Abstract

Building on social-psychological insights into social perception and judgment and empirical findings from the entrepreneurship literature, we propose that early-stage equity investors look at two main dimensions to assess entrepreneurs seeking early-stage financing: competence and cooperativeness. In all, 84 angel investors and venture capitalists active in Europe participated in a conjoint experiment. The results show that investors prioritize entrepreneurs’ competence over their cooperativeness. Entrepreneurs’ competence is even more appealing to investors when combined with coachability. We find that entrepreneurs can compensate for a lack of experience by demonstrating solid market knowledge and appearing to be coachable. Furthermore, the results suggest that investors differ in their consideration of entrepreneurs’ cooperativeness, but not competence, when making investment decisions—a finding that is conditional on investors’ usual level of involvement in their portfolio ventures. We discuss these findings from a theoretical and practical perspective.

Keywords

Introduction

The ability to obtain equity financing in the early stages of innovative new ventures is crucial for realizing their performance potential (Ber & Yafeh, 2007; Engel & Keilbach, 2007). Angel investors and venture capitalists are recognized as the two most important alternatives for financing such ventures (Drover et al., 2017). Accordingly, it is important for entrepreneurs who are seeking to finance their high growth potential ventures to understand the decision-making policies of these two sources of early-stage financing (Hsu et al., 2014).

Given that there is little reliable information about a venture in its early stage (Huang & Pearce, 2015; Plummer et al., 2016) and the market response to new, innovative product offerings can be highly unpredictable (Kollmann & Kuckertz, 2010), entrepreneur characteristics are the main consideration of early-stage equity investors (Bernstein et al., 2017; Huang & Pearce, 2015). In fact, entrepreneurs are considered to be the critical resource in the early stages of a venture’s lifecycle, since they shape the opportunity to be exploited (Kaplan et al., 2009; Svetek & Drnovšek, 2022). To date, researchers have examined more than 70 different decision criteria relating to the entrepreneur or entrepreneurial team that are predictive of obtaining early-stage financing (Ferrati & Muffatto, 2021). While this has helped us understand which entrepreneur characteristics investors use when evaluating investment opportunities, we still lack an understanding of how these criteria interact (Svetek, 2022).

In this paper, we seek to advance the understanding of venture capitalist and angel investor decision-making by building on social-psychological insights into social evaluation (Abele & Wojciszke, 2007; Abele et al., 2021; Abele & Wojciszke, 2014). Given that the chances of obtaining early-stage equity investment depend significantly on investors’ perceptions and evaluations of entrepreneurs (Mason et al., 2017), research on social evaluation may help us to better understand why some entrepreneurs obtain funding and others do not. Social-psychological research into social perception and judgment suggests that two major dimensions (the “big two”) underlie judgments about the self, others, social groups, nations, cultures, and more (Abele & Wojciszke, 2013). We argue that the primary dimension on which early-stage equity investors judge entrepreneurs is competence, while the secondary dimension is cooperativeness. Using a conjoint experiment, we test the proposition that these two dimensions are used together to inform investors’ evaluation of the entrepreneur. Furthermore, we test the suggestion that competence and cooperativeness can be signaled in different ways, implying that entrepreneurs can compensate for potential weaknesses and successfully manage investors’ perceptions through careful signaling. Finally, we consider the differences between types of investors and their individual differences in their involvement in value-adding behavior. We recognize that many early-stage equity investors make non-financial contributions in addition to financial ones (De Clercq & Manigart, 2007; Politis, 2008) and that the extent of their expected involvement in portfolio companies may explain differences in the selection criteria they use (Knockaert & Vanacker, 2013). Since heavy involvement also implies frequent interactions with entrepreneurs, we expect that the level of involvement partially explains the importance of competence and cooperativeness for investors.

To our knowledge, this is the first study on early-stage equity investment that builds on the well-established body of knowledge on social perception and judgment. As investors’ decisions depend on evaluative interpretations of their perceptions (Connelly et al., 2011), understanding the content dimensions that underlie these social judgments is important from a theoretical and practical standpoint. We explicitly consider the complementary and compensatory effects of different attributes that reflect the two underlying content dimensions, contributing to the emerging literature on the interaction effects of different attributes (Cardon et al., 2017; Plummer et al., 2016). We also take into account investor heterogeneity in decision-making, contributing to the growing stream of literature on individual differences among investors (Mitteness, Sudek et al., 2012; Murnieks et al., 2011).

Theoretical Background and Hypothesis Development

Competence and Cooperation in Evaluation of Early-Stage Entrepreneurs

People’s life outcomes are strongly influenced by other people’s impressions and evaluations of them (Leary et al., 2015). Social-psychological research has accumulated strong evidence that social perceptions are organized around two fundamental content dimensions (the “big two”): agency (competence) and communion (cooperation) (Abele & Wojciszke, 2007; Dubois & Beauvois, 2005; Fiske et al., 2007; Judd et al., 2005). This idea was first introduced to psychology by Bakan (1966), who described agency as the “urge to master” and communion as “non-contractual cooperation” (pp. 14–15). Cuddy et al. (2008) explained why these two content dimensions form the basis of social perception, arguing that it is vital for one’s survival to recognize the intentions of others and their ability to pursue these intentions. High communion reflects prosocial, cooperative intentions, while high agency represents the ability to bring about desired events. However, the entrepreneurial financing literature has yet to explore the role of entrepreneurs’ perceived agency (competence) and communion (cooperation) in investor decision-making.

In the early stages of new ventures, when products are not yet proven and markets not yet developed (Cassar, 2004; De Clercq et al., 2006; Plummer et al., 2016) and when entrepreneurs are expected to pivot (Gilbert et al., 2006; McDonald & Gao, 2019), equity investors must rely mostly on their evaluative perceptions of the entrepreneur or entrepreneurial team (Huang & Pearce, 2015). Since competence and cooperativeness are latent constructs, social judgments about the level and quality of these two dimensions are derived from the clusters of actions, achievements, and attitudes that individuals display.

The behaviors and characteristics that are adaptive for “getting ahead” are associated with the dimension of competence. In an entrepreneurial setting, competence refers to the ability to recognize and exploit entrepreneurial opportunities (Lans et al., 2008, 2011). This ability is determined not only by knowledge and skills, but also by personality and motivation (Baum & Locke, 2004; Reis et al., 2021). Entrepreneurship research has discussed a range of attributes investors believe an entrepreneur needs to possess in order to successfully develop and grow a business. Notably, these include industry experience (Becker-Blease & Sohl, 2015; Franke et al., 2008; Hoenig & Henkel, 2015), entrepreneurial experience (Hsu, 2007; Zhang, 2011), managerial experience (Polzin et al., 2018), attained education (Becker-Blease & Sohl, 2015; Bernstein et al., 2017; Hsu, 2007), and a track record of accomplishments (Ebbers & Wijnberg, 2012; Hallen & Eisenhardt, 2012). In addition, investors also pay attention to personal characteristics such as commitment (Cardon et al., 2017; Hsu et al., 2014) and preparedness (Ciuchta et al., 2018; Lu, 2018) when making decisions. These characteristics are believed to increase the likelihood that an entrepreneur will be able to advance the venture through competent entrepreneurial behavior (Huang & Knight, 2017). Therefore, these characteristics are key concerns for early-stage equity investors (Erikson, 2002).

Hypothesis 1. Early-stage equity investors’ likelihood of investment is positively related to their perceptions of the entrepreneur’s competence.

The behaviors and traits that investors believe are adaptive for “getting along” are associated with the dimension of cooperativeness. As the interests of entrepreneurs and investors are not always aligned (Van Osnabrugge, 2000), investors are particularly attentive to any signals of barriers to a cooperative relationship with an entrepreneur. Perceived untrustworthiness or opportunism is likely to lead to rejection of an investment proposal (Mason et al., 2017; Maxwell & Lévesque, 2014). The majority of early-stage equity investors provide non-financial resources in addition to financial ones (Large & Muegge, 2008). These investors are concerned about not only potential agency problems (moral hazard and adverse selection), but also the extent to which an entrepreneur is willing to take advantage of the non-financial resources offered (Huang & Knight, 2017). Factors such as the investor liking the entrepreneur (Huang, 2018; Mason et al., 2017; Sudek, 2006), the perceived similarity between investor and entrepreneur (Franke et al., 2006; Murnieks et al., 2011), the entrepreneur’s openness to feedback (Ciuchta et al., 2018), and the entrepreneur’s expressed fondness for an investor (Nagy et al., 2012; Westphal & Stern, 2007) have been shown to increase the likelihood of investment. These characteristics and behaviors influence the investor’s confidence that the entrepreneur will likely advance the venture by taking into account the investor’s interests and capitalizing on the non-financial resources provided (Huang & Knight, 2017). Since relationships, especially in the early stages of a new venture, are a primary source of financial and non-financial resources (Jiang et al., 2018; Zhang, 2010), investors might also be interested in how the entrepreneur interacts with other stakeholders. Due to high resource constraints, lack of organizational legitimacy, and high uncertainty, entrepreneurs need to rely on their interpersonal skills to leverage the resources embedded in their personal and business network (Baron & Markman, 2000; Leung et al., 2006). Consequently, the entrepreneur’s ability and willingness to establish and maintain mutually beneficial relationships with key stakeholders seems to be important for entrepreneurial success and is, as such, also recognized by early-stage equity investors (Hoenig & Henkel, 2015; Hsu et al., 2014).

Hypothesis 2. Early-stage equity investors’ likelihood of investment is positively related to their perceptions of the entrepreneur’s cooperativeness.

Primacy of Competence in Evaluation of Early-Stage Entrepreneurs

Researchers in the field of social psychology have proposed that perceptions of others are primarily guided by the communal dimension (Abele & Wojciszke, 2007). Considerable evidence supports this proposition (Abele & Bruckmüller, 2011; Cottrell et al., 2007; Wojciszke & Abele, 2008; Ybarra et al., 2001). Perceptions of another person’s intentions as good or bad determine whether people seek or avoid interaction with that person (Peeters, 2002) and therefore precede evaluations of that person’s competence (ability to realize intentions) (Fiske et al., 2007). However, when agency is crucial for the perceiver’s goals, the primacy of communion over agency will be reduced if not reversed. In fact, researchers have found that individuals in positions of power or in situations of high interdependence value agency as much as or more than communion (Abele & Brack, 2013; Cislak, 2013; Wojciszke & Abele, 2008). Entrepreneur–investor relationships are built around business ambitions. Ultimately, investors’ return on investment depends on achieving exit, which is the outcome of the entrepreneur’s ability to take advantage of the business opportunity (MacMillan et al., 1985). Therefore, entrepreneurial competence is a key consideration for early-stage equity investors (Brush et al., 2012; Landström, 1998). The majority of entrepreneur-level investment criteria identified (Ferrati & Muffatto, 2019; MacMillan et al., 1985; Sudek, 2006) fall under the broad dimension of competence (e.g., education, experience, expertise, track record, market knowledge, preparedness) and competence-enhancing personality traits (e.g., persistence, commitment, resilience), while the minority fall under the broad dimension of potential for cooperation (e.g., coachability, likability, trustworthiness). This suggests that investors are more sensitive to information about the entrepreneur’s competence than to information about the entrepreneur’s cooperativeness. MacMillan et al. (1985) found high agreement among venture capitalists in terms of the importance of the entrepreneur’s ability to take advantage of the opportunity at hand, with most being much less concerned about whether the entrepreneur has a compatible personality. Lu (2018) and Cardon et al. (2017) found that investors do appreciate displays of positive emotions, but are only willing to consider the investment when these are combined with signals of competence. Lack of entrepreneurial competence and lack of management knowledge were cited as criteria for rejecting investment opportunities (Feeney et al., 1999; Mason et al., 2017). This is even more pronounced in knowledge-intensive industries, such as biotechnology, where there is a high risk of product failure (Baeyens et al., 2006; Gompers et al., 2020). This suggests the primacy of competence in investors’ judgments of entrepreneurs who are seeking early-stage funding. The primacy of competence does not invalidate the importance of cooperation. Due to long-term relationships with entrepreneurs, investors attach great importance to their personal rapport with the entrepreneur and the potential for long-term cooperation (Huang, 2018; Mason et al., 2017; Polzin et al., 2018). However, due to the nature of the relationship, which is characterized by the investor’s high dependence on the entrepreneur’s abilities to exploit the business opportunity, we suggest that the entrepreneur’s competence is of primary importance to early-stage equity investors, while cooperation is of secondary importance.

Hypothesis 3. Early-stage equity investors place greater importance on the perceptions of an entrepreneur’s competence than on perceptions of the entrepreneur’s cooperativeness.

Complementary Nature of Competence and Cooperativeness

Negative social evaluations of others have been clearly associated with both perceived low communion and low agency (Imhoff & Koch, 2017; Wojciszke et al., 1998). It has been argued that communion and agency need to be integrated to mitigate the negative effects and enhance the positive effects of both (Frimer et al., 2011). Psychological research suggests that communal information (perceived cooperativeness) influences the valence of impression, while agentic information (perceived competence) influences the intensity of (positive or negative) impression (Wojciszke et al., 1998). Therefore, at least moderate levels of both agency and communion are desired in others. Importantly, very high levels of agency combined with very low levels of communion elicit the most negative social expectations, as these individuals are perceived as being capable of and inclined to engage in harmful behavior (Radkiewicz et al., 2013). This indicates that although agency and communion consistently emerge as two distinct dimensions that convey different information about an individual (Abele et al., 2016, 2021), they are used together when making social judgments about people. They do not simply complement each other by providing different relevant information and thus a more complete set of information for decision-makers (attribute-based complementarity); rather, each dimension shapes interpretation of the other dimension (elaboration-based complementarity) (Steigenberger and Wilhelm, 2018).

In the early-stage equity investment context, entrepreneurs’ lack of cooperativeness is directly related to agency risk (entrepreneurs’ opportunistic behavior at the expense of the investor; Fiet, 1995), while lack of competence increases execution risk (i.e., the inability to realize a business opportunity; Carpentier and Suret, 2015). Both the perceived lack of competence and poor potential for cooperation (i.e., due to inflexibility or lack of personal rapport) have been separately identified as reasons why investors did not back early-stage entrepreneurs (Mason et al., 2017). This suggests that entrepreneurs need to demonstrate above-threshold levels of both competence and cooperativeness to be attractive to investors. Different combinations of the two dimensions may also lend themselves to different interpretations. For example, investors may perceive entrepreneurs who appear highly cooperative but not very competent as potentially overly dependent. By contrast, entrepreneurs with low cooperativeness and high competence may be perceived as too arrogant and difficult to control and manage. It is therefore to be expected that investors will not only pay attention to both dimensions separately, but also require a balanced combination of cooperativeness and competence in entrepreneurs.

Hypothesis 4. Early-stage equity investors’ likelihood of investment is higher when they perceive the entrepreneur as both competent and cooperative.

Compensatory Effects of Different Demonstrations of Competence/Cooperativeness

Evaluations of the two dimensions can be inferred from the diverse actions, achievements, and attitudes that correspond to each dimension (Abele & Wojciszke, 2014). Overall, entrepreneurship research indicates that investors rely on multiple pieces of information to judge a new venture’s investment potential (Cox et al., 2017; Huang & Pearce, 2015). As these are usually available to early-stage equity investors, it is particularly important to understand how investors respond when the information points to the same or opposite directions (Drover et al., 2018). Certainly, the complementary versus compensatory role of the different information entrepreneurs use to communicate the strength of the investment opportunity is one of the most interesting questions in the entrepreneurship financing literature (Colombo, 2021; Svetek, 2022) because of its importance for understanding how resource-constrained entrepreneurs can increase the investment potential of their ventures. However, there is very limited evidence on the interaction effects of different information pertaining to the same content dimension (Svetek, 2022).

Given that more information about a dimension increases the perceiver’s confidence in judging that dimension (elaboration-based complementarity), especially when information is congruent (Drover et al., 2018; Paruchuri et al., 2021), different information about the same content dimension could reinforce each other. At the same time, multiple pieces of information that pertain to the same content dimension could be considered redundant, leading to one piece of information being perceived as superior and diminishing the value of other pieces of similar information (attribute-based substitution) (Bapna, 2019; Ozmel et al., 2013). Finally, different pieces of information pertaining to the same dimension may not interact with each other but build on one another. This also suggests that the presence of a particular attribute could compensate for the absence or low expression of another attribute belonging to the same dimension (attribute compensation).

Preliminary evidence from the entrepreneurial finance literature suggests that investors respond positively to multiple signals that relate to the same content dimension. For example, Warnick et al. (2018) found that investors were more likely to invest in entrepreneurs who displayed both entrepreneurial and product passion, but the effect was additive and not interactive. They also found that investors similarly rated the funding potential of profiles with one but not the other form of passion, regardless of which passion was displayed. This suggests that one type of passion could compensate for another type of passion. In another study, Nagy et al. (2012) showed that entrepreneurs could successfully compensate for lacking credentials by engaging in impression management (e.g., self-promotion). Again, no interaction effect between entrepreneurs’ credentials and impression management was found. However, the researchers observed that impression management increased the perceived legitimacy of ventures only when entrepreneurs had low credentials, but had no such effect when entrepreneurs had high credentials. These results were attributed to a diminishing marginal utility, in that, once a threshold level of perceived competence is reached, additional impression management has a very limited effect on investors’ decision-making.

Drawing on the available evidence, early-stage investors are more likely to invest when they are exposed to multiple positive signals about an entrepreneur’s competence or cooperativeness. For example, investors are expected to be more likely to invest in entrepreneurs who have substantial industry experience and demonstrate their industry knowledge through market research. In comparison, investors are expected to be less likely to invest in entrepreneurs who have prepared detailed market research but have no experience, or those who have experience but have conducted only cursory market research. In effect, investors assume that entrepreneurs who have experience and thorough knowledge of the market are more competent than those who lack in one of these areas. Therefore, the former type of entrepreneur represents a better investment opportunity. Assuming industry experience and market knowledge bear similar weight in investors’ decision-making, these two pieces of information can be used interchangeably. Consequently, an entrepreneur who lacks in one of these two areas can compensate for this shortcoming by demonstrating competence in the other.

Hypothesis 5. Early-stage equity investors use different pieces of information pertaining to the same content dimension in an additive manner. Hence, the presence or high expression of one attribute could compensate for the absence or low expression of another attribute belonging to the same dimension.

Investors’ Degree of Involvement

Early-stage equity investors are a diverse group (MacMillan et al., 1989; Sørheim & Landström, 2001). Although the literature habitually portrays early-stage investors as active, not all early-stage investors are active investors who are willing to offer connections and mentorship, or participate in strategic decisions (Sørheim & Landström, 2001). Researchers have found that one in two angel investors are actually passive (Avdeitchikova, 2008; Mitteness, Sudek et al., 2012; Sørheim & Landström, 2001). On the other side of the spectrum, angel investors sometimes take on the role of co-founder or become part-time or full-time employees in the venture, working with the entrepreneur (or entrepreneurial team) on a daily basis (Festel & De Cleyn, 2013; Van Osnabrugge & Robinson, 2000). Significant differences in involvement have also been observed among venture capitalists, with one-third of these investors undertaking a passive role (MacMillan et al., 1989). This speaks to the diversity of relationships between entrepreneurs and early-stage equity investors.

Early-stage investors who offer non-financial resources in addition to financial ones, pay attention to entrepreneurs’ potential to capitalize on non-financial resources (Huang & Knight, 2017). Previous research has shown that early-stage investors who actively engage in coaching entrepreneurs also place greater value on entrepreneurs’ coachability compared to investors who do not engage in coaching their investees (Ciuchta et al., 2018). Therefore, more heavily involved investors can be expected to place greater emphasis on the entrepreneur’s cooperativeness. Gaps in competence can be bridged by providing mentorship and access to the investor’s network or even the investor’s own skillset (Colombo & Grilli, 2010). At the same time, investors may have trouble convincing entrepreneurs who do not see value in their involvement to accept their active role in the company. By contrast, investors who are not interested in being actively involved in the new venture may base their investment decisions primarily on the entrepreneur’s perceived competence (Knockaert & Vanacker, 2013), as they will rely on the entrepreneur to unearth the business opportunity and maximize the return on investment. Therefore, we suggest that early-stage equity investors who expect to be more involved in their portfolio ventures will pay more attention to the entrepreneur’s cooperativeness, whereas investors who do not expect to be heavily involved in their portfolio ventures will place more emphasis on the entrepreneur’s competence.

Hypothesis 6a. Early-stage equity investors who are more actively involved in their portfolio ventures will be more likely to invest when they perceive the entrepreneur as cooperative.

Hypothesis 6b. Early-stage equity investors who are less actively involved in their portfolio ventures will be more likely to invest when they perceive the entrepreneur as competent.

Research Design

Conjoint Analysis

Researchers have used retrospective research methods such as surveys and interviews to identify investors’ decision criteria; however, these methods have been found inadequate for assessing the importance of the different investment criteria and identifying the relationships among them (Zacharakis & Meyer, 1998). This can be attributed, at least in part, to the fact that investors use heuristics rather than a fully compensatory decision model in their investment decisions (Maxwell et al., 2011). Consequently, decision-makers are often inaccurate when describing their heuristics retrospectively (Keats, 1991). In this study, we avoid problems related to biases in recall and reporting (Morewedge et al., 2005) by studying investor decisions using a real-time method: conjoint experiment. Conjoint experiments have been shown to be appropriate for examining early-stage investors’ decision policies, assessing the predictive validity of individual investment criteria, and exploring their dependence on individual demographics and psychographics (Riquelme & Rickards, 1992; Shepherd & Zacharakis, 2018).

In a conjoint experiment, respondents are asked to evaluate a set of profiles that differ systematically in the levels of predefined attributes. Based on evaluations of the different combinations of attributes, researchers can statistically deduce attribute-level utility and importance, and predict the overall desirability of any profile of the selected attributes. Ecological validity is the most frequent concern with conjoint analysis because of the use of hypothetical profiles and lack of consequences for the decision-makers (respondents) in the research (Lohrke et al., 2010). However, conjoint experiments have been shown to be ecologically valid when the profiles used are realistic (Green & Srinivasan, 1990). Therefore, researchers using conjoint analysis need to have a good understanding of the critical decision-making attributes.

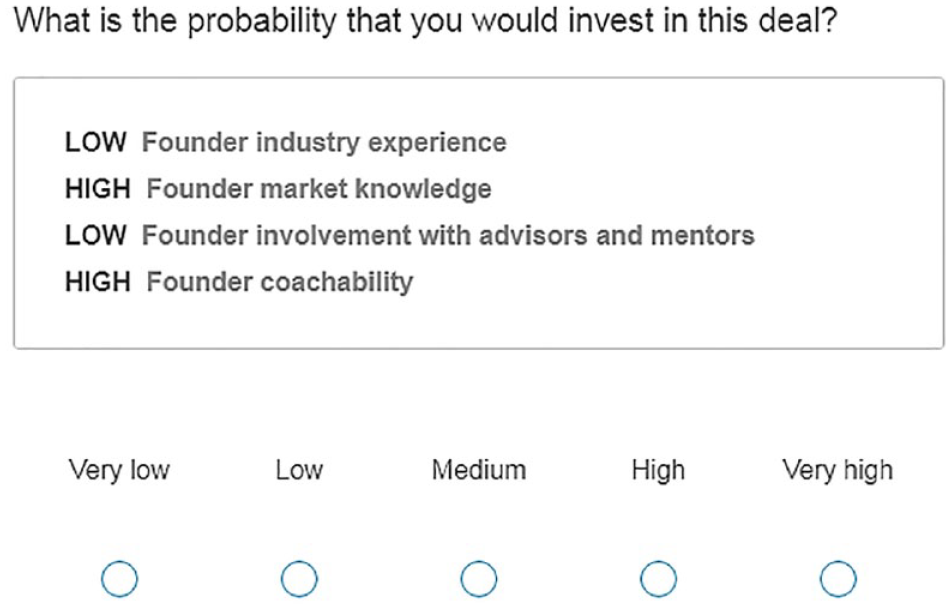

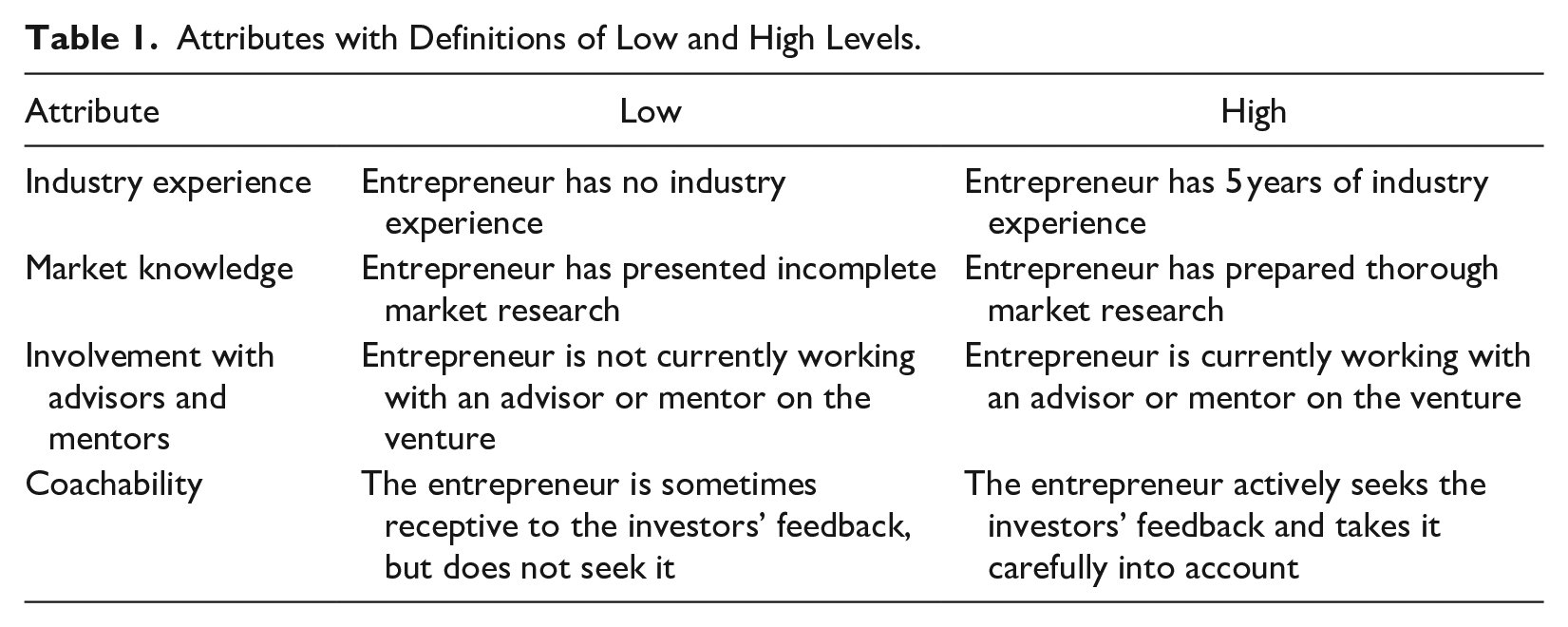

In our study, we employed a full-profile conjoint analysis (also called conjoint value analysis). Our respondents were presented with one profile at a time (see Figure 1). Each profile included four two-level attributes (see Table 1). The decision to use the full-profile conjoint analysis was made after we interviewed 10 investors (to validate attributes and their respective levels), who assured us that they assess investment opportunities individually and not comparatively. Because we were interested in interaction effects, we used a full factorial design. Therefore, the total number of distinct profiles was 24 = 16. Including three randomly selected practice profiles, each respondent had to rate 19 profiles on a 5-point Likert scale.

Profile example.

Attributes with Definitions of Low and High Levels.

We employed the following reference scenario adapted from Hoenig and Henkel (2015) to put participants on common ground and to ensure that the investment opportunities presented did not differ in anything other than the profile of the entrepreneur: “The ventures that are applying for early-stage funding are technology startups in the industry in which you normally invest. The ventures are based on a technical invention, have a compelling value proposition, clearly identified potential users, and a working prototype. The investment opportunities differ only in the following attributes of the lead entrepreneur.” We provided participants with attribute definitions (see Table 1) and three practice profiles to minimize response errors. To offset the order biases in conjoint analysis (Chrzan, 1994), profile order and attribute order were randomized across respondents. In addition to completing the conjoint task, respondents completed a questionnaire that included questions about their demographics and career.

Sample Characteristics

We identified European early-stage equity investors using the Crunchbase website. Crunchbase offers a comprehensive global database of private and public companies, equity investors, funding rounds, exits, and more, making it one of the recommended data sources for entrepreneurship research (Ferrati & Muffatto, 2020). We filtered the database by investor type (venture capital, angel group, and individual/angel), investor location (Europe), investment stage (seed, early stage), and location of organization receiving investment (Europe). We only included investors who had made at least one investment to ensure that they actually had experience with investment decisions. This yielded 5,470 results, from which individual results were drawn. We (cold) invited 707 venture capital partners, principals, or associates and 317 angel investors whose contact information (email or LinkedIn) could be found online to participate in the research. Each participating investor was also asked to share the invitation to the research with other angel investors or venture capitalists, or recommend other angel investors or venture capitalists to be invited to the research.

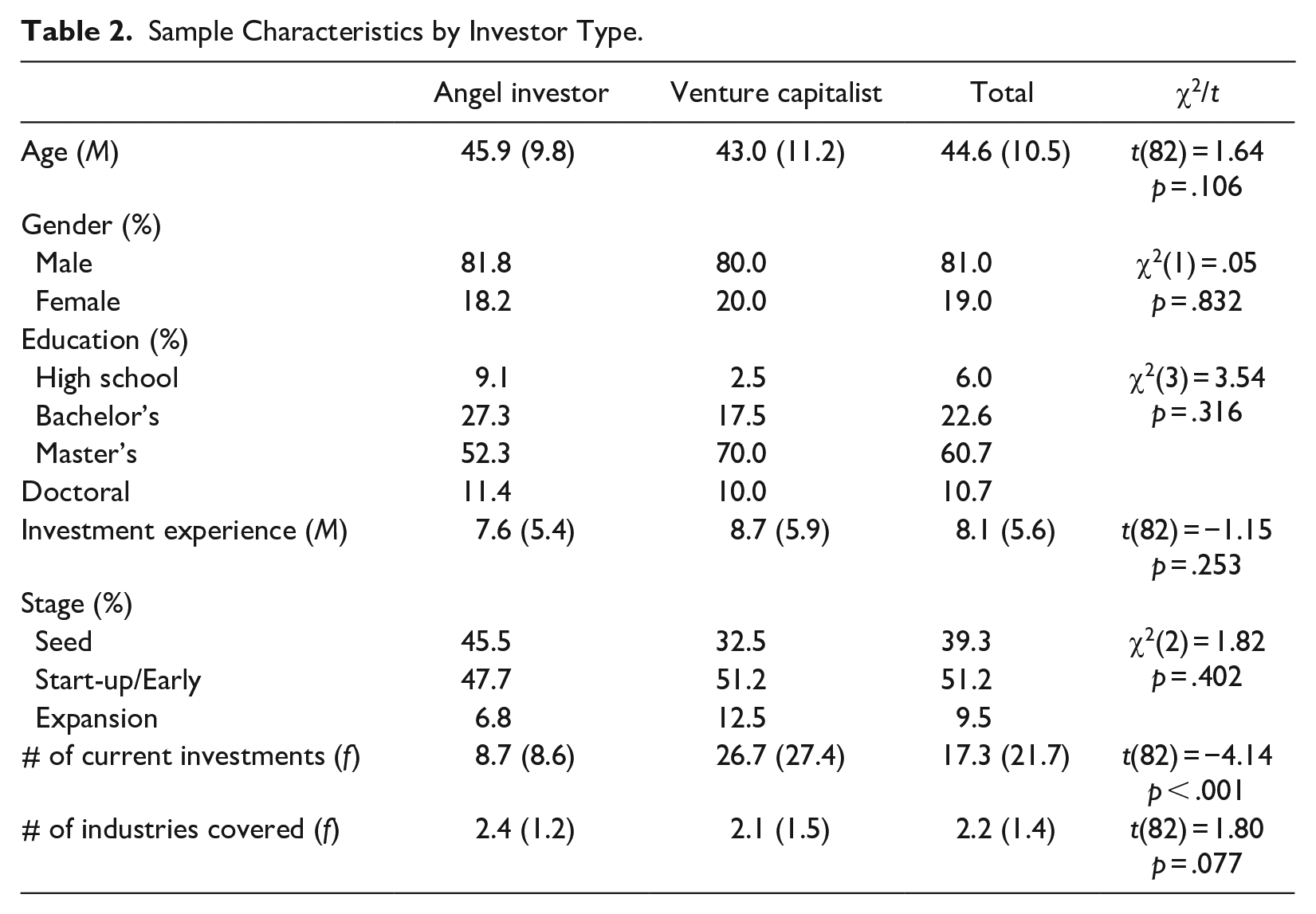

In all, 86 venture capitalists and angel investors from 24 European countries (Austria, Bulgaria, Croatia, Cyprus, Czech Republic, Denmark, Estonia, Finland, France, Germany, Hungary, Italy, Latvia, Netherlands, Norway, Poland, Portugal, Romania, Slovakia, Slovenia, Spain, Sweden, Switzerland, and the United Kingdom) participated in our study. Previous studies (Murnieks et al., 2011; Warnick et al., 2018) have found that this sample size is sufficient to obtain reliable decision data from early-stage equity investors, in line with the recommendation of Shepherd and Zacharakis (1999). We contacted the potential respondents twice, 2 weeks apart. The first email (message) included an invitation and a link to the online survey, and the second email (message) included a thank you note and a reminder with a link to the online survey where they could participate in the research.

Out of 86 investors who participated, 84 completed all 16 tasks in the conjoint experiment with minimum reliability of R2 > .60 and were included in further analyses. This resulted in a final sample size of 1,344 decisions. Of the participants, 44 (52.4%) self-identified as angel investors (private individuals investing own money directly in unlisted companies) and 40 (47.6%) self-identified as venture capitalists (professionals investing funds of outside limited partners directly in unlisted companies). In all, 63 (75.0%) respondents had made their last investment within the previous 6 months. The respondents’ investment experience ranged from 2 to 24 years, with the mean being 8.1 years (SD = 5.6). Most of our respondents invested predominantly in seed (39.3%) or early-stage (51.2%); only 9.5% invested predominantly in the expansion stage. In total, 68 (81.0%) were males and the average respondent’s age was 44.5 years (min = 24 years, max = 65 years, SD = 10.5). Most had attained a Master’s degree (61.7%), followed by a Bachelor’s (21.6%) and doctoral degree (10.7%). The majority had attained a degree in social sciences, business or law (63.1%), followed by engineering, manufacturing or construction (29.8%), natural sciences (8.3%), and health and medicine (7.1%). Demographics by investor type are presented in Table 2.

Sample Characteristics by Investor Type.

Measures

Dependent Variable

To measure the probability of investing in a presented opportunity based on the lead entrepreneur’s characteristics, investors were asked “What is the probability that you would invest in this deal?” The response was measured on a 5-point Likert scale, ranging from “Very low” (corresponding to a value of 1) to “Very high” (corresponding to a value of 5) (see Figure 1).

Decision Attributes

Independent variables in our study were attributes comprising the decision profiles used in this study. Two of the four decision attributes represented entrepreneur’s competence and two represented entrepreneur’s cooperativeness. Each of the four attributes had two levels, high or low, as presented in Table 1. The levels of attributes defined as “low” represented a baseline level of the attribute and not necessarily the absence of the attribute (as in the case of coachability and market knowledge). The relevance of the chosen attributes has been demonstrated in several previous studies and is elaborated in the following paragraphs. In addition, the attributes were pretested with five angel investors and five venture capitalists to ensure that the attributes were truly relevant, clearly described, realistic, and that they reflected the dimension of competence or cooperativeness as intended. These investors were recruited from a separate interview-based study we were running at the time. We presented these investors with a set of conjoint tasks and asked them to think out loud when making decisions based on the profiles presented. Investors were encouraged to discuss what each attribute signaled to them and to comment on the entrepreneur’s overall profile based on the set of presented attributes. This led to a gradual refinement of the attribute content and levels described in our research.

The two attributes corresponding to the dimension of competence were industry experience and market knowledge. The experience of the entrepreneur (or entrepreneurial team) is considered to be the most important competence signal for investors (Bernstein et al., 2017; Mitchelmore & Rowley, 2010), especially if the venture has no track record (Ko & McKelvie, 2018). Industry experience suggests that an entrepreneur has industry-relevant insights, knowledge, and networks that can be applied to develop the venture. In fact, an entrepreneur’s familiarity with the market plays a beneficial role in the recognition and exploitation of opportunities (Cassar, 2014; Chatterji, 2009). This is of particular importance in the early stages of a new venture when product–market fit remains unproven (Cassar, 2004; De Clercq et al., 2006; Plummer et al., 2016). Market knowledge and relevant connections can also be generated through comprehensive market research. Investors pay particular attention to the degree of substance and realism of market projections (Feeney et al., 1999; Mason & Stark, 2004). Well-prepared entrepreneurs are perceived as more credible and better positioned to execute the business idea (Ciuchta et al., 2018; Lu, 2018). Previous studies have shown that preparedness and skillful presentation of findings significantly influence the decisions of early-stage equity investors (Clark, 2008; Singh et al., 2016). Therefore, industry experience and market knowledge appear to be relevant signals of an entrepreneur’s competence in relation to the proposed investment opportunity.

The two attributes corresponding to a dimension of cooperativeness were coachability and founder’s involvement with advisors and mentors. Coachability has been found to be attractive to early-stage equity investors (Ciuchta et al., 2018; Warnick et al., 2018) by indicating how the entrepreneur will interact with the investor going forward (Huang & Knight, 2017). In entrepreneur–investor relationships, coachable entrepreneurs seek investor feedback that can be used to improve venture performance (Ciuchta et al., 2018). This display of openness to feedback, in turn, strengthens the relationship, increasing investors’ willingness to provide financial and non-financial resources (Ciuchta et al., 2018; Huang & Knight, 2017). An entrepreneur’s eagerness to take into consideration advice is also demonstrated through involvement with formal or informal advisors (Sudek, 2006). Such advisors can significantly contribute to the new venture’s readiness for funding and improve the experience of the negotiation phase (Lahti, 2014; Lehtonen & Lahti, 2009). Entrepreneurs who are involved with advisors and mentors demonstrate readiness to seek and cultivate relationships that can bestow on them the information and resources needed to advance the venture. Accordingly, both coachability and involvement with advisors and mentors signal that an entrepreneur is willing to form a relationship that is centered not only on the transfer of financial resources, but also on voluntary information exchange and cooperation beyond formal contracts (Carson et al., 2006; Huang & Knight, 2017).

Moderating Variable

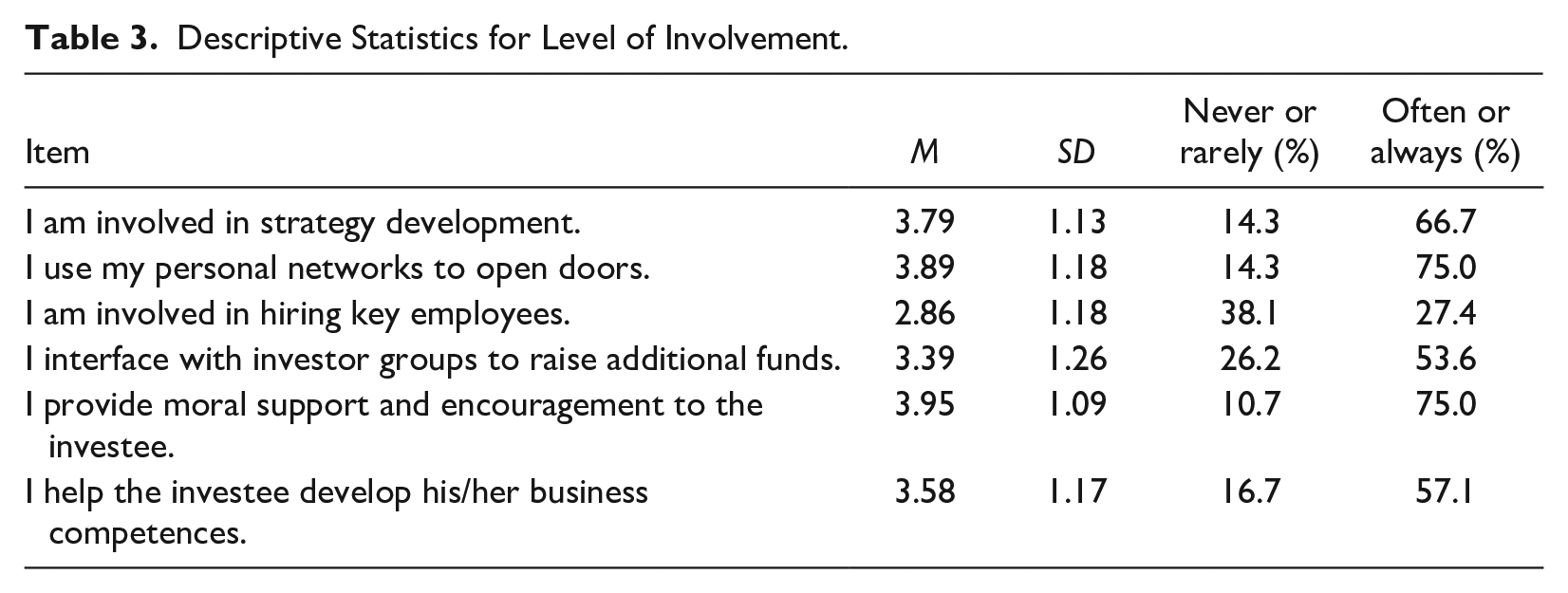

Investors’ involvement in the venture was measured by six items that describe investor value-adding activities (see Table 3). The comprehensive yet concise list of value-adding activities was based on a review of the literature (Knockaert & Vanacker, 2013; Large & Muegge, 2008). On a scale ranging from “Never” (corresponding to a value of 1) to “Always” (corresponding to a value of 5), respondents indicated how frequently they performed the listed activities as an investor in a new venture. Items were moderately highly correlated (min r = .43, max r = .72) and one component structure was found to be appropriate (λ = 3.88, R2 = .65). The degree of investors’ involvement in the new venture was indicated by a summated scale.

Descriptive Statistics for Level of Involvement.

Control Variables

Control variables were selected on the basis of prior research on angel investors and venture capitalists showing that investor characteristics can impact investment decisions (Franke et al., 2008; Hsu et al., 2014; Warnick et al., 2018). We controlled for the type of investor, investor’s age, gender, education level, investment experience in years, and (predominant) stage of investment.

Data Analysis

We analyzed the data from the conjoint experiment using hierarchical linear modeling (HLM) (Hofmann et al., 2000). Investor decisions (level 1) are nested within individual investors (level 2), who were either angel investors or venture capitalists. HLM is able to account for variance at the decision level (level 1 or within individuals) and at the individual level (level 2 or between individuals), thereby accounting for decision-making differences among investors. Individual attributes (such as age, gender, educational level, etc., including investor’s involvement in a venture) were modeled as static, while within-individual manipulations could vary across individuals.

To enable the analysis, the results from the full-profile conjoint analysis were organized by conjoint task for each respondent. The attributes were dummy-coded, with 1 reflecting a high level of an attribute and 0 reflecting a low level of an attribute. Main-effect regression coefficients therefore represented the preference for a high level of an attribute, whereas interaction-effect regression coefficients represented the preference for high levels of two attributes simultaneously. Cross-level interactions were also inspected, representing the preference for a high level of the task attribute when the investor is highly involved in portfolio ventures. All regression predictor variables were centered prior to analysis. Importantly, as recommended for conjoint research design cases (Hsu et al., 2014; Murnieks et al., 2011; Priem, 1994), we report only the full model with main and interaction effects together. In order to gain deeper insights into the potential compensatory effects of different attributes, we estimated marginal means for all first-level interactions between attributes and conducted post hoc contrasts using Holm correction.

Results

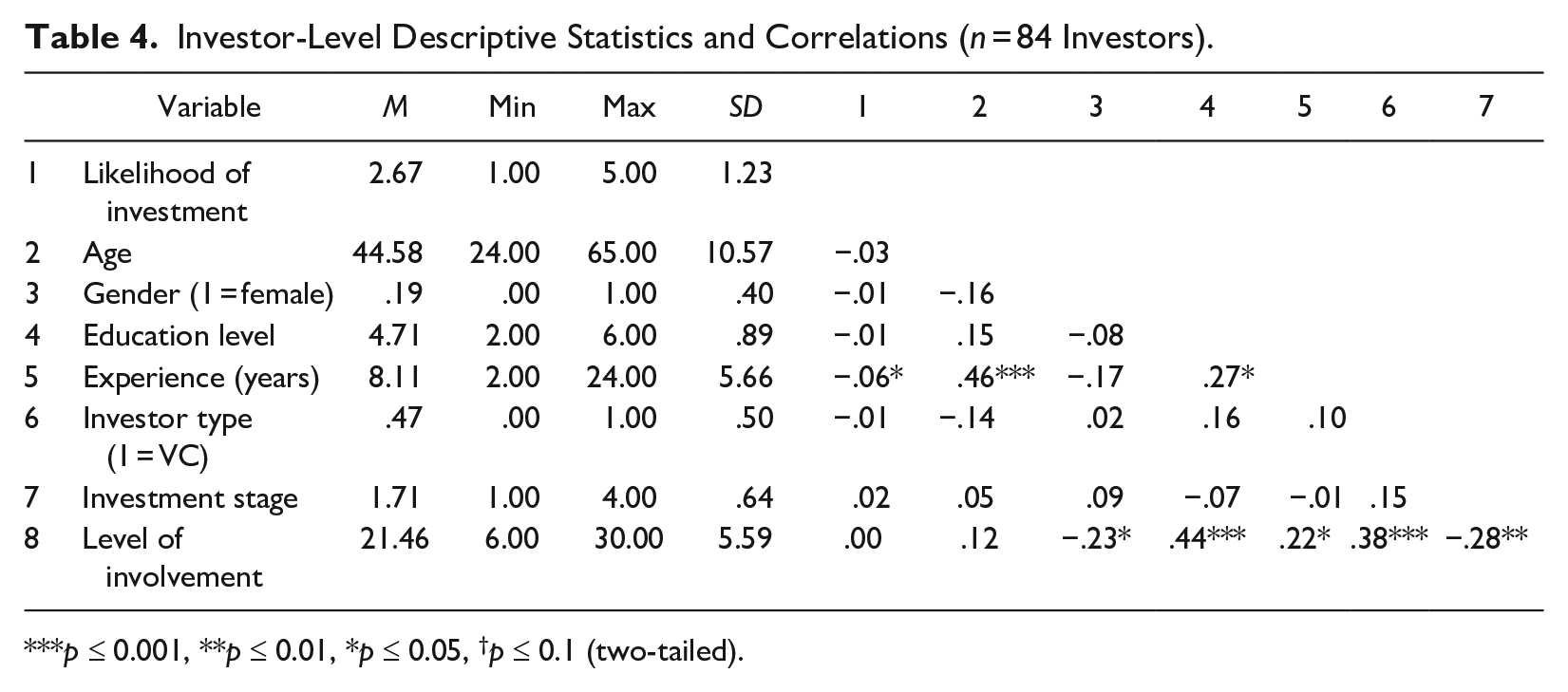

Descriptive statistics and correlations among outcomes, predictors, and control variables are presented in Table 4. As expected, older investors were also more experienced (r = .46, p < .001). Investors who attained a higher level of education were more involved in their portfolio companies (r = .44, p < .001), as were those with more investment experience (r = .22, p = .046). More experienced investors on average reported a lower probability of investment than less experienced investors (r = −.05, p = .048). Investors who invested in the later stages of a venture’s lifecycle were less actively involved (r = −.28, p = .011). Investors who took the role of lead investor more often reported higher involvement in portfolio ventures (r = .32, p = .003). Venture capitalists in our sample undertook the role of lead investor more frequently than angel investors (t[82] = −4.65, p < .001), although both groups of investors reported making the majority of their investments as part of a syndicate (t[82] = 0.49, p = .625). Venture capitalists were more involved than angel investors (t[82] = −3.74, p < .001), and male investors were more involved than female investors in our sample (t[82] = 2.09, p = .040). Almost all investors (95.2%) reported that they monitored a venture’s performance, but few were actually involved in the day-to-day activities of their portfolio companies (13.3%). Most investors in our sample take on, at least to some extent, an advisory or mentoring role. The descriptives for the particular activities reflecting investors’ active involvement in the venture are summarized in Table 3.

Investor-Level Descriptive Statistics and Correlations (n = 84 Investors).

p ≤ 0.001, **p ≤ 0.01, *p ≤ 0.05, †p ≤ 0.1 (two-tailed).

The mean internal consistency of respondents was R2 = 0.83 (min = 0.62, max = 0.95), indicating that the investors’ evaluations of 16 conjoint profiles were consistent. The four attributes (experience, knowledge, advisors, and coachability) explained 84% of the variance (conditional R2), which is consistent with the results reported in similar conjoint studies (Hsu et al., 2014; Murnieks et al., 2011).

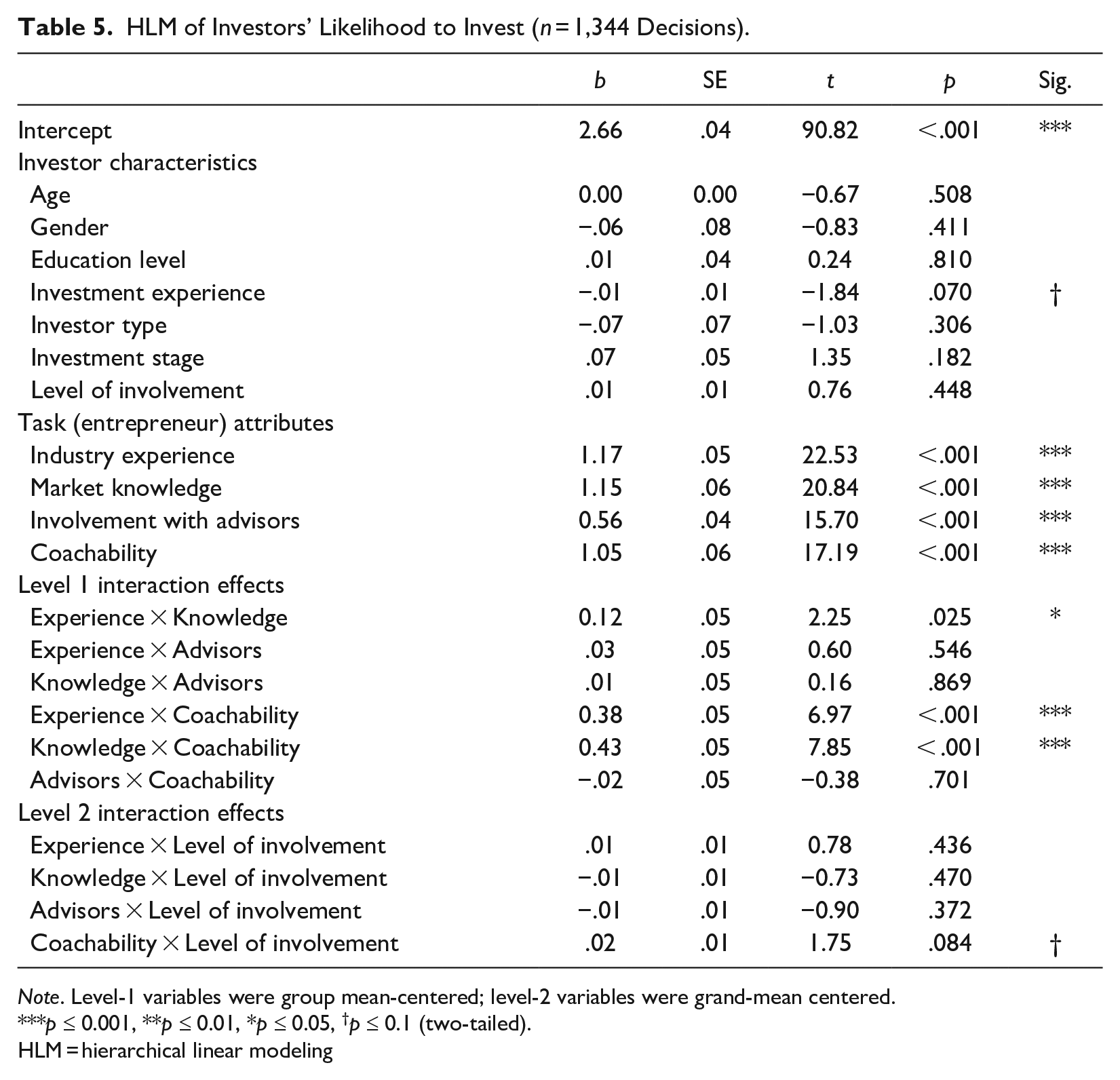

Table 5 shows the results of the HLM analysis of investor decisions. The main effects of all four attributes were positive and significant (p < .001), indicating that the four attributes positively and importantly influenced investors’ decisions and were the primary drivers of investment decisions captured by the dependent variable (likelihood of investment). Of the four attributes, industry experience had the highest impact on the investors’ investment decision (b = 1.17, p < .001), followed closely by market knowledge (b = 1.15, p < .001), then coachability (b = 1.05, p < .001), and involvement with advisors and mentors (b = 0.56, p < .001). These regression weights reflect the relative importance of the attributes. The post hoc comparisons showed that involvement with advisors and mentors was significantly less important to the early-stage investors in our sample than the other attributes, while the other three attributes did not differ significantly in their contribution to the investors’ decision. Given the combination of the four selected attributes, the importance of perceived competence (indicated by industry experience and market knowledge) was 59.1%, whereas the importance of perceived cooperativeness (as indicated by coachability and involvement with advisors and mentors) was 40.9%. These results suggest that competence (experience and knowledge) was the primary decision factor for the early-stage equity investors in our sample, while cooperativeness (coachability and involvement with advisors/mentors) was of secondary importance to the investors.

HLM of Investors’ Likelihood to Invest (n = 1,344 Decisions).

Note. Level-1 variables were group mean-centered; level-2 variables were grand-mean centered. ***p ≤ 0.001, **p ≤ 0.01, *p ≤ 0.05, †p ≤ 0.1 (two-tailed).

HLM = hierarchical linear modeling

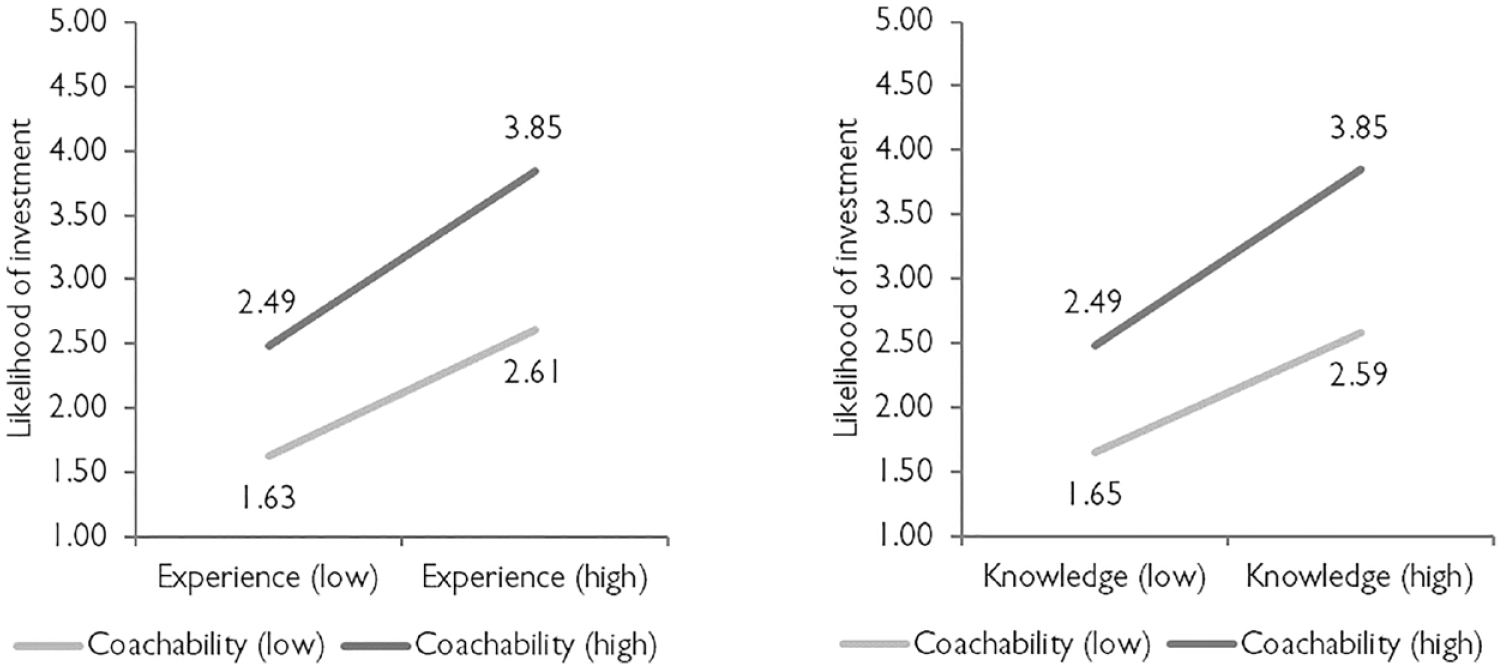

For the more important of the two signals of cooperativeness—coachability—the analyses showed a clear positive interaction effect between the entrepreneur’s industry experience and coachability (b = 0.38, p < .001) and market knowledge and coachability (b = 0.43, p < .001), indicating that investors are more likely to invest in entrepreneurs when they signal their coachability in addition to their competence (see Figure 2). Interestingly, in post hoc comparisons of the combinations of all levels of the selected attributes, we found that there was no difference in the reported likelihood of investment for the profiles that were high on experience and low on coachability, or for the profiles that were high on coachability and low on experience (t[82] = 1.32, pHolm = .190). This finding repeated for the profiles that were high on market knowledge and low on coachability, and those that were high on coachability and low on market knowledge (t[82] = 1.08, pHolm = .285). These results indicate not only that competence and cooperativeness, as indicated by coachability, complement each other, but also that a lower level of experience or knowledge can be compensated for by a higher level of coachability. By contrast, we found no evidence for an interaction effect between industry experience or market knowledge and involvement with advisors and mentors (b = .05, p = .546 and b = .018, p = .869, respectively). This suggests that early-stage equity investors use these attributes separately rather than together when making investment decisions.

Interaction effects between competence and coachability.

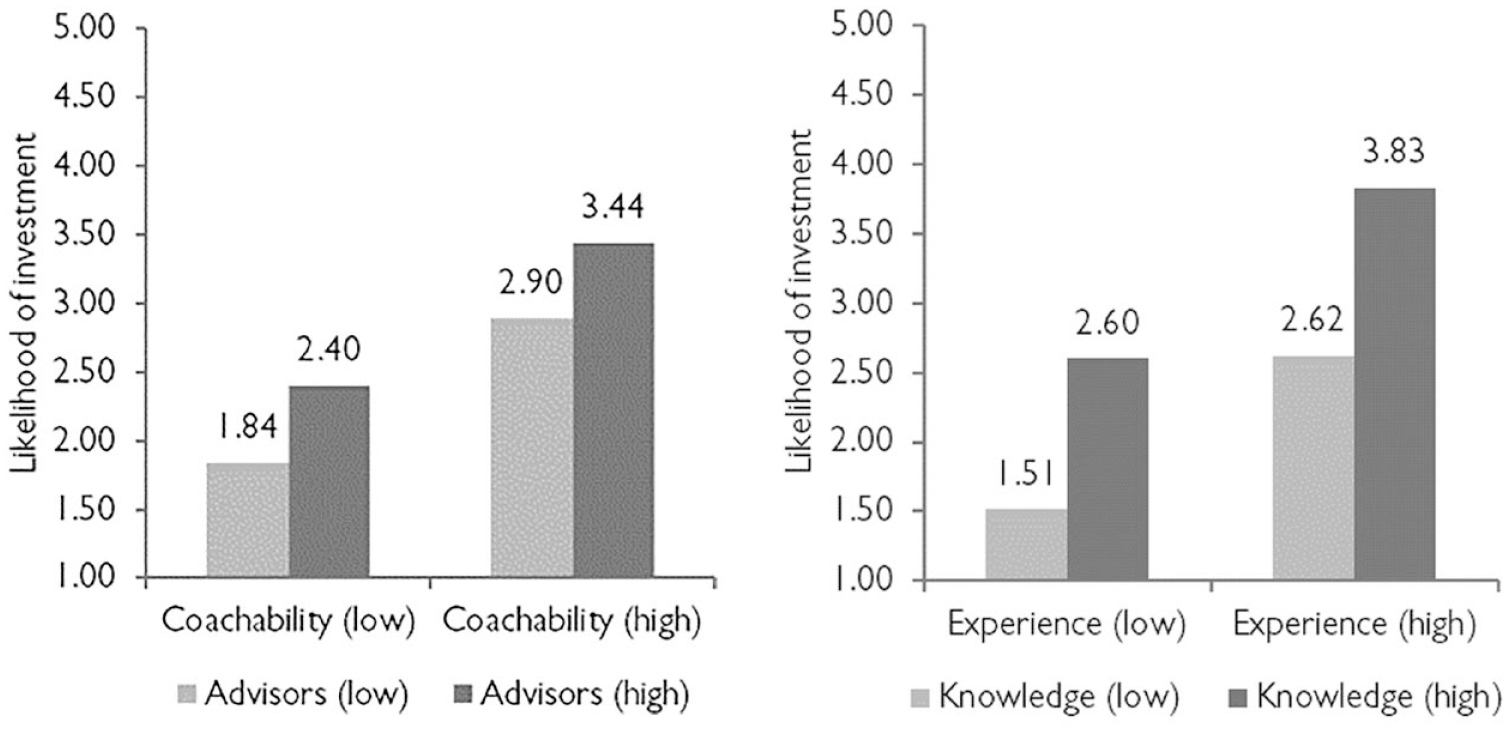

Furthermore, we found that the interaction effect between industry experience and knowledge was positive and significant (b = 0.12, p = .025), indicating that industry experience has a stronger effect on the investment probability of early-stage investors when combined with signals of high market knowledge. At the same time, the two attributes reflecting competence can be used to compensate for each other, as investors did not differ in their investment probability when confronted with profiles characterized by high industry experience and low market knowledge or by high market knowledge and low industry experience (t[82] = 0.33, pHolm = .745). This finding suggests that inexperienced entrepreneurs can compensate for their inexperience by demonstrating high market knowledge. No complementary or compensatory effects were found for coachability and involvement of advisors and mentors (b = −.02, p = .701) (See Figure 3).

Combination of attributes pertaining to the same content dimension and likelihood of investment.

Finally, we expected that more involved investors would place greater emphasis on the entrepreneur’s cooperativeness and less emphasis on the entrepreneur’s competence compared to less involved investors. We found no evidence that more involved investors placed less importance on industry experience (b = .01, p = .436) or market knowledge (b =−.01, p = .470) compared to less involved investors. Furthermore, although the coefficient for the interaction effect between investor’s level of involvement and entrepreneur’s coachability was positive, it was just marginally significant (b = .02, p = .084), and not significant for the interaction effect between investor’s level of involvement and entrepreneur’s involvement with advisors and mentors (b =−.01, p = .372). This indicates that investors with different levels of involvement assign similar weights to signals of competence and cooperativeness; however, those who are more involved may favor coachability slightly more.

Although not hypothesized, we also explored the cross-level interactions with one of the control variables: investor type. It has been suggested that angel investors may have a slightly different investment policy compared to venture capitalists (Fiet, 1995; Hsu et al., 2014). Angel investors placed more importance on entrepreneurs’ involvement with advisors or mentors compared to venture capitalists (b = −.16, p = .024). The results also indicated that venture capitalists may place slightly more weight on experience compared to angel investors (b = 0.18, p = .082), indicating that different types of investors do have slightly different investment policies.

In addition, we tested for potential between-country differences in investor decision-making that could be due to cultural differences. It has been suggested that individualism, uncertainty avoidance, and power distance significantly influence entrepreneurial activity (Hayton et al., 2002; Krueger et al., 2017). We grouped European countries into four clusters based on the level of these cultural dimensions 1 and performed a MANOVA. We found no statistically significant differences between the four groups in terms of the importance investors placed on each entrepreneur-level attribute or the investor’s level of post-investment involvement (V = 0.21, F[15, 234] = 1.19, p = .281).

To further explore any differences that might have arisen from differences between countries, we classified investors into four groups according to the development level of financial markets, following Farkas (2011), and the characteristics of the legal environment, following Farkas (2019). Financial market development and legal environment have been shown to influence early-stage investment activities across countries (Lerner & Tag, 2013). Again, we found no statistically significant differences in the importance investors attached to each entrepreneur-level attribute or the investor’s level of post-investment involvement between the four groups of countries based on the development of the financial market (V = 0.26, F[15, 234] = 1.48, p = .114) or the characteristics of the legal environment (V = 0.22, F[15, 234] = 1.24, p = .246).

Discussion

In this research, we leveraged social-psychological insights into social perception and evaluation (Abele & Wojciszke, 2007; Abele et al., 2021; Abele & Wojciszke, 2014) as the basis for developing hypotheses about how angel investors and venture capitalists evaluate the strength of the entrepreneur or entrepreneurial team, which has been shown to be a crucial consideration of early-stage equity investors (Bernstein et al., 2017; Huang & Pearce, 2015). In all, 44 European angel investors and 40 European venture capitalists participated in our conjoint experiment, which we analyzed using HLM to account for the nested structure of the data.

The results showed that signals of competence (industry experience and market knowledge) accounted for almost 60% of the investors’ final decision, while signals of cooperativeness (coachability and involvement with advisors and mentors) accounted for the rest. These results provide preliminary evidence for the hypothesis that early-stage equity investors prioritize an entrepreneur’s competence over cooperativeness. This finding was expected due to the highly interdependent nature of the relationship between investors and entrepreneurs. In situations of high mutual dependence, people’s concerns about the other party’s level of competence increase (Abele & Brack, 2013). In this particular case, the results suggest that early-stage investors are more concerned about whether the entrepreneur will be able to pursue his or her business goals than about the closeness of their relationship. Nonetheless, as indicated in previous studies (Ciuchta et al., 2018; Sudek, 2006), signals of the entrepreneur’s cooperativeness, especially coachability, are important to investors. One attribute related to cooperativeness (involvement of advisors and mentors) exerted notably less influence on early-stage investors’ decision-making than the others. Although the entrepreneur’s involvement with advisors and mentors is indicative of his or her openness to advice, it does not necessarily reflect the entrepreneur’s attitude toward a specific investor’s feedback. People are generally more concerned about others’ intentions toward themselves than toward others (Abele et al., 2021; Cuddy et al., 2008), especially when dealing with competent individuals (Wojciszke et al., 1998). This dynamic offers an explanation as to why investors prefer the combination of competence and coachability in entrepreneurs compared to competence and involvement with external advisors and mentors.

As hypothesized, we found that investors considered the entrepreneur’s competence and coachability together and were more likely to invest in entrepreneurs they perceived as both competent and coachable. This is possibly because this combination indicates that the entrepreneur is both able and willing to capitalize on the provided (financial and non-financial) resources (Allen, 2004) and more responsive to the relational governance mechanisms investors use to curb the entrepreneur’s opportunism (Carson et al., 2006). Although entrepreneurs who are perceived as both highly competent and coachable have an advantage in obtaining early-stage financing, our results revealed also that entrepreneurs can compensate for their lack of industry experience or market knowledge by presenting themselves as coachable, possibly because early-stage investors expect coachable entrepreneurs to be able to close this perceived competence gap by carefully considering and acting on the feedback they receive. This suggests that in entrepreneurship “getting along” might be essential for “getting ahead.”

Not surprisingly, more positive attributes pertaining to the same content dimension increase the likelihood of investment. However, the results regarding the interplay of attributes pertaining to the same content reveal a more complex picture. While our results showed that entrepreneurs could compensate for the lack of experience by demonstrating thorough market knowledge, this compensatory effect was not found in the case of cooperativeness. This likely reflects a big difference in importance and lower content similarity between coachability and involvement with advisors and mentors. While it is not surprising that an inferior (less important) attribute cannot compensate for a superior attribute (Bapna, 2019), these results could also imply that due to the variability in the content of attributes pertaining to the same overarching dimension, more nuanced theorizing is required.

Finally, the results showed that investors who were more involved had a slight preference for coachable entrepreneurs, a finding consistent with that of Ciuchta et al. (2018). However, we found no difference in the importance of the entrepreneur’s competence for investors with different levels of involvement, suggesting that there is high agreement across different investors about the importance of an entrepreneur’s competence; the preference for coachability, meanwhile, is more dependent on individual investor characteristics (MacMillan et al., 1985).

Although not formally hypothesized, we expected that angel investors would place more importance on attributes associated with the dimension of cooperativeness because angel investors are typically portrayed as being more involved in portfolio ventures than venture capitalists (Mason & Harrison, 1995; Mason & Stark, 2004; Morrissette, 2007). This differential involvement can be attributed to the non-financial motivations that often accompany angel investors’ financial motivations (Huang & Knight, 2017; Morrissette, 2007), as well as to their greater reliance (compared to venture capitalists) on relational governance to compensate for less comprehensive contractual governance (De Clercq et al., 2006; Fiet, 1995; Mason & Stark, 2004). However, in our sample, venture capitalists reported, on average, higher post-investment involvement compared to angel investors (as captured by the six items that describe investor value-adding activities, see Table 3). This may be due, in part, to the finding that more venture capitalists than angel investors in our sample undertook the role of lead investor, while both groups of investors were equally likely to syndicate investments. Indeed, the increasing syndication of angel investors has transformed the angel investment market (Mason et al., 2013, 2016). In particular, angel investors who invest as part of angel groups enjoy increased deal flow and improved due diligence, while reducing the need for individual angel investors to be involved in the investment and post-investment phase (Mason & Botelho, 2014). We did find that angel investors placed slightly greater importance on the entrepreneur’s current involvement with advisors compared to venture capitalists, but we observed no difference in the importance placed on the entrepreneur’s coachability. Compared to venture capitalists, angel investors have been shown to place more importance on the relevance of an entrepreneur’s network for venture development (Hsu et al., 2014). Although involvement with advisors and mentors indicates that an entrepreneur actively seeks out advice (a signal of cooperativeness), advisors are also an important source of legitimacy for a new venture (Becker-Blease & Sohl, 2015). So, on the one hand, this result can be seen as angel investors placing more importance on different signals of cooperativeness, while on the other hand, it could indicate a greater reliance on signals of new venture legitimacy in the face of more limited due diligence (Hsu et al., 2014).

Another interesting finding emerged from our post hoc inspection of the differences between countries. European countries are diverse both culturally (House et al., 2004) and in terms of institutional conditions (Farkas, 2011, 2019). Researchers that study the cultural impact on entrepreneurship typically argue that cultural values shape institutions and individuals and therefore impact the level and type of entrepreneurial activity in a particular nation, as well as the conditions for high growth potential entrepreneurship (Hayton et al., 2002). However, we did not find differences between clusters of countries grouped according to Hofstede’s cultural dimensions or financial or legal environment. This suggests that investors from different European countries to a large extent share the same investment policies regarding what they seek in entrepreneurs. This is in line with findings that the big two dimensions are used to assess others in comparable ways across cultures (Abele et al., 2016). Alternatively, these results could be attributed to shared values, beliefs, and investment practices across different nations. For example, entrepreneurship researchers have reported that entrepreneurs across culturally diverse countries share a universal culture of entrepreneurship (Mitchell et al., 2002). The values they hold often deviate from predominant values in a particular national culture (Hofstede et al., 2004; Jaén et al., 2013). The same could indeed hold for early-stage equity investors, many of whom have entrepreneurial experience themselves (Franke et al., 2006; Morrissette, 2007). Moreover, early-stage equity investors are also known for their large international networks (Drover et al., 2017) and most of them make investments in syndicates (Jääskeläinen, 2012; Mason et al., 2019). These factors could contribute to a high degree of shared values and beliefs among early-stage equity investors.

Implications for Theory and Practice

Early-stage equity investors’ perceptions are critical to understanding why some entrepreneurs receive funding and others do not (Connelly et al., 2011). Several studies to date have investigated how entrepreneurs can increase the likelihood of investment using a range of impression management tactics. Studies drawing on the impression management literature have greatly contributed to our understanding of how self-promotion, exemplification, flattery (Nagy et al., 2012; Parhankangas & Ehrlich, 2014), exaggeration (Cottle & Anderson, 2020), and skillful use of emotions during pitches (Chen et al., 2009) can influence investors’ evaluations of entrepreneurs. In this study, we focused particularly on investors’ evaluative perceptions, integrating the existing empirical evidence on angel investor and venture capitalist decision-making with well-established models of social judgment and evaluation from social psychology (Abele et al., 2021). We established competence and cooperativeness as two separate, overarching dimensions that early-stage equity investors consider in their decisions, and tested several hypotheses about the effects of the relationship between the two on early-stage investors’ likelihood of investing. Whereas previous studies on investor decision-making have assembled long lists of entrepreneur-related investment criteria (Ferrati & Muffatto, 2021), we suggest that early-stage investors’ evaluative judgments of entrepreneurs can be explained with two factors that have been shown to underlie social perception and judgment (Abele et al., 2021). This substantially reduces the number of factors needed to explain investors’ decisions.

We also considered the complementary and compensatory effects of the different attributes. We believe that this is an important step in the evolution of the literature on investor decision-making. To date, most studies have examined the importance of attributes for decision-making in isolation (Colombo, 2021; Svetek, 2022). However, the evidence suggests that early-stage equity investors integrate different information (Chen et al., 2009; Plummer et al., 2016; Warnick et al., 2018) to make holistic judgments about the entrepreneurs and proposed opportunities (Huang, 2018; Huang & Pearce, 2015; Svetek & Drnovšek, 2022). Instead of weighing all available information, investors rely on shortcuts (Harrison et al., 2015; Maxwell et al., 2011), which involve making aggregate assessments about factors of interest for early-stage investors (Jeffrey et al., 2016). This raises a key question about how early-stage equity investors combine information when assessing investment potential. Previous studies exploring interaction effects in the context of early-stage equity investment have focused on complementary effects, but have found mixed results (Cardon et al., 2017; Nagy et al., 2012; Plummer et al., 2016; Warnick et al., 2018). We propose and provide preliminary evidence that attributes representing different content dimensions (competence or cooperativeness) are in essence complementary, while attributes falling under the same underlying dimension can take on a compensatory role. This opens up several avenues for further theorizing and empirical research on the complementary, substitutive, and compensatory nature of different attributes in early-stage investor decision-making.

We also contribute to the emerging stream of literature on entrepreneur–investor fit by taking into consideration investors’ expected involvement in portfolio ventures. Previous research has shown that investors prefer entrepreneurs who are similar to them (Franke et al., 2006; Murnieks et al., 2011), which we propose is because people assume that similarity is conducive to cooperation (Toma et al., 2012). Ciuchta et al. (2018) and Mitteness, Sudek et al. (2012) have demonstrated that investors who are willing to mentor place more value on entrepreneurs’ displayed coachability when making investment decisions. Similarly, we found that more actively involved investors preferred entrepreneurs who were willing to accept their involvement in a venture, indicating that investors consider their compatibility with the entrepreneur. These results suggest that the selection and value-adding activities of early-stage equity investors are interrelated, thereby extending the contribution to the literature on the post-investment activities of early-stage investors (De Clercq & Manigart, 2007; Fili & Grünberg, 2016; Knockaert & Vanacker, 2013). Furthermore, we found that angel investors and venture capitalists evaluate entrepreneurs in a similar (although not identical) manner despite the differences in the source of investment funds, the range of investment motives, and the degree of professionalization. These results add to the scant body of empirical evidence on the differences in investment policies between angel investors and venture capitalists (Hsu et al., 2014; Mason & Stark, 2004; Van Osnabrugge, 2000).

With respect to practical implications, our results are relevant to entrepreneurs who are seeking early-stage financing. We show that there is a benefit for entrepreneurs to demonstrate not only their competence but also their cooperativeness, particularly their openness to the investor’s feedback, when interacting with angel investors and venture capitalists. Moreover, the results of our study show that entrepreneurs can mitigate some of their weaknesses through purposeful signaling to early-stage equity investors. Although industry experience is considered the most important entrepreneur-level factor in early-stage financing (Bernstein et al., 2017; Ko & McKelvie, 2018), we show that inexperienced entrepreneurs can compensate for their lack of experience by demonstrating thorough market knowledge and coachability. Inexperienced entrepreneurs may also benefit from the involvement of mentors and advisors. Although our research suggests that advisor/mentor involvement is the least important factor in assessing an entrepreneur’s funding potential, related research has shown that inexperienced entrepreneurs can substantially benefit from the assistance of an advisor or mentor (Lahti, 2014; Lehtonen & Lahti, 2009) in enhancing their venture’s investment readiness (Carpentier & Suret, 2015; Mason & Harrison, 2001) and consequently increasing the likelihood of obtaining early-stage financing.

Limitations and Future Research

The first set of limitations is related to the sample characteristics. Obtaining a good sample of participants is considered to be the most challenging issue in research on early-stage equity investors (Avdeitchikova et al., 2008; Farrell et al., 2008; Hsu et al., 2014). While the use of the Crunchbase database has been recently promoted in entrepreneurship research (Ferrati & Muffatto, 2020), such sampling methods have been criticized for their inability to identify the full spectrum of angel investors, especially smaller investors and investors who are not active in investor networks (Avdeitchikova et al., 2008; Farrell et al., 2008). Furthermore, response rates to cold email requests for participation in academic research among early-stage investors are low (Block et al., 2019; Mason & Harrison, 2002) and declining (Sheehan, 2001). To counter this, we asked participants to invite or recommend other early-stage investors to participate in the study. Snowballing is effective in increasing response rates, but is likely to result in an overly homogeneous sample of respondents (Avdeitchikova et al., 2008). It should be acknowledged that our sampling procedure may result in a biased sample due to undercoverage, non-response, and self-selection. That being said, the demographics of our sample resemble those reported in previous studies on European early-stage investors (EBAN, 2019; Franić & Drnovšek, 2019; Franke et al., 2006; Kollmann & Kuckertz, 2010; Zinecker & Bolf, 2015). Furthermore, there is a notable degree of heterogeneity between different European countries from which investor responses were sourced in terms of national culture (House et al., 2004) and conditions for entrepreneurship and early-stage equity investing (Bruton et al., 2005; Hege et al., 2003, 2009; Schwienbacher, 2008). We tested for differences between clusters of countries in terms of the importance of attributes and found no significant differences between them, suggesting that there is little variation in early-stage investors’ decision policies about entrepreneurs across European countries. Finally, it must be noted that although our sample size meets or exceeds that of comparable conjoint studies (Franke et al., 2006, 2008; Hsu et al., 2014; Murnieks et al., 2011; Warnick et al., 2018), the sample size of 84 investors may lack sufficient statistical power to detect differences among investors. Therefore, we may have missed some differences in investment policies resulting from differences in national contexts, levels of investor involvement in portfolio ventures, investor type, or other investor characteristics.

The second set of limitations arises from the research method employed. Conjoint experiments are particularly suitable for studying judgments and decision-making, as they mitigate threats to validity related to post hoc rationalization, social desirability, faulty memory, or inability to articulate complex or intuitive decision-making processes. This is why entrepreneurship scholars have advocated for a wider application of conjoint experiments in entrepreneurship research (Lohrke et al., 2010; Shepherd & Zacharakis, 1999, 2018; Wood & Mitchell, 2018). However, these types of studies are not without their limitations. The method requires a priori knowledge of the most critical decision attributes and the levels that affect the respondents’ decision-making (Lohrke et al., 2010). The importance of each attribute depends on the particular attribute levels and other attributes in the conjoint experiment (Orme, 2006). To date, researchers have uncovered numerous entrepreneur-level attributes that affect investor decisions (Ferrati & Muffatto, 2019) and could be interpreted as signals of competence or cooperativeness. The choices of attributes and their levels in our research were guided by the degree of published evidence. We also pretested these choices during interviews with early-stage investors. However, one should be mindful that a different set of attributes might yield different results. Therefore, we suggest that future studies test the proposed hypotheses using different sets of attributes pertaining to entrepreneurs’ competence and cooperativeness.

Angel investors and venture capitalists evaluate investment opportunities in a multiphase process. Often, only entrepreneurs who pass the screening phase have the opportunity to demonstrate to investors personal characteristics such as coachability (Carpentier & Suret, 2015; Harrison & Mason, 2017; Jeffrey et al., 2016; Mitteness, Baucus et al., 2012). One limitation of a conjoint research design is that it cannot closely mimic decision-making in situations that involve personal interaction. Although numerous researchers (e.g., Hsu et al., 2014; Warnick et al., 2018) have used this method to reliably identify and weight investor criteria related to entrepreneur personality and behavior, future studies should test the role of the “big two” in early-stage investor decision-making using methodological approaches in which entrepreneur behavior can be observed.

Finally, certain attributes may not fall neatly into one or the other dimension we proposed (competence and cooperativeness), nor may they be unambiguously perceived as positive or negative. This has been recently demonstrated in the literature on entrepreneurial passion. While, for example, Ciuchta et al. (2018) believed that entrepreneurial passion is reflective of the type of relationship entrepreneurs form with their stakeholders, Hsu et al. (2014) believed that passion is reflective of the commitment involved in pursuing entrepreneurial ambitions. Moreover, although the majority of scholars have found entrepreneurial passion to be a desirable trait (Mitteness, Sudek et al., 2012; Murnieks et al., 2016; Taylor, 2019), others have found that passion can signal uncooperativeness (Ho & Pollack, 2014). Different attributes can be equivocal/ambiguous and therefore difficult to understand in isolation (Plummer et al., 2016). Therefore, we encourage future studies to uncover the similarities between different decision attributes and their organization into broader dimensions. This could facilitate the study of complementary, substitutive, and compensatory effects of different attributes in early-stage financing. Lastly, this study takes a step toward uncovering how entrepreneurs can compensate for certain weaknesses they may have. However, as entrepreneurship is a team endeavor (Cooney, 2005; Harper, 2008), future studies could look into how different team members can compensate for each other’s weaknesses.

The above-mentioned limitations lead us to a discussion of the constraints on generality (Simons et al., 2017). Our data were collected from a set of European countries. The social-psychological studies on social judgments we draw on have been replicated in different world regions (Abele et al., 2008, 2016; Ybarra et al., 2008), which is why we would expect our findings to generalize across cultures (although there may be some variation in the relative importance of individual attributes according to culture). However, the hypotheses remain to be tested on Asian, African, and American samples before claiming cross-cultural generalizability. Moreover, our results also suggest that apart from investor type, other (non-hypothesized) respondent characteristics should not alter the results. Importantly, the results might not extend to alternative forms of early-stage financing such as crowdfunding. Compared to venture capitalists and angel investors crowdfunders make investment decisions quicker and with less information (Zafar et al., 2021), which is publicly available rather than acquired in the personal interaction with the entrepreneur (Macht, 2014; Mochkabadi & Volkmann, 2020). On the other hand, we do expect the uncovered investment policies of angel investors and venture capitalists to apply in both in-person and virtual communication situations. However, in the context of virtual communication, where establishing a trusting relationship is more challenging (Hsu et al., 2011), entrepreneurs may need to increase effort and make some adjustments to their signaling to achieve the required level of investor confidence in the entrepreneur’s cooperative behavior. Finally, we are confident that the findings will be reproduced with the same or similar methodology (e.g., conjoint analysis, maximum difference scaling, verbal protocol analysis) using the same set of attributes. However, testing the hypothesis in a complex real-world context is required to enable the generalization of results beyond a laboratory setting.

Conclusions

This research offers a novel perspective on early-stage investor decision-making by integrating social-psychological insights about social judgments with current understandings of the decision policies of angel investors and venture capitalists. We focused on the entrepreneur as a criterion in investor decision-making and proposed that investors perceive entrepreneurs who are seeking early-stage financing through the lens of competence and cooperativeness. Our empirical findings suggest that both dimensions significantly contribute to the perceived funding potential, with competence being of primary importance to early-stage equity investors. Moreover, the two dimensions are complementary, suggesting that entrepreneurs would benefit from signaling both competence and cooperativeness (coachability in particular). We also find that entrepreneurs can compensate for a lack of entrepreneurial experience by demonstrating good knowledge of the market. Finally, investors who are more involved in their portfolio ventures show slight preference for entrepreneurs who appear coachable. Our research highlights a range of interactions, configurations, and contingent relationships that provide deeper insight into how signals of competence and cooperativeness influence early-stage investors’ investment decisions.

Supplemental Material

sj-pdf-1-etp-10.1177_10422587221127000 – Supplemental material for The Role of Entrepreneurs’ Perceived Competence and Cooperativeness in Early-Stage Financing

Supplemental material, sj-pdf-1-etp-10.1177_10422587221127000 for The Role of Entrepreneurs’ Perceived Competence and Cooperativeness in Early-Stage Financing by Mojca Svetek in Entrepreneurship Theory and Practice

Footnotes

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author disclosed receipt of the following financial support for research, authorship, and/or publication of this article: This study was supported by a Sawtooth Software’s Academic Grant, which provided full access to their software for conjoint experiment design and data collection.

Notes

Author Biography

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.