Abstract

We examine the influence of founders’ prior shared international experience on the timing of their new ventures’ first entry into foreign markets. We propose that this experience, which is gained by founders working concurrently for the same international firm prior to the founding of the current company, provides them with shared knowledge and routines that they can use to enter foreign markets for the first time earlier in the venture’s life. Further, we propose that founders’ diversity strengthens this relationship, because diverse groups of founders have a broader range of knowledge, skills, and perspectives, which facilitates the adaptation of their prior shared international experience to their new venture setting. This is likely to further reduce the time it takes them to enter foreign markets for the first time. We also argue that industry dynamism weakens the relationship between founders’ prior shared international experience and the time to first foreign market entry, because this type of experience is likely to become obsolete in a rapidly changing environment. Finally, we hypothesize that early internationalizers enjoy higher performance than late internationalizers. We test these predictions using a sample of Swedish new ventures. Our results contribute to the literatures on founders’ shared experience and early internationalization.

Keywords

Founders play a pivotal role in shaping their new ventures’ strategic decisions (Knight, Greer, & De Jong, 2020; Shepherd, Souitaris, & Gruber, 2021). In the early stages of these ventures’ life cycles, founders are typically responsible for interacting with key stakeholders, securing resources, designing the organizational structure, allocating tasks and positions, and developing and implementing strategies. In undertaking these activities, founders oftentimes build on the knowledge and experiences they have accumulated prior to creating their current ventures (Clough, Fang, Vissa, & Wu, 2019; Jung, Vissa, & Pich, 2017). As a result, researchers have attributed new ventures’ focus on certain business domains (e.g., where to operate) to the experience-based knowledge that their founders have previously acquired in the same or a similar domain. Fern, Cardinal, and O’Neill (2012), for instance, argue that entrepreneurs are more likely to select a geographic or product market or a resource if they possess prior experience-based knowledge of such a market or resource. Other studies have also attributed new ventures’ performance in a given domain to the experience that their founders have previously acquired in that domain or a similar one (Delmar & Shane, 2006).

Research also suggests that when a group of cofounders decides to start a new venture together (see Lazar, Miron-Spektor, Agarwal, Erez, Goldfarb, & Chen, 2020), it matters greatly if the founders’ prior experience is shared (Shepherd et al., 2021). “Shared experience” indicates that founders have worked together before founding their new venture. Such shared experience is important because it typically enhances communication and trust among founders (Eisenhardt & Schoonhoven, 1990). Shared experience is also important because it can provide shared knowledge and routines that can be deployed in the operations of the new venture (Agarwal, Campbell, Franco, & Ganco, 2016; Wezel, Cattani, & Pennings, 2006). This, in turn, allows new ventures to make strategic decisions more rapidly—for instance, by expediting market entry (Beckman, 2006; Schoonhoven, Eisenhardt, & Lyman, 1990).

Given these benefits, prior studies have examined the advantages of founders’ prior shared experience for their new ventures (Honoré, 2020; Okhmatovskiy, Suhomlinova, & Tihanyi, 2020; Zheng, Devaughn, & Zellmer-Bruhn, 2016). However, past studies have left two issues unresolved. First, little is known about how founders can adapt shared knowledge and routines developed in their previous employers to the new venture context and devise solutions and actions accordingly. To this end, founders’ diversity becomes an important dimension, because even when they have prior shared experience, founders may still vary in other characteristics, such as gender, age, ethnic background, and education, which equips new ventures with different perspectives, skills, and knowledge (Van Knippenberg & Schippers, 2007). Hence, founders’ diversity constitutes an important contingency that affects in part their ability to “customize” their prior shared experience to the new venture context.

Second, we know little about what may happen to the benefits of shared experience when the task environment in which the new venture operates is unstable. Prior research indicates that in a dynamic environment, founders with prior shared experience can make decisions more efficiently and quickly and perform better because they can focus on business challenges rather than on issues related to group processes and dynamics (Eisenhardt & Schoonhoven, 1990; Roure & Maidique, 1986). However, volatile environments also change the underlying tasks that founders should perform and, as a consequence, the relevance of their shared knowledge and routines to the requirements for success in these environments (Zheng et al., 2016). Hence, the nature of the task environment (e.g., stable vs. dynamic) constitutes an important contingency that defines the extent to which founders’ prior shared experience serves to hasten or delay new ventures’ strategic actions, such as the timing of their first foreign market entry.

In this study, we address these issues by building theory regarding the conditions under which founders’ prior shared experience positively or negatively affects their ventures’ market entry actions. In today’s global business environments, new ventures are both pushed and pulled to internationalize their operations early in their life cycles to survive and grow (Fan & Phan, 2007; Shrader, Oviatt, & McDougall, 2000). Hence, time to first foreign market entry is particularly relevant for those ventures that need to seize fleeting opportunities in an increasingly competitive and international business environment. Following the literature (Yu, Gilbert, & Oviatt, 2011), we define time to first foreign market entry as the time from a new venture’s inception to its first entry into a foreign market through exporting. Such entry is a highly risky decision, as it entails significant resource allocations by otherwise resource-constrained new ventures (Cavusgil & Knight, 2015). Next, we align the conceptualization of founders’ prior shared experience to the domain of relevance of the outcome variable in our study. That is, we consider founders’ prior joint working experience in firms with foreign market sales before the founding of their new venture, and label it as founders’ prior shared international experience.

We draw on the literature on founding team diversity to propose that diversity brings a range of knowledge, skills, and perspectives that a group of cofounders can use to adapt “what worked” in a previous firm to the context of the new venture. This can improve founders’ action speed—for instance, by shortening the time to first foreign market entry. We also propose that industry dynamism is likely to alter which knowledge and routines are relevant to new ventures entering foreign markets for the first time. Consequently, founders’ shared knowledge and routines derived from their prior shared international experience need to be updated to ensure their relevance, sometimes at the expense of early first foreign market entry. Finally, we propose that early internationalizers perform better than late internationalizers in terms of both general and international performance. We test these predictions using a sample of 1,405 independent new ventures from Sweden.

Our study contributes to the research on the role of founders’ prior shared experience in entrepreneurship. Specifically, the study offers a new perspective to this literature by focusing on a more proximate strategic outcome that is related to that experience: first foreign market entry. If the key benefits of shared international experience relate to having shared knowledge and routines, then ventures with such experience should enter foreign markets for the first time earlier than those lacking it. Furthermore, we propose two boundary conditions that are critical in determining the potential benefits and drawbacks of prior shared experience: founders’ diversity and industry dynamism. In this way, we show how these dimensions influence how founders’ prior shared international experience can translate into a shorter/longer time to first foreign market entry. By recognizing these boundary conditions, our findings address criticisms of existing research in this area that noted that “this stream of research, though valuable, has implicitly assumed that PSE [prior shared experience] is always beneficial” (Zheng et al., 2016: 2504). Finally, our study contributes to the literature on new venture early internationalization by showing that founders’ prior shared international experience has a greater positive influence on the initiation of their ventures’ internationalization process than (the sum of) their prior independent international experiences.

Theoretical Background and Hypotheses

Founders’ Prior Shared Experience

Some new ventures are founded by a group of cofounders (Lazar et al., 2020) who had previously worked together for the same firm, making their prior shared experience a salient characteristic of these ventures (Shepherd et al., 2021). Research suggests a positive relationship between founders’ prior shared experience and their ventures’ performance (Honoré, 2020; Okhmatovskiy et al., 2020; Zheng et al., 2016). This relationship is often explained by founders’ ability to take strategic actions faster than competitors—for example, by reducing the time to market entry (Beckman, 2006; Schoonhoven et al., 1990).

The notion that shared experience and shared knowledge are critical for facilitating actions that need to be planned dates back to Penrose (1959: 46-47), who observed that “an administrative group is something more than a collection of individuals; it is a collection of individuals who have had experience in working together. . . . Extensive planning requires the cooperation of many individuals and this requires knowledge of each other.” More recently, the literature has used a knowledge-based perspective to explain the importance of founders’ prior shared experience for accelerating market entry (Beckman, 2006). The value of this type of experience is attributed to the shared knowledge that founders developed while working for the same organization before founding the new venture.

Building on insights from Penrose’s pioneering work, the knowledge-based literature also advances the notion that new ventures can benefit from having members with specialized and tacit knowledge (Castanias & Helfat, 1991) who can integrate and build upon such knowledge (Grant, 1996). Founders’ prior shared experience meets these criteria, as it provides the new venture with both shared understanding and shared know-how from the start. First, shared experience provides founders with a shared language, culture, and narratives (Eisenhardt & Schoonhoven, 1990). Since they have previously worked and interacted with each other, founders with prior shared experience are likely to have developed mutual trust, beliefs, and culture, including similar points of reference and examples of appropriate and inappropriate behaviors (Agarwal et al., 2016). Beckman (2006: 743) notes that these commonalities will “result in faster time to market because of the language and understandings that they [founders] share from their prior company affiliation.”

Second, shared experience is valuable for the development of common organizing frameworks and routines. This, in turn, helps cofounders to share knowledge about how to perform different activities. Founders’ independent experiences from previous jobs and organizations might not be sufficient for the transfer of routines to their new ventures. Prior shared experience, on the other hand, is more influential for the reproduction of these routines. Indeed, research suggests that groups of people who move together from an established organization to a new one may be better able to transfer routines (Wezel et al., 2006). Thus, new ventures whose founders have prior shared experience may be better equipped to undertake early strategic actions—such as entering new foreign markets—more quickly, because they already possess the well-established routines required to do so.

Time to Foreign Market Entry in New Ventures

Researchers have shown considerable interest in new ventures’ time to market entry. Prior studies have focused primarily on the time it takes a new venture to introduce its products to a specific market space. Other studies, often grounded in the international entrepreneurship (IE) literature (Keupp & Gassmann, 2009), have investigated entry into foreign markets. Studies in this area have typically examined new ventures’ “early internationalization,” defined as the time it takes new ventures from inception to enter foreign markets for the first time (Wu & Zhou, 2018).

The IE literature explains that some new ventures internationalize early because of their founders’ ability to rapidly discover, act on, and exploit opportunities across national borders (McDougall & Oviatt, 2000). International entry and expansion give new ventures opportunities to broaden their market reach, make better use of their capabilities and resources, acquire new knowledge and other resources, and widen their networks (Sapienza, Autio, George, & Zahra, 2006; Zahra, Ireland, & Hitt, 2000). However, entering foreign markets also entails considerable risks that are hard to manage for young ventures, which typically have limited resources and lack accumulated operational experience. These ventures must build the infrastructure needed to export and acquire the necessary licenses to operate in foreign markets and also identify relevant customers and find the best way to reach them. As such, “internationalization adds an additional layer of external uncertainty to the market and technological uncertainty to which the new firm is already subjected” (Autio, George, & Alexy, 2011: 31). These limitations can delay or even discourage new ventures’ first entry into foreign markets.

One of the key obstacles to new ventures’ early internationalization is their lack of resources and experience to manage the complex tasks of internationalization (Cavusgil & Knight, 2015). New ventures can offset this limitation by taking advantage of the experience that their founders have previously acquired while working for international firms (Autio, 2017). Such prior experience can lead to greater market knowledge, faster and easier access to networks that give new ventures the complementary assets needed for expansion, and improved identification and pursuit of opportunities (McDougall, Oviatt, & Shrader, 2003), all of which can facilitate early entry into foreign markets (Zucchella, Palamara, & Denicolai, 2007).

Despite the recognition that new ventures can draw upon their founders’ prior experience to acquire the knowledge and routines needed to hasten foreign market entry, researchers have primarily studied founders’ prior independent international experience (see Oviatt & McDougall, 1997). “Independent experience” refers to the prior experience that individual founders have gained independently from each other (i.e., in different organizations). While founders’ prior independent experience can eventually lead to the transfer of knowledge and routines to the new venture, the process of integrating and coordinating independent prefounding knowledge and routines from a group of cofounders is often lengthy. For instance, “if all team members independently gained their pre-founding experience at different organizations or at different time points, stark differences could occur among individuals regarding the core elements of success” (Zheng et al., 2016: 2506). This can make ventures slower to share independently acquired information or agree on the appropriate course of action, delaying their first entry into foreign markets. However, these challenges are easier to overcome when cofounders have developed prior shared experience.

We propose that founders’ prior shared international experience reduces new ventures’ time to first foreign market entry and that this relationship is contingent on two boundary conditions: the diversity of the founders and the dynamism of the firm’s external (task) environment. We also argue that early internationalizers enjoy higher performance than late internationalizers. We discuss these points next.

Founders’ Prior Shared International Experience and Time to First Foreign Market Entry

The literature underscores the importance of founders’ prior shared experience for new ventures. Prior studies focused on either general shared experience of founders or top managers (Eisenhardt & Schoonhoven, 1990; Leung, Der Foo, & Chaturvedi, 2013; Schoonhoven et al., 1990) or shared experience that is specific to a certain domain of action, such as a domestic market (Bruneel, Clarysse, & Autio, 2018) or an industry (Honoré, 2020; Okhmatovskiy et al., 2020; Zheng et al., 2016). In our study, the domain of action is foreign market entry. Therefore, we will focus on founders’ prior shared international experience, defined as founders’ prior joint working experience in firms with foreign market sales before the founding of their new venture. Such experience is important because the activities undertaken, and the strategic challenges faced by firms operating in international markets, differ significantly from those encountered by firms operating in domestic markets. Thus, founders who have worked concurrently in firms with foreign market sales should be able to develop shared knowledge and routines that are relevant and specific to initiating foreign market sales.

Eriksson, Johanson, Majkgard, and Sharma (1997) identify three types of foreign market experience-based knowledge: foreign institutional knowledge (e.g., knowledge about foreign cultures and institutions), foreign business knowledge (e.g., knowledge about customers and competitors), and internationalization knowledge (e.g., knowledge about how to engage in international activities). Shared knowledge of foreign institutions and markets gives new venture founders a shared understanding of the opportunities and problems they are likely to encounter in specific foreign markets. As a result, it can facilitate foreign market entry “by prompting entrepreneurs to seek certain types of data, give greater weight to particular pieces of data or interpret them in specific ways, and emphasize particular international opportunities” (Zahra, Korri, & Yu, 2005: 137). If founders have no prior foreign institutional or business knowledge, or they have gained it independently from each other, the foreign market entry process will be lengthier, as they will need to spend time either gaining such knowledge or sharing their independently acquired information and then agree on the appropriate course of action.

Shared internationalization knowledge, on the other hand, directly enables action, as it provides new ventures with shared knowledge of how to enter foreign markets and routines for doing so. Examples are knowledge and routines on how to develop and execute market entry strategies; assess the risks of partner opportunism when exploring, forming, and exploiting relationships in new foreign countries; and evaluate partners and distributors (Fletcher, Harris, & Richey, 2013). As proposed by prior research, “the importation of routines from the managerial team’s previous employment experience with international markets serves as the embryonic routines to enter new markets, consequently reducing the time and costs of capability development” (Sapienza et al., 2006: 916). The transfer of these routines to the new venture should be easier if a group of cofounders shares such prior employment experience. Together, these observations suggest our first hypothesis:

Hypothesis 1: There is a negative relationship between founders’ prior shared international experience and their new ventures’ time to first foreign market entry, meaning that new ventures that have such experience will enter foreign markets for the first time earlier.

Boundary Conditions

Although founders’ prior shared international experience can reduce the time it takes new ventures to enter foreign markets for the first time, some scholars have questioned whether prior shared experience is an unambiguous blessing for new ventures (Zheng et al., 2016). Two factors, in particular, can alter the potential benefits of this type of experience when it comes to first foreign market entry: founders’ diversity and industry dynamism. These factors relate to the context-dependent nature of shared experience and to its potential obsolescence, respectively.

Founders’ diversity

Failure to adapt the knowledge gained in the context of previous firms to the novel context of the new venture’s early internationalization may undermine the value of prior shared international experience. Knowledge tends to be contextualized and dependent on the surroundings in which it was developed, used, and refined (Kogut & Zander, 1996; Rodan & Galunic, 2004). This context-dependent aspect of knowledge has led some scholars to question the extent to which knowledge can simply be transferred from its original business context to a novel one. In fact, some prior studies have claimed that “to transfer knowledge effectively in the face of context dependence, firms must adapt knowledge to a new setting” (Williams, 2007: 868). This argument can be extended to the shared knowledge and routines that groups of cofounders bring to the new venture from their previous workplaces. Fortunately, these cofounders can still vary along dimensions that can affect the successful adaptation of knowledge and routines across organizational boundaries (Wezel et al., 2006). The diversity or homogeneity of cofounders, we argue, is one such dimension.

Building on prior research, we view founders’ diversity as an aggregate team-level construct that represents differences in founders’ characteristics, such as age, gender, ethnicity, and educational background (Van Knippenberg & Schippers, 2007). There is a long research tradition that holds that diverse groups are likely to possess a broader pool of knowledge, skills, and abilities—which, in turn, bring along different perspectives and opinions (Van Knippenberg & Schippers, 2007). Therefore, founders’ diversity increases the range of knowledge, skills, and perspectives available in a group. This can increase the possibility that the group of cofounders possesses the complementary knowledge that is needed to adapt “what worked” in their previous firms and to devise actions and solutions that fit the context of their new ventures (see Williams, 2007). Barkema and Shvyrkov (2007) provide an example of how diversity in the educational background of top management team members may play out in a firm’s foreign market entry. The authors note that an engineer might be more likely to focus on the manufacturing side of foreign expansion; a lawyer, on the legal aspects of investing in foreign markets; and an MBA, on organizational and financial issues. Such a team would be expected to have greater diversity in knowledge and perspectives than a team made up only of engineers. Groups of cofounders with diverse backgrounds may adapt their prior shared international experience more quickly to the new context of the new venture.

In contrast, groups of cofounders with prior shared international experience who are homogeneous in terms of age, gender, ethnicity, and educational background may be less able to adapt successful experiences with internationalization in their previous firms (i.e., “what worked”) and to devise solutions and actions tailored to the resources and conditions of the new venture, thus delaying first foreign market entry (Autio et al., 2011). This is because these groups of cofounders are likely to possess overlapping knowledge, skills, and perspectives. Thus, we would expect the combination of founders’ prior shared international experience and their background diversity to facilitate the adaptation of shared knowledge and routines and hasten their new ventures’ first entry into foreign markets. These observations lead to our second hypothesis:

Hypothesis 2: Founders’ diversity strengthens the negative relationship between founders’ prior shared international experience and new ventures’ time to first foreign market entry.

Industry dynamism

Another reason for concern over whether founders’ prior shared experience is an unambiguous blessing for new ventures stems from its vulnerability to knowledge obsolescence. The threat of knowledge obsolescence, which is imposed by continuous developments in the external environment, requires continuous updates of a venture’s knowledge base. In new ventures where founders share prior experience, updating the knowledge base may take longer because of the amount of prefounding shared knowledge and routines. Hence, it is questionable whether such prior shared knowledge would still be relevant for the environment that the new venture faces. Given this potential mismatch, some scholars have asserted that prior shared experience could constrain strategic actions (Fern et al., 2012), leading to competence traps as founders revert to what they already know while ignoring rapid external changes. Obviously, knowledge does not become equally obsolete across all markets or industries; it becomes obsolete more rapidly or more severely in certain markets than in others (Castrogiovanni, 2002; Rothman & Perrucci, 1971). The rate of knowledge obsolescence is connected to the characteristics of the task environment, such as the extent to which demand, competition, and/or technologies constantly change. In dynamic environments, knowledge becomes obsolete very quickly, even if it was highly valuable in the recent past (Shin & Pérez-Nordtvedt, 2020). Thus, the characteristics of the task environment, particularly market dynamism, set important boundary conditions for the relevance of prior shared experience.

Industry dynamism refers to the speed and magnitude of change in a new venture’s focal industry (Dess & Beard, 1984). A high level of dynamism usually signals the obsolescence of current knowledge and the arrival of a new stage in an industry’s evolution, requiring new thinking and the development of new strategies and business models (Larrañeta, Zahra, & Galán González, 2014). In this case, dynamism is likely to reduce the relevance of the founders’ prior shared knowledge. If “founding teams with PSE [prior shared experience] inherit a common basis for collective action because they acquired their experience in the same information environment at their former organization” (Zheng et al., 2016: 2505), then such collective action is likely to be delayed when the information environment changes because of increased dynamism. In particular, dynamism raises questions about the relevance of founders’ prior shared knowledge vis-à-vis the challenges posed by the changing competitive environment in the industry. First, founders with prior shared experience may feel confident about relying on the knowledge that already exists within the new venture team, when in reality the task environment is in constant flux. In fact, a longitudinal field study using multiple case studies of Finnish new ventures led Autio et al. (2011: 26) to report that ventures with prior shared experience “appeared reluctant to revise interpretations based on foreign market feedback, which retarded efforts to devise alternative solutions,” increasing these ventures’ risks of falling into a competency trap. Additionally, when industry dynamism is high, having prior shared international experience can limit founders’ ability to search for new knowledge and information, which will further delay the development and updating of routines for foreign market entry (Andersson, Evers, & Kuivalainen, 2014). These observations together suggest our third hypothesis:

Hypothesis 3: Industry dynamism weakens the negative relationship between founders’ prior shared international experience and new ventures’ time to first foreign market entry.

The Performance of Early Internationalizers

The implications of time to first market entry for firm performance are both complex and contingent in nature. However, there is consensus in the literature that a shorter time to market entry allows new ventures to exploit opportunities before they disappear or are exploited by others (Bakker & Shepherd, 2017). As Forbes (2005: 356) explains, time to market entry might be especially important to new ventures, which “seek to exploit the nimbleness conferred by their relative smallness.” In the case of first foreign market entry, early internationalizers are able to develop processes that are tailored to the conditions in international markets, to assimilate new knowledge and skills, and to develop their capabilities, which is consistent with the “advantages of newness” argument in the IE literature (Autio, Sapienza, & Almeida, 2000). Ultimately, early internationalizers learn how to adapt the venture’s resources and routines for different markets and conditions, providing them with learning gains (Zahra, Zheng, & Yu, 2018).

In contrast, late internationalizers typically need to adjust or change the existing routines and processes developed during the venture’s domestic operations. These changes and adjustments—including the inherent challenge of unlearning—grow more difficult as ventures age, because older ventures are more inert and reluctant to incorporate new knowledge (De Clercq, Sapienza, Yavuz, & Zhou, 2012; Schwens, Zapkau, Bierwerth, Isidor, Knight, & Kabst, 2018). Consistent with these arguments, a recent meta-analysis finds that earlier age at entry is associated with improved firm performance (Williams & Crook, 2021). On the basis of these observations, we propose our fourth and final hypothesis:

Hypothesis 4: Early internationalizers perform better than late internationalizers.

Method

Data

To test our hypotheses, we use a data set constructed from three different longitudinal data sources provided by the Swedish Central Bureau of Statistics (SCB): SCB’s exporter register, Registerbaserad arbetsmarknadsstatistik (RAMS), and Longitudinell integrationsdatabas för sjukförsäkrings—och arbetsmarknadsstudier (LISA). The SCB’s exporter register provides information on the destination countries and value for all export sales made by firms registered in Sweden (available between 1997 and 2018). The RAMS database includes a complete list of all registered businesses in Sweden that have corporate income tax accounts and that legally hire employees, and it provides information on each firm’s financial, demographic, and ownership characteristics. The LISA database provides information on all employed individuals in Sweden, including their employers, gender, age, ethnic background, and education. We use firms’ identification numbers to link them to their export activities and to link employees to their employers.

To develop our sample, we select firms that were established between 2001 and 2017 and track their export activities from inception until 2018. 1 Sweden is an ideal context for testing our predictions because it is a small, open economy where domestic demand is limited and where, consequently, foreign market entry is a critical strategic decision that new ventures need to consider from inception. We focus on the manufacturing and retailing sectors, as new ventures in these sectors in Sweden often tend to enter foreign markets from a very early age to achieve economies of scale and scope and overcome the limited size of their home market. Moreover, Swedish firms operating in these industries typically compete in niches, which pushes them to undertake foreign market entry right from the start.

As a key aspect of this study is founders’ prior shared international experience, we exclude new firms owned by a business group or by a foreign company, which typically have different resources at founding and pursue different strategies (Mudambi & Zahra, 2007). Thus, our sample excludes subsidiaries of established firms; it focuses only on independent new ventures owned and run by their founders. We also exclude new ventures that resulted from two or more existing companies merging or splitting as well as new ventures with more than 10 employees at founding, because these are typically not considered to be new firms but rather reorganizations of preexisting firms. Finally, we build on the work of Lazar et al. (2020) and focus on groups of cofounders by studying only those ventures with two or more founders (see Table A.1 in the supplementary Appendix A for the distribution of new ventures by number of founders). 2 Eliminating solo-founder ventures is in line with prior research on founders’ prior shared experience (see, e.g., Honoré, 2020; Zheng et al., 2016) and also limits the influence of potential confounding effects when comparing substantially different types of new ventures (Shepherd et al., 2021). To further align our approach to the idea that a group of cofounders generates the idea collectively (Lazar et al., 2020), we focus on individuals listed in our data as founders in the year when the new venture was started (Knight et al., 2020). In our register data, founders are identified as individuals who own and run the business (i.e., owner-managers); this approach has been used by prior studies using the same data (see, e.g., Bird & Zellweger, 2018). 3 Further, we focus only on incorporated new ventures. Finally, to ensure that our results are not biased by the inclusion of new ventures that never undertook foreign market entry because they failed or their founders exited before it could take place, we remove these ventures from our sample. In two additional analyses, we add these new ventures to the sample. The results are reported in the supplementary Appendix B and are largely in line with our main results. Our final sample contains 4,550 firm-year observations from 1,405 new ventures. Of these ventures, 806 initiated foreign market entry during the study observation period.

Estimation Strategy

To measure the time to first foreign market entry, we compute the elapsed time between the year a firm is created and the year it undertakes its first foreign market entry. This calls for a model that specifies this duration as a function of the observable variables, with the idea that a shorter duration represents faster first foreign market entry. Common models are parametric regression survival-time models, in which the effect of the covariates is modeled as having a proportional effect on the hazard rate. Such models are preferred over a traditional linear or logistic regression as the former are able to implement time-to-event analysis and handle right censoring—that is, observations that did not initiate foreign market entry during the observation period of the study but may do so in the future (see Jiang, Kotabe, Zhang, Hao, Paul, & Wang, 2020)—while the latter models (linear or logistic regression) lack both the implementation of time-to-event analysis and a treatment for right censoring. This last issue is even more prominent in our data because we use multiple cohorts that we follow for different periods.

Different kinds of models may be obtained by imposing different assumptions about the baseline hazard function. In this study, we employ a piecewise-constant exponential model that allows the hazard rate of first foreign market entry to vary across time periods, but the hazard rate is assumed to be constant within each time period. This approach is typically chosen when modeling time dependence in the absence of strong theoretical reasons that guide the choice of a certain specification of duration dependence for the phenomenon under assessment (Jenkins, 2005). 4

For the new venture performance variables, we are interested in comparing the performance of early internationalized firms to that of late internationalized firms. As such, we use a between-effects linear regression. Since having multiple cohorts followed for different time periods makes our panel unbalanced, we used weighted least squares.

Dependent Variables

Time to first foreign market entry

To estimate our model, we set the data such that our unit of observation is the new venture in each year of activity. Ventures are included in the data set repeatedly until either they have undertaken their first foreign market entry or the observation period of the study ends. Each observation is identified by the age of the firm in that year. Our indicator variable is a dummy that takes the value 1 if a new venture undertakes its first foreign market entry in that year. The observation period spans the time that elapses between founding and the year 2018; new ventures that did not initiate foreign market entry within this period are included in the sample and treated as right-censored cases.

Following the literature, we use foreign market sales as a key indicator of new ventures’ initiation of their foreign market entry activities (Oviatt & McDougall, 1994). As observed by Sullivan (1994: 331), “a company’s foreign sales are a meaningful first-order indicator of its involvement in international business.” Similarly, Yu et al. (2011: 431) argue that the first foreign sale constitutes an initial milestone that a firm reaches in overseas expansion and signals the acceptance of the firm by foreign customers.

We define foreign market sales as sales revenue derived from exports and compute this variable using both the SCB’s exporter register data source, which provides yearly information on firms’ export sales, and the RAMS data source, which provides information on firms’ founding year. The results from the Kaplan-Meier analysis appear in the supplementary Appendix C.

New venture performance

We use two time-varying variables to measure new venture performance. The first variable is operating profit per employee, calculated as operating profit divided by the number of employees. The second variable is domain-specific and focuses on international intensity, measured as the value of export sales divided by total sales.

Independent Variable

We measure founders’ prior shared international experience using a relational approach, considering each dyad of founders identified from the LISA data. Specifically, we look at whether new venture founders worked concurrently for a business with foreign market sales anytime between 1997 and the year before starting their new venture. To increase the chances that these individuals interacted with each other while working concurrently for the same prior employer, we restrict our measure to individuals who had worked in the same establishment, given that a single firm may consist of several separate establishments. 5 This variable is computed using both the SCB’s exporter register, which provides information on (the prior employer) firms’ export sales for the 1997-2018 period, and the LISA data source, which provides information on employees’ prior employers’ identification number. Tables A.2 and A.3 in the supplementary Appendix A describe the new ventures in our sample around this variable.

Moderating Variables

Founders’ diversity

We measure this variable by first calculating diversity indexes for four different variables: founder age, gender, ethnicity, and education. Tables A.4 to A.7 in the supplementary Appendix A describe the distribution of founders in our sample on these dimensions. For each dimension, we calculate diversity using the Blau index as follows:

where pk is the share of founders belonging to the kth group of the dimension under assessment in the new venture. For founders’ age, we consider four groups: the Silent Generation (born 1928-1945), baby boomers (born 1946-1964), Generation X (born 1965-1980), and millennials (born 1981-1998). 6 For founders’ gender, we consider male and female. For founders’ ethnic backgrounds, we consider their country of birth. 7 For founder education, we use the groupings of educational background based on the official International Standard Classification of Education, which is also implemented in the Swedish education nomenclature (SUN2000). Each individual has a single-digit “education” field that can take one of the following nine values: general education; pedagogy and teaching; social science, law, business, and administration; natural science, mathematics, and computer science; technology and manufacturing; agriculture, forestry, and animal care; health, medical care, and social care; services; or other. 8 After calculating diversity indexes for the four different variables, we add these four indexes into one single variable. The minimum value this variable can take is 0, which means that all founders share the same gender, belong to the same age group, and have the same ethnic and educational backgrounds. Tables A.8 to A.13 in the supplementary Appendix A describe the new ventures in our sample around these founders’ diversity dimensions.

Industry dynamism

Industry dynamism reflects the amount of change in each industry (Dess & Beard, 1984). Following Nielsen and Nielsen (2013), this measure is calculated by first regressing time against annual average sales for each industry for a 5-year window such that the value for year t is calculated from a regression covering years t − 4 through t. Then, the standard error of the regression slope coefficient is used to measure the value of dynamism. A larger standard error suggests that industry sales over time are more unpredictable. We define industry using four-digit Swedish Standard Industrial Classification (SNI) codes. Because the raw measure is right-skewed, we use the natural logarithm transformation (Baron & Tang, 2011). 9 In our sample, the average value of this variable for the retailing industry sector is 5.6 (SD = 1.58), whereas for the manufacturing industry sector, it is 7.02 (SD = 1.84). Figure A.1 in the supplementary Appendix A shows the distribution of this variable across these two industry sectors.

Control Variables

We use several time-varying industry-related and firm-specific controls. We control for the industry competition ratio, measured as the percentage of firms that ceased to exist (over the total number of firms) in each industry based on four-digit SNI codes, as well as for the industry’s degree of internationalization, measured as the natural logarithm of the sum of firms’ export sales in each industry based on four-digit SNI codes.

The analyses also control for new venture size, which we capture using the natural logarithm of the number of employees (including the founders). We also control for new venture productivity, measured as value added divided by the number of employees, and for new venture fixed assets. We control for the length of founders’ independent international experience, measured as the natural logarithm of (one plus) the number of years that founders worked independently for firms with foreign market sales before starting the new venture. We also control for the length of founders’ prior shared domestic experience (Bruneel et al., 2018), measured as the natural logarithm of (one plus) the number of years founders worked concurrently for the same organization without foreign market sales before starting their new venture, as well as for the length of founders’ prior shared industry experience (Zheng et al., 2016), measured as the natural logarithm of (one plus) the number of years founders worked concurrently for the same organization operating in the same industry as their new venture, based on two-digit SNI codes. Since we have different cohorts in our sample, we control for cohort effects using cohort dummies. We also control for year dummies and industry dummies using two-digit SNI codes. 10 Table A.14 in the supplementary Appendix A shows the distribution of the new ventures in our sample across the two-digit SNI codes, while Table A.15 compares new ventures in the two industry sectors (i.e., retailing and manufacturing) on some key firm-level characteristics.

Finally, given that prior research has shown that founders’ education, both general and specific, impacts the international intensity of their new venture (Ganotakis & Love, 2012), in our model predicting new venture performance, we control for two additional variables: founders’ general education, calculated as the average years of formal education among the founders (M = 11.27, SD = 3), and founders’ business education, which takes a value of 1 if at least one of the founders has their highest degree in social science, law, or business and administration, based on the Swedish education nomenclature (0 otherwise; M = 0.34, SD = 0.47).

Results

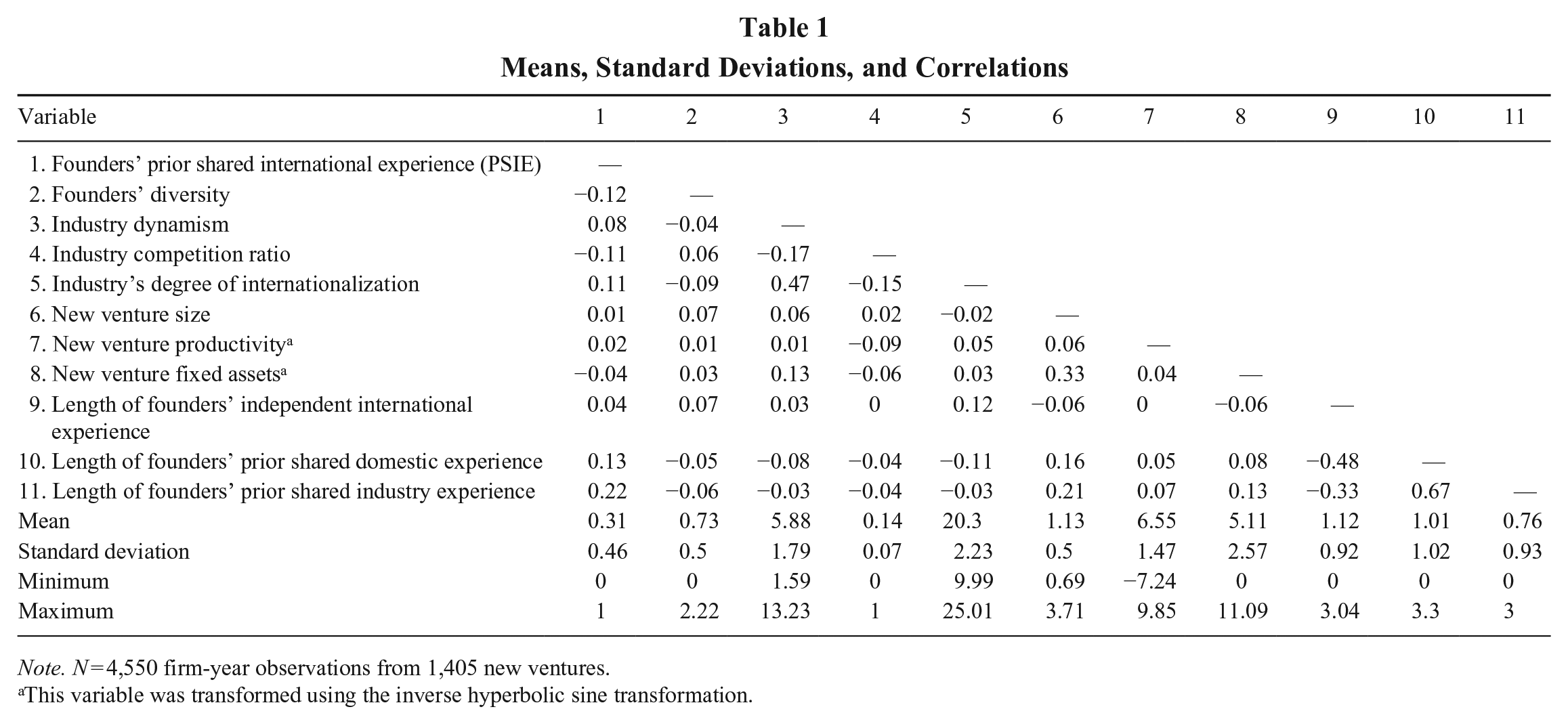

Table 1 presents the descriptive statistics and correlations for the variables in the model.

Means, Standard Deviations, and Correlations

Note. N = 4,550 firm-year observations from 1,405 new ventures.

This variable was transformed using the inverse hyperbolic sine transformation.

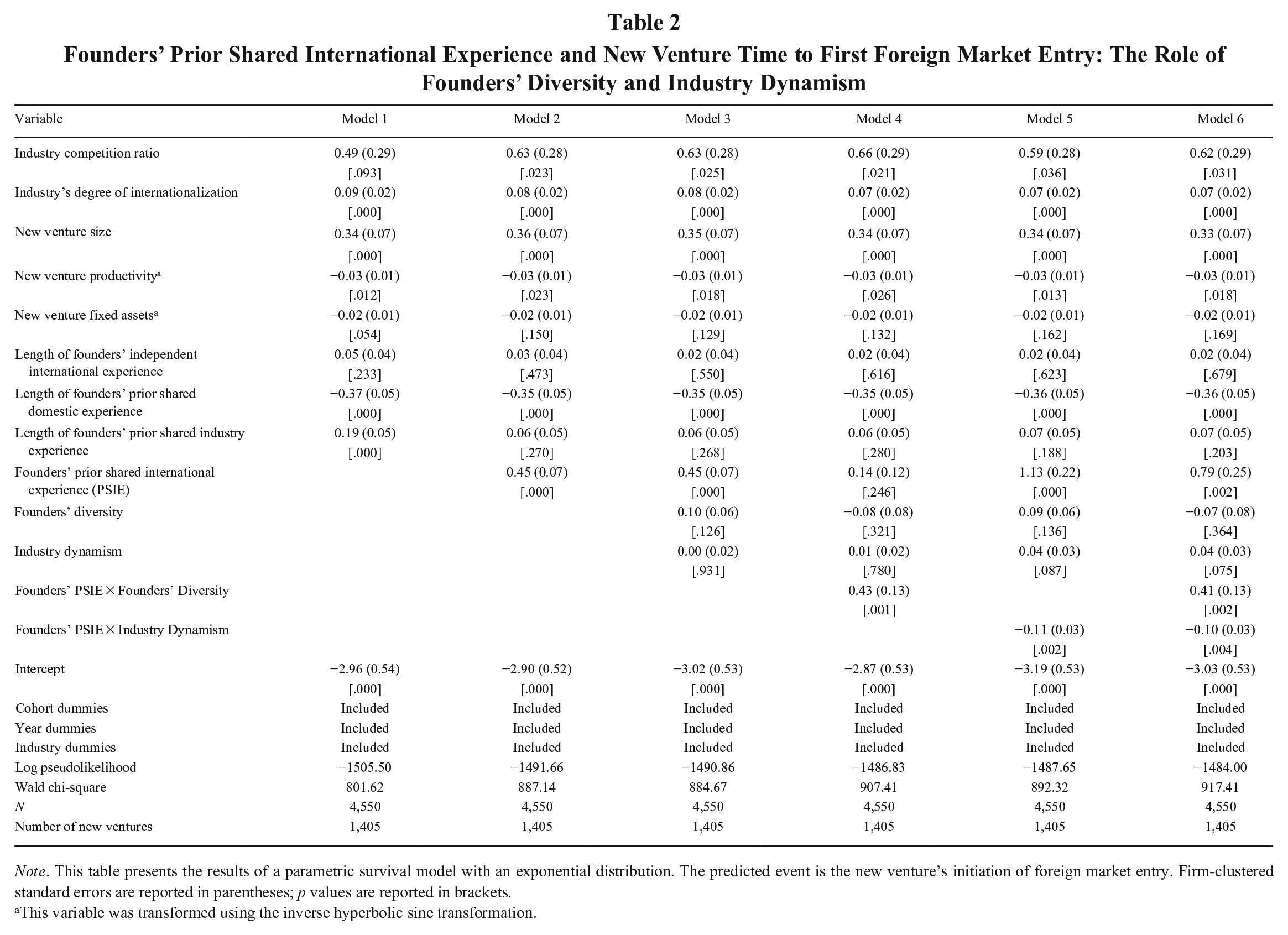

Table 2 presents the results of the parametric survival analysis. Positive coefficient estimates indicate that the covariate accelerates the hazard of first foreign market entry (i.e., it occurs earlier). Negative coefficient estimates indicate that the covariate decelerates the hazard of first foreign market entry (i.e., it occurs later). Model 1, in Table 2, includes the study’s control variables. Model 2 tests Hypothesis 1, on the relationship between founders’ prior shared international experience and new ventures’ time to first foreign market entry. The results show that new ventures with founders’ prior shared international experience undertake their first foreign market entry earlier than those that lack such experience (coefficient = 0.45; p < .001), consistent with Hypothesis 1. We also calculate the predictive marginal effect of the founders’ prior shared international experience on the time to first foreign market entry, holding all other variables at their mean value. The results show that the expected median time to first foreign market entry of new ventures with founders’ prior shared international experience in our sample is 5.8 years, compared with 9 years for new ventures without such experience. Finally, we test whether the coefficient of the founders’ prior shared international experience variable is different from both the coefficient of the length of founders’ independent international experience variable and the coefficient of the length of founders’ prior shared industry experience variable. To do so, we standardize the three variables, rerun Model 2, and use the postestimation test command in Stata. Our results show that founders’ prior shared international experience has a greater negative influence on time to first foreign market entry than both the length of founders’ independent international experience (χ2 = 12.44, p = .0004) and the length of founders’ prior shared industry experience (χ2 = 5.13, p = .0235). Altogether, these findings underscore the importance of founders’ prior shared international experience in explaining new ventures’ time to first foreign market entry. 11

Founders’ Prior Shared International Experience and New Venture Time to First Foreign Market Entry: The Role of Founders’ Diversity and Industry Dynamism

Note. This table presents the results of a parametric survival model with an exponential distribution. The predicted event is the new venture’s initiation of foreign market entry. Firm-clustered standard errors are reported in parentheses; p values are reported in brackets.

This variable was transformed using the inverse hyperbolic sine transformation.

Model 3 introduces both the founders’ diversity and industry dynamism variables. Model 4 adds the interaction between founders’ prior shared international experience and founders’ diversity. Hypothesis 2 predicts that founders’ diversity strengthens the relationship between founders’ prior shared international experience and new ventures’ time to first foreign market entry. The interaction coefficient is positive and highly significant (coefficient = 0.43; p = .001). Model 5 adds the interaction between founders’ prior shared international experience and industry dynamism. Hypothesis 3 predicts that industry dynamism weakens the relationship between founders’ prior shared international experience and new ventures’ time to first foreign market entry. In support of this hypothesis, the results show a negative and highly significant interaction coefficient (coefficient = −0.11; p = .002). Finally, Model 6 shows the saturated model where both interactions are highly significant when added simultaneously.

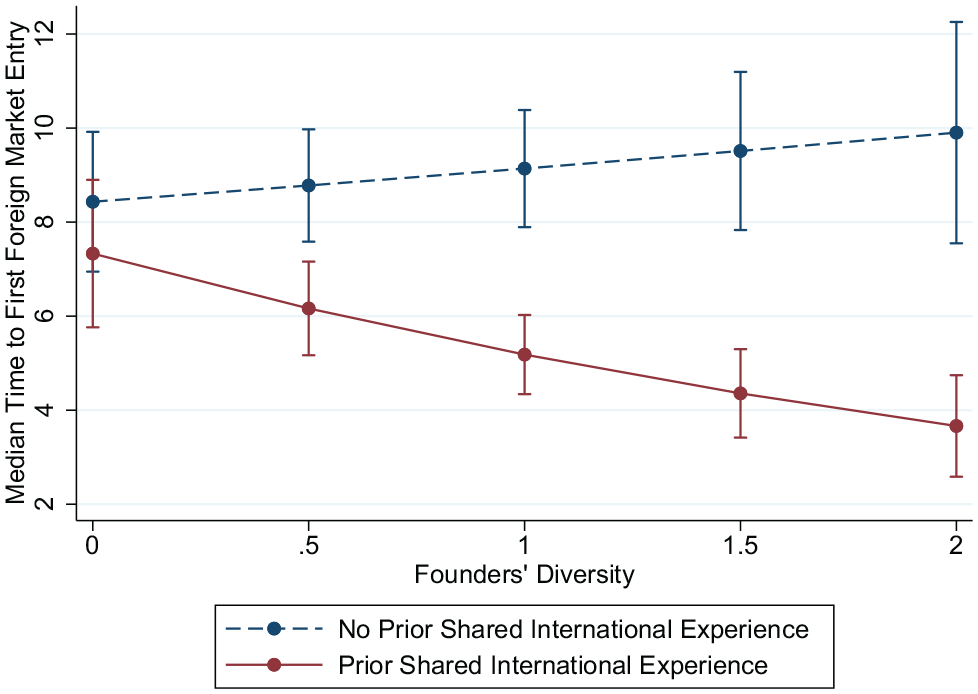

Next, we compute and plot the adjusted predicted values of the results testing Hypotheses 2 and 3. Figure 1 plots the interaction related to founders’ diversity (Hypothesis 2). The results show that when founders’ diversity is lowest (founders’ diversity = 0), the expected median time it takes new ventures with founders’ prior shared international experience to initiate foreign market entry is 7.3 years, compared with the 8.4 years it takes new ventures without such experience. In contrast, when founders’ diversity is high (founders’ diversity = 2), the expected median time it takes new ventures with founders’ prior shared international experience to initiate foreign market entry is 3.7 years, compared with the 9.9 years it takes new ventures without such experience. The difference in time to first foreign market entry between new ventures with and without founders’ prior shared international experience is thus larger when founders’ diversity is high compared with when it is low. These results indicate that the benefits of prior shared international experience increase with founders’ diversity, supporting Hypothesis 2.

Founders’ Prior Shared International Experience, Founders’ Diversity, and New Venture’s Time to First Foreign Market Entry

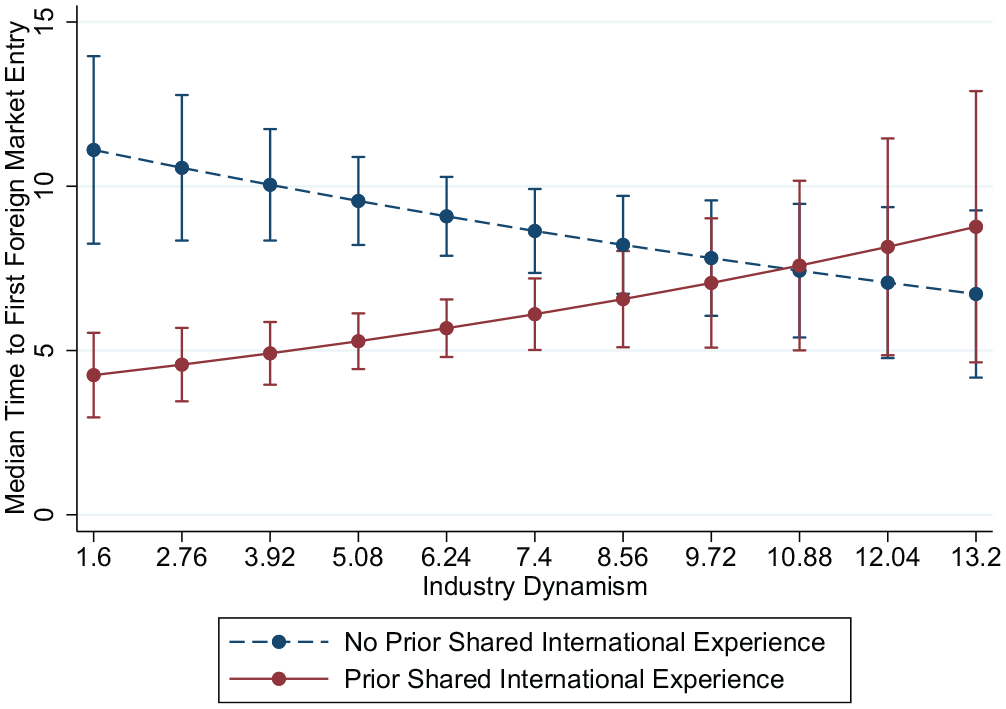

Figure 2 plots the interaction related to industry dynamism (Hypothesis 3). The results show that in less dynamic environments (industry dynamism = 1.6), the expected median time it takes new ventures with founders’ prior shared international experience to initiate foreign market entry is 4.3 years, compared with the 11.1 years it takes new ventures without such experience. In contrast, in highly dynamic environments (industry dynamism = 13.2), the expected median time it takes new ventures with founders’ prior shared international experience to initiate foreign market entry is 8.8 years, compared with the 6.7 years it takes new ventures without such experience. The difference in time to first foreign market entry between new ventures with and without founders’ prior shared international experience is substantially smaller when industry dynamism is high compared with when it is low. These results suggest that the benefits of prior shared international experience decrease with industry dynamism, providing support for Hypothesis 3.

Founders’ Prior Shared International Experience, Industry Dynamism, and New Venture’s Time to First Foreign Market Entry

Hypothesis 4 argues that early internationalizers perform better than late internationalizers. To test this, we follow Williams and Crook (2021) in creating two dummy variables: early internationalizers (1 if the new venture had carried out its first foreign market entry within the first 3 years of existence, 0 if not) and late internationalizers (1 if the new venture had carried out its first foreign market entry after the first 3 years of existence, 0 if not). The reference category in this analysis is new ventures that had not carried out any foreign market entry during the time frame of the study. 12

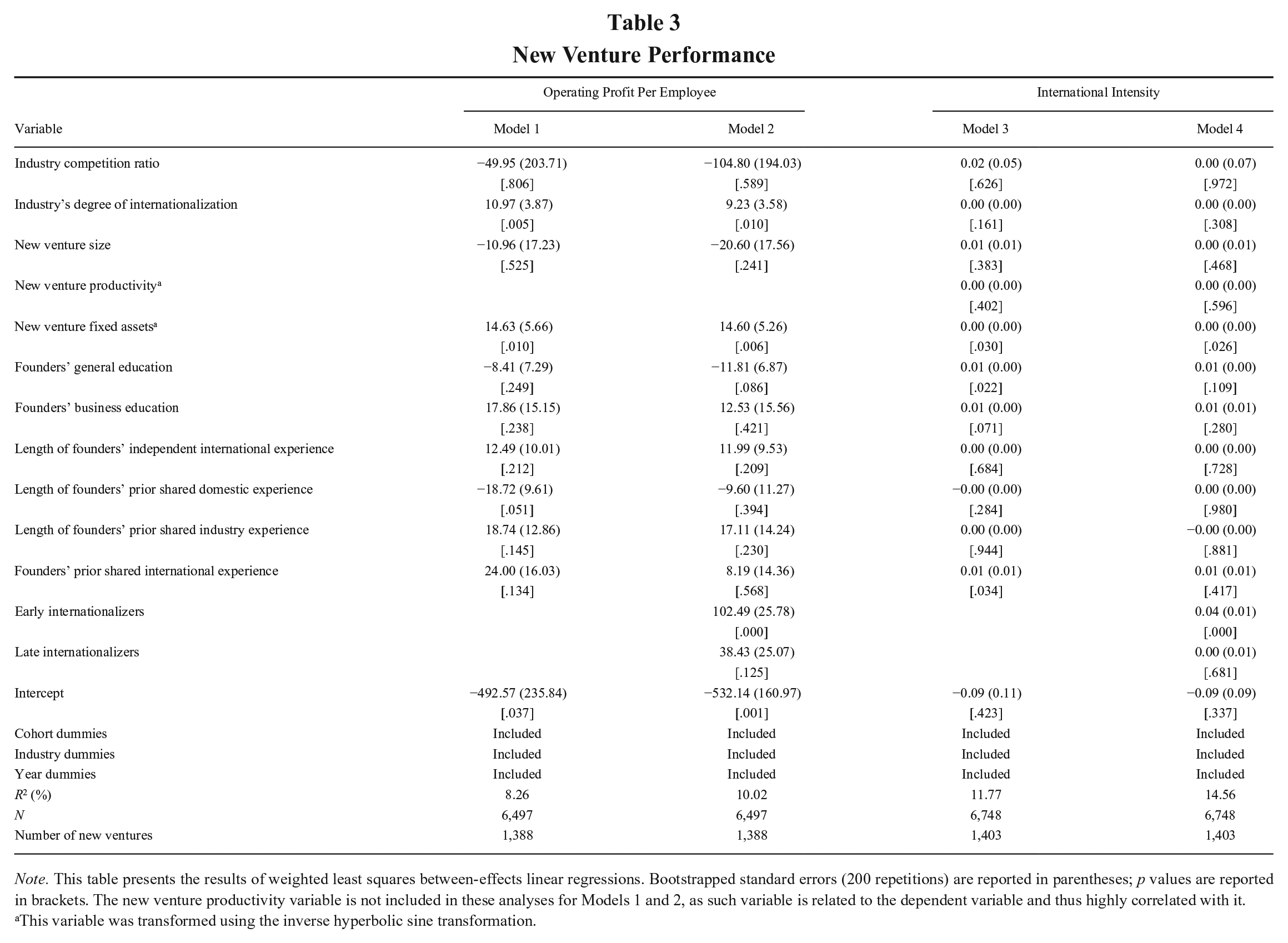

Models 1 and 2 in Table 3 show the results using operating profit per employee as a measure of new venture performance. Model 1 includes the control variables. Model 2 includes the two dummy variables early internationalizers and late internationalizers. The results show that the relationship between early internationalizers and operating profit per employee is positive and highly significant (coefficient = 102.49; p < .001). The relationship between late internationalizers and operating profit per employee, meanwhile, is positive but insignificant (coefficient = 38.43; p = .125). Our results also show that the difference between the coefficient of the early internationalizers variable and the coefficient of the late internationalizers variable is significantly different from zero, suggesting that the early internationalizers variable has a greater positive influence on operating profit per employee than the late internationalizers variable (χ2 = 4.37, p = .0365).

New Venture Performance

Note. This table presents the results of weighted least squares between-effects linear regressions. Bootstrapped standard errors (200 repetitions) are reported in parentheses; p values are reported in brackets. The new venture productivity variable is not included in these analyses for Models 1 and 2, as such variable is related to the dependent variable and thus highly correlated with it.

This variable was transformed using the inverse hyperbolic sine transformation.

Models 3 and 4 show the results using international intensity as a domain-specific measure of new venture performance. Model 3 includes the control variables. Model 4 includes the two dummy variables early internationalizers and late internationalizers. The results show that the relationship between early internationalizers and international intensity is positive and highly significant (coefficient = 0.04; p < .001). The relationship between late internationalizers and international intensity, meanwhile, is positive but insignificant (coefficient = 0.00; p = .681). Our results also show that the difference between the coefficient of the early internationalizers variable and the coefficient of the late internationalizers variable is significantly different from zero, suggesting that the early internationalizers variable has a greater positive influence on international intensity than the late internationalizers variable (χ2 = 36.25, p = .0000). Together, these analyses provide support for Hypothesis 4.

Robustness Checks

We conduct several tests to check the validity of our results. In this section, we present some of these robustness checks.

Length of founders’ prior shared international experience

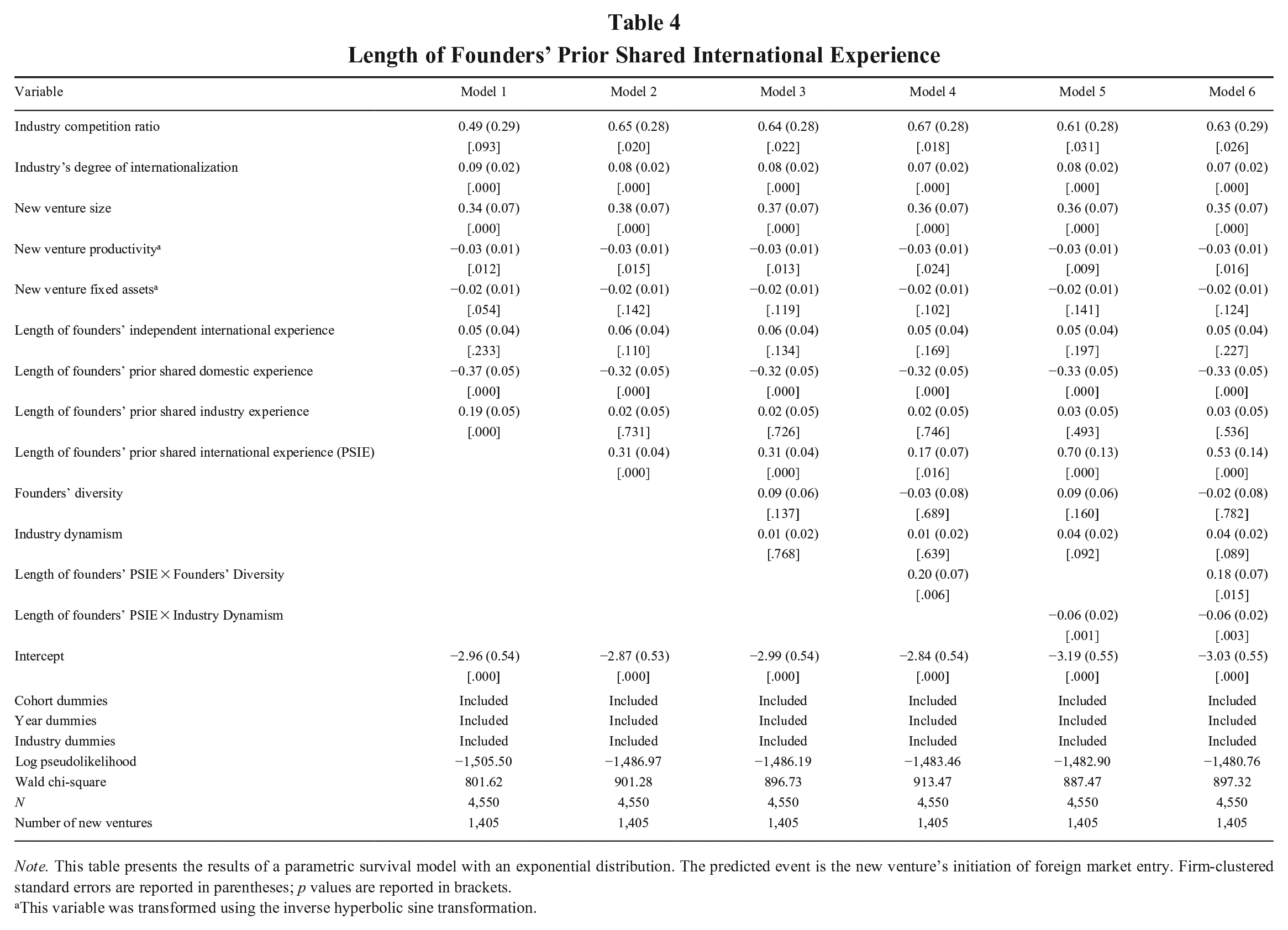

In this robustness test, we adopt an alternative measure of founders’ prior shared international experience. Given the literature that supports that shared knowledge is more pronounced the longer individuals have worked together (see, e.g., Berman, Down, & Hill, 2002), we replace our original dummy variable of founders’ prior shared international experience with a count variable that captures the natural logarithm of (one plus) the length of founders’ prior shared international experience. The results, which appear in Table 4, are largely in line with our main results.

Length of Founders’ Prior Shared International Experience

Note. This table presents the results of a parametric survival model with an exponential distribution. The predicted event is the new venture’s initiation of foreign market entry. Firm-clustered standard errors are reported in parentheses; p values are reported in brackets.

This variable was transformed using the inverse hyperbolic sine transformation.

Alternative measure of industry dynamism

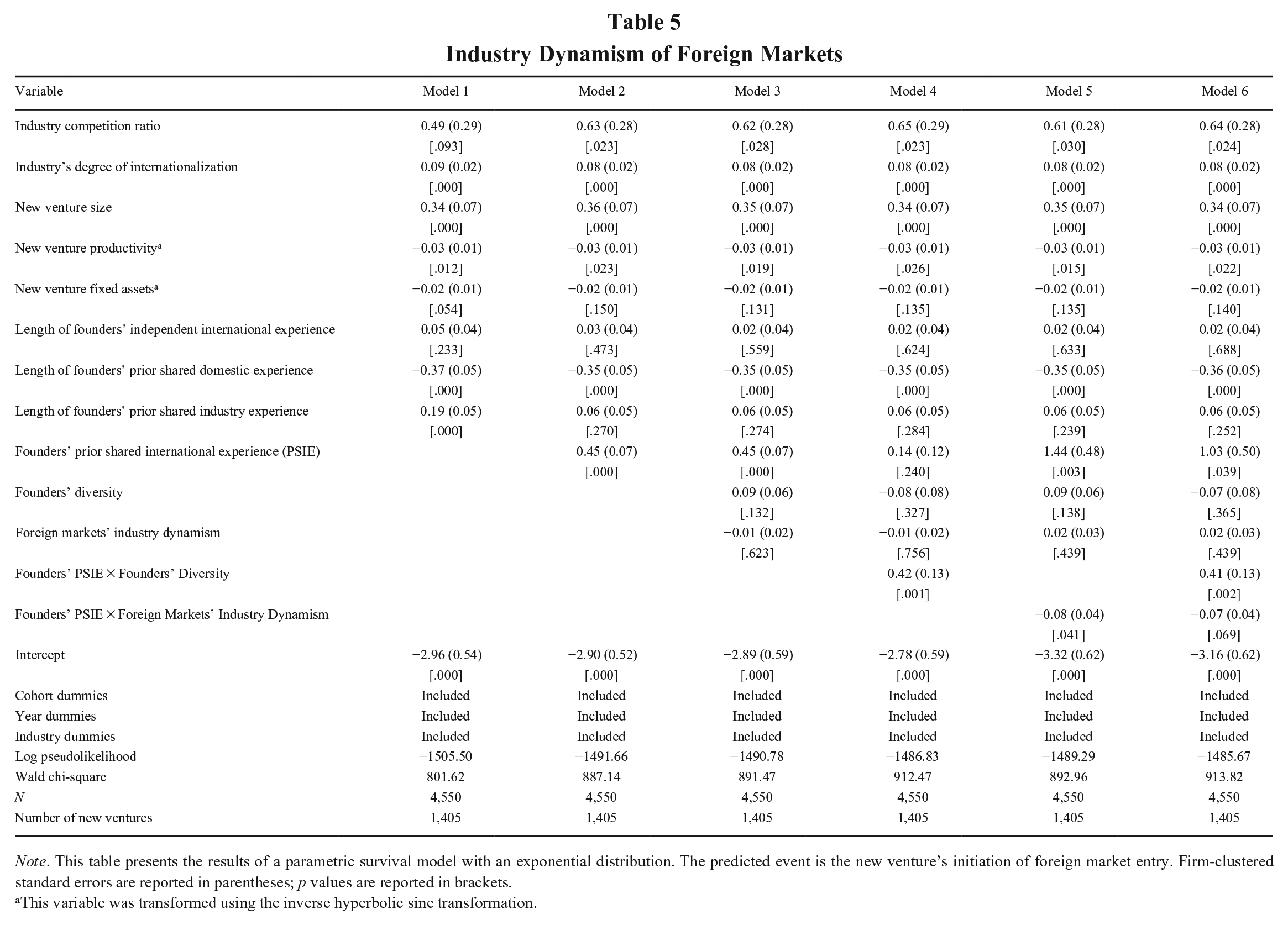

In our study, we argue that industry dynamism is likely to affect the relationship between founders’ prior shared international experience and the time it takes new ventures to enter foreign markets for the first time. In our main analysis, we calculate industry dynamism in Sweden. As a robustness test, we seek to show that the industry dynamism of foreign markets has a similar effect, for the same reasons explained in the theory section. Given that most of Sweden’s exports are destined to European Union countries (Nordisk Ministerråd, 2016), we use Orbis data to come up with a very large sample of firms in the European Union. We exclude Swedish firms since Sweden represents the home country for all new ventures in our sample. We replicate our original measure of dynamism described earlier in this sample of E.U. firms. The results using this alternative measure of industry dynamism are largely consistent with our main results, as shown in Table 5.

Industry Dynamism of Foreign Markets

Note. This table presents the results of a parametric survival model with an exponential distribution. The predicted event is the new venture’s initiation of foreign market entry. Firm-clustered standard errors are reported in parentheses; p values are reported in brackets.

This variable was transformed using the inverse hyperbolic sine transformation.

Founders’ position in prior international employers

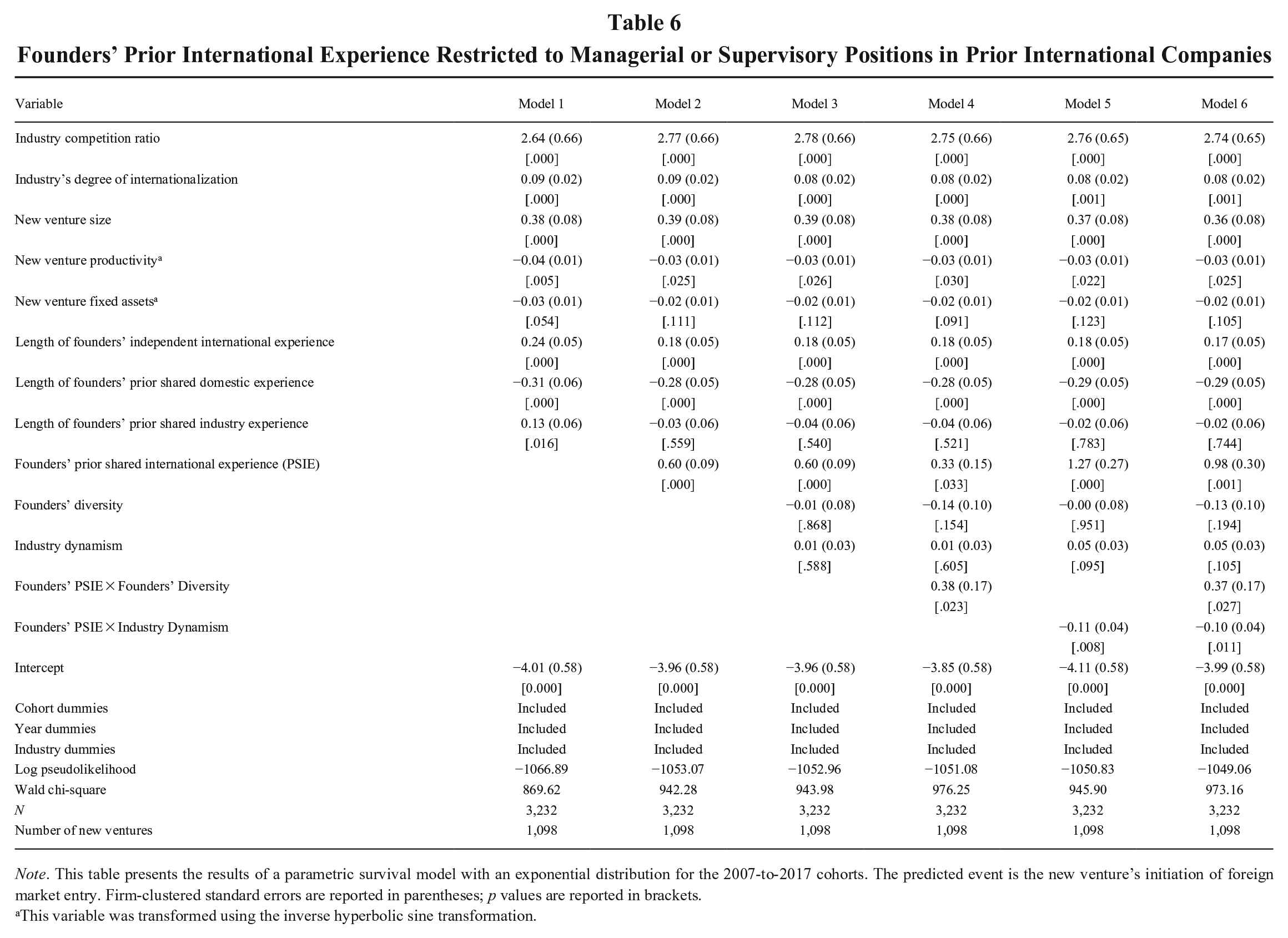

Our current operationalization of founders’ prior international experience (both shared and independent) allows for the possibility that some founders were not directly involved with international activities when working for their prior international employers. While this is indeed plausible, such founders could still become aware of and share knowledge about internationalization. Internationalization-related information is typically publicized by companies, and the results of international operations are published and diffused within companies both formally and informally. Companies also train their employees to handle activities related to international operations, a process that further makes them aware of international business activities. This learning could be useful as these employees move on to create their own companies. Despite the aforementioned considerations, in this robustness test we try to capture founders’ exposure to international activities in their prior employers. We do so by recomputing both the founders’ prior independent and shared international experience variables by focusing on employees who held managerial or supervisory positions in their prior international employers. 13 In line with prior research, we argue that employees occupying managerial or supervisory positions in firms with export sales activities are more likely to be exposed to internationalization themselves (Ganotakis & Love, 2012). Information on employee position in our data is captured through the “Standard för svensk yrkesklassificering” variable, which is based on the International Standard Classification of Occupation. This variable is available in our data from 2001 onward. As such, we cannot use the 2001 cohort as this variable is built retrospectively (i.e., occupation in prior employments). Because the average length of prior shared international experience among founders who possess it is approximately 4.8 years in our sample (M = 4.76, SD = 4.09), we focus on the 2007-to-2017 cohorts as to make sure that all cohorts enjoy a similar time window for the coverage of this variable. Older cohorts (e.g., 2002-2006) may score lower on this variable not because their founders did not hold managerial or supervisory positions in their prior international employers but simply because they had a shorter time window available for this variable to be computed retrospectively. We use Tåg, Åstebro, and Thompson’s (2016) procedure based on occupation codes to identify CEOs, senior staff, and professionals with a supervisory role. The results are reported in Table 6 and are largely in line with our main results.

Founders’ Prior International Experience Restricted to Managerial or Supervisory Positions in Prior International Companies

Note. This table presents the results of a parametric survival model with an exponential distribution for the 2007-to-2017 cohorts. The predicted event is the new venture’s initiation of foreign market entry. Firm-clustered standard errors are reported in parentheses; p values are reported in brackets.

This variable was transformed using the inverse hyperbolic sine transformation.

Discussion

New ventures are oftentimes started by groups of cofounders who have come up with a business idea jointly and decided to exploit it together (Lazar et al., 2020; Shepherd et al., 2021). These firms have clear advantages over solo-founder new ventures because they have a larger pool of resources, skills, and expertise available to draw upon (Clarysse & Moray, 2004). However, they also experience some disadvantages related to the time it takes them to orchestrate their various resources, skills, and expertise into one agreed course of action. An emerging body of literature suggests that founders’ prior shared experience can expedite new ventures’ strategic actions and increase their performance (Shepherd et al., 2021). The logic leading to these predictions is that such experience equips new ventures with well-established shared knowledge and routines that allow them to exploit opportunities and build strong market positions more quickly.

Focusing on the initiation of internationalization in new ventures, we show that founders’ prior shared international experience shortens the time it takes their new ventures to enter foreign markets for the first time (supporting Hypothesis 1). Furthermore, we examine two important boundary conditions of the negative relationship between founders’ prior shared international experience and time to first foreign market entry. The first is founders’ diversity, where we find that the early-foreign-market-entry premium associated with founders’ prior shared international experience becomes larger when founders are highly diverse (supporting Hypothesis 2). These results are consistent with the argument that diversity among founders gives the new venture a broader pool of knowledge, skills, and perspectives, which facilitates the adaptation of their prior shared knowledge and routines to the context of the new venture. The second boundary condition is industry dynamism; here, we find that the early-foreign-market-entry premium associated with founders’ prior shared international experience dissipates when industries are highly dynamic (supporting Hypothesis 3). These results are consistent with the argument that prefounding shared knowledge and routines can become obsolete under certain environmental conditions, and new ventures need to invest time and resources to update shared knowledge and routines to match changing environmental conditions. Finally, we show that early internationalizers perform better in terms of both general and international performance (supporting Hypothesis 4). These findings are in line with the notion that opportunities are fleeting and that new ventures that can act early to anticipate competition and exploit opportunities within their “time window” achieve higher performance (Bakker & Shepherd, 2017).

Implications for the Literature on Founders’ Prior Shared Experience

Entrepreneurship research has recently recognized founders’ prior shared experience as a salient dimension in new ventures that has clear implications for these ventures’ creation and performance (Shepherd et al., 2021). However, while the literature suggests that prior shared experience enables new ventures to take strategic actions more quickly than competitors (Beckman, 2006), this relationship has not been closely and systematically examined empirically. Our point of departure in this study is to empirically examine this relationship in the context of time to first foreign market entry. As such, our study contributes to this stream of literature by providing direct evidence of this relationship using a large-scale empirical study. We also show the relevance of early internationalization by demonstrating that early internationalizers perform better than late internationalizers (see Hypothesis 4 and Table 3). Exploiting opportunities in a timely manner is crucial to new ventures’ success (Baum & Wally, 2003), especially when they seek to enter foreign markets for the first time, as our results show.

Further, we have proposed two boundary conditions of the relationship between founders’ prior shared international experience and the time to first foreign market entry that can undermine the role of shared experience in new ventures: founders’ diversity and industry dynamism. Prior studies have typically suggested that founders’ prior shared experience expedites action in new ventures (Beckman, 2006; Schoonhoven et al., 1990). Research has “implicitly assumed that PSE [prior shared experience] is always beneficial, the more the better” (Zheng et al., 2016: 2504). Our findings show that this is not always the case. The benefits of founders’ prior shared international experience vis-à-vis time to first foreign market entry in new ventures can vanish if founders are highly homogeneous or if ventures operate in highly dynamic industries. We argue that this happens because founders’ diversity and industry dynamism influence the adaptation and relevance of shared knowledge and routines in new ventures, respectively.

Our panel study, moreover, has several strengths relative to prior research on founders’ prior shared experience. First, it allows us to accurately match the domain of founders’ prior shared experience with the strategic outcome under assessment. Prior studies on shared experience have focused either on the relationship between founders’ prior shared industry-specific experience and general, more distant outcomes, such as performance (see, e.g., Honoré, 2020; Zheng et al., 2016), or on the relationship between founders’ prior shared general experience and specific outcomes, such as product market entry or innovation (Heirman & Clarysse, 2007; Schoonhoven et al., 1990). Interestingly, the latter studies have typically found a nonsignificant or even negative relationship between their measures of prior shared experience and the outcomes of interest. In contrast, we start by focusing on a more proximate strategic outcome, and tailor the conceptualization and operationalization of founders’ prior shared experience to match the domain of experience related to such outcome, while still controlling for other types of founders’ (shared) experience.

Second, we are able to control for independent experience through the variable length of founders’ independent international experience as well as for shared domestic experience through the variable length of founders’ prior shared domestic experience and for shared industry experience through the variable length of founders’ prior shared industry experience, none of which were done in prior studies. Zheng et al. (2016: 2516), for instance, suggested that “future research should account for distinctions between independent and shared experience in evaluating the impact of experience.” Thus, accounting for founders’ independent experience, as well as for prior shared domestic and industry experience, allows us to control for and compare different types of founders’ experience to determine their relative importance vis-à-vis foreign market entry timing decisions.

Implications for the Literature on New Ventures’ Early Internationalization

Our results also enrich our understanding of early internationalization in new ventures (Jiang et al., 2020; Zhou & Wu, 2014). The literature suggests that the prior experience gained by founders while working in international firms is important for the early internationalization of their new firms (Zucchella et al., 2007) because it typically leads to greater market knowledge, network building, and improved opportunity identification and exploitation (McDougall et al., 2003) and to the creation of routines largely based on what their founders bring with them from their previous work in international organizations (Sapienza et al., 2006). Such knowledge and routines typically attenuate new ventures’ liability of foreignness—that is, the disadvantages incurred by firms venturing into foreign markets (Cavusgil & Knight, 2015). However, although prior researchers argue that new ventures’ early internationalization activities benefit from the prefounding knowledge and routines drawn from their founders’ prior experiences, most studies have examined (the sum of) prior independent experiences with internationalization (see Oviatt & McDougall, 1997). 14 Of course, new ventures can leverage their founders’ prior independent experiences with internationalization to (re-)create the knowledge and routines needed to kick-start their internationalization efforts. However, the initial advantages derived from such experiences may be hampered by the challenges that ventures may incur trying to negotiate, integrate, and coordinate the different knowledge strands and routines developed by their different founders in different prior international organizations. Knowledge and routines developed in different organizations are usually more difficult to share with others because of their idiosyncratic cognitive and experiential components (Ganco, 2013; Zahra, Neubaum, & Hayton, 2020). In addition, the content and utility of these knowledge strands and routines may not be easily shared or understood by others (Szulanski, 1996). In our study, we highlight founders’ prior shared international experience as a theoretically relevant dimension that eases the transfer of knowledge and routines across organizations, resulting in earlier first foreign market entry for new ventures. This is also true when this experience is compared with founders’ independent international experience, as shown by our results. Moreover, our study provides evidence that early internationalization has distinct benefits in terms of new venture performance. Previous research has posited that early internationalizers enjoy superior performance because of learning advantages (Autio et al., 2000; Sapienza et al., 2006); however, empirical findings are still mixed (Schwens et al., 2018; Williams & Crook, 2021). Our results contribute to this literature by showing that early internationalizers perform better than late internationalizers.

Finally, our panel study offers several methodological improvements over prior research on IE in general and on new ventures’ early internationalization in particular. Specifically, we address concerns regarding censoring and selection bias in prior work (see Jiang et al., 2020). We do so by following all new ventures from inception until the time when they undertake their first foreign market entry. We also include and control for right-censored observations—that is, ventures that did not undertake their first foreign market entry during our observation period. In our data, we use multiple cohorts (2001-2017) that we follow for different periods (until 2018). If we included only those ventures that initiate foreign market entry during our observation period, we would implicitly assume that those new ventures that do not initiate their foreign market entry during the observation period will never do so at all. This is an incorrect assumption for many of the ventures in our sample, as they may initiate foreign market entry at some point in the future. Our research design and analyses allow us to better understand the determinants of entry timing by including information on whether an observation was censored.

Practical Implications

Our study offers several takeaways for different stakeholders. For potential founders, our results indicate that starting a new venture with former coworkers at international firms has advantages, as it helps their new venture to enter foreign markets for the first time earlier. We argue that this is because prior shared international experience among cofounders may facilitate the transfer of shared knowledge and routines from former employers to the new venture. Nevertheless, founders also need to consider carefully which colleagues they should start a venture with. When developing connections with coworkers and other potential cofounders to start a new venture, potential founders might be influenced by homophily tendencies and mainly consider, as potential cofounders, colleagues who are similar to them in terms of gender, age, education, and ethnic background. As our study shows, new ventures started by homogeneous groups of cofounders with prior shared international experience take longer to enter foreign markets for the first time. In contrast, creating a new venture with former colleagues who are diverse in terms of gender, age, education, and ethnic background might facilitate the adaptation to the new venture of the shared knowledge and routines developed in prior firms. Our findings also alert potential founders to the risk that the shared knowledge and routines that they bring with them from previous international firms may quickly become obsolete. This is the case especially when the new venture operates in highly dynamic industries. Hence, by continuously questioning the limits of their prior shared experience and updating their shared knowledge and routines, founders of new ventures may overcome these problems and achieve early internationalization.

For potential investors, such as business angels, who are interested in investing in new ventures with the potential to enter early into foreign markets and achieve strong performance, our results indicate that they need to carefully consider not only whether the founders have gained prior international experience independently but also whether they have shared such experience with other cofounders.

Limitations and Future Research

Interpretations of our study’s encouraging results should be tempered by the fact that it has some limitations. For instance, while the fine-grained nature of our data allows us to match individuals in Sweden and across establishments of the same organization, there is still some chance that a group of cofounders that we identify as working concurrently for the same establishment of the same firm in the past did not interact in that organization. Nevertheless, it is reassuring that our results hold when we operationalize our independent variable considering only founders with managerial and supervisory positions in prior international employers, which increases the likelihood that these individuals interacted with each other while being in either chief–chief roles or chief–subordinate roles with each other (see Table 6). Additionally, Beckman (2006) argues that teams with common prior company affiliations, despite not working directly together, have commonalities based on a shared understanding of how organizational work should be managed and coordinated; possess a shared language, culture, and narratives; and share common routines and understandings, all of which can help their newly formed team quickly agree on what needs to be done and how to do it. Moreover, when two founders come from the same prior company, they are more likely to talk to each other about the firm-specific knowledge that they share (Beckman, 2006: 743).

Thus, even if two cofounders who worked for the same employer at the same time in the past did not work as a team, they still possess similar routines, understandings of organizational work, and firm-specific knowledge that they can leverage in the newly created firm. Nevertheless, a potentially fruitful avenue for future researchers is to use a survey-based approach to directly measure the extent to which individuals employed concurrently by the same prior organization worked together and to corroborate our findings further.

Further, while the comprehensiveness of our data allows us to focus on the whole population of employees in Sweden, making this one of the few large-scale empirical studies on founders’ shared experience, we have restricted our market entry conceptualization and measure to first foreign market entry. While this choice is in line with the macro drivers of early internationalization of firms in our sample (e.g., small home-country market, niche industries), future studies should consider the role of founders’ prior shared experience for other important market-entry choices in new ventures, such as new market spaces or new industries. For instance, future studies should investigate whether founders’ prior shared industry experience accelerates new ventures’ entry into the industries where this prior experience was acquired. Moreover, research underscores the importance of foreign strategic partnerships or business networks for the early internationalization and international performance of new ventures (Fernhaber & Li, 2013; Ibeh, Jones, & Kuivalainen, 2018; Mansion & Bausch, 2020; Zhou, Wu, & Luo, 2007). Therefore, future studies should focus on founders’ prior shared experience in such networks and whether it plays a similar or different role from the type of shared experience hypothesized in our study. In addition, future studies should focus on the potential trade-offs between the breadth and depth of prior shared international experience (Gruenhagen, Sawang, Gordon, & Davidsson, 2018). Likewise, the characteristics of the task environment in host markets may affect the international performance of new ventures in these markets (Deng & Sinkovics, 2018; Marano, Arregle, Hitt, Spadafora, & Van Essen, 2016). Therefore, delving deeper into how host-market characteristics moderate the early internationalization–performance relationship would be a worthwhile issue for future study.

In our study, we theorize about how the prior shared international experience of a new venture’s founders is negatively related to the time it takes for the new venture to enter foreign markets for the first time. However, this experience may affect other timing aspects of a new venture’s internationalization, such as the speed of internationalization, which prior research has argued is relevant for new venture performance (Chetty, Johanson, & Martín, 2014). Hence, future research could fruitfully extend our work in this direction and investigate, for example, the effects of prior shared international experience on the speed of a venture’s export expansion, focusing on areas such as how quickly a new venture expands into new foreign markets (Casillas & Acedo, 2013) or into markets with different institutional settings (Deng & Sinkovics, 2018). Alternatively, scholars could use survey-based measures of the speed of internationalization, which comprises, for instance, the speed of international learning and the speed of international commitment (see Chetty et al., 2014).