Abstract

Despite growing numbers of corporate venture capital (CVC) deals and alliances, their effectiveness is not guaranteed. This paper investigates the positive and negative impacts of CVC and alliance activity on product safety under different levels of market turbulence. Using a resource-based learning perspective and panel data from large U.S. firms, we find that both CVC and alliance activity have inverted U-shaped relationships with product recall likelihood. Market turbulence moderates both relationships, but differently. We discuss how learning theory complements the resource-based view to understand why no or rather bold external venturing are less harmful than small-scale “stuck-in-the-middle” initiatives.

Keywords

Introduction

Because it offers them fresh innovation capital, external corporate venturing is a way for established firms to tackle organizational inertia and keep up with a fast-paced, turbulent market environment (Belderbos et al., 2018). Two external venturing modes are receiving increasing attention in academia and practice. With an over 10-fold increase over the past decade (National Venture Capital Association, 2020) and record investments of $169.3 billion in 2021 (CB Insights, 2022), more and more established firms use corporate venture capital (CVC) to participate in innovative ventures through minority equity stakes (Belderbos et al., 2018). Similarly, strategic alliances, which are non-equity cooperation partnerships through mutual agreements about joint resource sharing activities (Dushnitsky & Lavie, 2010), have gained importance. In a KPMG (2018) study, for instance, 56% of CEOs said alliances were a fundamental part of their strategy for firm growth and innovativeness.

Affirming its importance, research has found that through external venturing, firms can enhance their innovativeness and “attain ends they could not achieve alone, or at least not as quickly” (Grunwald & Kieser, 2007, p. 369). This is because CVC and alliances promise access to valuable resources from external partners, especially knowledge about new technologies or markets (Wadhwa et al., 2016). Applying the resource-based view (RBV) and learning theory, scholars have argued that CVC and alliances create learning opportunities that help firms improve their resource position and adapt to their competitive environment (Basu et al., 2011; Maula et al., 2009; Srivastava & Frankwick, 2011).

Despite these benefits, learning from external sources is complex (Van de Vrande & Vanhaverbeke, 2013) and resource-intensive as internal resources need to be mobilized and external knowledge integrated (Posen et al., 2017). In competitive and turbulent environments, external learning is even more useful but also more difficult (Titus et al., 2014). Thus, learning from CVC or alliance partners can create valuable knowledge resources (Wiklund & Shepherd, 2009), but the risk of failure is high (Titus et al., 2019). If external learning fails, it can disrupt a firm’s innovation and new product development (Park & Ungson, 2001; Steven & Britto, 2016) and damage its resource position (D. Lee et al., 2017). Steven et al. (2014) found that reliance on external partners can decrease product quality and increase the likelihood of a product recall. Already a single recall can harm the recalling firm and its shareholders by reducing sales (Cleeren et al., 2013), shareholder wealth (Davidson & Worrell, 1992), and brand reputation (Eilert et al., 2017), and the faulty product that caused the recall can harm the general public (Thirumalai & Sinha, 2011). 1

Extant research on the consequences of CVC and alliances has, however, mostly focused either on financial value effects or innovation output in the form of patents. While some studies have found positive effects of strategic CVC investments on investors’ firm value (e.g., Dushnitsky & Lenox, 2006), other studies on CVC and alliance portfolios found counteracting mechanisms for patent output (e.g., Marhold et al., 2017). For new product development alliances, studies have reported failure rates of 50% to 70% (Gil & de la Fé, 1999; Sivadas & Dwyer, 2000). This dark side of external venturing was echoed in a recent meta-analysis by Huang and Madhavan (2021), who reported ambiguous implications of CVC investments due to positive learning and complementarity effects versus negative resource mobilization and misalignment effects. Despite increasingly mixed findings suggesting that CVC and alliance activities can have downsides (e.g., Huang & Madhavan, 2021; Moghaddam et al., 2016) and rising scholarly interest in the negative effects of investments on external innovation access, we lack theoretical knowledge about these negative impacts and their root causes (Anokhin, Wincent, et al., 2016). Following calls to identify meaningful consequences, positive and negative, of external venturing (Drover et al., 2017), we consider product recalls—the removal of potentially harmful products from the market—an outcome of CVC and alliance activity. In this way, we present a potential root cause for the mixed prior findings.

The present study combines two prominent theoretical lenses in external venturing research—the RBV and learning theory (Fels et al., 2021; D. Lee et al., 2017)—to explain existing tensions between beneficial and harmful effects of external venturing. In doing so, we build upon research that conceptualizes external venturing as a set of problemistic search activities (Titus et al., 2019) to spur organizational learning and experimentation from sources outside the firm (Keil et al., 2008; Wiklund & Shepherd, 2009). Complementing RBV (Penrose, 1959) with learning theory (Greve, 2021), we offer a theoretical perspective considering the costs and benefits of external venturing. To empirically investigate how two distinct external venturing modes affect firms in highly competitive and knowledge-focused environments, we use longitudinal data from large U.S. manufacturers regulated by the Food and Drug Administration (FDA) and their drug recalls. We investigate how the numbers of CVC and alliance activities affect firms’ likelihood of experiencing product recalls. Moreover, we test how market turbulence, an environmental contingency that complicates resourcing and learning processes, moderates the venturing–recall relationship.

This study makes several contributions. First, we address an archetypical tension in entrepreneurship research, the trade-off between the risks and benefits of corporate venturing (Covin & Miles, 2007). Identifying inverted U-shaped relationships between CVC and alliance activity on the one hand and product recall likelihood on the other, we advance the external venturing literature by showing when such activities benefit or harm firm operations. Thereby, we offer first insights into the impact of CVC and alliances on meaningful firm-level outcomes other than patents or financial value (Drover et al., 2017). These insights also bridge the thriving but heretofore isolated external venturing and product recall literatures. We shed light on strategic firm-level antecedents of recalls (K. D. Wowak & Boone, 2015) and show how firms’ venturing activities can have severe consequences for themselves and the public.

Second, demonstrating that the effects of both forms of external venturing on recalls are amplified—though in distinct ways—in turbulent markets, we provide a contingency perspective that distinguishes the effects of CVC and alliance activities. In turbulent markets, firms need more CVC deals until their product recall likelihood decreases, but less alliances. In our dataset, high alliance activity even reduced recall likelihood to zero, with the strongest effect per alliance under high turbulence. We explain these findings with differences between unilateral CVC investments and bilateral alliance agreements (e.g., Dushnitsky & Lavie, 2010). Although still rare, comparative studies like ours enhance our understanding of risk and reward profiles of different external venturing modes (Titus et al., 2019).

Third, providing a finer-grained picture than prior external venturing studies, our study uses a resource-based learning perspective to explain why some firms benefit from external venturing while others do not. The non-linear effects of CVC and alliance activity on product recall likelihood demonstrate that either no or rather bold external resource-seeking seems to pay off more than small-scale “stuck-in-the-middle” initiatives. These findings echo the RBV’s tenet that strategically important resources are indeed hard to transfer between organizations (Barney, 1991). They also support the ideas of path dependency and experience learning in firms’ learning through problemistic search (Greve, 2021; Posen et al., 2017). With greater external search activity, firms can offset related costs and benefit from external resource acquisitions due to learning curve effects (Greve, 2021).

Theoretical Background and Hypotheses

The Differential Effects of External Venturing

External venturing can be both financially and strategically driven, but for many firms, strategic motives prevail, with the goal of sourcing knowledge about new technologies, products, or market opportunities (for a discussion, see Dushnitsky, 2009). Thus, external venturing is a search for complementary innovation resources and capabilities outside a firm’s boundaries (Belderbos et al., 2018; Titus et al., 2019). External venturing can include CVC investments, strategic alliances, joint ventures (JVs), or mergers and acquisitions (M&A) (Titus et al., 2019). In the present paper, following Belderbos et al. (2018, p. 24), we focus on CVC and strategic alliances because firms operating in high-tech environments “often simultaneously employ international CVC investment and technology alliance strategies aimed at knowledge sourcing.” Both are particularly relevant in uncertain, turbulent high-tech environments, as they entail lower levels of commitment (Belderbos et al., 2018) and are thus more flexible than M&A or JVs (Srivastava & Frankwick, 2011; Van de Vrande & Vanhaverbeke, 2013). The parties involved in CVC deals and alliances remain independent legal entities with an own corporate identity (Vanhaverbeke et al., 2002). Niosi (2003, p. 745) found that in the turbulent biotech industry, VC deals were “as important as alliances in explaining rapid growth,” and hence explain within-industry performance variations as proposed by the RBV (Penrose, 1959).

Extant research on external venturing has largely measured its outcomes by firm/portfolio financial value or patents (Fels et al., 2021). Many studies have argued that access to complementary resources and capabilities can enhance firms’ innovation and financial performance (cf. Belderbos et al., 2018). Others, however, have found that absorptive capacity issues, misalignment, or resource constraints limit the positive effects or even lead to adverse effects (e.g., Rothaermel & Deeds, 2006; Wadhwa et al., 2016; Wadhwa & Kotha, 2006). Recent meta-analyses on CVC investments (Huang & Madhavan, 2021) and alliances (D. Lee et al., 2017) have confirmed what earlier M&A research (King et al., 2004) indicated: external venturing has both positive and negative effects.

CVC investments

CVC investments are minority equity investments by established corporations in entrepreneurial ventures (Dushnitsky & Lenox, 2005). In terms of financial outcomes, Dushnitsky and Lenox (2006) found that CVC investments increase investors’ market value if they are made for strategic reasons. Titus and Anderson (2018) added that the financial success of CVC investments depends on the organizational structure of the investing firm and the munificence of its environment. Yang et al. (2014) showed that the impact of CVC portfolio diversification on the investor’s market value is U-shaped because knowledge transfer and knowledge diversification drive the CVC portfolio value in opposing directions.

In terms of innovation outcomes, most CVC studies investigated firms’ patenting output (Drover et al., 2017). Wadhwa and Kotha (2006) used patents to show that the number of CVC investments has an inverted U-shaped relationship with investors’ knowledge creation when their involvement is low. The relationship between CVC portfolio diversity and patent citations also follows an inverted U-shape (Wadhwa et al., 2016). Portfolio diversity drives patent citations, but beyond a tipping point, high portfolio diversity can result in absorptive capacity issues and managerial resource constraints, which lower patent quality (Wadhwa et al., 2016). Recognizing that the amount and diversity of CVC investments had a curvilinear relationship with the technological diversity of the investing firm, Lee and Kang (2015) found similar results for the difficulties of CVC investors in absorbing knowledge. In sum, CVC can induce benefits through learning and complementary resources and costs through resource mobilization and misalignment (Huang & Madhavan, 2021). Because of the importance of learning and resources for CVC success, it is not surprising that the RBV and learning theory emerged as the most prominent theoretical lenses to investigate the consequences of CVC investments (Fels et al., 2021; Narayanan et al., 2009).

Strategic alliances

Unlike CVC deals, strategic alliances are usually formed by fairly equal partners to share resources along the value chain, without equity investments from the firms involved (Dushnitsky & Lavie, 2010). 2 Van de Vrande and Vanhaverbeke (2013) defined alliances as cooperative efforts of two or more organizations whereby they join forces to share reciprocal inputs while maintaining their own corporate identities. Typically, the alliance objectives and resources each partner contributes are contractually agreed upon, with concrete activities subject to joint coordination (Das & Teng, 2000, 2016). Despite considerable differences regarding inter-organizational relationships and knowledge exchange (Belderbos et al., 2018), the goals of CVC investments and alliances can be similar (for a comprehensive comparison, see Dushnitsky & Lavie, 2010). Both often aim at obtaining access to new technologies, innovations, and markets (Belderbos et al., 2018).

As with CVC and innovation, studies have found similar complex relationships between alliances and innovation. For example, Deeds and Hill (1996) and Rothaermel and Deeds (2017) found that the relationship between the number of alliances and the rate of new product development follows an inverted U-shape. Similarly, alliance portfolio diversity has an inverted U-shape relationship with patent citations (Marhold et al., 2017). Moreover, failure rates of 50% to 70% for new product development and innovation alliances (Gil & de la Fé, 1999; Sivadas & Dwyer, 2000) imply that alliance activities can significantly affect product failure. Despite the risk of failure, firms’ rationale to form alliances is “to aggregate, share, or exchange valuable resources with other firms when these resources cannot be efficiently obtained through market exchanges or mergers/acquisitions” (Das & Teng, 2000, p. 37). Again, it is plausible that the RBV and learning theory are important theoretical lenses when studying alliances (D. Lee et al., 2017).

A Resource-Based Learning Perspective on External Venturing

The RBV’s main point is that firms’ internal resources are idiosyncratic and can be sources of sustained competitive advantage (Barney, 1991; Barney et al., 2001). Vice versa, it is argued that “resources that transfer across organizations cannot produce sustainable advantages” (Greve, 2021, p. 1722). This poses the question of why firms engage in external venturing though it may not improve their competitive advantage. The answer may lie in a resource-based learning perspective on external venturing. Expanding Penrose’s (1959) seminal work on the RBV beyond the focal firm’s boundaries, scholars considered alliances (e.g., Eisenhardt & Schoonhoven, 1996; Wiklund & Shepherd, 2009) and CVC investments (e.g., Anokhin, Wincent, et al., 2016; Basu et al., 2011) as sources of complementary resources and learning opportunities, noting that the RBV is a “theory of (growth of) knowledge” (Penrose, 1959, p. xxxiii). Consequently, the RBV can be integrated with organizational learning theory due to meaningful overlaps and complementary differences (Greve, 2021). While both theories make similar arguments about why firms use external venturing, learning theory also considers how firms absorb and integrate external knowledge (Cohen & Levinthal, 1990). According to the RBV, firms use external venturing when their own resources are insufficient to compete in current or future markets (i.e., in turbulent environments) or when they pursue pioneering strategies (Das & Teng, 2000; Eisenhardt & Schoonhoven, 1996). Similarly, learning theory argues that firms use learning mechanisms when performance is below aspirations (Greve, 2021). Among these mechanisms, problemistic search is the main driver for learning; it is the way firms search for alternatives to enhance their performance (Greve, 2021; Posen et al., 2017).

However, these points pose at least two dilemmas concerning the “costs and benefits” (Penrose, 1959, p. 242) of external venturing. First, firms seek valuable resources to improve their competitive position but incur search costs to find partners and set up suitable external venturing activities (Penrose, 1959). For problemistic search, firms often “carve out resources” from other activities (Posen et al., 2017, p. 224). If strategic activities are complex or the environment is turbulent, evaluating alternatives is difficult; negative outcomes may ensue due to failures in the valuation of external resources (Titus et al., 2014). Second, problemistic search is highly path-dependent, and firms are likely to be more successful in internal than external learning due to the closer fit with their current resources and routines (Greve, 2021; Posen et al., 2017). Hence, external venturing can bring major learning and knowledge integration costs to a firm before the firm can build new routines to absorb and integrate external knowledge and capitalize on the benefits of experience learning (Titus et al., 2014; Wadhwa & Kotha, 2006).

Against this backdrop, we theorize that CVC and alliance activities are complex problemistic search processes that firms use to access new knowledge resources and improve their competitive position (Titus et al., 2019). Considering the contrasting costs and benefits of CVC deals and alliances, we argue that their relationships with product recalls are not linear.

Product Recalls

Going beyond the narrow focus of financial and patenting outcomes of CVC and alliances (Anokhin, Wincent, et al., 2016; Drover et al., 2017) to “generate deeper insights into […] the consequences for the parent firm and other key stakeholders” (Drover et al., 2017, p. 1841), we suggest that CVC and alliance activities can disrupt firm innovation efforts and lead to negative outcomes in the form of product recalls. A recall is the market removal of a product with potentially adverse health consequences (FDA, 2018a). According to the regulatory body of the U.S. FDA, items such as drugs are recalled “to protect the public from a defective or potentially harmful product” (FDA, 2018a). In 2019, the number of drug recalls in the U.S. reached an all-time high of 2,163 (FDA, 2019), making recalls an important topic for practitioners and researchers alike.

Research on product recalls has shown that they can have severe consequences for firms, for example, by reducing sales (Cleeren et al., 2013), shareholder wealth (Davidson & Worrell, 1992), and brand reputation (Eilert et al., 2017), while the faulty products that cause them can endanger peoples’ health. Although preventing product failures and recalls is extremely important, “empirical evidence of operational drivers of recalls is almost nonexistent” (Shah et al., 2016, p. 2439), and the understanding of what drives product failure and thus recalls is “still in its infancy” (Wowak & Boone, 2015, p. 54).

Studies in this area have shown that financial leverage (Kini et al., 2017) or the combination of stock repurchases with cuts to research and development (R&D) and marketing (Bendig et al., 2018) can lead to more recalls. In contrast, both managerial and family ownership can reduce the likelihood of recalls (Kashmiri & Brower, 2016). A firm’s approach to innovation can also affect product recalls. Firm innovativeness is related to higher costs from unexpected product failures, which increase further with the innovativeness of the industry (Mackelprang et al., 2015). Thirumalai and Sinha (2011) found that firms with broader product portfolios have an increased likelihood of recalls. Similarly, greater product variety (Shah et al., 2017) and product competition (Ball et al., 2018) drive product recalls. Considering external cooperation, Steven et al. (2014) observed that outsourcing can increase recalls. These findings emphasize the importance of a firm’s strategic position and innovation efforts as antecedents of its product recall likelihood.

The Impact of CVC Activity on Product Recall Likelihood

To develop our first hypothesis, we build on arguments derived from prior research about the costs and benefits of CVC activity. First, CVC investments are formally about committing funds, but investors also devote considerable other resources to searching promising investments (Anokhin, Peck, et al., 2016; Basu, Wadhwa, et al., 2016). Scanning the environment for suitable targets is a complex endeavor because CVC aims at young ventures with new technologies and business models. While new technologies always carry risk and uncertainty and have higher failure rates than incremental innovations (Mackelprang et al., 2015), information asymmetry increases as new technologies and markets go further beyond the core business of the parent firm (Wadhwa et al., 2016). To overcome information asymmetry, investors perform due diligence (Keil et al., 2008) and often have a venture funnel to screen potential targets before deciding to invest (Keil, 2004). Upon investment, the investor tries to establish formal relationships (e.g., filling board seats with executives or R&D/CVC managers) as well as informal ones (e.g., frequent social exchange through calls or visits) with the venture to ensure control and facilitate knowledge exchange and integration (Belderbos et al., 2018; Wadhwa et al., 2016; Wadhwa & Basu, 2013). In sum, these activities lead to “very high coordination costs in learning and leveraging” (Huang & Madhavan, 2020, p. 8) the knowledge from CVC activities. Tensions arise between the availability of resources for established internal routines of a corporate investor and their availability for external collaboration and explorative learning (Wadhwa et al., 2016). These tensions can lead to organizational discontinuities, which are a root cause of product failure and thus increase a firm’s recall likelihood (Ball et al., 2018; Mukherjee & Sinha, 2018).

Second, scholars agree that CVC activities provide valuable learning opportunities for investors, particularly concerning new technologies, markets, or business models (Wadhwa & Basu, 2013). However, because investees are often not contractually obliged to share their knowledge (Dushnitsky & Shaver, 2009), research has pointed out the importance of implementing new organizational routines for investors to assess and successfully absorb ventures’ knowledge (e.g., Belderbos et al., 2018). The newness and potential dissimilarity of the investee’s knowledge to the investor’s core business requires changes in existing learning modes (Cohen & Levinthal, 1990). With more CVC deals, investors establish “collaborative blueprints,” including routines, governance mechanisms, and dedicated personnel to facilitate knowledge exchange and integration into their own business units (Basu, Phelps, et al., 2016). This integration and recombination with firm-specific prior knowledge is important for effective learning and the generation of new idiosyncratic knowledge and capabilities (Kor & Mahoney, 2004; Penrose, 1959). Absorbing and creating new knowledge helps the investing firm cope with the uncertainty and complexity of new product innovation (Belderbos et al., 2018). In this way, CVC investments can be seen as a learning process from experimentation beyond firm boundaries (Keil et al., 2008). Participating in more related ventures helps experimenting corporate investors identify knowledge relevant to their own capability development and avoid costly errors (Keil et al., 2008). Investors with greater CVC activity have learning advantages (Wadhwa & Basu, 2013) and are better able to evaluate new technologies and markets, which decreases the likelihood of experiencing a product recall.

Finally, CVC investments entail great uncertainty not only about the target venture but also about the investor’s own capabilities to learn from its partner (Wadhwa & Basu, 2013). In studying CVC investors, Sykes (1990) found that learning the CVC activity itself is important for corporate investors, and Wadhwa and Kotha (2006) found that investors learn by doing. Experienced CVC investors realize their strategic objectives through the effective monitoring and management of their investments with informal interactions (Basu & Wadhwa, 2013). Wadhwa and Basu (2013) added that more experienced corporate investors enjoy better reputations and better embeddedness in VC networks, making them more attractive and trustworthy, thus increasing investees’ willingness to share knowledge. Hence, corporates learn how to do CVC (Sykes, 1990), become better at it with more CVC experience (Keil, 2004), and use their experience as a signal to investees to gain even greater benefits through increased openness and knowledge sharing (Wadhwa & Basu, 2013). Accordingly, and consistent with the notion of experience learning (Greve, 2021; Penrose, 1959), we expect that CVC investments initially lead to more product recalls, but with more knowledge and experience gained from greater CVC activity, the product recall likelihood will decrease. We hypothesize:

Hypothesis 1: CVC activity has an inverted U-shaped relationship with product recall likelihood. Higher CVC activity is associated with higher product recall likelihood; however, beyond a tipping point, higher CVC activity is associated with lower product recall likelihood.

The Impact of Alliance Activity on Product Recall Likelihood

For our second hypothesis, we draw on prior research about the balance between the costs and benefits of alliances to investigate how alliance activity affects product recalls. First, alliances can cause organizational discontinuities because they are complex in many ways. According to Park and Ungson (2001), the complexity of alliances is an important reason why they fail. Firms mobilize resources to find suitable partners and to negotiate, set up, and integrate alliance activities, but opportunism or misalignment can still jeopardize success (Srivastava & Frankwick, 2011). Kale and Singh (2009) identified three areas that are crucial for alliance success: formation and partner selection, governance and design, and post-formation management.

In the first area, partner complementarity, compatibility, and commitment are important (Kale & Singh, 2009) and subject to information asymmetry (Rothaermel & Deeds, 2004). Alliances are often formed by firms with different capabilities, making it hard to assess their compatibility (D. Lee et al., 2017). Upon initiation, allies need to mobilize the resources for joint activities (Kale & Singh, 2009). The second area concerns ownership, contractual provisions, and governance (Kale & Singh, 2009). Alliances typically use contracts to set common goals, rights and obligations, inputs, and formal exchange mechanisms (Kale & Singh, 2009). However, especially for exploration alliances, concrete activities and goals are hard to define, as the outcomes are highly uncertain (Oxley & Sampson, 2004). In addition to contracts, alliances rely on self-enforcing governance mechanisms, such as mutual adjustment, trust, and reputation (Kale & Singh, 2009). These mechanisms can increase complexity and potential misalignment because of different organizational structures, practices, and cultures (Jiang et al., 2010; Park & Ungson, 2001). The third area concerns joint coordination, relational capital, and conflict resolution (Kale & Singh, 2009). Sometimes, alliance partners have conflicting interests, which can cause further misalignment (Jiang et al., 2010). For example, opportunism, aiming at short-term individual advantages, impairs collective goals (Park & Ungson, 2001). Conflicts and misaligned coordination can disrupt operational processes and cause quality problems (Gokpinar et al., 2010). Thus, greater alliance activity may increase product recall likelihood.

Second, research has found that firms with many alliances have access to broader complementary resources and diverse knowledge (Cho & Arthurs, 2018; Wiklund & Shepherd, 2009). Alliances bring firms with different skills and knowledge bases together in purposeful ways, creating learning opportunities (Inkpen, 1998; Srivastava & Frankwick, 2011). The imperative for mutual exchange and learning in alliances is rooted in their nature because firms enter alliances when they are “convinced that through cooperation they are able to attain ends they could not achieve alone” (Grunwald & Kieser, 2007, p. 369). Wiklund and Shepherd (2009) posit that complementary partner resources drive the value of alliances. However, to fully realize their value, resources must be combined and integrated with prior knowledge held by each firm (Cohen & Levinthal, 1990; Wiklund & Shepherd, 2009). This is why the most common form of learning in alliances is interactive learning (Srivastava & Frankwick, 2011), mutual information exchange between the partners (Inkpen & Tsang, 2005), which creates new common knowledge, as well as realistic assumptions about the collaboration and each partner’s expertise (Das & Kumar, 2007; Srivastava & Frankwick, 2011). In new product development, such learning helps firms not only explore new ways to reconstruct and transform their existing resources but also avoid repeating previous mistakes (Armstrong & Shimizu, 2007). Interactive learning from more alliance partners might, therefore, reduce product failure.

However, sharing knowledge with alliance partners entails risks that can be alleviated by building trust through high investments in relational capital to foster openness and exchange (Becerra et al., 2008). Firms with no alliances or only a few might enjoy less openness from potential partners due to uncertainty about their trustworthiness (Inkpen, 1998). Being able to signal reputation through several alliance partners will likely reinforce trustworthiness and, consequently, the openness of partner firms, enhancing the transfer of knowledge and helping allies “recognize dysfunctional routines and blind spots” (Becerra et al., 2008, p. 691). Because alliances embrace a variety of goals, having only one alliance could also limit learning to a specific area. Hence, simultaneously learning from several alliances would be more beneficial (D. Lee et al., 2017). Findings in the field of biotechnology suggest that firms with multiple alliances often combine explorative (e.g., basic research and drug discovery/development) with exploitative (e.g., clinical trials, FDA regulations, and sales) alliances (Rothaermel & Deeds, 2004). Therefore, we expect firms with low alliance activity to exhibit a greater recall likelihood, whereas firms with more alliances enjoy both exploration and exploitation competencies to reduce recalls.

Finally, we posit that greater alliance activity results in experience of alliances, which helps firms cope with alliance-specific challenges. Experienced firms can reduce misalignment with partners due to greater capabilities that help them develop routines in managing their alliance portfolio (Y. Wang & Rajagopalan, 2015). Firms that frequently engage in alliances also tend to have a dedicated alliance unit bundling their alliance capabilities (Kale & Singh, 2007; Y. Wang & Rajagopalan, 2015) and fostering learning economies of scale and scope (He et al., 2021; Rothaermel & Deeds, 2006). Inexperienced firms might risk more product failure, but with higher alliance activity, they would have fewer concerns with product quality and a lower product recall likelihood due to their learning curve. We hypothesize:

Hypothesis 2: Alliance activity has an inverted U-shaped relationship with product recall likelihood. Higher alliance activity is associated with higher product recall likelihood; however, beyond a tipping point, higher alliance activity is associated with lower product recall likelihood.

The Moderating Role of Market Turbulence

Following the idea of the RBV that “a firm’s resources are only meaningful in the context of its environment” (Nair et al., 2008, p. 1027), and recognizing the importance of environmental change in organizational learning (Greve, 2021), research has shown that contingency factors influence a firm’s strategy and growth, for example by affecting its exploitation and exploration activities (Narayanan et al., 2009; Titus & Anderson, 2018). One important factor found to impact firms’ external collaborations is market turbulence, “frequent and unpredictable changes in product preferences and customer needs, in product and production technologies, and in the competitive landscape” (G. Wang et al., 2015, p. 1930). Market turbulence makes it harder for a firm to predict current and future demands, shifts in technology, and other dynamics that influence its competitive position. Thus, turbulence pushes firms to innovate more radically and develop new products beyond their core businesses or markets (Van de Vrande et al., 2011). However, turbulence may also offer opportunities for innovations that serve changes in consumer preferences (Saboo et al., 2016). In contrast, stable environments are characterized by gradually shifting technologies and customer preferences and therefore allow firms to learn and innovate incrementally and to rely on established organizational routines (Miller & Friesen, 1983; Simsek, 2009). We argue that market turbulence impacts the relationships we hypothesize between CVC and alliance activities and product recall likelihood.

CVC investments are risky and exploratory because firms use them to acquire a stake in relatively new and innovative high-tech ventures (Drover et al., 2017; Van de Vrande & Vanhaverbeke, 2013). In turbulent markets where innovation is sought, investing firms can benefit from CVC deals, as they offer them a window to emerging technologies (Van de Vrande et al., 2011). However, firms under pressure often display heightened opportunism (G. Wang et al., 2015), which can lead to more and riskier CVC investments in areas beyond their core competencies (Van de Vrande et al., 2011). Due to the high uncertainty of future market needs, firms might even invest in competing technologies with yet unknown outcomes (Basu, Wadhwa, et al., 2016). Turbulence makes it harder for boundedly rational executives to find, evaluate, and manage suitable investments and absorb useful knowledge from them, thereby hampering organizational learning. Because CVC investments typically provide early-stage knowledge (Van de Vrande et al., 2011), its transfer into business units is both especially important and especially difficult under turbulence (Titus et al., 2014). In line with prior CVC research on the importance of the environmental context for organizational learning and the investing firm’s resource position (Greve, 2021; Titus et al., 2014; Titus & Anderson, 2018), we argue that in more turbulent markets, the constraints on successful learning are amplified. Firms will likely engage in more diverse, opportunistic, and risky CVC deals, leading to more product failures before the benefits of learning are realized. We hypothesize:

Hypothesis 3: Market turbulence moderates the inverted U-shaped relationship of CVC activity with product recall likelihood. Higher market turbulence shifts the inverted U-shaped curve upwards.

Prior studies have found that in turbulent high-tech environments, alliances can help firms reduce or spread risk (Murray & Mahon, 1993; Van de Vrande et al., 2011) and keep up with new technologies (Vanhaverbeke et al., 2002), but the uncertainty can make it hard to find the right partner and scope for an alliance (Srivastava & Frankwick, 2011). Gathering and evaluating ambiguous information in turbulent environments complicates decision-making because familiar heuristics lose their effectiveness (Maula et al., 2013) and more data needs to be processed to make informed decisions (G. Wang et al., 2015). In response, firms in unstable environments tend to govern their alliances especially carefully, with frequent information exchange between partners to alleviate their information asymmetry (Hung & Chang, 2012; Maula et al., 2013).The bilateral nature of alliances with mutual adjustments, resource sharing, and other joint activities likely spurs learning and thereby reduces risks of uncertain environments (Srivastava & Frankwick, 2011). In sum, in a turbulent market, the pressure on a firm to acquire external knowledge and innovation increases (Vanhaverbeke et al., 2002), and allies adjust their governance and exchange mechanisms accordingly. Thus, we argue that market turbulence will initially increase the likelihood of product recalls, but tighter governance and more frequent exchange between alliance partners will accelerate learning. A steeper learning curve will result, helping prevent product recalls with fewer alliances. We hypothesize:

Hypothesis 4: Market turbulence moderates the inverted U-shaped relationship of alliance activity with product recall likelihood. Higher market turbulence steepens the inverted U-shaped curve.

Methodology

Sample and Data

Research context

We analyzed firms that are significantly regulated by the FDA and that were on the S&P 500 index between 2009 and 2017. This approach ensures that our results are comparable, because the FDA sets the same standards for all recalls in the U.S. (Ball et al., 2018). To be significantly regulated by the FDA, a firm must meet one or more of the following three criteria (FDA, 2018b): the firm makes 10% of its sales share with products regulated by the FDA, it operates predominantly in FDA-regulated fields, and/or its activities are likely to result in the development of FDA-regulated products. This guarantees a comprehensive list of firms that could recall a drug. Our final sample consisted of 75 firms.

Variables

Dependent variable

We followed Ball et al. (2018) and focused our analysis on drug recalls published by the FDA to account for product recall likelihood. The FDA lists all recalls issued on its website in so-called weekly enforcement reports. We hand-collected all recall announcements from these reports for the years 2009 to 2017. The announcements contain specific information about the recall events, such as the name of the recalling firm, the date, the product, and the level of danger the product poses for customers. In line with prior research about FDA product recalls (A. J. Wowak et al., 2015), we focused only on Class I and II recalls, the most severe for both firms and consumers. Following existing management literature (Kashmiri et al., 2017; A. J. Wowak et al., 2015), we used product recall likelihood as a binary variable (1/0) to account for the occurrence of product failures. The variable takes the value 1 if a company experienced at least one recall in the respective year and 0 otherwise, representing how likely it is for a firm to experience a product recall.

Independent variables

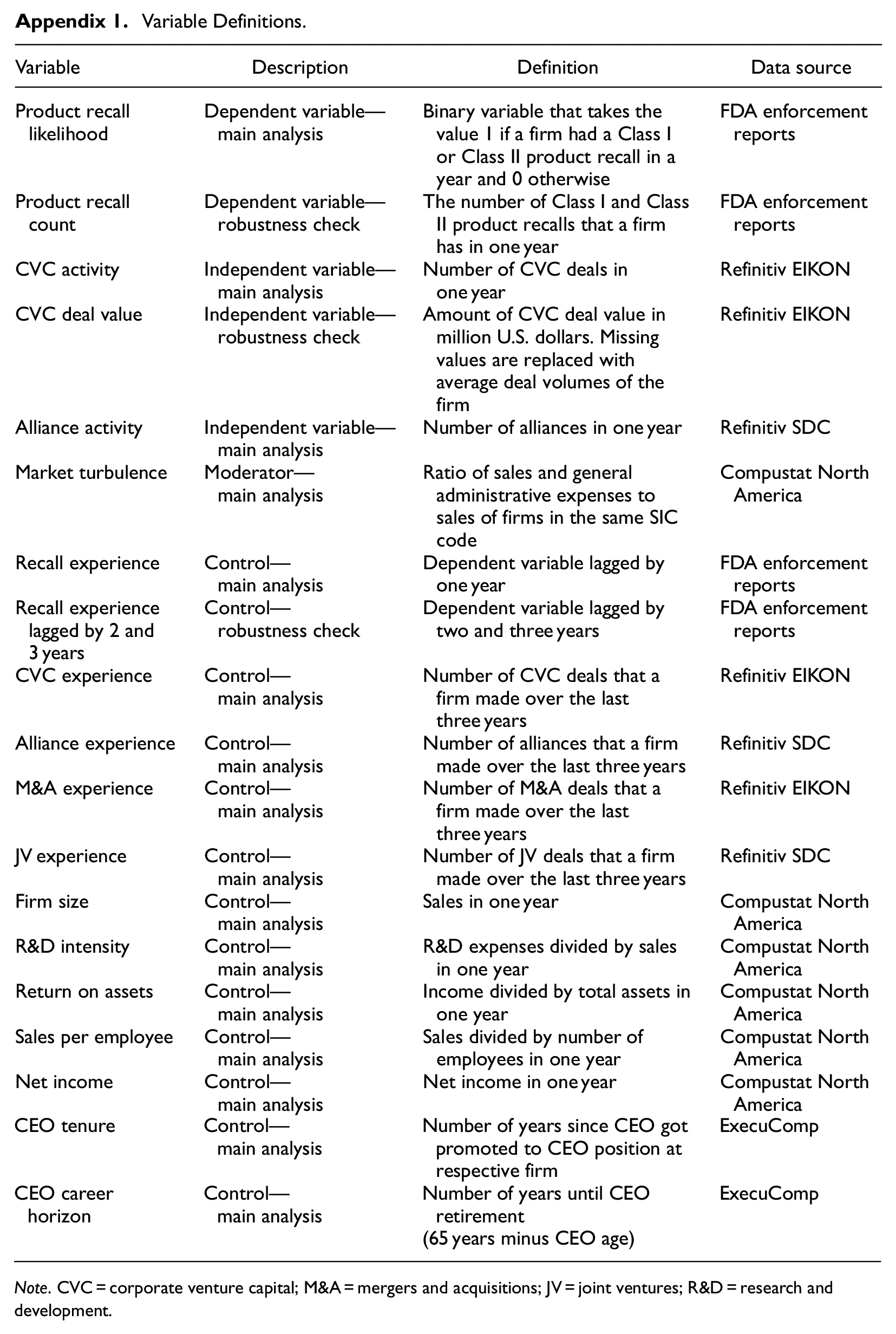

Following prior CVC research, we measured CVC activity as the number of deals a firm made in 1 year (Titus & Anderson, 2018). We collected the number of CVC deals made for all firms in our sample, their subsidiaries, and their respective CVC units from Refinitiv EIKON. We took the squared term of the number of CVC deals to test for the inverted U-shaped relationship. We lagged all focal variables by 1 year because of the time difference between a firm’s activities and the actual product recall. This follows prior recall research (A. J. Wowak et al., 2015) and mitigates reverse causality concerns.

To measure alliance activity, we used the number of alliances a firm made in 1 year, as done in prior alliance research (Mouri et al., 2012). We gathered this information from the Refinitiv SDC alliance database and included all signed non-equity alliances in our calculations. According to Schilling (2009), Refinitiv has the best coverage of alliance activity in the U.S.; recent research uses it (e.g., DesJardine et al., 2021).

Moderator variable

Market turbulence reflects the dynamics of environmental changes (Saboo et al., 2016). It is highly dependent on the type of industry (Segarra & Callejón, 2002) and corresponding customer preferences (Grewal & Tansuhaj, 2018). Following Saboo et al. (2016), we calculated market turbulence as the “ratio of sales and general administrative expenses to sales of firms in the same SIC code” (p. 9) as listed in Compustat. Compustat’s sales and general administrative expenses include selling, marketing, and market research expenses, which capture firm responses to shifting customer preferences (Saboo & Grewal, 2013). If a sector has stable customer preferences, such as in commodity markets (e.g., generics), firms have lower marketing and promotional expenses, whereas sectors with changing customer preferences require higher marketing and promotional expenses (Saboo & Grewal, 2013).

Control variables

We followed current recall literature (e.g., Ball et al., 2018) and controlled for recall experience, as past recalls can influence a firm’s likelihood of experiencing a recall again. Following prior recall studies (e.g., A. J. Wowak et al., 2015), we measured it as the lagged version of our dependent variable. We also controlled for certain firm characteristics. We controlled for prior external venturing experience by including the sums of all M&A, JV, CVC, and alliance deals a firm made over the last 3 years, as applied in previous research (e.g., Gamache et al., 2015). We gathered the information from the same sources as our independent variables. We controlled for firm size (sales) because large firms are more likely to have product recalls due to larger product portfolios. We controlled for R&D intensity because it can impact product recalls, as innovative companies have a higher chance of experiencing a recall (Mackelprang et al., 2015; Thirumalai & Sinha, 2011). We controlled for return on assets, sales per employee, and net income because these factors can influence product recall likelihood (Ball et al., 2018). Firm characteristics were gathered from the Compustat database. Because CEO characteristics are also associated with product recalls (A. J. Wowak et al., 2015), we controlled for CEO tenure and CEO career horizon. We collected CEO information from ExecuComp. Variable definitions are listed in Appendix 1.

Estimation Method

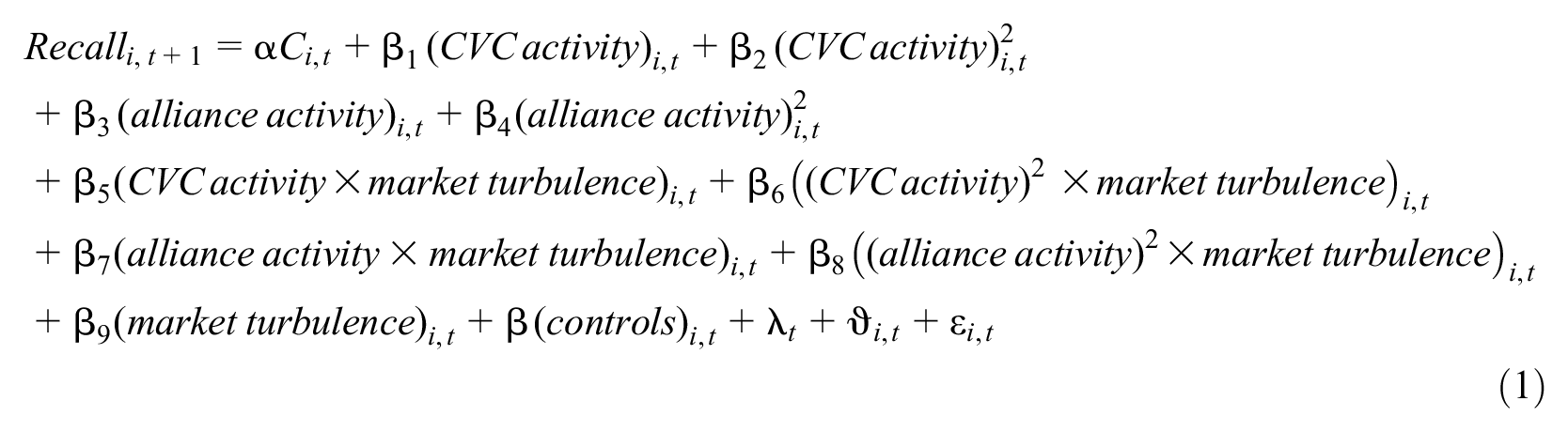

To test our hypothesized moderated relationships, we used the model shown in Equation (1):

where i represents the firms and t the different years. Recalli, t+1 is the likelihood of a firm to experience one or more product recalls 1 year after the CVC and alliance activity. We used generalized estimating equations (GEEs) for our regression analysis. This method was first developed by Liang and Zeger (1986) and is especially suited for the analysis of our dataset for three reasons. First, the regression type accounts for within-subject correlation of our dependent variable (Kalaignanam et al., 2012). Second, many of our observations are zero for all years for one firm. We need to include these observations in our regression as they contain relevant venturing information. GEEs account for these observations and, in contrast to fixed-effects models, do not exclude all firms where the observation is zero for all years from the analysis (Shah et al., 2017). Third, we have heteroscedasticity in our data that GEEs also control for (Shah et al., 2017). Because our dependent variable is binary, we follow A. J. Wowak et al. (2015) and use a binomial family with a logit link specification, an exchangeable correlation structure, and robust standard errors. This is in line with prior research that has a similar dependent variable (e.g., A. J. Wowak et al., 2015). We controlled for time-fixed effects (λt) and industry-fixed effects (ϑi,t) to account for potential time- and industry-series trends that are unobserved (A. J. Wowak et al., 2015). To test the presence of the hypothesized inverted U-shapes, three criteria must be fulfilled according to Haans et al. (2016). First, the coefficients of the squared terms in equation (1) (β2 and β4) have to be significant and negative (Haans et al., 2016). Second, the slopes of the curve have to be significantly positive at the low end of the data range of the respective independent variable and significantly negative at the high end of the data range (Haans et al., 2016). Third, the turning point and 95% confidence intervals need to be located in the data range of the independent variables. We tested the first criterion with the regression depicted in equation (1). To test the second and third criteria, we additionally performed a Fieller U-test for both quadratic relationships. Fieller’s (1954) approach provides information about slopes, confidence intervals, and the location of extremum points.

Results

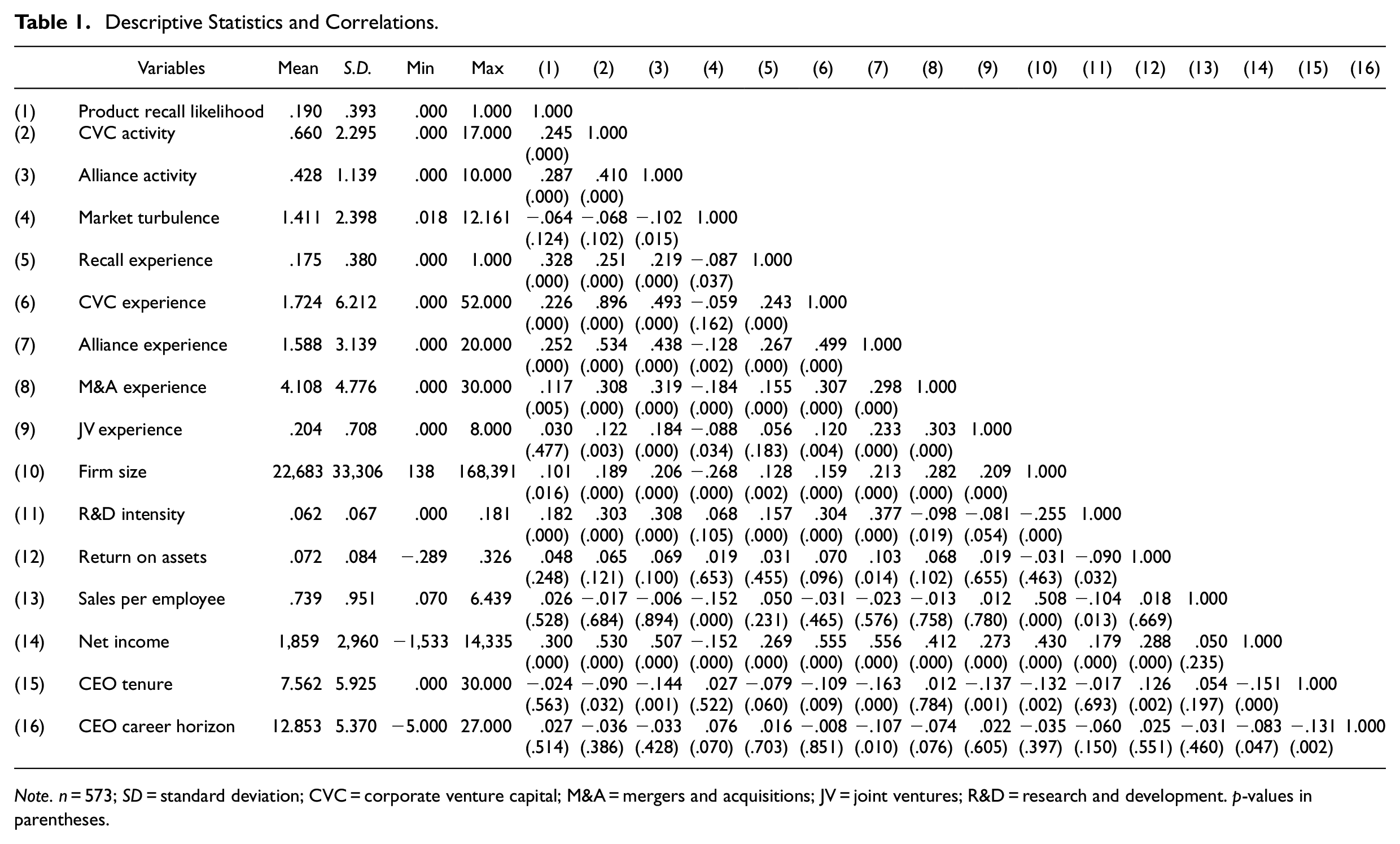

Table 1 shows the descriptive statistics and pairwise correlations. We see only one correlation larger than 0.6 between CVC activity and its respective experience term. To mitigate multicollinearity concerns, we calculated all regression models without the terms M&A, JV, CVC, and alliance experience and observed robust results. We also checked the variance inflation factors (VIFs) and condition indices to further assess multicollinearity concerns (e.g., Avkiran, 2018). The mean VIF value of our model is 1.85 and the highest value is 3.50, thus reducing multicollinearity concerns because the values are below the established threshold of 10 (Gómez et al., 2016). The condition number is 9.89 and is also below the established threshold (e.g., Ganco et al., 2020). Kalnins (2018) has asserted that the risk of multicollinearity cannot be fully mitigated by relying on low VIF alone. Therefore, we introduce a new model for each of our hypotheses in the regression table, as has been done in prior research (Mata & Alves, 2018). As we observe no sign flips of the coefficients of independent variables or other challenges, multicollinearity is not likely to bias our results.

Descriptive Statistics and Correlations.

Note. n = 573; SD = standard deviation; CVC = corporate venture capital; M&A = mergers and acquisitions; JV = joint ventures; R&D = research and development. p-values in parentheses.

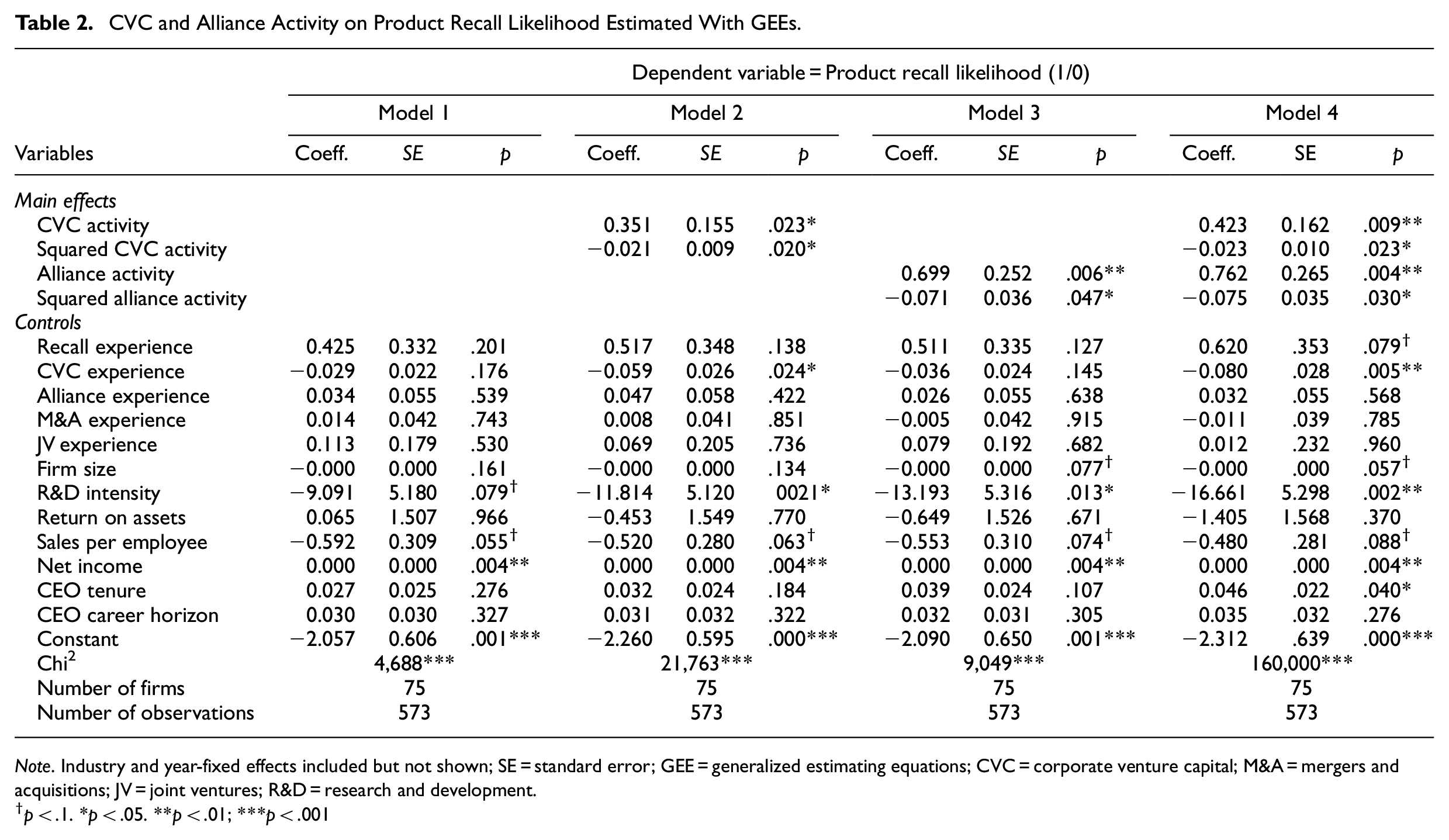

The results of the regression analysis of our main relationships are displayed in Table 2. Model 1 shows the effects of the control variables. Models 2 to 4 show the influence that CVC and alliance activity and their respective squared terms have on the likelihood of experiencing a product recall. Hypothesis 1 predicts an inverted U-shaped relationship between CVC activity and recall likelihood. We found a significant negative relationship between the squared CVC activity and product recall likelihood (Model 2: β = −.021, p < .05) which indicates the inverted U-shape relationship. Hypothesis 2 suggests that the relationship between alliance activity and product recall likelihood follows an inverted U-shape. We found a significant negative relationship between the squared alliance activity and product recall likelihood (Model 3: β = −.071, p < .05).

CVC and Alliance Activity on Product Recall Likelihood Estimated With GEEs.

Note. Industry and year-fixed effects included but not shown; SE = standard error; GEE = generalized estimating equations; CVC = corporate venture capital; M&A = mergers and acquisitions; JV = joint ventures; R&D = research and development.

p < .1. *p < .05. **p < .01; ***p < .001

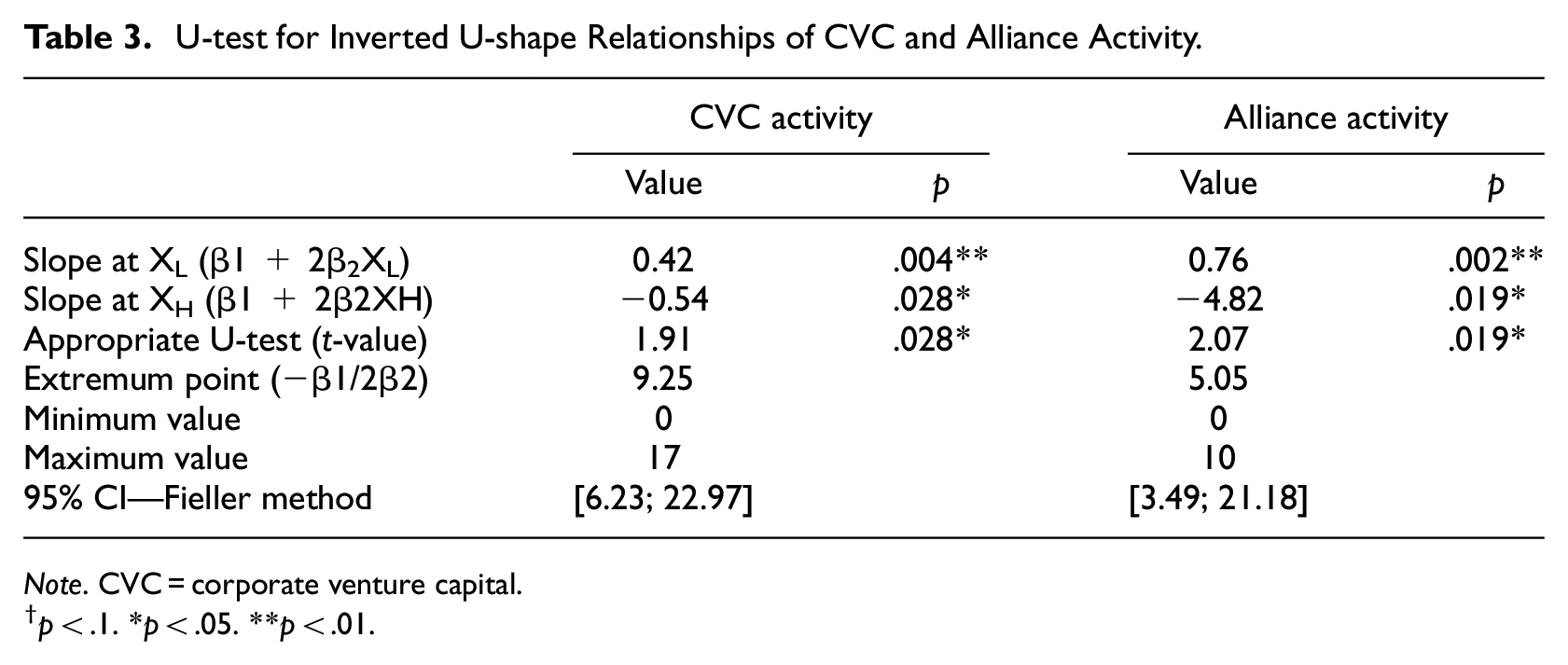

We followed the extant research and also performed a formal U-test, as proposed by Haans et al. (2016) to confirm the inverted U-shapes. Table 3 shows the results of the U-tests. All requirements for inverted U-shapes are met for CVC and alliance activity; the slopes at the low ends (XL) are positive, the slopes at the high end (XH) are negative and the extreme points lie within the Fieller intervals. All results are significant (p < .05). Taken together, our results support Hypotheses 1 and 2.

U-test for Inverted U-shape Relationships of CVC and Alliance Activity.

Note. CVC = corporate venture capital.

p < .1. *p < .05. **p < .01.

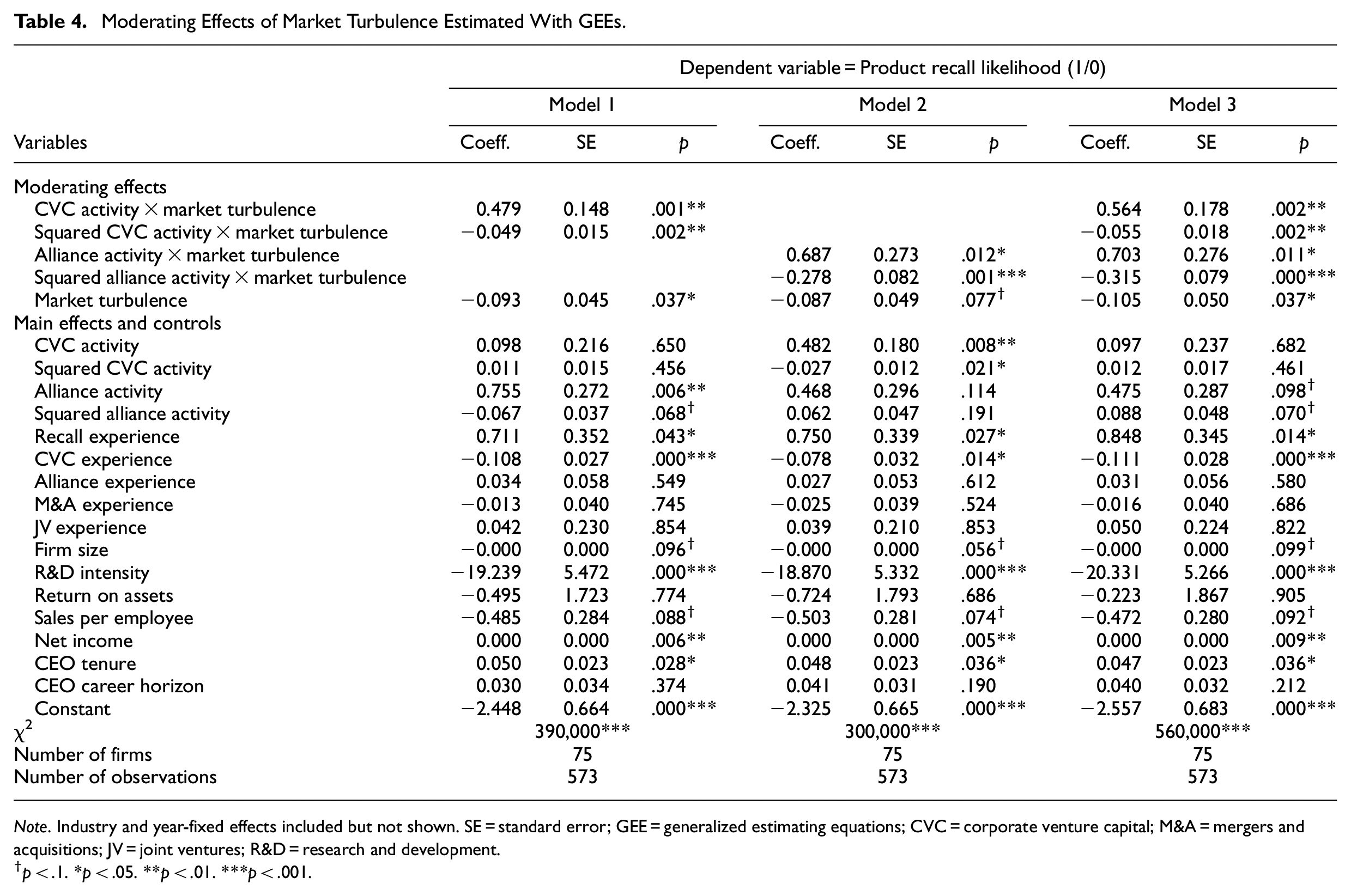

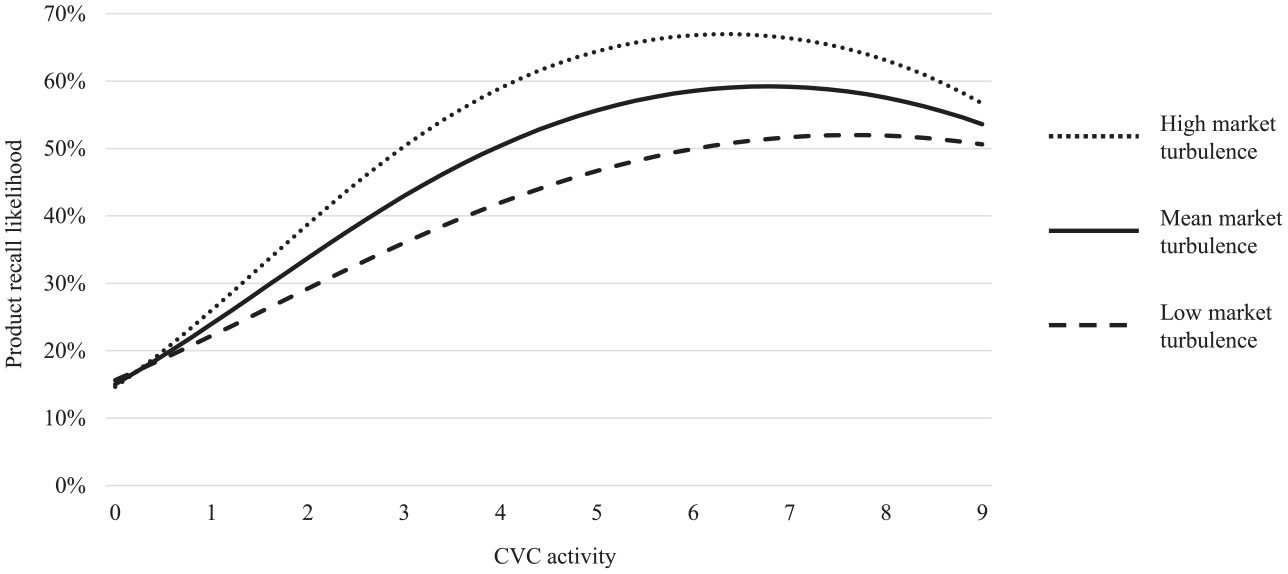

Hypothesis 3 predicts that the inverted U-shaped relationship between CVC activity and product recall likelihood is moderated by market turbulence. Table 4 shows the results of the moderation effects. According to Haans et al. (2016), testing for the moderation of a U-curve depends on the interaction term between the moderator and the squared terms of the independent variable. In Models 1 and 3 of Table 4, we see that the interaction effect of the squared CVC activity and market turbulence is statistically significant and negative (Model 1: β = −.049; p < .01). This supports Hypothesis 3, which posits that the inverted U-shaped relationship between CVC activity and product recall likelihood is moderated by market turbulence. In Models 2 and 3, the interaction term of the squared alliance activity and market turbulence is statistically significant and negative (Model 2: β = −0.278; p < .001). This supports Hypothesis 4, which predicted that market turbulence moderates the inverted U-shaped relationship between alliances and product recall likelihood.

Moderating Effects of Market Turbulence Estimated With GEEs.

Note. Industry and year-fixed effects included but not shown. SE = standard error; GEE = generalized estimating equations; CVC = corporate venture capital; M&A = mergers and acquisitions; JV = joint ventures; R&D = research and development.

p < .1. *p < .05. **p < .01. ***p < .001.

We plotted the interaction terms and show the results in Figures 1 and 2 to better interpret our results. High market turbulence levels are 30% above the mean and low turbulence levels are 30% below the mean (the ±1 standard deviation values are partially out of range). Figure 1 shows that firms that do not engage in CVC deals have a 15% likelihood of experiencing a product recall. We first look at the curve for mean levels of market turbulence. Firms with seven deals have a 59% likelihood (vertex). This likelihood then decreases to 53% for firms that make nine CVC deals. Market turbulence moderates the relationship between CVC activity and product recall likelihood such that high turbulence shifts the curve up (vertex at 67% and six CVC deals) and low turbulence shifts the curve down (vertex at 52% and eight CVC deals). The average cost of a recall is around $23 million 3 (Ernst & Young et al., 2011). Therefore, an increase of 44 percentage points in product recall likelihood from zero to seven CVC deals under mean levels of turbulence could lead to additional recall costs of $36.84 million, 4 which equals costs of $5.26 million per CVC deal. The average venture capital deal in the U.S. in 2019 had a size of $20.4 million (National Venture Capital Association, 2020). Thus, firms engaging in CVC deals pay 26% of the CVC deal value as recall costs under mean turbulence. For high turbulence, even higher recall costs of 36% occur.

The moderating influence of market turbulence on the relationship between CVC activity and product recall likelihood.

The moderating influence of market turbulence on the relationship between alliance activity and product recall likelihood.

Figure 2 shows the moderation for alliances and product recall likelihood. For mean levels of market turbulence, we see an increase from initially 16% to 34% (vertex) for two alliances. The slope converges to a 0% likelihood at around seven alliances. High market turbulence steepens the inverted U-shape, leading to a maximum recall likelihood of 36% (vertex), which decreases toward 0% at six alliances. The curve for low market turbulence looks more stretched out, with a peak at 35% between three to four alliances. It converges toward zero at around nine alliances. Based on the average cost of a recall (Ernst & Young et al., 2011), one could argue that—under mean market turbulence—an increase of 18 percentage points in the product recall likelihood from zero to two alliances would cost a company $15.07 million, 5 resulting in recall costs of $7.53 million per alliance. Prior research estimated that alliances create an average value of $44 to 65 million for a firm (Adegbesan & Higgins, 2011; Anand & Khanna, 2000; Kale et al., 2002). Thus, firms engaging in alliances pay 12% to 17% of the alliance value as product recall costs. Again, in turbulent markets, this value increases to 13% to 19%.

Robustness Checks

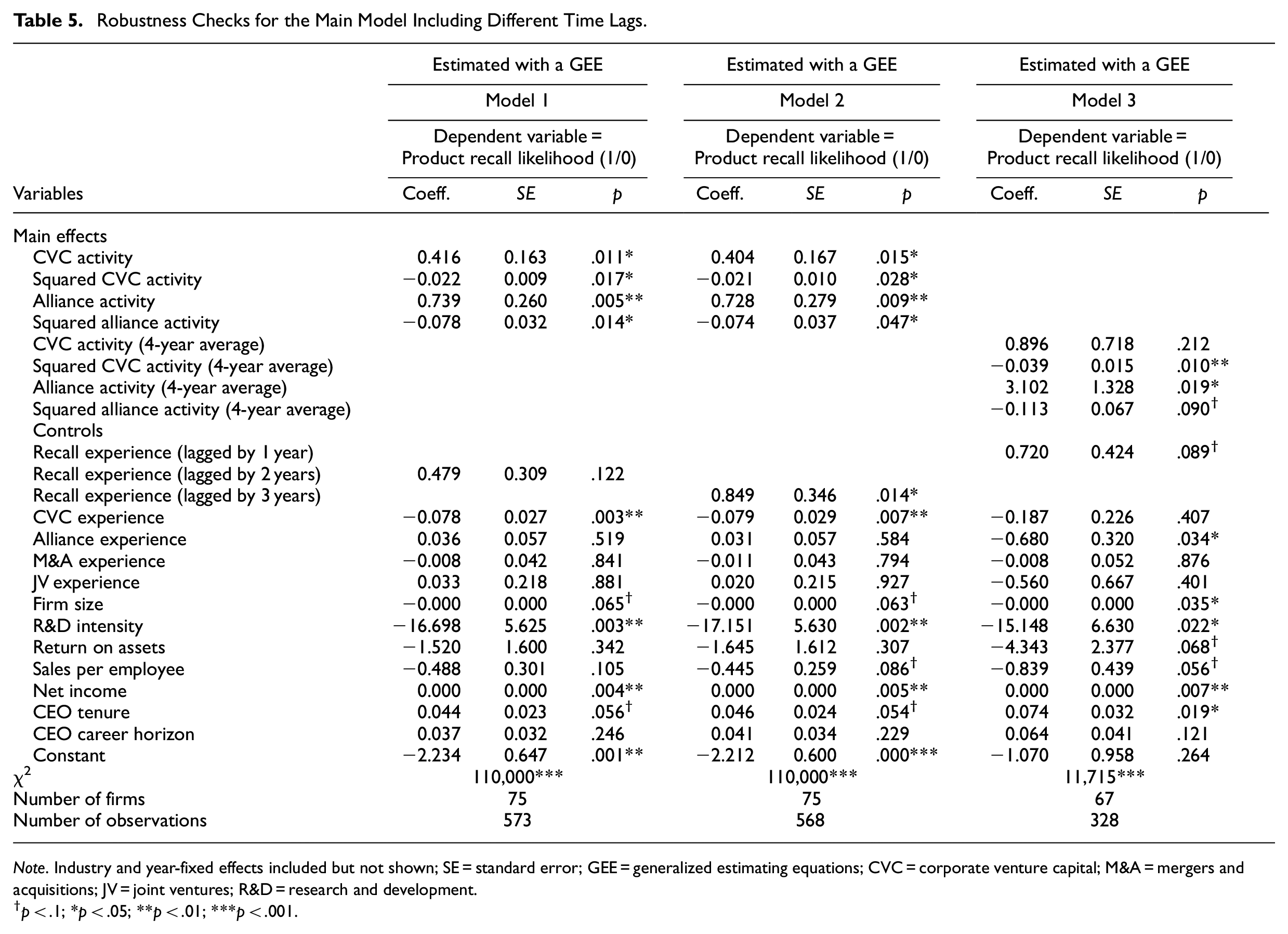

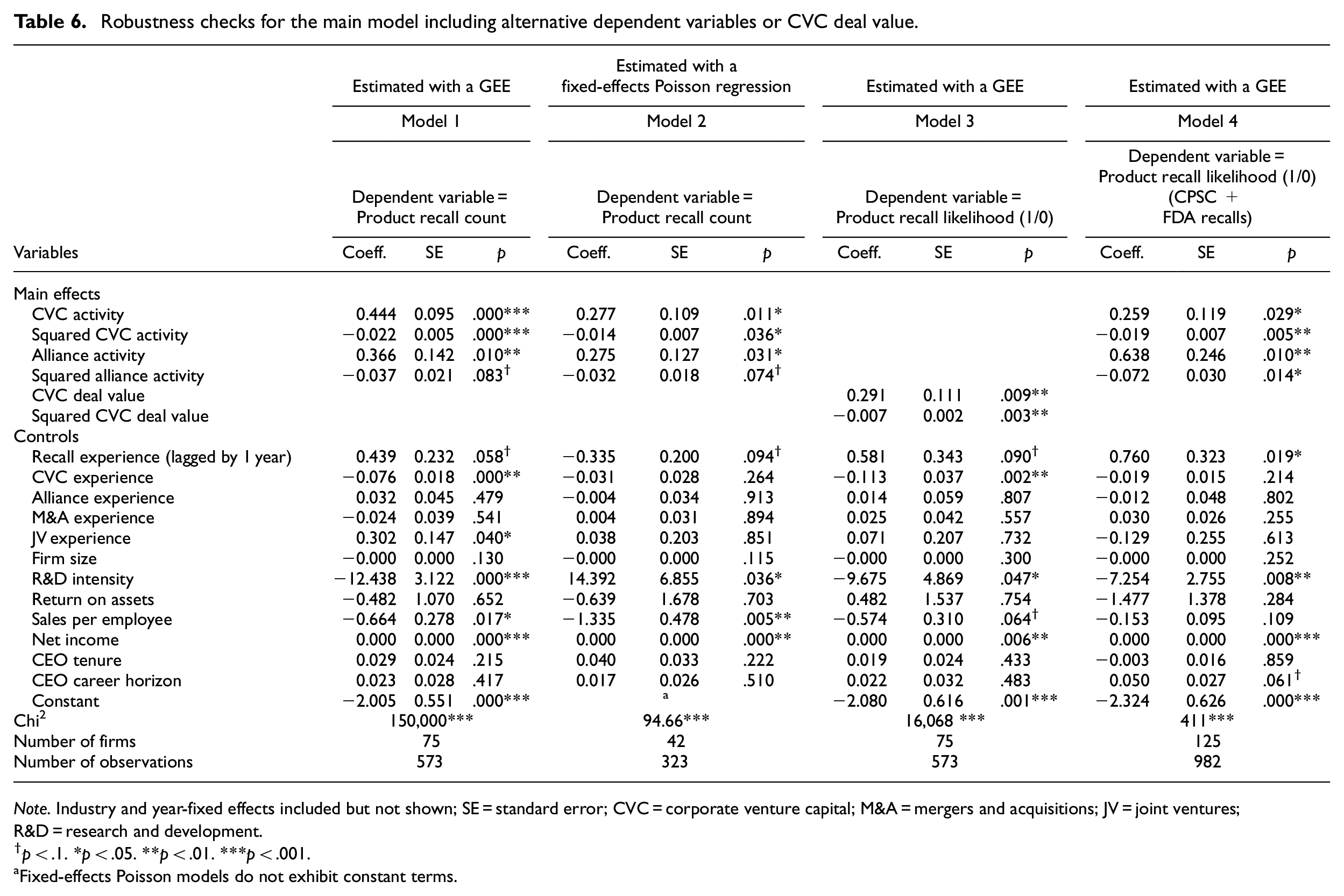

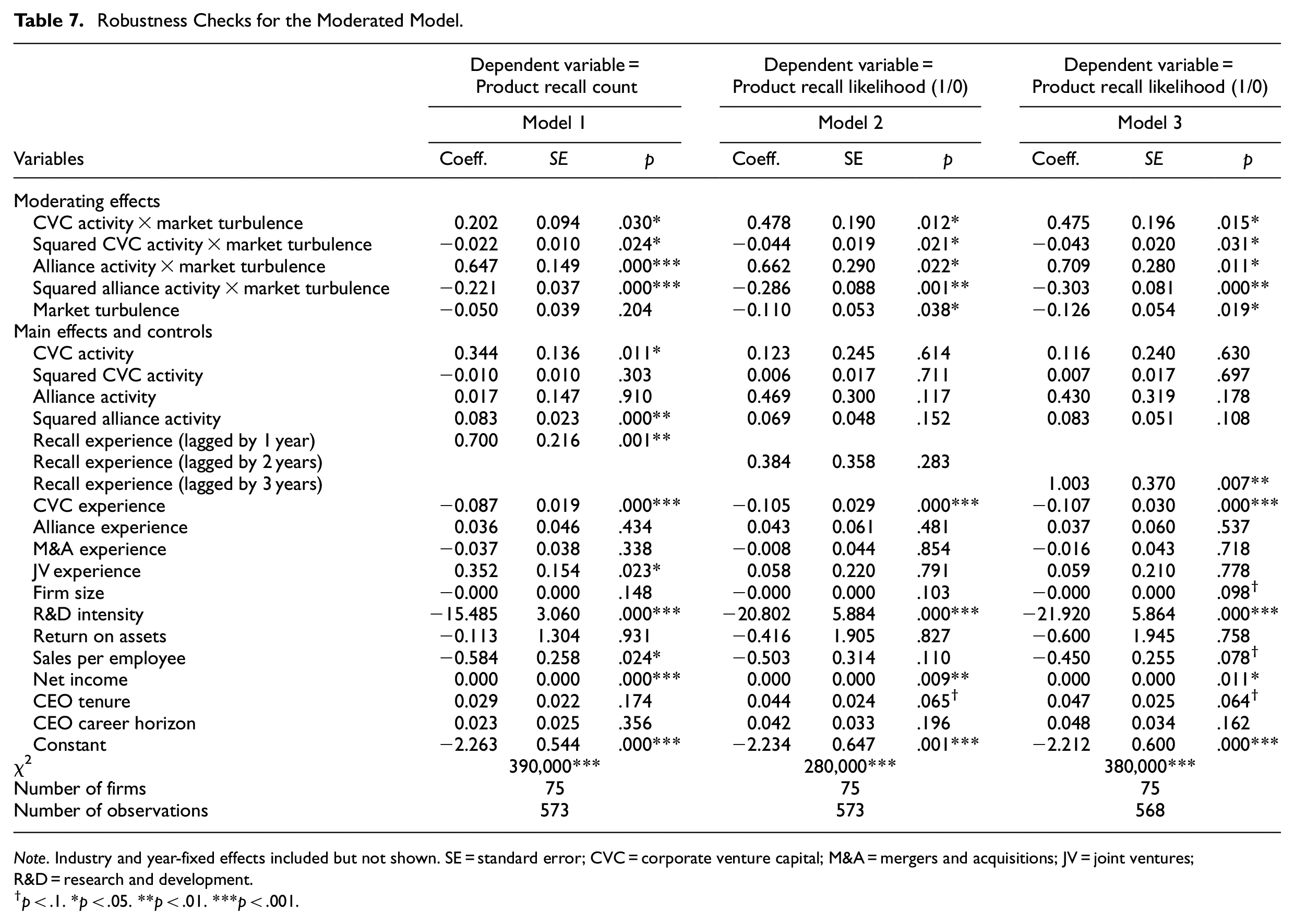

We performed several checks to ensure the robustness of our results (Tables 5–7). First, because product recalls could impact future product recalls for more than 1 year, we performed the regressions with recall experience lagged by 2 and 3 years and obtained similar results for the main model (Table 5, Models 1 and 2) and the moderated model (Table 7, Models 2 and 3). Prior research has found that most drugs and medical devices are recalled within 1 to 4 years (e.g., Ball et al., 2020; Lasser et al., 2002; Lexchin, 2014). We calculated the 4-year average of CVC and alliance deals a firm had before a product recall to account for such potential longer time lags (Table 5, Model 3) because some CVC and alliance deals might affect a firm’s recall likelihood for more than 1 year. The squared alliance term showed lower significance at the 10% level. The other results remained stable. Second, to account for the quantity of recalls a firm has, we performed our regression with the variable recall count as an alternative dependent variable (Wowak & Boone, 2015). Recall count is the sum of Class I and Class II recalls that a firm has in the respective year. We calculated GEEs with an nbinomial log-link specification, an exchangeable correlation structure, and robust standard errors. The directions of the main effects shown in Table 6, Model 1, remained consistent. The squared term of alliance deals showed lower significance at the 10% level. The moderated model shown in Table 7, Model 1, is robust to the count dependent variable. Third, following prior research on CVC and innovation (Chemmanur et al., 2014; Wu, 2012), we additionally performed a fixed-effects Poisson regression to ensure that our estimation approach did not bias the results and to account for omitted firm-level time-invariant variables. However, fixed-effects models are not recommended for product recall studies, as many observations are omitted for firms with zero recalls (Shah et al., 2017). The results in Table 6, Model 2, confirm this when we lose more than 200 observations. Still, the coefficient directions aligned with those of the main regressions, increasing confidence in our results. Fourth, we also used CVC deal value in million U.S. dollars instead of deal count as an independent variable. Missing values were replaced with the average deal volumes of the firm (Gamache et al., 2015). We found that the main results hold (Table 6, Model 3). For non-equity alliances, there are no deal volumes. Fifth, we enlarged our sample of product recalls by adding product recalls issued by the Consumer Product Safety Commission (CPSC), which regulates the U.S. consumer goods industry, from 2008 to 2014. Therefore, we included firms that produce CPSC-regulated products for the robustness check. The results, listed in Table 6, Model 4, remained robust for the larger dataset of 125 firms and 982 firm-year observations from two different industries. Sixth, to further mitigate potential endogeneity issues caused by omitted variables, we employed a two-stage instrumental variable approach (results are not reported to conserve space). We used average industry alliance activity and industry CVC activity as instruments for our linear terms and squared industry alliance activity and squared industry CVC activity as instruments for our squared terms, as proposed by Haans et al. (2016). In the first-stage regressions, we see that the industry variables and their respective squared terms have significant power to explain CVC and alliance activity. In the second stage, we replaced our original independent variables with the predicted values from the first-stage regressions. The squared terms in the second stage remained statistically significant and negative; however, the squared term of the alliance instrument showed lower significance at the 10% level. Overall, our results were robust to different specifications.

Robustness Checks for the Main Model Including Different Time Lags.

Note. Industry and year-fixed effects included but not shown; SE = standard error; GEE = generalized estimating equations; CVC = corporate venture capital; M&A = mergers and acquisitions; JV = joint ventures; R&D = research and development.

p < .1; *p < .05; **p < .01; ***p < .001.

Robustness checks for the main model including alternative dependent variables or CVC deal value.

Note. Industry and year-fixed effects included but not shown; SE = standard error; CVC = corporate venture capital; M&A = mergers and acquisitions; JV = joint ventures; R&D = research and development.

p < .1. *p < .05. **p < .01. ***p < .001.

Fixed-effects Poisson models do not exhibit constant terms.

Robustness Checks for the Moderated Model.

Note. Industry and year-fixed effects included but not shown. SE = standard error; CVC = corporate venture capital; M&A = mergers and acquisitions; JV = joint ventures; R&D = research and development.

p < .1. *p < .05. **p < .01. ***p < .001.

Discussion

The goal of this study was to investigate how CVC and alliance activity influence a firm’s chance of experiencing a product recall and how market turbulence affects these two relationships. Our findings show that the relationships between CVC and alliance activity and product recall likelihood follow an inverted U-shape. We find that both relationships are moderated by market turbulence such that the inverted U-shapes will shift up (for CVC) and steepen (for alliances) if firms operate under high market turbulence.

Theoretical Implications

First, we advance entrepreneurship research that views external venturing as problemistic search activities aimed at renewing firms’ resource endowments through external sources (Belderbos et al., 2018; Titus et al., 2019). By identifying product recalls as a result of CVC and alliance activities, we give empirical evidence for adverse effects of external venturing and one of the first assessments of how these activities relate to a firm outcome with a broader strategic and even societal impact, responding to calls by Anokhin, Wincent, et al. (2016) and Drover et al. (2017). These insights extend the understanding of the potential risks of CVC deals and alliances but also their risk mitigation potential. Recalls might be a root cause that can help explain prior mixed findings on the financial value effects of external venturing (Huang & Madhavan, 2021; D. Lee et al., 2017), as they can severely affect firms’ market value.

The curvilinear results point to the interplay of contrasting mechanisms in CVC and alliance activities. Investigating tensions between risks and benefits of corporate venturing is a common theme in entrepreneurship literature (e.g., Covin & Miles, 2007) and more granular investigations of the positive and negative effects of strategic entrepreneurship have yielded important insights, for instance, around entrepreneurial orientation (Lomberg et al., 2017). However, while such contradictory effects have received attention in the more mature M&A research (e.g., post-merger integration) (King et al., 2021), the downsides have been largely overlooked in other fields of external venturing. Drawing on the RBV (Barney, 1991; Penrose, 1959) and recent suggestions to integrate it with learning theory (Greve, 2021), we attribute the inverted U-curves to a trade-off between the costs and subsequent benefits of CVC and alliance endeavors. Both activities aim to enhance a firm’s knowledge resources, but they also consume resources and entail risks. Therefore, we theoretically explain the inverted U-curves with two certain costs (search costs and learning costs) and benefits (objective knowledge benefits and experience learning benefits) derived from literature (e.g., Penrose, 1959; Wadhwa et al., 2016; Wiklund & Shepherd, 2009).

After an initial adverse effect of resource investments into the CVC and alliance activities and the departure from existing routines, the learning accumulated through and about these activities helps to absorb and integrate knowledge resources from partners and thus decrease a firm’s recall likelihood. This resonates with the RBV and learning theory, confirming that valuable resources are indeed hard to transfer between organizations (Barney, 1991) and that path dependency of learning routines complicates resource integration (Greve, 2021; Kor & Mahoney, 2004). The benefits of greater venturing activity underline the importance of experience learning, a central element in both RBV and learning theory, for external venturing success (Anand & Khanna, 2000; Fels et al., 2021).

Second, our investigation of the venturing–recall relationship helps to connect the thriving product recall literature with the entrepreneurship literature. Although product recall scholars have argued that acquisitions can lead to structural discontinuities in a firm, causing product recalls (Mukherjee & Sinha, 2018), we are, to our knowledge, the first to find that recalls can also be caused by minority investments and non-equity alliances. In doing so, we add an entrepreneurship and strategic renewal perspective to the limited research on recall antecedents (Shah et al., 2017; K. D. Wowak & Boone, 2015). Our results further show that firms that want to reduce their recall likelihood may profit more from alliances than from CVC deals. Interestingly, in contrast to CVC deals, firms with many alliances can decrease the likelihood of a recall to zero. In this way, our study provides insights into how firms can align their venturing activities while maintaining, or even improving, product safety.

Third, by investigating the contingency effects of market turbulence on firms’ product quality, we add further nuance to the understanding of the curvilinear relationships. While there is consensus that external venturing modes vary in terms of the risks they entail, detailed comparisons of the risk profiles of different modes under different conditions are rare (Titus et al., 2019). From our resource-based learning perspective, market turbulence exerts greater pressure on firms to innovate but, at the same time, renders their existing resources and learning routines less useful due to ambiguity and changing customer needs (G. Wang et al., 2015). We consistently find that both relationships are amplified in turbulent markets. However, the exact effects of CVC and alliance activities on recall likelihood differ. Under high turbulence, the failure risk of CVC increases, indicating greater learning difficulties. For alliances, the initial adverse effect becomes greater but firms also enjoy greater subsequent learning benefits per alliance under turbulence.

Adding to scarce research that simultaneously investigates different external venturing modes (e.g., Titus et al., 2019; Wiklund & Shepherd, 2009), we explain these findings with inherent differences between CVC deals and alliances, particularly in terms of their formal and informal governance and exchange mechanisms (e.g., Dushnitsky & Lavie, 2010; Van de Vrande & Vanhaverbeke, 2013). While CVC deals are typically unilateral financial investments without the investee having legal obligations to share knowledge or cooperate (Dushnitsky & Shaver, 2009), alliances are bilateral agreements featuring joint resource sharing and collaboration (Van de Vrande & Vanhaverbeke, 2013). The highest initial costs and steepest learning curve under high market turbulence confirm that firms tighten alliance governance in turbulent environments (Hung & Chang, 2012; Maula et al., 2013). For CVC deals, our results suggest that investors cannot successfully adjust the governance.

Affirming the contingency view of firm resources (G. Wang et al., 2015), our study emphasizes that in making strategic decisions concerning the mode of external knowledge and innovation sourcing (Titus & Anderson, 2018; Vanhaverbeke et al., 2002), firms should consider not only their own resource position but also their market environment (Covin & Slevin, 1989). We hope that our insights help researchers explain why some firms can gain competitive advantage through external venturing while others cannot. Our study shows that this is because the value of venturing activities depends on a firm’s idiosyncratic learning curve and the turbulence of its environment. Considering learning theory can complement RBV to understand why similar resources have different values.

Overall, our study contributes to research that extends the RBV beyond the focal firm’s boundaries (Drover et al., 2017; Eisenhardt & Schoonhoven, 1996) and addresses calls to integrate RBV with organizational theories (Davis & DeWitt, 2021; Greve, 2021). Integrating learning theory and RBV enhances our understanding of firms’ resource boundaries and responses to environmental contingencies (Furr & Eisenhardt, 2021; Greve, 2021). RBV-based research has argued that firms in emergent or highly competitive industries, or that pursue pioneering strategies, engage in external venturing to enhance their resource position (Das & Teng, 2000; Eisenhardt & Schoonhoven, 1996). We extend this research on the why of external venturing by giving insights into the how and, in particular, the effectiveness of external venturing. We provide empirical underpinning for external venturing as problemistic search for valuable resources outside the firm that promises benefits but “is also fraught with risks” (Titus et al., 2019, p. 648). In fact, we find that it is almost always fraught with the risk of failure in terms of increased recall likelihood—except for high alliance activity.

Our findings suggest that the mode and intensity of external search are important (Posen et al., 2017), thereby highlighting the role of boldness for corporate venturing (Lumpkin & Dess, 1996). How, and under what conditions, firms engage in it makes a difference. In line with learning theory, the curvilinear relationships confirm the dilemma of problemistic search because “a firm must carve out resources […] by reducing the amount of resources invested in other activities” to improve its competitive position (Posen et al., 2017, p. 224). This finding helps to explain the initial negative effects of CVC and alliance activities and echoes the point that problemistic search only identifies potential solutions for resource improvements but does not always lead to improvements (Cyert & March, 1963; Titus et al., 2019). Considering the number or volume of external venturing activities as RBV-based indicators for valuable resources (King et al., 2021) and thus a proxy for the intensity of problemistic search (Posen et al., 2017) might enable further comparative research on external venturing modes.

Practical Implications

Our results offer insights for corporate decision makers and regulating agencies, such as the FDA, to help prevent product recalls. First, we create awareness of how CVC deals and alliances can result in product recalls, which can assist executives’ strategizing. We found that either no or bold external resource-seeking pays off more than small-scale initiatives. Firms with little experience in external venturing activities should focus closely on product quality after their first CVC or alliance investment. Our results further indicate that greater experience leads to better CVC and alliance outcomes in terms of product quality. Firms may therefore avoid low-scale stuck-in-the-middle strategies, which disrupt existing routines and consume resources but do not yield enough complementary knowledge and learning benefits. Executives should also consider the market environment. In turbulent markets, alliances, rather than CVC deals, appear more helpful in avoiding product recalls.

Second, our study informs executives and regulating bodies about the economic and societal significance of potentially negative outcomes from CVC deals and alliances and how venturing can increase or mitigate recall likelihood. Based on the likelihood estimates, firms might lose up to 36% of their CVC or 13% to 19% of their alliance deal value through product recalls. Under high market turbulence, this implies recall costs as high as $43.53 million resulting from six CVC deals or $16.74 million from two alliances. Executives should be aware that these are averages and that single recall events can be much more expensive. In a study on medical devices, Fuhr et al. (2013) reported that single incidents cost firms up to $600 million—costs of lawsuits not yet included. Still, high alliance activity can help mitigate these costs. Thus, firms affected by quality issues may seek alliances as a solution. On the other hand, regulating agencies, such as the FDA or CPSC, should be aware of the benefits and perils of firms’ engagements in corporate venturing. To identify and remove harmful products promptly, these agencies could monitor firms with CVC or alliance engagements more closely, especially when these firms have just started their engagements.

Limitations and Avenues for Future Research

Our study has limitations that offer research opportunities. We conducted our analysis at the firm level. Although we grounded our hypotheses in the RBV and learning theory, we did not explicitly measure the internal trade-off between costs and learning benefits, with which we theoretically explain our curvilinear findings. Future studies could investigate the internal processes that stand between increased CVC or alliance activities and product recalls. Like inquiries into post-merger integration in M&A research (King et al., 2021), inquiries into the post-investment integration of CVC deals and alliances could yield important insights. Moreover, firms might be quite different in terms of their organizational structures, processes, and resources. For instance, firms with experienced CVC/alliance managers or dedicated units might reduce the likelihood of product recall earlier. Furthermore, we investigated only the number of CVC and alliance deals, but our robustness test with CVC deal value opens up future research directions. One could examine how the type, scale, and scope of alliances and CVC deals influence product recalls. Studies on the level of the recalled products could also offer additional insights in this regard.

Finally, our sample consisted only of FDA-regulated S&P 500 firms. This is common in recall research (e.g., Eilert et al., 2017) because it ensures consistency in recall standards and increases the study’s internal validity. It is also recommended for studies using the RBV to reduce sample heterogeneity (Lockett et al., 2009) because the RBV explains inter-firm performance variations by means of a firm’s idiosyncratic resources instead of industry differences (Penrose, 1959). Nevertheless, this approach limits the generalizability of our findings. Our robustness test with additional CPSC data indicates the potential generalizability of our results to the consumer goods industry, but future research should test our findings for other industries and economies.

Footnotes

Appendix

Variable Definitions.

| Variable | Description | Definition | Data source |

|---|---|---|---|

| Product recall likelihood | Dependent variable—main analysis | Binary variable that takes the value 1 if a firm had a Class I or Class II product recall in a year and 0 otherwise | FDA enforcement reports |

| Product recall count | Dependent variable—robustness check | The number of Class I and Class II product recalls that a firm has in one year | FDA enforcement reports |

| CVC activity | Independent variable—main analysis | Number of CVC deals in one year | Refinitiv EIKON |

| CVC deal value | Independent variable—robustness check | Amount of CVC deal value in million U.S. dollars. Missing values are replaced with average deal volumes of the firm | Refinitiv EIKON |

| Alliance activity | Independent variable—main analysis | Number of alliances in one year | Refinitiv SDC |

| Market turbulence | Moderator—main analysis | Ratio of sales and general administrative expenses to sales of firms in the same SIC code | Compustat North America |

| Recall experience | Control—main analysis | Dependent variable lagged by one year | FDA enforcement reports |

| Recall experience lagged by 2 and 3 years | Control—robustness check | Dependent variable lagged by two and three years | FDA enforcement reports |

| CVC experience | Control—main analysis | Number of CVC deals that a firm made over the last three years | Refinitiv EIKON |

| Alliance experience | Control—main analysis | Number of alliances that a firm made over the last three years | Refinitiv SDC |

| M&A experience | Control—main analysis | Number of M&A deals that a firm made over the last three years | Refinitiv EIKON |

| JV experience | Control—main analysis | Number of JV deals that a firm made over the last three years | Refinitiv SDC |

| Firm size | Control—main analysis | Sales in one year | Compustat North America |

| R&D intensity | Control—main analysis | R&D expenses divided by sales in one year | Compustat North America |

| Return on assets | Control—main analysis | Income divided by total assets in one year | Compustat North America |

| Sales per employee | Control—main analysis | Sales divided by number of employees in one year | Compustat North America |

| Net income | Control—main analysis | Net income in one year | Compustat North America |

| CEO tenure | Control—main analysis | Number of years since CEO got promoted to CEO position at respective firm | ExecuComp |

| CEO career horizon | Control—main analysis | Number of years until CEO retirement (65 years minus CEO age) |

ExecuComp |

Note. CVC = corporate venture capital; M&A = mergers and acquisitions; JV = joint ventures; R&D = research and development.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed the receipt of the following financial support for the research, authorship, and/or publication of this article: We would like to thank the State of North Rhine-Westphalia’s Ministry of Economic Affairs, Industry, Climate Action and Energy as well as the Exzellenz Start-up Center. NRW program at the REACH – EUREGIO Start-Up Center and the Center for Entrepreneurship & Transfer for their kind support of our work.