Abstract

This study examines how gender diversity on nonprofit boards relates to chief executive officer (CEO) compensation using data of 1,835 501(c)(3) organizations with the GuideStar Platinum Seal of Transparency. The analysis reveals a positive association between women’s representation on a governing board and female CEO compensation until women’s proportion reaches 82%. By contrast, there is a negative relationship between women’s representation on boards and male CEO compensation. Overall, the findings suggest that board gender diversity has distinctive implications for CEO compensation depending on CEO gender and that having more women on governing boards contributes to closing the gender pay gap for nonprofit executives. These findings can be applied to other dimensions of diversity, including racial and ethnic diversity.

Women have made a substantial progress in nonprofit leadership in the past decade. While there are variations in exact numbers, national surveys report that women account for the majority of the sector’s chief executive officer (CEO) positions. For example, Urban Institute’s report of Nonprofit Trends and Impacts 2021 shows that women comprise 62% of CEO positions in the sector (Faulk et al., 2021). A study of more than 800 organizations by BoardSource (2021) reports an even higher percentage of female CEOs in the sector at 74%, an increase from 72% in its 2017 report (BoardSource, 2017).

Despite women’s significant gain in nonprofit leadership roles, however, research still finds a persistent gender gap in executive compensation in nonprofit organizations (Lee & Lee, 2021; Zhao, 2020). A 2017 survey of CEO compensation in private foundations shows that the average salary of female CEOs was 84% of the average male CEO salary (Nonprofit Times, 2018). Similarly, a study of nonprofit CEO compensation in South Florida by L’Herrou and Tynes (2020) reports a 12% female wage disadvantage. Even worse, research finds that gender pay gap for nonprofit CEOs persists regardless of the differences in personal characteristics and organizational and environmental contexts (Finley et al., 2019; Schneider et al., 2021).

The literature explains that prejudices and biases in the male-dominant culture create the perception that women leaders are less legitimate and less desirable (Byrne et al., 2021; Maran & Soro, 2010). As a result, female CEOs face challenges in establishing themselves as legitimate leaders, which means they do not have the same level of authority and influence within the organization compared with male CEOs (Brescoll et al., 2010; Main et al., 1995). The gender discrepancy in leadership authority suggests that gender is a status variable that leads to different expectations for compensation (Auspurg et al., 2017; Vial et al., 2016).

Gender pay gap exists regardless of economic sectors, with female executives being paid less than their male colleagues (Cook et al., 2019). However, gender pay gap for nonprofit CEOs is a more serious problem because women account for the vast majority of the nonprofit workforce, making up 75% of the sector’s workforce (BoardSource, 2021; Lee & Lee, 2021). Studies show that these women aim to be leaders of their organizations, and the persistent gender gap in CEO compensation will discourage aspiring women and increase their dissatisfaction and turnover (Di Mento, 2014; Lee, 2019). This will, in turn, prohibit nonprofit organizations from building a diverse and inclusive workplace. Studies also find that gender equity in leadership is closely associated with the positive image and performance of the organization (Glass & Cook, 2018; Liu, 2018; Silvera & Clark, 2021). These research findings suggest that gender disparity in executive compensation can take a toll on a nonprofit’s reputation and performance.

Because gender biases and stereotypes in leadership are too deeply rooted in organizational culture to be eliminated completely, closing the gender pay gap is an extremely difficult task. However, research suggests that board gender diversity, that is, increased representation of women on the governing board, contributes to gender equity in executive leadership (Cook et al., 2019; Lee, 2019). Scholars explain that the board of directors plays a major role in hiring CEOs and determining their compensation, and therefore, gender dynamics on nonprofit boards can affect gender equity in CEO compensation (Knippen et al., 2018; Lee & Lee, 2021; National Council of Nonprofits, n.d.). Then, can improving board gender diversity also help close the gender gap in nonprofit CEO compensation? This study examines how women’s representation on the governing board relates to CEO compensation, comparing organizations with male and female CEOs. The subsequent section reviews the theories on organizational outcomes of board gender composition. The description of the data and methods used in this study follows, and the results are discussed next. The study concludes with a discussion on this study’s implication for board gender diversity and gender equity in nonprofit leadership.

Board Gender Diversity and CEO Compensation

While advancing their career, women face implicit barriers which stem from gender biases and stereotypes. These biases and stereotypes, in turn, shape the perception of desired leadership qualities of men and women (Knippen et al., 2018). Women who ascend to executive positions face disparate treatment in terms of compensation and power because stereotypical views of the CEO position (regarding masculinity as a leadership trait) affect the board’s evaluation of executives (Hill et al., 2016). Research finds that gender stereotypes and status differences are more conspicuous at upper management from which women have traditionally been excluded (Eagly & Karau, 2002). Gender biases in leadership can then lead to underrating female CEOs’ qualities and performance by creating the perception that women are less qualified for leadership roles than men. A disadvantageous wage setting process based on gender stereotypes and biases, in turn, contributes to the gender gap in executive compensation even when women initially secure top management positions (Bergmann et al., 2019).

Provided that gender-biased perceptions and stereotypical views affect the pay equity between male and female CEOs, having a board with heightened awareness of gender discrimination can contribute to fair treatment of female CEOs by reducing gender-related biases and stereotypes in decision making. Research also suggests a trickle-down effect—gender equity at the higher level of organization has a positive impact on gender equity at the level immediately below (Gould et al., 2018; Lee & Won, 2014). Even though the relationship between a nonprofit organization’s governing board and CEO is not of a traditional hierarchy, the board has ultimate responsibility for the affairs and conduct of the organization and exercises the highest authority within the organization (Herman et al., 1996). Therefore, it is possible that a more gender-diverse board produces more gender-equitable organizational outcomes.

Social identity theory explains that a person’s interactions and behaviors are shaped by the sociodemographic groups with which one identifies. Individuals can identify with multiple categories, and a person’s identification with a particular category is strongest when this identity is psychologically salient (Chen et al., 2016). The theory posits that highly salient categories, such as gender, works as a prototype, which maximizes intra-group similarities and inter-group differences (Chen et al., 2016). According to this theory, people respond differently to in-group members than to out-group members (Markoczy et al., 2020; Voci, 2006). Research also finds that female CEOs’ experience with female board members differs from their experience with male board members, suggesting that the gender congruence between the board and CEO affects their dynamics (Dula et al., 2020). Social identity theory also posits that individuals seek positive social identity, and consequently, they tend to rate in-group members positively and allocate more resources toward in-group members (Kleissner & Jahn, 2020; Markoczy et al., 2020; Yzerbyt & Demoulin, 2010). Likewise, female directors may evaluate female CEOs’ performance more positively than male directors because women tend to be more aware of gender biases and stereotypes compared with men. Research suggests that the gender congruence between the board and the CEO facilitates mutual liking and attraction, and hence, female directors may form favorable characterization of a female CEO (Chen et al., 2016; Hentschel et al., 2019). With discrimination against women being deeply embedded in society at large, female board members’ favorable characterization of a female CEO can contribute to narrowing the gender gap in CEO compensation (Dahlvig & Longman, 2020; Hamilton et al., 2006).

The literature also suggests that individuals who represent marginalized or minority groups perceive the biases and stereotypes associated with their group identity as threats and seek to demonstrate their competitiveness with the majority (Branscombe et al., 1999; Chen et al., 2016). Pitkin (1967) categorizes the four dimensions of representation: formal representation, defined as the formal institutional processes through which representatives are chosen; descriptive representation, defined as the correspondence and resemblance between representatives and the represented; symbolic representation, defined as the feeling of the represented regarding fair and effective representation; and substantive representation or responsiveness, defined as the congruence between representatives’ actions and the interests of the represented (Zhang & Guo, 2021). While each dimension is unique and one dimension is not necessarily a prerequisite to another, research finds that the four dimensions of representation are closely linked (Campbell et al., 2010; Schwindt-Bayer & Mishler, 2005). In particular, feminist scholars focus on the connection between descriptive representation and substantive representation of women, based on the notion that women will act on the behalf of other women. Empirical studies on women’s political representation generally finds a positive correlation between descriptive and substantive representation, supporting this view (see Cowell-Meyers & Langbein, 2009; Jones, 2014). This suggests that female board members may promote gender diversity and equity in management by removing gender stereotypes and biases causing pay disadvantage for female CEOs.

Finally, the gender-ethics theory emphasizes distinctive value orientations between women and men and posits that women are more conservative in their ethical attitudes and have higher ethical standards (Doan & Iskandar-Datta, 2020 ; Ho et al., 2015). The theory also suggests that, based on gender, leaders bring different priorities and perspectives to leadership roles (Glass & Cook, 2018). In particular, research finds that gender-diverse boards exhibit more transparency than male-dominated ones, and the representation of women has a positive relationship with both financial and non-financial accountability of an organization (Byron & Post, 2016; Khan et al., 2021; Wasiuzzaman & Wan Mohammad, 2020).

Scholars explain that presence of women on the board prevents powerful CEOs from dominating their compensation schemes, and having women in the boardroom enhances board’s accountability by strengthening the link between CEO pay and firm performance, instead of determining CEO compensation based on non-measurable criteria, including gender and other demographic characteristics (Usman et al., 2018). Fair and more accountable behaviors by gender-diverse boards may enhance the transparency and equity in CEO compensation processes, reducing the gender pay gap. Studies also report that representation of women on boards is negatively associated with the CEO pay deviation and that gender-diverse boards are less likely to overpay or underpay their CEOs (Adams & Ferreira, 2009; Ahmed et al., 2021). Based on the theoretical explanations and empirical findings, this study tests the following hypotheses:

Data and Method

This study uses data from organizations that had earned and maintained the GuideStar’s Platinum Seal of Transparency (PST) as of July 2021. To receive a PST, organizations must provide the basic program information (bronze seal), brand information (silver seal), audited financial statement or equivalent financial details (gold seal), and information regarding goals and strategic plans (platinum seal) (Candid, 2021). There were 4,872 501(c)(3) organizations with a PST at that time, and among them, 3,832 organizations had also provided diversity, equity, and inclusion (DEI) information containing details on CEO gender and the gender proportion of the board. This information was prepared by the organization’s representative, which, in many cases, was the CEO. This study limits its focus on organizations with a paid CEO as CEO compensation is the dependent variable. After excluding observations with missing information, the final sample consists of 1,835 organizations. The financial and demographic information was collected from their GuideStar profile and IRS Form 990.

Dependent Variable

The dependent variable is the annual compensation of the CEO, and this study uses its logarithm due to the skewness in the distribution of CEO compensation.

Independent Variables

The variable of primary interest is the gender diversity within the board, measured by the percentage of women in the board [(number of female board members / number of total board members) × 100]. The regression model includes the squared term of women’s percentage on a board to test if there is a curvilinear relationship between board gender diversity and CEO compensation (Dula, 2022).

Control Variables

As CEO compensation is largely determined by organizational size, the regression model includes the variables of gross receipts and total assets (both in logarithmic forms) as measures of organizational size. The model also controls for the ratio of total contribution to total revenue, subsector, organizational age, and region.

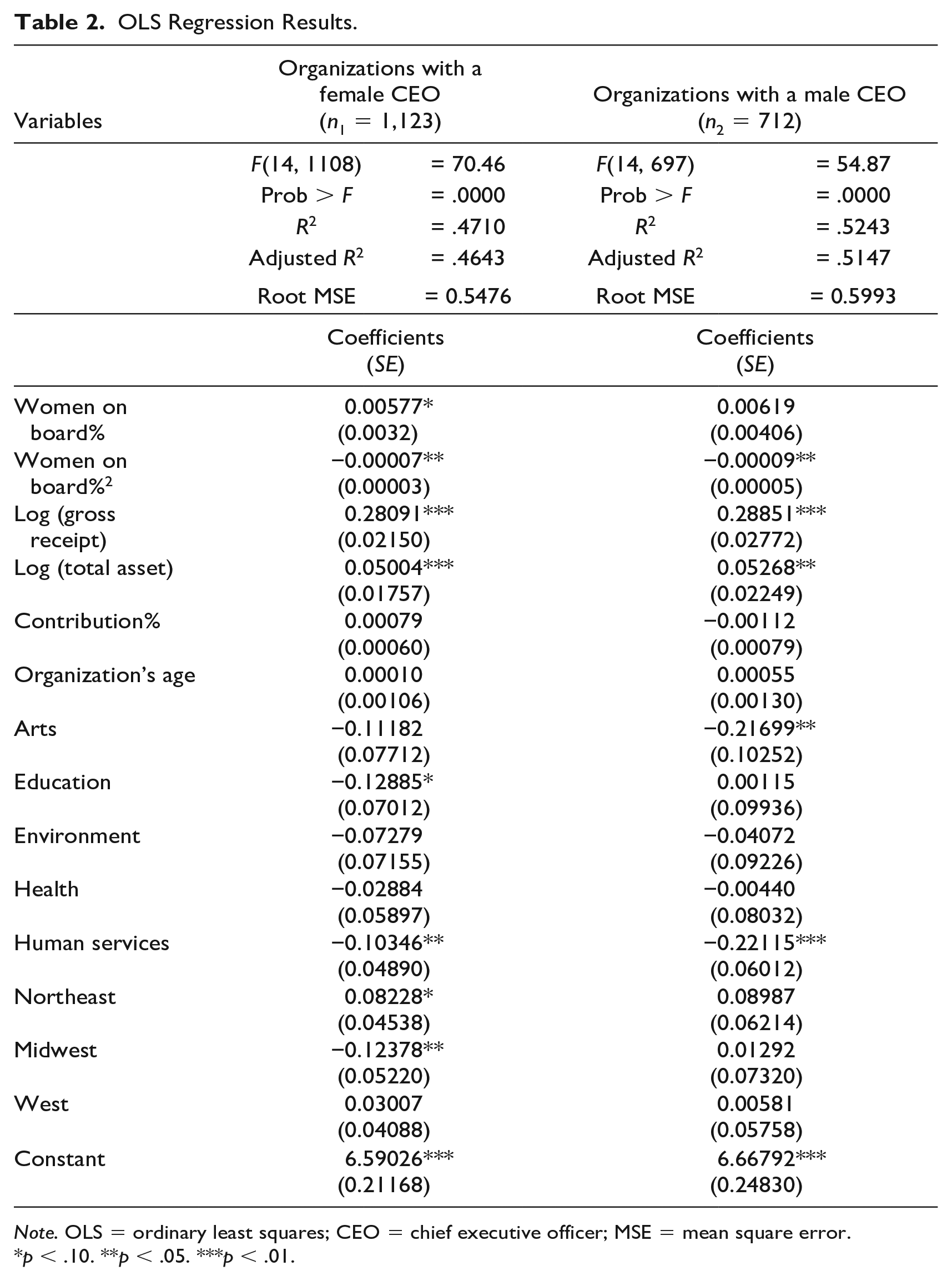

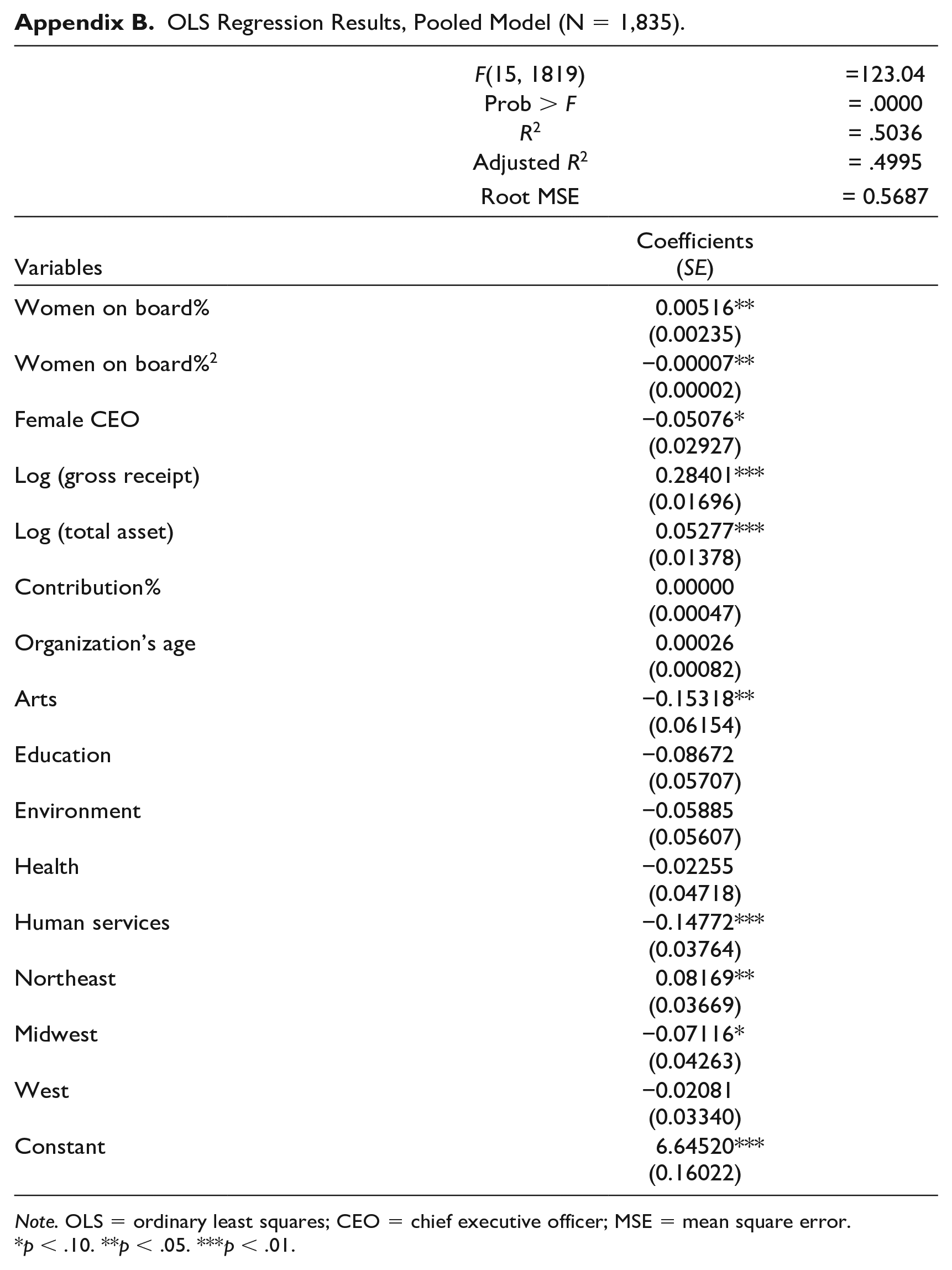

This study examines if the association between the board gender diversity and CEO compensation varies depending on CEO gender. Two separate regressions were estimated for organizations with a male CEO (712 observations) and organizations with a female CEO (1,123 observations), and a chow test was conducted to check if the regression coefficients are significantly different for the split samples. The results (probability F > .0601) indicate that coefficients in the male CEO and female CEO models are statistically different, suggesting that two separate regressions be estimated for organizations led by a female CEO and by a male CEO (see Appendices A and B for the results using the pooled sample).

Results

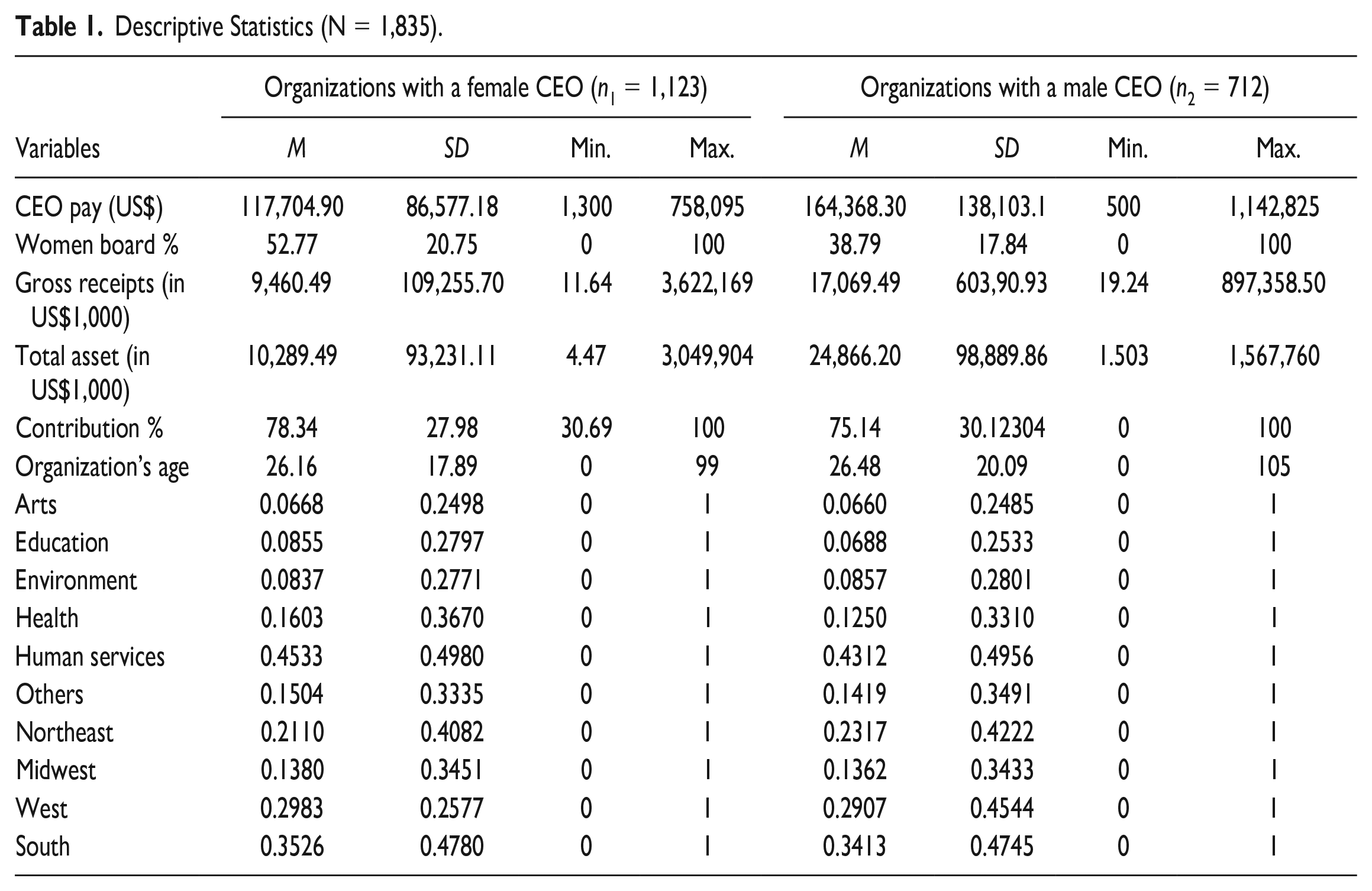

Descriptive statistics in Table 1 show that the mean annual compensation of female CEOs ($117,705) is about 30% lower than the mean annual compensation of male CEOs ($164,368). Women occupy slightly more than a half (53%) of the board seats in organizations led by a female CEO, but their proportion on the board drops to 39% in organizations led by a male CEO. Organizations with a female CEO tend to be smaller (gross receipt $9.5 million and total asset $10.3 million) than organizations with a male CEO (gross receipt $17.1 million and total asset $24.9 million). 1

Descriptive Statistics (N = 1,835).

Table 2 shows the results from the ordinary least squares (OLS) regression for CEO compensation in organizations led by a female CEO and organizations led by a male CEO. When an organization is led by a female CEO, the coefficient of the percentage of female board members is 0.00577 and the coefficient of its squared term is −0.00007. This means that there exists a curvilinear relationship between board gender diversity and female CEO compensation. Based on the quadratic equation with these two terms, when women account for 10% of the board, a female CEO’s compensation increases by approximately 5% if all other conditions remain the same. When 41% of the board members are women, the increase is the largest at 12%. If women comprise 60% of the board membership, a female CEO’s compensation increases by about 9%. The positive effect of women’s representation on governing boards on a female CEO compensation wears off when women’s proportion of the board membership reaches 82%, and after that, a further increase in women’s share of board membership is negatively associated with a female CEO’s compensation.

OLS Regression Results.

Note. OLS = ordinary least squares; CEO = chief executive officer; MSE = mean square error.

p < .10. **p < .05. ***p < .01.

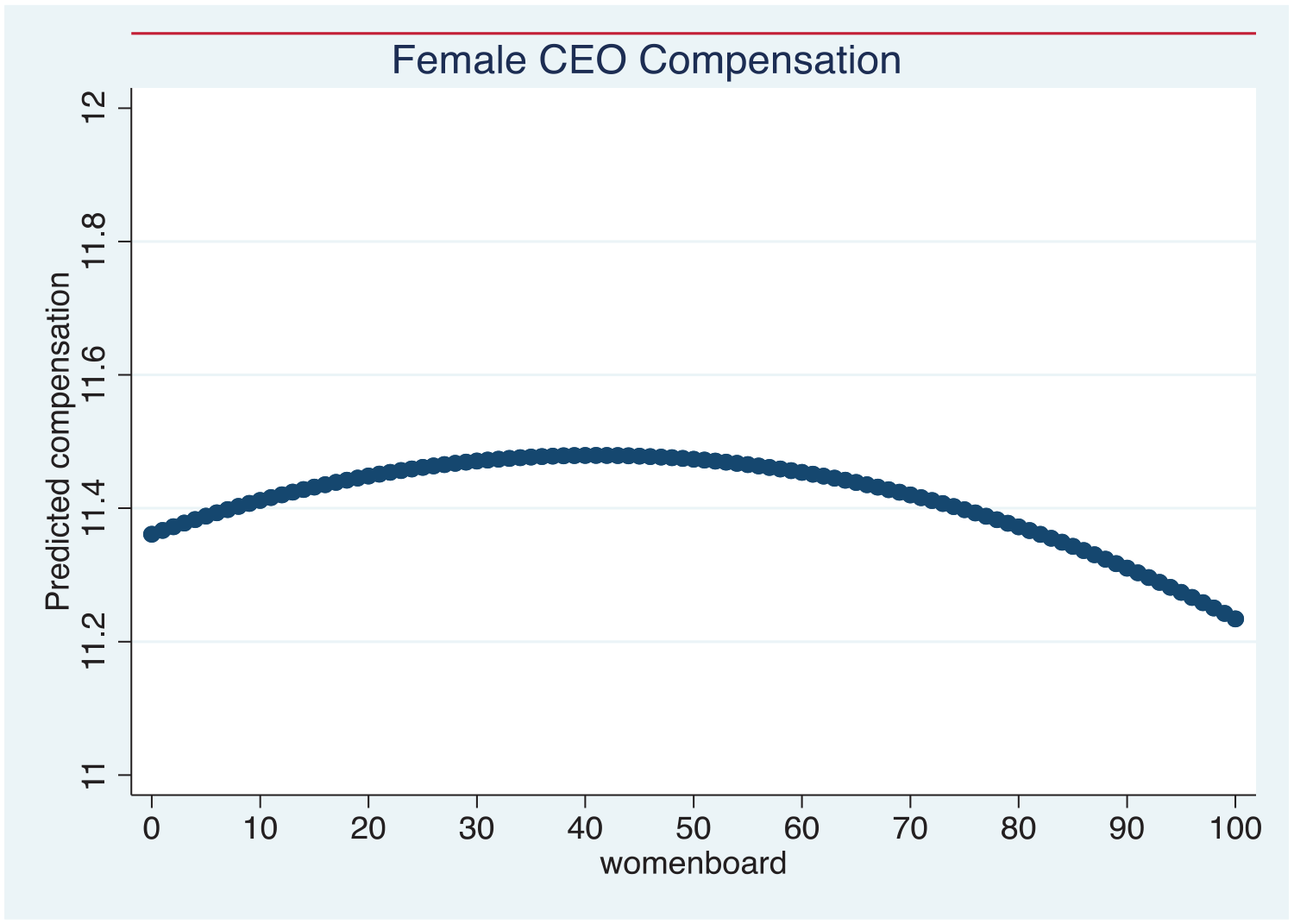

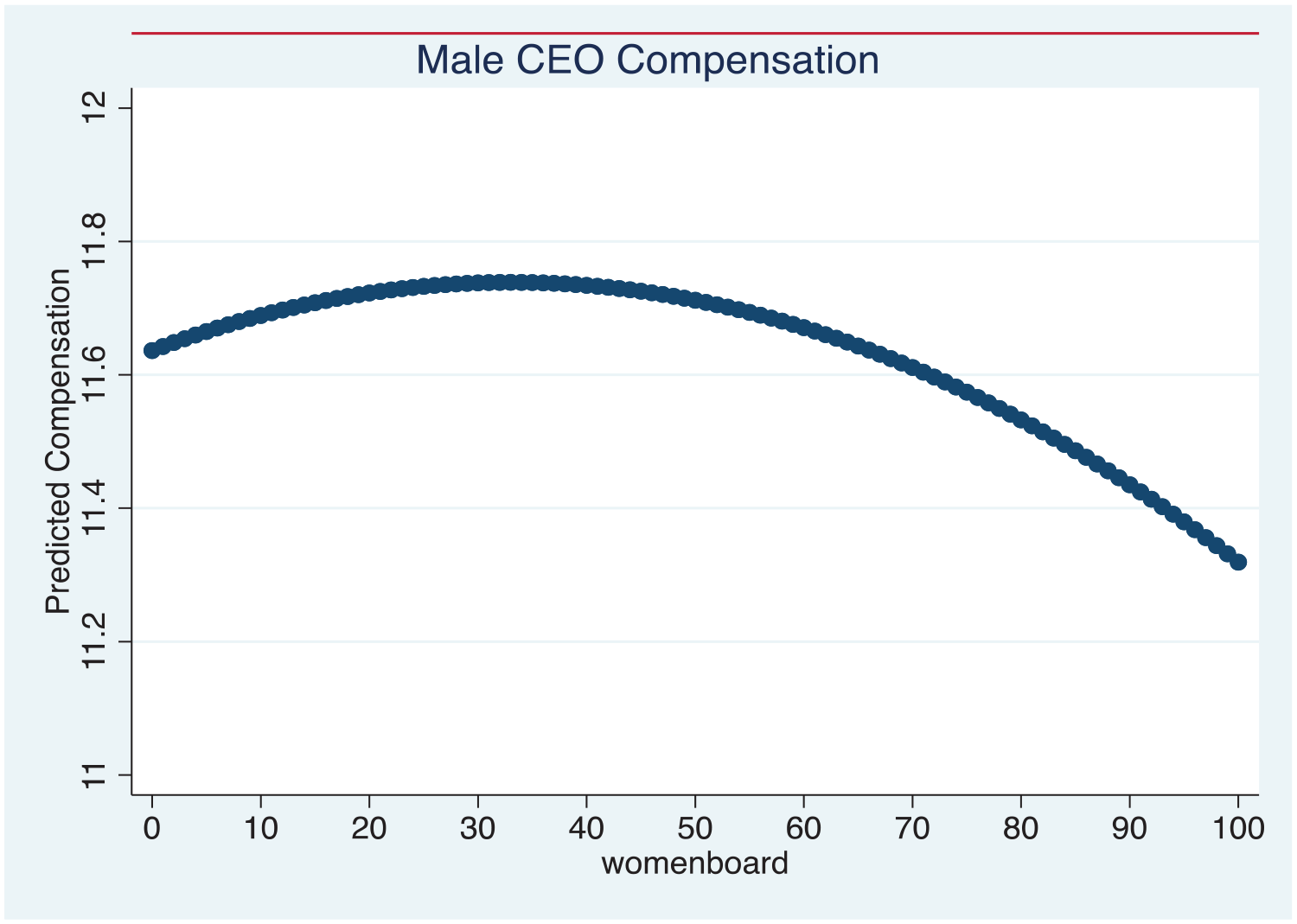

The results of the compensation equation for male CEOs, on the contrary, indicate a negative correlation (−.00009) between the squared term of board gender diversity and compensation. This means that when women account for 10%, there is a 0.9% decrease in a male CEO’s compensation assuming that all other conditions remain the same. When women make up 50% of the board, there is a 22.5% decrease in a male CEO’s compensation controlling for other organizational characteristics. If an organization has an all-women board (100%), a male CEO’s compensation decreases by 90%. Overall, these findings suggest that board gender diversity has distinctive implications for CEO compensation depending on CEO gender. Figures 1 and 2 show how the predicted CEO compensation of female and male CEOs (in logarithms) changes as the percentage of women on the board increases from 0% to 100%, using the regression model. Comparing the two graphs suggests that the difference in the predicted compensation between male and female CEOs decreases as women’s share of the board membership increases.

Predicted Ln(Compensation) of a Female CEO When the Percentage of Women on the Board Changes From 0 to 100.

Predicted Ln(Compensation) of a Male CEO When the Percentage of Women on the Board Changes From 0 to 100.

Not surprisingly, the gross receipts and total assets are positively associated with CEO compensation, regardless of CEO gender. In fact, an organization’s gross receipts are highly correlated with the CEO compensation in both models. The results also reveal different patterns in subsector variations in compensation between male and female CEOs; female CEOs in the education and human services sectors earn less than female CEOs in the other subsectors, and male CEOs of arts and human services organizations earn less than male CEOs of different types of organizations. Generally, the subsector variations in CEO compensation are larger among male CEOs than among female CEOs. The results also reveal that female CEOs in the Northeast region are paid an average of 8% more than those in the South while female CEOs in the Midwest region are paid 12% less than those in the South region. However, there is no statistically significant regional variation in male CEOs’ compensation. The distinctive patterns of subsector and regional differences between male and female CEOs call for further research.

Discussion

This study’s findings reveal that board gender diversity has distinctive implications for male and female CEO compensation. Women’s representation on nonprofit boards is closely linked to female CEO compensation and the relationship is generally positive, supporting the view that gender-diverse boards may mitigate the gender biases and stereotypes (Glass & Cook, 2018). The increasing presence of women on boards positively affects a female CEO’s compensation until women make up 82% of the board. The positive association may disappear after this point because gender is no longer a salient identity when women account for the vast majority (Abrams et al., 1990; Lee, 2019). The findings also reveal a negative association between women’s representation on the board and male CEO compensation. These findings are consistent with what the gender-ethics theory suggests—representation of women on boards is negatively associated with the CEO pay deviation, and gender-diverse boards are less likely to overpay or underpay their CEOs (Adams & Ferreira, 2009; Ahmed et al., 2021). Even though more women lead nonprofit organizations than ever, studies consistently find that female CEO salaries lag behind male CEO salaries (Candid, 2022; Lee & Lee, 2021). This study’s findings suggest that addressing the male-dominated governance structure and improving board gender diversity can contribute to the gender pay equity for nonprofit CEOs.

Due to the cross-sectional nature of the data, however, the positive connection between board gender diversity and higher compensation for female CEOs found in this study cannot be proven as a causal one. Nevertheless, scholars agree that the gender dynamics between the board and top management is causal and runs from boards to management rather than the reverse (Gould et al., 2018; Matsa & Miller, 2011). The governing board of a nonprofit organization defines the organization’s culture, and the board’s makeup demonstrates organizational values of diversity (Lee, 2021). Gender diversity on the board also sends a signal to the entire organization, contributing to gender equity at every level of organizational hierarchy. These findings offer support for the perspective that “diversity begets diversity” (Cook & Glass, 2015) and suggest that closing the gender gap in nonprofit leadership starts from board development. To test a causal relationship between board gender diversity and CEO compensation, future studies should employ longitudinal data of nonprofit compensation and diversity information. Use of longitudinal data will also allow researchers to test if this relationship changes depending on economic conditions (Owen & Temesvary, 2018).

This study used the data of organizations that had earned and maintained the GuideStar’s PST. To receive a PST, organizations must provide their strategic plan from the past 5 years and metrics used to track progress and results as well as their program, financial, and demographics information. The high-level of transparency required for a PST suggests that organizations with a PST are more likely to have adopted best governance practices, including DEI policies, which might have caused a selection bias in this study. However, while it is possible that organizations with a PST have a more diverse and equitable culture than organizations without a PST, the findings still reveal a considerable gender disparity in CEO compensation (see Table 1). In addition, the CEO gender and board gender composition data used in this study are provided by key personnel in each organization, CEO themselves in many cases, offering more accurate information than the data that had been used in the existing research. 2

Conclusion

Closing the gender pay gap for CEOs is an important task for nonprofit organizations, as the gender equity in executive compensation will contribute to work motivation and retention of female employees, who make up the vast majority of the nonprofit workforce. Moreover, equitable pay for female CEOs can help an organization construct a diversity image and reputation for DEI, which have critical impacts on donative income as well as commercial revenue (McMillan-Capehart et al., 2010; Smith et al., 2012). The positive link between women’s representation on governing boards and female CEO compensation found in this study suggests that board gender diversity contributes to narrowing the gender pay gap for nonprofit CEOs.

To increase board gender diversity, nonprofits must review existing board recruitment practices, conduct a self-assessment of their current board, and make DEI an organizational priority (Edelstein, 2020). Professional associations and accreditation agencies can also enforce diversity standards for board development as a membership or accreditation requirement. Having more women on the board’s CEO compensation committee and other important positions will help solidify the link between board gender diversity and gender equity in top management (Cook et al., 2019; Shin, 2012). This study’s findings can also be applied to other dimensions of diversity, including racial and ethnic diversity, and help nonprofits build more diverse and equitable leadership.

Footnotes

Appendix

OLS Regression Results, Pooled Model (N = 1,835).

| F(15, 1819) | =123.04 | |

|---|---|---|

| Prob > F | = .0000 | |

| R 2 | = .5036 | |

| Adjusted R2 | = .4995 | |

| Root MSE | = 0.5687 | |

| Variables | Coefficients |

|

| Women on board% | 0.00516**

(0.00235) |

|

| Women on board%2 | −0.00007**

(0.00002) |

|

| Female CEO | −0.05076*

(0.02927) |

|

| Log (gross receipt) | 0.28401***

(0.01696) |

|

| Log (total asset) | 0.05277***

(0.01378) |

|

| Contribution% | 0.00000 (0.00047) |

|

| Organization’s age | 0.00026 (0.00082) |

|

| Arts | −0.15318**

(0.06154) |

|

| Education | −0.08672 (0.05707) |

|

| Environment | −0.05885 (0.05607) |

|

| Health | −0.02255 (0.04718) |

|

| Human services | −0.14772***

(0.03764) |

|

| Northeast | 0.08169**

(0.03669) |

|

| Midwest | −0.07116*

(0.04263) |

|

| West | −0.02081 (0.03340) |

|

| Constant | 6.64520***

(0.16022) |

|

Note. OLS = ordinary least squares; CEO = chief executive officer; MSE = mean square error.

p < .10. **p < .05. ***p < .01.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.