Abstract

We study family firm status as an important condition in signaling theory; specifically, we propose that the market reacts more positively to positive, and more negatively to negative, CSR news (i.e., signals) from family firms than to similar news from nonfamily firms. Moreover, we propose that during recessions, the direction of these relationships reverses. Based on an event study of 1247 positive and negative changes in the CSR ratings for all firms listed on the French SFB120 stock market index (2003-2013), we find support for our hypotheses. Moreover, a post hoc analysis reveals that the relationships are contingent on whether a family CEO leads the firm.

Keywords

Introduction

Much research on family firms has focused on the consequences of family firms’ actions on family owners and managers (e.g., Gómez-Mejía et al., 2007), nonfamily managers and employees (Tabor et al., 2018), as well as partners within the family firm’s value chain (Mitchell et al., 2011). However, one important stakeholder has largely been ignored to date: outside (i.e., nonfamily) shareholders of listed family firms (Anderson & Reeb, 2004). For listed family firms, outside investors provide additional equity for growth (Kotlar et al., 2018; La Porta et al., 1999; Leitterstorf & Rau, 2014). Moreover, good firm valuation as measured by high stock returns can lead to an enhanced reputation for the family firm as well as for the family and the individual manager (Zellweger & Nason, 2008), and this improved firm reputation can be leveraged in the marketplace among suppliers, customers, or capital providers such as banks (Sirmon & Hitt, 2003).

The assessment of firms by outside investors is greatly affected by the signals that those investors receive on the behavior of the respective firms (e.g., Park & Mezias, 2005; Zhang & Wiersema, 2009). While signals indicating a high quality firm and “good” behavioral intentions lead to a positive assessment of those firms by investors, negative signals indicating doubtful behavioral intentions might ultimately decrease the firm’s market value (e.g., Maung et al., 2020). However, despite increasing academic knowledge on the signal–investor reaction relationship (Certo, 2003; Maung et al., 2020; Park & Mezias, 2005; Zhang & Wiersema, 2009), it is likely that insights gained in the context of listed nonfamily firms are not easily transferrable to family firms. The underlying reason is that investors might expect strategic behavior from family firms that is different from that of nonfamily firms (Miller et al., 2013) and thus react differently to similar signals referring to family versus nonfamily firms (Maung et al., 2020). However, to date, we have only limited knowledge about how outside shareholders perceive signals from family firms and, consequently, react to family firms’ activities compared to the same activities conducted by nonfamily firms (André et al., 2014; Chang et al., 2010; Wong et al., 2010). This constitutes an important research gap, given the relevance of family firms’ stock market valuation for firm reputation, liquidity, and potentially survival (Zellweger & Nason, 2008).

One particularly important context in which to study investors’ perceptions of firm signals is their reactions to information about firms’ corporate social responsibility (CSR), that is, CSR news—new public information on the firm’s socially responsible (or irresponsible) activities. 1 Prior research has shown that CSR has become increasingly common over the last few decades (Malik, 2015) for both family and nonfamily firms and that investors today also strongly consider CSR-related signals when evaluating firms (Krüger, 2015; Renneboog et al., 2008). In general, this stream of research suggests that investors favor positive CSR news, as such news is assumed to signal high firm quality, yet their final evaluations might depend on their assessment of the firm’s behavior and its underlying intentions (Connelly et al., 2010; Filatotchev & Bishop, 2002), given that the real motives of the firm to engage in CSR may not be obvious to a third party. 2 Moreover, prior research suggests that the assessment of CSR-related signals might depend on the signaling environment (Connelly et al., 2011), such as the economic conditions in which the firm operates. Hence, we ask the following research questions: How does family firm status affect outside investors’ perceptions of signals and thus their reactions to positive and negative CSR news? How do those relationships depend on the signaling environment and how do they change in times of recession?

We integrate research on signaling theory (Connelly et al., 2011; Spence, 1973, 2002) and family firms (Kotlar et al., 2018; Leitterstorf & Rau, 2014) to theorize how outside investors interpret similar signals from family and nonfamily firms differently, specifically in the CSR context (Maung et al., 2020). Our first two hypotheses posit that outside investors react more positively to positive CSR news and more negatively to negative CSR news from family firms than from nonfamily firms. When receiving signals such as CSR news, investors need to evaluate the behavioral intentions of the firm. We propose that, due to family firms’ long-term focus (Lumpkin & Brigham, 2011) and stakeholder orientation (Cennamo et al., 2012; Mitchell et al., 2011), positive CSR news is in line with their expected behavior, hence increasing the signal’s credibility (i.e., honesty and fit) and ultimately leading to a more positive reaction. In a similar vein, negative CSR news runs counter to the expected family firm behavior, decreasing signal credibility and resulting in an even more negative investor reaction. Moreover, we propose that the interpretation of the signal is dependent on the signaling environment (Connelly et al., 2011), specifically, the overall economic situation. We hypothesize that the influence of family firm status reverses during times of recession, since the recession alters what firm activities investors might perceive as expected or desired firm behavior. This change in investors’ perceptions occurs as recessions focus attention on “survival” rather than growth and increase the level of uncertainty in society and the economy (Davidsson & Gordon, 2016), leading to generally increased levels of information asymmetry (De Haas & Van Horen, 2011). We test our hypotheses with an event study of 1247 positive and negative changes in the CSR ratings for French public firms from 2003 to 2013 and find support for our hypotheses. Moreover, post hoc tests identify substantial heterogeneity among family firms, revealing that the identified effects also depend on whether the family firm is led by a family CEO or a nonfamily CEO.

Our study makes the following contributions to the literature, especially regarding family firms and signaling theory. First, we contribute to the important yet still emerging stream of literature on signaling in the family firm context (e.g., Maung et al., 2020) by hypothesizing how outside investors react differently to similar signals about family firms and nonfamily firms. We thereby advance research by theorizing outside investors’ specific interpretations of what is authentic and legitimate (or “expected”) for family firms, leading to different interpretations of signal honesty and ultimately the credibility of signals sent by family firms versus nonfamily firms. We also contribute to signaling theory in general and family firm signaling in particular by studying negative CSR news, which can be seen as an unintentional signal (i.e., a signal that signalers emit without being aware that they are signaling [Spence, 2002]), as well as recessions as a signaling environment—both of which relate to understudied areas in the signaling research field (Connelly et al., 2011). Second, we contribute to the research on family firms by investigating the consequences of CSR news, especially its effect on the stock market (Jayamohan et al., 2017). Specifically, we show that in general, positive CSR news about family firms is perceived positively and negative CSR news is perceived negatively by outside investors—a finding that also carries important practical implications. These findings might also help disentangle the (until now) puzzling effect of positive and negative CSR news on the stock market (e.g., Ramchander et al., 2012) by including family firm status and the economic environment as crucial influencing factors. Last, we show in our post hoc tests that the identified relationships depend on whether the firm is managed by a family CEO, thereby contributing to the research on family firm heterogeneity (Chua et al., 2012).

Literature Review

Stock Market Reactions to Family Firms and Nonfamily Firms: The Role of Signaling Theory

Shareholders are important stakeholders for any listed firm (Sauerwald et al., 2016), including listed family firms (Fernando et al., 2014), which are defined as firms in which multiple members of the same family, jointly or subsequently, own a controlling stake (Sraer & Thesmar, 2007) and which are the dominant form of firm ownership around the world (La Porta et al., 1999). Notably, in addition to their opportunity to challenge important firm activities, 3 outside noncontrolling shareholders are active in selling and buying shares on a continuous basis, thereby affecting the stock market value of the company.

Outside shareholders 4 are thus continuously seeking signals that indicate firms’ quality and intentions and are eager to gather timely information about whether they should invest in a specific company or whether they should maintain or sell their existing shares (Connelly et al., 2011). Signaling is particularly essential in the presence of information asymmetries (Spence, 2002). As outside investors have limited information about the underlying value of the firm (i.e., information asymmetries between the firm and investors), they seek signals (such as earnings announcements, acquisition behavior, or CSR news) in the market on which to build their perceptions about the firm. Hence, to understand shareholders’ investment behavior, signaling theory promises to be a useful theoretical lens. Signaling theory originates from the seminal work of Spence (1973), who demonstrated that job market candidates aim to signal their underlying abilities and skills to prospective employers. To count as a signal, shared information needs to be relevant to the decision to be made (e.g., education is likely relevant in the job application context, whereas preferred music style is not), observable (i.e., the receiver must notice the signal), and costly to imitate to allow high-quality signalers to distinguish themselves from their low-quality peers. Through signaling, the sender (e.g., a job application candidate or a firm seeking investment) reduces the information asymmetry between the sender and the receiver, especially about the quality or intentions of the sender (Spence, 2002), and hence might influence the receiver in their decision-making (e.g., about which candidate to hire or which firm to invest in).

Specifically, research has treated outside shareholders as important receivers of signals that are intentionally or unintentionally sent by listed companies and their controlling shareholders (Certo et al., 2001; Goranova et al., 2007). As a consequence, outside shareholders typically react almost instantaneously to such signals—especially when they perceive the signals to be true reflections of the firm’s stance and behavior (Botero, 2014; Ehrhart & Ziegert, 2005; Kahlert et al., 2017; Tabor et al., 2019) rather than PR—through adapting their buy, hold, and sell behaviors, which are mirrored in changes in the firm’s stock price (Sauerwald et al., 2016). As such, it is no surprise that an increasing number of scholars have paid attention to how certain signals, such as mergers and acquisitions (M&A) announcements (Francis et al., 2008) or releases about earnings surprises (Karpoff et al., 2008), affect the respective firm’s stock price.

Research on signaling theory has revealed a multitude of factors that affect how receivers react to signals that they notice. The interpretation of the signal, that is, the process of translating the signal into perceived meaning, depends on signal credibility (also often referred to as reliability; Connelly et al., 2011). According to Connelly et al. (2011), a signal’s credibility is determined by the combination of two concepts: (a) signal fit, which refers to the extent to which the signal is correlated with unobservable firm quality, and (b) signal honesty, which is associated with the extent to which the signaler indeed has the unobservable quality that is being signaled. More specifically, signal honesty refers to the assessment of whether the signal might reflect the expected behavior of the sender and thus reveals “true intentions.” For example, if firms that signal stock repurchases do not actually repurchase stocks in the future, this behavior results in a discrepancy between the signaled action and the realized action, often referred to as decoupling (Westphal & Zajac, 2001). Firms or individuals who engage in such decoupling may develop a reputation for dishonesty, and therefore their future signals would likely be interpreted as dishonest by receivers.

In addition to the characteristics of the sender (which affect signal credibility and thus its interpretation), the signaling environment has also been identified as an important boundary context in signaling theory (Connelly et al., 2011). For instance, management research has shown that the stock market reacts more favorably to alliances in a signaling environment characterized by a lack of munificence (Park & Mezias, 2005). Moreover, Gulati and Higgins (2003) study how young firms’ partnerships with venture capital firms and the resulting success of initial public offerings (IPOs) depend on the equity market conditions (i.e., hot or cold), which is an important signaling environment.

A nascent stream of research has focused on family firm status as an important boundary condition in signaling theory. In particular, this stream of research has studied the effect of family firm status on the signal perceptions of consumers (Barroso Martínez et al., 2019), job applicants (Arijs et al., 2018; Kahlert et al., 2017), and investors (Duncan & Hasso, 2018; Maung et al., 2020), especially in IPO situations (Chandler et al., 2019; Huang et al., 2019). Moreover, researchers have studied signaling in succession situations (Dehlen et al., 2014). Specifically, listed family firms have family members as controlling shareholders, who are characterized as long-term and dedicated investors in the family firm (Faccio & Lang, 2002; van Essen et al., 2013) and who are generally known to the public (Sauerwald et al., 2016). In many cases, family shareholders possess only a fraction—though controlling—of their firm’s shares (La Porta et al., 1999), while the remaining shares belong to outside shareholders, such as institutional and individual investors, that frequently sell and buy stocks (Fernando et al., 2014) based on their perceptions of future firm value.

To date, research on signaling in family firms has mostly treated family firm status as an isolated signal that can be either seen as positive (e.g., due to authenticity of their behavior [e.g., Maung et al., 2020] or due to family owners’ investments in their own firm [e.g., Huang et al., 2019]) or negative (e.g., due to family owners being assumed to be more risk averse [Chandler et al., 2019]). In our study, we go one step beyond this current research, thereby following up on a recent study by Maung et al. (2020). Instead of treating family firm status as a signal on its own, we argue that family firm status affects how other relevant signals (specifically CSR news) are perceived by signal receivers. In other words, we see family firm status as an important boundary condition in signaling research. Such theorizing is important given the prior empirical evidence that has found that family firm status triggers a more positive stock market reaction to signals of M&A announcements (André et al., 2014) but more negative reactions to announcements of corporate venture activities (Wong et al., 2010) and innovation announcements (Chang et al., 2010), hence pointing to family firm status as a relevant boundary condition. Specifically, we argue that family firm status affects signal credibility, and in particular signal honesty, as family firms differ from other forms of organizations (e.g., Feldman et al., 2016; Koenig et al., 2013; Miller et al., 2013) given their idiosyncratic governance (principal–agent alignment and specific principal–principal conflicts (Anderson et al., 2009), their socioemotional wealth considerations (Gómez-Mejía et al., 2007), and the goals that they pursue (Berrone et al., 2012). Those idiosyncrasies typically result in a stakeholder orientation (Cennamo et al., 2012; Mitchell et al., 2011), a long-term perspective (Lumpkin & Brigham, 2011), and substantial differences with regard to the prevalent agency costs (Schulze et al., 2001) compared to other firms. As such, investors might attribute a specific (“expected”) behavior to family firms, which affects their perceptions of signals sent by family firms.

CSR as an Important Signal

CSR is defined as “context-specific organizational actions and policies that take into account stakeholders’ expectations and the triple bottom line of economic, social, and environmental performance” (Aguinis, 2011, p. 855). CSR news, that is, communication about changes in a firm’s CSR, constitutes an important signal to outside investors (i.e., receivers; Akpinar et al., 2008) for the following reasons: first, CSR signals are relevant since investors incorporate nonfinancial information into their investment decisions (e.g., Certo, 2003), and CSR is an essential piece of nonfinancial information that investors care about (Krüger, 2015). CSR is also a relevant signal because an increasing number of outside investors are bound to investments in firms that care about socially and ecologically sustainable standards (Renneboog et al., 2008). Second, CSR activities are costly, at least in the short term, given the amount of human and financial resources required to conduct such activities (Certo, 2003; Schell et al., 2019).

Third, CSR signals are observable, as reporting standards for firm CSR have been heightened in recent years, and rating agencies, such as KLD for U.S. firms (Krüger, 2015) and Vigéo for European firms (Cellier & Chollet, 2016; Dupré et al., 2006; Ferrell et al., 2016), have emerged. As such, CSR news is now immediately visible to the public in general and to outside investors in particular because CSR agencies update their ratings in almost real time (Warner et al., 2006). The CSR signals sent by firms (and distributed by agencies) can be either positive (e.g., information about firms’ investments in employee health programs or initiatives to reduce their carbon footprint) or negative (e.g., information about employee layoffs or environmental scandals as well as the scaling down or abandonment of prior stakeholder-oriented programs). Hence, they serve to reduce investors’ information asymmetries regarding the firm’s quality.

What makes CSR news even more interesting from a signaling perspective is that the interpretation of CSR might be ambiguous and context dependent. While negative CSR news has previously been shown to trigger negative (Krüger, 2015) or insignificant (Fernandez-Izquierdo et al., 2009) reactions by investors, the effect of positive CSR news is more complex (e.g., Barnea & Rubin, 2010; Margolis et al., 2009). Some researchers have proposed that managers can “do well by doing good” (e.g., Falck & Heblich, 2007; Fatemi et al., 2015; Flammer & Ioannou, 2015), resulting in a positive market reaction, while others are more pessimistic. They accuse firms of “greenwashing” activities that seek to benefit managers instead of shareholders (Barnea & Rubin, 2010; Petrenko et al., 2016) and divert resources from other core firm activities (Barnett, 2007), ultimately leading to a negative market reaction. 5 Such ambiguous findings point to the need to study contingency factors to disentangle the CSR-stock market valuation puzzle.

Moreover, the specific literature on CSR signaling in family firms is rather scarce (Block et al., 2015; Dawson et al., 2020; Maung et al., 2020), revealing that family firms use CSR-related signals to communicate messages to their stakeholders about trustworthiness and their contribution to the economy, society, and the environment. Despite these advancements, the differential effect of CSR-related signals from family firms and nonfamily firms is still unknown.

Hypothesis Development

Stock Market Responses to Signals of Positive and Negative CSR News in Family Versus Nonfamily Firms

Researchers have argued that outside investors, in general, react positively to signals indicating positive CSR news (Ramchander et al., 2012). Building on signaling theory, positive CSR news, such as news regarding investments in environmental programs, can be seen as a signal that the firm values sustainability practices and cares about its stakeholders (Connelly et al., 2011)—which results in improved social capital and an improved reputation that might ultimately benefit investors (Maung et al., 2020). In addition, positive CSR news might serve as a signal of a firm’s generally high level of quality (Ding & Pukthuanthong, 2013), as research assumes that effective stakeholder management leads to a firm’s competitive advantage (Ramchander et al., 2012), which in the long term, despite some potentially unavoidable costs, increases value for the firm’s shareholders (Hillman & Keim, 2001). Indeed, this argumentation for positive CSR news as a positive signal that “fits” with overall firm quality (Block et al., 2015; Gavana et al., 2017; Lamb & Butler, 2018) is in line with prior literature proposing that “it pays to be green” (e.g., Dimson et al., 2015; Edmans, 2011; Orlitzky et al., 2003; Waddock & Graves, 1997).

Building on the literature that emphasizes the role of family firm status in signal interpretation by investors (Chandler et al., 2019; Ding & Pukthuanthong, 2013; Duncan & Hasso, 2018; Huang et al., 2019), we argue that positive CSR news from family firms is seen as a particularly positive signal by outside investors because family firm status increases signal honesty and thus signal credibility and hence determines how outside investors interpret the received signal (Connelly et al., 2011). In general, the interpretation of the CSR signal can be blurred by the presence of greenwashing activities (Mahoney et al., 2013). Therefore, investors need to carefully analyze signal credibility in terms of signal fit and honesty and determine whether the signal and signaler reflect the true nature of the business.

We propose that family firm status affects signal honesty and ultimately credibility and hence how investors assess CSR signals from family firms in the following specific ways. First, positive CSR signals might be perceived as particularly favorable in the case of family firms because investors might assess such signals as credible and reflecting the true nature and intentions of the family firm (Huang et al., 2019). Family firms are expected to send positive CSR signals due to their commitment to gain the acceptance and approval of their stakeholders and of society at large (Mahoney et al., 2013). Specifically, family firms, in contrast to nonfamily firms, are known to pursue not only financial goals but also nonfinancial goals (Kets de Vries, 1993; Tagiuri & Davis, 1992), including building sustainable connections with stakeholders and enhancing the family’s reputation through the firm (Berrone et al., 2012). Because of their socioemotional wealth considerations, which differentiate family firms from nonfamily firms, family firms are generally associated with socially (Cennamo et al., 2012) and environmentally (e.g., Berrone et al., 2010) friendly activities. While many nonfamily firms also dedicate time and effort to improving their stakeholder relations, leading to improved shareholder evaluations (Hillman & Keim, 2001), family firms have often been associated with extraordinary levels of stakeholder management (e.g., Cennamo et al., 2012; Mitchell et al., 2011) due to their long-term commitment and their community focus (Miller & Breton-Miller, 2005). In other words, family firms might use their family-specific resources (Habbershon & Williams, 1999; Sirmon & Hitt, 2003) to engage in particularly enduring and sustainable CSR activities that are valued by outside shareholders (Maung et al., 2020). As a consequence, we expect that outside investors perceive signals of positive CSR news related to family firms as more legitimate (Deephouse & Jaskiewicz, 2013) than similar signals sent by nonfamily firms and as a more authentic signal of genuine firm strategy and vision rather than a mere outcome of (dishonest) “greenwashing campaigns,” as is often the perception of positive CSR news for nonfamily firms.

Second, we theorize that the lower levels of principal-agent costs in family firms than in nonfamily firms (Chrisman et al., 2004) and the “insider status” of family owners, who know the family firm quality and its intentions very well, also increase the perceived signal credibility and thus lead to overall more positive shareholder assessments of positive CSR news. Given that CEOs in family firms are either intrinsically aligned with the owners’ goals (e.g., through family membership) or closely monitored (in the case of nonfamily membership because of the family owner’s wealth concentration and the resulting incentive and power to engage in close monitoring (Anderson et al., 2003), there is a high level of goal alignment among owners and managers in family firms (Anderson & Reeb, 2003), especially when compared to nonfamily firms. This alignment increases the legitimacy, and thus perceived honesty, of the emitted signal. In other words, CEOs of family firms are more trustworthy than CEOs of other firms when sending CSR-related signals because it is assumed that their CSR is not driven by the self-maximizing motivation of agents, as would be the case in nonfamily firms (Petrenko et al., 2016). As research has shown that investors react positively to an alignment of core beliefs and values with one’s actions (Du et al., 2007)—and hence the authentic demonstration of a firm’s social norms adds value (Godfrey, 2005)—we propose that family firm status enhances outside shareholders’ positive assessment of positive CSR news, as family firm status strengthens signal credibility. In summary, we propose the following:

While research on signals mostly focuses on positive, intentionally sent signals (e.g., Deephouse, 2000), it also acknowledges that firms may send out negative signals (e.g., Fischer & Reuber, 2007), for instance, as byproducts of their strategic activities. We propose that negative CSR news induced, for instance, through cuts in employee programs, the installation of an environmentally unfriendly factory, or governance scandals, are negative signals (unintentionally) sent by firms to outside investors. Extending the arguments proposed for H1a, we suggest that outside investors generally react negatively to signals of negative CSR news (Ramchander et al., 2012). Negative CSR news might be interpreted as a deviation from what is considered socially responsible behavior by the general public, including outside investors, and thus as a signal that lacks fit, as negative CSR news is not correlated with superior firm quality (but rather with low firm quality). Outside investors might also speculate that signals of negative CSR news, which are often associated with cuts in CSR budgets, are a sign of a firm’s latent competitive or financial challenges and might thus signal a lack of firm quality. Hence, outside investors likely react negatively to signals of negative CSR news, as previous CSR literature has revealed (Krüger, 2015), as they interpret such news as a signal of low firm quality, which discourages investment in the respective firm.

We continue to argue that outside investors react even more negatively to a signal of negative CSR news from family firms than to that from nonfamily firms, as they consider such a signal to be particularly inconsistent with the family firms’ expected behavior. The reason is that the public image of family firms consists of being “good stewards” (Neckebrouck et al., 2018) with a focus on social responsibility (Godfrey, 2005). As such, outside investors might assess the negative CSR news of family firms as being in stark contrast to their idiosyncratic goals and values, violating what is considered to be the true essence of the family firm. Given the misfit between the signal (negative CSR news) and what is considered the expected behavior of a high-quality family firm (positive CSR news), investors might refrain from further investing in the respective family firm, as they consider the negative CSR news to be a reflection of inferior family firm quality, assuming that those firms only engage in negative CSR activities if financially forced to do so. The reaction of investors to negative CSR news by family firms is likely stronger than to similar signals from nonfamily firms, as negative CSR news from the former is likely interpreted as an indication that the firm is truly doing badly (given their general stakeholder focus), whereas similar signals from the latter could be interpreted as common strategic decisions.

Moreover, outside investors might even speculate that negative CSR news from family firms is a signal of family firm owners expropriating other investors by maximizing their wealth (e.g., through increased dividend payments) rather than investing in CSR (Sekerci, 2020). For nonfamily firms, given their clear and exclusive focus on economic goals, investors might anticipate short-term-oriented decisions resulting in negative CSR news and thus react less negatively than they would to similar signals from family firms. In sum, as a consequence of perceived nonconforming firm behavior (Miller et al., 2013) and hence a perceived “misfit” between the signal and the expected behavior for high-quality (family) firms, outside investors might assess such signals from family firms even more negatively than those from other firms.

Recession as a Contingency Factor

In the following, we argue that outside investors’ interpretation of signals related to CSR depends on the signaling environment, particularly the overall economic situation. Specifically, we argue that in times of recession, outside investors interpret signals of CSR news from firms opposite to the way described above, and this effect is even stronger in the case of family firms. The economic situation is a particularly important signaling environment, as bad economic situations, such as recessions, increase levels of uncertainty (Davidsson & Gordon, 2016), leading to generally increased information asymmetries (De Haas & Van Horen, 2011) and thus increased importance for emitted signals and the interpretation thereof (Edelman & Yli-Renko, 2010).

In times of recession, which typically come along with liquidity shortages (Garcia-Appendini & Montoriol-Garriga, 2013), the expectations among outside investors of which signals are associated with high firm quality are likely reversed. Specifically, during a recession, outside investors might expect firms to concentrate more on the immediate economic well-being of their firms than on long-term sustainability with regard to stakeholder relationships (Chu & Siu, 2001). In other words, instead of “doing well by doing good,” signals related to positive CSR news in times of recession might be perceived as “doing worse by doing good” (Lins et al., 2013), as they detract the firm’s focus from core business units and divert resources to noncore areas. While signals of positive CSR news might be seen as positively in times of economic prosperity (see H1a), investors might interpret such signals as lacking legitimacy in times of recession because they expect firms to engage in different types of activities, that is, activities that lead to cutting costs and stabilizing revenues (Souto, 2009). In other words, there is a misfit between the signal (i.e., positive CSR news) and the expected behavior (i.e., focusing on firm survival and cutting budgets) when the signaling environment is characterized by recession. Investors might assume that firms are not taking the crisis seriously and hence might be discouraged from investing in firms emitting positive CSR signals in times of recession.

We expect that outside investors’ negative interpretation of signals of positive CSR news during recession is even stronger for family firms. The underlying reason is that the characteristics, and subsequent stereotypes, of family firms lead investors to expect those firms to focus particularly on saving resources (and hence avoiding positive CSR news) in times of recession. Family firms have been found to be more concerned about firm survival and bankruptcy risk than other firms (e.g., Chrisman & Patel, 2012; Kempers et al., 2019) due to the owning families’ socioemotional concerns (Gómez-Mejía et al., 2007) and their wealth concentration (Anderson et al., 2003). Hence, we argue that outside investors might assess signals of positive CSR news from family firms as particularly “noncredible” signals. Given the general expectation that family firms should engage in any action that increases efficiency, reduces costs, and ensures survivability throughout the recession, investors might evaluate positive CSR news from family firms in times of recession as an indication that those firms are not aware of the current situation, lack economic competence at the top, and hence lack overall firm quality. Such expectations among investors likely lead to an overall more negative reaction. In summary, we argue the following:

We further suggest that negative CSR news is not interpreted negatively by outside investors in times of recession. As argued above, in times of recession, firms are expected to focus on their (short-term) stability and survival (van Essen et al., 2013), as recessions are typically associated with a large number of illiquid or overindebted firms that ultimately suffer from insolvency or acquisition (Claessens et al., 2003). Negative CSR news, such as information on cutting voluntary employee benefit programs or voluntary environmental programs that exceed legal standards, signals to investors that the firm takes the required actions to cut costs and increase efficiency. In essence, outside investors likely interpret negative CSR news in times of recession as a signal that firms are aware of the economic situation and are willing to professionally handle the challenges at hand to benefit the firm financially in the short term and, as such, ensure its mid and long-term survival. As a consequence, we suggest that outside investors react positively to signals of negative CSR news in times of recession due to the high levels of perceived signal fit.

We argue that this relationship is even stronger in the case of family firms. As already indicated above, family firms, more than other firms, are incentivized to ensure their long-term survival. Cutting costs through reducing CSR activities—hence emitting signals of negative CSR news—particularly aligns with the behavior that investors expect of high-quality (family) firms in times of recession. As a consequence, outside investors might respond even more favorably to such signals from family firms than to those from nonfamily firms. Moreover, investors typically assume that family owners, despite their positive characteristics such as long-term commitment, are prone to take firm actions that are primarily beneficial to the family (instead of the firm) through increased family reputation, improved stakeholder relationships, and other benefits that might harm outside investors (Villalonga & Amit, 2006). Negative CSR news in times of recession might be interpreted as a clear signal that the family firm prioritizes economic goals in such times (as opposed to nonfinancial goals) and that it possesses experienced and professional management to handle such crises. Thus, investors might perceive negative CSR news from family firms during recession as an even more positive signal of high firm quality than they would for nonfamily firms. Hence, we propose the following:

Methodology

Sample and Data Collection

The dataset includes all firms listed on the French stock market’s SBF120 index of the 120 most actively traded stocks in the French market for at least 1 year in the 2003–2013 period. Due to missing data, the dataset was reduced from 153 initial firms to 133 firms. We used upgrades and downgrades in the Vigéo CSR ratings over the 2003–2013 period to identify positive and negative CSR news, which constitute the independent variables in our event study (see description below). Vigéo is a French-based, internationally active company that was established more than 15 years ago and has adopted a strategy similar to that of credit rating agencies. According to Agefi, Vigéo is the French market leader in ESG research, with 87% of institutional investors using this platform and its updates. Vigéo rates and monitors the CSR of listed companies and immediately changes the firm’s assigned rating if and only if it observes a change in the firm’s CSR. Specifically, Vigéo is an intermediary provider of social performance information (CSR news) that adopts an investor-pay model. Hence, investors pay the agency a fixed cost in exchange for information about the social performance of rated firms. This type of payment model should prevent the rating agency from having any conflicts of interest with the rated entities and should ensure timely updates of the ratings for the investors. Therefore, we assume that investors receive timely and neutral information about the rated entities.

For each firm analyzed, Vigéo provides ratings (on a scale from 0 to 100) regarding six CSR evaluation dimensions (i.e., Environment, Human Resources, Business Behavior, Human Rights, Community Involvement, and Corporate Governance) based on an in-depth evaluation of the subdimensions for each firm. 6 Then, it compares this numerical value for the firm to the sector average. Afterwards, Vigéo categorizes the firm into one of five groups, depending on whether its score is (substantially) higher than, equal to, or (substantially) lower than the mean score of the sector. 7

In addition to Vigéo, Datastream was used as the main source for collecting data on stock market reactions and firm controls. Additionally, we relied on hand-collected information from company websites and annual reports, for example, on family firm status and family CEO status.

Variables

Positive and Negative CSR News

The variable positive CSR news is set to “1” if Vigéo upgraded a firm’s CSR rating and “0” otherwise. Similarly, the variable negative CSR news is set to “1” if Vigéo downgraded the firm’s CSR rating and “0” otherwise. 8

Stock Market Reaction

We used the 21-day cumulative abnormal return (CAR; −10; +10) as the dependent variable (Krüger, 2015), which is in line with the best research practices (e.g., MacKinlay, 1997). This focus on immediate stock market reaction allows us to isolate the effect of positive and negative CSR news on stock values to the most accurate degree possible, avoiding confounding effects (such as those of acquisition or earnings announcements) as much as possible. We also included days prior to the event to capture the possibility that the information had leaked to the market prior to the event—an assumption that is quite common in event studies (e.g., Kothari & Warner, 2007; MacKinlay, 1997; Riley et al., 2017). Following MacKinlay (1997) and Krüger (2015), we also computed alternative event windows ([−5; +5]; [0; +5]; [0; +10]) and used them in our robustness checks.

Family Firm

We used a dummy variable to code family firms (“1”) relative to other types of organizations (“0”). Following the extant literature (e.g., Sraer & Thesmar, 2007), we categorized firms as family firms if one or more individuals connected by either blood or marriage, jointly or subsequently, possess at least 20% of the firm’s equity. 9 When coding this variable, we scrutinized firms with single individual owners to obtain information on potential predecessors involved in the firm or family members involved in management in order to identify and exclude lone-founder firms. 10 This approach is in line with the procedure proposed by Maury (2006) as well as Isakov and Weisskopf (2014).

Recession

We focused on the liquidity aspect of the financial recession that occurred during our study period, that is, the liquidity shock that the financial recession caused, as we argue that a liquidity shock can threaten the survival of a family empire. Therefore, we considered the starting point of the financial recession by taking the liquidity situations of French listed companies into account. Following the definitions from the literature (Chudik & Fratzscher, 2011; Garcia-Appendini & Montoriol-Garriga, 2013), we defined the starting point of the financial recession as August 2007 because the liquidity situations of firms substantially deteriorated at that point in time. Following Barron et al. (2012), we considered December 2009 as the end of the recession in France. Hence, we coded the dummy variable “recession” as “1” if a positive or negative CSR news event occurred between August 2007 and December 2009 and “0” otherwise.

Control Variables

Following the extant literature (e.g., Krüger, 2015), we controlled for the following variables that might affect a firm’s stock value. Leverage is measured as total debt over total assets. ROA (return on assets) is measured as net income over total assets. Liquidity is measured as cash over total assets. Size is measured as the logarithm of market capitalization. Moreover, we control for industry using two-digit SIC codes. We also included two further control variables to reflect the firm’s CSR history, as investors’ reaction to positive and negative CSR news might depend on the firm’s past CSR (Godfrey et al., 2009): (a) the firm’s global CSR rating (“GlobalCSR_Rating”) as provided by Vigéo (scale from 0 to 100) and (b) a dummy variable to demonstrate whether the firm is included in the ASPI (Advanced Sustainable Performance Indices) Eurozone index, an index that is created by Vigéo. ASPI is one of the leading sustainability indices in Europe, and hence, firms that belong to the list of top European CSR firms are included in it. “ASPI_CSR_Index” is a binary variable taking on the value “1” if the firm is included in the index and “0” if not.

Empirical Findings

Descriptive Statistics

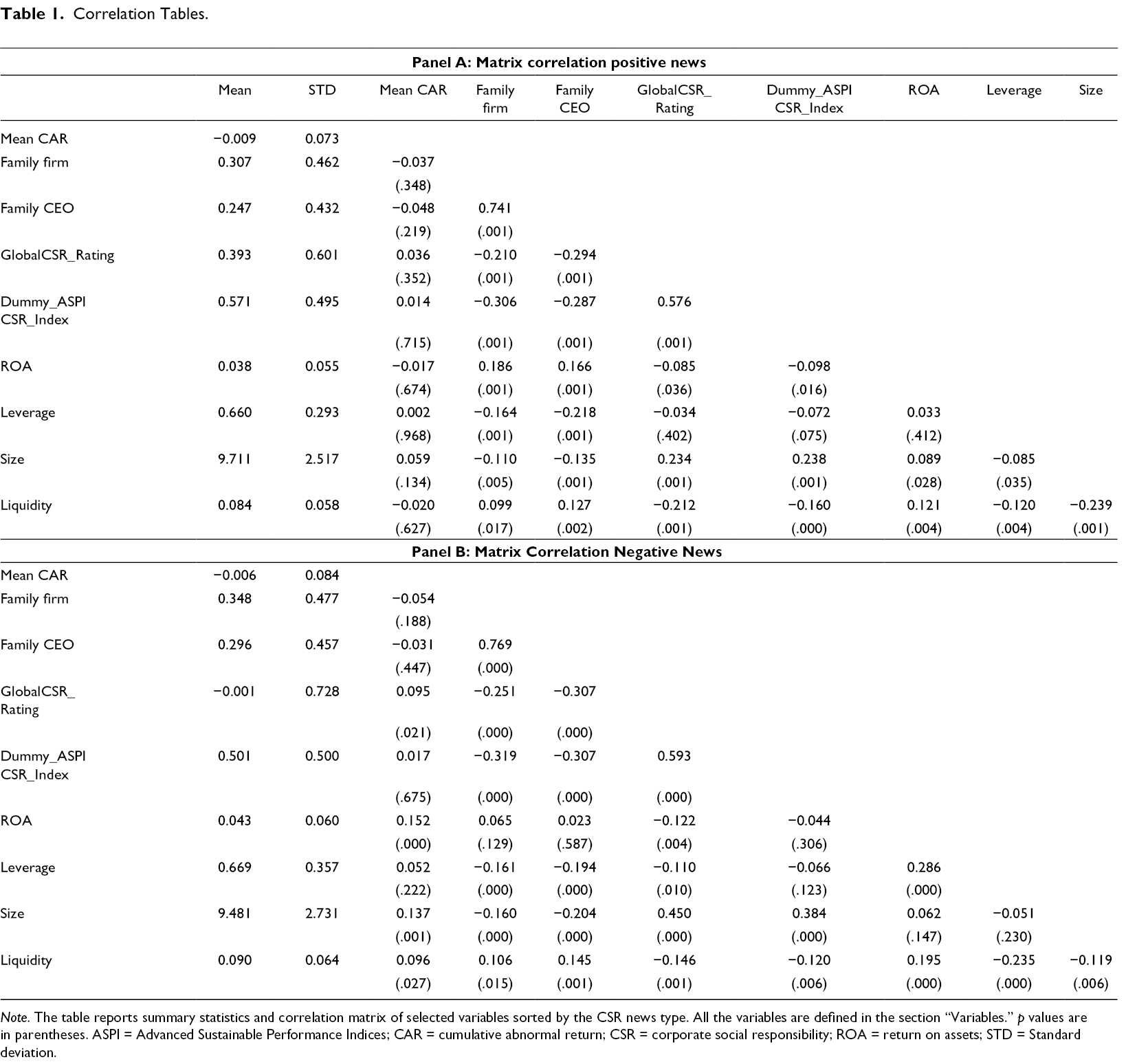

Table 1 provides the correlations among our variables. In our sample, we have 661 positive changes in the CSR ratings and 586 negative changes in the CSR ratings. The percentage of family firms with positive or negative CSR news (over the studied time period, an average of 35% of firms with negative CSR news and 31% of firms with positive CSR news were family firms), is in line with the general numbers regarding family firm presence on stock markets (La Porta et al., 1999).

Correlation Tables.

Note. The table reports summary statistics and correlation matrix of selected variables sorted by the CSR news type. All the variables are defined in the section “Variables.” p values are in parentheses. ASPI = Advanced Sustainable Performance Indices; CAR = cumulative abnormal return; CSR = corporate social responsibility; ROA = return on assets; STD = Standard deviation.

Empirical Model

We employed an event study methodology (Arya & Zhang, 2009; Krüger, 2015; Ramchander et al., 2012) to estimate stock market reactions to positive and negative CSR news. We therefore follow the classic MacKinlay (1997) study and use an estimation window of 120 trading days from t-140 to t-20, with the event date set to the date when Vigéo announced the CSR rating news. In our multivariate analyses, we included industry and year fixed effects to control for any industry- and year-specific factors that could affect stock market reactions. Accordingly, our model investigates the cross-sectional variation in the sample. In other words, following the family firm literature (e.g., Anderson & Reeb, 2003; Isakov & Weisskopf, 2014; Sraer & Thesmar, 2007), we do not use firm fixed effects in our model since the variation in the family variable over time is limited. Moreover, we control for heteroskedasticity using heteroskedasticity-robust standard errors (Huber–White standard errors).

Market Reaction to Positive and Negative CSR News: Regression Analyses

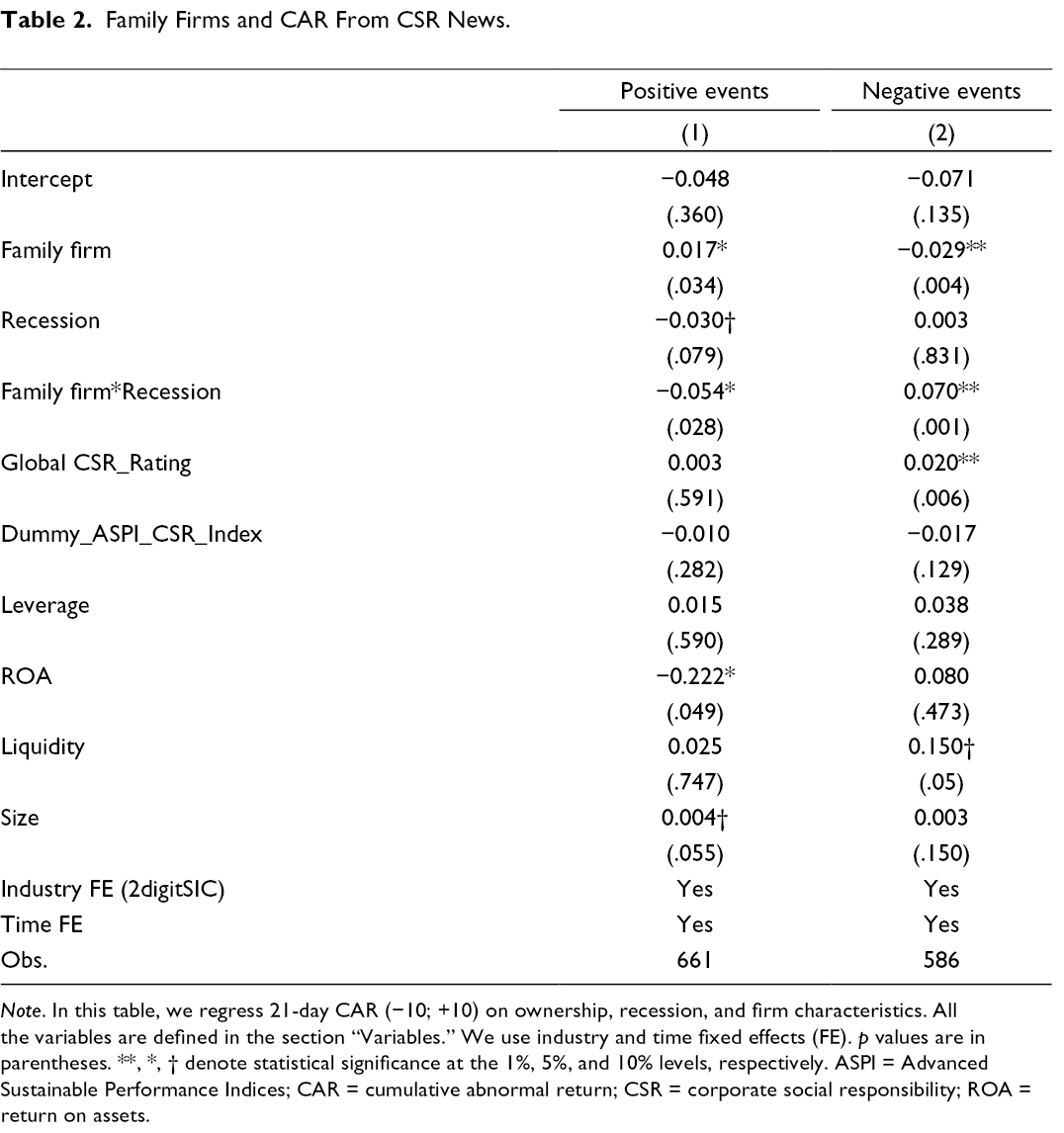

In this section, we tested the hypotheses with multivariate regressions. The results are presented in Table 2. Hypothesis 1a proposes that in general, investors react more positively to positive CSR news from family firms than to that from other firms. In Model 1, we find a positive and significant relationship (β = .017, p = .034), which supports H1a. The negative and significant coefficient (β = −0.029, p = .004) on the family firm variable in Model 2, the negative event regression, supports the claim in H1b that investors react more negatively to negative CSR news from family firms than to similar news from other firms.

Family Firms and CAR From CSR News.

Note. In this table, we regress 21-day CAR (−10; +10) on ownership, recession, and firm characteristics. All the variables are defined in the section “Variables.” We use industry and time fixed effects (FE). p values are in parentheses. **, *, † denote statistical significance at the 1%, 5%, and 10% levels, respectively. ASPI = Advanced Sustainable Performance Indices; CAR = cumulative abnormal return; CSR = corporate social responsibility; ROA = return on assets.

The interaction between family firm and recession in Model 1 (β = −0.054, p = .028) shows that positive CSR news from family firms during a recession is perceived more negatively by investors, providing support for H2a. Moreover, the interaction term in Model 2 in Table 2 (β = .070, p = .001) shows that negative CSR news from family firms during a recession is perceived more positively by investors, thus supporting H2b.

Robustness Tests

In this section, we conducted a series of tests to ensure the robustness of our findings.

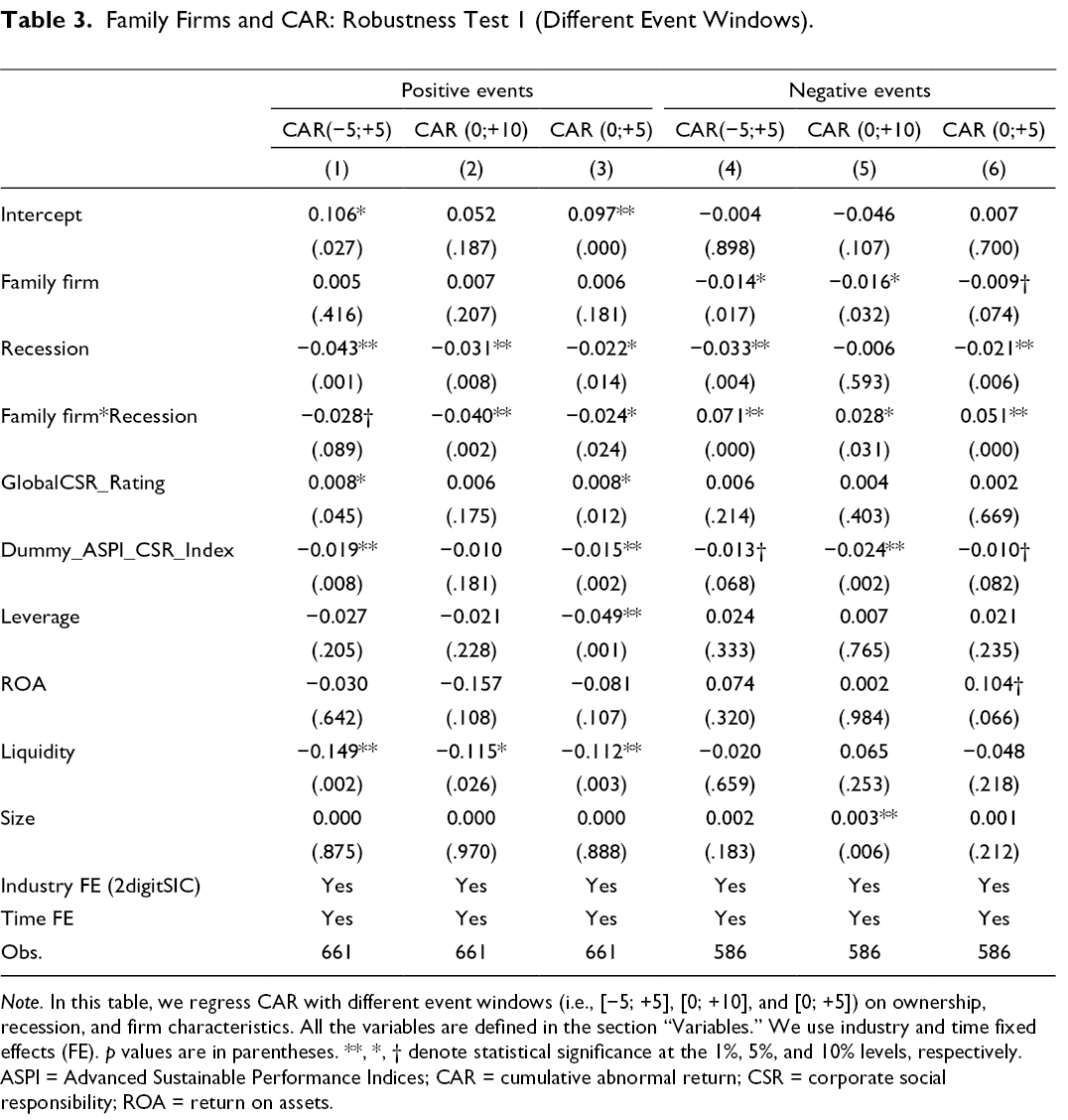

First, we used alternative event windows for our CAR (Table 3). Following MacKinlay (1997) and Krüger (2015), we used (−5; +5) as an alternative event window to examine the possibility that the reaction was more concentrated around the event. We also tested windows of (0; +10) and (0; +5) to allow for the possibility that the information may not have leaked to the market prior to the news release. The results presented in Table 3 are overall in line with those of the main analyses, with the exception of H1a, which is not supported when we narrow the portion of the event window that is prior to the event. This suggests that investors anticipate positive CSR news because such news may be “less unexpected,” and they react to it slightly earlier. One potential source of such leakage is employees involved in the respective firm decisions (e.g., a decision to increase investment in environmentally friendly production) or informed by firm-internal announcements who talk about such firm behavior before the change is officially communicated to the external world and, hence, before Vigéo updates its rankings. The empirics show that such a leakage effect is stronger for positive CSR news than for negative CSR news. One interpretation of this finding is that firms encourage their stakeholders, in particular their employees, to communicate about positive CSR behavior but urge them to remain silent about negative CSR behavior.

Family Firms and CAR: Robustness Test 1 (Different Event Windows).

Note. In this table, we regress CAR with different event windows (i.e., [−5; +5], [0; +10], and [0; +5]) on ownership, recession, and firm characteristics. All the variables are defined in the section “Variables.” We use industry and time fixed effects (FE). p values are in parentheses. **, *, † denote statistical significance at the 1%, 5%, and 10% levels, respectively. ASPI = Advanced Sustainable Performance Indices; CAR = cumulative abnormal return; CSR = corporate social responsibility; ROA = return on assets.

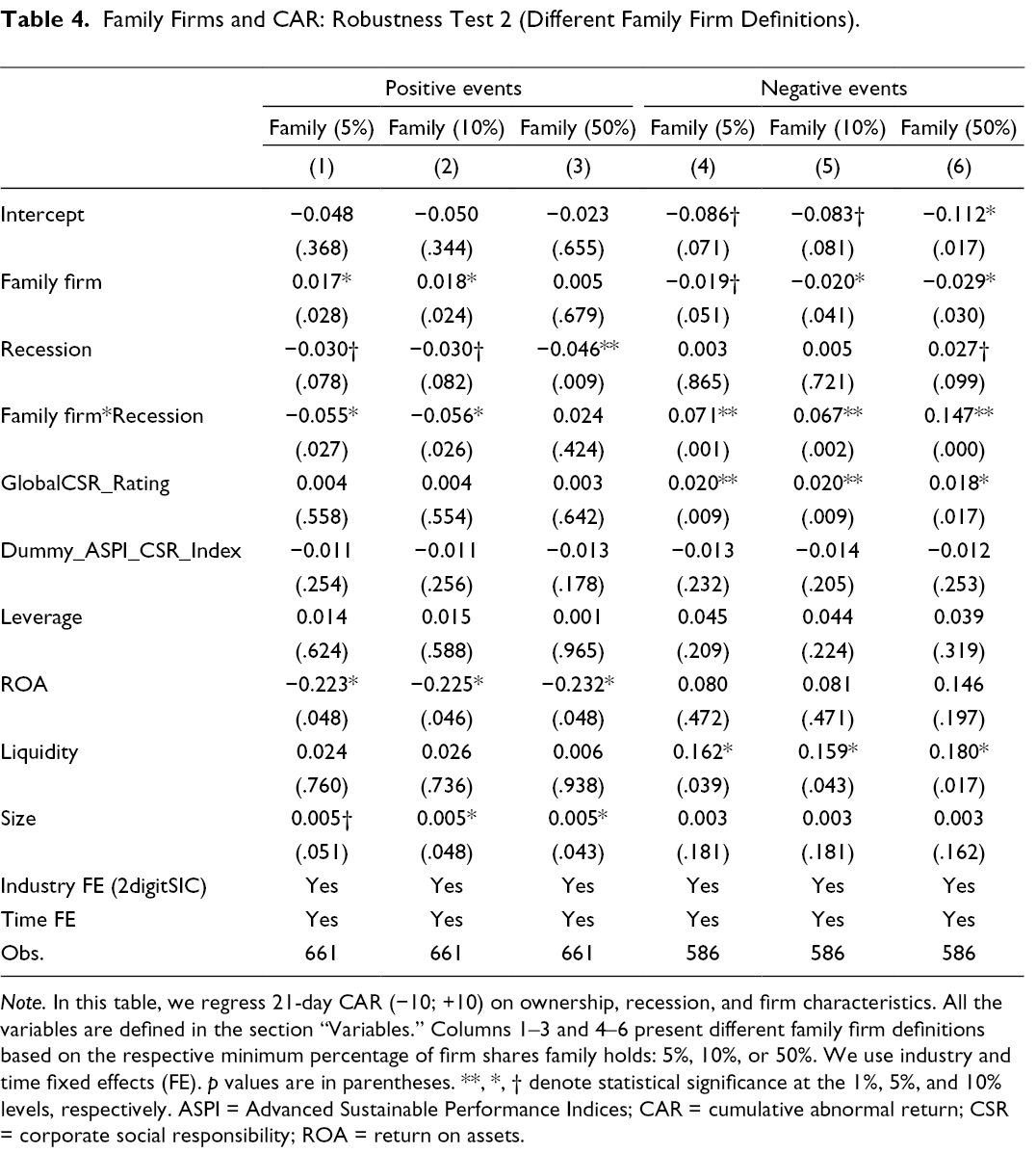

Second, we checked whether our results are contingent on the specific definition of family firm used. In Table 4, we reestimated our models by using alternative ownership thresholds for the family firm variable. Specifically, we employed 5% and 10%, which are other frequently used blockholder thresholds, as well as 50%, which is the majority threshold, thereby following prior research (e.g., Maury, 2006; Miller et al., 2007; Sacristán-Navarro et al., 2011). The results of these tests, as shown in Table 4, reveal that our models remain stable for ownership cutoffs below the majority stake. This finding shows that investors, when interpreting signals, are indifferent regarding the size of the ownership stake the family possesses—as long as there are substantial shares in the hands of outside investors. Interestingly, as soon as the family owns the majority of the firm, investors’ assumptions about family owners’ underlying quality and intentions alter. This finding is also very much in line with the premise of Franks and Mayer (2001) that 25% and 50% are critical control levels and that the owner’s power between these critical points provides similar levels of control over firm decisions.

Family Firms and CAR: Robustness Test 2 (Different Family Firm Definitions).

Note. In this table, we regress 21-day CAR (−10; +10) on ownership, recession, and firm characteristics. All the variables are defined in the section “Variables.” Columns 1–3 and 4–6 present different family firm definitions based on the respective minimum percentage of firm shares family holds: 5%, 10%, or 50%. We use industry and time fixed effects (FE). p values are in parentheses. **, *, † denote statistical significance at the 1%, 5%, and 10% levels, respectively. ASPI = Advanced Sustainable Performance Indices; CAR = cumulative abnormal return; CSR = corporate social responsibility; ROA = return on assets.

We further checked the robustness of our findings to any potential confounding effects. To this end, we manually searched the Factiva database for events occurring during the CSR news event windows that might also affect firm value, such as M&A as well as earnings and dividends announcements and updates (following the best practices in the literature: El Nayal et al., 2021; McWilliams & Siegel, 1997). To identify newspaper articles about confounding events in Factiva, we performed searches in both the French and English languages by using the name of the firm and various key words. Specifically, we selected the company and the dates (of the respective event windows) and entered one of the following keywords: “mergers and acquisitions,” “M&A,” “earnings,” or “dividends.” We repeated this process for all the firms in our sample. In total, we identified 73 negative and 109 positive changes in the CSR ratings that might be contaminated by confounding events. To ensure that market reactions were not confounded by these firm-specific events, we ran additional calculations excluding all positive and negative CSR news that overlapped with one of the previously identified event windows for positive or negative CSR news (detailed analyses available from the authors upon request). The results of our regressions overall remain stable after the exclusion of these potentially contaminated observations, with the exception of those that support H1a, which become insignificant. This result might be explained by humans’ general tendency to react more strongly to negative news than to positive news (Soroka, 2006).

Post Hoc Test: Family CEO as a Contingency Factor

Next, we scrutinize whether stock market reactions to signals of positive and negative CSR news depend not only on who owns the firm but also on who runs the firm (Breton-Miller & Miller, 2016; Martínez-Ferrero et al., 2016). Prior research has noted that investors might perceive signals sent by family-member managers differently from those sent by nonfamily managers (Chandler et al., 2019; Duncan & Hasso, 2018). Moreover, such a post hoc test is in line with recent calls for more research on family firm heterogeneity (e.g., Chua et al., 2012; Neubaum et al., 2019) and the research showing that family firms’ CSR is dependent on whether the CEO of a family firm is a family member (Cui et al., 2018). We used binary variables to distinguish family CEOs from nonfamily CEOs working in family firms (e.g., Anderson & Reeb, 2003; Sraer & Thesmar, 2007).

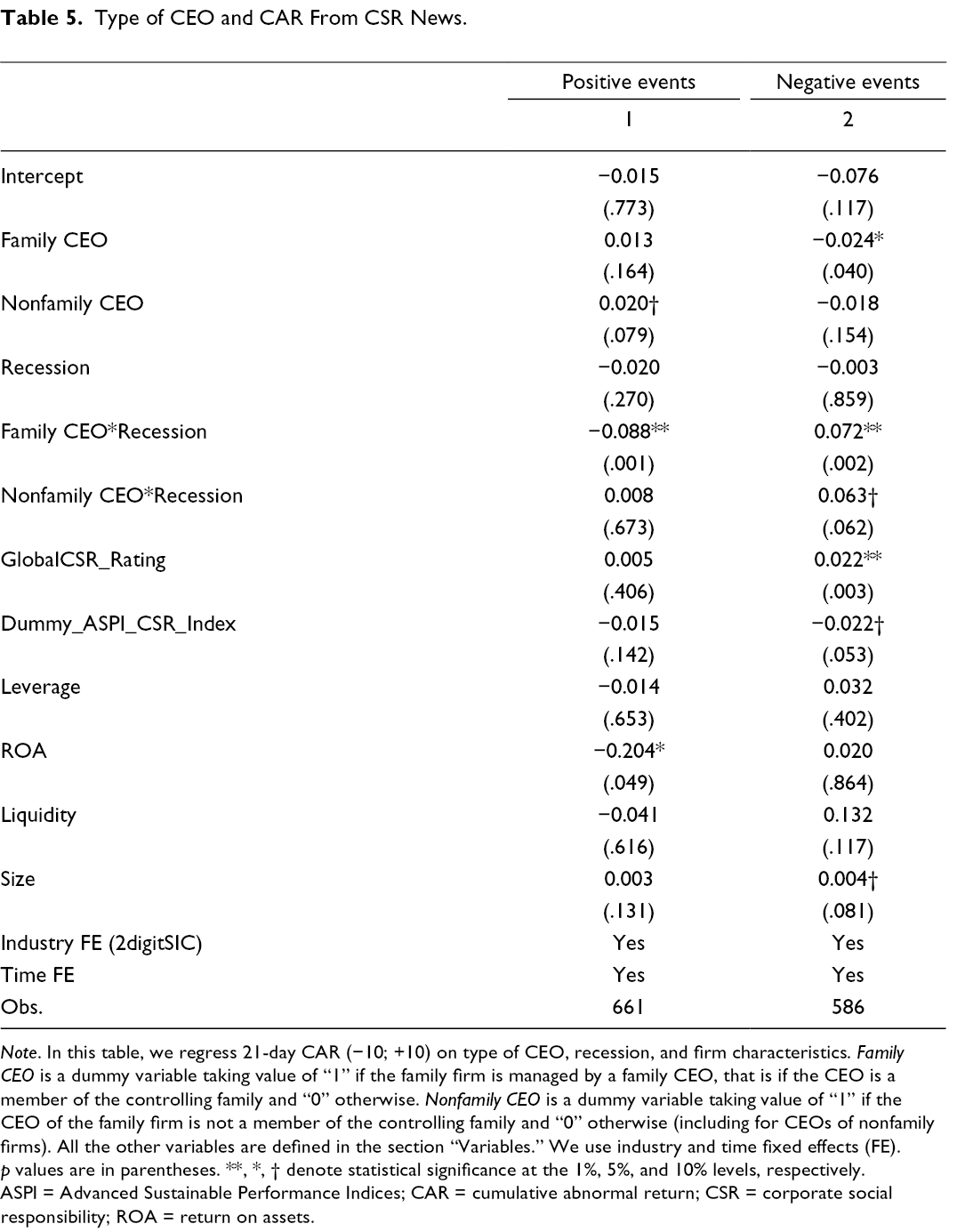

Table 5 reports the results. First, Model 1 shows that investors react more positively to positive news from family firms run by a nonfamily CEO (β = .020, p = .079), while the family CEO dummy is insignificant. Model 2 shows that markets react more negatively to negative CSR news from family firms if the CEO is a family member (β = −0.024, p = .040). The interaction terms in Model 1 show that in times of recession, the stock market reacts more negatively to positive CSR news if the CEO is a family member (β = −0.088, p = .001). Moreover, Model 2 reveals no differences in the interaction terms between family and nonfamily CEOs and recession with regard to negative CSR news, as both interaction coefficients in Model 2 are positive and significant with similar effect sizes that are not significantly different from each other.

Type of CEO and CAR From CSR News.

Note. In this table, we regress 21-day CAR (−10; +10) on type of CEO, recession, and firm characteristics. Family CEO is a dummy variable taking value of “1” if the family firm is managed by a family CEO, that is if the CEO is a member of the controlling family and “0” otherwise. Nonfamily CEO is a dummy variable taking value of “1” if the CEO of the family firm is not a member of the controlling family and “0” otherwise (including for CEOs of nonfamily firms). All the other variables are defined in the section “Variables.” We use industry and time fixed effects (FE). p values are in parentheses. **, *, † denote statistical significance at the 1%, 5%, and 10% levels, respectively. ASPI = Advanced Sustainable Performance Indices; CAR = cumulative abnormal return; CSR = corporate social responsibility; ROA = return on assets.

Discussion

Employing an event study by using data on French listed firms from 2003 to 2013, we investigate stock market reactions to signals of positive and negative CSR news regarding family versus nonfamily firms. We find that, as hypothesized, the stock market reacts more positively to signals of positive CSR news and more negatively to signals of negative CSR news from family firms than to similar news from nonfamily firms. In times of recession, however, outside investors react more negatively to positive CSR news and more positively to negative CSR news from family firms than to similar news from other firms. Our study makes several contributions to the literature.

First, we contribute to the emerging debate about whether and why outside investors might react differently to signals from family firms than to similar signals from nonfamily firms (e.g., André et al., 2014; Chang et al., 2010; Wong et al., 2010). We argue that due to family firms’ idiosyncrasies, outside investors hold specific beliefs about what is legitimate and authentic for those firms, specifically with regard to their expectations for CSR. Thus, the signal credibility of CSR news is different for family firms than for nonfamily firms. While prior research has primarily focused on the impact of family firm idiosyncrasies on firm behavior (e.g., Chrisman & Patel, 2012; Duran et al., 2016), we reveal that outsiders’ expectations about family firm behavior differ from their expectations about other types of firms, impacting how signals from those firms are interpreted. In general, outside investors value the stakeholder-oriented behavior of family firms, given family firms’ intrinsic focus on various stakeholders (Cennamo et al., 2012; Mitchell et al., 2011); as such, they perceive positive CSR news as a very credible signal of firm quality. During a recession, however, outside investors may assess prudent CSR budget cuts as appropriate due to family firms’ parsimony (Carney, 2005) and wealth concentration considerations (Gómez-Mejía et al., 2011).

Second, we advance the extant research by investigating the consequences of positive and negative CSR news related to family firms. Prior research has predominantly focused on whether family firms engage in more or fewer CSR activities than other types of firms (e.g., Berrone et al., 2010; Dyer & Whetten, 2006; Richards et al., 2017) and has revealed the antecedents of such engagement (e.g., Breton-Miller & Miller, 2016; Déniz & Cabrera-Suárez, 2005; Niehm et al., 2008). We take this research one step further by studying the consequences of CSR engagement for family firms. In particular, we show that the stock market interprets signals of family firms’ CSR in a particularly strong way and reacts negatively to negative CSR news from family firms in general and negatively to positive CSR news from family firms during recessions. Moreover, we illustrate that outside investors react positively to positive CSR news from family firms in general and positively to negative CSR news from family firms during recessions. Hence, we find a “preference reversal” among outside investors when the signaling environment is characterized by recession (Giannarakis & Theotokas, 2011) because investors might have different perceptions of “signal fit” at those times.

Moreover, we contribute to research disentangling family firm heterogeneity (Chua et al., 2012; Neubaum et al., 2019) by explaining how signals from firms led by a family CEO are interpreted differently from those of other firms, including those that are owned but not led by family members. Since CSR is an investment decision that is made by managers, investors might value CSR signals differently depending on who manages the firm. Interestingly, the results of our post hoc test reveal that outside investors react slightly more positively to signals of positive CSR news when nonfamily CEOs run family firms. We might speculate that the combination of positive CSR news from family firms and the presence of a nonfamily CEO signals an authentic stakeholder orientation (due to the family firm character; Mitchell et al., 2011), while at the same time signaling a potential business case and thoughtful economic considerations, given the professional nature of the nonfamily CEO (Stewart & Hitt, 2012), overall suggesting high levels of signal credibility.

Our results further reveal that, in the case of family CEOs, the stock market reacts more negatively to negative CSR news. Prior research has emphasized family CEOs’ emotional attachment to their family firms, their stock of personal socioemotional wealth (Zellweger et al., 2012), and their identification with the family firm (Davis et al., 1997), which might, in conjuncture, lead to an increased focus on stakeholder management (Kammerlander & Ganter, 2015). As such, outside investors might consider negative CSR news from firms led by a family CEO to be particularly illegitimate and hence lacking in signal credibility, ultimately leading to lower stock valuations. The results of our post hoc test further reveal a significantly more negative outside investor reaction to signals of positive CSR news from firms led by family CEOs during recessions. Positive CSR news during recessions from firms with family CEOs might be considered to reflect a lack of managerial cognition of the extant challenges, potentially a lack of managerial competencies, and family shareholders’ neglect of the interests of other minority shareholders (Anderson et al., 2009). Indeed, investors might anticipate family CEOs’ tendency to expropriate minority shareholders through mechanisms such as tunneling (Burkart et al., 2003; Morck et al., 2005), especially in times of crisis (Johnson et al., 2000). The anticipation of expropriation behavior during times of recession might increase the perceived “misfit” between the signals sent and what investors would assess as appropriate firm actions.

Further contributing to insights on family firm heterogeneity, we could not identify different results when applying various alternative blockholder threshold cutoffs. These results indicate that investors share stereotypes about family firms irrespective of the actual equity stake in the family’s hands. Interestingly, our results also show that the significant reactions to positive CSR news vanish for families with majority control. One might expect that due to the extraordinary wealth concentration in such cases, outside investors would tend to assume that family shareholders consistently pursue specific stakeholder-oriented approaches. Moreover, our results show significant influence from a firm’s prior CSR. Somewhat surprisingly, there is a positive correlation between high CSR ratings and reactions to negative CSR news (Table 2). One might speculate that investors favor moderate-high levels of CSR yet punish extraordinarily high values, following research that investors, as risk-averse decision-makers (Markowitz, 1952), favor moderate over extreme decisions. Additionally, the results of Table 2 illustrate that firms with higher firm performance experience substantially fewer positive reactions to their positive CSR news. One could assume that in such cases of recent overperformance, investors might dislike CSR efforts, viewing them as temporary greenwashing activities and hence attributing lower credibility to signals from these firms.

Last, our study also contributes to a better understanding of how outside investors react to positive and negative CSR news. Generally, our regression analyses reveal insignificant intercepts for both positive and negative CSR news (Table 2), which is in line with the previous findings of Capelle-Blancard and Petit (2019) and Fernandez-Izquierdo et al. (2009). Moreover, our research findings contribute to the disentanglement of the stock market implications of CSR by showing that investors’ reactions to such news substantially depend on factors that affect signal credibility (such as family firm status) or determine the signaling environment (i.e., the economic situation) and thus the signal fit (Jaskiewicz et al., 2020). As such, we inform and advance the current CSR debate by shifting it toward a discussion of contingency factors rather than a question of general directionality. In particular, our findings about preference reversals (i.e., different expectations of outside investors regarding what is legitimate during recessions) provide important insights into why current studies might have found inconclusive results when studying stock market reactions to positive or negative CSR news: to fully understand investors’ CSR preferences, the context of the firm and its environment need to be considered.

Our study also reveals relevant implications for practice. First, when considering the pursuit of CSR activities, family firms need to not only think about the implications for firm-internal and firm-external stakeholders but also to consider the potential impact on their stock market evaluation. Firm decision-makers need to further reflect upon the financial situation of the firm as well as firm leadership when making decisions to intensify (or downgrade) their CSR activities. Taking outside investors’ perceptions of CSR news into account is important, as it affects the family firm’s stock price, smooths or complicates its access to further equity, and indirectly determines the family firm’s reputation as well as power in negotiations, such as with banks. Despite the oft-circulated myth that investors mainly care about financial returns, our findings reveal a different and more nuanced picture: especially for family firms, and outside of recessions, outside investors do indeed value “good corporate citizenship.” Our findings might also help family firm decision-makers in their communications. Specifically, while positive CSR news should be promoted heavily during “good economic times,” as it is specifically valued by outside investors and might even lead to a competitive advantage for family firms, family firms are advised to remain rather silent about their CSR news in times of recession.

Limitations and Areas for Further Research

Our study has several limitations, most of which open up fruitful areas for further research. First, we relied on a sample from a single country and a single—albeit renowned—CSR rating agency. Researchers might investigate whether our results are generalizable to other contexts (Banalieva et al., 2015; Duran et al., 2019), which might differ with regard to what outside investors perceive as credible CSR signals. Second, in line with prior studies (e.g., Francis et al., 2008; Karpoff et al., 2008; Krüger, 2015; Maung et al., 2020), we relied on an event study methodology to carve out the specific effect of signals of CSR news on stock market valuation. Future studies might take further accounting and other market measures into account. In particular, it would be appealing to study long-term performance benefits and answer the question of whether some firms, such as family firms, are better able to align shareholder and stakeholder needs in the long run. Moreover, researchers might shift their attention to other nonfinancial consequences of CSR news, such as CEO dismissal (Hubbard et al., 2017) and employee workplace behavior (Flammer & Luo, 2017).

Additionally, researchers might advance our scholarly knowledge by focusing on the heterogeneity among family firms with regard to their effect on signal credibility. For instance, researchers might focus on whether public knowledge about conflicts and bifurcation biases (Verbeke & Kano, 2012) affect how shareholders evaluate family firms’ CSR news. Other factors to include in further analyses might comprise eponymy, the length of the family firm’s history, or the family firm image, all of which might have an effect on signal credibility. Moreover, future studies might consider whether and how a strong focus on values (Rau et al., 2019) or socioemotional wealth in publicly available documents might influence investors’ interpretation of CSR signals. Another interesting research avenue to pursue in future studies is the differentiation among various types of CSR news, relating, for instance, to ecological, social, or governmental issues or distinguishing between primary and nonprimary stakeholders (Hillman & Keim, 2001). Moreover, it would be interesting to shed light on other dominant owner types, such as institutional owners (Johnson & Greening, 1999; Saleh et al., 2010) or state-owned firms (Li & Zhang, 2010).

Our study reveals that outside investors react to signals of positive and negative CSR news from family firms differently from similar signals from nonfamily firms. This opens up the interesting research lacuna of determining which behaviors outside investors generally consider to be particularly legitimate and authentic for family firms beyond CSR. Prior research has revealed certain stereotypes regarding family firm behavior held by, for instance, job seekers (Block et al., 2019) or potential customers (Andreini et al., 2020). In addition, research has revealed that listed family firms tend to behave in a particularly conforming manner (Miller et al., 2013). Given that our study shows that outside investors’ expectations of the legitimate and authentic behavior of family firms might differ from their expectations regarding nonfamily firms, it would be of utmost interest to the family firm community to scrutinize which family firm actions are considered desirable (or credible) signals by outside investors.

Additionally, further studies investigating the consequences of negative stock market reactions to family firms would be fruitful. While some studies have highlighted the conformist behavior of family firms (Miller et al., 2013), others have stressed the long-term orientation of those firms (e.g., Lumpkin & Brigham, 2011), their independence (Koenig et al., 2013), and their patient capital (Sirmon & Hitt, 2003). Hence, qualitative and quantitative studies of family firms’ reactions to negative stock market reactions might be insightful.

Conclusion

Outside investors have specific expectations about family firms; their beliefs about what signals indicate legitimate and authentic firm actions with regard to CSR might differ for family versus nonfamily firms. We theoretically argue and empirically reveal that outside investors react more strongly to signals of positive and negative CSR news from family firms than to similar signals from nonfamily firms and that their reactions depend crucially on the signaling environment, particularly the economic situation, as well as on whether the firm is managed by a family or nonfamily CEO. We hope that our theorizing and testing will encourage fellow scholars to tackle the multitude of extant research lacunas in this area.

Footnotes

Appendix 1: Dimensions and Subdimensions of the Vigéo CSR Rating

Acknowledgments

We thank Jean-Luc Arregle, Miriam Bird, Melanie Richards, and Pengxiang Zhang for helpful comments on earlier versions of this manuscript.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Notes

Author Biographies

Naciye Sekerci holds a PhD in Corporate Finance from Lund University, Sweden. Her expertise lies in the field of Corporate Finance, Corporate Governance, Environmental, Social and Governance (ESG) Factors, and Sustainability.

Jamil Jaballah

Marc van Essen (PhD, Erasmus University) is a Professor of International Business at the Darla Moore School of Business, University of South Carolina. His research interests include comparative corporate governance, international business, family business, and meta-analytic research methods.

Nadine Kammerlander is a Professor of Family Business at WHU – Otto Beisheim School of Management, Germany, where she also serves as Director of the institute of family business and mittelstand. Nadine is Editor of Family Business Review and serves on the review boards of multiple academic and practice-oriented journals. Her work has been published, amongst others, in journals such as AMJ, AMR, JMS, ETP, JBV, JPIM, SBE, FBR, and JFBS. Moreover, she has received numerous awards for her research such as the Latsis Prize and the Carolyn Dexter Best International Paper Award. Nadine was named a “Top 100 Family Influencer” by Family Capital in 2020.