Abstract

Unlike traditional investing, where decisions follow a clear financial calculus, it is unclear how and why funders support hybrid ventures. To address this question, we analyze the varied priority that investors place on social impact versus financial returns and draw on categories theory to argue that different priority orderings associate with different perceptions of how hybridity aligns with different investment goals. Results show that funders who prioritize financial goals react positively when they perceive a venture exhibits greater hybridity, whereas funders who prioritize social impact do not. Our findings contribute to research on impact investing, hybrid organizations, and categories theory.

Keywords

Introduction

Social entrepreneurship has attracted attention in recent years as a tool to address societal issues like poverty, inequality, and environmental degradation. Scholars have yet to settle on a single definition, but most agree that social enterprise is a unique form of organizing, distinct from business and charity, where both commercial activity and social aims are central to an organization’s identity and operations (Austin et al., 2006; Battilana & Lee, 2014; Defourny et al., 2021). This can be seen in entities like green-energy producers (Pacheco et al., 2014), work integration social enterprises (Tracey et al., 2011), and microfinance banks (Wry & Zhao, 2018). In each case, revenue generation is intertwined with the pursuit of societal benefits, creating the potential that social issues can be addressed without grants or donor support (Dacin et al., 2011).

Still, excitement about social enterprise is tempered by the reality that these ventures—like most hybrid organizations—face unique challenges (Renko, 2012; Battilana & Lee, 2014). Organizational insiders often disagree about the primacy of social versus financial aims, creating tensions and tradeoffs that can lead to reduced efficiency (Wry & Zhao, 2018), mission drift (Grimes et al., 2019; Varendh-Mansson et al., 2020), and organizational failure (Tracey et al., 2011). Resource acquisition is also a challenge because social enterprises do not fit neatly into the categories that most funders use to compare and evaluate organizations. Providers of funding sources like banks and charitable foundations tend to prioritize either financial returns or social impact, and this leads them to support traditional businesses or nonprofits (Battilana & Lee, 2014). Entities that mix the two may be perceived as confusing or of low quality (Zuckerman, 1999). Indeed, there is evidence that even funders who claim to value social impact and financial returns are unlikely to support an enterprise unless it conveys a single, overriding focus on one type of value creation or the other (Lee et al., 2020; Moss et al., 2018).

As with prior studies, we expect that social enterprises are overall less likely to receive funding when they are perceived to have a high level of hybridity. However, we suspect that this masks a deeper pattern where some funders value hybridity and others do not. Our argument builds on two existing streams of categories research that each speak to a piece of the puzzle. The first stream—goal-based categorization—respects that evaluators may have goals that lead them to support different types of organizations (Paolella & Durand, 2016). This is germane to our context, as there is evidence that funders tend to prioritize either financial returns or social impact when evaluating social enterprises (Cobb et al., 2016; Moss et al., 2018). The second stream—causal-model categorization—argues that evaluators may perceive hybridity as sensible and valuable, as long as integrating features from another category helps an entity to perform better in its primary category (Wry et al., 2014). We unite these streams to suggest that funders who are primarily motivated by social versus financial goals may make different inferences about the consequences of hybridity, thus creating variance in the likelihood of them choosing to support a given social enterprise.

We argue that high levels of perceived hybridity will make a social enterprise less attractive to funders who are primarily interested in social impact goals. The causal-model approach to category cognition suggests these actors will evaluate an enterprise by making inferences about how commercial features affect the pursuit of social impact (Cudennec & Durand, 2023). Studies routinely find that social–financial hybridity fosters the perception that an organization is less committed to social impact creation (Hwang & Powell, 2009) and is more likely to engage in mission drift (Battilana & Lee, 2014; Grimes et al., 2019).

Conversely, we suggest that hybridity may appeal to funders who are primarily motivated by financial goals. To this end, we argue that it is important to recognize that many investment decisions are not isolated events but rather are aspects of a broader portfolio construction effort. Individual investments have different risk–return profiles, and not every investment needs to promise a big return to be useful. Social–financial hybridity may support inferences about lower financial upside, but it can also signal less risk (Hoepner & Yu, 2010) and returns that are uncorrelated with other types of assets (Krauss & Walter, 2009), making an investment attractive as a way to diversify and balance a portfolio (Cerqueti et al., 2021).

Our empirical approach follows prior studies that use crowdfunding data to offer insight into an individual’s funding decisions that are difficult to observe through other means (Greenberg & Mollick, 2017; Younkin & Kuppuswamy, 2018). It is also inherently useful to study such platforms since crowdfunding is a fast-growing source of social enterprise funding (Calic & Mosakowski, 2016; Moss et al., 2018). Analysis is based on survey responses from 233 funders who are active on two crowdfunding platforms that include social enterprises and which promise a financial return on investments. 1 We presented respondents with a case vignette describing a social enterprise and asked them questions about perceived social–financial hybridity and whether they would be willing to offer funding support. Other questions focused on individual goals, and the extent to which respondents seek to generate financial returns and/or social impact from their investments. We used probit regression to model the relationship between perceived hybridity and the likelihood that an individual intends to support the venture. We conducted 31 interviews to gain additional insight into respondents’ decision-making and to add nuance and context to our findings.

Contrary to expectation, we found a positive relationship between hybridity and the intent to financially support a social enterprise. Consistent with our theory, though, the effect is driven entirely by funders who are primarily seeking a financial return from their investment. In comparison, the strength of a funder’s social impact goal negatively moderates the effect of hybridity on the decision to fund a venture.

Our study makes three main contributions. First, we add to categories literature by integrating insights from goal-based and causal-model approaches (Durand & Paolella, 2013; Wry & Durand, 2020). The two perspectives offer complementary insights but have not yet been considered together. Our findings suggest that actors with different primary goals interpret and evaluate hybridity differently because their causal models are reversed: funders who are motivated by financial goals consider how social impact affects a venture’s risk–return profile, whereas those with strong social impact goals consider how commercial pursuits affect an enterprise’s ability to create meaningful impact. Second, our approach recognizes that individual funders may pursue a goal by making multiple decisions. This departs from extant categories research where decisions are treated as discrete events. Third, we contribute to research on social enterprise. Prior studies find that these entities have trouble acquiring resources unless they communicate a clear focus on profits or impact (Lee et al., 2020; Moss et al., 2018). Our results suggest that these findings may mask important nuance, and that certain types of funders are systematically more likely to value and support hybridity than others.

Hybrid Ventures and Resource Access

Category Spanning and the Devaluation of Hybrids

Social ventures exemplify hybrid organizing through the deep integration of social and financial aims. Both are core to these organizations’ identities and activities, and neither can be removed without changing the fundamental nature of the enterprise (Battilana & Lee, 2014; Smith & Besharov, 2019). Social ventures are thus distinct from both traditional profit-seeking firms, and charities and nonprofits that focus primarily on social impact creation. This hybrid orientation has the potential to advance new and sustainable solutions to longstanding social issues (Wry & York, 2017; Wry et al., 2023). However, it is also associated with resource acquisition problems since funders like banks, equity investors, and charitable foundations tend to prioritize either profits or impact, and support organizations that pursue one goal or the other (Battilana & Lee, 2014; Wry & Durand, 2020).

Thus, according to the classic, prototype-based view of categories (Zuckerman, 1999), social ventures face a categorization problem. As Lamont (2012) noted, categorization precedes evaluation because people cannot reasonably consider every potential choice alternative when making resource allocation decisions. Categories reduce this complexity by creating cognitively manageable consideration sets comprising items that share similar features (Rosch, 1978; Rosch & Mervis, 1975). Most organizational research focuses on categories that exist outside of individual actors and reflect shared understandings about the similarity and distinctiveness of different types of items (Durand & Paolella, 2013; Vergne & Wry, 2014). This work stresses that categories collate entities in meaningful ways, and provide the evaluative codes (Hsu & Hannan, 2005)—or theories of value (Paolella & Durand, 2016)—that are relevant for judging category members. For example, audiences expect comedy, horror, and romance films to have different features, and this is reflected in the criteria used to evaluate these movies (Hsu, 2006). Evaluation is thus thought to follow a two-step process where actors determine which category an item fits within, and then apply that category’s code to evaluate the item (Zuckerman, 1999).

A key theoretical implication of this research is that an entity is more likely to be evaluated favorably if it clearly fits an existing category (Vergne & Wry, 2014). An item does not need to have every feature associated with a category to be a member, but those with category-focused attributes are easier to understand and evaluate since they are closer to the category ideal (prototype) and can be judged using well-established criteria (Durand & Paolella, 2013). The corollary, however, is that audiences often find it difficult to understand items that integrate features from multiple categories and tend to judge these items unfavorably. The logic for this argument is that audiences have difficulty understanding how features from different categories fit together (Zuckerman, 1999). In turn, this supports causal mechanisms that lead to lower evaluations because category spanning: (a) reduces an item’s fit with a particular category, potentially making it difficult to understand; and (b) can signal a lack of focus that suggests an item is of lower quality than category-focused alternatives (Negro & Leung, 2013; Zuckerman, 1999). Mixing features from high-contrast, or oppositional, categories may further convey that an entity is unlikely to perform well on metrics related to either category, since their features or productive activities may be considered incompatible (Negro et al., 2010; Wry & Lounsbury, 2013).

The above dynamics clearly apply to organizations that mix “business” and “charity,” as these categories align with goals that many perceive as incompatible (Battilana & Lee, 2014; Besharov & Smith, 2014). Indeed, there is a widely held perception that social enterprises internalize tradeoffs that create lower profit potential than traditional businesses and lower impact potential than nonprofits or charities (Wry & Zhao, 2018). Illustrating this, Cobb et al. (2016) found that microfinance banks were less likely to receive funding when they vigorously pursued social and financial goals because this led to perceived misalignment with the financial priorities of commercial funders and the social priorities of public funders. Other studies suggest that these types of category effects can be so strong that even audiences who claim to value both social and financial goals are unlikely to support a social venture unless it conveys a clear focus on either impact or profits (Lee et al., 2020; Moss et al., 2018). Evaluators may appreciate different types of value creation, but it is difficult to generate a composite framework for comparing entities that combine multiple utilities in different ways (Tetlock, 2003; Tversky, 1972). As a result, actors tend to default to existing categories and codes that may disadvantage hybridity. As such, our baseline hypothesis is:

Goals, Causal Models, and Variance in the Valuation of Hybrids

While the classic, prototype-based view of categories supports a blanket prediction that hybridity makes a social venture less likely to receive funding, other perspectives point to potentially important variance. Research on goal-based categorization and causal-model categorization suggest that actors do not always rely on established categories and codes to judge items, and this may lead to differences in how they assess the same entity (Durand & Paolella, 2013; Wry & Durand, 2020). We build on and integrate these research streams to argue that modeling overall outcomes may mask a deeper pattern where hybridity makes a venture more attractive to some funders but less attractive to others.

Goal-Based Categorization

The key insight of goal-based categorization is that most resource allocation decisions are motivated by a desire to fulfill a personally valued utility. Established categories can be helpful in this regard, for instance if one wants to find a good restaurant (Kovács & Hannan, 2010) or a film that aligns with their tastes (Hsu, 2006). In other situations, though, items that come from different categories—or that merge features from multiple categories—can all plausibly serve the same goal. Audiences may thus draw on past experiences, contextual factors, and existing category knowledge to assemble ad hoc consideration sets that do not align with any one category or code (Barsalou, 1999). For instance, if one’s goal is to enjoy a night out, potential options might include a concert or a play, different types of movies, certain restaurants, or the local pub. Notably, evaluation in these situations is guided by one’s assessment of how well different options meet the goal at hand. Categorization and evaluation are thus theorized as actor-centric rather than category-centric processes and may reflect factors that vary among people (Barsalou, 1985; Ratneshwar et al., 2001).

Our argument builds on the insights that actors with different goals may form different judgments on the same item (Glaser et al., 2020; Paolella & Durand, 2016). From this perspective, an item’s worth does not reflect its position within or across categories but rather the degree to which its features align with audience-member goals. For example, Pontikes found that customers are unlikely to support ventures that claim membership to lenient categories (i.e., categories with “ambiguous social meaning”) (Pontikes, 2012, p. 2), as this develops confusion about a firm’s focus and quality, consistent with the prototype-based view of categorization (Zuckerman, 1999). Yet investors view these ventures favorably, as ambiguity is interpreted as a signal that a firm is trying to create a new market and thus generate outsized financial returns. This insight also aligns with the observation that funders often pursue goals that lead them to support different types of firms. This can be seen in the investments made by corporate venture capitalists, who prioritize a strategic fit in their decision-making, versus traditional venture capitalists, who are more concerned with investment returns (Pahnke et al., 2015). The distinction is even more stark when comparing the goals—and thus investment decisions—of commercial investors, charitable foundations, and public sector funders (Cobb et al., 2016).

Applying this approach to our context, we begin by identifying the aims that actors plausibly pursue when they fund a social enterprise (Durand & Paolella, 2013; Paolella & Durand, 2016). To this end, we build on prior research that suggests funders prioritize either commercial or social impact goals when deciding which enterprises to support, even if they see value in both types of aims. This variance is well-documented in ecosystems populated by financial investors and charitable funders, who value commercial versus social impact outcomes, respectively (Battilana & Lee, 2014; Cobb et al., 2016), and it is also evident in contexts like socially responsible investing, where funders consider social impact but prioritize investment returns (Arjaliès & Durand, 2019; Barber et al., 2021). Even in crowdfunding, where funders have broad leeway to pursue personally meaningful goals, studies suggest that either social impact or financial returns still tends to dominate (Lee et al., 2020; Moss et al., 2018). Reflecting this—and as described in detail in “Data and Methods”—our survey shows that crowdfunders variously prioritize commercial versus social impact goals in their funding decisions.

Causal-Model Categorization

We further expect that different goals support different views about how hybridity affects a social enterprise’s appeal. Our argument here merges insights about goal-based and causal-model categorization. In contrast to both the prototype-based view, which argues that items are classified based on certain predefined features (Rosch & Mervis, 1975), and the goal-based view, which argues classification follows actors’ personally valued aims (Barsalou, 1999), the causal-model approach argues that people classify items based on the relationships between different features (Rehder, 2003). From this perspective, a robin is a good example of a bird since its wings cause it to fly, whereas flightless birds like penguins and chickens are not good examples of the category.

Beyond providing a basis for classification, scholars have adapted the causal-model approach to argue that an entity’s perceived value may be enhanced or diminished when it integrates features from different categories. The key insight here is that actors do not necessarily view category spanning entities as confusing or automatically default to lower evaluations, as implied in the classic, prototype-based view (Zuckerman, 1999). Rather, they make directional inferences about how features from one category might cause an entity to perform better or worse on metrics associated with another category. As a result, certain types of hybridity can be seen as symbiotic rather than competing or dilutive. For instance, Wry et al. (2014) found that venture capitalists base their nanotechnology investment decisions on the extent to which a venture’s scientific research is perceived as an input that helps product commercialization efforts. A firm becomes more likely to receive funding when it signals it is using science to pursue profits and less likely to receive funding when it conveys the opposite. Similarly, Naumovska and Zajac (2022) showed that audiences are more likely to implicate a firm in an industry-level scandal (i.e., categorize the firm with verifiably bad actors) if it incorporates features that are perceived to have caused the focal misconduct in other organizations.

To date, this research has sought to understand the varied ways that organizations mix features from different categories, and how this affects overall audience evaluations; the central idea being that some types of hybridity are perceived as inherently more sensible or valuable than others (Wry et al., 2014). Yet as Durand and Paolella (2013, p. 1,107) noted, evaluations may also vary based “on causal knowledge and world theories that are particular to each audience.” Wry and Durand (2020) similarly argued that actors may have varied “theories of integration” that lead them to evaluate hybrids in different ways based on their own interpretation of how certain categories fit together. These insights have not yet been empirically investigated, though, and we extend this line of thinking by arguing that actors who pursue different goals may adopt causal models that create predictable variance in how they view and value hybridity.

Given the observed difficulty of making social and financial metrics commensurate in ways that allow for overall, additive assessments (Lee et al., 2020; Moss et al., 2018; Tetlock, 2003), we expect that evaluations will anchor on a funder’s main goal (i.e., financial returns or social impact creation) and reflect their causal-model for how that goal is affected by a venture’s perceived hybridity. Funders with a salient commercial goal will likely focus on how social impact pursuits affect a venture’s ability to generate financial returns. The direction of this relationship should reverse for funders with a salient social impact goal and focus on how financial pursuits affect a venture’s ability to produce socially impactful outcomes.

Following Cobb et al. (2016), we draw on studies that offer insight into how different funders are likely to perceive the causal relationship between a venture’s social and financial goals, and supplement this with data from 31 funder interviews to predict their reactions to a venture’s perceived hybridity. We identified interviewees from our survey data: we reached out to 14 respondents who indicated a salient interest in pursuing social impact goals, and 14 who indicated a salient interest in pursuing financial returns. The other three interviewees had a balanced orientation that values both social and financial goals. Appendix 1 provides details on each interviewee’s age, gender, and goal salience.

Different Goals, Different Causal Models

Funders Who Prioritize Social Impact Goals

Our first hypothesis predicts that a social enterprise is less likely to receive funding when it is perceived to have a high level of hybridity. We expect this outcome will become stronger depending on the extent to which a funder values social impact goals. Recall that the mechanisms which explain negative evaluations are that audiences: (a) do not understand how different categories fit together; or (b) interpret hybridity as a signal that an organization will perform poorly on category-specific metrics. We suggest that both mechanisms apply when funders prioritize social impact creation.

Social ventures may be promising vehicles to create both social and financial value (Santos et al., 2015; Wry & York, 2017), but academic research highlights that organizations risk losing sight of their social mission when they become more business-like, an outcome known as mission drift (Grimes et al., 2019). This is reflected in the longstanding concern that earned income strategies in nonprofit organizations dilute managerial focus and increase the likelihood that revenue generation will trump social impact (Hwang & Powell, 2009; Weisbrod, 2004). Studies suggest this hazard is accentuated for social enterprises since these ventures integrate social and financial aims directly and deeply in their core activities. A social venture can survive if it reduces its focus on social impact creation, but it is dependent on commercially generated revenue to sustain operations. As such, there is an inherent risk of prioritizing commercial activities over those that align with social mission pursuits (Battilana et al., 2017; Ebrahim et al., 2014). Moreover, it is often costly to serve high-need beneficiaries, creating a direct tradeoff between revenue generation and the vigorous pursuit of social impact. Although there are certainly exceptions where commercial aims are compatible with, and may reinforce, social mission pursuits (Besharov & Smith, 2014), tradeoffs are documented in contexts such as microfinance banks (Mersland et al., 2019; Wry & Zhao, 2018), work integration social enterprises (Pache & Santos, 2013), base of the pyramid ventures (Smith & Besharov, 2019), and many others (Santos et al., 2015; Tracey et al., 2011). Indeed, Vedula et al. (2022) noted that a focus on social–financial tradeoffs is a core tenet of social enterprise scholarship. In short, from an academic perspective, pursuing commercial goals is thought to have a negative causal effect on social impact creation.

To the extent that academic research mirrors real-world perceptions, it stands to reason that high levels of perceived hybridity will make a social venture less attractive to funders who value social impact goals highly. Our interviews support this intuition and suggest that crowdfunders who prioritize impact believe that commercial activities detract from this goal. Indeed, there was a common perception that hybridity may yield fiscal benefits, but at the expense of social mission pursuits. For instance, one interviewee (#18) stressed that “there is a tradeoff between the impact and basically the penalty for an investor in exchange for an impact,” whereas another (#22) noted that “[hybridity] is just a way to stand apart, there you have it, it’s an advertising differentiation as compared to others.” Interviewees also stressed that hybridity risks mission drift, especially as a venture grows: “[When growing], the basic project escapes from the hands of those who started it. The original ideal is no longer the same” (interviewee #3). “[The risk] is to grow at all costs, then they [the managers of the social enterprise] go back to the current trade which is often negative, because then they put money above ethical and moral values and that is not the goal for me” (interviewee #3). Offering evidence for the mechanism that suggests audiences find it difficult to understand how features from different categories relate to each other, there was also a general perception that hybridity can make it difficult to judge a venture’s impact potential. Speaking to this, one interviewee (#13) complained that “look, I can help you, either financially or because I have technical expertise, but I don’t know where to look.” Another (#30) noted that “I can’t do [the analysis], I don’t feel like doing it, I lack the competences.”

In short, interview data suggest that respondents believe commercial pursuits lead to weaker social impact performance—and thus make a venture less likely to satisfy social impact goals—while also complicating the task of assessing a social venture. We thus expect that the proposed negative relationship between perceived hybridity and venture funding becomes stronger when funders place more emphasis on social impact goals. Stated formally, we predict:

Funders Who Prioritize Commercial Goals

While prior studies and our interview data suggest that hybridity makes a venture less appealing if a funder’s primary goal is impact creation, we expect the opposite for funders who invest to create personal financial returns. In general, there is not much concern that a venture will drift away from its financial goals to deepen its social mission pursuits (Grimes et al., 2019), though it is certainly possible (Tracey et al., 2011). There is, however, some evidence that social impact can be symbiotic with financial pursuits and benefit a venture by helping it to differentiate itself from its competitors (Du et al., 2010), capitalize on emerging markets (Weber et al., 2008), and build a stronger reputation (Godfrey, 2005). As such, the pursuit of social goals may not be perceived as depleting from a financial perspective, contrary to the blanket, prototype-based view prediction that hybridity reduces an item’s appeal (Zuckerman, 1999). Indeed, our commercially oriented interviewees commonly expressed positive views. Put plainly, one such crowdfunder (#16) said that “I believe that [social impact and business dynamics] can very well go together.” Another (#24) noted that “I am all the same pretty convinced that the human and social aspect is already very important [from a business perspective] today and will become more and more so.” Yet another (#21) highlighted the differentiating potential of hybridity, noting that “I’m not aware of any company delivering [this product] to the market right now. That’s the difference, maybe, compared to others I know and others that are on the market.”

Beyond the potential for social impact aims to contribute to financial returns, though, it is important to realize that many potential investments are not solely assessed on financial upside. Rather, decisions reflect a risk–return calculus, and options with the most potential upside also tend to have high risks. Savvy investors try to build a balanced portfolio comprising multiple investments that are designed to collectively capture returns while minimizing downside risk. Some social impact investors also take a portfolio approach when deciding which initiatives to support, but this is done to balance philanthropic risk (i.e., supporting initiatives with varied impact potential) and is unrelated to an entity’s hybridity or revenue generation potential (Neave, 2023; Schreiber & Jackson-Ward, 2022).

Notably, there is evidence that businesses that pursue social impact vigorously may be considered less risky than others, and thus present attractive portfolio diversification options (Cerqueti et al., 2021). For instance, studies show that investing in firms with strong environmental, social, and governance metrics can yield strong financial returns by reducing the tail risk in an investment portfolio (Cerqueti et al., 2021; Hoepner and Yu, 2010; Verheyden et al., 2016). Social enterprises may be especially attractive in this regard to the extent that their financial performance is decoupled from risk factors that affect other types of ventures and markets. This is clearly illustrated in the microfinance sector, which attracts a great deal of commercial investment (Cobb et al., 2016) largely because risk–adjusted returns are weakly correlated with other asset classes (Krauss & Walter, 2009). Many of our interviewees echoed this view, confirming that social–financial hybridity can make a venture attractive as a portfolio diversification option. For example, one commercially motivated funder (#24) noted that they viewed hybridity favorably since “by financing this type of project, I am also chasing this idea of diversifying my investments.” Echoing this, another crowdfunder (#27) reported “the aim of developing my savings a little, diversifying them, making them more dynamic and, let’s say, giving them a little more meaning.”

Overall, academic literature and our interview data suggest that, while hybridity may require financial tradeoffs in some situations, there are reasons to expect that the vigorous pursuit of social impact can help to improve a venture’s financial performance. There is also evidence that hybridity can make a venture more attractive to commercially orientated funders even if it is not associated with stronger performance because the integration of social goals is associated with lower—and potentially uncorrelated—financial risks. We thus expect that funders with a stronger commercial focus are more likely to fund a social enterprise if they perceive that it has a high level of hybridity. Stated formally, we predict:

Data and Methods

Our data come from two crowdfunding platforms that include social ventures among other investment options. As a funding approach, crowdfunding was initially designed to facilitate donations—especially toward artistic, cultural, and social initiatives—in exchange for non-financial, symbolic rewards (Nielsen & Binder, 2021). However, the sector has since evolved to include lending and equity-based platforms that offer opportunities for ventures to raise early-stage capital (Calic & Mosakowski, 2016). These platforms, which initially focused on commercial ventures (Cholakova & Clarysse, 2015), now mostly also include social ventures. In parallel, some investment-based platforms specializing in impact investing have started to emerge (Hörisch & Tenner, 2020); their specific objective is to help social ventures raise funds.

Participants and Procedure

We gathered our data in collaboration with a royalty-based crowdfunding platform in France (WEDOGOOD) and a debt-based platform in Belgium (Crowd’in). Combining royalty-based and debt-based platforms allowed us to cover a more diverse universe of crowdfunding platforms that offer a financial return and include social ventures. Registered members on each site received an email from the platform manager inviting them to take part in a survey about crowdfunding. The survey was structured in two parts: the first contained questions about participants’ profiles, including their personal goals; the second contained the campaign of a fictional social venture called “EaTy” along with questions about how the respondent perceived the venture. Once they had started with the section on EaTy, participants could not go back to the first part of the survey.

The case vignette for EaTy was inspired by an actual Kickstarter campaign for a social venture in New York City that operated a food delivery service where refugees were employed as chefs and encouraged to cook their own traditional dishes (see https://shorturl.at/dmGHJ). Donations to the campaign were recognized by sending each funder a cookbook made by the refugee chefs. For our study, the campaign was modified so that the venture aimed to raise royalty funding on the WEDOGOOD platform, with royalties amounting to 3.25% of total sales. On the Crowd’in platform, the venture aimed to obtain loans with a return rate of 7%. According to the platforms’ managers, these are the average financial returns on their platforms. We also removed references to the specific reward product (the cookbook).

Prior research suggests that geographical proximity between the entrepreneur and capital providers can affect the success of crowdfunding campaigns (Agrawal et al., 2015). In response to this regional bias, the venture was presented as a Paris-based startup on the French platform (WEDOGOOD) and as a Brussels-based startup on the Belgian platform (Crowd’in). Further adjustments included the introduction of commercial discourse to signal the profit orientation of the venture in addition to its social goals. This included frequently used attributes on the target platforms, such as information about the market niche, financial performance, and the commercial background of founders. We conducted a pilot qualitative study with four participants to verify that social welfare and commercial categories were perceived as salient in the venture description (see Appendix 2).

Variables

Dependent Variable

Our dependent variable was a participant’s expressed willingness to support EaTy after reading about the venture. We measured this using a dummy variable (Dummy funding the venture) set to “1” if a participant indicated that they would like to fund the venture, and “0” otherwise (Wry & Lounsbury, 2013; Cholakova & Clarysse, 2015).

Independent Variables

Our first independent variable was the Degree of Hybridity that a respondent associated with the EaTy venture. The score is a composite measure based on the venture’s perceived Grade of Membership (GoM) in both the social welfare and commercial categories. GoM is a widely used metric and tells us about the extent to which an actor believes an entity possesses a category’s defining properties (Hannan, 2010). We asked crowdfunders to note, on a Likert scale from 1 to 5 (where 1 = “does not fit my conception at all” and 5 = “fits my conception very well”), the extent to which the social venture EaTy fits their representation of a welfare organization (“To what extent does the venture fit your own conception of a socially driven organization?”) and a commercial venture (“To what extent does the venture fit your own conception of a commercially driven organization?”).

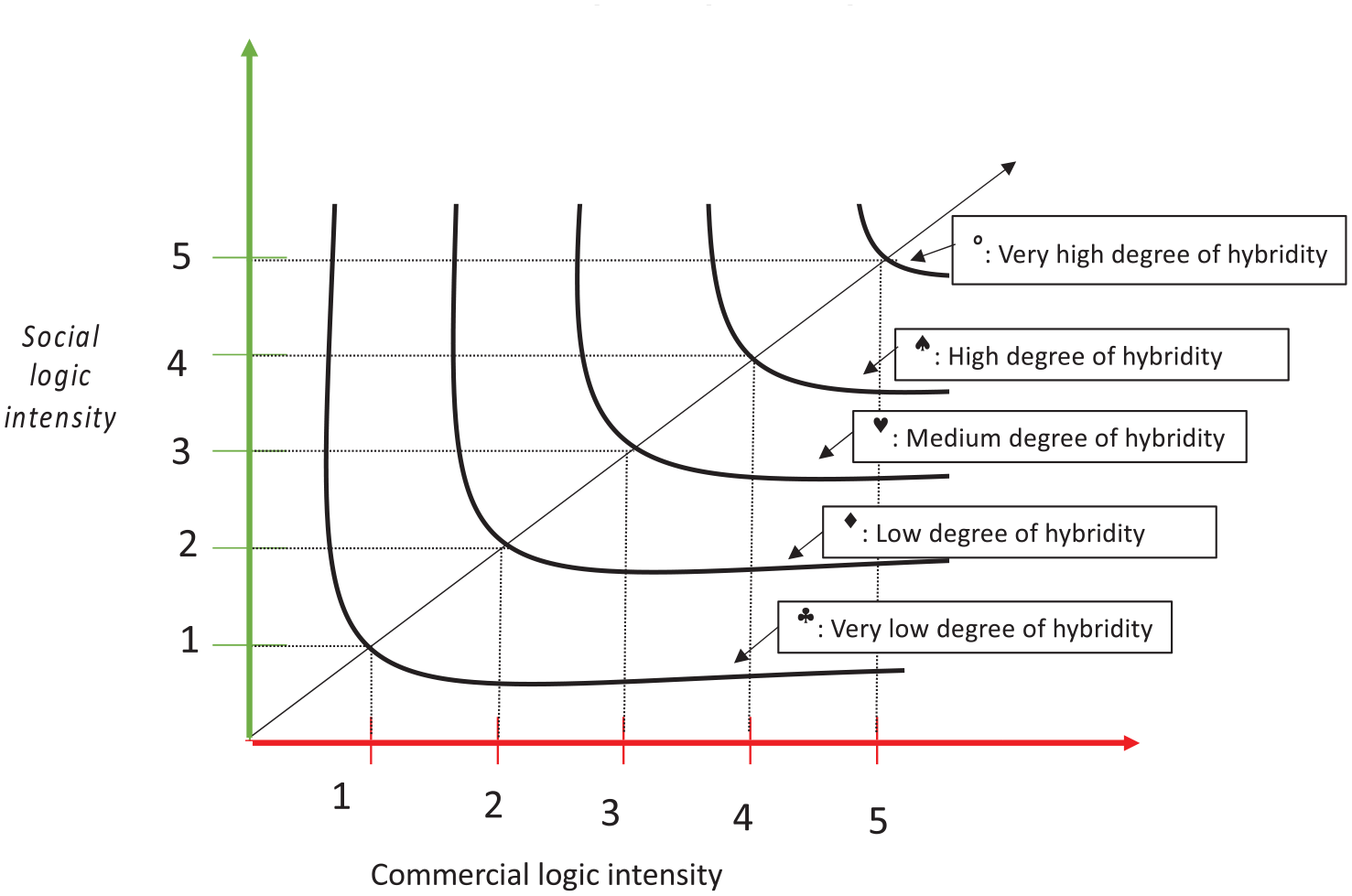

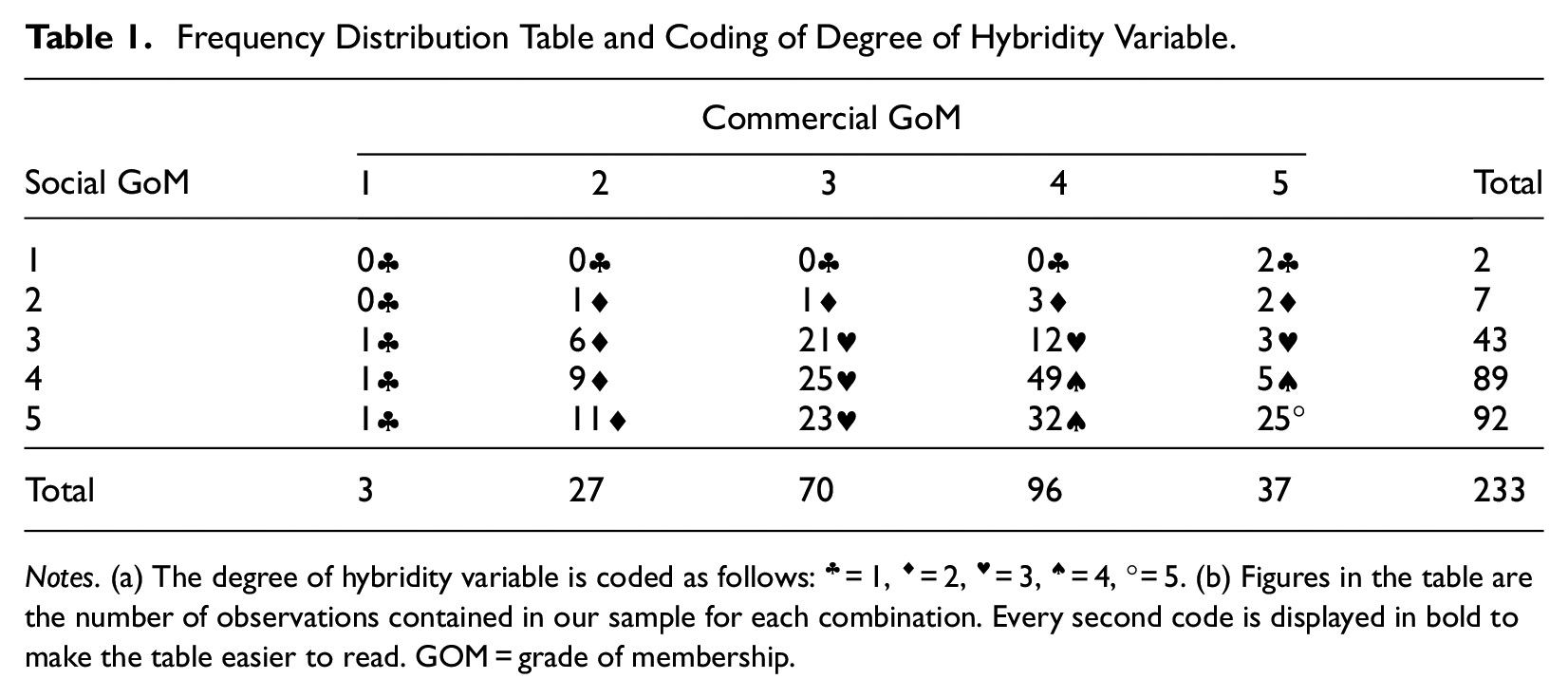

We coded Degree of Hybridity based on Shepherd et al.’s (2019) framework, which captures the relative importance of different features, and the intensity of their implementation in an organization (see Appendix 3). Figure 1 represents these relationships visually and shows that hybridity is high (above right in Figure 1) when an entity has a similarly high GoM in the social and commercial categories. Conversely, hybridity is low when an entity has a high GoM in one category and a low GoM in the other, or when it has a low GoM in both categories. Table 1 shows our coding scheme and reports the relative frequency of different codes. 2

Coding of degree of hybridity variable.

Frequency Distribution Table and Coding of Degree of Hybridity Variable.

Notes. (a) The degree of hybridity variable is coded as follows: ♣ = 1, ♦ = 2, ♥ = 3, ♠ = 4, ° = 5. (b) Figures in the table are the number of observations contained in our sample for each combination. Every second code is displayed in bold to make the table easier to read. GOM = grade of membership.

Our second independent variable was Personal Goal Salience. Following Ratneshwar et al. (2001), we identified this through a top-of-the-mind elicitation (Higgins et al. 1982) where we asked respondents to list three attributes that come to mind when they think about the types of ventures they like and would wish to fund. Two of the authors separately coded the responses to reflect whether the listed characteristics reflect social attributes (e.g., solidarity, ethics, social impact) or commercial attributes (e.g., entrepreneurial dynamics, profitability, creativity, innovation) (see Appendix 4 for more details). 3 We coded innovation as a commercial attribute based on the observation that it is often rewarded by commercially orientated funders (Baum & Silverman, 2004; Miller & Wesley, 2010). From this, we calculated goal salience scores for each respondent (Ratneshwar et al., 2001). The first attribute that a respondent listed was scored as a “3,” the second as a “2,” and the third as a “1.” For example, if a respondent mentioned a social attribute in first position and a commercial attribute in second position, a score of 3 was given to the social personal goal salience indicator and a score of 2 to the commercial personal goal salience indicator. To take recurrence into account, we summed the score associated with the different positions if an individual cited multiple attributes associated with commercial or social goals. For example, if a respondent mentioned a social attribute in first position, a commercial attribute in second position and another social attribute in third position, we assigned a score of 4 (3 for the first position plus, 1 for the third position) to the social goal salience indicator and a score of 2 to the commercial goal salience indicator. As per Ratneshwar et al. (2001), we rescaled the variable in a 0–1 index by dividing the score by six. The two variables are called the Social Goal Index and Commercial Goal Index. We centered both indexes for the analysis.

As an alternate measure of goal salience, we followed Moss et al. (2018) and calculated a Commercial Goal Emphasis Index, by subtracting a respondent’s social goal salience from their commercial goal salience. High values indicate greater commercial goal salience relative to social goal salience, and low values indicate greater social goal salience relative to commercial goal salience. We rescaled this variable in a 0–1 index and centered it for the analysis.

Control Variables

Our models include three sets of additional controls. The first reflects a respondent’s background, as studies show this can influence funding decisions (Greenberg & Mollick, 2017). We controlled for entrepreneurial background using two dummy variables: Social Entrepreneurial Background is a dummy set to “1” if a respondent has social entrepreneurial experience; Commercial Entrepreneurial Background is a dummy set to “1” if a respondent has commercial entrepreneurial experience. Since previous experience as a funder may also influence the funding decision (Shepherd et al., 2003), we included a control variable called Experience as a Funder, which is coded as “1” if a respondent has previously funded a venture (“0” otherwise). 4 The second set of controls relate to a respondent’s demographic profile, specifically Gender (female = “1”) and Age (in years). 5

We also included project and platform-level controls. We used a five-point Likert scale measure (Information on the Project) to control for the extent to which a respondent believes the venture description contains enough information to make an informed judgment. We also controlled for Social Affect with a five-point Likert scale variable that measures the extent to which a respondent values the cause that EaTy champions. 6 Finally, we included a Platform dummy which is coded as “1” if the campaign took place on the WEDOGOOD platform and “0” if it took place on the Crowd’in platform. This allowed us to check for potential platform and country effects. All continuous and Likert variables were centered for the analysis.

Analysis and Results

We tested our hypotheses using probit models, which is appropriate for analyses like ours that feature a binary dependent variable. We included robust standard errors to avoid possible biases due to heteroscedasticity.

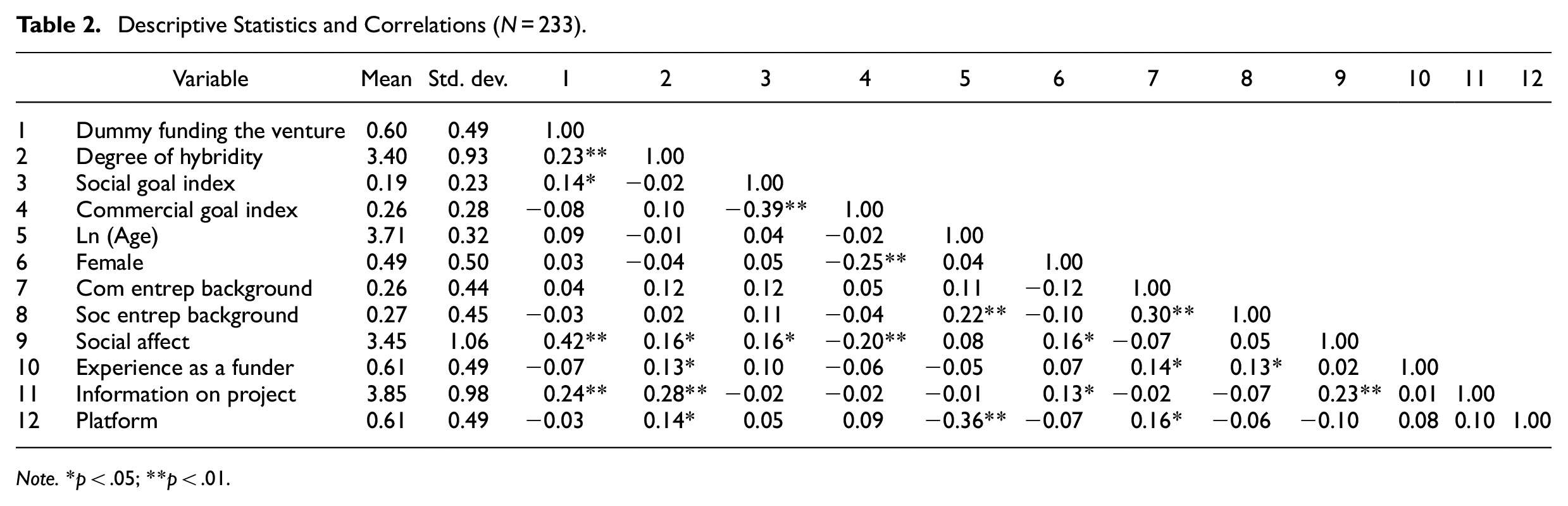

Table 2 presents descriptive statistics and correlations for all variables. Overall, 60% of respondents are willing to fund the venture and the average degree of perceived hybridity is 3.4 (on a five-point Likert scale). The average salience of the Commercial Goal Index is slightly higher than the salience of the Social Goal Index. The average respondent is 43 years old and 49% are female. In total, 26% of respondents have a Commercial Entrepreneurial Background and 27% have a Social Entrepreneurial Background. Finally, the average Social Affect score is 3.45 out of 5, suggesting that respondents generally value the cause that EaTy is pursuing.

Descriptive Statistics and Correlations (N = 233).

Note. *p < .05; **p < .01.

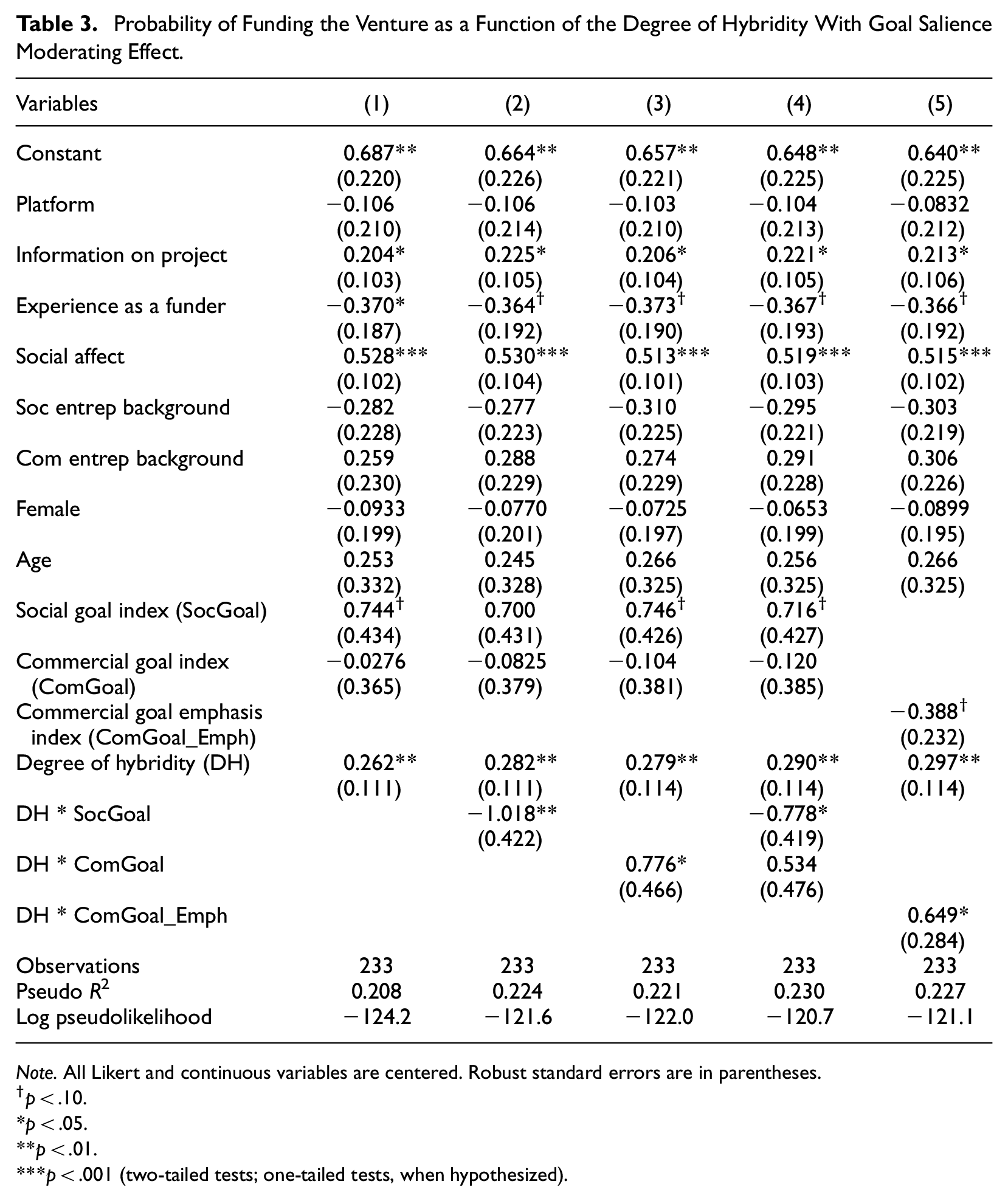

Table 3 presents our regression results. With regard to control variables, respondents are more likely to fund the venture if they value its cause. Respondents with more funding experience are less likely to fund the venture, consistent with evidence that such funders tend to rely on automatic processing, are more sensitive to availability bias, and are less likely to welcome novelty (Shepherd et al., 2003). Respondents are more likely to offer funding if they believe they have sufficient Information on the Project, highlighting the importance of information when assessing the specificities of a hybrid venture.

Probability of Funding the Venture as a Function of the Degree of Hybridity With Goal Salience Moderating Effect.

Note. All Likert and continuous variables are centered. Robust standard errors are in parentheses.

p < .10.

p < .05.

p < .01.

p < .001 (two-tailed tests; one-tailed tests, when hypothesized).

Hypothesis 1 argues that an enterprise is less likely to receive funding when audience members perceive that it has a high level of social–financial hybridity. Results do not support this prediction. The coefficient for Degree of Hybridity is positive and significant across all models (e.g., β = .262, p < .01 in Regression [1]).

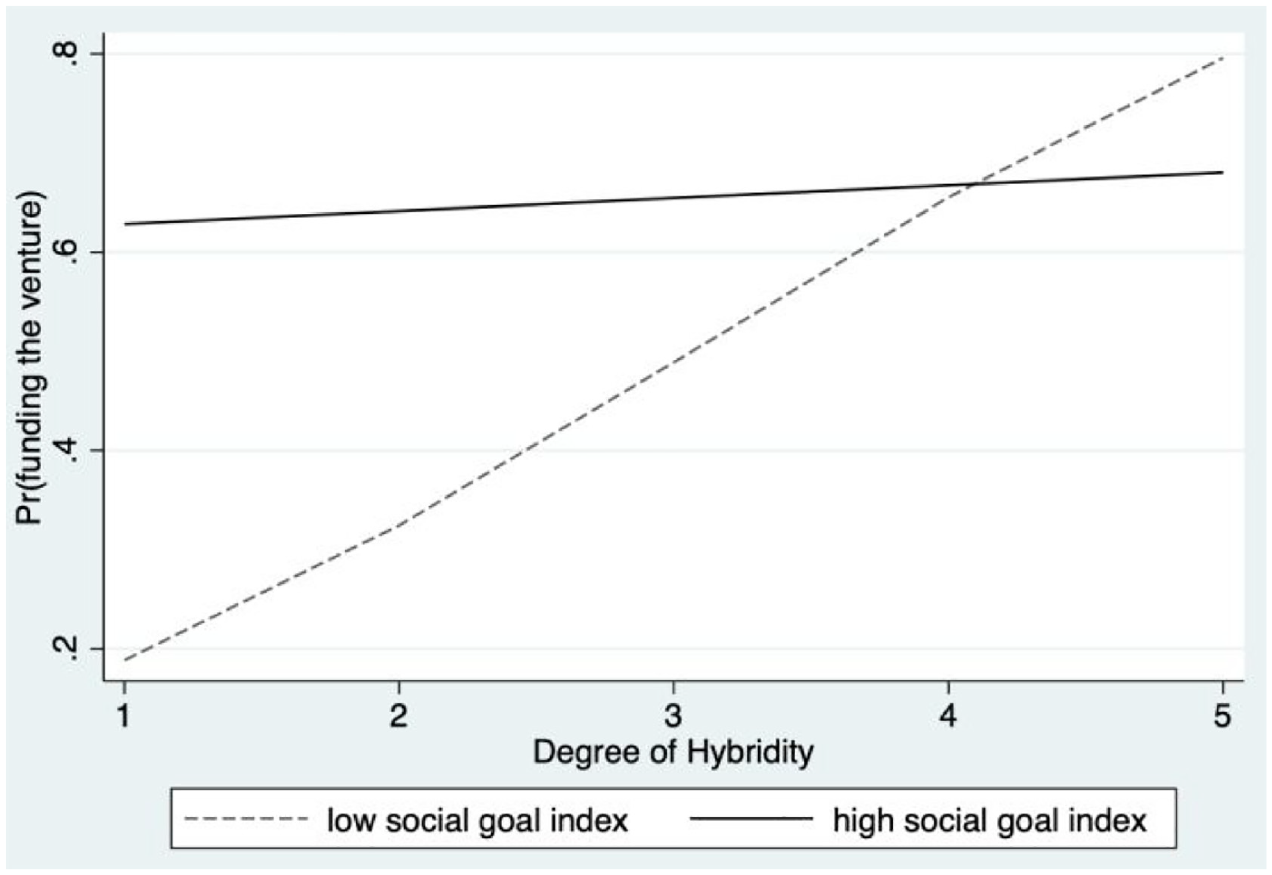

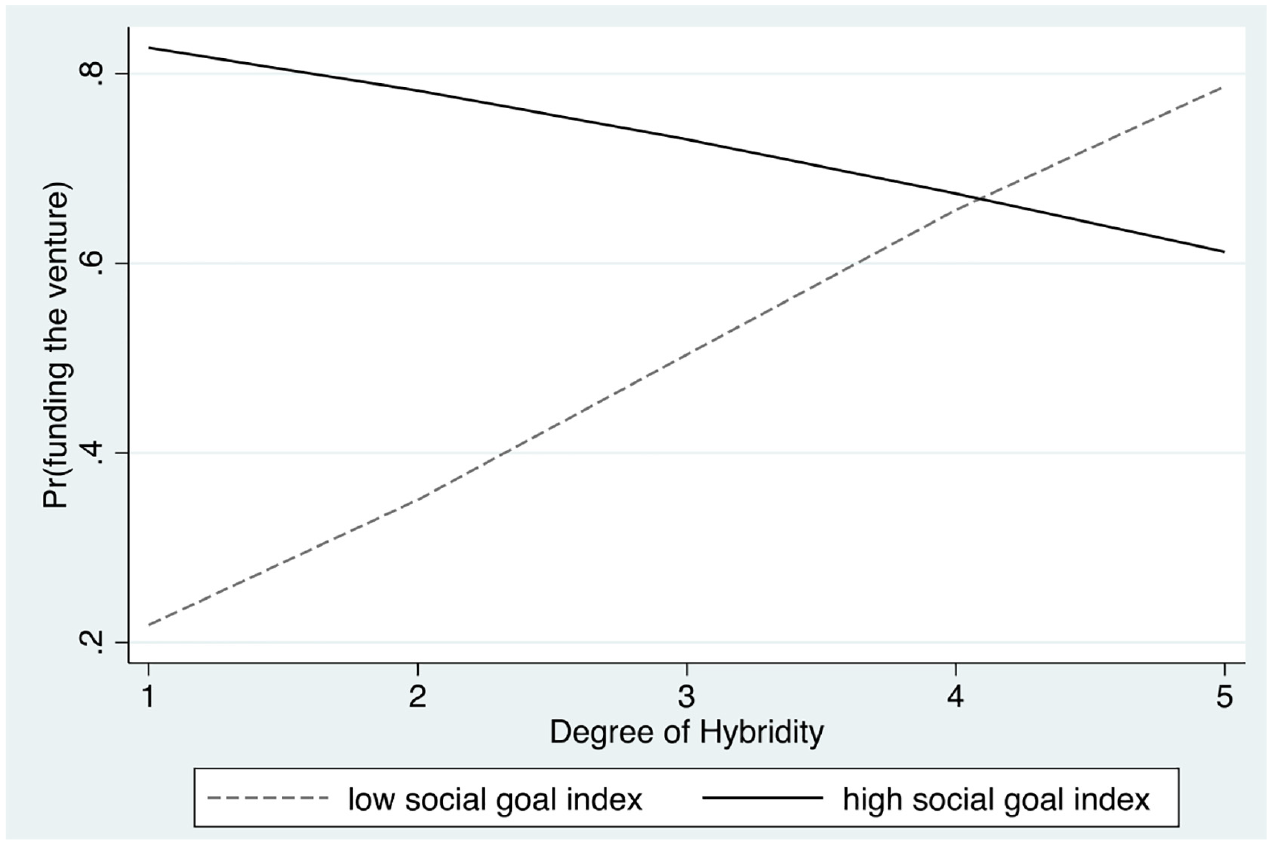

Hypotheses 2 and 3 argue that this relationship is moderated by a funder’s primary goal, which we suggest will affect how they understand and value hybridity (Wry et al., 2014; Wry & Durand, 2020). Hypothesis 2 argues that a salient social goal negatively moderates the effect of hybridity on the decision to fund a venture. Consistent with this expectation, we observe a negative and significant interaction between Degree of Hybridity and Social Goal Index (e.g., β = −1.018, p < .01 in Regression [2]). Figure 2 plots this relationship and shows that the positive effect of hybridity is neutralized for individuals with a salient social goal (one standard deviation above the mean). Following Butticè et al. (2017), Figure 3 plots this relationship for lower and higher values of the Social Goal Index (i.e., the 5th and 95th percentiles of the distribution) and suggests that socially minded crowdfunders may actually punish hybridity. Notably, when the Social Goal Index takes a high value (the 95th percentile of the distribution)—and all other continuous variables are held at their mean and dummies at their median—a one standard deviation increase in Degree of Hybridity leads to a 7.73% decrease in the probability of funding (from 70.86% to 65.38%). In comparison, we see a 24.20% increase (from 56.58% to 70.27%) when the Social Goal Index takes a low value (the 5th percentiles of the distribution).

Moderating effect of social personal goal salience.

Moderating effect of social personal goal salience.

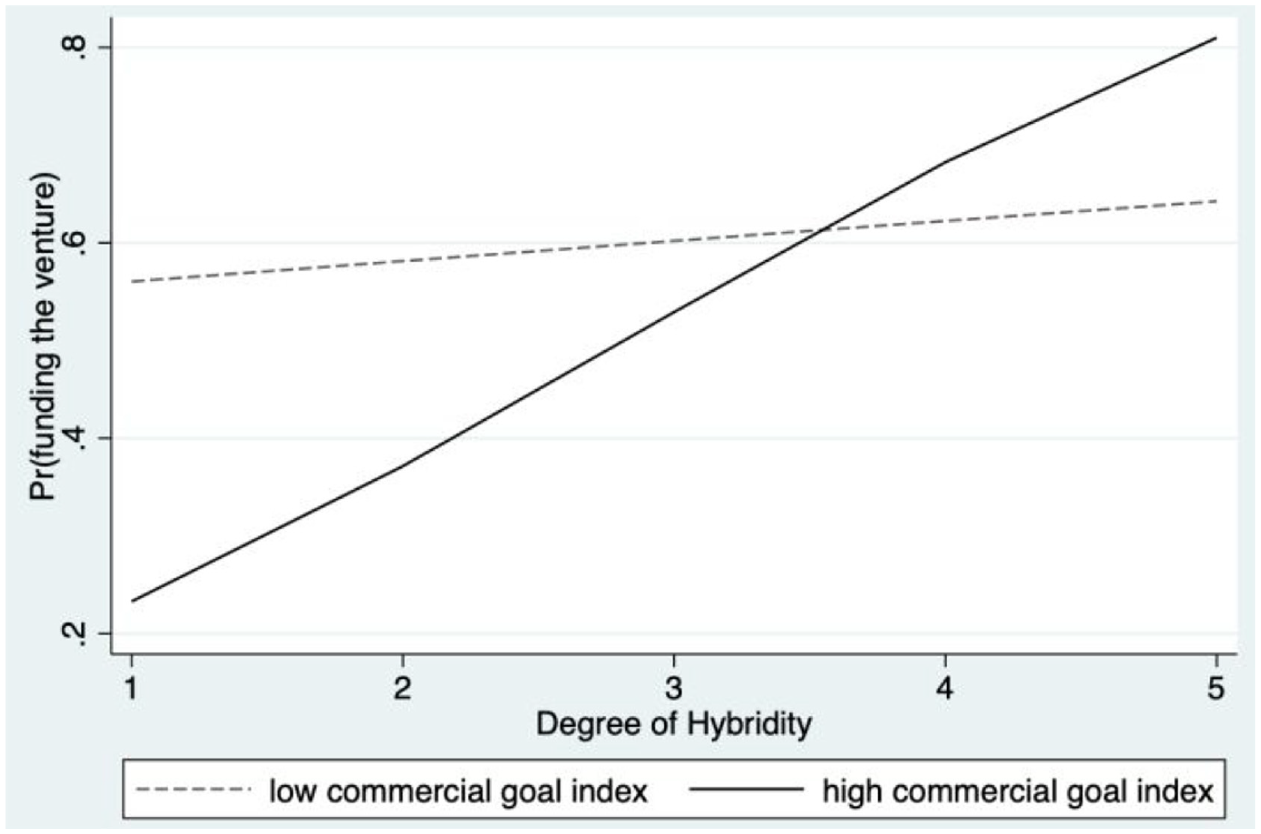

Hypothesis 3 argues that a salient commercial goal positively moderates the effect of hybridity on the decision to fund a social venture. Results are supportive. The coefficient for the interaction between Degree of Hybridity and Commercial Goal Index is positive and significant (e.g., β = .776, p < .05 in Regression [3]). Figure 4 plots this relationship and shows that participants with a salient commercial goal (one standard deviation above the mean) reward hybridity, but those with a non-salient commercial goal (one standard deviation below the mean) do not. When the Commercial Goal Index is high (95th percentile of the distribution), a one standard deviation increase in Degree of Hybridity results in a 33.43% increase in the probability of funding (from 58.21% to 77.67%), while this probability almost stagnates when the Commercial Goal Index is low (5th percentile of the distribution).

Moderating effect of commercial personal goal salience.

Regression (4) includes both product terms. In this case, only the product term between Degree of Hybridity and Social Goal Index remains significant. This can be explained by the partial overlap between the two goal salience variables, since low salience in one type of goal includes, among other cases, high salience in the other goal. As with Moss et al. (2018), we address this with a third variable, Commercial Goal Emphasis, that reflects the difference between commercial and social goal salience. High values indicate greater commercial goal salience (relative to social goals), and low values indicate greater social goal salience (relative to commercial goals). The interaction between Degree of Hybridity and Commercial Goal Emphasis is positive and significant (β = .649, p < .05 in Regression [5]), which corroborates our support for hypotheses 2 and 3.

Robustness Checks and Supplementary Analyses

We ran numerous robustness checks and additional analyses to enrich our findings and rule out alternate explanations (regression tables are available on request).

Alternate Approaches to Moderation Effects

Following Aiken et al. (1991), we cross-checked our moderation effects with simple slope tests on sub-samples. More precisely, we ran the same probit model, but restricted first the sample to funders who have a salient commercial personal goal (i.e., a Commercial Goal Index above the 55th percentile). As in our main results, higher social–financial hybridity significantly increases the probability that the venture is funded by participants who have a salient commercial goal (simple slope β = .583, p < .001). We then conducted the same regression restricting the sample to funders with a salient social goal (i.e., Social Goal Index above the 55th percentile). Here, we see a negative, but not significant, relationship between social–financial hybridity and the probability that the venture is funded (simple slope β = −.134, p > .10). This test corroborates our main results. Unlike those with a salient commercial personal goal, funders with a salient social goal do not reward hybridity.

Addressing the Desirability Bias

Studies have found that actors may give biased answers when asked about socially desirable actions (e.g., Larson, 2018). Given that funding a social venture may be considered socially desirable, and our dependent variable reflects intentions as opposed to actions, it is possible that our data are affected by this bias. However, this would only be problematic for our analysis if the likelihood of giving a socially desirable response was systematically different for funders with salient commercial versus social impact goals (i.e., if reporting a commercial motivation cued a socially desirable response). We could not find any studies that suggest such a pattern exists and, indeed, there is evidence that it does not exist (Sörqvist et al., 2016; Thøgersen, 2011). Furthermore, given that the bias involves emphasizing prosocial action, it seems unlikely that people who are motivated by a private goal (financial returns) would be prone to make such claims (Larson, 2018, 2019). We also controlled for variables such as gender, age, and social affect that may affect desirability bias (Chung & Monroe, 2003).

Another, related concern, is that there may be a gap between intentions and action, such that our results may over-estimate the magnitude of the observed effects. Without discounting this possibility, we note that our approach is common in both marketing and crowdfunding studies (Greenberg & Mollick, 2017; Thomas et al., 2020). Nevertheless, as a check, we ran the same probit regressions as our main analysis but restricting the sample to participants who have already made investments. Given that these respondents have already exhibited the behavior in question, there is arguably a smaller gap between their intentions and actions in this context. The results obtained with this subsample closely match our main findings.

Alternate Dependent Variable

Since our interest focuses on how hybridity affects the probability of a social enterprise being funded, our main models use a dichotomous dependent variable. This aligns with prior studies of how categories affect organizational funding (e.g., Wry & Lounsbury, 2013; Wry et al., 2014) and accounts for inequities in the amount that people are able to offer, which may be sensitive to factors like age, gender, and socio-economic status.

We nevertheless ran an additional model using a continuous dependent variable (Funding Amount) to see if there is evidence that hybridity may affect funding amounts. Since this variable is left censored at zero (the value assumed when funders are not willing to invest), we used a Tobit model: a non-parametric approach appropriate for this type of data. In addition, Funding Amount (FA) is best modeled as lognormal (lnFA), as is generally the case for expenditure data. To overcome the zero-threshold issue (which does not have a log value), we followed Cameron and Trivedi (2010), who suggest setting all censored observations to an amount slightly smaller than the minimum uncensored value of the lognormal transformed variable (lnFA). Results are very similar to our reported models, indicating that a salient commercial goal may increase both the likelihood and amount of funding at higher levels of hybridity.

Discussion

We began this article by noting that social ventures may have a categories problem since they integrate features associated with both business and charity (Battilana & Lee, 2014). This hybrid nature has the potential to advance new and financially sustainable solutions to social and environmental problems (Wry & York, 2017), but it is also associated with resource acquisition difficulties. Indeed, a key insight from the classic, prototype-based view of categorization is that entities that mix features from multiple categories—and thus show high levels of hybridity—are difficult for audience members to situate, making it unclear how they should be evaluated, and potentially signaling that they are of lower quality than category-focused options (Vergne & Wry, 2014). Reflecting this, studies have found that hybrid social ventures are less likely to obtain funding from traditional providers like banks, equity investors, and charitable foundations (Battilana & Lee, 2014; Cobb et al., 2016). Even funders who claim to value social impact and financial returns may rely on existing categories, and are unlikely to fund ventures that fail to signal a clear focus on one outcome or the other (Lee et al., 2020; Moss et al., 2018).

Consistent with prior literature, our first hypothesis argued that high levels of hybridity make a social venture less likely to receive funding. Going beyond this, though, we argued that hybridity might make a venture predictably more attractive to certain types of funders and less attractive to others. To advance this argument, we began by noting that research on goal-based categorization suggests that actors are not always bound by existing categories and will often judge items based on how well they serve a particular goal (Glaser et al., 2020; Paolella & Durand, 2016; Pontikes, 2012). We then noted that it is very difficult to generate a composite framework to evaluate entities that pursue multiple utilities (Tetlock, 2003), with the likely implication that social enterprise funders will prioritize either financial returns or social impact goals (Moss et al., 2018). We then drew on the causal-model approach to categorization to argue that a funder’s main goal will affect how they understand and evaluate hybridity. If a social goal is salient, funders will likely consider how a venture’s commercial activities affect impact creation, while the opposite should apply if a commercial goal is salient. A review of the academic literature and interviews with 31 members of our focal crowdfunding platforms led us to predict that hybridity will make a venture more attractive to funders with a salient commercial goal but less attractive to those with a salient social goal.

Analysis of survey respondents from two crowdfunding platforms supports our key arguments. Unlike prior studies, and contra to our first hypothesis, results show that a venture is overall more likely to receive funding when it is perceived to have a high level of hybridity. However, this outcome is driven almost entirely by funders with salient commercial goals who, as per our argument, are more likely to fund a venture with high perceived hybridity. Funders with a salient social goal do not reward any level of social–financial hybridity, and our results suggest that those with the strongest social goals may actually punish hybridity. Our theory and findings have implications for research on categories, hybrid ventures, and crowdfunding.

Contributions to Categories Research

Our article is the first that we know of to connect insights from the goal-based and causal-model approaches to categorization. Studies that adopt a goal-based approach show that categorization and evaluation are often ad hoc processes motivated by a desire to pursue a valued utility (Paolella & Durand, 2016; Glaser et al., 2020; Pontikes, 2012). The primary strengths of this approach are that it: (a) offers insight into sources of audience heterogeneity; and (b) shows that consideration sets can comprise items from different categories (Barsalou, 1999). However, studies in this milieu offer limited insight into the evaluation of hybrids, other than to note that audiences may appreciate ambiguous offerings (Boulongne & Durand, 2021; Pontikes, 2012), and sometimes pursue complex goals that favor organizations offering multiple products or services (Paolella & Durand, 2016). These are useful findings, but they say little about how actors evaluate entities that mix features from high-contrast, oppositional categories—such as charity and business—that are associated with distinct goals, practices, and outcomes (Kovács & Hannan, 2010; Wry & Lounsbury, 2013) and thus reflect high levels of hybridity (Battilana & Lee, 2014; Shepherd et al., 2019).

In comparison, studies of causal-model categorization have analyzed the different ways that entities mix features from oppositional categories, and with what results (Wry & Durand, 2020). This work shows that some types of hybridity are perceived to be sensible and valuable because actors make inferences about how features from one category may affect the outcomes associated with another category (Rehder, 2003). If an entity integrates features in a way that audiences perceive as directionally appropriate (e.g., using science to push product commercialization versus using product development to drive scientific research), this is associated with better evaluations and funding outcomes (Wry et al., 2014). Yet there has been little consideration of how or why audience members might evaluate such hybrids in different ways.

Our argument suggests that insight can be gained by integrating goal-based and causal-model approaches. We argue that people may interpret the same hybrid entity differently because their individual goals support different causal models. If a funder seeks financial returns, they will likely consider how this goal is affected by a venture’s social impact features. Yet if a funder seeks social impact, they will likely consider how a venture’s commercial pursuits affect this goal. We argue that these causal models will lead to predictably different assessments of the same entity. Commercial pursuits are likely to be interpreted as a source of tension that signals a reduced focus on impact creation (Hwang & Powell, 2009) and a greater likelihood of mission drift (Grimes et al., 2019). In comparison, social mission pursuits may be perceived as financially symbiotic because they are associated with reduced investment risk (Cerqueti et al., 2021) and increased product differentiation (Du et al., 2010).

While our data do not allow us to observe funder perceptions directly, interviews help to validate our theorized mechanisms, and empirical results are consistent with our predictions. As such, we provide evidence that audiences use different causal models depending on the primary goal they are pursuing, and this leads to different assessments of the same entity. Our approach thus provides novel insight into the varied ways that audiences evaluate hybrids and forges a bridge between previously unlinked streams of categories research.

Our argument also reminds that category-based decisions are not always isolated events. There is an assumption across all strands of categories theory that actors judge entities based on category codes or personal utilities, and reward the best offerings (Durand & Paolella, 2013). There has been little consideration about the potential for interdependence among decisions, how multiple decisions may be required to fulfil a goal, or how these considerations might affect the assessment of an entity (Kim & Jensen, 2011). We address this shortcoming, noting that investors often pursue financial goals by investing in multiple different assets that collectively balance risk and reward (Cerqueti et al., 2021). An entity does not need to have the most financial upside to be useful; rather it needs to fit within a portfolio of investments. This is an important insight in our context, as it suggests that commercially oriented funders do not find financial tradeoffs inherently problematic, so long as a social venture is perceived as having less risk than other investments in the portfolio. It is entirely possible, though, that funders who are trying to maximize returns from a single investment would arrive at a different evaluation. Decision criteria may thus vary based on an actor’s prior decisions. We believe that attending to the interrelated and temporal aspects of evaluation is an important research direction for categories studies.

Contributions to Crowdfunding and Social Enterprise Research

Many studies have analyzed factors that predict successful crowdfunding outcomes, and there is growing evidence that these platforms are promising channels for activist investing (Greenberg & Mollick, 2017) and funding social enterprises (Moss et al., 2018). However, studies to date have focused on the outcomes realized by funding campaigns with different features while treating audience members and their interests as more or less homogeneous. As a result, prior studies offer little insight into what leads different types of crowdfunders to support a hybrid social enterprise, or not.

Prior studies have mainly adopted a stimulus-based perspective, where a campaign’s characteristics or a project’s features, as communicated through the venture’s narrative, are considered the main determinants of funding decisions (Allison et al., 2015; Ahlers et al., 2015; Calic & Mosakowski, 2016). Studies suggest, for instance, that crowdfunders are attracted to a certain type of language in the description of social ventures (e.g., human interest, diversity, profit potential, risk-taking, and competitive posture) (Allison et al., 2015; Ahlers et al., 2015; Moss et al., 2014). Consequently, attention is directed toward the inner characteristics of social ventures and the strategic manipulations they practice through language and content to obtain funding. This echoes findings in entrepreneurial finance that stress the role of language and communication (Clarke & Cornelissen, 2011). Linguistic approaches have also been applied recently to address the role of hybridity in investment decision-making. Moss et al. (2018) found that lenders on social crowdfunding platforms tend to fund hybrid ventures that portray themselves as aligning with a single linguistic category.

In parallel, a few studies have looked at crowdfunder characteristics (profiles and motivations). For example, Lin et al. (2014) identify four distinct archetypes: active backers, trend followers, the altruistic, and the crowd. Related research analyzes the diverse motivations that actors have for engaging in crowdfunding (Cholakova & Clarysse, 2015; Nielsen & Binder, 2021; Ryu & Kim, 2016).

Combining both perspectives, we build on the findings of Moss et al. (2018) concerning the role of hybridity in decision-making by highlighting the moderating impact of crowdfunder characteristics (i.e., personal goals and causal models). Indeed, to the best of our knowledge, no study has yet investigated how the personal goals of crowdfunders affect the probability that they reward or punish the hybrid nature of social ventures through their funding decision. Our article remedies this shortcoming by adopting insights from diverse streams of categories theory and shows that hybridity makes a social venture predictably more attractive to commercially oriented crowdfunders and less appealing to impact-oriented crowdfunders. Although further research is needed to establish if our findings generalize beyond crowdfunding platforms, we nonetheless show that hybrid social ventures appeal to some funders who prioritize financial returns in their decision-making. Given that commercial impact investing represents a large and fast-growing capital pool (Hand et al., 2020), our findings have potentially important implications for the viability and scalability of hybrid social enterprises, especially if they frame their social mission pursuits as reducing risk and contributing to competitive differentiation.

Conclusion

In this article, we argue that analyzing overall patterns in funding for hybrid social ventures masks an underlying pattern, where hybridity makes a venture predictably more attractive to some types of funders and less attractive to others. By building on and integrating two emergent streams of categories research, we argue that funders may pursue different goals when deciding to support a social venture and that hybridity may create the perception that a venture is more or less likely to deliver on these outcomes. Interviews and survey data show that funders who prioritized financial goals in their decision-making react positively when they perceive that a venture exhibits high levels of hybridity, whereas funders who prioritize social impact creation do not react positively. Our study thus offers new insight into the relationship between goal-based and causal-model approaches to categorization, and how the interplay between the two can create variance in the appeal of hybrid social ventures.

We identify three main possible extensions of our research. First, our study suffers from a gap between intention and action. Although we discussed the potential biases that it can generate and ran additional tests to investigate those biases, further research could develop similar studies—adopting an audience-based perspective of categorization—but using experimental laboratory methods to complement our results (such as Greenberg and Mollick (2017) in their research about gender homophily in funding behavior).

Second, audience familiarity with categories and the relationships underlying their features varies a great deal (Taeuscher et al., 2021). This can affect the causal-model of socially and commercially oriented funders. Further research could investigate the impact of familiarity with hybridity on how funders with different goals judge a higher level of hybridity and, ultimately decide whether or not to invest in the venture.

Finally, to better understand the decision to invest in hybrid venture, while this article shows the importance of taking into account both funders’ goals and their causal-model for how these goals are affected by the venture’s perceived hybridity, little is known about the impact of contextual factors on these variables. Further research may usefully investigate how contextual factors (e.g., society’s values and religious involvement) influence perceptions of hybrid ventures and identify the factors that may be associated with a preconception that a venture’s social orientation is compatible (vs incompatible) with its financial objective.

Footnotes

Appendix

Appendix 2: Primary Checks

To verify that the social welfare and commercial categories were salient within the social venture, a pilot qualitative study was conducted with four participants, who had different profiles and levels of prior knowledge about the social and commercial categories. Drawing on the method developed by Porac et al. (1989), these four pilot participants were presented with the case study and asked to list competitors or similar ventures that they had seen or heard of.

Then, they were asked what the ventures listed had in common. Answers were classified within the social welfare category whenever participants had indicated aspects related to the social mission of the venture: for instance, when they mentioned firms seeking to achieve the same social impact (e.g., “serving refugees”) or similar social welfare organizations (e.g., work integration social organizations). Whenever participants mentioned aspects concerning industry competitors or marketing strategy, answers were classified within the commercial category: for instance, when they mentioned industry competitors (e.g., “food delivery firms” vs. “classical restaurants”) or firms targeting the same customers. This pilot qualitative study made it possible to verify that both the social and commercial missions of the venture were salient to participants.

Appendix 3: Shepherd et al. (2019) ’s Theorization of the Degree of Hybridity

Recent advances in hybrid ventures literature go beyond the simple dichotomy between hybrid and non-hybrid enterprises. Studies recognize the existence of varying degrees of hybridity. Looking at social ventures, Shepherd et al. (2019) theorize that the degree of hybridity involves two dimensions: the relative importance that social ventures give to social welfare and commercial logics (Battilana et al., 2017; Shepherd et al., 2019); and the intensity of the embedded logics. “Intensity” refers to the vigor with which the social welfare logic and the commercial logic are implemented within an organization.

Consequently, a high degree of hybridity (above right in Figure A1) involves both high relative hybridity and high hybrid logic intensity. Translated into a categorization perspective, a high degree of hybridity would correspond to a high similar GoM in both categories. On the contrary, a low degree of hybridity would correspond to both a low relative hybridity (i.e., when the enterprise is especially anchored in one or the other logic, above left or below right in Figure A1), which would correspond to a high GoM in one category and a low GoM in the other category, and a low hybrid logic intensity (i.e., when the enterprise gives the same low importance to both logics, below left in Figure A1), which would correspond to a low similar GoM in both categories.

Appendix 4: Attributes Coding

Table A2 includes all attributes coded as social and commercial attributes. The “others” category includes examples of other attributes, neither social nor commercial, mentioned by respondents. In terms of position, 16.74% of attributes placed in first position were coded as social attributes; 23.61% of attributes placed in second position and 18.45% of attributes placed in third position were also coded as social attributes. Concerning commercial attributes, 31.33% of attributes placed in first position were coded as such; 18.88% of attributes placed in second position and 22.32% of attributes placed in third position were also coded as commercial attributes.

Acknowledgements

We thank our editor, Dr. Maija Renko, and the three anonymous reviewers for their constructive feedback throughout the review process. We also thank Simon Cornée, Saskia Crucke, Benjamin Huybrechts, Marc Labie, and Ariane Szafarz, as well as participants at the 2020 EGOS conference for their helpful suggestions and critiques. We are grateful to the Wharton Impact Investing Research Lab and the Action de Recherche Concertée program (grant no. 19/24-101) from the Fédération Wallonie-Bruxelles entitled Platform Regulation and Operations in the Sharing Economy (PROSEco) for supporting this research.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.