Abstract

Are stakeholder management and innovation substitutes or complements in affecting firm performance? Extant research provides support for both positions and thus leaves us with a puzzle. We conduct an exploratory fuzzy set qualitative comparative analysis (fsQCA) of 204 publicly listed European firms combining survey and archival data to formulate theory on how stakeholder management and innovation work (in)effectively together. Distinguishing between internal and external stakeholders and exploitative and exploratory innovation, we elaborate that managing for stakeholders and innovation can be both substitutes and complements depending on a set of contingencies. We discuss boundary conditions and implications for future research.

Keywords

Introduction

Innovation—a central aspect in various conceptualizations of entrepreneurship (e.g., Ireland et al., 2003; Lumpkin & Dess, 1996; Zahra, 1996)—is gaining increased relevance in the stakeholder literature. Consequently, there has been a substantial amount of research interest in the impact of innovation and managing for stakeholders (MfS) 1 on firm performance (Bendell et al., 2020; Flammer & Kacperczyk, 2016; Gambeta et al., 2019; Garcia-Castro & Francoeur, 2016; Ghassim & Bogers, 2019; Harrison et al., 2010; Hull & Rothenberg, 2008; Jiang et al., 2020; Kazadi et al., 2016; Li et al., 2018; McWilliams & Siegel, 2000; Minoja et al., 2010; Partanen et al., 2014; Zhao et al., 2021; Zollo et al., 2018). This work has generated important insights into the effects of MfS and innovation as well as their interplay on firm performance.

However, this growing literature on the interplay between MfS, innovation, and firm performance is characterized by a puzzle: On the one hand, some studies indicate that MfS can complement firm innovation to jointly improve firm financial performance (Flammer & Kacperczyk, 2016; Ghassim & Bogers, 2019; Harrison et al., 2010; Jiang et al., 2020). On the other hand, several studies observe a substitution effect between MfS and innovation vis-à-vis firms’ financial performance (Garcia-Castro & Francoeur, 2016; Hull & Rothenberg, 2008; McWilliams & Siegel, 2000). Overall, the performance implications of the interplay between MfS and innovation are not well understood. Since both MfS and innovation may be essential strategies for high performing firms—but imply significant resource investments (He & Wong, 2004; Jansen et al., 2006; Orlitzky et al., 2003; Waddock & Graves, 1997)—it is important to better understand how they interact to influence firms’ performance outcomes. Past research has argued that firm strategies should be considered simultaneously, that is, configurationally, to allow for a better understanding of whether they work as substitutes or complements (Flammer & Kacperczyk, 2016; Hull & Rothenberg, 2008; Minoja et al., 2010; Partanen et al., 2014; Schweiger et al., 2019). Thus, we propose to study how MfS and innovation combine configurationally to impact firm performance.

The purpose of this paper is to begin solving this puzzle by taking a holistic approach to the study of the joint effects of MfS and innovation on firm financial performance, which allows us to consider these strategies simultaneously and configurationally. We first examine and integrate existing theory and research on the joint relationship of MfS and innovation on firm performance. We discuss past research that has studied how these strategies combine. Due to its specific ability to consider causally complex phenomena and enable configurational theorizing (Douglas et al., 2020; Furnari et al., 2020), we use fuzzy set qualitative comparative analysis (fsQCA; Fiss, 2011; Ragin, 2008b) to explore configurations of managing for internal and external stakeholders and exploitative and exploratory innovation among publicly listed European manufacturing and service firms that achieve high or low performance. Based on our analysis, we elaborate theory on how MfS and innovation work together (in)effectively as part of a configuration of firm strategies. We shed light on important boundary conditions and conclude by discussing our study’s implications for future research.

Theoretical Background

Managing for Stakeholders and Innovation: Substitutes or Complements?

Past research that has examined the effects of MfS and innovation on firm performance has taken very different perspectives on how these two strategies interact. Specifically, one stream has argued that MfS and innovation should be complements and improve firm performance, while another stream has leaned toward interpreting MfS and innovation as two substitutable strategies that can each lead to high performance individually.

The latter perspective predates the former: It was developed in response to early empirical research on the direct performance implications of MfS (e.g., Aupperle et al., 1985; McGuire et al., 1988; Waddock & Graves, 1997). Researchers soon suggested the positive firm performance effects of MfS found in early studies would diminish when a measure of innovation such as R&D intensity is included in the model (McWilliams & Siegel, 2000). These studies argue that differentiation is a typical way for firms to achieve competitive advantage, and that both MfS and innovation are possible ways to achieve such differentiation (Hull & Rothenberg, 2008; McWilliams & Siegel, 2000). This may therefore explain why MfS and innovation are substitutes. Studies in this research stream generally suggest that innovation appears to be the more powerful strategy for firms to differentiate themselves on the market: “Companies with superior, highly innovative products need offer little other reason for customers to choose them” (Garcia-Castro & Francoeur, 2016, p. 411). Overall, therefore, this literature stream suggests that MfS and innovation substitute each other in their effect on firm performance. However, these studies also acknowledge that certain boundary conditions may influence the extent to which there is a trade-off between MfS and innovation, and call for more research in this vein (e.g., Garcia-Castro & Francoeur, 2016).

In contrast to the literature above, the literature emphasizing complementarity between MfS and innovation argues that MfS entails certain advantages for firms that allow them to reap increased benefits from their innovation activities. This line of work generally highlights that MfS enables firms to build trusting relationships with their stakeholders. These relationships are based on distributional, procedural, and interactional justice and rely on reciprocity and commitment (Harrison et al., 2010). In establishing such relationships, firms are then able to derive benefits including reputation and legitimacy (Flammer & Kacperczyk, 2016). Most importantly, trusting relationships enable firms to gain access to various types of knowledge about stakeholder preferences, stakeholder requirements for maintaining an ongoing relationship, and knowledge that allows for mutual learning between the firm and its stakeholders; they also facilitate new approaches to problem-solving and the exploration of new business opportunities (Ghassim & Bogers, 2019; Harrison et al., 2010; Jiang et al., 2020; Kazadi et al., 2016; Zollo et al., 2018). This knowledge can be used in firms’ innovation activities (Flammer & Kacperczyk, 2016; Jiang et al., 2020; Li et al., 2018; Zhao et al., 2021). Consequently, this literature stream argues that MfS and innovation are complements.

The work advocating complementarity between MfS and innovation also acknowledges that firms must invest time and resources into establishing good relationships with their stakeholders (Garcia-Castro & Francoeur, 2016; Harrison & Bosse, 2013; Harrison et al., 2010). Harrison et al. (2010) explain: “We do not argue that incremental investments in stakeholder relationships, as a resource, will always result in superior firm performance. Firms can surely overinvest in particular stakeholder relationships or invest unwisely.” This literature, therefore, recognizes that MfS may have “dark sides” and that boundary conditions may play an important role in determining the extent to which MfS can positively impact firm financial performance. So far these “dark sides” and boundary conditions remain relatively underexplored with only a limited number of studies having examined potential areas of interest. First, in their conceptual piece on the link between stakeholder cohesion (i.e., alignment between the firm’s key decision makers and stakeholders), innovation, and competitive advantage, Minoja et al. (2010) argue that strong stakeholder cohesion may lead to inertia and resistance to change within the firm because cohesion tends to produce and reinforce homogeneity and strategic myopia. This ultimately reduces the firm’s propensity to innovate, thereby negatively affecting the firm’s competitive advantage. Second, Gambeta et al. (2019) examine the link between managing for a particular stakeholder group—employees—and the firm’s propensity to pursue local search (i.e., exploitative innovation) and distant search (i.e., exploratory innovation). The authors argue that managing for employees creates lower turnover among employees, increased mutual learning between employees, and incentive mechanisms that all encourage local search. Their study, therefore, suggests that managing for employees is only complementary with exploitative innovation, but not with exploratory innovation. Finally, a case study suggests that MfS and innovation may be complements if firms adapt their relationships with external stakeholders to the type of innovation they want to commercialize (Partanen et al., 2014). Overall, these studies indicate that the link between MfS and innovation can be positive, but that the relationship is quite complex.

To summarize the theoretical accounts of the relationship between MfS and innovation on firm performance, past research has proposed differing explanations of this relationship based on either differentiation or access to knowledge, reputation, and legitimacy. Both the substitutability and the complementarity literatures have also pointed to potential boundary conditions. In light of this, a more comprehensive examination is needed to gain a better understanding of when and why differentiation and/or the access to knowledge, reputation, and legitimacy are able to explain the relationship between MfS and innovation. Specifically, a more nuanced perspective may be needed to describe the complex nature of their relationship on firm performance and to reconcile the continued incongruencies between the substitutability and complementarity perspectives. Such an approach can build on initial research in both literature streams that has started to examine more specific aspects of either MfS or innovation. It can also respond to calls for a more encompassing perspective of MfS and innovation that is able to consider the fit between these strategies (Hull & Rothenberg, 2008; Li et al., 2018; Minoja et al., 2010; Partanen et al., 2014).

Dimensions of Managing for Stakeholders and Innovation

To a large extent, the aforementioned literature treats both MfS and innovation as unified constructs (Bendell et al., 2020; Ghassim & Bogers, 2019; Harrison et al., 2010; Hull & Rothenberg, 2008; Jiang et al., 2020; McWilliams & Siegel, 2000; Minoja et al., 2010; Zollo et al., 2018). However, a select number of past studies have attempted to shed additional light on the relationship between the two strategies by examining specific dimensions of MfS or innovation.

A stakeholder is “any group or individual who can affect or is affected by the achievement of a firm’s objectives” (Freeman, 1984, p. 24). This means that there is a wide variety of potential stakeholders that a firm can or should consider or include in firm activities ranging from employees to suppliers, customers, local communities, the media, and others. Past research has pointed out that certain stakeholders among the larger set of potential stakeholders can be considered more central to the firm’s operations. These primary stakeholders are those “without whose continuing participation the corporation cannot survive as a going concern” (Clarkson, 1995, p. 106). The existing studies on the nexus between MfS and innovation have generally focused on such primary stakeholders, which are highly salient to the firm’s operations. These studies have also distinguished between internal and external stakeholders with some focusing on employees (Garcia-Castro & Francoeur, 2016; Zhao et al., 2021) and others emphasizing the role of customers and suppliers (Li et al., 2018; Partanen et al., 2014).

The distinction between internal and external stakeholders is well-established in the literature (Korschun, 2015; Pirson & Malhotra, 2011; Schneper & Guillén, 2004). Prior work maintains that these two groups differ fundamentally based on their structural characteristics and their relation to organizational boundaries (Brickson, 2005, 2007). Due to these differences, past studies have proposed different ways in which managing for each of these stakeholder types affects the firm’s ability to innovate. In the case of the main internal stakeholder group, employees, various studies argued that building and maintaining good relationships with employees encourages employees to contribute to firm innovation broadly speaking (Bendell et al., 2020; Harrison et al., 2010; Ruppel & Harrington, 2000). There is some disagreement in past research as to whether managing for internal stakeholders (MIS) can contribute positively to both exploitative and exploratory innovation: Some studies posit this should be the case (e.g., Flammer & Kacperczyk, 2016; Zhao et al., 2021), while one study argues that managing for employees is likely to help firms’ exploitative rather than exploratory endeavors (Gambeta et al., 2019). In the case of external stakeholders like customers and suppliers, the literature generally agrees that managing for these stakeholders induces them to provide resources and support as well as reveal new ideas, valuable know-how, technical knowledge, and market information (Flammer & Kacperczyk, 2016; Partanen et al., 2014). Only three studies have discussed the effect of managing for external stakeholders (MES) on exploitative and exploratory innovation separately: Two inductive studies both argued that MES stakeholders could be beneficial for both types of innovation (Kazadi et al., 2016; Partanen et al., 2014). In the only deductive analysis of the relationships so far, Zhao et al. (2021) made similar arguments but found no empirical support for either relationship.

Both the substitutability and complementarity literatures on the relationship between MfS and innovation have so far mostly spoken about innovation in general, that is, without discussing its dimensionality (Bendell et al., 2020; Garcia-Castro & Francoeur, 2016; Ghassim & Bogers, 2019; Harrison et al., 2010; Hull & Rothenberg, 2008; Jiang et al., 2020; Li et al., 2018; McWilliams & Siegel, 2000; Minoja et al., 2010; Zollo et al., 2018). A few studies distinguish between exploitative and exploratory innovation (Gambeta et al., 2019; Kazadi et al., 2016; Partanen et al., 2014; Zhao et al., 2021). These studies suggest that MfS is helpful both for obtaining knowledge and commercializing it (Ghassim & Bogers, 2019; West & Bogers, 2014; Zhao et al., 2021). They also point out that MfS can lead to higher quality innovation (Flammer & Kacperczyk, 2016), that managing for employees is important for firms pursuing exploitative innovation (Gambeta et al., 2019), and that firms may need to manage for specific stakeholders depending on the type of innovation they are pursuing (Partanen et al., 2014).

Since the goal of the current study is to provide a more nuanced and comprehensive examination of the joint effect of MfS and innovation on firm performance, we intend to combine the dimensions outlined above: We will assess MfS by considering both managing for internal stakeholders (MIS) and managing for external stakeholders (MES). Innovation will be assessed using both exploitative and exploratory innovation strategies. Including separate measures for exploitative and exploratory innovation, our study acknowledges that firms may be heavily engaged in neither, one, or both of these innovation strategies.

Our study also considers a set of contingencies that are likely to influence how MfS and innovation affect firm performance. First, past research in this area has argued that environmental dynamism may exert a significant influence (Minoja et al., 2010). Higher dynamism requires greater commitment to innovation, so firms that continually adapt to their environments are more likely to maintain a competitive advantage (e.g., Brown & Eisenhardt, 1997; Eisenhardt, 1989). Second, firm size is often seen as an important contingency factor. Small firms generally have fewer resources and limited capabilities, which is why their approaches to both MfS and innovation strategies may differ from larger firms (Flammer & Kacperczyk, 2016; McWilliams & Siegel, 2000; Waddock & Graves, 1997). Finally, industry type can impact both MfS (Coombs & Gilley, 2005; Hillman & Keim, 2001) and innovation strategy (Castellacci, 2008; Ettlie & Rosenthal, 2011). Thus, industry is another important contingency that could influence the relationship of MfS and innovation on firm performance.

Method

Analytical Approach

Our goal is to identify high- and low-performing configurations of how firms manage for stakeholders and pursue innovation in different contexts. In so doing, we aim to uncover potential substitutes and complements that may influence firm performance. This requires a methodological approach that captures complex causal relationships inherent in configurations of multiple interconnected elements.

As a response to the need for more sophisticated techniques in configurational inquiries, a new approach was developed: qualitative comparative analysis (QCA; Ragin, 1987). One of its extensions, the fuzzy set qualitative comparative analysis or fsQCA (Fiss, 2011; Ragin, 2008b), has established itself as a viable method for studying complex phenomena in strategic management and entrepreneurship (Leppänen et al., 2019; Misangyi et al., 2017). It uses set theory to model relationships between outcomes and combinations of theoretically relevant conditions as “causal recipes” (Ragin, 2008b). This causal conjunction—the assumption that outcomes occur as a result of multiple simultaneously interacting conditions—is one of fsQCA’s advantages over more conventional correlation-based methods (Misangyi et al., 2017). For example, analyzing configurations by means of regression models would imply modeling higher-order interactions, which impose computational limitations on regression-based techniques and are difficult to interpret. Another commonly used method in configurations research, namely cluster analysis, identifies configurations, but it does not link them to an outcome. Moreover, it treats each configurational element as an equal contributor. By contrast, fsQCA identifies all theoretically possible configurations and shows to what extent they are necessary and sufficient for the outcome of interest, provided they are also empirically observed (Greckhamer et al., 2018). After minimizing the discovered configurations using Boolean algebra, it can also identify the most important elements in each relevant solution (Fiss, 2011).

In addition to causal conjunction, fsQCA is advantageous as it accounts for equifinality and asymmetric causality (Damian & Manea, 2019; Misangyi et al., 2017; Ott et al., 2019). Equifinality—the assumption that there are many ways to produce the same outcome—allows the researcher to assess the number and complexity of different paths leading to a sought outcome (Doty et al., 1993; Gresov & Drazin, 1997). While regression techniques focus on isolated effects of single variables, fsQCA provides information on first-order equifinality, where configurations differ in their core conditions, and second-order equifinality, where configurations have the same core conditions but different peripheral conditions (Fiss, 2011). Lastly, asymmetric causality assumes that configurations leading to an outcome of interest (e.g., high performance) do not mirror those that lead to the opposite outcome (e.g., low performance). This stands in contrast to regression analysis, where causal relationships are explained symmetrically as “If more of A leads to more of B then less of A must lead to less of B.” (Douglas et al., 2020; Meyer et al., 1993; Ragin, 2008b). Since we seek to uncover several high- and low-performing configurations of multiple elements—and are thus interested in causal conjunction, equifinality, and causal asymmetry—the fsQCA approach suits our purpose well.

Sample and Data

We consider publicly listed European firms operating in the manufacturing (SIC codes 2 and 3) and service (SIC code 6, 7, and 8) industries. European firms tend to possess relatively high latitude in adopting long-term strategies that take their stakeholders into account (Ioannou & Serafeim, 2012). Such latitude implies that firms can differ substantially in the extent to which they implement MfS, which facilitates detecting performance implications of such differences. Focusing on publicly listed firms allows our study to combine archival data obtained from Refinitiv Eikon (Thomson Reuters) with unique survey data collected from individual firms. To identify these firms, we analyzed the stock exchanges in various European countries (Austria, Belgium, Denmark, Finland, Germany, the Netherlands, Norway, Sweden, Switzerland, and the United Kingdom). We perused the firms’ web pages and made confirmatory phone calls to identify senior R&D and business development managers and to verify that the respective firm met our inclusion criteria. This approach enabled us to send our questionnaire to 1119 companies. To facilitate the implementation of our survey in different countries, we produced our questionnaire in three different languages (English, German, and French). Since we exclusively use scales originally developed and published in English, research assistants whose mother tongue is the respective language first translated the scales into German and French and then another research assistant who is a native speaker in English back-translated the scales into English to ensure maximum convergence with the original items.

Validated academic procedures of questionnaire design (Dillman, 2000) informed the production of a fully standardized questionnaire used to collect data on the measures of interest. After contacting the senior R&D and business development managers of the 1119 companies by phone, we emailed them a link to the online questionnaire. The questionnaire provided an account of the aims of the study, guaranteed confidentiality of all responses, and offered aggregated and anonymized results as an incentive to participate. Up to three bi-weekly reminder emails were sent following the initial mailing. The online survey database ultimately contained 204 questionnaires completed between October 2011 and September 2012 with few missing data points, yielding a favorable response rate of roughly 18.2%. We compared respondents and nonrespondents with respect to firm size, firm age, R&D intensity, return on equity (ROE), and the probability of being delisted from the stock exchange in the years since the survey was completed. Two-tailed t-tests indicated no significant differences between respondents and nonrespondents at p < .10 or smaller.

In line with Fiss (2011), we imputed missing values using information from all measures because list-wise deletion would have substantially decreased the total sample size (Little & Rubin, 2002). We use stochastic regression imputation as implemented in the MICE package in R, which is a preferred method for single imputation of Likert-scale type data (Buuren, 2012; Little & Rubin, 2002). We did not impute missing values for the outcome or contingency measures (Fiss, 2011), which is why our subsequent analysis uses 114 observations. The final sample contains 73 manufacturing and 41 service firms with an average of 14,836 employees (s.d. 51,816) and an average age of 40 years (s.d. 37) in 2012; 82 respondents were male, 30 respondents were female, and two preferred not to answer.

Measures and Calibration

Our study combines archival data with survey data that uses existing, validated measures. The only exception is the MIS scale, which combines insights from stakeholder theory (Harrison et al., 2010) and employee orientation research (e.g., Bowers & Seashore, 1966; Plakoyiannaki et al., 2008) and builds on existing employee orientation scales (Brulhart et al., 2019; Wang & Dewhirst, 1992; Zhang, 2010). To create a questionnaire for the survey part, we produced a preliminary item list based on the literature and the identified scales. Subsequently, we discussed this list with four academics and R&D managers from three companies and incorporated their feedback. Most of the survey measures consist of multi-item constructs where each item was measured on a seven-point Likert-scale. We calculated a composite score for each multi-item construct that equals the mean of its corresponding items (Reinholt et al., 2011; Trevor & Nyberg, 2008). We collected survey data from top R&D or business development managers on all measures pertaining to stakeholder management and innovation strategies. Respondents were asked to refer to the entire company when answering the survey questions. While this approach yields shared unit-level constructs (Klein & Kozlowski, 2000) that are naturally an approximation, interviews during the questionnaire development phase indicated that the targeted managers would be able to make valid and reliable assessments with respect to the survey questions.

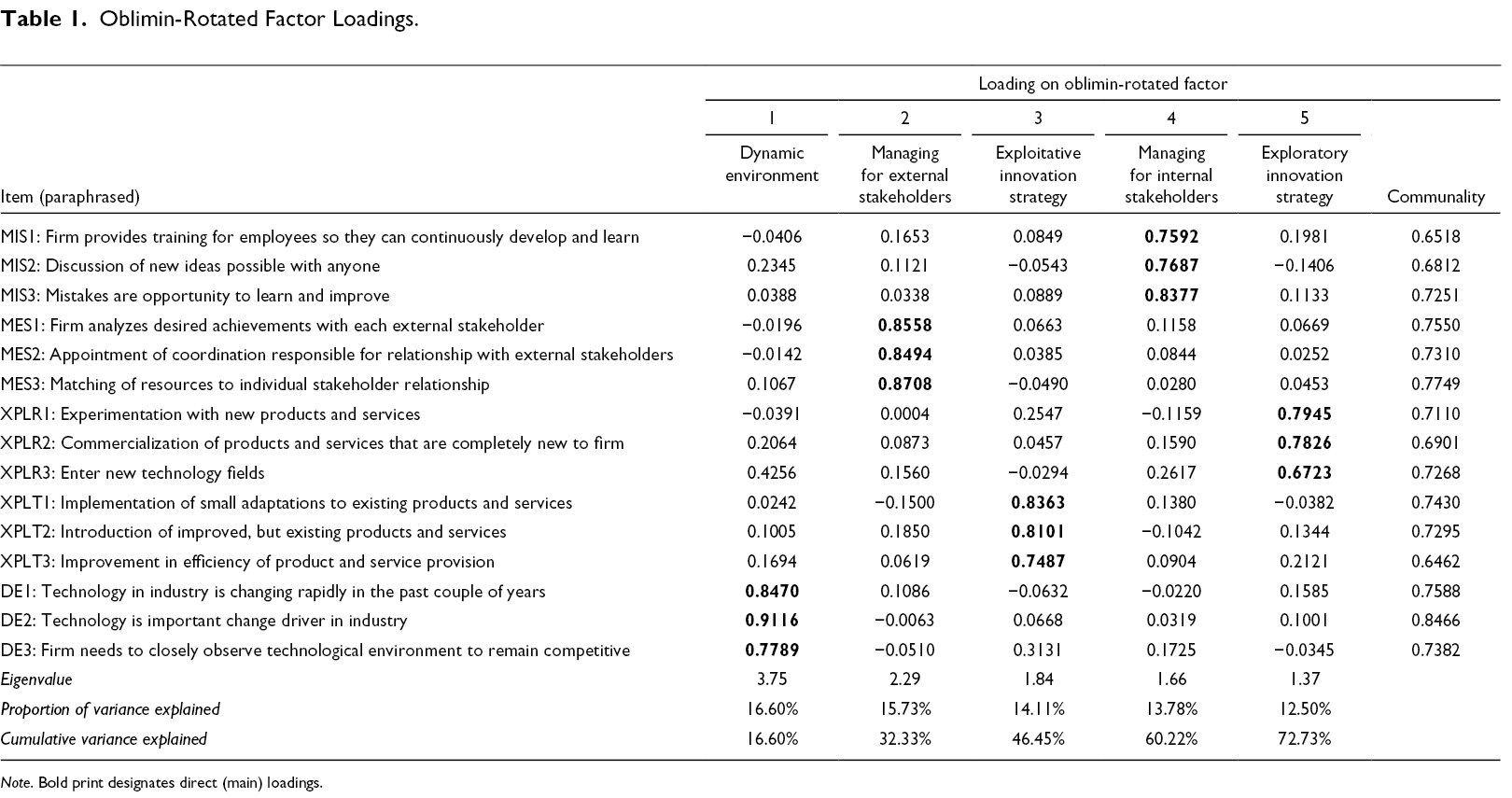

We tested the reliability and validity of our measures by calculating Cronbach’s α; examining the direct factor loadings as well as the cross-loadings found by conducting a principal component factor analysis with oblique rotation 2 (Table 1); and calculating the average variance extracted and comparing its square root to the correlation coefficients among the scales (Hair et al., 1998; Nunnally & Bernstein, 1994; Staples et al., 1999). 3 These methods indicate high levels of reliability and validity.

Oblimin-Rotated Factor Loadings.

Note. Bold print designates direct (main) loadings.

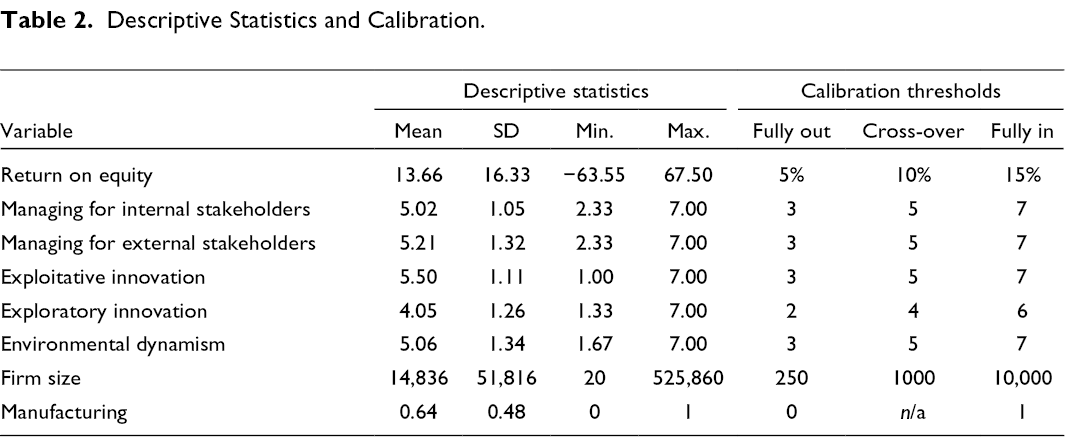

We calibrated all measures to carry out fsQCA. This implies converting identified variables into scales ranging from 0 to 1, whereby fuzzy sets can take on multiple values between these two points to account for varying degrees of set membership. We employed the direct method of calibration (e.g., Fiss, 2011; Greckhamer, 2016), where the researcher specifies the raw variable values that constitute full membership, the crossover point (point of maximum ambiguity), and full nonmembership for each causal condition included in the model (Ragin, 2008b). The software transforms the raw variables into fuzzy membership scores based on these three thresholds and the log odds of full membership (Ragin, 2008a). Consequently, depending on the value of a given variable, each observed case falls into one of four areas between 0 and 1: fully out, rather out than in, rather in than out, or fully in the set (e.g., fully in the set of high-performing firms if its performance exceeds the highest of the three thresholds). Both substantive and theoretical knowledge can be used to calibrate measures (Ragin, 2008a). In the following, we explain the measures we used in our fsQCA model and how we calibrated them.

Outcome Condition: Return on Equity

Like past literature on the performance effects of stakeholder management, our measurement for firm performance is ROE (e.g., Garcia-Castro & Francoeur, 2016). We measured performance lagged 3 years from the end of survey completion because the effects of both MfS and innovation typically realize only over time (e.g., Bertrand & Mol, 2013; Flammer & Kacperczyk, 2016; Hillman & Keim, 2001; McDonald et al., 2008). Therefore, we used ROE from 2015 as reported in Refinitiv Eikon (Thomson Reuters). ROE explains a firm’s efficiency in generating profits and is consequently used as an indication of how profitably a company has operated and how efficiently it has used resources (Hafenbrädl & Waeger, 2017; Klarner & Raisch, 2013). Using ROE as our performance measure is in line with recommendations in the literatures on MfS and innovation: Harrison et al. (2010) argue that MfS can help firms increase their efficiency. Similarly, the innovation literature has emphasized considering firm efficiency (Raisch & Birkinshaw, 2008).

While ROE above zero implies profitability, it does not necessarily mean high performance. Lacking meaningful information on ROE calibration thresholds for high performance, we followed the example of extant work and turned to data and percentiles (Fiss, 2011; Garcia-Castro & Francoeur, 2016; Misangyi & Acharya, 2014). Using the Compustat database, we found that the median ROE of all publicly traded firms in North America was 5.33% in 2015 and 5.73% in 2013–2015. Therefore, we set the threshold for fully out of the set of high-performing firms at 5%. Similarly, we found that ROE at the 75th percentile was 14.42% in 2015 and 14.78% in 2013–2015. Hence, we set the calibration threshold for fully in the set of high-performing firms at 15%. Lastly, we set the middle threshold between these two points at 10% to distinguish between rather in and rather out of the set of high-performing firms.

Since we are also interested in low performing configurations, we use another set of thresholds to calibrate firm performance. In line with past studies (Bell et al., 2014; Campbell et al., 2016; Fiss, 2011; Misangyi & Acharya, 2014), we calibrate low performance as not-high performance—that is, a set of firms that do not achieve high performance as described above—by using the inverse of high performance. Hence, if a firm obtained a membership score of 0.25 in the set of high performing firms, it would receive a membership score of 0.75 in the set of not-high performing firms.

Predictor Conditions

Harrison et al. (2010) point out that MfS involves acknowledging the relevance of stakeholder relationships for value creation, seeking to identify and understand how firm actions affect stakeholders, and demonstrating to stakeholders that the firm understands and respects its own influence on its stakeholders. These three aspects of MfS play an essential role in conceptualizations of “employee orientation” that have been used for decades: Building on McGregor (1960), Plakoyiannaki et al. (2008) argue that an employee orientation is characterized by “supportive relationships, mutual trust and [an] egalitarian management style” (p. 271). Similarly, Bowers and Seashore (1966) argue that organizations with an employee orientation are “less punitive, easy to talk to, and willing to help groom employees for advancement” (p. 243). Our managing for internal stakeholders (MIS; α = .735) scale builds on these established conceptualizations of employee orientation and the above aspects of MfS pointed out by Harrison et al. (2010). The first item is concerned with supporting employees in their advancement, thereby acknowledging their relevance for value creation. The second item concerns employee-management communication, which helps the firm identify and understand how firm actions affect its employees. The third item covers a firm’s trusting and less punitive stance toward its employees and their mistakes with which the firm can demonstrate to its employees that it understands and respects its own influence on them. The items thus asked respondents to what extent their firm (1) provides training for employees so they can continuously develop and learn; (2) allows new ideas to be discussed with anyone, regardless of rank or position; and (3) sees mistakes as an opportunity to learn and improve. These items were adapted from previous employee orientation scales (Brulhart et al., 2019; Wang & Dewhirst, 1992; Zhang, 2010).

The aforementioned aspects of MfS are also covered in the three items that we adapt from Walter et al. (2006) to measure managing for external stakeholders (MES; α = .834). Respondents were asked to consider their firm’s innovation process and to indicate to what extent their firm (1) analyzes what it would like to achieve with each external stakeholder involved (e.g., suppliers, customers, competitors, consultants and technology brokers, research institutes) 4 ; (2) appoints coordinators responsible for relationships with external stakeholders; and (3) matches resources to individual external stakeholder relationships. These items helped Walter et al. (2006, p. 552) appraise the extent to which the firm is able to “cultivate and shape close relationships” with external parties. Close relationships with external stakeholders are also a key characteristic of firms that manage for these stakeholders, further corroborating the appropriateness of using these items to measure MES.

We use innovation strategy variables based on Jansen et al. (2006) and Jansen et al. (2009). They indicate a firm’s reliance on exploitative and exploratory innovation strategies, respectively, where the former entails building on existing knowledge and extending existing products and services for existing customers, and the latter refers to pursuing new knowledge and developing new products and services for emerging customers or markets (Benner & Tushman, 2003, p. 243; Jansen et al., 2006). Exploitative innovation (α = .752) captures the extent to which the firm (1) implements small adaptations to existing products and services; (2) introduces improved, but existing products and services; and (3) improves the efficiency of product and service provision. Exploratory innovation (α = .716) measures the extent to which the firm (1) experiments with new products and services; (2) commercializes products and services that are completely new to the firm; and (3) enters new technology fields.

Our predictor conditions consist of multi-item constructs where each item was measured on a seven-point Likert-scale as explained above. Where appropriate, we adjusted the absolute calibration thresholds according to means (e.g., Cheng et al., 2016) to deal with low variance in scale responses. Therefore, we adopted Fiss’ (2011, p. 405) procedure to calibrate managing for internal and external stakeholders as well as exploitative innovation by coding the third point from the bottom of the Likert-scale as fully out of the set (3), the maximum of the scale as fully in the set (7), and the halfway mark as the crossover point (5). For exploratory innovation we set the thresholds at 2, 4, and 6, because the mean of this variable is close to 4 across several studies using the same scale (Jansen et al., 2006; Prajogo et al., 2013; Wei et al., 2011). Since our data are in line with these studies (mean = 4.05), we believe our choice of thresholds is well-grounded and generalizable beyond our sample.

Contingency Conditions

While the primary focus of our study is on the interplay of firms’ MfS and innovation strategy, prior work points to important contingencies. First, environmental dynamism may influence firms’ performance and how they approach MfS and innovation (Jaworski & Kohli, 1993; Rust et al., 2002; Sidhu et al., 2007). We obtained data on environmental dynamism from the same survey as the data on MfS and innovation. We measure it with three items (α = .837), each one on a seven-point Likert-scale. The items measured the extent to which the firm perceived (1) the technology in its industry to be changing rapidly over the last couple of years; (2) technological change to be an important driver of change in its industry; and (3) the need to closely observe the technological environment to remain competitive. Like the predictor conditions, except exploratory innovation, we use the points 3, 5, and 7 to set the thresholds for fully out, crossover point, and fully in, respectively.

Second, firm size is an important factor in entrepreneurship and strategy research. Large firms typically have better access to resources than small firms, which allows them to invest more time and effort in MfS and innovation (Galbreath, 2006; Lavie et al., 2010; McGuire et al., 1988). At the same time, however, large firms may have more stakeholders to manage and more complex innovation processes than small firms (Miles et al., 1978; Waddock & Graves, 1997). We use the number of employees to measure firm size and set 250 employees as a threshold for fully out of the set of large firms (Fiss, 2011). This is a common definition to distinguish between small and medium-sized enterprises (SMEs) and larger firms (OECD, 2019). We set the middle threshold at 1000 employees and the threshold for fully in the set of large firms at 10,000 to be able to capture meaningful differences between different sizes of firms. Data on employees were collected from Refinitiv Eikon (Thomson Reuters).

Finally, industry type can influence stakeholder management (Agle et al., 1999; Coombs & Gilley, 2005; Hillman & Keim, 2001) as well as innovation (Castellacci, 2008; Ettlie & Rosenthal, 2011). Consequently, we add a condition to our fsQCA model to depict whether the configurations refer to manufacturing or service firms. For industry affiliation, we use crisp sets instead of fuzzy sets and therefore binary calibration: Firms in manufacturing are assigned a value of 1, while service firms receive a value of 0. Industry information was obtained from Refinitiv Eikon (Thomson Reuters). Table 2 provides descriptive statistics and information on the calibration of the outcome and predictor conditions used in this study.

Descriptive Statistics and Calibration.

Analysis

We conducted our analysis using the QCA package of the software R, which uses a Boolean algorithm to determine minimal causal combinations that explain a given outcome (Duşa, 2007, Duşa, 2019). After calibrating all our measures, 5 a test of necessity showed that no condition passed the consistency threshold of 0.90 for necessary conditions (Greckhamer, 2016; Ragin, 2008b; Schneider & Wagemann, 2012). We then used the enhanced Quine-McCluskey algorithm function in the package to minimize the resulting configurations with respect to our outcome measure (Duşa, 2019, p. 161; Fiss, 2011; Ragin, 1987). The function first generates a truth table containing all theoretically possible combinations of the causal conditions considered in this study and then assigns all empirically observed combinations to their corresponding row. 6 The function takes arguments to set (1) a frequency threshold, indicating the minimum number of empirical cases needed per configuration for it to be included in further analysis, (2) a minimum level of consistency for a given solution, which indicates the extent to which cases with the same combination of conditions also share the same outcome, and (3) a proportional reduction in inconsistency (PRI), whereby the solutions avoid simultaneous subset relations of configurations that are consistent for both high and low performance (or presence and absence of the outcome). For the frequency threshold, we followed recommendations in the literature that at least 75%–80% of the cases be preserved after the cut-off is instituted (Ragin, 2017). We therefore used a threshold of two cases per configuration thereby retaining 75% of our sample. Our consistency cut-off was set at 0.80, again in line with prior work (Fiss, 2011; Ragin, 2008b). Finally, following current best practices (Misangyi & Acharya, 2014; Ragin, 2017), we kept the PRI threshold above 0.75.

We instructed the QCA package in R to account for fsQCA’s parsimonious and intermediate solutions (see Bell et al., 2014; Campbell et al., 2016; Crilly et al., 2012; Crilly, 2011; Fiss, 2011). The solutions are determined by the software’s Boolean algorithm, whereby the parsimonious solution is based on all simplifying assumptions, which indicates that it represents the most reduced form of the solution (Ragin, 2008b). To arrive at the intermediate solution, the algorithm eliminates those causal conditions from the complex solution that are inconsistent with existing knowledge (Ragin & Sonnett, 2005). Existing knowledge is considered in that the software asks the researcher for their input on how the causal conditions link to the outcome of interest through their presence and absence. In this study, we assume that both internal and external stakeholder management as well as exploitative and exploratory innovation contribute to high firm performance through their presence rather than their absence. We did not assume a contribution by the contingency conditions. Including both the parsimonious and intermediate solutions allows us to determine which conditions are core to the configurations and which represent peripheral conditions (Fiss, 2011). Core conditions are present in both the parsimonious and intermediate solutions, whereas peripheral conditions only appear in the intermediate solution.

Results

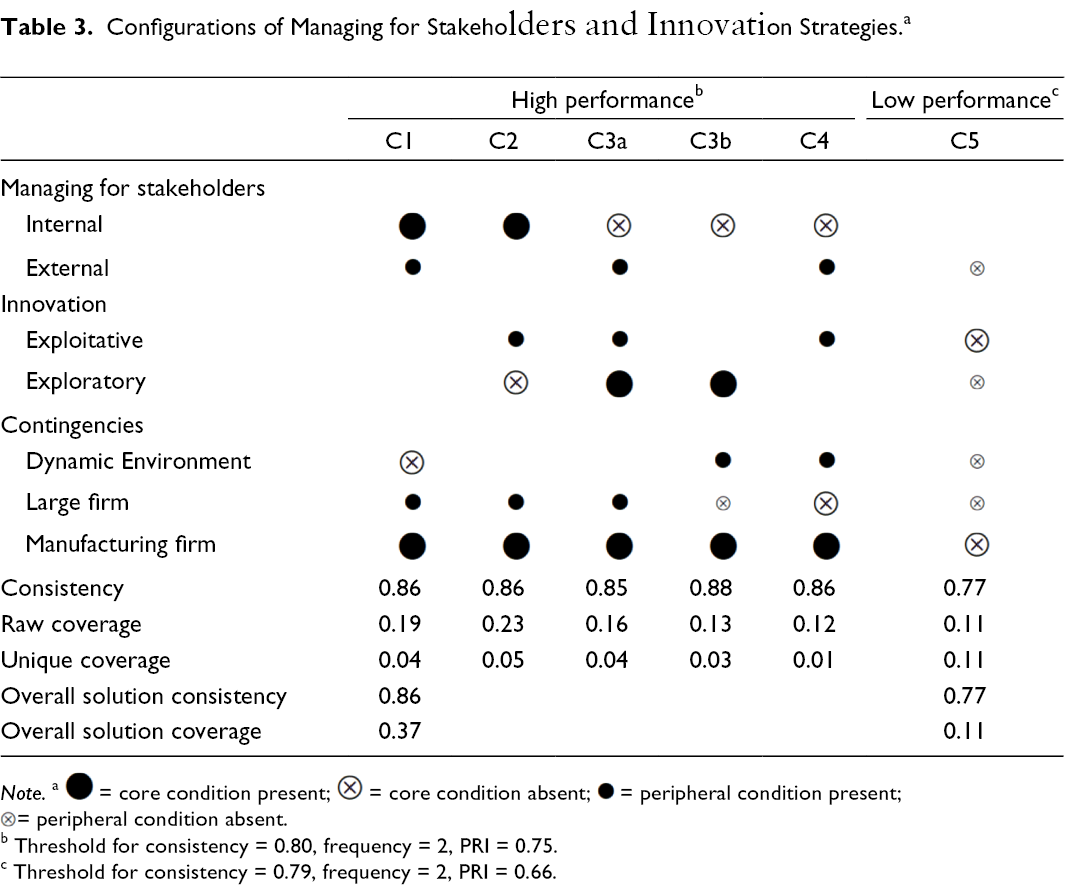

As we did not find evidence for necessary conditions, we proceeded to the standard analysis of sufficiency where fsQCA produces the configurations leading to the outcome of interest. We first focus on explaining the overall configurations we find for high performance, then move on to explain our findings regarding complements and substitutes, and finally, low performance. Table 3 shows all consistently high-performing configurations, whereby  indicates the presence of a condition and

indicates the presence of a condition and  indicates its absence. Large circles represent core conditions, whereas small circles indicate peripheral conditions. A blank space denotes a “don’t care” situation, where a given condition can be either present or absent. Table 3 also reports consistency and coverage for both the individual configurations and the overall solutions. All the individual configurations as well as the overall solution display appropriate consistency levels. Overall solution coverage provides an indication of the joint importance or empirical relevance of all causal paths (Bell et al., 2014; Schneider et al., 2010) and unique coverage elucidates the relative weight of each path in leading to high or low ROE (Fiss, 2011; Ragin, 2008b).

indicates its absence. Large circles represent core conditions, whereas small circles indicate peripheral conditions. A blank space denotes a “don’t care” situation, where a given condition can be either present or absent. Table 3 also reports consistency and coverage for both the individual configurations and the overall solutions. All the individual configurations as well as the overall solution display appropriate consistency levels. Overall solution coverage provides an indication of the joint importance or empirical relevance of all causal paths (Bell et al., 2014; Schneider et al., 2010) and unique coverage elucidates the relative weight of each path in leading to high or low ROE (Fiss, 2011; Ragin, 2008b).

Configurations of Managing for Stakeholders and Innovation Strategies.a

Note. a  = core condition present;

= core condition present;  = core condition absent;

= core condition absent;  = peripheral condition present;

= peripheral condition present;

= peripheral condition absent.

= peripheral condition absent.

b Threshold for consistency = 0.80, frequency = 2, PRI = 0.75.

c Threshold for consistency = 0.79, frequency = 2, PRI = 0.66.

Configurations Sufficient for High Performance

Table 3 presents the configurations of managing for internal and external stakeholders as well as exploitative and exploratory innovation sufficient for high performance in various contexts. Our analysis reveals first- and second-order equifinality as we observe four types of configurations that differ in their core conditions and two configurations that have the same core conditions but different peripheral conditions.

Configuration C1 applies to large manufacturing firms operating in a comparatively stable environment. These firms achieve high performance by focusing on their stakeholder management efforts: While the presence of both types of stakeholder management is important, managing for internal stakeholders is a core condition. In turn, innovation does not seem to matter for this configuration: Both exploitative and exploratory innovation are blanks, implying they can be either present or absent. Configuration C2 involves large manufacturing firms that operate either in stable or dynamic environments. These firms focus on managing for their internal stakeholders—this is a core condition in this configuration—while simultaneously pursuing an exploitative innovation strategy. C2 firms do not pursue exploratory innovation, and it does not matter whether these firms manage for their external stakeholders or not. Meanwhile, C3a involves large manufacturing firms that manage for their external stakeholders and simultaneously pursue both exploitative and exploratory innovation strategies to achieve high performance. Importantly, these firms do not put great effort into managing for their internal stakeholders to achieve high performance. Configuration C3b shares the same core conditions with C3a, namely the absence of internal stakeholder management and the presence of exploratory innovation and a manufacturing context. However, these firms are rather small and can be found only in dynamic environments. Unlike for firms in C3a, managing for external stakeholders or pursuing exploitative innovation are not important conditions for their high performance. Finally, configuration C4 also applies to small manufacturing firms in comparatively dynamic environments. These firms achieve high performance by managing for their external stakeholders and pursuing an exploitative innovation strategy. Like the configurations under C3, they do not manage for their internal stakeholders, which appears as a core condition. Different from C3, it does not matter for C4 firms which approach they take to exploratory innovation.

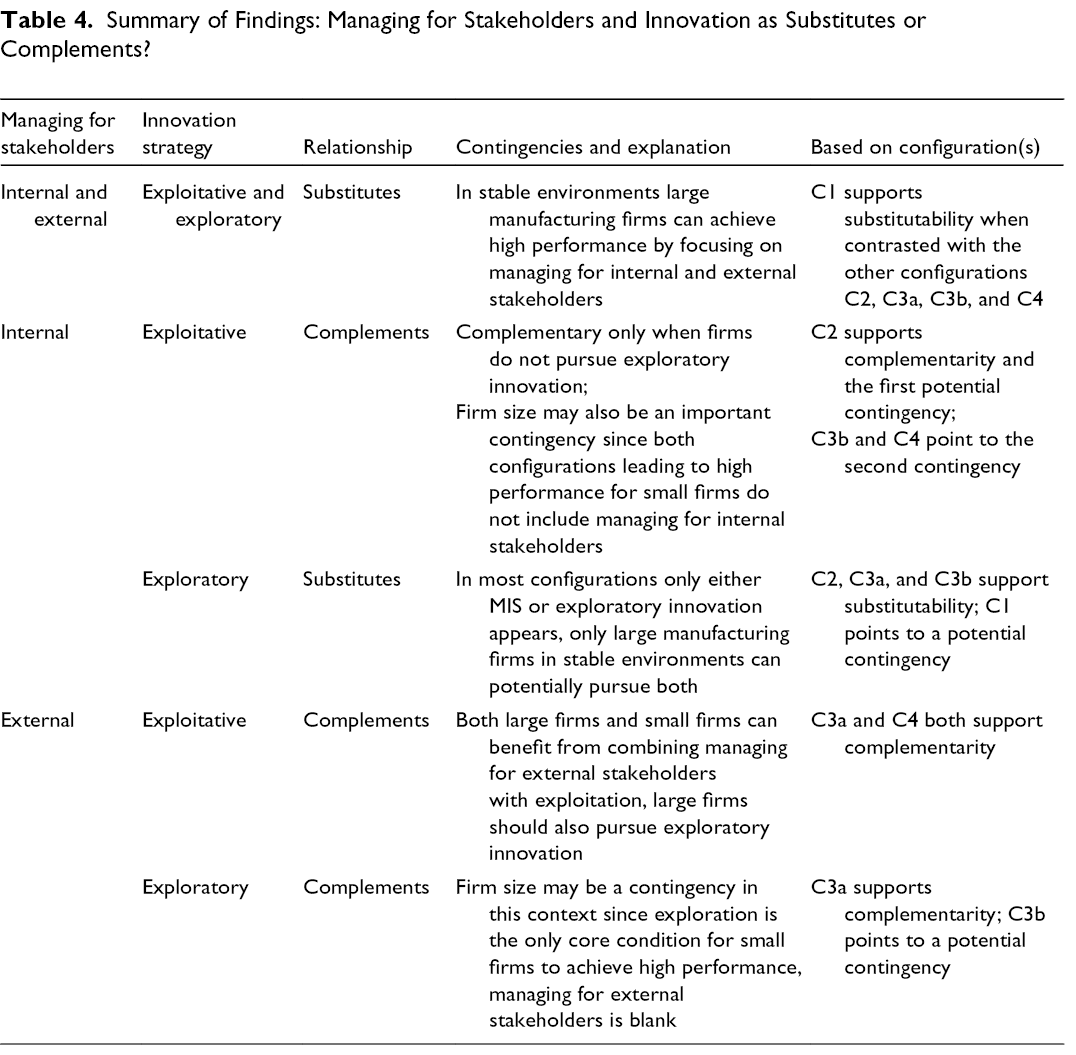

Insights on the Substitutability and Complementarity of Managing for Stakeholders and Innovation

Next, we analyze the high-performing configurations to derive insights about the potential substitutability and complementarity of MfS and innovation. We do this by examining patterns apparent within the configurations and by comparing the configurations with each other. Table 4 provides a summary of the findings. Since there is only one configuration for firms operating in relatively stable environments, we examine this configuration first and separately from the other configurations. In this configuration, C1, firms achieve high performance by managing for internal and external stakeholders without necessarily needing to pursue innovation. This suggests that, at least in comparatively stable environments, stakeholder management can substitute for innovation.

Summary of Findings: Managing for Stakeholders and Innovation as Substitutes or Complements?

Looking at configuration C2, we see that managing for internal stakeholders can complement an exploitative innovation strategy, but it appears to be the case only in large firms that are explicitly not pursuing an exploratory innovation strategy. We derive these boundary conditions by comparing configuration C2 with other configurations: Among the configurations where environmental dynamism is either irrelevant (C3a) or present (C3b and C4), C2 is the only configuration where managing for internal stakeholders leads to high performance jointly with exploitative innovation. It is also the only configuration where managing for internal stakeholders is combined with little or no pursuit of exploratory innovation.

The other configurations involving dynamic/indifferent environments (C3a, C3b, and C4) show the opposite relationship. In these configurations, the firms are explicitly not managing for their internal stakeholders while pursuing an exploratory innovation strategy (C3a and C3b) or being indifferent toward exploratory innovation (C4). This seems to indicate that in dynamic environments, managing for internal stakeholders and exploratory innovation can be substitutes.

Firms in configuration C3a combine managing for external stakeholders, exploitative innovation, and exploratory innovation, the latter being a core condition, to achieve high performance. This configuration, when analyzed in conjunction with configuration C4, which also combines managing for external stakeholders with exploitative innovation, suggests that managing for external stakeholders may complement exploitative innovation. Across all five configurations, we notice that these two strategies appear conjointly whenever environmental dynamism is high or does not matter.

Configuration C3a also indicates that managing for external stakeholders and exploratory innovation may be complements. Configuration C3b applies to small manufacturing firms in dynamic environments, and like in configuration C3a, exploratory innovation is a core condition. In this configuration, exploratory innovation is accompanied only by the absence of managing for internal stakeholders. As such, it is one of the configurations suggesting that managing for internal stakeholders and exploratory innovation are substitutes.

Finally, configuration C4 also applies to small manufacturing firms in dynamic environments. Here, high performance is the result of combining little or no management for internal stakeholders with managing for external stakeholders and exploitative innovation. Consequently, configuration C4 is also indicative of complementarity between managing for external stakeholders and exploitative innovation.

By comparing the two configurations that apply to large manufacturing firms (C2 and C3a) with the two configurations about small manufacturing firms in dynamic environments (C3b and C4), we can derive another important insight: Both of these paired sets of firms seem to display a similar pattern in that there is one configuration where the primary focus of the firms in the configuration appears to be exploitative innovation (configurations C2 and C4) and another configuration where the primary focus is on exploratory innovation (configurations C3a and C3b). This suggests that both foci are viable strategies for achieving high performance. Further, the approaches to internal and external stakeholders should match the innovation strategy pursued by the firm, but there are differences in terms of how such a match can be accomplished depending on firm size. High-performing large firms focus on managing for internal stakeholders and exploitative innovation with little or no pursuit of exploratory innovation. In turn, high-performing small firms combine their exploitative innovation approach with managing for external stakeholders and little or no managing for their internal stakeholders. Meanwhile, large firms pursuing exploratory innovation combine this approach with exploitative innovation and managing for external stakeholders, but they do not focus on managing for their internal stakeholders. Small firms focused on exploratory innovation do not simultaneously manage for their internal stakeholders.

Configurations Sufficient for Low Performance

Causal asymmetry implies that configurations leading to one outcome (high performance here) are not the inverse of configurations that lead to the opposite outcome (low performance here). As we seek to understand both kinds of configurations, we also run fsQCA for low performance, which we calibrated as the inverse of high performance. Using the same thresholds for consistency, frequency, and PRI as for the analysis of high performance, we find no evidence for consistently low-performing configurations. This could indicate the possibility of many ways to underperform as opposed to a few clear patterns that consistently link to low performance. It could also be that our model is better suited to explain high than low performance, at least with the applied parameters. However, we noticed that the consistency levels in our analysis of low performance were very close to our threshold. Therefore, we lowered our consistency threshold from 0.80 to 0.79 and PRI from 0.75 to 0.66 7 while keeping the frequency threshold of two cases. Using these new thresholds, we find one consistently low-performing configuration that involves small service firms in stable industries. These firms neither manage for external stakeholders nor do they pursue innovation. MIS does not matter as it can be present or absent with no effect on the outcome. These results show how simultaneous lack of both MfS and innovation may be detrimental for firm performance. Our findings also indicate that MIS is not a sufficient condition to produce high performance when firms do not care about their external stakeholders or innovation.

Robustness Tests

We conducted various tests to establish robustness of our results. First, our main analysis was with ROE lagged 3 years, so we ran the analysis again using ROE with a lag of 1 and 2 years. The results with a lag of 2 years are almost identical to the results presented above with the difference that the overall solution has one configuration less than the solution with 3-year lag. When the outcome condition lags by only 1 year, we identify only one high-performing configuration. This could be because the positive effects of MfS and innovation typically realize only over time and our sample firms were maybe less concerned with those prior to the survey. Firms may still have been recovering from the financial crisis that took place in 2008/2009 and only slowly started to become profitable again, or starting to invest more in MfS and innovation, which may have led to many different configurational strategies and therefore less consistent patterns for high performance. The low-performing configuration we identified was the same as in our main analysis.

Second, we used alternative thresholds for consistency and frequency to see whether these would change our results. We ran our model with consistency thresholds of 0.75 and 0.85 without observing any changes in the results. Moreover, we changed the frequency threshold from two to one and three. This resulted in a change in the number of identified high-performing configurations with four (threshold = 3) and nine (threshold = 1) configurations compared with five in our main analysis. However, we would still derive the same interpretations of the results as these new configurations were very similar to those presented in this study.

Discussion

The goal of this paper is to examine the puzzle in the stakeholder literature whether MfS and innovation are substitutes or complements in affecting firm performance. Due to the inherent complexity of this relationship, there have been several calls for research to take a more encompassing perspective of MfS and innovation to shed light on the fit between these strategies (Hull & Rothenberg, 2008; Li et al., 2018; Minoja et al., 2010; Partanen et al., 2014). In this study we integrated research on stakeholder management and innovation to detail the main arguments of both the substitutability and complementarity research streams as well as to identify the dimensionality of both constructs. We then used fsQCA to examine which configurations of managing for internal and external stakeholders and exploitative and exploratory innovation are likely to lead to high or low performance, and whether these strategies are likely to substitute or complement each other. Our goal in this discussion is to elaborate theory on configurations of internal and external stakeholder management as well as exploitative and exploratory innovation that allow firms to achieve high performance.

Theoretical Contributions

Starting with managing for internal stakeholders (MIS), our findings indicate that MIS can complement exploitative innovation under specific circumstances. Namely, large manufacturing firms that specifically put less emphasis on exploratory innovation may perform well by combining MIS with exploitative innovation. This finding is in line with research that has argued that employees can contribute substantially to incremental innovations within the firm (Anderson et al., 2004; Zhang et al., 2014). Managing for these employees will entice them to further engage in incremental innovation (Gambeta et al., 2019; Ruppel & Harrington, 2000). The fact that this configuration seems to apply only to large nonexploratory firms, may be indicative of two implications. First, the complementarity literature stream has most likely been correct to point to the costs of MfS being a potential limitation of stakeholder management. Our findings suggest that large firms may be better able to take advantage of MIS, perhaps because of their more abundant resources and slack, whereas small firms must be more selective (Galbreath, 2006; McGuire et al., 1988). Additionally, small firms may also be able to implicitly substitute MIS with features of their organizational structure. For example, recent research has shown that aspects of organizational structure such as centralization or formalization can have positive effects on small firms’ innovation activities (e.g., Gentile-Lüdecke et al., 2020; Palmié et al., 2016). Second, even large firms may experience a trade-off between MIS and exploratory innovation since these firms should explicitly not focus on exploratory innovation if they are pursuing MIS and an exploitative innovation strategy.

The second finding from our study relates to the relationship between MIS and exploratory innovation. Our study suggests that these two strategies may be substitutes. Prior research has argued that MIS may have adverse effects on a firm’s propensity to pursue exploratory innovation (Gambeta et al., 2019; Minoja et al., 2010). According to these studies, MIS reduces employee turnover and enhances mutual learning, leading to increased homogeneity in the firm’s knowledge base and an increased propensity to exploit rather than explore. Further, MIS creates incentives to pursue exploitative rather than exploratory innovation. As a result, and in line with our configurational analysis, firms attempting to pursue exploratory innovation should place much less emphasis on MIS to achieve high performance.

Our study also indicates that the relationship between mangaging for external stakeholders (MES) and exploratory innovation is complementary in nature. Research has shown that external stakeholders can provide firms with a variety of knowledge that may differ substantially from what the firm already knows (Beckman et al., 2004; Menon & Pfeffer, 2003; Phene et al., 2012; Rosenkopf & Almeida, 2003). Such diverse knowledge is particularly important for exploratory innovation since it primarily intends to create new knowledge and ideas (Hoang & Rothaermel, 2010; Rothaermel & Deeds, 2004). Therefore, when firms manage for external stakeholders, they should be able to improve their ability to obtain knowledge germane to exploratory innovation. Importantly, our findings suggest that the complementary relationship between MES and exploratory innovation may be more relevant for large firms than small firms. This may perhaps, again, be a result of the resource constraints experienced by smaller firms. Exploratory innovation is an especially resource-intensive strategy (Mueller et al., 2013). Therefore, small firms may primarily have to focus on their exploratory innovation efforts.

Our study also suggests that MES and exploitative innovation can be complements. Here too, the primary benefit of MfS may consist in its ability to improve firms’ access to knowledge held by stakeholders. We may glean some additional insights by considering the contingencies surrounding the complementarity of MES and exploitative innovation. Both large and small firms in our study can benefit from combining these two strategies. However, large firms do so by adding a third strategy, exploratory innovation, whereas this condition does not matter for small firms. Therefore, it seems likely that MfS enables firms to obtain different types of knowledge from external stakeholders; larger firms can likely access a broader range of knowledge, whereas smaller firms are likely gaining in-depth knowledge to be used specifically in their exploitative innovation endeavors.

Our study also points to the possibility that MfS can substitute for innovation in stable environments. Past research has argued that innovation substitutes for stakeholder management (Hull & Rothenberg, 2008; McWilliams & Siegel, 2000), but this early research in the substitutability literature stream did not consider environmental dynamism as a contingency factor. More recent work has argued that less innovative firms may benefit from investing in their stakeholder relationships (Garcia-Castro & Francoeur, 2016; Mackey et al., 2007). Our finding seems to be in line with these studies, although they appear to offer a different explanation for the substitution effect. As our configurational analysis indicates, the level of environmental dynamism and firm size may be key to explaining the substitutability between stakeholder management and innovation; large firms can still potentially also pursue exploitative and/or exploratory innovation as these strategies are not present in the configuration leading to high performance. Since firms in stable environments are less likely to need to commit to being highly innovative (Brown & Eisenhardt, 1997; Eisenhardt, 1989), the potential downside of MIS in particular—that MIS increases firms’ propensity to focus on exploitative innovation—is not as pertinent to firm success in stable environments. Our findings suggest that firms in this context may derive greater benefits from investing in relationships with both their internal and external stakeholders. Further, operating in a stable environment may also open up resources in these firms to more successfully deal with potentially conflicting demands of their internal and external stakeholders.

Our study offers a final insight on which types of configurations of MfS and innovation allow firms to achieve high performance. Our analysis revealed two approaches each for large firms and small firms. On the one hand, both large firms and small firms can fare well if they focus on exploitative innovation. On the other hand, both large and small firms could benefit by focusing on exploratory innovation. While the precise configurations differ for large and small firms, it is very notable that both an exploitative and exploratory strategy focus are viable paths to high performance. This finding suggests that firms may set their strategic orientation toward innovation first and then adjust their MfS approach to fit with their innovation strategy.

The low performance configuration identified in our results underscores the above finding regarding the potential importance of innovation. The low performance configuration provides support for the notion that not pursuing any innovation and neglecting to manage for external stakeholders appears to be deleterious to firm performance. Further, managing for internal stakeholders by itself is insufficient for high performance when firms do not manage for their external stakeholders or pursue any innovation strategy.

Our study makes several contributions to stakeholder theory. First and foremost, we provide a comprehensive and nuanced perspective on the substitutability and complementarity of MfS and innovation. In doing so, we are able to respond to calls for research that firm strategies should be considered simultaneously (Flammer & Kacperczyk, 2016; Hull & Rothenberg, 2008; Minoja et al., 2010; Partanen et al., 2014; Schweiger et al., 2019). Our configurational approach allows us to improve our understanding of the joint performance implications of MfS and innovation. We find that MfS and innovation can be both substitutes and complements depending on the specific circumstances.

Second, this study also speaks to a core topic in stakeholder theory, that of how firms should deal with multiple stakeholder groups and allocate their limited resources across those groups (Garcia-Castro & Francoeur, 2016; Harrison & Freeman, 1999; Hillman & Keim, 2001; Tantalo & Priem, 2016). This question is important for stakeholder theory because firms rarely encounter a single stakeholder group in isolation, but interact with multiple stakeholder groups simultaneously (Guaita Martínez et al., 2019; Rowley, 1997). Our findings indicate that in stable environments firms should manage for both internal and external stakeholders to achieve high performance. However, in most other situations, both large and small firms seem to be able to achieve high performance by focusing on a particular stakeholder group that most closely aligns with the innovation strategy the firm is pursuing. These findings corroborate the complexity and relevance of answering this “simultaneity question.” We agree with the above research that this question is a crucial path for further investigation.

Third, our findings also contribute to the literature on exploitation and exploration. Research in this area has focused chiefly on balancing exploitative and exploratory innovation strategies (Ebben & Johnson, 2005; Gibson & Birkinshaw, 2004; He & Wong, 2004; Hill & Birkinshaw, 2014; Mudambi & Swift, 2014; Rogan & Mors, 2014; Stettner & Lavie, 2014) and potential moderators to the balancing approach (Cao et al., 2009; Jansen et al., 2012; Lavie et al., 2011; Patel et al., 2013; Swift, 2016; Uotila et al., 2009; Voss & Voss, 2013). However, there have been repeated calls to examine the direct performance implications of exploitative and exploratory innovation strategies as well as to adopt contingency perspectives in studying the outcome effects of these innovation strategies (Benner & Tushman, 2003; Lavie et al., 2010; Mueller et al., 2013; Raisch & Birkinshaw, 2008). The contingency factors identified in previous work are often beneficial to either exploration or exploitation, but rarely both (Belderbos et al., 2010; Jansen et al., 2006; Mueller et al., 2013; Rothaermel & Alexandre, 2009; Yang et al., 2014). Our study suggests that managing for internal stakeholders may be detrimental to pursuing an exploratory innovation strategy. However, our findings also indicate that large manufacturing firms pursuing both an exploratory and exploitative innovation strategy may support these endeavors by also managing for their external stakeholders.

Paths for Future Research

Our study points to several intriguing paths for future research. First, our study considers a number of relevant contingency factors that appear to influence the relationship between MfS and innovation. We took industry, environmental dynamism, and firm size into account. We believe it will be valuable for future research to examine other potentially meaningful contingencies. Specifically, in examining the relationship between exploitative innovation and managing for internal stakeholders, we posited that small firms may be able to adjust their organizational structure to substitute for MIS. Therefore, future research may want to examine in detail whether and to what extent contingencies like organizational structure can substitute for MfS in general and MIS particularly.

Our analysis also suggested that MfS is a way for firms to obtain varied types of knowledge from stakeholders. We argued that large firms pursuing exploitative innovation may be able to access a broad range of knowledge from external stakeholders to use in their innovations. Conversely, due to their limited resources, smaller firms pursuing exploitative innovation may have to focus on acquiring more detailed and specific knowledge from external stakeholders. Future research may want to examine this intriguing finding more comprehensively by considering different types of knowledge as a further contingency in the interplay of MfS, innovation, and firm performance.

Finally, our study advanced the argument that firms may initially be setting their strategic orientation toward innovation and adjusting their MfS approach to fit their innovation strategy. This is a proposition that can be examined by future research taking a longitudinal approach to derive more in-depth insights into the sequential development of firms’ strategies. It would be very valuable to gain a better understanding of whether and how firms change the configurations of MfS and innovation over time.

Constraints on Generality

QCA is limited in its ability to provide conclusions that can be generalized to other samples (Rihoux & Ragin, 2009; Simons et al., 2017). Unlike correlation-based methods, QCA does not offer probabilistic estimations based on random samples drawn from the population, but rather narrow conclusions based on the cases along with the researcher’s input regarding the causal links examined in the study (Fiss, 2011). In fsQCA, even large random samples can miss (rare) cases that are highly relevant for the outcome of interest (Greckhamer et al., 2018). Yet, our goal was not to be able to fully generalize our findings to the population or to investigate rare cases, but to inductively examine a complex phenomenon that has not yet been studied from a configurational perspective. Thus, we add important insights to the literature and provide new evidence on relevant relationships regarding the substitutability and complementarity of MfS and innovation practices in various contexts. We encourage future research to test our findings with more representative samples, beyond the publicly listed European manufacturing and service firms we studied here, to establish more generalizable conclusions. Further, since our study relies on data collected during a period of relative economic stability, we are unable to ascertain whether the configurations of MfS and innovation we describe here also apply during times of crises like the COVID-19 pandemic. Considering that there have been multiple extraordinary events during the 21st century (Caligiuri et al., 2020; Donthu & Gustafsson, 2020) and that past research has shown that organizations often soon return to operating as normal (Lee et al., 2020, p. 1046), we are confident that our findings are still relevant under many circumstances. Nevertheless, we encourage future research to precisely examine to what extent different configurations of MfS and innovation are likely to succeed during crises and if there are any lasting changes brought about by the COVID-19 pandemic.

Conclusion

Innovation, which is traditionally considered a core element of entrepreneurship (Hitt et al., 2011; Ireland et al., 2003; Lumpkin & Dess, 1996; Michaelis et al., 2018), has attracted increasing interest among stakeholder scholars. To date, the growing number of studies looking at the performance implications of the interplay between MfS and innovation yielded seemingly inconsistent findings, with some studies supporting the notion that MfS and innovation are substitutes and others suggesting that they are complements with respect to firm performance. By distinguishing between different stakeholders and different innovation strategies, our study contributes to resolving this puzzle and reconciling both positions. It indicates that stakeholder management and innovation are both substitutes and complements, depending on the specific stakeholders and the specific innovation strategies considered. Our study further finds that the question of how firms should allocate their attention across stakeholder groups depends on their innovation strategy and the level of environmental dynamism. These findings suggest that studying the intersection between stakeholder management and innovation/entrepreneurship can advance both fields. We hope that our insights stimulate much more research along these lines.

Footnotes

Acknowledgments

Thank you to the special issue editors and the anonymous reviewers for their helpful feedback and guidance. We also express our appreciation to Oliver Gassmann, Tomi Laamanen, Johannes Meuer, and Vangelis Souitaris for their valuable comments on previous versions of the manuscript. Finally, we thank Marcus M. Keupp and Max Feider for their support in designing the survey questionnaire. An earlier version of this manuscript was nominated for the Conference Best Paper Prize at the Strategic Management Society’s 2016 Annual Conference in Berlin.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Notes

Author Biographies