Abstract

Female entrepreneurs and CEOs generally face greater challenges in securing funding to exploit entrepreneurial opportunities, yet contextual factors under which such challenges are more likely to arise are less understood. We find that female-led initial public offerings (IPOs) incur greater IPO underpricing, but this effect is moderated by their ownership structure, reflecting different institutional logics in which these firms operate. Specifically, the positive relationship between female CEOs and IPO underpricing is attenuated by venture capitalist ownership, whereas such a relationship is exacerbated by state ownership. Based on a sample of 958 IPOs in China between 2009 and 2015, this study corroborates these findings.

Introduction

Securing funding is one of the most critical yet challenging activities for entrepreneurial firms (Hsu & Ziedonis, 2013; Parhankangas & Ehrlich, 2014). This challenge is particularly daunting for female entrepreneurs or CEOs, who tend to face bias from investors. Studies have consistently shown that female-led firms are less likely to raise funding to exploit entrepreneurial opportunities across multiple settings, including startup capital (e.g., Coleman & Robb, 2009), debt financing (e.g., Eddleston et al., 2016), crowdfunding (e.g., Wesemann & Wincent, 2021), and in experimental studies in a laboratory setting (e.g., Kanze et al., 2018).

One context where the existence of gender bias against female entrepreneurs or CEOs is contentious is the context of initial public offerings (IPOs). Specifically, IPO underpricing, or the difference between the price of newly issued shares and the closing price of those shares on the first day of trading (Ljungqvist, 2007), reflects money left on the table for the IPO firms and is considered as an important metric of IPO performance. This line of research has pointed out how various quality signals, such as reputable venture capitalists (VCs) (Lee & Wahal, 2004; Megginson & Weiss, 1991) or inventive capability through patents (Heeley et al., 2007), help firms reduce underpricing. However, an important yet under-explored factor that might determine IPO underpricing is the gender of the IPO firm’s CEO. Although female CEOs generally encounter gender bias from external resource providers and face greater difficulties in securing capital during the early stages of entrepreneurship (Becker-Blease & Sohl, 2007; Lee & Huang, 2018), the effect of CEO gender on IPO underpricing is equivocal (Bigelow et al., 2014; Mohan & Chen, 2004). On the one hand, public investors may exert similar gender bias on female-led IPOs and question a female CEO’s capability of leading a firm (Eagly & Karau, 2002). On the other hand, because the proportion of female-led ventures is relatively low (Guzman & Kacperczyk, 2019) and investors perceive that female-led ventures may have overcome greater hurdles in gaining support to grow their business, the success of a female CEO in bringing a venture to the IPO stage could serve as a positive signal of her exceptional managerial capability. Indeed, studies conducted using a U.S.-based IPO sample show that female-led firms do not incur greater IPO underpricing compared to their male-led counterparts (Mohan & Chen, 2004).

However, gender roles and how investors perceive female CEOs at IPO are likely to be highly culture- and context-specific. Indeed, the same information cue can be interpreted differently combining with different institutional logics. For instance, in emerging and transitioning economies such as China, market capitalist and state socialist logics co-exist influencing important managerial decisions and outcomes (Greve & Zhang, 2017; Zhou et al., 2017). In such situations, market participants tend to be cognizant of various cues relating to the dominant logic coming out of focal firms, yet the influence of CEO gender on IPO outcomes may need to be examined with other contextual factors that provide more complex and informative cues about the IPO firms.

To further understand how CEO gender may affect a firm’s IPO underpricing in another context, we examine the relationship between CEO gender and IPO underpricing by using a sample of 958 Chinese firms that went public between 2009 and 2015. Compared to female leaders in the United States, those in China are subject to greater gender-based stereotypes. For instance, female executives in China are perceived as more risk-averse and less confident (Zhang & Qu, 2016). The long-lasting prevalence of the male-dominated culture in China makes female-led IPOs vulnerable to the public’s assessment and gender biases. Gender stereotypes on female-led IPOs lead to more uncertainties about the true value of the IPO firm, which may in turn require a higher discount on the initial stock price to entice investors. As a result, we expect that there will be a positive relationship between the presence of female CEOs and IPO underpricing in China. However, investor evaluation of CEO gender could also be contingent on other contextual informational cues (Park & Patel, 2015; Payne et al., 2013; Vanacker et al., 2020; Vergne et al., 2018). Public investors may refer to a firm’s ownership structure to gauge its institutional logic (Greve & Zhang, 2017; Thornton et al., 2012) and interpret the influence of a female CEO in such a situation, thus attenuating or intensifying investor bias on female-led IPO firms. These institutional effects are prevalent in the Chinese context where the new market efficiency and old state socialist logics co-exist. Our empirical study finds that the gender bias on female-led IPO firms is attenuated when these firms are associated with the market efficiency logic reflected in greater VC ownership, whereas it is exacerbated when these firms are associated with state socialist logic reflected in greater state ownership. More profoundly, we bolster our finding that the differences in IPO underpricing between male- and female-led firms are driven by gender bias at the time of IPO rather than by inherent quality differences between the two types of firms, by showing that the long-run stock performance of female-led firms is not inferior to that of male-led firms.

This study makes several contributions to the entrepreneurship literature. First, it joins a growing stream of studies examining the contextualized effects on how multiple informational cues about entrepreneurial firms are evaluated by market participants (e.g., Park & Patel, 2015; Payne et al., 2013; Vanacker et al., 2020). These cues are particularly important for young firms because they have limited track record and in contexts where competing institutional logics co-exist. Because the audience (e.g., investors, prospective employees, and so on) are likely to examine the multitude of informational cues about young firms simultaneously and interpret them in conjunction with others, it is important to examine how these informational cues interact in a complex manner and influence their effectiveness. Our study extends this line of literature by adding that investors would have different interpretations of the same cue (i.e., CEO gender) when combined with different types of financial backers representing different institutional logics. Second, whereas prior research on gender bias has shown that female CEOs are disadvantaged in seeking approval from external resource providers (e.g., Becker-Blease & Sohl, 2007; Eddleston et al., 2016; Guzman & Kacperczyk, 2019), limited research has examined conditions under which certain contextual factors may exacerbate or attenuate such biases (Lee & Huang, 2018). Our results show that, although female-led firms are subject to gender bias, financial backing by VCs can attenuate such a bias because the market efficiency logic associated with VCs lends legitimacy to female CEOs. Third, this study contributes to the IPO underpricing literature. Most studies examining the effect of CEO gender on IPO underpricing were conducted using a U.S. sample and show mixed findings (Bigelow et al., 2014; Mohan & Chen, 2004). We extend this stream of research by conducting empirical research in the world’s largest emerging economy, China. Indeed, our study shows that gender bias in the context of IPO underpricing is greater in China, particularly when a firm is also in part state-owned. These findings contribute to the stream of research through insights about a different entrepreneurial finance market from a very different geo-political and economic context.

Theory and Hypotheses

IPO Underpricing

IPO underpricing denotes the difference between the opening price of newly issued shares and the closing price of those shares at the end of the first trading day (Ljungqvist, 2007), typically expressed as a percentage of the offering price. IPO firms prefer incurring lower underpricing because it reflects money left on the table for their proceeds. Although underwriters generally face an incentive to price the newly issued shares as high as possible to maximize their commission from the IPO, they also face high uncertainty on the demand for these shares ex-ante and might also be pressured to offer some discount to initial investors to maintain business relationships with them (Arthurs et al., 2008).

Studies have mostly applied arguments from information asymmetry and signaling theory to explain this complex and puzzling phenomenon. Unlike angel investors or VCs, public investors cannot conduct detailed due diligence on the IPO firms. Because underwriters cannot perfectly predict the demand for the newly issued shares, they often discount their price from the presumed fair market price based on the attributes of the IPO firms. Certain attributes of the IPO firms could serve as signals verifying their quality and thus attenuate the information asymmetry problem with external investors. In such cases, underwriters could offer the newly issued shares with lower discount and still ensure the sale of all shares. For instance, IPO firms backed by reputable VCs (Lee & Wahal, 2004; Megginson & Weiss, 1991) or prestigious underwriters (Carter et al., 1998), managed by capable top management teams (TMT) (Cohen & Dean, 2005), or in possession of a greater number of patents (Heeley et al., 2007) can reduce information asymmetry about their quality and thus incur lower IPO underpricing.

Female Entrepreneurship and Gender Bias

Female entrepreneurs generally face disadvantages in growing their ventures. One of the key reasons for the difficulties is gender bias and the unfavorable social stereotyping of female roles (Eagly & Karau, 2002; Eagly & Steffen, 1984; Guzman & Kacperczyk, 2019). In the early stage of their ventures, female entrepreneurs encounter greater difficulties in obtaining financial capital from resource providers because evaluators believe that the female gender role is mismatched with the professional role of an entrepreneur (Becker-Blease & Sohl, 2007; Carter et al., 1998; Lee & Huang, 2018). Because people stereotypically link the cultural image of entrepreneurship with masculine characteristics, the conventional view about female leaders being “risk-averse” and “less decisive” is counter to such an image leading to role incongruity and skepticism about female founders. The incongruence incurs investor biases of “lack of fit” when seeing women as occupants of the entrepreneur role, thus discounting the firm value.

Most studies on female entrepreneurship have documented the obstacles that women face in the early stage of venturing. However, only a limited number of studies have examined whether female-led ventures encounter similar gender inequity at the later stages of entrepreneurship, particularly when ventures move to the IPO stage. Going public puts firms under the spotlight, and they are now exposed to judgment from a large group of stakeholders such as regulatory authorities, the financial community, and institutional investors. Unlike evaluating early-stage ventures that lack objective information, investors can get access to more historical data and financial results about firm performance from the IPO prospectus. The disclosure of “hard” information about IPO firms may attenuate the role of CEO gender when investors evaluate the potential of the firm.

CEO and TMT characteristics influence investor judgment about the potential of an IPO firm (Certo et al., 2001; Cohen & Dean, 2005; Nelson, 2003). In this vein, research has examined the relationship between CEO gender and IPO evaluation. Comparing female-led IPOs with male-led IPOs in the U.S. stock market from 1990 to 2001, Mohan and Chen (2004) conclude that there is no difference between IPOs led by female and male CEOs when subjects share similar opportunity sets, wealth, and knowledge. However, one recent experimental study indicates that female CEOs are perceived as less capable compared to their male CEO counterparts, and female-led IPO firms are less attractive compared to male-led ones (Bigelow et al., 2014). These mixed findings call for more research on female-led IPOs. Moreover, contextual factors need to be taken into consideration to better disentangle the underlying mechanism between CEO gender and IPO underpricing.

Hypotheses Development

IPO is one of the most important events for entrepreneurial firms and challenging for top managers because these firms need to adapt by transitioning from private to public firms. Top managers confront new demands and multiple expectations from a large group of stakeholders after IPO. The challenging transition and increased visibility make managerial capability and the legitimacy of the firm the focal points of attention. Hence, executives’ prior managerial and industrial experience (Cohen & Dean, 2005), CEO’s founder status (Certo et al., 2001), and the reputation of top managers (Lester et al., 2006) become credible signals of managerial quality, which could reduce the information asymmetry and thus reduce IPO underpricing.

Gender is a stable and unambiguous ascriptive characteristic that is associated with social status and affects external evaluation (Baron et al. 1991; Rudman & Phelan, 2008). Public investors can readily get access to CEO gender demographics from the IPO prospectus. CEO gender is an important social categorization attribute and can directly affect investor perception of managerial capability. Therefore, it could influence their assessment of firm value. Whereas men are often associated with agentic characteristics and are portrayed as “aggressive,”“dominating,” and “assertive,” women are perceived as “sympathetic,”“gentle,” and “sensitive,” demonstrating more communal characteristics (Eagly, 1987; Malmström et al., 2017). The role of entrepreneurs has stereotypically been seen as masculine and is misaligned with the communal characteristics represented by women (Ahl, 2006; Eddleston et al., 2016). Role congruity theory also suggests that women are often evaluated less favorably when occupying a leadership role due to the misalignment between conventional gender norms and role expectations (Eagly & Karau, 2002). As such, female CEOs can be perceived as “lacking fit” or as being “less legitimate” to take the leader role because the cultural stereotype about women is associated with being “less aggressive, less risk-taking, and less competitive,” which is contrary to the typical image of a leader (Chen et al., 2016; Eagly & Karau, 2002). Therefore, it serves as an important informational cue for investors to evaluate an IPO firm. 1

The gender stereotype against females is likely to be particularly salient in China where the “male-oriented” culture is widespread, and legal protection for women is weaker compared to western countries (Burt, 2019; Organization for Economic Co-operation and Development [OECD], 2012). Although women accounted for 43.7% of the total labor force in 2019 (World Bank, 2019), only 9.7% of board directors in Chinese publicly listed firms were female (Global Gender Gap Report, 2020, p. 11). The significantly lower presence of female leaders is due to different social expectations of men and women. Whereas men are perceived as the primary family income earners, the social expectation of women is as the primary caregivers to the children and other members of the family. Inherently divergent role expectations become setbacks for women to advance their career. Even if women overcome gender biases and become leaders, the fact does not preclude post-appointment stereotypes (Nekhili et al., 2018), and pay disparity between female and male CEOs is common in China (Wang, Markóczy, et al., 2019). As a result, male-led IPOs are likely to be perceived as more legitimate whereas female-led IPOs may invite greater skepticism by investors in China.

In addition, gender stereotypes may negatively affect female-led IPOs in China because 90% of investors in the Chinese IPO market are individual investors who lack access to verifiable information and hold insufficient market knowledge (Yang et al., 2020). Instead of aiming for long-term, value-added investment, Chinese individual investors tend to invest with a short-term perspective and are more likely to engage in speculative trading to earn quick returns (Chang et al., 2008). The scarcity of means to collect reliable information coupled with an opportunistic investing habit makes individual investors rely on more visible and superficial information, such as CEO gender, to evaluate a new offering. Therefore, the bias against female leaders and the large number of individual investors increases information asymmetry between public investors and IPO firms. As a result, underwriters would be more likely to set the IPO price lower to entice the investors to buy the newly issued shares.

Hypothesis 1. Firms led by a female CEO will incur higher IPO underpricing compared to firms led by a male CEO.

IPO research has mostly applied signaling theory to analyze how IPO firms and underwriters set an initial price for newly issued stocks, and how investors evaluate these stocks (Connelly et al., 2011). However, a growing number of studies have adopted a more complex and holistic view contextualizing the effectiveness of multiple, concurrent cues influencing IPO outcomes (e.g., Drover et al., 2018; Eddleston et al., 2016; Park & Patel, 2015; Payne et al., 2013).

We examine the dynamics and complexity of the environment because recipients may take multiple, sometimes even contrasting, informational cues simultaneously to infer the attributes of a firm (Steigenberger & Wilhelm, 2018; Vergne et al., 2018). Institutional logics reflect a firm’s shared patterns of belief, underlying values and assumptions, and affect its ways of thinking and doing (Thornton & Ocasio, 1999). Therefore, when investors evaluate the value of female-led IPO firms, they would also consider the institutional logics behind those firms and gauge the influence of the CEO. In particular, we examine how the effects of different ownership structures before the IPO interact with the CEO gender and influence IPO underpricing.

The Moderating Role of VC Ownership

The presence of VCs certifies the value of an IPO firm, and therefore reduces IPO underpricing in the United States (Lee & Wahal, 2004; Megginson & Weiss, 1991). The certifying value of VC firms is multifold. First, the value-maximizing incentive makes VC firms be very selective in choosing their investees. As a result, only a small portion of high-quality ventures can obtain VC funding (Gomper & Lerner, 2004). Second, following an investment, VCs play both monitoring and nurturing roles by providing the necessary resources and ensuring the venture’s development at every milestone. Third, as market intermediaries, VCs can get access to comprehensive firm-specific information before IPO and are in a better position to judge the underlying quality of an entrepreneurial firm compared to public investors. In sum, VC funding is an important cue to certify a new venture’s underlying quality. Therefore, VC-backed IPOs are generally less underpriced compared with non-VC-backed IPOs (Megginson & Weiss, 1991).

Although Chinese public investors might be skeptical about the legitimacy of female-led IPOs, the funding from VCs may at least partially alleviate their concern. First, VCs are specialized in screening, monitoring, and nurturing ventures, and success in taking portfolio ventures public improves their reputation and enhances their ability to attract future funding (Jain & Kini, 2000). VCs represent the profit-driven, market efficiency logic that underscores the importance of efficiency and profit maximization. IPO failures, such as the delisting of the newly formed public firms that VCs endorsed, will damage their reputation and lead to subsequent penalties (Gomulya et al., 2019). Therefore, VC ownership in an IPO firm may signal that VCs deem the venture is qualified for being publicly listed. Although this endorsement from VCs lessens investors’ concern about the legitimacy of IPO firms in general, we argue that it is particularly important for female-led IPOs because approval from a reliable third party gives investors confidence about the credibility of female CEOs. VC ownership highlights the market efficiency logic embedded in a firm and underscores the qualifications of female CEOs as business leaders.

Second, VCs can also play an important role in negotiating with underwriters to set a higher offer price for female-led IPO firms. With the awareness that female-led IPOs are discounted, underwriters may intentionally set a lower price to mitigate risks and costs in case that they fail to find enough investors to buy the shares (Certo et al., 2001). However, the presence of VCs can lower such possibilities because VCs are experienced in communicating with underwriters about the offer price. To increase the value of stock holdings, VCs are incentivized to set a higher offer price, thus reducing the degree of underpricing for female-led IPO firms. In particular, VCs have stronger incentive to negotiate a higher price for firms in which they hold more ownership because their ownership is linked to the financial return that they will obtain once they exit the investment. The role of VCs in helping startups negotiate more favorable terms is particularly beneficial for firms led by female CEOs because women tend to be less aggressive in negotiating for favorable terms (Stuhlmacher & Walters, 1999).

Hypothesis 2. The positive effect of female CEOs on IPO underpricing will be weaker for firms with more VC ownership.

The Moderating Role of State Ownership

In addition to VC owners, state ownership is another type of common funding source that draws public investors’ attention in China, where the government exerts strong influence on the economy. State ownership represents one type of non-market logic, that is, state socialist logic, and emphasizes strong control of government over the economy and firm governance. Although state ownership may provide some resource benefits that could be exploited by IPO firms, state ownership in general provides limited benefits to a firm’s economic performance because state controls represent administrative rather than economic imperatives, and state-owned firms may prioritize political tasks ahead of profit maximization (Shleifer & Vishny, 1994; Zhou et al., 2017). The non-market-based logic of state-owned firms runs counter to shareholders’ value-enhancing expectations on their stock holdings.

We posit that state ownership further increases public investors’ skepticism about female-led IPO firms. First, state-owned firms tend to have a blurred governance structure, which means shareholders can only exercise limited control over firm decisions. Top managers in state-owned firms have dual roles, both as managers and politicians, and are often appointed by the government instead of the board of directors. Hence, shareholders of state-owned firms are only nominal owners who lack effective contractual and monitoring means to align the objectives of politicians, who are the major decision-makers of firms, with different incentives from those of other shareholders (Cuervo-Cazurra et al., 2014). The absence of effective governance mechanisms provides opportunities for politicians to use firm resources to fulfill administrative mandates, secure political support, and get promoted. Because female leaders are perceived as more submissive and risk-averse (Vial et al., 2016; Zhang & Qu, 2016), investors may believe that female CEOs will work in favor of government mandates and be less willing to protect shareholders’ interests. Therefore, state ownership may further reduce the credibility of female CEOs. Second, investors may also challenge a female CEO’s managerial capability of leading a state-owned firm. The dual responsibilities of state-owned managers require them to be competitive, confident, and even dominant so that they can handle complex tasks and be flexible to fulfill both market and governmental needs. However, women are perceived to manifest traits such as caring, gentleness, and a sympathetic attitude that are in contrast to the image of competitiveness and risk-taking (Heilman & Okimoto, 2007). The perceptions of women being less fit for leading state-owned firms exacerbate investor biases toward female-led IPO firms. We suggest that higher state ownership will lead to a stronger positive relationship between female CEO and IPO underpricing, because investors could expect greater influence by the state on the firm’s managerial decisions in such cases. Taken together, although female CEOs do not increase the resource benefits of state ownership for newly formed public firms, their presence may lead to greater information asymmetry concerns for the newly formed public firms with more state ownership. As a result, we suggest that the positive relationship between female CEOs and IPO underpricing will be exacerbated for IPO firms with more state ownership.

Hypothesis 3. The positive effect of female CEOs on IPO underpricing will be stronger for firms with more state ownership.

Methods

Data and Sample

We draw our sample from Chinese IPO firms listed on the Small and Medium Enterprise (SME) and ChiNext boards of the Shenzhen Stock Exchange between 2009 and 2015. 2 As the largest transition and emerging economy, China provides a thriving IPO market for small businesses to seek public capital. In spite of significant developments in the past three decades, the regulations and disclosure requirements of the Chinese IPO market are still under development (Wang, Wan, et al., 2019), and the public often holds limited information on IPO firms. In particular, the information asymmetry between the public investors and IPO firms is more pronounced for firms listed on the SME and ChiNext boards, where most firms are in the growth phase of their lifecycle, as opposed to more mature firms on the main board. Firms on the SME board are characterized by fast revenue growth, strong profitability, and technology intensiveness. Conversely, although ChiNext was designed to provide financing channels and growth space for entrepreneurial firms that were not eligible to be listed on the main and SME boards, the board has predominantly technology firms that are young and small, but with high potential for future growth. The SME and ChiNext boards were launched in June 2004 and October 2009 respectively. By December 31, 2015, the total market capitalizations of the two boards were 10.24 trillion Renminbi (RMB) and 5.40 trillion RMB respectively. In such a context, CEO characteristics and firm ownership structure may serve as salient informational cues for the public investors to infer firm quality. Because one of our key hypotheses is that VC financing mitigates the positive effect of female CEO gender effect on IPO underpricing, it is important to obtain a sample of firms whose backers include VCs. Firms that are listed on the SME and ChiNext boards tend to receive more VC funding compared to established firms listed on the main board. As of December 31, 2015, there were 41.02% (315 out of 768) of listed firms on the SME board that were VC-backed at the time of IPO, and 60.82% (295 out of 485) on ChiNext, compared to 0.64% (3 out of 469) and 13.28% (140 out of 1054) on the main board of Shenzhen Stock Exchange and Shanghai Stock Exchange respectively. In terms of state ownership, there were 9.77% (75 out of 768) of listed firms on the SME board that were majority state-owned at the time of IPO, 1.65% (8 out of 485) on ChiNext, compared to 63.54% (298 out of 469) and 56.07% (591 out of 1054) on the main board of Shenzhen Stock Exchange and Shanghai Stock Exchange respectively. The proportion of female CEOs in our raw sample was 7.83% (75 out of 958).

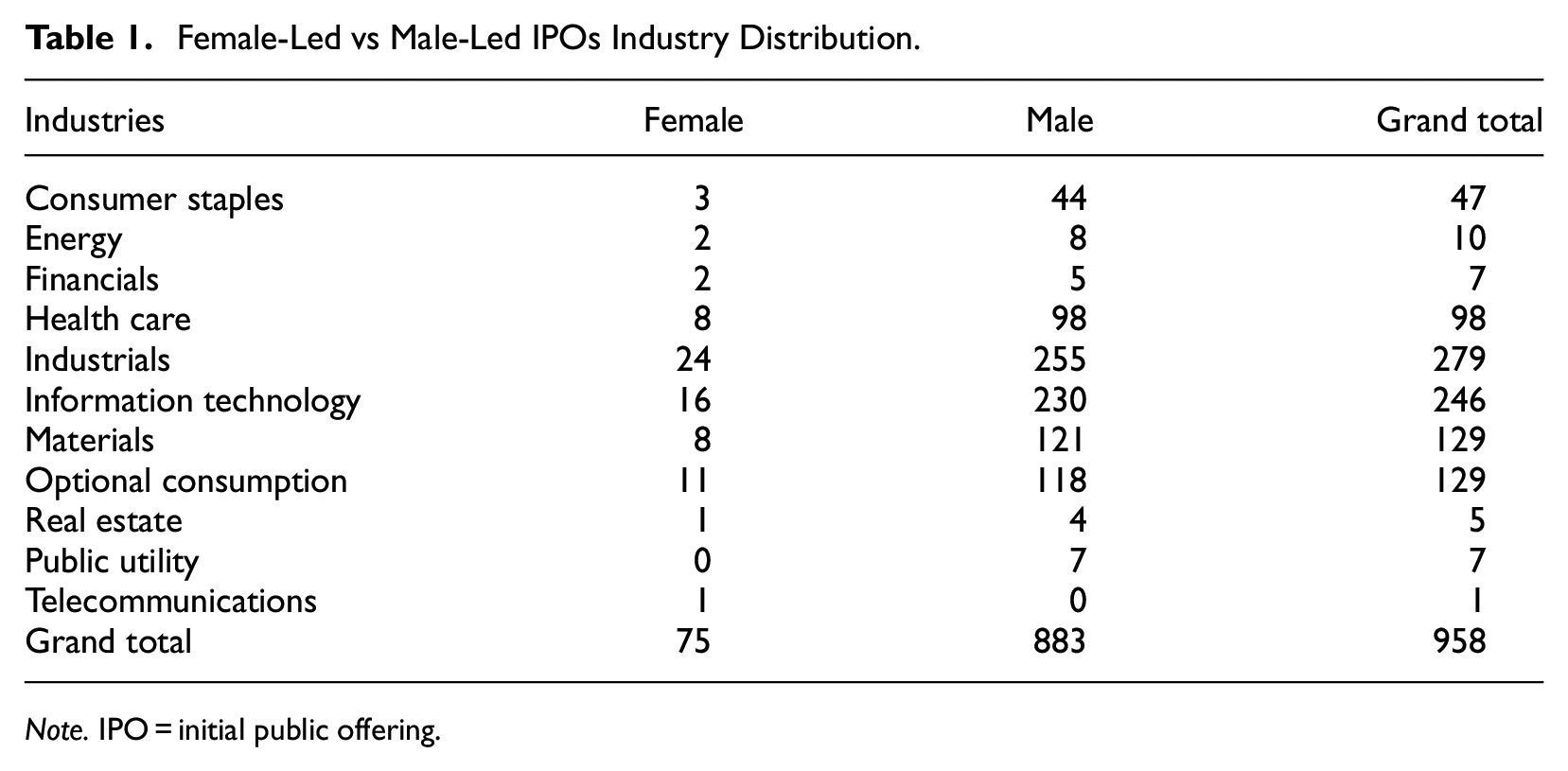

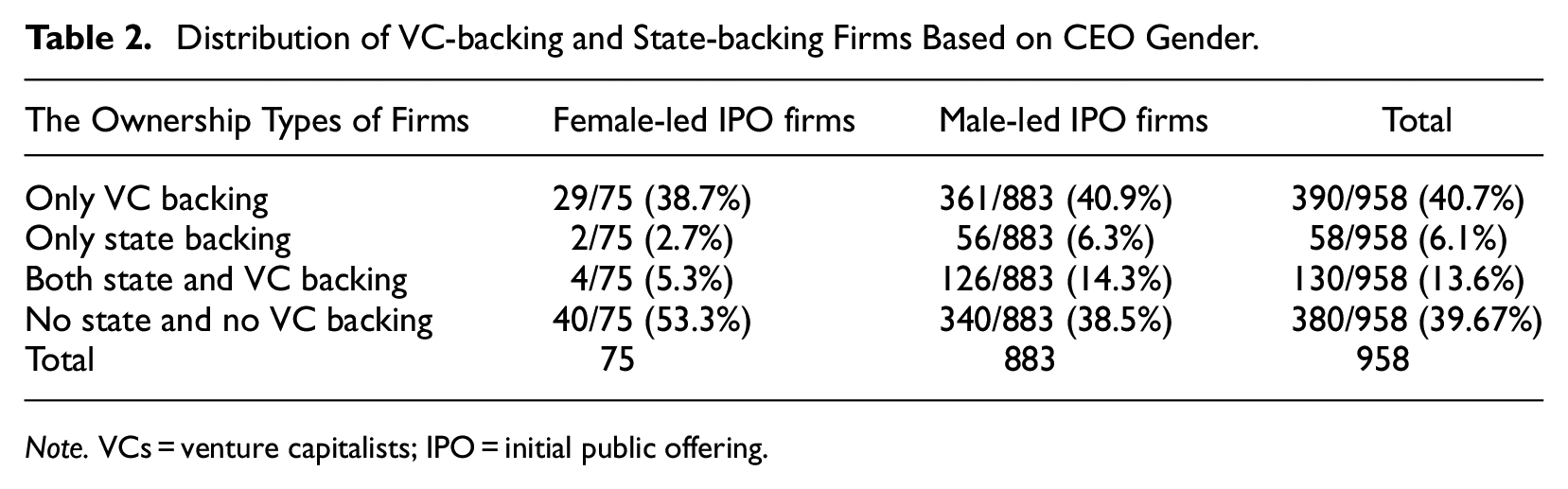

To assess whether firms led by female CEOs were qualitatively different from firms led by male CEOs, we ran T-tests based on key attributes by both groups of firms. The results indicate that firms led by female CEOs are not statistically different from those led by male CEOs in terms of return on assets (ROA) (p = .92), leverage ratio (p = .35), IPO proceeds (p = .34), and firm age (p = .68). We also drew a table based on female versus male-led IPOs’ industry distribution in Table 1. We did not find significant industrial differences between female-led and male-led IPO firms. We also present the percentage distribution of VC-backed firms and state-backed firms based on CEO gender of our sample and summarize the information in Table 2.

Female-Led vs Male-Led IPOs Industry Distribution.

Note. IPO = initial public offering.

Distribution of VC-backing and State-backing Firms Based on CEO Gender.

Note. VCs = venture capitalists; IPO = initial public offering.

We derived IPO firm listing and subsequent financial information from the WIND data set, which provides basic information of Chinese publicly listed firms (Zhang & Qu, 2016). Information on CEO characteristics and board composition were collected from China Stock Market and Accounting Research (CSMAR), which has been widely used in prior studies on China (e.g., Miller et al., 2008; Wang & Qian, 2011). In addition, we obtained VC and underwriter information from CVsource, a leading VC data provider of VC firms and their investments in China (Zhang & Gu, 2021). The data from the three different sources were matched by the unique stock code that was associated with each listing firm.

Dependent Variable

IPO underpricing is measured by the percentage difference between the offering price and the first-day closing price (Ljungqvist, 2007; Ritter, 1991). The higher the difference, the more capital the firm has “left on the table.” This difference also represents a larger information asymmetry between IPO firms and the public (Arthurs et al., 2008).

Theoretical Variables

Our main explanatory variable, CEO gender, is measured using a dichotomous measure. We code “female CEO” as 1 if the IPO firm had a female CEO when it went public. We use the percentage of ownership to capture the ownership structure of a listed firm. If the firm has received VC investment prior to IPO, we use the total percentage of ownership of VCs to indicate “VC ownership.” 520 out of 958 (54.3%) firms received VC funds before IPO. We coded State ownership as the percentage of ownership in a listed firm by any government or government agencies in China. 187 out of 958 (19.5%) firms had state ownership.

Control Variables

We inserted three sets of control variables, based on the literature, that could affect IPO underpricing in our empirical analysis. First, we controlled for several IPO-related variables, including (1) IPO proceeds, which indicates the amount of money raised in the IPO. Proceeds are measured as the natural logarithm of the number of shares offered in the IPO multiplied by the offering price. IPO proceeds reflect the scale/size of the IPO; (2) IPO price-earnings ratio (PE ratio) that is obtained by dividing the IPO price by the earnings per share in the year prior to the IPO. This variable is a proxy for firms’ future growth prospects; (3) Underwriter reputation. Because prior studies have shown the prestige of underwriters will affect IPO performance (Beatty & Ritter, 1986; Velamuri & Liu, 2017), we included underwriter reputation as a control variable. We used the amount of total IPO proceeds underwritten by an investment bank in the past 5 years (including the current IPO year) divided by total IPO proceeds in China in the past 5 years to capture underwriter reputation. Second, we controlled for a group of CEO and board characteristics that may influence corporate governance and investors’ evaluation of IPO firms: (4) board size is the total number of members on the board; (5) board independent director ratio is the percentage of independent directors on the board; and (6) the percentage of female directors (one recent study shows that board gender diversity is positively associated with IPO underpricing (Rau et al., 2022). We thus included the percentage of female directors; (7) the percentage of female executives. Likewise, we controlled for the percentage of female executives in TMT; (8) CEO duality is an indicator of whether the CEO also serves as chairman of the board; (9) CEO education level is coded as a dichotomous variable. If a CEO holds a bachelor’s degree or above, we coded it as “1”, otherwise “0”; (10) CEO founder status. Research has shown that CEO founder status is likely to increase information asymmetry and thus IPO underpricing (Certo et al., 2001). We inserted a dummy variable to indicate whether a CEO is also a founder or not; (11) CEO age. Public investors may value older CEOs more than younger CEOs with the assumption that older CEOs possess more experience and greater maturity; (12) CEO tenure. CEOs with short tenures hold less managerial experience with a specific firm and this may be positively related to IPO underpricing (Cohen & Dean, 2005). Finally, we included a group of firm characteristics that may also influence IPO underpricing: (13) ROA is the operating income as a percentage of total assets during the reporting period; (14) leverage ratio is obtained by dividing total liabilities by total assets and reflects firm risk; (15) firm age is included to control for firms’ liability of newness; (16) firm size is measured as the log number of total employees. In addition, we included year and industry fixed effects and (17) a binary indicator for which stock board the firm chose to list on, that is, SME or ChiNext, in our analysis.

Empirical Methods

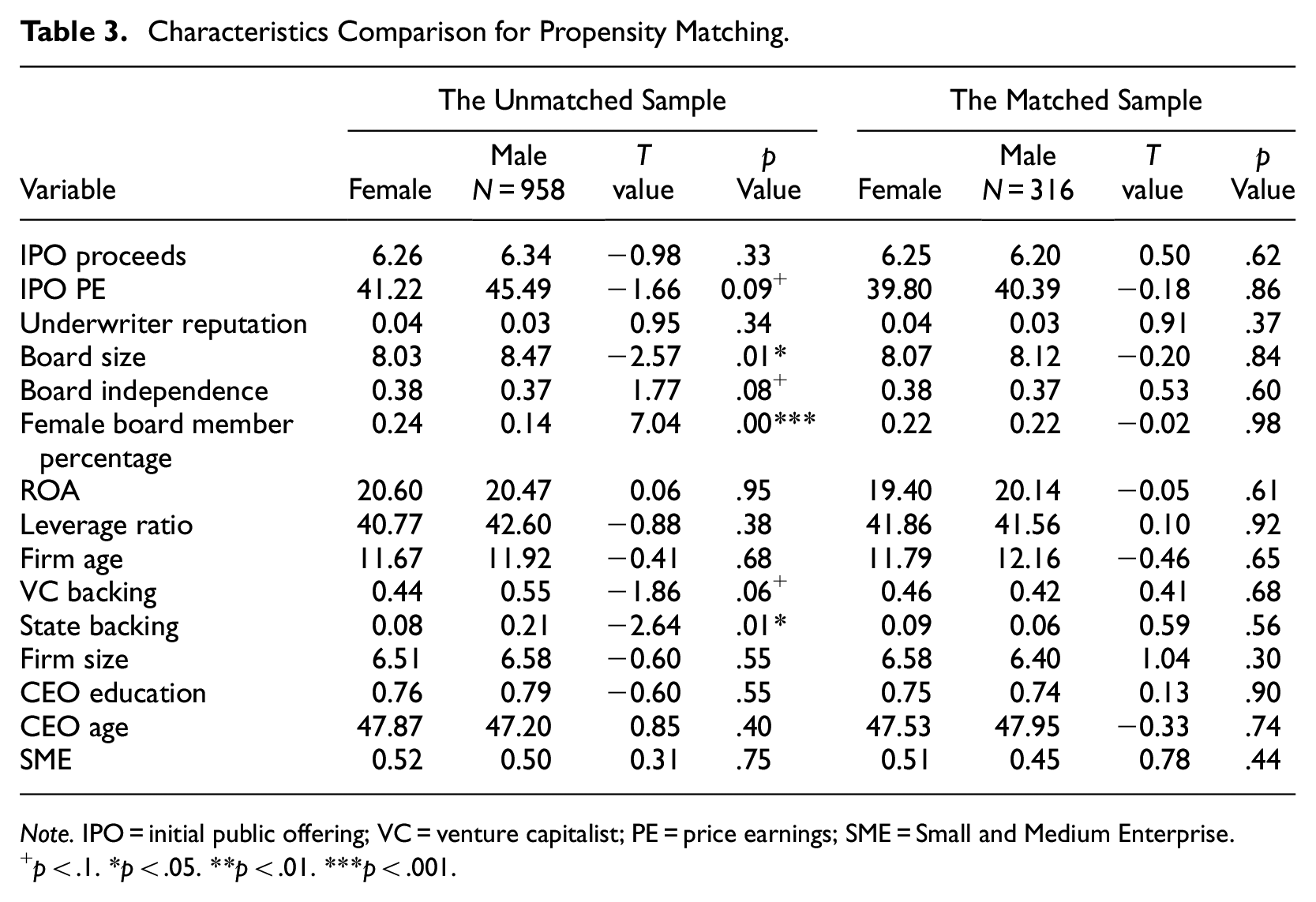

Because there might be differences in the characteristics between firms led by male and female CEOs, our results might be vulnerable to endogeneity. To alleviate such a concern, we created matched samples of firms by using nearest-neighbor propensity score matching (PSM) technique (Blevins et al., 2019; Sun & Zou, 2021). First, we used systematic factors to predict the likelihood of a female CEO leading an IPO firm. This selection model is based on our full sample and considers both firm and CEO characteristics. We matched groups (i.e., male- or female-led IPO firms) on the following variables: IPO proceeds (the size of IPO), IPO PE ratio (firm’s gr), underwriter reputation, the size and independence of Board, the percentage of female directors, ROA, leverage ratio, firm age, firm size, VC backing or not, state backing or not, CEO education, CEO age, SME or not, and we also inserted year and industry fixed effects to account for time trends and industry environment trends. Because of the cross-sectional nature and the small number of female-led IPOs (7.83%) of our sample, we applied probit regression to create propensity scores and used these propensity scores to match every female-led firm with five male-led firms with the closest propensity score, 3 only if the propensity score differed by 0.05 or less (Sun & Zou, 2021). We were able to find 243 male-led IPO firms that were matched with 73 female-led IPO firms in our sample. For each female-led IPO, there were 3.32 paired male-led IPOs in our sample on average.

Before we used the matched sample created by PSM to run the ordinary least squares (OLS) regression, we examined whether the matching procedure effectively reduced the differences of observable characteristics between treatment and control groups. To ensure good quality of matching sample, we ran balancing diagnostics, that is, individual t-tests, to examine whether treatment firms (female-led IPOs) differed from control firms (male-led IPOs) along the matching criteria. We present the comparison between female versus male-led IPOs in Table 3. The results suggest that the comparisons between treatment and control firms after matching are not statistically significant (p > 0.05).

Characteristics Comparison for Propensity Matching.

Note. IPO = initial public offering; VC = venture capitalist; PE = price earnings; SME = Small and Medium Enterprise.

p < .1. *p < .05. **p < .01. ***p < .001.

Results

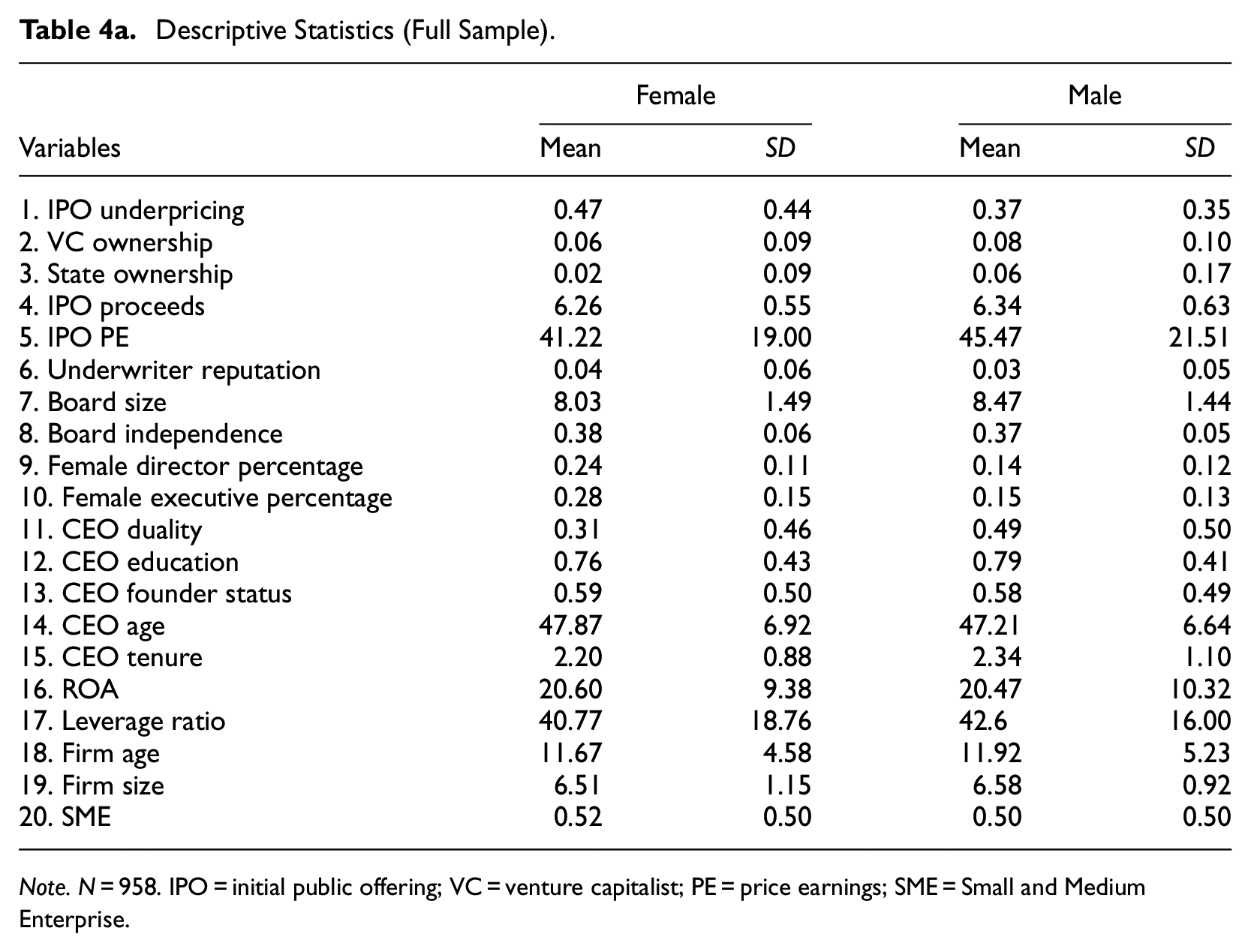

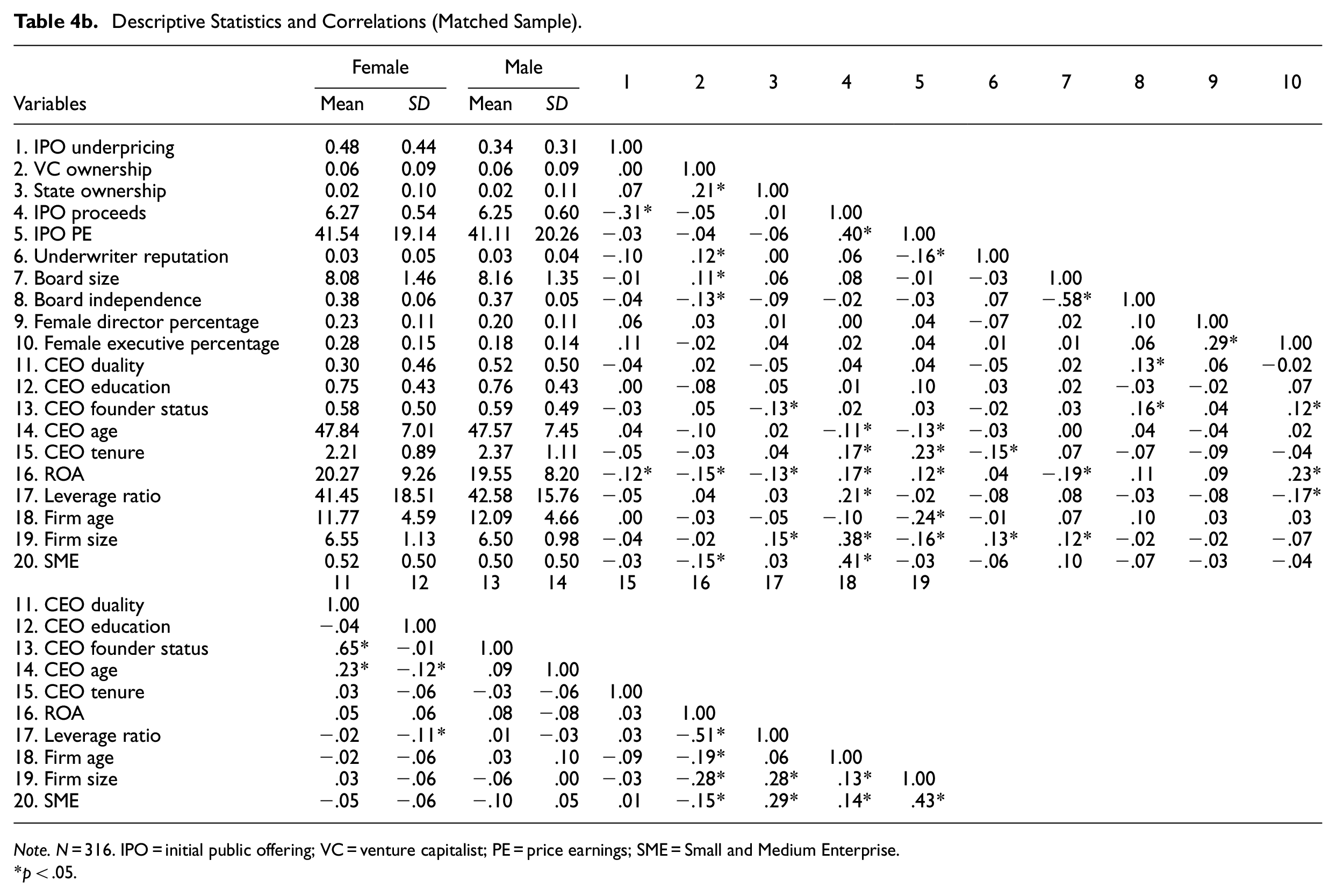

We tested our hypotheses by applying OLS regression analysis on the matched sample because the data structure of IPO is in cross-sectional format. This method has also been widely used in prior IPO literature (e.g., Sundaramurthy et al., 2014). Although we used the matched sample to run the regression, we report the descriptive statistics and correlations among variables using the full dataset. The descriptive statistics of female-led versus male-led IPOs are reported in Table 4a. We observe some differences between female-led versus male-led firms. Consistent with our main prediction, the average IPO underpricing of female-led firms is 0.47 whereas the mean value of male-led firms is 0.37. Firms led by male CEOs on average are more profitable, larger, and more financially risk-taking than firms led by female CEOs. In contrast, female-led IPOs have more female board directors and top executives compared to male-led IPOs. Table 4b reports descriptive statistics and bivariate correlation results for the matched sample.

Descriptive Statistics (Full Sample).

Note. N = 958. IPO = initial public offering; VC = venture capitalist; PE = price earnings; SME = Small and Medium Enterprise.

Descriptive Statistics and Correlations (Matched Sample).

Note. N = 316. IPO = initial public offering; VC = venture capitalist; PE = price earnings; SME = Small and Medium Enterprise.

p < .05.

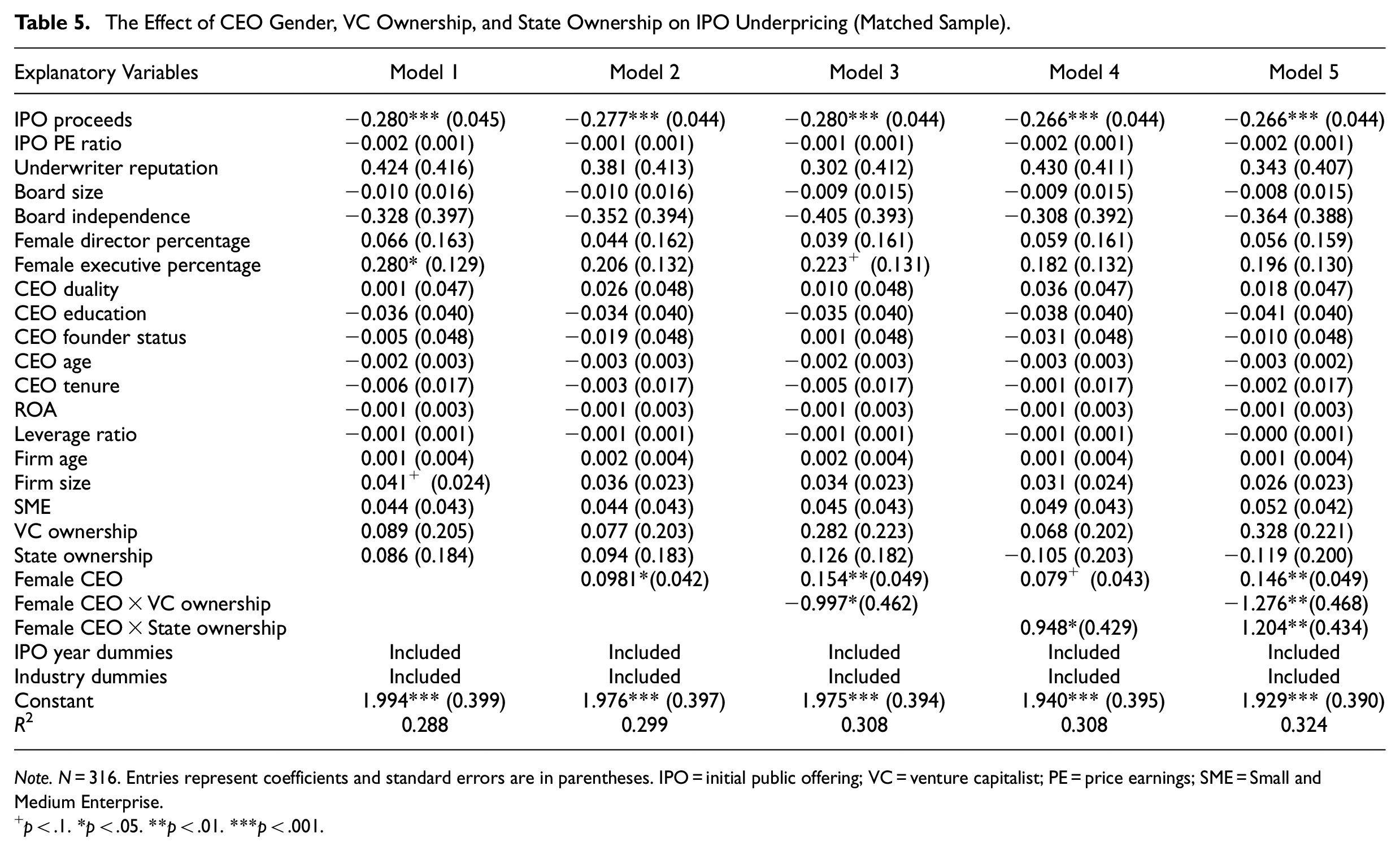

We do not observe any multicollinearity concerns with the sample. The correlation between “CEO founder status” and “CEO duality” is equal to 0.65. We conduct Variance Inflation Factor (VIF) test on matched sample and the mean VIF score is 1.49, which is well below the conventionally acceptable level of 10 (Freund & Littell, 1991). The main results of the regression analyses on the matched sample are reported in Table 5. Model 1 includes all control variables only. The independent variable is added to Model 2. Model 3 and Model 4 add the two moderating variables and interaction terms separately. Model 6 is the full model which includes the main effect and two interaction effects.

The Effect of CEO Gender, VC Ownership, and State Ownership on IPO Underpricing (Matched Sample).

Note. N = 316. Entries represent coefficients and standard errors are in parentheses. IPO = initial public offering; VC = venture capitalist; PE = price earnings; SME = Small and Medium Enterprise.

p < .1. *p < .05. **p < .01. ***p < .001.

Hypothesis 1 predicted that female CEO gender would be positively related to IPO underpricing. We found this effect is statically significant across all the models. Model 5 provides support for this hypothesis (β = .146, p < .01). Holding other variables constant, compared to male-led IPOs, female-led IPOs in China are underpriced by 14.6%. Hypothetically, if one firm led by a male CEO set 100 RMB per share as its initial stock price, and the closing price at the end of the first day is 120 RMB, the underpricing level of this stock would be 20%. Our result suggests that the closing price on the first day of the same firm led by a female CEO would be 134.46 RMB, suggesting that female-led IPOs would have left more money on the table.

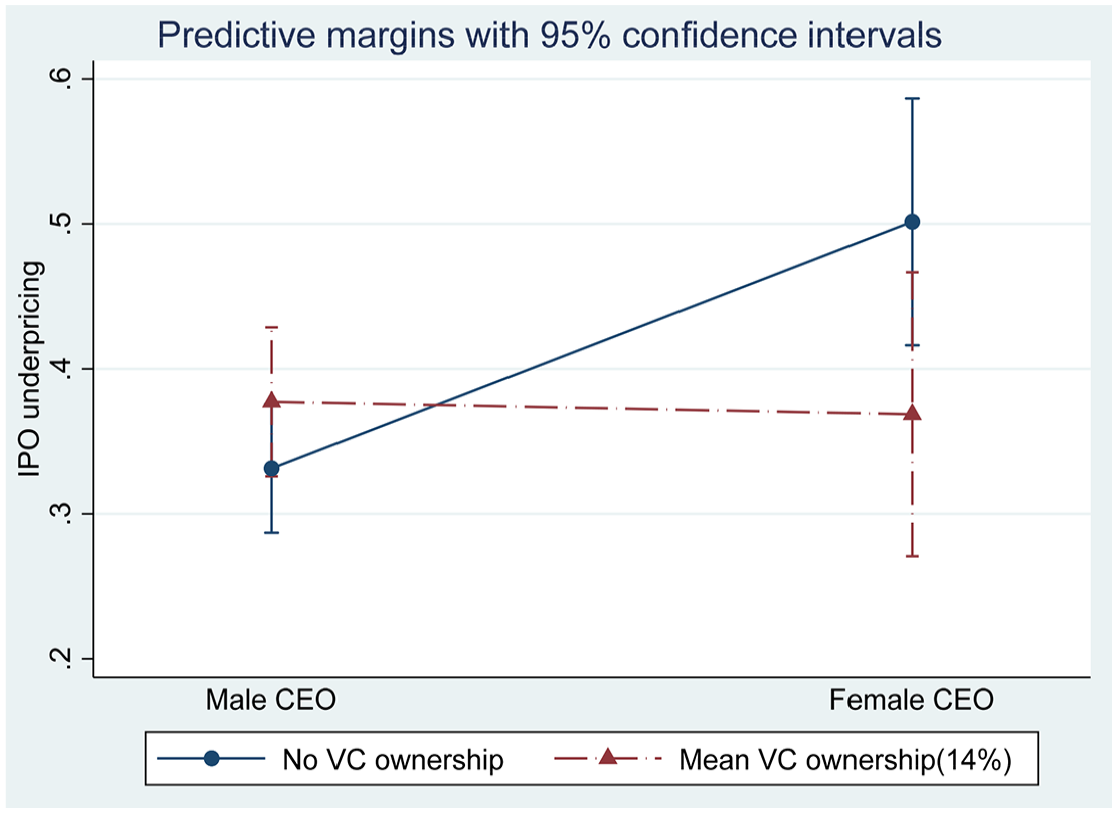

Hypothesis 2 posited that VC ownership would weaken the positive relationship of female CEO gender on IPO underpricing. We found support for this hypothesis in Model 5 as the interaction term between VC funding and female CEO gender is statistically significant (β = −1.276, p < .05). This means that, whereas female-led IPOs are underpriced by 14.6% compared to male-led IPOs, every 10% increase of VC ownership of female-led IPOs would reduce the underpricing level by 12.8%. Taking the previous example, if that same female-led firm held 10% VC ownership, its first day closing price would be 121.8 RMB. We plot this interaction effect in Figure 1. When a firm is not VC-backed, the plot shows that firms led by female CEOs incur much greater IPO underpricing compared to those firms led by male CEOs. In contrast, when VC ownership reaches a mean value (14%) conditional on receiving VC funding, firms led by female CEOs incur lower IPO underpricing compared to those led by male CEOs.

Interaction of female CEO and VC ownership.

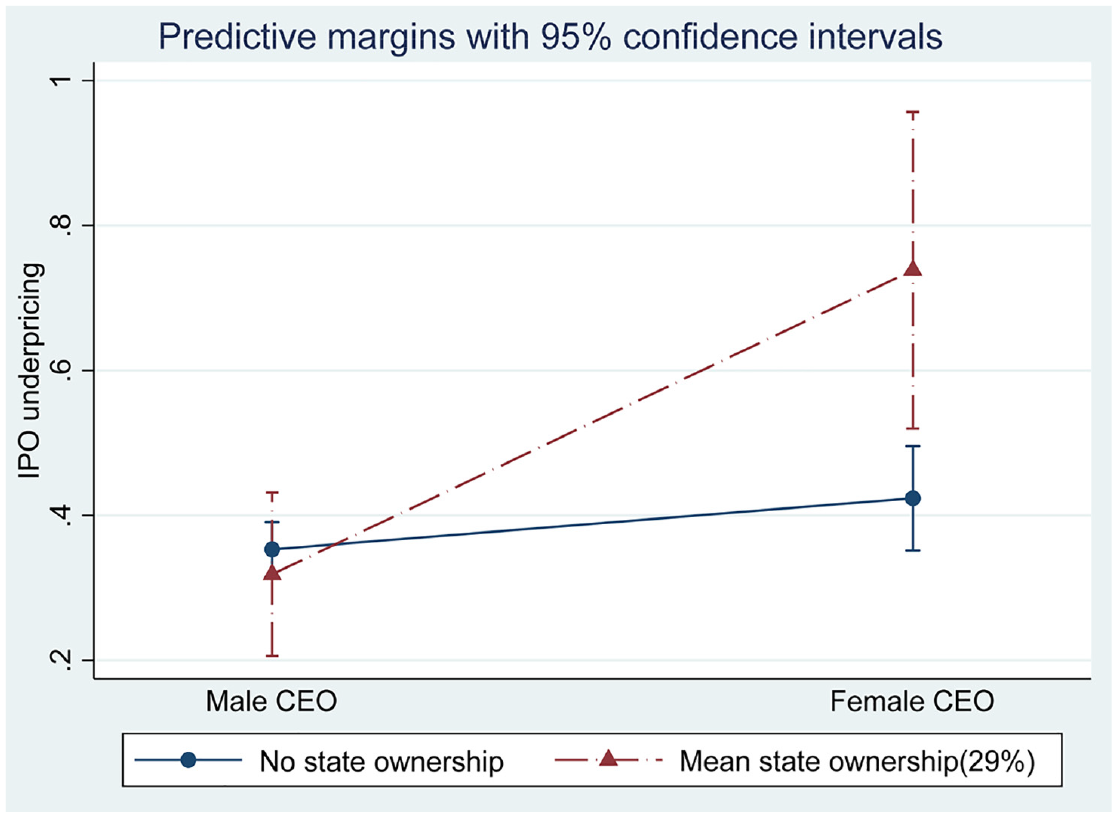

Hypothesis 3 predicted that state ownership would strengthen the positive relationship of female CEO gender on IPO underpricing. This hypothesis is also supported in Model 5 (β = 1.204, p < .05). This effect suggests that female-led IPOs with 10% state ownership will incur 12% more underpricing compared to female-led IPOs without state ownership. Likewise, the female-led firm of our previous example with 10% state ownership would have a closing price of 146.46 RMB. The interaction effect of state ownership is plotted in Figure 2. As the figure shows, the degree of female-led IPO underpricing is more pronounced with state ownership.

Interaction of female CEO and state ownership.

Robustness Tests

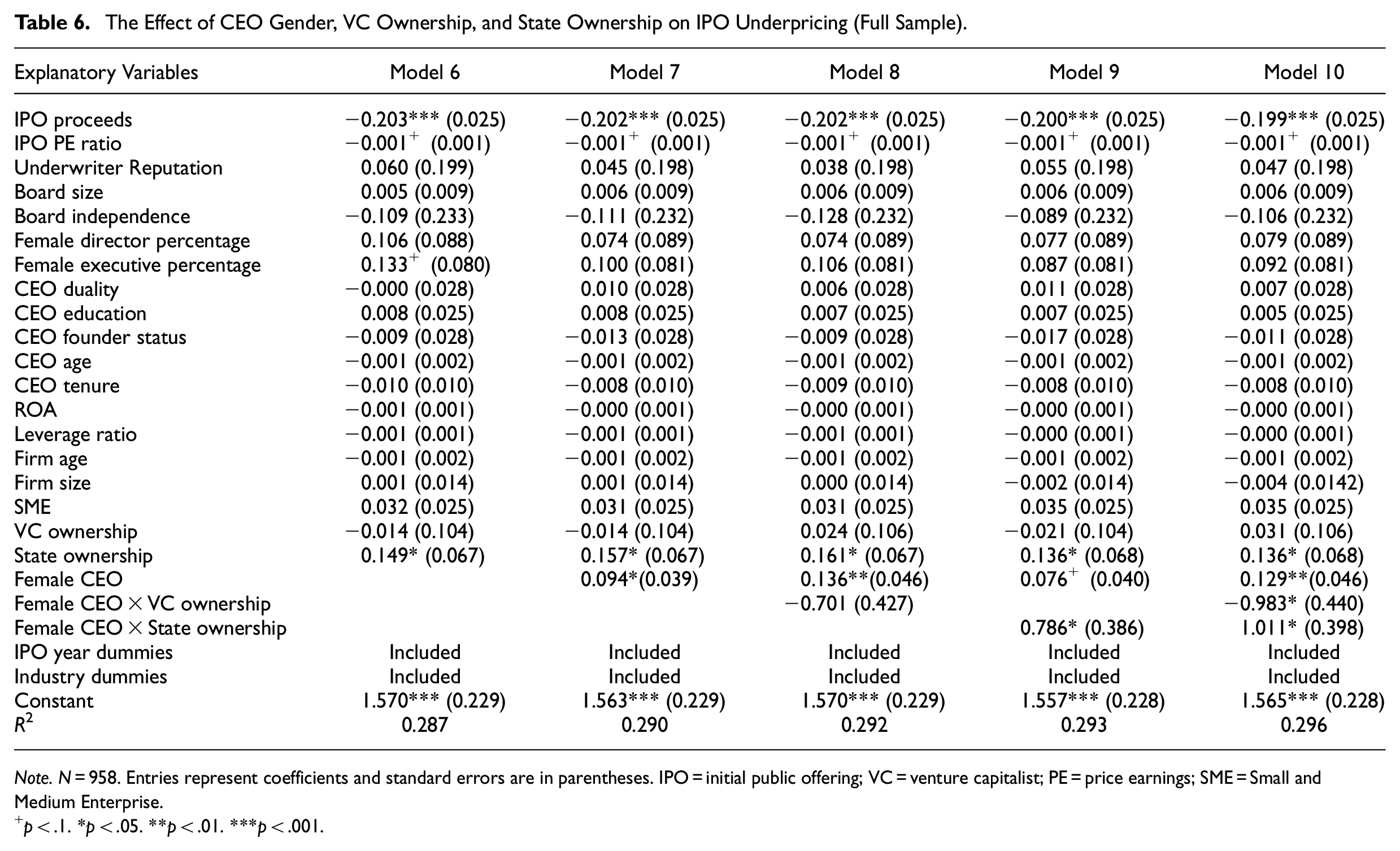

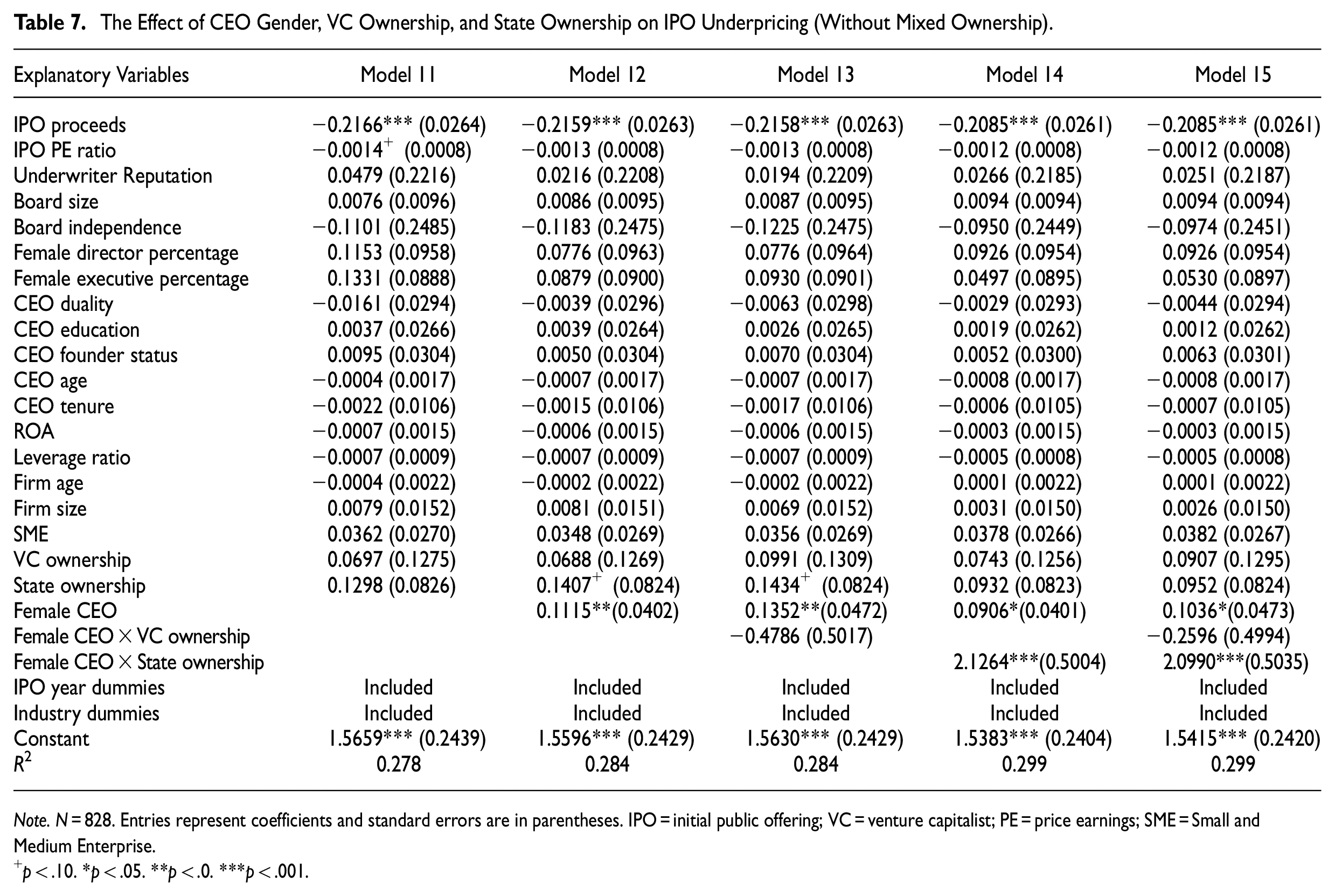

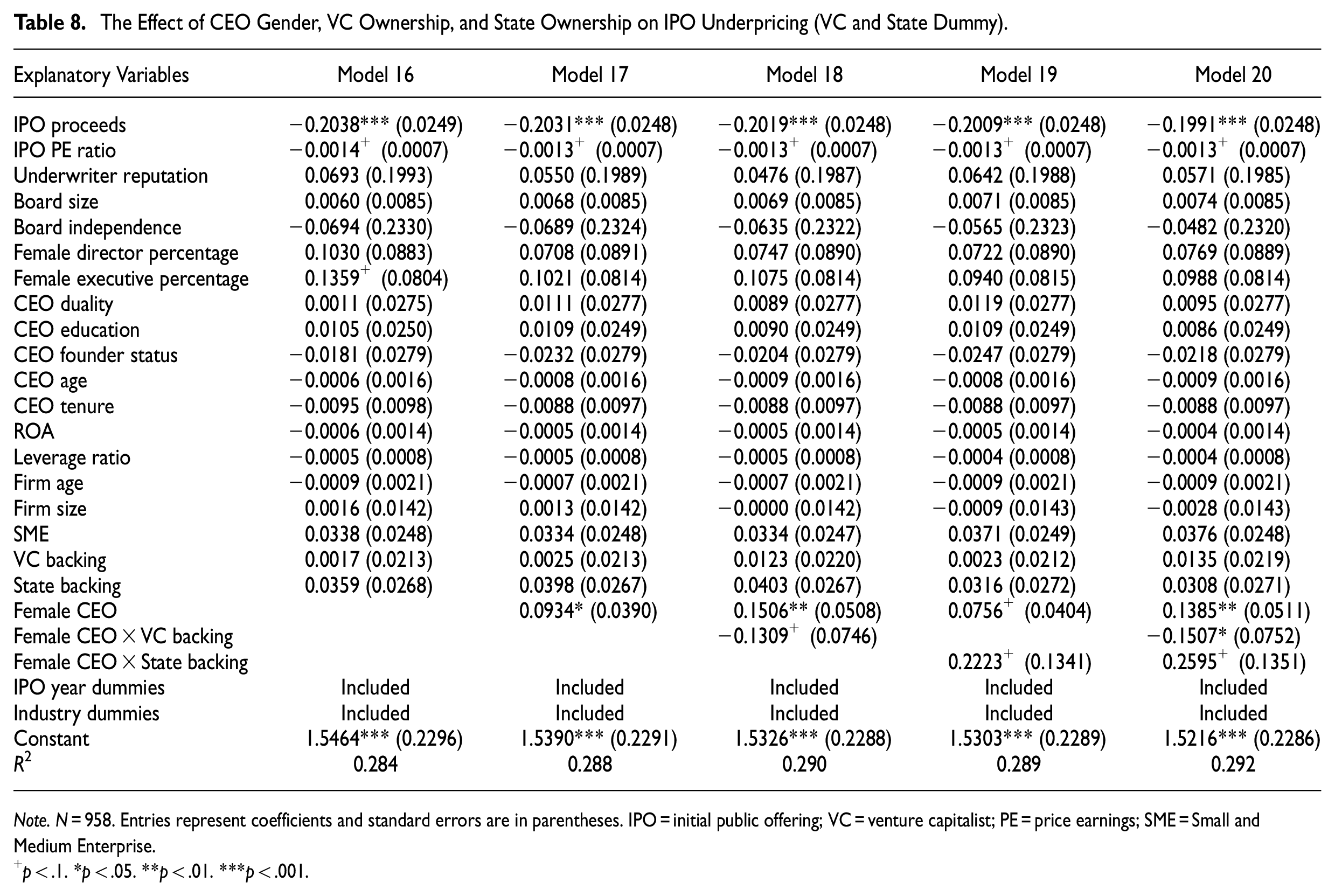

We conducted several additional tests to check the robustness of our findings. First, though the PSM technique alleviates the endogeneity concerns, our sample size was reduced due to the matching process. Therefore, we run OLS regression by using the full sample and present the results in Table 6. The results remain qualitatively the same. Second, we excluded firms that receive both VC and state funding, that is, firms with mixed-ownership (131 out of 958, 13.67%) and re-run OLS analysis. The results are presented in Table 7. H1 and H3 still hold across all models. However, we did not find statistically significant support for H2 in this sub-sample analysis. This non-significant result could be driven by sample selection bias because perhaps firms that received VC funding only are qualitatively different from other firms. Third, we replaced the continuous variables of VC and state ownership with dummy variables in the OLS analysis. If the firm has received any VC investment prior to IPO, we coded it as “1” and “0” otherwise. 520 out of 958 firms have received VC funds before IPO (54.28%). We also coded “state backing” as a dichotomous variable to indicate whether a listed firm has any state ownership by any government of government agencies in China. 188 out of 958 firms have state ownership (19.62%). Results remain similar with the main model and are presented in Table 8.

The Effect of CEO Gender, VC Ownership, and State Ownership on IPO Underpricing (Full Sample).

Note. N = 958. Entries represent coefficients and standard errors are in parentheses. IPO = initial public offering; VC = venture capitalist; PE = price earnings; SME = Small and Medium Enterprise.

p < .1. *p < .05. **p < .01. ***p < .001.

The Effect of CEO Gender, VC Ownership, and State Ownership on IPO Underpricing (Without Mixed Ownership).

Note. N = 828. Entries represent coefficients and standard errors are in parentheses. IPO = initial public offering; VC = venture capitalist; PE = price earnings; SME = Small and Medium Enterprise.

p < .10. *p < .05. **p < .0. ***p < .001.

The Effect of CEO Gender, VC Ownership, and State Ownership on IPO Underpricing (VC and State Dummy).

Note. N = 958. Entries represent coefficients and standard errors are in parentheses. IPO = initial public offering; VC = venture capitalist; PE = price earnings; SME = Small and Medium Enterprise.

p < .1. *p < .05. **p < .01. ***p < .001.

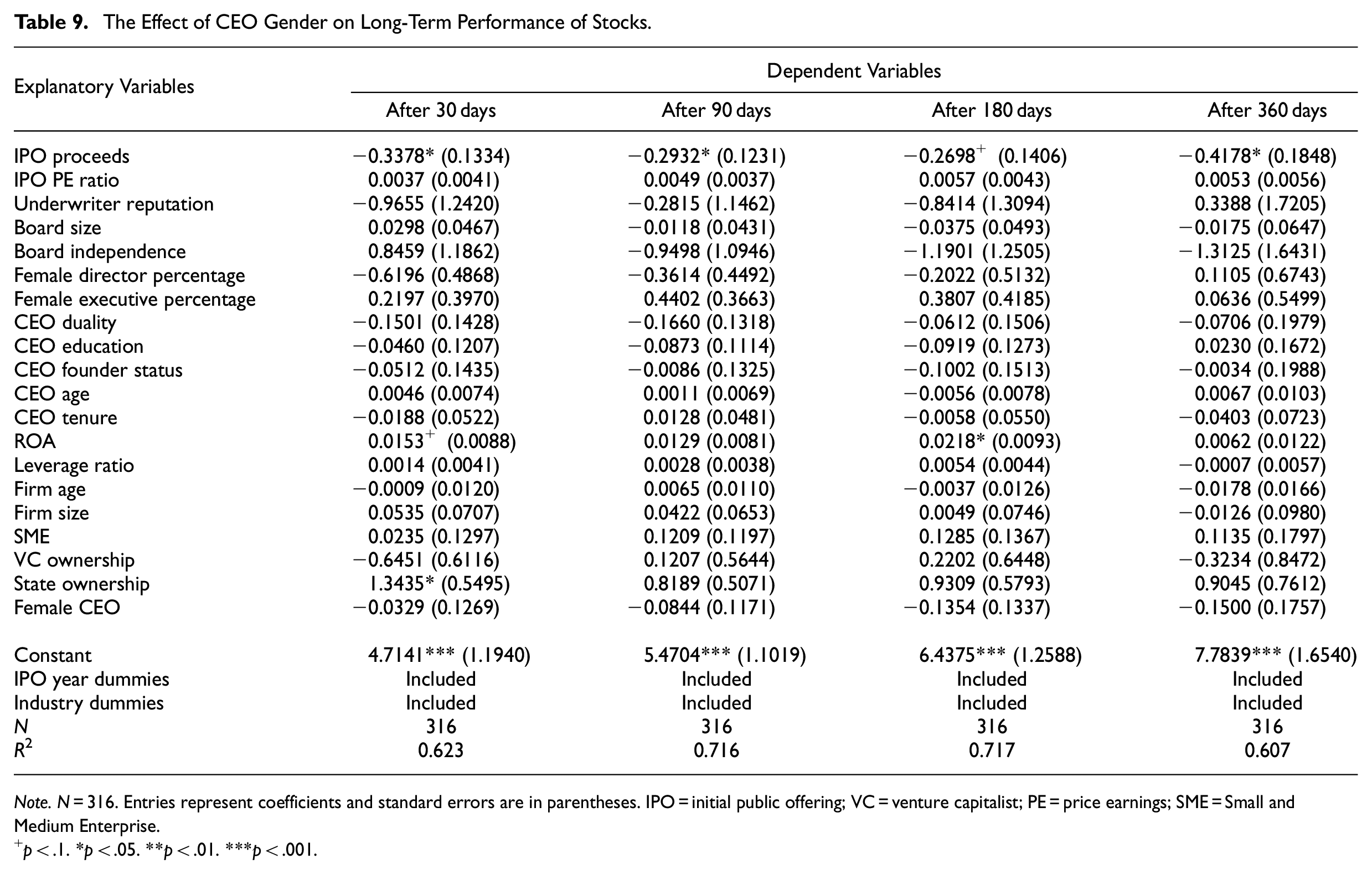

Further, because we argue that the gap in IPO underpricing between female-led and male-led IPOs is driven by gender bias, we need to further rule out the possibility that female-led firms have inferior quality compared to male-led firms. We tested the long-term performance of IPO firms by using the matched sample. In particular, we measure long-term returns as “return of IPO stock to that of the stock market index with respect to the first day’s closing price in intervals of 30 trading days” (Velamuri & Liu, 2017, p. 777), and test the results by using 30, 90, 180, and 360-day stock performance. We present the results in Table 9. Across four models in Table 7, we do not find CEO gender is positively related to the long-term returns of stocks, indicating that firms led by female CEOs are not qualitatively inferior to male-led ones in the long run.

The Effect of CEO Gender on Long-Term Performance of Stocks.

Note. N = 316. Entries represent coefficients and standard errors are in parentheses. IPO = initial public offering; VC = venture capitalist; PE = price earnings; SME = Small and Medium Enterprise.

p < .1. *p < .05. **p < .01. ***p < .001.

Discussion

Compared with male entrepreneurs, female entrepreneurs face greater challenges in raising funding to exploit their entrepreneurial opportunities. We examined the effect of CEO gender on IPO underpricing in China. We found that, although firms led by female CEOs incurred greater IPO underpricing, due to socially shared expectations on women and role incongruity, the funding source of these IPO firms may exacerbate or attenuate such an effect. In particular, VC funding certifies the value of firms and lends legitimacy to female-led IPOs, thus diminishing the degree of underpricing. In contrast, state ownership reinforces public investor bias on female-led IPOs and exacerbating the positive effect of CEO gender on IPO underpricing. Taken together, these results support the argument that the main effect of CEO gender influencing IPO underpricing is dependent on the context in which that information is displayed.

Contributions

Our findings make several contributions to the intersection between entrepreneurship, IPO, and gender research. First, this study contributes to female entrepreneurship research by examining the challenges that female entrepreneurs and CEOs face at the late stage of venturing in an emerging economy. Whereas existing literature has consistently documented that female founders encounter difficulties in securing resources at the early stages of venture development (e.g., Becker-Blease & Sohl, 2007; Guzman & Kacperczyk, 2019; Lee & Huang, 2018), research on female-led IPOs is scant and shows mixed findings (e.g., Bigelow et al., 2014; Mohan & Chen, 2004). Our study complements female entrepreneurship research by adding that female-led ventures encounter gender biases even at a late stage. However, such an effect is contingent upon the contextual factors with which the information is presented. Specifically, the market efficiency logic, which can attenuate information asymmetry between the IPO firms and external investors such as VCs, may limit the negative effects of female gender in elevating IPO underpricing, whereas the state socialist logic, which heightens information asymmetry through state backing, may exacerbate the main effect. Such contextual factors may be more pronounced in China, where market capitalist and state socialist institutional logics are present concurrently influencing market dynamics (Greve & Zhang, 2017; Zhou et al., 2017).

Second, our research contributes to the IPO underpricing research. Grounded in signaling theory (Spence, 1978), IPO underpricing research has investigated the certifying value of different signals to reduce information asymmetries (c.f., Certo et al., 2009). However, most studies have only examined the signaling effect of one single indicator at a time. Only recently, studies started to examine the interactive effects of multiple signals on IPO underpricing (Park & Patel, 2015; Payne et al., 2013; Yang et al., 2020). Although the gender of the CEO is not a signal per se because it was not produced by firms to seek market advantages, it serves as an informational cue for external investors to evaluate IPO firms, but such an effect is contingent upon other signals that interact with the main informational cue in a complex manner.

Third, this study contributes to gender research by showing that gender bias can be attenuated or exacerbated when combined with different institutional logics. Whereas female leaders are vulnerable to gender stereotypes and perceived as less fit for leadership roles in the eyes of the public (Eddleston et al., 2016; Malmström et al., 2017), recent research posits that effective framing strategies such as social impact framing can reduce the perception of “lack of fit” thus decreasing the bias (Lee & Huang, 2018). Our research adds that gender bias can also be diminished when presented with the market efficiency logic that lends greater legitimacy to women managers. However, the effect of gender bias in the unique emerging economy context of China could be more pronounced when combined with state socialist logic, highlighting the perceived lack of fit of women as leaders.

Limitations and Future Research Direction

This study has a number of limitations that could be addressed by future research. First, one surprising result from our empirical study is that, whereas VC backing can limit the positive effects of CEO gender on underpricing, we do not find the direct effect of VC backing on IPO underpricing in China. Although this finding is contrary to the majority of IPO research in the U.S. context (e.g., Lee & Wahal, 2004), it is consistent with previous research in China (Velamuri & Liu, 2017). The counter-intuitive findings can be explained by the development and maturity of VC industry in different contexts. Although the entrepreneurial financing market in developed countries is well-established and has gained social approval from investors, the Chinese VC market is still immature and lacks a sound governance system. Therefore, the certifying role of VCs is less recognized in the Chinese stock market. Nevertheless, our results show that VC backing does indeed interact with other informational cues to make an impact. That is, although a single informational cue is insufficient to alter the opinion of an evaluator, multiple cues can reinforce each other and can serve as a useful informational cue for the evaluator. Nevertheless, future research may further differentiate the effects of different types of VCs such as corporate venture capital or government backed venture capital in assessing entrepreneurial firms in emerging economies.

Second, although China provides a meaningful and important setting to study the influence of female CEOs on IPO underpricing, and the associated contingencies of VC and state backing, our results should not be generalized to other contexts. Indeed, despite abundant evidence of gender bias for access to entrepreneurial financing in the United States, previous studies using the U.S. sample have not found higher underpricing among firms led by female CEOs in the United States (Mohan & Chen, 2004). Therefore, future studies could further document how the influence of CEO gender differs across different institutional and legal contexts.

Third, whereas we highlight the joint effects of CEO gender and ownership structure on IPO underpricing, we are aware that other observable measures could also affect investor interpretation of CEO gender. In unreported analysis, we found that CEO founder status can also weaken the positive effect of CEO gender. This result implies that investors give more credit to female entrepreneurs who found and lead their firms to IPO stage. Future studies can further develop this line of research and theorize on the relationship.

Implications and Conclusion

Practical implications from this study are straightforward. Our study finds that firms led by female CEOs incur greater underpricing at their IPOs. However, our supplementary analysis shows that CEO gender does not lead to better or worse long-term stock market performance. This finding is daunting in a sense that it shows the value of female-led firms are discounted at IPO market, even if they are equally as good as male-led firms in the long-run. Our findings caution investors to be more mindful when they evaluate the value of entrepreneurial firms led by female CEOs. Whereas VC backing underscores the market efficiency logic embedded in the venture and lends legitimacy to female-led firms, investors and underwriters should judge the potential of firms based on the quality instead of the gender of CEO. Dissemination of the existence of our documented effect to the public might at least partially alleviate such a bias by investors, because human decision-making tends to suppress unconscious bias when decision-makers are aware of such a bias (Schwarz & Clore, 1983). More importantly, our research could inform the public about such a non-founded bias against female CEOs at the IPO stage in China. Indeed, psychology research shows that people tend to become less biased once they are aware that a particular non-conscious bias exists (Nisbett & Wilson, 1977).

This study examined the relationship between CEO gender and IPO underpricing, and the contingencies associated with the nature of financial backers—VC or state—on the relationship between CEO gender and IPO underpricing in the emerging economy of China. We hope that our findings can inform how female CEOs mitigate gender bias in the IPO process and raise external funding.

Footnotes

Acknowledgements

We are grateful for the helpful feedback and developmental comments from the editor Sophie Manigart and two anonymous reviewers. We also thank Tracy Zhang for her excellent research assistance in data collection for our paper.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed the receipt of the following financial support for the research, authorship, and/or publication of this article: We would like to thank China Europe International Business School (CEIBS) Cathay Private Equity Research Fund for their kind support of our work.