Abstract

Drawing on goal-setting and stewardship theories, this study examines the management of family and business goals in family firms under transgenerational complexity, presenting a dynamic model of family stewardship. Through multiple case studies, we identify four distinct stewardship strategies, each with a corresponding governance structure: cultivating family stewardship (with family-dense governance), professionalizing family stewardship (with professionalized governance), harnessing external stewardship (with externally dense governance), and perpetuating external stewardship (with public companies’ governance). These strategies shift from family-centric to business-centric goal-setting approaches in sustaining the family firm. The study introduces stewardship transition capability as a missing cog for managing these transitions.

Keywords

Introduction

Family involvement in business management is advantageous for family firms because family members may act as stewards 1 to preserve family and business interests for the long run (Le Breton-Miller & Miller, 2013, 2015; Miller & Le Breton-Miller, 2006; Miller et al., 2008). Stewardship can increase the benefits of participative governance and long-term orientation (Eddleston et al., 2012). Stewards exhibit altruistic behavior (Eddleston & Kellermanns, 2007) and gain value and a sense of worth from fulfilling the goals of the business (Davis et al., 1997). This results in greater goal congruence motivate stewards to innovate, take calculated risks, and improve firm performance (Corbetta & Salvato, 2004). Accordingly, stewardship theory assumes collective, pro-organizational behavior (not individual, self-serving) where firm performance is enhanced by maximizing wealth (Madison et al., 2016).

However, in family firms, this stewardship in taking responsibility for, deciding on, and acting for the welfare of the family as the chief stakeholder (Hernandez, 2008) is conflicting because family and business interests differ. Prioritizing business goals is essential to sustain the business financially for future generations while prioritizing family goals is vital to preserving the family’s essence and interest in the business (Chrisman et al., 2012). This difference creates a paradox where competing demands between family and business goals influence strategic decision-making and behavior (Williams et al., 2018). For example, scholars acknowledge that family decision-makers first prioritize family goals (Nason et al., 2019) to protect the family’s socioemotional wealth (Gómez-Mejía et al., 2011). Doing so tends to regulate the strategic decision-making and behavior of the managing family, restricting their willingness to act in risky ways (Williams et al., 2018), but stabilizing the firm’s performance (Gómez-Mejía et al., 2022). However, the family’s concern about family goals paradoxically competes with achieving the firm’s business goals necessary to maximize wealth (Madison et al., 2016), creating tensions in strategic decision-making and behavior.

These goal-related tensions suggest an influence on the family’s approach to stewardship as family businesses change. A prominent time of change in the life of a family business is transgenerational succession. As a new family generation takes control (generational stage; Beck et al., 2011) and the number of family generations simultaneously involved in the business increases (generational involvement; Sciascia et al., 2013), transgenerational complexity takes hold. Transgenerational complexity is defined as greater heterogeneity in relationships, personalities, interests and goals, abilities, and education as the number of involved family members in the business grows (Gimeno Sandig et al., 2006). Cohesion is made more problematic when family involvement is differentiated (Lambrecht & Lievens, 2008). Transgenerational complexity increases with the multiplicity of succeeding generations participating in the family business (Simon et al., 2012). When more family members and branches become involved in the business, its activities, and decision-making, transgenerational complexity increases as succeeding generations prompt family and business priorities to change or compete (Lambrecht & Lievens, 2008). Where there is a lack of governance over transgenerational succession, the family can burden the business heavily, jeopardizing its sustainability (Suess-Reyes, 2017). This goal-setting tension questions how stewardship toward the family and the business is maintained under this complexity. While not treated as static in theory (Chrisman et al., 2012; Zellweger et al., 2013), stewardship is usually treated statically empirically. In turn, scholars have yet to sufficiently examine how family firms transition across family-centric and business-centric goal-setting approaches because of transgenerational complexity and what happens to the form and content of stewardship behavior during these transitions. Further, what stewardship behavior and governance structure these goal tensions result in when exacerbated by transgenerational complexity is persistently omitted in family business literature (Williams et al., 2018). Given these theoretical conundrums in the current understanding of goals and stewardship in times of transgenerational complexity, we ask: how do multigenerational family firms manage the antithetical contrast of family and business goals to adapt to the family’s transgenerational complexity?

We draw on goal-setting and stewardship theories to provide new knowledge on stewardship as a family firm transitions through different goal-setting approaches instigated by transgenerational complexities. We account for the multigenerational family to decipher the transgenerational complexities that shift goal-setting approaches in ways that transform into changes in stewardship strategies and their corresponding governance structure. We conduct a firm-level analysis of multiple case studies of family firms in the Middle East to advance theory and knowledge on the transformation of family stewardship to accommodate the family’s transgenerational complexity. We theorize that depending on the managing family’s approach to goal setting (family-centric vs. business-centric approaches to goal setting), the governance of the family firm is adaptive, changing the stewardship of the family and the business to reconcile contrasting family and business interests. We make three important contributions to goal-setting and stewardship theories. First, we contribute to stewardship theory four new stewardship strategies that family firms transition through and among as their goal-setting approach shifts from family-centric to business-centric. We also show that each stewardship strategy exhibits a different approach to governance to maintain stewardship behavior as the goal-setting approach changes and prevents the family’s transgenerational complexity from burdening the business. Second, we contribute to the intersection of goal-setting and stewardship theories by providing a theoretical framework explaining how transgenerational complexities prompt stewardship transition. Our theoretical framework also explains how stewards’ understanding of goals erodes as the firm transitions to different goal-setting approaches. Third, we derive and conceptualize “stewardship transition capability” as essential to successfully transition across goal-setting approaches, manage the antithetical contrast of family and business goals during the transition, and change stewardship strategy timely and effectively to protect against transgenerational complexities.

Theoretical Background

Family Stewardship, Paradoxical Goals, and Transgenerational Complexity

Stewardship prioritizes the organization’s interest instead of self-interest, emphasizing responsibility and obligation toward the organization’s success (Hernandez, 2012). Stewardship theory typically draws attention to pro-organizational behavior (Davis et al., 1997) that uses the firm’s resources to support collective goals (Le Breton-Miller & Miller, 2006). Stewardship theory portrays managers as stewards who desire to serve the firm’s interest. Their self-interests will naturally align with those of their overseers (the firm’s owners; Madison et al., 2016). Governance structures are then put in place to support that natural alignment of interests (Davis et al., 1997; Madison et al., 2016). Family stewardship is a central premise in family firms due to the unification of ownership and management. However, unlike a nonfamily firm, the object of their stewardship is not necessarily the financial well-being and profit of the business but the pursuit of family goals (Kandade et al., 2021) to serve the family interest.

Stewardship manifests in maintaining and transferring a stable business to the next generation (Davis et al., 2010). However, family firms are hybrids combining family (social) and business (economic) logic, with different norms and expectations contained in both logics. Family firms then experience a paradox because the pursuit of family and business goals creates competing demands between the two distinct goal-setting approaches (Shepherd et al., 2019). These competing demands can disrupt allocating resources, reduce organizational efficiency, increase conflict, and hinder family firms’ decision-making (Shepherd et al., 2019). In time, tensions between family and business goals may invoke a “mission drift” where the family and business diverge from their originally intended mission because of an inability to reconcile relevant strategic acts with its stated (but paradoxical) goals (Shepherd et al., 2019). The conflict arises when stewarding the family interest clashes with preserving the business interest, and when pursuing family goals competes with pursuing business goals. These pressures require reconciling with stewardship to manage the competing interests of the family and business (Miller & Le Breton-Miller, 2021). Transgenerational complexity can further fracture the joint family–business identity, especially when appropriate governance structures are absent (Suess-Reyes, 2017). A family business is already emotionally and relationally complex (Labaki & D’Allura, 2021). Thus, as more generations (their members and their branches) take part in the family business (Simon et al., 2012), identities fracture, and family ties tend to loosen (Suess-Reyes, 2017). Therefore, sustaining stewardship and reconciling self-interest with collective interest becomes far more complex under these conditions.

Debates around managing stewardship over the family and the business are inconclusive. First, family influence yields a competitive advantage because it contributes resources to the business (Chrisman et al., 2005). However, family influence also creates conservative tendencies due to pursuing familial goals, reducing willingness to take business risks (Gómez-Mejía et al., 2007). Second, the managing family is committed to working in the interest of the family business, which mitigates monitoring costs and conflicting principal-agent interests (Miller et al., 2014). However, family concentration in management can lead to conflicts and disputes (Eddleston & Kellermanns, 2007). Increased generational involvement in the ownership and management of the family business then requires new governance structures. These can include a revised board of directors and confinement of family involvement to the strategic management level for control and monitoring purposes (Madison et al., 2017) to restore stewardship and ensure performance against family and business goals.

Competing demands also manifest in the diversity of family goals that influence strategic decision-making and behavior (Williams et al., 2018). Whereas some families favor pursuing family goals and benefit by preserving the family transgenerational control, others are more likely to pursue business goals (Miller & Le Breton-Miller, 2021). Family firms can sometimes endure the challenge of synthesizing the competing demands of the family and the business, for instance, dealing with the business demand for growth and expansion or meeting the family demands for financial liquidity (Ingram et al., 2016). Growth and profit maximization goals are pivotal to sustaining the business, and socioemotional targets are essential to maintaining family cohesion and interest. However, these competing demands are aggravated by the transversal nature of transgenerational complexity that characterizes multigenerational family businesses (Ingram et al., 2016). Transgenerational growth and transitions force family businesses to confront the different expectations and visions of multiple generations whose worldviews are also shaped by the societal nature (Magrelli et al., 2022) of those generations in the Arab Middle East (Samara, 2021). Therefore, understanding how family firms manage stewardship and the contrast between family and business goals when facing transgenerational complexity is essential.

Despite this importance, stewardship theory does not yet account for when families (and their businesses) transition from a family-centric approach to goal-setting to a business-centric approach (shifting between two points of a spectrum), omitting the circumstances that lead families to change their goal-setting approach or its balance. Also, stewardship theory does not consider that stewards acting in the organizational interest become misaligned when circumstances erode their understanding of new goals emerging while the family and business change (e.g., when approaching succession or during transgenerational transfer). While stewardship seems to be tacitly conceptualized as a state, we argue that stewardship is a property whose maintenance calls for bespoke stewardship strategies and corresponding governance structures. Moreover, because we conceptualize stewardship as not fixed, a single stewardship strategy cannot then exist. Capabilities are needed to support and protect stewardship behavior because families’ transition through goal-setting approaches (e.g., family-centric to business-centric) frays and erodes stewards’ understanding of goals.

A Goal-Setting Theory Lens to Family Stewardship and Transgenerational Complexity

Goal setting shapes the firm’s strategic decision-making, behavior, and outcomes. Goals transform into organizational strategies, policies, and actions (Locke & Latham, 1990) necessary for developing competitive resources and capabilities (Gagné, 2018). Goal-setting theory (Kotlar et al., 2018) presumes that conscious goals and intentions direct human action and that “goals are immediate, though not sole regulators of human action” (Locke & Latham, 1990, p. 27). Accordingly, goal-setting theory emphasizes converting individual goals into organizational policies and actions (Kotlar et al., 2018) to predict strategic decision-making and behavior. Kotlar and De Massis (2013) acknowledged the complexity of family firms’ goal setting due to the family’s integration into the business. This integration leads to goal diversity, typically around a general (but not exclusive) collective commitment to family goals. However, Le Breton-Miller and Miller (2013) argued that a family’s commitment to their goals may vary based on the family’s participation in the business, influenced by the family’s generational growth and evolution. This variation is attributed to family generational involvement and the generational stage where new generations prompt change in family firms’ business and familial goals. The generational stage represents the family generation in control (Beck et al., 2011; e.g., the founding, second, or subsequent generation after a succession occurs). Each generation has different family and business paradigms depending on their education, experiences, interests, and sociocultural exposure (e.g., Calabrò et al., 2021). Generational involvement represents the number of family generations simultaneously involved in the business (Sciascia et al., 2013). The larger the number and branches of generations involved, the more different goals and interests permeate the family business, exacerbating goal tension. Governance is indispensable under such complexity (Gimeno Sandig et al., 2006; Lambrecht & Lievens, 2008).

The paradox caused by needing to balance priorities between family and business goals creates competing demands. We reason these must influence the stewardship behavior of the firm—and the strategies needed to restore stewardship. Notwithstanding the significance of family goals in steering stewardship behavior, this perspective assumes a relatively static view of family complexity (Nason et al., 2019). The managing family must select among competing goal priorities that serve the family interest (family-centric) versus the business interest (business-centric) (Chrisman, 2019). Existing findings are inconclusive (Williams et al., 2018) because studies routinely overlook the acts of stewardship families must use to manage priorities distributed between family and business interests. Tensions around maintaining stewardship amplify in multigenerational family firms because of the presence of multiple family generations in their numbers, branches, and stages (Zellweger, 2017). The insertion of successive new generations introduces different ideas and worldviews that dilute consensus and compel priorities and goals to reshape and rebalance. For these reasons, family businesses are likely to shift between family-centric and business-centric goal-setting approaches and transition to new stewardship strategies to sustain the family business rather than those approaches remaining static. We contend that transition among new family stewardship arrangements is essential in times marked by transgenerational complexity and continued growth in the number of succeeding generations. Currently, there is no theoretical framework residing within either goal-setting theory or stewardship theory to explain this transition process, that records or depicts what may happen to stewardship strategies or the forms they may take, or describe the circumstances and conditions needed to contain and manage the antithetical contrast of family and business goals.

Methods

The study follows the multiple case studies method to collect comparative data to yield an accurate and generalizable theory (Eisenhardt, 1989, 2021; Yin, 2018). Following the aim of this study, the Gulf Council Countries (GCC) region was selected as the context of the study. Family firms in the GCC constitute a significant component of their local economies (Davis et al., 2000). For instance, in Bahrain, family firms contribute 80% of the local Gross Domestic Product (GDP) (Palalić et al., 2023). In Saudi Arabia, family businesses constitute 63% of the private sector and contribute 66% of the private sector’s GDP (Argaam.com, 2021). The GCC region is a rich context with long-standing family firms that have operated through many uncertainties and turbulences (Samara, 2021). Moreover, long-standing family firms in the GCC exemplify complexity as the majority are large multinationals and have diversified into many industries.

Multiple Case Study Method

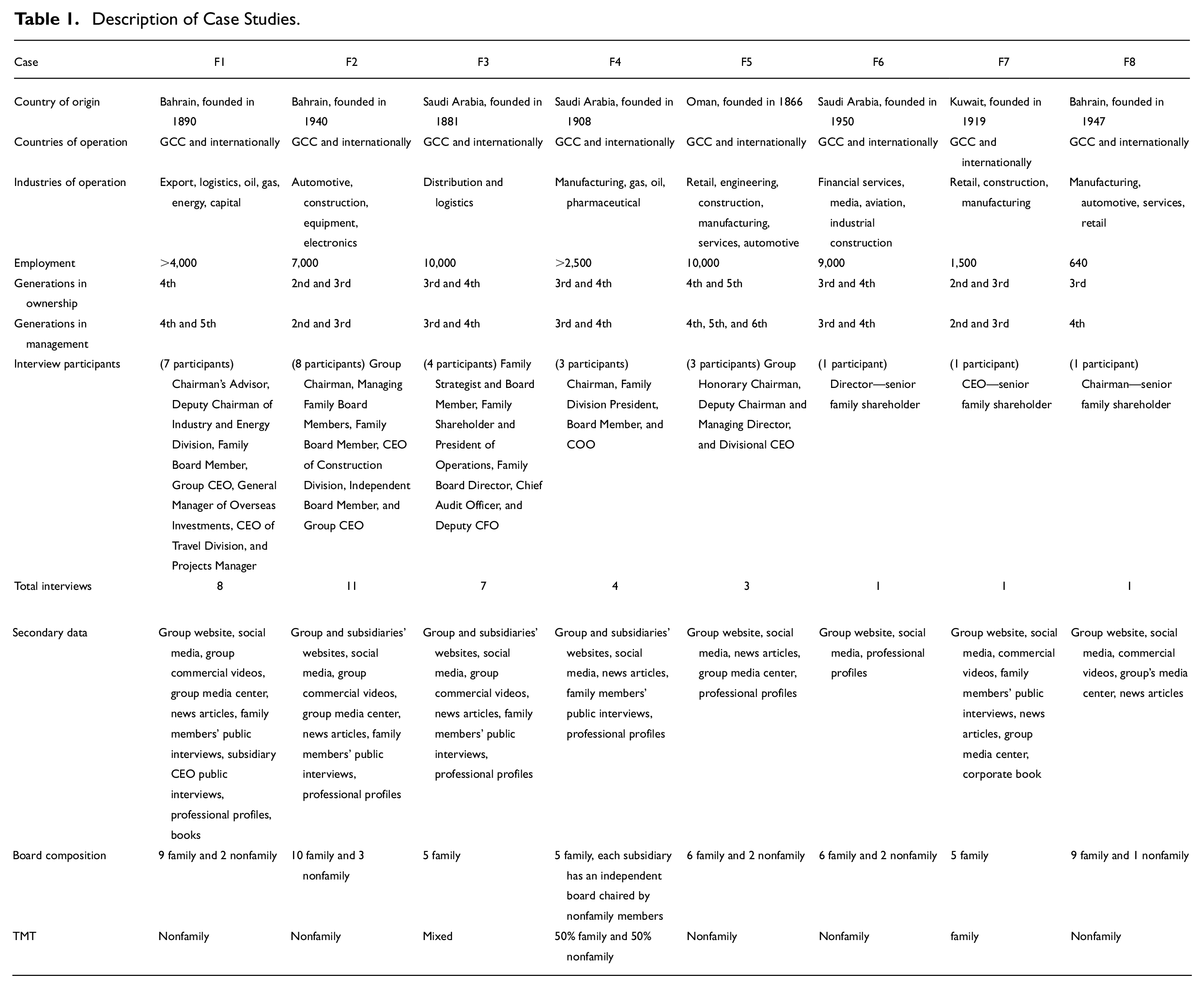

To capture the complex goal-setting and adaptive stewardship behavior of long-standing family firms, we followed a purposeful criterion sampling strategy (Fletcher & Plakoyiannaki, 2011; Patton, 2002) in selecting cases of family firms to study the phenomenon from “transparently observable” cases (Eisenhardt, 1989). The case sampling criteria include five elements: ownership, governance, generation, age, and industry. The sample family firms are 100% family-owned, with multiple generations involved in ownership and control of these firms (consistent with Chrisman et al., 2012). They are large, multigenerational, and diversified multinationals that follow the family’s vision across generations (Chua et al., 1999). The case selection process also ensured that each case had knowledgeable participants of the phenomenon of interest (Creswell, 2013). Following Eisenhardt’s (1989) recommendation, our study sample includes eight long-standing family firms from the GCC. Most of the selected cases are classified among the top 100 Arab family businesses for 2020, according to Forbes Middle East magazine (Forbes Middle East, 2020). They are prominent multigenerational family firms that have operated successfully for at least 50 years. These firms were founded between 1866 and 1950, representing a spread of generations that reached the sixth generation in our data. Table 1 provides the details of each case.

Description of Case Studies.

Data Collection

Data sources for this study include interviews, observations, and secondary data analysis, ensuring triangulation. Semistructured interviews were the main data collection method. The selection of interviewees followed the purposeful sampling method (Miles et al., 2014) and was informed by our research aims. Participants were selected based on their experiences with the phenomena of interest (Creswell, 2013) and their involvement in the strategic management of their firms. The study comprises 29 participants and 37 interviews from 8 different family firms. The interviews were 60 minutes on average. The interview protocol included questions about the history of the firms, current and future goals of the firms, the governance and management structure, historical changes in the goals and structure of the firms, adaptation to family- and environment-related dynamics, and corresponding changes in the strategic management of the firm. The participant sample consists of two groups: managing family members and nonfamily managing directors involved in strategic management (the participants are described in Table 1). However, F6, F7, and F8 did not grant approval to interview nonfamily participants, and interviews were limited to one family member in strategic management in each case. The participants from F6, F7, and F8 were senior family shareholders and had senior authority (Director, CEO, and Chairman, respectively) over strategic management. They are elite informants whose knowledge of the family, the business, and its strategies are exemplary and detailed (Solarino & Aguinis, 2021). Therefore, these interviews were included as they provided additional theoretical richness. Observation field notes were created, and secondary data sources, including various documents and publicly available information, were collected and analyzed. Further secondary data was collected and analyzed, including the websites of the family businesses, their groups and their subsidiaries, social media, group commercial videos, group media center material, news articles, senior management public interviews, and professional profiles. We achieved triangulation by collecting and analyzing interview data, observation field notes, and secondary data to observe and understand the studied phenomena from different perspectives (Patton, 2002).

Analytical Approach

Data analysis followed the process recommended by Gioia et al. (2012), Miles et al. (2014), and Eisenhardt (1989). This iterative data analysis process included four systematic stages that guide the development of cohesive constructs and an integrative conceptual framework.

Stage 1: Within Case Analysis

Initially, each interview of each family firm was analyzed and examined for similarities and variances, which resulted in identifying patterns related to the phenomena of interest (e.g., goal diversity and priorities, governance adaptation, stewardship). Follow-up interviews were carried out to resolve gaps recognized in the collected data. We then developed descriptions for each family firm and triangulated the primary data with secondary sources for comparisons and confirmation. We used NVivo 12 software by Lumivero for data analysis, which was consistent with the coding process advocated by Miles et al. (2014). First-order coding was performed for each family firm and was organized into categories in line with the interview questions to facilitate cross-case comparisons.

Stage 2: Linking Emergent Themes Within Each Case

This stage included identifying links of similarities and differences between the first-order codes, which were then grouped into second-order codes. This process allowed the emergence of themes and concepts from the data (Strauss & Corbin, 1998). It helped identify constructs of interest that enabled the creation of more abstract second-order codes to help answer the study question.

Stage 3: Cross-Case Analysis

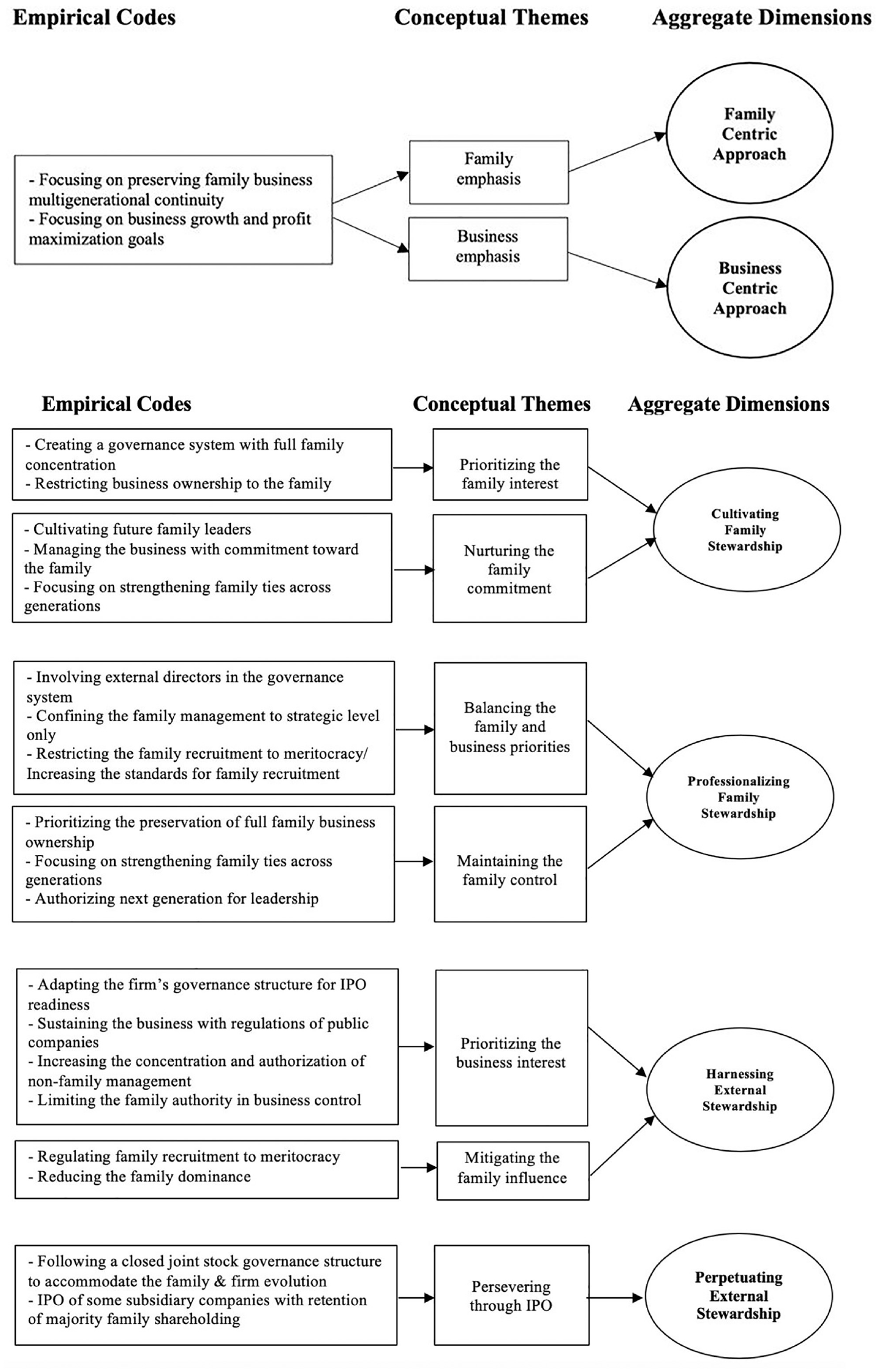

First, the cross-case analysis followed the standard techniques recommended by Eisenhardt (1989, 2021) and the use of tables (an explanatory effects table and effects and dynamics table; Miles et al., 2014) as an analytical tool for greater transparency and trustworthiness. This step included identifying commonalities and differences across the family firms based on the categories created in stage two. Following the case-oriented strategy for cross-case analysis (Miles et al., 2014), the eight family firms were grouped into four polar clusters based on common patterns and configurations and extreme dimensions that differentiated them (Eisenhardt, 2021). This analysis process derived six aggregate themes (Figure 1) representing the core patterns across the cases (Strauss & Corbin, 1998). These were used to inform the cross-case analysis and theoretical development.

Data structure and analysis.

Stage 4: Theoretical Framework Development

To sharpen the developed data structure and constructs, we carried out a data condensation (Miles et al., 2014) effort on the first-order coding by paraphrasing and grouping multiple codes that convey similar meaning into higher-order constructs linked to the extant literature. The most robust findings were considered and included to converge on a parsimonious set of constructs (Eisenhardt, 2021). This data analysis process derived several adaptive strategies and a novel theoretical framework.

Findings

We detail our main findings by reflecting on the aggregate theoretical dimensions that emerged from the data analysis. We then present how the family businesses in our data transitioned through goal-setting approaches and developed corresponding stewardship strategies to combat pressures caused by transgenerational complexities.

Goal-Setting Approaches and Corresponding Family Stewardship Strategies in Adapting to Transgenerational Complexity

By investigating and analyzing family firms’ goal-setting approaches, we identified a pattern of approaches to goal setting between being family-centric versus business-centric. With further data interpretation, we identified when family firms shift and vary between these goal-setting approaches due to transgenerational complexity. After these shifts, new stewardship strategies emerged with corresponding governance structures particular to each stewardship strategy.

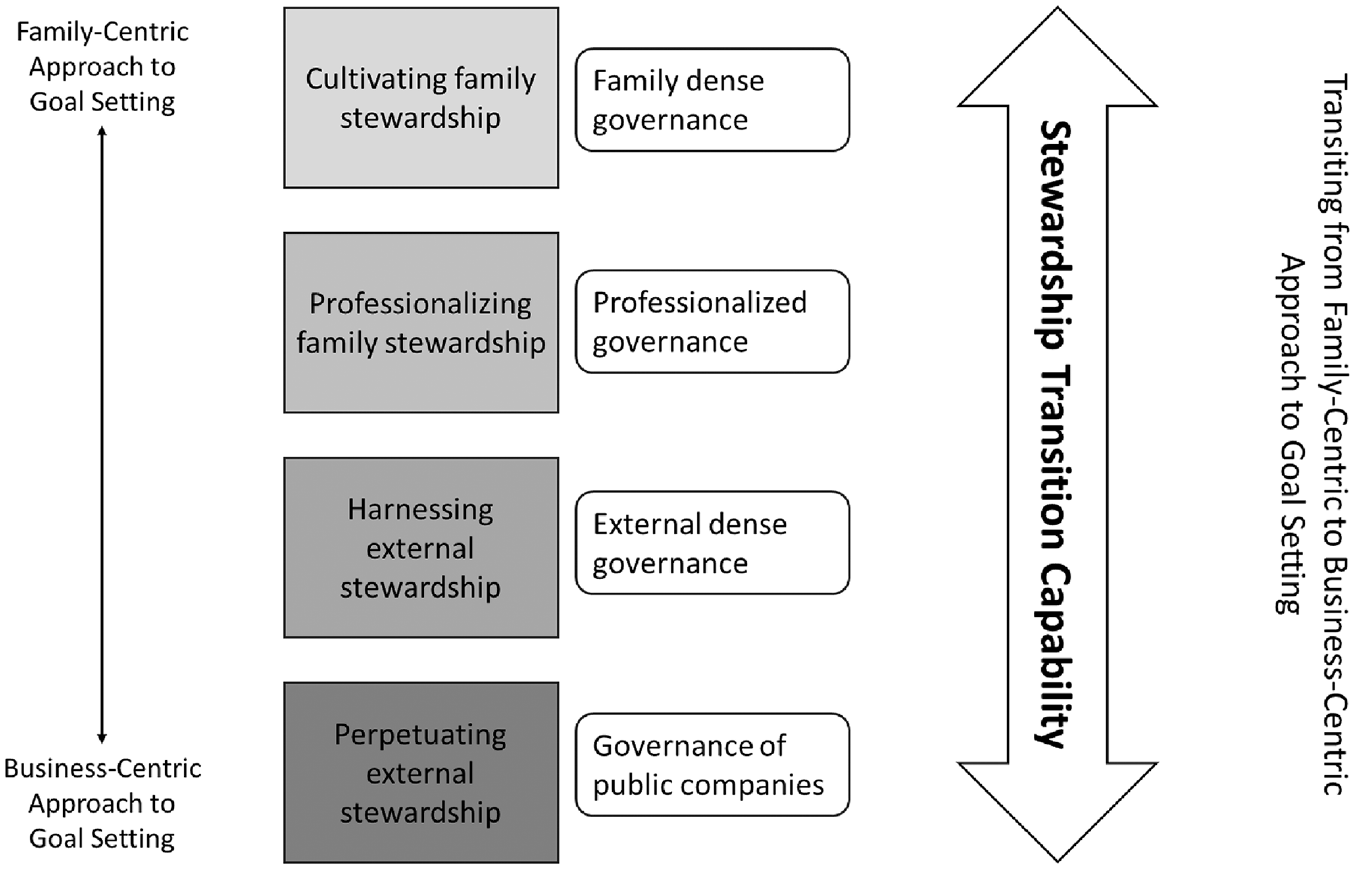

The eight sample family firms polarized in their goal-setting approaches between a family-centric approach to goal-setting and a business-centric approach to goal-setting (Figure 1). The family-centric approach denotes firms prioritizing the family interest in their stewardship strategies and governance. The business-centric approach denotes firms prioritizing the business interest in their stewardship strategies and governance. The eight family firms varied between four identified stewardship strategies and corresponding governance structures depending on their goal-setting approach to managing the contrast between family and business goals: cultivating family stewardship (family-dense governance), professionalizing family stewardship (professionalized governance), harnessing external stewardship (external dense governance), and perpetuating external stewardship (public companies governance). These are represented schematically in Figure 2. The findings show that these family firms transition between these different stewardship strategies as their goals and priorities change from family-centric to business-centric. Successfully transitioning between stewardship strategies relies on a stewardship transition capability, representing the force moving from one strategy to another one as the family businesses’ goal-setting approach shifts from more family-centric to business-centric. We do not expect a strictly linear force transitioning from family-centric to business-centric goal setting and through corresponding stewardship strategies. A family business may oscillate between degrees of email-centric and business-centric goal-setting approaches and change its stewardship strategies and corresponding governance structure in either direction.

Goal-setting approaches and corresponding stewardship strategies.

Family-Centric Approach to Goal Setting

The family firms following this approach focus on preserving the family’s interest by prioritizing family goals primarily or exclusively. Family stewardship in this group manifests in their commitment to preserving strong family ties and meeting their financial needs (i.e., dividends) regardless of the business interest. They prioritize maintaining the family’s welfare even at a cost to business growth and development. Depending on the circumstances of the family’s transgenerational complexity (e.g., a continuous increase in the number of shareholders), this group of family firms varied in their stewardship strategies between cultivating family stewardship and professionalizing family stewardship.

Strategy 1. Cultivating Family Stewardship

The family firms that followed this strategy are bound to family ownership and management to maintain complete family control over the business. They pursue stewardship by depending primarily on family members for senior operational and strategic management and business funding. These family firms are conservative about professionalizing the board and involving external directors and are more likely to retain full family ownership of the business.

The F3 family firm provides a compelling illustration of this strategy. Its third and fourth generations manage F3, and F3 has long followed a traditional flat management structure, where the family fully controls and manages the business. At a managerial level, external professionals are involved as operational managers, but none at the firm’s senior management. They are also conservative about involving independent directors on the board. This is related to trust issues toward externals and due to following a traditional and perhaps conservative approach, whereby the family is entrusted to manage (steward) the business. This traditional style of relying on complete family control has successfully preserved the family business by reinforcing trust in family management and maintaining harmony among family shareholders. Therefore, F3 is continuing multigenerationally with full family stewardship. The nonfamily deputy CFO stated, “board of directors is all family members, mostly from the remaining third generation (the active members), and from the fourth generation. There are no external directors yet.” In addition to the family’s conservativeness toward including external directors in senior management (professionalization), they believe in preserving family ownership in its entirety. They deny allowing external shareholding because they aim to cultivate full family control over the business across generations. Therefore, to deal with the transgenerational complexity associated with an increase in family shareholders, the solution they have is the internal buyout of shares of the existing shareholders. As stated by a fourth-generation family president: “In our case for the family business, it’s a no way, it’s a no-no, because we want to maintain it as a family business, it’s our business.” Consistent with maintaining family control over the business, members of this family have strong ties, and next generations show great respect to older generations. In F3, trust and strong family ties have been key factors that preserved business continuity through to the fifth generation. The family president of the fourth generation stated: “In the past, the success of the business was basically due to the close relations between second and third generations. We were able to manage the relationships in a traditional and informal setting until [this current] generation because there is trust and respect in relationships.”

Another family firm following the cultivating family stewardship strategy is F7, managed by its second and third generations. Similar to F3, this family firm is highly conservative about professionalization and thus heavily dependent on family management. F7 has a traditional governance structure to maintain its goal of preserving full family control over the business: “the second generation is still in management within the group; chairman and board members are all family” (CEO, G3). The older generation of F7 also recognizes the importance of nurturing family members in the business and developing family leadership to maintain family control. Therefore, involving the next generation in the business includes multilevel training before joining at a management level. As the family’s GM explains: “Some of the second generation is still in management within the group. Their presence in the business gave support to the third generation to work within the group gradually and wasn’t done in an unstudied way. The responsibility of each generation is to transfer the work to the next generation in a professional way.”

Strategy 2. Professionalizing Family Stewardship

The findings outlined a group of family firms (F2, F5, and F8), which transitioned from cultivating family stewardship to a professionalized family stewardship strategy by professionalizing the board of directors and executive management with external managers. This transition was enabled by an aspiration to grow the business with external professional inputs, thereby curtailing the family influence on the business to have higher objectivity in decision-making as the family’s transgenerational complexity increases. Although these family firms are conservative and bound to family ownership and management, they recognize the importance of professionalization to sustain and develop the business.

F2, managed by its second and third generations, decided to introduce external directors to the board years ago to benefit from the input of external professionals to support its business expansion. An independent nonfamily board director explains: “I was invited to be on the board about 15 or 16 years ago as an independent director to help them on the board. So, basically looking into how the family business could be structured to live for the next generations.” In F2, the roles of Chairman and CEO are separated, and the family leadership is confined to the strategic level to supervise the business. While the family dominates the board of directors and leads the business’ subsidiaries, external professionals are involved as senior managers at the operational level to maintain business growth and development to preserve family business continuity: “We decided that it’s really better if we act on the board level rather than working individually, so none of the family members is working inside in the company, we’re working on a supervisory level as directors in charge” (Chairman, 2G). Further, to steward the business from the family’s growing transgenerational complexity, F2 regulates the family influence on the business by incorporating a family constitution written directly by members of the third generation themselves, who were trained in a specialized educational institution in France on what is needed to maintain a family business multigenerational continuity. This effort includes regulating the entry of next generations into the family business and stabilizing transgenerational complexity: “We’re now working on the family charter to put all of the rules of how to enter into the business […] it’s very important to keep everything as transparent as possible” (Acting Director 2, 3G).

In F2, stewardship practices of the older generation manifest in monitoring the progress of the next generation and their ability to preserve business continuity by maintaining family unity for the next generations. This monitoring is with the view that if the third generation failed to show the ability to proceed with strong family ties and unity in preserving the business success and continuity, then the chairman would prepare the business for public offering, despite the interest in keeping full family ownership of the firm, as the chairman explained: “We sent them to a specialized school in France, 23 of them, to learn how to manage together […] they’re having meetings discussing about the future, if we see that they are unable to, then really we have to sell the company publicly as an IPO.” Whereas F2 is classed as having professionalizing stewardship and follows a family-centric approach to goal setting, the family is prepared to adapt their goal-setting approach and stewardship strategy to resolve complexities from the family’s intergenerational growth. F2 transitioned from a cultivating family stewardship strategy to a professionalizing family stewardship strategy as a precautionary step to avert conflicts between the 23 members of its next-generation regarding business leadership and avoid exposing the family business to failure or disintegration. This transition was driven by the learning developed from stories of other family business failures and disintegrations that occurred locally and regionally due to family conflicts regarding business leadership. Therefore, in F2, the next generations were sent for international training on sustaining the family business, and the governance structure was proactively adapted in the stewardship transition. This example shows a priority of the business interest (maintaining its longevity and viability) over the family interest (maintaining transgenerational family control).

Additionally, F5, managed by its fourth, fifth, and sixth generations, transitioned to professionalizing family stewardship to resolve the family’s transgenerational complexity. Until recently, F5 had followed a family-dense, traditional management structure, where the roles of chairman, deputy chairman, CEO, board members, and some executive management roles were all occupied by family members. However, since 2019, following the appointment of a younger family member as deputy chairman, the board of directors agreed to implement significant changes to the firm’s governance by transitioning to a professionalized governance structure. This transition aimed to renew and expand the family business and enhance its performance with diversified management and external professionals. Therefore, F5 adapted its governance structure by separating family ownership from business management, which limited family management to the strategic level. F5 was also in the process of changing the family constitution and introducing independent directors to the board, as stated by the 5G family Deputy Chairman: “So we’ve gone through a huge change process now, we reduced the family board members from 9 to 6, we professionalized our board and family members do not interfere in the day-to-day operations, we allow the professionals to run the business, which means we’ve separated the management from the family. We are now at the verge of revisiting the shareholders agreement and family constitution; we’re at the verge of creating a family council.” The appointment of the next generation in F5 is based on their competency: “the next generation as I mentioned, we only involved them based on meritocracy” (Deputy chairman, 5G). Nevertheless, the family has invested in maintaining strong family ties and relations across generations: “We are a very close family, we know each other very well, we trust each other very well” (Chairman, 5G).

Another family firm that followed this strategy is F8, managed by the fourth generation. This family firm was formed from the debris of a regional family business empire that failed to survive family conflicts in the second generation. F8 was first established by following the cultivating family stewardship strategy (with family-dense governance). However, following unresolved family feuds and the firm’s disintegration at the second generation, F8 was reinstated by a family member of the third generation in an attempt at business continuity. By following the professionalizing family stewardship strategy with a professionalized governance structure, F8 averted family conflicts and controlled the involvement of its next generations. Having learned from the previous disintegration, F8 separated the chairman and CEO roles, restricting family management to the strategic level and external professionals at the operational level. Therefore, central to family business continuity is the effective separation of family ownership from business management and the integration of a family constitution and succession planning into the family firm’s governance.

In F8, ownership and management are separated so that family members do not occupy managerial roles. Similar to F2 and F5, in order to control the family’s involvement and influence over the business, a family constitution was incorporated at F8 to standardize the introduction of family members to the business through predetermined criteria, as stated by the 4G family chairman: “before joining our company, any family member has to work outside the group for a minimum of 1 year. We joined the business in what we call supporting roles, roles that have an exposure to the business but not directly, which means we learn the business and build the skills set as we grow up.”

Business-Centric Approach to Goal Setting

Family firms that follow a business-centric approach to goal setting emphasize business interests by prioritizing business goals. These family firms are less conservative about involving externals in business ownership and management (professionalization). Despite having residual concerns about family goals, the priority is to meet business goals and business interests first and foremost, even if that mitigates the family interest. The family firms following this approach varied in how they adapted their stewardship strategies depending on their transgenerational complexity. Two strategies appear in our data: harnessing external stewardship and perpetuating external stewardship.

Strategy 3. Harnessing External Stewardship

The findings show that the firms that follow this strategy transitioned through the strategies of “cultivating family stewardship” and “professionalizing family stewardship” and reached the stage of adapting and transitioning to harnessing external stewardship as a strategy to accommodate the continuous increase in the number of family shareholders and evolution of the family transgenerational complexity.

In representing this strategy, F1, currently managed by its fourth and fifth generations, follows a harnessing external stewardship strategy. F1 professionalized the governance structure to expand the business and preserve its continuity through advanced professionalization. This professionalization included separating the family from business management, incorporating a family constitution and succession planning, and integrating external professionals on the board of directors and subsidiary management. F1 is on the verge of another stewardship transition by re-adapting the governance structure and succession planning to resolve the increasing complexities attributed to the growing number of family shareholders. Consequently, F1 is transitioning to ‘harnessing external stewardship’ with external dense governance (as a closed joint stock company) due to the management’s view that its current governance structure cannot sustain the family business as it endures increasing transgenerational complexities. The nonfamily Executive Advisor explains this: “We’re looking at new governance structures for the organization. We’re looking at a revised family constitution. We have a growing number of shareholders, a growing number of family members, and we have to adapt our practices as a family within the constitution, within the governance documents, within the articles, so even the legal structure has to somewhat change.” Therefore, F1 is adapting to a closed joint stock company structure by increasing the number of external professionals while reducing family members in management. This was, in part, a step toward IPO, where the firm needed to prepare for the regulations of public companies. The nonfamily Executive Advisor stated: “We’re on a path of IPO readiness. We believe that the rigorous implementation that IPO readiness brings will also help us.”

The modifications to the governance structure of F1 include increasing the prominence of external professionals in chairing its governing committees: “We have a nomination and remuneration committee, which is defined within the governance structure, like every large organization, but now we are talking that it has to be chaired by a non-family, non-staff member” (Executive Advisor, non-family). To further heighten objectivity in decision-making, F1 is also planning to give voting rights to independent board members: “The new governance structure, we’re now moving to voting for non-family members on the board, and ultimately, we have to have a board with no family members in it” (Executive Advisor, nonfamily).

Another family firm representing the harnessing external stewardship strategy is F6, managed by its second and third generations. F6 relies on an external dense governance structure as a closed joint stock company. F6 follows this stewardship strategy and governance structure to preserve the family’s control over the business. They safeguard the business from the family’s transgenerational complexity by proactively relying on regulations set for public companies. As the third-generation family director stated: “We are adopting the closed joint stock structure. It is very important. We still have the belief that it should go public at one point in time because that’s the only way that you can really manage a business group that will become extensively complicated with time and with new family members coming into it.” F6’s governance also regulates family appointments into the business by enshrining the founder’s values, meritocracy in the profession, and vacancy availability: “As an example, you cannot join the family business until you’re actively involved in external job and acquired experience and if there are vacancies” (Director, G3). Also, despite F1 and F6 following the harnessing external stewardship strategy, they prepared for stewardship transition to the perpetuating external stewardship strategy to mitigate the family transgenerational complexity.

Strategy 4. Perpetuating External Stewardship

This strategy involves listing the family business in the stock market to encounter a ceaseless family transgenerational complexity. F4 is a compelling representation of this strategy. The second generation reformed F4, and the third and fourth generations currently manage it. The original family firm disintegrated at the second generation due to conflicts around family firm leadership. Having learned from a previous business failure and in a reinforcement of the family stewardship over the business, when reformed, F4 followed the “harnessing external stewardship” with the governance of closed joint stock companies: “When we first started our business, it was a sole proprietorship, then we transferred it into an industrial company then into a holding company. The most recent procedure is we moved into adopting the closed joint stock holding company structure, to protect the business continuity and to prevent the negative influence that might arise from some shareholders” (Acting Director, G4). F4 then transitioned to the perpetuating external stewardship strategy with the governance of public companies and listing subsidiaries in the stock market. Business goals of increasing profitability, business expansion, wealth maximization, and managing family dynamics to protect business continuity drove the transition. For instance, if the family shareholder(s) decide to exit the business, the stock market is where to sell their shares. In F4, this strategy manifests in following the governance structure of public companies at the group level (owner of the business subsidiaries) and the subsidiary level and listing the business in the stock market. The group’s Chairman explained: “We are floating some of our subsidiaries in the stock market. So, we have the governance structure of a public company to protect the business.”

Discussion

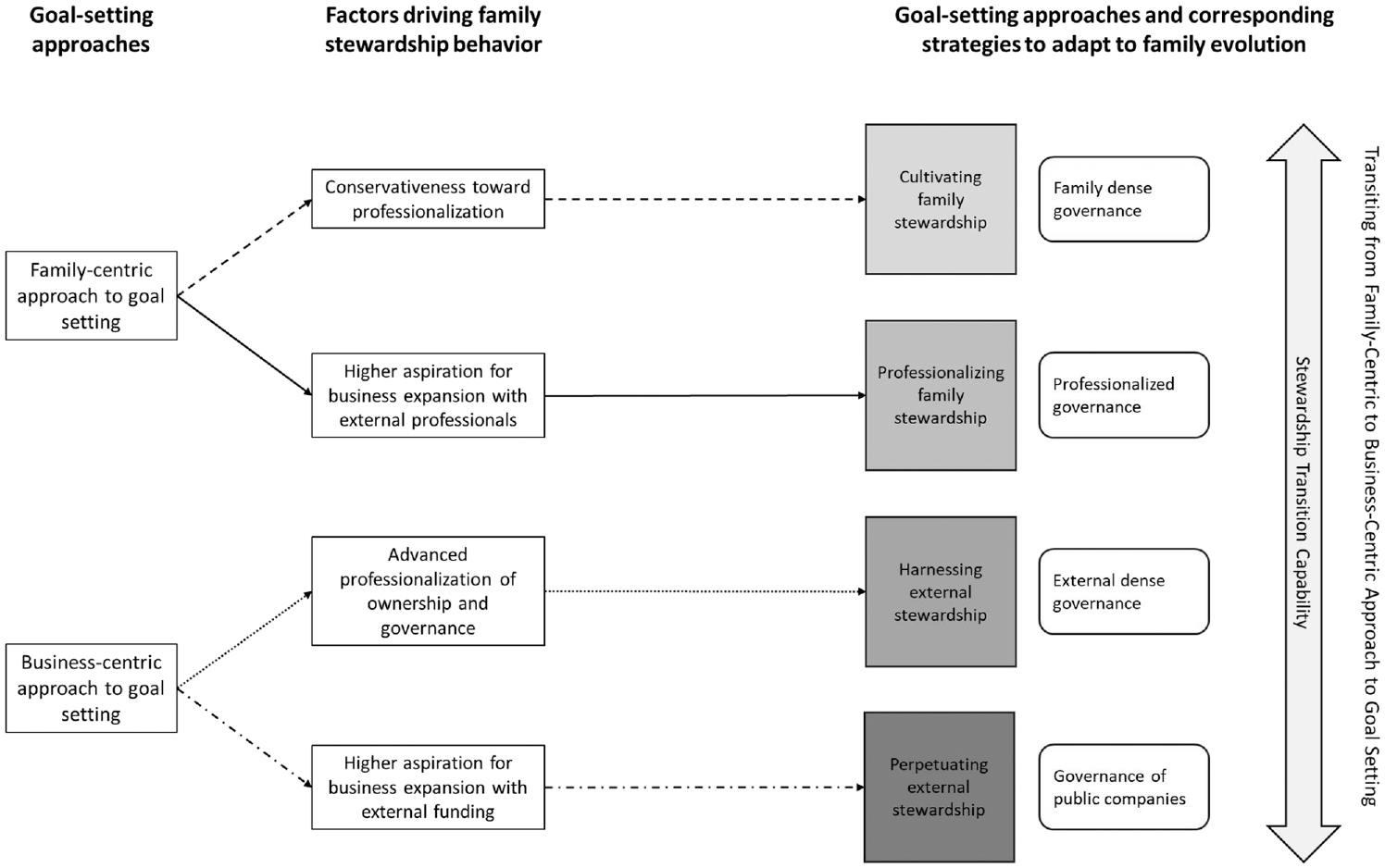

The study aimed to examine and theorize how multigenerational family firms manage the antithetical contrast of family and business goals and adapt their stewardship strategies when enduring transgenerational complexity. We now develop a theoretical framework from our findings, explaining how family businesses transition through goal-setting approaches and corresponding stewardship strategies when pressured by transgenerational complexities. Second, the framework provides four different stewardship strategies. Third, the framework outlines the novel concept of stewardship transition capability as a capability family firms must develop to adapt those stewardship strategies. Figure 3 illustrates our framework.

A goal setting and stewardship perspective to managing the antithetical contrast of family–business goals.

The dominant premise in the family business strategy literature is that family firms prioritize family goals, and these goals are tied (almost inextricably) to stewardship (Chrisman, 2019). However, such premises have been challenged as the link between stewardship and family goals has not been resolved and urgently needs research (Williams et al., 2018). The literature also postulates that family firms’ strategic decision-making behavior and outcomes reflect their goal setting (Kotlar et al., 2018). However, what stewardship is required to achieve goals is unknown (Williams et al., 2018), especially when transgenerational complexities reshape family and business priorities and goals. This study shows that navigating the goal-setting approach followed by multigenerational family firms requires different stewardship strategies in response to the family’s transgenerational complexity.

The findings outlined differences in how family and business goals are achieved through four different stewardship strategies conditioned by transgenerational complexity. The family firms that were family-centric and prioritized family goals followed strategies of cultivating family stewardship and professionalizing family stewardship. Other family firms followed a far more prominent business-centric approach, prioritizing business goals. These firms followed the strategies of harnessing external stewardship and perpetuating external stewardship. Extending the goal-setting theory, the findings show that the goal-setting approach (family-centric vs. business-centric) directs the stewardship strategy. The managing family acts as a steward in aligning the stewardship behavior with its goal setting. However, further extending goal-setting theory is that which goals are prioritized are conditioned by transgenerational complexity, and the pressures set in place by transgenerational complexities compel choices around specific stewardship strategies to ensure those collective interests continue to be pursued. For these reasons, we also find how stewardship strategies are associated with factors pertaining to how family involvement in the business creates a degree of conservativeness, prioritizing fuller degrees of family control (cf. Zellweger et al., 2013). Moreover, aspiring to greater professionalization and aspiring to externally financed business expansion further indicate which stewardship strategies are pursued. We summarize these as factors driving family stewardship behavior, which influence the choice of stewardship strategy (presented in Figure 3). In turn, our results elaborate stewardship theory by illustrating how stewardship is neither static nor monotonic. Next, we theorize the four stewardship strategies and develop a stewardship transition framework.

Propositions and Framework

The stewardship strategies of the family firms in the sample varied. This variation was first based on the priority attached to family-centric or business-centric goal-setting approaches. These approaches are then associated with distinct factors that drive or inhibit stewardship behavior and inform the selection of stewardship strategy. These driving (or inhibiting) factors include conservativeness toward professionalization, higher aspiration for business expansion with external professionals, advanced professionalization of ownership and governance, and higher aspiration for business expansion with external funding. These factors become especially acute as transgenerational complexity grows. Moments and episodes of transgenerational succession and transfer destabilize what goals are prioritized and the goal-setting approach in force, changing the composition of factors at play. This aspect is seen in the framework, indicating that family evolution can change the choice of stewardship strategy and is associated with shifts from family-centric to business-centric approaches to goal setting.

The cultivating family stewardship strategy is followed by family firms with higher conservativeness toward professionalization, relying on family management at senior operational and strategic levels. The efforts of the senior management in reinforcing family-centric goals are evident in the following conditions: trust, strong ties, and investment in informal training by family members. These firms follow a family-centric goal-setting approach, requiring family-dense governance and a cultivating family stewardship strategy. Therefore,

The transgenerational change of the family and the next generation’s involvement in business management within conservative family firms result in a stewardship transition toward the professionalized family stewardship strategy. Conservative firms that aspire to expand their business with input from external professionals follow professionalized family stewardship. The conditions for professionalized family stewardship include resolving or preventing conflict, implementing external professional training for the next generations, and proactive involvement of external consultants in management. The professionalized family stewardship strategy is followed by these conservative family firms when discretion over decision-making is conceded or granted to the next generation, which increases the flexibility and openness of the family business to professionalization. The decision to transition to the professionalized family stewardship strategy is also influenced by the recognition of the need to sustain market competitiveness and harness business growth and development through external expertise, all while maintaining the family interest. Accordingly, those family firms follow a family-centric goal-setting approach but require professional governance and a professionalized family stewardship strategy. We conclude:

Having professionalized family stewardship, the transgenerational complexity of the family caused by a continual increase in the number of family shareholders leads those family firms to tend to increase the presence of external professionals in business management. These efforts can include replacing family members with external professionals in senior management roles to increase objectivity, reduce the occurrence of decision-making conflicts between family members, and maintain business development and growth. Therefore, stewardship shifts toward protecting the business from the family for the family’s longer-term interest (i.e., protecting the business from the family’s transgenerational complexity for the greater welfare of the family). Accordingly, as these family firms shift to follow a business-centric approach to goal setting, the more advanced professionalization of ownership and governance requires the harnessing external stewardship strategy. We theorize:

The novel findings of this study further outline an example of perpetuating external stewardship strategy followed by a firm whose disintegration was fueled by unresolved and unfettered conflict across its generations. While conflict is not novel, how the firm learns from conflict and adapts its stewardship strategy is novel. Family firms following the perpetuating external stewardship strategy have higher aspirations for business expansion and are willing to pursue external funding. This is because the survival and longevity of the business are exposed to risk by unconstrained and unregulated transgenerational complexity. Offsetting against transgenerational complexities, seizing on external funding opportunities enables these business-centric family firms to preserve the business by relying on external actors while continuing to preserve the family interest inside the business by keeping a resemblance of family management and majority shareholding. Such a transition might occur linearly through the other stewardship strategies or nonlinearly because of the disintegration of prior strategies or a purposeful shift toward business-centric goals (e.g., from reform, as depicted in the case of F4). Following the perpetuating external stewardship strategy includes working toward listing the firm on the stock market. We theorize:

Relevant to goal-setting theory, we theorize how variation in approaches to goal-setting influences the choice of stewardship strategies. Stewardship strategies are chosen to manage the transgenerational complexity of the family and to account for shifts in the balance of family and business goals. The transitions between stewardship strategies foster the stewardship transition capability, which we define as the adaptive shift from one stewardship strategy and its corresponding governance structure to another in a strategic act to preserve the family business when enduring transgenerational complexities. Stewardship transition capability can incrementally develop with the family transitions between the different stewardship strategies. This occurs as transgenerational complexities gradually change the family management’s calculus about conservativeness, authority granted to the next generation, and aspiration for business expansion—commensurate with shifts in their goal-setting approach and distribution between family-centric and business-centric goals. In this situation, the family firm incrementally transitions from a family-centric approach to goal setting to a business-centric approach. Stewardship transition may also occur radically when family firms start following a business-centric approach to goal setting earlier or more aggressively due to heightened transgenerational complexities. This more punctuated transition may result from previous experience or learning but lead to a more rapid stewardship transition commensurate with changes in stewardship strategies and their corresponding governance structures. Accordingly, we theorize that

To successfully transition through types of stewardship strategies, we theorize that a stewardship transition capability is needed to ensure the fit, timeliness, and effective execution of changes in stewardship strategy as the family firm responds to its transgenerational circumstances. Stewardship transition capability develops concurrently with adapting to the family’s transgenerational complexity. From our qualitative data, we theorize that stewardship transition capability is reflected in the governing rules and regulations of the family firm, and its success is contingent on maintaining strong family relations and efficient family management. This theorization is set in the context that having an appropriate governance structure sets the formal conditions to sustain the business when enduring transgenerational complexities. Still, it is insufficient to sustain the familial element. This is consistent with the idea that governance and succession planning formalities are not enough to preserve the family business. We see this in our data where two of the cases in the sample avoided the danger of business failure or disintegration because of family complexities and reached the fourth and fifth generations by restoring and perpetuating trust and strong relations among family members. Two other cases that lacked these conditions disintegrated. That is, it can be said they lacked the stewardship transition capability—the processes and routines around transition needed to ensure timely and effective execution of changes in stewardship strategy essential to traversing familial circumstances around transgenerational complexity.

Family firms endure as a family business with the managing family’s efficiency and commitment and the integration of external expertise to support the family in achieving their (preferred) distribution of family and business goals. Therefore, we posit the following circumstances for a successful stewardship transition capability vital to transitioning between stewardship strategies and their corresponding governance structures as the balance of family-centric and business-centric goals shift and when pressured by transgenerational complexity:

Theoretical Contribution

We provide three novel and important contributions to goal setting and stewardship theories in family business research. First, we contribute a theoretical framework and narrative to explain why stewardship is neither static nor monotonic as the emphasis between family and business goals shifts over time and in response to transgenerational complexities. We identify and conceptualize four stewardship strategies that family businesses transition among to co-align interest and preserve stewardship. As a behavioral theory, stewardship theory starts with the assumption that employees’ interests naturally align with those of the firm’s owners (Madison et al., 2016). However, stewardship theory does not account for when families (and their businesses) transition from family-centric to business-centric approaches to goal setting. Also, stewardship theory has not considered that stewards’ understanding of business and familial interests risks becoming misaligned when circumstances erode their ability to interpret new goals emerging when the family and business are engrossed in transgenerational complexity. In turn, we identify four stewardship strategies that family businesses transition through as goal-setting approaches shift. We also reveal the corresponding governance structures needed to maintain stewardship behavior successfully. These four strategies and their corresponding governance structures are cultivating family stewardship with family-dense governance, professionalizing family stewardship with professionalized governance, harnessing external stewardship with externally dense governance, and perpetuating external stewardship with public companies’ governance. Consequently, we provide scholars with a new theoretical framework and narrative to theorize and explain how family firms can transition between stewardship strategies to manage their transgenerational complexity.

Second, we contribute to the intersection of goal setting and stewardship theories by identifying the factors that motivate change in goal-setting approaches and initiate the transition. Under stewardship theory, stewards, as employees, are expected to act in the organizational interest. Changes in goal-setting approaches create a risk that stewards’ understanding of these interests erodes as the firm transitions to different goal-setting approaches. This risk has escaped consideration because of a general tendency to think of stewardship as a state. Rethinking stewardship as a property, our theoretical framework and narrative provide for this erosion by planning the solution inside the co-occurrence of stewardship strategies with specific governance structures to restore co-interest alignment.

Third, currently, there is no theoretical framework residing within either goal-setting theory or stewardship theory to explain this transition process, that records or depicts what may happen to stewardship strategies or the forms they may take, or describe the circumstances and conditions needed to contain and manage the antithetical contrast of family and business goals. Our first two contributions remedy this deficit. However, we further show that a new capability is needed to manage these transitions effectively. In deriving the concept of stewardship transition capability, we contribute to stewardship theory a capability and mechanism needed to successfully transition across different stewardship strategies, manage the antithetical contrast of family and business goals during the transition, and change stewardship strategy timely and effectively. We present stewardship transition capability as essential to preserving family firms as transgenerational complexities affect the family and business.

Managerial Implications

Decision-makers can learn from the positive elements attributed to the stewardship strategies applied by family firms in prioritizing and managing family and business goals. Our findings advocate for a long-term view of the complexities that a family firm might contend with. This view allows family owners and managers to proactively prepare for stewardship transition as family and business goals evolve amidst transgenerational complexities. Our framework enables family business owners, managers, and advisors to tackle pitfalls through early strategic planning and enactment of the required rules and procedures in their governance structure and succession planning to align with the prioritized goals. This can help families re-evaluate their current strategies and adapt to the most appropriate strategy, as highlighted within our framework. Finally, we recommend that family business owners and managers invest early in developing a stewardship transition capability to preserve the family firm.

Limitations and Future Research

First, the Gulf Region site might limit some of the generalizability of our theoretical development, but we remain confident that the broader aspects of our theoretical framework are transferable. Second, our findings spotlight the nonstatic and nonmonotonic nature of stewardship and goal setting, particularly under transgenerational complexity. However, we recognize that additional complexities exist in family firms. A systems theory perspective may be well suited to examine conditions in which several complexities exist concurrently. These concurrent complexities may affect transitions to stewardship strategies identified in our study. We encourage renewed efforts to understand the nonstatic nature of family stewardship. Third, we see that priorities attached to family and business goals vary across generations. Our evidence suggests that the current understanding of family goals and priorities is too static. Relatedly, family firms have ample scope for intrafamily divergent goals beyond family (nonfinancial) and business (financial) goals. We encourage more research into how families attach priorities to divergent goals and how divergences may change approaches to stewardship.

Our findings drew attention to how family firms might use an Initial Public Offering (IPO) to sustain and grow the business as a product of a business-centric goal-setting approach. However, an IPO of the family firm reduces family control and authority over the business. In our study, an IPO as a prioritizing of business goals does not mean a depletion of family goals but rather a reordering of goal-setting priorities (e.g., business preservation through IPO becomes first in priority compared to pursuing socioemotional wealth (SEW), even if meeting the business goal inadvertently or deliberately meets the family goal). We also recognize that the essence of a family firm is family influence and control. Mitigating purely family-related transgenerational conflicts could be attained through regulations enacted using a family charter, internal buyout of exiting family shareholders, or other governance mechanisms more suited to such an outcome. Pursuing an IPO converts the family firm into a public company where the family may gradually become a minority shareholder, especially with succeeding generations who may be less incentivized toward their inherited shareholding and sell it on the stock market. While an IPO can solve some transgenerational complexity, it also risks eliminating the transgenerational outlook and family ownership of the business. More research is needed on family firms’ use of IPOs.

Footnotes

Acknowledgements

We thank the Scientific Committee of the 18th annual EIASM Workshop on Family Firms Management Research held in Naples, Italy, October 2 to 3, 2023, for awarding an earlier version of this paper the Best Paper on Conference Theme Award. We thank the participants at the presentation of our paper for their valuable feedback. Moreover, we thank the family businesses and individuals who participated in this study for their voluntary support and time and for sharing with us their rich insights and experiences.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.