Abstract

Ethiopia has pursued a manufacturing-led development strategy since the early 2000s, achieving substantial growth and poverty reduction. However, little attention is paid to the environmental costs of these results. Relying on the review of environmental policies and on 22 in-depth interviews with public and private stakeholders, we assess whether the existing command-and-control approach to environmental management is delivering on its promises, and whether there is scope for deploying environmental taxes. Our analysis demonstrates that, despite the implementation of a variety of regulatory measures, environmental management in Ethiopia is substantially ineffective. This is due to a combination of institutional instability, a lack of technical resources at the environmental protection authority, and to the low level of political priority of environmental protection. In this context, a switch to a market-based approach to environmental management would be ineffective, as the lack of political will to enforce environmental regulations is the real issue.

Keywords

Introduction

Ethiopia is a well-known example of a developmental state that over the last two decades aggressively pursued an industrial-led growth strategy with a strong emphasis on the manufacturing sector (Clapham, 2018; Dejene & Cochrane, 2019). This strategy, which focused on promoting the industrialisation of agriculture, on the development of labour-intensive and export-oriented sectors, and on infrastructural expansion, led to double-digit growth rates from 2005 to 2015 and to significant employment creation and poverty reduction (UNDP, 2017; UNIDO, 2018; Vrolijk, 2021). However, it is debated whether past growth levels can be sustained in a context of deteriorating macroeconomic conditions and a worsening security situation (UNDP, 2023), and whether this past growth led to any significant structural transformation (Vrolijk, 2021) or productivity increases (Gebrewolde & Rockey, 2023).

One potential consequence of this development strategy which so far received little attention is its environmental impact on the country’s natural resources (Daley, 2015). Despite the explicit focus on the expansion of manufacturing, a sector whose growth is often associated with increased urbanisation (Gollin et al., 2016; Khan et al., 2021), only 23% of the over 128 million Ethiopians live in urban areas, well below the sub-Saharan Africa average of 43% (World Bank, 2025). 1 It is then not surprising that much of the existing work on Ethiopian environmental issues focuses on resource pressure in rural areas (Wassie, 2020), although a few studies indicate that the impact of industrialisation on water quality is significant and negative (Akele et al., 2016; Kibret & Tulu, 2014; Zinabu et al., 2017). Indeed, recent evidence (Wakeford et al., 2017) indicates that greening industrial processes is not a current priority in Ethiopia despite the country’s commitment to embracing a low-carbon development path, indicating a possible preference for a ‘pollute first, clean-up later’ development model (Azadi et al., 2011). However, given the high vulnerability to climate change of many Ethiopian communities (Bedeke et al., 2020; Mekonnen et al., 2019; Tessema & Simane, 2019), a ‘development first, environment later’ approach might not be a viable option (Rudi et al., 2012).

The two main tools available to policymakers wanting to address the environmental externalities of industrial production are command-and-control (CC) approaches and market-based instruments (MBIs) such as environmental taxes and tradable permits. CC approaches remain more prevalent across low-income countries (Belletti, 2020; Luken & Clarence-Smith, 2019; Occhiali, 2024), despite a substantial agreement in the literature on the fact that MBIs provide stronger behavioural incentives, are more cost-effective, and can contribute to revenue generation (Harrington & Morgenstern, 2006; Moran, 1995; OECD, 2017). One of the main reasons for favouring CC over MBIs when dealing with environmental issues is that the latter are perceived as regressive and complex to implement. While this also somewhat applies to CC approaches, it is true that the proper implementation of environmental MBIs requires the existence of the necessary administrative infrastructures, as well as posing various challenges to policy design and political acceptance (Belletti, 2020; Carter & Cebreiro, 2011; Occhiali, 2024).

Given the suboptimal attention dedicated to the environmental sustainability of the current Ethiopian development strategy, this study aims to understand whether there are mechanisms in place to address environmental issues, whether they are effective, and whether MBIs could provide a useful policy addition. To answer these questions, we rely on the analysis of existing policy instruments addressing environmental issues and natural resources use, and on 22 key informant interviews with officials from the federal and regional governments, as well as the private sector, civil society, and academia.

Our analysis confirms that Ethiopia is currently facing a variety of environmental challenges, many of which are connected to industrial pollution, which is not surprising given its manufacturing-led development strategy. The country has opted for a CC approach, and has since late 1997 promulgated a set of policies covering a variety of topics, from water resource management to hazardous waste disposal. However, these policies appear widely inadequate, due to the ineffectiveness of the implementing agency, which has been subjected to extreme institutional instability, as well as lacking both technical and human resources, and the deprioritisation of environmental considerations against an economic growth imperative. While MBIs might be seen as addressing some of the current shortcomings, as long as tackling environmental problems does not become a stronger political priority and the necessary agencies are capacitated, they will likely suffer from the same issues of the existing CC approach. This study contributes to two distinct literatures, that on environmental issues and their management strategies in Ethiopia (Akele et al., 2016; Kibret & Tulu, 2014; Wakeford et al., 2017; Wassie, 2020; Zinabu et al., 2017) and that on the feasibility of CC and MBI approaches to environmental management in low-income countries (Belletti, 2020; Cottrell & Falcão, 2018; Granger et al., 2021; Occhiali, 2024).

The paper proceeds as follows. The next section discusses the related literature, while the following one briefly describes the study methodology. We then move onto setting the context by first outlining the most pressing environmental issues in Ethiopia and then describing the current legal and institutional framework to deal with them. After this, the next section discusses the effectiveness of the current approach to environmental management, covering the capacity of existing institutions and the existence of political will to enforce environmental standards. Subsequently, we discuss whether – given the described legal set-up, existing capacity, and political will – MBIs would fare any better than the current CC approach, while the final section concludes.

Related Literature: Command-and-Control versus Market-Based Instruments for Environmental Management

Command-and-Control (CC) approaches and MBIs are the most widely used tools to address environmental issues connected with production and consumption activities. In CC approaches, the government sets guidelines for various industrial sectors regarding maximum allowable levels of pollution or emission – and in extreme cases mandates specific production technologies – as well as fines for economic agents not respecting them. On the other hand, MBIs aim to provide economic agents with various incentives to decrease the environmental damage associated with their consumption or production, without mandating explicitly what the desired pollution level is (Harrington & Morgenstern, 2006; Karp & Gaulding, 1995; Moran, 1995; OECD, 2017). Which of the two approaches yields the best results in the most effective way has been the subject of frequent debate, and the answers depend on a variety of factors. Theoretically, a government with perfect information on all implemented production technologies, output levels, and without any bias could achieve an environmental optimum through a CC approach (Harrington & Morgenstern, 2006; Moran, 1995). However, in practice, this is never the case – regulators cannot possess perfect information on the myriads of production techniques, so blanket environmental criteria are applied regardless of the technology in use, increasing administrative costs (Kostka, 2016; OECD, 2017; Sinclair, 1997; Stavins & Whitehead, 1992). Hence, CC approaches on their own are unlikely to ever achieve an optimum environmental outcome.

This shortcoming is absent with MBIs – in this case, the government sets a cost for different polluting activities in the form of a tax, and it is left to each economic agent to determine what their optimum level of pollution is (Harrington & Morgenstern, 2006; Moran, 1995). Here lies the main potential of MBIs: each agent’s optimum might well lie below the maximum level of pollution mandated by any CC approach, and MBIs provide an incentive to achieve this optimum which is absent in the former. This incentive to minimise the – now internalised – cost of pollution is exactly the reason why MBIs encourage both innovation and technology uptake, which in turn can contribute to further lowering abatement costs (Cai & Li, 2018; Harrington & Morgenstern, 2006; Jaffe et al., 1995; Milne, 2011). On the other hand, optimal implementation of MBIs also requires substantial administrative and policy-creation capacity, and they are also more likely to elicit political opposition than CC measures (Belletti, 2020; Carter & Cebreiro, 2011).

The necessity of possessing significant administrative and policy capacities shows that the comparison between CC and MBIs is to an extent spurious, as which of the two approaches is optimal depends on a country’s institutional and socioeconomic characteristics (Tan et al., 2022). Additionally, in many cases, the optimal way of addressing environmental issues is through a combination of both CC and MBIs, which is what most countries actually pursue (Lamperti et al., 2020; Mansfield, 2006; Oltra & Saint Jean, 2009; Sinclair, 1997). This is because a CC approach can deliver results more quickly than MBIs, which is relevant when damage from polluting activities must be stopped right away, while the latter are usually implemented sequentially with raising rates (Harrington & Morgenstern, 2006; Rafique et al., 2022; Zatti, 2020). Ultimately, CC approaches have a long history in both high- and low-income countries, and remain predominant in the latter, where the existence of strong environmental laws and standards can pave the way for the successful deployment of MBIs (Stavins & Whitehead, 1992).

Very little is known about whether the current institutional and economic characteristics of Ethiopia make it more suitable for CC or MBI approaches, or about the deployment of MBIs such as environmental taxes, or their effectiveness. Mekonnen et al. (2013) assessed the regressivity of the current taxation of fossil fuels, one of the common arguments against this type of environmental taxation, finding that the impact varies across fuel types and their use. Fitiwi (2014) investigated whether Ethiopian tax, investment, and environmental laws prescribe the use of MBIs, concluding that very little environmental tax provisions existed at the time and that they could play an important role in protecting the environment. Gebregiorgis (2018) achieved a somewhat similar conclusion, although they focused only on environmental taxes which could be implemented by the Addis Ababa City Administration, adding that only a subset of existing environmental taxes would be feasible given existing environmental expertise and institutional and administrative set-up. Finally, Wakeford et al. (2017) maintain that the current environmental regulatory set-up in Ethiopia is not incentivising firms to innovate production processes to decrease their environmental impact, which could be provided by introducing a carbon tax.

Methodology

Our study relies on a combination of desk reviews of published materials, legislative instruments, and key informant interviews. First, we reviewed a variety of legal documents, listed in Table A1 in the Appendix, in order to understand the existing support for environmental protection, and whether this includes MBIs. Second, we carried out 22 key informant interviews with both public and private stakeholders. Amongst public stakeholders, we interviewed three officials from the Federal Environmental Protection Authority (EPA), two from the Addis Ababa City Administration EPA, and one each from the Ethiopian Energy Authority, the Industrial Park Development Corporation, the Ethiopian Forestry Development, the Ministry of Revenue, the Ministry of Finance, the Ministry of Transport, the Addis Ababa City Administration Fiscal Policy Division, the Hawassa EPA, and the Lake Tana and Other Water Bodies Protection and Development Agency. Amongst private stakeholders, we interviewed the managers of four factories (cement, textile, malt and leather), two members of local civil society organisations (CSOs) dealing with environmental issues, and two members of Addis Ababa University. All interviews were conducted in person during early 2023 and lasted between an hour and an hour and a half. Although the exact topics covered varied depending on the stakeholders interviewed, the general aim was to obtain information about existing environmental issues, about policy tools in place to tackle them either through a CC approach or through MBIs, whether there are mechanisms for effective enforcement of these tools, and whether there exists political desire to expand environmental protection through environmental fiscal reforms. Additionally, we verified information on existing environmental fees and charges given the scarcity and paucity of available data, as well as discussing the destination of the revenue collected through them.

Although we maintain that the information obtained through the interviews and document reviews allows us to paint a fairly accurate picture of the current approach to environmental management in Ethiopia, some limitations must be acknowledged. First, many of the public and private stakeholders interviewed were in managerial positions, so we cannot exclude the existence of some conflicts of interest in the information reported. However, as will become apparent, given the tone of the opinions expressed, this does not appear to be a significant concern. Second, it would have been ideal to obtain some hard figures about the existing collection of revenue from different environmental charges and fees by federal and regional authorities, but despite numerous requests, we did not have any success in accessing this data, so a more thorough quantitative investigation is left for future studies. Third, while carrying out a survey of industrial actors in polluting sectors was outside the scope of the study, it would have been interesting to obtain a more representative view of their experience with complying with existing regulations.

Context: Current Environmental Issues in Ethiopia

Given the abovementioned manufacturing-led development strategy, it will not come as a surprise that all interviewees stated that most environmental issues arise from industrial activities. Specifically, leather, textiles, cement, and food-processing companies were all identified as significantly contributing to various environmental problems. 2 To start with, most of these industries – especially tanneries, textiles, and breweries – discharge a relevant amount of process-water into nearby rivers or lakes. 3 This process-water is allegedly often either untreated or very poorly treated due to a combination of low environmental standards and lack of enforcement – most manufacturing firms do not possess wastewater treatment plants, and even those which do might decide not to use them. Consequently, agricultural crops relying on these water bodies for irrigation show a build-up of heavy metals dangerous to human health, with frequent biodiversity losses in rivers and lakes. 4 Cement and steel factories are also both highly reliant on coal for their operations, hence contributing greatly to air pollution, especially considering the low energy efficiency of their machineries. 5 Poor disposal of chemicals used in various industrial processes is also recognised as an increasing hazard. 6

Many of these manufacturing industries are based in industrial parks, which have been a prominent feature of the Ethiopian development strategy (UNIDO, 2018). Most of these industrial parks are located in close proximity to major urban centres, as this guarantees access to vast labour pools and reduces transport cost to important markets. However, this also implies that environmental pollution is increasing in areas that are more densely populated, with direct consequences on human health. 7

Environmental issues in urban and peri-urban areas are compounded by the main source of non-industrial pollution – an ageing fleet of mostly second-hand private vehicles. 8 While air pollution from traffic congestion is a common issue across sub-Saharan Africa (Granger et al., 2021; Occhiali, 2024), two factors contribute to make it particularly egregious in Ethiopia. First, fuel standards in Ethiopia are lower than in most other low-income countries, with much higher sulphur concentrations than those found in neighbouring countries. 9 Second, Ethiopia does not currently apply any limit to the age of vehicles to be imported, although a ban on any vehicle older than five years has long been under discussion (UNECE, 2022). 10 Additionally, poor management of waste from households’ consumption is also becoming increasingly problematic in urban areas, encroaching on the quality of sewerage management, and has been identified as a priority area to address. 11

Although they were not given the same relevance during the interviews, the existence of issues in rural areas was also recognised. Limited regulation currently exists on the use of pesticides, herbicides, fertilisers, and chemicals used in agriculture and floriculture, all of which can be dangerous for the environment and human health. 12 Industrial mining also create environmental concerns, and artisanal miners rarely seek any authorisation prior to commencing operations, with both of these activities leading to significant degradation of the environment. 13

Context: What Instruments Currently Exist to Tackle These Issues?

The constitution of the Federal Democratic Republic of Ethiopia (1995) grants all citizens the right to a clean and healthy environment, as well as establishing that they should be compensated in cases in which they are adversely affected by government policies (article 44). Additionally, the constitution squarely puts the responsibility of ensuring that project implementation does not affect the environment on the government’s shoulders (articles 89 and 92). Given Ethiopia’s federal nature, these articles should be read in relation to both the federal and regional governments, and article 50/9 of the constitution does indeed delegate the power to implement environmental protection activities to regional states. Accordingly, a Federal EPA was established in the same year (Proc. 9/1995), and all regional states were mandated to establish equivalent bodies.

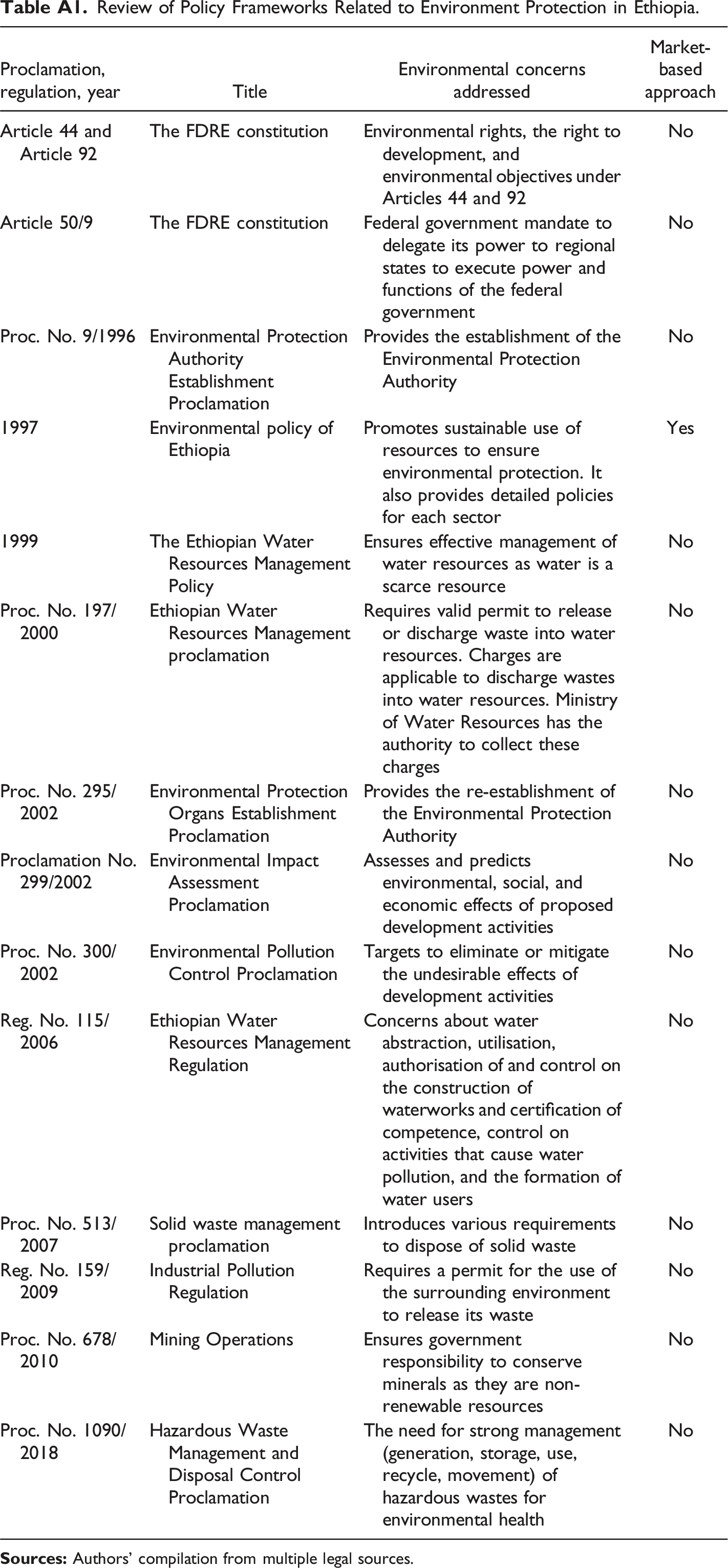

A series of further proclamations and policies were subsequently promulgated by the federal government to deal with general and sector-specific matters. Interestingly, the first policy ever promulgated on the topic in 1997 already contained provisions for the use of MBIs: ‘Market failures with regard to the pricing of natural, human-made and cultural resources, and failures in regulatory measures shall be corrected through the assessment and establishment of user fees, taxes, tax reductions or incentives’ (Federal Democratic Republic of Ethiopia, 1997). However, of the various legislations dealing with environmental issues passed since the introduction of this initial policy, 14 only one, regarding water resource management, explicitly referred to the possibility of introducing tax or price mechanisms to deal with resource scarcity. 15 All other matters, from the disposal of urban and hazardous waste to the management of industrial pollution, required instead the obtaining of permits from the federal or a regional EPA. All EPAs are jointly in charge of setting environmental standards, providing various licences, and monitoring and evaluating production processes, most importantly through the evaluation of environmental impact assessments (EIAs), made compulsory for all development activities in 2002 (Proc. No 295). When industrial actors are found to be non-compliant with the standards established, they are charged a variety of fines, and can be closed until they are capable of respecting existing standards – which is the very definition of a CC approach. 16

Nonetheless, there are a few federal measures that at face value could be considered environmental taxes. For example, there is an excise tax on used vehicles, with rates varying depending on engine size, which was introduced in equal measure for environmental and for revenue reasons. 17 Similarly, while there is a small fuel levy collected from petrol stations across the country, this has been introduced to provide funding for road maintenance rather than to disincentivise fuel consumption. 18 A final example is a recently introduced royalty on charcoal production from forest resources, which rather than regulating has simply legalised 19 one of the economic activities more strictly connected to deforestation (Tegegne et al., 2016). All these instruments at most qualify as environmentally related taxes, that is, taxes levied on environmental bads or on environmentally detrimental activities for the sole purpose of collecting revenue (Cottrell & Falcão, 2018), supporting the claim made by one interviewee that ‘no direct environmental tax policy currently exists in Ethiopia’. 20

Regional states also possess the power to introduce charges, fees, and taxes for activities taking place within their boundaries. For example, the Addis Ababa City Administration collects waste management fees, charged as a proportion of household water consumption directly on their utility bills. However, these fees are nominally insignificant due to high water subsidisation, and consequently not directly used to fund waste management. All other existing charges related to various types of pollution take the form of penalties for failure to respect existing standards, and are hence better classified as a CC measure. 21 This is not surprising – as mentioned above, all regional states have been mandated to establish their own EPA, so that a CC approach to environmental issues is deeply embedded across the country. For example, the Addis Ababa City Administration commissioned a study on environmental tax potential, as these measures can ‘increase the city’s revenue collection and reduce environmental pollution’, but whether its findings will be implemented any time soon remains an open question. 22 Conversely, the agency in charge of preserving Lake Tana in the Amhara Region is looking at the introduction of payments for ecosystem services, as it feels that approach is more in line with current government priorities than the introduction of compulsory tax payments. 23

Discussion: Effectiveness of the Current Approach to Environmental Management

As we have seen, while Ethiopia might not have implemented any proper environmental tax, it does have a variety of policies and proclamations enacted with the explicit scope of managing the environmental consequences of many economic activities. Despite this, there was a wide agreement amongst interviewees with a variety of different backgrounds that these policies are not particularly effective in protecting the environment from the most detrimental effects of a manufacturing-led development strategy. 24 Two main sets of issues, which we will address in turn, determine the ineffectiveness of the current CC approach: a lack of institutional and technical capacity in the EPA, and the absence of the necessary political will to enforce environmental regulation in the government at large.

EPA Institutional History and Technical Capacity

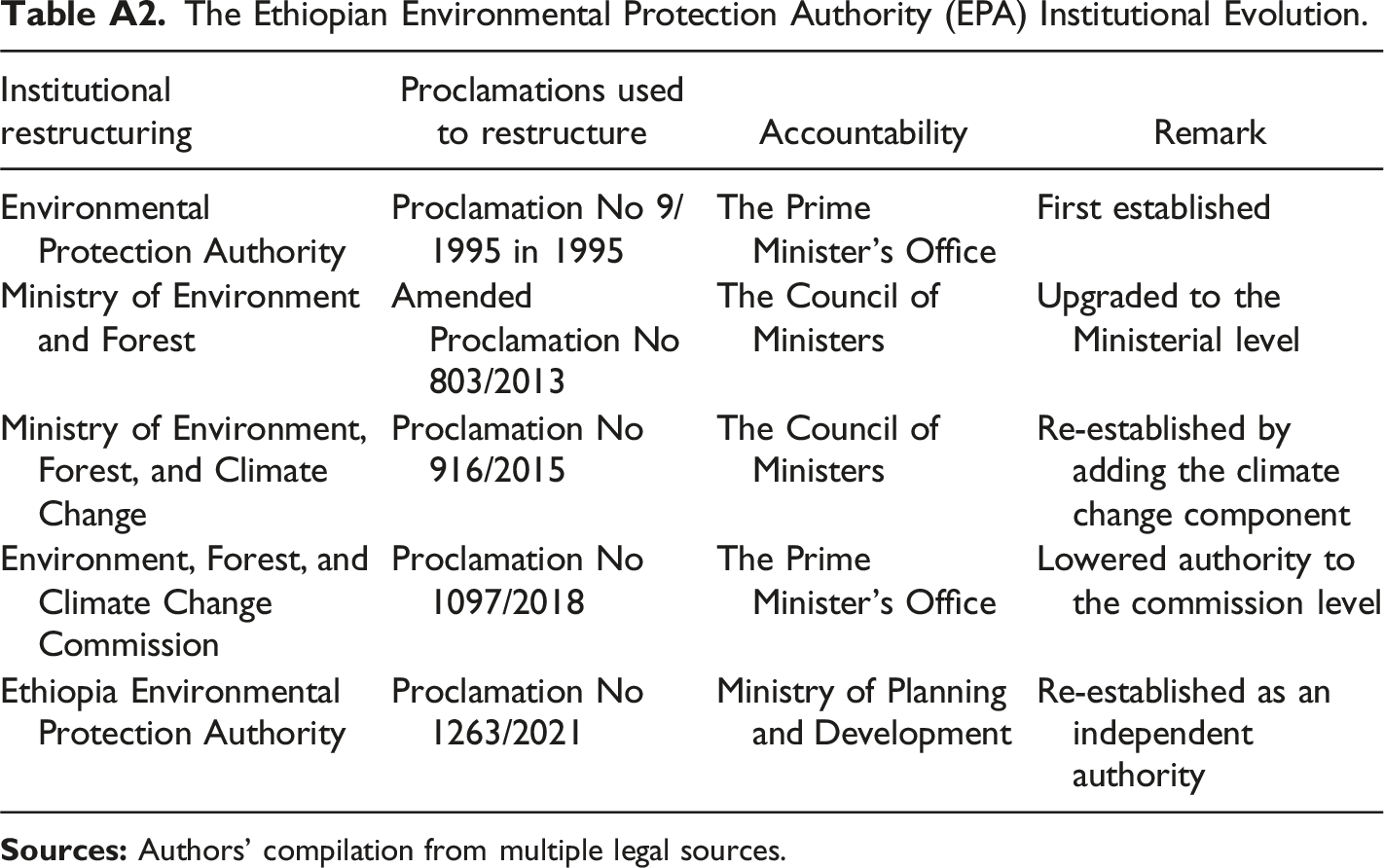

Since its establishment in 1995, the EPA has been subject to a significant number of institutional restructurings (Table A2). Soon after its creation, it was transformed into the Ministry of Environment and Forest; to then be re-established as an autonomous body in 2002 (Proc. 295/2002) and subsequently changed back to the Ministry of Environment and Forest in 2013 (Proc. 803/2013). The ministry was given an additional mandate on climate change in 2015 (Proc. 916/2015), to then be downgraded to a Commission in 2018 (Proc. 1097/2018), and finally returned to its original status of EPA in 2021 (Proc. 1263/2021). While all of these changes were implemented to improve the effectiveness and political relevance of environmental management, the effect achieved was quite the opposite. As a consequence of this constant restructuring, the actual prioritisation of policy, regulatory, and enforcement functions was subject to frequent changes, as was the actual mandate of the organisation itself. Organisational instability also brought a high staff turnover, both across top management and for various sectoral experts, so that the current EPA has very little institutional memory, and the projects pursued reflect the interests of the most recently hired officials. 25

These frequent reorganisations had three additional consequences. First, attention was drawn away from the need to update and reform the current environmental standards. While there is an array of policies to address a variety of environmental issues, many of them have been in place for well over a decade without ever being updated, despite great changes in the industrial practices, rate of urbanisation, and general economic structure. 26 The best practice would be to revise these standards every few years to account for these changes and for a better understanding of the potential hazards of various substances, but in the current system there is no provision for revising these policies at any given interval. 27 Consequently, there are various types of pollutants for which no regulation exists, or industrial sectors that have emerged since then but are not covered by any policy – simply put, ‘[e]xisting regulations and standards are not effective’ 28 as ‘[t]here are no sector-specific emission standards…old standards exist but are not stringent’. 29

Second, institutional fora to coordinate all actors active in the sector – such as federal and regional EPAs, federal ministries, private sector representatives, CSOs, and academia – have historically been absent. 30 One attempt to launch a National Environmental Rights Forum to bring at least some stakeholders together – with the notable exclusion of the Ministry of Revenue and the Ministry of Finance – was made in 2022, but this group met only once, without any clear indication of whether more meetings would take place. 31 While smaller fora exist – the Hawassa EPA organises a meeting with regional actors, and so do CSOs working on energy access 32 – creating a regular space for all stakeholders to flag common issues and share possible solutions seems highly desirable. 33 However, given that coordination is currently lacking even amongst government institutions, 34 and given the frequent restructuring of the EPA, it is not at all clear whether enough commitment exists to establish well-structured fora for sharing experiences and suggestions. 35

Third, both the federal and regional EPAs currently suffer from a significant lack of technical capacity, compounded by suboptimal testing facilities and a position that allows for significant rent-seeking opportunities. This point was made quite strongly by private sector interviewees, who stated that: ‘Government regulatory authorities should organise themselves with enabling systems, technology, and human technical capacity… the way laboratory tests are conducted is not right, not transparent, and they have limited capacity’.

36

‘The regulatory agency has limited technical, infrastructural, and human capacity… [The] existing monitoring authority audits factories irregularly, only when communities file complaints’.

37

‘The Addis Ababa EPA had a well-equipped laboratory a couple of years ago. But now, there is no laboratory equipped with reagents, technology, and technical personnel. Thus, the regulatory bodies are not capable to control environmental pollution… On the one hand, the experts who are undertaking the EIA study often cook the study without going to the field or without undertaking all the necessary tests. On the other hand, the regulatory authority approves defective EIA because they have affairs with the studying firms’.

38

To an extent, complaints on the capacity of a regulatory body from those being regulated should be expected. However, almost the exact same considerations were made by officials from both the Addis Ababa EPA 39 and the federal EPA, 40 lending credibility to the existence of significant capacity gaps in the main institutions in charge of the country’s CC approach. 41

Political Will and Enforcement

While there are various reasons for the presence of these capacity gaps, one of the most important is that ‘[t]he sector is being led by political appointees rather than professionals’.

42

Indeed, as we shall shortly see, several interviewees from state institutions, civil society, and the private sector stressed different aspects of how and why the political approach towards the management of environmental issues influences its effectiveness, which could be summarised by the fact that: Some [government stakeholders] think environmental conservation is a luxury as we are living in a poor country. We don’t compromise economic development for the sake of environmental protection.

43

This position was reflected in an interview with an official from the Ministry of Finance, who recognised that in Ethiopia ‘environmental, humanitarian, and labour standards are deliberately made lower to attract investors’ and that ‘environmental protection is not on the top list agenda of government stakeholders. That is why existing environmental standards and regulations are not effective’. 44 Similar comments were made by other interviewees from both the private and public sector, 45 demonstrating that this is a view shared across different segments of society. While the lower prioritisation of environmental protection against investment attractiveness certainly contributes to institutional instability and lack of capacity, it also results in further consequences as demonstrated by the allegation that ‘regulatory bodies are reluctant to enforce environmental compliance on international investors’. 46

However, from various interviews, it appears clear that insufficient enforcement of existing legislation does not only apply to international investors, and is on the contrary one of the biggest obstacles to increasing environmental sustainability in the country. 47 In fact, one of the private stakeholders interviewed stated quite openly that the wastewater treatment they have in place is ‘not up to the required standards – the cost of treatment is too much’ and that the ‘regulatory body of the government is negligent in taking appropriate action’. 48 Indeed, it seems that enforcement often happens only when prompted by affected communities seeking compensation, with the latter being randomly determined rather than based on an inventory of the damages caused. 49

In part, this could be due to the fact that the EPA can only take administrative actions, which, in the words of an official from the federal EPA, ‘include taking the investment licence, giving warnings – oral and written, and providing feedback [on the action taken]’. 50 Any more stringent measure requires the escalation of potentially criminal behaviours and acts to the Ministry of Justice. But there exists no environmental court in Ethiopia, so environmental cases are rarely brought in front of a judge without the direct involvement of CSOs. 51 Taken together, this approach to environmental enforcement has led to a situation in which ‘[t]here is a lack of accountability from the top to the grassroots level’. 52

Discussion: Is the Ground Ripe for MBIs?

The current CC approach to environmental management in Ethiopia does not appear to be particularly effective due to a combination of institutional instability, lack of technical capacity, and suboptimal enforcement explained by scarce political interest in conservation. One of the potential solutions to this situation could be a switch to a market-based approach. This was already envisaged in the first environmental policy promulgated in the country in cases of ‘failures in regulatory measures’ (Federal Democratic Republic of Ethiopia, 1997), which arguably describes the current situation well. While the introduction of MBIs could indeed play a positive role, they definitely do not represent a silver bullet, and a few obstacles are likely to exist to their successful deployment.

Indeed, while some see the future introduction of environmental taxes as ‘a must’, there is also recognition that little tangible discussion is currently taking place in Ethiopia, with mentions of this solution from politicians more likely to represent posturing than genuine commitment. 53 This is especially the case for carbon taxes, which are widely seen by government interviewees as unfeasible and as holding very little potential, both under a revenue and an environmental prospective, and hence not being actively discussed. 54 Nonetheless, other environmental tax instruments might help addressing various issues, from industrial pollution to household waste generation, while contributing to mobilising some revenue. 55 Indeed, even just discussing their introduction might help to highlight the extent of existing and upcoming environmental damages created by industrial pollution. 56 Additionally, the revenue authority could easily start collecting any new tax from enterprises, as the system they have in place is seen as quite effective, while the collection of charges from households will likely lie with city authorities, which are better positioned to reach them. 57

However, environmental taxes are perceived to be a hard sell to international investors, greatly decreasing their political appeal given the existing manufacturing-led development strategy, 58 and there was in fact opposition to the idea by both private and public stakeholders. 59 Interestingly though, many interviewees recognised that the government has different avenues for making environmental tax measures more attractive, from careful sensitisation strategies to earmarking revenue for environmental protection and rehabilitation. 60 On the other hand, doubts were raised about the opportunity to reduce the taxation of capital and labour concurrently with the introduction of environmental taxes – the often cited double dividend – as this might put domestic revenue mobilisation at risk. 61 Despite these nuances, there is currently little political interest in addressing environmental concerns, and equally little advocacy for these matters to become more prominent, so that substantial changes in the short run are unlikely. 62

The additional and final obstacle to the deployment of MBIs in Ethiopia has already been touched upon: the critical lack of technical infrastructure and human capacity to assess existing environmental practices. For environmental taxes to really provide an incentive for abatement, the tax rate needs to be high enough to induce a behavioural change, as too low a rate will leave production processes unchanged while slightly increasing revenue collection, which should not be the point of these measures. 63 There is little doubt amongst the interviewees that the country’s EPAs do not currently possess either the data on production processes or the technical capacity to determine these rates, 64 which hence will likely lead to environmental taxes as ineffective as the current CC approach.

Conclusion

Ethiopia has been pursuing a manufacturing-led development strategy since the early 2000s, achieving substantial growth rate and poverty reduction for over a decade (UNDP, 2017; UNIDO, 2018), although with mixed evidence on significant structural change (Vrolijk, 2021). While various facets of the Ethiopian development strategy have been studied (Clapham, 2018; Dejene & Cochrane, 2019), one aspect that has received relatively little attention is the environmental impact of an industrial development trajectory which seems to follow a ‘pollute first, clean-up later’ approach (Azadi et al., 2011). Indeed, a few studies indicate that significant industrial pollution has been taking place (Akele et al., 2016; Kibret & Tulu, 2014; Zinabu et al., 2017), with various negative consequences given the country’s high vulnerability to climate change (Bedeke et al., 2020; Mekonnen et al., 2019; Tessema & Simane, 2019). Our study focuses on Ethiopia’s environmental management strategy, debating whether the existing CC approach is delivering on its promises and whether MBIs could be more effective in tackling environmental issues. Based on the review of legal documents and in-depth interviews with 22 stakeholders from the public and private sector, we argue that the current environmental regulations do little to promote sustainable growth in the country.

From a legal perspective, the environmental policies promulgated since the enactment of the constitution in 1995 represent a solid bedrock, as the overarching environmental policy of 1997 envisaged the possibility of both regulatory and market-based measures. However, as only one of the policies that have been promulgated since includes MBIs, there is a demonstrated lack of interest in using these tools for environmental management. While a few federal taxes might seem to address environmental concerns, most were introduced for revenue reasons, so that they would better qualify as environmentally related (Cottrell & Falcão, 2018). Similarly, regional states, which are also competent for environmental management, have mostly relied on CC approaches, although some have introduced waste management fees or are considering introducing payments for ecosystem services.

While CC measures have been widely adopted throughout the world (Stavins & Whitehead, 1992) and might prove best suited to countries with particular socioeconomic characteristics (Kostka, 2016; Tan et al., 2022), they are currently widely ineffective in Ethiopia. This is due to three main interrelated issues. First, the federal EPA, the main agency in control of setting environmental standards and monitoring their implementation, has been subject to extreme institutional instability, changing its organisational structure six times between 1995 and 2021 (see Table A2 in the appendix). This led to a high turnover amongst both its senior and junior staff, which in turn caused the loss of any institutional memory and a constant reprioritisation between policy, regulatory, and enforcement functions. As a consequence, current standards and regulations are significantly outdated, and the EPA has no convening power, which is a relevant issue in a context in which parallel institutions exist at the state level and environmental issues are not a priority. Second, both federal and states’ EPAs suffer from a significant lack of technical and human capacity, leading to insufficient scrutiny of EIAs, to irregular environmental audits, and to ample room for rent-seeking behaviour. Third, and possibly most important, environmental protection is seen as a luxury that the country can ill-afford when trying to attract foreign investments. Consequently, even the lax existing standards are seldom enforced, and potentially criminal behaviour is rarely prosecuted, leading to a climate of unaccountability.

Given this context, it is highly questionable whether a stronger focus on MBIs might result in improving existing environmental issues. On the one hand, the combination of both the CC approach and MBIs has historically led to the best outcomes (Lamperti et al., 2020; Mansfield, 2006; Oltra & Saint Jean, 2009; Sinclair, 1997), the Ethiopian Revenue Ministry is capable of collecting its due from businesses, and even just discussing whether these measures could be attractive might help in highlighting current issues. On the other hand, the most significant problem appears to be the lack of any political interest in seriously tackling environmental degradation, without which it is unlikely that the required resources will be directed towards capacitating whichever agency could be put in charge of defining environmental tax policies.

Indeed, our study highlights that while some of the existing regulations is undoubtedly dated, the current situation was brought about by a failure of will rather than a failure of policy. Consequently, those interested in promoting a more sustainable growth in the country should focus on ensuring that the EPA is capacitated to carry out its mandate from a technical and human resource perspective, as well as being granted a modicum of institutional continuity. However, for this to be the case, there needs to be a fundamental reassessment of the value of preserving environmental quality. Lacking this, given the existing pollution rates, the only option available seems to be relying on the existence of a ‘later’ in which Ethiopia will have the resources to ‘clean-up’ – and that the environment will be healthy enough to survive up that point.

Footnotes

Acknowledgements

The authors would like to thank all stakeholders interviewed for this project for their availability, and referees from the International Centre for Tax and Development for their comments on an earlier draft of this paper.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by funding from UK Aid [300211-101], the Bill & Melinda Gates Foundation [OPP1197757], and the Norwegian Agency for Development Cooperation [QZA-17/0153].

Data Availability Statement

This paper only relies on interviews – anonymised transcripts can be accessed from the authors upon request.

Notes

Appendix

Review of Policy Frameworks Related to Environment Protection in Ethiopia.

Proclamation, regulation, year

Title

Environmental concerns addressed

Market-based approach

Article 44 and Article 92

The FDRE constitution

Environmental rights, the right to development, and environmental objectives under Articles 44 and 92

No

Article 50/9

The FDRE constitution

Federal government mandate to delegate its power to regional states to execute power and functions of the federal government

No

Proc. No. 9/1996

Environmental Protection Authority Establishment Proclamation

Provides the establishment of the Environmental Protection Authority

No

1997

Environmental policy of Ethiopia

Promotes sustainable use of resources to ensure environmental protection. It also provides detailed policies for each sector

Yes

1999

The Ethiopian Water Resources Management Policy

Ensures effective management of water resources as water is a scarce resource

No

Proc. No. 197/2000

Ethiopian Water Resources Management proclamation

Requires valid permit to release or discharge waste into water resources. Charges are applicable to discharge wastes into water resources. Ministry of Water Resources has the authority to collect these charges

No

Proc. No. 295/2002

Environmental Protection Organs Establishment Proclamation

Provides the re-establishment of the Environmental Protection Authority

No

Proclamation No. 299/2002

Environmental Impact Assessment Proclamation

Assesses and predicts environmental, social, and economic effects of proposed development activities

No

Proc. No. 300/2002

Environmental Pollution Control Proclamation

Targets to eliminate or mitigate the undesirable effects of development activities

No

Reg. No. 115/2006

Ethiopian Water Resources Management Regulation

Concerns about water abstraction, utilisation, authorisation of and control on the construction of waterworks and certification of competence, control on activities that cause water pollution, and the formation of water users

No

Proc. No. 513/2007

Solid waste management proclamation

Introduces various requirements to dispose of solid waste

No

Reg. No. 159/2009

Industrial Pollution Regulation

Requires a permit for the use of the surrounding environment to release its waste

No

Proc. No. 678/2010

Mining Operations

Ensures government responsibility to conserve minerals as they are non-renewable resources

No

Proc. No. 1090/2018

Hazardous Waste Management and Disposal Control Proclamation

The need for strong management (generation, storage, use, recycle, movement) of hazardous wastes for environmental health

No

The Ethiopian Environmental Protection Authority (EPA) Institutional Evolution.

Institutional restructuring

Proclamations used to restructure

Accountability

Remark

Environmental Protection Authority

Proclamation No 9/1995 in 1995

The Prime Minister’s Office

First established

Ministry of Environment and Forest

Amended Proclamation No 803/2013

The Council of Ministers

Upgraded to the Ministerial level

Ministry of Environment, Forest, and Climate Change

Proclamation No 916/2015

The Council of Ministers

Re-established by adding the climate change component

Environment, Forest, and Climate Change Commission

Proclamation No 1097/2018

The Prime Minister’s Office

Lowered authority to the commission level

Ethiopia Environmental Protection Authority

Proclamation No 1263/2021

Ministry of Planning and Development

Re-established as an independent authority