Abstract

Health care consolidation continues to increase in the United States. Most of the evidence focuses on horizontal consolidation or vertical consolidation between hospitals and physician practices. The lack of comprehensive and longitudinal data identifying insurer and hospital vertical consolidation has limited study of the prevalence, variations, and impact of this form of consolidation. Therefore, we created a novel dataset of hospital-Medicare Advantage (MA) contract consolidation from 1980 to 2024. We illustrate the power of this novel dataset through analysis of annual trends in hospital-MA contract consolidation and state-level geographic variation in the share of hospitals consolidated with MA contracts. We also show that a quarter of hospital integrated MA contracts are owned by an MA insurer that owns other non-hospital integrated MA contracts. We make this dataset public to facilitate research on hospital-MA contract consolidation that can inform health care policy and anti-trust law.

Introduction

Health care in the United States has become highly consolidated (Dafny, 2021; Furukawa et al., 2020; Rooke-Ley et al., 2024). The rise in health care consolidation has largely led to increased costs without clear benefits in health outcomes or care quality (Beaulieu et al., 2020; Borsa et al., 2023; Curto et al., 2022; Neprash, 2020; Sinaiko et al., 2023). There has been scrutiny of several types of health care consolidation from federal and state policymakers, Congress, Department of Justice (DOJ), and Federal Trade Commission (FTC; Federal Trade Commission, the Department of Justice and the Department of Health and Human Services Launch Cross-Government Inquiry on Impact of Corporate Greed in Health Care, 2024; Private Equity in Health Care—Looking at State Policy, 2024; “Ten Things to Know About Consolidation in Health Care Provider Markets,” 2024). The majority of research has focused on horizontal consolidation, which occurs between two firms on the same level of the supply chain, including hospital mergers and private equity roll-ups of independent physician practices (Beaulieu et al., 2020; Singh et al., 2022). Much less attention has been given to vertical consolidation, which occurs between two firms on different levels of the same supply chain, such as hospitals and insurers (Bejarano, Ryan, Trivedi, Offiaeli, & Meyers, 2024; Frakt et al., 2013; Hedquist et al., 2024; Meyers et al., 2020). The most recent merger guidelines from the DOJ and FTC in 2023, which are the first to include vertical consolidation after recommendations in the 2020 guidelines were withdrawn, signals the growing importance of this type of consolidation (Merger Guidelines [2023]—U.S. Department of Justice and the Federal Trade Commission, n.d.).

One important and accelerating type of vertical consolidation is between MA contracts and hospitals. In fact, enrollment in hospital integrated MA contracts (HIMACs) has risen from 1,766,026 beneficiaries in 2011 to 4,173,688 beneficiaries in 2022, which keeps with the rapid enrollment rise in MA overall (Bejarano, Ryan, Trivedi, Offiaeli, & Meyers, 2024; Freed et al., 2024; Hedquist et al., 2024). Currently, a quarter of MA enrollees (who now make up more than half of all Medicare beneficiaries) are enrolled in HIMACs (Freed et al., 2024). While the level of enrollment in HIMACs raises the importance of evaluation, little is known about their impact. Research examining HIMACs prior to 2015 found an association with higher premiums, better care quality, and an increase in coding intensity compared to non-integrated MA contracts (Frakt et al., 2013; Geruso & Layton, 2020; Johnson et al., 2017; Meyers et al., 2020). The lack of data identifying HIMACs after 2015 may have limited research on contemporaneous trends and impacts.

Given the importance of studying HIMACs, we created a novel dataset that identifies HIMACs from 1980 to 2024. We explore annual trends, geographic variation, and further subclassification of the different types of HIMACs. We also make this dataset publicly available to reduce data barriers to studying HIMACs.

New Contribution

To our knowledge, there is only one previous longitudinal dataset that identifies HIMACs, which has not been updated since 2015 nor made publicly available (Geruso & Layton, 2020; Johnson et al., 2017). Our dataset is current through 2024, uses several forms of data to provide the most comprehensive identification of HIMACs, and is publicly available to increase data access to the broader research community.

Study Data and Methods

This study was reported following the STROBE reporting guidelines (Elm et al., 2008).

Data Sources

To create a comprehensive and novel dataset that identifies HIMACs, several data sources were used including the Agency for Healthcare Research and Quality (AHRQ) compendium files, public MA landscape files, and several forms of public reporting (e.g., MA and hospital websites, industry reports, and press releases). The AHRQ compendium files include data on 639 health systems in the United States, which are defined as common ownership of at least one hospital and one physician group (Compendium of U.S. Health Systems, n.d.). The MA landscape files are public use files that include data on the offerings of each MA contract (Centers for Medicare & Medicaid Services [CMS], n.d.). To explore geographic variation, we linked each hospital to its state based on the American Hospital Association (AHA, n.d.) annual hospital file.

An author and a research assistant overseen by a different author (G.B. and G.M.) independently identified, screened, and verified each HIMAC. We started with the AHRQ compendium files which are at the health system level. First, we limited to health systems that had indicated they were consolidated with MA contracts in the AHRQ compendium files, which is based on hospital survey responses in the AHA annual hospital files. We manually verified each of these consolidations using public reports (e.g., websites, industry reports, and press releases) following previous research (Bejarano et al., 2025; Braun et al., 2021; Singh et al., 2025). If we were not able to verify the consolidation in public data, we considered the health system to be non-integrated with MA contracts. Next, to identify additional HIMACs that were not recorded in the AHRQ compendium files, we manually searched each MA contract that was active in 2024 using public reports. We added the HIMACs found via this method to those verified from the initial AHRQ compendium files. We considered the MA contract effective date found in public MA contract data as the year of consolidation. Our logic was as follows: when hospitals create their own MA contract the HIMAC is integrated from inception; similarly when hospitals partner with existing MA insurers a new MA contract is typically created for this partnership, which is also integrated from inception. We validated our approach by comparing the HIMAC contract effective date with the timing of press releases announcing vertical integration between the relevant hospitals and MA plans. We expanded this dataset to the hospital level using AHRQ health system-to-hospital crosswalks, which makes the assumption similar to prior studies that the MA contract is consolidated with all the hospitals in that health system (Meyers et al., 2020). Thus, we assume that any benefit of consolidation (e.g., data sharing between insurer and hospital) accrues to all hospitals in the health system. In addition, we identified whether a HIMAC was a hospital partnered MA contract (HPMAC) if their parent organization in public MA contract data was an MA insurer that also offers non-integrated MA contracts. For example, a hospital (e.g., University of Maryland Medical System) partners with an existing MA insurer (e.g., BlueCross BlueShield) to offer a HPMAC (University of Maryland, Hopkins to Offer Medicare Advantage Plans in 2016–Baltimore Sun, n.d.). The other HIMACs were classified as hospital-owned MA contracts (HOMACs) since their parent organization was the health system or hospital. For example, a hospital (e.g., Massachusetts General Brigham) can create its own HOMAC without partnering with an existing MA insurer (State House News Service, 2022). The dataset is provided in the Supplemental Appendix as a csv file along with a data dictionary. The final publicly available dataset includes the AHRQ health system identifier, MA contract number, hospital CMS certification number, insurance partnership identified, and year of consolidation.

Analysis

We describe the dataset in several ways including describing the annual trends in consolidation at the hospital and MA contract level, annual trends in MA contract termination, geographic variation in the share of hospitals that are consolidated with MA contracts in 2015 and 2024, and by subclassification (HIMACs affiliated with multiple health systems and insurance partnership). The annual trends used the first year that an MA contract or hospital were consolidated, which means that a hospital that consolidated with several MA contracts was only counted for the first consolidation and vice versa. Market penetration of MA integrated hospitals was calculated using the number of hospitals that were still consolidated with MA contracts as the numerator and all hospitals as the denominator by each state for both 2015 and 2024. We identified MA contracts that were affiliated with multiple health systems per the AHRQ compendium system identifiers. Finally, we classified HIMACs as HPMACs or HOMACs. There are 45 HIMACs that were terminated, and therefore their parent organizations are not in the MA contract data leading to a missing value for insurance partnership in the dataset.

Results

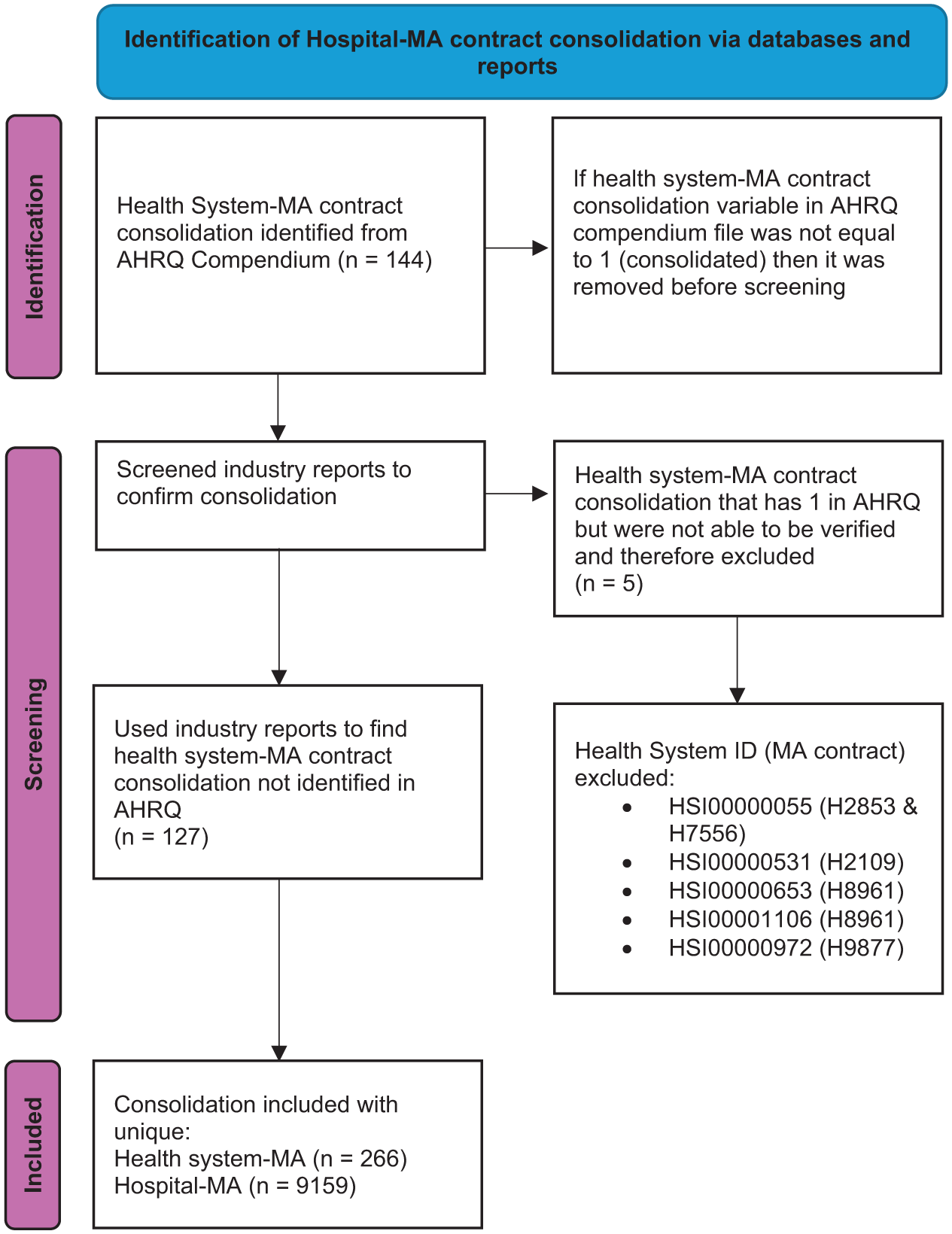

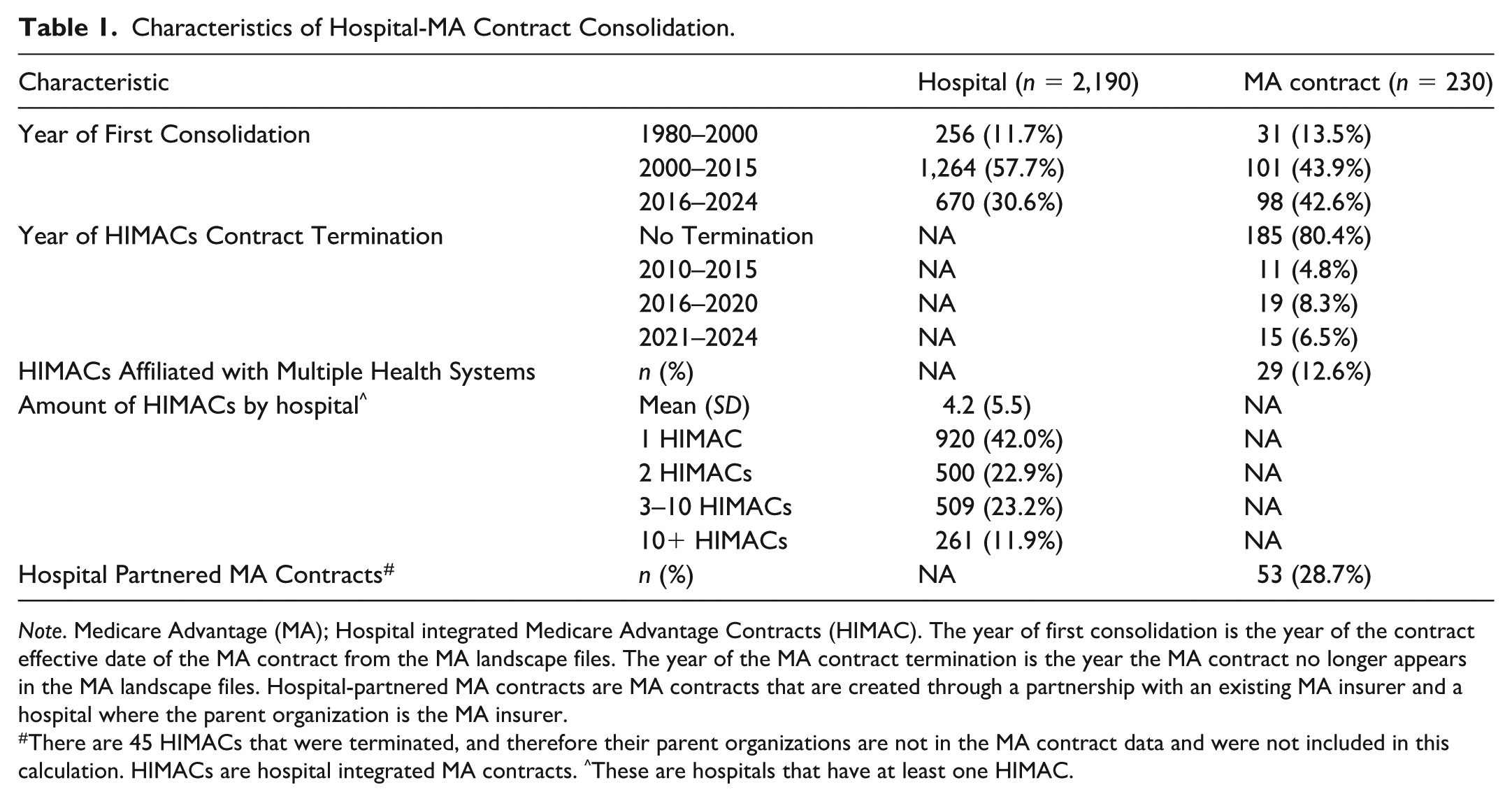

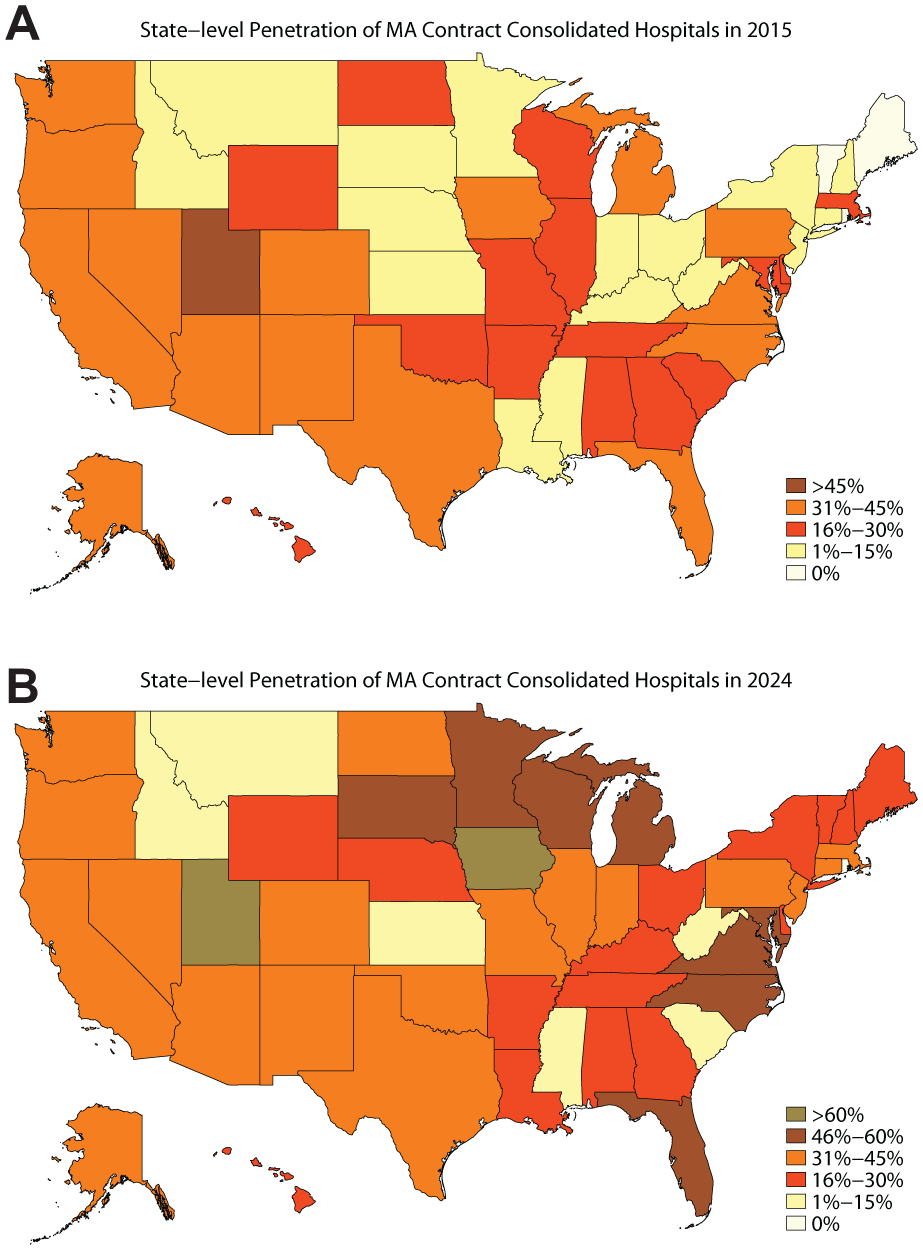

We identified and verified 9,159 unique hospital-MA contract pairs (266 unique health system-MA contracts) from 1980 to 2024 (Figure 1). There were 2,190 unique hospitals and 230 unique MA contracts, of which 30.6% of the hospitals and 42.6% of the MA contracts first consolidated after 2015 (Table 1). While most HIMACs are still active, 19.6% were terminated from 2010 to 2024. There was substantial state-level geographic variation in the share of hospitals that are consolidated with MA contracts in 2015 and 2024 (Figure 2A and 2B). In 2015, Utah was the only state with over half of their hospitals having a HIMAC. Meanwhile, Rhode Island, Vermont, and Maine did not have any hospitals with a HIMAC. By 2024, Rhode Island was the only state that did not have a hospital with an HIMAC and ten states (Virginia, Florida, Minnesota, North Carolina, Maryland, Michigan, South Dakota, Wisconsin, Iowa, and Utah) had more than half of their hospitals consolidated with a HIMAC. Utah and Iowa were the states with the most MA contract consolidated hospital penetration as of 2024. Interestingly, states on the West Coast and the Northeast that typically have high rates of horizontal consolidation from private equity acquisitions had middle-tier rates of MA contract consolidated hospital penetration (Borsa et al., 2023; Singh et al., 2022; Zhu et al., 2025). This finding may suggest that the hospitals and markets where HIMACs are likely to succeed differ from those that are priority targets for private equity hospital acquisition. Future research should investigate whether independent hospitals that are acquired by private equity are more likely to vertically integrate than those that are acquired by health systems. We found that 12.6% of HIMACs were affiliated with multiple health systems and 28.7% of those that had not been terminated were HPMACs. Hospitals had an average of 4.2 HIMACs, with only 42.0% of hospitals having only one HIMAC.

Flowchart of Identification of Hospital-MA Contract Consolidation.

Characteristics of Hospital-MA Contract Consolidation.

Note. Medicare Advantage (MA); Hospital integrated Medicare Advantage Contracts (HIMAC). The year of first consolidation is the year of the contract effective date of the MA contract from the MA landscape files. The year of the MA contract termination is the year the MA contract no longer appears in the MA landscape files. Hospital-partnered MA contracts are MA contracts that are created through a partnership with an existing MA insurer and a hospital where the parent organization is the MA insurer.

There are 45 HIMACs that were terminated, and therefore their parent organizations are not in the MA contract data and were not included in this calculation. HIMACs are hospital integrated MA contracts. ^These are hospitals that have at least one HIMAC.

(A) State-Level Penetration of MA Contract Consolidated Hospitals in 2015. (B) State-Level Penetration of MA Contract Consolidated Hospitals in 2024.

Discussion

Our study found that more than 2,000 hospitals and 200 MA contracts are vertically consolidated. Our dataset has a similar number of HIMACs as prior studies that used different datasets such as Hedquist et al. (2024; 196 HIMACs in 2022) and Johnson et al. (2017; approximately 113 HIMACs in 2015). In addition, almost a third of these hospitals and over 40% of these MA contracts were first consolidated after 2015. These trends highlight the continued growth of vertical consolidation in MA and the need for more rigorous research using data from the last decade.

The rate of termination of HIMACs is similar to overall MA contract termination rates (Dixit et al., 2024; Meyers et al., 2022). Termination of HIMACs may pose significantly higher risks to enrollees of losing access to care if consolidation is associated with a lower likelihood that a hospital is in-network with other MA plans. Given that HIMACs have been found to be associated with better beneficiary experience, higher star ratings, and better care quality outcomes (Bejarano, Ryan, Trivedi, & Meyers, 2024; Meyers et al., 2020), termination of such plans may lead to worse outcomes. HIMACs, however, tend to enroll healthier beneficiaries who are less likely to be dual-eligible, which raises concerns about whether prior beneficial associations are partly explained by favorable selection (Bejarano, Ryan, Trivedi, & Meyers, 2024; Bejarano, Ryan, Trivedi, Offiaeli, & Meyers, 2024; Meyers et al., 2022). Because there is no official registry of HIMACs, there is a possibility that we fail to capture some terminated contracts in the data sources we assembled, especially if they were terminated over a decade ago.

The current literature has considered HIMACs to be homogeneous. However, we found that nearly a third are HPMACs, MA contracts jointly owned by a hospital and an insurer that also offers non-integrated MA contracts. There are likely substantial differences in the priorities and levels of integration between HPMACs and HOMACs, MA contracts that are entirely owned by hospitals. Though clinical integration and data sharing between hospital and insurer has been highlighted as a key mechanism for the potential success of provider-insurer consolidation, HPMACs are likely to be less likely to engage in such activities (Chen et al., 2009; Orszag & Rekhi, 2020). In the commercially insured market, an insurance partnership between an insurer and health system was found to have no effect on health care utilization, quality, or spending (Garabedian et al., 2025). Interestingly, in qualitative interviews the leaders at both the insurer and health system stated that the insurance partnership was providing benefits to beneficiaries and lowering health care spending. The belief by insurer and health system leaders in this type of consolidation, coupled with the lack of rigorous research, may be the reason for the continued growth of HIMACs even if there is no actual effect on health care outcomes or spending. Past work has found that larger health systems are more likely to start HIMACs (Hedquist et al., 2024), meaning the only effect of this consolidation may, intentionally or unintentionally, be marketing for the hospital and MA contract.

There are also anti-trust concerns with hospital-MA contract vertical consolidation. Primarily, hospitals that own their MA contract may choose to either stop negotiating with or begin demanding higher prices from non-affiliated MA contracts. This can lead to beneficiaries choosing to disenroll from the non-affiliated MA plans if their preferred hospital is not in-network or if the premiums for the non-affiliated MA plans substantially increase from less competitively negotiated higher prices between the consolidated hospital and the non-affiliated MA contract. These phenomena are known as input and customer foreclosure, which has been highlighted as a risk of vertical consolidation in the pharmaceutical market (Gray et al., 2023; Vertical Merger Enforcement at the FTC, n.d.). Specifically, after an insurer acquires a pharmacy benefit manager (PBM), the non-affiliated insurers have to raise premiums due to anti-competitive prices from the rival insurer consolidated PBM (input foreclosure) and the PBM-consolidated insurer no longer negotiates with other non-affiliated PBMs (customer foreclosure), which leads to their foreclosure due to the reduction in business from that insurer. Future research should assess whether a similar dynamic also happens after hospital-MA contract consolidation and how it impacts MA beneficiaries.

Our study and dataset may be limited in several ways. First, although we took a systematic approach to identifying HIMACs, it is possible that there are some active HIMACs that we were not able to find. Second, some HIMACs may have been created and subsequently terminated without appearing in the AHRQ compendium or public MA contract data, and therefore, we were not able to identify them. Third, while the parent organization is a reasonable method of subclassification, there may be different types of partnerships with differing levels of ownership control by the hospital and the MA contract. Future research should attempt to disentangle these functional differences among HIMACs that share a similar structure.

Conclusion

Our study found that there has been continued growth in hospital-MA contract consolidation in the last decade, with geographic variation in trends, and substantial representation of both health plan-owned and hospital-owned subtypes. By providing this comprehensive dataset of HIMACs, there will be a reduction in the barriers to conducting necessary research into this type of vertical consolidation.

Supplemental Material

sj-csv-1-mcr-10.1177_10775587261437553 – Supplemental material for Hospital-Medicare Advantage Vertical Consolidation, 1980 to 2024

Supplemental material, sj-csv-1-mcr-10.1177_10775587261437553 for Hospital-Medicare Advantage Vertical Consolidation, 1980 to 2024 by Geronimo Bejarano, Grace Mackleby, Amal Trivedi, Meredith B. Rosenthal and David J. Meyers in Medical Care Research and Review

Footnotes

Acknowledgements

The authors acknowledge Josephine Roher for her help in verifying the dataset.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This study was funded by Arnold Ventures (DJM). Time for GB was funded by the PD Soros Fellowship.

Supplemental Material

Supplemental material for this article is available online.

Ethical Considerations

This study was deemed exempt from informed consent due to usage of deidentified data by the institutional review board at Brown University.

Data Availability Statement

The hospital-MA contract consolidation dataset is available in the supplement.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.