Abstract

Natural disasters and disease outbreaks cause substantial social turbulence and economic damage. The survival and continued operation of local small businesses and entrepreneurs are critical to the development activities in post-disaster recovery. However, these small businesses and entrepreneurs face greater challenges in accessing funding through traditional channels during a crisis. Crowdlending, also known as peer-to-peer microfinancing, has been successfully used to bypass traditional channels and raise funds directly from crowd lenders. However, it is unclear if such platforms can also be effectively used in the aftermath of crises, given that disasters induce both prosocial motivations and risk considerations in lender responses. To understand the operational implications of crowdlending for small businesses, we examine how crowdlenders respond to loan requests during a crisis and what factors moderate their responses. Drawing on the literature on disaster management and crowdlending, we hypothesize that lenders respond positively to loan requests from crisis-affected areas, and such responses are moderated by fundraising objectives and the lender's national culture. With observational data from an influential crowdlending platform and the 2014 Ebola outbreak as the treatment in a natural experiment design, we find that, on average, lenders respond positively to loan requests from crisis-affected areas, and they tend to favor loan requests emphasizing economic rather than social objectives. Furthermore, lenders from collectivistic cultures are more likely to respond positively during a crisis than lenders from individualistic ones. Our study contributes to research and practice in disaster management, particularly small business operations management during crises, by showing that crowdlending can be a useful fundraising channel for small businesses, which is meaningful for post-disaster economic development and recovery. We also offer implications for the recent conversation on the coronavirus disease 2019 (COVID-19) pandemic by analyzing and discussing the similarities and differences between the Ebola outbreak and the COVID-19 pandemic.

Keywords

Introduction

Natural disasters, such as Hurricane Katrina, and disease events like the Ebola outbreak and the coronavirus disease 2019 (COVID-19) pandemic, have caused substantial social turbulence and economic damage, particularly in the developing world (Yang, 2008). In 2022, natural disasters caused a worldwide total loss of $313 billion in their immediate aftermath and long-term recovery is usually as costly, if not more so. Scholars studying disaster management hope to alleviate the detrimental impact of crises on victims, businesses, and communities by focusing on developing better practices for mitigating the social and economic impacts across the different stages of disasters, namely preparation, relief, mitigation, and recovery.

There is a growing consensus among scholars that the final stage of disaster management—economic and social recovery—requires greater attention (Besiou et al., 2021). Research suggests that local businesses, particularly small businesses, and micro-enterprises, constitute the core of social and economic recovery in the aftermath of a disaster; they serve as local suppliers or distributors (Sodhi and Tang, 2014), supporting the development of supply chains (Sodhi and Knuckles, 2021) and humanitarian programs (Ibrahim and El Ebrashi, 2017). These operations provide social benefits for the community to ensure the attainment of post-disaster development goals. Therefore, the survival and continued operation of these local businesses are critical to the final stages of disaster management, i.e., in mitigating the detrimental impacts of and facilitating the recovery from a disaster.

However, it is not easy for local businesses to survive a major crisis. Small businesses often rely on microloans from banks, the government, or lenders (Sodhi, 2016) to sustain their business. Crises such as natural disasters and disease outbreaks increase both the competition for financial resources and the risk of loan defaults and bankruptcy among small businesses, hindering their access to sufficient financing through traditional channels. Although online crowdlending platforms 1 have been used for bypassing traditional channels to raise funds for entrepreneurs and small businesses (Lee and Tang, 2018), it is not yet clear if such platforms can also be effectively used in the aftermath of crises. This is because lenders on crowdlending platforms (crowd lenders) are often motivated by prosocial intentions (Allon and Babich, 2020), but they still expect full repayment, and they consider the risks and uncertainty associated with lending money on such platforms (Allison et al., 2015). When small businesses use crowdlending to raise funds during or after a crisis, crowdlenders may have the intention to act prosocially, but are also concerned about the risk of default or delinquency. It is therefore unclear how lenders on crowdlending platforms respond to loan requests during a crisis.

Furthermore, crowdlending platforms, being digital in nature, connect diverse borrowers and lenders with heterogeneous objectives and perspectives. Existing operations management (OM) literature on stakeholder preferences during post-crisis development and recovery periods suggests that there could be considerable variations in lender responses to loan requests (Sodhi, 2015; Sodhi and Knuckles, 2021). These variations in lender responses, due to their preferences, can be shaped by the objectives of borrowers and the perspectives of the lenders (Jonas, 2012; London et al., 2010). For example, factors such as the objectives of the fundraising operations and the national culture of lenders can impact lender responses (Burtch et al., 2014; Moss et al., 2018). It is thus crucial to delve into these moderating factors to gain insights into the conditions under which lenders are more inclined to respond positively or negatively during a crisis. More importantly, these moderators could materialize by shaping lender preferences regarding their inclination toward prosocial actions and their assessment of risks, further complicating the tension of lender responses in the event of a crisis (Galak et al., 2011). Therefore, the focus of our paper is to provide operational advice for small businesses by investigating how crowd lenders respond to loan requests during a crisis, and what factors moderate their responses during a crisis.

Drawing on the literature on disaster management and crowdlending, we develop a theoretical model of lender responses for small business fundraising during a crisis. We argue that in crowdlending, crises are associated with both stronger intentions to help victims due to their identifiability (i.e., identifiable victim effect) and greater consideration of the risks of loan delinquency and default (i.e., risk effect). As crowdlending tends to involve relatively small loan requests and small individual lender contributions, which can help to mitigate the risk effect, we suggest that the identifiable victim effect will likely supersede the risk effect (i.e., positive lender responses).

In gauging the moderating effects in question, we draw on the OM literature on disaster management which suggests the salience of business operation objectives and national culture. The disaster management literature has extensively argued the importance of the social and economic objectives of operations in sustaining businesses and supporting the development of supply chains (Sodhi, 2015; Sodhi and Knuckles, 2021). We propose that the information transparency in crowdlending (Mejia et al., 2019; Xiao et al., 2021) facilitates the exhibition of both social objectives (e.g., community benefits, social performance) and economic objectives (e.g., financial sustainability, economic growth), enabling them to positively moderate lenders’ responses during a crisis. In addition, the disaster management literature suggests the important role of national culture in disaster and risk operations (Gupta and Gupta, 2019). We propose that lenders from collectivistic cultures are more likely to exhibit positive responses during a crisis than lenders from individualistic cultures.

To test the proposed hypotheses, we use naturally occurring field data from Kiva, an influential crowdlending platform supporting small businesses in value creation. We employ the case of the 2014 Ebola disease outbreak in West Africa as the treatment in a natural experiment design and use the difference-in-differences (DID) approach to estimate the changes in lender responses to loan requests before and after the crisis. The Ebola outbreak exposed borrowers in affected areas to greater risk and uncertainties, and significantly increased small businesses’ operational risks, thus making access to funding more difficult for borrowers. 2 Our results suggest that lenders, on average, responded positively to loan requests from crisis-affected countries. By analyzing the loan narratives, we find that lenders tended to favor loan requests emphasizing economic, rather than social objectives during the crisis. Furthermore, by integrating cultural data from the World Values Survey, our analyses and results suggest that lenders from collectivistic cultures were more likely to respond positively than lenders from individualistic cultures during the Ebola outbreak. Supplementary matching analysis, country pair level analysis, and replication analysis on the COVID-19 pandemic further corroborate our findings and offer additional insights into lender responses during crises.

In integrating the literature on disaster management and crowdlending, this study adds to the OM literature on disaster management in terms of how small businesses raise funds to survive in times of crises (Gupta et al., 2022b). Local businesses are important stakeholders in supporting the development and recovery phase, and we offer them operational implications on using crowdlending during a crisis. We also contribute to the literature on online crowdlending via the examination of lender responses in extremely unstable circumstances. Moreover, we uncover variations in lender responses during a crisis from the perspective of fundraising objectives and national culture, which offer important implications for small businesses to better utilize crowdlending platforms. Our findings further add to the literature on the objectives of operations and national culture (Gupta and Gupta, 2019) while contributing to recent academic discussions on the COVID-19 pandemic.

Related Literature

The central theme of our work involves studying the fundraising operations of small businesses through online crowdlending. Specifically, we build on prior works on OM during disasters, crowdlending behaviors, and the role of operational objectives and national culture in disaster management.

Disaster Management and Small Businesses

There is a rich stream of literature studying OM in the context of disasters from various perspectives. The core topics include the humanitarian side of disaster response operations (Besiou and Van Wassenhove, 2020), the impact of disasters on supply chains and mitigation strategies (Farooq et al., 2021), and the handling of business operations in the immediate aftermath (Gupta et al., 2016).

Within this stream of research, the literature on small business operations during disasters or major crises is most pertinent to our study. This line of work has focused on two aspects of OM during major crises. The first examines how disasters affect small business operations, such as operational performance and supply chain capacity (e.g., Hendricks et al., 2020; Jola Sanchez, 2022). In a study particularly relevant to our theme, Alekseev et al. (2023) studied small businesses during the COVID-19 pandemic and found that they faced financial challenges and had limited access to funding. The second aspect focuses on the importance of OM for the survival of small businesses through major crises, such as leveraging operational slack and resilience (e.g., Chen et al., 2022; Li et al., 2022). Particularly relevant to our theme, prior research has shown that small businesses serve as suppliers and distributors within the local economy (Sodhi and Knuckles, 2021; Sodhi and Tang, 2014), thereby improving the chances of their own survival and supporting humanitarian or development supply chains in response to major crises.

Synthesizing these two aspects of the literature, we focus on the fundraising operations of small businesses during crises. For small businesses, raising funds to sustain their business is an important aspect of their operations. Traditionally, small businesses rely on microloans through banks, the government, or lenders (Sodhi, 2016) to sustain their business. Crises such as natural disasters and disease outbreaks increase the risk of loan defaults and bankruptcy among small businesses, hindering these businesses from raising funds through traditional channels. The current OM literature on disaster management, although discussing various aspects of small business operations during disasters, lacks an understanding of fundraising operations in such contexts. By understanding how small businesses should operate to raise funds and sustain their business, our study fills an important void in the OM literature on disaster management.

Such an investigation is meaningful given the growing popularity of online fundraising channels. While online crowdlending platforms have been used to bypass traditional channels and raise funds for small businesses and entrepreneurs (Lee and Tang, 2018), it is unclear if such platforms can also be effectively used in the aftermath of crises. In crowdlending, the outcome of fundraising is determined by lender responses to the microloan requests, and crowdlenders are characterized by mixed considerations in their lending decisions (Allison et al., 2015). Such considerations in lender responses create tension regarding the operational value of crowdlending and we discuss their foundations below.

Prosocial Motivations and Risk Considerations in Crowdlending

For small businesses, periods of natural disasters and disease outbreaks are characterized by both a greater need for financial help and higher operational risks (Corbett et al., 2022). These considerations also come into play when these businesses use crowdlending platforms to raise capital for their survival because crowdlenders are driven by both prosocial motivations and risk considerations (Allison et al., 2015; Galak et al., 2011). In other words, lenders on crowdlending platforms voluntarily respond to a loan request with no expectations of personal financial gains—no fees or interest payments are expected in return for lending their money. Lenders’ prosocial motivations have been prominent in supporting business operations and sustaining economic development (Lee and Tang, 2018; Yan et al., 2022).

Nevertheless, it is worth noting that the payments lenders make on crowdlending platforms are not a form of charity as they do expect to be repaid. Like any lending-based transaction, online crowdlending is associated with the risk of default or delinquency as well as exchange-related risks resulting from currency fluctuations (Allison et al., 2013). Prior studies found that risk cues decrease the attractiveness of loans to lenders (Allison et al., 2015) and cause them to behave strategically (Berns et al., 2018). In other words, risk is a focal consideration in crowdlending decisions.

The present study integrates these two aspects of crowdlending behaviors to examine the fundraising operations of small businesses in crowdlending. During major crises, small businesses have a greater demand for financial assistance while operating with higher risks and uncertainties, thus naturally aligning with crowd lenders’ prosocial motives and risk considerations. These two opposing lender preferences will then determine fundraising outcomes via lenders’ responses (Feldman et al., 2019). Hence, we consider these two key aspects of crowdlending behaviors during a crisis as the theoretical mechanism and further investigate the factors shaping them. In particular, the OM literature on disaster management has identified operational objectives and national culture as important factors in shaping operations during major crises. We discuss these in the following sections.

Objectives of Fundraising Operations

As the outcome of fundraising is determined by lender responses, crowd lenders serve as important stakeholders in fundraising operations and their preferences depend on their prosocial motivations and risk considerations (Galak et al., 2011; Sodhi, 2015). Therefore, the type of fundraising conducted by small businesses could determine the value crowd lenders may obtain from lending their funds (London et al., 2010) and, correspondingly, the relative strength of their prosocial motivations and risk considerations. In other words, what the fundraising operation is seeking to achieve (i.e., the objectives) can influence lender preferences and thus has the potential to shape lender responses.

Operations are typically characterized by a multitude of objectives, and business operations span from commercial for-profit objectives to socially responsible operations (Carroll, 1979; Sodhi, 2015). The disaster management literature has emphasized the importance of such objectives and suggested two primary operational objectives during major crises (Sodhi and Knuckles, 2021):

the social objective, related to mitigating social issues, supporting the local community, and improving the well-being of society; and the economic objective, focused on covering costs, making profits, and avoiding long-term dependency on additional funds.

In crowdlending, small businesses need to present these objectives to crowd lenders using loan narratives—a detailed description of what their business is about, why they need the loan, and how they plan to use the money. In the absence of conventional financial information for the purposes of due diligence, such as credit history or credit scores, lenders usually rely on unstructured information, like fundraising objectives, to evaluate loan requests and make lending decisions (Jiang et al., 2017; Liu et al., 2020). Accordingly, the crowdlending literature has stated that the fundraising objectives of a small business can be either socially or economically oriented, which is clarified as value orientations in the loan narrative (Moss et al., 2018); these two value orientations can be independent of one another and each manifests one aspect of the fundraising objectives of a loan request (Moss et al., 2015).

Given the importance of fundraising objectives in the disaster management and crowdlending literature, we use social value orientation (SVO) and economic value orientation (EVO) in the loan narratives to represent the extent to which a small business expresses its social and economic objectives of fundraising. Then, we use these specific and measurable value orientation constructs to examine how the fundraising objectives moderate crowd lender responses during major crises.

Besides the objectives of fundraising operations, the type of lenders could determine their preferences regarding prosocial motivation and risk consideration; i.e., lenders typically have in-built preferences due to their inherent backgrounds. National culture—defined as “the collective programming of the mind which distinguishes the members of one human group from another” (Hofstede, 1980)—is an essential factor guiding individual behaviors, especially in the face of uncertainty (Hofstede, 1980; Jonas, 2012). National culture has emerged as an important factor in OM, such as in risk management and supply chain logistics (Gupta and Gupta, 2019). In the context of the pandemic (e.g., COVID-19 pandemic), recent research has identified the important roles of national culture in preventive behaviors (Alekseev et al., 2023), contagion mitigation (Kumar, 2021), and the effectiveness of policy and governance (e.g., lockdown and technological intervention) (August et al., 2021; Gupta et al., 2022a). However, research on the role of national culture in disaster management has remained limited, despite its importance in understanding operations and behaviors in times of uncertainty (Gupta and Gupta, 2019).

Hypothesis overview.

The role of national culture is also expected to be salient in online crowdlending platforms as these platforms allow for fundraising calls to span geographical boundaries and reach a more culturally diverse audience (Burtch et al., 2014). When making lending decisions during crises, lenders face uncertainties regarding the demand for financial assistance and the risk of business failure. Under such uncertainties, their national cultures serve as one of the key factors guiding their decisions, especially regarding their preferences on prosocial motivations and risk considerations. Thus, we expect national culture to shape lender responses to loan requests during major crises.

In particular, the cultural dimension of collectivism versus individualism can have a profound effect on lender behavior, given its primary role in explaining cultural differences and its relevance in helping behaviors (Batson et al., 2002). Lenders from collectivistic or individualistic cultures may exhibit different response patterns to loan requests which, in turn, contribute to the effectiveness of fundraising operations during disasters. Therefore, by investigating this cultural dimension, we offer operational implications for small businesses to raise funds more effectively through crowdlending and contribute to the disaster management literature on the role of national culture.

In summary, our study investigates the operational implications of online crowdlending for small businesses. Drawing upon disaster management and crowdlending literature, we focus on lender responses during a crisis, which determines the fundraising outcome and examine fundraising objectives and national culture as moderators. Through this study, we extend the OM literature on disaster management in the context of online fundraising operations and offer empirical evidence for small businesses to raise funds effectively through crowdlending platforms during crises.

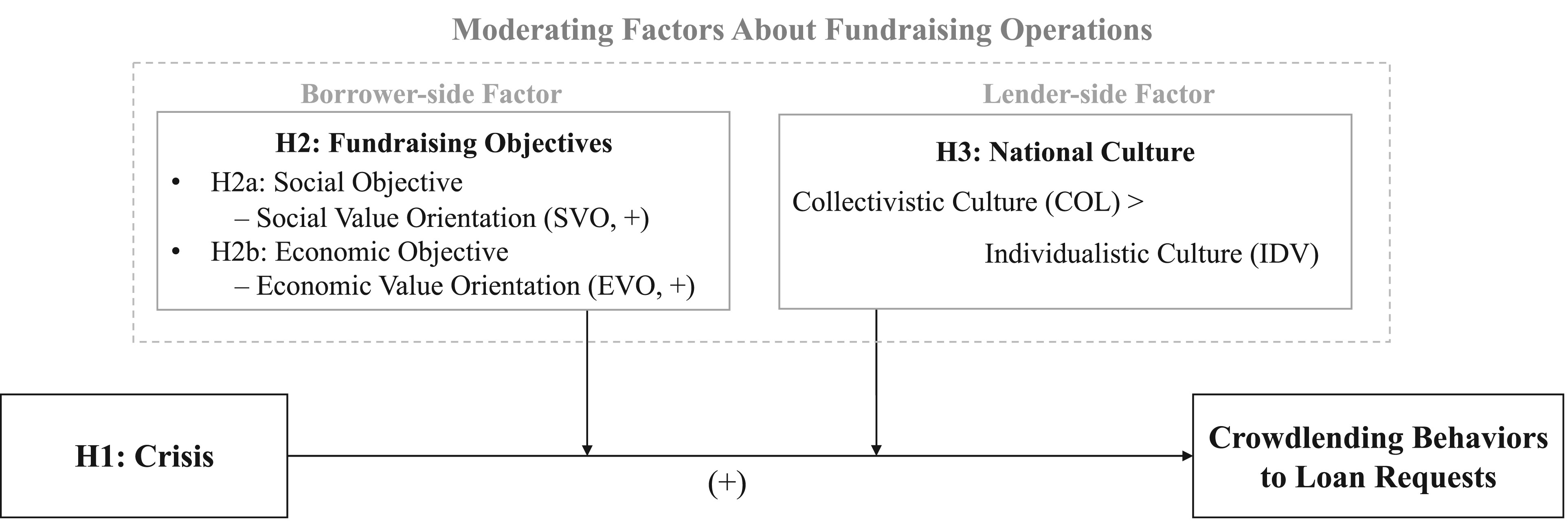

Online crowdlending platforms provide viable options for small businesses to raise funds. To understand the operational implications of crowdlending for small businesses during a crisis, lender responses should be examined as they determine the outcome of fundraising operations. Drawing on the disaster management literature, small businesses tend to need more financial assistance but are operating under greater risks and uncertainties (Alekseev et al., 2023), factors which also feed into lenders’ considerations in their responses. Furthermore, as suggested in the disaster management literature, fundraising objectives and national culture play essential roles in OM during disasters. As borrower-side and lender-side factors on crowdlending platforms, they potentially influence lender preferences on prosocial motivations and risk considerations (Gupta and Gupta, 2019; Sodhi and Knuckles, 2021). Taking these together, we develop hypotheses regarding how a crisis might influence lender responses and how lender responses can be shaped by fundraising objectives and national culture. Figure 1 displays an overview of the hypotheses.

Crowdlending for Fundraising Operations

We first focus on how crowdlenders respond to crises to develop a greater understanding of the value of crowdlending for small businesses during crises. It is not immediately clear how lenders on crowdlending platforms might respond to loan requests from small businesses in crisis-affected areas. Although prosocial motivations strongly characterize crowdlending behaviors (Galak et al., 2011), crowd lenders still expect to be repaid, so they will evaluate the risks accordingly (Wang et al., 2020). This induces tension in crowd lenders’ responses to loan requests from crisis-affected areas; below, we discuss the two potential effects of crises on lender responses and their relative strengths.

On the one hand, loan requests in online crowdlending are made by recognizable individual borrowers, rather than a group of unknown or anonymous borrowers, which is more common for conventional lending via financial intermediaries. In contrast to traditional channels, where financial institutions typically collect funds for general purposes and disburse them to small businesses, borrowers in crowdlending are characterized by greater transparency in terms of identity and purpose. Information transparency allows borrowers to be identifiable to lenders so that lenders know exactly who they are helping and what the borrowers plan to achieve with their money. Borrowers from crisis-affected areas are often seen as victims, whose social well-being and economic conditions have been threatened by the crisis. Kogut and Ritov (2005) suggested that identifying with these victims increases the likelihood that individuals would respond positively to relieving their plight, compared to unidentified sufferers of hardships. Hence, borrowers who request funds during crises become “identifiable victims” and are more likely to receive positive responses from lenders in what has been referred to as the identifiable victim effect (Jenni and Loewenstein, 1997). The identifiability of crisis victims tends to arouse stronger empathic emotions toward borrowers in affected areas as lenders can envision how these borrowers are struggling to make ends meet (Davis, 1994). In other words, a crisis outbreak tends to evoke greater empathy and prosocial intent, which motivates lenders to support borrowers in crisis-affected areas.

On the other hand, the disaster management literature has cautioned that crises and disasters have been associated with higher loan delinquency and default rates (Berg and Schrader, 2012). Eftekhar et al. (2022) note that a crisis can dramatically disrupt business operations, preventing borrowers from successfully executing their business plans. Such uncertainties increase the likelihood that borrowers will default on their loans or delay repayment, causing lenders to lose their money or experience losses due to exchange rate fluctuations. Hence, in the event of a crisis, lenders are exposed to heightened risks of delinquency and default, which the digital nature of crowdlending platforms can exacerbate as lenders may be unable to evaluate borrowers’ financial background information (such as credit score or history) to mitigate these risks. Even if other information is available, its accuracy can be undermined during a crisis (Comes et al., 2020). In the face of this increased uncertainty, crowd lenders may become risk-averse and avoid responding to loan requests from crisis-affected areas (Bourdeau-Brien and Kryzanowski, 2020; Cameron and Shah, 2015). Thus, we may expect a crisis to discourage lenders from responding to borrowers in crisis-affected areas, in what we refer to as the risk effect.

In sum, the identifiable victim effect suggests that lenders respond more positively to loan requests from crisis-affected areas, whereas the risk effect suggests the opposite. On balance, we hypothesize that the identifiable victim effect will prevail for the following reasons. First, online crowdlending enables borrowers to connect with and seek help from lenders globally, which increases access to funding sources. This allows borrowers to request relatively small loans for their current needs, mitigating the risks to which lenders are exposed (Galak et al., 2011). Second, in crowdlending, each lender typically contributes a small amount to a borrower's loan request, so that their capital risk exposure is also small. Moreover, any risk is shared across a large group of lenders, diluting the personal risk for each lender (Ng et al., 2015). For these reasons, crowd lenders’ sensitivity to the risk effect arising from the crisis is relatively weak. Based on these considerations, we formally state our first hypothesis:

Hypothesis 1: Lenders respond positively to loan requests from crisis-affected areas in online crowdlending.

The Moderating Role of Fundraising Objectives

In addition to the operational implications of fundraising through crowdlending, given lender responses during crises, we examine how lender responses are further shaped by the type of operations and the type of lenders. We first discuss the moderating role of fundraising objectives, as identified by the disaster management and crowdlending literature, and particularly the type of objectives that align with lender preferences during a crisis.

As discussed earlier, we follow the extant literature on disaster management in classifying the multitude of fundraising objectives into two groups, namely social and economic objectives (Sodhi and Knuckles, 2021). The social objective of a borrower's loan emphasizes how the money requested by the small business will be used to benefit the community and boost social outcomes (Nicholls, 2010), whereas the economic objective of a loan describes how it will be used for financial sustainability and/or economic growth (Berger and Udell, 2006). As suggested by prior works (Moss et al., 2018; Sodhi and Knuckles, 2021), businesses may pursue a mix of social and economic objectives simultaneously so that the two fundraising objectives are independent of each other.

Although social and economic objectives have been recognized as playing important roles in disaster management, their implications are not yet clearly understood as fundraising objectives in crowdlending. As previously discussed, lenders typically evaluate loan requests through loan narratives instead of traditional financial information, such as credit history or credit scores. However, crowd lenders are rarely finance professionals and do not typically face many of the constraints imposed by policies or regulations that loan officers commonly deal with in the traditional microfinancing context. Therefore, the fundraising objectives in crowdlending may incur preference-based responses from lenders, so lenders’ preferences and responses depend on fundraising objectives in the loan narratives, rather than the policy or environment related to a specific objective.

Social Objective

The social objective has become a focal objective for many small businesses, with stakeholders preferring businesses that benefit society and enhance social outcomes (Bhattacharya et al., 2008). As a result, small businesses are encouraged to emphasize social-oriented objectives to signal their intention to improve social welfare and their engagement in establishing social responsibility (Sodhi, 2015). Financial stakeholders, such as investors and lenders, also tend to prefer that their money be used to create social value (Allison et al., 2015; Mackey et al., 2007). Borrowers on crowdlending platforms can emphasize their social objectives in the narratives of their loan requests, such as enhancing social welfare, improving the lives of families and the community, and increasing environmental sustainability (Moss et al., 2018).

Accordingly, lenders will evaluate loan requests based on the social objectives of fundraising. We expect that, in crisis-affected areas, loans with greater emphasis on social objectives will likely garner more favorable responses from crowd lenders. In particular, expressing social objectives intensifies the identifiable victim effect during a crisis, facilitated by the information transparency of the online platform. During a crisis, affected areas may face severe social uncertainty, reflecting a tremendous need to improve overall social and community welfare. In such circumstances, borrowers articulating their social objectives might provide detailed descriptions of the lives of their families and the communities under the crisis. With vivid and realistic descriptions of the victims, families, and communities to be helped via social objectives, the greater information transparency, enables crowd lenders to better infer whether and how the small businesses will manage to engage in community improvement to benefit other victims and increase overall social welfare (Calic and Mosakowski, 2016). In this sense, emphasizing social objectives helps lenders envision how a small business can help victims and local communities. Accordingly, lenders’ empathy toward the victims during a crisis can be amplified as they get a better sense of what types of families or communities their funds will help. This could further induce crowd lenders to identify with the borrowers, strengthening the identifiable victim effect described earlier (Kogut and Ritov, 2005).

Given these considerations, we expect that a stronger emphasis on the social objective of a borrower's loan request, i.e., a greater level of SVO, will lead to a more intense identification with the borrower's plight and a more positive response toward the loan request. Therefore, we propose the following hypothesis:

Hypothesis 2: Lenders exhibit different responses to loan requests with different levels of SVO during a crisis, such that they respond more positively to loan requests with greater emphasis on SVO in online crowdlending.

Economic Objective

The economic objective is typically related to the economic sustainability and financial development of small businesses. It has been documented that demonstrating financial viability and sustainability is important for small businesses to receive investments and lines of credit (Berger and Udell, 2006). Survival and viability are also regarded as prerequisites to creating social value (Battilana and Dorado, 2010). Furthermore, when making decisions, investors and lenders expect to see a level of profitability sufficient to repay the loan; thus, it is critical for small businesses to be economically viable (Battilana et al., 2015). In crowdlending, borrowers articulate economic objectives by positioning their businesses to be profitable and cost-effective, emphasizing their available assets, and signaling their ability to repay the loan (Moss et al., 2018).

We argue that lenders evaluate loan requests based on economic objectives and that loans with a greater emphasis on such objectives will receive more positive responses from crowd lenders during a crisis. In particular, we propose that, due to the information transparency of online channels, expressing economic objectives mitigates the augmented risk effect from the crisis, thus encouraging more positive lender responses. Crises such as natural disasters and disease outbreaks are typically associated with lockdowns which are especially detrimental to local businesses, leading to a higher risk that borrowers will fall behind or fail to repay the money (Koetter et al., 2020). This risk effect could reduce the chances of receiving financial support from investors and lenders. In such circumstances, borrowers can articulate a roadmap toward survival, profitability, and economic recovery in their loan narratives. Such transparent economic objectives allow borrowers to signal that they have a sound business plan for making a profit with the funds and minimizing potential operational risks to not only survive but also grow during the crisis (Battilana et al., 2015). Accordingly, emphasizing economic objectives helps lenders envision how the borrower can make profits and then repay the principal despite heightened risks due to the crisis. Therefore, loan requests emphasizing profitability and the ability to repay could imbue lenders with more confidence and lower crisis-related risk perceptions, resulting in a reduced risk effect.

In a nutshell, loan requests conveying strong economic objectives, i.e., a greater level of EVO, could reduce the risks crowd lenders perceive, because borrowers have demonstrated their prospects to make their businesses sufficiently profitable to repay the loan. These loan requests are more likely to conform to lenders’ risk considerations and thus receive more positive responses from crowd lenders during a crisis. We hypothesize the following:

Hypothesis 3: Lenders exhibit different responses to loan requests with different levels of EVO during a crisis, such that they respond more positively to loan requests with greater emphasis on EVO in online crowdlending.

The Moderating Role of Lenders’ National Culture

Another factor that shapes crowd lender responses arises from the engagement of lenders from diverse nations and cultures who may behave differently due to their cultural background, posing challenges to effective fundraising operations (Gupta and Gupta, 2019). The existing literature has classified national culture into several canonical dimensions. Hofstede (1980) proposed the most widely quoted framework, with six dimensions. Among these, prior research identified the collectivism-individualism dimension of cultural differences as one of the most influential (Triandis, 2002; Triandis et al., 1988), portraying it as a key motive for community involvement and helping behaviors (Batson et al., 2002). More importantly, this dimension influences the ways in which people care about others, or what people tend to care about in social contexts, which makes it closely related to the intention to help others and to the motivations of crowd lenders. Thus, we examine how lenders’ collectivism-individualism orientation could influence their responses in a crisis.

The cultural dimension of collectivism-individualism has been widely examined in the literature (Buggle, 2020). Collectivism generally represents a set of cultural values or norms that favor the individual's subordination to, and dependency on (or conformity with), the group for survival and security (Oyserman et al., 2002). By contrast, individualism epitomizes the individual's independence (Schwartz, 1994). By and large, collectivistic cultures are characterized by a tight and embedded social fabric in which individuals expect to take care of their in-group (e.g., family, clan, organization), whereas individualistic cultures imply a loose social fabric in which individuals tend to take care only of themselves and their immediate families (Hofstede, 1980). In addition, compared with individuals from individualistic cultures, those in collectivistic ones are more likely to prioritize in-group goals, define themselves based on characteristics of the group, focus on context over content, and pay greater attention to external than internal processes (Triandis, 2002). The cultural orientation of collectivism has also been shown to be associated with agreeableness, self-esteem, empathy, and prosocial behaviors (Chopik et al., 2016).

Although prior research has extensively investigated the role of collectivism and individualism in a variety of settings, lenders may behave differently in the online context of crowdlending. It is interesting to note that lenders often fund geographically separated strangers, diverging from the general context of national culture within a country. In addition, since individuals are unlikely to be constrained by social norms or expectations in the online context, they may behave differently from they do in offline settings. Lenders also have stronger propensities to behave strategically and care more about risk, suggesting potential deviations between online and offline behaviors (Goldfarb et al., 2015; Zentner et al., 2013). Due to these special features of the online context, the comparisons of collectivism and individualism may not be fully replicated in online crowdlending. Therefore, it is unclear whether the cultural dimension of collectivism-individualism plays an important role in crowdlending behaviors.

Below, we propose that during a crisis, the national culture (i.e., collectivism or individualism) of the lenders will shape their responses, such that lenders from collectivistic cultures are more likely to respond positively to loan requests than lenders from individualistic cultures. Although prior studies suggest that individuals from collectivistic cultures are predisposed to help those in their in-group over strangers (Knafo et al., 2009), we argue that crowdlending is inherently a social process of collective action, given that a group of lenders jointly support a loan. Therefore, lenders from collectivistic cultures are more likely to engage in collective actions and herding behaviors in this process. In online crowdlending, information transparency makes lending behaviors observable to others, turning lending decisions into a social process in which collective action is taken to help a borrower with recognizable others while triggering potential herding behaviors. This is particularly salient in the event of a crisis, as borrowers need greater collective engagement to raise funds in time. The social psychology literature has described collectivistic orientation as an important driver for cooperation and collective action (Kelly and Kelly, 1994); since individuals in collectivistic cultures are more likely to follow others, they tend to exhibit stronger herding behaviors (Deleersnyder et al., 2009). Thus, it can be said that individuals from collectivistic cultures are more likely to engage in the social collective action of crowdlending, following other lenders during a crisis, because crisis-affected loan requests trigger their commitment and herding to help borrowers promptly (Chui et al., 2010).

In addition, it is notable that the prosocial aspect of crowdlending relies on empathic responses. As lenders from collectivistic cultures are shown to be more empathic compared with their counterparts in individualistic cultures (Chopik et al., 2016; Heinke and Louis, 2009), their responses to loan requests during a crisis are likely to be more immediate. This is particularly salient considering the information transparency that allows lenders to identify borrowers as individual victims within their specific circumstances. Therefore, the relatively strong empathy of collectivistic lenders is likely to amplify the identifiable victim effect, resulting in a stronger positive effect of the crisis on lending behaviors.

Conversely, lenders from individualistic cultures are inclined to attach a high priority to taking care of their own rather than engaging in collective action (van Zomeren, 2014). They tend to be more sensitive to their own costs and benefits as a result of lending (e.g., whether their lending actions entail fewer risks) rather than committing to the collective action of crowdlending or herding behaviors. Furthermore, it has been suggested that lenders from individualistic cultures have lower levels of empathy (Feldman et al., 2019; Levine et al., 2016). Following this line of reasoning, we contend that a crisis may induce risk-avoidance behavior in lenders from individualistic cultures, resulting in a stronger risk effect, since they tend to be more concerned about the potential risks of default or delinquency due to the dire conditions and uncertainties of a crisis. Therefore, the strengthened risk effect is likely to weaken the positive effect of crises on individualistic lender behaviors.

Taken together, we anticipate that, in the aftermath of a crisis, lenders from collectivistic cultures will respond more positively to loan requests from crisis-affected areas due to their commitment to collective action in crowdlending and the amplified identifiable victim effect, whereas lenders from individualistic cultures will tend to respond less positively to such requests because of the increased risk effect. Taken together, we hypothesize the following:

Hypothesis 4: Lenders from collectivistic cultures respond more positively to loan requests during a crisis than lenders from individualistic cultures in online crowdlending.

Empirical Analysis

Research Context

The context of our study is Kiva.org, an influential online crowdlending platform that facilitates loans for small businesses and individual borrowers. Its stated mission is to alleviate poverty, increase social welfare, and minimize social exclusion by ensuring broad access to credit. Kiva collaborates with local microfinance institutions (MFIs) in each country for its mission. Borrowers are individuals or groups raising funds as small and micro-enterprises, mainly from developing regions such as Africa, Asia, and South America. Loan requests come from various sectors, including agriculture, 3 food, health, and retail, and their purposes range from purchasing supplies or materials and reselling goods to improving living conditions. 4 Local MFIs, who act as mediators between potential borrowers and Kiva, work directly with borrowers to service the loans (Moss et al., 2015). For example, local MFIs help borrowers create their online loan profiles, which are then submitted to Kiva. A profile generally includes information about the borrower, such as their location, a biography, and the general purpose for the loan, as well as a narrative about the borrower's situation and the requested loan amount, repayment schedule, and information about the corresponding local MFI (Burtch et al., 2014). This information transparency enables lenders to identify to whom to lend, borrowers’ fundraising objectives, and what value a borrower can create through their loan. It also allows lenders to view other lenders who are supporting the same loan request. Each loan request has a predetermined expiry date, before which the borrower must reach the requested loan amount. The funding process stops when the requested amount is reached. Since most loan requests on Kiva are fully funded, a typical approach for comparing loan performance is to look at how quickly a loan gets fully funded (Allison et al., 2013).

While borrowers on the platform are mostly located in impoverished areas, prospective lenders come from across the world. At any given point in time, lenders are exposed to hundreds of loan requests from small businesses seeking funds. The lending amount options provided to each lender typically start at 25 USD. Notably, lenders do not earn any interest on the funds they lend through Kiva (Galak et al., 2011), but they expect full eventual repayment from borrowers.

Data

For this study, we collected naturally occurring field observations from Kiva. The data consist of information on (1) borrowers, (2) loans, and (3) lenders. Borrower information includes the name and gender of the borrower and whether the borrower has a profile picture. Loan information covers the loan's location (i.e., the country of borrower), sector, usage, start (posting) and end (expiry) dates, the delinquency rate of the MFI, as well as the requested loan amount, number of lenders, and the loan narrative. If a loan reached the requested amount prior to the predetermined date of expiry, we recorded the funding time. Lender information comprises the name, location (i.e., country), occupation, as well as the reason for lending. As relevant to our research focus, we drew upon the loan narratives to capture the fundraising objectives of the loan, and upon lenders’ location information to identify their culture.

Research Design and Identification Strategy

We adopted a natural experiment design, examining the influence of a specific crisis, to gauge how crises affect crowdlending behaviors. Given Kiva's focus on helping people in developing countries, especially in Africa, we based our study on the 2014 Ebola disease outbreak in West Africa, which caused a tremendous socioeconomic crisis in the region. This was the largest and most severe outbreak in the history of the disease (Koch and Siering, 2015). It resulted in a large number of casualties (more than 11,300 deaths from over 28,600 cases) in West African countries. The number of cases in the affected countries increased dramatically at the beginning of August 2014 and continued to rise in the subsequent months. On August 8, 2014, the World Health Organization (WHO) designated the West Africa Ebola outbreak as a Public Health Emergency of International Concern (PHEIC). The outbreak also received extensive public attention globally from the mainstream media.

The Ebola outbreak created severe socioeconomic impacts in the affected areas, with various sectors, ranging from agriculture to services being hit particularly hard. The crisis affected local business operations, employment rates, incomes, and the demand for goods and services (Wood, 2014). Considering the unique scale and scope of this crisis, we employed it as the treatment in a natural experiment design to examine how crowdlending behaviors changed with this unexpected outbreak. Since the outbreak was largely regional, it suited a natural experiment design with a clear distinction between a treatment group (affected areas) and a control group (unaffected areas). Meanwhile, the recognition of the Ebola outbreak was global, providing a feasible setting to understand crowdlending behaviors from various cultures.

With the Ebola outbreak as the treatment in a natural experiment setting, we employed the DID approach to estimate the changes in lender responses to loans on Kiva before and after the outbreak (Angrist and Pischke, 2008). As the WHO formally designated it a PHEIC on August 8, 2014, we took August 2014 as the event month. To incorporate sufficient periods before and after the event, we included all loans from the beginning of 2013 through the end of 2015 in our sample.

On Kiva, most borrowers are seeking funds for their small businesses across different sectors such as health, agriculture, and housing. Although loan requests did not directly target medical treatments for Ebola, borrowers were exposed to substantial collateral risks from the Ebola outbreak since the local business environment was critically affected by lockdowns, physical restrictions, and supply-demand shocks, given the disease's extremely high death rate. The funds collected from lenders during the Ebola outbreak went into helping borrowers overcome the challenges caused by the crisis.

For example, borrowers operating health services faced challenges purchasing machines or medicine for regular operations, due to sudden demand hikes resulting in a shortage in supply or price increases during the crisis. The funds would be able to help them overcome these challenges in a timely manner to weather the crisis. In a similar vein, for other service or business-related sectors, such as agriculture, food, or retail, borrowers were under greater urgency of purchasing the supplies or goods with the funds to overcome the challenges of supply chains during the crisis. In other sectors such as housing, borrowers sought to benefit from the funds to improve their living conditions and fulfill the basic needs of their families and communities. In general, although borrowers on Kiva may not have been directly related to the Ebola outbreak, such as being the patients or serving patients, their businesses and living conditions were under much greater uncertainty due to the Ebola outbreak. Funds from the crowdlenders could help them survive the crisis by sustaining their businesses or improving the living conditions of local communities. 5

Ebola cases were detected in a total of six West African countries, namely Liberia, Sierra Leone, Guinea, Nigeria, Mali, and Senegal. Kiva operates in all of these counties except in Guinea. Therefore, our treatment group includes loan requests from the remaining five Ebola-affected countries. To evaluate the treatment effect of the Ebola outbreak on crowdlending behaviors, we needed to identify a control group of countries or loans that were not affected by the Ebola outbreak. No Ebola cases were confirmed in African countries outside of West Africa during the study period; thus, due to their similar socioeconomic conditions, we drew upon all loan requests from non-West-African countries in Africa as the control group, to account for the counterfactual (i.e., changes in lending behaviors over time in the treatment group). 6 In Section 5.2, we formally test for the parallel trend assumption of DID by exploiting the time series nature of the data (Angrist and Krueger, 1999) and the estimates of leads and lags (Angrist and Pischke, 2008). In total, the treatment group contains 26,066 loans, and the control group includes 91,226 loans from the years 2013 through 2015.

Although we chose the 2014 Ebola outbreak in West Africa as the focal crisis to understand lender responses—particularly due to Kiva's core mission to support borrowers in developing countries—we also considered the more recent global Coronavirus (COVID-19) outbreak as the focal crisis to corroborate our findings. We discuss this replication analysis in Section 5.3.4.

Model Specifications and Variables

Hypothesis Testing

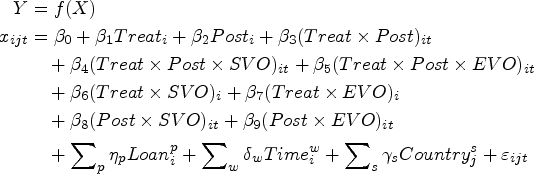

In a natural experiment setting, given the loans in the treatment and control groups, we used the DID estimator to identify the average treatment effect on lender responses. This captures the average change in lender responses, before and after the event in the treatment group, compared to the average change in the control group. The differences in changes between the treatment and control groups capture the treatment effect of the Ebola outbreak on lending activities (Angrist and Pischke, 2008). Our basic econometric model specifications are specified at the loan level, as below:

Following the conventions of prior research, we modeled lender responses with loan outcome, funding time, which captures the length of time (in days) it takes to reach the requested loan amount (Allison et al., 2015; Allison et al., 2013; Moss et al., 2018). When lenders respond more actively to a loan request, it is likely to be fully funded more quickly, resulting in a shorter funding time. Since uncertainty and delays associated with funding have often been cited as key reasons for impaired supply chain performance in disaster management (Natarajan and Swaminathan, 2014), this is in line with our argument that loan requests in crisis-affected areas are seeking urgent financial assistance (Burkart et al., 2016) and coincides with recent research interest in studying funding speed as an outcome variable (Jiang et al., 2020).

Given that the outcome variable (funding time) is a duration, we used survival analysis in the estimations. Specifically, we adopted the proportional hazard model

H1 proposes that lenders respond positively to loan requests during a crisis, so

H2 proposes the moderating effect of fundraising objectives captured by value orientations, including SVO and EVO. Following prior works, we constructed the measure for SVO and EVO using a text analytics approach to the loan narratives. Specifically, we adopted the dictionary from Moss et al. (2018) to identify words and word roots related to social and economic themes using Linguistic Inquiry and Word Count (LIWC) (Tausczik and Pennebaker, 2010), a dictionary-based text analysis tool, with which we quantified the proportion of words related to social and economic values, respectively. LIWC has been widely used in research for textual analysis (e.g., Hong et al., 2018; Song et al., 2022). In our context, examples of social value-oriented words include compassion, family, and harmony, and examples of economic value-oriented words include asset, cost, and profit (Moss et al., 2018). Sample excerpts from loan narratives highlighting social and economic objectives are presented in Appendix A. To test H2, we interacted these two variables, SVO and EVO, with the treatment effect, and also included the interactions between the single terms and value orientation variables.

8

The coefficients

H3 theorizes that lenders from collectivistic cultures respond more positively to loan requests during a crisis than lenders from individualistic cultures. It has been suggested that collectivism and individualism can be seen as the two endpoints of a continuum (Triandis, 2002), which means that an individualistic culture can be identified with a low-collectivistic orientation, and vice versa. To classify lenders into high- or low-collectivistic cultures, we integrated lenders’ country information and culture data from the World Values Survey (Buggle, 2020; Minkov, 2018).

9

The World Values Survey interviewed respondents from around 100 countries (with roughly 1400 respondents per country) on their norms and values across multiple waves. This survey has been used in recent studies to measure cultural factors (Burtch et al., 2014).

10

To measure the collectivistic orientation of a lender's culture, following Buggle (2020) and Triandis (2002), we used items related to opinions on child-rearing in the survey to operationalize the collectivistic orientation for each respondent, because, in collectivistic cultures, child-rearing emphasizes conformity, obedience, security and reliability, which is consistent with the notion of collectivism. We then aggregated the individual-level collectivism scores in the survey into a country-level score, and classified a country as exhibiting a collectivistic culture if its score was above the median of all country-level collectivism scores or as exhibiting an individualistic culture if below the median.

11

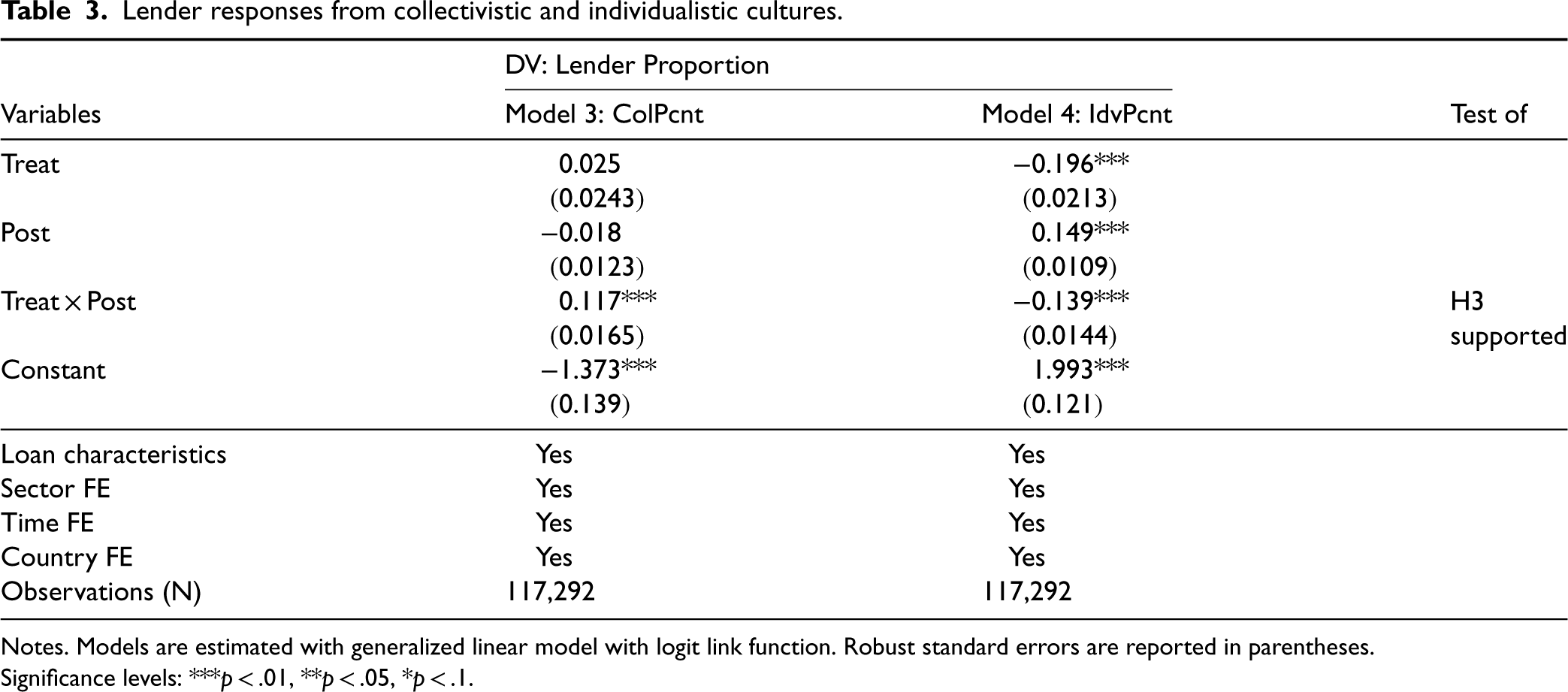

For each loan, we computed the proportion of lenders belonging to collectivistic or individualistic cultures (ColPcnt and IdvPcnt), and used these two measures as dependent variables to test H3.

12

To support H3, we expect that the treatment effect

As the dependent variables used to test H3 are proportional and bounded between 0 and 1, simply employing a linear model could lead to biased estimation (Papke and Wooldridge, 2008). Therefore, we adopted the fractional regression model in the estimations, specified as a generalized linear model with the logit link function

Control Variables

In all the estimation models, we incorporated a series of loan level characteristics

In addition to the loan content, we included the level of platform competition and a set of predefined loan characteristics. For platform competition, we controlled for the total number of active loans on Kiva when a focal loan request was posted (Gafni et al., 2020). For loan characteristics, we controlled for whether the loan request was initiated by a group of borrowers (as opposed to an individual borrower) since prior literature found that whether the borrower was a group or an individual affected lending behaviors (Galak et al., 2011; Kogut and Ritov, 2005). We added the length of loan narrative, operationalized as the number of words, as this signaled a borrower's preparedness, which has been shown to be influential in crowdfunding (Xiao et al., 2021). To account for the linguistic structure of loan narratives, we controlled for the average number of words per sentence. Other loan characteristics we considered include the loan amount a borrower requested; whether a local MFI dispersed the loan to a borrower before it was posted on Kiva;

13

the maximum duration (in days) a borrower set to reach the desired loan amount; and the repayment schedule for the loan (1 if borrowers chose to pay back the loan irregularly, 0 otherwise). Sector fixed effects were also used to account for the category of loans. In addition, we incorporated time fixed effects (

Results

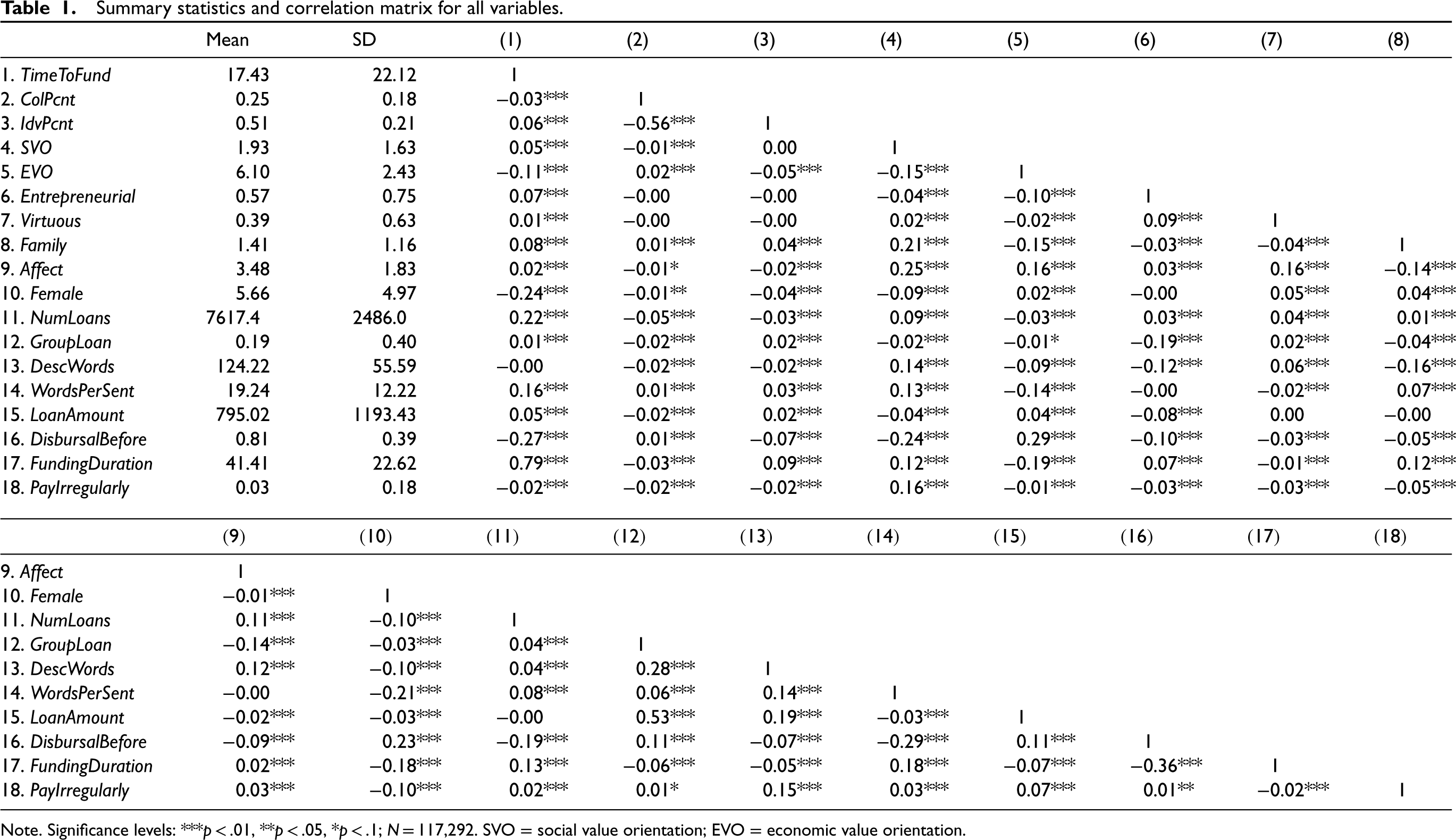

We present the summary statistics and correlation matrix of the loan level sample in Table 1. The variance inflation factors (VIFs) were checked for potential multicollinearity problems and were found to be below the recommended thresholds (Cohen et al., 2013). The maximum and mean VIFs in the analysis are 3.07 and 1.83, respectively, indicating no significant multicollinearity concerns.

Summary statistics and correlation matrix for all variables.

Summary statistics and correlation matrix for all variables.

Note. Significance levels: ***p < .01, **p < .05, *p < .1; N = 117,292. SVO = social value orientation; EVO = economic value orientation.

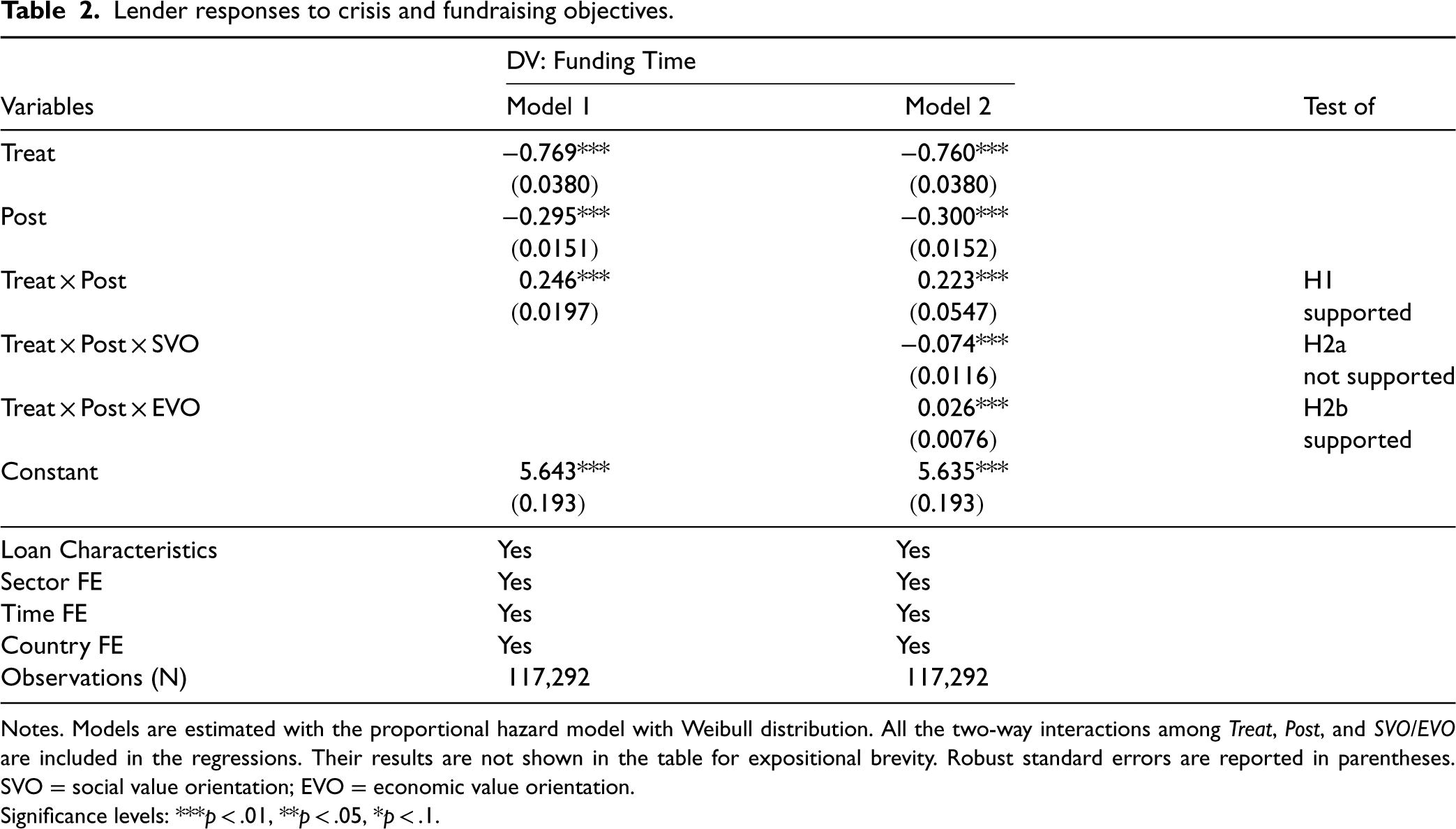

Table 2 presents the results of the estimation of the effect of the Ebola outbreak on lender responses (manifested as funding time of loans using DID) to test H1 and H2. In Model 1, the coefficient of

Lender responses to crisis and fundraising objectives.

Lender responses to crisis and fundraising objectives.

Notes. Models are estimated with the proportional hazard model with Weibull distribution. All the two-way interactions among Treat, Post, and SVO/EVO are included in the regressions. Their results are not shown in the table for expositional brevity. Robust standard errors are reported in parentheses. SVO = social value orientation; EVO = economic value orientation.

Significance levels: ***p < .01, **p < .05, *p < .1.

In Model 2, we investigated the moderating effect of the fundraising objectives (i.e., social and EVOs). The results show that EVO positively moderates the treatment effect of the crisis, whereas the moderation effect of SVO is negative. Therefore, H2a is not supported, while H2b is supported. This suggests that lenders likely shift their focus from social to economic objectives during a crisis, possibly because survival and economic recovery tend to be the central focus in such situations with high uncertainties (Yang, 2008). For small businesses, it seems that achieving economic objectives becomes the prerequisite for benefiting others and improving social welfare (Kent and Dacin, 2013; Moss et al., 2018). In other words, even if a loan's objective is to resolve social issues caused by the crisis and create social benefits, it first needs to demonstrate its economic viability and rely on economic aid to survive (Xiao and Drucker, 2013). Consequently, lenders may prioritize their responses to loan requests based on a greater orientation on economic rather than social objectives to first ensure the survival of borrowers and sustain their economic status for the purposes of repayment.

To further confirm the shift to prioritizing economic objectives, we analyzed the repayment schedule of loans before and after the crisis. Borrowers could choose to pay back the principal monthly or at the end of the payment term. The results suggest an increase in choosing repayment at the end of the term, as opposed to regular monthly repayments, after the crisis in Ebola-affected areas (from 18.8% to 72.5%, t-test p < 0.001), but such an increase is smaller for loan requests with greater orientation on economic objectives (high EVO: from 24.9% to 57.0%, t-test p < 0.001; low EVO: from 15.2% to 80.2%, t-test p < .001). This implies that borrowers experience economic suffering after the crisis, being less capable of fulfilling regular loan repayments, which engenders potential risks in repayment. In such circumstances, borrowers emphasizing economic objectives in their loan requests signify a plan for ensuring survival and minimizing potential risks, so that they are more likely to pay back the money on a regular basis. On the contrary, when borrowers primarily emphasize social objectives, lenders may concern whether the businesses could sustain to fulfill the objectives and repay the loan, thus less likely to positively respond to such loan requests (Battilana and Dorado, 2010). This analysis confirms that creating economic values for survival and recovery becomes the priority after a crisis, and therefore, loan requests oriented toward greater economic values are more likely to receive positive lender responses.

Table 3 presents the results for testing H3, which concerns lenders’ national culture, with lender compositions as the dependent variables. In Table 3, the coefficient of Treat × Post is positive and significant for collectivistic lenders (Model 3), but negative and significant for individualistic lenders (Model 4). This implies more positive responses from lenders in collectivistic cultures than from lenders in individualistic cultures, thus supporting H3. We also compared the coefficients of two models in a joint estimation through seemingly unrelated regressions, and the treatment effect on collectivistic lenders is significantly greater than on individualistic lenders (χ2 = 80.57; p < .001). This result implies that lenders in collectivistic cultures are more likely to engage in the collective action of crowdlending and exhibit more empathic responses during a crisis. Conversely, lenders in individualistic cultures tend to prioritize their own benefits and risk mitigation in their lending behaviors, thus exhibiting slower responses to loan requests from crisis-affected areas than lenders in collectivistic cultures.

Lender responses from collectivistic and individualistic cultures.

Notes. Models are estimated with generalized linear model with logit link function. Robust standard errors are reported in parentheses.

Significance levels: ***p < .01, **p < .05, *p < .1.

The employed DID model allows for the estimation of average treatment effects while eliminating selection bias and the effect of time. The validity of the DID design is based on the parallel trend assumption (Angrist and Pischke, 2008): time trends are the same across loan requests in the treatment and control groups prior to the treatment. To examine the validity of this assumption, we followed Angrist and Krueger (1999) and adopted the widely used approach to test pre-treatment trends. Specifically, we created a time trend variable and estimated the interaction effect between the time trend and the treatment group in the pre-treatment period. The interaction effect was not statistically significant, implying that the pre-treatment trend did not vary across treatment and control groups. This lends support to the validity of our DID identification strategy.

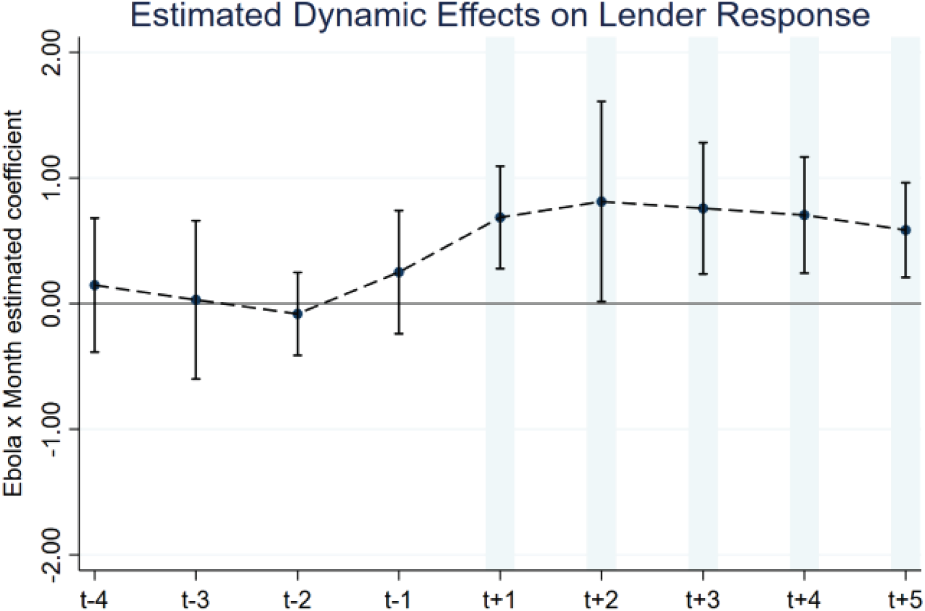

In addition, we confirmed the parallel trend assumption through the estimates of leads and lags (Angrist and Pischke, 2008). We created monthly placebo pre-treatment leads and post-treatment lags, and estimated the dynamic DID coefficients of leads and lags across time. We considered five months before and after the treatment and plotted the dynamic estimates (see Figure 2). The effects of leads in the pre-treatment periods are not significantly different from zero, indicating that the treatment and control groups followed similar trends prior to the treatment. The significant effects of lags in the post-treatment period also suggest the robustness of the treatment effect after the event. Therefore, the parallel trend assumption is likely to hold, given the similar time trends across the treatment and control groups in the pre-treatment periods.

Estimates of leads and lags for parallel trend assumption.

Loan-Level Matching Analysis

We first performed matching analyses to ensure the reliability of the findings. In particular, loan requests from Ebola-affected West African countries may differ from those from non-West African countries in terms of loan characteristics. Similarly, loan requests posted after the Ebola outbreak may be different from those posted before the outbreak. To address these concerns, we conducted two sets of matching analyses: (1) Treatment and control matching, and (2) before and after matching. The results corroborate our findings, and the details of matching analyses are presented in Appendix C. We also examined the quality of matching by checking the balance and common support. The standardized differences and variance ratios between the treated sample (treatment group or pre-Ebola loans) and the matched sample (control group or post-Ebola loans) fall within the suggested ranges, and the ratios of on support loans are satisfactory (see Appendix D).

Country Pair Level Analysis

We further complemented our analysis of lenders’ national cultures (i.e., collectivism versus individualism) through a country pair-level analysis. We followed prior works in crowdlending and international trade (Burtch et al., 2014; Chaney, 2018) to conduct country pair level analysis and examine the role of collectivism and individualism through a continuous measure. The details of performing country pair level analysis are presented in Appendix E. The results are consistent with our loan-level analysis.

Falsification Test and Additional Robustness Checks

We conducted a falsification test with a placebo treatment variable by replacing the loans in Ebola-affected countries with loans in other randomly selected African countries while keeping the loans in the remaining parts of Africa as the control group. The insignificant placebo treatment effect for the random “treated” countries suggests that our findings are valid, further alleviating concerns that our main results might be driven by potential confounds.

To further increase confidence in our findings, we conducted several additional robustness checks. First, we excluded all loan requests whose funding periods coincided with the Ebola outbreak—those overlapping with the event date when the outbreak was designated a PHEIC (i.e., August 8, 2014)—since the event may have affected the funding trends of loan requests already in progress. Second, we excluded all loan requests posted within the month the Ebola outbreak started, as lenders may not have immediately become aware of the crisis. Third, we used different time windows to test whether the results were sensitive to such time windows. Instead of using the time window from 2013 to 2015, we conducted the same analysis with loans in 2014 (the event year), and 10 months before and after the crisis (21 months in total). All tests with different samples exhibit consistency with our main results.

Replication Analysis with the COVID-19 Pandemic

Although we selected the Ebola outbreak as the focal crisis for the main part of our study, to align with Kiva's core mission of helping borrowers in developing countries, the crisis was largely regional (in West Africa) and may therefore have been too limited for our results to be meaningfully generalized. The Coronavirus outbreak in 2019 (COVID-19) has been recognized as a global crisis, having caused a much broader and more significant impact on society and the global economy. To better understand crowdlending as a fundraising channel for small businesses during crises, we replicated our empirical analyses with the COVID-19 pandemic as the focal crisis. The details and results of the replication analysis are presented in Appendix F. The results are consistent with our main analysis of Ebola outbreak but come with some notable differences. The treatment effect of COVID-19 was relatively smaller than that of Ebola outbreak, because lenders’ own countries (and communities) were also affected by the pandemic. Although lenders positively responded to affected loans during COVID-19, their responses were limited due to the global nature of COVID-19 pandemic.

Discussions and Conclusions

In this study, we examine how small businesses can use online crowdlending to raise funds in the aftermath of major crises. Drawing on OM literature on disaster management and online crowdlending, we discussed the operational implications of raising funds in crowdlending through lender responses and the variations in those responses. Specifically, we proposed that lenders respond positively to loan requests during a crisis, and that such responses are further shaped by fundraising objectives and lenders’ national cultures. Empirically, we used data from the online crowdlending platform, Kiva, and employed a natural experiment design using the 2014 Ebola outbreak in West Africa. Our results suggest that, on average, lenders respond positively to loan requests from crisis-affected areas, and they tend to focus on loan requests with economic objectives rather than those with social objectives. Furthermore, lenders from collectivistic cultures are more likely to respond positively during a crisis than lenders from individualistic cultures. Further matching analysis, country pair analysis, and replication analysis of the COVID-19 pandemic corroborate our findings.

Implications for Research

Our findings make important contributions to the related literature. First, we build on OM research on disaster management by examining how small businesses operate during crises to raise funds through online crowdlending channels, which serves as further support to development activities (Sodhi and Knuckles, 2021; Sodhi and Tang, 2014). As the adoption and maturity of digital technologies and online fundraising channels continue to grow, they have become viable options for small businesses to raise funds and survive major crises; however, the operational implications of fundraising through such channels are not yet well understood. This is of particular importance given that crowdlending allows for more sustainable funding flows but is associated with potential risks and uncertainties (Lee and Tang, 2018). Our findings suggest that online crowdlending is an effective channel for borrowers to raise funds and continue their businesses during crises. Online crowdlending platforms have the potential to alleviate the risk effect due to a crisis and facilitate collective actions across geographic boundaries. Crowd lenders, although subject to greater risk of default or delinquency from borrowers during a crisis, still respond positively to loan requests in crisis-affected areas to help small businesses to survive, which in turn facilitates post-crisis development activities. Hence, we advance prior research in disaster management, particularly OM during crises, by developing the theoretical foundation and offering empirical evidence on how small businesses make use of online channels to raise funds and continue their businesses in the aftermath of a crisis (Alekseev et al., 2023).

In addition, we add to the literature on online crowdlending behaviors by examining such behaviors in extremely unstable situations. In such cases, borrowers are regarded as victims who need more urgent financial assistance than during normal times to continue their businesses. Meanwhile, they are associated with greater risks and uncertainties (i.e., inability to repay) due to their disadvantaged and uncertain situations. Such a combination of the identified victim effect and the risk effect makes the role of crisis unique in fundraising operations. Examining the effects of crises on crowdlending allows researchers to go beyond solely prosocial motives for crowdlending behaviors and include risk considerations in lenders’ decision-making (Gupta et al., 2022b; Wang et al., 2020). Our results show that crowdlenders tend to exhibit overall positive responses to loan requests during a crisis insofar as the risk can be shared and mitigated by the collective nature of crowdlending. However, risk considerations during a crisis further induce lenders’ focus on the economic objectives and reduce individualistic lenders’ responses, characterizing crowdlending for fundraising operations with heterogeneous lender responses. Our investigation of the impact of a crisis on crowdlending behaviors also extends the literature on crowdlending in particular, and on crowdfunding in general, by identifying the influence of off-platform shocks rather than within-platform factors on contributor responses to loan requests and fundraising campaigns (Mejia et al., 2019).

Besides examining how small businesses effectively raise funds in online crowdlending and how crises affect online crowdlending behaviors, we identified the variations in lender responses during a crisis from both fundraising objectives and lenders’ national culture (Jonas, 2012). Although crowdlending is a viable option for businesses seeking financial support during crises and lenders tend to respond positively to loan requests from crisis-affected areas, different loans, and lenders may induce and exhibit heterogeneous financing outcomes during a crisis, which creates operational challenges in effectively using crowdlending for business survival. Our study delves into such operational challenges and variations in lender responses by examining the moderating role of fundraising objectives and lenders’ national culture. Notably, loans with a greater emphasis on economic objectives rather than on social objectives are more likely to receive positive responses from lenders during a crisis, while the nature of crowdlending and the risk considerations during a crisis induce more positive responses from lenders in collectivistic compared to individualistic cultures. Such differential outcomes from lender responses are important to understand the patterns of information and financial flows in disaster management. In this regard, we take one step further from prior works at the intersection between disaster management and online platforms (Cao et al., 2022) by identifying heterogeneous lender responses and the mixed preferences shaped by fundraising objectives and national culture during a crisis.

More importantly, our findings also offer insights into humanitarian operations in terms of local businesses supporting development activities. In humanitarian operations, the aim is not only to deal with the relief of immediate pain and hardship but also development operations for long-term recovery (Besiou et al., 2021; Ibrahim and El Ebrashi, 2017); however, research in humanitarian operations has been extensively focusing on disaster relief or minimizing the loss of life, paying less attention to the gap in long-term recovery (Sodhi and Tang, 2014). In the recovery process, small businesses and micro-enterprises play important roles in rehabilitation and reducing the dependency on humanitarian aid; however, they may have limited access to funding for survival. Our research shows that crowdlending can be an appropriate mechanism to support local businesses during crises, thus further increasing the potential for long-term development and recovery.