Abstract

This study investigates whether retargeting, an operational approach broadly adopted in traditional retail but underexplored in financial services, is effective in recovering valuable consumers. Whereas informative appeal retargeting operations have been found useful and thus prevalently employed in traditional retail, we propose that emotional appeals retargeting operations should be more effective in successful financial consumer persuasion drawing on the uniqueness of financial services. Particularly, we explore the value of two types of emotional appeals retargeting strategies tailored for financial services: empathetic support and privacy commitment retargeting. Our field experiment involving a microloan platform reveals the effectiveness of emotional appeals retargeting in the financial service market. Specifically, empathetic support retargeting successfully recovers 11.93% of consumers, whereas privacy commitment retargeting recovers 17.27% of consumers. These effects translate to 5.19 and 10.53 percentage-point increases in the rate of return, respectively, over the no-message operation. This study further evaluates the quality of consumers retained by these retargeting strategies and finds that consumers called back by the empathetic support and privacy commitment retargeting present high credibility, with loan approval rates 11.4 and 13.69 percentage points higher than those of nonabandoning consumers, respectively. Accordingly, a more specific retargeting strategy is explored. Our study provides a systematical implication for nascent retargeting operation practices in the financial service market by elucidating the causes and effects of consumer returns.

Keywords

Introduction

The rapid growth of financial technology (FinTech hereafter) has dramatically expanded financial services to millions of people (Guild, 2017). Various types of novel financial services are emerging, including microloans, consumer debt, virtual credit cards, and Internet-based insurance (Teja, 2017). However, despite the growing accessibility to financial services, financial websites exhibit the highest average abandonment among all industries. This abandonment rate, which signifies the proportion of consumers who exit in the middle of the application process before completing a transaction (Kriese et al., 2019), can be remarkably high, reaching as much as 83.6%. 1

Retargeting is a practice where companies deliver personalized reminders or recommendations to consumers based on their prior browsing history, encouraging them to revisit their website (Lambrecht and Tucker, 2013). Retail and e-commerce industries have effectively utilized diverse retargeting strategies to reengage consumers and encourage them to complete transactions (e.g., Bleier and Eisenbeiss, 2015; Luo et al., 2019). For instance, retargeting methods may involve sending consumers information about products they previously viewed (Lambrecht and Tucker, 2013) or promoting purchases through tactics such as scarcity or price incentives (Li et al., 2021). These retargeting efforts have demonstrated their ability to successfully persuade consumers back into the product purchase process. Lee et al. (2018) characterized this kind of retargeting as an informative (content) appeal that provides direct and detailed descriptions of products, pricing, promotions, and product availability, all aimed at stimulating consumer purchases.

Inspired by the findings regarding retargeting, financial practitioners should have greatly taken advantage of retargeting. However, it is notably less prevalent in the financial sector, accounting for just 9% of retargeting efforts, in stark contrast to the retail (27%) and media (17%) industries, as reported in FinanceOnline. 2 The limited number of retargeting strategies in use predominantly rely on an informative appeal approach (e.g., Alt et al., 2019; Lee et al., 2011). Regrettably, the effectiveness of current retargeting practices in the financial service market leaves much to be desired. A case in point is the reported acceptance rate of retargeting for financial services, which stands at a mere 6%, in stark contrast to the considerably higher rates observed for apparel and electronics products, reaching as high as 35%, as per Marketing Charts. 3

Several reasons concerning the characteristics of the financial service market account for the suboptimal utilization of informative appeals in retargeting therein. First, financial consumers are somewhat distinct from consumers in conventional retail or other similar contexts: they generally face financial difficulty and have the desire to adopt financial services but may be hesitant to take complete actions (i.e., possess indecisive motivation) (Ke, 2021; Shell and Buell, 2019). This is primarily because consumers may encounter difficulties in fully comprehending the content delivered through informative appeals due to limited financial or technical knowledge (Gaurav et al., 2011). This increases consumers’ perceived psychological distance from the financial service providers (FSPs) 4 (Liberman et al., 2007), rendering them more hesitant to accept the recommended services by FSPs (Ke, 2021). Consequently, consumers tend to be less receptive to the seemingly “cold” and purely informational messages conveyed by informative appeals (Czarnecka and Mogaji, 2020).

Second, an informative appeal runs the risk of triggering financial consumers’ counterproductive responses akin to “message scams.” This is because financial consumers tend to be particularly sensitive to retargeting messages, largely due to privacy concerns (Goldfarb and Tucker, 2011). This issue instills a profound sense of psychological unsafety and uncertainty among consumers regarding their limited control over personal information (Siemens et al., 2013). However, the informative appeals message provides them with detailed explanations and justifications, which may inadvertently remind them that FSPs are primarily focused on their self-interest and maximizing utility. Consequently, such informative appeals may intensify consumer suspicions regarding the hidden sales motives of FSPs (Rietveld et al., 2020). Indeed, some most recent studies have suggested that privacy mitigation with informative appeals may raise users’ privacy concerns as they counteractively make privacy issues more explicit (i.e., the “bulletproof glass effect”) (Brough et al., 2022; Liu et al., 2022).

Even though the financial industry has not experienced significant benefits from informative appeals retargeting, it does not imply that we should cease exploring retargeting practices. We contend that, by contrast, emotional appeals should be effective in bolstering conversion rates in the financial service market. Emotional appeals, or emotional persuasions, target the emotional or experiential facet of products or services (Andreu et al., 2015). Such an appeal seeks to affect consumers’ attitudes by conveying emotional responses (e.g., care, enjoyment, or sympathy). It could provide financial consumers reassurance and comfort, and help alleviate psychological distance while fostering trust and rapport (Czarnecka and Mogaji, 2020; He et al., 2020). Besides, a well-crafted emotional appeal message design can diminish the chances of evoking suspicions of “message scams” as emphasizing care and a commitment to privacy is inherently other-centeredness and altruistic.

Therefore, this study aims to empirically investigate the effectiveness of emotional appeals retargeting in winning consumers back within the financial service market. As previously mentioned and reinforced by the extensive survey conducted by Signicat, 5 two prominent factors contribute significantly to the high abandonment rate observed within the financial service markets: (1) consumers’ indecisive motivation in adopting financial services, stemming from their psychological distance to FSPs due to a lack of financial literacy (Liberman et al., 2007) and/or a reluctance to seek assistance from third-party financial institutions (Turvey and Kong, 2010), and (2) their substantial concerns regarding potential operational issues within FSPs, such as system vulnerabilities, misuse of personal information, and privacy breaches (Tang, 2019). Accordingly, we have devised two distinct emotional appeals to tackle these issues, aiming to reduce the perceived psychological distance and enhance the sense of psychological security within financialservices.

Specifically, as per the elaboration likelihood model (ELM) (Petty and Cacioppo, 1986), when consumers exhibit indecisive motivation, they are more influenced by peripheral cues such as those delivering empathy, as opposed to the so-called central cues. As such, an empathetic support retargeting message can evoke positive feelings of support, trust, and care (Taylor, 2011), effectively reducing psychological distance (Mei et al., 2018) and encouraging continued transactions. Conversely, when consumers have highly confirmed motivation but significant problem concerns (e.g., privacy concerns in financial services), the ELM suggests they prioritize cues concerning core service aspects that alleviate psychological uncertainty and ensure safety (Xu, 2010). Since a timely privacy commitment retargeting message demonstrates a commitment to addressing consumer-oriented privacy concerns (Gerlach et al., 2019), we propose that it can be particularly effective in alleviating privacy concerns and persuading consumers to resume their services.

Moreover, aside from financial consumer recovery, we believe it valuable to delve deeper into understanding the worth of emotional appeals retargeting, especially considering the considerable costs associated with managing returning consumers. In contrast to retail markets, financial consumers can pose a pronounced higher cost to FSPs (e.g., labor cost in the approval process and debt management). 6 Therefore, who to retarget and how to retarget them are crucial questions in the financial market setting, particularly for FSPs because they do not have complete information on consumer quality (e.g., credibility or credit risk) before an actual transaction. In other words, winning back consumers that pose a high credit risk may not be beneficial. Therefore, this study further evaluates the quality of consumers retained by these retargeting operation strategies. We deem that the consumers recovered by two emotional appeal retargeting messages would be “good” ones (i.e., no worse than the remained consumers) because emotionally impressionable people usually avoid harming others and thus have a lower possibility of financial default (Acevedo et al., 2014).

We partner with a leading Chinese microloan platform to conduct a randomized field experiment. We design two types of emotional appeals retargeting strategies: an empathetic support message and a privacy commitment message. Additionally, we employ a holdout group with no message operation and a control group with a neutral message. We mainly focus on measuring the number of recovered consumers and the credibility of these recovered consumers. Our findings confirm that empathetic support and privacy commitment messages markedly increase the rate at which consumers return to the loan application process. Specifically, compared to the 6.74% return in the no message condition and 7.05% in the neutral message condition, we find that 11.93% of consumers return in the empathetic support message condition, and that 17.27% of consumers return in the privacy commitment message condition. These effects translate to 5.19 and 10.53 percentage-point increases in the rate of return, respectively, over the no message condition. These findings can be attributed to different underlying abandonment causes across consumers. Empathetic support retargeting attracts consumers who initially have an indecisive adoption intention toward a financial service, whereas privacy commitment retargeting attracts consumers who already are willing to accept a financial service but have privacy concerns. Moreover, the results of a loan approval analysis suggest that consumers who return due to the empathetic support and privacy commitment retargeting present high credibility. The approval rate of nonabandoning consumers on the platform is 44.29%. We use this rate as the benchmark and find a significant increase in approval rates under empathetic support and privacy commitment messages conditions, with improvements of 11.4 and 13.69 percentage points, respectively.

Our study sheds light on the interface of operations, information systems, and finance, and combines multiple streams of research, namely retargeting operation, microfinance, prosocial theory, and privacy. Our study lays a firm theoretical foundation for nascent retargeting operation practices in the financial service market by systematically elucidating the causes and effects of consumer returns. First, our study has pioneered the validation of the comprehensive value (i.e., the possibility of recovering consumers and the quality of recovered consumers) of employing two distinct emotionally supportive appeals retargeting in the financial service market. Given the underperformance of conventional retargeting methods using informative appeals within the financial service market, we have turned our attention to the potential of emotional appeals retargeting. This shift is grounded in the distinct characteristics of financial services and the specific abandonment reasons observed among financial consumers. Consequently, our study results offer empirical support for the advantages of employing emotional appeals in retargeting efforts to reacquire high-value financial consumers. Second, we also enrich the financial service operation literature by focusing on an underexplored step in the service chain, namely consumer recovery. Many studies have investigated operational issues encountered either at pre-logging stages, such as the financial service design (Kumar et al., 2018) and consumer attraction (Chae et al., 2019); or at post-contract stages, such as credibility evaluation (Lin et al., 2013) and debt recovery (Chehrazi et al., 2019). Our research fills the research gap by proposing effective operation practices in the middle of the application process, i.e., after consumer arrival but before contract approval to enhance business outcomes. Finally, we add knowledge to the privacy literature by empirically revealing the dominant role of privacy concerns related to consumer abandonment in the financial services setting. Moreover, we illustrate that a consumer-centered emotional privacy commitment retargeting approach proves to be highly effective in recovering valuable consumers who abandoned their pursuit of services due to privacy concerns. Our study furnishes empirical evidence for the mechanisms at play, which alleviate consumers’ psychological safety concerns and enhance their trust in FSPs. Our research findings also provide clear guidance on how to call back consumers for FSPs and help them develop effective retargeting strategies for consumers who abandoned the service for distinct reasons.

Literature Review

Our work is mostly related to the following two streams of literature: retargeting operation strategies and current consumer management practices in financial services.

Retargeting Operation

Retargeting is a unique form of advertising operation that targets consumers who visited retailers’ websites but did not make transactions (Sahni et al., 2019). This operation strategy allows retailers to deliver relevant information to targeted consumers, thus increasing visits and conversions (Li et al., 2021). Consumers’ digital footprints created before they churn may indicate the levels of engagement and purchase intention and thus can be used to optimize retargeting strategies (Lambrecht and Tucker, 2013). As summarized in Table A1 in the Appendix, studies have investigated different instrumental retargeting operation strategies concerning the optimal timing, intensity, placement, and message content. Among these retargeting strategies, content designs, such as informative appeals vs. emotional appeals (Majumdar and Bose, 2018), which aim to improve the effectiveness of persuasion, are most widely discussed (Andreu et al., 2015). Table A2 in the Appendix summarizes related studies of informative and emotional appeals.

In specific, retargeting with informative appeals is designed to persuade users by presenting factual and evidence-based product/service information and to address potential problems (Rietveld et al., 2020). Lee et al. (2018) categorized informative content as any product-oriented facts or arguments, such as details about products, prices, and promotions. Informative appeals are prevalently adopted in traditional retail. Most studies suggested the positive effects of informative appeals as they provide relevant information to address consumers’ needs (Allison et al., 2017). Particularly, informative appeals are found effective when consumers are highly involved (Andreu et al., 2015) and capable of processing relevant product information (Xiang et al., 2019). Nonetheless, a few studies suggested insignificant or even negative effects of informative appeals. For example, Rietveld et al. (2020) found that most visual informative appeals posted on Instagram could not drive customer brand engagement, as self-centered informative appeals may signal an overt persuasion attempt and raise suspicion of ulterior sales motives, which increased incongruence with consumer motivations to follow brands.

In contrast, emotional appeals, or emotional persuasions, target the emotional or experiential facet of products or services (Andreu et al., 2015). Such appeals seek to change consumers’ attitudes by conveying emotional responses (e.g., care, enjoyment, or sympathy) (e.g., Sudhir et al., 2016). Studies have shown that emotional appeals work for persuading users with indecisive motivation of involvement (Xiang et al., 2019) as the appeals tend to be more positive and aroused (Rietveld et al., 2020). An increase in emotional arousal helps reduce psychological distance as people always feel the objects socially closer when they are more emotionally aroused (Van Boven et al., 2010).

Regarding our proposed two types of emotional appeals, namely, empathetic appeals and privacy commitment appeals, the utilization and scholarly exploration of both emotional appeals are still in their infancy. Specifically, empathetic appeals have been developed and studied narrowly within specific contexts such as soliciting donations (Cavanaugh et al., 2015; Sudhir et al., 2016; Xiang et al., 2019). Most of these appeals aim to evoke empathy from users. However, this approach may not be directly applicable in the financial service market, where consumers are the ones in need of support.

Besides, existing research has centered on exploring the value of privacy commitment through informative appeals, primarily within the realms of shopping and mobile applications. These informative appeals included highlighting legal limits on data practice (Wu et al., 2012), instructing protective measures (Adjerid et al., 2018), and elucidating ways of improving transparency (Gu et al., 2017; Martin et al., 2017). Overall, these studies indicated that privacy commitment has the potential to enhance individuals’ perceptions of privacy assurance. Nonetheless, as discussed before, privacy mitigation through informative appeals could inadvertently lead to consumers’ perceived “message scams.” They even heighten consumers’ privacy concerns, as these appeals may inadvertently draw attention to privacy issues, making them more explicit in the consumers’ minds (Brough et al., 2022; Liu et al., 2022).

Given the above-mentioned limitations of empathetic appeals and privacy commitment appeals used in previous research, this study aims to extend current literature by exploring the effectiveness of (1) a unique empathetic support appeal that communicates FSPs’ willingness to offer timely assistance, and (2) a user-centered commitment appeal to safeguarding the privacy of their consumers.

Consumer Management in Financial Services

For a long time, studies on financial services such as microfinance services have largely focused on sellers’ operational efficiency to support the rapidly expanding financial service industry. However, in contrast to the more mature retail industry, few finance, marketing, operation, and information systems studies have devoted sufficient attention to the consumer perspective. Researchers have primarily focused on increasing FSPs’ revenues by reducing financial risks. In particular, most of the studies in financial services have effectively assessed consumers’ credibility (Lin et al., 2013) and repayment management strategies (Chehrazi et al., 2019; Lu et al., 2021).

However, as the financial market becomes more crowded, FSPs now must become much more customer-centered (Gomber et al., 2018). To move ahead of competitors, FSPs and related researchers have started to adopt marketing and operation tools to compete for consumers in the market. For example, a few studies have designed effective strategies to offer attractive financial services to consumers, such as through collaboratively working with consumers (Amegbe and Osakwe, 2018) and offering personalized products (Yun and Hanson, 2020). Several studies have investigated the efficacy of advertising strategies in the financial service market, with most of them indicating a positive influence of advertising on consumer attraction (Chae et al., 2019; Hoban and Bucklin, 2015). Nonetheless, most previous studies have focused on methods to attract or retain existing consumers, often overlooking the significant issue of high abandonment rates and the potential losses incurred in the financial service market. In the present landscape, consumers tend to make financial service choices more thoughtfully than before, given the expanded range of available financial services (Gomber et al., 2018). This shift is accompanied by a notably high average abandonment rate among financial consumers (Charlton, 2019), highlighting the need for more research to delve into retargeting strategies in the middle of the financial service. However, although it becomes increasingly crucial for FSPs to identify effective strategies to call back churned consumers, retargeting in financial services has been rarely discussed in academia. Consequently, the information provided by existing studies is inadequate to support the development of principled retargeting operation approaches. Thus, as discussed before, drawing on the uniqueness of the financial service market, we examine retargeting content designs with emotional appeals to evaluate the effectiveness and quality of consumer recovery.

Hypothesis Development

Effectiveness of Retargeting in Financial Services

Our retargeting design and main hypothesis development are based on the theoretical perspective of the ELM. According to the ELM, individuals form their attitudes either through the central or peripheral route (Petty and Cacioppo, 1986). When individuals are highly motivated and cognitively capable, they will engage in issue-relevant thinking and tend to make decisions based on core information that directly relates to products or services, such as price and privacy (Allison et al., 2017). By contrast, when individuals lack explicit motivation or cognitive capability, they will attempt to shortcut the cognitive process by using simple heuristic rules. They are more likely to be affected by peripheral cues such as brand images and the direct emotion aroused by retailers (Xiang et al., 2019).

Although some consumers require financial services, they inherently have indecisive motivation to adopt such products from financial institutions, particularly if the services are new or unfamiliar (Ke, 2021). That is, they possess a desire to pursue financial services but with some reservations or hesitations about taking action (Dost et al., 2014). Compared with the retail market in which transactions are easy to handle, financial services require a higher knowledge base (Gaurav et al., 2011). This naturally builds up consumers’ psychological distance from FSPs (Darke et al., 2016). Specifically, consumers would experience a sense of emotional separation when they find it challenging to understand the complex financial terminology and rules used by FSPs; this separation or distance is not necessarily physical but rather a feeling of being disconnected or excluded from the financial process (i.e., psychological distance) due to the perceived complexity and difficulty in comprehending the information (Liberman et al., 2007). In addition, compared with other sources such as consumers’ relationships and friends, FPSs are less close to them (Turvey and Kong, 2010). Less close relationships increase the risk of dissolution, some consumers may thus prefer seeking financial help from more close relationships instead of FPSs (Turvey and Kong, 2010). Insufficient financial knowledge and social closeness both lead to far psychological distance (Liberman et al., 2007). Consequently, consumers are more sensitive toward and hesitant to adopt products from financial services (Ke, 2021). In such a case, from the lens of the ELM, we propose that delivering empathetic support information should reduce psychological distance and call back some abandoning consumers who have indecisive motivation.

Specifically, as indicated by the ELM, individuals with indecisive motivation tend to form their attitudes heuristically. Their judgments are majorly based on how they feel about something rather than the consideration of detailed information (Xiang et al., 2019). Empathetic support messages, which deliver care and intention to help, are common communication tools used for emotional appeals and are useful for reducing psychological distance (Mei et al., 2018). These messages can induce receivers’ positive emotions because they convey reassurance and arouse individuals’ feelings of being helped, trusted, and cared for (Taylor, 2011). Given that consumers experiencing financial distress have a strong need for emotional comfort (Ke, 2021), we believe that sending empathetic support messages at the proper time could be effective in attracting these consumers with indecisive motivation. Consequently, these consumers build up more positive attitudes (e.g., trust) toward FSPs and revisit financial services (Xiang et al., 2019). Therefore, we hypothesize:

H1: An empathetic support retargeting message is more effective in calling back consumers compared with the neutral retargeting message and the natural returns without a retargeting message.

According to the ELM, consumers who have strong and confirmed motivation but ultimately abandon applications due to the core issues of financial services would pay more attention to the persuading message related to the core issues (Petty and Cacioppo, 1986). As discussed before, privacy is a main concern in the context of financial services. FSPs usually require consumers to provide more confidential information for credit risk evaluation (Tang, 2019), and thus privacy-sensitive consumers may sense the loss of control over information and an invasion of privacy. Goldfarb and Tucker (2011) suggest that the most significant challenge in financial services marketing and operations is usually around anxiety related to privacy perceptions. Holding privacy concerns would cause consumers’ psychological unsafety, that is, a lack of trust in FSPs’ ability to properly leverage and effectively safeguard consumers’ personal information (Siemens et al., 2013). As an emotional protection state in response to negative consequences, psychological unsafety leads to consumers’ distrust toward FSPs and less risk-taking behaviors such as terminating the application process, to avoid the potential risks such as message scams or illegal debt collection from FSPs (Lu et al., 2021).

According to the ELM, messages aimed at mitigating privacy concerns would capture the attention of consumers who are highly motivated but abandon their applications due to privacy concerns. Research has suggested that the privacy statement message which conveys other-focused emotions, such as care and security commitment, will be more effective in reducing privacy concerns than informative appeals which focus on detailed explanations about privacy protection measures (Gerlach et al., 2019). Because an other-centered tone is less likely to elicit suspicion from consumers regarding ulterior sales motives than an informative self-centered tone (Rietveld et al., 2020). Moreover, the emotional commitment that personal information will be protected and kept confidential by institutions would provide consumers with higher confidence that they can exercise proxy control over their personal information (Xu, 2010), and in turn, enhance psychological safety and reduce privacy concerns. This aligns with the finding of Bandura (1982) that when people couldn’t exercise direct personal control over their information, they would seek “security in proxy control” (Bandura, 1982, p. 142); namely, they would ask for other powerful forces or commitments to improve controls over their information. Therefore, by sending a privacy commitment retargeting message through emotional appeals, FSPs deliver their purpose of alleviating consumers’ psychological uncertainties and unsafety, thereby weakening consumers’ concerns about potential private information abuse/breach (Gerlach et al., 2019) and calling them back. Accordingly, we propose the following hypothesis:

H2: A privacy commitment retargeting message is more effective in calling back consumers compared with the neutral retargeting message and the natural returns without a retargeting message.

Credibility of Consumers Returned Through Retargeting

From a practical perspective, we use the quality of nonabandoning consumers as the benchmark to explicitly show the value of our proposed retargeting strategies by examining whether the recovered consumers perform no worse than those who did not abandon applications.

The Credibility of Consumers Returned Through Empathetic Support Retargeting

Given that fulfilling financial obligations and maintaining high credibility can be considered as a form of prosocial compliance behavior (Du et al., 2020), we derive the credibility of returning consumers by retargeting based on the prosocial behavior perspective. The prosocial literature finds that consumers who are more emotionally impressionable and have a strong sense of empathy are more easily affected by affections in decision-making (Acevedo et al., 2014). Thus, consumers called back by an empathetic support retargeting message are likely to be empathetic and capable of placing themselves in others’ positions to understand others’ situations (Acevedo et al., 2014). Literature also suggests that people with intense empathy make efforts to live up to others’ expectations, avoid harming others, and exhibit prosocial compliance behavior (Stocks et al., 2009). For example, by performing various laboratory experiments, Calvet Christian and Alm (2014) showed that the presence of empathy is positively related to tax compliance. We believe that because an empathetic support message conveys institutions’ trust in receivers, returning consumers who tend to live up to trustworthiness expectations are less likely to default (Du et al., 2020). Therefore, the credibility of consumers whose decisions are altered by empathetic support retargeting would not be low. Accordingly, we hypothesize:

H3: The credibility of consumers called back by the empathetic support retargeting message would be equal to or even better than that of consumers who did not abandon their applications.

The Credibility of Consumers Returned Through Privacy Commitment Retargeting

Compared with empathetic support retargeting, privacy commitment retargeting does not aim to arouse consumers’ empathy for institutions. Instead, it functions primarily by providing a feeling of psychological safety and reducing consumers’ privacy concerns. We conjecture that the credibility of consumers called back by a privacy commitment retargeting should not be worse than that of consumers who did not abandon, for the following reasons. First, from the perspective of prosocial motivation, the need for privacy is a self-actualization need, 7 and thus returning consumers who have a high sense of privacy are merely to maintain a favorable financial status. The increased material and financial resources and relative rank afford people of higher socioeconomic status, greater personal control, autonomy, and reduced vulnerability to social and environmental threats (Kraus et al., 2009). Second, Zhang et al. (2018) suggest that these people usually receive a high level of education wherein they are taught to maintain high moral standards. These studies imply that consumers who pay much attention to privacy are overall less likely to default on financial services. Moreover, the privacy commitment message indicates to consumers that the financial institution in question excels at risk management, including credit risk assessment (Wang et al., 2021). In this scenario, high-risk consumers are less likely to return. Hence, we propose the following hypothesis:

H4: The credibility of consumers called back by the privacy commitment retargeting message would be equal to or even better than that of consumers who did not abandon their applications.

Experimental Design

We conduct a field experiment to test the hypotheses regarding the effect of the retargeting operation.

Experimental Background

The experiment is conducted on a leading microloan platform in China founded in 2011. At the time of the study, the partnered platform was serving over 250,000 consumers (borrowers) with collateral-free loans, with an average borrowing amount of approximately CNY3000 (US$430). Loans on the platform have a term of 5–7 months and are repaid in monthly installments starting a month after their issuance. The annual interest rate charged by the platform is 17% or 18%, which is lower than that of most competitors in the market. 8

The focal platform adopts a typical and standard loan application process. Specifically, to apply for a loan, a consumer must initially provide their basic personal information such as name, phone number, and gender, and choose the loan amount (CNY1000–5000; CNY3000 by default) and loan term (5–7 months) as well as check the specified annual interest rate (17% or 18%). In addition, they are required to clearly state the purpose of the loan. In the next step, consumers are asked to sign a consent form to offer some additional personal information (e.g., a copy of their resident identity card, educational level, income level, and the contact information of 2–3 family members) that is used for credit risk evaluation. Then, applicants can submit their applications. The platform assesses the consumer's credibility through industry-standard credit scoring services and makes approval decisions. Consumers cannot skip any step but can exit from the platform at any step, and the system will record the information they have provided before they churn. As per the platform's regular practice, no message is sent to consumers who abandon the platform. Consumers are allowed to resume (not allowed to initiate a new) application at any time. Before our collaboration, the platform has never adopted retargeting strategies.

Treatment Design

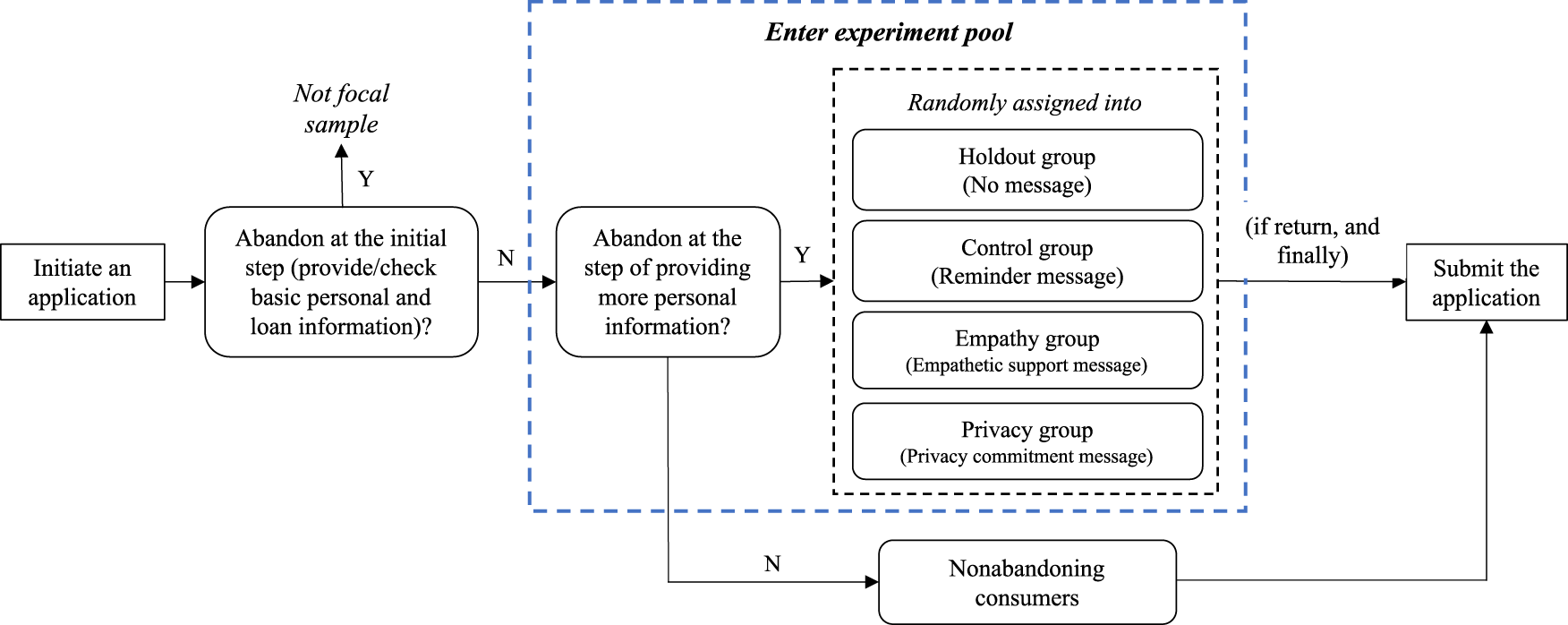

In our experiment design, we focus on all consumers who newly initiated a loan application on the platform in October and November 2017. Figure 1 presents the schedule of retargeting messages during the experiment. If consumers do not complete the initial step that involves providing basic personal information and checking loan information, we do not include them in the experiment because they would show very low interest or motivation to adopt related services. Yet, limited information from these consumers can be leveraged by the platform to design a retargeting strategy.

Experimental design.

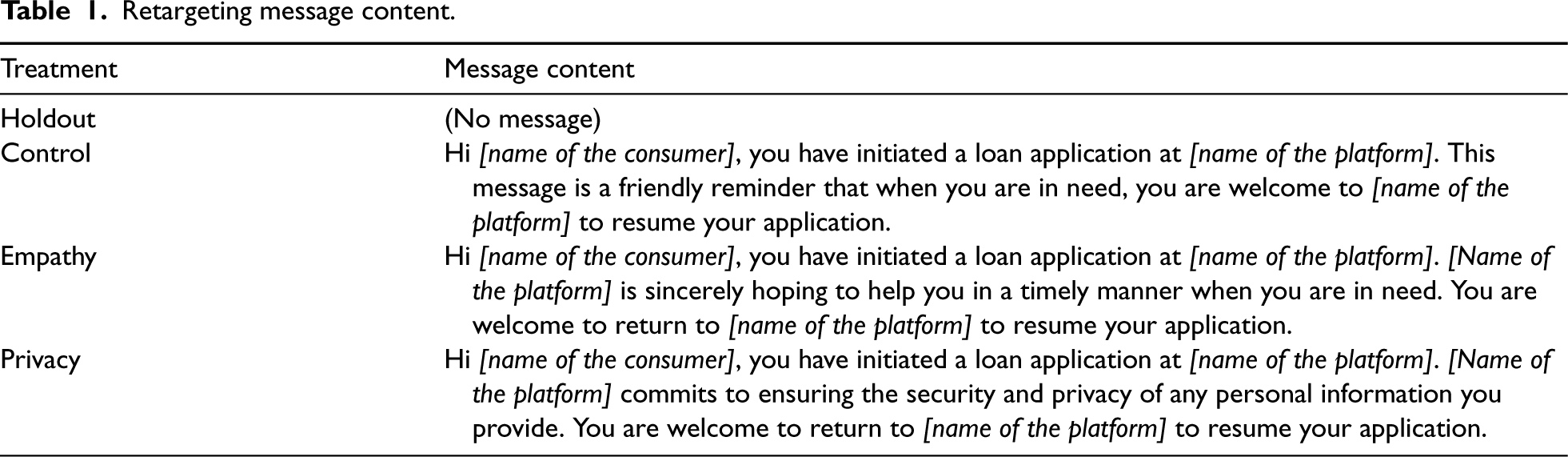

When consumers complete the initial step and proceed to the second step of providing private information such as a copy of the residential identity card, they enter the experiment sample pool. Consumers may abandon their pursuit at this step when they are not willing to provide private information (Lu et al., 2021). For these abandoning consumers, we randomly assign them to one of the four groups. In the holdout group, no retargeting message is sent. This group helps us identify the natural return rate of consumers who abandon the platform without any interference. In the control group, consumers who abandon the platform receive a retargeting message that simply reminds them of having initiated a loan application on the focal platform. The message is neutral and does not provide information regarding service attributes or operation-related issues. In the empathy group, consumers who abandon the platform receive a message delivering direct emotional care. In the privacy group, consumers receive a retargeting message indicating that the platform is committed to protecting the security and privacy of any personal information submitted to the platform. Borrowers who return to the focal platform after receiving a retargeting message are not granted any special privileges or benefits.

Finally, to control for the effect of the time at which the message is sent, we set the SMS system to send retargeting messages automatically at 3 p.m., 9 p.m., or 10 a.m. the next day for consumers who abandon their applications in the morning (before noon), afternoon (before 6 p.m.), or evening (evening to 6 a.m. the next day), respectively. These chosen time points are the peak hours of a loan application at different periods on the focal platform. In addition, the sending time ensures a proper time buffer (i.e., not too early or too late) after consumers abandon the platform (Sahni et al., 2019). All returning consumers during this buffer time are considered nonabandoning consumers. Besides, since some consumers may still not submit their applications after they return due to the first retargeting message (i.e., leave again), we do not retarget these consumers repeatedly to ensure that each abandoning consumer receives a retargeting message only once uniformly. This very small portion of consumers is not included in our sample. Table 1 lists the retargeting message content.

Retargeting message content.

In our experiment, no message is sent to consumers who do not abandon and directly submit their applications. All staff members do not know whether a consumer has abandoned (but returned) during their application; this guarantees that the staff's loan approval decision is based on consistent criteria and is not affected by consumers’ prior abandonment behavior. We collect the approval information for all submitted loans.

Sample

In total, 58,884 loan applications were initiated from October to November 2017 on the platform. To prevent interference with the previous experience of repeated consumers on the platform, we select only new applicants and remove 539 repeated applicants. In addition, 33,501 consumers who abandoned applications during the initial step are not included in the experiment. The remaining 24,844 consumers are our focal consumers; among these consumers, 19,144 are nonabandoning consumers. The other 5,700 consumers abandoned applications at the step of offering private information and are included in the experimental pool. The initial abandonment rate in our focal group is approximately 22.9% (5,700/24,844) (the abandonment rate is 66.6% if we include consumers who abandoned applications at the initial step). Since the focal microloan market is highly competitive, consumers tend to compare different FSPs (Gomber et al., 2018); the fact on our focal platform supports the high abandonment rate in the financial service market.

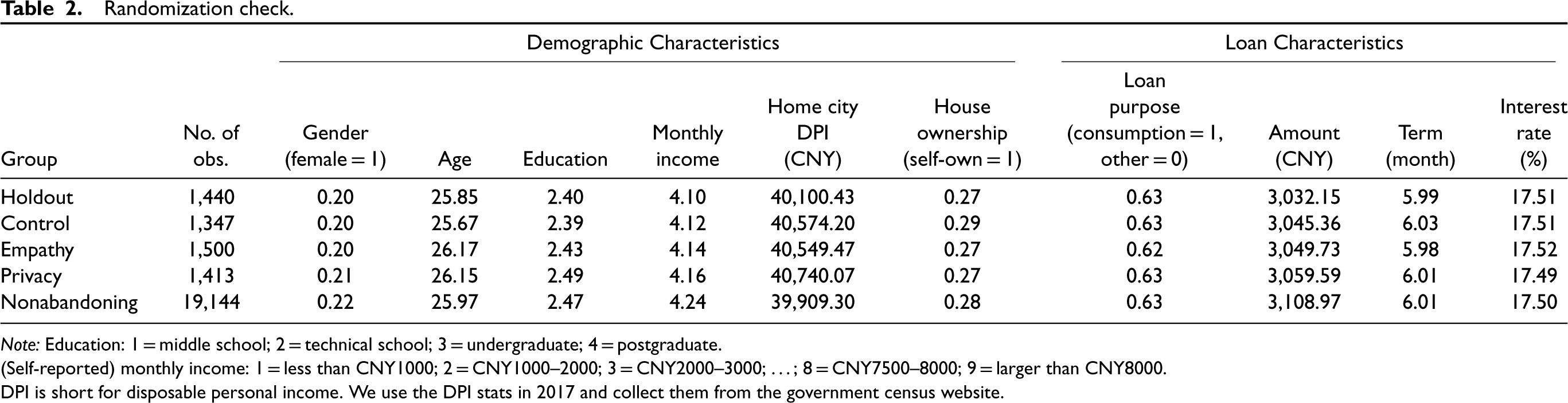

Randomization Check

Table 2 presents the consumer and loan characteristics of treatment groups as well as those of nonabandoning consumers. Compared with nonabandoning consumers, experimental consumers who abandon applications mainly due to privacy concerns have a favorable socioeconomic status, similar to that of nonabandoning consumers. 9 We observe no significant differences in sample sizes and characteristics between the groups, suggesting successful randomization.

Randomization check.

Randomization check.

Note: Education: 1 = middle school; 2 = technical school; 3 = undergraduate; 4 = postgraduate.

(Self-reported) monthly income: 1 = less than CNY1000; 2 = CNY1000–2000; 3 = CNY2000–3000; …; 8 = CNY7500–8000; 9 = larger than CNY8000.

DPI is short for disposable personal income. We use the DPI stats in 2017 and collect them from the government census website.

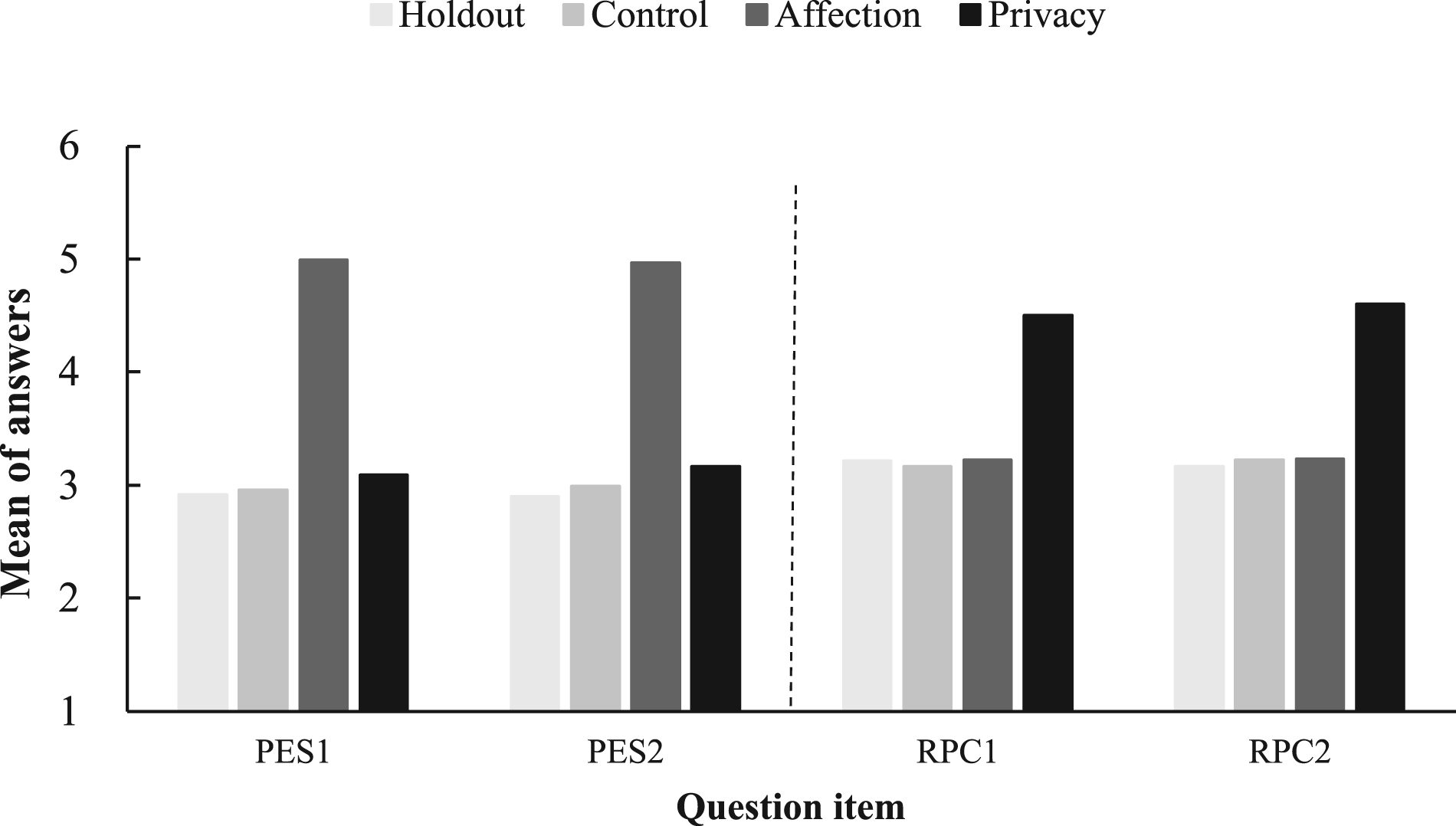

We argue that our proposed retargeting messages succeed in recovering consumers by offering empathetic support and mitigating their privacy concerns. We conduct a survey to examine how consumers perceive the designed retargeting messages, especially those who return within 24 hours after the messages are sent. 10 This simple survey contains six questions on the levels of perceived empathetic support (PES) and reduced privacy concern (RPC). Details are provided in Table C1 (Appendix), and the score of all question items ranges from 1 to 7. The survey page pops up when a consumer logs in again to the website, and the consumer is required to answer all questions. As shown in Figure 2, we find that the levels of consumers’ PES and RPC are low (scores of ∼3.0). However, our designed empathetic support and privacy commitment retargeting messages considerably improve consumers’ corresponding perceptions, resulting in a score of approximately 5.0. That is, consumers who receive the empathetic support message have a higher level of PES. We observe similar findings for consumers who receive the privacy commitment retargeting message. These results confirm the effectiveness of our proposed emotional appeals retargeting messages and suggest successful manipulation in our experiment.

Mean of answers across experimental groups. Note: In total, 433 consumers have provided answers to the survey. PES: perceived empathetic support; RPC: reduced privacy concern. Answer scores range from 1 to 7. A larger score indicates a higher level of perception.

To test the proposed hypotheses, we examine the effectiveness of different emotional appeals retargeting messages in winning back consumers and the credibility of returning consumers.

Effects of retargeting messages on return rate.

Descriptive Analyses

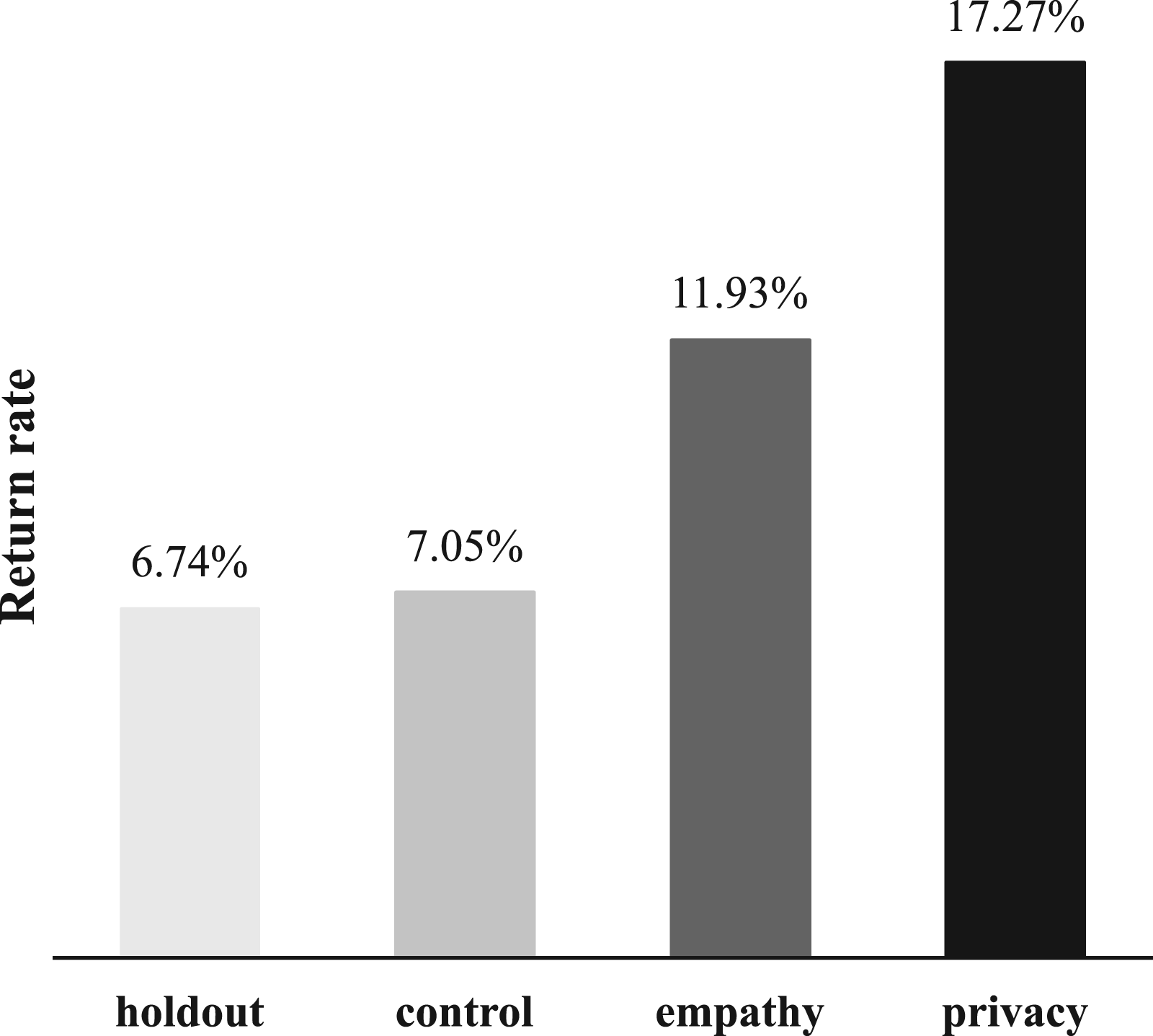

We use the return rate (or recall rate), which is defined as the proportion of returning consumers among all abandoning consumers, to measure the effect of retargeting messages. Note that, “return” herein refers to the case that a consumer has returned and then completed their loan application on the focal platform. Figure 3 presents the return rate of each experimental group. The return rates of the holdout group and control group are 6.74% and 7.05%, respectively. These two rates are not significantly different (p = 0.742 from a t test). This finding suggests that a simple reminder is ineffective in winning most consumers back, and a more delicate retargeting message design is warranted.

The return rate of the empathetic support retargeting message is 11.93%. That is, the empathetic support retargeting successfully increases the return rate by 5.19 percentage points (= 11.93% – 6.74%, p < 0.001) compared with the holdout group. Moreover, the return rate of privacy commitment message is as high as 17.27%, with an increase of 10.53 percentage points (= 17.27% – 6.74%, p < 0.001) compared with the holdout group, indicating the strong effect of such an emotional appeal retargeting strategy in recovering consumers.

Regression Analyses

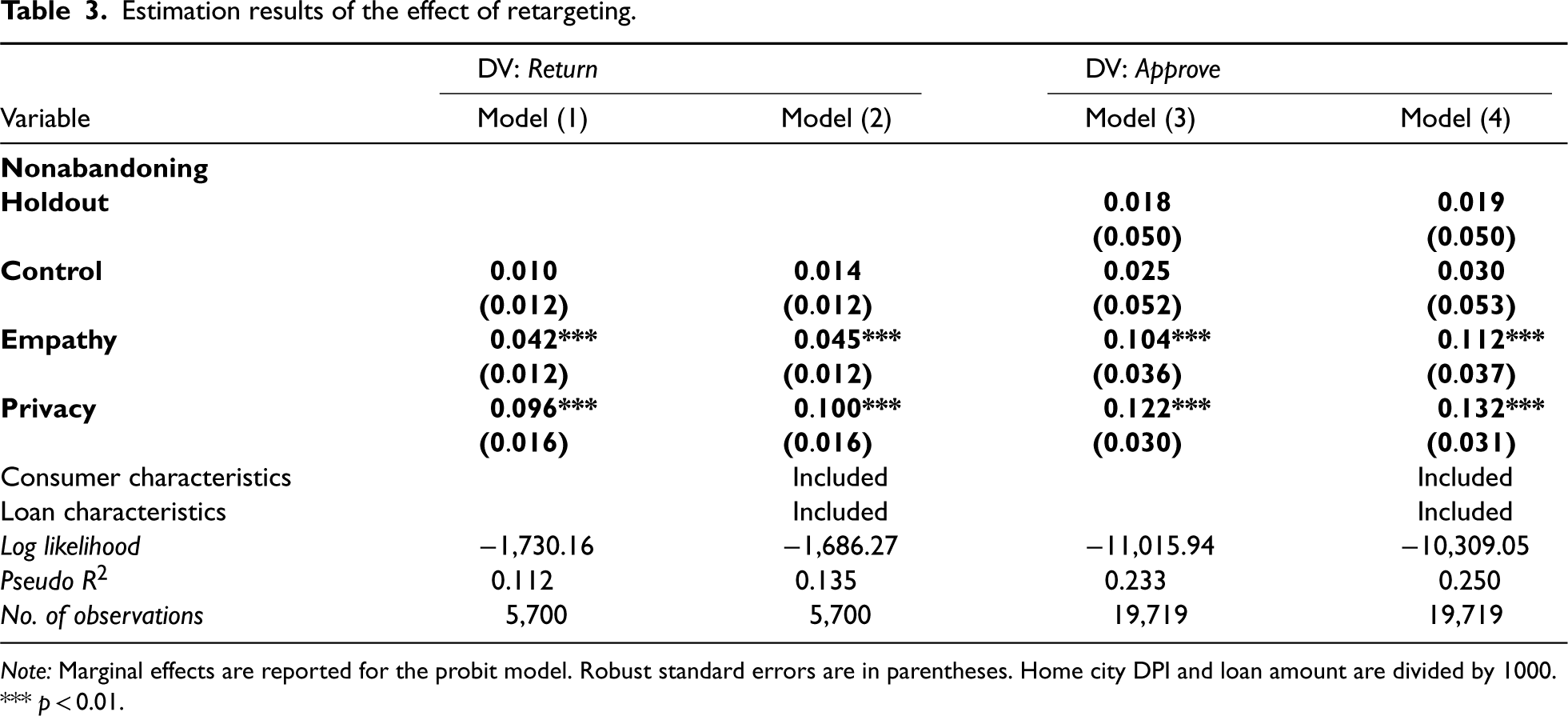

We next perform formal regression analyses. Table B1 in the Appendix reports the descriptive statistics. To systematically investigate the effects of different emotional appeals retargeting messages on winning back consumers, only the sample of abandoning consumers is employed. We apply the holdout group as the benchmark. Based on our treatment design, we use the following treatment variables: Control, Empathy, and Privacy. We use the following independent equations to examine the effects of treatments on the return of an abandoning consumer (Return, 1 = yes, 0 = no). The model is specified in equation (1). Because both dependent variables are dummy variables, we conduct probit regressions (refer to Table B6 in the Appendix for using linear probability models as robustness checks). In the equation, we control for some consumer characteristics (Table 2) that may affect dependent variables. We mark all these covariates as Consumer. We also control loan characteristics, namely the loan amount, loan term, annual interest rate, purpose of the loan, and whether the loan application is initiated during weekends (Weekend). We mark all these covariates as Loan. The subscript i indicates an individual consumer.

Estimation results of the effect of retargeting.

Note: Marginal effects are reported for the probit model. Robust standard errors are in parentheses. Home city DPI and loan amount are divided by 1000.

*** p < 0.01.

Descriptive Analyses

In the financial market, credibility is one of the most representative and straightforward indicators for measuring consumer quality (de Andrade and Thomas, 2007). A common indicator to measure consumer credibility is loan repayment performance. However, the consumers whose loan applications are rejected by the platform are unobservable. In our experiment, we use the loan approval decision, whether a submitted loan application is approved by the platform, to measure a consumer's credibility. Since this study focuses on the stage before loan issuance, the platform's perceived credibility of a consumer at this stage is manifested by the final loan approval decision. This indicator is feasible because the platform staff employs consistent criteria for credibility assessment across experimental groups; thus, the loan approval decision is not affected by whether consumers have abandoned their applications during the process. Table B3 in the Appendix supports this assumption because the loan overdue rates or default rates across the experimental groups are similar. This ensures that loan approval decisions are comparable across groups.

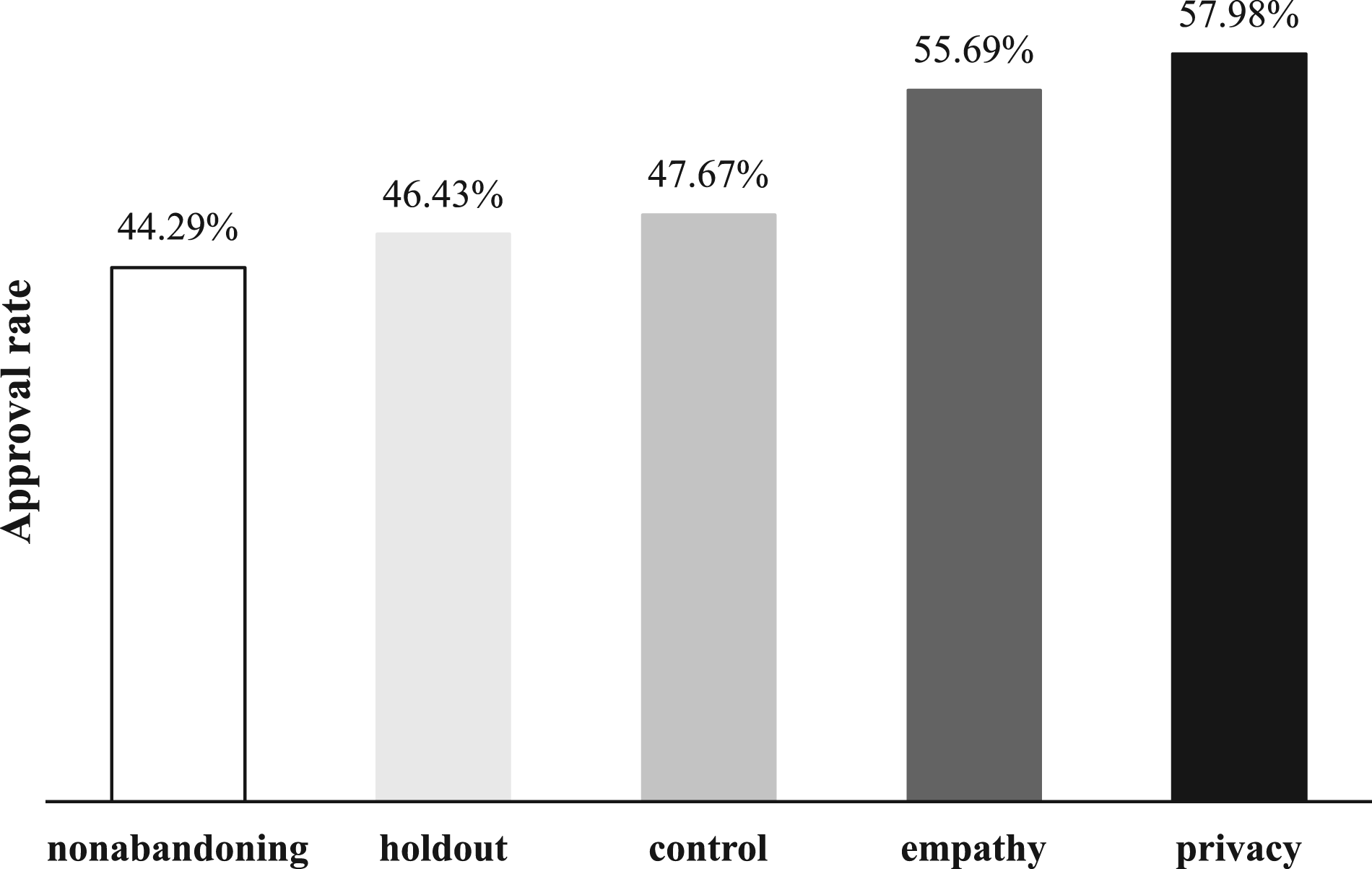

Figure 3 presents the approval rate in our experiment which is calculated as the proportion of approved loans among total submitted applications. The approval rate of nonabandoning consumers on the platform is 44.29%. Considering this rate as the benchmark, we do not find significant differences in the credibility of returning consumers in the holdout group (46.43%, p = 0.693) and that of consumers in the control group called back by the neutral retargeting message (47.67%, p = 0.528). By contrast, consumers returning due to the empathetic support retargeting have an 11.4 percentage-point (= 55.69% – 44.29%, p = 0.003) increase in approval rate over nonabandoning consumers, indicating the overall excellent credibility of these returning consumers.

For consumers called back due to privacy commitment retargeting, we find that they generally have high credibility, with an approval rate as high as 57.98%. In particular, this approval rate is 13.69 percentage points (= 57.98% – 44.29%, p < 0.001) higher than that of nonabandoning consumers (Figure 4).

Approval rates across experimental groups.

We next report the formal regression results. The sample used here to test the impact of retargeting on consumer credibility comprised of two sources: 5,700 returning by experimental retargeting and 19,144 nonabandoning consumers. A dummy dependent variable Approve, indicating whether a loan application is approved by the platform (1 = yes, 0 = no), is implemented to examine consumers’ credibility. We investigate whether the abandon-but-returning consumers (i.e., the treatment samples) have a markedly different loan approval probability compared with nonabandoning consumers. Therefore, we consider nonabandoning consumers as the benchmark group. The focal treatment variables are Holdout, Control, Empathy, and Privacy, which are dummy variables indicating the group to which a consumer belongs (1 = yes, 0 = no). Equation (2) is the model specification. Similarly, we control the characteristics of consumers and loans. The subscript i indicates an individual consumer. We run Probit regressions and report the marginal effects of estimations.

As observed in Models (3) and (4) of Table 3, the loan applications of consumers who return due to the privacy commitment retargeting are 13.2% more likely to be approved by the platform compared with those of nonabandoning consumers. This effect is statistically significant, indicating the higher credibility of these returning consumers. We believe that consumers who maintain a greater sense of privacy protection generally have a high socioeconomic status and are thus more likely to be granted loans. Therefore, H4 is supported.

Despite the loan approval selection, we also applied whether an approved loan defaulted as the dependent variable based on the subsample of approved loans (refer to Appendix). Table B5 presents similar results to Table 3, suggesting the validity of using approval as a credibility metric and the robustness of our findings. Furthermore, we report the return rates and approval rates across different experimental groups and timeframes (i.e., within 24 hours, between 24 and 48 hours, and beyond 48 hours) in Table B6 (Appendix) to offer more insights.

Our two emotional appeals retargeting designs are motivated by the two major causes of consumer abandonment in the financial service market and are based on the ELM. It is thus critical to examine whether the reasons underlying consumer abandonment and their return are in line with our theoretical justifications. We elucidate the mechanisms with a second survey in this section.

Reasons for Consumer Abandonment

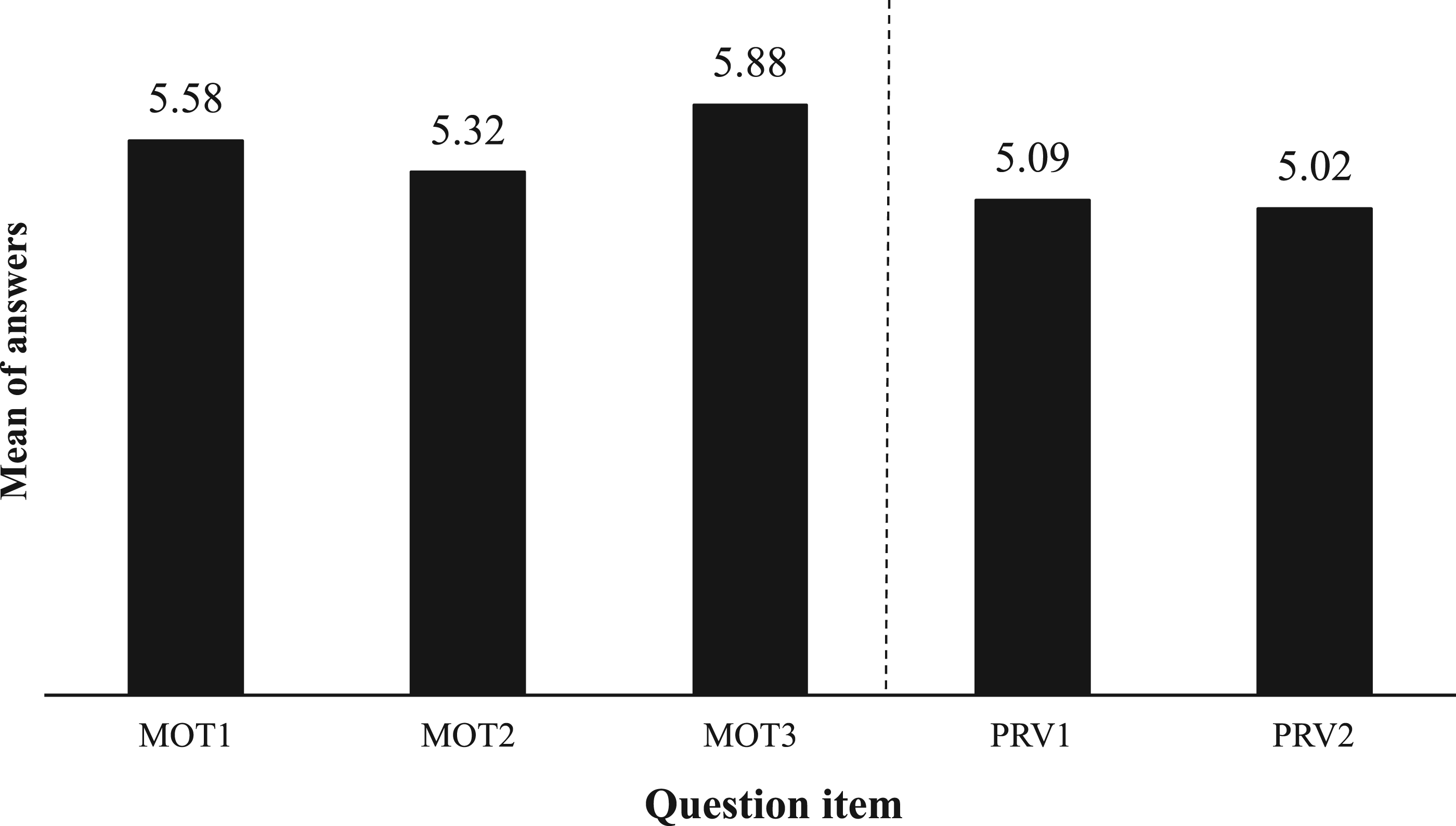

The survey majorly investigates why consumers abandon FSPs. As shown in Table C2 (Appendix), we design several question items based on previous literature to measure consumers’ motivation for service adoption on the focal platform (MOT1, MOT2, and MOT3) and privacy concerns (PRV1 and PRV2). The survey page pops up immediately for all consumers when they click the Exit button. For each question, a higher score (ranging from 1 to 7) indicates a higher level of confirmed adoption motivation (in contrast to indecisive motivation) or concern. In total, 2,376 (41.68%) abandoning consumers completed the survey and provided effective answers. 11 The similar values (including sample size and mean of each question and demographic variable, refer to Tables C3 and C4 in the Appendix) across groups indicate the presence of trivial self-selection (nonresponse) bias of survey participants across groups, suggesting the results are valid and irrelevant to consumers’ returning decisions.

As shown in Figure 5, consumers overall have a strong level of confirmed adoption motivation because they offer a score of >5 for relevant questions (MOT). If we apply the score of 4 as the threshold to define categorical highs (>4) or lows (≤4) motivation/concern, 12 we obtain 106 (i.e., 4.46%) consumers having both indecisive adoption motivation but low privacy concerns (type 1), 214 (9.01%) having indecisive adoption motivation and high privacy concerns (type 2), 502 (21.13%) having highly confirmed adoption motivation and low privacy concerns (type 3), and 1,554 (65.40%) having highly confirmed adoption motivation but high privacy concerns (type 4). In particular, we expect that our proposed retargeting messages would be especially effective in recovering type 1 and type 4 consumers.

Reasons for consumer abandonment. Note: MOT: motivation; PRV: privacy concern. The answer score ranges from 1 to 7. A larger score indicates a higher level of confirmed motivation or concern.

In the survey, we measure some other potential factors that might lead to consumer abandonment as well, including concerns regarding other loan attributes (e.g., loan term, price) and process complexity, effort cost, and self-evaluated likelihood of being approved. Table C3 in the Appendix suggests that these factors are not the major reasons underlying consumer abandonment.

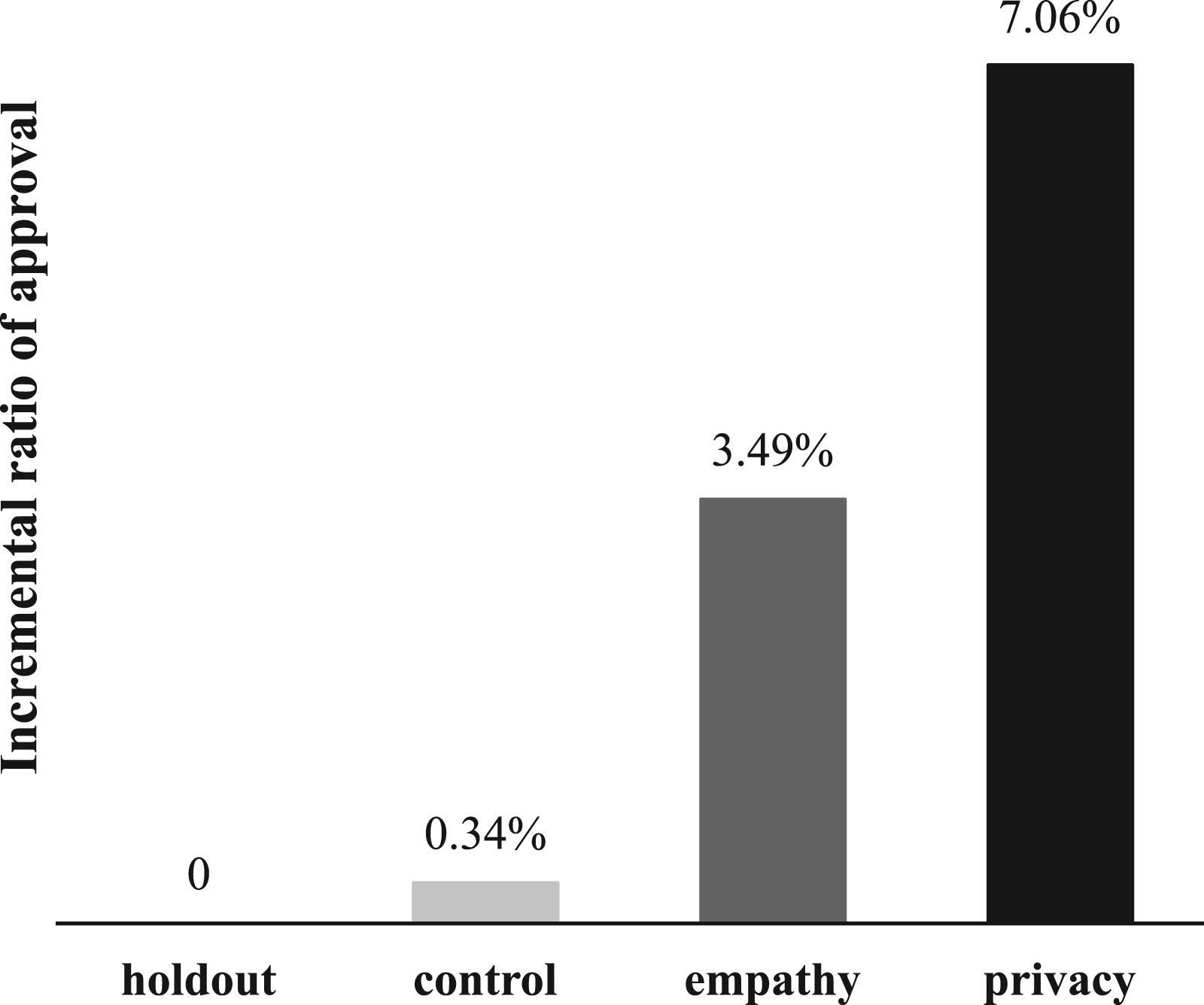

Figure 6 shows the incremental ratio of approved consumers to the total number of abandoning consumers across experimental groups, with the holdout group taken as the benchmark. As shown in Figure 6, the incremental consumers called back by the empathetic support and privacy commitment retargeting present a higher likelihood of loan approval (∼3.49% and 7.06%, respectively).

Incremental ratio of loan approval across experimental groups.

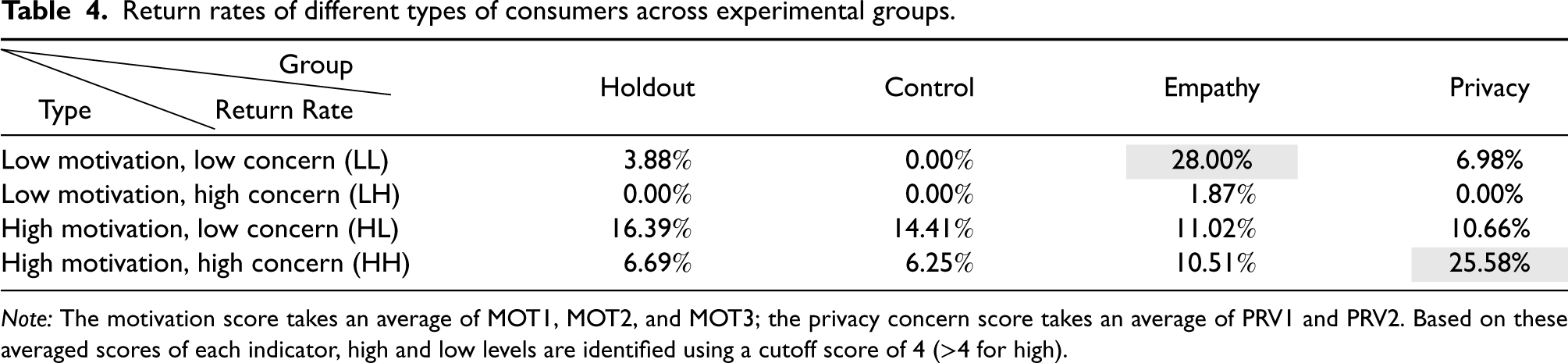

By using the subsample who completed the second survey, we examine the returning consumers in each group. We categorize returning consumers into four types: low/high adoption motivation × low/high privacy concern (i.e., LL, LH, HL, and HH). 13 The classification is based on the cutoff score of 4 for questions related to adoption motivation and problem concerns in the survey (refer to Table C6 in the Appendix for our usage of an alternative cutoff score of 5 as a robustness check). Table 4 reports the return rates of different types of return consumers across experimental groups (refer to Table C5 and Figure C1 in the Appendix for additional analyses). As illustrated in the table, empathetic support and privacy commitment retargeting messages lead to significantly higher return rates for the consumers with indecisive adoption motivation but low privacy concern (i.e., LL, 28.00%) and with highly confirmed adoption motivation but high privacy concern (i.e., HH, 25.58%), respectively, consistent with our theoretical conjectures. In contrast, it is intuitive to find that consumers with highly confirmed adoption motivation and low privacy concerns are more likely to return to the platform than other types of consumers in the holdout (16.39%) and control (14.41%) groups. In sum, these heterogeneous treatment effects support the fact that our proposed two types of emotional appeals retargeting strategies indeed affect the returning decisions of distinct consumers via central or peripheral routes as per the ELM.

Return rates of different types of consumers across experimental groups.

Note: The motivation score takes an average of MOT1, MOT2, and MOT3; the privacy concern score takes an average of PRV1 and PRV2. Based on these averaged scores of each indicator, high and low levels are identified using a cutoff score of 4 (>4 for high).

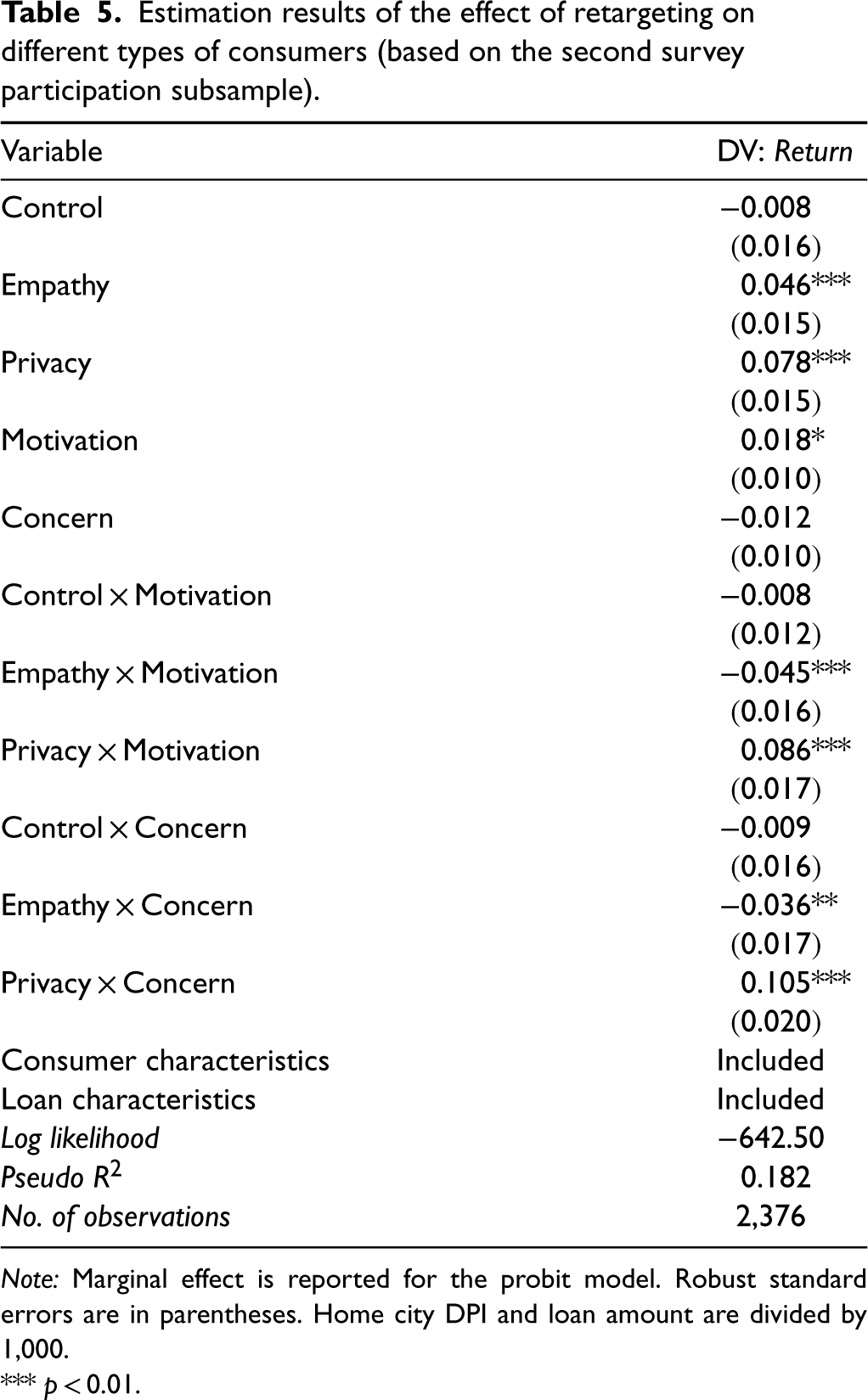

We also conduct a regression accordingly with two variables and corresponding moderators adding to equation (1). The model specification and estimation results are as equation (3), where Motivation and Concern are two continuous variables indicating consumers’ financial service adoption motivation and privacy concern obtained directly from the survey. The moderating terms of Table 5 indicate that generally, empathetic support and privacy commitment retargeting are significantly more effective in recovering abandoning consumers with indecisive adoption motivation but low privacy concern (i.e., LL) and with highly confirmed adoption motivation but high privacy concern (i.e., HH), respectively, which heterogeneous treatment results align with the model-free results reported in Table 4.

Estimation results of the effect of retargeting on different types of consumers (based on the second survey participation subsample).

Note: Marginal effect is reported for the probit model. Robust standard errors are in parentheses. Home city DPI and loan amount are divided by 1,000.

*** p < 0.01.

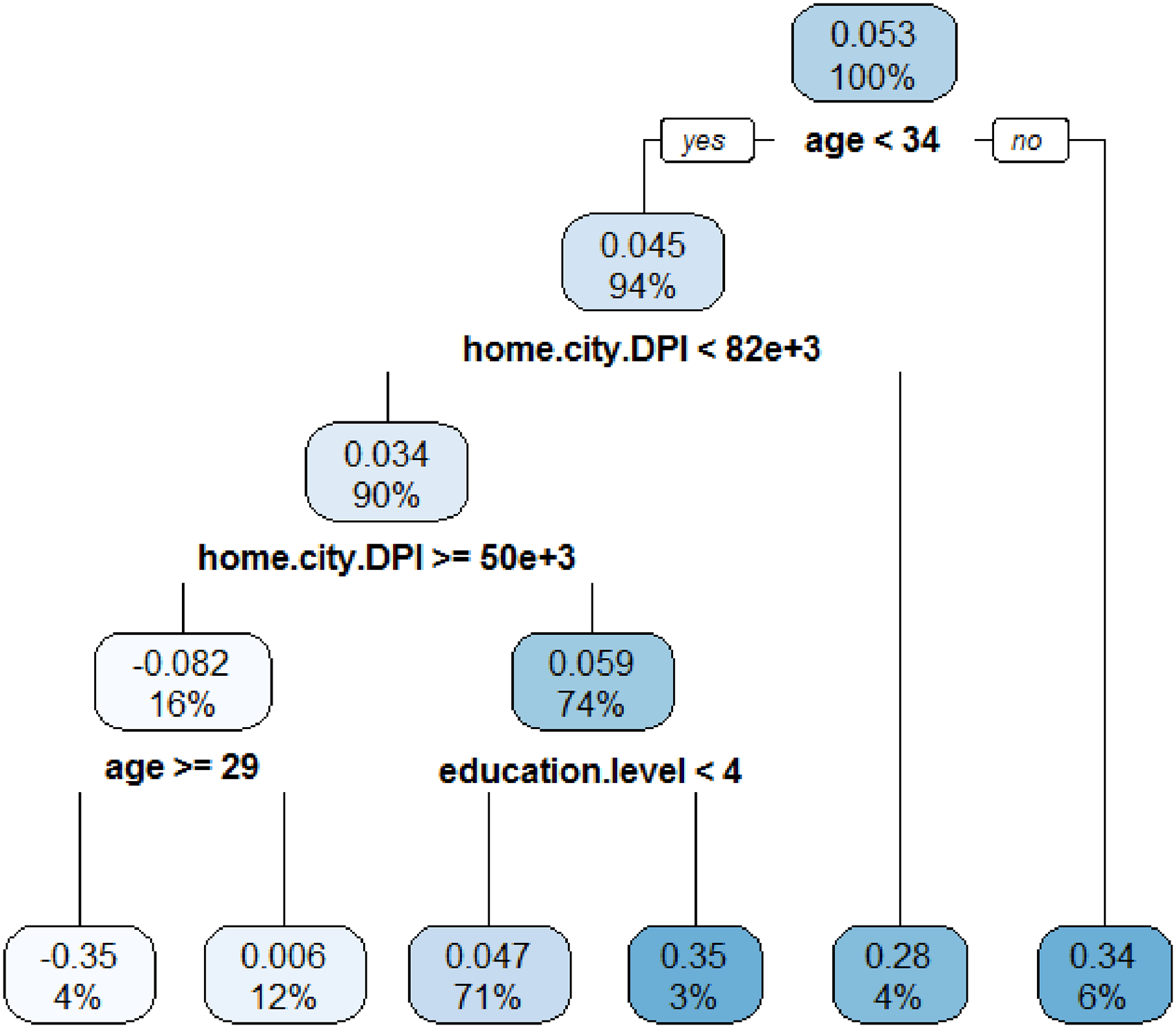

So far, we have elucidated the heterogeneous effectiveness of emotional appeals retargeting in calling back abandoning consumers with different levels of credibility. Whereas the above analyses, consumers’ adoption motivation and privacy concerns are usually unobservable to FSPs. Practically, FSPs should thus anticipate a more intuitive retargeting guidance that fits every single abandoning consumer, in addition to the homogeneous treatment effect of our proposed retargeting strategies. Therefore, we devised a more tailored retargeting strategy that further optimizes the retargeting with these two emotional appeals across different consumer characteristics. To this end, we leverage the state-of-the-art causal random forest with an honest tree algorithm (Wager and Athey, 2018). This algorithm can yield relative heterogeneous treatment effects (RHTE) by simulating the treatment effects for every combination of consumer demographics (Luo et al., 2019). We include consumer characteristics of age, gender, education level, income level, and home city DPI in running the algorithm. We simulate the RHTE of privacy commitment over empathetic support for retargeting as illustrated in Figure 7.

Heterogeneous treatment effects (privacy commitment vs. empathetic support).

Figure 7 depicts a straightforward rule to guide the optimal choice between empathetic support and privacy commitment retargeting strategies. That is, only for the 4% of consumers who are aged larger than 29 and from cities with a DPI between CNY50,000 and CNY82,000, the empathetic support retargeting is more effective (effect: −0.35). For other consumers, using privacy commitment retargeting can call back more consumers. Particularly, privacy commitment retargeting is quite effective in recovering the consumers who are 34 years old or above (0.34, 6% of the consumers) and who are from very developed cities with DPI of larger than CNY82,000 (0.28, 4% of the consumers). This is why the recovered consumers by such retargeting present higher credibility in our previous analyses. Figure C2 in the Appendix suggests that generally, consumers whose home city DPI is larger than CNY46,395 or whose age is larger than 28 are more likely to be highly credible to acquire loan approval. FSPs can thus leverage personalized privacy commitment or empathetic support retargeting operations on the consumers with these characteristics to achieve optimal economic outcomes.

Discussions and Implications

Based on the uniqueness of financial service markets, our theoretical discussions suggest some boundaries might hinder the effectiveness of informative appeals retargeting strategies on calling back financial consumers. We, thus, have turned our eyes to the potential of an alternative strategy, namely emotional appeals, as a means to address the challenges associated with consumers’ indecisive motivation and privacy concern. We develop and validate that the emotional appeals retargeting can call back high-quality consumers via mitigating consumers’ psychological distance and unsafety from financial services. Our findings offer nontrivial contributions and implications.

First, we are among the first to employ emotional appeals retargeting operation strategies in the financial service market. Our empirical analyses of the two developed retargeting messages based on a field experiment offer valuable results. We show that despite the consumers may present some hesitation and concerns toward financial services, empathetic support retargeting can successfully yield a 5.19 percentage-point increase in the return rate compared with no message scenarios, and privacy commitment retargeting can call back 10.53 percentage points more consumers compared with no message scenarios. These effects are significant, echoing the effect magnitudes of retargeting messages in other studies (e.g., Hoban and Bucklin, 2015,; Lambrecht and Tucker, 2013) and therefore, indicating the potential of behavioral nudge.

Second, different from traditional retail wherein retailers need majorly consider consumer recovery, we further reveal that the empathetic support and privacy commitment retargeting both call consumers back with high credibility, presenting the high potential for improving platform revenues. This yields another contribution that although many studies have examined how to balance the trade-off between better service quality (through data analytics based on more information collected) and economic loss from privacy (e.g., Hann et al., 2002; Wottrich et al., 2018), our study offers a useful and low-cost ex-post remedy from the emotional perspective (i.e., a consumer-centered privacy commitment retargeting) to retrieve the opportunity loss of high-quality consumers due to privacy concerns regarding personal information collection.

Finally, our research delves into the mechanisms behind retargeting, which work to reduce consumers’ psychological distance and safety concerns, ultimately bolstering trust in FSPs. Our mechanism test reveals that empathetic support retargeting is particularly effective in attracting consumers who exhibit a strong level of indecisiveness in adopting services due to a perceived psychological distance from FSPs. Conversely, privacy commitment retargeting is more successful in re-engaging consumers who have a high level of motivation but express significant concerns about privacy, leading to a sense of psychological unsafety. This finding strengthens the ELM (Petty and Cacioppo, 1986) by indicating that peripheral cues, such as empathetic appeals, are useful for persuading consumers with indecisive motivation to continue their transactions, whereas core cues, such as issues related to service quality regarding privacy, can attract consumers with highly confirmed motivation but significant problem concerns.

Practically, our research findings offer FSPs clear guidance to craft effective, actionable, and cost-effective retargeting strategies to recover high-quality consumers. FSPs can readily integrate our findings into their day-to-day operations. In particular, our finding implies that empathetic support and privacy commitment retargeting can be employed complementarily to reengage consumers of different types. Therefore, we can personalize retargeting messages to achieve optimal outcomes (Ascarza, 2018). Specifically, empathetic support strategies convert indecisively motivated consumers to adopt the service; this strategy may attract new consumers to financial services overall and thus potentially contribute to financial equality (Tang, 2022). A privacy commitment message would win back consumers who already have a high intention to adopt and are in the process of choosing between service providers. Finally, a more tailored machine-learning-based retargeting strategy for practice is explored accordingly.

Limitations and Directions for Future Studies

Our research has several limitations that indicate avenues for future research. First, privacy concerns can be addressed by both informative appeals and emotional appeals. Our study validated that emotional appeals retargeting that conveys consumers-focused information security commitment is useful to call consumers back by reducing their psychological safety concerns and increasing their trust in the platform. However, we are unable to directly compare the effectiveness of privacy concern reduction between informative appeals and emotional appeals as Gerlach et al. (2019) did. Future research could go deep on this point and contribute more evidence toward privacy literature. Second, although we have documented the respective effects of empathetic support and privacy commitment retargeting, future studies can further investigate the effect of a combinatorial group of these two message types. Third, we conduct our study in a single context and cultural setting, which might limit the generalizability of our findings to other countries. Replicating our experiment in different contexts and cultures can enrich our understanding of consumer responses to retargeting in the financial service market. Finally, due to data limitations, we have been unable to decompose the effectiveness of retargeting messages on consumers who abandon applications at distinct points of personal information provision. Future studies, with data available, can work on this aspect to offer more granular insights.

Supplemental Material

sj-pdf-1-pao-10.1177_10591478231224925 - Supplemental material for Being Emotionally Supportive: Exploring the Value of Emotional Appeals Retargeting in Recovering Consumers of Financial Services

Supplemental material, sj-pdf-1-pao-10.1177_10591478231224925 for Being Emotionally Supportive: Exploring the Value of Emotional Appeals Retargeting in Recovering Consumers of Financial Services by Tian Lu, Xianghua Lu, Hui Yang and Peter Zhang in Production and Operations Management

Footnotes

Acknowledgements

Tian Lu and Xianghua are the joint first authors. Hui Yang is the corresponding author. The authors thank the Department Editor, the Senior Editor, and three anonymous reviewers for their constructive feedback. This work was partially supported by the National Natural Science Foundation of China (#72225004).

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the National Natural Science Foundation of China (grant number 72225004).

Notes

How to cite this article

Lu T, Lu X, Yang H, Zhang P (2023) Being Emotionally Supportive: Exploring the Value of Emotional Appeals Retargeting in Recovering Consumers of Financial Services. Production and Operations Management 33(1): 166–183.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.