Abstract

In contemporary times, developed economies are adopting environmentally friendly initiatives such as green finance and energy efficiency. However, the factors affecting energy efficiency are widely explored, and green finance remains overlooked in the empirical literature. The present research examines the drivers of sustainable green finance in OECD economies during 2004–2021. The study uses several panel diagnostic tests and validates the mixed integration order of the variables. Still, the long-run equilibrium relationship is valid between financial inclusion, energy efficiency, human capital, foreign trade, composite risk, and green finance. Using panel autoregressive distributed lag model, the study found that financial inclusion, energy efficiency, foreign trade, and composite risk significantly improve green finance in the long run. However, only energy efficiency is effective in the short run. On the other hand, human capital exhibits a significant adverse influence on green finance. The long-run results are robust due to the significant estimates offered by panel dynamic ordinary least square. Besides, there exist one-way and two-way causal associations between variables. The study recommends improving the financial sector performance to enhance financial inclusivity, increase investment in the energy efficiency sector, and encourage trade in environmentally friendly initiatives.

Keywords

Introduction

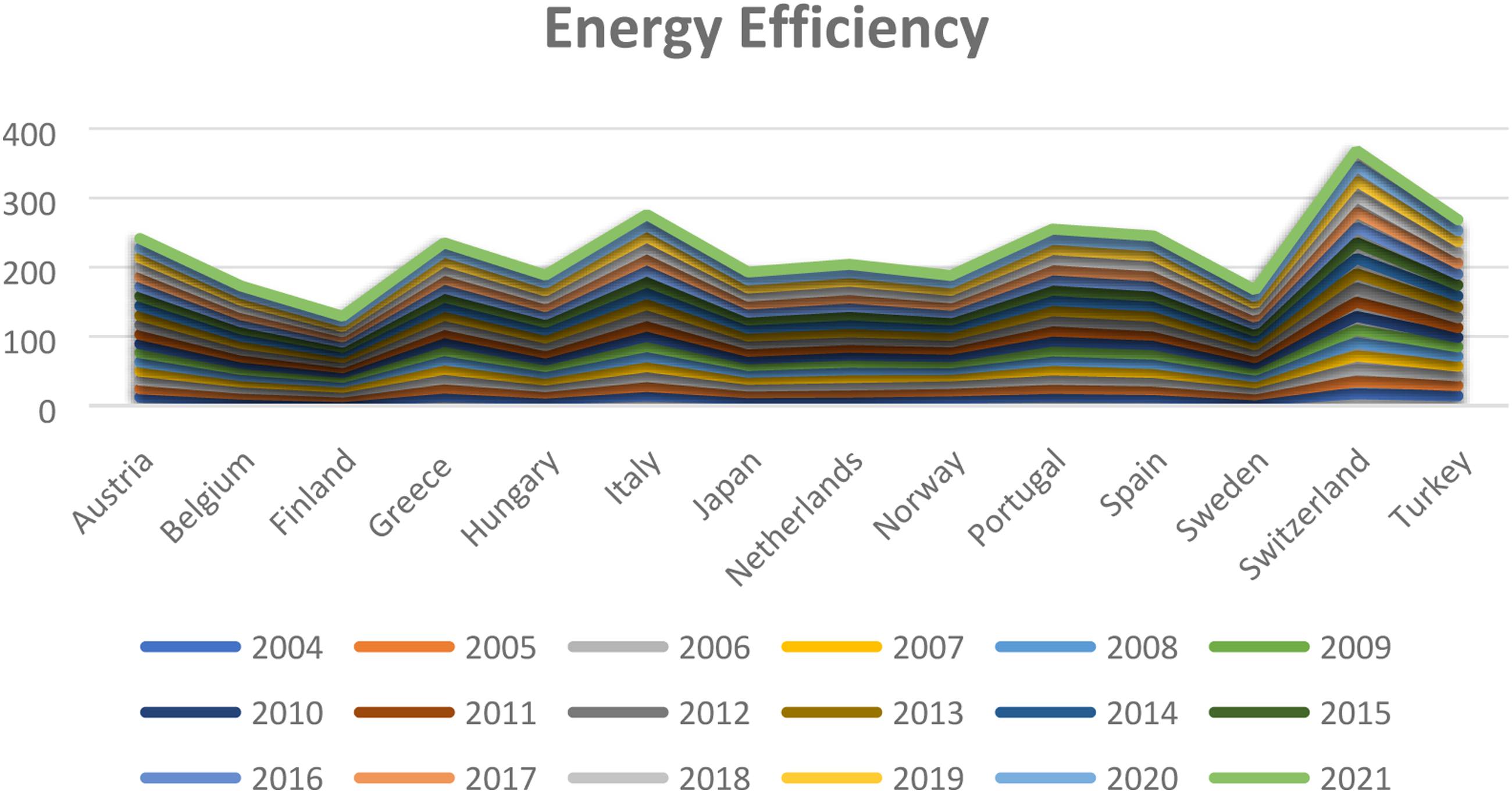

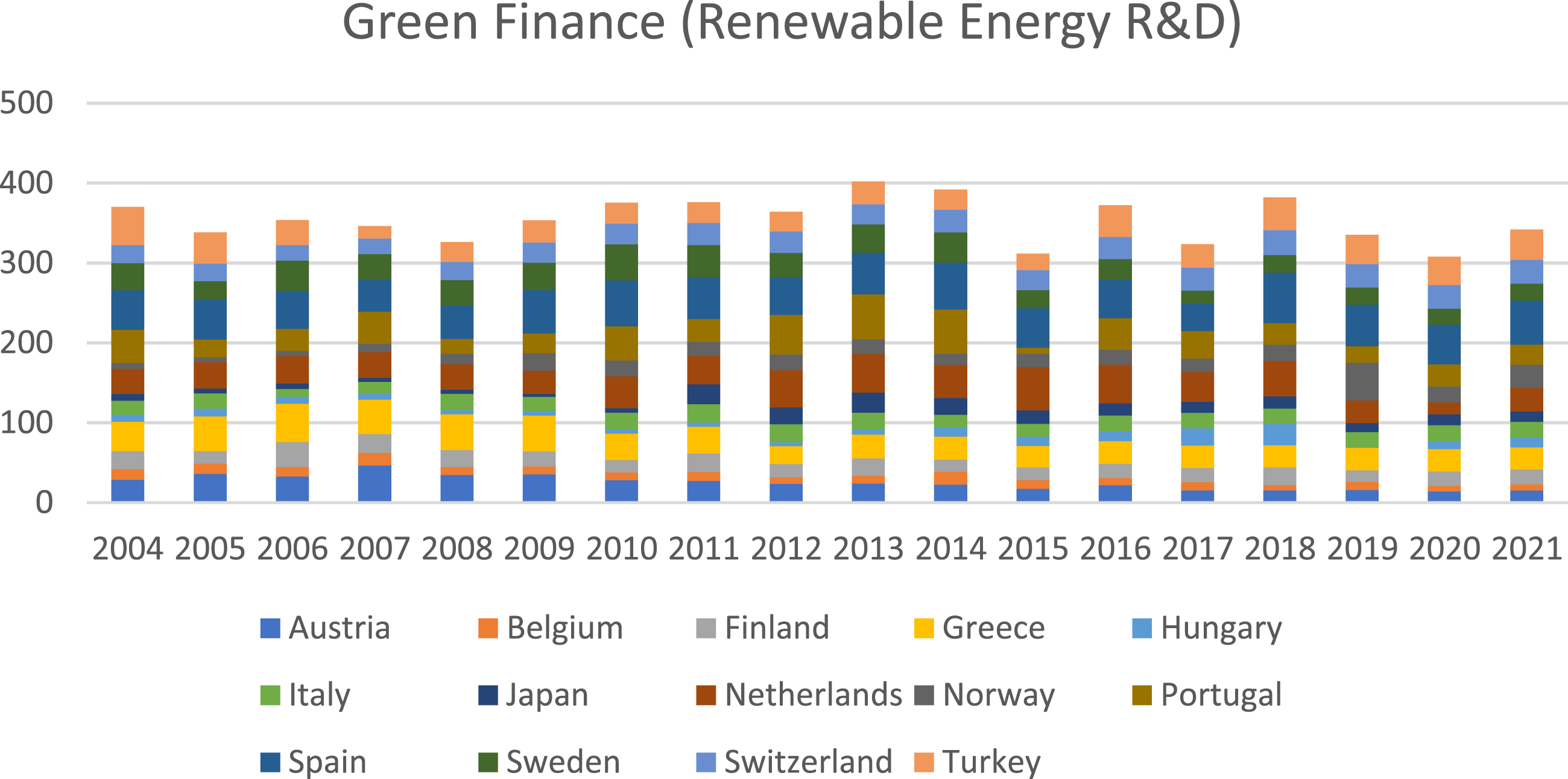

The integration of financial inclusion and green finance is a critical focal point within the framework of OECD countries. As countries progressively align themselves with sustainability objectives, it becomes crucial to comprehend the theoretical connection between these two notions. The impact of financial inclusion on green finance might be better understood by exploring how it enables marginalized communities to engage in sustainable financial endeavors. The decentralization of access to financial services, as enabled by inclusive regulations and innovations in fintech (Havranek & Zigraiova, 2015; Zigraiova and Havranek 2016), leads to a more varied foundation for green finance contributors. Diversification has the potential to stimulate the inflow of money into initiatives that prioritize environmental responsibility. Furthermore, aligning financial inclusion policies with the UN Sustainable Development Goals establishes a collective objective of encouraging accountability and sustainable practices, which may lead to increased investments in environmentally friendly initiatives (Gillingham & Palmer, 2014). The underlying theoretical basis for this correlation is rooted in the ideals of inclusive and equitable economic growth, as people and organizations develop the capacity to allocate resources towards environmentally sustainable initiatives (Cherniwchan, 2017). The existing theoretical framework supports a positive correlation between financial inclusion and green financing. However, the empirical data within the specific context of the OECD is still being established (Beck et al., 2004; Demirguc-Kunt et al., 2018). In the context of the stated nations, it can be noted that collective green finance has been volatile during the last two decades (see Figure 1). Still, the level of green finance is found to decrease during COVID-19. However, these economies are at the recovery stage, where green finance is increasing in 2021. To provide empirical support for the aforementioned theoretical framework, this research aims to investigate the relationship between financial inclusion and green financing across OECD nations (Figure 2). Energy efficiency in OECD economies. Green finance in the OECD economies.

The advancement and introduction of green financing within the OECD economies play a crucial role in the international effort to address and alleviate environmental problems. This undertaking necessitates the analysis of several facets, including energy efficiency, foreign trade, composite risk index, and human capital, and their prospective influence on green finance. The development of energy efficiency is of the utmost significance in advancing green finance. Theoretical frameworks propose an inherent connection between heightened energy efficiency and investments prioritizing environmental responsibility. The optimization of energy use not only leads to a reduction in operating expenses but also coincides with the SDGs. The implementation of enhanced energy efficiency practices results in a decrease in overall energy use (Gillingham & Palmer, 2014). This aligns with the fundamental concepts of sustainable finance. Enhancing energy efficiency in manufacturing processes may provide economic advantages while also fostering the adoption of sustainable financial practices. From the perspective of the given statistics, it must be noted that the level of energy efficiency is steadily increasing in the OECD economies, as shown in Figure 2. This indicates that these economies are more concerned about adopting environmentally friendly measures to tackle environmental issues of continuous emissions (Hassan et al., 2022; Pata et al., 2023). Nevertheless, the impact of international trade on green financing in OECD nations is complex and has several dimensions. According to Cherniwchan (2017), trade serves to disseminate sustainable practices and innovations worldwide. The theoretical correlation between international commerce and green finance highlights the possibility of increased market opportunities and financial capital. The exportation and importation of environmentally friendly technology and goods serve as catalysts for investment in sustainable sectors, promoting green finance growth (Handoyo et al., 2022; Hao et al., 2021).

Additionally, human capital is a crucial catalyst for developing green finance, as it actively contributes to creating and enhancing environmentally sustainable technology. The underlying theoretical framework in this context is based on the notion that a workforce with advanced skills is more inclined to stimulate development within green sectors (Li & Xu, 2021; Lin et al., 2021). The facilitation of higher education and skill development plays a crucial role in fostering the emergence of individuals with the knowledge and expertise necessary to become green entrepreneurs and specialists. These individuals are at the forefront of pushing green finance projects within OECD countries. Moreover, the impact of the composite risk index (CRI) on green financing is a multifaceted but crucial factor. A lower CRI score indicates economic resilience and stability (Zhang et al., 2022; Zhang and Xu, 2023). In theory, settings characterized by low risk tend to stimulate investments, including capital allocation towards efforts in the realm of green finance. Establishing measures to reduce economic, financial, and political risks is advantageous in fostering an atmosphere receptive to sustainable funding and investments.

Theoretical linkages among these factors indicate that energy efficiency, international commerce, CRI, and human capital may facilitate the advancement and growth of green finance throughout the OECD countries. The comprehension of these interrelationships serves as the fundamental basis for this research work, which seeks to examine these factors impact on green finance empirically. The main aims of this study are to examine, via empirical analysis, the relationship between financial inclusion, energy efficiency, human capital, foreign trade, and the CRI in the context of green finance in OECD nations from 2004 to 2021. The primary objective of this research is to investigate the enduring associations between the variables under consideration via the use of diverse diagnostic tests and panel econometric methodologies, such as Panel Autoregressive Distributed Lag (ARDL) and panel Dynamic Ordinary Least Squares (DOLS). This study’s main focus is to investigate these variables' impact on green financing and to analyze if these associations exhibit temporal variations. Furthermore, the objective of this study is to ascertain causal relationships among the variables above to fully comprehend the factors influencing green finance within the setting of the OECDC nations.

Examining the factors influencing green financing in OECD nations has significant implications for various convincing reasons. These nations have a significant role in global pollution emissions, emphasizing the need to switch to green financing as a crucial step in addressing climate change. Furthermore, green finance exhibits alignment with the SDGs and facilitates the advancement of environmentally friendly economic development, a fundamental component for enduring prosperity. Moreover, understanding the factors influencing green financing in OECD nations provides valuable insights for officials and investors, enabling them to implement specific interventions and make informed investment decisions. Lastly, the OECD countries, being at the forefront of financial innovation, have the potential to provide models for other economies, enhancing the influence of green finance in the worldwide effort to combat global warming and the degradation of the environment.

This research study provides valuable insights into the existing body of knowledge on green finance and the factors that influence it within the OECD nations. The contribution of this study is in its provision of empirical evidence about the interplay of the variables mentioned above in the context of green finance. The study enhances the knowledge of these connections. It broadens the inquiry to include both long-term and short-term dynamics, thus dealing with the temporal aspect that has often been neglected in prior research. The results of this study provide significant policy implications and practical recommendations for stakeholders who want to advance the adoption of environmentally sustainable financial practices in OECD nations. These efforts are in line with the broader global aims of promoting sustainability. Furthermore, identifying causal connections augments our understanding of the complex processes that propel green finance, making a valuable contribution to the existing body of knowledge in environmental economics and finance.

The remaining of the manuscript is organized as: Section 2 presents review of the literature; Section 3 provides methodology; Section 4 indicates the results and discussion, and Section 5 reports the conclusion and policy implications.

Literature Review

This section covers the literature on the importance of financial inclusion, human capital, energy efficiency, trade, and composite risk index in developing green finance in different economies. Nonetheless, contemporary scholars have paid less attention to identifying drivers of green finance than discovering determinants of environmental quality, emissions, or economic development. Still, the literature offers substantial insights into the importance of the stated variables in developing green finance. For instance, recent studies offered significant empirical evidence concerning the progressive role of green finance and financial inclusion in environmental sustainability in different economies and regions (Khan, Haouas, et al., 2023; Zhan et al., 2023; Mirza et al., 2023; Saydaliev and Chin, 2022; Liu et al., 2023; Qin et al., 2021a, 2021b). Technological innovation advancements significantly stem financial inclusion and financial development to eradicate environmental degradation (Brahmi et al., 2023; Fakher & Ahmed, 2023; Xie et al., 2023). Besides, financial inclusion is one of the key drivers of energy efficiency and renewable energy consumption (Khan, Haouas, et al., 2023; Li et al., 2022; Liu et al., 2022; Zheng et al., 2023), whereas green financial development substantially improves the level of green energy adoption, enhance research and development, encourage green agriculture (Lee et al., 2023; Xu et al., 2023). As a result, Hawash et al. (2022) claimed that a higher level of financial inclusion and foreign direct investment significantly leads to sustainable economic growth. However, Ahmad et al. (2022) and Ahmed et al. (2021) oppose such claims by empirically validating the adverse influence of financial inclusion and financial development on environmental quality in the BRICS economies and Japan, respectively. Recently, Guang-Wen and Siddik (2023) used the data of 302 financial institutions and concluded that green innovation substantially influences environmental performance. Also, the study claims that green innovation mediates green finance in the banking sector.

Similar to the above nexus, the empirical work concerning the association between energy efficiency, human capital, and green finance is also scant in the existing literature. Yet, the studies have focused on exploring the factors influencing energy efficiency in different economies and regions. Specifically, Khan, Haouas, et al. (2023) examine the Malaysian economy using non-parametric approaches. The study concludes that financial inclusion, human capital and political risk significantly improve the initiatives that support environmentally friendly initiatives, that is, energy efficiency. Concerning such initiatives including energy efficiency, tech innovation, and renewable’s consumption, Yang and Song (2023), Dai et al. (2022), Ibrahim et al. (2022), Ning et al. (2023), Rasoulinezhad and Taghizadeh-Hesary (2022), Wang and Wang (2022, 2021), and Zhang et al. (2021); Destek et al. (2023); Kartal and Pata (2023) asserted that income growth, human capital, and foreign trade are the significant drivers of these initiatives in different economies and regions. Besides, these initiatives are directly linked to environmental sustainability (Feng et al., 2022). Similarly, Chen et al. (2022) revealed that financial inclusion, industrial production, renewables-related R&D and foreign trade are the significant drivers of energy efficiency in the US during 1990–2020. In China’s provincial setup, Ma et al. (2022) revealed that the total energy efficiency progressively increased during 2008–2020. However, human capital negatively correlates to the total energy efficiency factor, while green finance exhibits a U-shaped association with the former. For the same country, Zhang et al. (2022) asserted that financial inclusion and green finance are advantageous to global development by enhancing trademark filing, investment in the private sector, and patent registration. However, human capital and international trade significantly influence the above-discussed association.

In the case of the OECD economies, Gu et al. (2023) use the MMQR approach along with the panel diagnostic tests and conclude that composite risk index, trade openness, and natural resources extraction adversely and significantly influenced green finance during 2004–2020. However, energy efficiency and environmental policies significantly improve green finance in the region. Besides, Li, Dong, and Dong (2022) and Lee and Lee (2022) claimed that green financial development and green regulations significantly improve investment in environmentally friendly energy resources and green total factor productivity, which reduces the level of emissions in the region (Du & Wang, 2023). Furthermore, human capital, the energy sector, and pollution significantly direct the association between green finance and environmental quality (Nawaz et al., 2021). Nonetheless, green finance is a significant and leading driver of sustainable development, significantly disturbed by environmental degradation (Hunjra et al., 2023). Similarly, Adebayo et al. (2023) claimed that financial risk, economic risk, which are the substantial contributors to the composite risk index, and energy efficiency tend to reduce environmental degradation. The same results are also validated by the earlier study of Wang, Elfaki, et al. (2022), along with the mixed results concerning trade. However, in the case of OECD economies, Wang, Dong, et al. (2022) asserted that the composite risk plays an essential role in mediating the positive influence of renewable energy economic development when it reaches a threshold level.

Research Gap

After analyzing the available literature, this study observed that there is limited to no literature concerning the influencing factors of green finance except the one authored by Gu et al. (2023). However, the literature provides potential factors and drivers of environmental indicators such as carbon emissions, renewable energy, and energy efficiency. Besides, the literature provides evidence that green finance is a potential influencing factor of environmental sustainability (Khan, Haouas, et al., 2023; Mirza et al., 2023; Zhan et al., 2023). Still, no literature analyzes the factors affecting green finance in developing or developed economies. Since most of the developed economies are trending in enhancing green finance. Therefore, it is crucial to address the existing research gap in identifying the factors influencing green finance in developed economies, which could have substantial policy implications for sustainable development.

Data and Methods

Model Construction

Following the research objectives and literature above, this research observed that financial inclusion and energy efficiency could be substantial influencing factors of green finance (GF), where the latter is measured as renewable energy public RD&D budget, % total energy public RD&D. Here, financial inclusion (FI) is assessed using six parameters as pioneered by Kebede et al. (2021): the number of commercial bank branches per 1000 km2, the number of commercial bank branches per 100,000 adults, the number of automated teller machines (ATMs) per 1000 km2, the number of ATMs per 100,000 adults, the number of deposit accounts with commercial banks per 1000 adults, and the ratio of domestic credit to the private sector in GDP. However, energy efficiency (ENEF) is considered GDP per unit of energy use (constant 2017 PPP $ per kg of oil equivalent). In addition, this research considered three significant variables as mentioned in the existing literature, such as human capital index (HCI), trade (TRD: % of GDP), and composite risk index (CRI including financial, economic, and political risk). Following the recent study of Gu et al. (2023), this study develops the research model as

Analytical Techniques

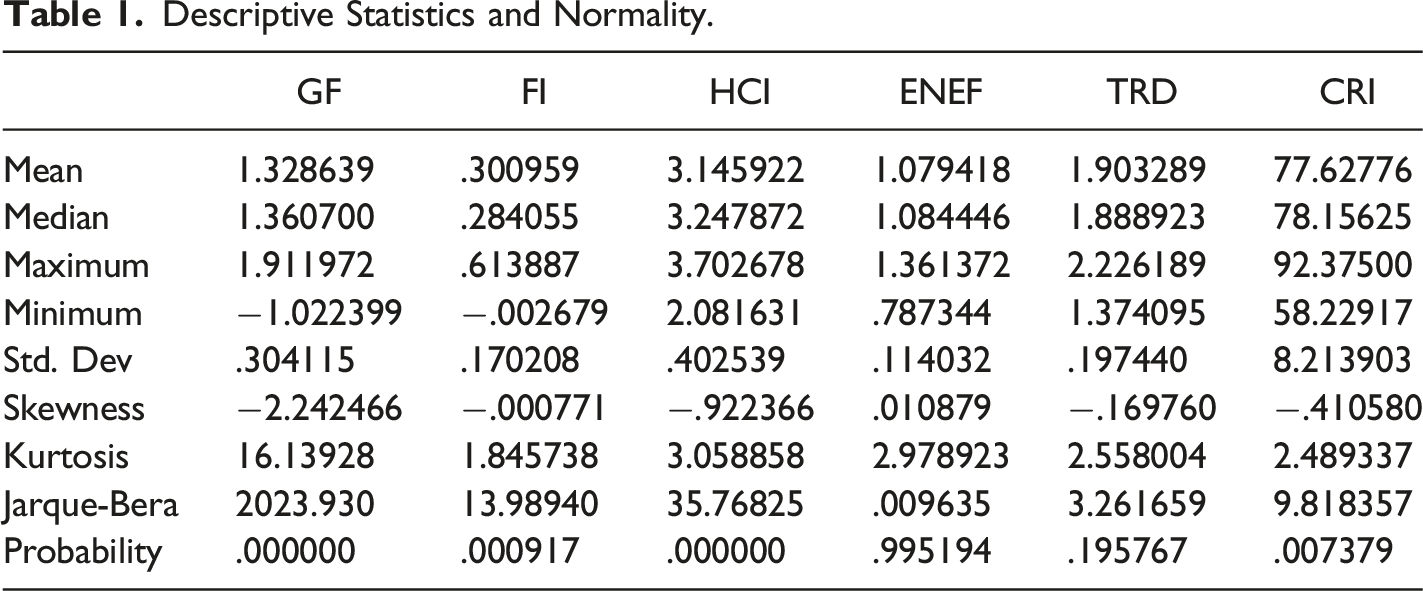

The first phases of this inquiry involve performing a descriptive assessment and conducting normality checks for each element. The present research used statistical analysis to determine the panel data series’s median, mean, and range (maximum and lowest). The computed standard deviation quantifies the extent of dispersion in the time series resulting from fluctuations in the observed values and the mean estimate. Furthermore, the utilization of kurtosis and skewness is applied in this research to assess the normality of the data. However, a comprehensive measure of Jarque and Bera (1987) for normality examination provides more insights concerning the distributional properties. Therefore, this study uses the stated test, which may be expressed as follows

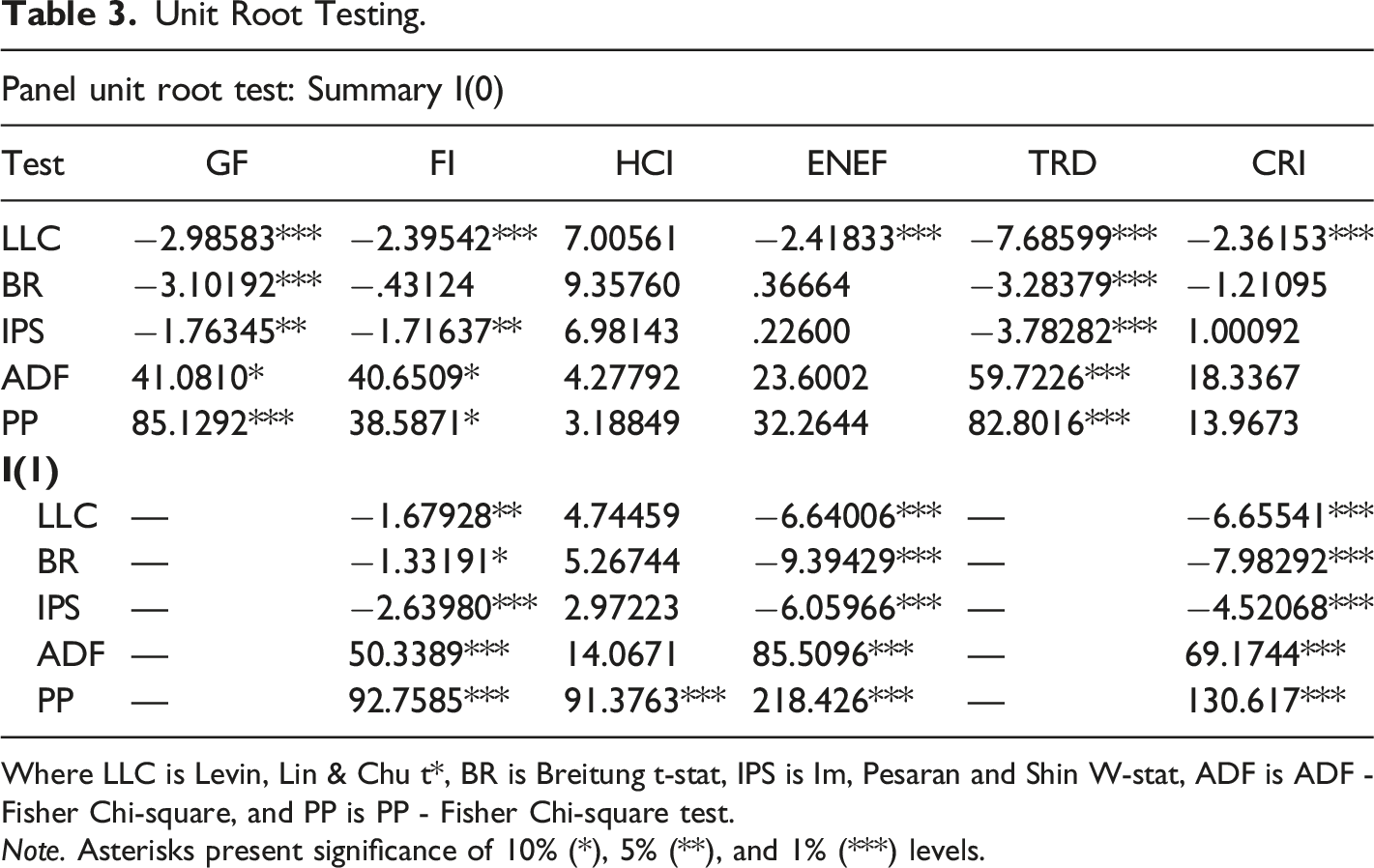

The diagnostic procedure entails doing a stationarity assessment for each designated parameter. The current research employs multiple unit root statistical methods, including those introduced by Breitung (2001), Phillips and Perron (1988), (Im, 1997), ADF-Fisher (ADF) (Maddala & Wu, 1999), and Levin et al. (2002). The experiments are performed on information at both levels [I(0)] and first-difference [I(1)] in order to undertake a thorough analysis of stationarity. According to the null hypothesis (H0), all of these assessments depend on the assumption that a unit root exists. The equations representing the formula for the LLC, IPS, ADF, and PP tests are denoted as equations (3)–(6), correspondingly

The term (

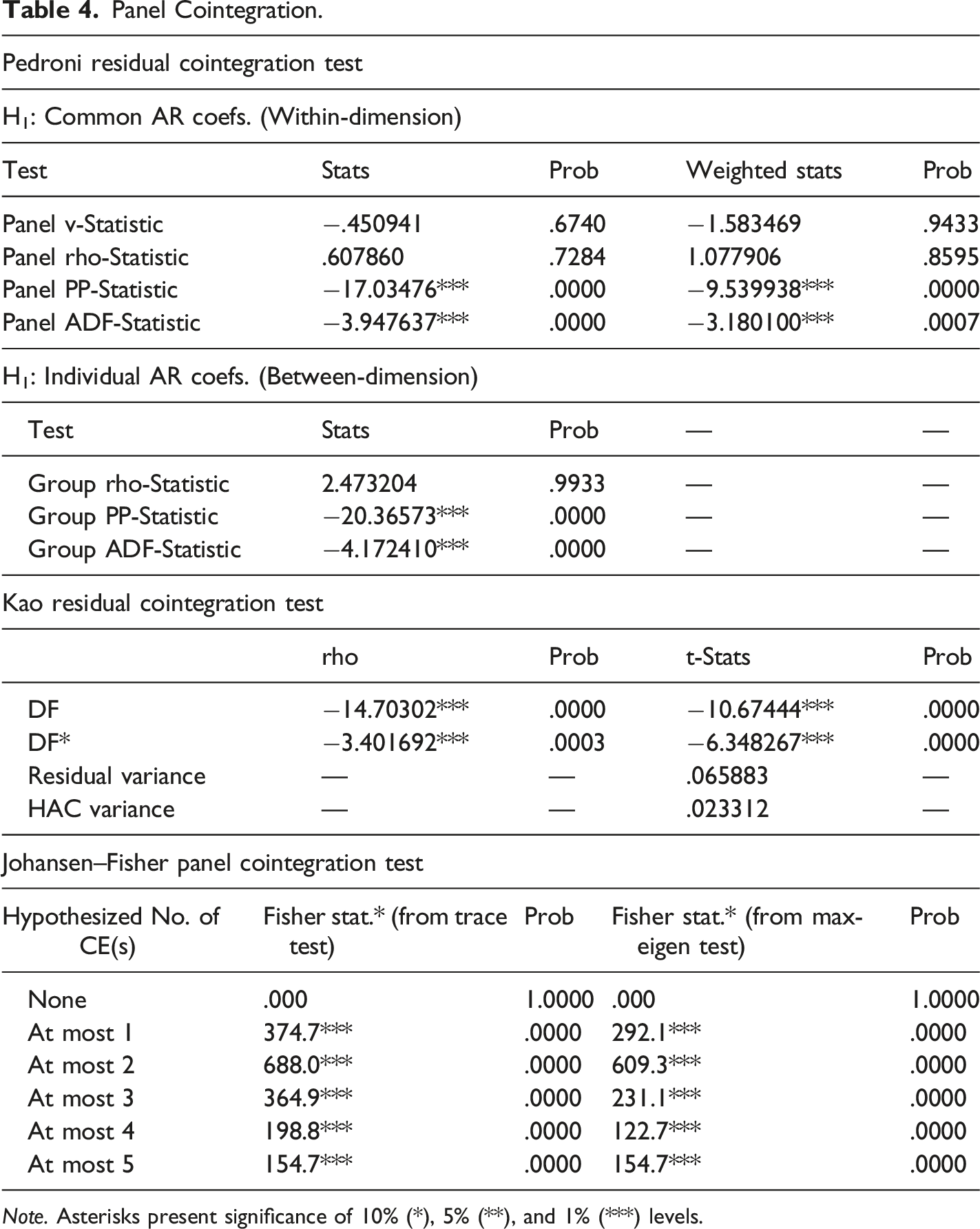

After executing unit root evaluation, this research investigated cointegration by using the Pedroni Residual Cointegration test (Pedroni, 2001, 2004), hypothesis testing (examining specific AR coefficients across dimensions), the Kao (1999) residual cointegration, and Johansen–Fisher cointegration tests for the panel data analysis. These various methodologies were used to confirm the presence of cointegration in the present research. All the above analyses presume a null prediction of the absence of a cointegration connection between the variables.

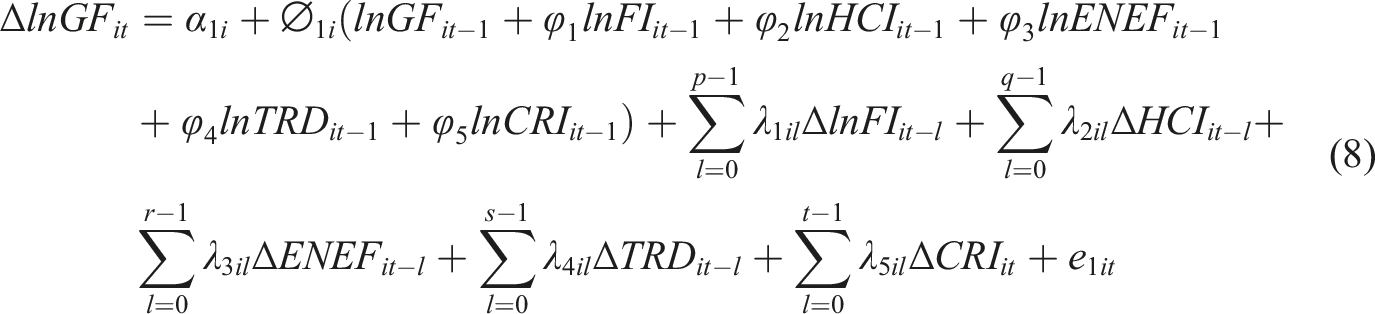

The panel Autoregressive Distributed Lag model (panel ARDL) applies when the parameters under consideration follow mixed order regarding integration. This approach has been put forward by Pesaran and Shin (1997), while the improved version with further improvement by Pesaran et al. (2001). Nonetheless, there are numerous empirical approaches to data estimations. Still, the panel ARDL is more effective in accounting for the mixed order of integration. Estimators such as the pooled mean group (PMG) and dynamic fixed effect (DFE) may be calculated. The ARDL model for the long-run coefficient estimations may be put forward based on the given research model below

The equation (7) could adopt the below given form after parameterization

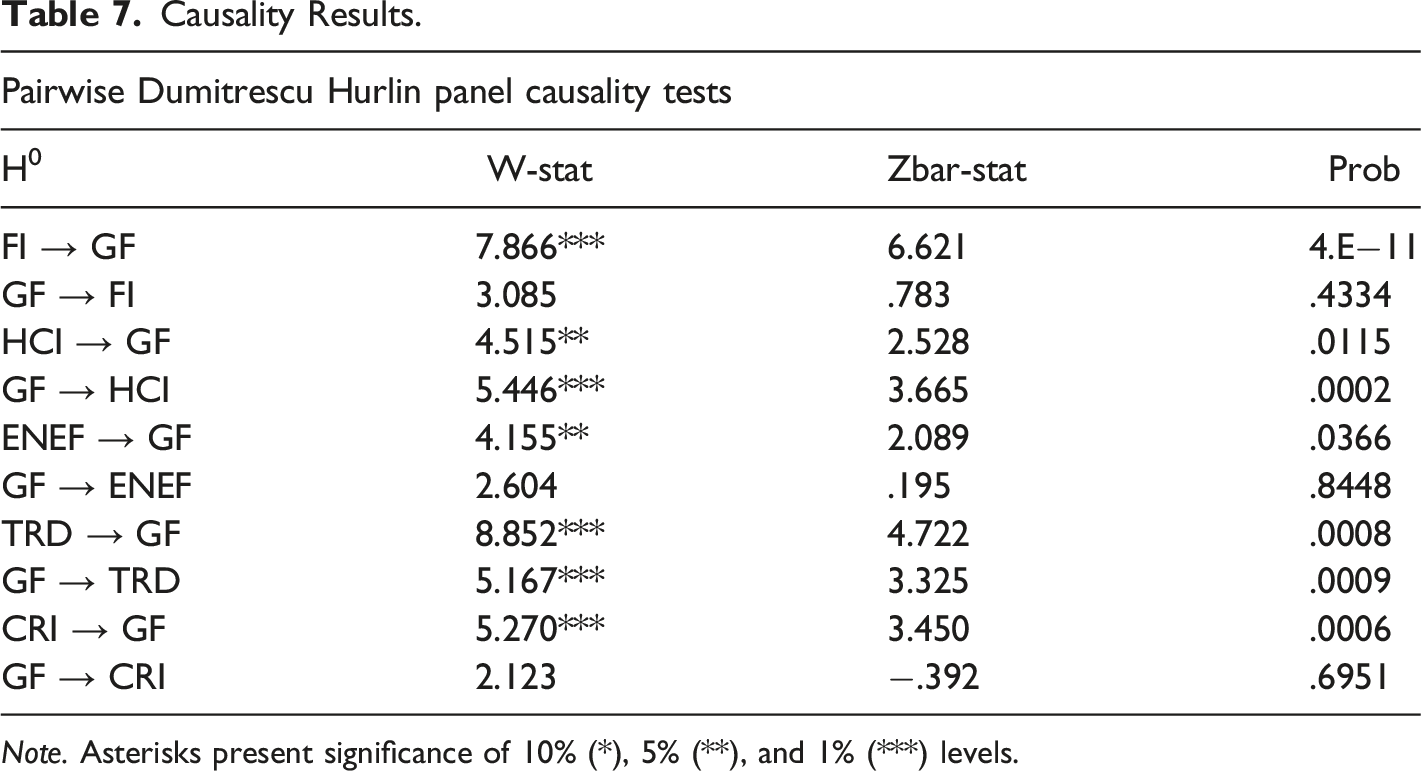

Once the short and long-run estimations are achieved, this research examines the authenticity of the long-run coefficients. In this regard, the study employs the panel dynamic ordinary least square (DOLS) approach, which offers more robust long-run estimates based on the mean influence of each regressor on the GF. Moreover, the research used the “pairwise Dumitrescu and Hurlin panel causality test” to determine the causation path, a concept supported by several empirical investigations (Khan et al., 2022; 2023).

Results and Discussion

Descriptive Statistics and Normality.

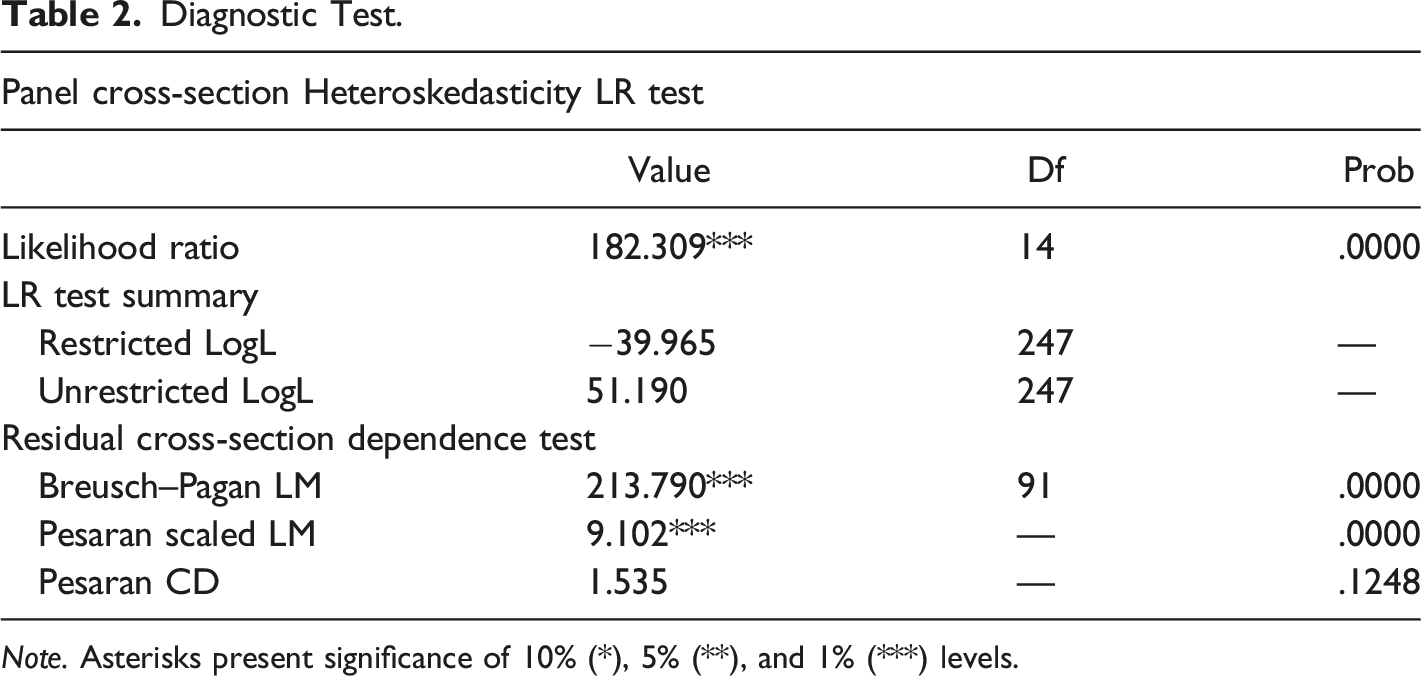

Diagnostic Test.

Note. Asterisks present significance of 10% (*), 5% (**), and 1% (***) levels.

Unit Root Testing.

Where LLC is Levin, Lin & Chu t*, BR is Breitung t-stat, IPS is Im, Pesaran and Shin W-stat, ADF is ADF - Fisher Chi-square, and PP is PP - Fisher Chi-square test.

Note. Asterisks present significance of 10% (*), 5% (**), and 1% (***) levels.

Panel Cointegration.

Note. Asterisks present significance of 10% (*), 5% (**), and 1% (***) levels.

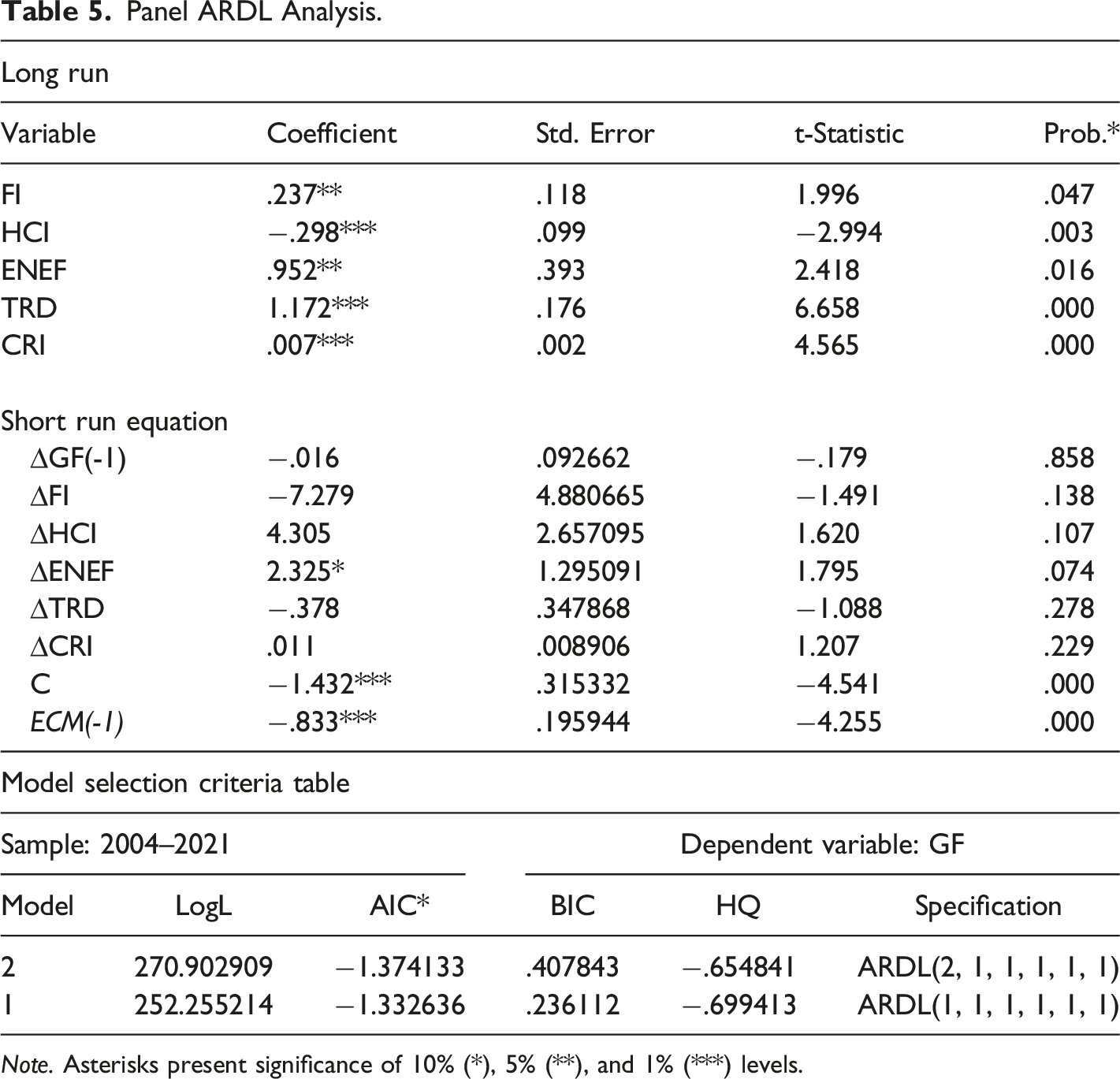

Panel ARDL Analysis.

Note. Asterisks present significance of 10% (*), 5% (**), and 1% (***) levels.

The promotion of FI, via the enhancement of financial service accessibility, facilitates a wider demographic’s involvement in GF activities. When people and companies are allowed to use financial services and credit facilities, they are empowered to invest in environmentally friendly initiatives and technology. Furthermore, establishing inclusive financial systems may effectively support the provision of microfinance services for environmentally friendly projects, enhancing the accessibility of sustainable practices for smaller businesses and disadvantaged populations (Demirguc-Kunt et al., 2018). Furthermore, the implementation of ENEF measures serves as a direct means of contributing to the field of GF, as it effectively diminishes the ecological impact of both commercial enterprises and residential dwellings. Investments in ENEF technology and practices, including efficient lighting, HVAC systems, and manufacturing procedures, provide dual benefits of reducing operational expenses and facilitating the acquisition of GF for organizations. According to the International Energy Agency (IEA, 2017), financial institutions often prefer projects with the potential for decreased energy use and emissions. In addition, the facilitation of international TRD may catalyze the advancement of GF via the promotion of sustainable products and services. Export-oriented companies have the potential to invest in environmentally friendly technology to comply with global sustainability requirements, hence attracting potential for GF. Furthermore, it is common for trade agreements to have environmental elements, which incentivize adopting sustainable practices in return for the opportunity to access new markets (Subramanian & Mattoo, 2003). Additionally, using a CRI that evaluates environmental, social, and governance (ESG) issues has the potential to incentivize firms and investors to adopt GF practices. Financial institutions and investors tend to have a more positive perception of entities that exhibit reduced ESG concerns. Enterprises may mitigate perceived risks, improve their creditworthiness, and get easier access to GF choices by incorporating ESG factors into their operational and investment strategies (World Economic Forum, 2019). These results are in line with the empirical works of Guang-Wen and Siddik (2023), Khan, Haouas, et al. (2023), Zhang et al. (2022), and Gu et al. (2023) in the existing literature.

On the contrary, the ARDL estimates asserted that HCI is the only variable that has a significant adverse influence on the GF in the selected economies. That is, a percentage increase in the HCI reduces the level of GF by .298% in the long run. The statistical results are significant at a 1% level. The presence of a strong HCI can enhance the workforce’s quality, possibly reducing the need for GF via the promotion of sustainable practices and technologies. According to Acemoglu and Linn (2004), highly trained labor may contribute to advancing energy-efficient technology and processes, reducing the need for green funding in well-established economies. Moreover, the presence of well-informed workers can facilitate the implementation of business sustainability efforts, hence reducing the need for external financial assistance specifically targeted toward environmentally friendly endeavors (Russo & Fouts, 1997). These dynamics emphasize the role of HCI as an inherent catalyst for environmentally aware practices, which may reduce the need for GF initiatives. The adverse influence of HCI is consistent with Ma et al. estimated results (2022). In the context of the short-run estimates, this study found that only ENEF positively and significantly influences the GF, with a magnitude of 2.325% and significant at 1%. However, the remaining variables are found insignificant concerning its short-run influence. Still, the ECM is found to be 83.3%, which indicates that the model tends to approach the equilibrium point with an 83.3% speed of adjustment. Besides, the table under discussion also displays the specification of the lags selection.

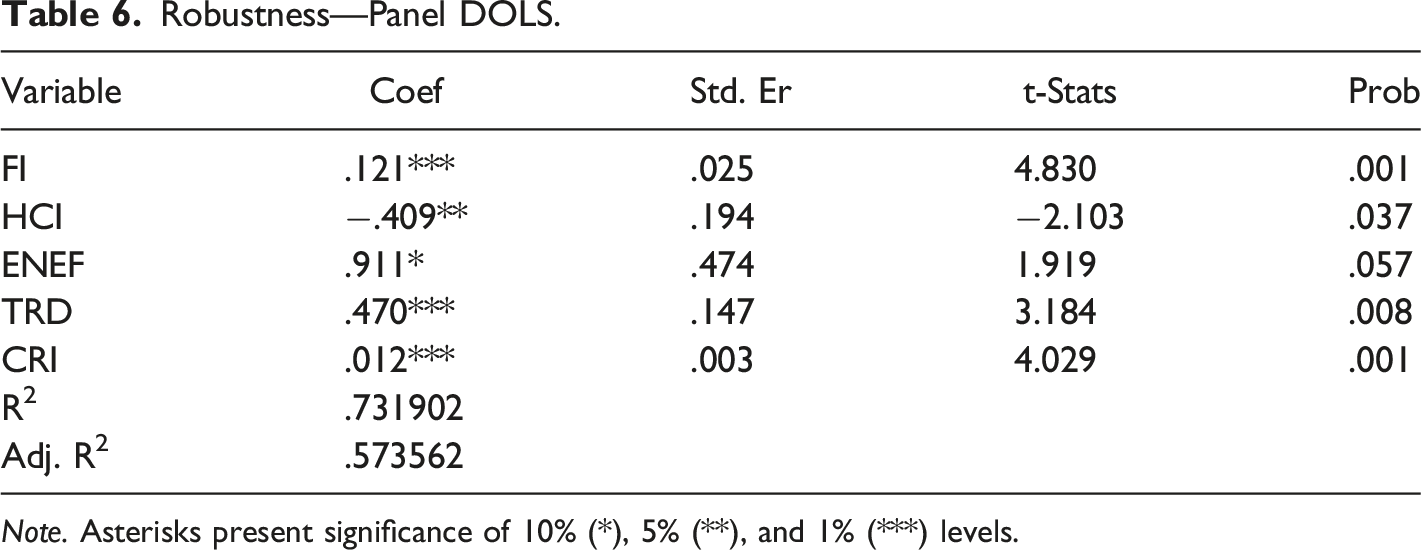

Robustness—Panel DOLS.

Note. Asterisks present significance of 10% (*), 5% (**), and 1% (***) levels.

Causality Results.

Note. Asterisks present significance of 10% (*), 5% (**), and 1% (***) levels.

Conclusion and Policy Implications

The present investigation aimed to examine a multifaceted range of influencing variables on the development of green finance across OECD nations from 2004 to 2021. Using an extensive framework, this study conducted diagnostic examinations to validate analyses, revealing significant findings regarding the long-term cointegration connections among variables such as financial inclusion, energy efficiency, human capital, international trade, composite risk index, and green finance. In the long-run, our research has shown an advantageous relationship among financial inclusion, energy efficiency, international trade, and the composite risk index favoring green finance. Promoting financial inclusion via increased accessibility to financial services enables a broader society to participate in environmentally sustainable investment opportunities. Concurrently, the implementation of energy-efficient practices serves to diminish resource use and pollution, therefore promoting the concept of sustainability. The alignment of foreign trading with ecological standards has the potential to foster the development and growth of the green finance sector. Nevertheless, a surprising discovery emerged about the adverse influence of human capital on green finance, which contradicts established beliefs and necessitates more investigation. The findings from our study indicate that energy efficiency has a favorable effect on green financing in the long run. However, in the short term, it was seen that only energy efficiency was able to sustain this influence. The results underscore the need to continuously emphasize energy efficiency to facilitate speedy improvements in green financing. In addition, our research has confirmed the accuracy and validity of the findings by using the panel DOLS methodology, creating a high level of dependability of the findings. The causality analysis revealed unidirectional and bidirectional connections among the variables, highlighting the intricate nature of their relationships. The empirical results presented in this study provide valuable insights for stakeholders and policymakers in OECD nations. These insights emphasize the need for a comprehensive strategy to enhance green financing and facilitate sustainable development.

Policy Implications

This research presents several policy implications based on the empirical findings. These implications are outlined as follows: It is essential for governments to actively promote the development of inclusive financial services throughout financial institutions to broaden the availability of green financing to both consumers and companies. This objective might be accomplished by using customized financial instruments and educational campaigns. Moreover, it is essential for these economies to effectively implement and enhance energy efficiency legislation and subsidies to foster the adoption of ecologically responsible practices. Promote companies' engagement in allocating resources towards developing and implementing clean energy technologies, therefore mitigating resource depletion and minimizing emissions. It is imperative for the OECD economies to actively promote global trade agreements that prioritize rigorous compliance with environmental regulations. The promotion of sustainable practices and innovations via this collaboration has the potential to drive green financing. Authorities need to recognize and effectively mitigate the unanticipated adverse consequences of human capital in green finance. One potential approach is redirecting education and training programs to prioritize cultivating sustainable practices and integrating the workforce with green targets. Furthermore, it is essential to include environmental, social, and governance (ESG) risk analyses into investment decision-making processes and regulatory frameworks. Developing an extensive framework that incentivizes investments with minimal ESG risks may effectively enhance the advancement of green finance.

Study’s Limitations and Future Research Directions

The present study is vulnerable to constraints in data availability and possible concerns with endogeneity. Future research should take into account more comprehensive and intricate datasets. Furthermore, it is important to acknowledge that the outcomes of this study may not fully include the diverse policy settings present in OECD nations. These various policy settings can significantly change the effect of the elements under investigation. Further investigation is required to have a more comprehensive understanding of the influence of policy frameworks on the nature of green financing. Further investigation is required to examine the mediating processes underpinning the connections this study highlighted. In addition, executing a comprehensive examination of the intricacies surrounding policy actions and their impact on the results of green financing in various settings within the OECD will provide significant value. Long-term research investigations that monitor and analyze the shifts in green finance practices and regulations may provide useful information into the progression of sustainable financial systems.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Zhejiang Provincial Philosophy and Social Sciences Planning Project (24NDJC264YBM).

Author Biographies