Abstract

Current research suggests that entrepreneurship in the family business context is mainly induced by top-down firm-level activity. We propose that entrepreneurial activity is also initiated autonomously as a bottom-up process by individual members or a group of individual members of an entrepreneurial family (EF). Building on 63 interviews with EF members involved in 39 venturing cases, we reveal a set of unique motives driving the venturing activity and show how these motives are intertwined with six heterogeneous family venture types. We also emphasize how positioning (i.e., inside or outside of family firms’ boundaries), family support, emotional attachment, and transgenerational intention vary among the different venture types.

Keywords

Introduction

Corporate entrepreneurship commonly refers to entrepreneurial activity by individuals or a group of individuals, in association with an existing firm, that often results in new venture creation (Sharma & Chrisman, 1999) and is initiated for a variety of reasons, including adapting firms’ offerings to environmental change and expanding the firm’s scope into new business areas of strategic importance to develop and sustain competitive advantage (Covin & Miles, 1999; Miles & Covin, 2002; Zahra & Covin, 1995). Corporate entrepreneurship is particularly important to family firms since they frequently strive to create value not only in the present but also for future generations (Cruz & Nordqvist, 2012; Habbershon & Pistrui, 2002). Not surprisingly, scholarly interest in family firm corporate entrepreneurship has increased in recent years (Bettinelli et al., 2017; Jaskiewicz et al., 2015; Kellermanns & Eddleston, 2006; Minola et al., 2016; Ramírez‐Pasillas et al., 2021). The literature has suggested that family firms engage in corporate entrepreneurship to enable the persistent involvement of multiple generations in the business, to develop portfolio entrepreneurship, and to foster transgenerational entrepreneurship (Habbershon & Pistrui, 2002; Jaskiewicz et al., 2015; Marchisio et al., 2010; Sieger et al., 2011) through the establishment of internal and external new ventures (Brumana et al., 2017; Minola et al., 2016; Ramírez‐Pasillas et al., 2021).

In fact, various methods of new venture creation can exist in the context of family businesses comprising the family firm, the family, and the individual family members (Chrisman et al., 2003; Habbershon et al., 2003). So far, most studies have focused on analyzing entrepreneurship from the perspective of family firms as a formal, top-down firm-level activity (e.g., Bettinelli et al., 2017; Nordqvist & Melin, 2010; Randolph et al., 2017; Zahra, 2005). This view, however, overlooks informal, autonomous bottom-up entrepreneurial activity by individual members of an entrepreneurial family (EF), that is, an “institution, or social structure, that can both drive and constrain entrepreneurial activities” (Nordqvist & Melin, 2010, p. 214). Hence, much remains to be understood about how and why new ventures are initiated by EF members and what these ventures look like. Indeed, the drivers causing members of EFs to create new ventures individually or as a group instead of continuing or starting to work in the existing family firm have, so far, been overlooked by prior research, resulting in a knowledge gap on venturing motives within and across multiple family generations (Michael-Tsabari et al., 2014; Minola et al., 2016; Zellweger, Nason, et al., 2012). Moreover, little is known about how venturing motives are intertwined with the types of new ventures created by EF members (Michael-Tsabari et al., 2014; Zellweger, Nason, et al., 2012).

In an effort to examine newly created ventures of EF members, we address the following research questions: (1) Why do EF members engage in the creation of new ventures? and (2) How do the motives driving entrepreneurial activity relate to the resulting family venture type? Our study is based on the analysis of data from 63 in-depth interviews with members of 24 EFs involved in 39 venturing cases, as well as substantial firm-related material (e.g., websites, press releases, internal documents). The findings of our study contribute to the literature in three ways. First, regarding research on corporate entrepreneurship in family-influenced firms (Kellermanns & Eddleston, 2006; Minola et al., 2016), we offer new insights into the antecedents of informal, autonomous bottom-up entrepreneurial activity by EF members that highlight aspects unique to the family business context. Specifically, we identified six motives that encouraged EF members to engage in entrepreneurial activity: preserving the entrepreneurial mindset, sustaining family harmony, finding family fit, qualifying as successor, facilitating succession, and emancipation from the EF. Second, regarding research on family entrepreneurship (Habbershon & Pistrui, 2002; Habbershon et al., 2010; Ramírez‐Pasillas et al., 2021; Zellweger, Nason, et al., 2012), we show that entrepreneurial activity of EF members is not necessarily driven by the EF as a monolithic entity, but often by individual EF members who create new ventures together with nonfamily co-founders or selected members of the EF, albeit often triggered at the level of the family (e.g., by motives such as sustaining family harmony or qualifying as successor). Thus, we provide a more nuanced understanding of how EF members create their own new ventures. Third, we contribute to the broader family business research, particularly to a better understanding of differences between nonfamily business and family business contexts as well as of family firm heterogeneity (Chua et al., 2012). An important distinction is the identified motives for entrepreneurial activity, which in the family business context is as much about noneconomic goals (e.g., sustaining family harmony) as about economic goals, such as financial performance or competitive superiority of the firm (Covin & Miles, 1999; Zahra & Covin, 1995). In addition, we show how EF members’ idiosyncratic venturing motives lead to heterogeneous venturing outcomes and propose a family venturing model. We identified six different family venture types: preserver, innovator, conqueror, benefactor, explorer, and autonomous investor. We also underscore how positioning (i.e., inside or outside of the family firms’ boundaries), family support, emotional attachment, and transgenerational intention vary among the identified family venture types and suggest that the development of newly created ventures by EF members may be influenced by these dimensions, which are unique (except positioning) for family business contexts compared to nonfamily business contexts.

Theoretical Background

A rich body of literature has recognized corporate entrepreneurship as an important antecedent to achieving and perpetuating competitive superiority (Barrett & Weinstein, 1998; Covin & Miles, 1999, 2007; Ireland et al., 2003; Miles & Covin, 2002, Zahra, 1996; Zahra et al., 2000, 2004). The concept of corporate entrepreneurship is broadly defined as “the process whereby an individual or a group of individuals, in association with an existing organization, create a new organization or instigate renewal or innovation within that organization” (Sharma & Chrisman, 1999, p. 18). Corporate entrepreneurship is also seen as an important strategic element, to be sustained and renewed in the volatile, competitive environments (Cruz & Nordqvist, 2012; Kellermanns & Eddleston, 2006; Zahra et al., 2004) of family firms, which are defined as businesses “governed and/or managed with the intention to shape and pursue the vision of the business held by a dominant coalition controlled by members of the same family or a small number of families in a manner that is potentially sustainable across generations of the family or families” (Chua et al., 1999, p. 25). Of the three forms of corporate entrepreneurship, innovation is the most studied in the family business context, followed by strategic renewal and then corporate venturing (for a detailed overview, see Bettinelli et al., 2017; Minola et al., 2021). It is the latter, corporate venturing in the family business context, which is the focus of our study.

As one form of corporate entrepreneurship, the main objective of corporate venturing is creating new businesses (Covin & Miles, 2007). Corporate venturing can be either internal or external, depending on whether the newly created ventures are positioned inside or outside an existing organization (Corbett et al., 2013; Miles & Covin, 2002; Sharma & Chrisman, 1999). External corporate venturing includes joint ventures, spin-offs, and spin-outs as well as venture capital initiatives (Sharma & Chrisman, 1999). These activities aim to leverage learning opportunities (Keil, 2004), provide access to new competencies, adjust existing firms’ technology portfolios (Reimsbach & Hauschild, 2012), and realize quick returns from promising business opportunities (Miles & Covin, 2002). In the family business context, external corporate venturing is often seen as fostering collaborations in the family network (Toledano et al., 2010) and extending an EF’s business platform in relation to its innovativeness and geographical scope (Calabrò et al., 2016). Internal corporate venturing attempts to develop an existing firm, build its entrepreneurial capabilities (e.g., Miles & Covin, 2002), empower employees (e.g., Reimsbach & Hauschild, 2012), and exploit slack resources and available capabilities (e.g., Block & MacMillan, 1993).

Corporate venturing may take various forms (Biggadike, 1979; Burgelman, 1983a; Sharma & Chrisman, 1999); for example, ventures may be created and developed in different ways, have different relationships with the parent firm, involve varying levels of innovation, and pursue various strategic goals for the existing firm. Sharma and Chrisman (1999) suggest that corporate venturing may vary in at least four dimensions that influence the development of newly created ventures: structural autonomy (i.e., the extent of embeddedness in existing organizations in terms of where to locate a new venture in the organizational system); relatedness to the existing business (i.e., the degree of relatedness of a new venture to the parent firm’s products, markets, and technologies); extent of innovation (i.e., the degree of newness of a venture in a marketplace); and nature of sponsorship (i.e., whether the entrepreneurial activity is formally induced or surfaces informally through autonomous efforts by individuals in an organizational system). This typology seems applicable not only in the context of nonfamily firms but family business and EF contexts as well. For example, Brumana et al. (2017) have recently analyzed how the development of ownership structure, corporate governance characteristics, and national legal systems influence how family firms pursue corporate venturing and make decisions on family ventures’ relatedness to the family firm and their autonomy.

Recalling our research focus on newly created ventures by individual members of EFs, the dimension of sponsorship, that is, whether the entrepreneurial activity is formally induced or surfaces informally through autonomous efforts by individuals (e.g., Burgelman, 1984; Sharma & Chrisman, 1999), is of particular importance. Research in the area of sponsorship refers to a formally induced entrepreneurial activity as a top-down process whereby the firm’s strategic and structural contexts provide the frame within which the activity is supported; informal, autonomous entrepreneurial activity is a bottom-up process driven and coordinated by entrepreneurial participants (e.g., employees at the operational level) that occurs outside of the formal procedural structures and strategies of organizations (Burgelman, 1983a, 1983b, 1983c, 1984). Interestingly, scholars have argued that the most effective way of creating new ventures is through originating and developing them autonomously as a bottom-up process, implying that highly innovative ventures emerge from the entrepreneurial activity of lower-level participants who often possess the most current knowledge and information critical for innovative venture outcomes (Burgelman, 1983a, 1983c; Day, 1994; Kimberly, 1979). To be successful, however, the newly created ventures need to be accepted by the organization in terms of integration with its strategy (Burgelman, 1984).

In this study, we apply this logic to the EF setting. Instead of entrepreneurial participants in an organizational system, we consider individual EF members in the overall family business context (Chrisman et al., 2003; Habbershon et al., 2003) an important driving force for innovative venturing activities that may or may not be supported by the EF with their family’s or the family firm’s resources (e.g., Brumana et al., 2017; Habbershon et al., 2003; Ramírez‐Pasillas et al., 2021). Prior literature, for example, suggests that businesses in which a family is involved are often influenced by the preferences and interests of their members (Brundin et al., 2014; Chua et al., 1999; Habbershon et al., 2003; Sharma et al., 1997), who can facilitate, but also impede, entrepreneurship. Indeed, some researchers have reported that families might be especially interested in growing and protecting their entrepreneurial legacy by means of continued entrepreneurial activity (e.g., Jaskiewicz et al., 2015), while others have suggested that family-influenced firms might be less entrepreneurial due to the risks associated with entrepreneurial failure (e.g., Naldi et al., 2007; Zahra, 2005).

Although there is a broadly held belief that individual EF members may be an important driver of entrepreneurial activity, the literature has, so far, mainly focused on analyzing entrepreneurship as a top-down firm-level activity (e.g., Bettinelli et al., 2017; Nordqvist & Melin, 2010; Randolph et al., 2017; Zahra, 2005). The literature has suggested that family firms engage in new venture creation to enable the persistent involvement of multiple generations in the business and to develop strategic portfolio entrepreneurship (Habbershon & Pistrui, 2002; Jaskiewicz et al., 2015; Marchisio et al., 2010; Sieger et al., 2011). Insight on informal, autonomous bottom-up venturing activities by EF members, however, is scarce. Indeed, the drivers motivating EF members to create new ventures individually or as a group instead of continuing or starting to work in the existing family firm have, so far, been overlooked by prior research, resulting in a knowledge gap on venturing motives within and across multiple family generations (Michael-Tsabari et al., 2014; Minola et al., 2016; Zellweger, Nason, et al., 2012). Scholars have called for more research on the motivations for entrepreneurial activity of EFs and their members as well as how EF members’ venturing motives are intertwined with the types of new ventures created (Michael-Tsabari et al., 2014; Sieger et al., 2011; Zellweger, Nason, et al., 2012).

Considering these gaps in the literature and calls for research in this area, we examine why EF members engage in the creation of new ventures and how the motives driving entrepreneurial activity relate to the resulting family venture type. Building on previous work (e.g., Burgelman, 1983a, 1983b, 1983c, 1984; Day, 1994; Sharma & Chrisman, 1999), we define family venturing as entrepreneurial activity by individual EF members or a group of individual EF members that leads to the creation of new businesses. While the more standard or traditional setting for corporate venturing is typically associated with the creation of new ventures centering around an existing organization (Covin & Miles, 2007), venturing actitivites by EF members may or may not include an existing family firm. Hence, in line with research that views entrepreneurial activities by EF members in between corporate and individual entrepreneurship (Minola et al., 2021), we recognize that the creation of new ventures may not necessarily be a top-down, formally induced firm-level activity but may surface autonomously as a bottom-up process by entrepreneurial individuals or a group of entrepreneurial individuals who are members of an EF. Connecting newly created ventures to the EF and the core family firm (if existent) as well as the interaction of EF venture founder(s) with the EF or family firm renders the application of the corporate venturing logic an adequate theory base for our study.

Methodology

Empirical Setting and Sample

To address the identified gaps in the literature and take further steps toward theory building regarding entrepreneurship in the family business context, we chose an exploratory, qualitative multiple case study research approach (Eisenhardt, 1989). Due to the lack of prior empirical insights into and substantiation of venturing motives of EF members and idiosyncratic features of “family” as factors that might impact the outcomes of venturing activities, a qualitative research design was required (Eisenhardt, 1989). In addition, this qualitative approach is appropriate for studying complex phenomena and social contexts that underlie human interactions, such as the intra- and transgenerational entrepreneurial activities of EF members (Nordqvist & Zellweger, 2010; Sieger et al., 2011), as well as answering “why” and “how” research questions.

We base our study on unique, in-depth data on family ventures gathered in Germany and Austria in 2017, 2018, and 2019. Both countries are home to many entrepreneurial family firms and share a similar cultural context. Our sample comprises mid-sized family firms, frequently considered the backbone of the German and Austrian economies (De Massis et al., 2018), the business activities of which generate less than €5bn but more than €50mn in annual revenue. 1 These EFs had sufficient wealth to support their members’ venturing activities, yet their firms were small enough to lack formalized venture hubs. Given our research questions, we focused on those EFs that engaged in entrepreneurial venturing beyond their family firm, which is in line with the theoretical definition of EFs provided in the Introduction. In sum, we required that EF cases consisted of a set of related individuals (by birth, marriage, or adoption), who engaged in planned or unplanned entrepreneurial activities.

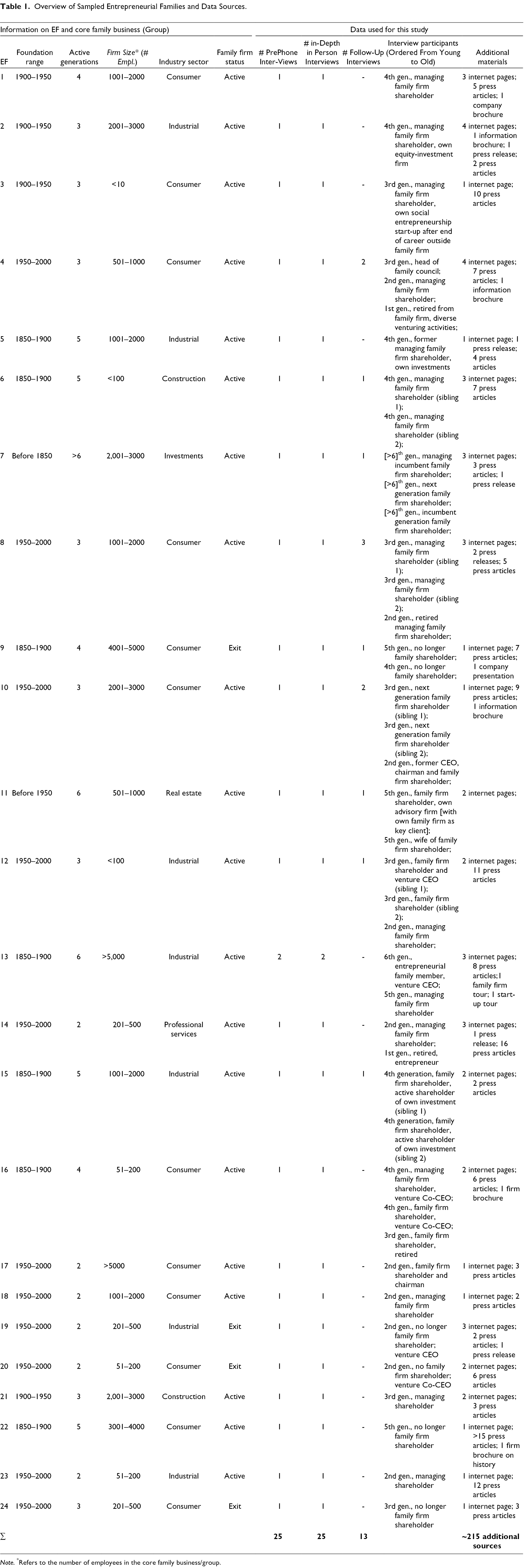

Because EF members are frequently reluctant to share insights about their activities with outsiders given confidentiality concerns (Brockhaus, 1994), we applied several strategies to obtain participation commitments from EF members that met our criteria. For example, we visited the websites of family firms, searched press articles (retrieved via Factiva) on family firms listed in public rankings, and we sought signs of entrepreneurial activity by EF members on the Internet. We then contacted relevant EFs with a detailed, personal letter. Our final sample included 24 EFs involved in 39 venturing cases. Table 1 provides an overview of the characteristics of these cases and the associated family firms.

Overview of Sampled Entrepreneurial Families and Data Sources.

Note. *Refers to the number of employees in the core family business/group.

Data Collection

We conducted three rounds of interviews to collect data on EFs, their members, and their new ventures. In the first round, we conducted short interviews (approximately 15–20 min) via phone with family firm owner-managers whom we had identified as potential participants. The phone calls served to familiarize the possible interviewees with our research, to explain the confidentiality guidelines, and to obtain initial insights into their entrepreneurial activity 2 to ensure that their venture cases were appropriate for our research objective. In the second round, we visited EF members in their firm headquarters to conduct in-depth interviews using semistructured guidelines that were built based on existing research on EFs. Interviews started with questions about the history of the EF, followed by deep dives into entrepreneurial activities from past years regarding three topics: (1) drivers of entrepreneurial activity; (2) entrepreneurial processes; and (3) outcomes, including contextual information. To allow flexibility, we asked primarily open-ended questions and encouraged our interviewees to share their thoughts and provide examples, specifically, their motives when engaging in entrepreneurial activity. To circumvent the risk of single-interviewer bias, 17 interviews were conducted by two interviewers together. Each interview lasted, on average, for 1 hr and 24 min; written transcriptions totaled more than 900 double-spaced pages. We complemented our data collection with publicly available information on the EFs and their activities (press releases, corporate websites, etc.), as well as substantial firm-related material (e.g., brochures, presentations, internal documents) provided by some EFs. After the initial data collection was completed, we conducted a half-day workshop in March 2018 with interviewees (13 participants) to discuss our preliminary findings and gather initial feedback. Focusing on family-owner managers as interviewees is common in family business research (e.g., Kammerlander et al., 2015) because it assumes that those individuals are well aware of any entrepreneurial activity of their family members. To validate our initial insights, from September 2019 to December 2019, we conducted 13 follow-up interviews (representing a third round) with EF member interviewees from the previous rounds; these interviews were also recorded and transcribed.

Data Analysis

We used an iterative five step process that involved switching between our cases and existing theory. Following prior research (Bertschi-Michel et al., 2020; Langley & Abdallah, 2011), we combined inductive and deductive analysis techniques, starting with an inductive analysis of the single cases based on the design of our research questions (Eisenhardt, 1989). To code statements related to our research questions, two researchers first engaged in one round of open coding using NVIVO software. We then discussed and aligned the primary codes, aggregated them into second-order themes, compared them with the categories extant in the literature, and engaged in a second round of coding. Subsequently, we created detailed case descriptions in a Microsoft Excel file and then organized the insights of each case according to the topics addressed in the interviews. This process helped us to develop a cross-case perspective to disentangle overarching patterns in a fourth step. Finally, we developed our model by iterative discussion of any potential linkages in our coding within and between cases, as well as insights from the extant literature. To further refine our research model, we gathered additional feedback from the interviewees through in-person discussions during a workshop as well as in follow-up interviews. Throughout the data analysis process, we triangulated data to the highest possible degree. For instance, data from archival press releases, web archives, and brochures allowed us to scrutinize interviewees’ information on venturing start, scope, and size. Moreover, data from other interviewees (i.e., family members) allowed us to ascertain entrepreneurs’ motives, family support, emotional attachment, and transgenerational intentions.

Findings

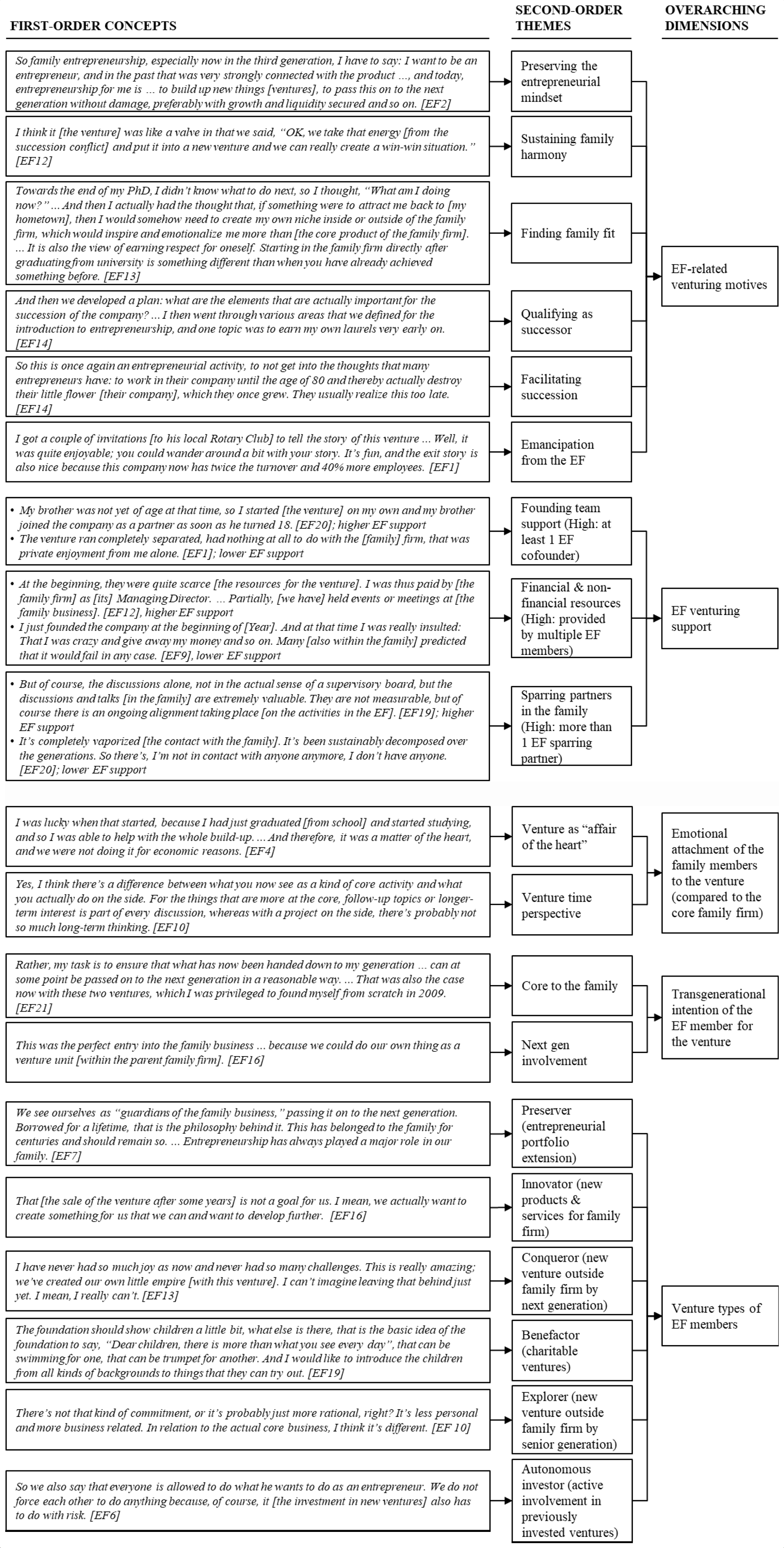

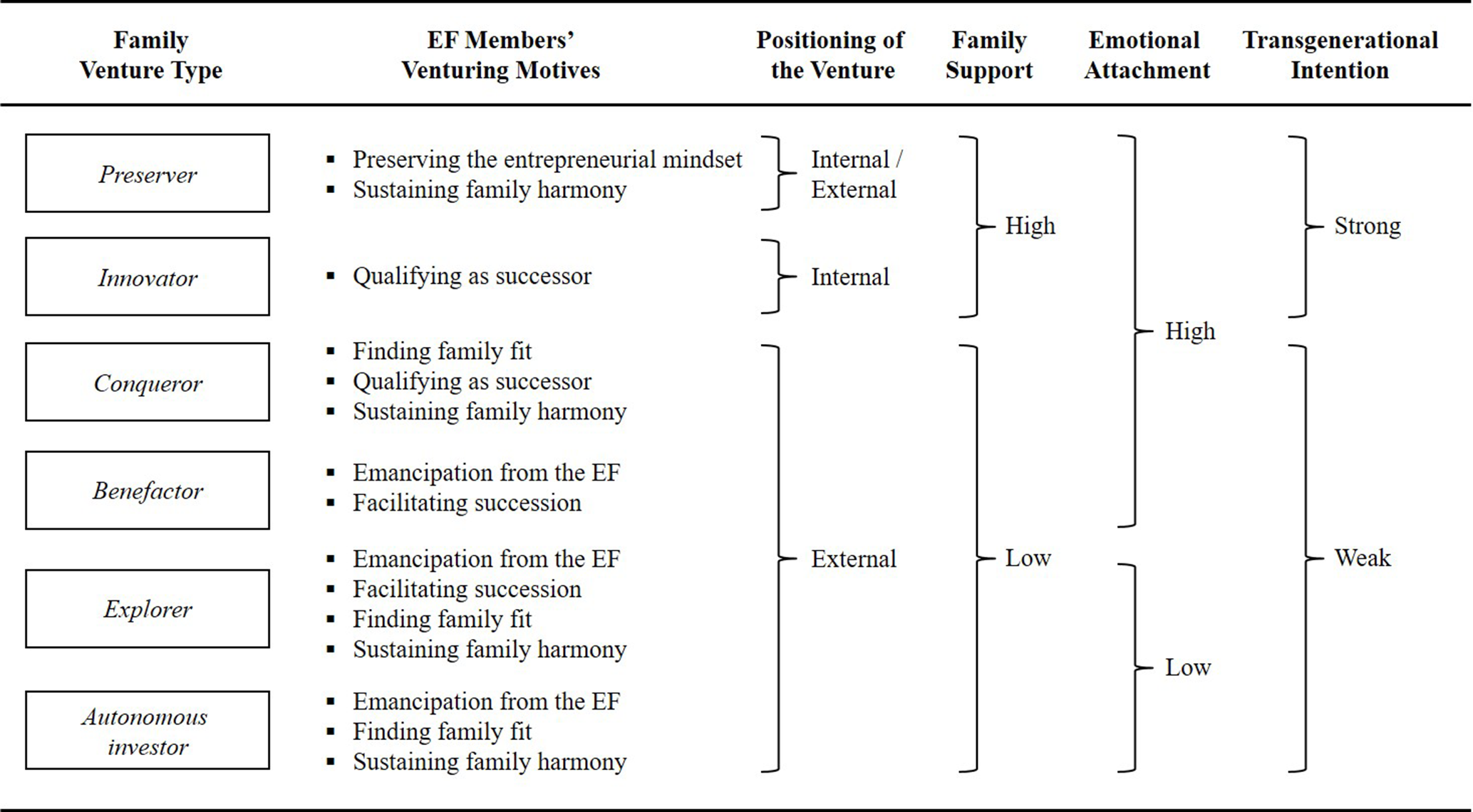

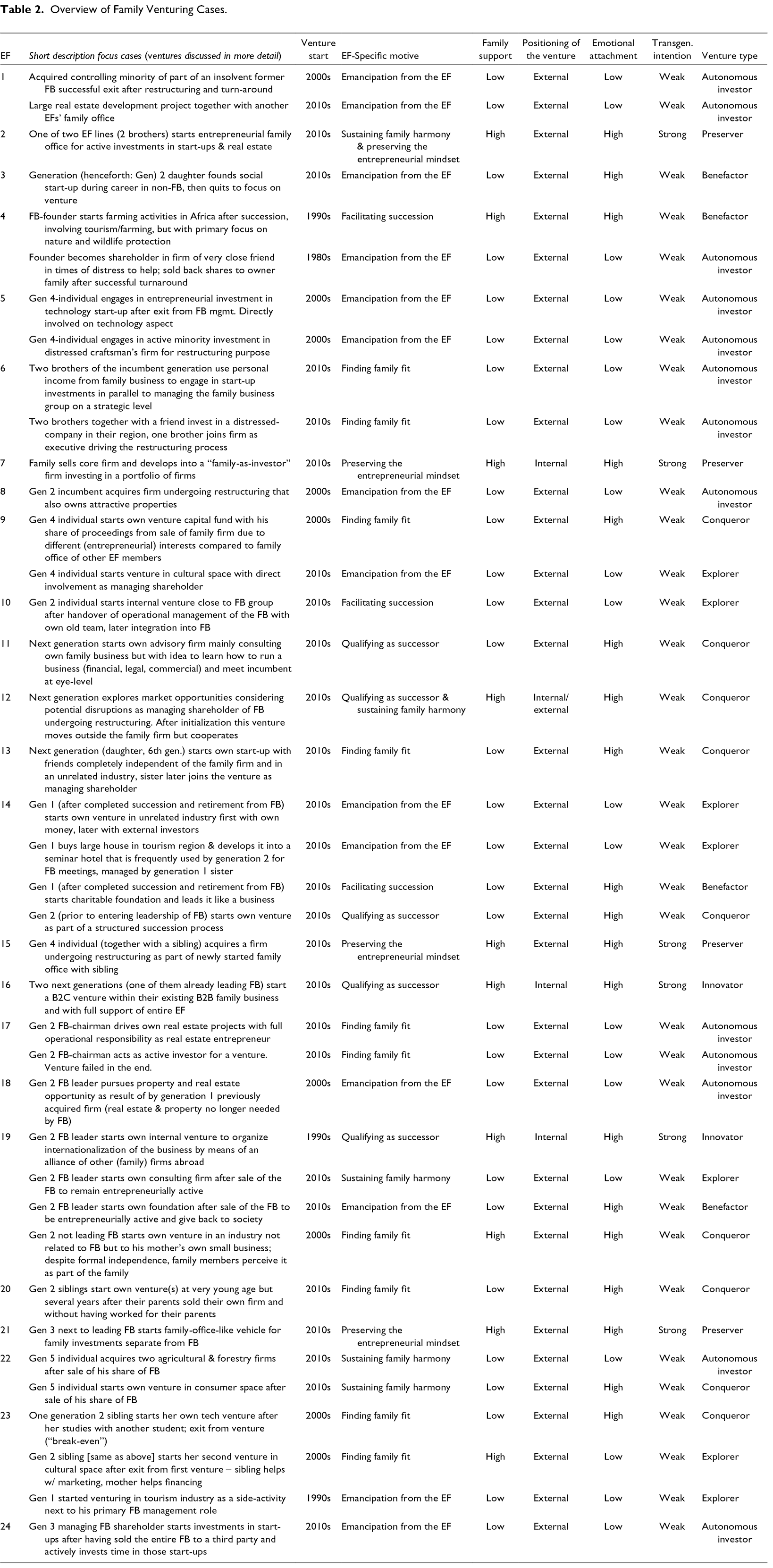

In Figure 1, we present the derived concepts, themes, and overarching dimensions from the individual cases. Based on insights from the cases as well as prior research, we conflated the constructs into a family venturing model (Figure 2). We describe the individual constructs in Figure 2 in more detail and illustrate EF members’ venturing motives and EF members’ venturing types that resulted from the entrepreneurial activity. Table 2 provides a summary of the key characteristics of all cases that we analyzed.

Data structure with 1st and 2nd order concept illustration.

Family Venturing Model.

Overview of Family Venturing Cases.

EF Members’ Venturing Motives

We identified six motives that encouraged EF members to engage in entrepreneurial activities: (1) preserving the entrepreneurial mindset, (2) sustaining family harmony (3) finding family fit, (4) qualifying as successor, (5) facilitating succession, and (6) emancipation from the EF. We discuss each motive separately.

Preserving the Entrepreneurial Mindset

In four cases (EF2, EF7, EF15, EF21), venturing activity was motivated by the desire to preserve the entrepreneurial mindset across multiple generations. Underlying this motive was the EF member’s self-perception of belonging to a group of transgenerational entrepreneurs and the perceived duty to grow the EF’s financial and socioemotional wealth for present and future generations. Consequently, members of the EF considered it an important part of their self-identity to continuously create new ventures rather than merely administering their wealth. Looking back to the past and being proud of previous entrepreneurial achievements were additional sources of motivation for EF members to engage in entrepreneurial activity and to continue on the path of transgenerational entrepreneurship. For example, the head of case EF7, an EF with a history of more than six generations, explained that his family has a long tradition of entering new markets whenever circumstances changed significantly:

To this day, our business has not changed in one respect: We never invented anything [and] never were the intelligent ones; we were the smart ones, if at all. … And our ancestors, yes, that is my theory, they noticed changing environments and opportunities in time and started to change; something changed, they saw that, [and] started to engage in different business activities. [EF7]

Building on this statement, the interviewee in case EF7 further added that the most recent entrepreneurial activity was due to today’s short-lived business models, which is a challenge that the EF had to tackle to stay active as did entrepreneurs from the previous generation:

We enjoy running [one business], we enjoy running [another business], that is how it is as of today. However, I don’t know whether we’ll still have that [specific business] in 25 years. [EF7]

The interviewee in case EF7 further emphasized the importance of an active EF for preserving the family tradition across generations:

The most important thing is the entrepreneurial family itself because if the entrepreneurial family no longer backs the company, because the entrepreneurial family can no longer provide active board members who understand what is happening in the business and who have their own entrepreneurial impetus, then, I would say, then you should urgently sell [the family venture]. [EF7]

In case EF21, to run the two ventures, the third-generation successor dismissed the possibility of managing the core family firm. Instead, he took a broader viewpoint on the longevity of the EF’s entrepreneurial activity and family wealth, a perspective similar to that of the interviewee from case EF2, who stepped down from managing the family firm. He described his venturing motive as follows:

So family entrepreneurship, especially now in the third generation, I have to say: I want to be an entrepreneur, and in the past that was very strongly connected with the product …, and today, entrepreneurship for me is … to build up new things [ventures], to pass this on to the next generation without damage, preferably with growth and liquidity secured and so on. [EF2]

Sustaining Family Harmony

In five cases (EF2, EF12, EF19, EF22 [two cases]), an important driver for EF members to engage in venturing was the existence or emergence of family conflicts. These conflicts arose for various reasons; for example, interpersonal conflicts (e.g., power conflicts among EF members; EF22 [two cases]), disagreement about family strategy (e.g., succession conflicts across generations; EF12), and disagreement over family firm strategy (e.g., whether to keep or sell the firm; EF2, EF19). Such conflicts drove EF members to create their own ventures to reduce or even avoid contact and working with certain EF members in the existing family firm. For example, in case EF2, one of the two siblings who left the family firm after a long-lasting conflict with another family member explained:

So it was also a bit due to coercion because you just didn’t want to be exposed to this [power] conflict. Let me put it this way: this forced constellation of having to work with all the other family entrepreneurs would have made me sick in the long run because fighting makes you sick at some point; … that is really to be taken literally. So in this respect, a total burden has been lifted [through the venturing activity]; I really like going back to the office, I’m much more self-determined …, and I choose this business myself. [EF2]

Venturing activities were often seen as a path to conflict resolution rather than causing the family to break up. This view was also confirmed by the interviewee in case EF12:

I think it [the venture] was like a valve in that we said, “OK, we take that energy [from the succession conflict] and put it into a new venture and we can really create a win-win situation.” [EF12]

Finding Family Fit

In ten cases (EF6 [two cases], EF9, EF13, EF17 [two cases], EF19, EF20, EF23 [two cases]), a central motive for EF members engaging in entrepreneurship centered on finding their own position in the EF. This relates to fundamental questions concerning EF members’ personal development and future career plans, such as their future role and position in the EF and whether they want to pursue a career in the family firm or outside, either as an entrepreneur or in a completely different profession (e.g., hospital doctor, university researcher). One frequent concern was how the EF member could gain respect from older and already successful EF members. For instance, the next-generation interviewee in case EF13 concluded that:

Towards the end of my PhD, I didn’t know what to do next, so I thought, “What am I doing now?” … And then I actually had the thought that, if something were to attract me back to [my hometown], then I would somehow need to create my own niche inside or outside of the family firm, which would inspire and emotionalize me more than [the core product of the family firm]. …It is also the view of earning respect for oneself. Starting in the family firm directly after graduating from university is something different than when you have already achieved something before. [EF13]

Interviewees who sought to establish their position in the EF often considered new venture creation to be a viable career path. Growing up in an EF, the interviewed EF members had the impression that venturing is the norm compared to being employed by an established company. In this regard, the interviewee in case EF17, who is the chairman of his family firm’s supervisory board and a full-time real-estate entrepreneur, explained:

It is true that we have been entrepreneurs again and again, at least since our great-great-grandfather. If you define me as an entrepreneur …, then it‘s probably an attitude, an affinity, where that comes from—genetics, I don‘t know, passed-down interests. [EF17]

Qualifying as Successor

For EF members in their 20s and 30s, entrepreneurial activity was strongly driven by their desire to prepare for the role of successor in the family firm. We observed this motive in five cases (EF11, EF12, EF14, EF16, EF19). For example, the next-generation interviewee in case EF11 stated:

I’m not keen on an abrupt succession, but my siblings and I are insisting that he [the senior generation] gradually implements a structured succession. … This does not mean that he should immediately hand over the management of the family. … It was important to me, if I would follow this call from the family and work for the family firm …, that I would be able to do this in an entrepreneurial manner myself and learn the basic tools of a managing director. That is why I started my own venture first. [EF11]

Similarly, the next-generation EF member in case EF14 engaged in entrepreneurial activity as part of the succession:

And then we developed a plan: what are the elements that are actually important for the succession of the company? … I then went through various areas that we defined for the introduction to entrepreneurship, and one topic was to earn my own laurels very early on. In 1999, I founded my own company. … I left after four years, and the others continued running it; and I then joined the parent company, where I became a managing director. The next step was to say, “OK to the preparation for the actual succession.” In between, I made many attempts, and that is also part of entrepreneurship, founding two or three ventures, which were then simply discontinued. [EF14]

This motive was frequently coupled with the next generation’s desire to add something of its own and meaningful to the existing family business by acting as entrepreneurs, rather than only administering the achievements of prior generations. Some next-generation interviewees emphasized that their own entrepreneurial accomplishments and the potential to integrate entrepreneurship into the family firm eventually drove them to become family firm successors. For example, the next-generation interviewee in case EF16, who started a B2C business within the context of the existing B2B family firm, noted:

I think it was exactly the right thing to do [return to the family firm to work in the venture], to earn my spurs there. It was perfect because the heart beats for the family business. … I grew up with my father, who worked for [the family firm]. That means you can imagine what a Sunday brunch looked like: they always discussed how the market was developing. … That means I really grew up with this entrepreneurial awareness. Right from the start, I was interested in the products, and then, of course, I had to fill these huge footprints [of the senior generation]. This was the perfect entry into the family business … because we could do our own thing as a venture unit [within the parent family firm] but independent from its [the family firm’s] core business. [EF16]

Facilitating Succession

For EF members in their 60s and 70s, one important motive of engaging in venturing activities was the desire to facilitate the transgenerational handover of the existing family firm while satisfying their own passion for entrepreneurial activity. Thus, to create space for the next generation and allow them to become fully responsible for the family firm, senior-generation EF members engaged in new venture creation to avoid interfering with their family firm successors. We observed this behavior in three cases (EF4, EF10, EF14). In the case of EF14, for example, the retired founder engaged in entrepreneurial activity directly after succession because he did not want to interfere with his son’s managerial discretion:

I would say that it is always bad if you are a restless entrepreneur; it is the worst thing not to be allowed to do anything any longer [after succession]. So in my opinion, an entrepreneur who is a true entrepreneur with heart and soul, thinks about what will happen later [after succession]. …And that is of course the thought: “I want to take decisions, I want to do something else, I don’t feel old yet, I’m [more than 70 years] now, but I don’t feel old yet.” … So I just said, “I have to look for a new playground in my life,” right? [EF14]

The interviewees noted that such venturing activity by the senior generation was particularly important in the case of planned family-internal succession because it was not easy for this generation to relinquish control. Hence, starting a new venture not only filled the senior generation with joy and a feeling of being needed but also provided the next-generation successor with the freedom to run the existing family business. Related to this point, the retired founder in case EF14 explained:

So this is once again an entrepreneurial activity, to not get into the thoughts that many entrepreneurs have: to work in their company until the age of 80 and thereby actually destroy their little flower [their company], which they once grew. They usually realize this too late. You only have to read the business press to see how many companies go down the drain because parent and child disagree or have different perspectives. I can’t save the company anymore either. … The young man has to sort it out himself now. [EF14]

The next-generation EF member in case EF4 confirmed that his father’s continued entrepreneurial activity provided sufficient freedom for him to assume leadership of the family firm:

The big activity came in [the year] when my father left [the family firm], moved from the board of directors to the supervisory board and then left [to start his new venture in Africa]. … When I took over [the CEO role], my father gave me complete freedom in my decisions. He always said to me, “I’m here if you need advice, but I won’t come and interfere.” At the first annual board meeting after I joined [the family firm], he [the senior generation] resigned from the supervisory board so as not to be a formal supervisory body for me, and since then, he has always been my most important advisor, but passive. [EF4]

Emancipation From the EF

This motive relates to EF members’ desire to establish themselves as successful entrepreneurs beyond the EFs’ and family firms’ fields of activities. By collecting memorable entrepreneurial experiences and “war stories” of their own ventures, they could share their own experiences and achievements within the EF community and beyond (e.g., Rotary Clubs, Lions Clubs, chambers of commerce). We observed this motive in fourteen cases (EF1 [two cases], EF3, EF4, EF5 [two cases], EF8, EF9, EF14 [two cases], EF18, EF19, EF23, EF24). For example, the family firm CEO in case EF1, who joined a distressed venture, restructured it, and then exited the venture, explained:

I got a couple of invitations [to his local Rotary Club] to tell the story of this venture. … Well, it was quite enjoyable; you could wander around a bit with your story. It’s fun, and the exit story is also nice because this company now has twice the turnover and 40% more employees. [EF1]

Those stories were often shared, not only within the EF member’s family and with friends but also at business events. The EF members engaged in those ventures to live their entrepreneurial dream outside the EF and family firm, as reflected in the example of EF23, who referred to an unprofitable hotel venture that her father had once established:

My father was a visionary of the finest sort. … He made the claim, “I’m going to create the greatest hotel, and I want the coolest chef.” … It never took off; but my father enjoyed it [running the venture] as his personal hobby … and still managed to run the core business [the family firm]. [EF23]

Such venturing activity often originated from personal interest, achieving self-actualization, or emancipation from the EF, rather than taking advantage of a financial opportunity. For example, the interviewee in case EF24, who sold his family firm and became entrepreneurially active in new ventures, explained his activities:

It was simply a product I could stand fully behind, and I also liked the fact that I had this opportunity to develop a small, beautiful ‘manufactory.’ Then, to turn it into a really nice growth model and develop it into a family business—that was what appealed to me. … We wanted to establish a nice little family business with a decent growth story. … One is e-commerce in the animal sector, that is, pet food. The other is in the healthcare sector, and the third is in the sports industry. I was attracted to e-commerce, that pet food story, because it has many parallels to my time as a retailer. In addition, the sports industry interested me because I’m an active runner myself, and that has a lot to do with it. [EF24]

As this quote shows, these activities were not focused merely on profits but also on personal interest and proving that he could be a successful entrepreneur by himself.

The interviewee in case EF19 described his own perception of entrepreneurship as a source of personal confirmation that is not achieved from simply investing in ventures or financial instruments (e.g., stocks):

You always have to sort out: how much of it is ego and thus done because it is great for yourself. I’m far from being satisfied with a bank account. Knowing that 10 or 20 people have a job because you are working a little bit [running a venture] satisfies me more personally. That is, of course, as I said, inherent in egoism, that the employees say, “Good that we have you”; this is a confirmation that we all need—one that children give you. [EF19]

The financial outcome appeared to be of lower relevance; that is, a profit from the entrepreneurial activity would be appreciated, but a loss is neither excluded nor feared. Instead, the entrepreneurial activity was often attributed to achieving self-actualization and emancipation from the EF.

EF Members’ Venturing Types

In the prior section, we have identified and discussed six motives that encouraged EF members to engage in entrepreneurial activity. These motives can be considered as antecedents of informal, autonomous bottom-up entrepreneurial activity by EF members and highlight aspects unique to entrepreneurship in the family business context; they are as much about noneconomic goals as about economic goals, such as firm performance or competitive superiority, that are typical drivers of entrepreneurial activity in nonfamily business contexts. The identified motives were associated with six heterogeneous venture types varying in (1) their positioning, either inside or outside of the family firms’ boundaries; (2) family support in the form of provision of financial and nonfinancial resources provided either directly by the family (e.g., advice) or via the family firm (e.g., office space in the firm); (3) venturing EF members’ emotional attachment to the newly created venture relative to the core family firm; and (4) venturing EF members’ transgenerational intentions (Figure 2).

Preserver Venturing

This venture type (EF2, EF7, EF15, EF21) describes preservation-oriented venturing, in which EFs as an entity engage in profit-oriented venturing activities in various industries, also partly unrelated to the family firm, to secure the long-term survival of the EF rather than that of a specific business; here, the ventures were positioned either inside or outside of the family firm. Entrepreneurial activity was frequently driven by the motive of preserving the entrepreneurial mindset (EF2, EF7, EF15, EF21) and was especially characterized by high levels of family support in terms of providing both financial resources (e.g., investment) and nonfinancial resources (e.g., advice, access to networks, office space). For example, the next-generation interviewee in case EF7 explained the venturing activities as follows:

[Our entrepreneurial strategy is] we buy to hold and develop [new ventures]. Of course, in the last decades, there has been a decision to sell [the new ventures] from time to time. However, this is motivated by the fact that we either cannot see or develop the future, or we are not the best owner. [EF7]

This next-generation EF member claimed that emotional attachment to these ventures relative to the core family firm is high due to the high level of interrelatedness between the family and entrepreneurship. The venturing activity had effectively become a “family affair” going beyond the pure business aspect. Thus, EF members frequently perceive preserver venturing as part of the family’s identity, as the next-generation member of EF7 explained:

Personally, I say: this is a more personal, direct, sustainable way [of venturing]. You are closer to it; tradition plays a big role, also obligation does. Ownership is an obligation. There is also an emotional component because you grow up with it. We have been introduced to it very personally. It was an exciting process and has to do with family membership, not just entrepreneurship. [EF7]

At the same time, transgenerational intention is typically strong with this venture type—first, because the underlying motive is to preserve the entrepreneurial mindset and sustain EF wealth across generations and, second, because the family acts according to a “hold and develop” mindset with limited or no intention to sell the venture in the future, a mindset learned from previous generations. The next-generation interviewee in case EF7 explained that the family acted in order to pass on EF wealth to the next generation:

We see ourselves as “guardians of the family business,” passing it on to the next generation. Borrowed for a lifetime, that is the philosophy behind it. This has belonged to the family for centuries and should remain so. … Entrepreneurship has always played a major role in our family. [EF7]

With this venture type, the relationship to the core family firm (if still existent) is often rather strong. Specifically, those preserver ventures that were positioned closer to the family business had a rather high interaction with the EF including the family firm. The next-generation interviewee in case EF7, for example, explained that the family had developed a specific EF governance structure consisting of a family council to coordinate and supervise the venturing activities as well as the family’s engagement in the family firm.

High levels of family support and interaction are likely related to strong transgenerational perspectives and use of EF or family firm resources for the venturing activity. This relationship creates an incentive for EF members to become involved with EF venturing activities, at a minimum by actively electing EF representatives to preside over all venturing activities.

Innovator Venturing

This venture type (EF16, EF19) describes entrepreneurial activities inside a family firm’s boundaries that typically receive high levels of family support, often from the entire EF. The focus of this venture type is on innovation and strategic renewal with an emphasis on preparing the core family firm for the future. Here, the prevalent motive was qualifying as successor (EF16, EF19); often, the entrepreneurial team consisted of next-generation EF members (i.e., intragenerational entrepreneurship) who attempted to bring something new to the firm. With this venture type, family support and interaction was rather high, and included the provision of financial resources (e.g., investment via the family firm) and nonfinancial resources (e.g., advice). For example, the two next-generation EF members in case EF16 established an internal corporate venture in the B2C sector, utilizing the family’s multigenerational knowledge about the product gained from their traditional B2B business activities. Although the new B2C business operates under a different brand, the venture was part of the wider family business and extensively used the resources of the family firm. Emotional attachment with this venture type is high relative to the core family firm; EF members (mainly from the next generation) wanted to create their generation’s own identity within the family firm. The transgenerational intentions associated with innovator ventures are also rather strong given that this venture type operates within the family firm’s sphere.

The location of the venturing activity (e.g., inside the family firm) connects with the venturing EF members’ perception of being part of something bigger, that is, the family firm’s future and longevity. If a venture is perceived as part of the family business, transgenerational intentions might spill over to the innovator venture. The location inside the family firm renders long-term integration into the core family business more likely; EF members may perceive this venture as an activity with high transgenerational potential. According to two next-generation EF members:

That [the sale of the venture after some years] is not a goal for us. I mean, we actually want to create something for us that we can and want to develop further. As I said, … to build something up here and then sell it off, that is definitely not the goal. [EF16]

The [young children in the EF] are already interested [in the venture]. … If they see an advertising column somewhere in the city, they say, “Dad, there is [the venture’s product].” Well, they are already involved [emotionally]. … I would always be happy if this [the venture] continues somehow through one of them. [EF16].

Conqueror Venturing

This venture type (EF9, EF11, EF12, EF13, EF14, EF19, EF20, EF22, EF23) describes stand-alone new ventures outside, and mostly unrelated to, the family firm. Specifically, these ventures can be seen as independent, often (co-)founded by selected EF members from the next generation with a clear for-profit orientation. The three central motives of creating conquerors were finding family fit (EF9, EF13, EF19, EF20, EF23), qualifying as successor (EF11, EF12, EF14), and sustaining family harmony (EF12, EF22). These motives specifically relate more to EF members’ personal desires and less to the interests of the EF or the family firm. With conqueror ventures, family support and interaction with the family firm is typically lower compared to, for example, innovator and preserver venture types, where the EF and the family firm were core drivers for entrepreneurial activity. Also, with this venture type, EFs provided nonfinancial backing; for example, in the case of EF20, the parents of the next-generation founders frequently provided advice.

This lower family support and, thus, interaction with the family firm might be also attributed to low proximity to the family firm and the subordinate role for EF wealth (e.g., due to the absence of financial investment from the EF) with this venture type. For example, after graduating from university, the next-generation interviewee in EF13 co-founded a beverage production venture together with two nonfamily individuals to gain professional experience. This beverage business had nothing in common with the family business (producer of industrial labels). Support by the EF was limited to a sibling who joined the venture later. Similarly, the next-generation EF member in case EF23 co-founded a software company with a nonfamily co-founder. Again, the venture operated in a completely different business area than the family firm (engineering products and services).

As with the other venture types, interviewees frequently exhibited a strong emotional attachment to the venture (relative to the core family firm); for example, the interviewee in case EF13 concluded:

I have never had so much joy as now and never had so many challenges. This is really amazing; we’ve created our own little empire [with this venture]. I can’t imagine leaving that behind just yet. [EF13]

Such high emotional attachment might be explained by the venturing EF members perceiving their ventures to be something that they created on their own from scratch, which cost them much time and effort. The transgenerational intentions of EF members of the conqueror type, however, were rather weak compared to other venture types, which might relate to lower family support and the nonfamily character of this venture type. Moreover, weak transgenerational intentions might also be rooted in strategic orientation; unlike the family firm, which was often built to last for generations, conqueror ventures were frequently built with the purpose of selling. According to the next-generation founder of EF12:

Yes, at some point there will be a sale or even a loss of power for yourself and for the strategic investor. That is, whether it’s a quick exit, a slow IPO, a merger at some point, or an acquisition, I think we’re relatively open about that. [EF12]

Benefactor Venturing

This type (EF3, EF4, EF14, EF19) describes ventures in which mainly senior-generation EF members become involved in new ventures outside the family firm, primarily for social and charitable reasons, such as environmental protection. With this venture type, two motives were prevalent: emancipation from the EF (EF3, EF19) and facilitating succession (EF4, EF14). Support by the EF for benefactor ventures was deemed rather low (EF3, EF14, EF19), often limited to the provision of nonfinancial resources (e.g., advice). This low support and interaction as well might relate to the prevalence of more personal motives, such as the joy of entrepreneurial activity, giving back to society, finding challenges after retirement or succession, and experiencing new entrepreneurial adventures outside the family firm. The interaction with the family firm was also rather low, because venturing activities usually had nothing to do with the family firm’s core business.

For example, the senior-generation interviewee in EF14 started a charitable venture of educational support for students in secondary schools. Another example is case EF4, in which the senior-generation EF member engaged in an environmental protection venture in Africa by buying land and creating a nature reserve (i.e., protecting plants and animals in the region while creating economic benefits for the local population). With this venture type, emotional attachment for the venturing EF members (relative to the core family firm) was high and might be attributed to the social or charitable character of these ventures and the noneconomic benefits ascribed to them. As the senior-generation interviewee in EF4, who founded multiple benefactor ventures explained:

I also did it because I simply enjoyed it, not so much for the success; of course, you want to have that too, but I didn’t say, “I have to do it here now, no matter how, to be successful.” Rather, it is an affair of the heart for me if you want to put it that way. [EF4]

One next-generation interviewee of case EF4, who became involved in the venture at a later point in time to support the aging founder, further stated:

My children grew up partly in [the country where the charitable venture was launched], which means that it had an incredible emotional significance for us. … And therefore, it was a matter of the heart, and we were not doing it for economic reasons. [EF4]

Given that these ventures were “pet projects” of individual, senior EF members, however, there was no strong transgenerational intention (unless a junior EF member shared the same passion).

Explorer Venturing

This type describes ventures (EF9, EF10, EF14 [two cases], EF19, EF23 [two cases]) in which senior-generation EF members became involved in newly initiated ventures outside the family firm for the purpose of generating profits (as opposed to benefactor ventures). Here, emancipation from the EF (EF9, EF14 [two cases], EF23) appeared to be the primary motive for the entrepreneurial activity; another important venture motive was facilitating succession (EF10), where the senior generation focused on increasing the successor’s discretion in the family business. With this venture type, family support was rather low and mainly nonfinancial; for example, the mother of the venturing EF member in case EF9 supported the venture by providing advice. In addition, explorer ventures typically had quite different business models and foci than the existing family firms and were, despite the general profit focus, not necessarily relevant to EF wealth. Hence, the interaction with the family firm of this type of venture is low to non-existent. The interviewee in case EF14, for example, acquired real estate and successfully developed a business center that offered rental space to firms for seminars and trainings. This venture was completely separate from the existing family firm. Similarly, after retirement, the interviewee in case EF19 started his own consulting firm apart from the family firm, and the senior-generation EF member in case EF23 bought property on which he later built a hotel; neither of these new businesses was related to that of the existing family firm. With explorer ventures, emotional attachment was rather low (relative to the core family firm). For example, the next-generation member of EF10 stated:

Yes, I think these side businesses are different. There’s not that kind of commitment, or it’s probably just more rational, right? It’s less personal and more business related. In relation to the actual core business, I think it’s different. [EF10]

The rather low emotional attachment could be rooted in the ambivalent relationship to the new venture compared with the family firm. Although the experience of founding a new venture inevitably leads to a certain level of emotional attachment, the senior generation might especially feel a lower attachment compared to the core family firm because of their association with the family firm for a much longer period of time (i.e., often for decades). We found the transgenerational intention of these ventures to be weak, possibly because explorer ventures were often created by EF members to distance themselves from the family firm, due the motives of emancipation from the EF or facilitating succession, rather than building a new economic prospect for future EF generations, which is typically attributed to the existing family firm. As the next-generation EF member in case EF10 stated:

Yes, I think there’s a difference between what you now see as a kind of core activity and what you actually do on the side. For the things that are more at the core, follow-up topics or longer-term interest is part of every discussion, whereas with a project on the side, there’s probably not so much long-term thinking. [EF10]

Autonomous Investing

This type describes ventures (EF1 [two cases], EF4, EF5 [two cases], EF6 [two cases], EF8, EF17 [two cases], EF18, EF22, EF24) in which EF members in their 30s, 40s, 50s, and 60s engaged in entrepreneurial activity outside the family firm, primarily actively managing ventures in which they had previously invested. The primary motives here were emancipation from the EF (EF1 [two cases], EF4, EF8, EF18, EF24), finding family fit (EF6 [two cases], EF17 [two cases]), and sustaining family harmony as a consequence of a family conflict (EF22). For example, with his own financial means, the family CEO in case EF1 acquired a subsidiary venture of an insolvent conglomerate, restructured the company, and later sold it because he felt that it would be a lucrative opportunity:

I already knew that the [subsidiary of the insolvent conglomerate] within the [insolvent group] was already a gem. That it already worked very well … and I could tell from the numbers that there was “music inside.” … I said, if that is true, then the business certainly works. … Even if we make losses at the beginning, which is normal, we get out relatively quickly [reach break-even] because we inevitably did not have much equity capital. [EF1]

Similarly, the two brothers in EF6 initially invested in early-stage ventures in parallel with running the family business; in another example, the second-generation CEO of the family business engaged in real estate and selective venture capital initiatives, relying on his own capital and driven by the motivation to make these investments his own professional full-time activity. With ventures of this type, emotional attachment was rather low (relative to the core family firm) since the activities were perceived as financial opportunities that exhibited a professional investment character, rather than being intrinsic to the family. As the interviewee of EF6 explained:

And we have the [venture activities] again in different constellations. Partly my brother together with friends. Partly my brother together with me. Partly me alone. So we also say that everyone is allowed to do what he wants to do as an entrepreneur. We do not force each other to do anything because, of course, it [the investment in new ventures] also has to do with risk. [EF6]

Transgenerational intention with this venture type was also rather low since the ventures were primarily seen as sources of potential personal income in the present and not transgenerational wealth vehicles. Support by the EF was particularly low for autonomous investor ventures in which the primary motive was emancipation from the EF, possibly because these motives cater solely to the egocentric interests of individual EF members who want to distance themselves from the EF rather than to those of the EF or the family firm. In fact, there is low to virtually no interaction between the family firm and this type of venture.

Discussion

The focus of this research has been on examining newly created ventures of EF members. We drew on rare and difficult-to-obtain in-depth data on family ventures (i.e., 63 interviews with EF members involved in 39 distinct venturing cases in addition to substantial firm-related material) to address the following research questions: (1) Why do EF members engage in the creation of new ventures? and (2) How do the motives driving entrepreneurial activity relate to the resulting family venture type? In doing so, we identified a number of venturing motives unique to the EF context as well as six heterogeneous family venture types and discussed how specific venturing motives were associated with venture types, positioned either inside or outside an existing family firm. We also explored how family support directly or via the family firm, emotional attachment, and transgenerational intention varied among the venture types. Overall, these insights contribute to a better and more fine-grained understanding of why and how EFs and their members pursue entrepreneurial activities both within (horizontally) and across (vertically) generations through the establishment of new ventures and have led to our model (Figure 2), which portrays the idiosyncratic features of newly created family ventures.

Theoretical Contributions

First, regarding research on corporate entrepreneurship in family-influenced firms (Bettinelli et al., 2017; Brumana et al., 2017, Kellermanns & Eddleston, 2006; Minola et al., 2016, 2021; Ramírez‐Pasillas et al., 2021), we offer new insights into the antecedents of informal bottom-up and autonomous entrepreneurial activity by EF members that emphasize aspects unique to the family business context. In particular, we identified six motives that encouraged EF members to engage in such activity: preserving the entrepreneurial mindset, sustaining family harmony, finding family fit, qualifying as successor, facilitating succession, and emancipation from the EF. These motives had not been explicitly discussed in prior research; we went above and beyond the current literature on drivers of entrepreneurial activity in the family business context (Bettinelli et al., 2017; Chrisman et al., 2003; Habbershon et al., 2003; Ramírez‐Pasillas et al., 2021). Preserving the entrepreneurial mindset and sustaining family harmony clearly fall outside the pure economic logic of corporate entrepreneurship in nonfamily firms and reside at the level of the family, rather than at the level of the family firm. Similarly, the motives finding family fit, qualifying as successor, facilitating succession, and emancipation from the EF would not occur without being an EF member. Hence, our study shows that the motives driving EF members to engage in new venture creation arise from a unique system, which not only considers the broad perspective of the family firm but also integrates the interests of the EF and individual EF member(s). Moreover, our study adds to research on portfolio entrepreneurship (e.g., Michael-Tsabari et al., 2014; Sieger et al., 2011). We find that EFs’ venture portfolios are frequently not the result of strategic portfolio management but may also occur as a “patchwork” of ventures that are tied together through the membership of entrepreneurs or entrepreneurial teams in an EF. Moreover, our analysis shows that—in line with corporate entrepreneurship literature (e.g., Sharma & Chrisman, 1999)—a distinction of internal versus external ventures is also relevant in the family business context. While corporate entrepreneurship literature has often emphasized the importance of sponsorship or parent firm support (e.g., Burgelman, 1984), the findings of our study point to the importance of family support in the EF context. In addition, two family-related dimensions, which are unique to the EF context, that are important for venture categorization emerged from our study: emotional attachment and transgenerational intentions. These insights advance our overall understanding of entrepreneurship in the family business context and how it differs from corporate entrepreneurship in nonfamily business settings.

Second, regarding research on family entrepreneurship (Habbershon & Pistrui, 2002; Habbershon et al., 2010; Zellweger, Nason, et al., 2012), we found that entrepreneurial activity of EF members is not necessarily driven by the EF as a monolithic entity, as frequently conceptualized in the literature (Nordqvist & Melin, 2010), but often by individual EF members who create new ventures together with nonfamily co-founders or selected EF members, albeit often triggered at the level of the family (e.g., by motives such as sustaining family harmony or qualifying as successor). Consequently, we show that EFs rarely function as homogeneous entrepreneurial actors with a unified mindset, but consist of individual entrepreneurial participants who team up with particular EF members, either of the same generation, such as siblings or cousins, or across generations, such as parent-child teams, to create a new venture associated with the EF or family firm. Our study also contributes to research proposing that the family and the family business play central roles in EF members’ venturing activities (Aldrich & Cliff, 2003; Randerson et al., 2015) by shedding light on the relationship between venture motives and family support—provided either directly by the family (e.g., advice from certain EF members) or via the family firm (e.g., office space in the family firm offered to EF members)—for the entrepreneurial activity of EF members. In nonfamily firms, support typically refers to resources received from the parent firm and depends on new ventures’ overall strategic relevance for the parent organization. We have shown that in the EF context new venture support and interaction between venturing EF members, EFs, and family firms also occurs even without such strategic importance, as some of the venture cases studied had nothing in common with the products or markets of the parent family firm or the activities by the EF. This insight adds to a more nuanced understanding of how EF members act together to develop the ventures that emerge in the sphere of EFs (e.g., Ramírez‐Pasillas et al., 2021).

Moreover, while some previous work has viewed entrepreneurship as a strategic activity at the level of the family firm (Bettinelli et al., 2017; Clinton et al., 2018; Nordqvist & Melin, 2010), the insights of our study show that this view is frequently not the case. In line with prior exploratory research (Minola et al., 2021; Zellweger, Nason, et al., 2012), we propose that entrepreneurship is not solely at the level of the firm and centered around one core business (an existing family firm), which is passed on from one generation to the next. Rather, it seems that many family ventures are the result of informal, autonomous bottom-up entrepreneurial activity (Burgelman, 1983a, 1983b, 1983c, 1984). Different generations of EF members continuously engage in entrepreneurial activity driven by various motives, whereby the resulting new ventures can be, but do not need to be, part of the existing family firm, owned by the EF as one entity or passed on to the next generation. For example, our interviews revealed that ventures are frequently built and owned by individual EF members together with nonfamily co-founders or family dyads with the purpose of selling the venture instead of passing it on to the next generation. Our cases reveal that entrepreneurial activity by EF members can also occur within EFs that have sold their original family firm (e.g., EF9, EF20), potentially leading to new ventures becoming the emotional entrepreneurial nucleus of the EF (Bierl & Kammerlander, 2019). Therefore, our study makes important strides toward a better understanding of EFs’ entrepreneurial activities.

Third, we contribute to the broader family business research, particularly to a better understanding of differences between nonfamily business and family business contexts as well as of family firm heterogeneity (Chua et al., 2012; Jaskiewicz & Dyer, 2017). Prior research has recognized that entrepreneurial activity in nonfamily firms is often driven by goals, such as achieving or perpetuating competitive superiority of the firm or financial performance (Covin & Miles, 1999; Zahra & Covin, 1995). Based on our analyses, we have found that family business settings differ significantly in this respect. An important distinction is the identified motives for entrepreneurial activity, which in the family business context is as much about noneconomic goals (e.g., preserving the entrepreneurial mindset, sustaining family harmony) as it is about economic goals. In addition, with regard to differences among family businesses, we show how EF members’ idiosyncratic venturing motives are associated with heterogeneous outcomes and propose a family venturing model (Figure 2). We identified six different family venture types: preserver, innovator, conqueror, benefactor, explorer, and autonomous investor. While some venture types were implicitly connected with certain motives, others are founded for multiple reasons. The preserver venture type, for example, is clearly associated with the motive preserving the entrepreneurial mindset. The motive sustaining family harmony, on the other hand, is found in many venture types, which in turn may have to do with the fact that this motive is attributed to a variety of factors; among others, it is associated with conflicts involving business decisions in the family firm, but also with conflicts that affect the venturing EF member in private life. Another example is the motive qualifying as a successor: some entrepreneurs prefer to prove themselves within the family firm (e.g., innovator) and for others, it is important to earn their laurels with their own venture outside (e.g., conqueror).

With regard to positioning and family support, while the preserver type is positioned either inside or outside the family firm, the innovator type is positioned solely inside, and the conqueror, benefactor, explorer as well as autonomous investor venture types are typically positioned outside the family firm. Interestingly, those types of ventures that are positioned inside the family firm received greater support from the family (directly or via the family firm) than those that are positioned outside; thus, positioning seems to be related to the interaction between the newly created family ventures and the EF or the family firm, whereby specifically the interaction with the EF is a unique aspect compared to corporate entrepreneurship in nonfamily business contexts (e.g., Burgelman, 1984; Sharma & Chrisman, 1999).

Moreover, we inductively identified emotional attachment and transgenerational intention as dimensions of venturing activities in the family business and EF context in our data and underscored how these dimensions vary among the different venture types. Specifically, preserver, innovator, conqueror, and benefactor types induce high emotional attachment of EF members to their ventures, while explorer and autonomous investor types induce low emotional attachment. Of the ventures with high emotional attachment, preserver and innovator types also displayed strong transgenerational intentions. Although initiated by EF members, conqueror, benefactor, explorer, and autonomous investor ventures displayed rather weak transgenerational intentions (see the Findings section). Hence, while prior research has concluded that family-influenced ventures primarily strive for transgenerational wealth (Pistrui et al., 2010), we show that this assumption does not hold for all types of family ventures (Figure 2). Interestingly, we found that transgenerational intentions were higher with those ventures in which family support was strong, meaning that transgenerational intention might not be connected with emotional attachment but is likely connected to family support.

In theory, more than the six identified ventures types are conceivable. In particular, based on the four dimensions there are potentially 16 types possible, assuming that each dimension can take on one of two values (e.g., internal-external positioning; high-low family support; high-low emotional attachment; strong-weak transgenerational intention). Practically, however, some configurations may have a very low probability of occurrence. For example, given the motives we have identified in this research it may be unlikely that externally positioned ventures would be associated with strong transgenerational intentions. We could speculate, however, that if one or several dimensions change over time, this may have an effect on the other dimensions and, ultimately, on the transformation into another family venture type or even the emergence of completely new family venture types. For example, if an external venture becomes successful and is institutionalized in the EF structure, transgenerational intentions and likely also emotional attachment may later emerge.

Limitations and Future Research

As with all studies, our research has some limitations that provide fertile ground for future inquiries. The first can be found in the limited number of EF members interviewed per venture case; the second is the time between the venturing activity and the interviews (i.e., in some cases, several years had passed and, thus, our findings may be subject to recall bias). The third limitation is the cultural setting in which our data were collected. Regarding the first and second limitations, while we often interviewed two or three EF members, we occasionally had to rely on data gathered from only one EF member, the key informant, who was the primary driver of the entrepreneurial activity. As we observed very similar narratives among the cases with multiple respondents, we believe that this is not a significant concern. Regarding the third limitation, since our interview data were obtained in Germany and Austria only, our results might be influenced by these cultural settings. Hence, we cannot determine whether our findings are generalizable and apply to other cultural settings. To address these limitations, researchers are encouraged to scrutinize our findings with replication studies based on data from recent venturing cases collected from multiple informants in different cultural settings. In this context, it would also be interesting to investigate—based on longitudinal data—whether and how venture types from our model change over time and how the individual dimensions depend on each other. Moreover, quantitative follow-up studies might investigate the effects of family size, EF member’s age, and number of total ventures in the portfolio. This point leads to another question that our study did not cover in greater detail: how family is defined and whether the term “family” is interpreted differently across EFs and cultures. While the families in our study conformed to traditional conceptualizations (i.e., a set of individuals related by birth, marriage, or adoption), it is important to note that the definition and general composition of the family is changing (Aldrich & Cliff, 2003). Compounding the effects of this change are the different kinship ties between EF members and the implications for business decisions. To date, we know very little about how varying kinship ties affect decision making. Accordingly, future research should investigate how changes in family structure impact the EF over time and whether these changes facilitate or hinder venturing activities.

The fourth limitation is that our research has not looked deeper into the role of familial altruism. For example, Steier (2003, p. 616) described family “members as generally altruistic towards one another.” Although we disentangled various EF members’ specific motives for new venture creation and various family support levels, we did not focus on the influence of altruism on family support. While we show in selected cases that next-generation EF members tend to support the senior generation (e.g., in the case of benefactor ventures, which focus on social rather than financial goals), we did not study whether the family support provided was the consequence of economic business rationales (e.g., strategic relevance for the family firm) or altruistic reasons (e.g., support EF members with their ventures). Further research might shed light on both the role of business-related justifications and familial altruism as antecedents of support for EF members’ venturing activities.

Our last limitation refers to the lack of information on EF wealth. While not our initial research focus, we assume that such information might reveal further insights into new venture creation by EFs; for example, whether EF wealth affects decisions to engage in new venture creation and relates to levels of family support in terms of providing financial and nonfinancial resources to EF entrepreneurs. Collecting such information, however, is likely to be difficult, given that EFs are highly reluctant to share such information with outsiders. Consequently, this study’s main limitations suggest several future research directions.

First, the importance of family harmony and the desire to avoid negative conflict was a key behavioral driver in the observed venture cases. While the outcomes of conflict in family firms are well documented (e.g., Kellermanns & Eddleston, 2004), counterintuitively, very little is known about family firm conflict management. This fact points to the need to focus on understanding conflict and its management better not only in EFs but also in the general family firm literature. Family members exiting firms, founding their own ventures, and maintaining fruitful family member relationships can be very desirable outcomes. Future research is necessary to understand why such exits do (or do not) occur and whether these outcomes can be facilitated by family governance (e.g., De Massis et al., 2016).