relationship between the municipality and the national government during this period was dramatic. The state provided Copenhagen with limited support during its decline, which the municipality strongly resented (J. Andersen 2002).

During the same period, a liberal-conservative Danish government adopted a new economic growth strategy that, unlike countries with more liberal policies, had a very elaborate social paragraph. In this strategy, Copenhagen was to become the “growth locomotive” for all of Denmark (H. T. Andersen and Jørgensen 1995). This was in line with the tendency of European cities to develop urban competitiveness (Van den Berg and Braun 1999).

Within Denmark, Copenhagen was the only city with the potential to compete internationally. To do so, however, it was essential to improve the local infrastructure (H. T. Andersen and Jørgensen 1995). Thus, the municipality and the state had a common interest in making investments that would revitalize Copenhagen. However, the poor economic situation of the municipality and the national culture of financial redistribution prevented the two governments from providing public funding.

East of the city center, there was an empty military training area of about 310 hectares, jointly owned by the municipality and the state. As the spatial expansion of the region had taken place towards the west until the 1980s, this area had long received little attention. However, a newly built bridge to Malmö gave the peninsula a much more central position in the region (Majoor and Jørgensen 2006).

By deploying and developing their land, the municipality and the state saw an opportunity to develop the metro lines “without taxpayer's money,” as a former director of By & Havn explained. This gave them a strategy to accomplish their mutual goal of economic development in Copenhagen without political controversy. Because the land was perceived as having no value without the infrastructure, as was reconfirmed in several of our interviews, its free transfer to the development organization did not meet much resistance.

Subsequent Projects

Satisfied with the funding model, the municipality and the state employed By & Havn to fund multiple subsequent infrastructure projects. Each new project, however, demanded a new deal between the two government tiers, based on the project characteristics and the resources available to both parties at each point in time.

The first follow-up project was an inner-city metro ring that was developed to serve the main inner-city neighborhoods (Knowles 2012; Majoor 2015). The state transferred several port sites near downtown to By & Havn free of charge, with the proceeds making up their portion of the funding. The remaining part came from operating revenues and the sale of power plants that were partly municipal, a politically acceptable strategy at the time.

By & Havn has given the city ring two branch lines to two area developments, each with their own funding arrangement. The branch line to the newly developed Nordhavn neighborhood was partly funded through the value uplift resulting from the area development. Because the area was developed before the subway line was built, By & Havn included a special clause in its land transfer contracts: property owners were to pay a sq. m. surcharge the moment a subway station opens near their buildings (Noring 2019). By contrast, securing funding for the branch line to Sydhavn proved much more difficult, especially for the state. Denmark eventually decided to sell 40% of its shares in By & Havn to Copenhagen in order to cover its share of the funding.

Institutional Change

In contrast to the other two cases, land transfers to a separate legal entity have already been used repeatedly in Copenhagen, suggesting that this new VC strategy has displaced public funding as the dominant method of funding new subway lines in the capital. In all instances, state and municipality were both the beneficiaries and the change agents.

This does not mean, however, that the barrier of path dependency imposed by the critical support of the beneficiary has been definitively resolved in Copenhagen. With each project, the two tiers of government have reassessed what land or other resources they can provide and whether they are willing to do so. This barrier therefore persists on a project-by-project basis, and its resolution continues to depend on the available resources of the beneficiaries and the voluntary willingness to use these resources for funding purposes.

Discussion

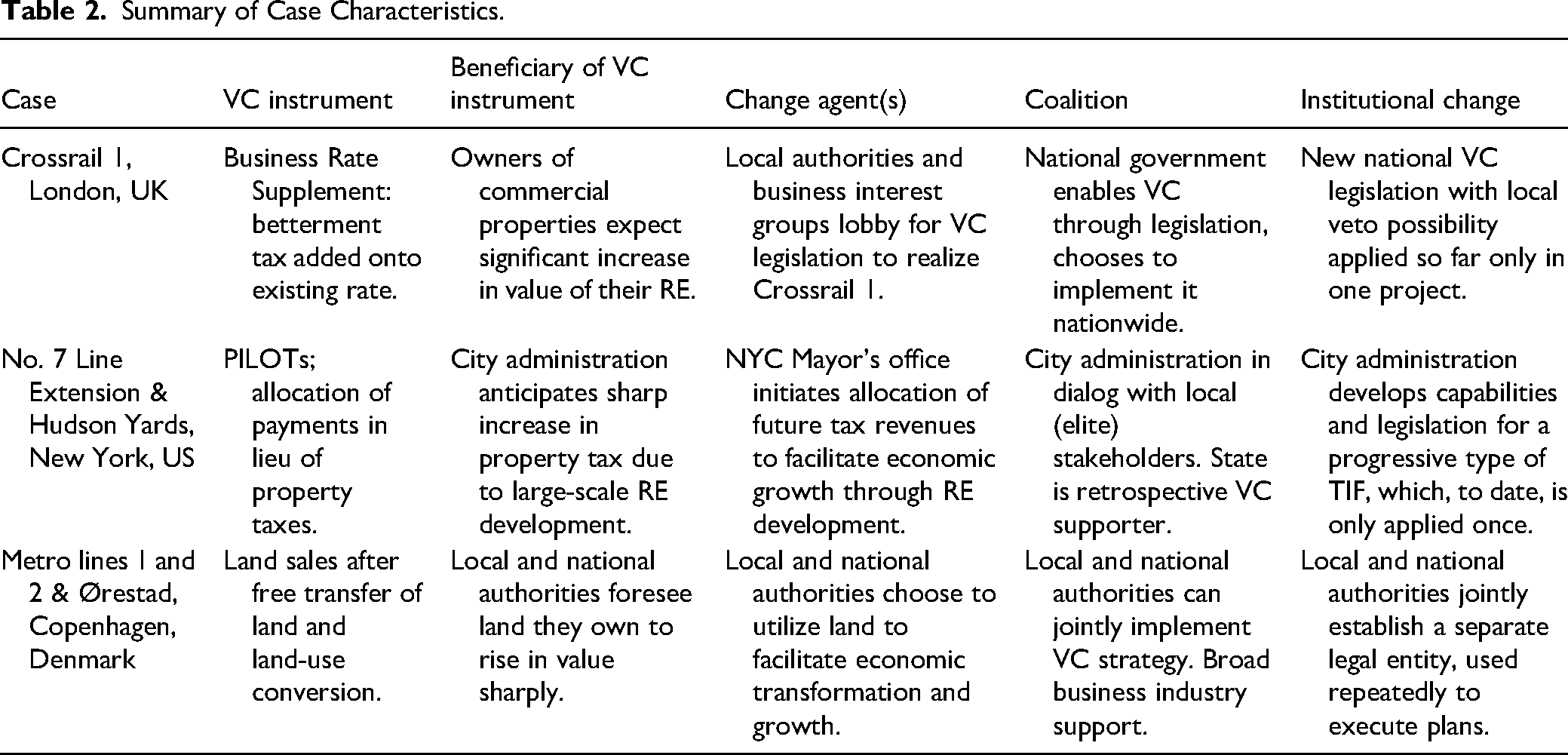

Based on the theoretical insights discussed, we assumed that the implementation process around novel VC instruments to fund public infrastructure projects resembles a process of institutional change. A process, moreover, that the beneficiaries of the public infrastructures would resist. However, the empirical evidence summarized in Table 2, shows a somewhat different picture. In all three cases studied, beneficiary groups were involved in initiating the implementation of the new VC instrument, either alone or in cooperation with other groups. In two of the three cases, however, the implementation process of the VC instrument can only be associated with institutional change to a limited extent. A closer examination, in which we adopt a power-based political bargaining perspective on institutional change and consider the distributional effects and other motives of individual actors, helps to explain this apparent discrepancy.

Summary of Case Characteristics.

Although the cases cover a wide range of project characteristics, local circumstances, and VC instruments, there are noteworthy similarities in the process by which VC was implemented. A key trigger in all three cases was the inability of higher levels of government to fund a specific strategic infrastructure project for the city in question, making traditional funding methods inadequate. Simultaneously, it was clear to the authorities that the projects in question could be expected to generate significant economic value uplifts in the surrounding area, making VC theoretically possible.

Comparing our empirical findings with the modes of institutional change outlined in Table 1, we can see that the implementation of VC in our cases would not have been possible by exploiting ambiguities in the rules, which would have counted as drift or conversion. Neither do our cases show that VC could have been implemented by making minor changes to the rules that powerful veto players could not block, as is the case with layering. Rather, all three cases show that displacement was necessary.

As we have discussed, this type of institutional change often occurs through the rediscovery or activation of a “foreign” or previously deviant practice (Streeck and Thelen 2005, 20; see also Castaldi and Dosi 2006). This is consistent with our findings. Implementing a betterment tax has been attempted before in the United Kingdom, but was deemed unworkable at the time (Alterman 2012; Booth 2012). Meanwhile, the strategies in Copenhagen and New York are based on examples from elsewhere: the Copenhagen model is based on the New Town Development funding schemes in the United Kingdom, while the New York City strategy is inspired by TIF legislation common in many other US states. The authorities involved have adapted these foreign or deviant practices to be pragmatic and sensitive to local circumstances, which is increasingly seen as a success factor for VC in practice (Crook 2016).

Following our power-distributional approach to institutions, we can conceptualize the implementation of a new VC instrument as the outcome of a power-based bargaining process, involving different actors participate with varying motives and power to influence the outcome. Based on the premise that “winners” of the existing system defend the status quo while “losers” drive institutional change, it can be expected that beneficiaries will resist the implementation of VC because of its negative distributional effects for them. Owners of commercial property in London, for example, were accustomed to receiving the full value uplift of their properties resulting from infrastructure development. Nevertheless, a group of London-based businesses lobbied for Crossrail 1 and were willing to sacrifice some of their value uplift to help fund the project. The beneficiaries in New York and Copenhagen even chose to dedicate all of their value uplift to fund the infrastructure projects at hand, an arrangement the cities had never seen before.

All three cases clearly show that it was not institutional change—i.e., a structural change in the way public infrastructure is generally funded—that the beneficiaries were after. Rather, the beneficiary groups perceived the change in existing funding rules primarily as a necessary means to realize the strategic urban development project they wanted. This finding fits well with the Mahoney and Thelen's (2010, pp. 22–23) notion that institutional change is not necessarily driven by actors with transformative motives: it can also be the unintended by-product of distributional struggles.

The change agents in our cases, including the beneficiaries, worked with other actors to enable the implementation of the VC instrument. The actors involved had diverging reasons for cooperation, which is particularly evident in the role of higher levels of government. While for the beneficiaries VC was primarily a means to enable a specific urban development project, for the higher levels of government it is also a way to structurally free up funds for other expenditures. It is therefore understandable that the State of New York is advocating the use of TIF for a range of projects, while the UK government has made the BRS applicable nationwide. Meanwhile, in Denmark, the national government has already shown support for the repeated use of public land transfers.

While these higher levels of government could suspend traditional funding, they did not have the power to replace it with an institutionalized VC instrument themselves. In all three cases, the beneficiaries retained veto power over the use of the new VC instrument for each new infrastructure project. As a result, New York City has not yet responded to the State's desire to use TIF more broadly, nor has the British Betterment Tax been used a second time. Only the two government tiers in Denmark have repeatedly used their VC instrument, albeit on the basis of specific land transfer negotiations for each new project.

Considering the above, should we understand the implementation of VC as a process of institutional change? Or can we better explain this phenomenon as the output of an instrumental regime or urban growth coalition, in which collective action revolves around the realization of one specific urban development project? 6 We argue for an institutional perspective on the basis of three arguments. First, broadly applicable funding methods are vital to respond to the increased demand for sustainable urban infrastructure. For VC to become a serious alternative to public funding, it is essential that it becomes applicable beyond a single project. This requires institutional change. Second, institutional theory, with concepts such as vested-interest path dependency, helps to explain why this is so difficult. Finally, the Copenhagen case shows that an initial application of VC in one project may well serve as a precedent for subsequent projects, thereby potentially leading to a gradual process of institutional change. This is in line with Thelen's (2009, 475) argument that “significant change often takes place through a cumulation of seemingly small adjustments […] in the absence of some obvious historic rupture”.

Our findings suggest that beneficiary support is a key condition for the application of VC to fund infrastructure. Based on the above, we hypothesize that if a group of beneficiaries repeatedly agrees to the use of a VC instrument, it is possible that, over time, it becomes a shared norm to allocate a portion of the value uplift to fund the infrastructure that caused the uplift. In this way, a form of VC may eventually displace traditional funding methods or persist as an important complement to them.

Conclusion

In both research and practice, value capture (VC) is widely cited as a method for local authorities to continue to provide urban public goods to their cities in the face of fiscal stress. At the same time, the application of VC in practice remains limited, raising questions about how to understand the implementation process of VC. In this article, we therefore aimed to explain the implementation process of VC as a strategy for funding public transportation infrastructure.

Adopting a power-based political bargaining perspective on institutional change, we argued that the implementation of VC is not only an instrumental choice but also depends on the modification of contested distributional institutions. We found the role of the beneficiaries of the public investment to be particularly important, because the implementation of VC involves a payment that these actors may seek to oppose. Although in theory it should be possible for authorities to implement VC without the support of beneficiaries, all our cases show that the beneficiaries had access to veto power. Based on our findings, we expect beneficiary support to be a key prerequisite for the implementation of new VC strategies in all countries with a well-functioning legal system with enforced property rights.

The need for beneficiary support can pose a serious barrier to the implementation of VC, but our findings show that a strategic urban development project can act as a driver to overcome this impediment. If a beneficiary group of a project really wants the project to be delivered, and it is perfectly clear that it will not be realized without the implementation of VC, that group can decide to contribute some or even all of its value uplift. Our findings show that the beneficiary group can even act as a change agent for the implementation of VC.

However, if the support for the implementation of VC is based solely on a single project, this can negatively affect the institutionalization potential of the new instrument. The beneficiaries in our cases were not after a process of institutional change that would structurally displace traditional public funding with a new strategy. What mattered to them was the delivery of the project they wanted, and they were willing to waive their veto power for just that. Consequently, in London and New York, the novel VC instrument implemented has so far only been used once. At the same time, however, the Copenhagen case shows that the first use of a novel VC instrument can serve as a precedent for subsequent projects, making the allocation of value uplifts for funding purposes slowly but surely commonplace.

As with other urban governance innovations, VC can be easily politicized or misunderstood in practice, leading to an underestimation of its potential (Dunning and Keskin 2019). Our institutional perspective reveals that the multilayered nature of its implementation process—involving complex legal instruments as much as local behavioral changes—can make such governance innovations difficult to fathom (see also Canelas and Noring 2022). However, by providing benefits that actors with diverse interests can rally around, an urban development project is clearly capable of acting as a tangible driver of change.

To deepen our understanding of the implementation process of urban governance innovations like VC, it is therefore relevant to further investigate whether the application of VC to one urban development project can indeed catalyze a process of gradual institutional change, for example through longitudinal analysis of multiple cases.

Finally, in the research presented in this article, we chose to take specific projects as an empirical starting point. This approach has proven useful for developing our institutional perspective on VC implementation, but this also has its drawbacks. For one, VC can also be initiated outside the spatial scope or institutional arenas associated with specific urban projects. And second, selecting cases on the dependent variable—here: successful VC implementation—has a limiting effect on establishing causal relationships (Denters and Mossberger 2006; King, Keohane and Verba 1994).

Research on unsuccessful VC implementation processes, or on those that emerged more independently of specific urban projects, can therefore be recommended. Nevertheless, we hope that the institutional change perspective adopted in this article informs other scholars that seek to further our understanding of what it takes to adapt our cities to new challenges, and that our cases inspire those interested in making it happen.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Foundation for Area Development Knowledge (Stichting Kennis Gebiedsontwikkeling) and the Ministry of Infrastructure and Water Management.