Abstract

Entrepreneurs are driven by varied motives ranging from financial gain to social impact and more. Understanding this multifaceted landscape of entrepreneurial activity often requires a standardized outcome metric. Relying on measures specific for single types of entrepreneurs fails to account for this diversity and to conduct studies targeting wider samples. Thus, we argue that venture survival could serve as a more universally applicable performance measure. As a baseline for all entrepreneurial types, it represents a prerequisite for growth, profitability, or impact. This research note thus calls for adopting venture survival as a foundational metric, enabling researchers to delve deeper into different entrepreneurial motivations, providing practical guidance for entrepreneurship research. Future studies should furthermore explore differences between the survival of the company and of the venture's core idea.

Keywords

When trying to understand the vast and diverse landscape of entrepreneurship, having some kind of dependent success or performance variable seems imperative. If we want to understand how different entrepreneurial activities, support programs or characteristics of entrepreneurs influence the performance of a venture, we ultimately need an outcome to investigate regarding such influences. To be practically relevant – for instance, for policy makers or entrepreneurship support providers – this outcome must be normative and comparable across studies focusing on different aspects of entrepreneurship. It should enable us to identify whether a high or low score on the outcome is desired or not.

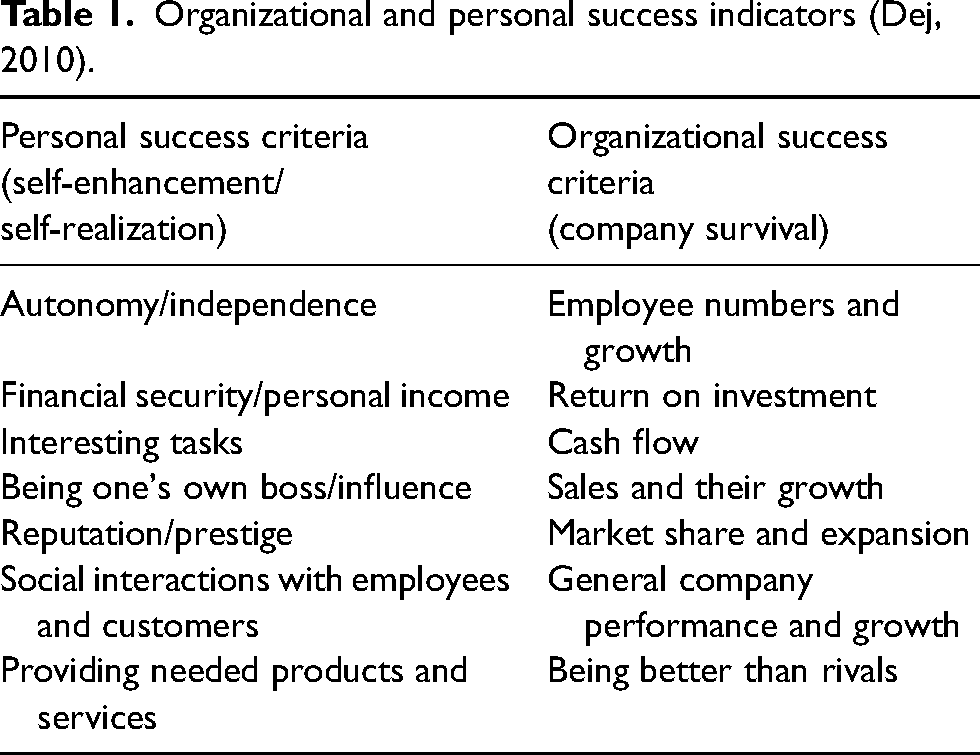

As success in entrepreneurship is a complex phenomenon, there is a wide array of financial and non-financial outcome indicators (Dej, 2010: Table 1). Those range from entrepreneurial intent and achievement motivation (ACH – e.g. Collins et al., 2004; Krueger et al., 2000), over the establishment of a formal company, to revenue, profitability, growth, as well as impact indicators related to the physical, societal or economic environment of the venture (e.g. Murphy et al., 1996; Subedi, 2021; Zahra and Covin, 1995). However, authors often remain vague in their statements on the measurement of survival (e.g. Jalil et al., 2021; Mitze and Makkonen, 2024).

Organizational and personal success indicators (Dej, 2010).

Investigating the extant literature, we see that traditional economic measures are dominating the field. For instance, a comprehensive literature study researching the relationship between human resources and entrepreneurial success finds that all papers exclusively use growth, profitability and size as the success criteria (Unger et al., 2011). A rare example of a different approach is provided by Wach et al. (2016), who conceptualize entrepreneurial success in a subjective way as understood by the entrepreneurs themselves, rather than using constructs imposed by politics or research. A reason for the extensive use of financial measures might be that non-financial or personal criteria are just that, very personal and subjective – thus being hard to deploy as a systematic measure in a study.

So why do we argue for venture survival? To answer this question, we first require a working definition, as there is no generally accepted one yet (De Cock et al., 2020; Löfsten, 2016; Stenholm and Renko, 2016). Grounded in the definition of entrepreneurship, we can define a venture as an entrepreneurial project striving to explore and exploit opportunities for the creation of new goods or services (e.g. Cunningham and Lischeron, 1991; Shane and Venkataraman, 2000). As emerging organizations, such ventures face the liability of newness (Stinchcombe, 1965; Yang and Aldrich, 2017), often lacking resources or capabilities that established organizations already possess (Soto-Simeone et al., 2020). Thus, venture survival can be defined as overcoming this liability of newness by the continuity of operations and prevailing as an economic entity (Chrisman et al., 1998; Josefy et al., 2017; Terjesen et al., 2016). This can be regarded as a dichotomous indicator: a venture is either operational (alive) or not (discontinued). This approach may be particularly useful for large-scale or cohort-based studies where comparability across different types of ventures is essential. At the same time, we acknowledge that survival can also be assessed using more nuanced metrics, such as time since founding or continuity of operations, depending on data availability and research design. While the binary measure provides a shared baseline, these alternative metrics offer additional depth, especially in longitudinal studies where the dynamics of survival are of interest.

While the concept of venture survival applies across firm stages, this paper focuses on early-stage ventures – nascent or recently founded firms still navigating the ‘liabilities of newness’ (Stinchcombe, 1965). At this stage, survival is a particularly relevant performance measure, as discontinuation risks are highest and harder to separate from financial or social outcomes. For more mature firms, we recognize that other metrics such as profitability, impact, or growth may carry greater relevance.

This conceptualization of venture survival as the absence of venture failure (Morse et al., 2007; Soto-Simeone et al., 2020) is a quite controversial measure of entrepreneurial performance. For instance, venture capitalists claim the barely surviving companies (lovingly nick-named as ‘living dead’, e.g. Ungerer et al., 2021) are much worse for society than bankrupted ones, as the former continue to lock up human and financial resources while creating little economic value (Bourgeois and Eisenhardt, 1987; Ruhnka et al., 1992).

However, not all entrepreneurs want to create economic value. According to a range of studies, motivation for entrepreneurship is highly varied and individual (Amit et al., 2001; Birley and Westhead, 1994; Hessels et al., 2008; Jayawarna et al., 2011; Toscher et al., 2019). The reason for choosing the life of an entrepreneur depends on the individual's values, passion, motivations and attitudes (Cardon et al., 2009; Gollwitzer and Brandstätter, 1997; Fayolle et al., 2014), and varies between a combination of autonomy or independence, increasing wealth and necessity (Carter et al., 2003; Cassar, 2007; Douglas and Shepherd, 2002; Feldman and Bolino, 2000; Hessels et al., 2008; Hughes, 2003; Shane et al., 2003; van Gelderen and Jansen, 2006), positive impact on society (Carsrud and Brännback, 2011; Kirkwood and Walton, 2010; Linnanen, 2016; Shepherd and Patzelt, 2011; Williams and Shepherd, 2016), self-realization or procedural utility (Benz and Frey, 2008; Cardon et al., 2009; Carter et al., 2003), plain necessity or lack of other options (Acs, 2006; Baum et al., 2007; Block and Koellinger, 2009; Reynolds et al., 2001; Shane et al., 2003). This is also reflected in a new role of venture capital, where an increasing importance of investments in the social and ecological context, not relying on purely economic performance measures, can be seen (e.g. Barber et al., 2021; Croce et al., 2021; Dhayal et al., 2023). Thus, measuring the success of an entrepreneur solely motivated by contributing to a more sustainable world with revenue or profit seems as unreasonable as measuring the success of entrepreneurs solely wanting to get rich with their social impact. For investors and venture capitalists prioritizing sustainable growth, survival metrics may thus serve as a useful early indicator of potential returns and stability.

One could try to measure them individually, separating the entrepreneurs into different types, such as commercial, and social entrepreneurs, high-technology entrepreneurs, lifestyle entrepreneurs, sustainability entrepreneurs, senior entrepreneurs, mum-preneurs, refugee-preneurs, and many more. However, doing that solely based on their motivation involves the risk of missing out on communalities and differences between these sub-groups – you run the risk of not seeing the forest for all the trees (Douglas et al., 2021). You also ignore the fact that individual entrepreneurs may fit into more than one of the above-mentioned groups simultaneously (Toscher et al., 2019). It is completely possible to be a senior, a refugee and a social entrepreneur at the same time, further complicating the picture.

Can we exemplify how certain outcomes will not be a consistent performance measure across different motivations? We know that revenues vary significantly based on entrepreneurs’ main motivation. The median annual revenue of an entrepreneur with financial motives is more than double the one from an entrepreneur out of necessity/lack of alternatives (Toscher et al., 2019). Thus, for a study that would, for instance, focus on solely analysing financially motivated entrepreneurs, revenue may be a useful indicator. On the other hand, for comparing the performance of differently motivated ventures, other measures might be more useful.

Thus, venture survival simply is the least common denominator for different types of entrepreneurs and represents the only reasonable object of comparison between them. After all, if your venture does not exist, you have no chance of achieving either growth, profit, or impact. Looking at it from the other side, venture survival represents the prerequisite for growth, profit, or impact to be achieved. This reduces the complexity of many interacting success factors to one simple dichotomy positively related to all possible performance indicators. Compared to other measures, venture survival provides a more universally applicable baseline, as it avoids the inconsistencies that arise when comparing financial and non-financial outcomes across ventures driven by different motivations. Policy makers and economic development agencies could use venture survival as a practical indicator for evaluating the effectiveness of entrepreneurship support programs. Focusing on the longevity of ventures, these stakeholders gain insights into the impact of their policies on fostering sustainable business environments. Moreover, entrepreneurship support programs that possess a wider target group of differently motivated ventures can use the measure as a benchmark to assess the success of their interventions. Survival metrics help these organizations understand which types of support correlate with long-term resilience, guiding resource allocation and program adjustments.

On this basis, there are opportunities for future cross-sectional studies of differently motivated ventures with a single comparable outcome variable, as well as opportunities for identifying new target-group-specific outcome variables adapted to different types of entrepreneurs and their ventures. The possibility of investigating venture survival can thus be used as a starting point for the development of new indicators. For example, different approaches for measuring the social impact of socially motivated entrepreneurs can be tested and compared across surviving and non-surviving ventures. That way, venture survival can be used as a prerequisite for venture performance to calibrate finer-grained outcome variables. Thus, for the purposes of trying to understand the broader picture of entrepreneurship in a way that provides normative advice for practical entrepreneurs, the advantages of using venture survival as the main outcome variable may outweigh its disadvantages.

In addition to intensifying comparative studies across different venture types to better understand their commonalities and differences, future research should address further developing the measurement of venture survival. There are already opportunities beyond relying on a venture being formally registered, such as checking for the existence of any revenue, transaction relations or (social) media presence (Ungerer et al., 2021). Operationalizing venture survival may benefit from such additional indicators, ensuring the suitability for one normalized measure for different venture types that can account for economic and non-economic goals.

An important avenue for future research lies in clarifying the relationship between venture survival and the construct of the entrepreneurial opportunity (Shane and Venkataraman, 2000). As highlighted by Ramoglou and McMullen (2024), opportunities are tied to the imagination of the entrepreneurs (Bylund and Packard, 2022) and the tangible entities they create in the course of entrepreneurial action (Alvarez and Barney, 2007; McCaffrey et al., 2023). While a registered company can constitute one such tangible entity, it might be the case that entrepreneurs continue to explore and exploit the same opportunity even when one company vanishes. The opportunity can outlive the company.

Building on this reasoning, we argue that venture survival should be analytically distinguished from company survival. Where data allows, it may be more meaningful to track the continuity of the opportunity enactment, rather than focusing solely on the persistence of a registered entity. We thus propose the entrepreneurial project as a more comprehensive unit of analysis – capturing the continued pursuit of a perceived opportunity across formal entities, informal efforts, or side-projects. In this framing, venture survival refers to the persistence of this broader opportunity enactment, rather than the survival of a single legal entity. This shift enables a more opportunity-centric perspective, consistent with theories of opportunity actualization.

This broader framing aligns with opportunity actualization theory (Ramoglou and McMullen, 2024), which conceptualizes survival as the temporal window during which an opportunity is being actively actualized. Measuring survival at this level could offer a more nuanced understanding of entrepreneurial resilience, especially in contexts where legal entities are fluid but opportunity pursuit remains continuous.

Footnotes

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.