Abstract

We study the effects of diversity in national culture on new technology ventures’ founding teams on their financial harvest exit strategy. Exits represent a pivotal event in the entrepreneurial process that reflects the strategy and performance of technology startups. Following a quasi-replication of the seminal study of Chaganti and colleagues in 2008, aimed at generalizing their findings to different technologies and periods and assessing their robustness, we demonstrate that diverse founding teams are significantly more likely than non-diverse teams to exit via financial harvest. We add to the literature by identifying a novel contributing factor—diversity in national culture—in founding teams’ financial harvest strategies. The economic implications, both at the micro and macro levels, of the diversity factor are considerable. The contribution of this study thus extends beyond the academic literature.

Keywords

Introduction

The importance of immigrant entrepreneurs and diverse management teams is well demonstrated in the literature (e.g., Balachandran et al., 2019; Boone et al., 2019; Kulchina, 2016; Ndofor & Priem, 2011; Nielsen & Nielsen, 2013; Saxenian, 2001). Yet, the only existing study on the effects of immigrant entrepreneurs on the strategy and performance of new technology ventures (NTVs), which are considered the engine of the modern economy, is Chaganti et al. (2008). Focusing on one type of NTV (a sample of 52 public Internet firms) in 1997 to 2000, Chaganti et al. (2008) presented inconclusive evidence about the effects that the presence of immigrants in the top management team, which they refer to as the founding team, has on the team’s prospector strategy and the venture’s performance. Considering the inconclusive results and the fact that the evidence is not generalizable, as Chaganti et al. (2008) acknowledged, 1 it is important to replicate and extend their work.

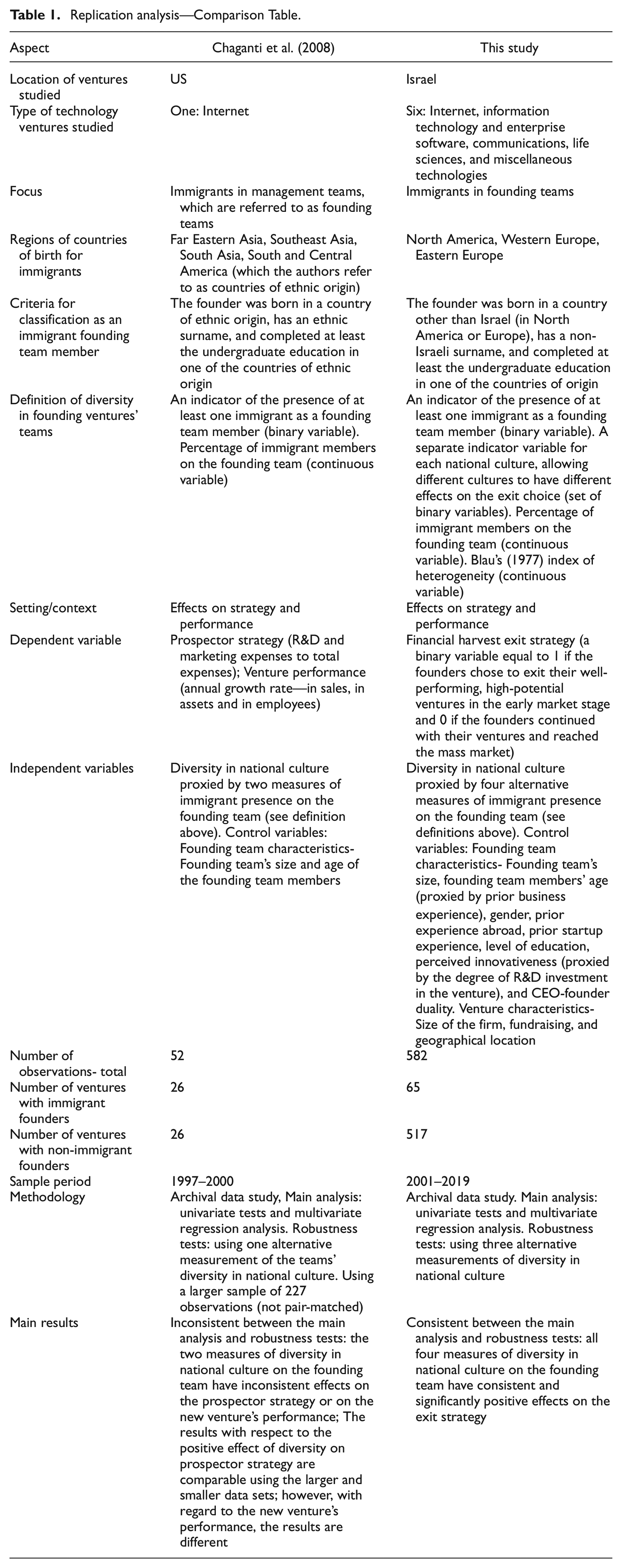

This study provides a quasi-replication and extension of their research using a larger number of NTVs (582) from various technology industries (six different technologies) over a more recent and extended time period (2001–2019). The quasi-replication is intended not only to generalize the results to different technologies and periods but also to assess their robustness. Using different measures and methods, we explore the effect of diversity in national culture, captured by the presence of immigrants on the founding teams of NTVs, 2 on their financial harvest exit decisions. Such decisions represent a pivotal event in the entrepreneurial process that reflects the founders’ strategy and the ventures’ performance (Aldrich, 2015; Cumming, 2008; DeTienne, 2010; DeTienne et al., 2015; DeTienne & Wennberg, 2016; Wasserman, 2003). Table 1 summarizes the replication analysis.

Replication analysis—Comparison Table.

New technology entrepreneurship is a major driver of economic growth in developed countries (e.g., Farhat et al., 2018; Song et al., 2008). In these countries, the demand for technology talent is substantial due to the shortage of skilled individuals in technology industries (e.g., Bagley, 2014; Bureau of Labor Statistics, 2015; Israel Innovation Authority Report, 2022). Indeed, the considerable and increasing diversity in national culture due to the ongoing immigration to these countries is also evident in technology entrepreneurship (e.g., Anderson, 2016; Brown et al., 2019; Hunt & Gauthier-Loiselle, 2010; Saxenian, 2001; Wadhwa et al., 2007a, 2007b). Nevertheless, despite its pertinence to entrepreneurship, there is hardly any research about the consequences of diversity in national culture among founders in technology startups (Chaganti et al., 2008). Recent research has also emphasized the need to further advance our understanding of founder exits, especially in high-potential ventures (Souitaris et al., 2020). In particular, it is important to investigate the decision to voluntarily exit from a high-potential NTV, as it has substantial implications for both the micro- and macro-economic levels. Indeed, in contrast to forced exits from poorly or even well-performing ventures (e.g., Ewens & Marx, 2017) or voluntary exits to avoid further losses (e.g., DeTienne et al., 2008), the decision by founders to voluntarily leave their successful ventures is most intriguing. Nevertheless, this type of exit decision is the least studied thus far (Souitaris et al., 2020). Our study aims to address these gaps in the literature.

The most typical exit strategy in NTVs is financial harvest where founders voluntarily leave their venture, either by being acquired by another company (acquisition) or by issuing an initial public offering (IPO), giving them substantial added value (Cumming, 2008; DeTienne et al., 2015; Poulsen & Stegemoller, 2008; Souitaris et al., 2020). We focus on exit via acquisition, which is more universal in technology startups than an IPO (Cotei & Farhat, 2018; Farhat et al., 2018, Giot & Schwienbacher, 2007). To investigate the effect of diversity in national culture on the founding teams on the likelihood of a financial harvest, we build on entrepreneurship theories about the characteristics of founders who choose this type of exit strategy (Cardon et al., 2009; Cotei & Farhat, 2018; DeTienne et al., 2015) and those of immigrant founders (e.g., Anderson, 2016; Chaganti et al., 2008). In addition, we build on business management theories about the impact of diverse teams’ human and social capital on performance (e.g., Boone et al., 2019; Nielsen & Nielsen, 2013), and social psychology theories about differences in entrepreneurial activity across cultures (e.g., McClelland, 1961; Shane, 1992; Thomas & Mueller, 2000; Weber, 1904). Based on a comprehensive review of the theoretical mechanisms established in these studies, we predict that, ceteris paribus, diversity in national culture will be positively associated with financial harvest exits.

We analyze the effects of diversity in national culture on the founding teams on financial harvest exits in NTVs using a unique sample of 582 high-potential NTVs in Israel. In 299 of them, the founders exited via acquisition, and in 283, the founders remained in place. All exits in our sample occurred after the NTVs demonstrated technological success and had products accepted by early adopters. The average time until the exit is about 5 years from the venture’s establishment. Note that the main obstacle facing technology startups is the transition from an early market, made up of early adopters, to a mainstream market consisting of a large block of customers who accept the new technology (Moore, 1999). Acquisition by another firm at an early stage signals strong potential. Founders often view it as a means to harvest their investments at the riskiest stage of their venture. In contrast to the founders in our sample who chose to exit, the founders in our control sample chose not to leave in the early market phase. Instead, they remained with their ventures, helping them “cross the chasm” (Moore, 1999) between the early market and the mass market. 3 Thus, both groups consist of high-potential NTVs at the early adopter stage, one with founder exits and the other without. Furthermore, both groups of firms made the transition from early adopters to the mass market, one with and one without the founders leaving the company.

Israel serves as an appropriate setting for our study. It is globally recognized as a leader in innovation and thus has been dubbed the “startup nation.” 4 In addition, like other developed countries, Israel is an immigration country. Immigrant founders in our sample were born and spent their formative years outside of Israel. Hence, they differ in culture and nationality from native-born founders. 5 Consistent with Chaganti et al. (2008), we measure diversity in national culture based on the presence of immigrant founders as members of the founding teams who were born outside of Israel, have a non-Israeli surname, and completed at least an undergraduate degree outside of the country. Given that the measurement of diversity could affect the results, we examine the robustness of our findings using various measures of the presence of immigrants, in addition to Chaganti et al.’s (2008) main measure of having at least one immigrant on the founding team.

Our study contributes to two important research strands in the entrepreneurship literature: immigrant entrepreneurship and entrepreneurial exits. We add to the existing literature by identifying a novel contributing factor—diversity in national culture—in founding teams’ financial harvest strategies. This effect in well-performing NTVs which, as indicated, are essential to long-term sustainable economic growth (see also, Castells & Hall, 1994; Saxenian, 1996), has important practical implications for founders, investors, employees, and even the government (via the tax collected on the proceeds from the sale transaction). The contribution of this study thus extends beyond the academic literature.

Theory and Development of the Hypothesis

Immigrants and Entrepreneurship

Studies show the strong presence of highly skilled, professional immigrants in technology-based entrepreneurial ventures in developed countries. Evidence from the U.S. establishes that immigrant entrepreneurship has a substantial positive impact on innovation in the high-tech sector (e.g., Brown et al., 2019; Hunt & Gauthier-Loiselle, 2010; Kerr & Lincoln, 2010). Immigrants in the U.S. have increasingly become a major driving force in the creation of new, fast-growing technology ventures (e.g., Anderson, 2016; Brown et al., 2019; Chaganti et al., 2008; Ndofor & Priem, 2011; Saxenian, 2001; Wadhwa et al., 2007a, 2007b). Likewise, Niebuhr (2010) documents a positive relationship between diversity in national culture in the highly skilled workforce in Germany and R&D activity, measured as patents per capita. Levie (2007) reports a positive link between immigration and new business activity in the U.K. Smallbone et al. (2005), Nathan and Lee (2013), and Nathan (2016) also provide evidence of the positive effect of diversity in national culture in the U.K. on creativity and innovation in various types of firms, particularly in knowledge-intensive ones such as software and computing.

Nevertheless, despite its pertinence to entrepreneurship, there is hardly any research about the consequences of diversity in national culture among founders in NTVs. One exception is Chaganti et al. (2008), who examine the effect of immigrants in the top management team at the time of IPOs on the strategy and performance of Internet firms. They find a more aggressive prospector strategy in 26 ventures with at least one immigrant founder than the matched sample of 26 ventures without any immigrant founders. The study reports no significant impact on performance except when founding teams are comprised of relatively young members. However, when diversity is measured by immigrant intensity, meaning the proportion of immigrant members in the founding team, there is no impact on prospector strategy or the venture’s performance.

Founders’ Exit

The literature examines the key role of founders’ exit in the entrepreneurial process (e.g., Aldrich, 2015; Cumming, 2008; DeTienne, 2010; DeTienne et al., 2015; DeTienne & Wennberg, 2016; Wasserman, 2003). In particular, the extant research focuses on how and why founders leave their ventures. They may be forced to exit their poorly performing ventures (Laitinen, 1992; Wiklund et al., 2010) or even well-performing ones (Ewens & Marx, 2017; Wasserman, 2003). Alternatively, they may voluntarily choose to leave their poorly performing ventures to cut their losses (DeTienne et al., 2008; Gimeno et al., 1997; Thorburn, 2000), or even well-performing ones to harvest their investments in their ventures (Souitaris et al., 2020). As noted earlier, exits where founders choose to leave well-performing or high-potential ventures, which we investigate, are the most intriguing, but least studied scenarios.

Financial Harvest

The typical exit strategy in highly innovative, growth-oriented ventures, such as our NTV sample, is financial harvest (e.g., Cefis & Marsili, 2012; DeTienne et al., 2015). In this exit strategy, founders seek to recoup their investments, preferably with a high return. Once the venture’s performance allows for the greatest financial payback, founders can exit via an IPO or the sale of the venture to another company (Bayar & Chemmanur, 2011; Brau et al., 2003; Cumming, 2008; Poulsen & Stegemoller, 2008). Choosing this exit strategy enables founders to seek new investment opportunities and reinvest in new innovative ventures to redeploy their creativity. This is especially true for full exits where founders withdraw entirely from their ventures and are no longer involved in any manner with them (e.g., via holding a managerial or directorship position or retaining significant ownership of the company’s shares).

Founders’ Characteristics Associated with a Financial Harvest

Consistent with the notion of financial harvest, we would expect founders who choose this exit strategy to be motivated by financial reward. DeTienne et al. )2015) show that founders who regard their ventures as highly innovative and those using causation-based decision-making processes are more likely to develop a financial harvest exit strategy. Entrepreneurs who regard their ventures as highly innovative are willing to invest greater resources to maximize their payoffs, leading, in turn, to improved firm performance and ultimately high returns (e.g., Bates, 2005; Cohen, 2010; Samuelsson & Davidsson, 2009; Thornhill, 2006). A causation-based decision-making approach means starting “with the end in mind” (DeTienne et al., 2015, p. 262). Founders who favor this approach will use long-term planning and forecasting to maximize their profits (Sarasvathy, 2001).

Founders who choose financial harvest strategy are younger and better educated than those who use other exit methods (DeTienne et al., 2015; Levesque & Minniti, 2006). In addition, serial entrepreneurs are more likely than others to choose financial harvests because of their previous experience in selling their firms and because they are passionate about founding new ones (Cardon et al., 2009; Cotei & Farhat, 2018; Shu & Simmons, 2018). Finally, for IPO exits, Souitaris et al. (2020) show that the likelihood of the exit declines with the power of the founder in the venture at the time of the IPO (e.g., being the CEO, chairperson of the board of directors, inventor, or leading developer of the new product).

Development of the Hypothesis

Studies have demonstrated that diversity in national culture in a firm’s key positions increases its human and social capital. Such firms are more creative and innovative than their non-diverse counterparts (e.g., Blomkvist et al., 2017; Boone et al., 2019; Hambrick et al., 1998). There is further evidence of a significant positive relationship between such diversity in key positions (top management, the board of directors) and a firm’s value and performance (Carter et al., 2003; Erhardt et al., 2003; Nathan, 2016; Nathan & Lee, 2013; Nielsen & Nielsen, 2013). Based on the discussion above, greater innovativeness and improved financial performance are expected to be positively associated with the likelihood of developing a financial harvest exit strategy.

In addition, the personality traits of immigrant entrepreneurs documented in the literature, particularly the need for achievement (Kerr et al., 2018; Markman & Baron, 2003; McClelland, 1965; Vandor, 2021), are also expected to be positively associated with the likelihood of exiting via financial harvest. 6 Furthermore, the entrepreneurship literature indicates that immigrant entrepreneurs are more likely than their native-born counterparts to continually seek new growth options via new markets and new products (e.g., Chaganti et al., 2008). Note that many of them have indeed immigrated to seek new opportunities (e.g., De Haas, 2007; Sowell, 1994; Vogler & Rotte, 2000). As indicated, choosing a financial harvest exit strategy allows them to seek new investment opportunities and reinvest in new innovative ventures to redeploy their creativity.

The sociology literature suggests that differences in entrepreneurial activity can be explained by cultural factors (e.g., McClelland, 1961; Shane, 1992; Weber, 1904). Thomas and Mueller (2000) document that national culture heterogeneity (proxied by national culture distance from the United States) 7 is associated with a lower propensity for taking risks, less internal locus of control, and lower energy levels in entrepreneurship. A lower propensity for taking risks translates into entrepreneurs being less inclined to take financial and psychological risks and being less tolerant of ambiguity (e.g., Begley & Boyd, 1987; Bird, 1989; Brockhaus, 1982; Kets de Vries, 1977). Less internal locus of control signifies that the entrepreneurs feel they have less influence over the outcome of their new venture (e.g., Begley & Boyd, 1987; Brockhaus, 1982). Finally, lower energy levels indicate a lack of commitment to “working the long hours associated with the founding and management of new businesses” (Thomas & Mueller, 2000, p. 292; see also, e.g., Begley & Boyd, 1987). All of these factors—a low tolerance for risk and uncertainty about the future, both financially and psychologically, a reduced motivation to invest time and energy in the new venture, and feeling that one has little influence on its outcomes—indicate that founding teams whose members vary in their national culture would be inclined to exit and recoup their investments at the riskiest stage of their venture. This is particularly true for the case of NTVs, given the magnitude of the investment, lengthy time period, and riskiness and complexity of the R&D and marketing, all of which are greater in high-tech companies than in other sectors (e.g., Branscomb & Auerswald, 2001; Moore, 1999).

Consequently, we posit that:

Hypothesis: Diversity in national culture in NTVs’ founding teams is associated with a greater likelihood of founder exits via financial harvest.

Data and Methods

Sample and Data Sources

Our NTV data source is the Israel Venture Capital (IVC) Online database. IVC Online is a comprehensive database about Israel’s high-tech industries, created by the IVC Research Center. 8 Israel is suitable for an entrepreneurship study like ours because at 5% of Gross Domestic Product (GDP), it has the world’s highest R&D intensity, which is more than twice the OECD average of 2.4%, and substantially higher than the U.S. 2.8% average. 9 Furthermore, like other developed countries, Israel has a diverse population whose people vary a great deal in their national culture. While immigrants, in general, originate from various countries worldwide, 10 immigrant entrepreneurs in the technology sector in Israel are mostly (over 90%) from North America (Canada and the U.S.) and Europe (Western and Eastern). 11 Thus, this study is focused on them.

Our sample includes the list of NTVs founded in 2001 and thereafter, meaning those founded after the bursting of the tech bubble. We exclude NTVs operating during the tech bubble and its bursting from the sample because of the potential confounding effects of these anomalous periods in the technology sector on the performance of NTVs, their exit decisions, and the market for mergers and acquisitions (M&As). Given our focus on high-potential ventures, we also exclude NTVs classified by IVC as “suspended operations” or “ceased to operate.” Given our interest in diversity within a founding team, we also exclude one-founder NTVs. We then identified firms with founder exits via acquisition and those with exits via IPOs. Due to the small number of exits in the latter category (21 in the initial revenue stage and 63 in the revenue growth stage), 12 we focus our analysis on exits via acquisitions. Thus, we also exclude exits via IPOs from the sample. After dropping observations with missing data, our sample consists of 368 acquisition-based exits, including 299 NTVs in the initial revenue stage and 69 in the revenue growth stage.

The explanation for the prevalence of acquisitions in the initial, rather than growth, revenue stage lies in the technology adoption lifecycle. Due to the unique characteristics of the market for new technologies, they are first embraced by early adopters and then sold to mainstream markets consisting of large blocks of customers. Given their different attitudes toward innovative technologies, these two customer groups require different marketing strategies. 13 The inherent discontinuity in the transition from early adopters to mainstream customers presents risks in terms of the effectiveness of ongoing marketing efforts and the possibility of ultimately missing out on the larger market where the real profit is. The risk of falling into the “chasm” between the two groups is extremely high (Moore, 1999). Hence, founders with an exit strategy tend to harvest their investments in their ventures on the brink of the potential abyss. At this risky stage of the venture, it is more likely to find a buyer outside the stock market than to succeed in an IPO.

NTVs in the early market stage with a strong likelihood of reaching the mass market make enticing acquisition targets. The acquisition of the venture by another firm at this stage signals the NTV’s strong potential and, as indicated, it is perceived by founders as a vehicle to harvest their investments at the riskiest phase of their venture. Thus, the founders in our treatment sample chose to leave well-performing high-potential ventures, not ventures in which the likelihood of mass market success was just too low.

We focus on the 299 exits that took place in the early revenue stages. To create a control sample, we identified the NTVs in which the founders made the transition from early adopters to the mass market, gaining revenue growth without leaving the company. Thus, both groups include high-potential NTVs in the early adopters’ stage, one with and the other without founder exits. 14 Overall, our final sample consists of 582 high-potential NTVs that ultimately made the transition from early adopters to the mass market. In 299 of them (51%), the average (median) time of the founders’ harvesting of their investment in the early adopters’ stage is approximately 5.5 (5) years from the venture’s establishment. In the remaining 283 NTVs, the founders remained through the stages of the technology adoption lifecycle. In other words, they crossed the “chasm” on their own.

We retrieved the information about the variables for the empirical analyses detailed in the following section, including the biographical information on the founding team members, manually from IVC. 15 Sixty-five NTVs (11%) have at least one immigrant member on the founding team. The low prevalence of founding teams in our sample with members who vary in their national culture is consistent with the well-documented phenomenon of homophily—our desire to associate with those like us—in general (e.g., in marriages, friendships, and professional networks), 16 and in the formation of entrepreneurial teams in particular. The evidence indicates that ceteris paribus, entrepreneurs are more likely to team up with people with similar demographic characteristics, particularly with regard to culture and gender (Aldrich & Waldinger, 1990; Gompers et al., 2017; Ruef et al., 2003).

On average, diverse founding teams in our sample include three members, of whom 1.79 are immigrants. Immigrant founders come from Europe (54%) and North America (46%). The industries in our sample include information technology and enterprise software (36%), the Internet (27%), communications (19%), life sciences (7%), and miscellaneous technologies (11%). The distribution by industry is not significantly different in the exit versus continuation and the diverse versus homogeneous subsamples.

Methods and Variable Definitions

To analyze the relationship between diversity in national culture on founding teams and exits via acquisition, we use a combination of univariate tests and multivariate logistic exit regressions. Our tests account for all other factors from the literature potentially influencing a founder’s choice of a financial harvest exit strategy.

The exit choice (Exit) is represented by a binary variable equal to 1 if the founders chose to exit in the early market stage and 0 if the founders continued with their ventures and reached the mass market. We measured diversity in national culture on the founding team by the presence of immigrants as founding team members. Consistent with Chaganti et al. (2008), our main measure is an indicator of the presence of at least one immigrant as a founding team member (Diversity in National Culture). We extended the analysis using different indicators for different countries of origin of the immigrants based on Thomas and Mueller’s (2000) measures of difference in entrepreneurial activity across cultures. Furthermore, we repeated the analyses using two alternative measurements of the teams’ diversity in national culture from the literature (the percentage of immigrant members and Blau’s (1977) index of heterogeneity on the founding team) as a robustness test (see the Online Appendix).

To be categorized as an immigrant founder, we require that all of the following three conditions be met. The founder was born in a country other than Israel, has non-Israeli surname, and completed at least the undergraduate degree outside Israel. As per Chaganti et al. (2008), we expect that these combined conditions indicate that the immigrant founder spent his or her formative years outside the country where he or she founded the venture, and thus was not directly influenced by this country’s social, cultural, and economic context, at least until becoming an adult. 17

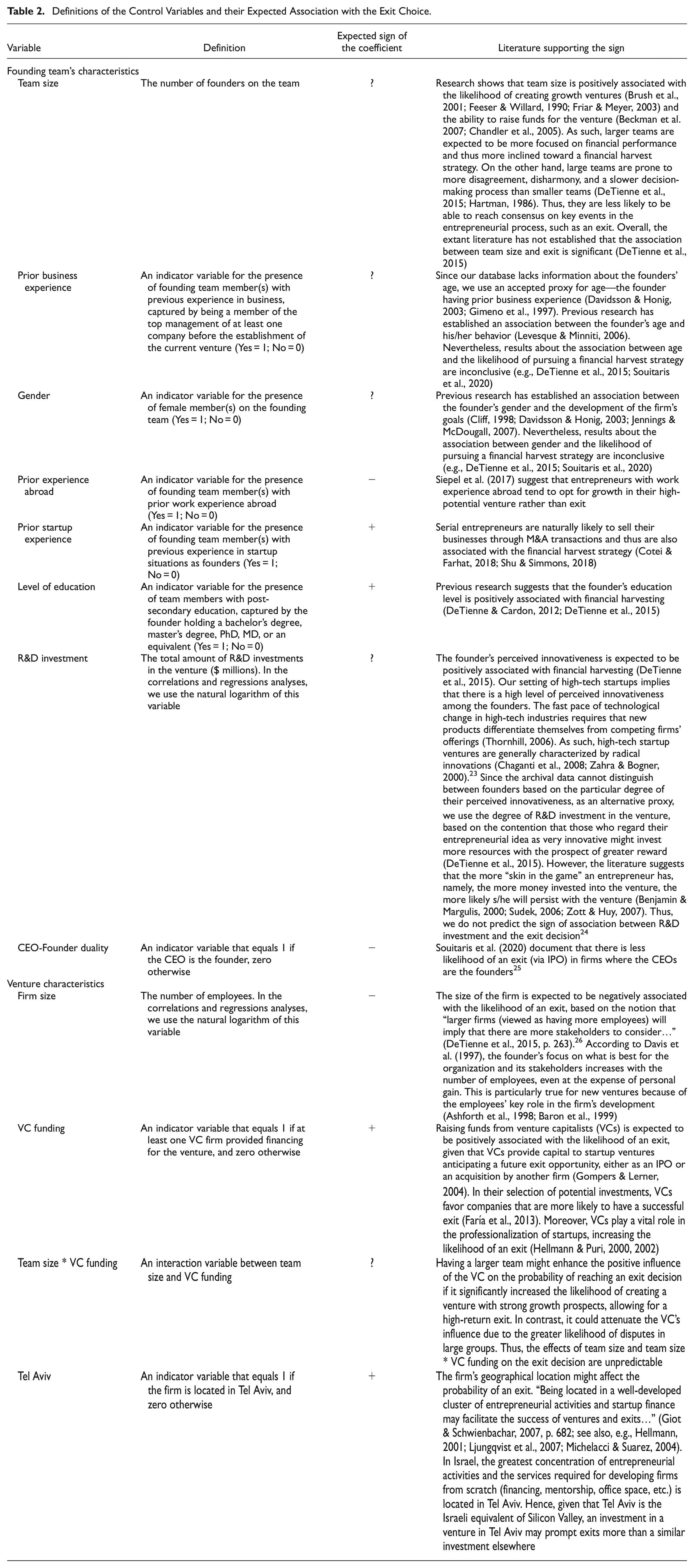

In the multivariate analyses, we control for the size of the founding team, the size of the firm, fundraising, geographical location, and the founders’ characteristics possibly affecting the exit decision. Table 2 describes the control variables and their expected association with the exit choice.

Definitions of the Control Variables and their Expected Association with the Exit Choice.

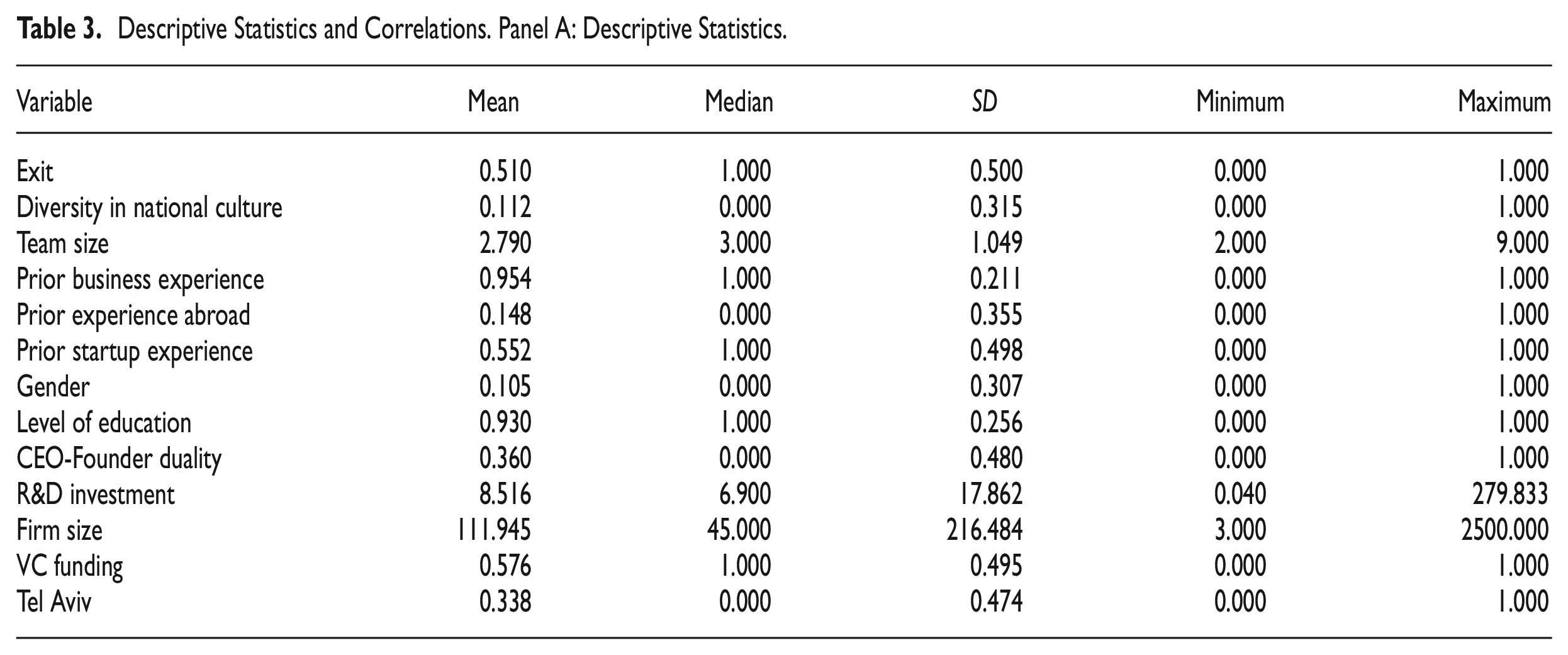

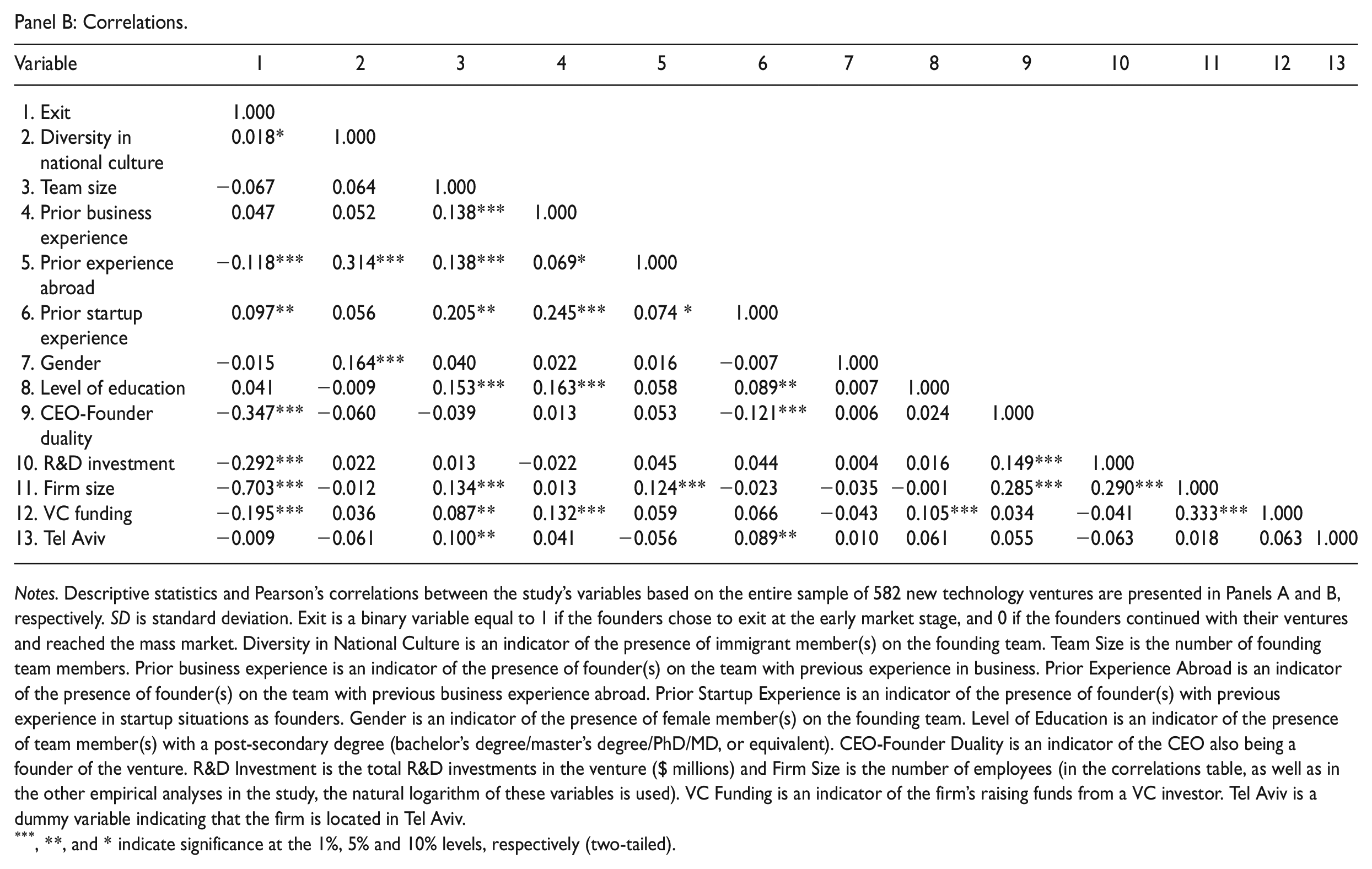

Table 3 provides the descriptive statistics (in Panel A) and univariate correlations (in Panel B) of the variables used in the study’s analyses. Exit is positively correlated with Diversity in National Culture (at the 10% significance level), consistent with our hypothesis. It is also positively correlated with Prior Startup Experience (at the 5% level) and negatively correlated with Prior Experience Abroad, CEO-Founder Duality, R&D Investment, Firm Size, and VC Funding (all at the 1% level). All of these associations are consistent with expectations based on previous literature except for VC funding. Nevertheless, in the multivariate analyses (Section 5 below), we observe a direct positive association, as expected, between VC funding and the decision to exit after controlling for the impact of other exit determinants. Finally, as Table 3 shows, the correlations among the independent variables are moderate to low, suggesting limited potential for distortions due to multicollinearity. In the Online Appendix to this study, we provide the results of additional univariate analyses comparing exit versus continuation and diverse versus non-diverse founding teams. In addition, the Online Appendix presents the results of robustness tests of the findings to different measurements of diversity. All of the results are consistent with our hypothesis and the univariate correlations in Table 3. In what follows, we examine the direct effects of diversity in national culture using various specifications of multivariate exit choice regressions.

Descriptive Statistics and Correlations. Panel A: Descriptive Statistics.

Notes. Descriptive statistics and Pearson’s correlations between the study’s variables based on the entire sample of 582 new technology ventures are presented in Panels A and B, respectively. SD is standard deviation. Exit is a binary variable equal to 1 if the founders chose to exit at the early market stage, and 0 if the founders continued with their ventures and reached the mass market. Diversity in National Culture is an indicator of the presence of immigrant member(s) on the founding team. Team Size is the number of founding team members. Prior business experience is an indicator of the presence of founder(s) on the team with previous experience in business. Prior Experience Abroad is an indicator of the presence of founder(s) on the team with previous business experience abroad. Prior Startup Experience is an indicator of the presence of founder(s) with previous experience in startup situations as founders. Gender is an indicator of the presence of female member(s) on the founding team. Level of Education is an indicator of the presence of team member(s) with a post-secondary degree (bachelor’s degree/master’s degree/PhD/MD, or equivalent). CEO-Founder Duality is an indicator of the CEO also being a founder of the venture. R&D Investment is the total R&D investments in the venture ($ millions) and Firm Size is the number of employees (in the correlations table, as well as in the other empirical analyses in the study, the natural logarithm of these variables is used). VC Funding is an indicator of the firm’s raising funds from a VC investor. Tel Aviv is a dummy variable indicating that the firm is located in Tel Aviv.

, **, and * indicate significance at the 1%, 5% and 10% levels, respectively (two-tailed).

Multivariate Analyses and Results

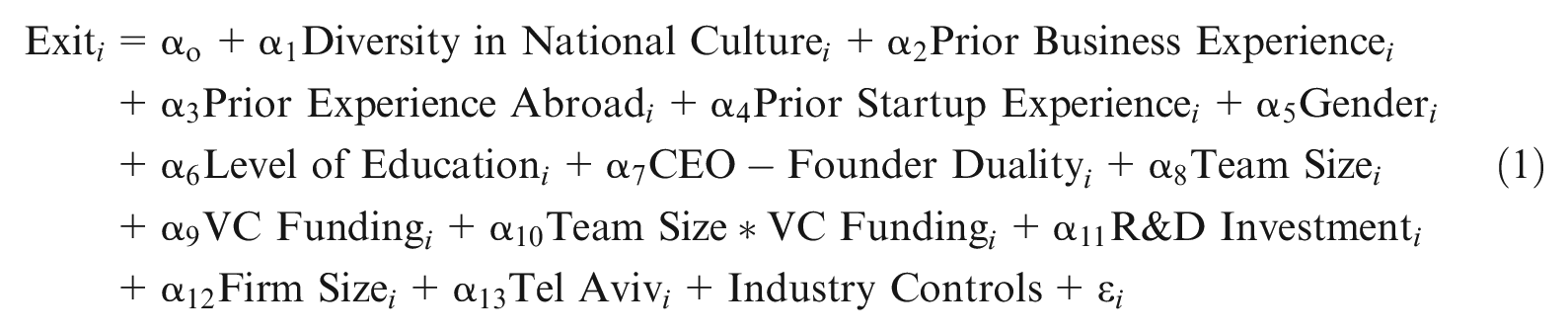

We run a logistic exit regression model on our diversity in national culture variable and the controls, with robust standard errors clustered by firm:

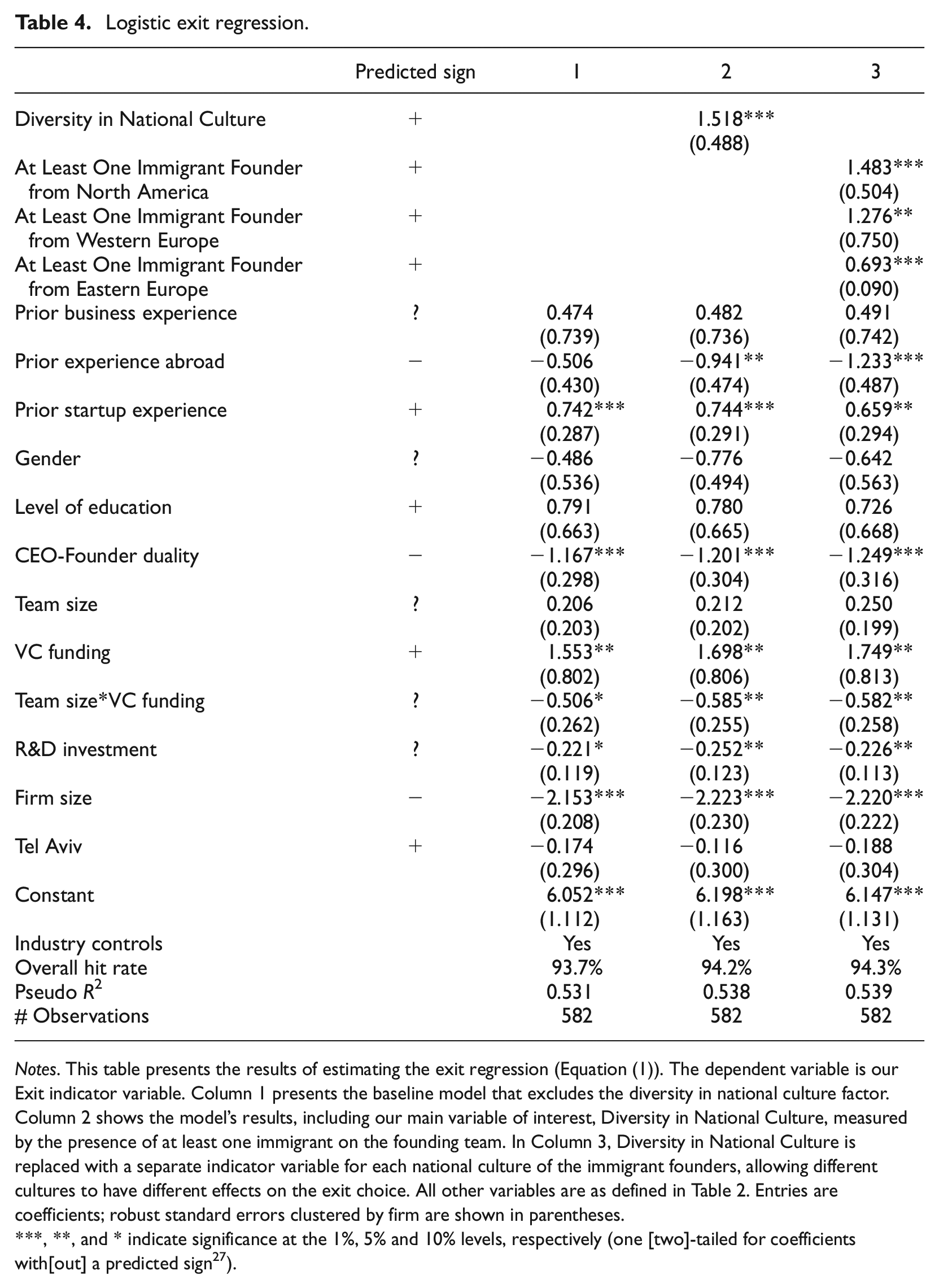

The model’s variables are as defined in section “Multivariate Analyses and Results.” In the regressions, we control for differences among industries by including industry dummy variables. The estimation results of Equation (1) are reported in Table 4. We first present the baseline model that excludes the diversity in national culture factor (Column 1 of Table 4). The model’s results, including our main variable of interest, Diversity in National Culture, appear in Column 2 of Table 4. The coefficient of Diversity in National Culture is highly significant and positive (1.518, p-value < 1%), demonstrating that the presence of at least one immigrant on the founding team significantly increases the likelihood of an exit. Notably, the magnitude of the impact of Diversity in National Culture on the probability of an exit is not trivial. Specifically, the results indicate that ceteris paribus, for teams with at least one immigrant founder, the odds of an exit are 4.6 times higher than that for teams with all-native founders. The sign and significance of the coefficients of the control variables are also consistent with expectations. In addition, compared to the baseline version, displayed in Column 1, the model’s specification improves when including the presence of at least one immigrant founder. 18

Logistic exit regression.

Notes. This table presents the results of estimating the exit regression (Equation (1)). The dependent variable is our Exit indicator variable. Column 1 presents the baseline model that excludes the diversity in national culture factor. Column 2 shows the model’s results, including our main variable of interest, Diversity in National Culture, measured by the presence of at least one immigrant on the founding team. In Column 3, Diversity in National Culture is replaced with a separate indicator variable for each national culture of the immigrant founders, allowing different cultures to have different effects on the exit choice. All other variables are as defined in Table 2. Entries are coefficients; robust standard errors clustered by firm are shown in parentheses.

, **, and * indicate significance at the 1%, 5% and 10% levels, respectively (one [two]-tailed for coefficients with[out] a predicted sign 27 ).

We repeated the analysis including a separate indicator variable for each national culture, allowing different cultures to have different effects on the exit choice. The results presented in Column 3 of Table 4 reveal that the effect size differs across the national cultures of the founders. Specifically, for teams with at least one North American and/or Western European and/or Eastern European immigrant founder, the odds of an exit are about 4.4, 3.6, and 2.0 times higher than that for teams with all-native founders, respectively. 19 As expected, the impact of entrepreneurs from Western Europe is closer to that of entrepreneurs from North American countries than that of those originating from countries within Eastern Europe. 20 This result is consistent with the importance of cultural versus geographical distance in our setting. Lastly, and importantly, the results are robust to alternative measurements of diversity (see the Online Appendix).

Discussion

Theoretical Contribution

Our study is a quasi-replication and an extension of Chaganti et al. (2008), the only research on the impact of immigrant entrepreneurs on the strategy and performance of NTVs. Chaganti et al. (2008) presented inconclusive evidence about the effects of the presence of immigrants in the top management team, which they refer to as the founding team “for the purposes of this paper” (p. 124). As such, one of the contributions of the current study is providing conclusive evidence about the effects of immigrant founders in NTVs using data on the actual founding teams rather than the top management team as a proxy. We show that, beyond other characteristics of the founders (such as their gender, their power in the venture, education, and prior experience) and the firm’s size, funding, and geographic location, the presence of immigrants on the team substantially increases the chances of an exit via a financial harvest.

Another contribution of this study is its extension of Chaganti et al.’s (2008) ideas to entrepreneurial exit decisions in NTVs. Exits represent a pivotal event in the entrepreneurial process that reflects the founders’ strategy and the ventures’ performance. The decision by founders to adopt a financial harvest strategy and voluntarily leave their currently well-performing ventures that have a great deal of future potential is most intriguing. Nevertheless, this type of exit decision is the least studied thus far. Uncovering a significantly positive association, as our paper does, between diversity in national culture among the founding teams’ members and their exits is critical. Moreover, given that financial harvest exits from high-potential technology startups entail substantial financial rewards, as indicated above, the economic implications, both at the micro and macro levels, of the diversity on the founding team are considerable.

In addition, we contribute to the literature by examining the generalizability of the results using a larger number of NTVs from different technology industries over an extended time period. Furthermore, we assess the robustness of the findings to different measurements of the study’s key variable. Indeed, the evidence documented in our empirical analyses about the effects of diversity among NTV founders on their exit decisions is substantial, even using various measures of diversity in national culture and differentiating between the countries of origin of the immigrants.

Limitations

Inevitably, our study suffers from some limitations. First, as a quasi-replication of Chaganti et al. (2008), our study differs from theirs in three regards. Table 1 presents the full comparison with Chaganti et al. (2008). The first is that our sample is based in Israel, as opposed to Chaganti et al. (2008), whose sample comes from the US. This difference might limit the generalizability of the findings. The fact that these NTVs also operate in markets outside of Israel, including the US, may help minimize this risk. Moreover, the fact that Israel is a leader in innovation potentially makes it an archetypal setting for our research.

Second, the immigrant founders in our study come from North America, Western Europe, and Eastern Europe, whereas in Chaganti et al. (2008) they come from Far Eastern Asia, Southeast Asia, South Asia, and South and Central America. Hence, whereas Chaganti et al. (2008) refer to the ethnicity of immigrant founders, we refer to diversity in national culture.

Third, we do not have the same dependent variable as Chaganti et al. (2008). We examine the effect of the presence of immigrant members on the founding teams’ financial harvest exit decisions. As indicated, such exits represent a pivotal event in the entrepreneurial process that reflects the strategy and performance of technology startups. In contrast, Chaganti et al. (2008) examined the immigrants’ effects on prospector strategy (proxied by the ratio of R&D and marketing expenses to total expense) and performance (proxied by annual growth rate in sales, assets, and employees).

Another limitation relates to the focus on financial harvest exits via acquisition only and, therefore, may not be generalizable to other exit forms such as IPOs. The literature, however, shows that financial harvesting through acquisition is a more universal exit channel in technology startups than an IPO and therefore, our study arguably addresses the vast majority of founder exits in the new technology entrepreneurship setting.

Lastly, we acknowledge the possibility of potential bias resulting from a self-selection problem. Self-selection in our setting would result if native-born founders who are more likely to exit their ventures choose non-native co-founders and vice versa. However, determining the exclusion criteria, and thus a viable instrument variable, is challenging, and the challenge is even greater in team self-selection. Indeed, we attempted to identify factors potentially affecting the choice of co-founders from different national cultures but that do not affect the exit decision. For example, the relevant literature on how entrepreneurs form ties and the formation of entrepreneurial teams indicates an inherent inclination to homophily and task considerations. 21 However, since these factors can affect the exit decision, they do not meet the exclusion criteria. 22

Conclusion

This study provides a quasi-replication of Chaganti et al.’s (2008) research by exploring the association between the diversity of national culture among the members of the founding teams and their financial harvest exit strategies in well-performing high-tech ventures. We compare Israeli NTVs in which the founders fully exited voluntarily in the early market phase and those where the founders continued with their ventures. Our analyses show that, ceteris paribus, diversity in national culture on the founding team substantially increases the chances of their exit. Our results have important implications for investors in NTVs, entrepreneurs who embark on a new venture, government policymakers, and, moreover, society at large.

The new evidence and insights from this study will hopefully prompt further research on this important topic. For example, future research can explore the behavioral, sociological, or psychological reasons behind our findings, which relate to entrepreneurship.

Future replications of our work could look at extending this study to other countries using NTVs outside of Israel. Another possible replication could explore how entrepreneurial personality traits such as the founders’ perceived innovativeness, internal locus of control, risk-taking propensity, and energy levels affect their exit decisions in addition to their national culture. Identifying these personal characteristics would require an alternative methodology such as a scenario-based survey study of entrepreneurs. Lastly, although the literature shows that financial harvesting through acquisition is a more universal exit channel in technology startups, our study addresses what is arguably the most common form of founder exits in NTVs. Nevertheless, future replications could look at other exit forms such as IPOs.

Supplemental Material

sj-docx-1-etp-10.1177_10422587231211006 – Supplemental material for Diversity in National Culture and Financial Harvest Exit Strategy in New Technology Ventures

Supplemental material, sj-docx-1-etp-10.1177_10422587231211006 for Diversity in National Culture and Financial Harvest Exit Strategy in New Technology Ventures by Ramy Elitzur, Ilanit Gavious and Orit Milo in Entrepreneurship Theory and Practice

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was supported by the Israel Science Foundation (grant No. 883/19), the Guilford Glazer Faculty of Business and Management at Ben-Gurion University, and the Rotman School of Management at the University of Toronto. All errors remain our responsibility.

Supplemental Material

Supplemental material for this article is available online.

Notes

Author Biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.