Abstract

This study develops a theory of social proof in angel investing. We propose that availability bias leads angel group members to copy the highly visible decisions of new investors evaluating the same opportunity (external social proof) and overlook the more insightful reinvestment decisions of prior investors (internal social proof). We also theorize that more experienced investors generally herd less but selectively imitate knowledgeable investors from prior rounds. A study of investments by 469 angel group members and a vignette experiment with 367 participants support our hypotheses. Our findings contribute to research on social proof, decision-making under uncertainty, and investment experience.

A prudent man will always try to follow in the footsteps of great men.

Niccolò Machiavelli, The Prince (1532)

Introduction

Angel investors—high-net-worth individuals who invest their own money in entrepreneurial ventures (Murray et al., 2020)—make investment decisions under extreme uncertainty (Huang & Pearce, 2015; Wiltbank et al., 2009). Unlike private equity funds or stock traders, angel investors typically invest before new ventures make their first sales, and without reliable data on financial performance, customer satisfaction, or market development (Huang & Pearce, 2015). The already considerable complexity of evaluating early-stage ventures has increased with the recent formation of angel groups in which angel investors pool knowledge and capital in order to access more deal flow (Bonnet et al., 2022; Drover et al., 2017). While this results in more investment opportunities, it also presents angel group members with a dilemma—they face so many investment opportunities that they cannot evaluate all of them in detail (Antretter et al., 2020a; Kerr et al., 2014).

Fortunately, angel group membership comes with a shortcut for evaluations. Rather than determining the value of all opportunities on their own, investors can consider the investment decisions of other group members as social proof—endorsements that can be copied when investors are uncertain about an opportunity (Cialdini, 1984; Hallen & Eisenhardt, 2012). These endorsements can come from various sources, such as fellow investors looking to make their first investment in the venture (i.e., external investors), or investors who have already invested in the focal venture and are considering a follow-on investment (i.e., internal investors). Potential investors can use others’ decisions as a quick indicator of the attractiveness of an investment opportunity (Gulati & Higgins, 2003; Malhotra et al., 2015) without expending real effort to understand the value of that opportunity (Courtney et al., 2017; Logue & Grimes, 2022). However, social proof in angel groups remains largely underexplored. We therefore ask: Do angel group members use social proof in their investment decisions? If so, what type of social proof do they utilize?

Further complicating the role of social proof in angel group members’ investment decisions is the fact that not all investors are alike. Notably, angel group members differ in their investment experience (for a discussion, see Botelho et al., 2021). For inexperienced group members, social proof can help compensate for a lack of deep investment knowledge and can teach them the ropes of investing (Bandura & Walters, 1977). However, relying on social proof may become less appropriate as the investor becomes more experienced (Blohm et al., 2022). After all, experienced investors can usually identify promising opportunities without the help of others (Campbell et al., 2014; Elliott et al., 2008). To them, following the crowd may seem a sure way to obtain only average investment returns. Therefore, we ask: Do investors stop relying on social proof as they become more experienced?

This article draws from the social proof principle (Cialdini, 1984) to develop a theory of social dynamics within angel groups. Inspired by Welch (1992), we differentiate between two kinds of social proof: internal social proof (i.e., decisions by investors who have previously invested in the opportunity) and external social proof (i.e., decisions by investors who have not previously invested in the opportunity). We propose that the value of these two kinds of social proof differs. Specifically, we suggest that relying on external social proof in which little information is revealed qualifies as indiscriminate herding (Rao et al., 2001; Spyrou, 2013). In contrast, we propose that selectively imitating internal social proof reveals useful, private information that can improve investment returns. Finally, we theorize that the use of internal and external social proof depends on investor experience—inexperienced investors herd on more visible but less valid external social proof, while experienced investors use the less visible but more useful internal social proof. This may help explain why experienced angel investors achieve superior returns (Blohm et al., 2022; Capizzi, 2015). The results of two analyses using data on the investments of 469 angel group members and the responses from 367 investors in a vignette experiment support our hypotheses.

Our study makes three primary contributions. First, we advance the theoretical literature on the social proof principle (e.g., Bapna, 2019; Cialdini, 1984). While prior research shows that investors copy social proof (e.g., Gaba & Terlaak, 2013; Rao et al., 2001), it has rarely investigated which kind of social proof is used by whom. Our theoretical framework addresses this gap by differentiating between the two types of information and explaining why external social proof produces unproductive herding (Spyrou, 2013) while internal social proof aggregates useful knowledge (Evans & Foster, 2011).

Second, we draw on the distinction between internal and external social proof to uncover an availability bias (Tversky & Kahneman, 1973). Although external social proof is not particularly useful, it is highly visible, so angel group members use it more than the more valuable but less visible internal social proof. Consequently, for some investors, what they see becomes all there is (WYSIATI; Kahneman, 2011). In this regard, our theorizing and findings answer recent calls to study angel investments as a dynamic social process (e.g., Butticè et al., 2021; Murray et al., 2020; Wesemann & Antretter, 2023), and add to the study of biases in angel investing (e.g., Blohm et al., 2022; Harrison et al., 2015; Maxwell et al., 2011).

Finally, we contribute to the literature on the role of experience in angel investing (e.g., Botelho et al., 2021; Capizzi, 2015; Croce et al., 2023) by showing that experienced angel group members generally copy other investors less, and pay more attention to internal social proof than external social proof. They engage in less indiscriminate herding on external social proof and more selective imitation of internal social proof. These findings indicate that experience does not make investors act independently but teaches them which peer behavior is linked to better investment performance. They excel at analyzing not only opportunities but also their peers.

Social Proof Model: Angel Group Members’ Decisions

In the following sections, we build on the social proof principle (Cialdini, 1984) as well as the literature on angel decision-making (e.g., Gregson et al., 2013; Hallen & Pahnke, 2016; Mason et al., 2016) and angel investment groups (Antretter et al., 2020b; Bonini & Awuni, 2023; Bonnet et al., 2022) to build a social proof model of angel group members’ decisions. We theorize that angel group members (1) base their decisions on social proof, (2) are particularly prone to follow the decisions of investors who have not yet invested in the venture (i.e., external social proof), and that investors with more experience (3) generally rely less on social proof (4) but when they use it they selectively imitate the decisions of investors who already know the venture (i.e., internal social proof).

Social Proof and Angel Group Members’ Investment Decisions

The angel investment market has changed in recent years. While angel investors used to act alone, they now increasingly invest through semi-formal or professionally organized groups (e.g., Bonnet et al., 2022; Gregson et al., 2013; Mason et al., 2016). This trend toward structured angel groups has fundamentally transformed the sector, giving angel group members access to a broader deal flow that allows them to make more deals (Kerr et al., 2014) and build diversified early-stage investment portfolios (Antretter et al., 2020a). However, as deal flow increases, investors have less time to analyze each investment opportunity. Unlike venture-capital funds, angel group members are boundedly rational individuals, not organizations. Therefore, they cannot scale their attention or expertise by hiring more analysts to evaluate opportunities (as a venture-capital firm might). These cognitive limitations make angel group members vulnerable to information overload (Hallen & Pahnke, 2016). It can be overwhelming to screen hundreds of investment opportunities to find a “diamond in the rough” (Huang & Pearce, 2015, p. 641). A potential solution is to use peers’ decisions as a screening mechanism to identify the most promising investment opportunities. In other words, rather than making decisions independently, angel group members may view investments by their peers as an indication to invest.

Basing a decision on the decisions of others is often referred to as social proof (Asch, 1956; Bikhchandani et al., 1992; Cialdini, 1984). When copying the decisions of others in uncertain situations, individuals learn by observing their peers’ behaviors and thought patterns (Bapna, 2019; Bikhchandani et al., 1998; MacCoun, 2012; Wesemann & Antretter, 2022). Social proof has been used to study financial decision-making for decades (for a review, see Spyrou, 2013). For example, in initial public offerings (IPOs), analysts copy each other (Rao et al., 2001) and investors adjust their valuations to be closer to those of other investors (Aggarwal et al., 2002; Amihud et al., 2003).

Research on social proof in the context of early-stage investments in venture capital emerged around 20 years ago (for an early example, see Lee & Wahal, 2004). This stream of literature indicates that venture-capital herding depends on general market conditions (Gompers et al., 2008), that the reputation of venture capitalists affects later IPOs (Nahata, 2008), and that venture capitalists herd on media attention (Petkova et al., 2013). Since 2012, research has mostly focused on the more recent phenomenon of crowdfunding (starting with Zhang & Liu, 2012). Among other insights, this research has shown that crowdfunders follow fellow platform members more than external investors (Colombo et al., 2015), and that social proof is most effective at a campaign’s start (Bhargava et al., 2024), when it is combined with external signals like product certifications (Bapna, 2019), and when prior investors reveal their identities (Jiang et al., 2022).

The fact that investors in these groups rely on social proof is not particularly surprising—there are too many opportunities to evaluate each in detail. This problem is even more pronounced in angel groups, where boundedly rational individuals invest their money in overwhelmingly complex deals under considerable uncertainty (Mason, 2016). As angel group members do not have the cognitive capacity required to evaluate all opportunities, we expect them to also look for external validation in the behavior of others. We hypothesize:

External Versus Internal Social Proof

While the investments of others look alike in contexts like crowdfunding, we propose that social proof in angel groups can be either external or internal.

External Social Proof

External social proof refers to the investments of other angel group members presented with the same investment opportunity. This construct is consistent with social proof in other contexts, such as stock markets (Welch, 1992) and crowdfunding (Bapna, 2019; Vismara, 2018). The argument for relying on this type of social proof is simple—if something draws the attention of many, the “wisdom of the crowd” suggests it is likely of high quality (Surowiecki, 2005). More specifically, if different investors have different competencies, their collective assessment can more accurately approximate the true value than any individual assessment might. As such, external social proof confers status on an organization and convinces individuals to invest (Paik et al., 2023), sometimes to the point where actual information on the underlying company is lost in the process (Bindra et al., 2022).

Internal Social Proof

Internal social proof refers to information obtained from investors who have previously invested in the focal venture and are, therefore, privy to internal venture information (Shafi et al., 2020; Warnick et al., 2018). Such information may include detailed performance metrics, knowledge of successes and failures, and insights into the founders’ strengths and weaknesses (Huang, 2018). Internal social proof does not exist in contexts where current investors do not have access to insider information, such as stock markets (e.g., Google’s investors have no company information that is not available on the internet) and crowdfunding (i.e., when thousands of people coinvest, the entrepreneur does not interact with them individually). It only arises in circumstances where a company’s investors become privy to exclusive, private information.

Some angel group members have valuable private information on ventures owing to their prior interactions with them, and they may not want to openly share that information. In addition, investors rarely invest all the money they earmark for a venture immediately. Instead, they typically retain some funds for follow-on rounds (Agrawal et al., 2018; Zhelyazkov & Tatarynowicz, 2021). This sequential investment approach allows them to refuse to recommit to the venture if it fails to meet expectations (Tennert et al., 2018). Therefore, a voluntary reinvestment is a valuable source of information for new investors, as it indicates that insiders looking “behind the curtain” approve of the opportunity (Shafi et al., 2020).

The Relative Visibility of External and Internal Social Proof

Of the two types of social proof, only external social proof is highly visible. This visibility arises from its creation in non-shareholder social contexts. More specifically, external social proof in angel groups stems from discussions of investment opportunities among people who are not yet shareholders. Interested group members share their impressions after hearing a venture’s pitch. They may even start chat groups with other interested investors. If they are convinced of a venture’s likely success, they commit and often try to convince others to co-invest. This is, in part, a result of their excitement about their new investment and, in part, because they want to shield themselves from reputational damage in case of failure (Butticè et al., 2021; Scharfstein & Stein, 1990). This makes external social proof highly visible to all angel group members.

Internal social proof is less visible. Investors who are already shareholders rarely attend public discussions on ventures in their portfolios. Instead, they rely on internal channels to communicate with the board and other shareholders. These stakeholders are more informed and their shared access to confidential information allows discussions to run more freely in private settings.

Moreover, publicly opting out of a reinvestment can feel like a betrayal to the entrepreneur (Shafi et al., 2020). Investors and entrepreneurs typically form personal relationships throughout their collaboration (Collewaert, 2016). When the personal relationship is good but the investment is not, the investor wants to find the least problematic way of avoiding “throwing good money after bad.” This introduces agency problems, as the goals of different stakeholders diverge (Eisenhardt, 1989). While agency arguments are most commonly applied to relationships between investors and investees, they can also apply to relationships among members of an angel group (Meuleman et al., 2010). A prior investor wants new investors to act on information that presents the venture favorably, while new investors seek information that accurately reflects reality. To maintain the venture’s reputation, prevent down rounds, and avoid making an investment look like a mistake (Macey, 2010), prior investors might avoid publicizing a decision to drop out in the hope that others will still invest (Tergiman & Villeval, 2023). Therefore, prior investors often “quiet quit” on investments, making it even more difficult for fellow angel group members to obtain information about a venture from existing shareholders (Mitteness et al., 2016).

In summary, external social proof is more visible and accessible than internal social proof. As all social proof increases investment likelihood (H1) and as external social proof is more visible, we expect the share of external social proof (of all social proof) to moderate the relationship between social proof and the likelihood of investment. We hypothesize:

Social Proof and Investment Experience

We also propose that angel group members differ in their reliance on social proof. This distinction has received little attention in the early-stage investment literature, primarily because most studies of social proof in early-stage investments focus on anonymous crowdfunding. However, we suggest that investment experience changes the effect of social proof on investment likelihood in several ways. First, and most intuitively, experienced investors depend less on social proof because their experience enables them to evaluate opportunities themselves. Experience teaches investors what information matters most (Croce et al., 2023) and how to obtain that information (Meuleman et al., 2010). Their intuition tells them where to look (Murray et al., 2020) and what information to double-check (Warnick et al., 2018).

Second, experienced angel group members trust social proof less because they know its shortcomings. The presence of many co-investors can even lead to competition, which drives up participation prices (Ning et al., 2015). Often, this results in overpriced investment rounds into which investors unquestioningly follow each other (Rao et al., 2001).

Third, experienced investors are less likely to take part in a popular investment opportunity with the aim of establishing themselves as part of an investor group. The “feeling of being part of the entrepreneurial community” (Civardi et al., 2024, p. 306) is an essential aspect of individuals’ motivations to join investment groups and most pronounced among inexperienced investors who are not yet fully embedded in the ecosystem and wish to become part of it by participating in popular investments (Deci & Ryan, 1985; Sabia et al., 2022). This makes experienced investors less likely to react to social proof with a fear of missing out (FOMO)—an “apprehension that others might be having rewarding experiences from which one is absent” (Przybylski et al., 2013, p. 1841). We hypothesize:

Experienced Investors Use More Internal Social Proof

While we hypothesized above that experienced investors are less sensitive to social proof in general, we also theorize that (1) internal social proof is more valuable and (2) experienced angels are more equipped to obtain internal social proof.

Internal Social Proof is More Valuable

External social proof is often based on incorrect information. It comes from voluntary disclosures from an entrepreneur, who is selling an idea to obtain funding (Lee & Huang, 2018; Sine et al., 2022). Entrepreneurs are bound only by the law’s general rules and are often desperate to raise funds (Wilhelm et al., 2023), so they tend to exaggerate achievements (Murray & Fisher, 2023). These conditions can negatively affect wisdom-of-the-crowd assessments (Stevenson et al., 2022; Surowiecki, 2005), which can only be accurate if the underlying information is not systemically biased (Budescu & Chen, 2012). External social proof based on entrepreneur-provided information is often “grounded in little or no ‘real’ information” (Pollock et al., 2008, p. 338).

In contrast, internal social proof arises from the opinions of insiders who have a contractual right to receive regular, detailed, unfiltered reports on the venture’s actions and performance. In other contexts, this would be considered illegal insider information (Meulbroek, 1992). Such preferential access allows internal investors to evaluate the entrepreneurs as they build their ventures, lead employees, and solve problems (Cipollone & Giordani, 2019; Solodoha et al., 2023). If their observations leave them unconvinced, they will withdraw from later funding rounds (Shafi et al., 2020). Therefore, reinvestments by prior investors represent positive signals (Evans & Foster, 2011) that suggest that insiders consider the venture a good investment.

Moreover, external social proof does not meaningfully aggregate information. Instead, it stems from various interpretations of the same pitch, slide deck, and financial statement (Vismara, 2018) and does not resolve uncertainty about the venture’s product, market, or team (Bapna, 2019). In contrast, internal social proof aggregates the various types of information collected by prior angel investors (Mason et al., 2019). For example, some focus on financial details (Cipollone & Giordani, 2019), while others focus on the entrepreneur (Block et al., 2019), internal processes (Lee & Huang, 2018), or sustainability (Wesemann & Antretter, 2023). As internal social proof aggregates these different viewpoints, it provides a more reliable overall picture of the venture (Alevy et al., 2007).

Experienced Angels are Better at Obtaining Internal Social Proof

More experienced angels are better at obtaining and interpreting peer information that is not shared voluntarily. Experienced angel investors tend to have better intuition (Murray et al., 2020) that tells them what to look for and which questions to ask (Warnick et al., 2018). Indeed, these investors often rely on their gut feelings to learn truths about investment opportunities (Huang, 2018; Huang & Pearce, 2015). This can help them uncover hidden information (Piezunka & Dahlander, 2015), focus on relevant decision criteria (Bapna, 2019), and vet information (Croce et al., 2021). Experienced investors’ relational embeddedness further enables this process through long-term collaborations (Guenther et al., 2022; Wang et al., 2022). This social embeddedness generates trust that these investors will not abuse any information they receive, thereby facilitating more information-sharing (Uzzi, 1997) and efficient knowledge transfers (McEvily et al., 2003). Ultimately, this helps experienced investors obtain otherwise hidden information from their colleagues (Mitteness et al., 2016). Especially in contexts characterized by high information asymmetry, like early-stage investments, relational embeddedness can be useful for uncovering high-quality information about a venture (Meuleman et al., 2010). Using experience-based intuition, angels can obtain private information and reduce information asymmetries (Croce et al., 2023), ultimately minimizing herding mistakes (Ioannou & Serafeim, 2015).

In comparison, inexperienced investors lack the skills and networks needed to collect hidden information, making internal social proof a “black box” (Bascle & Jung, 2023, p. 173). Moreover, they are less likely to see the qualitative differences between external and internal social proof. As only external social proof is easily obtainable, they may fall into the cognitive bias of “what you see is all there is” (Kahneman, 2011, p. 84) and rely on the more easily obtained external social proof (Blaseg & Hornuf, 2024). Therefore, we propose that although experienced angel group members are less drawn to social proof in general, they are more sensitive to internal social proof. Based on the above, we offer the following hypothesis:

Study 1: Field Study

We tested our hypotheses using field data on a U.S.-based angel group (Study 1) and a vignette experiment with manipulated levels of social proof (Study 2).

Study 1: Context of the Field Study

We tested our hypotheses using investment and investment–return data from a large, U.S.-based angel group. We were granted access to the group’s deal-monitoring system, which allowed us to see their investments, including information on who participated in each round as well as deal-specific information, such as who had already invested in each venture. At the time of our study, the angel group had 708 members who had joined on personal invitation. Of these, 595 had made at least one investment. The angel group was a pure investment network not linked to other social contexts like alumni networks or professional associations.

Early-stage ventures that sought funding from the group’s members submitted information, including a pitch presentation, fact sheets, financial breakdowns, and other details, such as the founders’ views on potential exit scenarios. The group’s gatekeepers pre-screened investment opportunities and decided whether an early-stage venture’s material would be presented to the group’s members (Paul & Whittam, 2010). The gatekeepers only admitted early-stage investments they felt met the group’s overall investment criteria (in terms of, e.g., stage of development and investment size). These investment opportunities were first communicated in emailed newsletters and then discussed in regular, in-person, social gatherings at which group members interested in specific opportunities could discuss them with each other. The meetings, which usually occurred once per month at various locations, included an initial presentation of selected ventures, Q&A sessions, and informal networking sessions during which investors could discuss new investment opportunities, try to assess each other’s opinions, and collect additional information from each other.

After the networking sessions, investors decided individually whether to invest in each opportunity. They could find information on how many investors had newly committed to investing in the venture using the group’s updates and website, but they had no immediate access to additional information. As such, each angel investor had to discover on their own whether prior investors had reinvested or had any information to share about the venture. The group’s size and efficient but incomplete communication made this network ideal for our investigation, as it allowed for social ties and information-sharing but was loose enough for information asymmetries to exist among investors.

Our dataset contained data on 85,602 investment decisions made over 319 deal rounds in 106 ventures. An investment decision refers to an investor’s exposure to an investment opportunity and their decision on whether to invest (i.e., both investment and rejection constitute an “investment decision”), and the actual overall investment rate was 6.36%. On average, each investor had invested USD 42,005 in their portfolio of early-stage ventures. We removed all follow-on investment decisions by group members who had previously invested in the respective company (to avoid cases in which investors already had proprietary information), resulting in 77,312 investment decisions made by 469 angel investors. Of these decisions, 4,044 were decisions to invest (5.23% investment rate).

With only 5.23% of decisions resulting in an investment, a random sampling of data would result in an unbalanced dataset that would be heavily skewed toward non-investment decisions. Although this makes a robust statistical analysis difficult, it can be solved by using a case–control design that matches each investment decision with a fixed number of non-investment decisions (King & Zeng, 2001). This design is commonly used in early-stage investment studies, as it minimizes sampling bias (Zhelyazkov & Tatarynowicz, 2021). In line with current practice in management research, we matched every investment with 10 non-investments (e.g., Maula & Lukkarinen, 2022; Sorenson & Stuart, 2008). This ensures that both investment and non-investment cases are well-represented and provides sufficient variation for statistical modelling while maintaining the overall characteristics of the dataset. Therefore, our final sample consisted of 44,484 investment decisions made between 2008 and 2021. We collected all available venture information (e.g., investment date, the amount invested, and the agreed share price). As we had access to all investments and the respective background information, we had full transparency on the internal and external social proof for a venture (i.e., decisions on new investments and reinvestments).

Study 1: Methods of the Field Study

In line with previous research on similar investment decisions (e.g., Maula & Lukkarinen, 2022; Sorenson & Stuart, 2008; Zhelyazkov & Tatarynowicz, 2021), we used conditional logit modeling (equivalent to fixed effects logistic regression; Stata: clogit) for our estimations of investment likelihood. This approach avoids pseudo-replication problems and allows us to account for fixed firm characteristics and, thereby, avoid issues related to unobserved variance between firms, such as differences in venture risk (Ahlers et al., 2015), legal institutions (Hornuf & Schwienbacher, 2018), and market attractiveness (Shafi et al., 2020). While theory and prior publications endorse the use of a conditional logit model, we also tested the correctness of our fixed effects assumptions by calculating the Sargan–Hansen (SH) statistic (for a similar approach, see Collewaert et al., 2021). The test yielded statistically significant results (SH = 148.66, Chi-square = 13, p < .001), which also support the use of a fixed effects model (as opposed to a random effects model).

The ventures in our sample completed consecutive investment rounds with the angel group and investors could invest during different rounds, each associated with different levels of social proof (i.e., number of co-investments). Our dataset included complete information on the investors’ decisions, so we had data on the level of internal and external social proof available to each investor. This data captured the decisions of different angel investors regarding the same venture at different levels of social proof. This approach is well-suited for analyzing investment decisions nested in communal deals, as multiple deals per venture create variation in outcomes while accounting for unobserved variables, such as venture quality.

Investment decision: We created a binary dependent variable that took a value of 1 if the angel group member invested and 0 otherwise.

Social proof: We operationalized social proof by taking the sum of all new investments and reinvestments committed to a venture at the time the angel group was presented with the opportunity.

Share of external social proof (of all social proof): We calculated the external share of social proof as the number of new investments divided by all investments (number of new investments and reinvestments). For example, if three new group members and one already invested group member commit to a deal, the share of external social proof is 0.75.

Investor experience: We followed previous research (e.g., Antretter et al., 2020a; Bonini et al., 2018) and operationalized investment experience as the natural logarithm of the number of investments each angel group member made in the network before the focal transaction.

Controls: Our first two control variables accounted for the possibility that existing relationships affected early-stage deal decisions (Wang et al., 2022). As such, we controlled for group-led deal, a dummy variable that indicated whether the deal was initiated by a group member or introduced by an alternative source (0 = external stakeholder; 1 = group member). The second control variable, group first round, accounted for whether the focal investment round was the first time the venture raised money from the angel group. Third, as the ratio of investors to opportunities may affect information cascades (Vismara, 2018), we controlled for group activity, which measured the number of active investors in the group at the time of the deal. Fourth, we controlled for average prior investments—the logarithm of the amount currently committed angel group members had previously invested in previous deals—to account for high-status investors’ outsized effect on fundraising (Rao et al., 2001).

We also included several investor-level controls. We controlled for investor age as a proxy for knowledge accumulated before joining the investor network (Greenwood & Nagel, 2009). In addition, we accounted for investor education, which we coded based on LinkedIn profiles, as education can affect perceptions and knowledge access in specific industries (Blohm et al., 2022). We also controlled for investor gender (0 = male; 1 = female), which has been shown to affect personal decision-making processes (Harrison & Mason, 2007). Finally, our conditional logit model controlled for all fixed venture characteristics.

Study 1: Results of the Field Study

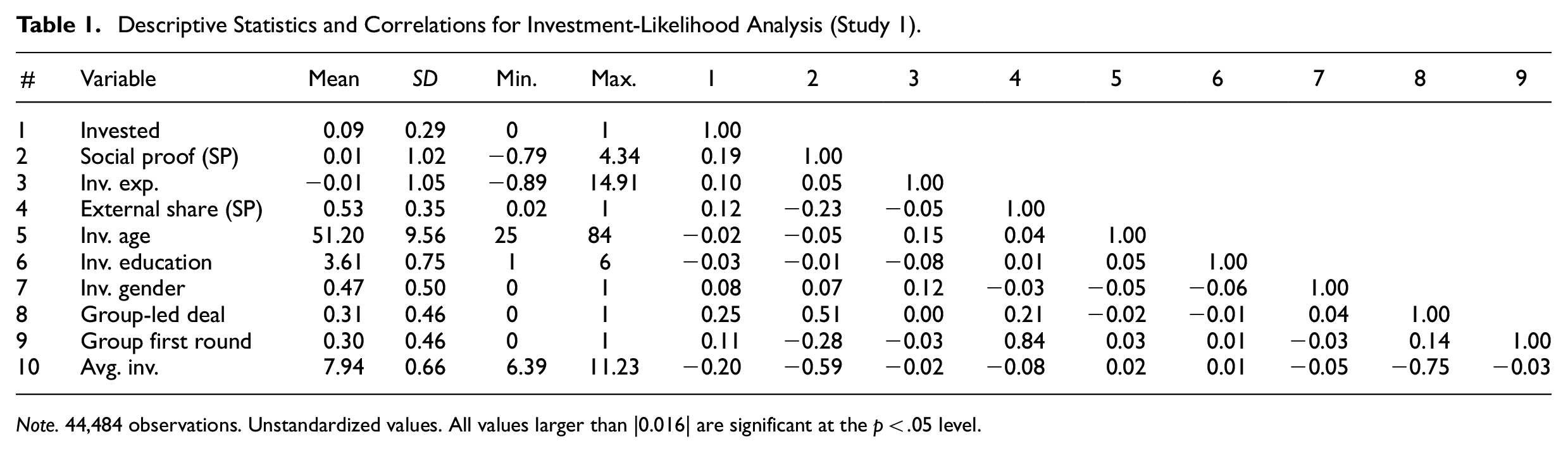

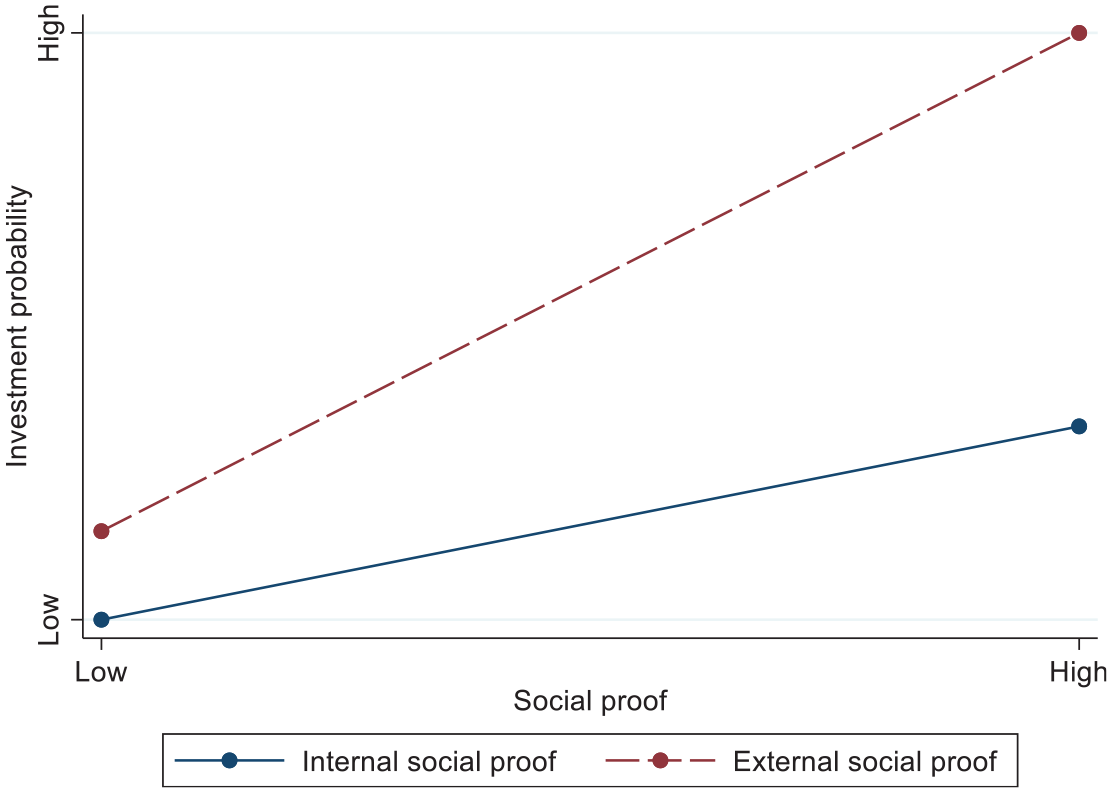

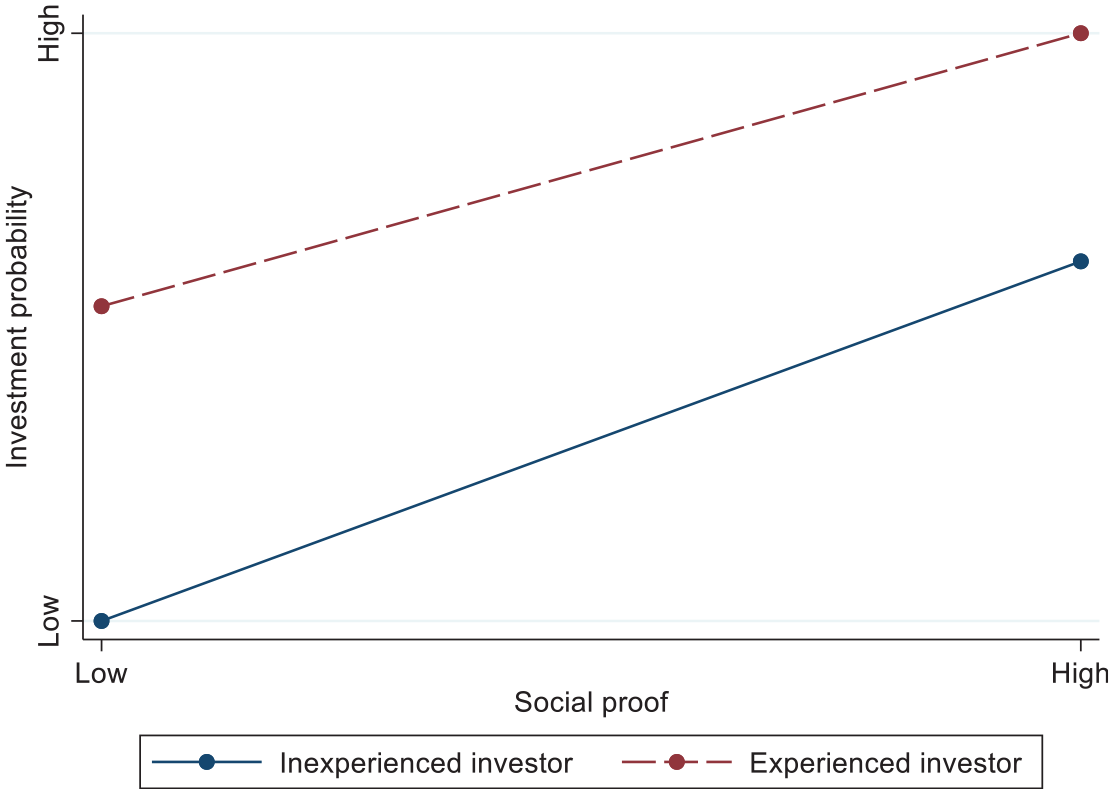

Table 1 provides the descriptive statistics and correlations for the unstandardized variables. Table 2 presents the analysis in which all non-binary independent variables are standardized and conditional fixed effects are included for each specific venture (Stata: clogit) with robust standard errors. Model 1 reports the baseline model of control variables and investor experience. Model 2, which includes social proof (β = .389, p < .001), indicates that the greater the amount of social proof, the more likely angel group members are to invest in that venture. This finding supports H1. Model 3 adds the first moderator and shows that the higher the share of external social proof (of all social proof), the stronger the positive relationship between the amount of social proof and the investment likelihood (β = .434, p < .001). These findings support H2. Model 4 introduces investor experience as a moderator. Its effect is also significant (β = −.023, p = .034), which indicates that the greater the investor’s experience, the weaker the positive relationship between the amount of social proof and the investment likelihood. This finding supports H3. Model 5 introduces the three-way interaction. It shows that the positive moderation by the share of external social proof (in the positive relationship between the amount of social proof and the investment likelihood) is weaker for more experienced investors (β = −.219, p < .001). This finding provides support for H4.

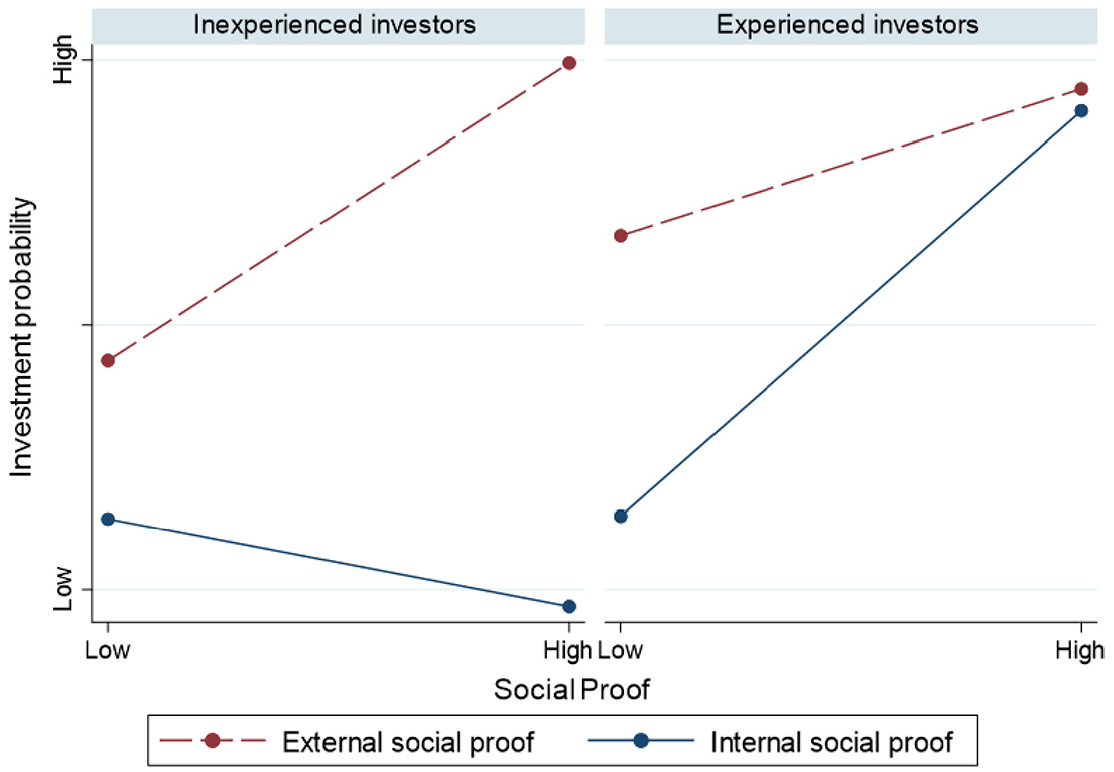

Descriptive Statistics and Correlations for Investment-Likelihood Analysis (Study 1).

Note. 44,484 observations. Unstandardized values. All values larger than |0.016| are significant at the p < .05 level.

Models for Investment-Likelihood Analysis (Study 1).

p < .001, **p < .01, *p < .05.

Figures 1 and 2 show the moderations, and Figure 3 illustrates the three-way interaction. For illustrative purposes, Figure 3 treats the social-proof type and experience as binary variables (i.e., all angel group members with experience above the median of the number of investments are considered “experienced” and all others are considered “inexperienced”; all ventures with a share of external social proof above the median are viewed as emphasizing “external social proof” and all others are viewed as emphasizing “internal social proof”). In Figure 3, several of the theorized effects are evident. First, we see that in the absence of social proof (left side of both graphs), experienced investors have a higher investment likelihood, which suggests that they make investments even before social proof emerges. Moreover, we see that experienced angel group members are less responsive to increasing external social proof than inexperienced angel group members (dashed red lines), and that experienced angel group members are more responsive to increasing internal social proof than inexperienced angel group members (solid blue lines).

Moderation: social proof * external share of social proof.

Moderation: social proof * investor experience.

Three-way interaction (Study 1).

These results are also notable in terms of their effect sizes. Overall, greater social proof (+1 SD) is associated with a 5.32% increase in investors’ investment likelihood. However, this increase depends heavily on the type of social proof and investor experience. When social proof is largely external, an increase in social proof (+1 SD) leads to an 8.29% increase in investment likelihood for inexperienced angels but only a 3.27% increase for experienced investors. In contrast, when social proof is mostly internal, an increase in social proof (+1 SD) leads to a 1.99% decrease in investment likelihood for inexperienced angels but an 11.37% increase for experienced investors.

Robustness Tests

We also conducted a series of robustness tests. First, we ran our main analysis without control variables and found that all effects maintained their direction and significance (H1: β = 0.989, p < .001; H2: β = .394, p < .001; H3: β = −.171, p = .001, H4: β = −.199, p < .001). Second, while theory and data support the use of our main fixed effects logit model, we also tried a random effects model. All effects maintained their direction and levels of significance (H1: β = .382, p < .001; H2: β = 1.283, p < .001; H3: β = −.021, p = .046, H4: β = .791, p < .001). Third, we tested a regular logit model without nesting the data in the companies and again found support for our hypotheses—social proof is associated with more investments (H1: β = .900, p < .001), especially when it is external (H2: β = .714, p < .001). Experienced angels still herd less (H3: β = −.145, p < .001), but they are more sensitive to internal social proof (H4: β = −.318, p < .001). Fourth, we excluded first-round investments, as these could, by definition, contain no prior investments and, therefore, only offer external social proof. Again, all effects except those related to H3 maintained their direction and level of significance (H1: β = .368, p < .001; H2: β = .703, p < 0.001; H3: β = −.006, p = .624, H4: β = −.106, p < .001). Fifth, we repeated our analysis while retaining the previously excluded angel investors who had already invested in the company. We originally excluded them because their insider knowledge of companies makes their investment decisions unrepresentative of the type of angel investment decisions we want to investigate (i.e., investment decisions of investors without insider knowledge). Their inclusion did not change the results for H1, H2, and H4, but those for H3 became insignificant (H1: β = .253, p < .001; H2: β = .397, p < .001; H3: β = −.013, p = .188; H4: β = −.106, p < .001). The non-support for H3 is interesting, as it suggests that already invested angels are often experienced but still interested in both kinds of social proof. While this matter deserves additional exploration, it seems to suggest that committed investors may suffer from confirmation bias (seeing new investments as a confirmation of their past rationalizations; Tversky & Kahneman, 1974) or an increased endowment effect (where seeing others compete for something one is endowed with may increase the attachment; Kahneman et al., 1991). Sixth, given the visual similarity of the slopes in Figure 2, we ran additional marginal effects tests at high and low values of our moderator (±1SD) while holding all other covariates at their means. A contrast analysis between the two slopes showed that they differ significantly from each other (contrast dy/dx:−0.091, p < .001). A likelihood ratio (LR) test also showed that the interaction model improves fit relative to the restricted model without interaction (LR χ2 = 3.92, p = .048).

Study 2: Vignette Experiment

We conducted a second study to validate the role of experience in the reliance on internal and external social proof, as well as rule out alternative explanations. This study involved a vignette experiment where investors with varying experience levels evaluated investment opportunities. The investment opportunities were identical in every regard except for randomized variation in the type of social proof. While this experiment lacks the nuanced social interactions observed in the angel group from Study 1, it isolates the interaction between social proof type and investor experience. This isolation serves as a conceptual replication (also see Derksen & Morawski, 2022), enabling a complementary test of our theoretical mechanisms. To ensure transparency and rigor, we pre-registered this experiment on aspredicted.org (https://aspredicted.org/D6W_HHQ).

Study 2: Context of the Experiment

Participants

In line with previous research, we recruited participants with investment experience through the online survey-recruiting tool Prolific in October 2023 (e.g., Liao et al., 2024; Zunino et al., 2022). While these participants are not identical to the angel group members of Study 1 (e.g., the Prolific participants are not necessarily part of formal investment groups and tend to invest less money overall than the angel group members in Study 1), this conceptual replication with a broader sample allows us to test the findings from Study 1 in a more general investor population.

We invited 500 individuals to participate in the survey and asked them to evaluate three investment opportunities each. We required participants to be active investors from the United States or Great Britain. They could not be unemployed or students, and they had to have survey-approval ratings on Prolific of at least 98%. In our survey, we asked participants to confirm that they were employed and active investors, and removed 126 individuals who stated that they were not. We also dropped seven individuals who did not pass our attention checks and removed nine incomplete evaluations. All remaining participants were included in the study, resulting in a final sample of 367 individuals who completed 1,078 venture evaluations.

Study 2: Methods of the Experiment

In line with established practice (e.g., Huang et al., 2021), we asked participants to read each venture’s pitch before indicating their impressions of that venture. We randomly allocated participants to one of two conditions: Condition 1, in which external social proof was present (i.e., the description stated that other new investors not previously associated with the venture had already committed to the deal); and Condition 2, in which internal social proof was present (i.e., the description stated that existing investors had already reinvested). The condition randomization took place separately for each of the three pitches, such that an investor could, for example, be exposed to one pitch with external social proof and two pitches with internal social proof, each of which they evaluated immediately after the respective pitch.

Dependent variable: Investment Success

We followed previous entrepreneurial finance research and measured our dependent variable using a scale covering how successful the participant expected the investment opportunity to be. Specifically, we adapted the scale by Lee and Huang (2018), which asks participants to assess whether a venture will grow to have 100+ employees, will be successful in obtaining the investments it needs, and will be successful in negotiating with investors. All items were evaluated on a Likert scale ranging from 1 = “strongly disagree” to 5 = “strongly agree.” The consistency between the three items was strong (α = 0.86).

Independent variable: Social Proof

Our independent variable captured the manipulated social proof. It took a value of 0 when the investment opportunity indicated external social proof and 1 when the investment opportunity indicated internal social proof. While this eliminates most of the underlying social dynamics of social proof in Study 1, it allows us to isolate the investors’ sensitivity to being informed of reinvestments versus new investments.

Moderator: Investor experience

We measured investment experience using a Likert scale in which investors evaluated their investment knowledge, which is also used by companies certified by the International Capital Market Association (IMCA, 2025). In addition, we tested our models with our investment experience moderator, which we measured as the number of years of experience. Our results were robust to this alternate operationalization.

Control Variables

Our models included a series of control variables. The results without these control variables were consistent with the primary analysis and are reported as part of the robustness analyses. First, we controlled for investor age, education, gender, and ethnicity, which have been shown to affect venture-funding outcomes (Blohm et al., 2022; Kanze et al., 2018). Furthermore, we controlled for prior entrepreneurial experience to account for a potentially deeper understanding of the venture sector (Hsu, 2007; Ko & McKelvie, 2018). We also controlled for the specific pitch, as each investor evaluated three pitches in a random sequence. Finally, we controlled for the survey-completion rate and the survey-completion time to account for outside circumstances that participants may have experienced while participating in the experiment.

Study 2: Results of the Experiment

To ensure the validity of our findings, we conducted a series of ANOVA and t-tests for our manipulation and attention checks. The manipulation check, which we placed at the end of the experiment, asked participants to recall factors about the investment opportunity. Participants in the internal social proof condition were more likely to say that they noticed that prior investors had reinvested (F = 18.61, p < .001). Those in the external social proof condition were more likely to say that they noticed that new investors had chosen to invest (F = 5.37, p < .001). Moreover, our tests revealed no significant differences between participants who were excluded based on the attention check and those in the final sample on any dimension, including investment experience (F = 1.34, p = .247), assigned experimental condition (F = .04, p = .842), or experiment-completion rate (F = .63, p = .428).

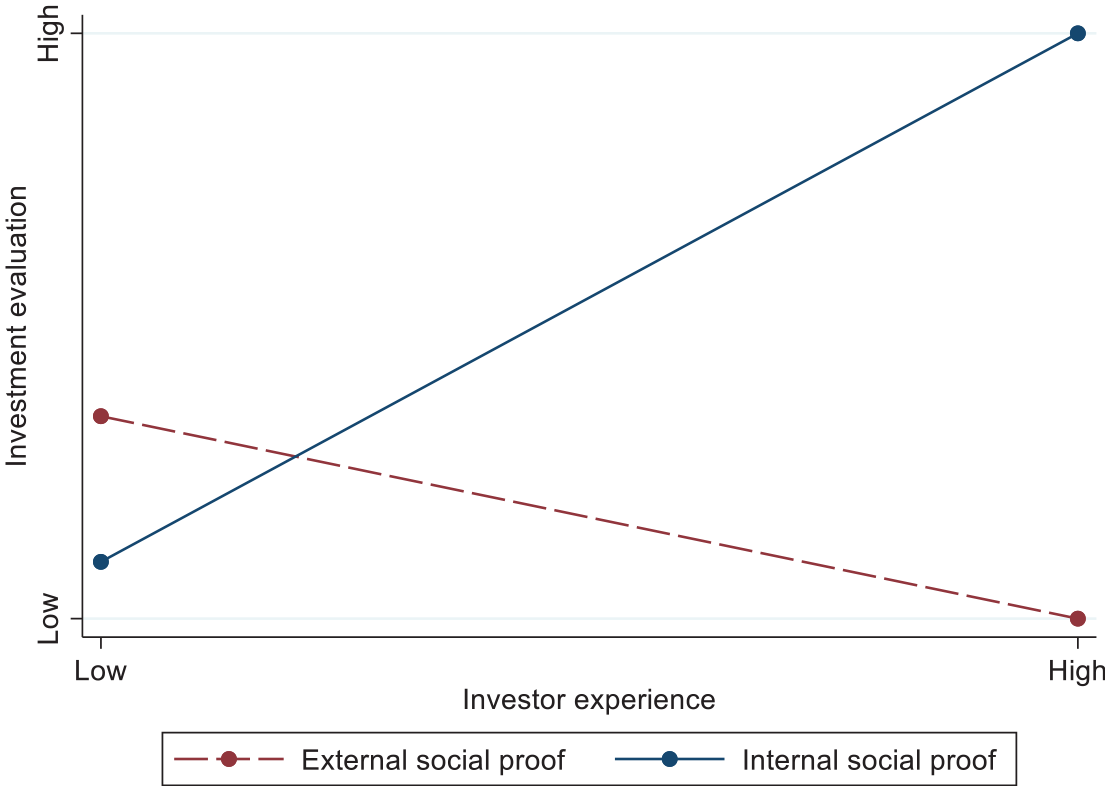

Table 3 provides descriptive statistics and correlations, and Table 4 reports the regression results. Model 1 includes the control variables and investor experience. Model 2 introduces social proof and indicates that internal social proof is linked to higher venture evaluations than external social proof. Model 3 introduces the interaction effect between investor experience and social proof. H3 states that the greater an investor’s experience, the weaker the positive relationship between the amount of social proof and the likelihood that they invest in that venture. The results of Model 3 show that the moderation is significant (β = .156, p = .004), providing additional support for H3. Figure 4 depicts this relationship.

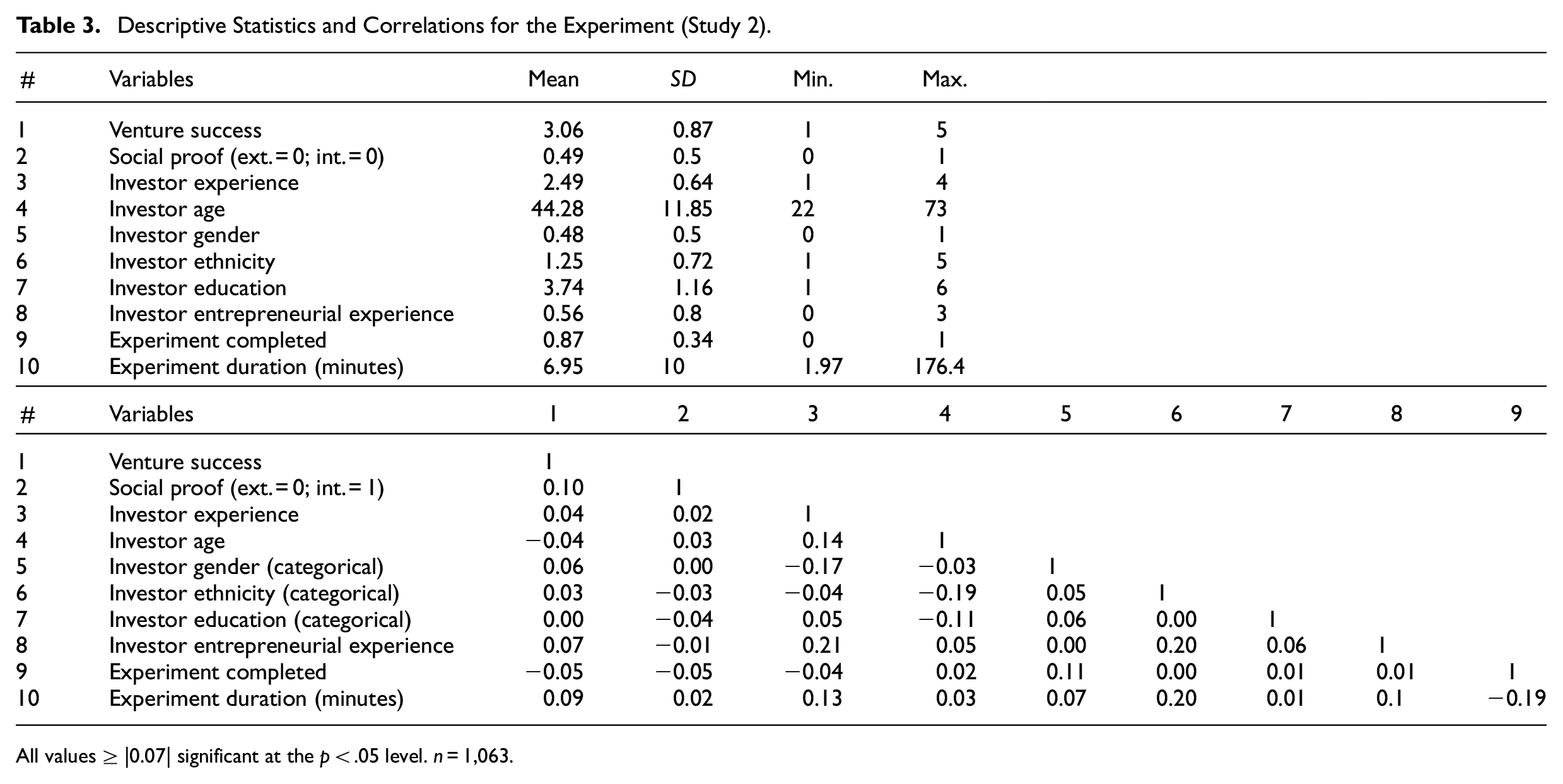

Descriptive Statistics and Correlations for the Experiment (Study 2).

All values ≥ |0.07| significant at the p < .05 level. n = 1,063.

Models for Investment Evaluation in the Experiment (Study 2).

p < .001, **p < .01, *p < .05.

Moderation results in the experiment (Study 2).

The difference in effect sizes is also considerable. For experienced investors (average +1 SD), internal social proof is more important and the estimated value of the corresponding venture is 10.2% higher than the estimated value of an otherwise identical venture with external social proof. In contrast, inexperienced investors (average −1 SD) do not differentiate between the two types of social proof (evaluations differed by only 0.3%).

Robustness Tests

We conducted a series of robustness tests. First, we used investment experience in years as an alternative independent variable. The moderation maintained its direction and significance (β = .106, p = .026). Second, we used the alternative dependent variable of investor’s self-proclaimed investment probability (IMCA, 2025). The moderation again maintained its direction and significance (β = 0.154, p = .016). Third, randomization generally makes the inclusion of control variables unnecessary (Camuffo et al., 2020). Therefore, we reran our models without any controls and found that the moderation maintained its direction and statistical significance (β = .131, p = .022). Fourth, we independently ran each of the venture evaluation’s three scale indicators (instead of the aggregate score) to account for the wide variation in metrics for investment likelihood (Kerr et al., 2014). The results were almost identical, with the direct and indirect effects for all three subdimensions remaining statistically significant. Fifth, we excluded all individuals who indicated that they had the lowest possible amount of experience in order to remove individuals who might not have actually been investors. The results were consistent, and the moderation maintained its direction and significance (β = .152, p = .014).

Complementary Analyses

While our two quantitative studies supported our hypotheses, our theorizing is based on several assumptions and boundary conditions. Therefore, in this section, we explore the implications of our model’s two most central assumptions: (1) internal social proof is more valuable than external social proof, and (2) inexperienced investors tend to herd more than experienced investors because they feel more FOMO when evaluating opportunities.

Complementary Analysis 1: Internal Social Proof and Investment Returns

We theorized that internal social proof has considerable benefits that make it more predictive of performance than external social proof. As our data contains information on the financial returns of all investments, we tested whether internal social proof is associated with higher financial returns than external social proof. This analysis was based on the same angel investment group as Study 1 but focused on the deal level (i.e., 319 investment rounds; for a similar approach see Zhang et al., 2021).

To illustrate the structure of our deal-level data, we offer the following example from our sample: a venture developing a new type of battery raised its first round of capital with the angel group in 2014 at USD 275 per share, its second round in 2015 at USD 439 per share, and its third round in 2017 at USD 439 per share (the same valuation as in the prior round). In 2021, the angel group exited at USD 558 per share. This venture represents three data points for an analysis at the deal level: one for the growth from USD 275 to USD 558 over 6 years and 359 days, one for the growth from USD 439 to USD 558 over 5 years and 183 days, and one for the growth from USD 439 to USD 558 over 3 years and 285 days. As all angels in a round invested under the same conditions, we used every round only once in our investment analysis.

We analyzed the 319 investment rounds using a mixed effects generalized linear model (Stata: meglm) for the deal data nested in the focal venture and the general stage of venture development.

Variables

We measured our dependent variable, investment return, as the capital gains multiple (CGM) on a deal-by-deal basis (e.g., Antretter et al., 2020a; Mason & Harrison, 2002). We computed it as the increase in the net asset value (NAV) per share at the end of our study period (for a similar approach, see, e.g., Antretter et al., 2020a; Blohm et al., 2022). The angel group’s administration determined NAVs twice per year following International Private Equity and Venture Capital Valuation Guidelines (IPEV, 2018). In line with previous research, we did not account for dividends, fees, or remuneration for board positions (Antretter et al., 2020a; Mason & Harrison, 2002).

External social proof is the share of previously not-invested angels who chose to invest in this round. Internal social proof is the share of previously invested angels who chose to reinvest, and investor experience is the natural logarithm of the number of investments the investor made in the network before the focal transaction (same as Study 1). We controlled for investment duration (i.e., how long the investor held the investment); the deal year to account for economic conditions; and the venture stage, venture industry, and venture country to account for the venture’s development, the sector’s attractiveness, and distance effects, respectively (Antretter et al., 2020a).

Results

Table 5 presents the descriptive statistics and correlations for our investment–return analysis. Table 6 provides the regression results. Model 1 reports the baseline model, and Model 2 introduces external social proof, which has no significant relationship with investment returns (β = 0.139, p = .311). Model 3 introduces internal social proof, which is significantly and positively related to investment returns (β = .176, p < .001). Therefore, we find evidence of a positive link between internal social proof and investment returns, but not between external social proof and investment returns. Model 4 contains both types of social proof and the effects remain the same. This supports our claim that internal social proof is more useful than external social proof.

Descriptive Statistics and Correlations for Financial-Return Analysis.

All values ≥ |0.12| significant at the p < .05 level. N = 319.

Models for Financial-Returns Analysis.

p < .001, **p < .01, *p < .05.

Complementary Analysis 2: FOMO as a Mediator

We also considered the possibility that inexperienced investors are, in general, more susceptible to peer information because they experience more FOMO than experienced investors. Our experiment included a five-point scale for FOMO (Przybylski et al., 2013), which participants used to rate how worried they were that they might not be part of a deal, how anxious they were because their fellow investors did not tell them about opportunities, and how important it was for them to be in touch with other investing peers.

We found that inexperienced investors feel more FOMO (β = .122, p < .001) and that FOMO makes ventures seem more attractive (β = .472, p < .001). We tested the mediation with the PROCESS Macro in SPSS (Model 4; Hayes, 2012) with 10,000 bootstrapped samples and found that the indirect effect was significant (β = −.056, 95% CI [−0.085, −0.028]). An additional analysis in Stata (command: sem) revealed that the Sobel test was also significant (β = −0.058, p < .001), and the mediated effect was 18.5% larger than the direct effect. This shows that FOMO is particularly relevant for inexperienced investors, while more experienced angel group members are less susceptible to this cognitive bias. These findings add to the literature on the interplay between experience and cognitive biases in early-stage investing (e.g., Blohm et al., 2022; Harrison et al., 2015).

Discussion

In this article, we developed a social proof model of angel group members’ decisions and tested it using investment data on 469 members of an angel group and a vignette experiment with 367 investors. While most studies of social proof in investments focus on either the person delivering the proof or the person interpreting it, we discovered a dynamic interplay between the two: the value of social proof is determined by whether it is internal or external, and its interpretation depends on the extent to which the investor perceiving it is experienced.

Prior studies of social proof have usually disregarded the specific circumstances of the imitated investor. While this omission is reasonable in anonymous contexts like stock markets (e.g., Rao et al., 2001) and crowdfunding (e.g., Bapna, 2019), it does not suit the growing phenomenon of investing through structured angel groups. Members of these groups have complex personal relationships with each other and some of them have access to private information from the ventures. As a result, following the right group member reveals important insights and reduces information asymmetries, while following the wrong group members leads to non-productive herding. Thus, whether an investor can financially benefit from social information depends on their relational embeddedness and their ability to draw out private information.

This distinction also justifies the occasional use of imitation. Imitation can be valuable in contexts where learning or speed are critical, as it allows decision-makers to efficiently leverage the expertise or insights of others. In such contexts, investors should imitate without shame. However, this does not justify following others blindly—doing so would constitute herding rather than imitation. Imitation requires discernment in the form of carefully selecting credible sources of information, and choosing to follow individuals with superior knowledge or relevant expertise. A reliance on social proof does not absolve one of the responsibility to differentiate between sources to make informed choices.

Research Contributions

Our study contributes to the literature on social proof, investor networks, and experience.

Social Proof Theory

Our main contribution is to social proof theory (Cialdini, 1984, 1987). Our findings highlight the importance of differentiating between two types of social proof that are often used synonymously: herding and imitation (for examples of synonymous/mixed use, see Andreu et al., 2009; Gaba & Terlaak, 2013; Goethner et al., 2021). This synonymous use of the two terms is not surprising when the focus is on anonymous financial markets like the stock market (e.g., Chiang & Zheng, 2010; Rao et al., 2001) or crowdfunding (e.g., Bapna, 2019; Rodríguez-Garnica et al., 2024; Vismara, 2018), as their size, complexity, and lack of exchange makes the distinction meaningless. If, for instance, a certain stock is named as the most popular stock of the month, it tells us little about who is buying it and why.

However, the distinction between herding and imitation becomes meaningful if we look at markets that are sufficiently small for investors to be acquainted with each other and large enough for information flows to be imperfect. We therefore distinguish between the two by noting that herding describes following others indiscriminately, whereas imitation is a selective process of following individuals who have access to particularly valuable information. Due to the underlying dynamics, external social proof produces nonproductive herding (Spyrou, 2013), while internal social proof aggregates metaknowledge (Evans & Foster, 2011) and reduces information asymmetries through selective imitation (Ahlers et al., 2015; Courtney et al., 2017).

One realm in which this difference is visible is angel groups, where herding generally leads to the use of the most available kind of information (i.e., external social proof) and imitation leads to the selective use of the most valuable kind of information (i.e., internal social proof). This distinction between internal and external social proof advances the social proof literature (Cialdini, 1984) by showing how social proof materializes in investor groups, and theorizing about when and why investors rely on it. It also answers calls to study asymmetrical attention as a foundation of social proof in the “dynamic processes of social influence” (Maula & Lukkarinen, 2022, p. 723).

Angel Groups

Our results also add to the study of the empirical context of angel groups. First, we demonstrate that angel investors use social proof to navigate the uncertainty of early-stage investing in ways that echo the patterns seen in equity crowdfunding and venture capital (Colombo et al., 2015; Vismara, 2018). However, we uncover one additional distinction—in addition to the readily available external social proof that also exists in these other contexts, internal social proof can offer better venture-specific insights but is harder to access. This highlights the dual role of angel groups as collaborative networks and information ecosystems (for a discussion, see Butticè et al., 2021) and advances our understanding of peer influence in early-stage investing.

Second, we find that angels who have access to good information often do not share it. Prior investors may withhold their concerns in order to preserve relationships with entrepreneurs or protect the value of their earlier investments, thereby creating information asymmetries within the group (Maxwell et al., 2011). This reluctance mirrors findings on knowledge herding in larger organizations, where interpersonal dynamics and perceived risks suppress information-sharing (Connelly et al., 2012). Ultimately, this limits the wisdom-of-the-crowd dynamics of angel groups, as it reduces the availability of high-quality internal social proof.

Third, we show that angels often use low-quality social proof, even though doing so hurts their investment returns. This is partially due to the aforementioned secrecy of well-informed investors. In other words, the high visibility of the less valuable types of information results in an availability bias (Tversky & Kahneman, 1973)—angels follow the more visible external social proof and end up with worse investment returns than if they had followed internal social proof. For angel group members, what they see (external social proof) becomes all there is (Kahneman, 2011), which leads them to herd on the wrong type of social proof. In this regard, this article addresses recent calls to study angel investments as a dynamic social process (e.g., Butticè et al., 2021; Murray et al., 2020; Wesemann & Antretter, 2023) and adds to the literature on decision biases in angel investing (e.g., Blohm et al., 2022; Harrison et al., 2015; Maxwell et al., 2011).

Investment Experience

Our work also adds to recent explorations of the role of experience in angel investing (e.g., Botelho et al., 2021; Collewaert & Manigart, 2016; Croce et al., 2023). While extant studies show that investment experience can increase returns by improving information filtering (Elliott et al., 2008), trade quality (Nicolosi et al., 2009), or financial theorizing (Campbell et al., 2014), they focus on assessments of venture information instead of peer information. We theorize and find that experienced angel investors’ superior financial returns are based not only on a better understanding of ventures but also on a better understanding of their peers.

More specifically, we show that experienced investors copy other investors less. We also demonstrate that while the extent of copying among experienced investors is lower, its quality is higher—experienced investors tend to avoid indiscriminate herding on readily available external social proof and instead selectively imitate the more informative internal social proof. This finding may be somewhat dismaying for inexperienced investors, as it demonstrates that they are not just worse at analyzing ventures but also worse at analyzing their peers. As such, the investors who would benefit the most from imitating others are also those least able to do so. However, our findings offer hope—experience teaches investors how to move from indiscriminate herding to more productive selective imitation.

Practical Implications

Our results also have implications for practitioners. The first of these implications relates to angel group members and administrators. We find that while reliance on social proof is common in angel groups, it is often misguided—investors mostly copy external social proof, which is more available but does not lead to better financial results. By falling for an availability bias, investors score lower returns than they would otherwise. However, the results are not always bad. When used correctly, imitation can provide useful metaknowledge that serves as a proxy for valuable insider information (Evans & Foster, 2011). This should reduce the shame that some investors feel when imitating others. It also raises questions for angel group organizers (also see Antretter et al., 2020a): Should information-sharing be left to individuals or should the group’s leadership intervene? Are there ways to raise awareness of the information that matters (i.e., internal social proof)? The facilitation of information exchange among group members may improve the group’s overall investment returns and, thereby, increase member satisfaction, recruitment, and member lifetime value.

Second, our findings have implications for fund-seeking entrepreneurs. The increasing interconnectedness among investors means that early investors’ impressions affect the decisions of later investors. A venture that convinces many new investors to invest when they start a new fundraising round generates highly visible social proof that helps them raise a lot of money, but most of that money is from inexperienced investors. In contrast, a venture that convinces previously invested angels to reinvest tends to raise fewer funds but likely receives “smarter money” because it comes from more experienced investors who can assist the venture more. Recognition of this effect may change fundraising strategies, as fundraising carried out under false pretenses early on may haunt ventures when they try to raise more funds later, as experienced angels are less likely to invest if they see that the original investors are unwilling to do so. Therefore, pleasing existing investors is essential for securing more high-quality investors with experience in later funding rounds. This also addresses a recent call to study how social proof helps young ventures secure valuable late-stage funding (Rodríguez-Garnica et al., 2024).

Limitations and Future Research

While our theoretical foundations for social proof exist in many contexts, the angel context creates some constraints on generalizability. Angel groups are interesting because their members maintain interpersonal relationships, are boundedly rational, and have “skin in the game.” All of these factors may be necessary conditions for our findings to hold. Without them, imitation may be impossible (e.g., if there is no network), unnecessary (e.g., if investors are not boundedly rational), or without benefits (e.g., if there is nothing to gain). For example, crowdfunders have no personal relationships with each other and, therefore, rarely obtain meaningful information from their peers, making imitation based on internal social proof impossible. Venture-capital firms are not boundedly rational individuals but organizations that can react to increased deal flow by hiring additional analysts, making imitation less tempting. Banks that provide loans have no skin in the game for extreme returns and are less interested in finding the “diamond in the rough,” making imitation less beneficial. As a result of these differences, we expect that our findings on social proof may not be replicated in contexts like online crowdfunding, but they may hold in contexts where mutually acquainted individuals face the same risky choices. An example is a job market in which acquainted recruiters assess the same applicants. In such a context, an offer from the applicant’s past employer may say more about the applicant’s ability than an offer from a very prominent firm that only interviewed the candidate.

Notably, our results may not apply to all angel groups. We intentionally conducted our study in an angel group that was sufficiently large to contain considerable information asymmetries with imperfect information exchanges but also intimate enough to enable private information flows. Few angel groups are this large—most consist of only a handful of investors who openly share information. In that sense, our context is consistent with the frequently studied large organizations that develop information flow dynamics that do not necessarily exist in the more numerous small- and medium-sized enterprises. While larger angel groups’ relative size and prominence make them important to study, smaller groups also have interesting interaction patterns. For example, in smaller groups, people likely get to know each other better, form tighter bonds, and might even develop friendships that extend outside of angel group meetings. Therefore, we encourage future research to investigate small-group ties and at what point the information flow of smaller angel groups becomes disrupted by subgroup formation, lack of in-group sentiment, and/or social complexity.

Additionally, this project tested the experience hypotheses with large-ticket business angels (Study 1) and small-ticket equity investors (Study 2). However, various types of experience may influence how investors interpret and rely on social proof. For example, entrepreneurial experience may help investors focus on intrinsic venture qualities rather than external cues, while broader investment experience, such as private equity or venture capital, might equip these investors to better assess risks and opportunities. Future research could examine how these distinct experiences shape decision-making across different investment contexts and settings.

Moreover, in an abductive analysis of the data, we found a significant interaction between gender and social proof and the likelihood of investment in the focal venture. Specifically, we found that women respond more to both external social proof (moderation: β = 1.242, p < .001) and internal social proof (moderation: β = 0.994, p < .001). It would be interesting to investigate why this is the case. Prior research has shown that venture environments function differently for women (Wesemann & Wincent, 2021). In the context of this study, the facts that women have broader social networks (Szell & Thurner, 2013) and communicate differently within them (Kimbrough et al., 2013) may be particularly relevant. Such differences in the use of social proof along with differences in underlying communication deserve additional scientific exploration. This call for research connects to a recent publication on early-stage funding that asked whether women are more likely to herd (Rodríguez-Garnica et al., 2024) and presented initial evidence that they might be. These dynamics offer exciting opportunities for future research.

While our analysis demonstrated that early-stage investors rely on social proof, it does not consider specific investors’ status and interaction patterns, which can affect other investors’ perceptions (Milanov & Shepherd, 2013). Indeed, some evidence suggests that investors are more likely to trust social proof from high-status investors, and that past shared investments increase the likelihood of collaborating again (Blaseg & Hornuf, 2024). In Study 1 (angel group), there may well be high-status investors who are known for their past investments or dominate group conversations for other reasons (e.g., their past entrepreneurial experience or net worth). In Study 2 (experiment), we isolated the hypothesized mechanisms and intentionally simplified the available social proof. While this shows that the experience effects are not simply the result of unobserved heterogeneity in social ties, we note that angel groups are social contexts in which mentorships and even friendships develop. Future research should test the role of such social ties in angel investments to determine how status, past collaborations, and tie strength affect how angel investors rely on social proof in their decision-making.

We note that the outcomes of venture investments are not only measured in financial terms. For entrepreneurs, the resulting quality of guidance, networking opportunities, and access to critical resources (e.g., access to industry knowledge or customer contacts) also matter. Similarly, the degree of imitation might impact how quickly financing rounds can be closed, which affects the amount of time entrepreneurs have to work on their products instead of fundraising. For investors, it is important to play a role in the entrepreneurial ecosystem, support inspiring projects, and develop relationships with other investors that they appreciate or even admire (Brettel, 2003). Investigations of these broader outcomes and how social dynamics form them could offer a richer understanding of how angel groups create value for both entrepreneurs and investors that goes beyond purely financial metrics.

Outside the venture-finance context, internal and external social proof may also arise in organizational decision-making with constrained information flows. For example, decision-makers in large corporations may prioritize highly visible external input (e.g., industry reports) over richer internal insights (e.g., feedback from frontline employees). Over time, this reliance on external signals can cause skilled individuals to disengage, which may reduce decision quality. Future research could explore how visibility and access in organizations affect engagement and effective decision-making.

Conclusion

Although social proof is central to investment behavior, it has received little attention in the context of angel investments. Our study addressed this gap by theorizing how the unique context of angel groups produces different types of social proof. Specifically, we differentiated between internal and external social proof, showed that only internal social proof is associated with better investment performance, and illustrated that an investor experience informs their reliance on social proof. These findings contribute to research on angel groups, investment experience, and social proof, and present an interesting foundation for future research.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.