Abstract

Many individuals worldwide retire financially unprepared. The most evident factor for low retirement savings is due to a lack of retirement planning, especially from an early age. Financial literacy is a key element in navigating the current complex financial landscape, as it enables the individual to effectively manage personal finances and make sound financial decisions regarding earning, consuming, saving, investing, debt management, insurance, mitigating risk, identifying suitable financial sources when needed, and also ultimately saving enough for retirement. Financial education provided by employers is usually voluntary and generally designed as a one-size-fits-all solution. The current methods used to teach financial literacy are effective in accessing financial education, but whether they change financial behaviour that results in leaving individuals better prepared for retirement is not evident. Millennials thrive in a digital environment and prefer a trial-and-error approach when learning takes place. To make financial education more practical and appealing to millennials, programme developers should consider the use of gamified applications portraying real-life events where problems need to be solved and active engagement and immediate feedback, which can promote financial literacy and might change the saving behaviour of the younger generations. Gamification is explored as a potential educational tool that can be used in teaching retirement preparedness and financial literacy in the workplace.

“Through active engagement and immediate feedback, gamification can promote financial literacy and might change the saving behaviour of the younger generations.”

Many individuals worldwide retire financially unprepared. Issues such as societal ageing, fundamental changes within the pension landscape, and a more complex financial environment all contribute to this ongoing phenomenon (Suh, 2022). However, the most evident factor for low retirement savings is due to a lack of retirement planning, especially from an early age (Harlow et al., 2020). There is a definite need for in-depth financial education; however, it is costly and the impact thereof is not always clear (Klapper et al., 2015). Financial education provided by employers is usually voluntary. These workshops are generally designed as a one-size-fits-all, and those who choose to attend them need to relate their current financial situation to the topic of the workshop (Schwartz, 2010). Gamification has emerged as a highly popular method of engaging and retaining specifically the millennial workforce, as it taps into this generation’s natural desire to compete and play. Furthermore, learning can be personalised and the content can be tailored to the employee’s unique needs and preferences (Jain & Dutta, 2019). With the success rate of gamification, it is worth exploring the potential it might have to engage adults in their retirement planning and enhance their related financial knowledge (Bayuk & Altobello, 2019). The objective of this article is to explore the possibility of using gamification as an effective method in teaching retirement preparedness and financial literacy in the workplace. The lack of financial literacy and how that relates to insufficient retirement savings will be discussed. Current methods of teaching financial literacy and the possible reasons why these methods tend to fail will be examined. Lastly, the concept of gamification will be considered a possible way to avoid the retirement crisis.

Lack of Financial Literacy

Financial literacy is the knowledge and understanding of financial concepts and risk and having the ability, motivation, and confidence to apply this knowledge. This enables individuals to make sound decisions in different financial situations and enhance their own and society’s financial well-being (OECD/INFE, 2023). The lack of financial literacy is a critical issue that affects both younger and older individuals and governments around the world (Lusardi, 2019). Financial literacy is a key element in navigating the current complex financial landscape. Financial skills and knowledge enable individuals to effectively manage personal finances and make sound financial decisions regarding earning, consuming, saving, investing, debt management, insurance, mitigating risk, and identifying suitable financial sources when needed (Molchan, 2023). Financial literacy has a positive effect on one’s awareness of post-retirement financial needs, financial product comparison, the shift from present-time bias to future-time bias, and saving for retirement. Financial literacy also contributes to a reduction in financial behavioural biases (Yeh, 2022).

Unfortunately, the most recent international survey of adult financial literacy showed that a significant portion of the population lacks basic financial literacy skills, despite the many financial literacy initiatives around the world. The survey focused on three components of financial literacy: financial knowledge, behaviours, and attitudes. The 40 participating countries and economies showed an average financial literacy score of 60% (a minimum target score of 70% is considered to be financially literate). Only one in every three adults from the participating countries achieved the minimum target score (OECD/INFE, 2023). The shift from companies providing retirement benefits in the form of a defined benefit plan to a defined contribution plan meant that the responsibility has now been placed on the shoulders of the employees to secure their own retirement. Consequently, this means that retirement literacy (knowledge and understanding of complex retirement products), as part of the broader umbrella term of financial literacy, becomes a key competency needed to exercise this responsibility (Eling & Jaenicke, 2023). Financial illiteracy is a strong indicator of the mismanagement of personal finances and a lack of engagement in retirement planning. As a result, individuals may end up with high levels of debt and make poor investment decisions, which may lead to insufficient retirement savings (Lusardi, 2019). Indicators of low levels of financial literacy, such as not keeping a budget, a lack of keeping copies of financial records, and not saving for retirement can have serious consequences for an individual’s personal financial management practices. It may lead to the inability to make correct financial decisions, participate in regular investment programmes, and the tendency to spend more than they earn (Ndou, 2023). Furthermore, financially illiterate individuals may fall victim to phishing scams and financial frauds, facing the risk of losing their hard-earned money (OECD/INFE, 2023). These struggles can lead to high stress and anxiety for individuals who fail to effectively navigate their personal finances (Ohrt et al., 2024). Inadequate retirement planning not only affects the individual but also their families and friends, and, eventually, society as a whole (Topa et al., 2018). Furthermore, the lack of financial literacy can put governments under severe pressure to provide social security to a rapidly increasing retiree population with little or no retirement savings of their own. Individuals need to improve their financial literacy for them to have more control over their financial well-being. This may ultimately lead to a better quality of life and contribute to economic stability (Lusardi, 2019).

Insufficient Retirement Savings

The biggest regret pensioners currently face is not saving for retirement from an earlier age (Sanlam, 2019). Currently, the youngest dominating workforce constitutes millennial employees (born more or less between 1981 and 2000) (Hill, 2017). This generation specifically, should be made aware of the need to plan and avoid making the same mistakes as their predecessors. According to the Financial Perspectives on Aging and Retirement Across the Generations Survey conducted in the United States, results indicated that individuals’ biggest financial priority is being able to pay everyday bills. All generations have probably struggled financially to get started in adulthood. However, millennials are worse off than previous generations due to more time spent in education, ending up with higher student debt, rapidly increasing living expenses, and the fact that they missed out on early career opportunities due to the Great Recession that started in 2007 (Rappaport, 2019). Furthermore, societal ageing contributes to the already significant burden on individuals to save for retirement with most retirees running out of retirement savings on average 10–13 years before they pass away (World Economic Forum, 2019). Society is living longer, and economically active parents have fewer children, which leads to fewer people in employment to support an increasingly ageing society that is dependent on government financial support in retirement (Bodnár & Nerlich, 2022).

For most retirees, government retirement benefits form their income base in retirement and the remainder of retirement expenses are covered by workplace pensions and personal savings (Fidelity, 2020). Saving for retirement over 40 years, contributions of 10%–17% of monthly income (an income replacement rate of 70%) is the suggested guideline for medium-income earners to reach a financially secured and independent retirement. American workers are currently only saving about 6%–8% of their monthly income (Stanford Center on Longevity, 2018). Some of the costliest retirement planning mistakes by retirees, that end up with insufficient retirement savings, are: • Underestimating how long they will live after retirement. • Overestimating investment income. • Not factoring in healthcare costs. • Relying too much on government support (Natixis, 2022).

People are struggling to make ends meet financially, with barely any savings. An unexpected financial event can ultimately push them over the edge, leaving them with nothing left to save for retirement. Thus, developing and implementing a financial plan is crucial to weathering financial storms and securing a financially independent retirement (Exton, 2019).

Current Financial Literacy Methods

There has always been a pressing need to strengthen the financial literacy of individuals and households to help them make sound financial decisions. However, this need has been exacerbated due to the rapid increase in living costs, high inflation, and rising interest rates together with the growing interest in cryptocurrencies, new and alternative forms of financial advice (e.g. financial influencers on social media platforms), and the rising incidence of financial fraud and scams. Digital financial products and services are becoming significantly more popular, which emphasises the need to equip individuals with the necessary financial literacy and digital financial literacy skills to use such products and services safely (OECD/INFE, 2023).

Current financial literacy education and awareness initiatives are incorporated across a variety of platforms, including but not limited to school curricula, websites that provide information and advice regarding investments and savings, interactive advice via telephone, internet, and face-to-face seminars, and workshops that focus on adult financial education. A vast number of online programmes and resources offering financial literacy education are readily available; however, the method of interaction is mostly one-way and theory-based. These offerings are either in a narrative or visual form (Lusardi, 2019; Lusardi et al., 2017; Van Wyk et al., 2018). Visual tools (videos) and narratives created in the right format are effective educational methods for creating cognitive involvement and altering knowledge and behaviour change, and can easily be scalable to reach different numbers of users (Lusardi et al., 2017).

The increasing popularity of financial software, such as online financial tools, internet banking, and mobile-based financial planning applications, requires individuals to constantly educate themselves on how to use these platforms. People use financial technology with the intent to plan, whether short-term or long-term. When these technologies are used skillfully and effectively, individuals can positively change their financial behaviour biases (Bi et al., 2020). Existing personal finance websites are in the form of financial data aggregators (advanced computing tools), financial decision tools (e.g. bond calculators), and personal finance communities on social media platforms. Unfortunately, in some cases, an individual must have basic mathematical literacy to understand the complexity of the data generated. Also, an individual must provide unique and personal data to perform specific complex calculations which may require too much effort, resulting in a lack of interest to continue analysis. The integrity of these sites is also questionable, as it is generally used for marketing purposes to sell financial products. Social media sites are also overcrowded with personal finance groups, blogs, and vlogs where anyone can share investment advice with others which might be incorrect and, in some cases, damaging. Other forms of financial education initiatives include card games, board games, and online games (Bi et al., 2020; Reiter & Qing, 2023; Van Wyk, 2018). Robo-advisors are new promising personal wealth management and investment digital platforms that provide automated, algorithm-driven financial planning services with little to no human control. However, using robo-advisors may require an individual to have a high level of financial knowledge (Yi et al., 2023).

Why Current Methods Are Failing

A systematic and comprehensive meta-analysis on financial education interventions by Miller et al. (2015) revealed that from the 188 studies analysed, the majority was conducted in the United States, half of these studies lectured varied financial topics, and only a third solely focused on savings and retirement. The majority of the interventions were offered face-to-face, a quarter of the studies targeted the community in general, and only a fifth of the studies were set in the workplace. The outcomes and measurements used to determine the effectiveness of the interventions were too diverse, which made it difficult to compare the studies (Miller et al., 2015). The current methods used to teach financial literacy are effective in accessing financial education, but whether they change financial behaviour that results in leaving individuals better prepared for retirement is not evident (Safari et al., 2021). Retirement literacy is either not included or stressed enough when teaching financial literacy, and it is more complex than basic financial literacy topics (Eling & Jaenicke, 2023). The content that policymakers think is important to include in a financial education curriculum may not reflect the actual evidence of what individuals deem important or need at different life stages (She et al., 2023). Furthermore, recruiting individuals to participate in financial education workshops is a challenging task. Offering these programmes requires full-time facilitators or counsellors, which can be costly. The individuals who need help with their finances the most are the least likely to attend such workshops (Lusardi et al., 2017).

Research concluded that financial education programmes should start at a young age, focus on specific target groups that are linked with their specific needs, avoid one-time seminars and workshops, simplify financial decision-making, avoid complex jargon and advanced communication, and provide individuals with basic financial literacy tools (Gibson et al., 2022; Horwitz, 2015; Lusardi, 2019; OECD, 2019). Digital financial education as a delivery channel should take preference, as it is easier to deliver the educational content, easily accessible, interactive, and entertaining, especially to the younger generations as they prefer using online resources (Zaimovic et al., 2023).

Methods, such as face-to-face seminars, workshops, and practical training programmes that might have been effective for the Baby Boomers and Generation Xers, are no longer the preferred method of learning for the younger working cohort, namely millennials (Sutton, 2019). Interactive teaching methods such as simulation and experiential learning in the form of visuals, pictorials, games, and narratives that connect with the individual’s goals and needs can potentially diminish adverse financial behaviours and improve the ability to retire financially independent from others (OECD, 2019; Sharma et al., 2021).

The Potential of Gamification

Millennials thrive in a digital environment (Jain & Dutta, 2019), and it has been suggested that to make financial education practical and appealing to millennials, programme developers should consider gamified applications portraying real-life events where problems need to be solved in a trial-and-error approach (Van Deventer & De Klerk, 2016). Gamified applications can aid millennials in gaining personal experience in managing money in different life situations (Jain & Dutta, 2019). More companies are realising the popularity and effectiveness of gamification due to its likelihood to promote behaviour change and foster education (Alsawaier, 2018).

The development of an effective gamified application or programme for financial literacy will require the adoption of learning theories with the intent to increase the likelihood of participants performing the desired behaviour (O’Donovan et al., 2013). Gamification is based on two major types of psychological theories, which include learning theories and motivational theories. One of the most commonly used learning theories is the theory of gamified learning. It is a psychological process of incorporating specific game elements to change a particular behaviour or attitude. For example, goals are used to enhance the meta-cognitive activity of the participant during the facilitating process (Landers et al., 2019), thus being aware of their thinking processes. The Self-Determination Theory is more commonly related to gamification, focussing on the fundamental purpose of human motivation to perform a task. Individuals seek to fulfil three fundamental psychological needs: autonomy, competence, and relatedness. These interconnected needs boost both intrinsic motivation (engaging in a task out of interest and enjoyment) and extrinsic motivation (engaging in a task for a reward or incentive) (Richter et al., 2015). The key concept of gameplay is motivation which includes both intrinsic and extrinsic motivation elements. Intrinsic motivation happens when the learner finds it rewarding when carrying out a task. Extrinsic motivation happens when the learner is more concerned with finishing a task to earn a reward and not necessarily to enjoy the learning process (Kapp, 2012).

Gamification is defined as a process of using game-based mechanics, aesthetics, and game thinking to engage people, promote learning, motivate action, and solve problems (Kapp, 2012). Game thinking is the most important part of gamification, taking an everyday experience and converting it into a task that involves elements of competition, cooperation, exploration, and storytelling. Gamification aims to attract the interest of individuals to the task created. Once engaged in the task, they need direction and purpose in their actions to keep them motivated to continue. Gamification can promote learning by adding a layer of interest in the task created to both motivate and educate an individual. Gamification has the potential to solve problems through cooperation and competitiveness (Kapp, 2012). Gamification can provide individuals with immediate, clear, and accurate feedback and could reduce overconfidence when making financial decisions (Reilly, 2012).

When game elements are incorporated into a learning programme, it creates a play environment where the brain tends to function differently compared to a natural setting. The brain will be more receptive to receiving information and increasingly more stimulated (Chen, 2015). A tedious and difficult training programme, like teaching a young adult about retirement planning, can be converted through gamification into an engaging, immersive, informative, and enjoyable experience (Craven, 2015). Gamification is about storytelling that will allow individuals to gain a personal experience that will give them a sense of belonging (Bell, 2018). When individuals find meaning in why the learning activity is important, they will be more likely to be motivated to engage in the activity. Meaningful gamified education is achieved when the needs and goals of an individual in a learning environment are considered (Kotini & Tzelepi, 2015). Learning a complex subject matter may trigger the feeling of fear that one can easily fail, but gamification can eliminate that fear (Bell, 2018).

Practical Examples of Gamification in Learning Settings

Below is a list of successful and innovative gamified applications in and outside the field of finance: • GravyStack is a digital application that was designed to enhance the financial literacy skills of children and teenagers. This application automates and gamifies the financial literacy process for individuals aged 6 to 18, by instilling positive money habits. The online platform includes a full bank account, a functional kids debit card for subscription payments, guidelines, and parental approval tools, which assist young users in learning about money while engaging in the gamified environment (Ritchie, 2023). • My Retirement Picture is a web-based tool developed by Alexander Forbes, a registered financial institution in South Africa. The tool allows individuals to enter their current income, expenses, assets, and liabilities and provides them with an illustration of the type of retirement future they can expect. Additionally, it calculates whether they are currently saving enough and helps them to understand retirement options. The My Retirement Picture tool includes a basic narrative, an avatar of an elderly person at retirement, and immediate feedback on choices made within the application (Alexander, 2024). • Avo, a digital retirement coach, develops personalised savings plans for its users. It adds a gamified element by turning saving into a challenge, with level achievements and rewards for reaching milestones. Users compete in challenging other users or participate in groups with the aim to earn additional points and bonuses (The American Association for Retired Persons & Ad Council, 2024). • Wells Fargo’s Retirement Score tool uses game elements in retirement planning by giving users a personalised score that indicates their retirement preparedness. The savings rate, investment strategy, and financial behaviours are all factors determining the final score. To enhance their score towards a more secure retirement, users need to engage (Wells, 2024). • Mint, a money manager and financial tracker budgeting app, brings together all of one’s finances (account balances, budget planners, expense tracker, and debt payments) in one place and allows one to set financial goals to be achieved (Intuit Mint, 2024).

Points of criticism against gamified learning programmes include the over-simplification of real-life situations; overconfidence among learners concerning the subject matter; and the effect programme being only short-term. Nevertheless, the advantages of using game elements in teaching far outweigh the disadvantages (Fouché, 2006).

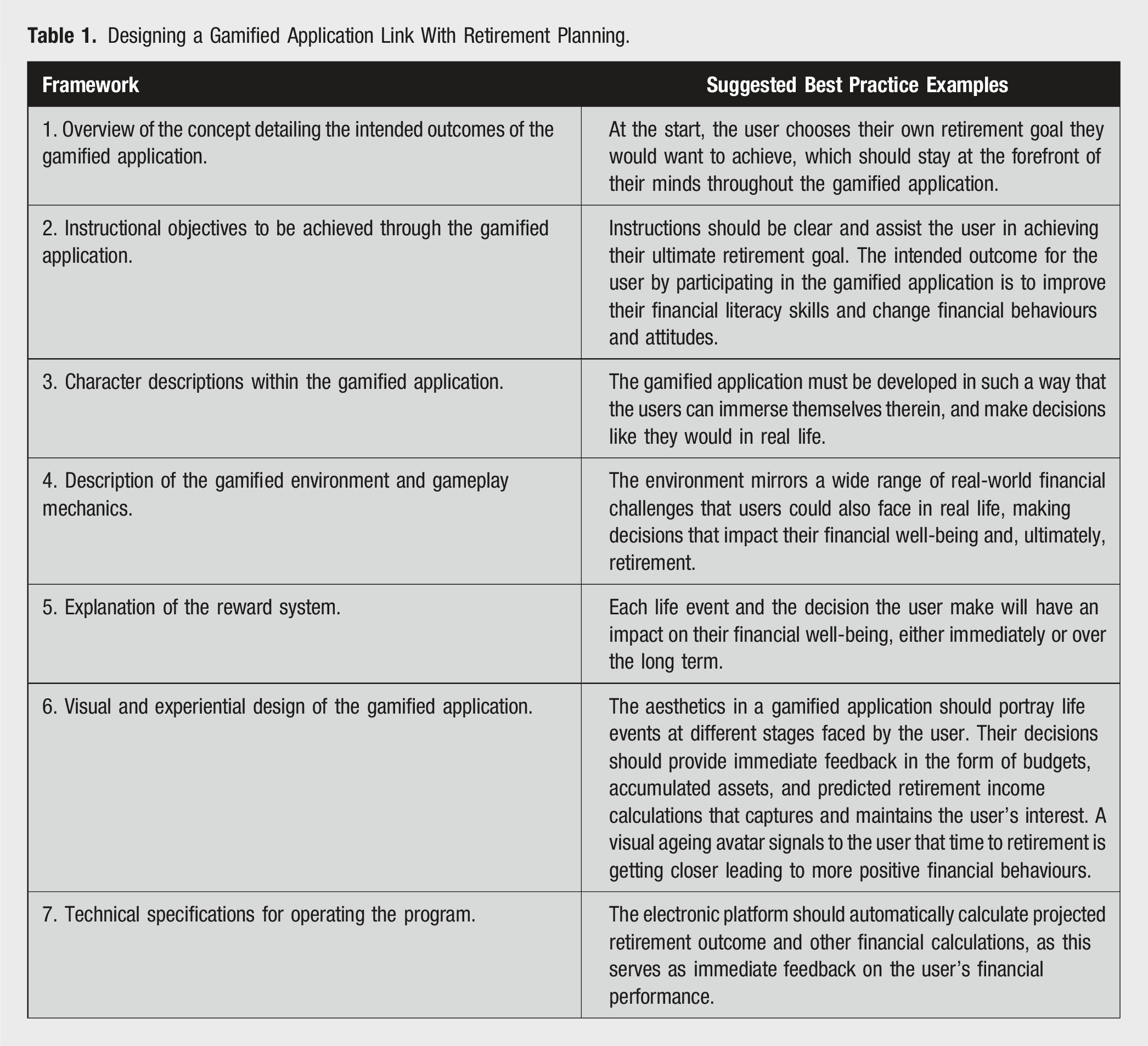

Best Practices for Employing Gamification in Retirement Planning Context

A basic framework when designing a gamified application suggested by Kapp (2012) can be linked to retirement planning as follows:

Designing a Gamified Application Link With Retirement Planning.

Implications for Practice

Creating a narrative where individuals are faced with real-life situations focussing on different phases during an individual’s life (e.g. entering employment, buying a house, making investment decisions, and planning for retirement) can teach them the skills needed to operate in the real world. Difficult concepts (complex financial jargon) can be taught successfully when incorporated into the narrative and creating a personalised experience (Bell, 2018). Furthermore, creating life-like avatars of learners vividly growing older in a gamified environment increases the chance of them saving more for retirement (Ersner-Hershfield, 2009). Applying the Self-Determination Theory to fulfil individuals’ needs of autonomy, competence, and relatedness gives them control over their financial decisions through immediate feedback. This will allow them to change previous financial decisions to achieve a better outcome (Campbell, 2016; Richter et al., 2015).

Incorporating the appropriate learning theories and game elements when designing a gamified application can result in an effective educational tool that can teach individuals how to solve problems. It can be done by creating a gamified learning environment that allows them to freely practice various techniques of problem-solving, without the fear of failure, and providing a clearer representation of a situation that is not always evident in real life (Kapp, 2012). Designing and implementing a gamified application is a highly complex task. There is no set formula or one-size-fits-all solution (Werbach & Hunter, 2020). The financial services industry can, through avatars, narrative, and replay, combined with a broad range of financial decisions and retirement concerns, create an online automated gamified application that can offer a safe and secure environment where individuals can make financial decisions and learn from their mistakes without suffering the consequences in real life. Teaching individuals to save for retirement through hands-on experience can make it a less daunting and achievable task (Yeo, 2019).

Conclusion

Retirees worldwide are not prepared for retirement. Younger generations need to be confronted with the urgency to start saving for retirement as early as possible, but current financial literacy education initiatives do not succeed in convincing them to do so. In lessening the financial burden on governments, financial education developers and policymakers must consider new ways to educate the younger generations more effectively through mediums that are familiar and exciting to them. The financial industry plays a vital role in the future of financial services and how it will change the context of how professional advice will be offered. A combined effort must be made by all parties to create a tool to revolutionise the way to teach and assist an individual in how to plan for retirement. Using gamification to illustrate how current saving behaviour affects retirement, the consequences of saving, budgeting, and planning for retirement can be made more tangible. Through active engagement and immediate feedback, gamification can promote financial literacy and might change the saving behaviour of the younger generations.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.