Abstract

We examine the causal effects of nearby terrorist attacks on supplier–customer relationships. We find that for supplier firms located near terrorist attacks, the probability of relationship termination with their major customers increases by 2.9 percentage points within two years following the attacks. The major customers’ intensified perceptions of supply chain risk largely drive the relationship termination. Further analyses show that major customers tend to switch to suppliers with lower terrorism risks after they end their relationships with the suppliers near attacks. This study provides new insights into the consequences of terrorism by extending the focus to the response of a key stakeholder group (i.e., trade partners) instead of the attack-afflicted firms per se.

Introduction

Terrorism, defined as “the threatened or actual use of illegal force and violence by a nonstate actor,” has become one of the most serious threats to humanity in recent decades. 1 A burgeoning body of literature has documented that terrorist attacks impose adverse consequences on corporate activities in various aspects, such as risk-taking (Antoniou et al., 2017), corporate disclosure (Chen et al., 2021), CEO compensation design (Dai et al., 2020), and research and development (R&D) investment (Fich et al., 2020; Li et al., 2022). This study extends this line of research by investigating the impacts of terrorist attacks on firms’ relationships with their major customers.

Major customers are among the most important stakeholders in many firms, with durable trading relationships with suppliers being a prevailing business practice in the U.S. (Fee et al., 2006). On the one hand, forging enduring trading relationships with major customers can enable firms to achieve strong competitive advantages (Patatoukas, 2012). On the other hand, trading with major customers generally entails relationship-specific investments that offer little value outside the relationships (Banerjee et al., 2008; Wagner and Bode, 2014). Hence, understanding the factors that influence the duration of firms’ relationships with their major customers is of great importance.

Terrorist attacks, as unanticipated negative shocks to the environment where firms operate, could affect firms’ relationships with their major customers for several reasons. First, terrorist attacks introduce uncertainty to corporate operations by suppressing market demand (Becker and Rubinstein, 2004), disrupting value chains (Czinkota et al., 2010), reducing employee productivity (Luo et al., 2020), and increasing external financing costs (Abadie and Gardeazabal, 2008). Terrorism-induced uncertainty can adversely affect firms’ fundamentals and undermine their capability to sustainably fulfill obligations to their customers. Major customers may therefore choose to reduce or even end their trading with suppliers exposed to terrorism-induced uncertainty and switch to alternative suppliers facing no terrorism risk.

Second, terrorism-induced uncertainty to supplier firms may intensify their major customers’ perception of their operating risks, even though terrorist attacks per se do not cause any real adverse impact on their fundamentals. Terrorist attacks exert strong negative impacts on individuals’ emotions, eliciting heightened perceptions of threat, anxiety, and depression (e.g., Galea et al., 2002; Hughes et al., 2011). Due to intense media coverage, terrorism-induced negative sentiments have been found to be widespread and naturally synchronized among the population beyond attacked regions (Nellis and Savage, 2012; Slone, 2000), thereby increasing safety uncertainty and fear among economic agents stemming mostly from psychological reasons (Abadie and Gardeazabal, 2008; Ahern, 2018). Individuals experiencing negative emotions, such as fear caused by terrorist attacks, are more likely to overestimate risk and become more risk-averse (e.g., Lerner and Keltner, 2001; Lerner et al., 2003; Wang and Young, 2020). Top managers of acquiring firms are most likely reluctant to make acquisition investments in terrorism-afflicted areas partly because of their increased disinclination out of safety concerns to travel to the headquarters of target firms located near terrorist attacks (Nguyen et al., 2022). Without exception, managers of major customers could also be shocked by terrorist attacks that occur near their supplier firms. The negative psychological impact of terrorism could induce the managers to change their business-as-usual mindset and overestimate the operating risks of their attack-affected suppliers, destabilizing the relationship between the two trading parties. Safety uncertainty and fear induced by terrorism could also discourage major customer managers from on-site visiting the supplier firms in terrorism-affected areas, especially in the near period following the incident, impairing efficient communication between the two trading parties and thereby adversely affecting the duration of the supplier–customer relationship. Taken together, we conjecture that supplier firms are more likely to suffer disruptions in their relationships with major customers in the period following terrorist attack incidents near their headquarters.

We use a sample of terrorist attacks that occurred in the U.S. from 1976 to 2017 to examine our research questions. Based on the supplier–customer pairs from Compustat Segment files, we mainly rely on probit model analyses to investigate the effects of terrorist attacks on the supplier–customer relationship duration. After controlling for supplier-, customer-, and relationship-specific characteristics, we find a consistently positive association between terrorist attacks near supplier firms and the termination of their relationships with major customers within the two years following the terrorist attacks. The probability of supplier–customer relationship termination increases by 2.9 percentage points on average for suppliers located near terrorist attacks within the subsequent two years. These findings support that terrorist attacks cause significant adverse consequences for nearby supplier firms in maintaining relationships with their major customers. Our results are robust to a series of sensitivity tests, such as alternative samplings, alternative terrorism measures, and alternative regression specifications.

In addition to the effect on supplier–customer relationship termination, we conduct difference-in-differences (DiD) analyses to examine the impact of terrorist attacks on the sales of nearby suppliers to their major customers in the three-year period around terrorist attacks. The treatment group comprises supplier–customer pairs, with the suppliers located in terrorism-afflicted areas. The control group comprises supplier–customer pairs, of which the supplier firms operate in the same industry and share the same major customers with the suppliers in the treatment group. We find that compared with the firms in the control group, the terrorism-affected suppliers experience a decline of 16% in sales to major customers in the years following terrorist attacks. Our additional dynamic analysis reveals that the relative decrease in sales to major customers for the treatment suppliers is observed not before terrorist attacks but only after them, lending credence to the causal effects of terrorist attacks on supplier–customer relationships.

Next, we investigate potential mechanisms through which terrorist attacks affect the relationship of nearby supplier firms with their major customers. We first examine whether the increased likelihood of supplier–customer relationship termination associated with terrorist attacks is driven by potential harm to the nearby supplier firms’ fundamentals caused by terrorist attacks. We find no evidence that terrorist attacks deteriorate the nearby supplier firms’ fundamentals captured by financial performance or adversely affect the suppliers’ operating activities, including trade credit provision, R&D investment, cash holdings, and inventory turnover, in the two quarters following terrorism incidents. Presumably, terrorist attacks directly affect the security and defense risk of the nearby firms, but these risks change little around the quarter in which attacks occur, as shown by our empirical analyses. We also do not observe significant negative stock market reactions to terrorist attacks for the nearby supplier firms in short windows following terrorism incidents. Furthermore, we find that two key groups of market participants, namely, financial analysts and institutional investors, do not expect that the fundamentals of supplier firms would be significantly impaired by nearby terrorist attacks. Taken together, these results do not support the notion that the increased likelihood of supplier–customer relationship termination associated with terrorist attacks near suppliers is attributable to the potential fundamental deterioration caused by terrorist attacks.

Major customers’ intensified risk perceptions regarding suppliers near terrorist attacks are another possible mechanism underlying the increased likelihood of supplier–customer relationship termination associated with terrorist attacks near suppliers. We find that the negative effect of terrorist attacks on nearby firms’ relationship with their major customers is more pronounced when their major customers exhibit more risk aversion, indicated by lower performance volatility, the experience of nearby terrorist attacks in the prior three years, and membership in durable industries. These findings are in line with the conjecture that terrorist attacks near supplier firms intensify their major customers’ perceptions of supply chain risk or safety uncertainty, or both, in turn destabilizing their relationship with major customers.

A transparent information environment of supplier firms and efficient communication between the two trading parties can help mitigate major customers’ misperceptions of supplier firm risks. Our additional analyses find consistent evidence that the adverse effect of nearby terrorist attacks on supplier–customer relationships is weakened for supplier firms with a higher financial reporting quality and a higher percentage of common dedicated institutional investors with major customers. These investors promote private communication between the two trading parties and prevent major customers from overestimating the supplier firm risks associated with nearby terrorist attacks. Based on risk factor disclosure in firms’ Securities and Exchange Commission (SEC) filings, we also find that customer firms are more likely to express concerns about the terrorism risks of their suppliers in fiscal years in which terrorist attacks occur near their supplier firms’ headquarters. Major customers are also inclined to switch to supplier firms with lower terrorism risks after they terminate their relationships with the supplier firms near terrorist attacks. Furthermore, we find that among the terminated supplier–customer relationships, those interrupted by nearby terrorist attacks are more likely to be resumed in the near future. In sum, all these findings support the view that the increased likelihood of supplier–customer relationship termination associated with terrorist attacks near supplier firms is mostly attributable to major customers’ intensified perception and overestimation of supplier chain risks that terrorist attacks near supplier firms could cause.

Finally, we conduct additional tests to examine variation in the effect of terrorist attacks on nearby suppliers’ relationship with their major customers. First, customer firms that are less asymmetrically dependent on their suppliers have relatively greater bargaining power (Cheung et al., 2020; Pfeffer and Salancik, 1978) and are more likely to replace the affected supplier firms in the event of terrorist attacks. Consistent with this prediction, we find that the effect of terrorist attacks on supplier–customer relationship termination is more pronounced when the suppliers near terrorist attacks are more asymmetrically dependent on major customers. Second, customers facing higher costs of switching to alternative suppliers are less likely to terminate the relationship (e.g., Barrot and Sauvagnat, 2016; Intintoli et al., 2017). We indeed find that the effect of terrorist attacks on supplier–customer relationship termination is attenuated for suppliers near terrorist attacks that produce more differentiated products, increasing their customers’ switching costs (Barrot and Sauvagnat, 2016). Third, trade credit serves as an important financing source for customer firms (Fisman and Love, 2003; Tirole, 2006). We find that the effect of terrorist attacks on supplier–customer relationship termination is mitigated for the suppliers near terrorist attacks that provide higher levels of trade credit. Fourth, as one of the most catastrophic tragedies, the 9/11 terrorist attack significantly changes the attitudes of U.S. people toward terrorism risks (Murphy et al., 2004). We find that the observed effect of terrorist attacks on supplier–customer relationship termination grows stronger in the period after the 9/11 incident.

This study contributes to the literature in several ways. First, we extend the growing literature on the economic consequences of terrorism to the effect on bilateral relationships along supply chains. Existing studies mainly focus on the behaviors of firms or market participants themselves that are directly affected by terrorist attacks, such as financial policy (Antoniou et al., 2017), CEO compensation (Dai et al., 2020), R&D investment (Fich et al., 2020; Li et al., 2022), investor market participation (Wang and Young, 2020), and analyst forecasts (Cuculiza et al., 2021). Our research provides new insights into how terrorist attacks affect the reactions of major stakeholder groups, trade partners in particular, by examining major customers’ recalibration of supplier–customer relationships in response to terrorist attacks near their supplier firms. This study is especially related to the research highlighting the negative psychological impact of terrorism (e.g., Ahern, 2018; Becker and Rubinstein, 2004; Nguyen et al., 2022). Our findings reveal that major customers’ intensified risk perceptions and resultant overestimation of supplier risks, rather than the actual fundamental deterioration caused by terrorist attacks near supplier firms, largely lead to the termination of supplier–customer relationships following terrorism incidents.

Second, this study contributes to the literature on supplier–customer relationships by providing comprehensive evidence that uncertainty caused by terrorist attacks adversely affects supply chain relationships. Prior studies have documented various determinants of supplier–customer relationship duration, including equity ownership held by trade partners (Fee et al., 2006), social connections in bilateral relationships (Dasgupta et al., 2021), and firm characteristics of trade partners such as customer CEO turnover (Intintoli et al., 2017), and supplier internal control quality (Bauer et al., 2018). Our study reveals that the negative psychological impact caused by terrorist attacks near supplier headquarters on major customers also plays an important role in affecting supplier–customer relationships.

Finally, this study contributes to the literature on supply chain risk management. Existing supply chain risk management studies are mostly qualitative or analytical analyses (e.g., Gao et al., 2019; Kumar et al., 2010) or empirical analyses based on survey data with limited sample sizes (Ho et al. 2015) or subject to endogeneity (Kleindorfer and Saad, 2005). By contrast, our study exploits terrorist attacks as exogenous shocks to supply chain risks and conducts empirical analyses using a large sample of supplier–customer pairs in the U.S. Our findings provide important implications for supplier managers to take timely action, such as by enhancing private communication, to counterbalance the risk overestimation of their major customers induced by nearby terrorist attacks, especially when their customers are more risk averse or have higher bargaining power.

The remainder of the paper proceeds as follows: Section 2 develops the hypothesis. Section 3 discusses the sample and research methodology. Section 4 reports the main empirical results. Section 5 explores the mechanism underlying the association between terrorist attacks near supplier firms and supplier–customer relationship duration. Section 6 describes additional tests. Section 7 concludes.

Hypothesis Development

Disruption risk is among the two broad categories of risk affecting supply chain design and management (Kleindorfer and Saad, 2005). Firms not only themselves adopt but also push their suppliers to develop a disruption orientation to ensure operations and supply chain continuity (Stekelorum et al., 2022). Terrorist attacks, as critical sources of supply chain disruption risk, can trigger firms’ reevaluation of supply chain risk associated with their supplier firms located near terrorist attacks and adjust the trading relationship between the two parties for two reasons.

On the one hand, terrorist attacks spread public fear through violence and induce high uncertainty in business environments (Dai et al., 2020), adversely affecting the operations of supplier firms in the terrorism-stricken areas in various ways. Firms located close to attacks tend to temporarily reduce R&D investment following the attacks because they generate the pessimism of corporate managers in risk assessments (Antoniou et al., 2017) and terrorism-induced uncertainty increases the value of the deferral option in R&D (Li et al., 2022). More importantly, terrorism-induced safety uncertainty among economic agents could distort human capital productivity in the afflicted areas (Abadie and Gardeazabal, 2008; Ahern, 2018). Terrorism-induced fear and safety uncertainty not only lead some key risk-averse employees to leave the afflicted areas but also make it difficult for affected supplier firms to recruit new qualified employees, especially highly skilled labor such as inventors (Fich et al., 2020). Terrorist attacks could also impose negative psychological impacts on existing employees and adversely affect their sentiment, job satisfaction, effort, and creativity (Ahern 2018; Becker and Rubinstein, 2004). Thus, firms near terrorist attacks might need to devote additional resources to incentivize employees and avoid productivity deterioration.

Additionally, terrorist attacks might directly disrupt the affected firms’ normal operating activities and prevent the timely delivery of finished products to their customers (Czinkota et al., 2010). All these potential adverse impacts of terrorist attacks would therefore impair terrorism-afflicted firms’ fundamentals and undermine their capacity to provide services and products as scheduled to customers. Anticipating this increased disruption risk, major customers are likely to switch to other attack-immune suppliers and reduce or even end their trading with supplier firms in terrorism-afflicted areas.

On the other hand, terrorist attacks might adversely affect supplier–customer relationships even though they do not directly harm the fundamentals of supplier firms in terrorism-stricken areas. Terrorism attacks, as an unseen, hovering existential threat, spread fear and anxiety among the population far beyond the attacked areas via wide media publicity and induce negative sentiment and safety uncertainty among economic agents, stemming mostly from psychological reasons (Abadie and Gardeazabal, 2008; Ahern, 2018). Negative emotions such as fear caused by terrorism attacks can increase individuals’ risk aversion and enhance their propensity to overestimate risks (e.g., Lerner and Keltner, 2001; Lerner et al., 2003; Kuhnen and Knutson, 2011). Consistent with this notion, Wang and Young (2020) find that terrorist activity in the U.S. increases the aggregate risk aversion of retail investors and reduces their investment in risky assets. Nguyen et al. (2022) document that terrorism-afflicted firms are less likely to receive acquisition bids for two years after the attack, partly driven by the acquirer CEOs’ safety uncertainty and fear caused by terrorism attacks.

In a similar vein, terrorist attacks near supplier firms can shock the managers of their major customers due to the close business linkage between the two trading partners. The resultant negative emotions such as fear and safety uncertainty experienced by customer managers will intensify their risk aversion and lead them to overestimate the operating risk of their supplier firms near terrorist attacks. Terrorism-induced fear and safety uncertainty could also prevent customer managers from visiting supplier firms and discourage close interactions with supplier executives in terrorism-stricken areas, in turn increasing the likelihood of customer managers misperceiving their suppliers’ disruption risk arising from terrorist attacks. Customer managers are therefore likely to overestimate the negative impact of terrorist attacks on the supply chain risk associated with the afflicted suppliers and overly downward adjust the focal supplier–customer relationships.

The above two potential channels through which terrorism attacks affect focal suppliers’ relationships with their major customers are non-mutually exclusive. Both channels predict that the trading relationship between major customers and their supplier firms located near terrorist attacks will be negatively affected by terrorism incidents. Therefore, we state our hypothesis as follows:

Hypothesis: Compared with their counterparts, supplier firms located near terrorist attacks are more likely to experience relationship termination with their major customers after terrorism incidents.

Although our hypothesis states the alternative, we also note that terrorist attacks near supplier firms might have little impact on their relationship with major customers. Terrorism-afflicted suppliers might strive to effectively communicate with their major customers about the potential impact of nearby terrorist attacks on their fundamentals through various channels (Park et al., 2013; Sreedevi and Saranga, 2017), helping prevent their customers’ overestimation of terrorism-induced supply chain risk. Terrorism-afflicted suppliers could also take additional actions such as offering more trade credits to retain their major customers (Chen and Forman, 2006; Shapiro and Varian, 1999).

Sample, Data, and Methodology

Sample and Data

Our sample starts from all supplier–customer relationships identified by the Wharton Research Data Services from 1976 to 2018 2 , which are based on Compustat Segment files. The Segment database includes customer names and supplier sales to each major customer. We use the 10-K Headers Database constructed by Bill McDonald 3 to identify firm headquarters. 4 We keep only firms that are headquartered in the U.S. and exclude firms in utility (SIC codes 4900–4999) and financial industries (SIC codes 6000–6999) because both industries are highly regulated.

Terrorist attack information is obtained from the Global Terrorism Database (GTD), an open-source database that contains systematic data on global terrorist events. GTD defines a terrorist attack as “the threatened or actual use of illegal force and violence by a nonstate actor to attain a political, economic, religious or social goal through fear, coercion or intimidation” (START, 2018: 10). From the database, we collect information on the exact source, date, location, number of casualties, and specific motive behind the terrorist attacks. 5 Following prior literature, we include terrorist attacks that resulted in at least one casualty because these attacks incur great negative impacts on human emotions (Dai et al., 2020).

We retrieve financial data from Compustat, stock price data from CRSP, institutional ownership data from the Thomson Reuters Institutional 13(f) Holdings database, and analyst forecast data from the I/B/E/S database. Our final sample comprises 53,843 supplier–customer–year observations involving 14,197 unique supplier–customer relationships, 5058 unique suppliers, and 2817 unique customers.

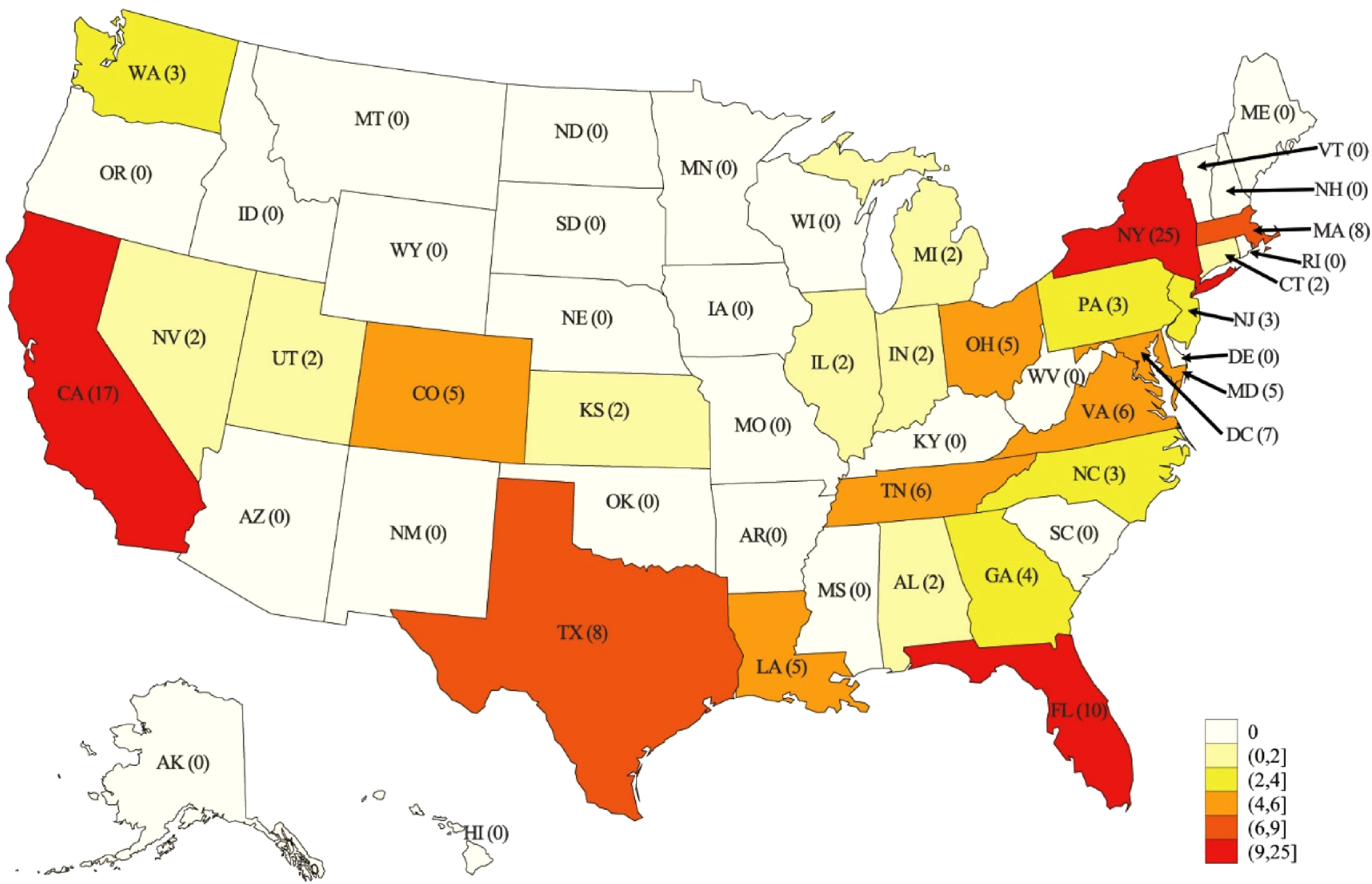

Figure 1 shows the distribution of terrorist attacks in our final sample across states in the U.S., with the largest numbers of attacks in New York, California, and Florida. Table A2 of EC.2 presents a roughly even distribution of terrorist attacks across calendar years, with 2017 witnessing the most terrorist incidents.

The geographic distribution of terrorist attacks in the final sample.

This figure shows the distribution of terrorist attacks in our final sample across states in the U.S.

For our main analyses, to estimate the association between terrorist attacks near supplier headquarters and supplier–customer relationship termination, we follow prior literature (e.g., Bauer et al., 2018) and employ the following probit model specification:

Drawing on prior research (e.g., Bauer et al., 2018; Dasgupta et al., 2021), we control for the following relationship characteristics: Sales dependence, defined as sales to a customer divided by the total sales of a supplier, and Cost dependence, defined as purchases from a supplier divided by the cost of goods sold of a customer. We further control for several supplier- and customer-specific characteristics. Supplier market share is defined as sales of a supplier over total sales of the supplier's industry based on the four-digit SIC code, whereas Customer market share is defined as sales of a customer over total sales of the customer's industry based on the four-digit SIC code. Tenure is the number of years for the presence of the supplier–customer relationship in the Compustat Segment database by the beginning of year t. Supplier R&D and Customer R&D measure the R&D intensity (R&D expenditure over total assets) 8 of suppliers and customers, respectively. We also include the natural logarithm of firm age of suppliers (Supplier LogAge) and customers (Customer LogAge), the natural logarithm of total assets of suppliers (Supplier size) and customers (Customer size), and the indicator of nonpositive free cash flows of suppliers (Supplier free cash flow ≤ 0) and customers (Customer free cash flow ≤ 0). Finally, we include the supplier industry and state interacted with year fixed effects to control for the effect of industry and time-varying state-level factors. 9 The details of the variable definitions are presented in the E-Companion EC.1 Table A1.

In this section, we first provide the descriptive statistics for the regression variables. We then discuss our baseline results regarding the effect of terrorist attacks near supplier firms on supplier–customer relationship termination and provide some robustness checks.

Descriptive Statistics

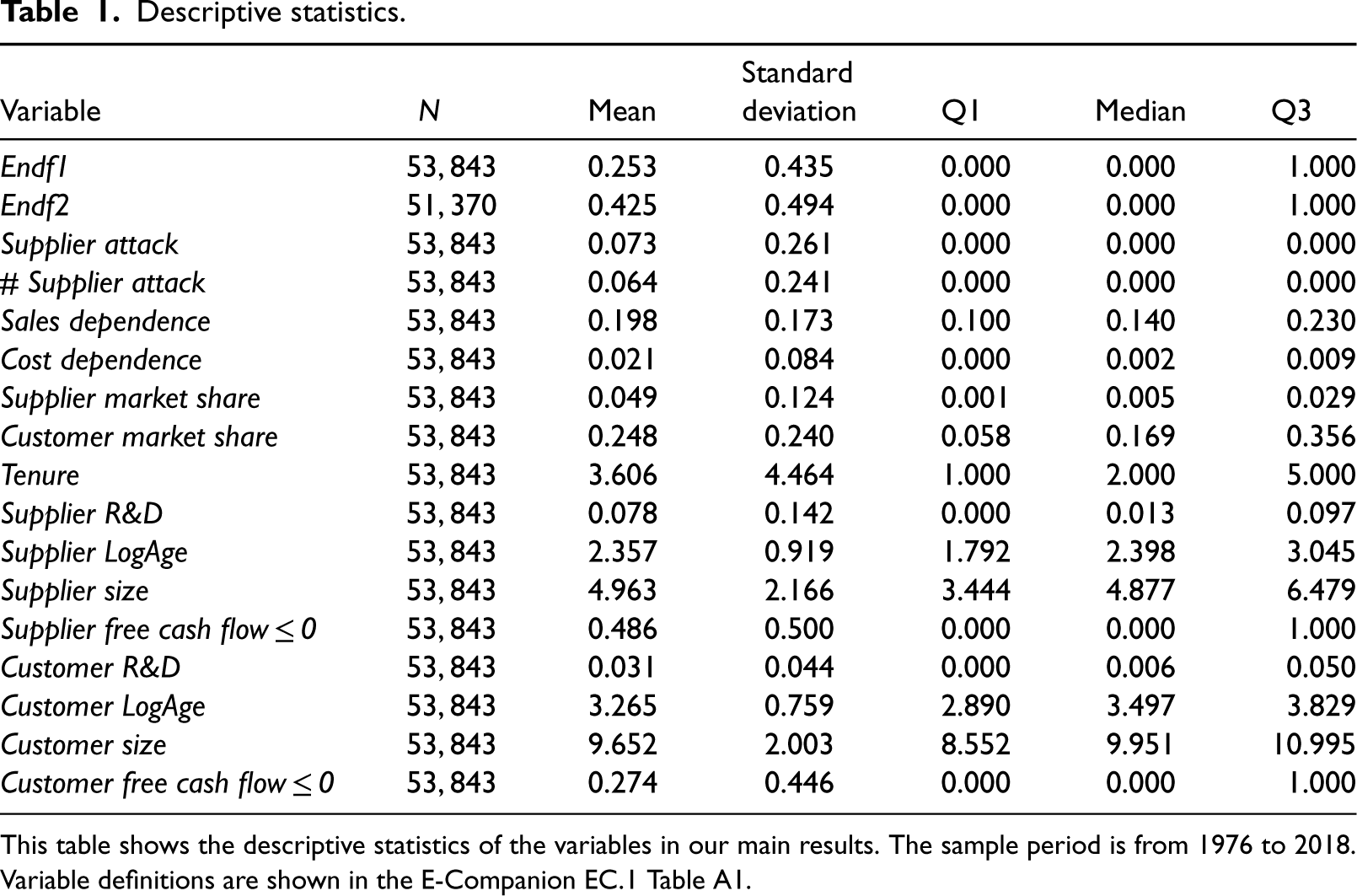

Table 1 provides the descriptive statistics of the variables used in our main regression model. All continuous variables are winsorized at the 1st and 99th percentiles for each fiscal year. 25.3% (42.5%) of supplier–customer relationships end in the subsequent one (two) year(s). In 7.3% of customer–supplier relationships, the suppliers experience at least one terrorist attack that occurs near their headquarters. The average number of terrorist attacks near supplier headquarters plus one in natural logarithm form is 0.064. The average percentage of supplier sales to the customer is 19.8%, and the mean percentage of customer cost of goods sold from the supplier is only 2.1%. This asymmetric dependence of the supplier on the customer in the U.S. is well documented in the literature (e.g., Bauer et al., 2018; Cheung et al., 2020). 10 The average market share of the supplier (4.9%) is significantly lower than that of the customer (24.8%), suggesting that in our sample, it might be easier for a major customer to find alternative suppliers than for a supplier to find alternative major customers. This fact also indicates the relatively lower bargaining power of the supplier in an average supplier–customer relationship. The average tenure of the supplier–customer relationship observed at the beginning of each year is around four years. The R&D intensity of suppliers (7.8%) is generally greater than that of customers (3.1%). Compared with suppliers, major customers tend to have a longer history in Compustat, a larger size, and a lower likelihood of nonpositive free cash flows.

Descriptive statistics.

Descriptive statistics.

This table shows the descriptive statistics of the variables in our main results. The sample period is from 1976 to 2018. Variable definitions are shown in the E-Companion EC.1 Table A1.

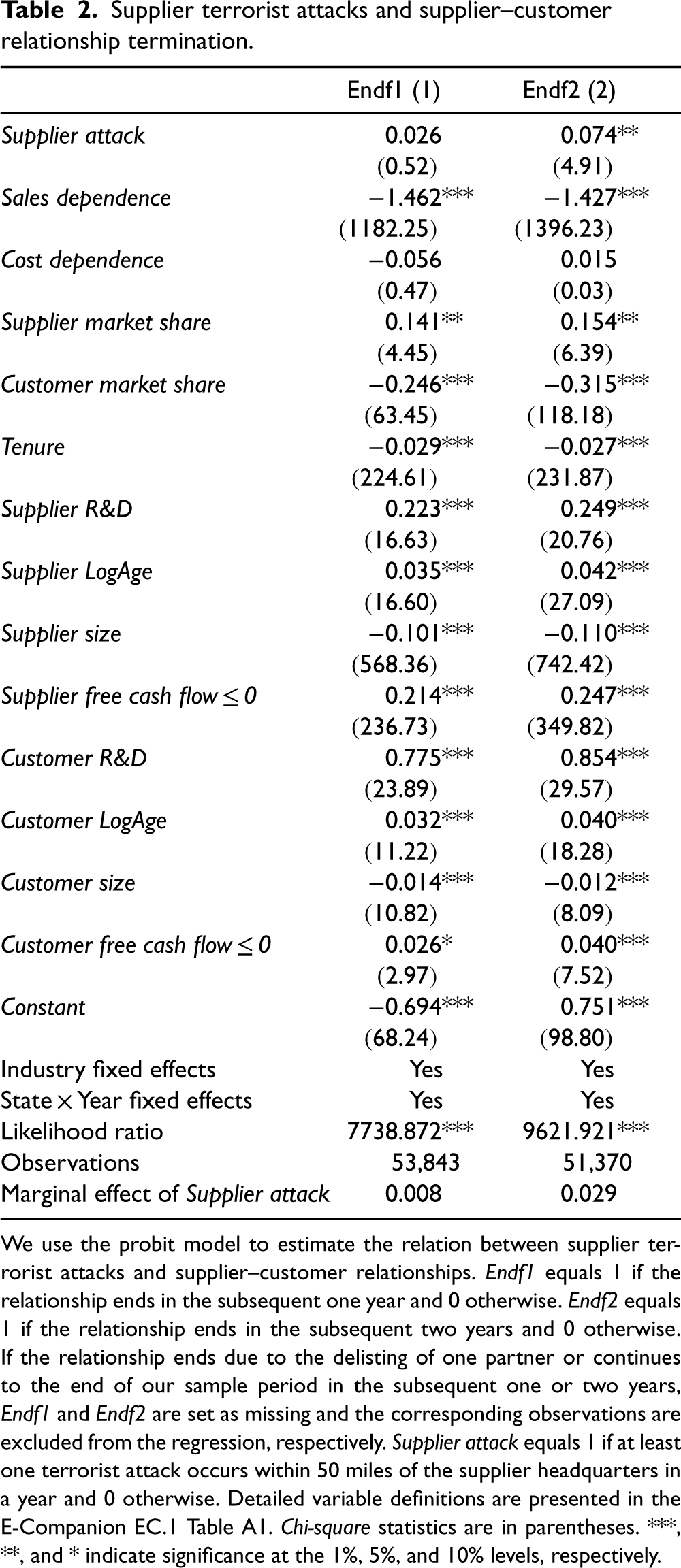

Table 2 presents our baseline results regarding the relationship between terrorist attacks near suppliers and supplier–customer relationship termination. Column (1) reports the results using Endf1 as the dependent variable. The variable Supplier attack is positive but statistically insignificant, suggesting that suppliers near terrorist attacks do not have a higher likelihood of losing major customers in the year after terrorist attacks. Column (2) reports the results using Endf2 as the dependent variable. The variable Supplier attack is positive and statistically significant (p < 0.05), indicating that suppliers near terrorist attacks experience a higher likelihood of losing major customers within the two years after terrorist attacks. Taken together, the results in Table 2 indicate that terrorist attacks near supplier headquarters adversely affect the relationships of the nearby suppliers with their major customers, but finding alternative suppliers and ending the relationship with terrorism-afflicted suppliers can be time-consuming for major customers (Beil, 2011). 11 The marginal effect of Supplier attack in Column (2) suggests that the probability of relationship termination within the two years following terrorist attacks for the suppliers located near terrorist attacks increases by 2.9 percentage points. In sum, these results support our hypothesis that compared with their counterparts, suppliers located near terrorist attacks are more likely to experience relationship termination with their major customers after such attacks.

Supplier terrorist attacks and supplier–customer relationship termination.

Supplier terrorist attacks and supplier–customer relationship termination.

We use the probit model to estimate the relation between supplier terrorist attacks and supplier–customer relationships. Endf1 equals 1 if the relationship ends in the subsequent one year and 0 otherwise. Endf2 equals 1 if the relationship ends in the subsequent two years and 0 otherwise. If the relationship ends due to the delisting of one partner or continues to the end of our sample period in the subsequent one or two years, Endf1 and Endf2 are set as missing and the corresponding observations are excluded from the regression, respectively. Supplier attack equals 1 if at least one terrorist attack occurs within 50 miles of the supplier headquarters in a year and 0 otherwise. Detailed variable definitions are presented in the E-Companion EC.1 Table A1. Chi-square statistics are in parentheses. ***, **, and * indicate significance at the 1%, 5%, and 10% levels, respectively.

The results regarding the control variables are generally consistent with those in prior literature (e.g., Bauer et al., 2018). Specifically, supplier–customer relationships with lower percentages of supplier sales to customers, higher market shares of suppliers or lower market shares of customers, shorter lengths of tenure, higher R&D investments of suppliers or customers, longer histories in Compustat of suppliers or customers, smaller firm sizes of suppliers or customers, and nonpositive free cash flows of suppliers or customers are more likely to end in the subsequent two years.

Given that we observe no significant impact of terrorist attacks on relationship termination in the subsequent year, we hereafter focus on relationship termination within the subsequent two years to conduct robustness checks and further analyses.

In the E-Companion EC.3, we conduct several tests using alternative samples, alternative terrorist attack measures, and alternative empirical model specifications to check the robustness of our baseline results. Our results survive all the robustness tests.

DiD Analyses

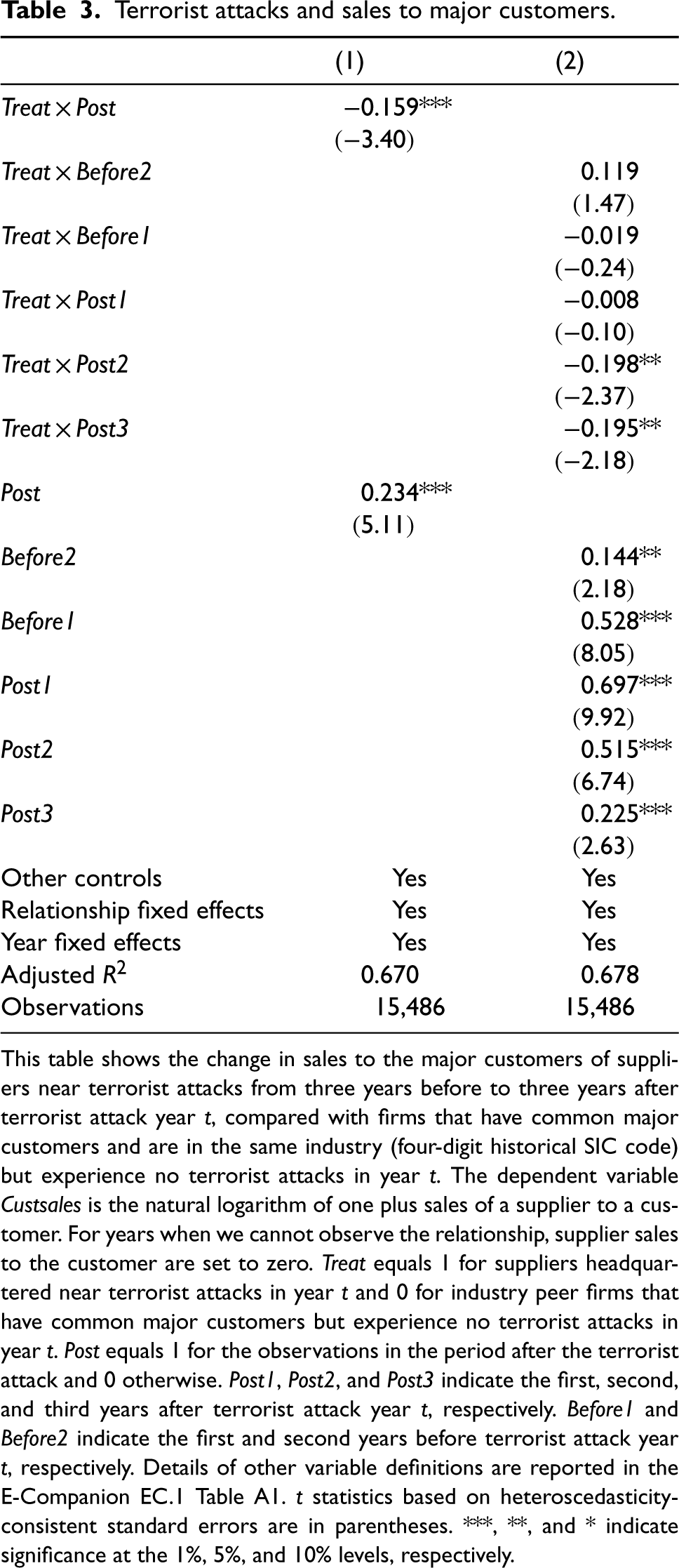

Relationship termination is the most severe disruption to supplier–customer relationships. Major customers could not totally end the trading relationship but rather shift part of their purchases from the suppliers near terrorist attacks to other firms. In this subsection, we conduct DiD tests to explore the impact of terrorist attacks on the sales of nearby suppliers to their major customers. The treatment group includes the relationships between the suppliers located near terrorist attacks and their major customers. The control group includes the supplier–customer relationships in which the suppliers belong to the same industry (four-digit historical SIC codes) and share the same major customers as the treated suppliers. 12 We then examine the change in supplier sales to the customer in the period from three years before to three years after the terrorist attack year (with the attack year excluded). The dependent variable Custsales is the natural logarithm of one plus sales of a supplier to a customer. Supplier sales to the customer are set to zero if a given supplier–customer relationship disappears in Compustat. 13 Treat equals 1 for the relationships in the treatment group and 0 otherwise. Post equals 1 for the observations in the period after the terrorist attack and 0 otherwise. We control for the same supplier- and customer-specific variables as in Model (1) and include both the relationship and year fixed effects.

Column (1) in Table 3 presents the results. The coefficient on Treat × Post of interest is significantly negative (p < 0.01), indicating that the sales of the suppliers near terrorist attacks to their major customers experience a significant decline compared with those of their counterparts following terrorist attacks. The success of the DiD approach hinges on the parallel trends assumption, which states that in the absence of treatment, the DiD estimate should be insignificant. In Column (2), we estimate a dynamic DiD model by decomposing Post into five dummies for each year during the event period. That is, Post1, Post2, and Post3 indicate the first, second, and third years after a terrorist attack, respectively, whereas Before1 and Before2 indicate the first and second years before the attack, respectively. The third year before the terrorist attack serves as the benchmark year.

Terrorist attacks and sales to major customers.

Terrorist attacks and sales to major customers.

This table shows the change in sales to the major customers of suppliers near terrorist attacks from three years before to three years after terrorist attack year t, compared with firms that have common major customers and are in the same industry (four-digit historical SIC code) but experience no terrorist attacks in year t. The dependent variable Custsales is the natural logarithm of one plus sales of a supplier to a customer. For years when we cannot observe the relationship, supplier sales to the customer are set to zero. Treat equals 1 for suppliers headquartered near terrorist attacks in year t and 0 for industry peer firms that have common major customers but experience no terrorist attacks in year t. Post equals 1 for the observations in the period after the terrorist attack and 0 otherwise. Post1, Post2, and Post3 indicate the first, second, and third years after terrorist attack year t, respectively. Before1 and Before2 indicate the first and second years before terrorist attack year t, respectively. Details of other variable definitions are reported in the E-Companion EC.1 Table A1. t statistics based on heteroscedasticity-consistent standard errors are in parentheses. ***, **, and * indicate significance at the 1%, 5%, and 10% levels, respectively.

The results show that the interactions of Treat with Before1 and Before2 are not significant. By contrast, the interactions of Treat with Post2 and Post3 are statistically negative, although the interaction Treat × Post1 is negative but statistically insignificant. These results suggest that the relative decline in sales of terrorism-affected suppliers to major customers begins from the second year after terrorist attacks, consistent with our results regarding relationship termination in Table 2 that major customers need time to find alternative suppliers and gradually reduce purchases from terrorism-affected suppliers. Figure A1 in the E-Companion EC.4 plots the estimated coefficients for our DiD estimators (i.e., the interactions between Treat and each year dummy) in Column (2) of Table 3 and provides visual support for the validity of the parallel trends assumption as the treatment and control pairs exhibit no significant difference in sales to major customers in the period before terrorist attacks. In sum, our DiD analyses lend support to the causal effect of terrorist attacks near supplier firms on supplier–customer relationship termination.

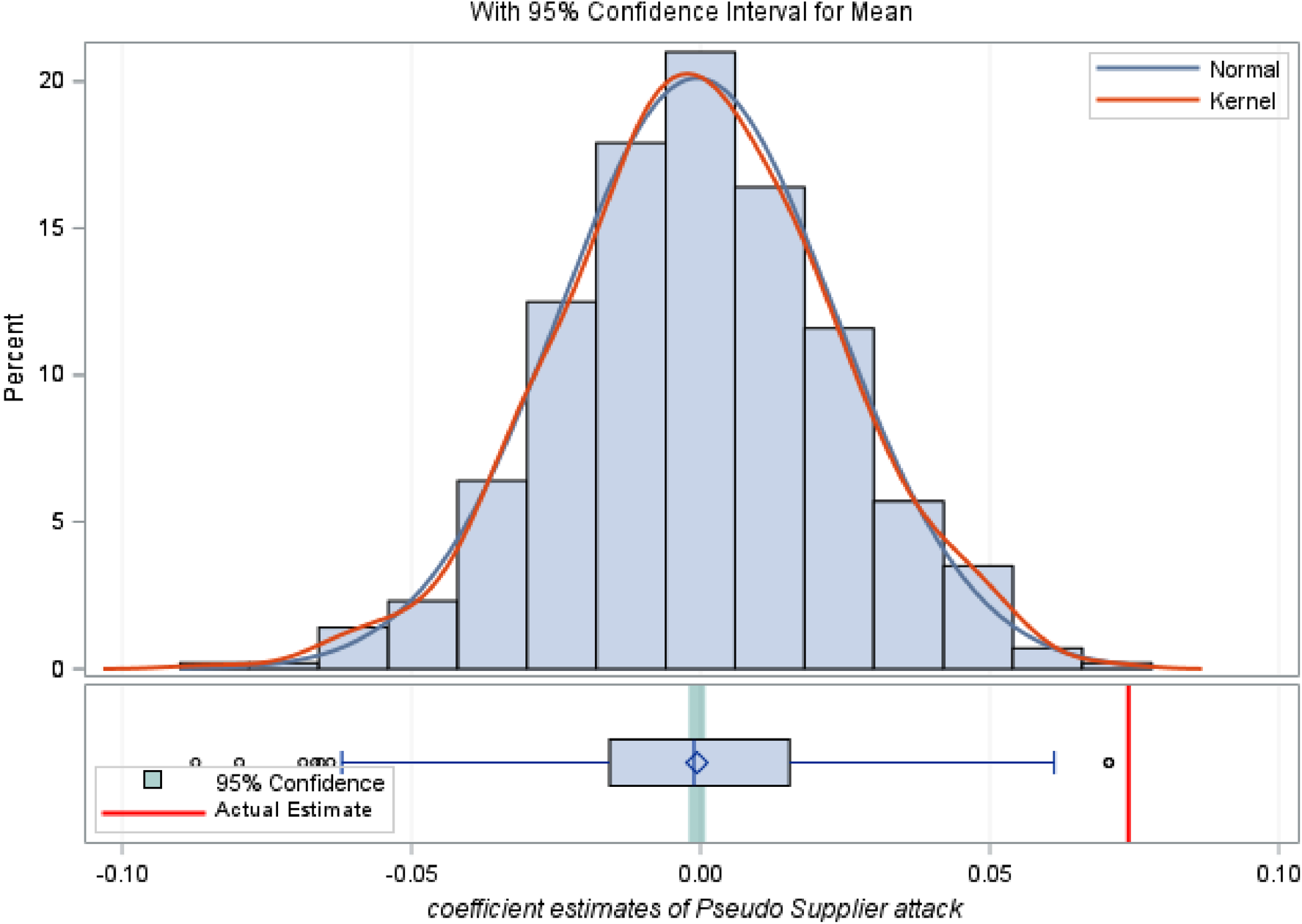

In this subsection, we conduct placebo tests to further address the concern that our baseline results in Table 2 could be spurious. Specifically, we randomly assign the value of Supplier attack to each sample supplier–customer–year (i.e., define terrorist attacks randomly) and generate the variable Pseudo Supplier attack 1000 times. We then rerun Model (1) with Endf2 as the dependent variable by using Pseudo Supplier attack in place of the original variable Supplier attack. Figure 2 illustrates the distribution of the coefficient on Pseudo Supplier attack. The mean value of the coefficient is centered near 0 and insignificant, as shown by the unreported Wilcoxon signed rank test. The vertical line in red indicates the magnitude of the coefficient on Supplier attack in Column (2) of Table 2, which is significantly (p < 0.01) greater than its counterpart using the random sample. Again, the results in Figure 2 support that our main results in Table 2 are not spurious.

Distribution of the coefficient estimates of Pseudo supplier attack. For each supplier–customer pair in our final sample, we randomly assign the value of Supplier attack, generating the variable Pseudo Supplier attack, and rerun Model 1 with Endf2 as a dependent variable using the new variable instead of the original Supplier attack, 1000 times. This figure plots the distribution of the coefficient estimates of Pseudo Supplier attack in our main model with a mean value of −0.0006 and a standard deviation of 0.024. The actual coefficient estimate of Supplier attack in the model of Column (2) of Table 2 is 0.074. The vertical line in red indicates the actual coefficient estimate.

In this section, we attempt to identify the potential reasons underlying the increased likelihood of relationship termination for supplier firms located near terrorist attacks. As discussed, one possible reason is that terrorist attacks directly impair the fundamentals of nearby suppliers, increase their operating risk, and undermine their capability to meet customer demands, leading their major customers to rationally reduce or even end trading with them. The other possible reason is that the negative psychological impact imposed by terrorist attacks near supplier firms induces major customers to overestimate disruption risk on the side of suppliers in terrorism-afflicted areas and in turn withdraw from the supplier–customer relationship, regardless of whether supplier fundamentals are directly harmed by terrorist attacks.

Real Effect of Terrorist Attacks on Supplier Fundamentals

To determine whether terrorist attacks adversely affect supplier fundamentals, we first directly examine the impact of terrorist attacks on future supplier fundamentals, including future performance, operations, and firm risk. We then indirectly investigate whether supplier fundamentals are expected to be impaired by terrorist attacks in the eyes of key market participants such as investors and financial analysts.

Terrorist Attacks and Supplier Fundamentals

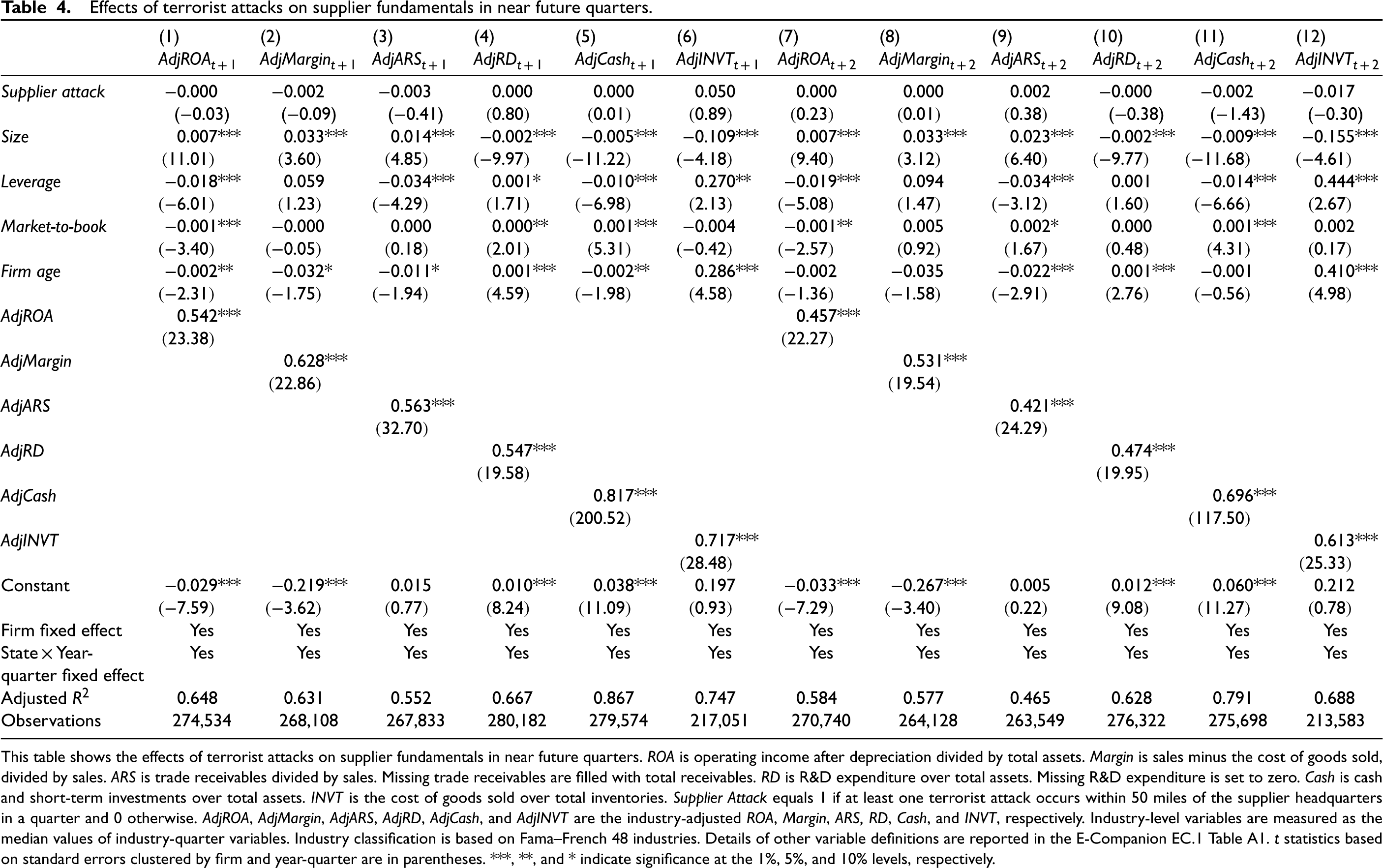

In Table 4, we examine the effect of terrorist attacks on the future performance and operations of suppliers located near terrorist attacks. We capture supplier performance using return on assets (ROA, operating income after depreciation over total assets) and profit margin (Margin, net sales minus cost of goods sold, divided by net sales). We capture supplier operations using trade credit provision (ARS, trade receivables divided by sales), R&D investment (RD, R&D expenditure over total assets), cash holdings (Cash, cash and short-term investments over total assets), and inventory turnover (INVT, cost of goods sold over total inventories). We use quarterly data to detect the direct effect of terrorist attacks. Each of the performance and operational measures is adjusted for industry effect by excluding the median values in each industry quarter. We control for firm size, leverage, market-to-book ratio, firm age, and performance/operational measures in quarter t to address the persistence of firm performance or operating policies, in addition to firm and state interactions with year–quarter fixed effects. Detailed variable definitions are presented in the E-Companion EC.1 Table A1. Columns (1)–(6) of Table 4 report the results for supplier performance/operations in quarter t + 1 and Columns (7)–(12) report the results for supplier performance/operations in quarter t + 2. The coefficient on Supplier attack is never statistically significant in any of the regressions. Therefore, we do not find evidence that terrorist attacks adversely affect the performance or operations of nearby suppliers in the subsequent quarter(s) after terrorist attacks.

Effects of terrorist attacks on supplier fundamentals in near future quarters.

Effects of terrorist attacks on supplier fundamentals in near future quarters.

This table shows the effects of terrorist attacks on supplier fundamentals in near future quarters. ROA is operating income after depreciation divided by total assets. Margin is sales minus the cost of goods sold, divided by sales. ARS is trade receivables divided by sales. Missing trade receivables are filled with total receivables. RD is R&D expenditure over total assets. Missing R&D expenditure is set to zero. Cash is cash and short-term investments over total assets. INVT is the cost of goods sold over total inventories. Supplier Attack equals 1 if at least one terrorist attack occurs within 50 miles of the supplier headquarters in a quarter and 0 otherwise. AdjROA, AdjMargin, AdjARS, AdjRD, AdjCash, and AdjINVT are the industry-adjusted ROA, Margin, ARS, RD, Cash, and INVT, respectively. Industry-level variables are measured as the median values of industry-quarter variables. Industry classification is based on Fama–French 48 industries. Details of other variable definitions are reported in the E-Companion EC.1 Table A1. t statistics based on standard errors clustered by firm and year-quarter are in parentheses. ***, **, and * indicate significance at the 1%, 5%, and 10% levels, respectively.

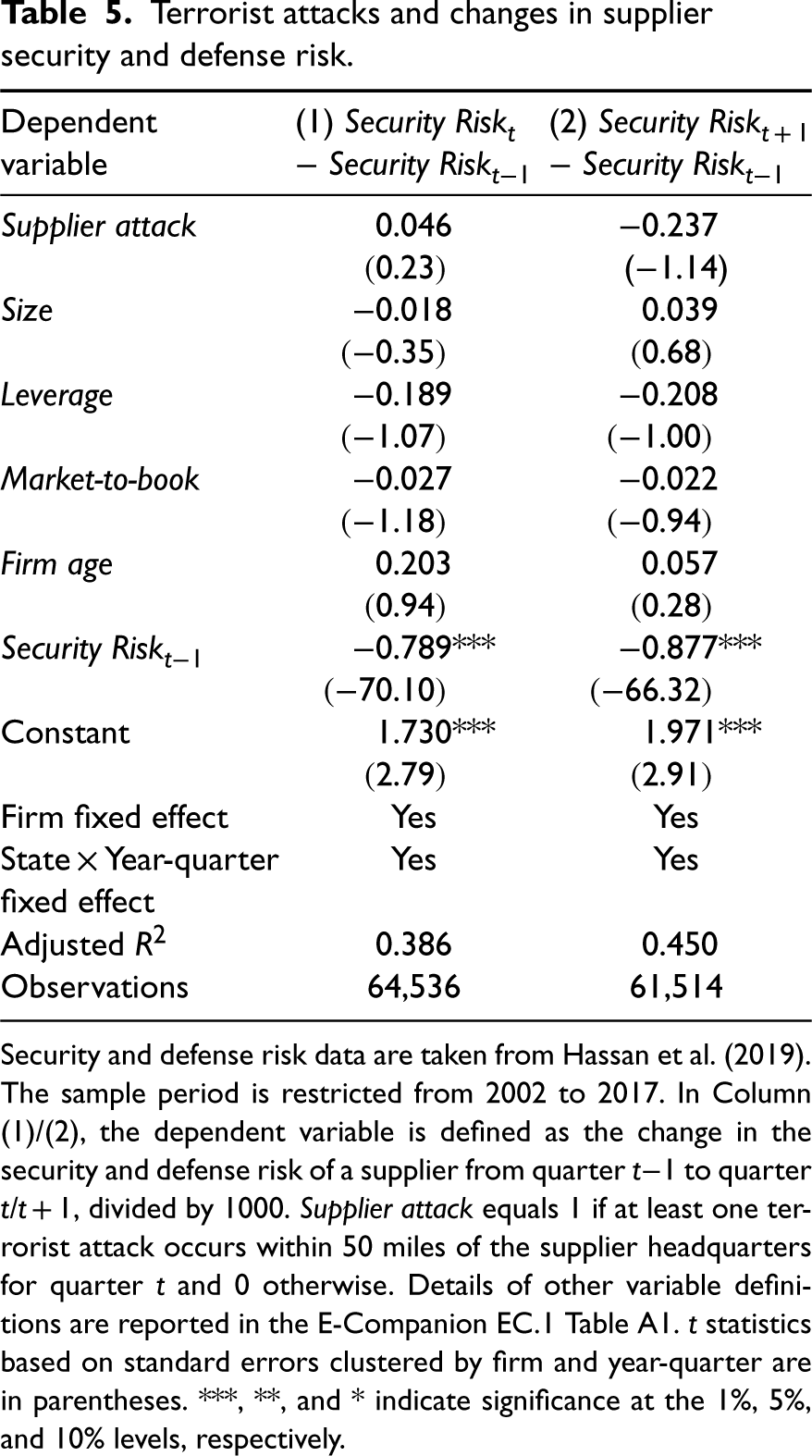

In Table 5, we investigate whether terrorist attacks increase the firm risk of nearby suppliers. We focus on firm security and defense risk, which is closely related to terrorist attacks. We use firm security and defense risk data constructed by Hassan et al. (2019), who measure the risk by calculating the share of conversation in quarterly earnings conference calls that center on security and defense risk. 14 Given that the security and defense risk data begin in 2002, we restrict our sample period from 2002 to 2017. In Column (1)/(2), the dependent variable is defined as the change in a firm's security and defense risk from quarter t−1 to quarter t/t + 1, divided by 1000. Consistent with the analyses in Table 4, we control for firm size, leverage, market-to-book ratio, firm age, and firm security and defense risk in quarter t−1. The coefficient on Supplier attack is insignificant in both regressions, suggesting that terrorist attacks have little effect on nearby suppliers’ security and defense risk.

Terrorist attacks and changes in supplier security and defense risk.

Security and defense risk data are taken from Hassan et al. (2019). The sample period is restricted from 2002 to 2017. In Column (1)/(2), the dependent variable is defined as the change in the security and defense risk of a supplier from quarter t−1 to quarter t/t + 1, divided by 1000. Supplier attack equals 1 if at least one terrorist attack occurs within 50 miles of the supplier headquarters for quarter t and 0 otherwise. Details of other variable definitions are reported in the E-Companion EC.1 Table A1. t statistics based on standard errors clustered by firm and year-quarter are in parentheses. ***, **, and * indicate significance at the 1%, 5%, and 10% levels, respectively.

Taken together, we find no evidence that terrorist attacks adversely affect the fundamentals of suppliers located close to attacks in the near future. 15 Therefore, it is unlikely that terrorist attacks’ immediate harm to supplier fundamentals results in supplier–customer relationship termination.

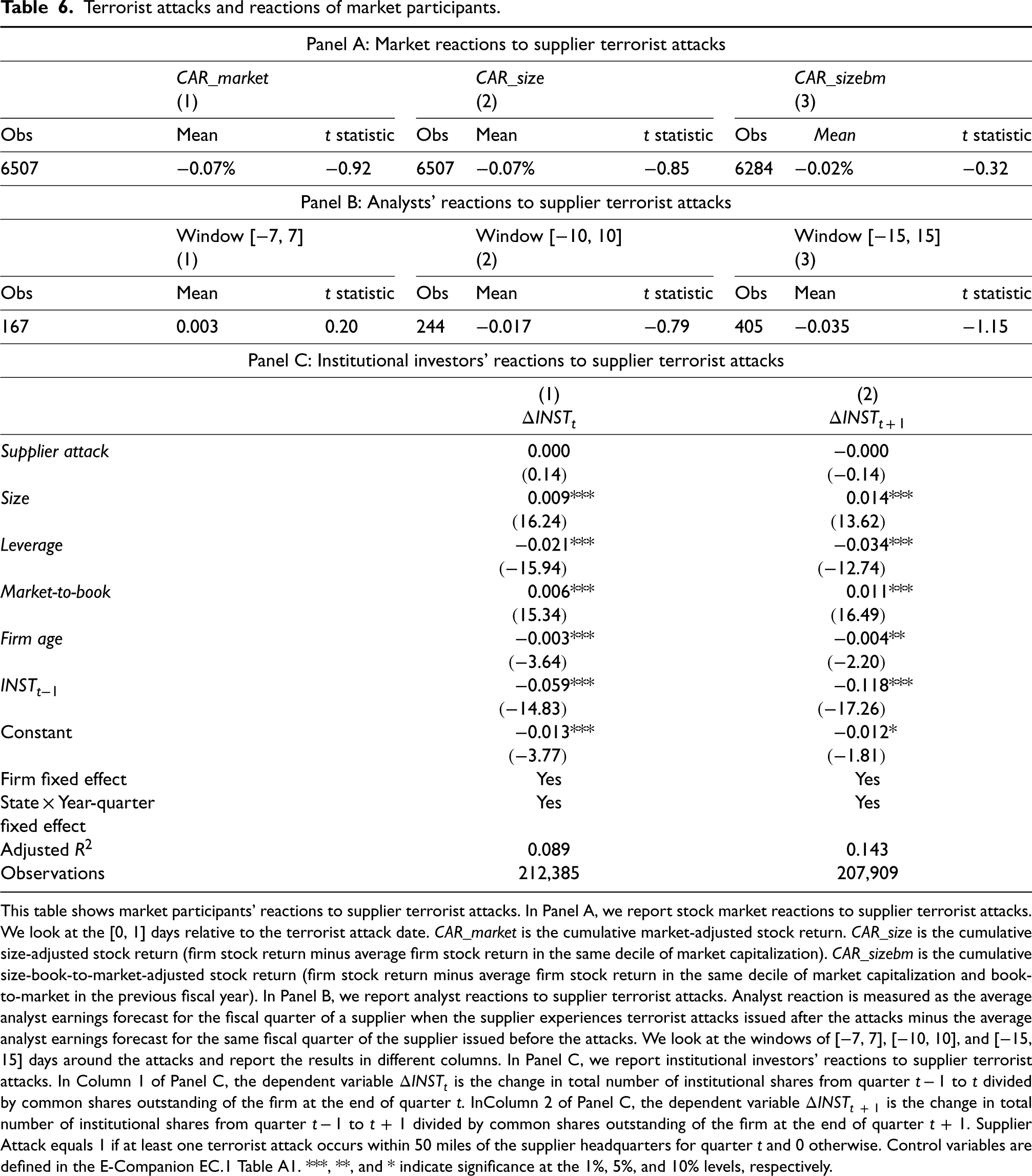

In Table 6, we examine whether terrorist attacks are expected to harm supplier fundamentals in the eyes of key market participants (i.e., investors and financial analysts). In Panel A, we examine suppliers’ market reactions in the window of [0, 1] days relative to the terrorist attack date. We measure market reactions using cumulative market-adjusted stock returns (CAR_market), cumulative size-adjusted stock returns (CAR_size), and cumulative size-book-to-market-adjusted stock returns (CAR_sizebm). The detailed variable definitions are reported in the E-Companion EC.1 Table A1. None of the suppliers’ market reaction measures are significantly different from zero, suggesting that general market investors do not believe that nearby terrorist attacks will significantly affect supplier fundamentals.

Terrorist attacks and reactions of market participants.

Terrorist attacks and reactions of market participants.

This table shows market participants' reactions to supplier terrorist attacks. In Panel A, we report stock market reactions to supplier terrorist attacks. We look at the [0, 1] days relative to the terrorist attack date. CAR_market is the cumulative market-adjusted stock return. CAR_size is the cumulative size-adjusted stock return (firm stock return minus average firm stock return in the same decile of market capitalization). CAR_sizebm is the cumulative size-book-to-market-adjusted stock return (firm stock return minus average firm stock return in the same decile of market capitalization and book-to-market in the previous fiscal year). In Panel B, we report analyst reactions to supplier terrorist attacks. Analyst reaction is measured as the average analyst earnings forecast for the fiscal quarter of a supplier when the supplier experiences terrorist attacks issued after the attacks minus the average analyst earnings forecast for the same fiscal quarter of the supplier issued before the attacks. We look at the windows of [−7, 7], [−10, 10], and [−15, 15] days around the attacks and report the results in different columns. In Panel C, we report institutional investors' reactions to supplier terrorist attacks. In Column 1 of Panel C, the dependent variable ΔINSTt is the change in total number of institutional shares from quarter t − 1 to t divided by common shares outstanding of the firm at the end of quarter t. InColumn 2 of Panel C, the dependent variable ΔINSTt + 1 is the change in total number of institutional shares from quarter t − 1 to t + 1 divided by common shares outstanding of the firm at the end of quarter t + 1. Supplier Attack equals 1 if at least one terrorist attack occurs within 50 miles of the supplier headquarters for quarter t and 0 otherwise. Control variables are defined in the E-Companion EC.1 Table A1. ***, **, and * indicate significance at the 1%, 5%, and 10% levels, respectively.

In Panel B, we examine the reactions of financial analysts to terrorist attacks near supplier firm headquarters. Specifically, we focus on the changes in analyst earnings forecasts of terrorism-afflicted suppliers in the window of [−7, 7] around the attack date. These changes are measured as the average analyst earnings forecast for the fiscal quarter of a terrorist attack issued in the window of [0, 7] days minus the average analyst earnings forecast for the same fiscal quarter issued in the window of [−7, −1] days relative to the terrorist attack date. Similarly, we measure analyst reactions in the windows of [−10, 10] and [−15, 15] days relative to the terrorist attack date. None of the analyst reaction measures is significantly different from zero, suggesting that analysts do not expect that nearby terrorist attacks will immediately affect supplier fundamentals.

In Panel C, we examine institutional investors’ reactions to terrorist attacks near supplier firm headquarters. We construct two variables to capture institutional investors’ reactions: ΔINSTt in Column (1) and ΔINSTt + 1 in Column (2). The two variables are calculated as the change in institutional shareholdings of suppliers from quarter t−1 to quarter t and from quarter t−1 to quarter t + 1, respectively. We control for firm size, leverage, market-to-book ratio, firm age, and the institutional ownership of suppliers in quarter t−1. The coefficient on Supplier attack is not statistically significant in either regression, suggesting that institutional investors do not expect terrorist attacks to significantly affect the nearby suppliers’ fundamentals as well.

Next, we examine whether customers’ perception of supply chain risk can explain our main results. First, we investigate whether the positive association between terrorist attacks near suppliers and supplier–customer relationship termination varies with customer risk tolerance and supplier information asymmetry. Second, we explore whether customers are more likely to express their concerns about supplier terrorism risk in response to terrorist attacks near their suppliers’ headquarters. Third, we examine whether terrorist attacks affect customers’ selection of new suppliers. Finally, we test whether the relationships that end in the year or within two years after terrorist attacks near suppliers are more likely to reemerge in the near future.

Customer Risk Tolerance

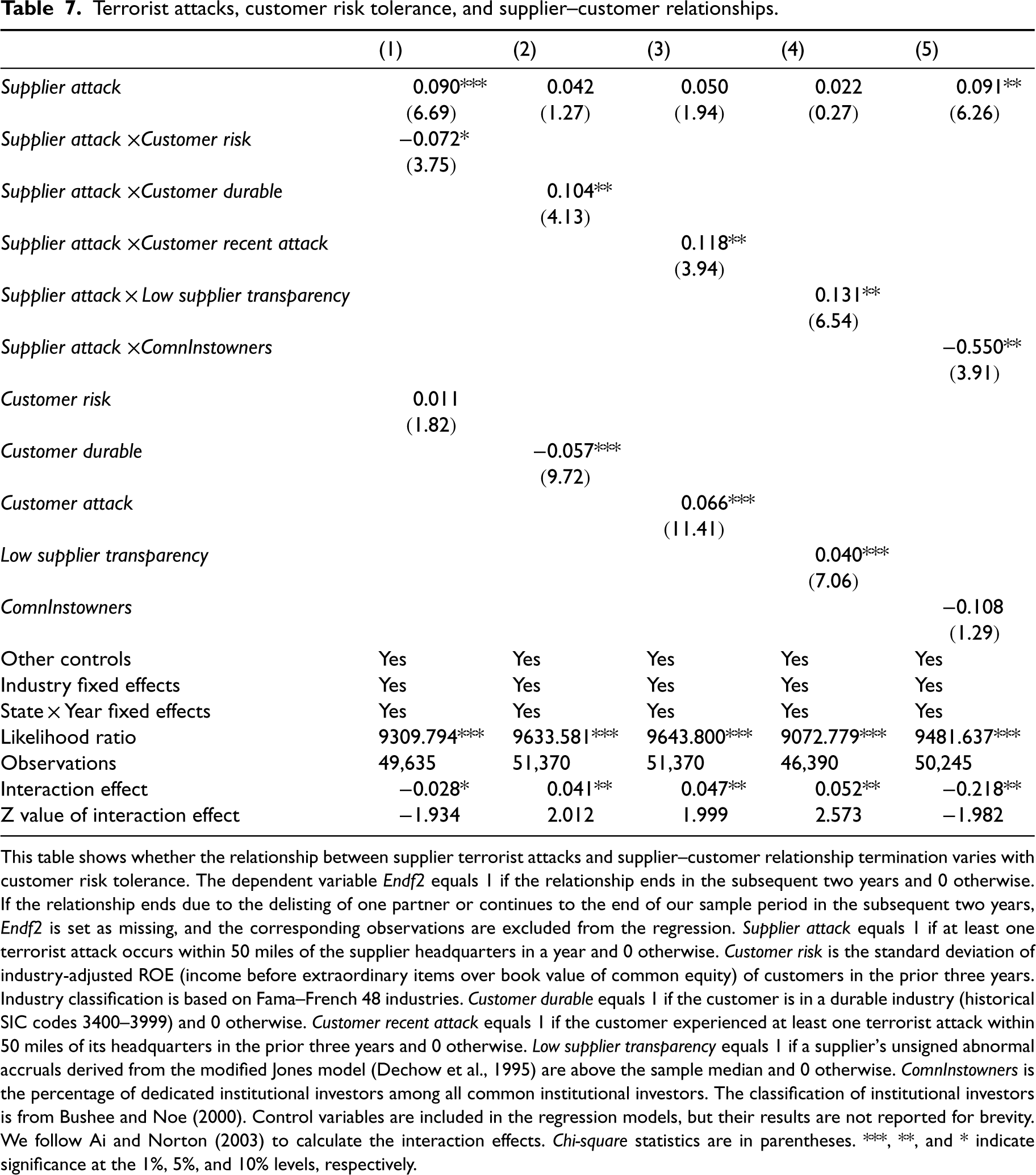

Customer firms that are more risk-averse tend to take less risk. Following prior research (e.g., Ferris et al., 2017), we use the volatility of ROE to measure the aggregate level of a customer's risk-taking. Specifically, we define Customer risk as the standard deviation of a customer's industry-adjusted ROE (income before extraordinary items over book value of common equity) in the prior three years. We then estimate Model (1) by further including Customer risk and the interaction between Customer risk and Supplier attack. Column (1) of Table 7 reports the results. We follow Ai and Norton (2003) to calculate the magnitude of the interaction effect between Supplier attack and Customer risk 16 and report it in the bottom lines. The interaction effect is significantly negative (p < 0.1), suggesting that the effect of terrorist attacks on supplier–customer relationship termination is reduced for less risk-averse customers.

Terrorist attacks, customer risk tolerance, and supplier–customer relationships.

Terrorist attacks, customer risk tolerance, and supplier–customer relationships.

This table shows whether the relationship between supplier terrorist attacks and supplier–customer relationship termination varies with customer risk tolerance. The dependent variable Endf2 equals 1 if the relationship ends in the subsequent two years and 0 otherwise. If the relationship ends due to the delisting of one partner or continues to the end of our sample period in the subsequent two years, Endf2 is set as missing, and the corresponding observations are excluded from the regression. Supplier attack equals 1 if at least one terrorist attack occurs within 50 miles of the supplier headquarters in a year and 0 otherwise. Customer risk is the standard deviation of industry-adjusted ROE (income before extraordinary items over book value of common equity) of customers in the prior three years. Industry classification is based on Fama–French 48 industries. Customer durable equals 1 if the customer is in a durable industry (historical SIC codes 3400–3999) and 0 otherwise. Customer recent attack equals 1 if the customer experienced at least one terrorist attack within 50 miles of its headquarters in the prior three years and 0 otherwise. Low supplier transparency equals 1 if a supplier's unsigned abnormal accruals derived from the modified Jones model (Dechow et al., 1995) are above the sample median and 0 otherwise. ComnInstowners is the percentage of dedicated institutional investors among all common institutional investors. The classification of institutional investors is from Bushee and Noe (2000). Control variables are included in the regression models, but their results are not reported for brevity. We follow Ai and Norton (2003) to calculate the interaction effects. Chi-square statistics are in parentheses. ***, **, and * indicate significance at the 1%, 5%, and 10% levels, respectively.

Existing literature documents that customer firms in durable industries are more risk-averse due to their greater reliance on the supplier's relationship-specific investment (Banerjee et al., 2008). We thus examine whether the effect of near terrorist attacks on supplier–customer relationship termination is more pronounced when major customers are in durable industries. We construct an indicator Customer durable equal to 1 if the customer is in the durable industries (historical SIC codes 3400–3999) and 0 otherwise. We then estimate Model (1) by further including Customer durable and the interaction between Customer durable and Supplier attack. As shown in Column 2 of Table 7, the interaction effect between Supplier attack and Customer durable is significantly positive (p < 0.05), suggesting that the increased likelihood of the supplier losing major customers following nearby terrorist attacks is more pronounced when major customers belong to durable industries.

Finally, prior psychology research suggests that people who experience fear, such as those who are exposed to terrorist attacks, exhibit more pessimistic sentiment and overestimate risk assessments (e.g., Lerner and Keltner, 2001, Lerner et al., 2003). Customer managers with recent in-person experience of terrorist attacks are more likely to be risk-averse and overreact to terrorist attacks near their supplier headquarters. We thus introduce an indicator Customer recent attack equal to 1 if the customer experienced at least one terrorist attack within 50 miles of its headquarters in the prior three years and 0 otherwise. We then estimate Model (1) by further including Customer recent attack and the interaction between Customer recent attack and Supplier attack. Column 3 of Table 7 reports the results. The interaction effect between Supplier attack and Customer recent attack is significantly positive (p < 0.05), suggesting that the effect of terrorist attacks near suppliers on supplier–customer relationship termination is more pronounced when major customers ever experienced terrorist attacks around their headquarters in the prior three years.

Taken together, the results in Table 7 indicate that the increased likelihood of the supplier losing major customers following nearby terrorist attacks is more pronounced when major customers or customer managers are more risk-averse, consistent with the notion that customers’ intensified perception of supply chain risk induced by terrorist attacks near supplier headquarters drives supplier–customer relationship termination. 17

Existing literature highlights the importance of information exchange between trading partners in mitigating supply chain risk (Park et al., 2013; Samvedi and Jain, 2012; Stekelorum et al., 2022). Lower information asymmetry between suppliers and customers makes it easier for customers to track suppliers’ financial status and accurately evaluate supply chain risk. Efficient information exchange can be achieved through the suppliers’ high-quality public disclosures, especially financial reporting, the suppliers’ private communication with their major customers (Bauer et al., 2018; Costello, 2013; Dasgupta et al., 2021), or both, thereby preventing major customers from misperceiving supply chain risk caused by terrorist attacks near the suppliers. In Column (4) of Table 7, we examine whether the effect of terrorist attacks near the suppliers on supplier–customer relationship termination varies with the suppliers’ information asymmetry captured by accrual quality. We measure accrual quality as unsigned abnormal accruals derived from the modified Jones model (Dechow et al., 1995) and construct an indicator Low Supplier Transparency equal to 1 if the suppliers’ unsigned abnormal accruals are above the sample median and 0 otherwise. We then estimate Model (1) by further including Low supplier transparency and the interaction between Low supplier transparency and Supplier attack. The interaction effect between Supplier attack and Low supplier transparency is significantly positive (p < 0.05), suggesting that the effect of terrorist attacks near suppliers on supplier–customer relationship termination is more pronounced when the suppliers’ information asymmetry is higher. 18

In addition to relying on suppliers’ public disclosures, major customers can also communicate with suppliers through private channels (Bushee et al., 2020). Given that direct communication between suppliers and customers is not observable, we rely on the presence of common dedicated institutional investors between the supplier and customer to capture private communication between the two partners (Bushee and Noe, 2000; Cheung et al., 2020). Specifically, we define the variable ComnInstowners as the percentage of dedicated institutional investors among all institutional investors that simultaneously invest in the supplier and customer. The classification of institutional investors is from Bushee and Noe (2000). We then estimate Model (1) by further including ComnInstowners and the interaction between ComnInstowners and Supplier attack. Column (5) of Table 7 reports the results. The interaction effect between Supplier attack and ComnInstowners is significantly negative (p < 0.05), suggesting that common dedicated institutional investors promote private communication between suppliers and customers and discourage the customers from overestimating supply chain risk arising from terrorist attacks near the suppliers.

Customers’ Expression of Concerns About Supplier Terrorism Risk

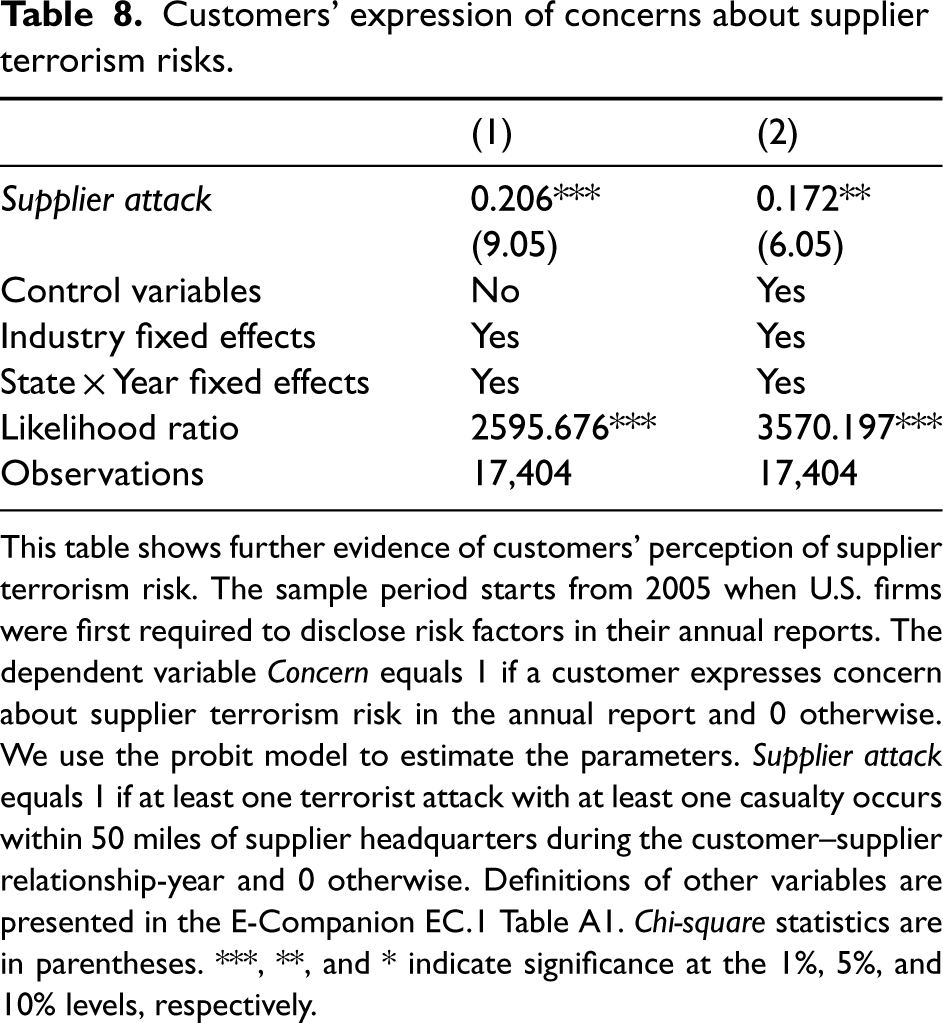

In this subsection, we directly examine whether customers are more likely to express their concerns about supplier terrorism-related risk when terrorist attacks occur near their supplier headquarters. Since 2005, the SEC has mandated that public firms disclose risk factors in annual reports. 19 Our sample period thus begins in 2005 for risk disclosure analyses. To identify whether customers express their concerns about supplier terrorism risk, we first search the sentences in the customers’ 10-K or 20-F filings that include any possible combinations of the keywords related to terrorist attacks (i.e., terror, terrorist, and terrorism) with the keywords related to suppliers (i.e., suppliers, vendors, third parties, third-party, interconnected company, supply, supplies, provider, purchase, receive, deliver, obtain, import, raw materials, feedstocks, and collaborators). 20 We then manually read each output sentence to ensure that the sentences actually mention the customers’ concerns about supplier terrorism risk. For example, in its 2006 10-K filing, Wyeth mentions supplier terrorism risk by stating that “a number of factors could cause production interruptions at our facilities or the facilities of our third party providers, including equipment malfunctions, labor problems, natural disasters, regulatory action, power outages or terrorist activities.” 21 The E-Companion EC.5 Table A5 provides additional examples of the customers’ concerns about supplier terrorism risk.

We next construct the dependent variable, Concern, which is equal to 1 if a customer mentions supplier terrorism risk in its annual filings and 0 otherwise. We estimate a probit model by including Supplier attack along with(out) all control variables in Model (1). Table 8 reports the results. The coefficient on Supplier attack is positive and statistically significant in both regressions with (p < 0.05) and without control variables (p < 0.01), suggesting that customers are more likely to express their concerns about supplier terrorism risk when terrorist attacks occur near their suppliers. These findings provide direct evidence that major customers do care about supplier terrorism risk and could thus take actions, such as switching to alternative suppliers, to avoid the potential adverse impact of terrorist attacks on their suppliers.

Customers’ expression of concerns about supplier terrorism risks.

Customers’ expression of concerns about supplier terrorism risks.

This table shows further evidence of customers’ perception of supplier terrorism risk. The sample period starts from 2005 when U.S. firms were first required to disclose risk factors in their annual reports. The dependent variable Concern equals 1 if a customer expresses concern about supplier terrorism risk in the annual report and 0 otherwise. We use the probit model to estimate the parameters. Supplier attack equals 1 if at least one terrorist attack with at least one casualty occurs within 50 miles of supplier headquarters during the customer–supplier relationship-year and 0 otherwise. Definitions of other variables are presented in the E-Companion EC.1 Table A1. Chi-square statistics are in parentheses. ***, **, and * indicate significance at the 1%, 5%, and 10% levels, respectively.

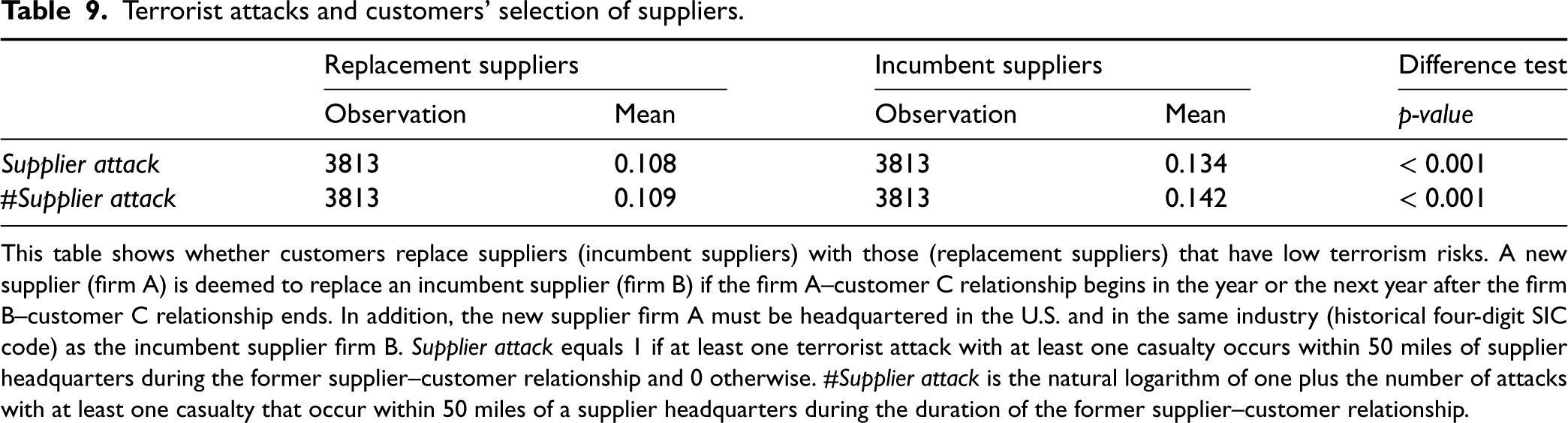

Next, we examine whether terrorist attacks affect customers’ selection of new suppliers. If terrorist attacks near supplier headquarters heighten the customers’ perception of supply chain risk, thereby inducing them to end their relationships with terrorism-affected suppliers, the customers will select new suppliers with lower terrorism risk as replacements. To provide a whole picture of whether customers incorporate supplier terrorism risk into their choices of new suppliers, we first determine all incumbent suppliers that end relationships with their major customers during our sample period and identify the new suppliers that likely replace the incumbent suppliers. We require the new suppliers to be in the same industry (historical four-digit SIC code) as the incumbent suppliers and establish a relationship with the same major customers in the year or the next year of the incumbent relationship termination. We then compare the occurrence and the number of terrorist attacks within 50 miles of firm headquarters between the incumbent and replacement suppliers over the duration of the incumbent relationships.

Table 9 shows that the occurrence and the number of terrorist attacks are significantly higher among the incumbent suppliers than among their replacement suppliers. Further sign tests (unreported) show that the likelihood of incumbent suppliers with terrorism experience being replaced by new suppliers without terrorism experience is significantly greater (p < 0.01) than that of the reverse incidence. These results support that customers consider supplier terrorism risk and tend to switch from suppliers with higher terrorism risk to other firms with lower terrorism risk.

Terrorist attacks and customers’ selection of suppliers.

Terrorist attacks and customers’ selection of suppliers.

This table shows whether customers replace suppliers (incumbent suppliers) with those (replacement suppliers) that have low terrorism risks. A new supplier (firm A) is deemed to replace an incumbent supplier (firm B) if the firm A–customer C relationship begins in the year or the next year after the firm B–customer C relationship ends. In addition, the new supplier firm A must be headquartered in the U.S. and in the same industry (historical four-digit SIC code) as the incumbent supplier firm B. Supplier attack equals 1 if at least one terrorist attack with at least one casualty occurs within 50 miles of supplier headquarters during the former supplier–customer relationship and 0 otherwise. #Supplier attack is the natural logarithm of one plus the number of attacks with at least one casualty that occur within 50 miles of a supplier headquarters during the duration of the former supplier–customer relationship.

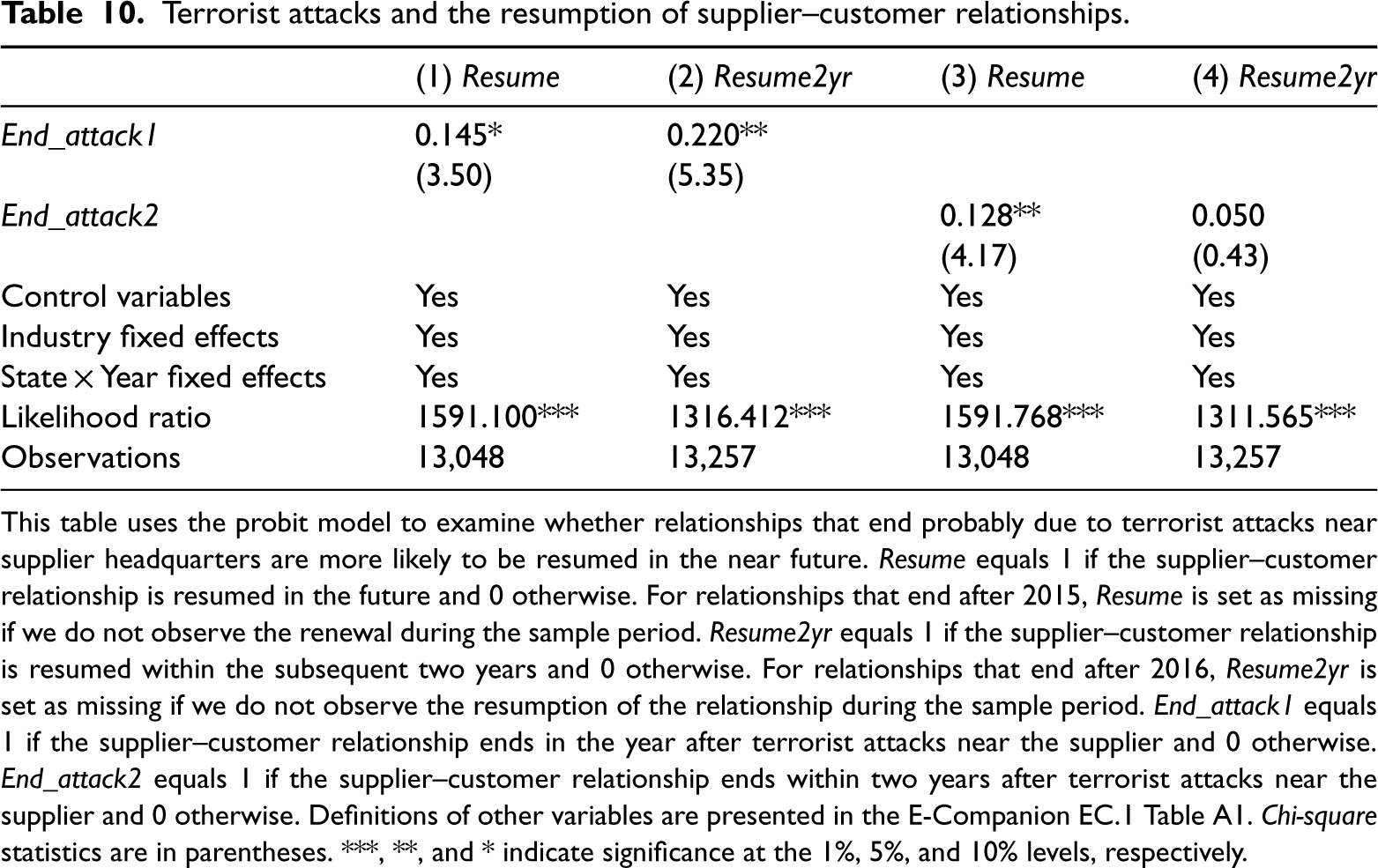

To provide further evidence that the effect of terrorist attacks near suppliers on supplier–customer relationship termination is mainly driven by customers’ overreaction to terrorism-induced supply chain risk, we examine whether the relationships that end in the year/within two years after terrorist attacks near suppliers are more likely to reemerge in the near future in Table 10. Specifically, we focus on all supplier–customer relationships that ever end during our sample period. In Columns (1)–(2)/(3)–(4), we construct the variable End_attack1/End_attack2, which is equal to 1 if the supplier–customer relationship ends in the year/within two years after terrorist attacks near the supplier and 0 otherwise. In Columns (1) and (3), we define the dependent variable Resume as an indicator equal to 1 if a supplier–customer relationship reemerges after termination and 0 otherwise. For the relationships that end after 2015, Resume is set as missing if we do not observe the resumption of the relationship during the sample period. 22 In Columns (2) and (4), we define the dependent variable Resume2yr as equal to 1 if the supplier–customer relationship is resumed within two years following termination and 0 otherwise. For relationships that end after 2016, Resume2yr is set as missing if we do not observe the resumption of the relationship during the sample period.

Terrorist attacks and the resumption of supplier–customer relationships.

Terrorist attacks and the resumption of supplier–customer relationships.

This table uses the probit model to examine whether relationships that end probably due to terrorist attacks near supplier headquarters are more likely to be resumed in the near future. Resume equals 1 if the supplier–customer relationship is resumed in the future and 0 otherwise. For relationships that end after 2015, Resume is set as missing if we do not observe the renewal during the sample period. Resume2yr equals 1 if the supplier–customer relationship is resumed within the subsequent two years and 0 otherwise. For relationships that end after 2016, Resume2yr is set as missing if we do not observe the resumption of the relationship during the sample period. End_attack1 equals 1 if the supplier–customer relationship ends in the year after terrorist attacks near the supplier and 0 otherwise. End_attack2 equals 1 if the supplier–customer relationship ends within two years after terrorist attacks near the supplier and 0 otherwise. Definitions of other variables are presented in the E-Companion EC.1 Table A1. Chi-square statistics are in parentheses. ***, **, and * indicate significance at the 1%, 5%, and 10% levels, respectively.

The coefficient on End_attack1 is positive and significant at levels better than 0.1 in the first two columns, suggesting that the relationships ending just following terrorist attacks near suppliers are more likely to be resumed in the future. In comparison, the coefficient on End_attack2 is positive in both regressions but statistically significant (p < 0.05) only in Column (3), suggesting that the relationships which end within two years following terrorist attacks near suppliers are more likely to be resumed in the longer future but not within two years following the termination. The results in Table 10 combined together also indicate that it takes a longer time for major customers to revert back to original suppliers if they take longer time (more than one year) to find alternate suppliers. Overall, these findings are in line with the conjecture that customers overreact to terrorist attacks near their suppliers by quitting business relationships upon attack occurrence but switch back to terrorism-affected suppliers after they learn about little impairment to supplier fundamentals actually caused by terrorist attacks in later periods.

We also perform additional tests to examine the variation in the association between terrorist attacks near suppliers and supplier–customer relationship termination. We provide detailed discussions on these additional cross-sectional tests in the E-Companion EC.6. As shown in Table A6, the effect of terrorist attacks near suppliers on trading relationship termination is strengthened for relationships with a higher asymmetric dependence of the supplier on the customer and mitigated when major customers face higher switching costs and suppliers increase trade credit provision following attack events. We also find the effect of terrorist attacks near suppliers is more pronounced in the period after the 9/11 attack, which significantly changes the attitudes and behaviors of U.S. citizens (Murphy et al., 2004) and intensifies concerns about terrorism-induced security risk and supply chain disruptions (Stecke and Kumar, 2009).

Conclusion

This study investigates the impact of terrorist attacks around supplier headquarters on supplier–customer relationships. We find that supplier firms located near terrorist attacks are more likely to lose major customers in the period following terrorist attacks. We find no evidence that terrorist attacks directly impair the fundamentals of nearby supplier firms and in turn result in a higher likelihood of relationship termination with their major customers. Nevertheless, we find evidence consistent with the notion that customers tend to overestimate supply chain risk induced by terrorist attacks near their suppliers and thereby unfavorably adjust their trading relationships with their suppliers in terrorism-afflicted areas.

Supplier firms tend to experience a decrease in sales to their major customers and are more likely to be replaced by their rival counterparts with lower terrorism risk in the period following terrorist attacks near their headquarters. Customers are more likely to express their concerns about supplier terrorism risk in the year when terrorist attacks occur near their suppliers. Our additional analyses show that the effect of terrorist attacks near suppliers on supplier–customer relationship termination is more pronounced when customers have higher bargaining power and lower switching costs. The salient 9/11 attack also intensifies customers’ risk perceptions regarding terrorism and further increases the likelihood of ending their relationships with the suppliers near terrorist attacks.

This study contributes to the literature on both the economic consequences of terrorist attacks and the determinants of supplier–customer relationship duration. Our findings provide important implications for supplier firms to take timely actions, such as by improving communication with major customers through public and private channels, to keep their customers from overestimating supply chain risk that could be caused by terrorist attacks near their headquarters.

Supplemental Material

sj-docx-1-pao-10.1177_10591478231224920 - Supplemental material for The Effects of Terrorist Attacks on Supplier–Customer Relationships

Supplemental material, sj-docx-1-pao-10.1177_10591478231224920 for The Effects of Terrorist Attacks on Supplier–Customer Relationships by Weiqiang Tan, Wenming Wang and Wenlan Zhang in Production and Operations Management

Footnotes

Acknowledgments

We thank the department editor Anil Arya, the senior editor, two anonymous referees, Jun Chen, In-Mu Haw, Jian Zhang, and seminar participants at the Education University of Hong Kong and Zhejiang University for their helpful comments and suggestions. All authors have contributed equally to this paper.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Tan thanks the Dean's Research Fund of the Faculty of Liberal Arts and Social Sciences (FLASS/DRF 04724, 04740, CB365) and Departmental Special Project (04807) of Education University of Hong Kong for financial support. Wang thanks financial support from the Key Projects of Philosophy and Social Sciences Research sponsored by Ministry of Education of China (No. 20JZD014), and Zhejiang Provincial Philosophy and Social Science Planning Project (No. 24NDJC123YB). Zhang thanks financial support from the National Natural Science Foundation of China (No. 72272024).

Notes

How to cite this article

Tan W, Wang W and Zhang W (2024) The Effects of Terrorist Attacks on Supplier–Customer Relationships. Production and Operations Management 33(1): 146–165.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.