Abstract

Research shows that early internationalization is more likely when founders have international and business-related experience. But what if experience was obtained in other ways? We study the scientist-founders of 149 academic spin-offs (ASOs), using cognition theory to argue for a curvilinear relationship between breadth of pre-founding R&D collaboration and internationalization timing. Our longitudinal study combines survey and patent data to show that increased breadth of collaboration with international scientists increases and then decreases the likelihood of early internationalization. The results are similar but less robust for collaboration with industry partners. Our findings suggest that studies on experience in new venture internationalization underestimate the role of R&D collaboration and the research-based heritage of many new firms.

Keywords

Research in international entrepreneurship draws attention to a striking characteristic of some new ventures: their early entry into foreign markets (Coviello & Munro, 1997; Oviatt & McDougall, 1994; Sapienza et al., 2006). One common explanation for early internationalization is that founders bring relevant knowledge to their new venture if they have, for example, sold to foreign markets or worked abroad (Reuber & Fischer, 1997) or have managerial experience in international markets (Sapienza et al., 2006). The knowledge derived from such experiences appears to help expedite internationalization decisions such that foreign market entry occurs soon after the firm is founded (Bruneel et al., 2010; Casillas et al., 2015; De Clercq et al., 2012). In turn, early internationalization increases the growth of a new firm’s international share of sales (Autio et al., 2000; Hilmersson et al., 2017).

However, what happens when founders were scientists in a research organization? This describes most “scientist-founders” of academic spin-offs (ASOs), a vital yet understudied organizational context in the international entrepreneurship literature (Kriz & Welch, 2018; Styles & Genua, 2008). From studies in academic entrepreneurship, we know that ASOs convert basic research and nascent technologies into value-creating innovation (Fini et al., 2019; Perkmann et al., 2021). As a result, their leaders need to understand both their new technologies and the market (Molner et al., 2019; Visintin & Pittino, 2014). ASO founding teams are, however, quite homogenous (Ensley & Hmieleski, 2005), with knowledge specific to, and focused on their scientific domain. This means they tend to have limited knowledge about markets or industries (Knockaert et al., 2011; Vohora et al., 2004). And, although Naldi et al. (2020) suggest that scientist-founders can assess the international potential of their new technology, others argue they lack the experience and knowledge needed for internationalization (Bjørnåli & Aspelund, 2012; Franco-Leal et al., 2016; Pettersen & Tobiassen, 2012).

Despite these reservations about ASOs from the literature, their new technologies are typically intended for global markets (Kriz & Welch, 2018; Styles & Genua, 2008). Prominent examples include Genentech (biotechnology), Oxford Nanopore (DNA sequencing), OpenText (enterprise information management software), Menlo Systems (optical measurement technology), or Logitech (electronics). Styles and Genua (2008) are some of the earliest scholars to identify ASOs as an important yet neglected category of firms that internationalize, along with Nordman and Melén (2008) and more recently, Kriz and Welch (2018) and Civera et al. (2019).

One type of pre-founding experience specific to scientist-founders of ASOs is collaborative R&D. This involves “defining and conducting R&D projects jointly by enterprises and science institutions” (Debackere & Veuglers, 2005, p. 322). R&D collaboration allows partners to share resources and risks, and diversify their knowledge base (Husted & Michailova, 2010). As Dodgson (1992) argues, the linkages that develop through R&D collaboration encourage effective transfer of knowledge, and they can provide access to global technologies and markets. This leads us to ask: As a common type of pre-founding experience for scientist-founders, what role does R&D collaboration play in an ASO’s internationalization timing?

To begin to address this question, we draw on cognition theory. With the premise that founders bring their experience to a new venture (Beckman, 2006; Boeker, 1989), an ASO’s founding team members will have been imprinted by their involvement with R&D collaboration. In turn, they imprint their ASO as creators of a new organization (Boeker, 1989; Marquis & Tilcsik, 2013). We argue that if scientist-founders had pre-founding experiences with R&D collaboration, they will have developed cognitive diversity, that is, variation in cognitive resources including their beliefs and preferences (Miller et al., 1998). The greater the experience breadth (i.e., the total range or scope of individual founding members’ R&D collaboration experiences available to the team), the greater the cognitive diversity in the founding team. The benefits of cognitive diversity (e.g., enhanced creativity, problem-solving) are expected to enhance the possibility of early internationalization because they can improve the nature and timing of actions, one of which is initial entry to foreign markets. However, experience breadth can also lead to complexity-induced cognitive load (Kirschner et al., 2009; Sweller, 1988). This is when excess demands are placed on working memory, storage, and information processing (Sweller, 1988). As a consequence, cognitive load can impair scientist-founders’ attention to new information and their ability to act quickly (Laamanen et al., 2018). This suggests that early internationalization will become less likely. Accordingly, we reason there are inverse U-shaped relationships between (1) pre-founding R&D collaboration experiences with industry partners or international scientists and (2) the likelihood of early internationalization.

Using a longitudinal study combining survey and patent data, we examine the founding teams of 149 new ventures spun out of universities and public research institutes in Germany. As expected, we find curvilinear results whereby lower, or higher, breadth of either type of pre-founding collaboration reduces the likelihood of early internationalization. The results for industry partners are, however, less robust. We also see that the internationalization timing of ASOs benefits more from pre-founding R&D collaboration activities than, for example, prior international work experience or business experience.

Given technology firms provide the organizational context for much research in both international and academic entrepreneurship, our results are theoretically and practically relevant, and they offer a number of contributions. First, we take a novel approach to study the internationalization timing of new ventures by applying cognitive diversity theory and cognitive load theory to frame our arguments regarding a nonlinear relationship between experience breadth and time to first international revenues. This contributes to the international entrepreneurship literature by replacing a linear relationship with an inverted U-shape relationship. Second, we identify a new type of breadth liability, complementing Mannor et al. (2019). That is, in ASOs, the scientist-founders’ experience breadth with pre-founding R&D collaboration helps shorten the time to first international revenues—but only to a certain point. After that, experience breadth brings no further acceleration due to increased cognitive load, that is, internationalization timing slows.

Third, we conceptualize and measure experience in a new and distinct way by considering the breadth of scientist-founders’ pre-founding experiences with R&D collaboration involving different types of partners. This approach also offers a fresh way to consider “international” experience, and it further develops our theoretical understanding of drivers of academic entrepreneurship and early internationalization. Fourth, we show the particular benefits that come when scientist-founders have pre-founding R&D collaboration with other (international) scientists, as compared to industry partners. This suggests that the scientist imprint identified by Hahn et al. (2019) is beneficial rather than detrimental in terms of early internationalization, and their pre-founding collaboration experience in the lab should be leveraged. Finally, these and other findings respond to calls for a better understanding of what prospective entrepreneurs bring from academia as a legacy to bridge the gap to both business (Bellini et al., 2019; Nikiforou et al., 2018) and internationalization (Siegel & Wright, 2015).

Theory and Hypotheses

We comment first on the decision context and theoretical framing of this study. At a general level, internationalization involves a number of decisions including when the firm should enter its first foreign market (aka internationalization timing). Although this is just one dimension of internationalization speed (Casillas & Acedo, 2013; Vermeulen & Barkema, 2002), it is considered an important strategic choice because it involves “the adoption of courses for action and the allocation of resources necessary for carrying out these goals” (Chandler, 1962, p. 14). The relevance of internationalization timing is seen in Yu et al.’s (2011) argument that it is an initial “milestone that a firm reaches in overseas expansion and signals the acceptance of a firm by foreign customers.” Furthermore, Criaco et al. (2021, p. 3) argue that early internationalization is particularly important for new ventures because they need to “seize fleeting opportunities in an increasingly competitive and international environment.”

From a theoretical perspective, we use cognition theory to frame our arguments, assuming that cognition and its related knowledge structures derive from the backgrounds and prior experiences of decision-makers. As explained by Walsh (1995), knowledge structures act as mental templates (aka frames of reference, cognitive maps). When a team forms, “some kind of emergent collective knowledge structure is likely to exist” (Walsh, 1995, p. 291) that will also act as a template to organize and give meaning to information and the environment. When decision-makers associate past experiences with new ones, they use these knowledge structures to engage with the new type of decision (Felin & Zenger, 2009). But why is cognition relevant to the internationalization timing of ASOs? For scientist-founders, a typical experience is R&D collaboration with external parties. This involves high levels of interaction and knowledge transfer, and we reason that R&D collaboration builds cognition that later guides scientists when they are in an ASO founding team. In other words, the cognition and related knowledge structures formed in one organizational context (R&D collaboration in a research institute) can later be relevant in another (internationalization timing of the ASO). Here, we focus on the concepts of cognitive diversity and cognitive load.

Cognitive Diversity and Cognitive Load

Cognitive diversity is defined as “differences in beliefs and preferences held by upper echelon executives within a firm” (Miller et al., 1998, p. 41; see also Horwitz & Horwitz, 2007).Theorizing in this area of research argues that members of a team bring unique cognitive resources to it (Hambrick et al., 1996; Horwitz, 2005). Some use multi-item measures to capture cognitive diversity, such as Miller et al.’s (1998) assessment of preference diversity regarding goals. In entrepreneurship, researchers tend to use the career histories of team members, on the assumption that diverse experience generates cognitive diversity. For example, Furr et al. (2012) examine the team’s prior work experiences to determine how technology change is influenced by the balance of “insiders” and “outsiders” on the team. Furr (2019) expands on this to study how the likelihood of product adaptation is influenced by team diversity, assessed by pre-entry breadth and depth of industry experience, and type of experience. Interestingly, although some international entrepreneurship research is at the team level (e.g., Bruneel et al., 2018; Reuber & Fisher, 1997), relatively little work attends to team diversity. One exception is a recent study from Criaco et al. (2021, p. 3) that employs a Blau index to assess team diversity using the age, gender, ethnicity, and educational background of each member, arguing that it “contributes to action and speed.” They do not, however, link team diversity to cognitive diversity.

Our point of departure for the current study is Walsh’s (1995, p. 291) observation that: “…when a group of individuals is brought together, each with their own knowledge structure about a particular information environment, some kind of emergent collective knowledge structure is likely to exist.” Similarly, Fern et al. (2012) argue that entrepreneurial action is not only based in one’s own knowledge structures but is also “…a social process, as founders incorporate the experiences of others into their own knowledge structure.” These points suggest that if a team’s pre-founding experiences are characterized by social interaction and social processes, they could be relevant to later strategic choices in the new venture. Although some study the impact of shared prior experience on internationalization (e.g., Bruneel et al., 2018), their interest is in the shared experience with one’s team members. We believe other social processes are relevant. One is R&D collaboration, a core activity in ASOs.

Scientists consider collaborative R&D as an “admission ticket to an information network and a vehicle for the rapid communication of news about opportunities and obstacles” (Powell et al., 1996, p. 120). If they participated in pre-founding R&D collaboration, they were immersed in shared processes where cooperation was required (Chung & Jackson, 2013). Following from Greve and Taylor (2000) and Pierce and Delbecq (1977), this will have shaped their cognitions because innovation creation involves a social system of interactions where socialization, exchange, and learning are central (an argument that parallels those in entrepreneurship).

Following cognitive diversity theory, if R&D collaboration experiences involved scientist-founders working with domain “outsiders” such as industry partners, cognitive diversity should have developed. Scientist-founders may have also collaborated with international scientists. The latter are “insiders” (as per Furr et al., 2012) given they—like the ASO founders—are entrenched in their scientific domain (Dane, 2010; Fern et al., 2012). Yet they are also “outsiders,” offering, for example, an international perspective. As such, R&D collaboration with international scientists should also generate cognitive diversity.

Extrapolating from Furr’s (2019) findings regarding product adaptation, cognitive diversity should strengthen the ASO team’s ability to make less constrained decisions and take faster action. In the current study, that action is the timing of internationalization. However, if pre-founding R&D collaboration experiences were broad in nature, for either type of partner, excess cognitive load may develop. This can result in negative effects for team integration, communication, and coordination (Miller et al., 1998; Visintin & Pittino, 2014) and, consequently, have an adverse impact on decisions and actions. We consider these perspectives in the next sections and start by explaining the two types of R&D collaboration in this study.

Pre-Founding R&D Collaboration Experience

R&D collaboration involves different types of partner, each of which contributes unique mindsets (Molner et al., 2019) and types of knowledge (Un et al., 2010). If scientist-founders collaborated with industry partners for R&D, prior to founding their ASO, there was likely transfer of knowledge pertaining to business, industry, and customers, including how to understand a market or how to create product-market fit. If they collaborated with international scientists pre-founding, they may have identified new applications for the technology, or acquired some foreign market knowledge and expanded their international mindset, despite lacking their own experience with working, selling, or living abroad. These points suggest that both types of R&D collaboration, that is, with industry partners or international scientists, can build cognitive diversity in a team of scientist-founders. However, we go beyond “type of partner” to consider the founding team’s breadth of experience with those partners. As noted above, for experience breadth, we consider the total range or scope of individual founding members’ R&D collaboration experiences available to the team. This is similar to, for example, Furr (2019) and Gruber’s (2010) consideration of the breadth of experience with different industries.

Industry Partners

Industry partners are what Furr et al. (2012) might refer to as “domain outsiders” for the scientist-founders of an ASO. This means they are cognitively distal (O’Connor et al., 2021) or from outside the scientist-founder’s focal area of expertise, and they have very different organization and institutional cultures, ways of managing projects, etc. (Bellini et al., 2019). Therefore, industry partners should bring new and complementary perspectives to decision-making (Criscuolo et al., 2018; Molner et al., 2019). For a scientist-founder, this creates new domain-spanning insight that, as explained by Fern et al. (2012), provides the opportunity for knowledge recombination and new solutions. As seen in D’Este and Perkmann (2011), for example, when universities have prior collaboration experience with industry partners, there is a positive impact on the ASO’s exploitation of opportunities.

If scientist-founders collaborated with industry partners for R&D, pre-founding, they may have tested the practical applications of their own research (Lee, 2000; Powell et al., 1996), learned about the importance of developing industry-relevant technology (D’Este & Perkmann, 2011; Sherwood & Covin, 2008) and the commercial elements of their new technology (Furr, 2019). Furthermore, because industry partners tend to have a shorter-term focus and quicker cycle time for decisions (D’Este & Perkmann, 2011; Molner et al., 2019), scientist-founders may have learned to work to faster deadlines. As one example, Molner et al. (2019) find that working with downstream actors (here, industry partners) can provide insights that help scientist-founders clarify user benefits for their new technology, identify and establish its market space, and quickly resolve any perceived market ambiguity. These arguments suggest that pre-founding R&D collaboration with industry partners should increase the likelihood of early internationalization because of the cognitive diversity that it generates. Even if cognitive conflict emerges, this could help improve decision quality (Amason, 1996).

At the same time, broad pre-founding R&D collaboration experiences could have a negative impact (Miller et al., 1998). For example, if many different industry partners were involved (creating high experience breadth), the knowledge structures that come into play or are used could be unconnected and idiosyncratic (Åstebro & Yong, 2016; Taylor & Greve, 2006). Consequently, the quality of decisions may diminish (Hwang & Lin, 1999) because of volume- and complexity-induced information overload. Experience breadth with outsiders such as industry partners could also lead to increased communication and integration costs (Hoisl et al., 2017) due to the potentially rich cognitive diversity that comes with this type of collaboration. Thus, decision processes could slow (Mannor et al., 2019). This means that beyond a certain level, the benefits of cognitive diversity from broad pre-founding R&D collaboration with industry partners will be offset by the costs of knowledge processing and integration.

The mechanism behind this argument pertains to cognitive load theory (Kirschner et al., 2009; Sweller, 1988) and the understanding that the working memory and cognitive abilities of individuals are limited (Miller, 1956). We reason that the cognitive diversity gained through pre-founding R&D collaboration with industry partners increases an ASO founding team’s cognitive load because of additional knowledge complexity. This can lead to founders feeling cognitively overwhelmed (Baron, 1998), unable to process more new content (Van Burg et al., 2022), and unable to make useful connections between different knowledge pools. As shown in Laamanen et al. (2018), excess cognitive load can prevent team members from effectively communicating their understanding of information, negotiating individual belief structures, and developing a deep understanding of the implications of strategic issues for the firm.

These arguments suggest a curvilinear relationship between breadth of pre-founding R&D collaboration with industry partners and the likelihood of early internationalization. We expect that internationalization timing will be slow when the founding team’s experience breadth with pre-founding R&D collaboration is low; it speeds up as experience breadth increases. At the same time, the benefits of cognitive diversity will be offset by the limitations presented by mounting cognitive load. At the point where the marginal benefit equals zero, we argue that the additional costs or burden of knowledge processing, coordination, and team integration increase disproportionately compared to the benefits that accrue from higher experience breadth in prior R&D collaboration with industry partners. That is, the benefits of this type of experience diminish. Our first hypothesis is as follows:

H1: For ASOs, there is an inverse U-shaped relationship between founders’ breadth of prior R&D collaboration experience with industry partners and the likelihood of early internationalization.

International Scientists

If international scientists were the partners for pre-founding R&D collaboration, they are “insiders” by virtue of being scientists. That is, they are more cognitively proximal (as per O’Connor et al., 2021) given their similar expertise in terms of scientific research. This means there is likely to be some shared cognition in the way the scientist-founders and international scientists perceive, interpret, and understand their environment (Ensley & Hmieleski, 2005). Extrapolating from Horwitz (2005) and Beckman (2006), these collaborators—all scientists—are likely to share a common technical language that enhances communication and synergy (O’Connor et al., 2021).

However, international scientists also represent a type of “outsider” because working with them can produce knowledge transfer beyond the development task of creating innovation. Examples include cognitively distal knowledge about different cultures and institutions (Perry-Smith & Shalley, 2014) or exposure to country-related expertise (Archibugi & Pianta, 1992). R&D collaboration with international scientists might also help scientist-founders learn how to identify new opportunities for their technology in a way they could not with industry partners (Gruber et al., 2013; Molner et al., 2019). As such, the ASO team’s resultant cognitive diversity could help reduce perceptions of uncertainty associated with serving foreign markets (De Clercq et al., 2012) and influence decisions such as internationalization timing. These arguments suggest that the likelihood of early internationalization should increase when scientist-founders have broad experience in pre-founding R&D collaboration with international scientists.

As with industry partners, however, problems related to cognitive load may arise because collaborating across an array of nationalities and being exposed to their varied knowledge about international markets can create awareness of, or concern about, country-specific variations. Scientist-founders could be overwhelmed by international market complexities if they have too much information to process (Baron, 1998). As per Dokko et al. (2009), this could lead scientist-founders to perceive high risk or costs due to their lack of task-specific knowledge and skills regarding internationalization. A diverse range of insights about foreign markets might also lead to misunderstandings or conflict among decision-makers regarding internationalization (Lee & Park, 2006; Miller et al., 1998) and collaboration with international scientists could reinforce scientist-founders’ comfort with the academic cycle of timing (Furr, 2019; Molner et al., 2019); timing that is typically slower than that found in industry.

Drawing on the above, we argue that although pre-founding R&D collaboration with international scientists can increase the cognitive diversity of scientist-founders, lead to perhaps better technology, and increase the likelihood of early internationalization, there is a downside. That is, if the ASO founding team collaborated with a broad range of international scientists, cognitive diversity becomes more complex. The additional cognitive load could lead to scientist-founders spending extra time on foreign market assessments, coordination, or decision-making, due to perceived risk and uncertainty. This could slow time to internationalization. The effect is similar to that for industry partners, but different sources of decisional ambiguity come into play. We hypothesize the following:

H2: For ASOs, there is an inverse U-shaped relationship between founders’ breadth of prior R&D collaboration experience with international scientists and the likelihood of early internationalization.

Method

We study ASOs and their founding teams. Such organizations are created by scientists from universities or other publicly-funded research organizations to commercialize a core technology developed from a scientific base in the parent organization. As per Clarysse and Moray (2004), the scientist-founders will have either left their parent organization to found the ASO or started operations while still affiliated with the parent. We consider ASOs and their founding teams appropriate for this study for a number of reasons. First, ASOs internationalize but receive little attention in the international entrepreneurship literature (Kriz & Welch, 2018; Styles, 2008). Second, they are an extreme example of a technology firm and, as such, might offer insights to the most commonly studied type of venture in international entrepreneurship. Third, ASOs offer a unique context to study (Valentin & Jensen, 2007), because for founders coming out of public research organizations (e.g., universities, research institutes) shared understanding and unique knowledge is embedded in their prior science- and technology-related experiences and affiliations (Clarysse & Moray, 2004; Vohora et al., 2004).

Sample and Data

The study is part of a larger project on ASOs in Germany and analyzes a unique, mixed-method, longitudinal dataset. To build this dataset, we began by screening directories from (a) university transfer offices, (b) public research organizations, and (c) major trade fairs. We also conducted internet searches and inspected print media. This led to a list of 1,339 potential firms. We were able to reach 1,009 firms by telephone and of those, 446 agreed to participate in the study. The identification of these firms and the collection of our first round of survey data occurred between 2005 and 2010 (i.e., the window of time used to build the initial database). Trained interviewers conducted on-site survey-based interviews with one founder per firm (n = 446). All participants were part of the firm’s original founding team and involved in the development of their ventures’ core technologies. Despite interviewing only one informant per firm, every member of each founding team was identified, and their information was validated using the German commercial register (Handelsregister).

In addition to collecting survey data, we incorporated variables derived from patent family applications in order to provide objective information on the R&D collaborations of all founders. Patents filed for application report the names and addresses of applicants and inventors. We used these as indicators of R&D collaboration between firms or individuals (cf. Bercovitz & Feldman, 2011; Picci, 2010) based on the assumption that inventors listed on the same patent document know each other and have exchanged information, even across national borders. These data were obtained from the “PATSTAT” database provided by the European Patent Office, released in October 2020. We include technological inventions where at least one member of the founding team is listed as inventor or applicant on the patent document. Boolean searches were employed to identify the founders in the PATSTAT database. To rule out the possibility of disambiguation errors, for example, the case of popular inventor names, we manually checked the content of the patent applications and the residence of the listed inventors and applicants. Members of the founding team were sometimes listed as “inventor” rather than “applicant” on the patent document. In these cases, the applicant(s) might be the firm itself (due to transfer of ownership which results from patent assignment agreements), the parent research organization, or another firm. Again, all such data were carefully recorded and checked.

Because our interest lies with the impact of pre-founding R&D collaboration, we wanted to ensure that the patent applicant or inventor was still engaged in a parent organization at the time the first application for a specific invention was filed. That is, s/he had not yet founded the new venture. We manually inspected the biographies or curriculum vitae of all members of every founding team on websites (university and firm homepages) and in press (venture prospectuses or early company reports, reports in business journals). We include only those patents fulfilling this criterion, that is, patents developed before venture foundation. This extensive search of secondary data was enriched through searches on sites such as LinkedIn and Xing. Finally, we supplemented our information using telephone interviews with members of the founding teams.

Between June 2012 and March 2017, we re-contacted the original informants to gather information on their firm’s international activities and performance. This involved short mail surveys in conjunction with telephone calls. Our goal was to identify continuing, exited, and failed ventures. We contacted all initial informants in a first wave, and this was followed by two more waves of data collection. This helped ensure that we identified all firms with international revenues before the year-end of December 2016. The German databases of the “Handelsregister” and “Unternehmensregister” (German Company Register) provided information about market exit dates. An intensive web-based search of press releases provided additional information. Only exits that represented liquidations or bankruptcies were coded as failures. Follow-up contacts with our key informants were used to ascertain firm non-survival and merger activities. Ventures that changed name or address were treated as continuing entities.

These data collection procedures allowed us to identify 163 ASOs that were (a) no more than 10 years of age and (b) with founders that filed patents prior to their venture’s inception. The 10-year cut-off means that we study new ventures at a stage when learning is important for their development and growth (Bruneel et al., 2010). However, during the second phase of data collection, fourteen firms reported insolvency without generating international revenues, reducing our sample to 149 firms. Of the 149 ASOs, 127 generated their first international revenues within 6 years of founding, and 86 of those did so within 2 years. As such, most of the firms in our study are “early internationalizers” as per Coviello (2015). We also note (and account for) three firms that had no international revenues at the end of our study.

At the time of the on-site interviews, all but 10 firms had sales revenue. The ASOs operated in a variety of science and technology industries (pharmaceutical 34%, mechanical engineering 21%, electrical 17%, chemistry 13%, software 5%, and “other” 10%). Mean firm age was 5.07 years (SD = 2.41), with a mean of 12.75 employees (SD = 17.16). Key informants were predominantly male (97%), with a PhD (73%) and a university degree in engineering (41%), science (43%), medicine (14%), or other (2%).

Measures

Dependent Variable

Our dependent variable is the “hazard” of an ASO obtaining its first international revenues (selling outside Germany) within 6 years of founding. This variable equals 0 when the firm receives no international revenues and 1 if the firm attains its first international revenues during the observation period. To calculate our outcome variable “likelihood of first intentional revenues,” we tracked whether or not a firm obtained international revenue in each year of the observation period.

We examine how early a firm obtains its first international revenues because revenue generation is a primary objective of an international new venture (Patel et al., 2014). This variable also captures the timing and outcome of first foreign market entry (i.e., revenue), and international revenue generation is beneficial to ASOs because it sends a valid quality signal regarding the potential of their new technology. As Yu et al. (2011) observe, initial foreign market sales are “…true indicators of beginning involvement in foreign markets” (p. 431). For the 146 ASOs that generated international revenues before our study ended, the average number of years to first international revenues is 2.98. This compares well to other studies such as Teixeira and Coimbra’s (2014) time to first exports at 2.36 years or Zhou and Wu’s (2014) entering the first international market at 2.19 years.

Because internationalization can be discontinued, sporadic, or the result of an unsolicited order, we conducted several tests to determine how consistent and relevant time to first international revenue is for an ASOs’ continued international activity. First, in our initial survey, we asked respondents to report annual foreign sales for that year and the previous 4 years. Our empirical design allowed us to track whether 95 ASOs had annual international sales in the 4 years immediately following the year of the first international revenues. We included cases that fulfilled the following criteria: (a) no observation gap between the initial and subsequent international revenues and (b) ASOs with international revenues until the year of our on-site interviews. We created a bivariate variable “non-intermittent international revenues” that took the value “1” if ASOs reported continuous annual international sales revenues of at least 5% of total sales (“0” otherwise). A partial correlation analysis shows a reliable relationship between this variable and “time to first international revenues” when controlling for the mean of ASOs’ average annual sales over the 4-year period (mean = 601,570 EUR; SD = 1,029,513 EUR) prior to the survey (r = −.343, p = .001).

Second, in June and July 2022, we re-contacted the ASOs. Of the 149 firms, 106 were still active. We asked if they had continuous international revenues every year since their first international revenues (“1” = yes, “0” = no). If the ASO had merged with another firm (n = 5), they answered the questions for the period of time up to the last full year preceding the merger. By the end of July, we had a response rate of 25.50% based on answers from 38 firms (34 original respondents plus four current/new CEOs). The correlation between “continuous revenues from abroad” and “number of years to first international revenues” is negative and significant (r = −.436, p = .006). We also correlated (a) export intensity, measured as the ratio of foreign sales to total sales in 2021 or at the time prior to a merger, and (b) the number of countries to which the ASO sells, with (c) the number of years until the first international revenues were generated. Again, the correlation results (r = −.328, p = .015; r = −.378, p = .019) suggest that our dependent variable is a meaningful indicator of the onset of internationalization for ASOs.

Independent Variables

Two independent variables capture the breadth of experience held by members of a founding team. Similar to other studies assessing experience breadth (Furr et al., 2019; Gruber et al., 2013; Mannor et al., 2019) we use count variables. The data were extracted and calculated based on patent families with priority dates up to 5 years prior to firm foundation (excluding the foundation year itself), where at least one founder of the ASO was mentioned. This time frame reflects the period that occurs immediately prior to firm foundation; a period of experience considered particularly influential (Boeker, 1989; Knockaert et al., 2011; Marquis & Tilcsik, 2013). The two independent variables pertain to the breadth of pre-founding R&D collaboration experience with either (a) industry partners, or (b) international scientists. To build these variables, we carefully checked the names and nationalities of all inventors to rule out the possibility of inflating the founders’ R&D collaboration network size or their industry access or internationality.

Industry Partner (IP)–Breadth is the founding team’s number of prior R&D collaborations with unique industry partners. This is a count of distinct industry partners listed on patents on which at least one founder is named as inventor. As an example, assume an ASO has three co-founders. Prior to establishing the firm, two of the founders collaborated with a common industry partner (A) within two patent families. The third founder brings pre-founding collaboration experience from two other patent families with (A) as well as two industry partners (B and C). Thus, the IP–Breadth index equals three (i.e., A + B + C).

International Scientist (IS)–Breadth is the number of unique non-German nationalities across the range of inventors that are listed on non-single inventor patents on which at least one founder is named as inventor. For example, assume there are three co-founders: two with a German nationality and one with a Brazilian nationality. The Brazilian founder filed a single-inventor (i.e., non-collaborative) patent prior to firm foundation. Both German founders were involved in four pre-founding patent projects (family level) as co-inventors. They had six additional co-inventors across all projects: two Americans, one Japanese, two Danes, and one German. This means that pre-founding collaboration occurred with three different non-German scientists on a total of five pre-founding patent project. Therefore, the IS–Breadth index equals three (i.e., USA + Japan + Denmark) but not Brazil.

To assess the external validity of our breadth variables, we built an aggregate construct as an external criterion. We want to account for the ASO’s access to collaboration partners given Katila and Mang (2003) find that the number of prior technological collaborations accelerates collaboration timing during product development for new biotech firms. In our study, respondents indicated (on a seven-point scale from “strongly disagree” to “strongly agree”) whether, when founding the ASO, team members were able to quickly establish contacts. Contacts included (a) industry experts in different markets, (b) experts in different technology fields, (c) suppliers, and (d) competitors. We summed items to create this measure, available for 102 of the 149 cases. Standardized regression coefficients of .188 (p = .026) for IP–Breadth and .219 (p = .006) for IS–Breadth support the validity of our experience breadth variables.

Control Variables

We include numerous control variables pertaining to the team, prior work-related experiences of the founding team, prior R&D collaboration experiences of the team, their firm, their technology, and the external environment. These are provided in Appendix A.

Common Method Variance

Our overall research design helps mitigate the risk of common method variance for several reasons. First, we integrate different data sources and part of our data are obtained from the “PATSTAT” database provided by the European Patent Office. Second, our dependent variable (time to first international revenues) is a fact-based variable provided by the key informants. We also validated our dependent variable with a second sample of respondents. This involved randomly contacting 75 firms from the initial sample plus we obtained 30 responses from a second (i.e., different) team member. We conducted t-tests for differences in the means of the two subgroups (nG1 = 116 and nG2 = 30) on a set of descriptive variables assessed by the first respondent. No differences in means were seen for founding team size (t = −0.194), venture age at time of first survey (t = 0.602), pre-founding business experience (t = 0.558), market pull (t = −0.356), and stage of technology development (t = −0.401). There is, however, a .79 correlation (p < .001) between the first and second respondents for time to international revenues. This indicates strong validity for our dependent variable. Third, because we have a large and distinct time separation (at least 2 years) between the measurement of independent and dependent variables, the potential for common method variance is reduced (Podsakoff et al., 2003).

Analytical Approach

Given the longitudinal nature of our data, we use the Cox proportional hazards regression model (Cox, 1972) to examine the likelihood of first international revenues. We use the Cox regression model instead of parametric survival models because we cannot make reasonable assumptions about the parametrization of the baseline hazard and hence, the shape of the hazard over time (Cleves et al., 2010; Cox, 1972). To ensure that hazard rates are proportional, we conducted the Schoenfeld (1982) residual test. None of our variables has non-zero slopes, indicating that the effects are proportional over time.

Time to first international revenues is measured in number of years. Selecting the length of the observation period starting in t0 influences the measurement window and the point at which “time to first international revenues” is right-censored. Due to the presence of right-censored cases (firms that did not internationalize during the observation period or left the observation involuntarily), we use modifications to the survival and hazard function estimators. This let us use partial information instead of simply dropping entire cases (cf. Morita et al., 1993). For right-censored cases, their venture age until the end of the observation was recorded as a waiting period for first international revenues (minimum time span during which no event occurred), qualified by a dummy variable in the analysis. For the main analysis, we follow Coviello and Jones’ (2004) conclusion that 6 years is a common cut-off to define an international new venture. Thus, our observation period is 6 years, from year “t0” (year of inception) to the end of year “t6” as the measurement window to observe our dependent variable (event “first international revenues” in year ti).

Because our initial search and screening processes identified only active ASOs, we control for sample selection bias using a common econometric technique. Recall that fourteen ventures were identified as insolvent without generating international revenues. The probability of venture survival (“0” if it was disbanded; “1” if it was still active at the end of 2016) was estimated following the traditional Heckman (1979) two-step approach. That is, the inverse-Mill’s ratio from the probit model of survival over the observation window is used as an additional predictor in the Cox regression. We added technological ambiguity to the Heckman selection model as a regressor because it represents a general inability to make sense of outcomes or benefits associated with new technology, and thus may ultimately reduce the survival chances of the ASO. However, technological ambiguity does not necessarily impact internationalization timing because early entry to international markets might be undertaken to assess an unclear relationship between innovative technological means and predicted ends (Sillince et al., 2012).

To build a composite indicator of technological ambiguity, we summed the responses of five items to the following question: “To what extent do the following statements apply to your company’s situation during the founding phase?” (1 = I completely disagree; 7 = I completely agree). Sample items include: “There was a good theoretical understanding within my company regarding how the core technology worked” (reverse scored) and “Progress in my company’s technology field was dependent on advancements in many different scientific/technological disciplines.” This survey-derived variable influences the probability of an observation appearing in the internationalization sample (rSurvival = −.367; p = .000) but does not influence our dependent variable in the second-stage model (rTime to first international revenues = −.044; p = .598).

Results

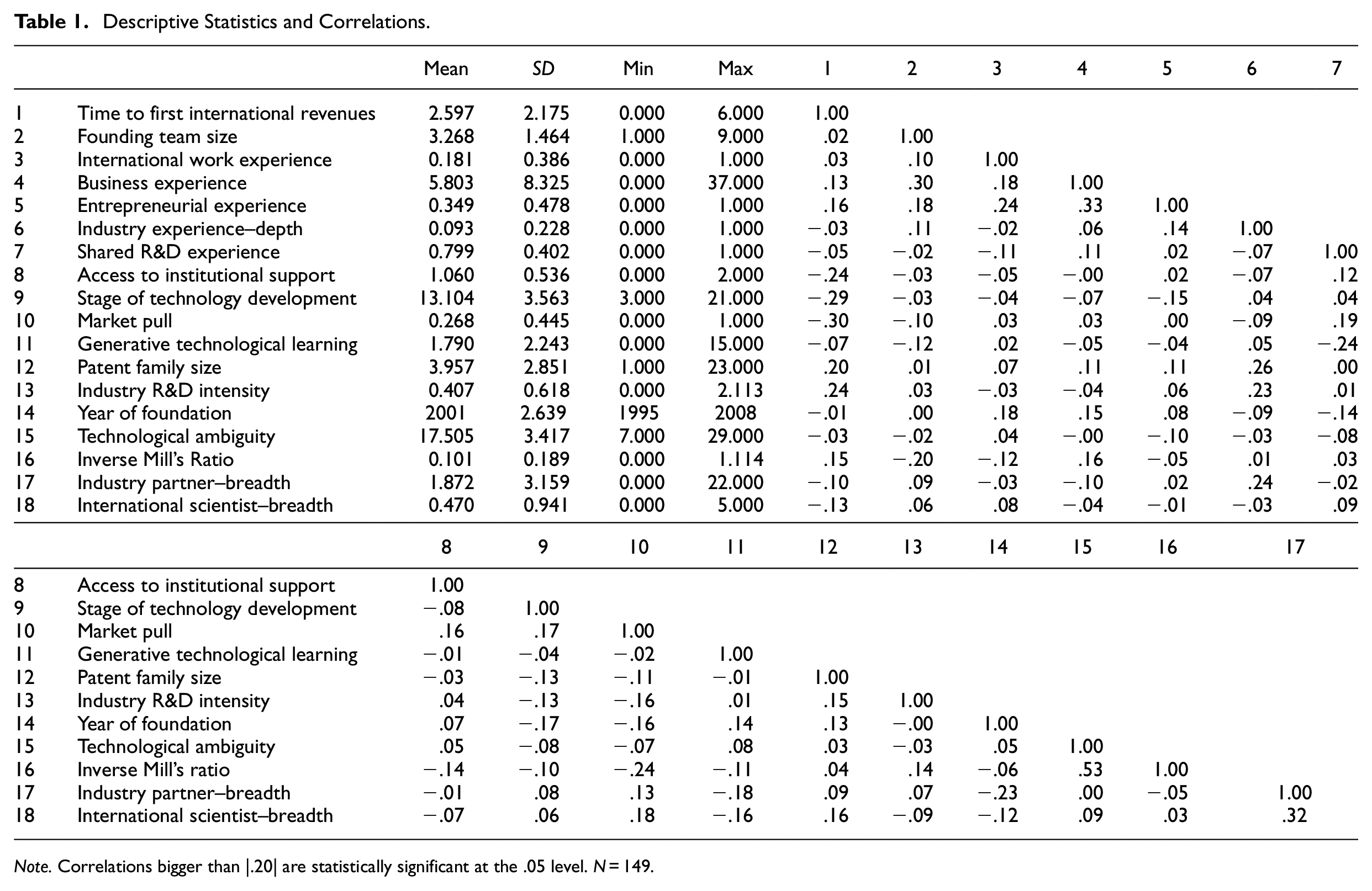

Descriptive Statistics and Main Findings

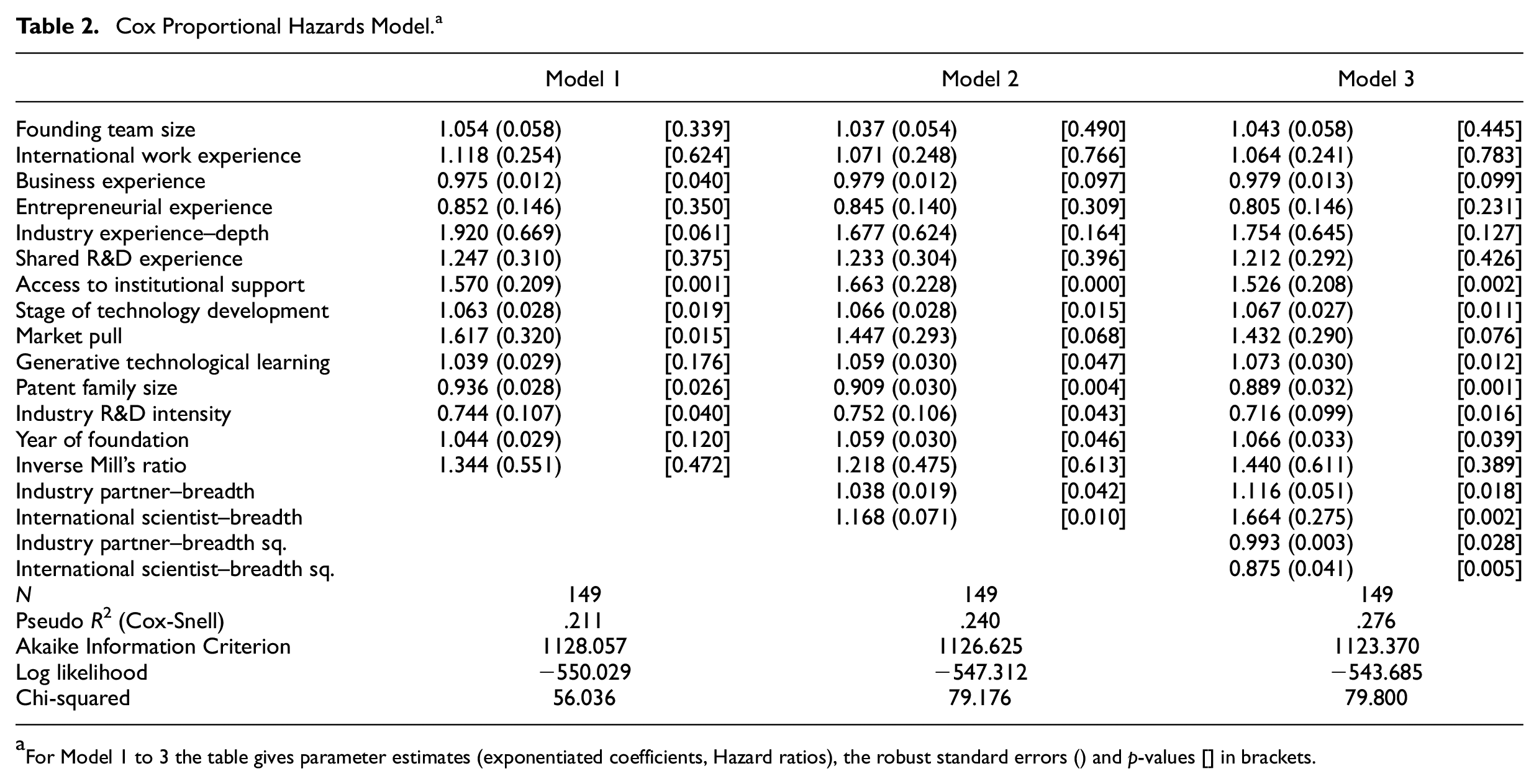

Table 1 presents the descriptive statistics and correlation matrix for all variables. Table 2 presents the results of the Cox proportional hazard regression models. We report hazard ratios (HRs = exponentiated coefficients [eβ]) that indicate how much the “hazard” (understood here as a chance) of the binary (0/1) event “first international revenues” during the observation period of ti years increases for a unit change in the covariates. Values greater than 1 imply that a higher xi has an increasing effect on the hazard (instantaneous risk of event) and thus, a lower expected duration for time to first international revenues. Independent variables are entered hierarchically to assess the value of adding covariates by examining the decrease in log-likelihood between the models. Table 2 reports the exact p-values (two-sided tests of significance) and robust standard errors in parentheses.

Descriptive Statistics and Correlations.

Note. Correlations bigger than |.20| are statistically significant at the .05 level. N = 149.

Cox Proportional Hazards Model. a

For Model 1 to 3 the table gives parameter estimates (exponentiated coefficients, Hazard ratios), the robust standard errors () and p-values [] in brackets.

A multicollinearity check reveals no problematic variance inflation factor (VIF) values (cf. Cohen et al., 2003) for the squared breadth indices (VIFIP–Breadth = 4.02; VIFIS–Breadth = 4.32). We therefore test the curvilinear relationships of internationalization timing with (a) industry partner breadth and (b) international scientist breadth, simultaneously (VIFmax = 5.13). Model 1 (see Table 2) is our baseline model, consisting only of control variables. Six controls show a significant influence (p < 5%) on the dependent variable. We begin with the three that are positive. For every unit increase in R&D being motivated by market pull, the likelihood of first international revenues is 61.7% higher also, each unit increase in access to institutional support increases the likelihood of first international revenues by 57%. For every unit increase in stage of technology development, the likelihood of first international revenues between year 0 and year 6 increases by 6.3%. Turning to the negative effects, the likelihood of first international revenues is 6.4% lower with each step increase in patent family size. Also, a 1% increase in industry R&D intensity decreases the likelihood of first international revenues by 25.6%. We also see that for each 1-year increase in a founding team’s prior business experience, there is a 2.5% decrease in the likelihood of first international revenues (Note: each founding team averages 5.8 years of prior business experience). No significant impact is seen for prior international work experience, prior entrepreneurial experience, or shared R&D experience.

In Model 2, we add the linear terms of the two main variables. The hazard rates for both predictor variables are larger than 1 and significant (HRIP–Breadth = 1.038; p = .042; HRIS–Breadth = 1.168; p = .010). This indicates that breadth of either type of prior R&D collaboration experience shortens the time to first international revenues. The findings of Model 3 pertain to the quadratic terms. Hypotheses 1 and 2 are supported given the squared terms of the predictor variables display significant Hazard rates less than 1 in Model 2 (HRIP–Breadth = 0.993; p = .028; HRIS–Breadth = 0.875; p = .005). These results indicate an inverted U-shaped relationship between (a) breadth of pre-founding R&D collaboration with either industry partners or international scientists and (b) the likelihood of first international revenues within the first 6 years of founding.

To test the relationships from the Cox regression more rigorously, we use the three-step testing procedure recommended by Haans et al. (2016). First, when we add the quadratic terms to Model 2, the fit for Model 3 improves significantly (ΔChi2 = 7.25; p = .026). Second, slope tests (Lind & Mehlum, 2010) for both curvilinear relationships reveal significantly steep slopes at both ends of the data range (IP–Breadth: p = .009 low bound; p = .027 = upper bound; overall test inverse U-shape: p-value = .027; IS–Breadth: p = .001 low bound; p = .004 upper bound; overall test inverse U-shape: p-value = .004). Third, we construct the 95% confidence intervals of the estimated turning points following Hirschberg and Lye (2005), using the Delta method and the Fieller method. The estimated turning points and confidence intervals using the Delta method are in the data range (IP–Breadth: estimated turning point = 7.34, lower bound = −1.87, upper bound = 20.13; IS–Breadth: estimated turning point = 2.65, lower bound = −0.47, upper bound = 6.53). The derived Fieller intervals also confirm lower and upper bounds around the turning points that lie well within the range of both R&D collaboration scales. These results strongly support Hypotheses 1 and 2.

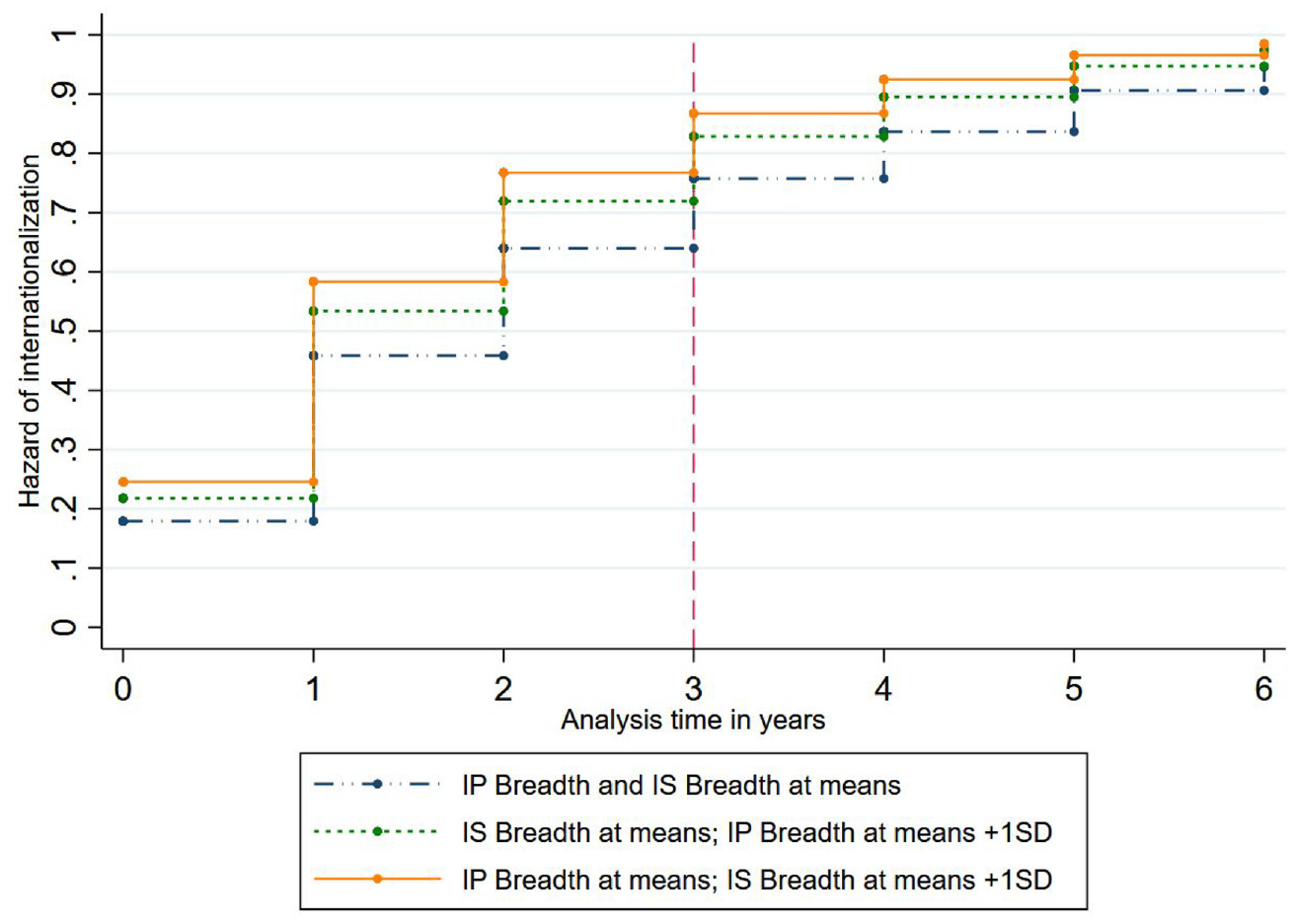

Figure 1 depicts the cumulative hazard of internationalization for ASOs at different levels of (a) IP–Breadth and (b) IS–Breadth. The reference situation is the dashed-dotted line. It shows that the cumulative hazard of internationalizing over the 6-year observation period is lowest for ASO founding teams with both types of R&D collaboration experience fixed at their means. If we add one standard deviation to the mean of each type of collaboration and fix all covariates at their respective means, different results emerge. Both IP–Breadth (dashed line) and IS–Breadth (solid line), show a steep increase in the cumulative hazard of internationalizing in the first 3 years after founding.

Cumulative hazard of internationalizing during the 6-year observation period by industry partner (IP)–breadth and international scientist (IS)–breadth.

If prior experience with R&D collaboration is one standard deviation above the mean, when the ASO was founded, the cumulative hazard of achieving international revenues 1 year after founding increases from 23.43% to 56.53% for IP–Breadth and from 25.31% to 59.77% for ISs–Breadth. By year three, ASOs have a 77.41% cumulative hazard of internationalization if their founding teams brought in the average amount of experience breadth with each type of partner, For those with an IP–Breadth at mean plus 1SD (ISs–Breadth at mean) the cumulated hazard of internationalization increases from 77.41% to 85.79%. The cumulative hazard for IS–Breadth at mean plus 1SD (IP–Breadth at mean) increases to 88.15%. Furthermore, the hazard of generating international revenues within 6 years of founding is highest if R&D collaborations were conducted with an average of (a) about seven different industry partners and (b) scientists from three different non-German countries.

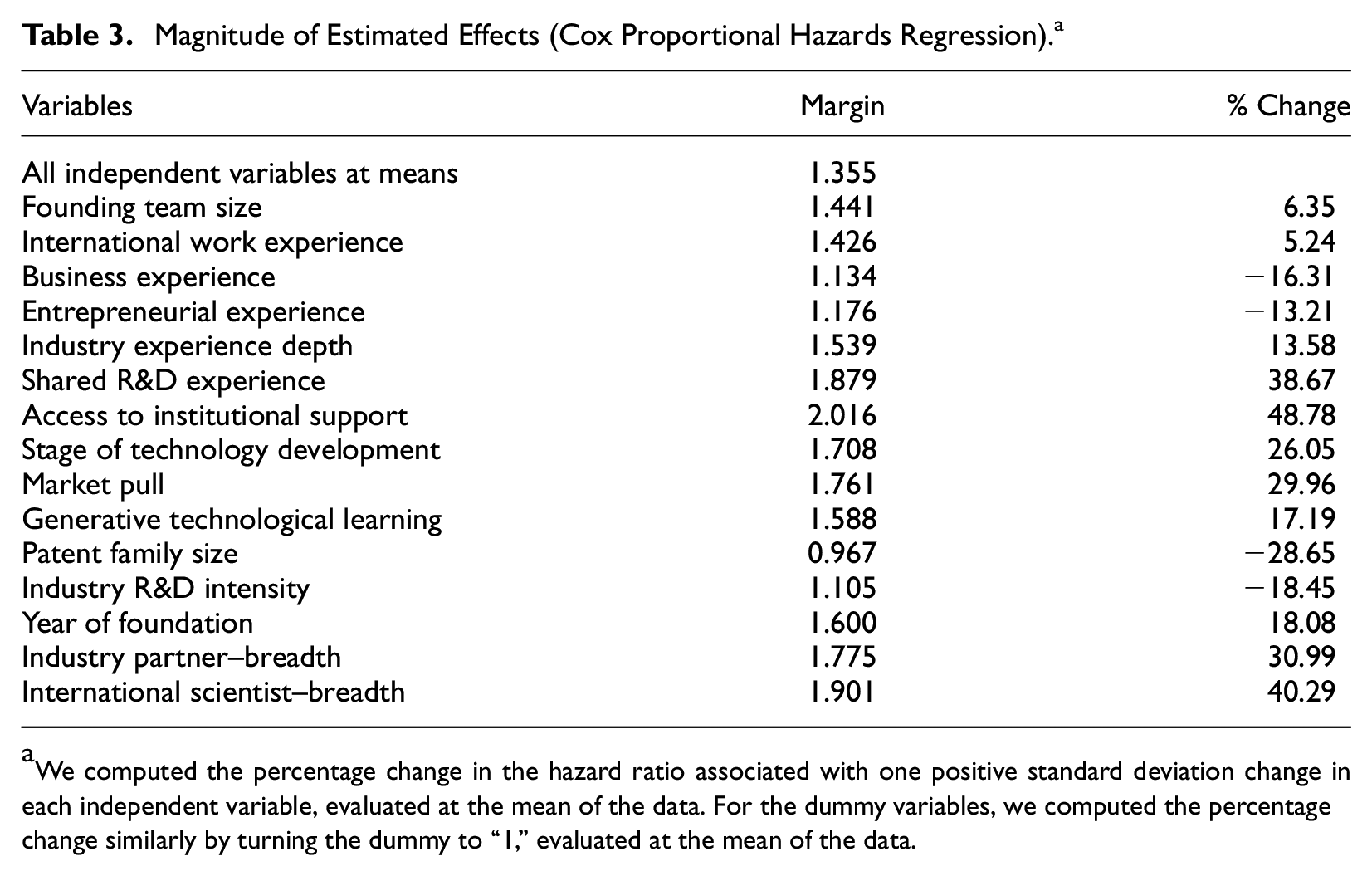

Table 3 shows the magnitude of estimated effects for our independent variables in Model 3. The percentage change in hazard ratios associated with a positive standard deviation for each independent variable is shown, evaluated at the mean of the data. For the dummy variables, we compute the magnitude change by turning the dummy to “1.” For the two independent variables, a one standard deviation unit increase from the mean of IS–Breadth exerts the largest increase in hazard ratio (40.29%), followed by IP–Breadth (30.99%).

Magnitude of Estimated Effects (Cox Proportional Hazards Regression). a

We computed the percentage change in the hazard ratio associated with one positive standard deviation change in each independent variable, evaluated at the mean of the data. For the dummy variables, we computed the percentage change similarly by turning the dummy to “1,” evaluated at the mean of the data.

A series of robustness checks confirm our results. These are found in Appendix B.

Discussion

The results of this study suggest that for new ventures, the relationship between prior experience and internationalization timing is more nuanced than previously understood. Based on our findings from ASOs, two highly relevant but overlooked types of experience are pre-founding R&D collaborations with industry partners and international scientists. Our analysis of a unique, longitudinal dataset shows that as the breadth of pre-founding R&D collaboration with either type of partner increases, so too does the likelihood of generating first international revenues within 6 years. However, this happens only to a certain point after which additional pre-founding R&D collaboration appears to create high cognitive load. This may strain the scientist-founders’ cognitive capacity such that internationalization timing slows. These findings have several implications for the international entrepreneurship and academic entrepreneurship literatures.

Theoretical Contributions

In terms of the international entrepreneurship literature, our nonlinear (inverse U-shaped) results go beyond the common linear arguments that link accumulated experience or the possession of certain demographic characteristics to early internationalization (e.g., Criaco et al., 2021; Zucchella et al., 2007). This provides a number of contributions. First, by combining cognitive diversity theory (Hambrick et al., 1996; Horwitz, 2005; S. K. Horwitz & I. B. Horwitz, 2007) and cognitive load theory (Kirschner et al., 2009; Sweller, 1988), we argue that at a certain point, the cognitive load created by having collaborated with a relatively large number of R&D partners will disproportionately diminish the cognitive diversity benefits for scientist-founders. That is, variety in pre-founding R&D collaboration experience has a tipping point beyond which increased breadth of experience leads to lower gains in the internationalization timing of ASOs. This leads to a second contribution: a new type of “breadth liability” distinct from that identified by Mannor et al. (2019). They use cognitive categorization theory (Dutton & Jackson, 1987) to show in which situations experience breadth might be “viewed negatively” by investors, due to the environmental context. Although Mannor et al. (2019) offer nascent insight on the downsides of experience breadth, we use our nonlinear results to challenge the commonly used argument that it benefits a new venture team in terms of the cognitive resources it brings (Criaco et al., 2021; Fern et al., 2012; Gruber, 2010).

Third, we conceptualize and measure “experience” in a new way by recognizing the potential role of a founding team’s pre-founding R&D collaboration experiences with different types of partners. This builds on arguments regarding team-level experience and diversity in entrepreneurship (Fern et al., 2012; Furr, 2019; Mannor et al., 2019), and international entrepreneurship (Criaco et al., 2021). By considering R&D collaboration with international scientists in particular, we also introduce a new type of “international” experience. This indicates the need to incorporate both standard and contextualized operationalizations of experience in scholarly research. It is also reinforced by our results, for example, for prior international work experience and entrepreneurial experience, both of which have no identifiable influence on internationalization timing for the ASOs in our study. Also notable is that business experience negatively impacts time to first international revenues for ASOs. As Walsh (1995, p. 304) notes: “the utility of a knowledge structure is always situationally dependent,” and the team’s previous international, entrepreneurial, or business experiences might well be derived from a context that is less relevant for ASOs.

To this point, the general homogeneity of founding teams in ASOs has led scholars to recommend collaboration with industry partners (e.g., Franklin et al., 2001; Vohora et al., 2004). Our findings support this but as a fourth contribution, we also identify the particular relevance of prior R&D collaboration with scientists from other nationalities. One explanation for this comes from Hahn et al. (2019) who argue that scientists (in the context of commercialization) have a mindset that is well suited to seeking and valuing diverse sources of new information. Relatedly, Molner et al. (2019), find that collaboration with other scientists can shape the market-scoping mindset of scientist-founders and help them accept market ambiguity. In our study, that ambiguity pertains to internationalization, and prior collaboration with international scientists may build “international” cognitive diversity that later guides ASO scientist-founders. If scientist-founders and international scientists worked together, their cognitively proximal homogeneity (as domain experts) might allow for easier access to international market knowledge. As per Un et al. (2010) and Knockaert et al. (2011), easier knowledge access facilitates the combination and application of new insights, and this should allow for faster decision-making. Such benefits may be possible because as previously noted, international scientists are both “insiders” and “outsiders.” Nevertheless, we also caution that as with industry partners, the positive effect of experience breadth and its related cognitive diversity turns negative, restricting the likelihood of early internationalization.

Finally, these findings and contributions also pertain to the literature on academic entrepreneurship. That is, we help address Nikiforou et al.’s (2018) concern that research in that domain still pays too little attention how entrepreneurs from academia bridge the gap to business. Here, we show that two context-specific types of pre-founding collaboration can differentiate ASOs in terms of how quickly they generate their first international revenues. This also responds to calls for more research on academic entrepreneurship and internationalization from Cumming et al. (2009) and Siegel and Wright (2015).

Practical Implications

If the scientist-founders of ASOs collaborated for R&D with either industry partners or international scientists, prior to founding their new venture, they will likely internationalize faster than ASOs whose scientist-founders have no such experience. Thus, when considering strategic decisions like internationalization, scientist-founders should identify and leverage the cognitive diversity in their team that comes from prior R&D collaboration. This experience helps scientist-founders get a solid head start on internationalizing their ASOs. Yet ASO founders should also be aware that if their pre-founding R&D collaboration history involved a high number of partners, they could experience cognitive load where their knowledge structures become too diverse and too complex, increasing team coordination and decision-making. Thus, scientist-founders should be aware of the potential dark side that comes with R&D collaboration experience in terms of the internationalization timing of their ASO. This applies regardless of partner type. Although some might argue that scientist-founders will benefit the most from having worked with industry partners as domain “outsiders,” both types of collaboration experience increase the likelihood of internationalizing within our time frame of interest. Indeed, doing so with international scientists (compared to industry partners) appears to have a greater impact.

For investors interested in ASOs, and science- and technology-based firms in general, we caution against assessing or forming teams by relying primarily on, for example, prior business experience or international work experience. Without acknowledging founders’ experiences with R&D collaboration, investors will not have a full picture of the team’s potential. This is particularly relevant if investor objectives include early revenue generation because this outcome is facilitated by early internationalization. And, as seen here, the likelihood of early internationalization occurring is higher when the ASO’s team has a certain level of prior R&D collaboration experience with industry partners or international scientists.

Finally, if we consider other actors in the new venture ecosystem, public research institutions increasingly strive for, and are measured by, their start-up activities and success. Our results should reassure these organizations that their natural habitat of research provides an important resource for ASOs that intend to internationalize. Given we establish theoretical and empirical grounds for a fruitful connection between (a) the cognitive diversity that comes with breadth of pre-founding R&D collaboration, (b) cognitive load, and (c) the internationalization timing of ASOs, we hope that public research institutions can work to build this bridge.

Limitations and Future Research

In this study, we consider only time to first international revenues as a dependent variable. Future research could capture revenue generation annually, post-internationalization. For example, we are inspired by Bruneel et al. (2010) to ask: when and how are the benefits of pre-founding R&D collaboration experience replaced in the context of the oscillating internationalization trajectory that Kriz and Welch (2018) identify in their study of ASOs? Also, do the benefits and costs associated with the two partner types change over time? Other research could link our findings to new venture survival given international entrepreneurship research in this area has mixed results. For example, some show that later internationalization will benefit survival (Freixanet & Renart, 2020) and others report the opposite (Carr et al., 2010). This leads us to ask: does the early internationalization facilitated by pre-founding R&D collaboration experience help or hinder survival?

Although proxy data (such as our patent data and other secondary sources) are increasingly common, they have limitations. For instance, our measures assume that experience contributes to cognition. Although R&D collaboration is understood to involve a learning process (Greve & Taylor, 2000; Pierce & Delbecq, 1977), we do not study that process. Similarly, we consider scientist-founders to be scientific experts but lack data on their experience versus expertise as per Reuber and Fischer (1994). Incorporating this distinction in future studies would provide a finer-grained view of the sources of cognition. We recognize too that the collaboration experiences studied here, albeit distinct from demographic characteristics, are still a proxy for founder cognitions. As discussed by Miller et al. (1998), direct measures to capture cognitive diversity regarding, for example, goals, beliefs, or decision processes could be collected in future research, framed in the context of new venture internationalization. Similarly, as seen in Laamanen et al. (2018), the various dimensions of cognitive load could be explicitly assessed. So too could the concept of experience depth. Limitations in our data mean that we can use depth of target industry experience in R&D collaboration as a control, but as per Mannor et al. (2019) and Furr (2019), more work on experience depth as a distinct influence (relative to breadth) is warranted.

In this study, we assume that scientist-founders’ cognitive diversity can come from pre-founding collaboration experiences with two types of partner. However, we do not capture the specific types of knowledge acquired. In terms of ASOs, future research could identify when, how, and from which type of partner, founders generate congenital knowledge that is declarative versus procedural. As discussed by Monaghan and Tippmann (2018), the former will help founders understand “what to do” regarding internationalization while the latter refers to “how to do it.” Similarly, future research could examine which type of partner builds congenital knowledge pertaining to Eriksson et al.’s (1997) three types of international knowledge: market, institutional, and internationalization knowledge.

Finally, our sample is drawn from the population of ASOs headquartered in Germany with public research organizations as parents from the same country. Given corporate spin-offs do not share the same type of history and initial conditions (Clarysse et al., 2011), we call for comparative research that includes other types of spin-offs as well as independent technology startups. Finally, the potential impact of the German institutional environment may not apply to firms from other nations. Again, comparative research will provide additional insight.

Footnotes

Appendix B

Appendix A.

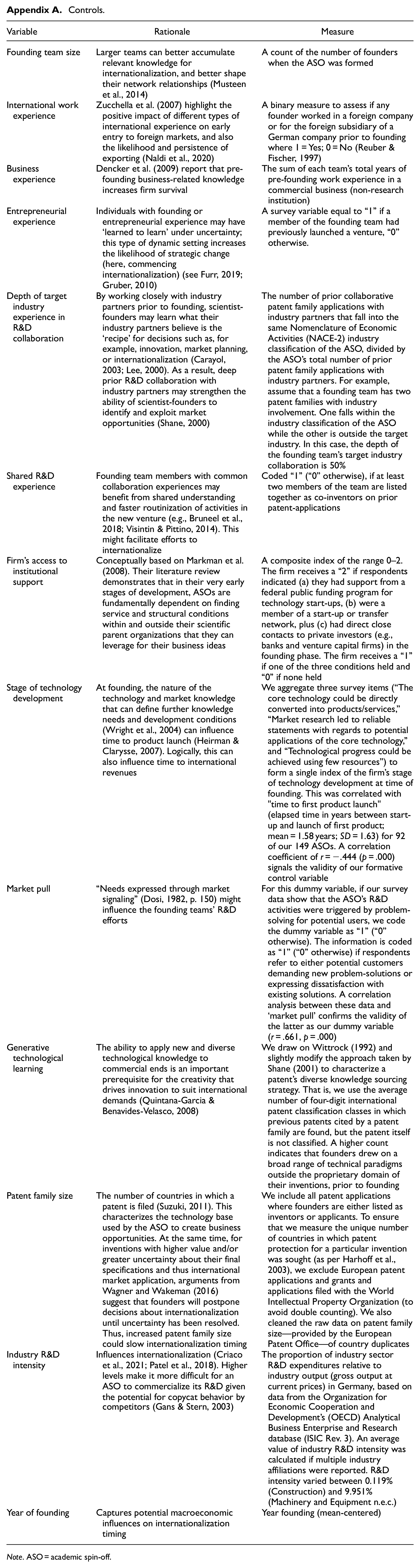

Controls.

| Variable | Rationale | Measure |

|---|---|---|

| Founding team size | Larger teams can better accumulate relevant knowledge for internationalization, and better shape their network relationships (Musteen et al., 2014) | A count of the number of founders when the ASO was formed |

| International work experience | Zucchella et al. (2007) highlight the positive impact of different types of international experience on early entry to foreign markets, and also the likelihood and persistence of exporting (Naldi et al., 2020) | A binary measure to assess if any founder worked in a foreign company or for the foreign subsidiary of a German company prior to founding where 1 = Yes; 0 = No (Reuber & Fischer, 1997) |

| Business experience | Dencker et al. (2009) report that pre-founding business-related knowledge increases firm survival | The sum of each team’s total years of pre-founding work experience in a commercial business (non-research institution) |

| Entrepreneurial experience | Individuals with founding or entrepreneurial experience may have ‘learned to learn’ under uncertainty; this type of dynamic setting increases the likelihood of strategic change (here, commencing internationalization) (see Furr, 2019; Gruber, 2010) | A survey variable equal to “1” if a member of the founding team had previously launched a venture, “0” otherwise. |

| Depth of target industry experience in R&D collaboration | By working closely with industry partners prior to founding, scientist-founders may learn what their industry partners believe is the ‘recipe’ for decisions such as, for example, innovation, market planning, or internationalization (Carayol, 2003; Lee, 2000). As a result, deep prior R&D collaboration with industry partners may strengthen the ability of scientist-founders to identify and exploit market opportunities (Shane, 2000) | The number of prior collaborative patent family applications with industry partners that fall into the same Nomenclature of Economic Activities (NACE-2) industry classification of the ASO, divided by the ASO’s total number of prior patent family applications with industry partners. For example, assume that a founding team has two patent families with industry involvement. One falls within the industry classification of the ASO while the other is outside the target industry. In this case, the depth of the founding team’s target industry collaboration is 50% |

| Shared R&D experience | Founding team members with common collaboration experiences may benefit from shared understanding and faster routinization of activities in the new venture (e.g., Bruneel et al., 2018; Visintin & Pittino, 2014). This might facilitate efforts to internationalize | Coded “1” (“0” otherwise), if at least two members of the team are listed together as co-inventors on prior patent-applications |

| Firm’s access to institutional support | Conceptually based on Markman et al. (2008). Their literature review demonstrates that in their very early stages of development, ASOs are fundamentally dependent on finding service and structural conditions within and outside their scientific parent organizations that they can leverage for their business ideas | A composite index of the range 0–2. The firm receives a “2” if respondents indicated (a) they had support from a federal public funding program for technology start-ups, (b) were a member of a start-up or transfer network, plus (c) had direct close contacts to private investors (e.g., banks and venture capital firms) in the founding phase. The firm receives a “1” if one of the three conditions held and “0” if none held |

| Stage of technology development | At founding, the nature of the technology and market knowledge that can define further knowledge needs and development conditions (Wright et al., 2004) can influence time to product launch (Heirman & Clarysse, 2007). Logically, this can also influence time to international revenues | We aggregate three survey items (“The core technology could be directly converted into products/services,”“Market research led to reliable statements with regards to potential applications of the core technology,” and “Technological progress could be achieved using few resources”) to form a single index of the firm’s stage of technology development at time of founding. This was correlated with "time to first product launch" (elapsed time in years between start-up and launch of first product; mean = 1.58 years; SD = 1.63) for 92 of our 149 ASOs. A correlation coefficient of r = −.444 (p = .000) signals the validity of our formative control variable |

| Market pull | “Needs expressed through market signaling” (Dosi, 1982, p. 150) might influence the founding teams’ R&D efforts | For this dummy variable, if our survey data show that the ASO’s R&D activities were triggered by problem-solving for potential users, we code the dummy variable as “1” (“0” otherwise). The information is coded as “1” (“0” otherwise) if respondents refer to either potential customers demanding new problem-solutions or expressing dissatisfaction with existing solutions. A correlation analysis between these data and ‘market pull’ confirms the validity of the latter as our dummy variable (r = .661, p = .000) |

| Generative technological learning | The ability to apply new and diverse technological knowledge to commercial ends is an important prerequisite for the creativity that drives innovation to suit international demands (Quintana-Garcia & Benavides-Velasco, 2008) | We draw on Wittrock (1992) and slightly modify the approach taken by Shane (2001) to characterize a patent’s diverse knowledge sourcing strategy. That is, we use the average number of four-digit international patent classification classes in which previous patents cited by a patent family are found, but the patent itself is not classified. A higher count indicates that founders drew on a broad range of technical paradigms outside the proprietary domain of their inventions, prior to founding |

| Patent family size | The number of countries in which a patent is filed (Suzuki, 2011). This characterizes the technology base used by the ASO to create business opportunities. At the same time, for inventions with higher value and/or greater uncertainty about their final specifications and thus international market application, arguments from Wagner and Wakeman (2016) suggest that founders will postpone decisions about internationalization until uncertainty has been resolved. Thus, increased patent family size could slow internationalization timing | We include all patent applications where founders are either listed as inventors or applicants. To ensure that we measure the unique number of countries in which patent protection for a particular invention was sought (as per Harhoff et al., 2003), we exclude European patent applications and grants and applications filed with the World Intellectual Property Organization (to avoid double counting). We also cleaned the raw data on patent family size—provided by the European Patent Office—of country duplicates |

| Industry R&D intensity | Influences internationalization (Criaco et al., 2021; Patel et al., 2018). Higher levels make it more difficult for an ASO to commercialize its R&D given the potential for copycat behavior by competitors (Gans & Stern, 2003) | The proportion of industry sector R&D expenditures relative to industry output (gross output at current prices) in Germany, based on data from the Organization for Economic Cooperation and Development’s (OECD) Analytical Business Enterprise and Research database (ISIC Rev. 3). An average value of industry R&D intensity was calculated if multiple industry affiliations were reported. R&D intensity varied between 0.119% (Construction) and 9.951% (Machinery and Equipment n.e.c.) |

| Year of founding | Captures potential macroeconomic influences on internationalization timing | Year founding (mean-centered) |

Note. ASO = academic spin-off.

Acknowledgements

We thank Nora Otte for her work on the initial analysis of this research. We are also grateful to insightful feedback from Anne Domurath, Liena Kano, Thomas Hellmann, Moren Lévesque, Wendy Bradley, George Yip, and Ivo Zander. Finally, thanks go to seminar participants at Imperial College Business School, Saïd Business School, University of Turku, University of Windsor, and Uppsala University. A previous version of this research was presented at the Academy of Management Meeting, Vancouver, 2015.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The authors received financial support for the data collection as part of a larger research project on science-industry technology transfer from the German Federal Ministry of Education and Research (BMBF 01SF0720 and 01SF0918).