Abstract

This study explores whether and under what conditions women CEOs engage in behavioral consistency when promoting CSR practices. Specifically, drawing from the social role and behavioral consistency theories, we argue that women’s CEO presence will positively affect CSR consistency. We use two categories to capture the firm’s consistency in CSR practices: inter-domain and temporal consistency. Inter-domain consistency indicates reliability in a firm’s conduct across its various stakeholder groups. Temporal consistency refers to the consistency of a firm’s behavior toward its stakeholders over time. Using 167 unique S&P 500 firms over the 2005-2013 sample period, we found that women CEOs maintain higher temporal and inter-domain consistency than men. Our results also show that women CEO-led firms with greater gender diversity on their boards exhibit higher temporal and inter-domain consistency levels. Our study advances our understanding of how women CEOs use their situational and positional power to improve such equity and consistency.

Keywords

Introduction

Both the public and scholarly attention focused on firms’ social responsibility practices have become more intense in recent years. Stimulated in part by the mixed empirical evidence on the drivers of a firm’s CSR and its financial impact on the firm (McWilliams & Siegel, 2000), scholars have become more focused on factors that shape the characteristics of the firm’s CSR investments and how these characteristics affect the firm’s intended rewards (Petrenko et al., 2016; Wang & Choi, 2013). Several scholars have argued that the firm’s desired financial rewards from its CSR investments are largely influenced by how it engages in socially oriented activities (Tang et al., 2012). For example, Tang and associates (2012) highlighted consistency as a major factor determining the extent to which firms benefit financially from their CSR engagements. Wang and Choi (2013) argued that both CSR temporal and inter-domain inconsistency negatively affect the firm’s realized rewards from its CSR investments. Based on such studies, it appears that managing the conflicting demands of the various stakeholder groups and ensuring that all groups are equally considered when designing the firm’s CSR policies has become a major challenge for organizational decision-makers and a topic of growing interest in the management literature (Harrison et al., 2020; Schnackenberg & Tomlinson, 2016).

Recent studies show that firms may prioritize some groups of stakeholders over other groups or might alternate their CSR focus between groups depending on the firm’s motives and resources. Such prioritization ultimately results in inconsistency across CSR practices (Scheidler et al., 2019; She & Michelon, 2019). The emerging evidence is that when firms engage in inconsistent CSR behavior, whether across time or across stakeholder groups, the firm is likely to suffer reputational loss and disincentives from internal and external members (Andersen & Høvring, 2020; Babu et al., 2020; Chen et al., 2020; Christensen et al., 2020; Scheidler et al., 2019). These findings highlight that the consistency of the firm’s CSR practices significantly impacts various stakeholders, which can, in turn, affect the firm’s reputation and desired financial rewards that result from the firm’s CSR investments. As Wang, Dou, and Jia (2016) put it, “these intra- and inter-firm variations in corporate social performance imply that focusing only on the level of corporate social performance may not give a complete picture of the CSR–financial performance relationship” (P.417). Given the importance and implications of the consistency of the firm’s CSR behavior, it becomes more important for both scholars and practitioners to understand the antecedents to the inconsistency of a firm’s CSR behavior (Al-Shammari et al., 2022; Wang et al., 2022).

We respond to the calls made in recent studies to explore the specific factors that might lead to inconsistent CSR engagements and that can, in turn, result in undesired consequences for the firm by focusing on one of the most important characteristics of CSR investments: the consistency of the firm’s social practices over time and across stakeholders. We define CSR as a relational activity in which the firm does social good that is aimed at the various groups of the firm’s stakeholders (Chen et al., 2020; den Hond et al., 2014; Matten & Moon, 2008; McWilliams & Siegel, 2000, 2001). As documented by recent studies (Hawn & Ioannou, 2016; Wang & Choi, 2013; Wang et al., 2016), the level of a firm’s CSR practices fluctuates over time and across the stakeholder groups. The magnitude of fluctuation varies across firms such that some firms demonstrate consistent and unswerving social performance while others exhibit both temporal and inter-domain inconsistencies in their social performance. Recent studies have documented that these inconsistencies have negative reputational and financial consequences for firms (Hawn & Ioannou, 2016; Tang et al., 2012; Wang & Choi, 2013).

Although prior studies have rightly uncovered the far-reaching implications of inconsistent CSR practices across time and stakeholders (Andersen & Høvring, 2020; Hawn & Ioannou, 2016; Tang et al., 2012; Wang & Choi, 2013), we still know very little about what factors contribute to such variations and inconsistencies. The goal of our research is to better understand the role of female leaders in promoting behavioral consistency in a company’s corporate social responsibility (CSR) practices. We explore the unique contributions of women leaders in shaping CSR practices, provide some insight into how organizations might gain unanticipated CSR benefits from addressing the gender gap in the corporate upper echelon, and how firms might lever the diverse perspectives women CEOs provide to drive sustainable business practices. We organize our effort around two specific research questions: a) Do women CEOs promote behavioral consistency in firms’ CSR temporal and inter-domain consistency? and b) Is this relationship stronger when there is greater gender diversity on the board? We posit that the presence of women leaders at the executive and board level influence the consistency of a firm CSR strategy which, according to the current theoretical framework, should result in positive outcomes both for the firm and the firm’s stakeholders.

Previous studies have shown that both gender diversity on the board and the presence of women CEOs are significantly associated with greater levels of CSR investments and that women are more likely to promote CSR practices to the top of their agendas (Bear et al., 2010; Cook & Glass, 2016, 2018; Ho et al., 2015). However, we know very little about whether and under what conditions women leaders promote behavioral consistency in the firm’s CSR practices. Drawing from the social role and behavioral consistency theories, we argue that women’s CEO presence will positively relate to CSR temporal and inter-domain consistency and that this relationship will be stronger when there is greater board gender diversity. In so doing, we address an important shortcoming in the extant gender diversity-CSR literature -- the impact of women leadership on the equity of stakeholders’ treatment and the adoption of consistent practices across the portfolio of the firm’s CSR practices. We also advance our understanding of how women CEOs use their situational and positional power to advance such equity and consistency.

An Overview of Temporal and Inter-Domain Consistency

Prior studies have emphasized the role of behavioral consistency in shaping individuals’ behavior and the outcomes of such consistency at the individual level (e.g., Bloeser et al., 2015; Cronqvist et al., 2012). However, despite its far-reaching implications for firms, behavioral consistency has received very little attention in the strategy literature (Sauerberger & Funder, 2017; Wang & Choi, 2013). Perhaps the dynamic nature of the business landscape and the competitive environments in which firms operate have limited the effort devoted to understanding firm’s behavioral consistency. For example, the strategic change and dynamic capability literatures emphasize that firms resisting change and adaptation are less likely to survive (Fiol & Lyles, 1985; Fortune & Mitchell, 2012; Greve, 1998; Worch et al., 2012). These arguments are typically developed in the context of market-related strategies and actions (Datta et al., 2003; Dutton & Duncan, 1987; Kelly & Amburgey, 1991; Miller & Shamsie, 2001). However, in the non-market domain, especially in the firm’s social responsibility strategies and practices, failing to perform consistently across various stakeholders or across time may result in undesired consequences for the firm (Wang & Choi, 2013).

The extant literature has shown that a firm’s behavioral inconsistency in the social domain is related to firm performance. Inconsistent behavior can hurt the firm financial performance (Crilly et al., 2012; Hawn & Ioannou, 2016; Scheidler et al., 2019; Wang & Choi, 2013). For example, Scheidler et al. (2019) found that inconsistent CSR strategies lead to costly employee turnover because employees perceive the firm’s CSR efforts as ingenuine. On the other hand, firms that maintain high consistency in their CSR engagements have better chances of building and sustaining stronger relationships with all stakeholder groups including employees (Hawn & Ioannou, 2016; Tang et al., 2012; Wang & Choi, 2013). Moreover, sustainable consistency in the firm’s CSR engagements is difficult for rivals to replicate and may be an essential component of the firm’s overall competitive advantage (Barin et al., 2015; Dupire, 2018; Flammer, 2018; Susanne Johansen & Ellerup Nielsen, 2012). Such results highlight the importance of consistent CSR efforts.

Recent studies have shown that establishing a sound and sustainable pattern of stakeholder relationships does not require a high level of corporate social performance but rather that the firm delivers consistent social performance (Hawn & Ioannou, 2016; Wang & Choi, 2013). Wang and Choi’s study was the first to report that “the level of a firm’s social performance varies over time and across its various stakeholder domains” (Wang & Choi, 2013, p. 417) and that such variations differ across firms. Some firms have consistent social performance, while others show significant variations over time and across their different stakeholder domains (Agle et al., 1999; Porter & Kramer, 2002; Waddock & Graves, 1997). Such variations imply that the overall magnitude of CSR investments between firms varies independently from the consistency of the CSR investment within a firm. Further, independent of the magnitude of CSR investment, inconsistency in CSR engagement may have far-reaching implications for the firm’s public image and affect its reputation, thereby limiting the desired outcomes from their CSR engagement. Previous studies, in contrast, have largely been limited to considering only the financial consequences of these temporal and inter-domain inconsistencies in the firm’s CSR. As a result of this limitation, what has not yet been adequately addressed is what factors, either at the firm-level or outside of the firm’s formal boundaries, result in CSR engagement variations and inconsistencies.

We address this limitation in the extant literature by examining the effect of women CEOs on the firm’s behavioral consistency in the non-market strategy domain. Although we acknowledge that using ‘presence’ to test for impact is less than ideal, research shows that women leaders contribute to corporate social responsibility policies and commitments (Bear et al., 2010). Their presence often leads to heightened CSR activities within firms. Hence, understanding whether women CEOs go beyond merely engaging in CSR activities and consistently commit to CSR practices can serve as crucial knowledge for various firm stakeholders. We define CSR consistency as the firm’s consistent patterns of CSR engagements over time and across the stakeholders’ domains. We use two categories to capture the firm’s consistency in CSR practices: inter-domain and temporal consistency. Temporal consistency refers to the consistency of a firm’s behavior towards its stakeholders over time, while inter-domain consistency indicates reliability in a firm’s conduct towards its various stakeholder groups (Wang & Choi, 2013).

Behavioral Consistency and Social Role Theory Explanations

Behavioral consistency theory is a well-established psychological perspective (e.g., Allport, 1966; Epstein, 1980; Funder & Colvin, 1991) asserting that an individual’s behavior in one situation and time can be predicted based on behavior from a previous situation and time. Scholars are beginning to argue that behavioral consistency theory has the potential to explain congruencies between personal and corporate-level decision-making (Cronqvist et al., 2012) because some of these within-person tendencies transfer from the personal setting to the workplace. For example, Cronqvist et al. (2012) found that firms behave consistently with their CEOs’ personal preferences and choices. Using data on CEOs’ leverage preferences in their recent home purchases, the authors showed a robust and positive link between firm leverage and CEOs’ personal leverage choices. In another study Cha et al. (2019) found that CEOs with personal convictions toward civic engagements tend to support corporate environmental practices by leveraging resources to address various environmental issues.

Given the influence our tendencies exert on organizational decision-making, it is essential to understand how our propensities are shaped. Social role theory suggests that individuals have varying preferences, propensities, social priorities, and orientations, which are primarily influenced by their position in organizations, social groups, audience expectations, and social norms and roles (Eagly & Karau, 2002; Koburtay et al., 2019; Koenig et al., 2011). This notion is built on the gender socialization literature which contends that women and men face different circumstances in their early lives, and thus they are motivated to behave in different ways because they were subject to different sources of approval and reward early in life (Bem, 1981; Cook & Glass, 2016; Diekman & Schneider, 2010; Fyall & Gazley, 2015; Koenig & Eagly, 2014).

Among the central pillars of gender socialization theory is the notion that gender-related socialization engagements stimulate different types of behaviors in women compared to men (Cook & Glass, 2016). Relatedly, behavioral consistency theory suggests that these gender-based differences and tendencies may transfer from one’s personal pre-professional life to the managerial context (e.g., leadership styles, communication styles, occupation choices, risk-taking behaviors, etc.) For example, a meta-analysis examined studies using three leadership paradigms (i.e., think manager–think male, agency–communion, and masculinity-femininity paradigms) and found that all three paradigms demonstrated overall masculinity of leader stereotypes (Koenig et al., 2011). Another study found that while helping behavior, collaboration, and ties-building behaviors are more prevalent in women, independency and rivalry are more prevalent in men (Gilligan, 1993). Based on the analysis of 11,970 labor lawsuits, Liu (2021) found that woman-CEO-led firms face fewer labor lawsuits. Women are more likely to show commitment to a firm or professional code of ethics and to have a stronger sense of moral obligations because they know how important it is to gain public credibility (Kakabadse et al., 2015). A recent study using Bloomberg ESG data found that women CEOs are linked to a 19% increase in ESG scores (Aabo & Giorici, 2022).

Although the argument that strategic leaders rely on their personal experiences, values, and convictions when engaging in strategic decision-making is plausible regardless of a leader’s gender, we suggest that women CEOs and directors on corporate boards may have to adjust their behaviors due to pressuring social gender roles (Castaño et al., 2019). Despite decades of discourse on socially accepted gender roles and how they disproportionally affect women in organizations and leadership roles, much has yet to change and improve. Hence, awareness of such biases and stereotypes may make women CEOs feel pressured to behave in ways that garner the acceptance of the firm’s internal and external stakeholders (Moake & Robert, 2022; Saeed & Riaz, 2023). Women may also feel compelled to consistently engage in such behaviors over time to mitigate the liability of newness and gain legitimacy in the eyes of their subordinates, colleagues, and superiors. Based on these arguments and drawing from behavioral consistency and social role theory tenets, we posit that women CEOs will use temporal and inter-domain consistency in their CSR activities to demonstrate their prolonged commitment to various firm stakeholders.

Does CSR Consistency Matter?

In 2019 the Business Roundtable’s Statement on the Purpose of a Corporation was changed from stating that “The notion that the board must somehow balance the interests of stockholders against the interests of other stakeholders fundamentally misconstrues the role of directors” (Business Roundtable, 1997) to stating that “Each of our stakeholders is essential. We commit to deliver value to all of them, for the future success of our companies, our communities and our country” (Business Roundtable, 2019; as cited in Harrison et al., 2020). This change in statement of purpose reflects the growing believe among more than 200 of top CEOs in the United States that the firm should consider the interests of all of their stakeholders equally; it is no longer ethical for businesses to be focused only on the interests of shareholders (Harrison et al., 2020). Such calls signal the mounting pressure firms face to attend to the needs and expectations of all stakeholders. However, firms’ stances towards CSR continue to vary over time and across the stakeholder spectrum. Such variation has contributed at least partly to the inconclusive evidence regarding the business case for a firm’s social responsibility investments (Kim et al., 2018; McWilliams & Siegel, 2000).

Many studies have pointed to contingency conditions that may either help or hinder the realization of improved financial performance from the firm’s CSR investments (Oh et al., 2016; Q. Wang, Dou, & Jia, 2016; Wu et al., 2020; Zhu et al., 2014) and explored the effect that some of these characteristics have on the firm’s financial returns from CSR investments. For example, (Zhang et al., 2020) stressed that a strategic balance must be managed between CSR conformity and CSR emphases. This balance entails meeting the expectations of various stakeholder groups to achieve a sufficient level of legitimacy while simultaneously differentiating the firm’s CSR strategy to achieve a level of distinctiveness that sets the firm apart from its peers. Tang et al. (2012) argued that unless firms continuously and equitably include all stakeholders in their CSR policies, they are less likely to benefit financially from their CSR investments. In the same vein, Hawn and Ioannou (2016) found that the attention gap in the firm’s efforts devoted to different groups of stakeholders contributes significantly and negatively to the financial returns of those CSR investments. Wang and Choi (2013) theorized that the firm’s inconsistent CSR practices could be detrimental to the firm’s financial performance and discovered that the firm’s temporal and inter-domain inconsistency could have a significant and negative moderating effect on the relationship between the firm CSR and financial performance.

In light of such findings, the CSR literature should place more emphasis on the dynamics of CSR characteristics. Specifically, we argue that how firms conduct themselves socially and the characteristics of their social responsibility investments are critical concerns if we are to advance CSR research. While researchers have begun to identify CSR consistency as an important characteristic of CSR strategy that impacts the effectiveness of such strategies, little is known about various factors that contribute to CSR consistency. As an initial step in this direction, the current study focuses on the effect of women CEOs and board gender diversity on the firm’s CSR temporal and inter-domain consistency.

Theory and Hypothesis Development

The Effect of Women CEOs on Firm’s CSR Temporal and Inter-domain Consistency

Do women leaders exhibit consistent behavior toward CSR issues over time? Despite the lack of specific research or empirical evidence suggesting that women CEOs commit to specific CSR practices over time, there are theoretical reasons to predict that women will demonstrate behavioral consistency in their approach to CSR strategies. We argue that social role expectations help us develop our theoretical predictions that women CEOs tend to engage in CSR activities more consistently. For example, research shows that social role expectations prompt women leaders to engage in social issues (e.g., CSR, DEI issues, corporate misconduct, etc.) more than their male counterparts, and overall, women’s leadership actions positively affect those contexts (Aabo & Giorici, 2022; Liu, 2021). Equipped with these findings, corporations with women leaders have been improving their diversity efforts and CSR initiatives over the years, albeit slowly. Women CEOs face harsher performance evaluations and perceptions than their male counterparts due to social role expectations (Yang & del Carmen Triana, 2019; Vial et al., 2016). For example, Moake and Robert (2022) found that women face narrower social role expectations and have less social latitude in their use of humor at work despite their high organizational status. Vial et al. (2016) showed that men are perceived as more legitimate “power-holders” than women. Unless women “power-holders” legitimize their position, they face more challenges than men in garnering their subordinates’ respect and status/admiration.

Experiencing such biases, both implicit and explicit, will act as a cautionary tale for women leaders and help them choose what aspects of their background, personal beliefs, propensities, and experiences should be brought into organizational settings as part of their behavioral consistency. Given that they are constantly faced with social role-ridden dilemmas in their daily corporate decision-making, it is precarious for them to exhibit eccentric behaviors. Hence, women CEOs may feel the need to legitimize their role and earn the respect of others through consistent behaviors over time to showcase their worth to the firm stakeholders. As a result, women CEOs’ behavioral consistency in caring for various firm stakeholders should translate into CSR temporal consistency for their firms. Based on these arguments, we hypothosize that women CEOs will promote a consistent CSR policy that meets the demands of firm stakeholders over time. More formally:

Women CEO presence will be positively related to CSR temporal consistency. The logic of social role and behavioral consistency theories also suggest that women CEOs are more likely to engage in inter-domain consistency in their CSR activities. Social role theory suggests that women are more responsive to the needs of others and more likely to feel responsible for not harming others (Konrad & Kramer, 2006; Setó-Pamies, 2015; Zhang et al., 2013). Thus, women leaders are more adept at attending to and balancing the needs of various firm stakeholders. For example, women or more likely to show empathy, especially to those who face biases and stereotypes in their work life (Dadanlar & Abebe, 2020). Despite women’s documented tendency to exhibit more pro-social behaviors, other studies report that in some contexts women suffer the same ethical shortcomings as men (Ellemers et al., 2004; Kennedy et al., 2017). For example, Kennedy et al. (2017) show that although women tend to internalize ethical behavior into their identities more than men, women act similarly to men when attractive financial incentives are present. Additionally, women’s tendency to act morally may be driven purely by social roles rather than a genuine commitment to one’s moral values (which is beyond the scope of this study). Women leaders may exhibit such behaviors to avoid backlash from organizational actors and society. Such examples demonstrate how social role expectations may manifest themselves in women leaders’ personal and professional lives through behavioral consistency. Other scholars report that women leaders tend to engage in greater supervision and monitoring, and they seek to protect the interests of all stakeholders (Fondas & Sassalos, 2000; Watson et al., 1993). For example, Nielsen and Huse (2010) suggested that “women’s attention to and consideration of the needs of others may lead to women’s active involvement in issues of a strategic nature that concern the firm and its stakeholders” (p.138). Women leaders have been shown to positively influence the firm’s overall level of CSR commitment during the development of corporate social responsibility policies (Bear et al., 2010; Cook & Glass, 2016, 2018). Additionally, women are more aware of and committed to environmental concerns (Wehrmeyer & McNeil, 2000), more protective of the environment, and more ecologically conscious (Park et al., 2012). Davidson and Freudenburg (1996) found strong support for the notion that women tend to express more significant concern than men about the health and safety implications of any given level of technological risk. Women, therefore, are more likely to take measures that would be aimed at reducing risks, increasing the welfare of others, and positively addressing environmental and social concerns (Ciocirlan & Pettersson, 2012; Mainieri et al., 1997; Park et al., 2012). These findings showcase how women leaders exhibit behavioral consistency across CSR-related contexts such as environmental concerns (Wehrmeyer & McNeil, 2000), corporate diversity misconduct (Dadanlar & Abebe, 2020), social concerns (Jouber, 2022), diversity in corporate C-suites and boards (Byron & Post, 2016; Helfat et al., 2006; Sheridan & Milgate, 2005; Terjesen et al., 2009) and so on. In summary, women CEOs are more likely to promote a consistent CSR policy that meets the demands of various firm stakeholders and we hypothesize:

Women CEO presence will be positively related to CSR inter-domain consistency.

The Moderating Effect of Board Gender Diversity

Board gender diversity is the extent to which a company’s board of directors includes a composition of women and men directors. It is common practice across corporate boards that the CEO also sits on the board as an insider director. Hence, women CEOs commonly contribute to the gender diversity of the board. Studies have shown that women in leadership positions, including CEOs, are associated with stronger business practices and equity initiatives (Glass & Cook, 2017). In advancing their careers, women in CEO positions are more inclined to encounter workplace discrimination themselves (Bigelow et al., 2014) or be aware of coworkers subjected to dysfunctional workplace behaviors (Bell & Nkomo, 2001). These firsthand experiences equip them with a more profound comprehension and empathy regarding the detrimental impacts of workplace discrimination, as such behaviors tend to diminish employees' productivity and engagement with organizational activities (Volpone & Avery, 2013). Hence, because non-CEO women directors may face similar social role expectations and pressures as women CEOs (Bigelow et al., 2014), they can readily empathize with women CEOs and show similar behavioral consistency during board deliberations. Considering these arguments and findings, we examine whether women directors who may be similarly affected by social role expectations like women CEOs exhibit behavioral consistency to align with women CEOs and promote CSR temporal and inter-domain consistency. Unpacking the contingency effect of board gender diversity on women CEO-CSR consistency relationship not only enriches the scholarly conversation on gender diversity and CSR relationship but also help us earth the intricate and dynamic nature of corporate governance.

Research has shown that women CEOs feel more empowered when their firms have more women directors on their boards (Cook & Glass, 2015). Additionally, women directors on the board create a psychologically safe environment for other women leaders and catalyze their emboldened decision-making (Cook & Glass, 2016). For example, Milliken and Martins (1996) suggested that the beneficial effects of gender diversity in board decision-making can be attributed to at least three influences on decision-making processes: supporting a broader range of alternative viewpoints, enabling more effective communication, and encouraging a more thorough analysis of organizational decisions, that lead to more effective decision-making and problem-solving processes. For example, gender diversity increases the number of alternative viewpoints during board deliberations by bringing various skills and perspectives into focus (Harjoto et al., 2015). Minority directors (demographic minority) contribute to board decision-making processes by providing different angles/viewpoints and thus provoking the status quo held by majority directors (Westphal & Milton, 2000). It is no surprise that the large presence of majority directors has coincided with the dominance of shareholder strategy over stakeholder strategy because shareholder strategy emphasizes maximizing shareholder returns while stakeholder strategy emphasizes balancing the needs of other stakeholders with shareholder returns. Thus, board gender diversity disrupts the majority director status quo while empowering women CEOs and supporting their continuous efforts to adopt consistent CSR practices.

Because women CEOs are regarded as minority business leaders, their ability to implement desired organizational change rests on two factors: (1) the presence of various similar minority group members with official positional authority within the organization; and (2) the comparative impact of similar minority leaders (Cohen & Huffman, 2007; Cotter et al., 1997). According to Torchia et al. (2011), women on corporate boards will enhance the board’s ability to make high-quality decisions because greater board gender diversity will increase the consideration of alternative solutions. The literature also suggests that the success of women CEOs depends, at least in part, on their ability to empower their women counterparts and colleagues within the organization (Baker & Cangemi, 2016; Cook & Glass, 2016). Thus, having women directors on the board will increase the quality of decisions and may affect the solution to complicated issues such as CSR activities or disclosures.

Investigating the intersection of gender diversity, the decision-making process, and board dynamics is essential. It lays the foundation for how social role expectations are manifest in women’s behavioral consistency in organizational settings. The joint effects help women manage various firm stakeholders’ demands (interdomain consistency) in CSR activities over time (temporal consistency). Consistent with the social role and behavioral consistency tenets, board gender diversity will heighten the firm’s potential to manage conflicts among various stakeholders as they tend to bring diverse skills and prior experiences into the workplace. For example, Zhang and associates’ (2013) research shows that a larger representation of outside and women directors are related to better CSR performance within a firm’s industry. Glass et al. (2016) found that firms with gender-diverse leadership teams are more likely than other firms to pursue environmentally friendly strategies. Additionally, women directors tend to care more about the CSR orientations of their firms because they are more sensitive to CSR reputational effects (Hyun et al., 2016). Rao and Tilt’s (2016) literature review on the relationships between board gender diversity and organizational strategies stressed the importance of studies that link gender diversity and CSR decision-making processes. Landry et al. (2016) found that a greater presence of women directors predicted whether the firm will appear in prestigious company recognition lists (i.e., the most admired companies, the most ethical companies, the best companies to work for, and the best corporate citizens). It is plausible to argue that getting into these lists would require firms to showcase their frequent and meaningful efforts in CSR-related issues.

Finally, Byron and Post’s (2016) a meta-analysis of 87 independent samples reported a positive relationship between women’s board presence and social performance among boards when there are shareholder protections and gender parity. This study alone highlights how women directors engage in CSR inter-domain consistency (across stakeholders given the diverse set of studies in the meta-analysis) and temporal consistency (across time given the longitudinal study findings). Consequently, the greater representation of women on the boards can ensure the effectiveness of the board in dealing with issues of CSR overall (Nielsen & Huse, 2010; Setó-Pamies, 2015; Williams, 2003) and their commitment to rally around women CEOs in their pursuit to engage in CSR temporal and inter-domain consistency.

Based on the above discussion, we posit that board gender diversity will further empower women CEOs to promote a consistent CSR practice and propose:

In firms with greater board gender diversity, the relationship between women CEO presence and CSR temporal consistency will be stronger.

In firms with greater board gender diversity, the relationship between women CEO presence and CSR inter-domain consistency will be stronger.

Method

Sample and Data Sources

This study focuses on the S&P 500 firms from the year 2001–2013. We began with 5,330 observations for which financial and CEO information are available. Data for the corporate financial features and CEO characteristics were drawn from Standard & Poor’s Compustat North America Fundamental Annual and Execucomp databases. CSR information from KLD Stats was used to measure the dependent variables and several relevant control variables. We merged this initial panel data with KLD Stats using CUSIP and year ended our sample in 2013 because this is the last year for which KLD published CSR data and reduced our sample to 4,151 total observations. Based on CUSIP, annual corporate governance-related information was drawn from GMI Ratings which began reporting data in 2004. This restricted our sample to 3,164 observations between the years 2004 and 2013.

Although information from GMI Ratings is available from 2004 onward, we had access to KLD data preceeding 2004. Thus, we were able to begin computing temporal consistency, which is based on information for the last five years with information beginning in 2001. This limited the number of observations lost to unavailable data. Following the existing literature (Gupta et al., 2018; Malm & Krolikowski, 2017; Peters & Taylor, 2017), we also dropped observations from firms in several incompatible industries [electric, gas, and sanitary services (SIC codes 4900-4999); finance, insurance, and real estate (SIC codes 6000-6999); and public administration (SIC codes 9000+)] because these industries are highly regulated and employ different accounting procedures. Further, because a CEO may need help to exercise true power in her or his first year in the office (Chen et al., 2019; Chin et al., 2013), we delete observations with a CEO tenure of less than one year. These procedures reduced our sample size to 2,139 observations over the 2004-2013 period.

The Sample Industry Coverage.

Source: Divisions are as defined by Occupational Safety and Health Administration.

Measures

Construct Validity

The CSR-related measures in the current study are based on four dimensions – environment, community, employee, and diversity. The first two dimensions assess external stakeholders and the other two dimensions assess internal staketholders. Like most existing studies, the multi-item measure is preferred over the single-item because our sample is of moderate size, the average interitem correlation is .28, and Cronbach’s alpha is .60 (Diamantopoulos et al., 2012). Further, a confirmatory factor analysis of a four-factor measurement model is employed to examine the validity of our construct. The χ2 (2) statistic is 3.32 with a .191 significance level; root mean squared error of approximation, pclose, and standardized root mean squared residual is .030, .645, and .016; and comparative fit index and Tucker-Lewis index are .996 and .988, respectively. All these statistics support the goodness of fit for the model.

Dependent variables

Temporal consistency and inter-domain consistency. The variables are generated following Wang and Choi (2013). We define CSR as the set of voluntary actions (i.e., not legally mandated) that the firm undertakes to address the concerns and demands of its various stakeholders. The four major dimensions that most previous studies have adopted are included in this study. Prior studies have regarded the firm environmental CSR, employee CSR, community CSR, and governance as the most influential activities and stressed that most firms prioritize these four categories of activities (Chih et al., 2010; Chin et al., 2013; Cook & Glass, 2018; Kim et al., 2020; Wang et al., 2022). Thus, using these four dimensions to capture the firm’s actions is a meaningful approach for assessing the consistency of the firm’s CSR behaviors with respect to major stakeholders.

To compute the consistency measures we first regressed the latest five years of net CSR from each stakeholder domain (environment, community, employee, and diversity) against time to obtain standard errors. For illustrative purposes, we use the following regression model.

Again, we followed Wang and Choi (2013) to generate inter-domain consistency. The inter-domain consistency score is the variance of in the standardized social performance scores for each of the four CSR dimensions. We use the natural logarithmic transformation of the score to correct for skewness.

Independent Variable

Women CEO Presence. Women refer to a binary item related to CEO gender (Martin et al., 2020). The variable equals 1 if a CEO is a woman and 0 otherwise.

Moderating Variable

Board gender diversity. Board gender diversity refers to the proportion of women on the board. We measured this variable by dividing the number of women directors on the board by the total number of board members (Abebe & Dadanlar, 2019).

Control Variables

Several control variables are included in all models. We control for board independence, defined as proportion of outside directors to the total number of directors, because outside directors play a key role in satisfying different stakeholders in society through promoting CSR and the prevalence of outside directors is an indicator of a CEO’s structural power (Chen et al., 2019; Petrenko et al., 2016). We control for board size, operationalized as the natural logarithm of the total number of directors on a company’s board, because it improves firms’ social performance (Aggarwal & Nanda, 2004). CEO tenure is the natural logarithm of the number of years as the CEO at the focal firm and an indicator of a CEO’s structural power (Chen et al., 2019; Petrenko et al., 2016). CEO age, the natural logarithm of the number of years, was included as a control because it has been shown to be related to CSR practices (Li et al., 2020; Malik et al., 2020). CSR level is measured as the average of the standardized net scores (strengths minus concerns) on four dimensions – environment, community, employee, and diversity (Wang & Choi, 2013). These four strands of CSR cover both external and internal stakeholders’ concerns. CSR trend is the coefficient on the CSR level obtained by regressing against time (Wang & Choi, 2013) and included as a control variable because the CSR trend is likely to be associated with both consistencies.

Previous researchers have also noted the importance of market performance, size, leverage, R&D intensity, advertisement intensity, and time-series variation in determining firm-level CSR-related activities (Chen et al., 2019; McWilliams & Siegel, 2000). Hence, we also include Tobin’s Q, the market value of a firm’s common stock plus the book value of its preferred stock and debt scaled by the book value of its total assets (Lim & McCann, 2014). Firm size is measured as the natural logarithm of a firm’s total assets (Jo & Harjoto, 2011). We control for leverage by including the ratio of a firm’s total debt to its total assets (Chen et al., 2019). Following tradition, R&D intensity, R&D expenses scaled by total assets (McCarthy et al., 2017), advertisement intensity, advertisement expenses scaled by total assets (McCarthy et al., 2017), and time trend (represented with year dummies) (Chen et al., 2019) are used as control variabless. Following the existing literature, missing information on advertisement expenses is replaced by 0 (Koh & Reeb, 2015). As a robustness check a dummy variable (equals 1 or 0 if non-missing or missing, respectively) is included in all regressions. However, we exclude the dummy variable in the main results’ regressions to save degrees of freedom.

Model and Estimation Method

Tan et al. (2017) recommend either pooled OLS or the fixed effects (FE) or the random effects (RE) models to analyze panel data. A general form panel data is:

Applying pooled OLS to this time-demeaned FE model yields consistent fixed effects or within estimators because

Results

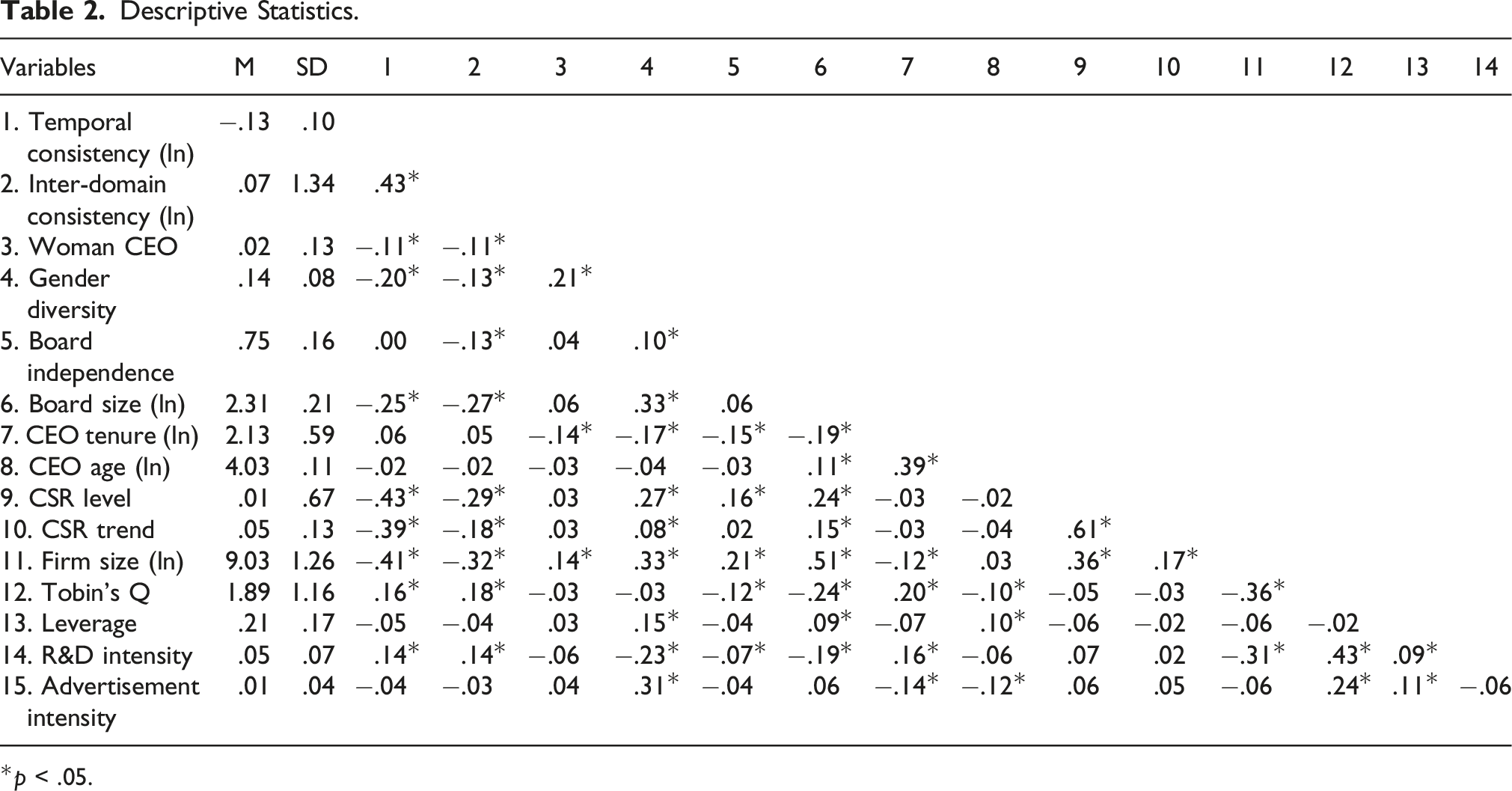

Descriptive Statistics.

*p < .05.

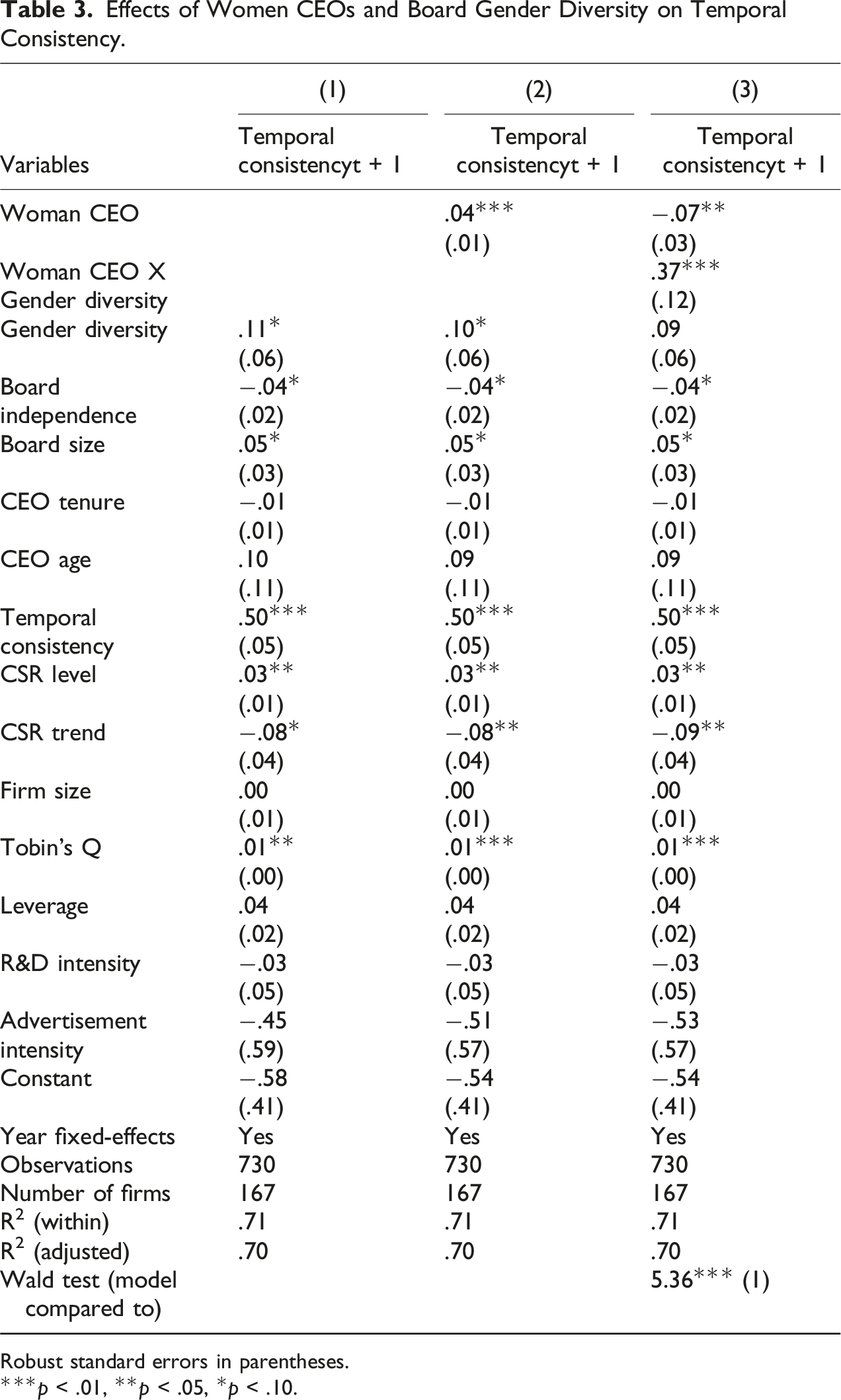

Effects of Women CEOs and Board Gender Diversity on Temporal Consistency.

Robust standard errors in parentheses.

***p < .01, **p < .05, *p < .10.

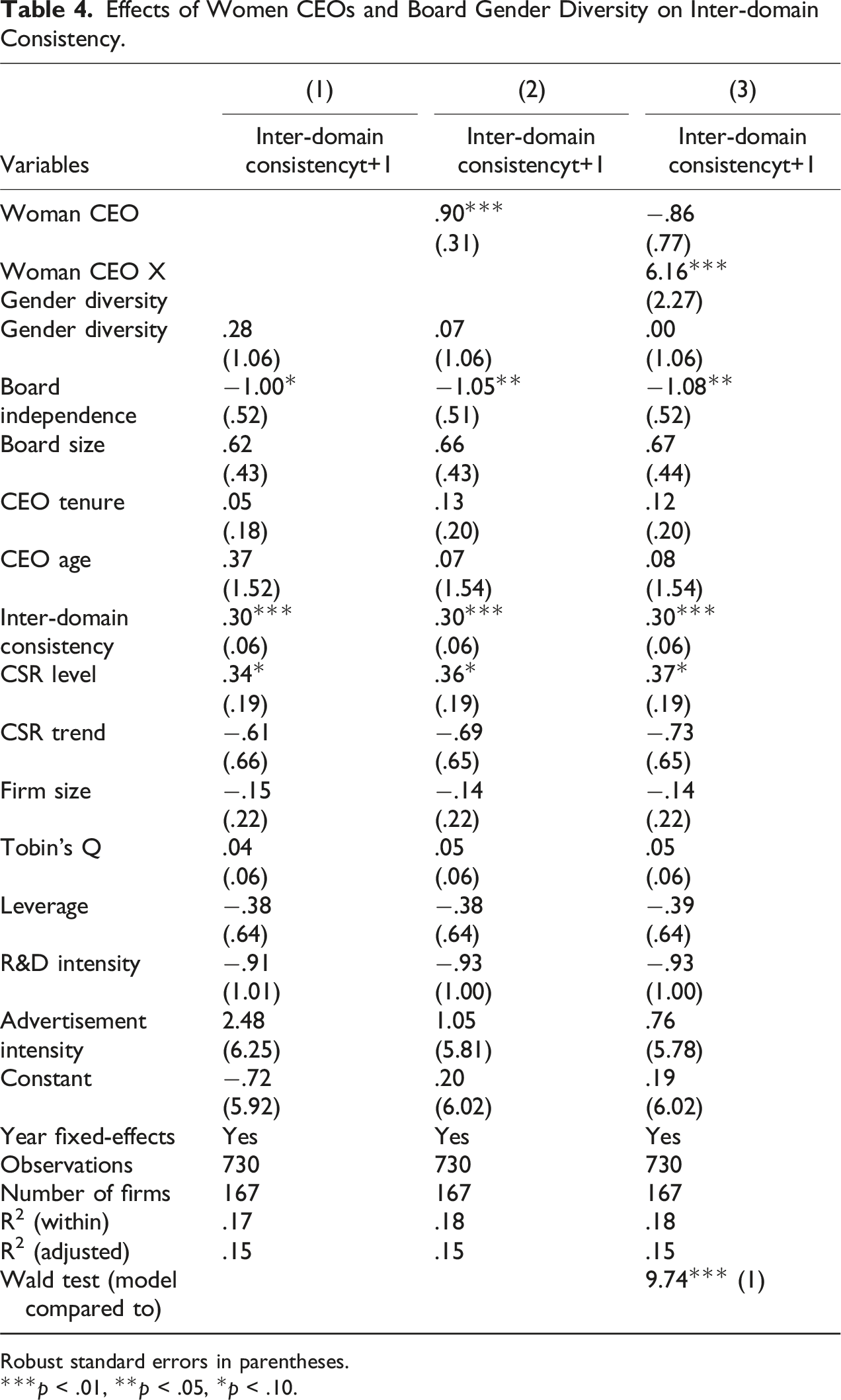

Effects of Women CEOs and Board Gender Diversity on Inter-domain Consistency.

Robust standard errors in parentheses.

***p < .01, **p < .05, *p < .10.

Given that little research has compared the consistency of women CEOs behavior with that of men CEOs, these findings offer new insight into this topic. Future research will be needed to clarify whether such consistency can hold across the political activity and CSR domains of non-market strategies. Moreover, although prior research has shown that such consistency influences a firm’s financial performance, the current results support the idea that women CEOs can be more efficient in CSR resource allocation and materialization of the firm’s CSR investments. This provides additional evidence documenting women’s unique value in senior positions.

Hypothesis 2a suggests that the greater the board gender diversity, the stronger the women CEO-temporal consistency relationship. Board gender diversity strengthens the positive impact of women CEOs on temporal consistency as indicated by the positive and statistically significant (p < .01) interaction term in Model 3 of Table 3. Similarly, board gender diversity appears to strengthen the positive connection between a woman CEO and inter-domain consistency as reflected through the positive statistically significant coefficient on the interaction term (p < .01) in Model 3 of Table 4. Here, our result corroborates other scholars’ findings that women leaders act as sounding boards and support each other (Konrad, et al., 2008; Terjesen et al., 2009). For example, Terjesen et al. (2009) found that a critical mass of women on the board empowers fellow women directors in their governance and monitoring responsibilities.

We are also sensitive to the reports of others that women managers may experience a ‘queen bee’ effect from other women colleagues as described by Derks et al. (2016). The queen bee phenomenon occurs when women executives dissociate themselves from other women holding more junior-level managerial roles to counter gender stereotypes (Derks, et al., 2016). Our study’s findings support the arguments that board gender diversity helps women CEOs in their quest to implement firm strategies, but provide no evidence of queen bee effects among members of the firm’s upper echelon.

Further, significant Wald test results in both interaction models in Table 3 and Table 4 signify the importance of the additional variables with respect to the first model, base or control model, in each table.

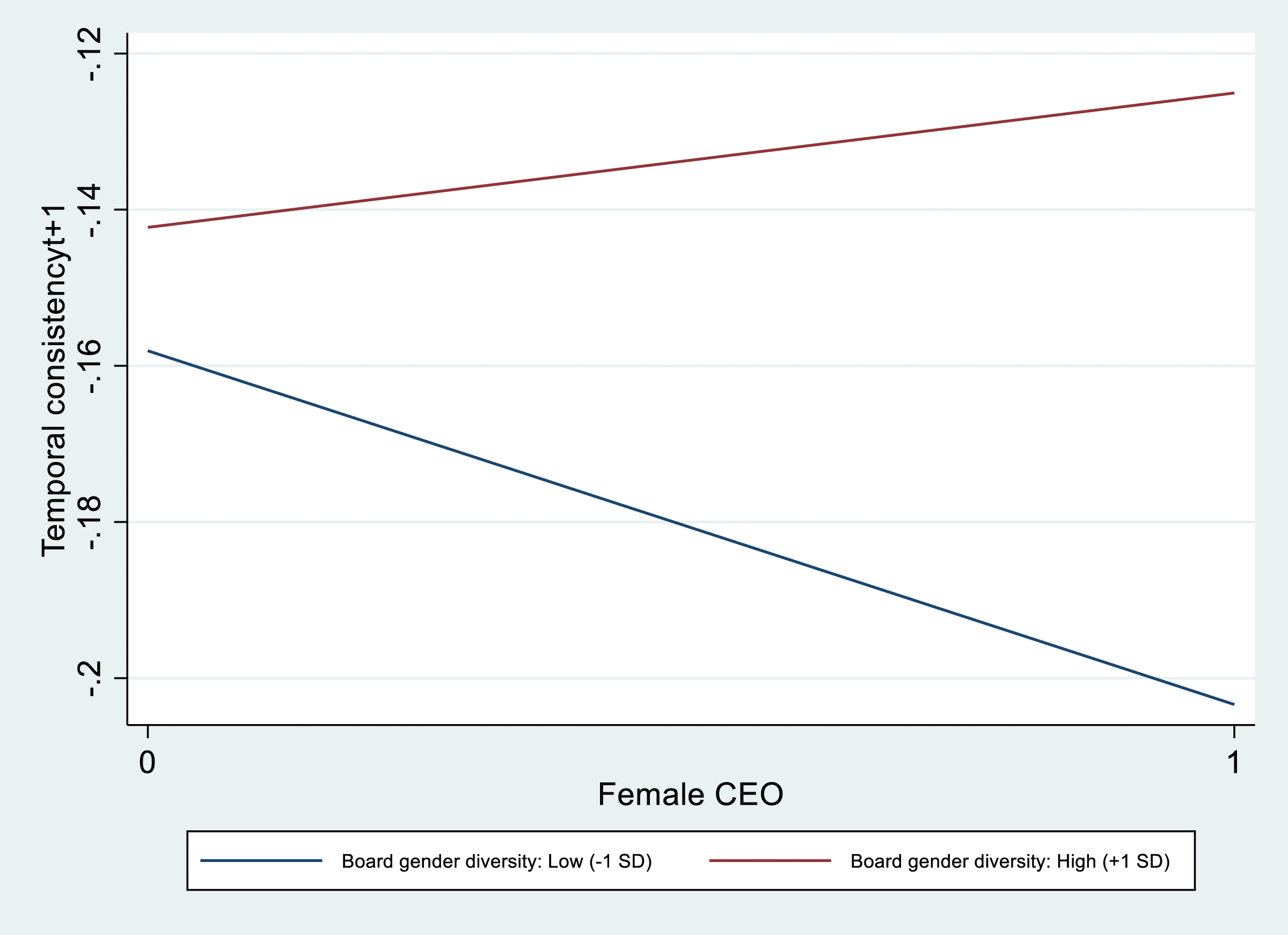

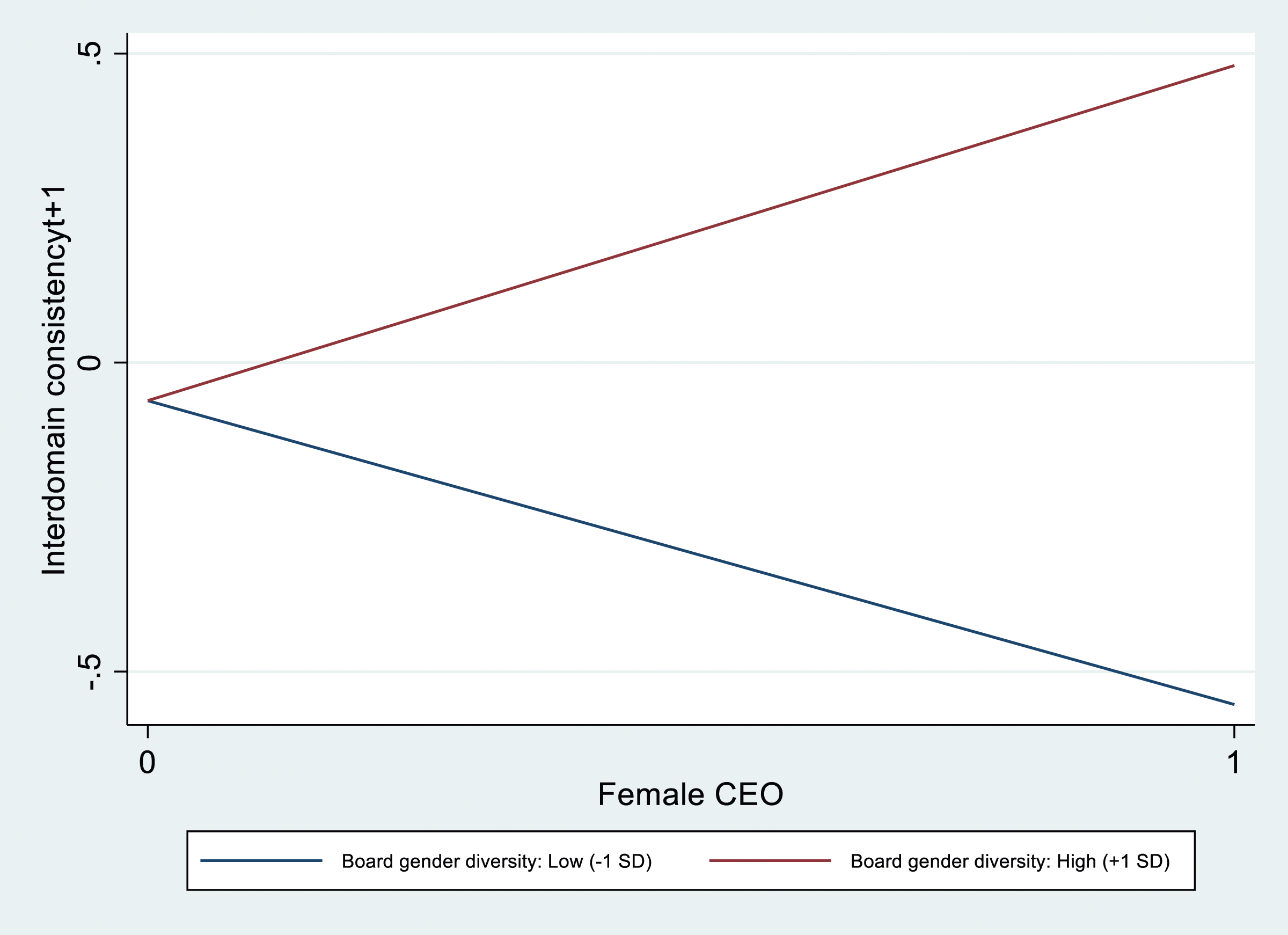

We plot the interaction between women CEOs and board gender diversity using one standard deviation above and below the mean of board gender diversity. As shown in Figure 1, based on the magnitude of board gender diversity on the board of directors, the presence of women produces very different outcomes. Women CEOs are more effective in improving a firm’s temporal consistency when more women directors are on the board. This revelation is consistent with our prediction supporting Hypothesis 2a. The interaction between women and board gender diversity in predicting inter-domain consistency is shown in Figure 2. Like Figure 1, the presence of women is positively associated with inter-domain consistency when board gender diversity is high. However, the association becomes negative when board gender diversity is low, confirming Hypothesis 2b. The effects of woman CEOs on temporal consistency: The moderating role of board gender diversity. Effects of women CEOs on inter-domain consistency: The moderating role of board gender diversity.

Endogeneity Check

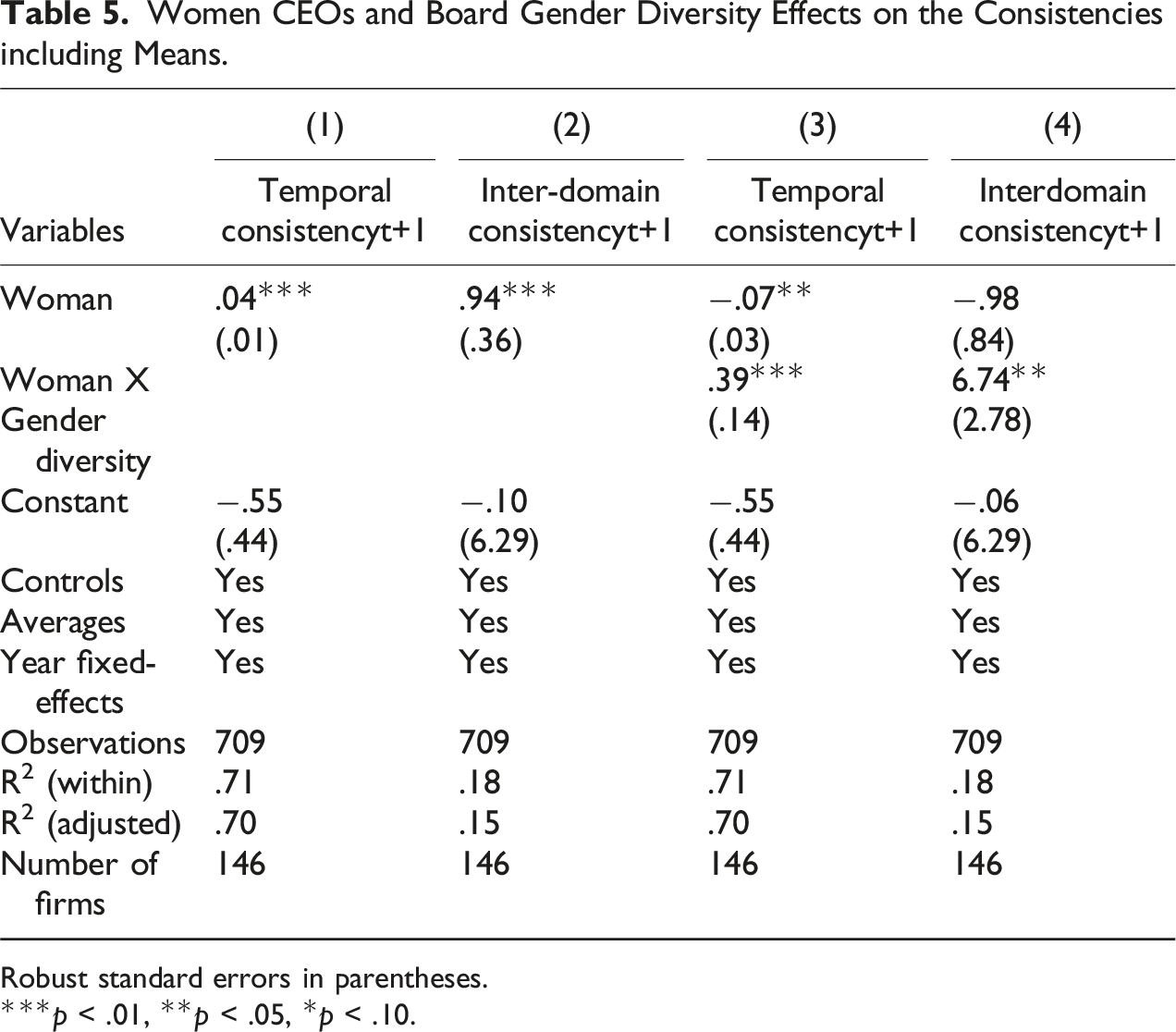

Women CEOs and Board Gender Diversity Effects on the Consistencies including Means.

Robust standard errors in parentheses.

***p < .01, **p < .05, *p < .10.

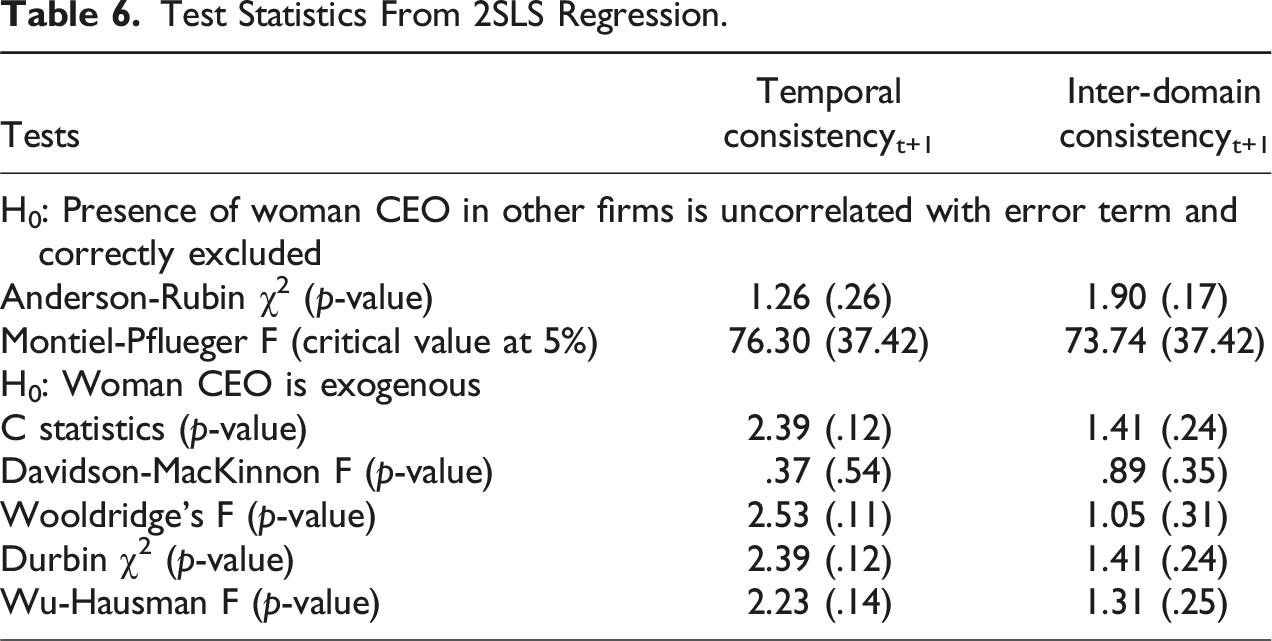

Reverse causality exists because the relationship of interest runs both ways – a woman CEO improves CSR consistencies, and a woman CEO may self-select in a company with higher CSR consistencies. Hence, we resort to the instrumental variable approach to ensure that the observed woman CEO-CSR consistency relationships do not result from endogeneity. As an instrument, we include a dummy variable indicating the presence (equals 1) or absence (equals 0) of at least another woman CEO in a focal firm’s primary industry in the first-stage model. Industry hiring trend should impact a firm’s CEO choice without affecting its CSR consistencies levels.

Test Statistics From 2SLS Regression.

Robustness Check

We conducted robustness tests by rerunning all models with alternate measures of firm financial performance (ROA, ROE, ROI, ROS), alternate measures of firm size (the natural logarithm of the firm’s employees and the natural logarithm of the firm’s net sales), the natural logarithm of different measures of leverage (book value scaled by market value of equity, total liabilities scaled by total assets, and long term debt scaled by total assets), the natural logarithm of R&D intensity (R&D expenses scaled by either number of employees or net sales), and the natural logarithm of advertisement intensity (advertisement expenses scaled by either number of employees or net sales). The results were unchanged – a woman CEO’s presence improves both temporal consistency and inter-domain consistency, and board gender diversity strengthens these affirmative relationships. Additionally, our main effects results remain strong even after replacing board gender diversity with Blau’s index of heterogeneity or a dichotomous measure showing the presence (equaling 1) or absence (equaling 0) of at least one woman on board. The results are available upon request.

Discussion and Implications

Prior studies have linked women CEOs and directors to a better overall CSR profile. We have suggested that, at least in the context of non-market strategies, such findings may be related to greater CSR consistency on the part of women CEOs and empirically examined whether gender differences help to explain varying levels of CSR consistency across firms. Our efforts were partly stimulated by the attention that researchers, practitioners, and the media are focusing on the importance of a firm’s CSR consistency over and above a firm’s CSR activity levels. We used inter-domain and temporal consistency as the two components of the firm’s CSR consistency and examined the relationship between women CEOs and these consistency components. We found that women CEOs are more able to maintain higher temporal and inter-domain consistency than men. This is particularly important given that recent research has shown that higher levels of CSR may not help firms reap the desired financial benefits and that both inter-domain and temporal consistency in the firm’s CSR practices may play a significant role in determining the extent to which firms benefit financially from their CSR strategies (Wang & Choi, 2013). Moreover, such findings indicate that women CEOs are more likely to contribute to a sustainable positive image of the firm in the eyes of stakeholders and the media, which is particularly important and has significant implications for the firm in the short and long term. A sustainable positive image for the firm can be a source of competitive advantage because it is difficult to replicate (Wang & Choi, 2013).

A second purpose of this study was to examine whether board gender diversity, measured as the percentage of women serving on the board, facilitates women CEOs’ efforts to accomplish their agendas. A key question regarding women in the upper echelons has always been whether women on the board can help women CEOs enact their agendas. In the context of our study, our goal was to examine whether that is the case with the firm’s CSR consistency. We find that firms led by women CEOs with greater gender diversity on their boards exhibit higher temporal and inter-domain consistency levels. This is particularly important given the conflicting evidence on the role of women directors in enabling/hindering the success and the enactments of women CEOs’ agendas (Cook & Glass, 2018; Saggese et al., 2021; Wang & Kelan, 2013; You, 2019). Our results support the notion that gender diversity on the board accentuates the effectiveness of women CEOs.

The findings of this study also support increasing the number of women CEOs and women serving as corporate directors. Based on the results of the current work, increasing the number of women in the upper echelon of a firm may translate into a source of competitive advantage for the firm. Our findings suggest that women CEOs are more likely to help firms achieve an inimitable advantage by performing consistently in the social domain. Such consistency has been previously shown to significantly affect the extent to which firms can materialize their CSR investments and also help firms achieve relational capital with key stakeholder groups (Wang & Choi, 2013). Our findings also suggest that promoting more women to the board of directors in corporations enhances the efforts of women CEOs to achieve CSR consistency. These tangible effects of increasing gender diversity in the upper echelons support the moral case of advancing women CEOs and women on board (Burgess & Tharenou, 2002; Burke, 1997; Kakabadse et al., 2015; Terjesen et al., 2009).

At the application level, our results suggest that firms will benefit from greater systematic efforts to create career paths that advance women into the upper echelon. The barriers women encounter as they push into the upper echelons are well documented. Much of the relevant work has focused on the factors that prevent women from occupying executive positions and also on factors that hinder their success (Brinkhuis & Scholtens, 2018; Cowen & Montgomery, 2020; Dwivedi et al., 2018b; Elsaid & Ursel, 2018; Ho et al., 2015; You, 2019). Previous research has revealed that women are under-represented in the corporate upper echelon as the result of two primary constraints. First, women encounter difficulties trying to push through the glass ceilings because of their numerical underrepresentation in the upper echelons (Dwivedi et al., 2018a; Kanter, 1993). Second, women are less likely to succeed in the CEO role because of the stereotypical expectations regarding what is required to be a successful leader (Eagly & Karau, 2002; Koburtay et al., 2019; Koenig et al., 2011).

More recent research has focused on explaining why women can and should be given more chances in the upper echelons and how they can add value to their organizations (Baker & Cangemi, 2016; Cook & Glass, 2016; Ho et al., 2015; Ingersoll et al., 2019). While this research has provided a compelling rationale that should encourage firms and shareholders to promote women into leadership positions, the ongoing underrepresentation of women in top executive roles suggests that firms need to be faster to assimilate the research findings into organizational practices.

Future Directions and Limitations

Despite the consistent support the results of the current study provide for the theoretical arguments (Bear et al., 2010; Ciocirlan & Pettersson, 2012; Wehrmeyer & McNeil, 2000), the generalizability of our results must be evaluated in the context of several potential limitations. For example, the current sample was restricted to publicly traded corporations with highly diverse ownership. Thus, independent of gender, each firm’s CEO faces formidable social, political, and legal constraints that may limit the ability of the CEO to craft and execute CSR strategies. To overcome this limitation, we suggest a comparative study of the CSR strategies between firms wholly or largely owned by women versus similar firms that men wholly or largely own. Such a study would provide additional insight into the strength of the gender effect on temporal and inter-domain CSR consistency and clarify the effects of such consistency on a firm financial performance.

A related limitation is that women currently occupy only a few upper-echelon positions in corporate America (Baker & Cangemi, 2016). Thus, while we have included as representative a set of corporations as possible, there is a chance that companies with more women in the upper echelons are “more progressive” and thus more inclined to engage in CSR. Further, such companies may also be inclined to be more inclusive with respect to the breadth of stakeholder groups included in the firm’s CSR engagement activities. Thus, future studies in this arena should explore the overall socio-political belief profile of the board to determine how political agendas interact with board gender diversity.

A third limitation is that the arguments in the current study inadvertently treat gender diversity as an independent and the primary dimension of diversity. Clearly, other dimensions are as important and as visible as gender. Members of these other minority categories are as under-represented as women in corporate upper echelons. Future studies need to examine a more complex pattern of diversity to understand better the effects of overall diversity on CSR strategies and tactics. Such studies may reveal, for example, that different patterns of diversity may relate differently to different CSR engagement patterns. For example, while gender diversity is related to both temporal and inter-domain consistency, ethnic diversity might be related to inter-domain consistency but not temporal consistency.

The generalizability of the current results is also limited because the current sample was restricted to the U.S. and thus constrained by US cultural norms. In the global context, the US is less accepting of women in high-level leadership positions than many other developed economies. As a result, the supporting role played by women board members may be far more important to women CEOs in the US than in these other countries. Where women are more culturally accepted in leadership positions, a single woman, either as the CEO or board member, may have a stronger ability to influence the pattern of the firm’s CSR strategies. Thus, we suggest that the current work be replicated in studies more accustomed to women’s leadership, possibly in countries such as the UK or Germany, where women have been elected to the highest government leadership positions.

Finally, future researchers need to conduct more fine-grained investigations to flesh out the contextual factors and individual differences that drive our observed effects. For example, although our results provide strong support for board gender diversity research, investigating the threshold effects of gender diversity on boards would provide additional insights into this research stream. Specifically, drawing on critical mass perspectives, future work can examine how many women directors are needed to affect organizational outcomes (e.g., CSR in our case) and/or rally support around women CEOs to promote and implement their vision and priorities. The underlying causal variables for the effects we observed might also be the result of social differences associated with an individual’s upbringing and early professional development. Indeed, several studies have already speculated that many of the differences between genders that we observe in the workplace result from development differences rather than physiological differences.

Another potentially crucial micro-level variable that seems to vary systematically by gender is risk propensity. The literature suggests that men CEOs are more risk-taking than women CEOs (Elsaid & Ursel, 2011; Faccio et al., 2016), and these differences in risk preferences result in different strategic priorities and preferences between men and women CEOs. Having different priorities means that men CEOs are more likely to change their temporal focus depending on the external and internal circumstances and key factors that they use to assess situations. Non-market and market strategies of the firm are among the key areas where the CEO makes the final decisions for the firm. Given the different preferences that men CEOs have, it is possible that the men CEOs grow accustomed to change and downplay the importance of consistency in certain types of policies that are aimed at the firm’s larger base of stakeholders.

We should also note that some inconsistencies may be necessary. For example, firms that face negative performance feedback and external or internal challenges might need to engage in fundamental changes requiring a completely different set of actions and behavior. This type of change might be later labeled as inconsistency, but it is necessary and important for the firm in the dynamic and very competitive business environment. Such environmental adaptation may be necessary to maintain environmental fit. Thus, not all inconsistencies are detrimental to the firm.

Given that most CEOs in the corporate world today are men it might be the case that men CEOs get accustomed to change, even if when it is not good or may not be well-received outside the company. For example, men CEOs seem to change the stakeholder focus of their CSR policy and tend to have larger variations over time, and that could be due to resource allocation or different temporal priorities that vary over time. As additional micro-level causal variables are revealed in future work, a greater effort can be made to design different developmental experiences into young professionals' early career paths that help balance the competing benefits of dynamic capability and strategic consistency.

Conclusions

While an increasing number of authors have examined the unique challenges women face as they enter the upper-echelons, most of the resulting studies have focused either on the personal success of upper-echelon women executives or the financial outcomes of firms with greater levels of upper-echelon gender diversity. Like previous research, our findings indicate that gender diversity does explain managerial differences in firm behavior and that multiple women in the firm accentuate these effects. More importantly, our study extends gender diversity research in two different directions. First, while the previous studies of been most concerned with market-oriented activities, such as competitive strategies or operating decisions, we focused on a non-market context, CSR strategy, and engagement. Second, we suggest that it is not the magnitude-specific content of the CSR strategy that is affected by gender diversity but rather the pattern of CSR engagement, which we capture as temporal and inter-domain consistency. Our results demonstrate that greater gender diversity at the highest levels of the firm leads to the more consistent strategic implementation of a key non-market strategy, resulting in better social relations for the firm and, ultimately, better financial performance. Future research can now extrapolate our general findings to the market context to see how different levels of gender diversity affect the patterns of strategy-making and implementation and whether differential strategic patterns have implications for long-term firm performance.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Data Availability Statement

The data that support the findings of this study are available from several third parties which are listed in detail in the method part but restrictions apply to the availability of these data, which were used under license for the current study, and so are not publicly available. Data are however available from the authors upon reasonable request and with permission of the parties mentioned in the method section.