Abstract

Persistent evidence of a male advantage in equity fundraising has led entrepreneurship scholars to assume that while women face fit penalties in male-typed industries, men are exempt from penalties in female-typed ones. Yet underlying sociological theory implies that lack-of-fit penalties would apply to both sexes. Analyzing 718 equity deals from 408 ventures in Femtech, we find that male CEOs raise smaller deal amounts than female CEOs. Post hoc analyses and interviews provide interpretive triangulation consistent with two plausible explanatory accounts, embodied task competence and moral legitimacy. This challenges the assumption that men are exempt from fit penalties in female-typed industries.

Introduction

The male advantage in acquiring capital from professional investors has been well documented in entrepreneurship research (Alsos et al., 2006; Jennings & Brush, 2013; Marlow & Patton, 2005), and recent studies show the persistence of this gender gap (Guzman & Kacperczyk, 2019; Kwapisz & Hechavarria, 2025; Malmström et al., 2024). Especially in equity fundraising, the Diana Project, a field-defining research program, has repeatedly documented women’s challenges in accessing venture capital (VC) (Brush, 1992; Brush et al., 2004, 2018). Not only are women less likely to seek VC funding (Orser et al., 2006), but conditional on seeking it, they also obtain smaller investment amounts than male-led ventures (Brush et al., 2018; Guzman & Kacperczyk, 2019; Koziol et al., 2025). Such results align with broader societal stereotypes: “think successful entrepreneur—think male” (Eddleston et al., 2016, p. 497).

The research findings on the male advantage in professional equity fundraising are so many and so consistent that entrepreneurship scholars default to the theoretical assumption of a universal male fit in this context: Men “have no fit deficit for which to compensate through industry served” (Kanze et al., 2020, p. 2). More than 10 years ago, Jennings and Brush (2013) questioned whether the field lacked a more balanced investigation of gender in entrepreneurial resource mobilization, where it would be possible that men experience lack-of-fit penalties in female-typed contexts. Since then, collective evidence suggests that gendered industry effects hold only for female entrepreneurs. Consumers penalize women offering gender-opposite products (craft beer) but not men (offering cupcakes) (Tak et al., 2019). When accessing resources through referrals, only female entrepreneurs in male-typed sectors are at a disadvantage (Abraham, 2020). And in the VC context, only female CEOs are penalized when fundraising in gender-opposite industries (like finance and automotive; Kanze et al., 2020).

However, the original theories from sociology and social psychology that entrepreneurship research draws on to explain gendered lack-of-fit penalties—such as role (Anglin et al., 2022b; Biddle, 1986; Heilman, 1983) and status expectation states theory (Berger et al., 1972; Correll & Ridgeway, 2003)—would predict penalties for both women and men operating in an opposite-gender-typed domain. In fact, evidence outside entrepreneurship shows that men can incur penalties in female-typed contexts, especially when evaluated by other men (Bode et al., 2022; Heilman & Wallen, 2010). Men are seen as less likable employees in elementary education (Moss Racusin & Johnson, 2016), even as wimpy and less effective as leaders in employee relations counseling (Heilman & Wallen, 2010). Similarly, a meta-analysis shows that male leaders in education tend to be evaluated as less effective than female leaders (Paustian-Underdahl et al., 2014).

This tension between entrepreneurship and the gender theories on which our field builds is not just an inconsistency. It produces exclusions and silences, reflecting critiques of entrepreneurship as a field mostly “by men, about men and for men” (Holmquist and Sundin, 1988, p. 1 cited in Marlow, 2020, p. 40) in which men’s experiences are universalized as the norm (Calás et al., 2009). Consequently, the field struggles with unexamined and “contradictory assumptions and knowledge about the reality of entrepreneurs” (Ogbor, 2000, p. 605). This lens risks taking women’s lack of fit for granted while rendering such a possibility for men impossible. By assuming that gender sticks only to women, while male entrepreneurs are immune to gendered industry penalties (Kanze et al., 2020), we risk reinforcing the kind of theoretical blind spots that feminist perspectives urge us to confront (Coleman et al., 2019).

The purpose of this study is to probe entrepreneurship theory’s assumption of an industry-invariant male fit in professional equity fundraising by studying men as gendered individuals in entrepreneurship within Femtech. The industry’s name was coined in 2016 by Ida Tin in response to long-marginalized needs of women in health, and refers to ventures that use technology to address women-specific health needs (e.g. menstrual, maternal, pelvic/sexual health, fertility, menopause, and contraception; Hendl & Jansky, 2022; Kemble et al., 2022).

We build on status expectation states theory (Berger et al., 1972; Correll & Ridgeway, 2003) to argue that investors in Femtech may infer gendered founder-market fit along two dimensions. 1 First, perceived task competence: because women’s health problems are sex-specific and embodied, competence expectations may be cued more by biological sex than by stereotypical gendered beliefs, potentially making male CEOs appear less able to understand and address users’ needs in this context (Correll & Ridgeway, 2003). Second, moral legitimacy: given Femtech’s feminist and activist mission to tackle the neglect of women in healthcare (Hendl & Jansky, 2022), audiences may view men as out-group members (Diani, 1992), driven by self-interest, and question their alignment with the industry’s activist motives (Anesa et al., 2024; Suchman, 1995). These dimensions relate to the “ideal worker” prototype fit, meaning the local prototype—an evaluative schema translating gender status beliefs into performance expectations. As women are the majority not only of Femtech employees but also of Femtech entrepreneurs, the local prototype is feminine (Meuris & Merluzzi, 2024; Thébaud, 2015). Consequently, if gendered industry misfit penalties arise anywhere in professional equity fundraising, they are likely to arise for men fundraising in Femtech.

To test this hypothesis, we analyzed 718 equity deals from 408 Femtech ventures in the 2001 to 2024 period using PitchBook data (Brush & Elam, 2024; Brush et al., 2018). In line with our theorizing, we find that female CEOs in Femtech are associated with larger deals than male CEOs. This result is robust across multiple model specifications, including venture fixed effects to compare “apples-to-apples” (Brush & Elam, 2024). In post hoc analyses, we find that men’s lack-of-fit penalty is larger for Femtech ventures with a social orientation, a pattern consistent with the plausibility of the moral legitimacy account. We also conducted post hoc interviews to gather interpretive, illustrative insights into how evaluators talk about these issues.

Our study’s first contribution is to entrepreneurship theory of gendered resource mobilization. We challenge the long-standing field assumption of the industry-invariant male fit in professional equity fundraising (Kanze et al., 2020) in the context of Femtech. Drawing on Status expectation states theory, we find that men in Femtech are associated with lower fundraising outcomes than women, consistent with the possibility that locally gendered status beliefs shape founder-market fit in this context (Berger et al., 1972; Correll & Ridgeway, 2003). In this way, we respond to calls for re-examining blind spots in theorizing where gender “only sticks to women” (Jennings & Brush, 2013; Marlow, 2020) and advance the field’s fixed baseline assumption of industry-invariant male fit toward a more status-contingent, locally cued view of founder-market fit.

Second, we contribute to gender theories in entrepreneurship by nuancing what makes a context “female-typed” and demonstrating when such typing may not be sufficient for observing a male lack of fit (Kanze et al., 2020). The finding that the male CEO penalty appears in Femtech, but not in other female-typed sectors or broader healthcare, suggests boundary conditions for this gendered penalty, with post hoc interviews providing interpretive triangulation. We conceptualize Femtech as a particularly gendered context not only due to its numerical composition (majority female founders) and associated feminine stereotypes (e.g. caring, nurturing) but also because it focuses on embodied, sex-specific health needs, for which evaluators may treat female sex as a salient, observable cue of understanding (even if imperfect), further compounded by its historical and ideological anchoring in the feminist Women’s Health Movement (Hendl & Jansky, 2022; Nichols, 2000). By theorizing embodied task competence and moral legitimacy as plausible explanatory accounts through which founders’ sex may shape evaluation, we develop a more granular theoretical understanding for identifying when and how female-typed contexts may produce evaluative penalties for men.

Theoretical Background and Hypothesis

Gendered Lack of Fit in Professional Equity Fundraising

Professional equity fundraising shows a persistent gender gap, where women-led ventures secure smaller deals than male-led ventures (Brush et al., 2018; Guzman & Kacperczyk, 2019). A substantial body of work documents this gender gap (Alsos et al., 2006; Jennings & Brush, 2013; Kwapisz & Hechavarria, 2025; Malmström et al., 2024; Marlow & Patton, 2005). Supporting evidence spans decades (Brush, 1992; Brush et al., 2004, 2018), and the male advantage is rarely questioned in the entrepreneurship literature (cf. Brush & Elam, 2024).

Although the gender gap partly stems from structural factors, such as the lack of female investors (Brush et al., 2018), many scholars find that it is driven by venture capitalists’ implicit or explicit biases when evaluating entrepreneurs (Johansson et al., 2021; Koch et al., 2025; Malmström et al., 2017, 2020). Investors tend to characterize young women as inexperienced and young men as promising (Malmström et al., 2017). They ask women prevention-focused questions (i.e. how to avoid losses), but men promotion-focused ones (i.e. how to attain gains), furthering the male advantage (Kanze et al., 2018). Experimental studies accompanying such field evidence document the causal effect of gendered perceptions about entrepreneurs’ ability on fundraising success (Kanze et al., 2018; Snellman & Solal, 2023).

A dominant explanation for the gendered evaluations in entrepreneurship stems from the personal qualities expected of those occupying the role of an entrepreneur (Anglin et al., 2022b). Success in entrepreneurship is stereotypically linked to male-typed traits (e.g. being aggressive, competitive, and risk-taking; Ahl, 2006), which is incongruent with stereotypes that society holds about women (e.g. being nurturing, trustworthy, and gentle; Cejka & Eagly, 1999). This role incongruity has been used to explain sex differences in bank financing (Eddleston et al., 2016), reward-based crowdfunding and microfinance (Anglin et al., 2022a, 2023), social accelerator applications (Yang et al., 2020), investor pitches (Balachandra et al., 2019), and equity finance more broadly (Koziol et al., 2025). In the context of VC fundraising, these lack-of-fit penalties for women have been found not only for entrepreneurs (Kanze et al., 2020; Lee & Huang, 2018) but also for investors (Butticè et al., 2023).

This notion of social beliefs driving the gender gap in entrepreneurial fundraising broadly aligns with status expectation states theory, 2 which states that people rely on social attributes (like race or sex) to form expectations about individuals’ competence and performance, leading people to attach perceptions of social status to said attributes (Berger et al., 1972; Correll & Ridgeway, 2003). Sex, in particular, functions as such a “status characteristic.” Widely held cultural beliefs ascribe men greater competence and status worthiness than women across a broad range of tasks, regardless of their actual ability (Ridgeway & Correll, 2004). This general belief about men and women is commonly shared, as most people are aware of it and assume that others also apply it (Eagly et al., 2000; Fiske et al., 2002).

In entrepreneurial fundraising, characterized by uncertainty and high information asymmetry (Colombo, 2021), such widely held and often unconscious beliefs (Correll & Ridgeway, 2003) become especially impactful as evaluators rely on status beliefs as a heuristic (Trapido, 2022). In entrepreneurship, these status beliefs create anticipations that men are more capable entrepreneurs, shaping interactions in ways that grant them more opportunities, resources, and favorable evaluations (Thébaud, 2015). Performance expectations thus become self-fulfilling, as investors defer to male founders’ claims and scrutinize female founders more harshly (Kanze et al., 2018; Lee & Huang, 2018; Snellman & Solal, 2023).

Gendered Lack of Fit and the Gender-Typing of Industries

Status expectation states theory explains not only how gendered status beliefs shape evaluations but also when sex becomes a salient task-relevant signal—namely, when (a) there is a dominant sex representation of actors in the context and (b) the core tasks are gender-typed (Ridgeway & Correll, 2004). These features determine context-specificity in gendered evaluations, from negligible to substantial (Deaux & Lafrance, 1998; Ridgeway & Smith-Lovin, 1999). Many industries (e.g. nursing, human resources, engineering, policing, finance) are culturally “gender-labeled” (Doering & Thébaud, 2017, p. 543). Thus, context matters for entrepreneurs for at least two reasons. First, entrepreneurs tend to self-select into gender-fitting sectors (Greenberg & Mollick, 2017). Second, evaluations hinge on the entrepreneur’s perceived fit, or lack thereof, with an industry’s stereotypical tasks (Seigner et al., 2022).

Sex representation at the industry level turns sex into a task-relevant status cue, as observers treat it as informative for evaluating who is more competent (Alonso & O’Neill, 2022; Correll & Ridgeway, 2003; Tak et al., 2019). The link between sex and the gendered tasks prompts evaluators to expect higher performance from those who fit the “ideal worker” prototype for this task (typically the more represented sex) and to apply stricter standards to those who do not (Meuris & Merluzzi, 2024). Accordingly, men are not only seen as more competent entrepreneurs in general, but especially so in science, technology, engineering, and mathematics fields in which they are disproportionately represented (Poggesi et al., 2020), consistent with the status belief that portrays men as more competent in quantitative, analytical, and mathematical tasks (Cejka & Eagly, 1999).

In female-typed settings, task-specific competence expectations can also shift away from men and toward women, counterbalancing—or even outweighing—the general high status of men (Ridgeway & Correll, 2004). Accordingly, research shows that men in female-typed contexts can experience penalties when stereotypes about women’s greater competence are more salient (Kalokerinos et al., 2017; Manzi, 2019) or when men’s underrepresentation makes their lack of fit with the “ideal worker” prototype obvious. Evidence ranges from care-intensive occupations like nursing and elementary education, where men report more bullying and receive lower likability/effectiveness ratings (Eriksen & Einarsen, 2004; Moss Racusin & Johnson, 2016; Paustian-Underdahl et al., 2014), to leadership contexts where male leaders are evaluated as less effective leaders in female-typed relational tasks like employee counseling (Heilman & Wallen, 2010). Conversely, as communal attributes gain value in leadership, women’s perceived lack of fit attenuates (Koenig et al., 2011; Sczesny et al., 2004).

Despite such evidence for the applicability of gender fit, or lack thereof, to both men and women in gender-opposite tasks (Manzi, 2019), in professional equity fundraising, there is no evidence of men being penalized in female-typed sectors (Kanze et al., 2020). Even beyond the fundraising context, male entrepreneurs do not face evaluation penalties in product markets when selling female-typed products (Tak et al., 2019) or when seeking referrals in female-typed sectors in networking organizations (Abraham, 2020). In VC funding, scholars argue that male entrepreneurs are presumed to fit regardless of the industry, yielding “no fit deficit” for men, whereas only women are penalized in gender-opposite industries (Kanze et al., 2020). 3 Taken together, entrepreneurship theorizing has sustained the assumption of a universal male fit regardless of the venture’s industry.

Investor demographics and homophily likely reinforce this “no fit deficit” assumption for men. With most professional equity investors being men (Gompers & Kovvali, 2018), gender homophily tendencies in investing (Ewens & Townsend, 2020; Snellman & Solal, 2023) likely reinforce masculine fit in entrepreneurship. This is exemplified by evidence that female entrepreneurs are seen as even less competent when backed by female investors (Snellman & Solal, 2023). Female investors, in turn, are challenged by male entrepreneurs on the grounds of lacking legitimacy as investors (Butticè et al., 2023). Related evidence from business angel groups suggests that gendered investment behavior can be shaped by context (e.g. being a minority in male-dominated groups) (Cohen et al., 2025).

Viewed through the lens of the sociological theories the entrepreneurship literature borrows from to explain the gender gap in professional equity fundraising, it is striking to see only one-sided evidence documenting almost exclusively women’s disadvantages, while dismissing the possibility that men could also be subject to gendered lack-of-fit penalties (we present a table summarizing the corresponding literature in Online Supplemental Appendix I). Yet “absence of evidence” does not mean “evidence of absence.” One reason for not finding a lack-of-fit penalty for male entrepreneurs could be the tendency in the entrepreneurship literature to focus on testing the “female underperformance hypothesis” (Du Rietz & Henrekson, 2000) (see also the reviews by Anglin et al., 2022b; Jennings & Brush, 2013; Koziol et al., 2025). From a feminist scholarship standpoint, this empirical blind spot could be critiqued as part of the “silence” that results from entrepreneurship’s field tendency to universalize men’s experiences as the norm and rarely question them (Calás et al., 2009).

The one-sided evidence may also be partly due to empirical choices in research design. Specifically, some studies that examine gender-typed contexts within entrepreneurship often operationalize “gender-typing” using numeric proxies based on the sex composition in an industry’s workforce (e.g. ≥70% of one sex in Abraham, 2020; ≥56% in Kanze et al., 2020), rather than capturing the gendered meaning of the focal context and the connected tasks. However, these gendered meanings about contexts and tasks are the very features that role and status expectation states theory suggest should activate (mis)fit dynamics. Other work that moves beyond industry employment proxies and conducts survey-based inquiry of gendered product perceptions (Tak et al., 2019, surveying perceptions on MTurk in the United States), potentially holds different drawbacks. For example, Tak and colleagues’ (2019) experiment stays within one industry (food) to hold constant broad domain features, and contrasts gendered notions of specific products within that industry (craft beer as masculine-coded vs. cupcakes as feminine-coded). However, in doing so, the study perhaps does not account for the less clean-cut view on competencies in the food sector, given the cultural repertoire that many US consumers likely draw on in evaluating entrepreneurs (not just products). Widely recognizable “celebrity chef” figures are often men (e.g. Gordon Ramsay, Bobby Flay), and even the pastry/dessert space features prominent male exemplars familiar to broad audiences (e.g. Buddy Valastro, Dominique Ansel).

Conclusively identifying why there is an absence of evidence for male lack-of-fit penalties in equity fundraising in the entrepreneurship literature is difficult. The reasons may likely reflect a mix of taken-for-granted assumptions (and thus few attempts to challenge it, cf. Brush & Elam, 2024) and a lack of investigating “revelatory, extreme exemplars” (Eisenhardt & Graebner, 2007, p. 27), meaning boundary industries in which male misfit would plausibly be sufficiently salient. Our study examines this “entrepreneurship exception” through the broader lens of status expectation states theory, upholding that a context-sensitive status characteristic, such as sex, should penalize anyone who violates strongly gendered task expectations (Correll & Ridgeway, 2003; Eagly & Karau, 2002). We treat the “no fit deficit” assumption in professional equity fundraising as a theoretical problem and examine it in such a “revelatory” industry where male entrepreneurs’ lack of fit could be pronounced enough to surface penalties.

CEO Sex and Funding Performance in Femtech Ventures

We build on status expectation states theory to argue that Femtech is a context in which male CEOs would experience gendered lack-of-fit penalties when fundraising from professional equity investors. This is due to Femtech’s distinctiveness along what we argue to be at least two fit-relevant dimensions: (a) perceived task competence, meaning perceptions of the CEO’s ability to understand and address women’s health needs, and (b) moral legitimacy, meaning the CEO’s legitimacy to represent the industry’s feminist and activist mission. These considerations impact the “ideal worker” prototype fit, conceptualized as the CEO’s conformity with the dominant default norm.

First, when it comes to perceived task competence, investors care about an entrepreneur’s ability to identify with the user’s problem, elicit honest feedback, test the product, and build traction with users (Chen et al., 2023; Yang et al., 2020), which determines founder-market fit. In Femtech, an entrepreneur’s core tasks revolve around understanding and serving women’s needs, which are sex-specific and embodied (menstruation, fertility, menopause, pelvic/sexual health) and commonly tied to stigma and vulnerability (Johnston-Robledo & Chrisler, 2020). Such embodied task competence should make CEO sex (being a woman)—not only the associated gender stereotypes linked to the predominance of women in the industry (e.g. femininity as caring)—especially salient in judging an entrepreneur’s fit. 4 Thus, we suggest that a female CEO will have a higher fit because she belongs to the relevant biological sex category (female), which investors are likely to treat as task-relevant in women’s health. In status expectation states terms, sex operates in Femtech as a status cue that is used to infer CEO’s competence expectations under uncertainty, because it is cognitively readily “available” (even when it may be an imperfect proxy for true capability). In contrast to Femtech, in human resources or baking products—domains often culturally coded as feminine—men can still personally relate to products (Seigner & Milanov, 2023; Tak et al., 2019). Femtech is different as core problems such as menstruation, pregnancy, and menopause are clearly biologically unique to women, even if not all women have experienced all of these. Men in Femtech can be perceived as less able to understand those needs or relate to those who have them, and instead be seen as marginalizing women as knowers of their bodies (Hendl & Jansky, 2022).

This lack-of-fit dimension has been illustrated by international backlash against male-led Femtech ventures, such as Pinky Glove, a pink tampon disposal product. The two male founders were accused of “inventing a problem” to design a “pink” solution around it and “mansplaining tampon removal” (Keiser et al., 2021; Marriner, 2025). Similarly, coverage of the period-tracking app Flo noted pushback, with Forbes reporting that Flo’s male-led structure has led to criticism that, while addressing women’s health issues, they may not “understand the issues they’re addressing” (Oberoi, 2024). These criticisms reflect broader concerns documented in the analysis of over 2,000 user reviews of period-tracking apps (Epstein et al., 2017). Many users expressed frustration with stereotypical, gendered app aesthetics—such as pink color schemes and floral imagery—which they viewed as patronizing. As one user noted, “a lot of them just felt kind of condescending or like they were designed by dudes who were designing what they thought a woman would like” (Epstein et al., 2017, p. 6,882). Thus, in Femtech, men may be perceived as lacking the embodied task competence deemed necessary to competently address women’s problems.

Second, in Femtech, evaluations also hinge on whether an entrepreneur is perceived to be in it for the “right” reasons and aligned with the field’s mission, which ultimately shapes a CEO’s moral legitimacy. Femtech emerged as not only an industry but a social movement with the mission to tackle the structural neglect of women in healthcare (Gutterman, 2023). In the 1960s and 1970s, the Women’s Health Movement argued for a shift that would center women’s needs, autonomy, and collective agency (Nichols, 2000). It was a female movement driven by values of equity, voice, and understanding of their bodies, and it framed access to health and care as a feminist and politically charged issue, not just a clinical one. The very term Femtech was coined by a woman, Ida Tin, fundraising for a menstruation app in 2016, to attract attention to female health issues, which received much positive media attention (Kemble et al., 2022). As such, Femtech is linked to feminist activism in entrepreneurship in a way that traditional female-typed sectors like education or fashion are not (Calás et al., 2009; Hendl & Jansky, 2022). This social movement quality of Femtech increases the importance of perceived values complementarity of Femtech ventures and their CEOs with the values of the Women’s Health Movement (Gish et al., 2025).

Accordingly, a CEO’s moral legitimacy in Femtech hinges on whether audiences see them as in-group advocates rather than outsiders. Legitimacy—“the generalized perception … that the actions of an entity are desirable, proper, or appropriate within some socially constructed system of norms, values, beliefs, and definitions”—is foundational to (gender) status hierarchies and shapes social evaluations (Correll & Ridgeway, 2003; Ridgeway et al., 1995; Suchman, 1995, p. 574). In particular, moral legitimacy concerns normative evaluations, where audiences judge whether actors are operating for the “right” reasons. Applied to Femtech, female CEOs—because of their biological sex—can more readily claim moral legitimacy, whereas men face a legitimacy gap because they cannot relate to women’s health needs firsthand (Hussain et al., 2023; Park et al., 2022).

This argumentation is in line with the literature on activist movements, which shows that in-group membership (i.e. being a woman in Femtech) matters (Diani, 1992) because individuals who might be personally affected by the issue are more likely to be seen as legitimate voices for change (Sherf et al., 2017). In contrast, when men engage in diversity-related work (Bosak et al., 2018; Hekman et al., 2017), they often face backlash. These dynamics surfaced in Femtech surrounding the two mentioned male-led Femtech ventures. On Reddit (2023), users accused Flo of being “money hungry.” And on social media, users argued that instead of Pinky Glove “earning a shitload of money by selling products no one really needs” (Moss, 2021), “these guys … need to crawl back under whatever 1940s sexist rock they crawled out of when they came up with this crap” (Marriner, 2025). Thus, in spite of broader competence beliefs, men in Femtech likely have lower moral legitimacy than women.

Such backlashes, characteristic of politically charged and social movement-rooted contexts, such as Femtech, mean that investors could reasonably be concerned about how their own funding decisions will be perceived by relevant third parties (limited partners, syndicate partners, entrepreneurs, or the media). Funding decisions commonly involve discussions among VC partners. In such coordinating contexts, expectations of third-party evaluations become especially prominent (Correll et al., 2017). Specifically, what matters here are expectations of what “other people think” is the most fitting sex for founder-market fit. Satisfying third parties’ expectations has already been documented as a source of potential gender bias in entrepreneurship (Abraham, 2020), as has investors’ desire to protect their reputations (Vanacker & Forbes, 2016). Thus, even if individual investors themselves do not consider women to be a better fit for Femtech CEOs, their expectations of third parties’ values in this regard could impact their investment decisions.

Consequently, in Femtech, investors are likely to see women—more than men—fit the “ideal worker” prototype that defines performance expectations in status expectation states theory. “Ideal worker” refers to a cultural schema, meaning the default norm, that specifies the standard against which individuals are evaluated (Meuris & Merluzzi, 2024). It is the template that translates gender status beliefs into concrete performance expectations, especially under ambiguity (Thébaud, 2015). In male-dominated domains, the prototype is typically masculine, and in female-dominated domains it is feminine (Thébaud, 2015). Although women are strongly represented in female-typed sectors like the fashion and food labor forces, high-status positions (e.g. fundraising CEOs) are still often occupied by men (Doering & Thébaud, 2017). In Femtech, women not only constitute nearly 70% of the broader healthcare workforce (World Health Organization, 2021), they are also the majority of fundraising CEOs (60.17% of the Femtech deals have a female CEO leading the venture, according to our PitchBook data). This makes women strongly salient and also contrasts with the gender dynamics in the broader VC market, where men dominate (Bittner & Lau, 2021). Because numerical dominance can also be seen as a reflection of the ideal worker template (Floge & Merrill, 1986), Femtech likely recalibrates this template for both the workforce and the CEOs leading ventures (Eagly & Koenig, 2021). In turn, this creates a context in which men tend to be perceived as outsiders who lack this prototype fit. Consequently, if gendered industry lack-of-fit penalties arise in professional equity finance, they should hold for men fundraising in Femtech. Therefore, we hypothesize:

Empirics

Sample

To test our hypothesis, we follow prior research on gender in venture finance and use data from PitchBook (Brush & Elam, 2024; Brush et al., 2018), a database that provides “an unparalleled breadth of information on market activity around the world” including structured information on companies, funding rounds, founders, and investors (Hechavarria et al., 2025, p. 82). Retterath and Braun (2020) identified this database as one of the most reliable sources for information on companies, founders’ profiles, and funding. Moreover, PitchBook is the first database, to our knowledge, to categorize Femtech as an industry sector, and we thus examined equity deals of companies classified under the Femtech label. To focus specifically on venture fundraising, we restricted the sample to ventures that were no more than 10 years old at the time of the deal (Milanov & Fernhaber, 2009). The final sample consists of 718 equity deals with complete data from 408 Femtech ventures funded across 34 countries between 2001 and 2024.

Variables

Dependent and Independent Variables

In line with prior literature examining sex-based differences in venture fundraising, our dependent variable is Deal size in millions of USD (Brush et al., 2018; Guzman & Kacperczyk, 2019; Kanze et al., 2020). This is the amount of capital observed at the deal level, raised by a venture in a specific round, which we source from PitchBook. We transform this variable using the inverse hyperbolic sine (IHS) to account for skewness. This transformation has been used in prior literature examining gendered differences in venture fundraising (Anglin et al., 2018; Seigner et al., 2022) and functions similarly to a logarithmic transformation. 5

Following Brush and Elam (2024), our predictor of interest is CEO sex at the time of closing the deal. CEO male is a dummy variable collected from PitchBook (1 indicates that the CEO at the time of the deal is male; 0 indicates a female CEO at the time of the deal).

Control Variables

We include a range of control variables. We control for Capital raised to date (IHS transformed) to capture the venture’s cumulative ability to secure external financing (Seigner et al., 2022; Snellman & Solal, 2023). To reflect the venture’s market valuation and expected growth potential, we further control for the Pre-money valuation (IHS transformed). We also control for the Number of new investors and the Number of prior investors (both IHS transformed), which may both signal different social proof for the venture’s viability (Wesemann Lekkas et al., 2025) and give access to a larger pool of resources and networks (Snellman & Solal, 2023). We include Country dummies to account for institutional or cultural differences that might influence funding performance. We also include dummies for the Year of the deal to address year-specific effects, including macroeconomic conditions (Brush et al., 2018), as well as Deal type dummies to capture any systematic differences among, for example, early-stage, follow-on, or late-stage financing. In this vein, we also include Business status dummies, such as whether the venture is in clinical trials, generating revenue, or still in product development, since these stages can signal different levels of venture maturity and associated funding needs.

LLM-Assisted Variable Coding and Validation

We also use additional variables in robustness and post hoc analyses that we coded with the help of a deterministic Large Language Model (LLM) classifier (GPT-3.5-Turbo; temperature = 0) with structured prompts (reported in footnotes; for the coding logic in Python, please see Online Supplemental Appendix II): Femtech (to recode to see if PitchBook’s industry classification is accurate, Yes/No from company description; used in robustness), Social venture (Yes/No; post hoc), B2B versus B2C (robustness), CEO education relevance for Femtech (Yes/No; robustness), and CEO highest degree (Undergraduate/Graduate/Doctorate; robustness). Although ChatGPT is reliable in categorization tasks (Le Mens et al., 2023), we followed prior literature in gendered entrepreneurial finance (Seigner et al., 2022) and assessed construct validity ourselves. We drew a random sample of 60 ventures (2 times 30 observations as per the central limit theorem; 1 deal per venture) and independently hand-coded all items (education variables have a smaller N due to missing data). Using standard benchmarks (Hallgren, 2012), agreement between human and LLM was substantial (κ ≥ .61) to almost perfect (κ ≥ .81): Femtech 98.33% (κ = .90), Social venture 95.00% (κ = .883), B2B/B2C 95.00% (κ = .827), Education relevance 90.62% (κ = .762; N = 32), and CEO highest degree 96.55% (κ = .947; N = 29). McNemar tests on the binary tasks indicated no directional asymmetry.

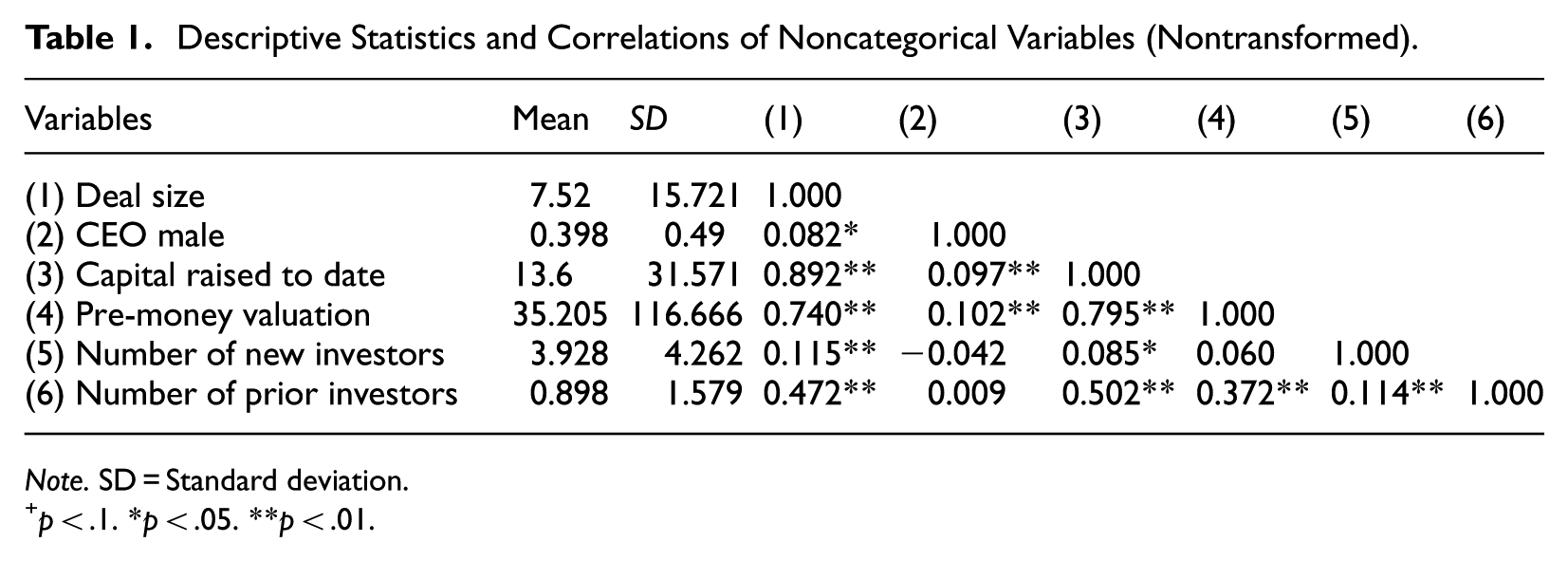

Descriptive Statistics

In Table 1, we present the descriptive statistics and pairwise correlations for our noncategorical variables in their original form. The average deal size in our sample is USD 7.52 million. Most deals in our sample are seed rounds (33.29%) or early-stage VC (31.62%). Our sample is US-dominant, with 54.60% of observations representing US funding. Male CEOs closed the funding round in 39.8% of our observations. These statistics are supportive of the premise that Femtech is a female-typed industry not only in terms of occupational representation of women in the industry but also at the fundraising CEO level. 6

Descriptive Statistics and Correlations of Noncategorical Variables (Nontransformed).

Note. SD = Standard deviation.

p < .1. *p < .05. **p < .01.

Empirical Approach

We build our analysis on Brush and Elam (2024), who predicted total capital raised from a gendered perspective using PitchBook data and ordinary least squares estimates. While they examined cross-sectional variation, we take advantage of our panel data structure and exploit within-venture variation. Namely, we, like them, also apply linear estimation but extend it by incorporating venture fixed effects. This is possible as we observe multiple funding rounds per venture and within-venture variation in our independent and control variables. This approach accounts for all time-invariant, venture-level unobservables, taking care of much of the usually problematic omitted variable bias. Put differently, we observe CEO switches within ventures, and therefore our results are driven by comparing the same ventures with a male versus a female CEO, which is the strictest form of capturing “an apples-to-apples comparison” (Brush & Elam, 2024, p. 2,299). Using fixed effects compared to random effects was also validated by a Hausman (1978) test (p < .001). To address potential heteroskedasticity, we use robust standard errors.

According to the variance inflation factors (VIF) among our noncategorical variables, multicollinearity does not seem to be a concern. The highest value without venture fixed effects is 8.59 for Capital raised to date (IHS transformed) (Belsley et al., 2005; Franke, 2010).

Results

We show our linear regression models in Table 2. In Model 1, we include only control variables, and in Model 2, we test our hypothesized relationship.

Deal Size (IHS Transformed) Regressed on CEO Sex.

Note. Robust standard errors in parentheses. IHS = Inverse hyperbolic sine.

p < .1. *p < .05. **p < .01. ***p < .001.

Our hypothesis suggested that a Femtech venture led by a male CEO would show a lower fundraising performance compared to one led by a female CEO. In Model 2, we found a significant and negative estimate for CEO male (b = −0.143, p = .018). Our hypothesis is thus supported. This estimate suggests that a Femtech venture led by a male CEO, compared to when it is led by a female CEO, is associated with a smaller deal, with a decrease of 13.3%, translating to an average reduction of USD 1.0 million in funding if the CEO is male, given an average deal size of USD 7.5 million.

Robustness Analyses

To first provide an intuitive before/after visualization around CEO-sex switches, we plotted mean and median deal sizes (IHS) in event time around these switches for switching ventures (Figure 1). The figure is constructed on a firm-year panel using the largest sample available for this purpose (only requiring nonmissing deal size, CEO sex, venture identifier, and year). We report the number of firm-year observations contributing to each event-time bin and restrict attention to a ±2-year window around the first observed switch year (t = 0). While we treat these patterns as purely descriptive, they are directionally consistent with our main within-venture estimates that associate male CEOs with smaller deal sizes as compared to female CEOs.

Descriptive event-time means and medians; window [−2,+2] years.

We address potential concerns related to our modeling choices through multiple sets of robustness analyses, shown in Table 3. Our first set of robustness checks (Models 1 and 2) addresses concerns related to the selection and specification of our control variables, including the potential for omitted variable bias. First, although our VIFs did not indicate multicollinearity concerns, there are some recent doubts regarding the reliability of VIFs (Kalnins & Praitis Hill, 2025). Thus, we replicated our analysis, orthogonalizing highly correlated control variables (Capital raised to date and Pre-money valuation). The estimate for CEO male remained negative and significant (b = −0.143, p < .05, Model 1).

Robustness Analyses.

Note. Robust standard errors in parentheses. IHS = Inverse hyperbolic sine; VC = Venture capital.

p < .1. *p < .05. **p < .01. ***p < .001.

Next, as VC allocation is high in uncertainty, venture capitalists may pay attention to other signals about the founding CEO (Brush & Elam, 2024), in addition to sex (Kanze et al., 2020). Therefore, we accounted for CEO education using descriptions on PitchBook, allowing us to determine if it was Femtech relevant, as well as their highest Degree category. Both variables were classified using OpenAI’s API using structured queries. 7 When introducing these additional controls into our regression model, the estimate of CEO male remained negative and just missed one-sided significance (b = −0.104, p = .109, Model 2). These findings indicate that differences in education are unlikely to fully account for our observed relationship. 8

Finally, to assess the more general impact of omitted variable bias, we calculated the Impact Threshold for a Confounding Variable (ITCV; Busenbark et al., 2022; Frank, 2000). This analysis showed that an omitted variable would need to be correlated at 0.162 with both the dependent and independent variables to eliminate the observed association. Examining the partial correlations, we find that no control variable exceeds this threshold. The largest observed partial correlation is 0.067 for Capital raised to date. Any omitted variable (e.g. CEO age, which is unavailable in our data) would need a partial correlation ≥0.162 with both CEO male and Deal size (IHS-transformed)—that is, more than twice the correlation magnitude of Capital raised to date, to overturn the effect. These numbers suggest that the likelihood of any omitted variable exerting a strong enough influence to eliminate the observed association is low. 9

Our second set of robustness analyses tests the generalizability of our findings when accounting for both within- and between-venture variance using random effects. As the Hausman test clearly favored the fixed-effects specification over random effects (p < .001), we re-estimated our model using a Chamberlain–Mundlak approach to “more closely approximate fixed effects” (Seigner et al., 2023, p. 12). This random-effects approach also includes the means of all time-varying variables. In line with prior entrepreneurship research on VC-backed ventures, we also incorporated an additional control variable obtained “at the time of data retrieval of the respective venture” (Seigner et al., 2023, p. 12)—namely, the venture’s last recorded Business status (described in the Variables subsection). Including it helps control for differences between ventures that would otherwise have been accounted for by the fixed effects. The estimate for CEO male remained negative and one-sided significant (b = −0.052, p = .082, Model 3).

The Chamberlain–Mundlak specification also allows incorporating additional variables that do not vary within a venture, as they would have been absorbed by the fixed effects in our main model: business model (B2B/B2C; coded from PitchBook descriptions via GPT prompts) 10 and, where available from PitchBook, the number of active patents to proxy intellectual property. To have a complete set of controls, we also added controls referring to CEO education (Femtech relevance and their highest Degree category). Across these extensions, CEO male remained negative and one-sided significant (full sample without patents: b = −0.055, p = .070, Model 4; patents subset with available patent count: b = −0.073, p = .080, Model 5). These analyses indicate that the negative association between CEO male and Deal size also holds when incorporating between-venture variance, supporting the generalizability of our findings beyond the subset of ventures with CEO sex switches.

Another potential concern with fixed effects relying on CEO switches is whether there are any systematic patterns surrounding the CEO sex switch (e.g. whether ventures were underperforming prior to a CEO switch). We therefore directly tested whether CEO-sex switches are systematically preceded by weaker observable performance using the funding-related proxies available in PitchBook. This deal-event test is run on the main fixed-effects analytic sample, but uses only the subset of CEO-sex switch events. Within each venture, we compare the deal immediately prior to a switch to the switch deal itself (post–pre). Using the IHS-transformed measures (as in our regressions), the average pre/post changes are positive and statistically significant: Δ IHS capital raised-to-date (mean = 1.079, t = 8.921, p < .001), Δ IHS deal size (mean = 0.677, t = 4.103, p < .001), and Δ IHS pre-money valuation (mean = 1.025, t = 5.358, p < .001). Thus, switches are not observed at deals preceded by declines in these funding-related observables. Because PitchBook records CEO characteristics at deal close, these tests describe patterns around observed funding events (i.e. switches are timed to deal closings, not continuously observed between deals). We also tested whether these pre/post changes differ by switch direction (Male → Female vs. Female → Male). Two-sample tests are not significant for any proxy (Δ IHS raised-to-date: diff = −0.162, p = .514; Δ IHS deal size: diff = −0.318, p = .347; Δ IHS pre-money valuation: diff = −0.106, p = .789), indicating no systematic directional asymmetry in observable shifts around switch events.

For context, in the main fixed-effects sample (N = 718 deals; 408 ventures), we observe 32 CEO-sex switch events across 26 ventures (18 Male → Female; 14 Female → Male), with 77 deal-observations in switching ventures (10.7% of the analytic sample). Because venture fixed effects identify the CEO male coefficient from within-venture changes and our setting implies limited CEO turnover, we additionally report (Model 6) a “no-controls” FE model that maximizes usable observations (N = 2,527 deals; 928 ventures; 134 switch events across 93 ventures; 454 deal-observations in switching ventures). The CEO male coefficient increases in both magnitude and is even more significant (b = −0.415, p < .001, Model 6). To provide transparency on sample composition and the basis for within-venture identification, Online Supplemental Appendix IV reports a detailed comparison of the “main (full-controls) sample” versus the excluded observations from the “no-controls” sample, and Online Supplemental Appendix V-VI report CEO-sex switch descriptives (counts/patterns and timing) for both samples.

In further analyses, we also estimated a complementary difference-in-differences-style venture fixed-effects postswitch specification focused on ventures experiencing a female-to-male CEO switch. Specifically, we identified, for ventures that ever experienced such a transition, the first observed female-to-male switch year, mapped this timing back to deal-level observations, and estimated a postswitch indicator model with the full set of main-analysis controls. Given the relatively small number of observed switch events and postswitch observations, this analysis should be interpreted cautiously. The postswitch coefficient was negative but not statistically significant (b = −0.257, p = .426). We also estimated follow-on fundraising models in which the dependent variable indicates whether an observed financing round was followed by another observed round within a 3-year window, treating late-year observations without a full forward window as right-censored. These models likewise did not indicate a statistically significant CEO-sex difference, whether estimated as a logit (b = −0.004, p = .984) or a linear probability model (b = −0.010, p = .833), although both estimates are directionally consistent with the main analysis.

Our third set of robustness analyses tests sensitivity to research-design choices within the main sample, such as which rounds are included, age cutoffs for “new ventures,” industry labeling, and outlier treatment (Models 7–12). To be able to directly speak to Brush, Greene, and colleagues’ work on gendered VC funding and the Diana project, we restricted our sample to VC deals only. The estimate for CEO male remained negative and significant (b = −0.137, p < .05, Model 7). Additionally, we also restricted the sample to the first VC funding round, when the uncertainty around the venture’s potential is highest, and there is no prior track record impacting the results. The estimate for CEO male remained negative and, despite the sharp drop in sample size from 718 to 248 observations, one-sided significant (b = −0.047, p = .094, Model 8). Next, given that prior work also used stricter age boundaries for sampling new ventures, we restricted our sample to ventures 7 years old or younger to examine whether firm age influenced our results (Pollock et al., 2015). The estimate for CEO male remained negative and significant (b = −0.191, p < .01, Model 9). We also wanted to guard against potential misclassification issues of PitchBook’s industry tagging (see Brush & Elam, 2024). To address this, we reclassified each company according to its fit with the definition of Femtech. 11 When restricting our sample to firms that were classified as Femtech based on their company description provided by PitchBook, the estimate for CEO male remained negative and one-sided significant (b = −0.130, p = .052, Model 10). Additionally, we limited the sample to deals occurring from 2016 onward, as this is when Ida Tin coined the term “Femtech” and established it as a distinct industry category. The estimate for CEO male remained negative and significant (b = −0.149, p < .05, Model 11). To assess whether outliers in terms of deal size were driving our results, we winsorized the dependent variable at the 1st and 99th percentiles to examine whether our analysis was driven by outlier observations. The estimate for CEO male remained negative and significant (b = −0.146, p < .05, Model 12). 12

Post hoc Analyses

Quantitative Post hoc Analyses

Given that our findings reflect the lack-of-fit perspective with male CEOs raising smaller funding amounts in Femtech, we probed aspects that would give further credence to our lack-of-fit theorizing that we did not hypothesize ex ante. We present these post hoc results in Table 4.

Post hoc Analyses.

Note. Robust standard errors in parentheses. IHS = Inverse hyperbolic sine.

p < .1. *p < .05. **p < .01. ***p < .001.

To investigate a relationship that would be consistent with the moral legitimacy account, we examined heterogeneity in ventures’ social orientation, as it speaks to Femtech’s social movement characteristic. 13 Claiming social orientation signals that ventures center their activity on social problems and value creation for others, which heighten audience expectations about being in it for the “right” reasons and, in turn, the salience of moral legitimacy. If social framings increase the salience of legitimacy demands, then out-group individuals should face stronger penalties. We re-estimated our main model separately for ventures with and without social-orientation. In the subsample of only social ventures, CEO male was more negative and significant (b = −0.192, p < .05, Model 1) than in the subsample without social ventures (b = −0.130, p = .118, Model 2). The interaction CEO male × Social venture in the full sample was negative and significant (b = −0.193, p < .05, Model 3). Male CEOs are associated with an additional 17.6% reduction in deal size—over and above the baseline sex difference—in Femtech ventures’ social orientation, echoing moral legitimacy relevance in Femtech evaluations. Figure 2 plots this interaction. 14

CEO sex × social venture in Femtech.

We next explored whether our documented relationship could be found in other female-typed sectors, starting with healthcare as the next adjacent industry sector. Though health is generally also considered broadly female-typed, it lacks the specific social movement anchoring and lifts the expectation of women’s higher competence in women-specific health needs. Using PitchBook’s “Healthcare” primary sector, the sample includes 21,279 deals by 12,639 ventures; male CEOs led 85.3% of these deals (vs. 39.8% in Femtech). Replicating our main venture fixed-effects specification with identical controls, CEO male was positive and nonsignificant (b = 0.008, p = .787; Model 4). To further examine the generalization of our findings, we then repeated the same specification in three industries that entrepreneurship and sociology commonly describe as feminine (early childhood education, elder care, sustainable fashion; Eriksen & Einarsen, 2004; Moss Racusin & Johnson, 2016; Seigner & Milanov, 2023). 15 Estimates for CEO male were directionally negative, but they were nonsignificant: early childhood education (b = −0.005, p = .984; Model 5); elder care (b = −0.305, p = .349; Model 6); sustainable fashion (b = −0.101, p = .339; Model 7). Taken together, these analyses suggest that the male fit penalty we observe is not a general feature of all female-typed industries but is specific to Femtech, where the embodied nature of women’s health and its activist framing make men’s lack of fit particularly salient.

Post hoc Interviews

To triangulate our field study findings and the proposed accounts of embodied task competence and moral legitimacy, we conducted post hoc, semistructured interviews (Jick, 1979; Patton, 2002) (for the interview guide, see Online Supplemental Appendix VII) modeled on a three-step protocol by Fuchs et al. (2019). We purposively sampled informants who view Femtech deals from different angles—a business angel, a founder/CEO, and a VC investor. All interviews (∼30 min each) were conducted by two co-authors (male and female to mitigate the effect of sex of the interviewers), audio-recorded with consent, and written up within 24 hr. After a participant provided informed consent under IRB approval, we first asked neutral questions about the participant’s recent Femtech deals (or experience, in the case of the entrepreneur) and decision processes. We then asked how the CEO’s sex shaped evaluation and why (requesting concrete examples); and finally presented our quantitative findings, without theoretical labels, to get (dis)confirmations and explanations. Given the post hoc nature and relatively small number of these interviews, they are not intended to test mediation or establish causal mechanisms. Instead, they offer illustrative accounts that we found to be broadly consistent with the explanatory logics we theorized (embodied task competence and moral legitimacy). We report illustrative quotes that we have not grammatically corrected to stay true to the informants’ voices.

In sharing a recent experience with a Femtech deal at the start of the interview, a VC investor shared that they invested in that particular Femtech venture only after a CEO turnover from a man to a woman. This anecdote is consistent with our identification strategy on looking at CEO switches within a firm: The person who stepped in as CEO, she actually had personal experiences, so she has four kids, and had, you know, some, some issues, issues to conceive. So, there was also this, like, personal motivation.

In line with this quote, participants often described evaluation concerns that align with our theorizing about the entrepreneur’s embodied task competence. For example, the female founder (of similar age as her male cofounder) highlighted the “matter-of-fact” role of founder sex in orchestrating task division between her and her co-founder: Of course, like, I did all the user interviews. I talked to all the women, even though he was the doctor, because I think … a 29-year-old guy asking a, let’s say, 50-year-old woman about their menopause, it seemed a bit off. It seemed a bit weird.

She made the same point for pitches: “[As a man] You have never tried your own product, like, you can’t talk out of first-hand experience.” The angel explicitly brought up competence perceptions when investing in Femtech ventures: “Maybe the investors assume the males are less competent. Maybe it’s a primitive brain assumption that has nothing to do with the pitch, you know, maybe it’s totally unconscious.” And the VC, who initially downplayed sex as relevant in decision-making, nevertheless grounded competence credibility in sex-specific embodiment: “Maybe it’s … that … experience … Probably, it brings more credibility … [when pitched] by a woman.”

Another recurring theme in the interviews concerned perceived legitimacy and value alignment in Femtech, which is consistent with our moral legitimacy account. For the angel, this aspect was so important that she described walking away from otherwise attractive opportunities when teams lacked meaningful female representation: When, let’s say, menopause online clinic, plenty popping up. Okay. Only gentlemen involved. … So, I have to let go because I cannot align my values to the venture. … I was really surprised how more emotional I allowed myself to be, or to choose, or also to say no to deals when I thought this is not aligned with how I think this industry should develop.

The VC stressed the mission of Femtech as an industry tackling “overlooked/under-served” women in the healthcare system and described why, in their view, male CEOs may be perceived as less legitimate advocates for this mission: You know, there was an underinvestment in women’s health … if you look at clinical trials, for example, pregnant women were not included for a very long time, and women in general were not included, right? So that’s kind of the storyline that I see a lot [in pitches]. … I think, you know, adding this personal touch, and in a way, helping people to imagine how that feels helps.

The founder further challenged whether men have moral legitimacy to address women’s neglect in healthcare: When you think about a man then doing one of these companies, you almost think, okay, he can’t really be genuine. He’s probably doing it for the capitalistic side of it, for the profit-making side of it.

Finally, when asked to interpret our quantitative results, interviewees offered explanations that were also broadly consistent with our theorized accounts. The angel, while being surprised by the result, again pointed to competence and commitment: “Generally, we hear the opposite … Maybe the investors assume the males are less competent … maybe investors believe he will be less committed than if it was a female CEO.” The founder interpreted the result through a founder-market fit lens: One criteria they’re [the investors] always talking about is founder-product, or founder-market fit, right? And…if we’re talking a market being Femtech or women’s health, a founder being a male, I can assume that’s already one of their criteria, where it’s like. This just doesn’t check here.

Discussion

Studying Femtech ventures, we revisited entrepreneurship’s “no fit deficit” assumption for men in professional equity fundraising, aiming for the most direct “apples to apples” comparison available in a real-world setting (Brush & Elam, 2024). When the same Femtech ventures are led by women rather than men, they secure roughly 13% (about USD 1 million) larger equity deal sizes. Enriching our theorizing with public accounts of controversies around male-led Femtech ventures, we have proposed two Femtech-specific plausible explanatory accounts through which gendered founder-market fit may be assessed: embodied task competence—beliefs about sex-linked expertise, and moral legitimacy—beliefs about alignment with Femtech’s activist mission.

The first contribution of our study is to challenge the assumption in entrepreneurship theorizing that male fit in professional equity fundraising is industry-invariant (Kanze et al., 2020; Tak et al., 2019). This field assumption is at odds with status expectation states theory, which predicts that penalties are possible for whoever, women or men, lacks fit with locally gendered status beliefs (Berger et al., 1972; Correll & Ridgeway, 2003). We outlined why this theoretical tension appears in entrepreneurship and examined it in Femtech, where the assumed baseline appears to reverse. Ours is one of the first studies, if not the first, to provide evidence consistent with a male lack-of-fit penalty in professional equity fundraising. Theoretically, this reframes founder-market fit in professional entrepreneurial finance from an assumed, industry-invariant male baseline to a status-contingent view influenced by local cues.

Second, we contribute to gender theories in entrepreneurship through a more granular understanding of what constitutes a “female-typed” context. Much prior research treats sector gender-typing largely on the basis of the sex representation of men and women in an occupation (Eagly & Karau, 2002) and on empirically determined numerical cut-offs (Abraham, 2020; Kanze et al., 2020). While this approach is efficient in quantitative studies, it risks simplifying the heterogeneity of female-typed domains and overgeneralizing their effects. Our findings nuance this simplification by showing that not all sectors that are female-typed by traditional measures function alike when it comes to male lack of fit in professional equity fundraising. Our empirics illustrate this differentiation, as male CEOs face a lack of fit in Femtech but not in adjacent sectors commonly considered feminine, such as early childhood education, elder care, or broader healthcare. Thus, a high sector-level representation of women is not, in itself, sufficient to trigger penalties for men in equity fundraising. Instead, the deeper contextual elements shape whether and how gender “sticks to men” in a context (Marlow, 2020).

In this vein, our study refines gender-typed contexts by suggesting that embodied task competence and moral legitimacy may serve as plausible explanatory accounts of how gendered evaluations may be activated. Embodied task competence refers to beliefs that women’s sex is linked to bodily aspects that Femtech addresses (e.g. menstruation, fertility, menopause, pelvic/sexual health), suggesting inherently greater task-relevant understanding than men. Moral legitimacy refers to beliefs that women are more aligned with Femtech’s activist mission to stand up against the long-standing neglect of women’s health needs, whereas men may be viewed as outsiders with ulterior or self-interested motives. These features distinguish Femtech from other female-typed sectors, where investor judgments may still default to presumed entrepreneurial competence as stereotypically male (Kanze et al., 2020). Our combination of status expectation states theory and feminist accounts of embodied knowledge contributes to a more granular account of when and how gender lack of fit may theoretically unfold. While task competence is a construct commonly discussed in the VC evaluations literature, moral legitimacy is less discussed. However, Femtech’s feminist movement roots supply a normative screen (Calás et al., 2009; Hendl & Jansky, 2022), meaning whether the entrepreneur is “in it for the right reasons” (Anesa et al., 2024; Suchman, 1995). Our post hoc findings on Femtech ventures’ social orientation are consistent with the idea that it is important to keep biological sex and gender distinct. Sex-linked embodiment might make task-relevant competence expectations salient, while gendered movement aspects, as prompted by the ventures’ social orientation and the CEO’s sex, could further activate moral screening.

Limitations and Future Research

While our study should be understood in light of its limitations, these also open up what we believe to be interesting opportunities for future research. First, our empirics are correlational. The venture fixed effects, extensive controls, and the battery of robustness checks mitigate, but cannot fully eliminate, endogeneity concerns. Likewise, our mechanism evidence (media reports, social media posts, and post hoc interviews) is interpretive, not statistically identified. We thus call for future research to experimentally manipulate CEO sex and measure the two plausible explanatory accounts we theorized—perceived task competence (for items, see Fiske et al., 2002) and perceived moral legitimacy (for items, see Alexiou & Wiggins, 2019)—alongside investment outcomes to test whether these perceptions mediate investors’ decisions. While such a study would require a representative, field-relevant sample of professional early-stage investors, ideally with Femtech experience that we did not have access to, we provide suggested experimental materials in Online Supplemental Appendix VIII.

Second, our evidence relies on PitchBook data. While widely used and comparatively strong on founder coverage (Brush & Elam, 2024; Retterath & Braun, 2020), it tracks ventures visible to institutional investors and omits unfunded attempts. For our results, this would mean that if, consistent with our theory, early gatekeeping disproportionately excludes men, then the men observed in our data are positively selected. In this case, our estimates are conservative as the penalty we detect emerges even when comparing “average” women to “highly selected” men. If early gatekeeping in Femtech runs counter to our theorizing and echoes dominant dynamics in other sectors (Kanze et al., 2020), this would disproportionately exclude women from our data. In that case, women captured in our data may be unusually strong, and their larger deals may reflect higher quality rather than investor beliefs about men’s performance. While we cannot rule this out fully, available descriptives are more consistent with the first scenario. 60.2% of funded Femtech deals in our data are led by female CEOs, and industry estimates put 70% of Femtech companies as having at least one female co-founder (company-level, not CEO-at-deal-time; see Trok, 2025). Read against the 74.3% of VC deals that went to male-only teams in the United States in 2024 (PitchBook, 2025), the 60.2% figure makes a systematic underrepresentation of female-led Femtech deals in our data not evident. Still, future research could triangulate across sources (e.g. regulatory filings, accelerator records, Crunchbase) and, where available, add direct measures of evaluator judgments (e.g. diligence memos, Q&A transcripts) that inform funding decisions.

Third, our interest was to examine the field’s assumption of an industry-invariant male fit in professional equity fundraising. In doing so, we focused on the CEO’s sex, because the CEO is the venture’s face for investors and the broader public (Brush & Elam, 2024; Kanze et al., 2020). However, gendered fit may also be venture team-embedded (Engel et al., 2023). Future research could incorporate the venture team’s sex composition to see whether “venture bearding” dynamics operate in reverse, meaning whether female representation (via team, board, or advisory members) attenuates penalties for male CEOs (Edwards & McGinley, 2018; Godwin et al., 2006). It would also be interesting to examine lead-investor-CEO dyads to understand homophily effects of women funding women noted in recent literature (Snellman & Solal, 2023) operate in Femtech. 16

Finally, we had access only to fundraising outcomes, not to long-term venture performance metrics. We thus cannot assess whether the fundraising patterns we document translate into differences in downstream venture performance or investor returns. However, we encourage future research to study any such effects of CEO sex. Doing so would require long-term, quantitative data on venture performance combined with information on CEO sex. Additionally, qualitative data could shed further light on internal dynamics (e.g. leadership) and how they shape investor beliefs or venture performance, where Femtech ventures could again serve as “revelatory, extreme exemplars” (Eisenhardt & Graebner, 2007, p. 27).

Practice Implications and Considerations

Our findings must be interpreted in the broader context of persistent gender inequities in entrepreneurial finance. Despite decades of scrutiny, male-led ventures continue to dominate the professional equity funding space (76.3% of VC money went to male-only teams in the United States in 2024, see PitchBook, 2025). While recent work shows that CEO sex does not predict venture performance (Brush & Elam, 2024), and even that female-led ventures provide higher revenue per dollar invested (Abouzahr et al., 2018), identical ventures are still judged more favorably when pitched by men (Brooks et al., 2014). Men are more likely to be asked about growth potential, women about risks (Kanze et al., 2018), and even government VCs in Sweden, who are required to consider equality, employ narratives that reinforce entrepreneurial potential in men, while undermining it in evaluating women (Malmström et al., 2017).

It is against this backdrop that our results indicate a penalty for men in a specific industry—Femtech. Interviews and media discussions offer interpretive triangulation consistent with the idea that evaluators may see women as more attuned to Femtech products, customers, and the moral mission of the industry. Whether these beliefs are warranted is beyond what our data can reveal; as mentioned in the limitations section, we do not have data on venture outcomes or fund returns from these investments. But even if we had these outcomes in hand, it is important to remember that what counts as “performance” is contested, and often gendered, in entrepreneurship (Justo et al., 2015). What matters here is that gendered expectations intersect with industry context to shape investment decisions in systematic ways that can penalize men, too.

Our findings must not be mistaken as evidence that gender inequality in entrepreneurial finance has generally been resolved or reversed. On the contrary, the very fact that one must turn to Femtech, an industry born out of women’s health activism (Hendl & Jansky, 2022), to find a context in which women-led ventures are favored speaks volumes about the enduring nature of a male advantage. Yet, we believe that our study is warranted and necessary. Although a male lack of fit in female-typed sectors is “expected” according to sociological gender theory, the entrepreneurship field has not been able to document it across a number of contexts (Abraham, 2020; Kanze et al., 2020; Tak et al., 2019). In that sense, had we found male-led ventures to receive more funding even in Femtech, the result would have been seen as unremarkable, upholding the prevailing assumption that men enjoy an industry-invariant fit. Our results challenge this taken-for-granted baseline. They also speak back to recent media narratives, which, relying on aggregate descriptives, have claimed that “even in Femtech, it pays off to be a male founder,” only briefly noting an emerging reversal (Bucak, 2023; Hill, 2024). 17 With our study, we do not seek to suggest parity where it does not exist, but to expose a paradox: the disruption of the assumed male default in a highly gender-salient context may be read as a sign of progress, yet it simultaneously highlights just how profoundly gender continues to impact entrepreneurial evaluation.

Interpreted in the tradition of research that identifies individual-level coping mechanisms for counteracting larger forces of gender inequity (Balachandra et al., 2019; Kanze et al., 2018; Zhang et al., 2023), our study raises the possibility that Femtech ventures may increase their prospects of higher funding amounts by employing a woman as CEO and that when they have a woman as CEO, it may pay off to stress her connection to products, customers, and the industry’s feminist and activist mission. Yet, it is important to note that while such strategies can make a difference on the margin, the beliefs about diffuse status characteristics, like gender, are powerful and unlikely to be resolved by micro-level strategies alone. Beliefs about entrepreneurship and gender do not arise in a vacuum, but stem from many sources, including mass media and academic research (Lundmark et al., 2022; Suárez et al., 2021). In that vein, this study challenges a widely held assumption of an industry-invariant male fit that reinforces existing notions of entrepreneurship as male-typed (Ahl, 2006; Marlow, 2020; Ogbor, 2000). It also underlines that Ida Tin was onto something important when she coined the term Femtech: our beliefs about gender and entrepreneurship are not static but fluid, and the words we use to talk about them matter (Hechavarría et al., 2018).

Conclusion

In this study, we challenged a field assumption of industry-invariant fit for male entrepreneurs in professional equity fundraising and advanced a theoretically more balanced alternative: founder-market fit may be status-contingent and locally cued. We proposed two plausible explanatory accounts, embodied task competence and moral-legitimacy perceptions, and provided interpretive triangulation consistent with their relevance in Femtech. In our data, the male-CEO disadvantage appears specific to Femtech, not replicating in other sectors that are female-typed by traditional measures. Our post hoc analysis suggests that venture social orientation may be an important boundary condition for the salience of moral legitimacy considerations, and is associated with stronger male-CEO disadvantage in Femtech. Using post hoc interviews for interpretive triangulation, we offered an illustrative account of how competence and legitimacy considerations may shape perceived fit in Femtech. Together, these findings shift entrepreneurship theory from an industry-invariant assumption of male fit to a more boundary-aware account of founder-market fit that highlights the role of local cues in entrepreneurial finance.

Supplemental Material

sj-docx-1-etp-10.1177_10422587261444752 – Supplemental material for Can Lack-of-Fit Penalties Apply to Male Entrepreneurs? Equity Fundraising in Femtech

Supplemental material, sj-docx-1-etp-10.1177_10422587261444752 for Can Lack-of-Fit Penalties Apply to Male Entrepreneurs? Equity Fundraising in Femtech by Hana Milanov, Benedikt David Christian Seigner and Erik Lundmark in Entrepreneurship Theory and Practice

Footnotes

Acknowledgements

We are grateful for the feedback received on versions of this manuscript at the Babson College Entrepreneurship Research Conference 2024, the “Menstruation, Maternity, and Menopause: Milestones That Shape Women’s Work Experiences and Careers” symposium at the Academy of Management Conference 2024, at the ETP paper development workshop at the Australasian Consortium for Entrepreneurship Research Excellence 2025, and at research talks at IMD Business School, Macquarie University’s Innovation, Strategy, Entrepreneurship (ISE) Research Centre, and the Gender & Diversity Workshop Series of IE University. We also thank faculty members of IE University’s entrepreneurship department, and (in alphabetical order of their last names) Oliver Alexy, Aaron Anglin, Donato Cutolo, Dimo Dimov, Maw Der Foo, Tobias Kretschmer, Aaron McKenny, Lucia Naldi, Anna Carmella Ocampo, Joe Ploog, Jack Sadek, Juan Santaló, Jeroen Verbouw, and Henrik Wesemann Lekkas for their helpful feedback. We are particularly grateful to Cristina Cruz, Director of the IE Center for Families in Business, for generously providing funding for the data used in this study. Finally, we are grateful for the helpful and developmental guidance of our editors, Diana Hechavarria and Cristiano Bellavitis, and three anonymous expert reviewers.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This article was partially funded by MICIU /AEI /10.13039/501100011033 / FEDER, UE, Grant No. PID2024-155788OA-I00.

Supplemental Material

Supplemental material for this article is available online.

Notes

Author Biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.