This paper investigates the interaction between cheap-talk advertising and credible third-party product reviews to inform customers about product quality. We find that cheap-talk advertising can be informative when the firm’s private information helps predict a credible product review. A more informative credible product review has two effects on cheap-talk advertising. First, a credible product review plays a disciplinary role that enables the firm to provide informative advertising. Second, it reduces the incremental value of cheap-talk advertising. We find that, in equilibrium, whether or not the advertising is consistent with a credible product review is informative about product quality. The results also imply that an overly informative product review can reduce the total information available to customers by deterring the firm from providing informative advertising.

Customers have a variety of channels to learn about product quality. They can collect information from product rating agencies. Credible third-party rating agencies are common in the experience goods sector such as consumer electronics, auto, and hotel sectors (Dranove and Jin, 2010; Zhu et al., 2021). For instance, the credible third-party testing organization Antutu provides ratings for cellphones, J.D. Power provides ratings for automobiles, and TripAdvisor provides ratings for the hotel sector. In addition, firms often voluntarily disclose product information to customers on their websites and advertise in newspapers, television, and online. Unlike credible third-party rating agencies, research has found that most firms’ advertisements focus on subjective perceptions of products rather than objective attributes (Abernethy and Butler, 1992). Many commercials feature customers’ endorsements of products and show enjoyable experiences without providing direct information about technical attributes. These advertisements aim to enhance customers’ subjective perceptions of product quality and are typically unverifiable. Although both information channels are commonly available to customers, the existing literature has largely examined the two information channels in isolation and ignored the interaction between these channels. This paper examines the interaction between the two information channels and studies how the interaction affects the credibility of firm disclosures and customers’ perceptions of product quality.

We consider a model where product quality is either high or low. A firm can be either a high type or a low type. A high-type firm is more likely to offer a high-quality product than a low-type firm. The firm knows its type, but customers do not, and neither the firm nor the customers know the product quality. Customers can learn about product quality through two information channels: the firm’s voluntary disclosure and a product review from a third-party rating agency. In our model, these two information channels differ in two aspects. First, the third-party rating agency issues a credible product review that provides noisy information about product quality for customers. In contrast, the firm provides a cheap-talk voluntary disclosure about product quality as in Crawford and Sobel (1982). It represents a setting where the firm has soft information on product quality that cannot be verified. Therefore, the firm can make false or biased claims about product quality such as in advertisements (Gardete, 2013). The second difference is that the firm’s voluntary disclosure is more timely but less precise than the product review. This is the case when the firm advertises the product right after its release, but the third-party rating agency relies on customers’ feedback after a period of use. Before the firm makes a cheap-talk voluntary disclosure, it can choose to collect costly private information that reflects customers’ feedback about product quality. Such private information helps the firm predict the upcoming product review. After having observed the firm’s disclosure and the product review, customers update their beliefs about product quality, and they buy the product at the equilibrium price.

Our main findings are as follows. First, an equilibrium exists where the high-type firm acquires private information and discloses it truthfully, and the low-type firm does not acquire private information and makes an uninformed disclosure about product quality. In this equilibrium, consistent disclosures, that is, the firm disclosure and the product review reveal the same information about product quality, are indicative of a high-type firm and thus high product quality. This is because privately informed high-type firms are more likely to make a consistent disclosure than uninformed low-type firms.

The second main finding is that the interaction between a credible product review and a firm’s voluntary disclosure arises in two ways. On the one hand, a credible product review provides truth-telling incentives so the high-type firm’s voluntary disclosure is credible. On the other hand, the more information the product review reveals about product quality, the lower the incremental information of the voluntary disclosure, which, in turn, reduces the firm’s benefits of acquiring costly private information and truthfully disclosing this information. When the product review becomes sufficiently informative, the firm’s benefits of acquiring private information will be lower than the information acquisition costs, so the firm no longer finds it beneficial to acquire information and issue an informed voluntary disclosure. Prior literature on third-party product reviews has focused on how such reviews can reduce information asymmetry between firms and customers. Our findings indicate that third-party product reviews also have an impact on firms’ information acquisition and disclosure strategies.

Our results have several implications. We find that credible product reviews can induce informative cheap-talk disclosures such as firm advertisements. However, the product review should not be overly informative, as it could reduce the total information available to customers by eliminating informative disclosures from the firm. Having overly precise product reviews means that the firm disclosure contains little incremental information, so the information acquisition costs for the firm exceed the benefits of providing informative disclosures. We also find that when the firm’s voluntary disclosure is more likely to be consistent with the product review, the firm is more likely to produce a high-quality product and is more likely to collect soft information about its products from customers at lower costs.

We also performed three extended analyses of our main model. First, we consider an alternative information structure where the firm can collect private information that is a noisy signal about the product quality rather than the product review, as in our main model. We refer to the respective information structures of our main model and the extension as the dependent information structure and the independent information structure. Interestingly, we find that the equilibrium with informative firm disclosures cannot be sustained in the extended model because, for the independent information structure (i.e., where the firm’s private information is a noisy signal about product quality), the truth-telling incentives provided by the product review are too weak. As independent private information also provides direct information on product quality, the firm does not want to truthfully disclose relatively bad information. Next, we analyze a setting where private information can be a mix of dependent and independent information structures and find that complete reliance on the dependent information structure is not necessary to obtain informative firm disclosures. Finally, we allow customers to purchase the product after the firm disclosure but before the product review. We find that even though early adopters increase the firm’s incentive to disclose good news to boost the price at which early adopters purchase the product, there can still exist an equilibrium with informative firm disclosures.

The paper proceeds as follows. Section 2 summarizes the related literature. Section 3 describes the model, Section 4 presents the equilibrium analysis, and Section 5 discusses several implications. Section 6 analyzes three extensions of the main model, and Section 7 concludes. Detailed analyses of the extensions are discussed in the Online Appendix.

Related Literature

Our study relates to several strands of literature in operations research, economics, and accounting. A stream of literature in operations research and economics has analyzed the role of credible quality disclosure in product markets and supply chains.1 Researchers have examined factors that can explain partial disclosure of quality information, including the positive cost of quality information disclosure (Jovanovic, 1982), the existence of multiple product attributes (Sun, 2011), and the market structure (e.g., Ghosh and Galbreth, 2013; Levin et al., 2009). Studies on mandatory disclosure of quality information have examined the impact on customers and firm behavior (e.g., Dafny and Dranove, 2008; Jin and Leslie, 2003). Additionally, Fishman and Hagerty (2003) and Cao et al. (2020) have compared the impacts of mandatory versus voluntary disclosures on consumers and supply chain members. Another stream of literature has relaxed the truthful disclosure assumption and examined false advertising and its regulations. Chakraborty and Harbaugh (2014) study how heterogeneous tastes of customers can lend credibility to false advertising. Corts (2014) and Rhodes and Wilson (2018) focus on how legal penalties can induce informative false advertising and analyze the optimal level of legal penalties. While legal penalties on false advertising discipline the firm by imposing exogenous costs on non-truthful disclosures, we find that a credible third-party product review can impose endogenous costs on non-truthful firm disclosures and thus discipline firm disclosures in the absence of exogenous penalties. Such endogenous costs on cheap-talk advertising are also present in Gardete (2013) and Gardete and Guo (2021) through customers’ information search decisions. These literature streams have either analyzed one information channel or two information channels in isolation. In contrast, our research focuses on the interaction between two information channels: a firm’s cheap-talk style voluntary disclosure and a credible product review from a third-party rating agency.

Several papers in marketing have also analyzed the interaction between firm advertising and product reviews. Mayzlin (2006) assumes that product reviews and firm advertising are perfect substitutes. Chen and Xie (2005) and Chen and Xie (2008) consider settings where product reviews are available before firms choose their advertising strategy.2 We consider a setting where the firm provides timely advertising before product reviews are available and show that an informative credible third-party product review can lend credibility to the firm’s cheap-talk voluntary disclosure, but that it also reduces the benefits of acquiring private information and providing informed voluntary disclosure.

The accounting literature on cheap-talk disclosure finds that when voluntary disclosure does not need to be true, truth-telling incentives can be provided by another credible disclosure (e.g., Lundholm, 2003; Stocken, 2000) or by different users of the disclosed information with opposing interests (e.g., Gigler, 1994; Newman and Sansing, 1993). In our study, truth-telling arises due to the confirmatory role of a credible product review. This view is also consistent with the confirmation hypothesis in accounting, as demonstrated by Gigler and Hemmer (1998) and Ball et al. (2012). In these studies, the role of mandatory disclosure is to lend credibility to voluntary disclosure so all value-relevant information is revealed in the voluntary disclosure and the mandatory disclosure does not provide any incremental information. Our study differs in that it is the (in)consistency of voluntary disclosure rather than the voluntary disclosure that provides useful information about the firm type and product quality. In equilibrium, only a high-type firm acquires private information, so it is more likely to disclose information that is consistent with the product review. Hence, the information value of a voluntary disclosure arises from the endogenous information acquisition decision, and thus it can also arise in a single-period game with information users with the same interests.

Lastly, one can also interpret our disclosure setting as a management earnings forecast setting, where voluntary disclosure is the management earnings forecast, and the credible product review is the audited annual report. We show that a management forecast error can provide valuable information on the firm type. In the literature on management forecast accuracy, Beyer (2009) shows that the difference between a voluntarily issued management earnings forecast and an earnings report can contain information on the volatility of earnings. Ramakrishnan and Wen (2016) assume that firms exogenously receive private information about different qualities, so the forecast accuracy helps investors distinguish the quality of firms’ information environments. Mittendorf and Zhang (2005) also find that biased earnings guidance motivates the analyst to conduct an independent assessment of firm performance. Aghamolla et al. (2021) analyze a signaling model where managerial ability determines both the level of earnings and the forecast accuracy and find that, in equilibrium, only intermediate-ability managers issue forecasts. The main differences between our paper and previous papers are that we endogenize the manager’s information acquisition decision that determines the forecast accuracy and we study how a credible product review influences managerial information acquisition and disclosure decisions.

The Model

Consider a firm selling a product (or service) to risk-neutral customers. A firm can be one of two types, a high type or a low type . We assume that the firm type is known to the firm but that the firm cannot credibly communicate this information to customers.3 We denote firm type by and assume that a firm is a high type with probability .

A type firm produces a high-quality product with probability and a low-quality product with probability , where we assume that ; that is, a high type firm is more likely to produce a high-quality product than a low-type firm. Customers value a high-quality product at and a low-quality product at .4 Hence, represents product quality. We assume that the quality of the product is uncertain for both the firm and the customers. It is uncertain for the firm because the quality can depend on factors beyond the firm’s control. For instance, while the firm can adopt advanced technologies in the manufacturing process to improve quality, human error and environmental factors such as temperature and humidity in the production process can still influence the quality of the product. Hence, the firm only knows its type, that is, the probability that the manufacturing process yields a high-quality product, but does not know the quality of all products. For the same reasons, customers are uncertain about product quality before consumption. In addition, the customers’ perceptions of product quality can also depend on each customer’s experience during usage or on how product performance matches the customer’s preferences and/or expectations. This can also make the firm uncertain about product quality as perceived by customers. We incorporate this uncertainty about product quality in a simple fashion by assuming that product quality is a random variable .5

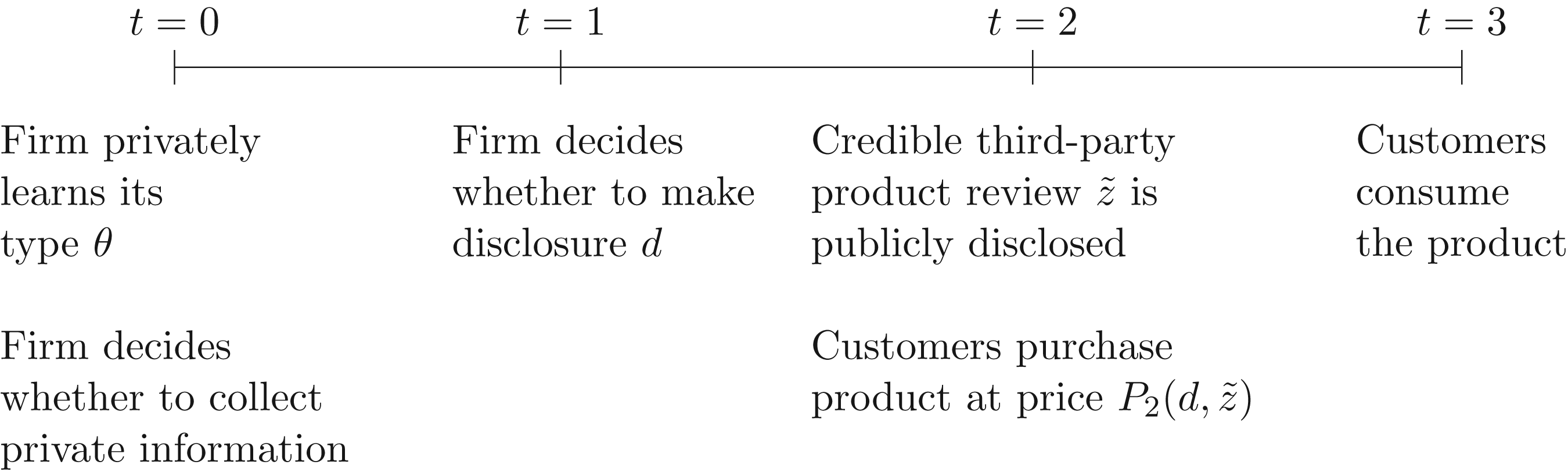

Figure 1 summarizes the sequence of events in our model. At , the firm privately observes its type and then decides whether to collect private information about product quality at a cost . Similar to Arya et al. (2014), Dye (1985), and Jung and Kwon (1988), we assume that the firm cannot credibly disclose the information acquisition decision. At , the firm decides whether to provide a voluntary disclosure about product quality. At , a third-party rating agency issues a product review about product quality. After learning both the firm’s voluntary disclosure decision and the third-party product review, customers purchase the product at price . Finally, customers consume the product at . In our main model, we assume that customers only purchase the product after observing both the firm’s voluntary disclosure decision and the product review. Section 6.3 discusses an extension where a fraction of customers are early adopters who purchase the product after the firm’s disclosure decision, but before observing a product review.

Sequence of events.

In our setting, customers can learn about product quality via two channels: a product review from a credible third-party rating agency and a voluntary disclosure from the firm. Following the existing literature (e.g., Guan and Chen, 2017; Arya et al., 2014), we assume that the third-party product review is credible. The voluntary disclosure from the firm, however, is a cheap-talk style disclosure as in Crawford and Sobel (1982). The firm can make a disclosure without acquiring private information at ; if the firm does acquire private information, the firm does not need to truthfully disclose this information. This represents a disclosure channel where the firm can make false claims about the product, such as in advertisements (Gardete and Guo, 2021; Rhodes and Wilson, 2018). The existing literature finds that most firm advertisements focus on subjective perceptions of products rather than objective attributes (Abernethy and Butler, 1992). Many commercials feature customers’ endorsement of products and enjoyable experiences without direct information on technical attributes. Such advertisements aim to enhance customers’ subjective perceptions and are typically unverifiable. Hence, we choose not to include any legal penalties for false voluntary disclosure in our model.

The information structure of the private information and the product review is as follows. The product review is a noisy signal of product quality . This product review is binary and contains either relatively good news or relatively bad news about product quality, with . The parameter is a measure of the precision of the product review . When , it is completely uninformative about product quality; and when , it perfectly reveals the product quality . The precision is assumed to be common knowledge. We denote by the probability of having a relatively good product review given the firm type . Because and , the product review also provides information about firm type .

For the private information of the firm, we also assume that the private information is either relatively good news about product quality or relatively bad news . The firm can collect private information about product quality by testing products with customers or collecting customer feedback, which is similar to a product review. The firm cannot credibly reveal the collected private information to customers. This applies to soft information on customers’ perceptions of product quality that the firm has collected and that cannot be supported by hard evidence.6 For example, in the context of food manufacturers, represents information collected from customers about the taste of the food products.

We assume that the private information is a noisy signal of the product review and we refer to this information structure as the dependent information structure. The private information satisfies . The parameter is a measure of the precision of the private information . When , it is completely uninformative about the product review; and when , it perfectly reveals the product review. The precision is assumed to be common knowledge.7

In this case, we assume that the firm has less precise information about customers’ perceptions about product quality than the product review. This can arise for several reasons. First, while the firm might be able to collect customer feedback about its own product, a third-party product review usually covers multiple products from different firms and makes comparisons between different products. Thus, a third-party rating agency has better information about customers’ preferences and quality perceptions than the firm. Second, the firm can start advertising the product before or right after the product is released. At this early stage, the firm might have less precise information about customers’ perceptions of the new product because customers have used the product for a very short time. The third-party rating agency, on the other hand, decides on ratings by collecting customer feedback after customers have used the product for a longer period of time. For instance, the company J.D. Power provides car ratings based on customers’ experience both during the first 90 days of ownership and after the first three years of ownership. Hence, the rating agency has better information about customers’ experiences with the product.

In summary, the dependent information structure represents a setting where the firm can disclose timely soft information regarding customers’ perceptions of product quality, which can later be verified by a more precise credible product review. Hence, the model fits with firm advertising about customers’ subjective perceptions of product quality, which is likely to be unverifiable, rather than firm disclosures about verifiable technical features of products.8 In Section 6.1, we consider an alternative case where private information is a noisy signal of product quality (referred to as an independent information structure).9 In this case, we show that there is no equilibrium where the firm acquires private information and discloses this information truthfully. We also weaken the dependent information structure and discuss an extension where the firm’s private information is a combination of the dependent and independent information structures in Section 6.2. We show that our results remain qualitatively the same under this mixed information structure.

The focus of our analysis is on how the product review can lend credibility to cheap-talk voluntary disclosure and how it can enable firms to communicate information about the firm type. We denote the firm’s voluntary disclosure decision by , where represents no disclosure. The firm’s voluntary disclosure strategy, denoted by , has support . For the outcome pairs and , we say that the firm’s voluntary disclosure is consistent with the product review and for the outcome pairs and , we say that the voluntary disclosure is inconsistent with the product review. In addition, we refer to voluntary disclosure based on acquired private information as an informed disclosure, and we refer to voluntary disclosure without acquisition of private information as an uninformed disclosure.

The objective function of the firm equals

where denotes the information acquisition decision of the type firm and denotes the acquisition cost of the type firm. denotes the market price of the product after customers have observed both the firm’s voluntary disclosure and the product review. In a perfectly competitive market with risk-neutral customers, the product price equals the expected value according to customers’ beliefs:

Observe that the expected price is higher when the firm is believed to be a high type than when the firm is believed to be a low type; thus, a low-type firm would want to mimic a high-type firm, whereas a high-type firm would always try to distinguish itself from a low-type firm.

The structure of the model is common knowledge. Information asymmetry exists between the firm and its customers with respect to firm type, the information acquisition decision of the firm, and the private information of the firm (if acquired).

Equilibrium Analysis

An equilibrium consists of an information acquisition decision , a disclosure strategy and customers’ beliefs about firm type such that given the beliefs of customers, the pair of strategies is optimal for the firm, that is, . In addition, customers’ beliefs are rational with respect to the strategies of the firm.

Given our interest in whether information acquisition and informative firm disclosures can arise with cheap-talk voluntary disclosure, we focus the equilibrium analyses on pure information acquisition strategies.10 For the firm’s information acquisition decision, the firm’s type and action space give rise to four different combinations: . As is standard in cheap-talk models, there is always a babbling equilibrium where both firm types do not acquire private information, that is, , and thus make uninformative voluntary disclosures. In that case, customers do not use the firm’s voluntary disclosure to update their beliefs about product quality so the price is independent of . Consequently, there is no incentive for a firm to acquire costly private information and provide an informed disclosure.

For the other information acquisition strategies, one might expect that the firm has no incentive to acquire costly private information to provide an informative disclosure about the product. Under the dependent information structure, disclosure from the firm is a noisy signal about the product review . After customers learn about the product review, the firm’s disclosure no longer provides direct information on product quality . However, we find that an equilibrium can exist where a firm’s disclosure adds information to customers for the information acquisition strategy . In this case, only a high-type firm acquires information and is thus more likely to provide a disclosure that is consistent with the product review than the low-type firm. Consequently, consistent disclosures and increase customers’ beliefs about dealing with the high-type firm, while inconsistent disclosures and decrease these beliefs.

For the voluntary disclosure to be informative under the information acquisition strategy , one necessary condition is that the high-type firm should have incentives to truthfully disclose the acquired information, which holds when the private information is sufficiently precise.

If an equilibrium exists where the high-type firm acquires private information () and the low-type firm does not acquire private information (), then the high-type firm truthfully discloses the private information when

where for .

In equilibrium, the high-type firm always truthfully discloses the information when it receives private information , since the high-type firm is more likely to receive a good product review than a low-type firm. However, the high-type firm may not credibly communicate the private information . captures the precision of private information that, given bad news and the equilibrium disclosure strategy of the low-type firm, the high-type firm is indifferent between disclosing and truthfully disclosing . That is, holds for . When is low () and the private information is , there is a relatively high probability that the private information is incorrect and the final outcome with truth-telling would be . As is indicative of a high-type firm, the high-type firm is then better off disclosing even when it receives private information . This implies that the high-type firm is better off not acquiring private information and always disclosing . The high-type firm can credibly communicate the private information that it has acquired only if .

Also, for to be an equilibrium, the high-type firm would prefer to acquire private information while the low-type firm would not. We summarize the equilibrium conditions in the following proposition.

If the information acquisition costs satisfy and , with

then there exists an equilibrium in which only the high-type firm acquires private information () and discloses it truthfully, and the low-type firm does not acquire private information () and discloses with probability , which satisfies

Otherwise, only a babbling equilibrium arises where both firm types do not acquire private information, that is, , and both firm types follow the same disclosure strategy.

Out-of-equilibrium beliefs are such that when there is no voluntary disclosure, customers believe the firm is a low type, that is, . We present the proof of the above equilibrium existence conditions in the Appendix and relegate a complete equilibrium analysis of the dependent information structure to the Online Appendix.

The term in Proposition 1 captures the difference between firm ’s expected payoff of acquiring private information and truthfully disclosing it, and firm ’s expected payoff of not acquiring private information and following an optimal uninformed disclosure strategy. An equilibrium with informative firm disclosure exists under two conditions. First, for the high-type firm, the information acquisition costs should be lower than the benefits of acquiring private information , that is, . Second, for the low-type firm, the information acquisition costs should be higher than the benefits of acquiring private information , that is, .

In equilibrium, the prices support a mixed disclosure strategy of the low-type firm, as defined by equation (5). To explain the need for a mixed disclosure strategy, note that when a low-type firm would always disclose , the outcomes and would reveal that the firm is a high type as only a high-type firm would disclose . In contrast, a low-type firm would be better off always disclosing . A similar argument applies when a low-type firm would always disclose . Thus, the low-type firm must choose a mixed disclosure strategy in equilibrium. Finally, note that the truth-telling condition described in Lemma 1 is not binding in equilibrium, as implies that the term between the square brackets in (4) is non-negative, which is always satisfied given the equilibrium condition .

Information acquisition strategies and cannot be supported in equilibrium. For the strategy , where only the low-type firm acquires private information, consistent disclosures are indicative of a low-type firm as the low-type firm is more likely to provide consistent disclosure than the high-type firm. Then the low-type firm is better off by pooling with the high-type firm and not acquiring private information.

The strategy where both firm types acquire private information, also cannot be supported in equilibrium. Importantly, under the dependent information structure, voluntary disclosure does not provide direct information on product quality. Only consistency between the firm’s disclosure and the product review can provide information about whether or not the firm has acquired information. When both firm types acquire information and truthfully disclose it, both the high-type firm and low-type firm are equally likely to provide consistent disclosure, so the consistency of the firm’s disclosure no longer provides information about the firm type. Consequently, neither firm type has an incentive to acquire costly private information. Alternatively, when both firm types acquire private information and disclose it non-truthfully, the high-type firm is more likely to disclose than the low-type firm, as the high-type firm is more likely to receive a good product review . This implies that is indicative of a high-type firm, so the low-type firm is better off disclosing without acquiring private information.

Summarizing the equilibrium analysis, the equilibrium with the information acquisition strategy described in Proposition 1 is the only equilibrium where voluntary disclosure provides additional information for customers. We refer to this as the equilibrium with informative firm disclosures for the rest of the paper.11

Discussion

This section discusses several implications of the equilibrium results. For this, we partially rely on numerical analyses because of tractability issues in the equilibrium strategies. In particular, the mixed disclosure strategy of the low-type firm is only implicitly defined by the four price expressions of , , , and . This makes it difficult, if not impossible, to check when all the equilibrium conditions in Proposition 1 are met.

The Interaction Between Two Information Channels

In our model, the interaction between the firm’s voluntary disclosure and the credible product review arises in two different ways. First, the credible product review serves as an ex-post verification device that provides truth-telling incentives for voluntary disclosure. When only the high-type firm has private information on the outcome of the product review , consistent disclosures and are indicative of a high-type firm. This holds true even when the product review is completely uninformative, that is, . In fact, when the product review is completely uninformative, the pair is the only valuable information customers receive: a consistent pair is indicative of a high-type firm and thus a higher likelihood of high product quality, while an inconsistent pair is indicative of a low-type firm and thus a lower likelihood of high product quality.

This information value of disclosure consistency provides a potential explanation for why firms provide advertisements focusing on subjective product perceptions with limited information on objective attributes of the product. Our results suggest that even though firm advertisements offer no additional information about the product, advertisements that are consistent with the product review can improve customers’ perceptions of the firm, and thus of product quality.

For the second type of interaction, the information that the product review provides on product quality reduces the incremental information content of the firms’ consistent disclosure and thus reduces the benefits of acquiring information. The more informative the product review is, the lower the benefits of providing an informative voluntary disclosure. When these benefits fall below the information acquisition costs, the firm no longer finds it beneficial to acquire private information and provide informed voluntary disclosure.

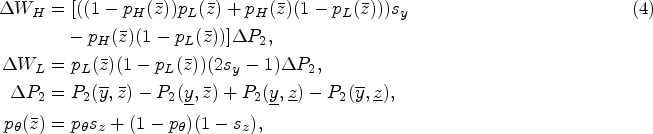

Figure 2 illustrates how the benefits of acquiring private information for firm type change with information precision and in a numerical example. It shows that the benefits are decreasing in the precision of the product review . In particular, the benefits reduce to zero when the product review discloses without error, that is, . Figure 2 also shows that the benefits of acquiring information increase with the precision of the private information. This is so because when the private information becomes more precise, the high-type firm’s disclosure is more likely to be consistent with the product review . Given the same product review , consistent disclosures result in a higher price .

Relation between precision of third-party product review and precision of manager’s private information on firm’s benefits of acquiring information (). Parameter values equal , , , , . The figure shows the combinations of for which the truth-telling condition holds, that is, .

The interactions above suggest that a more informative product review does not always provide more information for customers. A very precise product review can decrease the incremental information from consistent firm disclosure, which then reduces the firm’s incentive to collect private information and issue an informed disclosure. When the precision of the product review marginally increases, it can change the equilibrium from one with informative firm disclosures to one without informative firm disclosures. Empirically, the precision of the product review can depend on both the product characteristics and the product review process. For instance, for newly developed innovative products, it is more challenging to work out which product features are relevant to customers. This can make the product review less accurately predict product value to customers. In addition, a product review based on a small number of customer testimonials on a single product is likely to be less informative about product quality and thus has lower precision than a product review based on a large number of customer testimonials on multiple, comparable products.

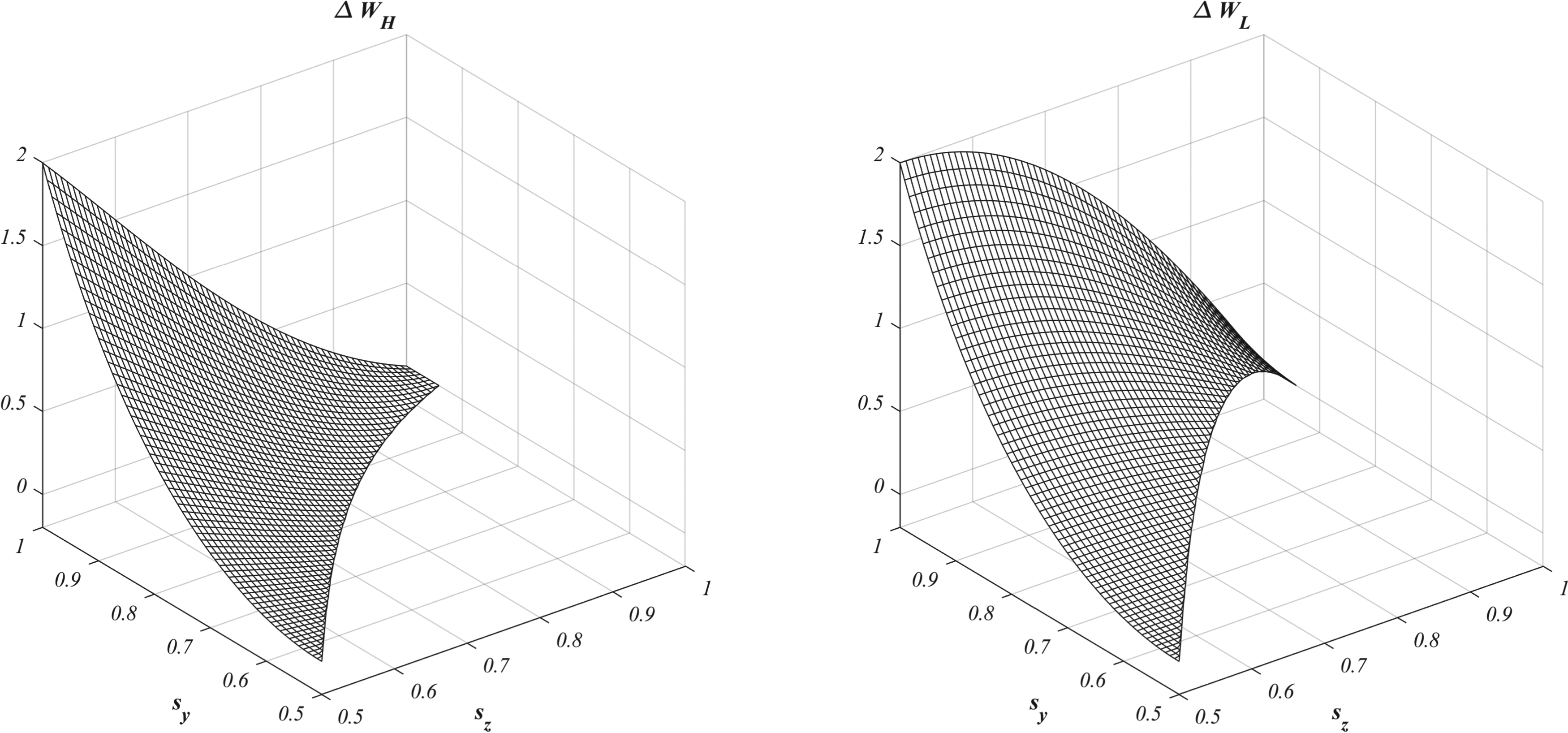

For the same numerical example, Figure 3 illustrates when the equilibrium with informative firm disclosures exists for given information acquisition costs , given precision of the firm’s private information, and given precision of the product review. The figure shows that for given precision , the equilibrium only exists for intermediate precision levels , that is, . The lower bound is determined by the equilibrium condition , that is, the private information needs to be sufficiently precise so the high-type firm would want to acquire it. The upper bound is determined by the equilibrium condition , that is, the private information cannot be too precise; otherwise, the low-type firm also would want to acquire private information. We can use similar reasoning for given precision of private information: the equilibrium with informative firm disclosures exists when , with being the inverse of and being the inverse of . As the benefits of acquiring private information decrease with , ensures that the benefits are not too high so the low-type firm would not want to acquire private information, and ensures that the benefits are not too low so the high-type firm would want to acquire it.

Existence of the equilibrium with informative firm disclosures as a function of the precision of manager’s private information and the precision of third-party product review . Parameter values equal , , , , , , and .

Figure 3 also shows that when the product review is more precise, the lower bound and upper bound both increase, that is, the high-type firm should be able to collect more precise private information at the same cost. When the product review is more precise, it reveals more information about product quality so the incremental benefits of issuing a consistent disclosure decrease. To sustain the equilibrium with informative firm disclosures, higher precision of private information increases the benefits of acquiring private information, as the firm is more likely to provide consistent disclosures based on private information.

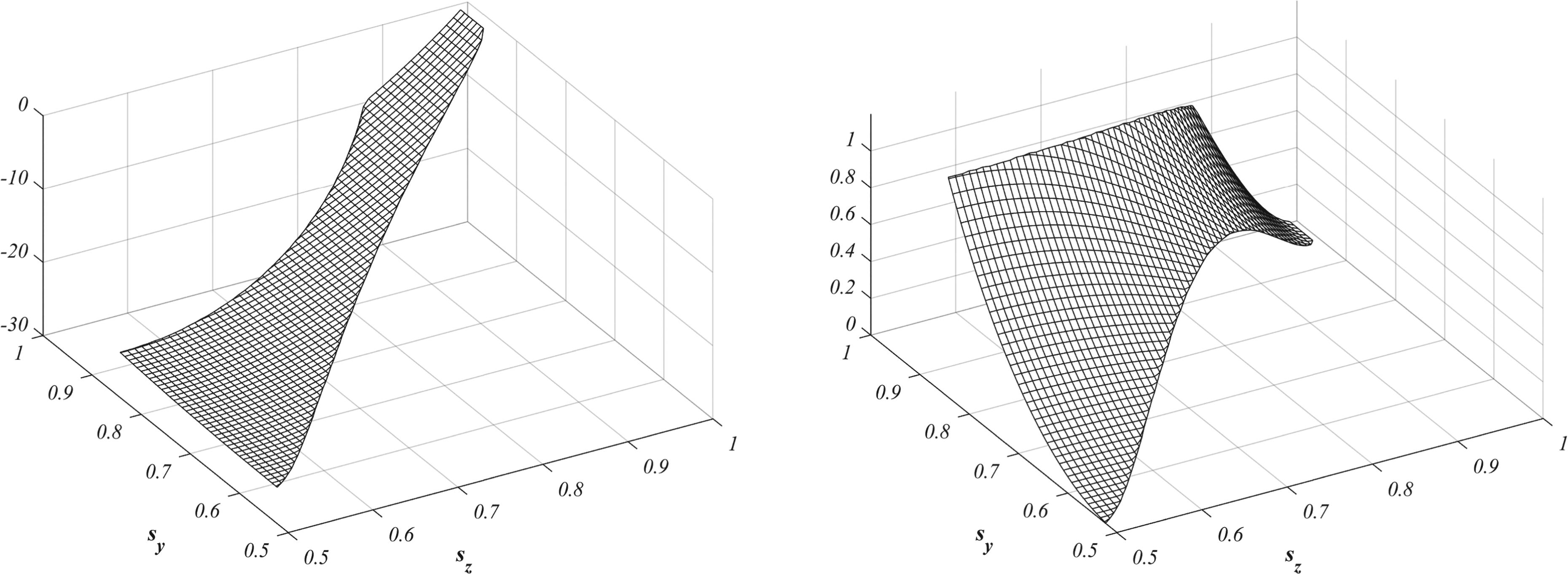

Price efficiency as measured by (a) and (b) as a function of the precision of manager’s private information and the precision of third-party product review . Parameter values equal , , , , , , and .

This result also suggests that the equilibrium with informative firm disclosure exists when there is a (weak) positive relation between the precision levels and . Interestingly, this result implies that when the third-party product review provides more precise information about product quality, customers will receive more information if the firm can more accurately predict the product review, all else being equal. However, when the third-party product review is not very informative about product quality, firm disclosures are likely to be informative if the firm is also unable to accurately predict the product review. Therefore, empirically, one expects to see more firm disclosures consistent with third-party product reviews when the product reviews are more precise.

Price Efficiency and Product Review

In the presence of an equilibrium with informative firm disclosures, the information content of the firm disclosure changes with the precision of the private information and the product review. To analyze the information content of the firm disclosures, we consider the following measures of price efficiency for the equilibrium with informative firm disclosures and uninformative firm disclosures, respectively.

The first measure captures the expected squared difference between the price and the true product quality in the equilibrium with informative firm disclosures. If customers perfectly learn about the product quality, then the measure is equal to zero. The less information customers learn about product quality, the more negative the measure is. The second measure follows the same idea, except that it is calculated for the babbling equilibrium without informative firm disclosures. Therefore, the price depends only on the product review and the measure is independent of the precision of the private information. We provide detailed expressions of and in the Online Appendix.

Figure 4(a) presents a numerical example of price efficiency for the equilibrium with informative firm disclosures. It suggests that price efficiency and thus total information learned by customers is increasing in both and . This is intuitive. If the precision of the private information increases, the high-type firm is more likely to provide consistent disclosures. Thus, the consistency of firm disclosures provides more information about the firm type and product quality for customers. If the precision of the product review increases, customers also learn more about product quality from the product review.

Figure 4(b) presents the difference in price efficiency between the equilibrium with informative firm disclosures and the equilibrium without informative firm disclosures. It represents the additional information customers learn about product quality through firm disclosures. The larger this difference, the larger the information content of the firm disclosure. The figure suggests that the information content of the firm disclosures is increasing in and decreasing in . The explanation for is the same as that for Figure 4(a). For precision , an increase of indicates that the product review provides more information about the firm type. Then there is less additional information to provide by the firm disclosures. Therefore, the information content of the firm disclosures is relatively high when the product review is less informative.

While Figure 4 shows that price efficiency monotonically changes with and when the equilibrium with informative firm disclosures arises, overall, price efficiency non-monotonically changes with and . This is because a change in precision levels or also affects the existence of the equilibrium with informative firm disclosures. Specifically, price efficiency increases when a marginal increase of either or changes the equilibrium from a babbling equilibrium to the equilibrium with informative firm disclosures. The price efficiency is always higher in the equilibrium with informative firm disclosures than in the babbling equilibrium, because disclosure consistency reveals additional information about the firm type in the equilibrium with informative firm disclosures. However, price efficiency decreases when a marginal increase of either or eliminates the equilibrium with informative firm disclosures.

Firm Type and Information Acquisition

In this subsection, we also analyze how the firm’s benefits from information acquisition vary with the firm type . For the equilibrium with informative disclosures, the low-type firm receives higher benefits from acquiring private information than the high-type firm, that is, . We explain this using the following simplified example. Suppose the high-type firm realizes the high product quality with probability , while the low-type firm realizes with probability . Recall that in equilibrium, a consistent disclosure is indicative of a high-type firm so the benefits of acquiring private information arise from the increased likelihood of providing a consistent disclosure. Then to maximize the likelihood of making a consistent disclosure, an uninformed high-type firm would disclose and an uninformed low-type firm would disclose . As this disclosure strategy immediately reveals firm type, the low-type firm has to disclose with positive probability, that is, the low-type firm has to use a mixed disclosure strategy. Since a mixed disclosure strategy increases the likelihood of providing an inconsistent disclosure, the low-type firm benefits more from acquiring private information than the high-type firm.

When there is an equilibrium with informative firm disclosures, the high-type firm receives lower benefits from acquiring private information than the low-type firm, that is, , where and are as defined in Proposition 1. Hence, if the high-type firm has equal or higher information acquisition costs than the low-type firm, that is, , then the equilibrium with informative firm disclosures does not exist.

Corollary 1 implies that if a firm can make informative voluntary disclosures about the product quality and firm type, we expect to observe that a firm with more consistent disclosures has lower information acquisition costs. In other words, a firm that produces high-quality products has lower information acquisition costs.12 In practice, many factors can impact the costs of collecting customers’ perceptions of product quality. Low costs can arise from having a strong product and market research team, from having local customers in contrast to overseas customers, or from having a stable homogeneous customer group instead of dynamic heterogeneous customer groups. Whether firms that are good at producing high-quality products are also capable of efficiently collecting customers’ feedback may depend on the firm’s strategy. Informative firm advertisements are more likely to exist among firms (industries) that assign equal importance to developing high-quality products and understanding customers’ feedback about the product. In contrast, informative firm advertisements are less likely to exist among firms that mainly concentrate on developing innovative product features with little emphasis on customers’ preferences and perceptions.

In summary, our findings have implications on how third-party product reviews affect firms’ information acquisition and advertising strategies. Prior literature has mostly focused on how third-party product reviews can provide useful information for customers. Our findings suggest that third-party product reviews can also influence the firm’s disclosure strategy. We show that a credible third-party product review can lend credibility to a firm’s advertisements. However, an informative product review also reduces the firm’s incentive to advertise. Therefore, an overly informative product review can also lead to less information available to customers. In addition, differences in private information acquisition costs are essential to support informative firm advertisements.

Extensions

This section briefly discusses three extensions of our model. Detailed analyses of these extensions are presented in the Online Appendix. The first two extensions relax our assumption of the dependent information structure. The third extension incorporates early adopting customers.

Independent Information Structure

Under the independent information structure, we assume that the firm’s private information is an independent noisy signal about product quality , with . This information structure can be interpreted as the firm directly learning about product quality by monitoring the production process. For an example of an independent information structure in the context of service industries, consider a customer help desk. Firm management can collect private information about product quality by observing how friendly and patiently employees serve customers. Compared to the dependent information structure, if the third-party product review focuses more on the ability of the help desk to solve customers’ problems rather than the friendliness of the employees, the private information under the independent information structure provides less information about the outcome of the product review than the dependent information structure.

Similar to the dependent information structure, customers use both voluntary disclosure and product review to update their beliefs about product quality . In contrast to the dependent information structure, a babbling equilibrium where neither firm type acquires private information and provides informative disclosures is the only possible equilibrium. Complete equilibrium analyses of the independent information structure are provided in the Online Appendix.

Under the independent information structure, there only exists an equilibrium where both firm types do not acquire private information, that is, , and follow the same (non)disclosure strategy so a firm’s voluntary disclosure is uninformative.

The reason an equilibrium with informative firm disclosures cannot exist is as follows. When the private information follows the independent information structure, private information and product review are two independent signals of product quality . Although acquiring private information and disclosing consistent bad news disclosure can provide positive news about the firm type, disclosure also provides negative news about product quality in addition to the bad product review . This negative news dominates the positive news about the firm type, so customers perceive that the product quality is worse under consistent bad news than under inconsistent good news , that is, . In this case, truthful disclosure of private information is suboptimal, so the firm is better off not acquiring private information and always disclosing good news . Consequently, informative firm disclosures cannot arise with an independent information structure.

Comparing the equilibrium result between the independent and dependent information structures, we find that a subtle difference in the information structure can significantly influence the firm’s information acquisition and disclosure strategies. While the firm’s private information under the independent information structure can potentially provide more information about product quality for customers, the informational value of the signal also creates strong incentives for untruthful disclosure, which cannot be disciplined by a credible product review. Without such informational value under the dependent information structure, a product review can discipline and lend credibility to the firm’s voluntary disclosure.

Mixed Information Structure

In this subsection, we show that a fully dependent information structure is not necessary to support an equilibrium with informative firm disclosures. For this, let denote private information based on a mix of the dependent and independent information structures. One way to interpret is the probability that the acquired private information has the dependent information structure and is the probability that it has the independent information structure. Hence, results in the dependent information structure with precision and results in the independent information structure with precision . The higher the value of , the more information the private signal provides about the product review . Hence, we can interpret as the extent to which the firm’s collected private information about product quality overlaps with the product review. Full details of the mixed information structure are presented in the Online Appendix.

We find that a pure dependent information structure is not necessary to obtain an equilibrium with informative firm disclosures. When the incremental information from disclosure consistency is high or when the information content of independent private information is low, the benefits of acquiring private information can be relatively high. Thus, an equilibrium with informative firm disclosures can still be sustained with a relatively low value of .

Early Adopting Customers

In our model, the product review can be interpreted as being based on the experiences of customers who have already purchased and used the product at an earlier date, that is, early adopters. In this subsection, we analyze how the presence of early adopters affects the existence of the equilibrium with informative firm disclosures under the dependent information structure.

Assume that there exists a proportion of early adopters who buy the product at date after the firm has made its voluntary disclosure decision.13 These customers purchase the product at price , which is equal to the expected product quality given the firm’s disclosure , that is, . The remaining proportion of customers purchase the product after learning both the firm’s disclosure and the third-party product review, as in our main model. The firm’s objective function incorporates both prices and ; that is, the firm maximizes

We analyze two cases. One case is where and does not change the precision of the product review. The other case is when the precision of the product review depends on the proportion of customers who are early adopters. Intuitively, one can expect that the precision of the product review increases in the fraction of early adopters. The equilibrium results of the dependent information structure remain qualitatively the same in both cases. An equilibrium with informative firm disclosures can still exist. Detailed analyses and some numerical examples are presented in the Online Appendix.

Compared to our main model with , the benefits of acquiring private information and making a consistent disclosure are weaker when since the firm also cares about the date price . Hence, when firm disclosures are informative, . Then it becomes more attractive to not acquire private information and always disclose good news . Our numerical analyses show that for , and equilibrium with informative firm disclosures no longer exists when the precision is sufficiently high. The equilibrium breaks down for two reasons. First, a positive value of decreases the benefits of consistent disclosures and a very informative product review further reduces the incremental information from (in)consistent disclosures. Thus, the benefits of acquiring private information are lower than the information acquisition costs so the high-type firm does not want to acquire private information. Second, the lower incremental information of consistent disclosures also implies that it becomes more attractive for the low-type firm to disclose good news to increase . Consequently, the low-type firm may prefer to always disclose good news instead of following the mixed disclosure strategy.

Conclusion

This paper examines the interaction between two product quality disclosure channels and how it can influence customers’ perceptions of product quality. Specifically, we consider a cheap-talk style of voluntary disclosure from the firm and a credible product review by a third-party. Firms can choose to acquire costly private information that helps them predict credible product reviews before making a voluntary disclosure decision.

We find that an equilibrium can exist with informative firm disclosures even when the firm’s private signal does not add any information about product quality besides the product review. In equilibrium, the high-type firm acquires private information and truthfully discloses it, whereas the low-type firm does not acquire information and issues an uninformed disclosure. In this case, whether the voluntary disclosure is consistent with the credible product review is informative about the firm type and product quality. In addition to the positive effect of providing truth-telling incentives, a product review also has a negative effect on information acquisition incentives. The more information the product review reveals about product quality, the lower the incremental value of the firm’s voluntary disclosure. When the product review becomes sufficiently informative, the firm has no incentive to acquire private information and to provide an informed voluntary disclosure. Hence, we find that an overly precise third-party product review can reduce the total information available to customers by eliminating the informative voluntary disclosure from the firm.

Although we have used cheap-talk advertising and credible product reviews to motivate our setting, the implications of our model can also be generalized to other settings. For instance, one can also interpret a cheap-talk voluntary disclosure as a management earnings forecast and a credible product review as an audited financial report. In this case, we find that a firm’s forecast accuracy can reveal information about the firm type and that the firm with higher forecast accuracy is likely to have lower information acquisition costs.14

Appendix: Proofs

Proof of equilibrium conditions in Lemma 1 and Proposition 1. We prove the equilibrium conditions in four steps. First, we derive the equilibrium prices given the equilibrium strategies of high- and low-type firms. Second, we prove the equilibrium condition and existence for the low-type firm’s mixed disclosure strategy, given its equilibrium information acquisition strategy. Third, we derive the equilibrium conditions for the high-type firm’s disclosure and information acquisition strategies. Lastly, we derive the condition under which the low-type firm would not deviate to an alternative information acquisition strategy.

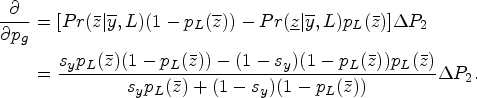

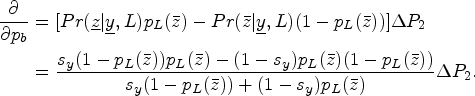

Step 1: Let denote the equilibrium probability that the low-type firm makes an uninformed disclosure . Note that influences prices , , , and . Under the equilibrium strategies of both firm types, the equilibrium prices equal

Step 2: Without any private information, the low-type firm is indifferent between always disclosing and always disclosing if and only if

Based on the equilibrium prices derived in Step , one can show that when , ; when , . In addition, increases with , while decreases with . Therefore, there always exists a that satisfies (9). Moreover, exists when both and hold, or when both and hold. One can show that when , when , when , and when . Given , exists only when both and hold.

where . For the remainder of the proof, it thus holds that .

Step 3: In equilibrium, the high-type firm acquires private information and discloses it truthfully. This yields the expected payoff:

There are two alternative strategies for the high-type firm: first, not acquire private information and offer an uninformed disclosure with probability ; second, acquire private information and disclose it non-truthfully. For the first alternative strategy, the expected payoff equals

Taking the partial derivative with respect to and substituting (10) and (11) yields . Observe that and imply that . Then is optimal. When the high-type firm does not acquire private information, it prefers to disclose . The expected payoff equals , which is less than the equilibrium payoff in (12) if and only if

Substituting (10) and (11) into the above inequality, one obtains

which is equivalent to the condition in Proposition 1. When , the high-type firm will not acquire private information so the babbling equilibrium arises.

Next, consider the second alternative strategy. For private information , the high-type firm would always disclose truthfully. To see this, note that given , the expected payoff of the high-type firm from disclosing with probability equals

As the expected payoff shown above is linear with respect to , the optimal strategy is either or . Taking the derivative with respect to and using (10) and (11) yields

One can show that when , so the high-type firm truthfully discloses .

Assume that the high-type firm discloses with probability when it receives private information . Then the expected payoff given the signal equals

Taking the derivative with respect to and using (10) and (11) yields

As , if and only if . Rewriting this inequality yields condition (3) in Lemma 1. Note that and imply that this inequality always holds. When , the high-type firm would not deviate to the alternative strategy of acquiring private information and disclosing it non-truthfully. When , the high type discloses truthfully and discloses given private information . Consequently, truthful disclosure is not an equilibrium strategy when .

Step 4: We now show when the low-type firm will not deviate from the equilibrium strategy. In equilibrium, the expected payoff of the low-type firm is

There are two alternative strategies for the low-type firm: first, acquire private information and disclose it truthfully; second, acquire private information and disclose it non-truthfully. For the first alternative strategy, the low-type firm’s expected payoff equals

The equilibrium payoff in (14) exceeds the payoff in (15) if and only if

Substituting (10) and (11) yields , which is equivalent to the condition in Proposition 1. When , the low-type firm also acquires private information. We provide the proof in the Online Appendix showing that equilibrium does not exist where both firm types acquire private information. Hence, the babbling equilibrium arises.

For the second alternative strategy, let denote the probability that the low-type firm discloses when it receives private information and let denote the probability that the low-type firm discloses when it receives private information . Given , the low-type firm’s expected payoff from disclosing with probability equals

Taking the derivative with respect to and using (10) and (11) yields

Then and imply that so the low-type firm discloses truthfully.

Given the private information , the low-type firm’s expected payoff is equal to

Taking the derivative with respect to and substituting (10) and (11) yields

Again and imply that , so the low-type firm discloses truthfully.

In summary, the low-type firm would always disclose truthfully when it acquires private information. Recall that acquiring private information and disclosing it truthfully is suboptimal for the low-type firm when condition holds. This completes the equilibrium proof of the information acquisition strategy .

Proof of Corollary 1

Using that , it holds that if and only if . Rewriting and rearranging terms yields . This inequality holds because and . Therefore, in an equilibrium with informative firm disclosures, .

Supplemental Material

sj-pdf-1-pao-10.1177_10591478241279987 - Supplemental material for On the Interaction Between Cheap-Talk Advertising and Credible Product Reviews

Supplemental material, sj-pdf-1-pao-10.1177_10591478241279987 for On the Interaction Between Cheap-Talk Advertising and Credible Product Reviews by Xue Jia and Jeroen Suijs in Production and Operations Management

Footnotes

Acknowledgments

The authors gratefully acknowledge the department editor Anil Arya, the senior editor, and two anonymous referees for their valuable comments. An earlier version of the paper was circulated under the title “The role of private information acquisition on the signaling value of management forecasts.” We thank Jeremy Bertomeu, Bala Dharan, Michael Kirschenheiter, Robert Magee, Ivan Marinovic, Ram Ramakrishnan, Richard Sansing, Sri Sridhar, Jack Stecher, and seminar participants of Tilburg University, Maastricht University, Norwegian School of Economics, the Accounting Research Workshop and Kellogg Accounting Research Conference for helpful comments on the earlier version.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The research is partially supported by the Dutch Research Council (NWO, 40612042).

ORCID iD

Xue Jia

Supplemental Material

Supplemental material for this article is available online (doi: ).

Notes

How to cite this article

Jia X and Suijs J (2025) On the Interaction Between Cheap-Talk Advertising and Credible Product Reviews. Production and Operations Management 34(2): 262–278.

References

1.

AbernethyAMButlerDD (1992) Advertising information: services versus products. Journal of Retailing68(4): 398–419.

2.

AghamollaCCoronaCZhengR (2021) No reliance on guidance: Counter-signaling in management forecasts. The RAND Journal of Economics52(1): 207–245.

3.

AryaAGongNRamananRNV (2014) Quality testing and product rationing by input suppliers. Production and Operations Management23(11): 1835–1844.

4.

BagnoliMWattsSG (2007) Financial reporting and supplemental voluntary disclosures. Journal of Accounting Research45(5): 885–913.

5.

BallRJayaramanSShivakumarL (2012) Audited financial reporting and voluntary disclosure as complements: A test of the confirmation hypothesis. Journal of Accounting and Economics53(1-2): 136–166.

6.

BeyerA (2009) Capital market prices, management forecasts, and earnings management. The Accounting Review84(6): 1713–1747.

7.

CaoHGuanXFanT, et al. (2020) The acquisition of quality information in a supply chain with voluntary vs. mandatory disclosure. Production and Operations Management29(3): 595–616.

ChenYXieJ (2008) Online consumer review: Word-of-mouth as a new element of marketing communication mix. Management Science54(3): 477–491.

11.

CortsKS (2014) Finite optimal penalties for false advertising. The Journal of Industrial Economics62(4): 661–681.

12.

CrawfordVPSobelJ (1982) Strategic information transmission. Econometrica: Journal of the Econometric Society50(6): 1431–1451.

13.

DafnyLDranoveD (2008) Do report cards tell consumers anything they don’t already know? The case of medicare HMOs. The RAND Journal of Economics39(3): 790–821.

14.

DranoveDJinGZ (2010) Quality disclosure and certification: Theory and practice. Journal of Economic Literature48(4): 935–963.

15.

DyeRA (1985) Disclosure of nonproprietary information. Journal of Accounting Research23(1): 123–145.

16.

EinhornE (2005) The nature of the interaction between mandatory and voluntary disclosures. Journal of Accounting Research43(4): 593–621.

17.

FengMLiCMcVayS (2009) Internal control and management guidance. Journal of Accounting and Economics48(2): 190–209.

18.

FishmanMJHagertyKM (2003) Mandatory versus voluntary disclosure in markets with informed and uninformed customers. Journal of Law, Economics, and Organization19(1): 45–63.

19.

GardetePM (2013) Cheap-talk advertising and misrepresentation in vertically differentiated markets. Marketing Science32(4): 609–621.

20.

GardetePMGuoL (2021) Prepurchase information acquisition and credible advertising. Management Science67(3): 1696–1717.

21.

GhoshBGalbrethMR (2013) The impact of consumer attentiveness and search costs on firm quality disclosure: A competitive analysis. Management Science59(11): 2604–2621.

22.

GiglerF (1994) Self-enforcing voluntary disclosures. Journal of Accounting Research32(2): 224–240.

23.

GiglerFHemmerT (1998) On the frequency, quality, and informational role of mandatory financial reports. Journal of Accounting Research36: 117–147.

24.

GodigbeBGJenningsJSeoH, et al. (2024) The effect of geographic diversity on managerial earnings forecasts. European Accounting Review33(3): 995–1024.

25.

GuanXChenY (2017) The interplay between information acquisition and quality disclosure. Production and Operations Management26(3): 389–408.

26.

JinGZLeslieP (2003) The effect of information on product quality: Evidence from restaurant hygiene grade cards. The Quarterly Journal of Economics118(2): 409–451.

27.

JovanovicB (1982) Truthful disclosure of information. The Bell Journal of Economics13(1): 36–44.

28.

JungWKwonYK (1988) Disclosure when the market is unsure of information endowment of managers. Journal of Accounting Research26(1): 146–153.

29.

KwonYKNewmanPZangY (2009) The effects of accounting report quality on the bias in and likelihood of management disclosures, Working paper, Singapore Management University, Singapore.

30.

LevinDPeckJYeL (2009) Quality disclosure and competition. The Journal of Industrial Economics57(1): 167–196.

31.

LiuYCooperWLWangZ (2019) Information provision and pricing in the presence of consumer search costs. Production and Operations Management28(7): 1603–1620.

32.

LundholmR (2003) Historical accounting and the endogenous credibility of current disclosures. Journal of Accounting, Auditing and Finance18(1): 207–229.

33.

MayzlinD (2006) Promotional chat on the internet. Marketing Science25(2): 155–163.

34.

MittendorfBZhangY (2005) The role of biased earnings guidance in creating a healthy tension between managers and analysts. The Accounting Review80(4): 1193–1209.

35.

NewmanPSansingR (1993) Disclosure policies with multiple users. Journal of Accounting Research31(1): 92–112.

36.

RamakrishnanRWenX (2016) Meeting company-issued guidance and management guidance strategy. Journal of Law, Finance, and Accounting1(2): 319–359.

37.

RhodesAWilsonCM (2018) False advertising. The RAND Journal of Economics49(2): 348–369.

38.

SpenceM (1973) Job market signaling. The Quarterly Journal of Economics87(3): 355–374.

39.

StockenPC (2000) Credibility of voluntary disclosure. The RAND Journal of Economics31(2): 359–374.

ZhuHYuYRayS (2021) Quality disclosure strategy under customer learning opportunities. Production and Operations Management30(4): 1136–1153.

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.