Abstract

Executive Summary

The pricing efficiency of initial public offerings (IPOs) is documented to be positively influenced by some of the certification mechanisms. Such mechanisms claim to reduce the information asymmetry between the issuers and investors. The certifications that have a positive influence include investment banker reputation, group or venture capital affiliation, association with financial institutions and analyst coverage, among others. The positive influence is claimed to be greater in the emerging markets, where frictions due to information asymmetry are relatively greater compared to the developed markets. It is in this context that the Indian market regulator added a unique certification for IPOs in May 2007 by mandating the grading of IPOs by an independent rating agency. It is expected to reduce the information asymmetry by providing comprehensive issue-related information to the market, especially to the retail investors in an ‘easy-to-use' format. While the grades make no comments on the issue pricing, they are expected to reflect the fundamental strength of the IPO.

The article empirically examines whether the introduction of grading has influenced the demand and pricing efficiency of IPOs. The approach involves cross-sectional regressions of the measures of underpricing and demand as dependent variables with a set of dependent variables to represent various firm, issue and market characteristics. The sample of graded IPOs used in the study has 182 issues during the 6-year period between October 2005 and September 2011.

The study does not find any significant impact of grading on IPO pricing or demand. Grading, which is expected to guide the retail investors, does not appear to influence their demand. While the grades appear to have an impact on the demand of the institutional investors, it has no influence on the IPO pricing efficiency. The graded issues, which are expected to have lower information asymmetry, do not have a relatively lower underpricing compared to the ungraded issues. Further, we find that the differences in the grading do not significantly explain the cross-sectional differences in market-adjusted underpricing. These results do not support any incremental certification role of IPO grading, as reported earlier by some studies with a smaller sample.

The Indian stock market regulator, the Securities and Exchange Board of India (SEBI), mandated the grading of all initial public offerings (IPOs) by a credit rating agency starting from May 1, 2007. 1

Prior to the introduction of mandatory grading, the regulator had introduced optional grading of IPOs in April 2006.

Frequently asked questions on IPO grading. Retrieved 31 July, 2012 from http://www.sebi.gov.in/faq/ipo.html

The expected positive role of IPO grading appears to be theoretically linked to two different strands of evidence. First, it is well known that the IPO market faces significant information asymmetry. Several IPO underpricing models use information asymmetry as the key explanatory factor (e.g., Benveniste & Spindt, 1989; Rock, 1986) with greater information asymmetry leading to higher underpricing. Accordingly, firms attempt to reduce underpricing through credible signalling of their true quality. The employed signalling mechanisms include (a) underwriter's reputation, (b) the presence of venture capitalists in the pre-issue funding, (c) group affiliation, (d) the quality of the board of directors and (e) credit rating, among others. These are found to have some degree of positive impact on the pricing efficiency of IPOs. For instance, association with venture capitalists (Barry, Muscarella, Peavy & Vetsuypens, 1990; Megginson & Weiss, 1991) and underwriter reputation (Carter & Manaster, 1990) are found to reduce underpricing. Credit rating, a certification mechanism very close to IPO grading, is also reported to reduce underpricing in the US market (An & Chan, 2008). Second, there is evidence that individual investors often fail to objectively assess IPOs, as they suffer from behavioural biases (e.g., Ljungqvist, Nanda & Singh, 2006). Grading could help them to make a more objective judgement, as it claims to compress the various issue-related information into an ‘easy-to-use' symbol. These suggest that the impact of grading on IPO bidding and pricing could largely depend on the degree to which the rational investors regard grades as a unique source of incremental price-relevant information. If indeed, grading provides unique, unbiased and more accurate issue information, it could positively impact the demand for high-quality IPOs and improve the pricing efficiency of IPOs.

The introduction of mandatory grading, however, was not uniformly welcomed in the Indian market on the following grounds. First, it was contended that investors who are unable to understand and analyse the issue information would also be unable to understand the meaning of grades. A popular financial daily wrote, ‘Indeed, assigning grades to new issues can lull investors into a false sense of security about the risks and rewards of equity investing and can make equity look safer than it is' (The Economic Times, 2007). Second, there were concerns whether the rating agencies would have enough incentives to strive for objective grades. While the reputation of a credit rating agency could be verified with the actual defaults of debt securities, it would be difficult to ascertain the truthfulness of IPO grades due to the volatile nature of equity cash flows. Third, the investment banking community maintained that grading would increase the issue costs. Fourth, analysts asserted that without a comment on the issue price, IPO grading had very little relevance. On the contrary, retail investors generally welcomed the idea of IPO grading. They possibly felt that grading would reduce their dependence on issue advertisements and brokers. However, they demanded that the issue pricing be also brought into the scope of grading.

The available evidence on the impact of IPO grading presents conflicting evidence on its role. While Deb and Marisetty (2010), one of the earliest studies on grading, found that the IPOs after the introduction of grading were associated with lower underpricing, Khurshed, Paleari, Pande, and Vismara (2011) found no such role for grading in underpricing. Further, Khurshed et al. (2011), with a larger sample, found no support for the two key findings of Deb and Marisetty (2010): (i) the high-grade issues are associated with better IPO pricing and (ii) retail investors respond to IPO grading with increased subscription of the high-grade issues. Khurshed et al. (2011), instead, argued that grading positively influenced the subscription pattern of the institutional investors, which, in turn, positively impacted the retail subscription. This close link between the institutional and retail investors' demands was attributed to the evidence of retail investors following the institutional investors' bids, which was possible due to the high transparency of book building in India. However, the submission of bids by the retail investors towards the end of the bidding window significantly improves their ability to assess the probability of receiving an allotment. Such an assessment also helps them to reduce the opportunity cost of funds underlying the application. This behaviour would be more salient during the hot IPO periods due to greater subscription levels and the availability of more investment opportunities. These motives of the retail investors imply that ‘the retail demand following the institutional demand' cannot be fully attributed to the information asymmetry faced by the former. It is somewhat surprising that IPO grades influence the demand of the relatively more informed institutional investors rather than that of the individual investors. If the institutional demand is influenced by the IPO grade, then it is critical to examine whether it necessarily improves the pricing efficiency in a market like India, where institutions dominate price discovery and the market demand. The results of Deb and Marisetty (2010) may be partly attributed to their relatively small sample of graded issues from a cold market period, as they did not control for the market conditions. Overall, the available research on the IPO grading leaves a number of important questions not adequately addressed. This article is a modest attempt to resolve some of the contentious findings on the impact of IPO grading, given its status as a unique certification.

The results suggest that grading has not significantly impacted the pricing of IPOs in India. While the institutional demand for IPOs seems to be influenced by the IPO grades, it does not have any significant impact on the retail demand, once the possible influence of the demand of institutional investors is accounted for. No significant change is observed in the bidding approach of retail investors after the introduction of grading. For institutions, the low-grade IPOs appear to have weaker demand and IPOs with high grades experience stronger demand. These findings together tend to suggest that the IPO grading as a certification mechanism has not performed its expected role to a great extent. It is perhaps difficult to assign reliable IPO grades due to the volatile nature of the equity cash flows. Further, the transparency of book building in India affords retail bidders to learn from the real-time demand schedule of the institutional investors. This could also make IPO grading redundant for the retail category demand. The failure of IPO grading needs to be examined at a deeper level.

IPO GRADING

Important Features

IPO grades are assigned on a five-point scale. The lowest grade (Grade 1) denotes poor issue fundamentals and the highest grade (Grade 5) denotes strong fundamentals, relative to that of the listed firms in India. The grade is expected to only reflect the various issue fundamentals such as the industry prospects, firm's financial position, the quality of its management and governance, risks and prospects of its new projects and the firm's regulatory compliance. It does not take the issue pricing into account and, thus, does not constitute an assessment of the fairness of the IPO price.

The rating agency is expected to use the information disclosed by the issuer and that obtained from other sources. An issuer dissatisfied with the grade assigned by one agency can approach another. However, the issuer is bound to disclose all the assigned ratings. The IPO grade along with the rationale given by the agency has to be displayed in every advertisement of the issue, including the issue prospectus and the abridged prospectus. The rating rationale is expected to detail the key findings and conclusions about the various aspects considered in assigning the grade. 3

Every grade report explicitly mentions that the grade is not an opinion on the issue pricing.

TESTABLE HYPOTHESES AND METHODOLOGY

Testable Hypotheses

The nature of IPO grading suggests that it can be regarded as an additional certification of the IPO fundamentals. This approach had been adopted by the earlier articles on this issue (Deb & Marisetty, 2010; Khurshed et al., 2011). Based on the literature on information asymmetry and the role of certification in IPO pricing, we hypothesize the following impacts in the IPO market with the introduction of grading.

First, if grading performs its expected role as a certification, it is reasonable to expect that the more informed institutional investors (qualified institutional buyers [QIBs] hereafter) would be less reliant on the IPO grades in their bidding compared to the retail investors, as they have greater access to information and better analytical skills. The retail investors, on the contrary, are more likely to use the IPO grades. Hence, we expect a varying level of influence of grading on the retail and institutional demand.

Second, if the IPO grade provides incremental, price-relevant information and summarises the bulky public information into an easy-to-use form, it could potentially improve the IPO pricing efficiency. This is expected as the IPO grading could potentially improve the information quality and reduce the information asymmetry in the market. Both these outcomes are claimed to reduce IPO underpricing over time. Ljungqvist (2004) provided a detailed discussion on these issues. Further, if the grading reduces information asymmetry, then it could nudge the pricing of all IPOs towards their respective fair price in a rational market, and all issues, irrespective of their grades, should have similar levels of risk-adjusted underpricing. This could reduce the cross-sectional variation of underpricing with the introduction of grading.

Third, by acting as a certification mechanism, if grading helps to reduce underpricing, then its role would possibly be more evident in the case of the relatively small firms and firms belonging to relatively nascent industries, as these firms are documented to suffer from greater information asymmetry.

Methodology

The possible influence of IPO grading on the demand for issues from various investor categories is examined with cross-sectional regressions. The regressions take the following form:

where N T Si is the number of times IPO i is subscribed by an investor category (retail or QIB), and Xi is a set of variables to reflect the firm and issue characteristics, and market conditions around the time of the issue (as explained later in this section).

DGRADE represents a dummy variable to reflect the issue grade. The economic and statistical significance of the grade-related dummy would indicate the influence of grade on the demand for IPOs.

The impact of grading on IPO pricing efficiency is examined with the following cross-sectional regression involving net underpricing as the dependent variable. The independent variables reflect the key firm, issue and market characteristics along with categorical variables to reflect the grades:

where U Pi is the market-adjusted return on IPO of stock i defined as below:

The market return is proxied by the return on Sensex, one of the most popular equity indices in India. Primarily, the regressions examine whether the grade, which is expected to convey the issue characteristics, has any direct influence on the pricing efficiency.

The independent variables (X

DATA AND PRELIMINARY FINDINGS

Data

The IPO-related data are taken from the Prime database and the firm-level financial data from the CMIE Prowess database. The sample comprises all the 352 IPOs over the 6-year period between October 2005 and September 2011. One of the IPOs is removed from the sample due to the unavailability of its post-listing price. IPOs before October 2005 are not included in the sample primarily due to an important change in the book-building process—replacement of discretionary allocation with proportionate allocation on September 19, 2005. Moreover, the Indian IPO market has significantly evolved on many fronts, such as the institutional profile, issue pricing, allocation, disclosures and listing norms, etc., in the last decade. These changes would make comparison of the IPO pricing efficiency or bidding patterns over a long period of time unreliable in India.

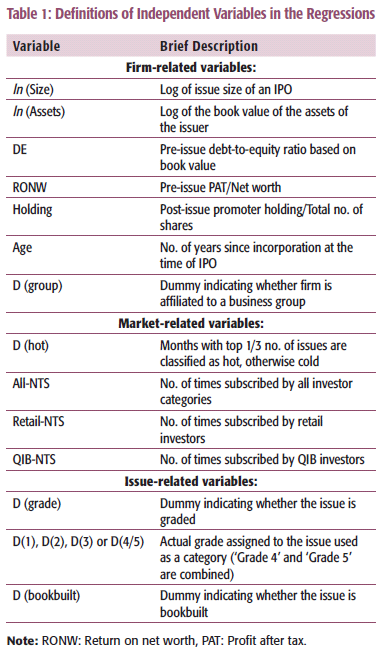

Definitions of Independent Variables in the Regressions

Overall Characteristics of the Sample

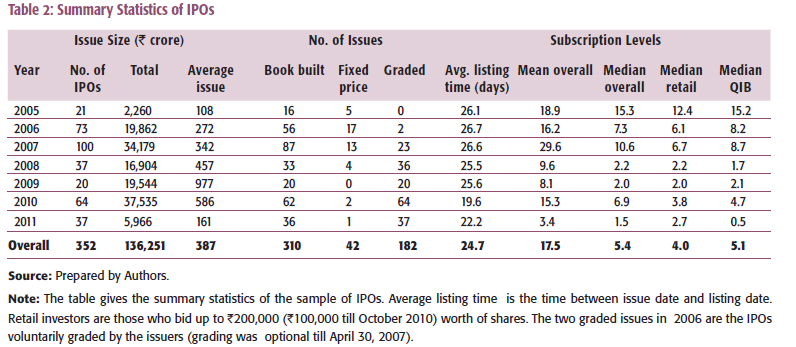

A brief description of the sample IPOs is provided in Table 2. The sample represents a total issue size of about ₹136,250 crore, which averages about ₹19,464 crore per year and about ₹415 crore per issue. The sample period corresponds to one of the most active phases for IPOs in India and accounts for nearly 79 per cent of the issue volume and 84 per cent of the issue value during the decade ending September 2011. Most of the IPOs are offered through book-building method (88 per cent). The median of the overall subscription of IPOs is about 7 times and the mean about 14 times. This suggests that there are many highly subscribed issues. For instance, eight IPOs are subscribed more than 100 times. The category-wise subscription also has many extremes. The retail has subscribed three IPOs more than 100 times and the QIBs have crossed the ‘100 times' mark in as many as 16 issues. The mean subscription levels peaked in 2007, which is also the peak IPO activity year. The subscription level has significantly declined towards 2011. Among the investor categories, the demand of the QIBs appears to be greater than that of the retail for most of the years.

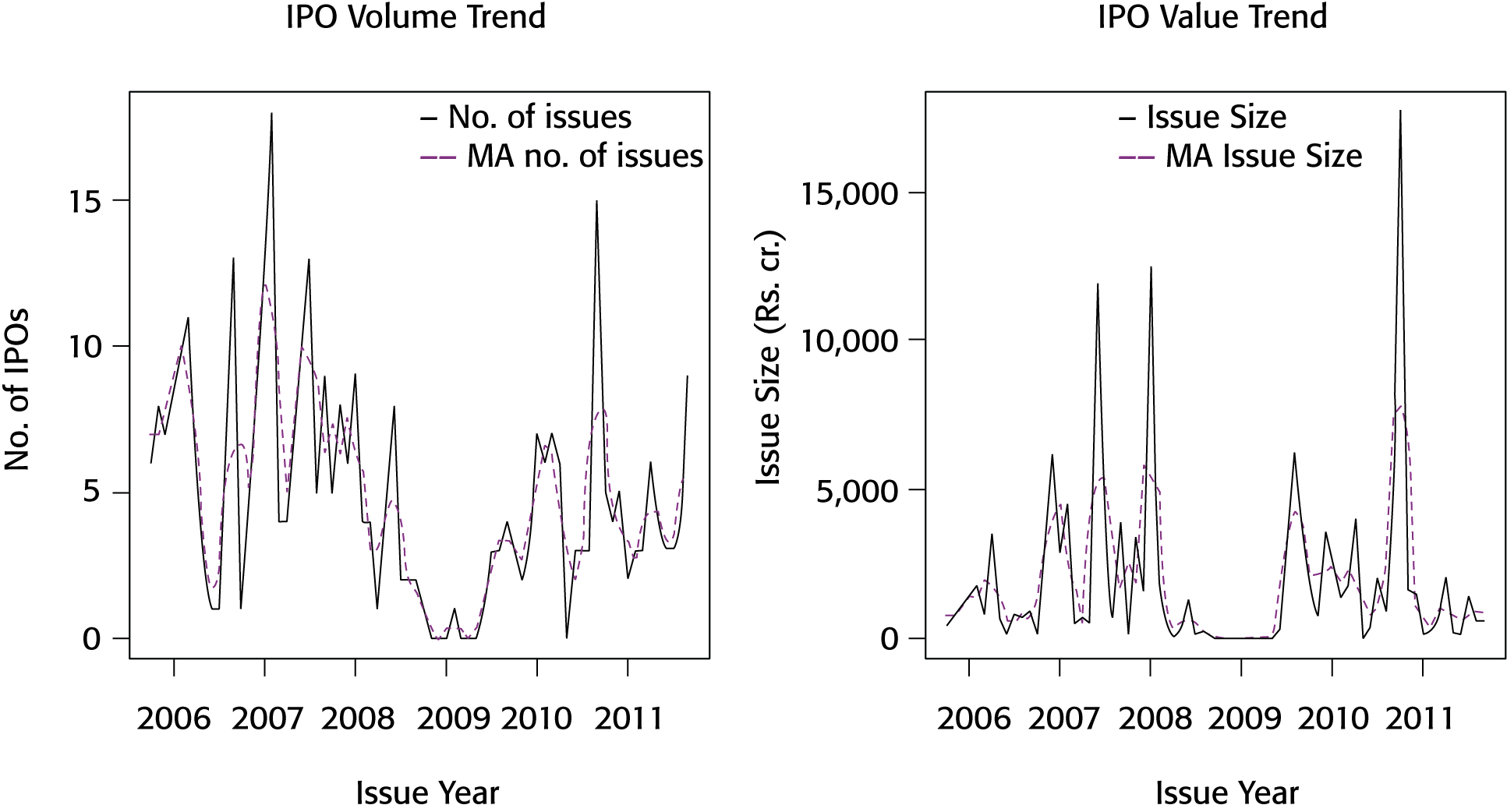

It appears that there is clustering of IPO activity in India, as reported from other markets. The monthly issue volume, issue size and its three-monthly moving average over the period are given in Figure 1. The maximum IPO volume (18 issues) is in February 2007 and the maximum issue amount is in October 2010 (₹ 17,674 crore). 4

The maximum issue size in October 2010 was contributed by a large IPO of a public sector firm.

Summary Statistics of IPOs

There are no IPOs in 7 months out of the 73 covered by the data, and another 7 months have only one issue each. The time periods between 2007 and 2008 and 2010 and 2011 appear to fit the description of a ‘hot phase' in the Indian IPO market.

Given the apparent IPO clustering and the documented evidence of the conditions on issue pricing, the study attempts to control for market conditions in the regressions. Each month in our dataset is classified as a ‘cold' or a ‘hot' month, based on the 3 month centred moving average of the number of IPOs during that month relative to the average number of IPOs during the period. The moving average takes care of any seasonality in the issue of IPOs. The top one-third months are classified as hot months and the remaining months as cold months. Out of the total 73 months, 18 months are classified as hot months. 5

Cold months outnumber the hot months due to a large number of months in the calendar period without any issues.

By the issue size, the IPOs appear to be concentrated around two sectors: power, and ‘construction and real estate'. These two industries together accounted for about 47 per cent of the total issue size. By the number of issues, ‘construction and real estate' was the dominant industry, with about 16 per cent share of the IPOs. The industry clustering suggests the need to control for industry in the regressions.

Characteristics of the Graded IPOs

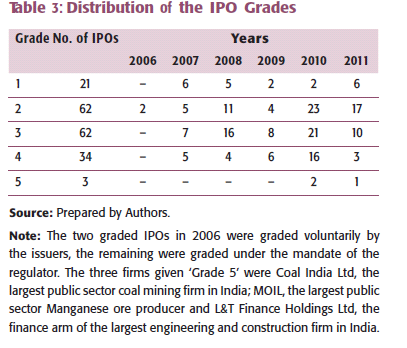

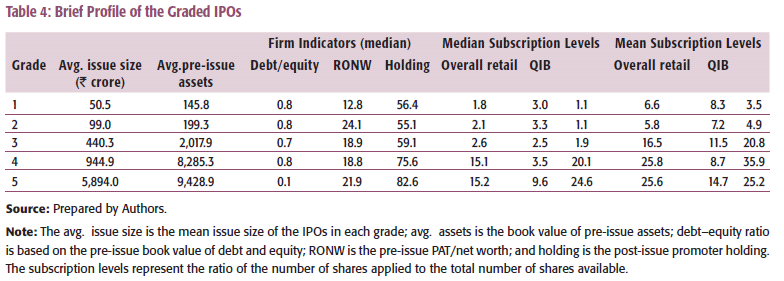

The final sample has 182 graded issues. The distribution of the IPO grades and a brief profile of the graded issues are given in Tables 3 and 4, respectively. As given in Table 3, only about one-fifth of the graded IPOs have been assigned high grade (Grades 4 or 5) and about 12 per cent are graded at the lowest level (Grade 1). The lowest grade IPOs accounted for a large share of the IPOs during the year 2007. By the issue size, nearly 60 per cent of the IPOs are high grade and only 1 per cent is in the lowest grade. This skewness could possibly be due to a link between firm size and grades. Overall, the distribution of the grades suggests no significant bunching in the IPO grades. It appears that the issuers, who are larger, relatively low-levered and have a greater return on equity, tend to receive the highest grading. This pattern could be expected, as grading focuses solely on the fundamentals of the firm.

As given in Table 4, the high-grade IPOs seem to attract greater overall subscription. Across the entire sample, the median QIB and retail demand appears to be greater for the high-grade IPOs. For instance, the median QIB subscription of₹ ‘Grade 4' issues are about 20 times, compared to 1.1 times of the ‘Grade 1' IPOs. For low-grade IPOs, the retail demand seems to be greater than that of the QIB demand. For instance, the median ‘Grade 2' IPO is subscribed 3.3 times by the retail compared to 1.1 times by the QIB. Partly, the lower QIB subscription of low grade IPOs could be due to the internal investment restrictions on issuer features such as firm size, leverage, profitability, etc. It appears that compared to the large variation in institutional subscription across grades, the retail subscription does not vary as much. These features of the subscription pattern suggest, at least, that the IPO demand of retail and QIB are not always similar.

Distribution of the IPO Grades

Brief Profile of the Graded IPOs

Features of IPO Underpricing

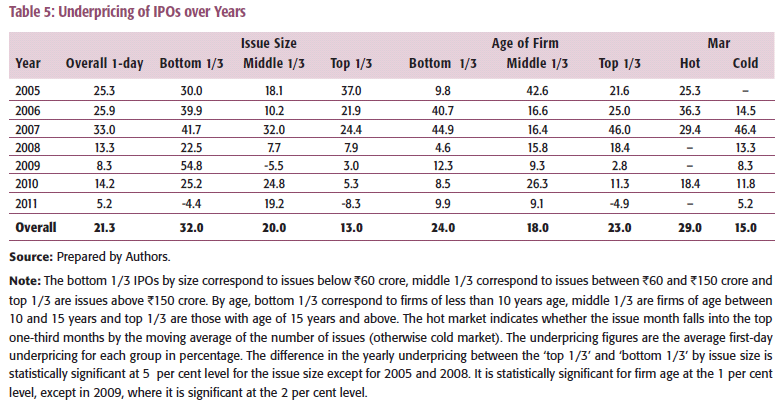

A comparison of the pricing efficiency, as reflected in the underpricing, is given in Table 5. All the issues in the sample period are not underpriced. A sizeable number (about 36%) of the issues are found to be overpriced, relative to their first-day closing price. Nearly two-thirds of the overpriced IPOs are issued in cold market conditions. IPO underpricing appears to have significantly declined over the sample period. The 2005 average first-day underpricing of 25 per cent has declined to about 5 per cent in 2011. The apparent improvement in the pricing efficiency could be attributed to a number of developments in the Indian market such as a broadened investor base, improved information disclosure by issuers, more effective aggregation of issue-related information and improved regulation. While there are many significant regulatory and structural changes in the market over this period, the higher underpricing of the earlier years could also be due to the greater time gap between the issue and listing and the associated cost of tied-up funds. For instance, the average time period between issue date and listing date in 2005 is 26 days; the corresponding figure in 2011 is only 18 days.

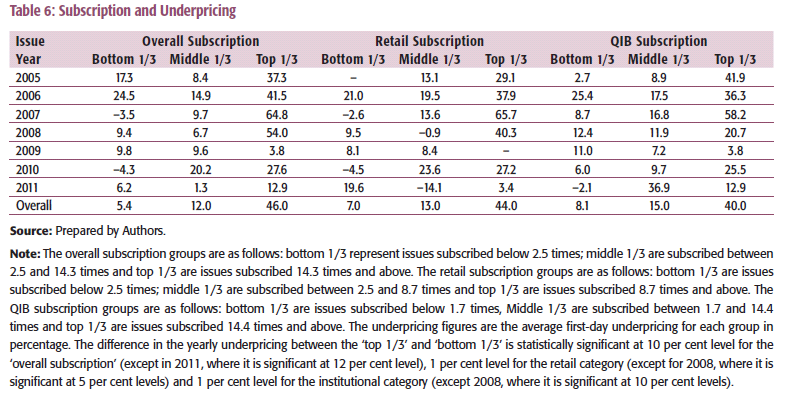

It appears that larger IPOs have more efficient pricing in India. The average underpricing of IPO groups varying in issue size and firm age is given in Table 5. The top one-third of IPOs by size (issues of ₹150 crore and above) have an average underpricing of about 13 per cent as against 32 per cent of the bottom one-third (issues below ₹60 crore). The larger issues are documented to have lower information asymmetry world over. The age of the firm does not seem to have any significant unconditional influence on the IPO pricing efficiency. The underpricing appears to be greater during the hot periods than the cold periods. For example, IPOs experience average underpricing of about 29 per cent during the hot months compared to about 15 per cent during the cold months. This pattern is similar to the finding from markets including the United States (Helwege & Liang, 2004). Table 6 gives the average underpricing of IPOs grouped by the overall and category-wise subscription levels. IPOs that have attracted the top one-third overall subscription (subscribed more than 14.24 times) have significantly greater underpricing than the IPOs with bottom one-third overall subscription (subscribed less than 2.48 times). This relatively higher underpricing of the IPOs with greater investor demand can be understood as a hot market phenomenon having greater investor sentiment.

Underpricing of IPOs over Years

Subscription and Underpricing

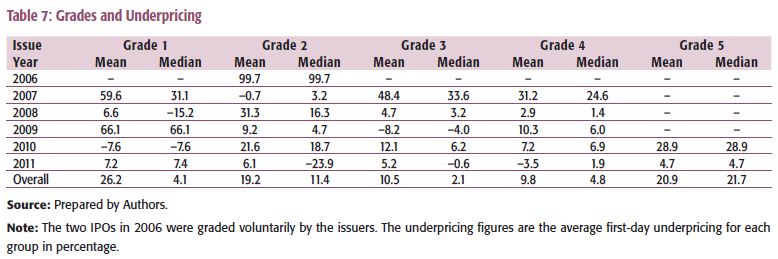

The grade-wise average underpricing is given in Table 7. The average underpricing seems to decline with higher grading, except in the case of Grade 5. However, the Grade 5 sample has only three IPOs, which makes the finding less reliable. The median underpricing does not show a declining trend with higher grading. Hence, the averages are being influenced by large underpricing values of a few IPOs.

Grades and Underpricing

These univariate relations suggest that IPOs that are larger or issued in cold markets have lower underpricing and grading has no conspicuous influence on the underpricing.

FINDINGS AND DISCUSSION

Grading and IPO Demand

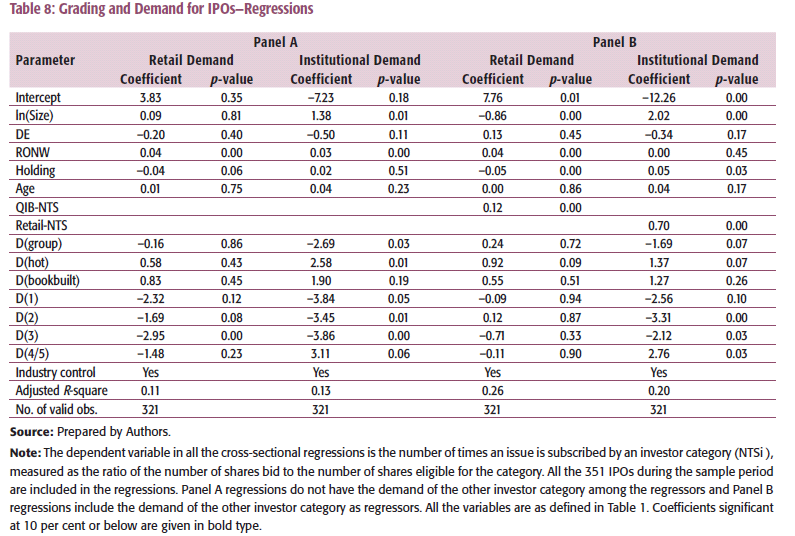

We adopt a robust regression procedure to analyse the influence of grading on IPO demand due to the presence of many outliers in the subscription data. The results of the robust regressions involving the demand (Equation 1) of the retail and QIB investors are given in Table 8. Panel A gives the results where the demand of the other investor category is not included among the regressors and Panel B gives the results where the demand of the other investor category is included among the regressors. The overall results suggest that both the institutional and retail demand for IPOs is apparently influenced by the grades. The coefficient of the grade dummy for the low-grade IPOs (D(1), D(2) and D(3)) is negative for both the retail and QIB demand. The significance of the coefficients of grading is greater in the case of QIBs.

Grading and Demand for IPOs-Regressions

For the QIB category, the results (given in Panel A of Table 8) indicate that the demand is weaker for the relatively low-grade IPOs, compared to the high-grade or ungraded IPOs. The coefficient of the grade dummy is positive for the high-grade IPOs. These results are intuitive as the institutional investors are believed to be relatively more informed and rigorous in their investment approach, compared to their retail counterparts. It is also likely that the institutional investors have investment policy constraints that restrict their investments in IPOs having poor fundamentals. The other variables with significant impact on the IPO demand of this category are the issue-related fundamentals: RONW, group affiliation, issue size and market conditions. As suggested by the coefficient of the ‘hot–cold' dummy (D(hot)), the demand for IPOs is greater during the hot period. These variables carry their expected signs.

On the contrary, the demand from the retail investors (as given in Panel A of Table 8) for both the low- and high-grade IPOs appears to be negative, relative to the ungraded IPOs. The negative coefficient of the grade dummy is significant only for ‘Grade 2' and ‘Grade 3' IPOs. As the relatively low-grade IPOs have poor fundamentals and are risky, the appetite for such IPOs ought to be lower, especially when these risk–return characteristics are revealed to the market. The weaker demand for the low-grade IPOs, compared to the ungraded IPOs, tentatively suggests a guidance role for the IPO grade in the case of the retail investors. While the coefficient of the dummy representing the high-grade issues (D(4/5)) is insignificant for the retail category, its negative sign merits some explanation. It is found that the high-grade IPOs are larger issues by amount. For instance, the average issue size of the overall sample is about ₹388 crore and the average size of ‘Grade 4' and‘Grade 5' issues is about ₹1,346 crore. These issues are oversubscribed by the retail to a lower degree compared to the average issue. This is possibly due to the limited investible funds available with them. The institutional investors have far more funds to invest, and hence may invest more aggressively in the high-grade IPOs, as indicated by the positive coefficient of the grade dummy in that case. Generally, the very large issues are unlikely to top the demand, when measured as the ‘number of times subscribed'. Hence, employing the ‘number of times subscribed' as a measure of the demand from the investor categories itself is not without problems in capturing the true relative issue demand. 6

For instance, the IPO of Coal India Ltd, a very popular issue in India, with an issue size of about ₹15,200 crore was subscribed only about 15.2 times compared to the sample average of 18 times.

In a related article, Khurshed et al. (2011) found that it was the demand of the institutional investors that was significantly influenced by the IPO grade. They found that the institutional demand was relatively weaker for the low-grade issues and stronger for the high-grade issues. However, they did not find any significant role of IPO grading in the retail demand and linked this insignificance of the grades to the claim of the retail bids following the QIB bids, due to high transparency of book building in India (Khurshed, Pandey, & Singh, 2008).

Based on the evidence of the mutual influence of retail and institutional demand, we modify the cross-sectional demand regressions (given in Equation 1) by adding the demand of the other category as a regressor. The results of these regressions are given in Panel B of Table 8. The demand of each of the investor categories apparently influences the demand of the other, as indicated by the significance of the associated coefficients (QIB-NTS and retail-NTS). On inclusion of the demand of institutional investors, the coefficients of the grade dummy turn insignificant in the case of the retail demand.

Overall, these results tend to suggest that the IPO grade has some degree of influence on the investor demand. The impact appears to be stronger in the case of the institutional investors. The direction of the impact for both the categories suggests the following. First, the low-grade issues experience weaker demand compared to the ungraded issues. Second, the high-grade issues experience greater demand from the QIBs compared to the ungraded IPOs. It is apparently puzzling to see why the grade leaves a greater impact on the demand of the more informed institutional investors, rather than that of the retail category. It is possible that the association between grades and demand for the institutional category found here could be just a reflection of the independent IPO investment assessment done by the institutions based on the issue fundamentals.

Grading and Bidding Behaviour

If grading had effectively supplemented or improved the quality of issue-related information, available to the retail investors, it would have allowed bidders to take more informed IPO investment decisions. Such an outcome could influence the bidding behaviour of the investors, such as the (a) proportion of individual bids at cut-off and (b) bidders' degree of distinction of IPOs with bright future prospects from their poor counterparts. One would expect effective IPO grades to reduce the number of bids submitted by the retail investors without a price quote (bids at cut-off). 7

In India, the retail investors are allowed to bid at ‘cut-off price', which leads to bidding for shares without quoting a price. This is allowed on the assumption that many retail investors might not have the wherewithal to quote a price. If the IPO grading reduces information asymmetry, for the retail investors, then more retail investors could be able to form an opinion about the IPO price.

First, the proportion of individual investors bidding for IPOs at cut-off price for the graded IPOs is apparently no different from that for IPOs without grade. About 62 per cent of the individual investors' bids continue to be at cut-off price. 8

About 31 per cent of the total bids are submitted at cut-off. Assuming a total individual investor quota of 50 per cent and an almost equal level of subscription by individual and institutional investors, this translates into 62 per cent of individual bids.

Grading and IPO Underpricing

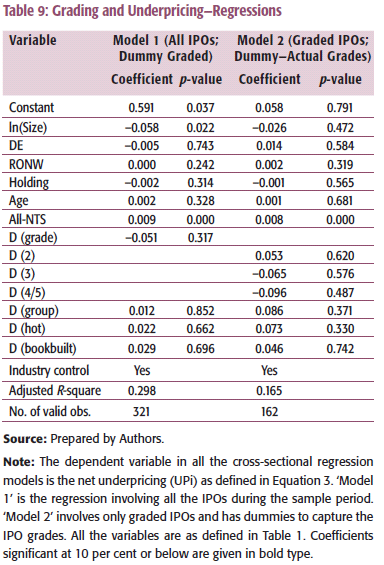

The possible impact of grading on underpricing is examined with cross-sectional regressions involving underpricing (as given in Equation 2). Two sets of regressions are estimated: (i) with only a single dummy variable to distinguish the graded issues from the ungraded ones and (ii) with multiple dummy variables to distinguish across the grades. The significance of the grade dummies could imply the influence of grading on the IPO pricing.

The results of the regressions involving a single dummy are given in Model 1 of Table 9. The results indicate that whereas grading is expected to be negatively related to underpricing, the related dummy variable is not significant (D (grade)). This seems to suggest that grading has no significant influence on the pricing of IPOs. This insignificance of grading has been reported earlier by Khurshed et al. (2011). However, our results contrast with that of Deb and Marisetty (2010) who had found that IPO grading helped to significantly reduce underpricing in India. The differences might be due to the larger sample employed in this study and for the reasons identified earlier in the article.

Grading and Underpricing—Regressions

The results further suggest that the only significant factors that influence underpricing are the issue size (ln(Size)) and demand for IPOs (All-N T S). Larger issues appear to achieve better pricing, as expected. This could be attributed to its lower information asymmetry. The market demand of IPOs, captured by the number of times the IPOs are subscribed (All-N T S), suggests that IPOs with greater market demand have higher underpricing. This somewhat counter-intuitive result can be understood as IPOs that experience high demand during a hot period are often listed at a premium. This is possibly due to the unmet demand in the primary market. During hot markets, investors often exhibit a greater inclination to own assets, irrespective of their price. The greater underpricing of IPOs during hot markets is also reported from elsewhere (Helwege & Liang, 2004).

The study further examined whether, among the graded cohort, IPOs with higher grades have lower underpricing compared to those with relatively lowergrades. The results of the cross-sectional regressions with the actual grades as categorical variables are given in Model 2 of Table 9. The insignificance of all the grade dummies (D(2), . . . , D(4/5)) reinforces the earlier evidence on the failure of grading to positively influence underpricing. As in the case of Model 1, the most significant factor influencing underpricing is the demand of IPOs.

It was expected that IPO grading would help to alleviate the information asymmetry around the IPOs. It is interesting, therefore, to examine whether grading has any impact on the pricing of relatively small IPOs, where the information asymmetry is believed to be high. The study examined this issue through cross-sectional regressions involving the IPOs of only small firms similar to regressions in Table 9. All the firms that belong to the bottom one-third when ranked by the pre-issue assets are taken as the sample of small firms. We find no evidence for the significance of grades on underpricing (results not reported for brevity).

CONCLUSION

‘IPO grading' attempts to give comprehensive issue-related information in an ‘easy-to-use' format to the investors. This was expected to positively influence the IPO demand and improve the efficiency of IPO pricing in India. We examine the extent to which these expectations from IPO grading are realised in the market.

While it appears that grading positively influences the demand for high-grade IPOs, there is a significant difficulty to regard it as an evidence in favour of the mitigation of information asymmetry by grading for the following reasons. First, grading, which is expected to guide the retail investors, does not appear to influence their demand. There is also no evidence that the grading helps to better translate the issue information into a price quote. Even with grading, the proportion of retail bids without a price quote remains very high. Second, while the grades appear to have an impact on the demand of the institutional investors, it has no influence on the IPO pricing efficiency. The extent of underpricing is unrelated to grades. The graded issues, which are expected to have lower information asymmetry, do not have a relatively lower underpricing compared to the ungraded issues. Further, the high-grade issues do not have lower underpricing relative to the low-grade issues. It is possible that the evidence of the influence of grade on the demand of the institutional investors could be just due to the independent processing of the issue-related information by them rather than the use of grades. For these reasons, it is not appropriate to argue that the significance of IPO grading in the institutional investor demand is sufficient evidence for the contributory role of grading. These results on the impact of IPO grading in India on pricing efficiency sharply contrast with the finding of Deb and Marisetty (2010) that the grading leads to lower underpricing.

The insignificant role of grading in IPO pricing almost suggests that grading has not performed its expected role as a certification of the underlying issue quality. The reasons for the failure of this innovative certification could be many. It is perhaps difficult to assign reliable IPO grades due to the residual nature of the equity cash flows. Whereas credit rating is based on a set of reasonably measurable criteria whose failure can be tracked, the post-IPO stock performance has only a weak tractability. This weak tractability may not sufficiently incentivise agencies to assign grades objectively and, thus, erodes its role as a credible signal of IPO quality. Further, the transparency of book building in India appears to allow prospective retail bidders to benefit from the almost real-time demand schedule of IPOs of the institutional investors. This could also make IPO grading redundant.

Footnotes

Acknowledgement

The authors thank the participants of the India Finance Conference, held at the Indian Institute of Management Calcutta during 19–21 December 2012, and the participants of Eastern Finance Association 2013 Annual Meeting, held at St. Petersburg, Florida during April 2013, for their useful suggestions and comments. The financial support from the Indian Institute of Management Ahmedabad is gratefully acknowledged. The authors also thank Aditya Jagannath, Research Associate at the Indian Institute of Management Ahmedabad for his excellent research assistance.