Abstract

Local governments view land banks as an improvement to the municipal management of foreclosed property. Critics contend that land banks wield too much power, concentrate demolitions in poor and majority neighborhoods of color, and have unfortunate parallels to the flawed, top-down policies of mid-twentieth century urban renewal. Examining land banks through a lens of social equity and reparative planning, this research asks “To what extent do land banks in New York state work toward equitable urban development?” Interviews with land-bank leaders, property acquisition and disposition data, and spatial analysis of neighborhood dynamics were triangulated in a comparative case study of three land banks in New York state communities. Although land-bank leaders show an awareness and desire to address issues of equity, the authors observed that more community engagement, expanding partnerships with nonprofits, and shifts in approaches to demolition could provide more equitable outcomes in disinvested communities. Some land banks had clearly adopted policies aimed to acknowledge and address the role land banks can and should play in addressing historical inequities. Whether that commitment to equity will remain strong into the future remains an open question. In a COVID-19 context, land banks were operating with significantly reduced inventories and resources. More resources could be provided to land banks from Federal and State sources to support equity initiatives. But those resources should be provided under the condition that land banks become vehicles for repairing past White supremacist and structurally racist policies that created the uneven landscapes that land banks were created to address.

Introduction

The management of vacant and abandoned property poses significant challenges for regions that are losing population. Often associated with rising crime and illicit activities, vacant and abandoned properties have been shown to depress property values, drive down property taxes, and can be major targets for arsonists (Heins and Abdelazim 2014). Within the US, land banks have become a popular model to transform derelict sites into productive properties in cities facing population decline. Land banks acquire, manage, and dispose of abandoned, vacant, foreclosed and tax-delinquent properties. Acting as a nonprofit intermediary between a municipality and property owners, land banks provide municipalities an opportunity to generate tax revenue through redevelopment, while taking the burden of managing vacant, abandoned, and tax-delinquent properties off the municipality itself.

Land banks are often touted as solutions for managing vacant and abandoned property, removing blight, increasing property values, and growing the local tax base (Alexander 2015; Heins and Abdelazim 2014; Mallach 2015; New York Land Banking Association 2017). Historically, local municipalities were responsible for managing vacant and abandoned properties. Municipalities enforced foreclosures, collected from tax-delinquent owners, sold properties at auctions, and often accumulated a large backlog of tax-delinquent and foreclosed properties (Alexander 2015; Heins and Abdelazim 2014; Fletcher 2017; Wright 2017). Local governments have viewed land banks as an improvement to the municipal management of foreclosed property in cities losing population and a tool to provide community programs that support social equity. However, land banks have been criticized for wielding too much power, concentrating demolitions in poor and majority Black, Indigenous, and People of Color (BIPOC) neighborhoods, and paralleling the flawed top-down policies of mid-century urban renewal.

Following the 2008 financial crisis, a multitude of land banks emerged throughout the US in response to growing inventories of vacant and abandoned properties and new land bank enabling legislation.

1

Financed largely from the Obama administration's Neighborhood Stabilization Program funding, and supported by the land-banking nonprofit Center for Community Progress, over 250 land banks now play a significant role in urban development policy in cities in the United States (Center for Community Progress 2022a). The increased influence has come with significant legal powers. These include:

The ability to select among prospective buyers based on other factors rather than just price.

The ability to use reverter clauses, which grant the ability to seize property from purchasers who have not completed agreed-upon renovation work in an agreed-upon time.

Super bid authority—the ability to intervene ahead of other buyers.

Acquisition of foreclosed properties at lower or no cost from a government foreclosure unit.

The ability to hold properties tax-free, and indefinitely if needed.

The ability to use property that is not distressed if it benefits a development for a parcel (Center for Community Progress 2017, n.p.).

Land bank proponents argue that these significant powers land banks wield are tamed by the political ramifications of abusing them, and by legal requirements for transparency, and public notification (Alexander 2015). Furthermore, some land banks emphasize their role in promoting social equity and providing community programming.

Despite significant influence in urban development policy, relatively little scholarship critically examines the impact of land banks on the communities they serve. Additionally, there is a need to examine social equity initiatives among land banks in the post-COVID-19 era, where many communities are facing widening inequality and housing shortages. Land banks wield significant powers, assembling land and disposing of property. Without an equity lens, land banks risk exacerbating inequality by demolishing swathes of racialized neighborhoods, repeating or reinforcing patterns of segregation and disinvestment, and gentrifying some areas while neglecting others. Alternatively, they may serve as an important tool in helping to redress the structural racism that has shaped many US cities.

This article provides a critical analysis and comparative case study of three land banks, evaluating how land banks approach development through the lens of social equity. It asks the question: “To what extent do land banks in New York state work toward equitable urban development?” Equitable urban development is defined in relation to the literature of equity planning (Krumholz and Forester 1990; Zapata and Bates 2015), the Just City (Fainstein 2010), and informed by the concept of reparative planning (Goetz, Williams and Damiano 2020; Williams 2020).

Only in 2011, did New York State give land banks legal authority to acquire tax-delinquent, vacant, and abandoned properties from cities that have acquired property using the power of eminent domain (Hancock and Acquario 2011). Since that time, the number of land banks has grown within New York State and nationally. This suggests a growing need to critically examine what role land banks can or should play in redressing historical and contemporary racial and economic segregation.

Drawing on interviews with leaders of land banks in New York state, this research explores the different ways land banks approach urban development and the distributional effects of these approaches. We incorporate recent information about the challenges land banks have faced during the COVID-19 pandemic. Although land bank leaders show an awareness and desire to address issues of equity, the authors observed that more community engagement; expanding partnerships with nonprofits, especially community land trusts; and shifts in approaches to demolition could provide more equitable outcomes in disinvested communities. Some land banks have clearly adopted policies aimed to acknowledge and address the role land banks can and should play in addressing historical inequities. Furthermore, the case study land banks have mostly shifted away from demolition in recent years. Whether that commitment to equity and the turn away from demolition will remain in the future remain open questions. In a COVID-19 context, land banks were operating with significantly reduced inventories and resources. We argue that the resources could be provided to land banks from Federal and State sources to support equity initiatives. But that resources should be provided under the condition that land banks become vehicles for repairing past White supremacist policies that produced the uneven landscapes that land banks were created to address.

Literature on Land Banks

Land banks commonly reference economic development and social equity goals. Publications from land-banking nonprofits and state land-banking associations celebrate the success of land banks in improving the management of vacant and abandoned property, removing blight, increasing property values, and growing the local tax base (Alexander 2015; Heins and Abdelazim 2014; Mallach 2015; Center for Community Progress 2017). Alexander (2015) discusses the role of community coalitions in establishing land banks and the duty of land banks to adapt to respond to local community needs. In addition to the core role in stabilizing vacant buildings and demolishing the blighted property, many land banks feature programs that seek to renovate homes, provide affordable housing, support community gardens and arts programs, and encourage first-time homeownership (Fletcher 2017; Wright 2017; Bertron and Hamilton 2016).

Hackworth (2014) explores land banks in the context of market-based strategies to address land abandonment in shrinking cities, classifying three types of land development policies as reflections of differing ideological approaches. He describes “managerial” approaches “designed to regulate private development by placing conditions on it,” “market-first” approaches intended to entice owner-occupants or outside investors to invest in blighted property, and “market only” approaches that limit the government's role in managing vacant and abandoned property (p. 12). Acknowledging the success of land banks that embrace managerial and market-first orientations, he argues that municipal intervention in the market through land banks will encourage more responsible property owners, reduce speculation by private investors, and decrease disinvestment.

Despite these benefits, there are also critiques of land banks as being too powerful, privileging private capital over community needs, and perpetuating the mistakes of top-down community renewal policy in communities of color (Hackworth 2016; Benediktsson 2014; Kirkpatrick 2015; Taylor 2017). Specifically, Hackworth (2016) attacks demolition—a policy land banks often engage in—as the continuation of unjust planning policies in marginalized communities. Citing the lack of economic development in distressed neighborhoods that have been subject to widespread demolitions, scholars have critiqued the assumption that blight removal—absent other community and economic development interventions—will positively benefit communities (Hackworth 2016). Benediktsson (2014) argues that a sense of community disorder is socially constructed and based on residents’ “disorderly collectivities that frame modes of civic response in terms of collective identity and culpability” rather than the physical presence of blight (p. 191). Others suggest that demolition has the potential to speed up rather than slow disinvestment. By attempting to triage “problem” homes or neighborhoods, planners signal that an area may be “beyond hope”—beginning a self-fulfilling prophecy that can accelerate cycles of disinvestment (Kirkpatrick and Owen 2015; Metzger 2000).

Current land abandonment policy may be replicating the flaws of mid-century urban renewal in a way that does not improve quality of life for low-income or racialized communities (Taylor 2017; Hackworth 2016). Theorists find parallels between the policy flaws of contemporary rightsizing policy brought on by disinvestment in shrinking cities to the recognized stigmatization of “blighted” communities of color during 1960s urban renewal. Rosenman, Walker and Elvin (2014) discuss parallels between the top-down policies of 1960s urban renewal and powerful quasi-governmental structure and land appropriation strategies of contemporary land banks. They suggest that land banks may be privileging efficient and flexible management at the expense of democratic planning and community oversight. Notably, community leaders in Michigan have criticized the Detroit Land Bank Authority for its lack of transparency and for concentrating renovations only in specific neighborhoods. The federal government investigated the land bank's awarding and payment of demolition contracts and the rising costs of demolition in Detroit (Goldstein 2017, November 4; Stafford 2018).

Theorists have also criticized programs focused on blight removal as a top-down policy that does not acknowledge the value of existing community spaces (Metzger 2000; Kirkpatrick 2015; Hackworth 2016; Taylor 2017). In this view, by stigmatizing blight in low-income communities of color, policy may reinforce existing geography of segregation. To the White community at large, blighted Black neighborhoods become stigmatized spaces associated with danger and crime (Sampson and Raudenbush 2005).

Prior Studies of Equitable Urban Development

In prior studies, success in achieving equitable urban development has been attributed to the strength of networks of economic justice and community development nonprofits (DeFillipis 2008; Briggs 2008). Strong relationships between community advocates, governments, and professionalized community development organizations have led to successful lobbying for community control in disinvested housing markets and influenced development policy in low-income communities of color. Notably, community land trusts offer an alternative inclusive development approach to the quasi-governmental land bank model (Davidson 2012; Fujii 2016a). Community Land Trusts (land trusts) are nonprofit organizations which own and manage property with the goal of preserving housing affordability and empowering communities to manage their own development (Greenstein and Sungu-Eryilmaz 2007). Unlike land banks, land trusts retain ownership and stewardship of parcels indefinitely, using ownership of property and an underlying land lease to homeowners to retain affordability and restrict redevelopment (Fujii 2016b). Land trusts typically work in gentrifying and economically prosperous neighborhoods, but some have developed in communities in decline. In addition to their housing goals, successful land trusts such as the Dudley Street Neighborhood in Boston support other community programs related to food justice, education, and youth leadership (Dudley Neighbors Inc 2017). Embracing what Kretzmann and McKnight (1996) define as an assets-based approach to community development, land trusts focus on utilizing a community's existing resources, skills, and capacities to increase a sense of ownership and community capacity, as opposed to focusing on “deficiencies and problems” (Kretzmann and McKnight 1993, 1) of an area.

Further Advancement of Equitable Urban Development: From Social Equity to Reparative Planning

Land banks are commonly described as a vehicle for putting vacant and abandoned properties back into “productive use” and using partnerships to achieve goals toward social equity. Land banks use the term “productive use” in a variety of ways, from turning vacant lots into larger lots for nearby properties, to the creation of community gardens that are collectively managed, to the sale of properties to developers for new affordable or market-rate development, to the sale of houses to tenants for first-time home-ownership. Depending on the type of use, who benefits, and where the development is located this helps a community reach social equity goals. However, other than a few sources (see e.g., Center for Community Progress 2022b) and the aforementioned literature, there has been little systematic study of land banks and equitable urban development. Furthermore, equity initiatives are a growing phenomenon among many organizations and can be defined in a variety of ways. To understand how or to what extent land banks can contribute to social equity and equitable urban development, it is necessary to define both terms in relation to the operation of land banks.

Equity planning is a common framework in urban planning, in which the work of governmental agencies should provide for those who have the least (Krumholz and Forester 1990). The ideas of equity planning were reconsidered in a special issue of the Journal of Planning Education and Research edited by Zapata and Bates (2015). Critiques of equity planning in this issue include revisiting the idea of planning on behalf of communities who have the least and instead planning with them. Land banks that use an equity planning framework would then prioritize the needs of those who have the least. They would work directly with marginalized communities to help them achieve their own goals.

Fainstein’s (2010) conceptualization of the “just city” seeks to move beyond definitions of justice that focus on inclusion, partnership, and collaboration to the measurement of social justice and equity in terms of the outcomes that are achieved through urban policies. Thus, the measure of a land bank would be an increase in social justice through the outcomes of their actions. Thus the effect of a land bank's decision must have material outcomes that positively benefit those members of the community who need it the most.

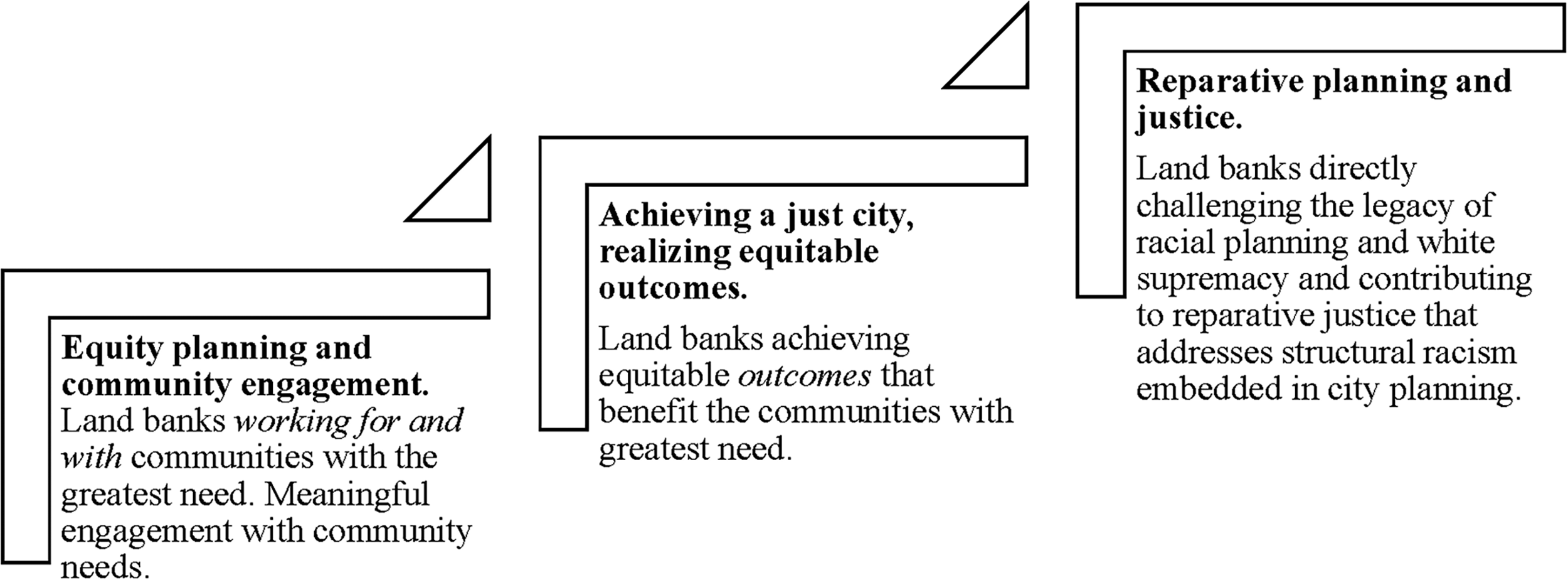

Young's (2011) conceptions of social equity, considers the historical context of racialized urban inequity and advocates for a planners’ responsibility to address historical injustices (Brand 2015). Further elaborating, Williams (2020) and Goetz, Williams and Damiano (2020) call for reparative planning that seeks justice by directly addressing the effects of structural racism and White supremacy. Williams writes (2020, 8): “Reparations in the planning context not only requires fundamental changes in the distribution of public goods and services and a confrontation with white ignorance but a fundamental rethinking of the role of African American communities in setting planning goals and enacting planning policies.” To realize equitable development through this framework, the work of land banks must not only work with or within communities that have the least and benefit them tangibly, but they must also work toward rectifying past harms within neighborhoods that have been negatively impacted through urban policies. Further, reparative planning “challenges not only racial inequality, but the whiteness on which it is predicated” (Williams 2020, p. 9). Thus, land banks would work toward a model of reparative justice where they work with communities and are perhaps directly governed by people affected—to repair the uneven landscapes produced through the inequitable development that necessitated the creation of land banks in the first place. They would further find means of challenging the racial assumptions that remain in the wake of racial planning. Figure 1 provides a conceptual framework for understanding the differences between these visions for land banks in contributing to progress toward realizing socially equitable practices, with reparative planning as the most difficult to reach.

Conceptual framework with three models for socially equitable practices among land banks.

This research extends from both critiques of land abandonment policy and its legacy of disparate impacts by race and class, and scholarship that acknowledges the potential for land banks and organizations they partner with to embrace reparative community development approaches. This research sought to examine the perspectives of land bank practitioners in New York state. In doing so, it probes the tensions between land-banking policy and social equity goals, seeking to illuminate the tools, policies, and resources that can foster stronger partnerships and contribute to better land abandonment policies in shrinking cities. The conceptualization of social equity operationalized in this research was initially focused on the first two steps articulated in Figure 1. To operationalize “reparative planning” approaches (Goetz, Williams and Damiano 2020; Williams 2020), the outcomes of land banks’ work would need to lead to equitable urban development that serves the needs of residents who have historically been deprived of intergenerational wealth. Inclusion and community engagement by land banks would not be enough; there would need to be evidence of socio-spatial justice through the actions of land banks.

Methodology

Initially, four New York State land banks were selected of varying scale as measured by the number of properties acquired per year and the degree to which the organization promoted social equity versus quality of life in annual reports and online. This was also a selection based on the authors’ ability to gain sufficient depth and gather critical data about each land bank. After reviewing the promotional material on the websites of land banks, the first author spoke with directors of the Newburgh Community Land Bank (NCLB), Buffalo Erie Niagara Land Improvement Corporation (BENLIC), and Syracuse Property Development Corporation and attended a community renewal conference featuring members of the Albany County Land Bank (ACLB). Based on an evaluation of the website material consisting of a critical content analysis and interactions with the land bank lenders four land banks were selected: ALBC; Greater Syracuse Property Development Corporation, NCLB; and the BENLIC.

Table 1 summarizes the underlying themes related to answering the central research question. These included understanding community characteristics, the purchase process, community perceptions, and tools for social equity. To understand the racial, socioeconomic, and built environment characteristics of the communities, a comparative spatial analysis of land bank properties was performed using data provided by the land banks, 2015 American Community Survey data from the US Census, and publicly available county and city property data. In Albany, a land bank with a large number of properties, an optimized hot spot analysis (Getis-Ord Gi*), was performed using ArcGIS to identify spatially significant clusters of properties acquired and properties sold. An optimized hotspot analysis identifies statistically significant clusters of high values (hot spots), which indicate areas where clustering is not likely to be caused by random chance.

Underlying Themes, Subquestions, and Research Methods.

In order to provide an overview and comparison of the scale and scope of the land banks’ activities, records of acquisition and disposition of properties of the various land banks were compiled based on data provided by the land banks, and from publicly available data on land bank websites. In addition, eight semi-structured interviews were performed with land-bank leaders in the four New York State communities. Two additional nonprofit leaders in Buffalo were interviewed about their perceptions of the Buffalo Erie County Land Bank to the Community. The 2017 Community Renewal and its Discontents Conference at the Albany Law School also informed this study; this conference included discussants on land banks and social equity.

In 2022, the directors of the four case study land banks were contacted again. Additional e-mail correspondence and a Zoom interview were incorporated into the analysis to account for COVID-19 pandemic-era conditions for land banks in New York state. More recent efforts at pursuing social equity are incorporated into the case studies and analysis. The case study analysis that follows focuses on three of the four land banks where the authors were able to obtain comments and incorporate additional information about current conditions and equity initiatives.

Case Studies

The following are in-depth case studies of the three selected land banks, emphasizing the relationship of land-banking practices to social equity. It is important to note how the COVID-19 era has dramatically changed conditions for land banks. During the pandemic, a New York State moratorium on foreclosures and evictions prevented land banks from acquiring properties. This had a major effect on land banks’ inventory as foreclosures “comprise the vast majority of properties acquired by any land bank in NYS” (Zaranko 2022). Another State source of funding for land banks, the NYS Attorney General Grant Community Revitalization Initiative was depleted during the course of the pandemic. This eliminated a primary source of funding for stabilizations and demolitions. According to Adam Zaranko, director of the Albany County Land Bank (ACLB): I would argue [this has been] the most challenging in the history of the program – at a time when the program has grown to 26 land banks—and a few land banks almost didn’t make it through. Fortunately the NY Land Bank Association and all of our partners were able to secure $50 million in designated funding from NYS in the recent state budget and we have begun to see reinvestment. The moratoriums have also expired and now we are bracing for the backlog of properties to wash across communities throughout the state (Zaranko 2022).

The COVID-19 era has challenged land banks all the while deepening inequities in many communities within New York. This underlines the complexity and importance of addressing both resources for land banks and paying greater attention to equitable urban reinvestment.

Albany County Land Bank

The ACLB acquires virtually all properties that Albany County has foreclosed upon. Since 2014, the ACLB has acquired over 1,250 properties, disposed of over 900, and completed more than 100 demolitions (Zaranko 2022).

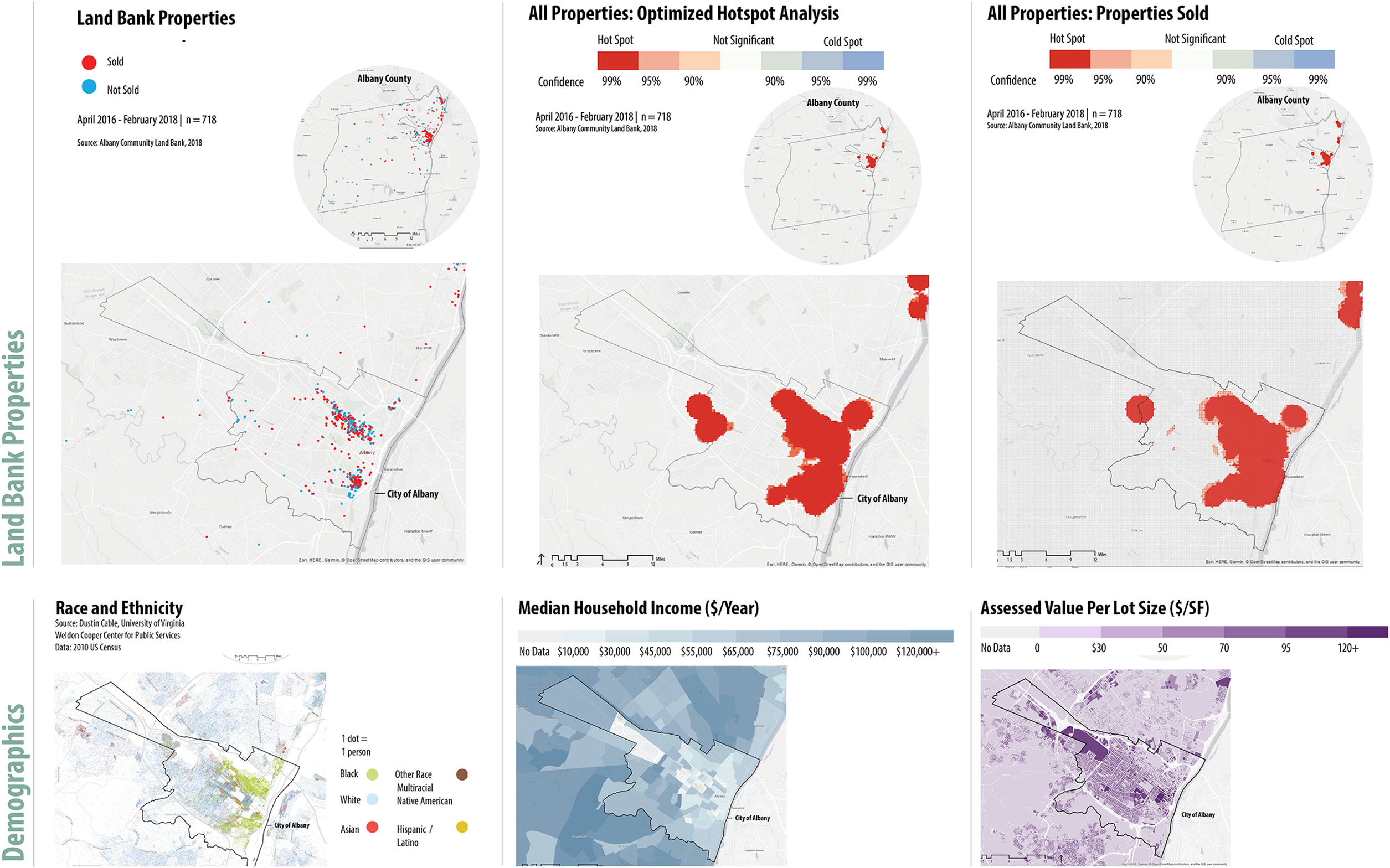

ACLB's portfolio reflects the broader geography of disinvestment in the county as illustrated in a spatial analysis of data to the year 2018 (Figure 2). The land bank's properties have been concentrated within the City of Albany in predominantly African American areas south and north of the central city. Central Avenue and Delaware Avenue serve as dividing lines between the more affluent and predominantly White areas bordering University at Albany and the predominantly Black neighborhoods north and south of the State Capitol. A number of wealthier, predominately White bedroom communities surround the City of Albany. In general, foreclosures have not occurred in the wealthier outer-ring bedroom communities of the city. A scattering of rural properties also exists throughout the county, with a concentration in Cohoes and Watervliet.

Albany County Land Bank properties and demographics. For color figures, please see online version of the article.

The land bank has faced challenges in selling properties in various conditions in neighborhoods throughout the county. According to ACLB's Executive Director, the lowest-quality properties often have very few purchasers and are generally sought after by contractors who can invest and perform a lower-cost renovation. Low-quality properties require substantial structural and/or stabilization work to make the properties habitable. High-quality properties may require some cosmetic or minor repairs but are generally habitable. Higher quality properties typically tend to be sought after by savvy investors, who regularly scan the land bank's website. Typically, these buyers have more financial capacity, own contracting companies, or have a large existing portfolio of rental properties (Zaranko 2018).

Zaranko contends that the added value of the land bank is in its ability to create a more equitable purchaser process that ensures that less experienced buyers have an equal footing with experienced investors. Like other land banks in New York state, Albany has a purchaser review process, in which a board of directors evaluates all applications for a property, weighing a purchaser's financial capacity, the offering purchase price, and plans to renovate and manage the property. ACLB often leaves the property on the market for several months and promotes it through real estate listings such as Zillow, Realtor.com, and MLS. For higher quality properties, this typically means that the land bank has a number of offers from various buyers. In these cases, the board has favored a homeowner applicant over an investor intending to rent the property in order to provide an opportunity “for someone that a normal real estate market would… just box out” (Zaranko 2018).

The ACLB's partnership with the Albany Community Land Trust as part of the Center for Community Progress’ National Technical Assistance Scholarship Program also shows work promoting social equity through affordable housing. The Albany Community Land Trust maintains 46 affordable rental units, including lease-to-purchase units (Graziani and Abdelazim 2017).

In higher-income neighborhoods in the inner ring suburbs, the Albany Land Bank sells property at a reduced price to the Albany Community Land Trust (Graziani and Abdelazim 2017). According to Zaranko, this helps the land bank avoid the operating costs of maintaining additional properties while allowing the land trust to work toward its affordable housing mission (Cotner and Zaranko 2017; Albany County Land Bank 2018b). Although the focus on promoting affordable housing may ultimately reduce its own revenue, Zaranko maintains that ACLB's mission extends beyond just maximizing revenue and offers an improvement to the land management regime previously administered by local government (Zaranko 2018). In other words, the land bank is more flexible and able to address properties on a case-by-case basis rather than simply selling properties to the highest bidder like the county government.

ACLB faces challenges in disposing of properties in economically distressed areas. In these cases, the land bank may sell properties to contractors who have the ability to renovate at a lower cost and develop rental units as investment rental properties. Zaranko acknowledged the barriers to homeownership in distressed areas, where renovating a property requires rehab knowledge and financing that many potential buyers lack.

ACLB has created a homeownership pilot program in conjunction with the nonprofit Affordable Housing Partnership. The Equitable Ownership Pilot Program (EOP) offers families living in the area making 50–70% of the area median income a discounted buying price or they are given a credit equivalent to hire a qualified contractor to help them renovate a property. Pairing buyers with additional grant resources and homeownership training, the program aims to reduce barriers to homeownership and give families in traditionally disinvested neighborhoods the opportunity to build and retain wealth. In 2018, when rolling the program out, the ACLB planned to select middle-level properties that required some renovation and conducted outreach to find residents in target communities interested in taking part in the program (Zaranko 2018). The aim of the program was to have a positive impact on the communities it serves and eventually scale up (Albany County Land Bank 2018a). As of 2022, ACLB lists no properties currently participating in the EOP Program. As noted above, New York State's eviction and foreclosure moratoriums associated with the COVID-19 pandemic “effectively stopped the pipeline of properties available to ACLB for 2+ years—consequently, this has resulted in a dearth of properties available for our various programs including EOPP” (Zaranko 2022).

Zaranko describes other current efforts that are organized around “equitable redevelopment principles that advance community priorities and create affordable housing” (Zaranko 2022). This includes a Lots for Less program that makes vacant lots available to qualifying residents for $100. Another initiative called “100in5” involves working with Habitat for Humanity to leverage +$3.5 million in American Rescue Plan Act funds provided by the City of Albany to build 100 new affordable homes in five years.

The ACLB touts its success in reducing the number of vacant, abandoned, and tax-foreclosed properties in the county and promoting programs that support social equity and raise awareness about issues of blight and abandonment. In addition, the ACLB has adopted a disposition policy that explicitly addresses redlining and historically discriminatory policies:

SECTION 5. DISPOSITION POLICIES AND CONSIDERATIONS – ACLB property dispositions and demolitions will comply with all statutory requirements and be guided by the following general criteria:

a. Activities benefitting neighborhoods and residents impacted by long term disinvestment and historically discriminatory policies and practices such as redlining

b. Activities that will serve underserved populations and communities to help address disparities in housing conditions and income as a result of generations of discriminatory housing and lending practices which have been exacerbated by the COVID-19 pandemic.

c. Activities that advance active municipal plans created with input from residents, organizations, and institutions

d. Activities that support housing, economic and community development priorities and opportunities for residents with low to moderate incomes

e. Activities, including but not limited to demolitions, to eradicate properties that impact the health, safety, or welfare of neighborhoods

f. Activities that leverage public, private, not-for-profit, and philanthropic funds

g. Activities that create or preserve quality, affordable and mixed income housing

h. Activities that support first time homebuyers, help build wealth, increase local ownership or stabilize neighborhoods (ACLB 2022).

The ACLB also includes a statement on its homepage that states “we recognize the injustices of discriminatory housing and lending practices that have systemically harmed communities of color and plagued our country and region for far too long” (Albany County Land Bank 2023). The statement continues “We recently formed an initiative to ensure that we are applying our resources effectively to address systemic disparities, support underserved populations and strengthen underserved communities… We call upon financial institutions, foundations, nonprofits, for-profits and all levels of government to partner with us so that we can continue to eliminate blight while creating more fair and just opportunities for homeownership in our county (Albany County Land Bank 2023).

In a COVID-19 era that follows the 2020 Black Lives Matter Protests and a heightened public discourse around race, this kind of statement is not unusual but is notably present and directly speaking to racialized disparities and the responsibility they bear in addressing injustices due to the discriminatory housing and lending policies.

Newburgh Community Land Bank

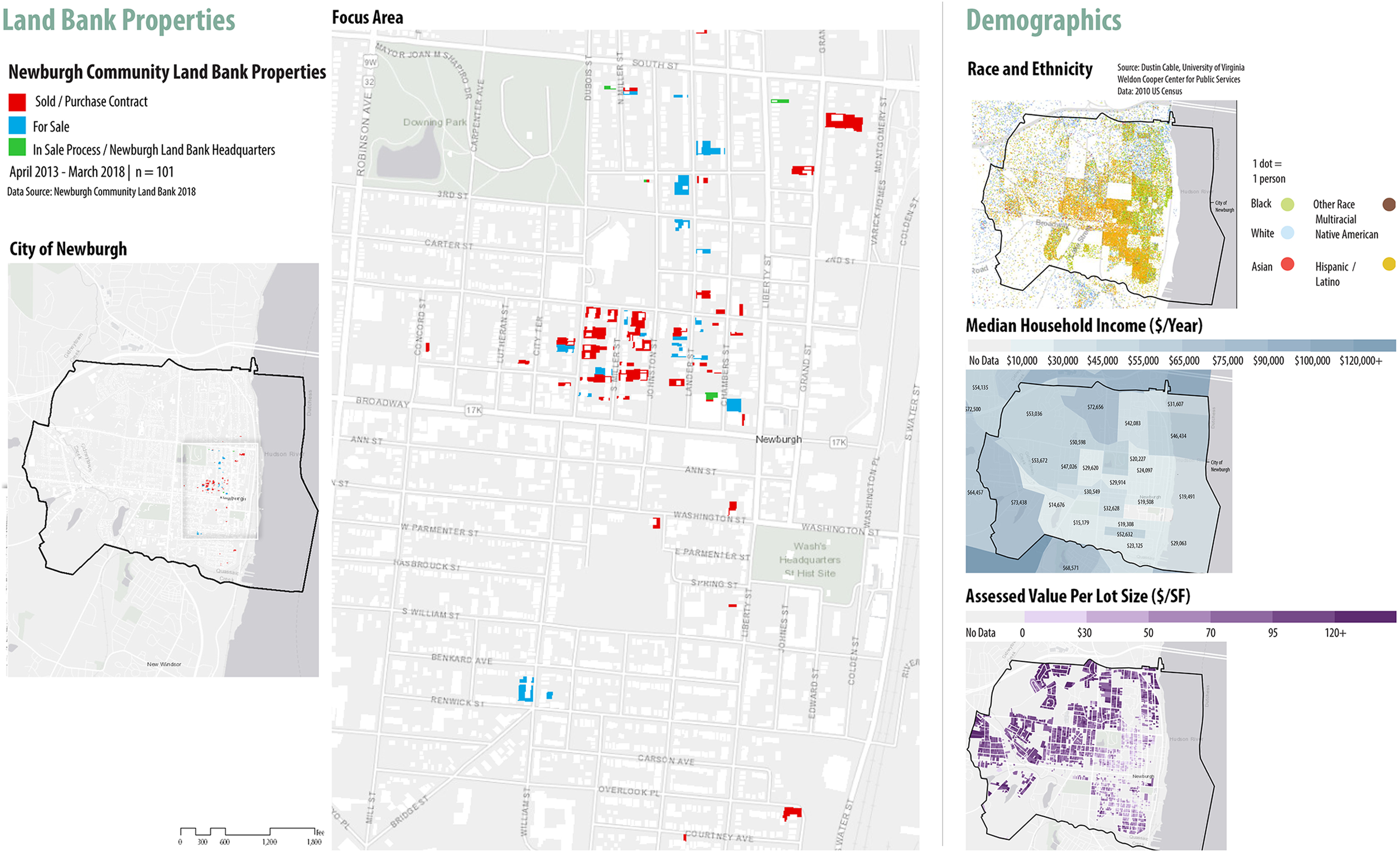

The NCLB began in 2012 as an effort to improve the city's code enforcement and development processes and provide a flexible nonprofit entity to put the backlog of tax-foreclosed property to productive use. Unlike in Albany, the City of Newburgh does not directly hand over all vacant, abandoned, and foreclosed properties to the NCLB. Instead the NCLB targets specific tax-foreclosed properties, it would like to acquire from the City (Fletcher 2018). Of the three case study land banks, NCLB had the highest percentage of properties put to productive use as of data from 2018. This can be attributed to the stronger housing market and the fact that Newburgh selects the properties it wishes.

A total of 47.5% of Newburgh's population identifies as Hispanic or Latinx. Primarily Latinx areas are concentrated in the south of the city, with a larger Black population along the waterfront. Areas to the west of downtown are wealthier, with the higher poverty areas in the south and east of the city. The land bank has focused on the revitalization of the city's downtown core, targeting a five-block focus area within one census tract. The area is predominantly low-income and Latinx (Figure 3). The three census tracts comprising the core area have a median household income ranging from $19,000 to $32,000. The area, which contains a high concentration of city-owned, tax-foreclosed property, had an over 50% vacancy rate when the land bank began

Newburgh Community Land Bank properties and Newburgh demographics. For color figures, please see online version of the article.

Operating primarily within the East End Historic District, where costs of buying and renovating property typically exceed the sale value of an improved property, the NCLB has focused on absorbing the upfront costs of development downtown. The land bank's initiatives have facilitated the development of affordable housing, created partnerships with community organizations, and led to place-based arts and community garden initiatives. The land bank's partnerships with Habitat for Humanity and LIHTC developers have incentivized affordable housing development in the land bank's target area.

Jennifer Welles, the Executive Director of the Newburgh Land Bank since 2019, emphasized that conditions have changed dramatically in Newburgh since COVID-19, due to gentrification pressures, the dramatic increase of construction costs and supply issues, and the depletion of available New York State funding. We have focused a lot of our resources on providing fully rehabilitated homes to local residents to occupy as owners in order to address the low homeownership rates in the neighborhood particularly among Black residents and deal with some of the hurdles minority buyers face in purchasing homes, such as low or no credit, discrimination in the buying process, insufficient income to cover the mortgage and taxes, etc. This work is challenging given the current conditions of the housing stock we have access to, the rising cost of construction compounded by the constraints of the historic district requirements, the high property tax rate in the City of Newburgh, and the inadequacy of funding to support affordable homeownership (Welles 2022).

Buffalo Erie Niagara Land Improvement Company

The Buffalo Erie Niagara Land Improvement Company (BENLIC) began in the spring of 2012 as a product of intermunicipal agreement between the Erie County Executive's office and the four other municipal foreclosing units in Erie County. Limited by the New York State Land Bank Act's restrictions on total number of land banks within the state, the Erie County Executive's office created a county-wide regional land bank comprising the City of Buffalo, the Town of Lackawanna, the Town of Tonawanda, and Erie County. Erie County operates as the foreclosing unit for the other 25 towns and the 16 villages within the county (Gordon 2018).

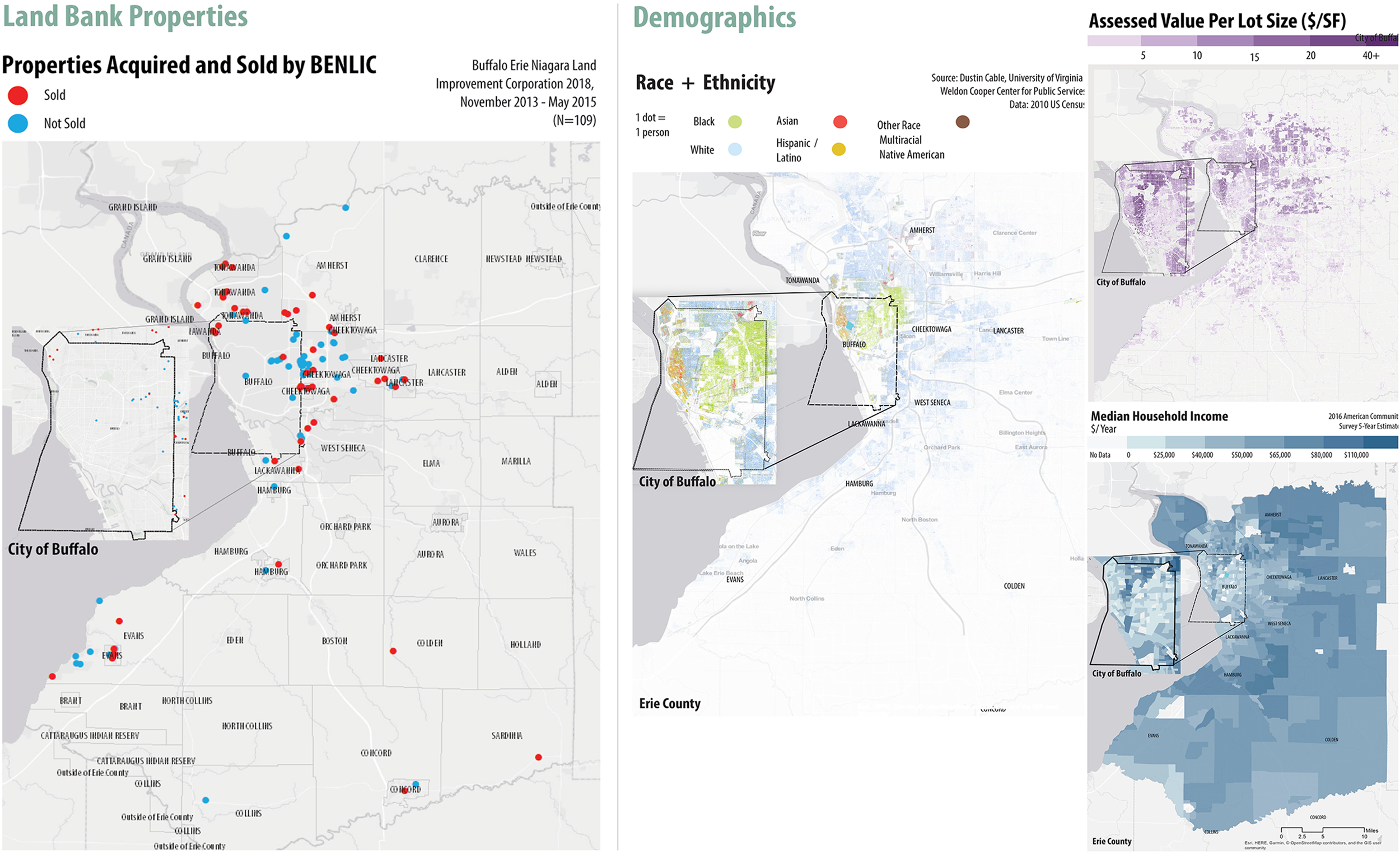

Between its inception and 2018, the land bank acquired 109 properties throughout the county and put 50 properties to productive use (Buffalo Erie Niagara Land Improvement Corporation 2018) (see Figure 4). Operating as a small nonprofit with a limited budget and small staff, the land bank's decision to acquire a property involves a sophisticated process. BENLIC receives a list of foreclosure inventories from Buffalo, the Town of Tonawanda, the Town of Lackawanna, and requests for foreclosures from towns whose properties are foreclosed on by the county. The land bank considers possible proposals against the resources available to them. BENLIC uses the “A-B-C rule” as a rule of thumb to evaluate which properties to acquire. “A properties” have the most value, while “B properties” require some repairs. “C properties” are the most challenging and need significant investment to renovate. Accordingly, the land bank typically takes on one A property in order to pay for the renovation and stabilization of two B properties and one C property (Gordon 2018). The acquisition of properties is determined by the BENLIC board of directors, which is composed of 11 representatives representing the four different government foreclosure units (BENLIC 2018). The City of Buffalo has the greatest representation on the board of directors with five representatives. Erie County has three representatives. The City of Tonawanda, the City of Lackawanna, and Empire State Development, have one representative each.

Buffalo Erie Niagara Land Improvement Corporation (BENLIC) Land Bank properties and Erie County demographics. For color figures, please see online version of the article.

Despite greater representation from the City of Buffalo on the board of directors, BENLIC had acquired only 10% of their properties within the City of Buffalo as of 2018, instead focusing on the suburban communities of Erie County. According to BENLIC Executive Director Jocelyn Gordon, this reflects the City of Buffalo's desire to maintain the already well-established land management regime in the city proper (Gordon 2018).

White flight and suburbanization have created substantial geographies of segregation in Buffalo and Erie County (see Figure 4). White suburban communities surround the City of Buffalo, with the exception of the large African American population in inner-ring suburbs northeast of the City of Buffalo boundary. Within the city, Main Street serves as a dividing line between the wealthier west side and the poorer predominately African American east side, where a legacy of urban renewal and city-led demolition has led to significant disinvestment. Although active throughout Erie County, BENLIC has focused primarily on acquiring properties in the suburban communities of Evans, Cheektowaga, and Tonawanda. According to Executive Director Jocelyn Gordon, working in the suburbs helps the land banks subsidize renovations in the City of Buffalo.

Over the past 40 years, the City of Buffalo has aggressively foreclosed on property. Notably in the 2000s, former mayor Byron Brown's campaign to reduce vacancy rates to 5%, resulted in the demolition of over 6,000 structures (Lyons 2009). This has led to a land management program of properties owned by the City of Buffalo that operates separately from the land bank. Additionally, the land bank is apprehensive about the high cost of renovation and limited resale potential of investing in Buffalo. Gordon contends that in the city proper, the land bank may have to spend $135,000 on a house that will sell for $70,000. By focusing on higher quality properties in stronger housing markets in the city suburbs, the land bank is able to subsidize their work on more expensive rehabilitation projects in the City of Buffalo (Gordon 2018).

A majority of BENLIC's property comes via Requests for Foreclosures from municipalities within Erie County, which the land bank acquires at County in-Rem Auction. Because BENLIC selects the properties it acquires, it typically sells a higher percentage of properties than Albany, which operates as default manager of vacant and abandoned properties.

In addition to supporting its own operations through sales, BENLIC has leveraged significant funding from grants from the New York State Attorney General's office. The land bank has touted its success in rehabilitating vacant, tax-delinquent homes and returning them to tax-paying status, and creating side lot programs to expand neighborhood lots and public lands. Additionally, the land bank has cultivated relationships with large banks, which has resulted in donations of property along with cash contributions from JP Morgan Chase, Wells Fargo, and Bank of America (Gordon 2016).

As a small nonprofit in a county with a large number of vacant and abandoned properties, BENLIC sees itself as a tool to help municipalities and nonprofits meet their goals. According to BENLIC Executive Director Jocelyn Gordon: We just say “Tell us how it's going to help you meet your goals and then our board will decide let's do that and we'll help you. We're not trying to plan for you.” We're really just more of an implementation mechanism for everybody to meet the goals of their land use plans, of their comprehensive plans, of their not-for-profit missions. You tell us how it's going to meet your mission and our board will decide and say, “Yes, you are deserving and here it is and here's how we can help you.” (Gordon 2018)

Analysis: Land Banks’ Adoption of the Language of Equity

These case studies suggest that land bank leaders were aware of and were addressing issues of social equity to varying degrees. In 2017 and 2018, when this research began, social equity appeared to be viewed as one of many goals, largely subservient to the underlying mission of putting property to productive use. In the COVID-19 era, following the 2020 Black Lives Matter protests that spurred a national dialog around race, the language of social equity and systemic racial inequities had become more common among the case study land banks. Although the goals of promoting affordable housing and improving neighborhood services may inherently conflict with improving the tax base and funding land operations through sales revenue, the large scale of land abandonment—particularly in the most disinvested areas—makes disposing of properties for any productive use difficult. ACLB, the land bank that acquires all county-wide foreclosures—had put just 40% of properties to productive use during the study period, while Buffalo and Newburgh—the land banks with a more selective acquisition process—had, respectively, disposed of 47% and 62% of their total inventories. Efforts to partner with nonprofit developers to develop affordable housing were present among all three land banks.

Each land bank studied represents a particular response to the previous land management regime of the municipality and the politics of their respective region. In Albany, the land banks have responded to the municipality's backlog of tax-delinquent-foreclosed properties, with large-scale programs that have moved a significant amount of property to responsible tax-paying owners. In Buffalo, the land bank has navigated the complex politics of the region to work primarily as a tool for suburban local governments. More recently, it has new initiatives on the Eastside of Buffalo. Newburgh's small-scale place-based model has targeted development in downtown Newburgh, lowering barriers to development within a historic district. In all three cases, the land banks have a close relationship with their respective municipalities, but a desire to distance themselves as distinctive, separate, and flexible nonprofit organizations.

Although land banks do have the ability to hold on to property indefinitely, the land-bank leaders viewed banking property as an undesirable alternative to selling it to a responsible owner. In their view, the responsibility to maintain the property places costs and burdens on the land banks’ limited staff and financial resources and undermines their mission to put properties to productive use.

Accordingly, the donation of property or sale at a reduced cost to a housing nonprofit benefits the land bank by relieving them of the costs associated with managing a portion of their real estate. Although the motivation of the land bank may be social equity-oriented, the decision to partner with nonprofits in the community is also a pragmatic approach that allows a land bank to sustain its operations. In severely disinvested communities, affordable housing developers with access to federal subsidies may be the only buyers willing and able to invest in a property. Conversely, other properties may be primarily sought after by local landlords or investors intending to flip a house for profit. Although the land banks’ purchaser process guarantees that only nondelinquent, responsible homeowners are able to purchase, the relative demand for a particular property ultimately determines its future use.

Some land banks did clearly promote affordable housing and homeownership. This appears to be a stronger commitment to equitable urban development than simply acting as a mechanism to ensure future property owners will pay their taxes. The dual role as a community-based organization that promotes social equity and an organization closely tied to municipalities’ efforts to raise the tax base and promote economic development was a central tension that defines how a land bank approaches its operations.

Community Perceptions and Engagement as Barriers

As organizations focused on managing “blighted” properties in low-income communities, land-bank leaders saw challenges in both connecting to community members in neighborhoods in which the land bank operates and a need to promote the mission of the land bank to members of the community at large. According to ACLB Executive Director, Adam Zaranko: [Our properties] are mostly concentrated in low-income economically-distressed neighborhoods where the majority of the population in the county doesn't go through every day, hardly ever goes, maybe avoids. And so not everyone is aware of the scale and scope and size of the challenge, but everyone is paying for it, one way or another. Just because you don't live next to these buildings doesn't mean it's not creating a burden on you. If you're a taxpayer, it's drawing more government services, which is higher cost for garbage, which means limited revenue for other things. [The owners] of these properties aren’t paying taxes. [It] disproportionately harms and impacts people in the neighborhood, which we know could bear the least, and have lowest income (Zaranko 2018).

Zaranko also expressed difficulty in promoting the land bank's property inventory to a variety of buyers, including issues of communication with first-time home buyers, real estate investors, and neighborhoods where they are focused: First-time home buyers say, they don't approach us because they think we only sell to real-estate investors. Real-estate investors think that we only work with first-time home buyers, and people in our Focus Neighborhoods think that we only work with people outside of the Focus Neighborhoods, so a lot of it is managing perception… we work with everyone. There's plenty of real estate to go around, unfortunately (Zaranko 2018).

Shaping the general public's perceptions also appeared to be central to maintaining political support and funding from a municipality. However, independence from the municipality also appeared to be important in shaping the neighborhood residents’ perceptions of the land bank, particularly in distancing the organization from a legacy of previously unpopular planning policies. This was especially apparent in Buffalo, where the land bank had to distance itself from the City's legacy of large-scale demolition and the current environment of speculation. The lack of public understanding of the mission and operations of a land bank was echoed among staff of all three land banks.

Efforts to engage with neighborhood residents living near land bank properties appear to be a focus of all three land banks, but most notable in Albany and Newburgh. When land banks were initiated, the leaders formed formal community advisory boards. As time has gone on, the role of these formal bodies has faded as volunteers have left and the organizations embrace a more professionalized apparatus for community engagement. All three land banks have hired AmeriCorps volunteers to do public outreach. In Newburgh, the staff performed long-form interviews with 30 neighborhood residents about neighborhood identity and safety issues. In Albany, the land bank has moved from a formal advisory commission of volunteer citizens to a more professionalized staff that seeks out community input. The land bank has a rotating workshops series in focus neighborhoods, has a full-time staff member that does one-on-one counseling on purchase applications, and has made an effort to increase their presence on social media. The ACLB has also considered creating a land bank neighborhood ambassador structure to connect with knowledgeable neighborhood leaders on the ground.

As organizations focused on disinvested areas primarily in BIPOC communities, it is unclear whether the land banks’ outreach has allowed them to sufficiently distance themselves from the top-down planning policies of the past. Although all three land banks’ efforts show a desire to connect with low-income communities they must serve, these efforts would likely benefit from greater engagement. Additionally, limited staff resources and funding may stifle the land banks’ ability to do effective community engagement.

The Future of Demolition and the Just City

Demolitions are a controversial, yet common practice in shrinking, Rust Belt cities. The argument for demolition, embodied in programs such as Detroit's Blight Force Removal Task force view removing problem buildings as a way to rid problem areas of crime, arson, and diminished property values, until a time when new investment will be attracted to the neighborhood (Detroit Blight Task Force 2014; Hackworth 2016). Additionally, demolition relieves municipalities of the financial burden of collecting, maintaining, and providing infrastructure to tax-delinquent, vacant, abandoned, and foreclosed properties. Others have critiqued the assumption that blight removal—without other development interventions—will positively benefit communities (Hackworth 2016). As mentioned above, by attempting to triage “problem” homes or neighborhoods, planners signal that an area is in decline—beginning a self-fulfilling prophecy that can accelerate cycles of disinvestment (Hackworth 2016; Kirkpatrick 2015; Metzger 2000).

Land-bank leaders viewed demolitions as a necessary tool to be approached pragmatically on a case-by-case basis. Albany, which has inherited the largest portfolio of properties from the city, performed demolitions at a faster rate than Newburgh—the land bank with the most selective approach to property acquisition. The decision to perform demolition is largely determined by condition and limited demand for a property. Land-bank leaders spoke of the decision to demolish as based on the best use of limited resources. Demolition funding typically comes from a separate source of municipal funds that in most cases are limited.

Funding spent on demolitions can lead to widespread demolition patterns that not only make it more difficult to return properties to tax rolls but impede neighborhood revitalization efforts. The requirement to perform triage to determine which buildings should be demolished can leave the opportunity for neighborhood rehabilitation later on. Limited resources can result in more rehabilitation rather than demolition. If land banks are provided more resources, these resources should be tied to either the requirement to look at a range of options for their inventory or consider not only the options best for tax rolls but also for the community over the long term. Quick demolition fixes may not be the answer to achieving socially equitable outcomes.

The decision to demolish a structure based on factors such as limited demand, building condition, and funding suggests land banks’ general acceptance of rightsizing as a useful tool for disinvested communities. Nevertheless, some land bank directors expressed an underlying concern that demolition may undermine community revitalization efforts, revealing some skepticism about the aggregate effects of widespread demolition policy. As limited funding forces the three land banks to prioritize their operations, demolition appears to have taken a back seat to work that prioritizes reinvestment of existing properties. As lack of funding stifles the ability of land banks to perform demolitions, it appears that the land banks have made a greater effort to prioritize policies that emphasize reinvestment and rehabilitation over demolition. Nevertheless, without these concerns, it is unclear whether or not land-bank leaders would fully acknowledge that the effects of widespread demolition policy undermine their social equity goals.

Land banks potentially have an important role in revisioning their approaches to demolition. Mothballing—the process of boarding up and securing abandoned property until a time when reinvestment can occur—provides a more reinvestment-focused alternative for the hardest-hit neighborhoods. The unique ability of land banks to hold property tax-free and indefinitely makes them the ideal entity to carry out this process. Although many land banks perform mothballing, political pressures to show immediate results, lack of stable funding sources, and land banks’ unwillingness to hold properties long-term often make demolition an all-too-common choice. This suggests the need for more research and policy development related to means of mothballing properties to support rehabilitation years later. In finding resources to work in the longer term and retain existing building stock, there is the potential to spare neighborhoods from more vacant lots while retaining buildings that in the longer run may prove useful in providing affordable housing and retaining urban fabric in the neighborhoods hardest hit by generations of structural racism. Land banks should be working toward solutions that prevent the further creation of racialized landscapes of vacancy in those neighborhoods that have been deprived of the capital to maintain and improve properties.

Another approach could be to embrace whole building deconstruction as an alternative to demolition. Deconstruction policies have been adopted in rapidly growing cities such as Portland, Oregon; San Antonio, Texas; and Vancouver, British Columbia. The Circularity, Reuse, and Zero Waste Development (CR0WD) network has created a guide for local governments to support the adoption of deconstruction and reuse policies in New York State (Circularity, Reuse and Zero Waste Development 2023) . These policies emphasize the benefits of deconstruction in working toward new green jobs, protecting neighborhoods from the toxins associated with mechanical demolition, and creating a regional circular economy, as well as conserving embodied carbon as part of a toolkit for realizing municipal Green New Deal resolutions. Given land bank's traditional role in demolition, land banks could play an important role in working with local governments toward deconstruction policies and programs.

Equitable and Reparative Land Banking

The case studies presented in this article reflect different approaches to addressing land abandonment issues in various contexts. Each responds to the previous land management regime of the municipality and the politics of their respective regions. In Albany, the land bank has responded to the municipality's backlog of tax-delinquent foreclosed properties, with large-scale programs that have moved a significant amount of property to tax-paying owners. In Buffalo, the land bank has navigated the complex politics of the region to work primarily as a tool for suburban local governments, but with new initiatives within the central city. NCLB's small-scale place-based model has targeted development in downtown Newburgh, lowering barriers to development within a historic district. In all three cases, land banks have a close relationship with their respective municipality or municipalities, but a desire to distance themselves as distinctive, separate, and flexible nonprofit organizations. As Hackworth (2016) has suggested, these land banks have served as improvements to the previous municipal land management's regimes that sold the property to the highest bidder. Additionally, land banks in New York state have lacked the controversies that have embroiled the land bank authority in Detroit.

Land bank leaders indicated an awareness and desire to address issues of social equity as a goal to be achieved alongside their principal mission of putting properties to productive use. Ultimately, the level of commitment to address equity issues greatly depended on the demand for a property, and the strength and presence of other nonprofits in the region. Because subsidized, low-income housing developers may be the only buyers willing to develop in significantly disinvested neighborhoods, relationships with nonprofit housing developers show promise in providing quality housing to existing residents. In addition, partnerships with community land trusts and first-time home buyer programs for existing residents can promote community-led development. Although programs and partnerships focused on affordable housing and homeownership serve as an important component of the land banks missions, they have remained a relatively small portion of their total operations. Without significant efforts to connect with community residents, land banks will at best serve as mechanisms that ensure that only tax-paying landlords purchase property, and at worst, demolish homes deemed too dilapidated to renovate.

Land abandonment policy in shrinking cities has historically lacked the input of communities of color and has prioritized the municipal tax base over their needs and concerns. The origins of land banks as agents of municipal government focused on “blight” removal has led to a land abandonment policy that has been successful in promoting redevelopment and improving local tax bases but has only just begun to incorporate social equity goals. Research addressing the mistrust of top-down planning approaches in low-income communities of color provides valuable insights into the role of land banks in forging relationships with the communities they serve. Although widespread demolitions, aggressive code enforcement, and the language of blight removal represent painful parallels to mid-century urban renewal that undermine a social equity mission, the growing embrace of housing affordability, homeownership, and community engagement as an important objectives of a land bank suggests a step in the right direction. However, more steps must be taken.

Despite the promising language adopted by the land banks, we believe they should take more steps toward transforming their practices through a reparative planning framework. Although precedents for adopting reparative justice or a reparative planning paradigm as theorized by Williams (2020) are limited, we believe land banks would serve the needs of residents who have historically been deprived of intergenerational wealth. Inclusion and community engagement by land banks would not be enough; evidence of sociospatial justice should be evident in their outcomes. A reparative planning framework suggests that they should be substantially governed by the communities they seek to repair and that achieving social equity and equitable urban development should become their highest priorities.

Given the deepening inequalities during the COVID-19 pandemic era, there is a growing need to address long-standing structural inequities. Land banks have been granted significant powers that have the potential to reshape U.S. cities for better or for worse. They also operate with limited resources at this time. More resources could be provided to land banks from Federal and State sources, but that should be under the condition that they become vehicles for repairing the racialized geographies, uneven landscapes, and racial wealth gaps that White supremacist policies have generated.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

This research received support from the Cornell University Office of Engagement Initiatives (now the Einhorn Center for Community Engagement) through the Faculty Fellowship for Engaged Scholarship and Engaged Opportunity Grant programs.