Abstract

In this article, we examine how the sovereign state of Australia used accounting to assert its monopoly of sovereignty by suppressing the micronation of the Principality of Hutt River. With an increasing trend toward postnationalism, the status quo of sovereign states as sole providers of citizenship has been challenged by micronations. The Principality of Hutt River adopted the formal trappings of a sovereign state to uphold its independence from its host state, Australia. However, Australia responded through boundary work. Accounting was mobilised to deliver the coup de grâce to the principality by constraining its financial resources through a legal battle over tax collection. The Principality of Hutt River's formal trappings of a sovereign state and Australia's reaction through boundary work in dismissing any potential legitimacy for the micronation towards sovereignty illuminate the notions of the advent and operation of micronations in competition with sovereign states and the roles of accounting in the advance of a post-national zeitgeist.

Keywords

Introduction

In January 2020, the Principality of Hutt River closed its borders to foreigners due to financial hardship from owing the Australian Taxation Office (ATO) AUD 3 million (Meachim, 2019). The principality subsequently announced it was rejoining Australia, placing the property comprising the micronation on the market for sale to raise the funds to pay the debt to the ATO. The demise of the principality through the taxation system of the host state sent a shockwave throughout the micronational community and led other micronations to undergo accounting reforms and register themselves as nonprofit entities. 1

In this article, we examine the role of accounting in societal transformation (Brighenti, 2010; Turner, 2017; Womack, 2012), including the increasing levels of postnationalism in liberal societies in the twenty-first century. We examine how a sovereign state used accounting to suppress a micronation, thereby asserting its monopoly on sovereignty. The research question addressed is: How was accounting used by a sovereign state to suppress the performance of micronationality? Applying interdisciplinary theories for understanding, critiquing and explaining accounting in different contexts reveals accounting as an instrument of power and control in organisations and society (Carnegie et al., 2020; Napier, 2009).

With an increasing trend toward post nationalism, the status quo of sovereign states is challenged by micronations because, under the perspective of a post-nationalist realpolitik, sovereign states could lose ground as the sole providers of state membership (Anderson, 2006; Bloemraad, 2004; Hobbs and Williams, 2021b; Keating, 2018). The growing establishment of micronations (e.g., Hobbs and Williams, 2022; Ryan et al., 2006) and the performance of micronationality (e.g., Hayward, 2018, 2019a, 2019b) serve as evidence of how individuals and organisations are willing to decouple from sovereign states.

A micronation – and thereby whoever performs micronationality – is not recognised as a nation or sovereign but nevertheless mimics acts of sovereignty by adopting the formal trappings of a sovereign state (Hobbs and Williams, 2022). 2 Micronations challenge existing understandings of nationalism and globalism (Hobbs and Williams, 2021b) since the performance of micronationality serves as a small-scale exercise of sovereignty that clarifies the way you think ‘about the world, and about the role that you and the established country from which you are seceding play in it’ (Strauss, 1999: 30). The micronation examined in this article is the Principality of Hutt River, surrounded by the State of Western Australia and whose host state is the Commonwealth of Australia.

Although a disagreement with the Western Australian state government regarding wheat quotas was the raison d’être of the principality's unilateral secession in 1970, the principality subsequently flourished due to tourism, notoriety and publicity received through a succession of challenges against the Australian Government. The principality maintained that it was not subject to legislation passed by the Australian federal government or the Western Australian state government. The most recent dispute between the principality and the Australian Government was over the non-payment of goods and services tax (GST), which made the principality a cause célèbre. Unsurprisingly, the Australian Government considered the principality a thriving business. In 2020, 50 years after Leonard Casley unilaterally seceded from Australia to create the principality, the principality ended its existence by rejoining Australia. Casley died in 2019, leaving an AUD 3 million debt to the ATO due to a lengthy, unsuccessful legal battle over tax collection within the principality. This article investigates the story of the principality from its unilateral secession from Australia in 1970 to its abeyance in 2020.

In this article, we present the increasing number of micronations as a product of postnationalism (Archibugi et al., 1998; Bloemraad, 2004) and the reaction from the Australian Government framing the principality's actions as boundary work (Gieryn, 1983, 1999). The evidence regarding the principality is analysed through the lens of established political rationalities and technologies as presented by Miller and Rose (1990). Governing a state involves a constant succession of programmes, and a dual nature is identified (i.e., political rationalities and technologies) in these formal trappings of a sovereign state. It is important to note that the whole draping of political rationalities and technologies must be steeped in the performance of micronationality. Therefore, although inevitably accounting is relevant to the narrative by leading to the demise of the principality, accounting is only part of the history examined in this article.

We show how accounting was used by the Australian Government as an apparatus of power, being a territorialising activity and a subjectivising practice (Mennicken and Miller, 2012; Miller and O’Leary, 1987; Miller and Power, 2013). There is an evident tension due to post-nationalism propelling a new status quo, whereas the establishment invokes boundary work as a reactionary impulse. Hence, this article is motivated by the increasing relevance of micronations with the advance of a post-national zeitgeist. 3 This article contributes to Australian history since it records the trajectory of one of the most notorious and lasting micronations in Australia. Although a young country, Australia is noteworthy for its (unsuccessful) secessionist movements (e.g., the Eureka Rebellion in 1854, Princeland in 1861–1867, Western Australia in 1933) and micronations (Roth, 2015; Ryan et al., 2006), with the Principality of Hutt River being branded one of the more obscure footnotes in Australian political history (Botterill, 2012). 4 Finally, this article broadens the perspective of accounting beyond examining its role in sovereign states (e.g., Constable and Kuasirikun, 2007; Neu and Graham, 2006; Spence, 2010) to investigate the role of accounting in suppressing a micronation (Kurunmäki et al., 2011). Despite the increasing research focus on micronations in law (e.g., Hobbs and Williams, 2021b), political science (e.g., Furnues, 2018), geography (e.g., Hayward, 2019a), vexillology (Hayward, 2019b) and performative arts (e.g., Motum, 2025), there is no accounting research on micronations. Therefore, we are addressing a literature gap since this article also broadens the perspective of accounting, including entities ‘from below’, which have previously been ignored in accounting research, that is, micronations (Napier, 2006).

The remainder of this article is structured as follows. The next section describes the concepts examined in this study, followed by a section on the research method. A further section provides a brief history of the Principality of Hutt River, which is followed by a section presenting the performance of micronationality. An analysis and discussion are then provided, and, finally, the last section concludes the article.

The state, postnationalism and boundary work

Accounting functions as a cohesive and influential mechanism for economic and social management (Carnegie and Napier, 1996, 2012). We explore the role of accounting as more than a technical practice, expanding to a social and moral practice (e.g., Carnegie et al., 2021, 2022; Twyford, 2023; Twyford and Abbas, 2023). Accounting is seen as a social and institutional practice that is constitutive as reflective of form and change in society (Napier, 2006; Walker, 2016), and examination of the interrelations between accounting and states has been a rich vein of accounting history research (e.g., Constable and Kuasirikun, 2007; Neu and Graham, 2006; O’Regan, 2010; Spence, 2010). The concepts presented in this section are the scope of accounting, statehood and the relation between the two (the first subsection), postnationalism (the second subsection) and boundary work in relation to how recognised sovereign states dismiss claims of sovereignty by micronations (the third subsection). The first subsection defines the subject matter of this study, namely, the scope of accounting, statehood and the relation between the two. Constable and Kuasirikun (2007) argue that the role of accounting for states has been largely ignored by historians and accountants, partially due to accounting's self-limiting claims. Nonetheless, thanks to the broadening of accounting research through accounting history (Carnegie and Napier, 1996), contemporary accounting research has been able to encompass this relation between accounting and the state (Colquhoun and Parker, 2012; Kurunmäki et al., 2011). Consequently, this article establishes the scope of accounting and the state as defined by Miller (1990). This is followed by the second subsection with a discussion of post nationalism, required for identifying the threat to the status quo of sovereign states as sole providers of citizenship. Finally, the last subsection identifies the rhetoric used to dismiss claims of sovereignty by micronations.

It is worth noting that accounting, postnationalism and boundary work are concepts belonging to different bodies of disciplines, which are used to explore and explain the role played by both the principality and the Australian Government. Applying interdisciplinary theories for understanding, critiquing and explaining accounting in different contexts reveals accounting as an instrument of power and control in organisations and society (Carnegie et al., 2020; Napier, 2009). By looking to other disciplines, the perspective of accounting can be broadened beyond examining its role in sovereign states to examining the role of accounting in the performance of micronationality through interdisciplinarity research (e.g., Carnegie et al., 2021; Mennicken and Espeland, 2019; Twyford and Abbas, 2023).

Accounting and the state

In this section, we present the scope of accounting, statehood and the relation between the two. Since the performance of micronationality involves adopting the formal trappings of a sovereign state, including accounting practices, the concepts of political rationalities and technologies (Miller, 1990) are used to examine the performance of micronationality.

Government and accounting are not easily separable constructs because the operationalisation of governmental programmes requires the deployment of the calculative practices of accounting, and such calculative practices of accounting take form in association with particular conceptions of government and of the appropriate mechanisms through which they are enacted (Lemke, 2001; Miller, 1990). Accounting can be defined as the use of numerical, monetarised calculations and techniques that mediate relations between individuals, groups and institutions (Miller and Napier, 1993). Accounting is more than a technical mechanism for recording transactions; it is a process of attributing financial values and rationales to a wide range of social practices (Miller, 1990). Through this perspective, accounting becomes a central component of a broad range of practices of economic calculation rather than an independent set of techniques that have come to play a pivotal role in organising contemporary economic and social life (Mennicken and Miller, 2012). In this regard, Miller (1990) defines the state as an assemblage of practices, techniques, programmes, knowledge, rationales and interventions that are at most provided with temporary unity and individuality.

Understanding what the state is involves an examination of the practices of government. The state is considered a particular form taken by the government and not the other way around (Miller and Rose, 1990). Therefore, the state is a composite reality whose materiality and effects arise from practices and rationales delivered by a government seeking to programme and intervene in economic and social life. Governing a state involves a constant succession of programmes. Consequently, the formal trappings of a sovereign state have a dual nature identified by Miller (1990) as based on political rationalities and technologies.

Miller (1990) defines political rationalities as statements, claims and prescriptions that set out the objects and objectives of the government. These statements, claims and prescriptions will take a form amenable to political scheming, argumentation and deliberation (Miller and Rose, 1990). Political rationalities highlight the goals and principles to which the activities of government should be directed, revealing the ideals or principles to which government is devoted. This nature directs government discourse surrounding matters such as what and how to govern and the principles of government. The political rationalities used by the government are operated by technologies, which are defined by Miller (1990) as a wide range of calculations, procedures and mechanisms of government. Such technologies embody the interventionist power of the government. As Miller and Rose (1990: 8) explain, if political rationalities bring reality into the domain of thought, these ‘technologies of government’ seek to translate thought into the domain of reality and to establish ‘in the world of persons and things’ spaces and devices for acting upon those entities that they dream and scheme about. Interestingly, political rationalities are exemplified through the distinctive use of language, depicting reality thinkable in such a way that it is agreeable to political deliberation (Rose and Miller, 1992).

The programmes of government articulated by political rationalities are deployed through technologies (Miller and Rose, 1990). Accounting is a subset of the technologies of government, with tax collection being considered part of these accounting practices (Boden et al., 2010; Sikka and Hampton, 2005). Accounting information provides insights that enable future political and economic interventions to be planned and implemented (O’Regan, 2010). Accounting can be used to provide vital information that is then used to intervene on subjects, acting in subtle and unseen ways to discipline and to make people knowable and calculable from a distance (Miller and O’Leary, 1987).

Hopwood (1987) argues that accounting originates from social conflicts enacted in the organisational arena. Based on research on the interrelations between accounting and the state (e.g., Baker and Rennie, 2017; Bartocci and Natalizi, 2020; Constable and Kuasirikun, 2007; Gomes et al., 2014; Kuasirikun and Constable, 2010; Neu and Graham, 2006; O’Regan, 2010; Platonova, 2009; Spence, 2010; Yayla, 2011), such a statement can be expanded beyond the organisational arena to the relation between accounting and the state (Kurunmäki et al., 2011). For instance, Spence (2010) documents how the mobilisation of an accounting discourse was used for the formation/dissolution of a state (i.e., the Treaty of Union between England and Scotland of 1707), and Neu and Graham (2006) examine the role played by accounting in the process of nation building in Canada. Kuasirikun and Constable (2010), O’Regan (2010) and Sargiacomo (2015) show how accounting practice can be used by the state as an instrument to organise society. In their discussion on accounting for the state, Constable and Kuasirikun (2007) argue that accounting has contributed in both economically and socioculturally instrumental ways to the formation, consolidation and maintenance of the nation state in the modern era. As an apparatus of power, accounting is an inherently territorialising activity, making both physical and abstract spaces calculable (Mennicken and Miller, 2012; Miller and O’Leary, 1987; Miller and Power, 2013).

Postnationalism

Having defined accounting and the state, we now focus on the notion of postnationalism. We use postnationalism as the lens through which we identify micronations as a threat to the status quo of sovereign states as sole providers of citizenship and to explain why the Australian Government deemed it necessary to assert its monopoly of sovereignty over the principality.

Key principles that shape states include the principle of sovereignty (or self-determination), from which derives the principle of multilateral security, or the notion that each state has the right to defend its sovereignty, and the balance of powers, or the idea that in the arena of international affairs states are regarded as equals, irrespective of population or geographic size (Chirindo, 2018). However, with the rising influence of multinational corporations and transnational institutional authorities (the United Nations, the European Union, the North Atlantic Treaty Organization, etc.) and increased international economic links, it is increasingly difficult for sovereign states to operate in isolation, since external authorities have developed a growing influence over the internal affairs of sovereign states (Archibugi et al., 1998; Palacios, 2004). Hence, the question arises as to whether sovereign states have become less significant (Panić, 1997).

There is much contentious debate on whether globalisation is changing the face of geographical boundaries and leaving the world devoid of territorial sovereignty (Furnues, 2018). The state, as a particular form taken by the government (Miller and Rose, 1990), has been a key player in intervening in people's lives (e.g., Anderson, 2006; Scott, 1998), but what represents a community has been rapidly changing, including to whom the members of the community choose to subject themselves (Tiryakian, 2011). The concept of a territory subject to a state has gone beyond the definition of a given area towards the creation of ‘ordered social relations, which are, in many cases, relations of dominance’ (Brighenti, 2010: 67). Consequently, postnationalism arises as the idea that, over the long term, sovereign state membership will cease to be relevant as rights are increasingly invested in the individual and not in a legal relation between individuals and the state (Bloemraad, 2004). Advanced technologies have provided greater interconnectedness and more choice, allowing people to choose which groups they perceive and recognise themselves as belonging to (Furnues, 2018; Garcia, 2015; Hobbs et al., 2023). Postnationalism challenges the idea that the sovereign state is indispensable to the functioning of the domestic rule of law and the order of international affairs (Archibugi et al., 1998). The monopoly of sovereign states towards a territory is questioned as follows: The most important political and legal implication of a relational and processual conception of territory is that, despite claims to control and monopoly, despite hegemonic homogeneity-claiming plans, each territory is as heterogeneous as the ensemble of subjects and agents who form it by inhabiting (territorialising upon) it. (Brighenti, 2010: 68)

Some researchers use postnationalism to argue that, due to international human rights institutions and conventions, immigrants will not integrate into their new host states, since their rights are guaranteed (e.g., Jacobson, 1997; Soysal, 1994). Bloemraad (2004) brands this argument regarding the integration of immigrants as strict postnationalism, and this is not the perspective of postnationalism explored in this study. For this article, we examine what Bloemraad (2004) brands weak postnationalism. Proponents of weak postnationalism argue that the deterioration of sovereign states leads to increased claims of plural citizenship (i.e., individuals claiming multiple citizenship). Interestingly, there has been an evident change in how claims of plural citizenship are viewed. In the nineteenth and early twentieth centuries, Western states engaged in the human equivalent of turf contests over individuals. State power was correlated with the control of resources, and states sought to control all resources, both physical and human. Just as world order was undermined by unclear jurisdiction over and competing claims to territory, this was also the case for persons (Hartley, 2010; Spiro, 2018).

This detachment of the individual from the state and the resultant deterioration of sovereign states are attributable to both internal and external processes. First, the state's position as the predominant unit of social organisation (Scott, 1998) is being eroded from the outside by forces of globalisation and the shifting of the locus of power from the national to the supranational and transnational levels. Second, the state's legitimacy, authority and integrative capacities are being weakened from within by the increasing pluralisation of modern liberal societies (i.e., nonauthoritarian states; see Koopmans and Statham, 1999). Elements of the transition depicted by postnationalism regarding the individual decoupling from the sovereign state have been foretold by Miller and Rose (1990). Under postnationalism, individuals rely on their individual rights and argue that their identities transcend the ‘trappings of citizenship’ (Bloemraad, 2004: 397). Therefore, Spiro (2006) argues that plural citizenship may emerge as a feature that is defining and irreversible in a new era where membership in states is relegated to the level of membership in other forms of association. Globalisation can encourage the reactive creation of micronations with societal demand moving away from the uniformisation offered through globalisation (Furnues, 2018; Garcia, 2012).

Although sovereign states are being challenged, the state will remain a robust form of association, but one situated along a scale with other forms of community, rather than standing in a separate category of its own (Spiro, 2006). As sovereign states weaken, national cultures thrive and grow through their breakup into regions and potential new states (Furnues, 2018). Spiro (2006) goes further in arguing that the post-national era will witness a rise of challengers to sovereign states, which, however, are unlikely to fully emulate the formal trappings of sovereign states for years to come. Anyone who controls a territory can claim independence, but unless key powers give support, the odds are heavily weighted against creating an independent sovereign state (Clanton, 2008; Furnues, 2018; Strauss, 1999). Consequently, micronations are not identified as sovereign states by their host state. Nonetheless, with the ongoing deterioration of sovereign states, many individuals have tried to establish micronations, declaring autonomy from their host state (Strauss, 1999).

Boundary work

Having articulated and defined the scope of accounting and the state and given the perspective of postnationalism adopted in this analysis, we now focus on the notion of boundary work. We use boundary work to identify the rhetoric used by the host country to dismiss the principality's claims of sovereignty.

Boundary work involves applying strategies to establish, obscure or dissolve distinctions between groups of actors (Gieryn, 1983, 1999). The boundary work rhetoric is often used to support a group's goals for the expansion, monopolisation or protection of its autonomy, and in accounting research it has been examined regarding accounting professionalisation, audit practice and tax regulation (e.g., Annisette, 2017; Gracia and Oats, 2012; Humphrey et al., 2009; Sidhu et al., 2021). However, in this article, we draw on boundary work as a means of distinguishing between two different entities, micronations and sovereign states. Boundary work is useful for understanding relational processes between the different entities (Lamont and Molnár, 2002). Entities that identify themselves as the higher-status group tend to defend existing boundaries, whereas those entities identified as the lower-status group often strive to change these boundaries (e.g., Bucher et al., 2016). When the goal is monopolisation, boundary work excludes rivals from within by defining them as outsiders with labels such as pseudo, deviant or amateur (Gieryn, 1983: 792). In this article, we focus on the monopolisation of sovereignty by the host state, henceforth, precluding the micronation (i.e., the newcomer) from the status of a sovereign state: The demand for respect constitutes the consensual side of territorial relationships, a consensus which makes ordering attainable. Territorial respect is primarily focused on the other and her ownership. A demand for respect of the other qua owner is directed, in the first place, towards the newcomer. Territory helps stabilize a certain distribution of respect by setting up a visible stage for the taking place of the relationships which are played out interactionally. (Brighenti, 2010: 68)

It is noteworthy that the labels used for micronations often express a tacit lack of respect towards the newcomers striving for legitimisation. Thereof, entities belonging to the higher-status group (i.e., the sovereign states) attribute selected characteristics that establish what comprises a sovereign state for the purposes of constructing a social boundary that distinguishes the lower-status group (i.e., the micronation) as not belonging. Such selected characteristics attributed to sovereign states can be established through both statutory and conventional practices (Carlson, 2016). For this article, the Australian Government represents the host state from which the Principality of Hutt River unilaterally seceded.

Research method

Similar to any other social phenomenon, accounting and its use are decisively influenced by the historical and geographical context in which they operate (Miller and Napier, 1993). Given the importance of understanding the processes, interactions and environments that documents represent, in this study we adopt documentary and bibliographic research. As noted by Carnegie and Napier (1996), to conduct such research, it is paramount to identify what constitutes the historical archive.

Sources

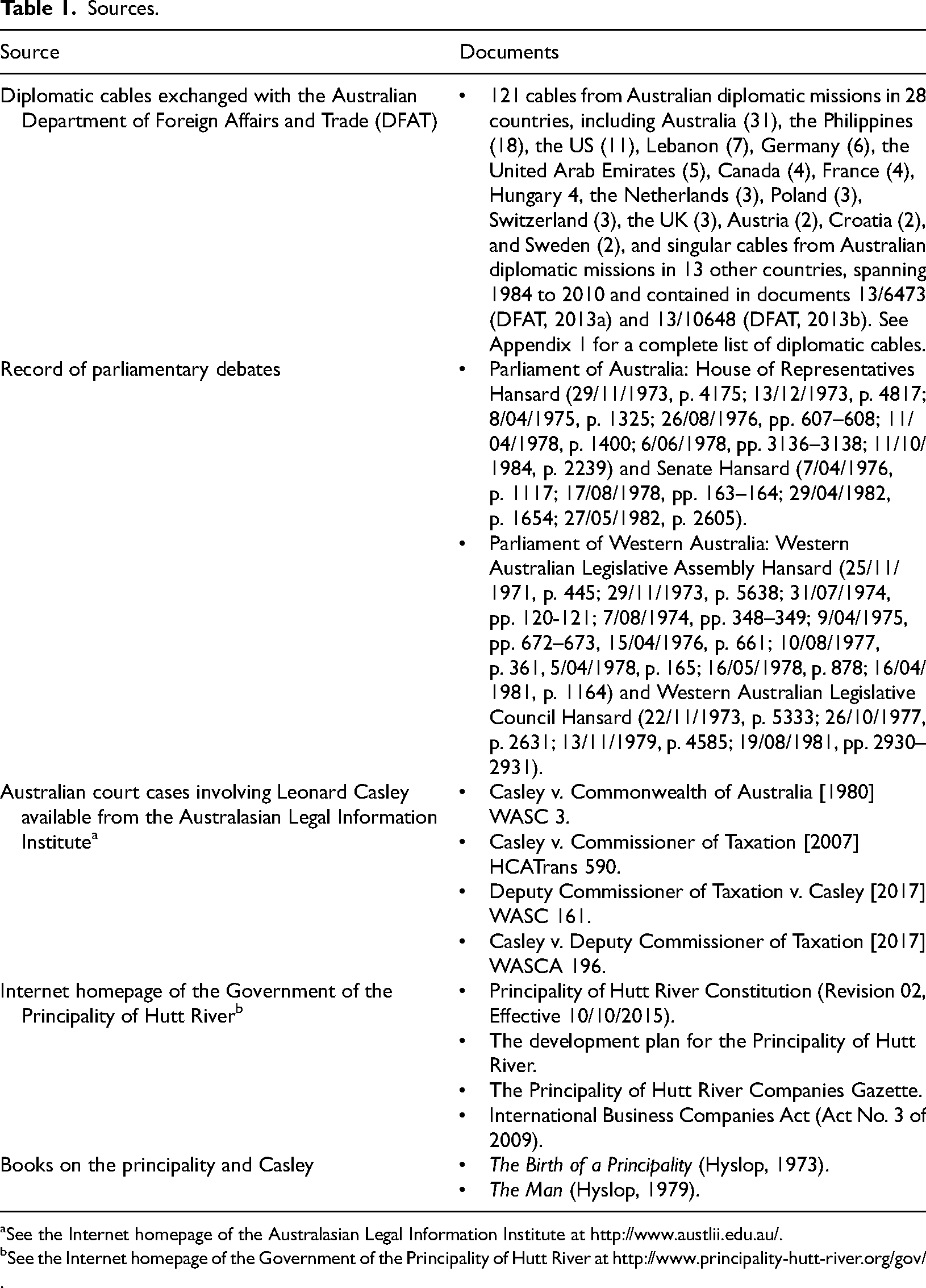

We draw from public archives, including digital sources, covering the period from the establishment of the Principality of Hutt River in 1970 to when the principality rejoined Australia in 2020. We undertake an archival search regarding the principality using Australian diplomatic cables, the record of parliamentary debates, Australian court cases, the homepage of the Government of the Principality of Hutt River, as well as books written on the principality and its founder, Casley. 5 Table 1 lists the sources for this article.

Sources.

aSee the Internet homepage of the Australasian Legal Information Institute at http://www.austlii.edu.au/.

bSee the Internet homepage of the Government of the Principality of Hutt River at http://www.principality-hutt-river.org/gov/.

Regarding diplomatic cables from the Australian Department of Foreign Affairs and Trade (DFAT), 121 spanning 1984 to 2010 and totalling 216 pages, were exchanged through Australian diplomatic missions in 28 countries concerning activities relating to the principality and were released under the Freedom of Information Act 1982. Appendix 1 has the complete list of diplomatic cables, including the reference numbers, numbers of pages, dates and locations of the Australian diplomatic missions that sent them.

Regarding the parliamentary debates, the Hansard from the Australian Parliament and parliaments of Australian states were searched for terms such as Leonard Casley, Prince Leonard, and Hutt River. The parliamentary sessions used in this study are not exhaustive because some sessions referred to the principality only in passing. Since the Australian Government did not recognise the Principality of Hutt River as a sovereign state, court cases regarding the principality were aimed towards members of the Casley family (Meachim, 2019).

Data analysis

For this study, the data analysis was conducted using a qualitative approach drawing on multiple sources (see Table 1), covering the period beginning with the establishment of the principality in 1970, to when the principality rejoined Australia in 2020. After identifying sources, a search for news related to the principality was carried out, producing more data for analysis and contextualisation (Meachim, 2019; Murphy, 2010).

We adopted an interpretive textual analysis approach to analyse the data (Laine, 2009; Safari et al., 2020). The interpretations were developed through a two-phase process of subjective sensemaking, involving multiple rounds of reading and efforts to organise the findings into a coherent understanding in which all authors were involved. In the initial reading phase, all passages related to the concepts under investigation in this study were highlighted. This resulted in the creation of an archive comprising several documents. Following a second reading of these documents, relevant portions were compiled. These excerpts consisted of brief extracts from the original documents and were accompanied by notes based on the concepts pertinent to this study. In certain instances, direct quotations were deemed less significant and detailed notes were taken instead. This process not only unveiled key factual events concerning the principality but also shed light on the rhetoric employed by sources associated with the principality and those linked to the Australian Government. The final interpretation of the first phase was subsequently refined through an iterative process that paid constant attention to commonalities and differences among documents, the emergence and fading of dominant themes over time, shifts in expressions used and more. During the second reading phase, a meticulous comparison was made between the initial interpretation and the interpretation generated in this second stage. This led to another round of reading of the original dataset and the comprehensive research notes crafted during the analysis stages. Ultimately, the original interpretation was revised considering the insights gained from this additional round of reading and the points discussed.

The books written by Hyslop (1973, 1979) in collaboration with Casley and content provided on the homepage of the Government of the Principality of Hutt River are biased towards the principality and provide rhetoric favourable to it, whereas documents from the Australian DFAT, the record of parliamentary debates, and the Australian court cases are biased against it and provide rhetoric favourable to the Australian Government. Consequently, to maintain an objective view of the events, evidence from one set of sources was often counterbalanced with evidence provided from the other set of sources. From the interpretive textual analysis of the data, it was possible to identify the major factual events regarding the principality and the difference between the rhetoric used by the principality and that used by the Australian Government.

When analysing the data and working on the arguments, we identified and paid attention to the different units of analysis because conflating them would compromise the quality of the analysis and undermine the narrative of the manuscript (e.g., Buckley, 2021; Lubinski, 2018). Some concepts and evidence pertain to sovereign states, some are geared towards the performance of micronationality (i.e., the principality pretending to be a sovereign state), and some are geared towards individuals (i.e., the response of the host state towards Casley and his associates). Accounting applies to all entities depicted in the case, bearing in mind the different units of analysis. The postnationalism zeitgeist, as the detachment of the individual from the state and the resultant deterioration of sovereign states, comprising ‘a pattern in meaningful practices that is specific to a particular historical time-period, links different realms of social life, and extends across geographical contexts’ (Krause, 2019: 8), and is a concept used as the backdrop for the narrative of our manuscript. Consequently, the unit of analysis permeates the host country, the principality, Casley and his associates.

Regarding the principality, Casley, and his associates as the unit of analysis, such a unit is used to identify political rationalities developed by the principality and technologies adopted by the principality to develop its economy and reaffirm its sovereignty (i.e., accounting and the state). The homepage of the Government of the Principality of Hutt River and the books on the principality and Casley provide a substantial amount of information on running the principality and its programmes of government, with a rhetoric favourable to the principality. Such evidence and such a unit of analysis are also used for examining the postnationalism of Casley and his associates, who are willing to decouple from a sovereign state and establish a micronation, challenging the status quo of the host country. There is also evidence of the principality's political rationalities and technologies in the diplomatic cables exchanged with the DFAT, the record of parliamentary debates, and Australian court cases; however, such evidence does not acknowledge the principality, since it is biased against Casley and his associates. Accounting applies to the performance of micronationality since such performance permeates the whole draping of political rationalities and technologies, including but not limited to accounting technologies. Accounting also applies to Casley and his associates, since the host state did not recognise the principality as a sovereign state and acts of suppression of the micronation were aimed towards Casley and his associates.

The host country is a unit of analysis as the entity asserting its monopoly of sovereignty over the principality, due to the challenge of the status quo of sovereign states (i.e., postnationalism). It is worth noting that such suppression is identified as boundary work, with evidence of the host country excluding the principality by identifying itself as belonging to a higher-status group with selected characteristics that establish what comprises a sovereign state for the purposes of constructing a social boundary that distinguishes the lower-status group as not belonging. The diplomatic cables exchanged with the DFAT, the records of parliamentary debates, and Australian court cases provide evidence that the Australian Government used its departments and agencies to suppress the principality's activities. Accounting applies to the host state since governing a state involves a constant succession of programmes (i.e., political rationalities and technologies), including but not limited to accounting.

A brief history of the Principality of Hutt River

The Principality of Hutt River, formerly known as the Hutt River Province, was in the Australian state of Western Australia, approximately 500 kilometres north of Perth, occupying 75 square kilometres. The principality consisted mainly of farmland and bushland, and, before the Declaration of Independence, the land was owned by Leonard Casley. The main town site was called Nain and contained the required buildings for the principality's government operations and for those serving tourism. The origins of the Principality of Hutt River date back to its founder, Casley, challenging the Western Australian Government regarding wheat quotas (Hobbs and Williams, 2021a; Hyslop, 1973). The matter is summarised in one of the cases brought against Casley by the ATO and recorded in the Supreme Court of Western Australia (Deputy Commissioner of Taxation v. Casley [2017] WASC 161: 6): In 1970 Leonard Casley was a wheat farmer. He was aggrieved by the wheat quotas allocated to his business. He served a notice of secession on the Western Australian Premier, the Governor, the Prime Minister, and the Governor-General. He also notified the Queen. Since then he has taken other steps which he believes are the acts of an independent sovereign state including declaring war on Australia. He is convinced that, in taking these steps, he succeeded in separating the Hutt River from Australia.

Once he declared independence, Casley no longer abided by wheat quotas and succeeded in becoming a non-resident of Australia for income tax purposes (Hobbs and Williams, 2021a). Soon after seceding, the principality became an international tourist attraction. In a 1972 interview, Casley stated his intention to invest more in tourism (Murphy, 2010); in 1973, a post office was opened, and by 1985, Casley had ‘built his wheat-growing property in Western Australia into a thriving tourist attraction’ (DFAT, 2013b: 193). As a member of the Western Australian Legislative Council, James McMillan Brown stated in 1981, To my knowledge, the only thing that ever came out of the introduction of wheat quotas was the setting up of the Hutt River Province by ‘Prince’ Leonard. […] As a protest against the introduction of wheat quotas and the unfair treatment that he considered he was receiving, he formed his own ‘Principality’. […] He has conducted himself quite profitably in his establishment of the Hutt River Province. (Western Australia, 1981b: 2930)

A court case held during the 1970s records that Casley failed to furnish the ATO with certain documents (Casley v. Commonwealth of Australia [1980] WASC 3). Casley was given an ultimatum to pay the fine and costs. However, a few days before the deadline, the principality declared a brief state of war on Australia (i.e., 2–4 December 1977). Casley sent a telegram to the Governor-General of Australia declaring war, and a few days later sent another telegram ceasing hostilities. The short state of war between the principality and Australia was a scheme in which the purpose was to argue that under the Geneva Treaty Convention of 12 August 1949, a government should show full respect to a nation undefeated from a state of war (Bicudo de Castro and Kober, 2018). Despite the brief state of war occurring between the principality and Australia, the fine was later paid.

The principality remained a curious attraction of the Western Australian outback for decades; as the then Western Australian Minister for Lands, Brendon Grylls, stated in 2010, Casley was still doing quite well ‘attracting people to the principality’ (Murphy, 2010). However, as tourism flourished in the principality, the Australian Government's attention moved from wheat quotas to the taxation of income generated inside the principality, and the issue of having to pay Australian taxes became for the principality a matter of questioning the sovereignty of the state itself. It is noteworthy that the issues surrounding the payment of taxes by the principality did not pertain to the local shire rates. It has been reported several times that the principality paid its shire rates, with the payment being variously reported as an annual gift, a goodwill gesture to the local community, an international courtesy or a donation (Bicudo de Castro and Kober, 2018).

Regarding the dispute between the principality and the Australian Government, the ATO claimed that Leonard Casley and his son Arthur Casley owed approximately AUD 3 million in GST, interest and penalties in taxes payable for the financial years ended 30 June 2006 to 30 June 2013 (Deputy Commissioner of Taxation v. Casley [2017] WASC 161). The GST is a federal tax that commenced on 1 July 2000. Based on the information provided by the principality, the ATO arrived at this figure based on the expected GST not collected from the principality from tourists using the principality's caravan park and from other goods sold and services provided to people visiting the principality.

Due to old age and declining health, Leonard Casley abdicated in 2017 at the age of 91, while the court case was running, and his son Graeme Casley became the new ruler of the principality. Leonard Casley passed away in February 2019. On 31 January 2020, the principality closed its borders to foreigners due to financial hardship and in August of the same year announced it was rejoining Australia, once again becoming part of the Commonwealth of Australia. In September 2020, the property was placed on the market for sale. After 50 years of existence, the principality became part of Australian history (Hobbs and Williams, 2021a).

The performance of micronationality

In this section, we illustrate how the Principality of Hutt River implemented some of the formal trappings of a sovereign state (i.e., the performance of micronationality). The constitution of such performative political rationalities and technologies is a statement of the principality as a tentative sovereign state and itself a contestation of the sovereignty of the host state. Furthering the discussion as to the reflective versus constitutive role of accounting (Napier, 2006), from the perspective proposed by Miller (1990), there is evidence that during its years of activity, the principality established political rationalities and adopted technologies to develop its economy and reaffirm its sovereignty.

Running the principality

The Principality of Hutt River had an established government and a constitution. The latest version of the Principality of Hutt River Constitution (Revision 02, effective 10 October 2015) included almost 100 articles, setting the principality as a hereditary constitutional monarchy with a national flag, a national seal, a national anthem and other symbols of state. As per the constitution, the sovereign had the right to confer orders, titles and other distinctions on any person he thought fit (art. 16). The constitution also devoted articles to liberties and fundamental rights, the right to vote, Parliament and other topics. In addition, the constitution devoted articles to the principality's National Budget (arts. 37–41) and Municipal Budget (art. 87). As described in the constitution, the National Budget included all receipts and public expenditures of the principality and represented the principality's economic and financial policy. The expenses of the Sovereign House were fixed in the budget and taken by priority from the general receipts of the budget, and any budget surplus was to be transferred to a constitutional Reserve Fund. Any budget deficit was to be drawn from the same account. The Municipal Budget was provided by the product of Municipal Services and by the budgetary allocation registered in the annual budget. The approval of the National Budget was also discussed in the constitution, where the budget had to be voted on during a session of the Parliament (arts. 70–73).

The principality's executive power was exercised by the Minister of State as the sovereign's representative, assisted by a cabinet, which consisted of ministers, vice-ministers and state secretaries. The Minister of State assumed responsibility for the executive services of government and was responsible for the day-to-day running of the principality. As of 2020, there were roles for the Ministry of Foreign Affairs, Ministry of Electronic Communications, Ministry of Finance/Treasury, Ministry of Education, Ministry of Arts and Culture and Ministry of Postal Services. In addition to the ministries, there were several government bodies, such as the Treasury, the Royal College of Heraldry, the Royal College of Advanced Research, the Royal Mint of Hutt River and the Royal Hutt River Postal Service. There was the Office of the Registrar of Companies and Banks, which was responsible for the Companies House and Companies Gazette. The Companies House handled general business names and company registrations as well as all associated licensing, and the Companies Gazette was available online on the website of the Government of the principality.

The principality also had its own defence forces, the Royal Hutt River Defence Forces (RHRDF), founded by the Royal Hutt River Defence Force Act of 1988. The RHRDF included the Royal Hutt River Air Force, Royal Hutt River Army, Royal Hutt River Navy, Royal Hutt River Military College and Royal Hutt River Legion. The RHRDF was a non-combative service charged with the security of the principality and the usual logistical functions associated with the armed forces. The RHRDF had mostly a ceremonial role both in providing a guard of honour for the sovereign and in participating in celebrations and other important occasions.

The principality drafted a development plan for the territory, as outlined by Hyslop (1979: 85): Everyone is very active with development projects, building or primary industry projects, all moving with purposeful intent toward achievement and completion. Yet other projects await available time, manpower, or the appropriate season for commencement. International banking, shipping registration, construction of an international airport, completion of the lakes, allocation of land to applicants for home building, shops, motels, caravan park, international grade hotel, casino, and duty-free shops are matters steadily moving through their various phases toward completion or achievement. The intentions, the aims, the direction in which the Government is guiding the Principality, and the purpose for all this are being considered knowledgeably and with clarity.

The principality issued regular statements through its Royal Rhetoric, which were released through the website of the Government of the Principality of Hutt River.

Programmes of government

Examples of technologies implemented by the principality include honours bestowed on people and its foreign affairs activity, postage stamps, currency, passports, driving licences and registration of foreign companies. The principality bestowed honours in recognition of people who had contributed to the principality (Hyslop, 1973, 1979), including the creation of peers and four orders of chivalry, namely, the Order of Wisdom and Learning, the Illustrious Order of Merit, the Serene Order of Leonard and the Royal Order. The Royal College of Heraldry provides the lists of honours bestowed and their recipients. 6

The principality tried to establish diplomatic missions in other countries and achieve international recognition (Bicudo de Castro and Kober, 2018). The contacts section of the homepage of the Government of the Principality of Hutt River included a list of overseas representatives/offices under the principality's Ministry of Foreign Affairs. The list contained several overseas representatives and/or offices from the Balkan States, Bangladesh, Brazil, Canada, Central Europe, France, Monaco, Pakistan, and South America and US diplomatic cables regarding the principality's activities were exchanged between 28 Australian diplomatic missions 7 and the DFAT (2013a, 2013b). The diplomatic cables have reports of people passing as diplomats or consuls for the principality in Croatia, Mexico, the Philippines, Portugal, Germany and the United Arab Emirates (UAE).

Despite having its post box, the principality struggled to receive and deliver mail in its early years. Mail addressed to the principality was treated as undeliverable until an arrangement was sought with the Northampton Post Office. The Royal Hutt River Postal Service issued the principality's postage stamps (Hobbs and Hohmann, 2023; Hyslop, 1973, 1979). However, having outgoing mail accepted by the Australian Post Office (APO) using the principality's own postage stamps was challenging, and the principality thus resorted to creative solutions: Cocos Island stamps are purchased through the APO. These are affixed to the face of the envelopes or packages. Hutt River Province Principality stamps to an equal face value are then affixed to the reverse side of the postal items. These postal items are then despatched through the APO. (Hyslop, 1979: 37)

The principality created its own coins and paper money (Hyslop, 1979), which have become collectors’ items. In 1974, the principality commissioned the printing of paper currency, and the Treasury of the Principality of Hutt River issued banknotes. In 1975, the Cabinet decided to issue coinage, which led to the formation of the Royal Mint of the Principality of Hutt River and its first coins minted in 1976. Since then, the Royal Mint has been responsible for the minting of over 200 coins, including commemorative coins.

The principality reportedly had approximately 13,000 citizens, mostly non-residents (Bicudo de Castro and Kober, 2018). The homepage of the Government of the principality provided forms for individuals interested in becoming a non-resident subject of the principality, obtaining a principality Gold Pass Photo Identification Card, applying for a Domestic Driver Licence and applying for an International Driver Permit. It appears that the principality also accepted the registration of vessels since a boat seized in the United States in 1987 claimed Hutt River registration (DFAT, 2013b). The principality issued passports for its citizens that were used to enter foreign countries (Hyslop, 1979), including diplomatic passports (Bicudo de Castro and Kober, 2018; DFAT, 2013b).

The principality accepted the registration of foreign companies through its Registrar of Companies and Banks. The International Business Companies Act (Act No. 3 of 2009) is comprehensive, with more than 100 articles devoted to topics such as company formation and constitution, company powers, restrictions and liabilities, capital and dividends, directors and officers, company administration, the registration of charges, debentures, winding up, dissolution and striking off. The Companies Gazette provided a list of five companies that were suspended and/or struck off or no longer registered in the principality. More specifically, one company was struck off for failing to pay its annual fee and penalties, two companies were suspended, and two companies were no longer registered in the principality.

Analysis and discussion

As highlighted in the performance of micronationality section, the principality has established political rationalities and adopted technologies to reaffirm its sovereignty (Lemke, 2001; Miller, 1990). The principality had a constitution, an established government, an honours system, foreign affairs activity, postage stamps, currency, passports, driver's licences and the registration of foreign companies. It must be noted the performance of micronationality does not necessarily mean the trappings are de facto carried out; for instance, although the principality declared war on Australia, there were no acts of violence, and, although the principality adopted the Hutt River Dollar, the currency was pegged to the Australian dollar and Hutt River dollars became collectors’ items, as the principality itself was using Australian dollars for all commercial transactions. Therefore, although there was a comprehensive constitution, including provisions for an annual National Budget and Municipal Budget, there is no factual evidence of its adoption. Nonetheless, the evidence points to the fact the principality had a government and an assemblage of practices, albeit both often rudimentary, that emulated the formal trappings of a sovereign state (Miller, 1990; Miller and Rose, 1990) as expected from the performance of micronationality (Hayward, 2018, 2019a, 2019b; Petermann, 2019; van Lessen and Petermann, 2021).

Boundary work

Casley did not identify the principality as a micronation, in an attempt to legitimate the principality among sovereign states. Although not recognised by sovereign states, the principality persevered for 50 years before its abeyance. Seeking legitimation, the principality took measures and experienced all three possible outcomes listed by McConnell et al. (2012: 810) regarding how secessionist states declare autonomy from their host states. The three outcomes are (1) the non-response from the Australian Government, (2) the legal imbroglios, and (3) addressing Casley as the administrator of the province. The principality claimed its sovereignty based on the 1933 Montevideo Convention on the Rights and Duties of States and the Geneva Treaty Convention of 1949. On several occasions, the principality declared its autonomy to the local and national governments, as well as applied for membership to the United Nations. When the Australian Government did not respond to its secession note, the principality maintained that a matter not contested within two years is taken as a victory, meaning that the Australian Government recognised the independence of the principality in 1972, two years after the secession note was served. When the ATO filed court cases due to the non-collection of the GST, such legal matters became an opportunity for a legal debate (and media scrutiny) over the matter of secession. When the Western Australian Government responded by addressing Casley as the administrator of the province, this was considered an acceptance of the declared autonomy of the principality.

When questioned about the legitimacy of the principality in 1971, the Premier of Western Australia responded that Any land within the boundaries of Western Australia is part of the State of Western Australia. The Government's attitude to this area is the same as that for any other part of the State. (Western Australia, 1971: 445)

A similar answer was provided by the Attorney-General of Australia when questioned about the legitimacy of the principality in 1973 (Commonwealth, 1973a: 4817). The Australian Government used its departments and agencies to suppress the principality's activities, and such suppression is especially evident against the technologies used by the principality (Miller and Rose, 1990). Examples of technologies implemented by the principality include the honours bestowed on people, its currency, its foreign affairs activity, passports and the registration of foreign companies. About the honours bestowed on people, the titles were not recognised by the Australian Government or by any other sovereign state. The Australian Government refers to the honours bestowed by the principality broadly as a scheme that has ‘no legal validity’ (DFAT, 2013a: 10). When questioned in 1975 by Ray Young, the Premier of Western Australia made clear his opinion on Casley, the principality and its titles: Mr Young: Does he [the Premier] agree that the continued use of assumed royal titles by Mr Casley and the inability of the Government to lawfully prevent such abuses could lead to a situation where the public at large and overseas visitors accept the absurdity that Mr Casley is the head of a ‘royal family’; and has any action been considered to prevent a continuation of the Casley type of misrepresentation? Premier of Western Australia: I think some people are misled. Whilst the average citizen of this State would be fully aware of the stupidity of Mr Casley's claims, people in, and from other places have less cause to realise that they are being duped. As certain elements of the media seem intent on sustaining this hoax, it may become necessary to consider what special action can be taken, if only to save visitors to this State, and people in other places, from being misled and commercially exploited. (Western Australia, 1975: 672–673)

Stamps from the principality have been called ‘postage stickers’ (Commonwealth, 1973b: 4175) and, following advice from the Australia Postal Commission in 1984, all mail addressed to the principality was endorsed as ‘address unknown’ (Commonwealth, 1984: 2239). Notably, the principality claimed its currency had parity with equivalent Australian denominations, but this claim was rejected by the Australian Government, which stated that Under Australian Law, legal tender consists only of notes issued by the Reserve Bank of Australia under the authority of the Reserve Bank Act 1959 and coins issued by the Treasurer under the authority of the Currency Act 1965. The self-styled ‘Hutt River Province’ run by a Mr L G Casley, is merely a private property on the Australian mainland and has no other standing. Items offered for sale by or on behalf of Mr Casley purporting to be legal tender have no such status. (DFAT, 2013b: 182)

Regarding foreign affairs activity, the principality was discredited by the Australian Government on all occasions in which local authorities sought advice regarding the principality's status as a sovereign state. On at least two occasions, alleged diplomats were arrested by local authorities; namely, in the UAE in 2008 (DFAT, 2013a) and in Germany in 1996 (DFAT, 2013b).

8

Regarding the occasion in the UAE in 2008, diplomatic cable AB611147L highlights how the Australian diplomatic missions reported such events to the DFAT: The ‘Ambassador’, an Iranian with French nationality, has claimed diplomatic immunity. The main local English-language newspaper today carried an article about the court hearing, and a prominent piece on Australia's refusal to recognise Hutt River, drawing on a press release we issued in October 2007 which is still on our embassy website. (DFAT, 2013a: 16)

Also notable are the Australian Minister for Foreign Affairs’ views regarding the use of Hutt River diplomatic passports by international travellers: I am aware of the claim that a Hutt River ‘diplomatic passport’ was used by a television producer to get through Customs and Immigration in Beirut. I am unaware how many of these documents have been issued by Mr Casley or to whom they have been issued. They are not of course, genuine passports. A genuine passport is a document issued by a sovereign state to a person who is a subject of that state. It is the accepted international means of identification and evidence of nationality and of the holder's right as a subject to the protection of the state which issued it as well as the preparedness of that state to extend protection. Since the self-styled Hutt River Province is not a state (in international law) clearly the documents printed and distributed by Mr Casley do not meet these criteria. The use of Hutt River Province ‘passports’ would facilitate the movements of terrorists and drug runners only as long as other countries are prepared to accept them as valid travel documents. I do not believe the abuse of these ‘passports’ should have any impact on Australia's relations with the Middle East region. In 1976, my Department advised all overseas posts that any inquiries from governments regarding the activities of Mr Casley should be advised that the Australian Government does not recognise the Hutt River Province and any assertions to the contrary are false. The Australian Government will take whatever steps are necessary to protect its international status and role in combating international terrorism and drug running. (Commonwealth, 1982: 2605)

While the principality welcomed foreign companies, the ATO warned Australian citizens not to purchase any foreign companies registered in the principality as part of a tax avoidance scheme (Murphy, 2010). When questioned in 1975 about whether residents of the principality did not pay taxation on income earned totally within the principality, the Treasurer of Australia stated that Contrary to the impression conveyed by Mr Leonard Casley, the so-called Hutt River Province has not seceded from Australia and has no legal status. The Commissioner of Taxation has advised that there is no provision in the income tax law under which persons residing in the Hutt River area of Western Australia may be granted an exemption from tax on income arising from sources in that area. (Commonwealth, 1975: 1325)

Diplomatic cable CH252073 from 1985 reinforces that ‘the Australian Government does not recognise the Hutt River Province and any assertions to the contrary are false’ (DFAT, 2013b: 193). The cable discredits the principality by defining it as a thriving tourist attraction but also states that Casley ‘pays Australian taxes and his activities generally remain within the limits permitted by Australian law’ (DFAT, 2013b: 193). However, this statement from cable CH252073 disappeared from later DFAT communications. In 2007, the High Court of Australia dismissed an application by Casley for leave to appeal against a judgment against him relating to his failure to file tax returns (Casley v. Commissioner of Taxation [2007] HCATrans 590). Based on the records, Casley argued that the principality was not part of Australia and hence not subject to Australian taxation laws, whereas the judge classified the arguments as ‘fatuous, frivolous and vexatious’ (Casley v. Commissioner of Taxation [2007] HCATrans 590: 2).

In 2009, Administrative Circular P0958 was issued (DFAT, 2013a) requesting diplomatic missions to act swiftly when identifying any international activity related to the principality. The document is quite straightforward regarding the Australian Government's position on the principality and its honours, foreign affairs, currency, citizenship, foreign companies and tax: On occasion, ‘representatives’ of these ‘principalities’ have contacted the Australian Government and other governments to seek recognition, including recognition of travel documents which purport to be ‘passports’. Further, some of these ‘principalities’, notably ‘Hutt River’, have been associated with schemes offering ‘royal’ titles, ‘diplomatic’ or ‘consular’ appointments, ‘legal tender coins’ and ‘international business companies’ purportedly incorporated or registered in the ‘principality’. Many of these schemes have been promoted through a range of websites, both in Australia and overseas. The Australian Government's position is that these ‘principalities’ have no separate sovereignty and remain subject to the Australian Constitution and the laws of Australia. As such, the purported ‘passports’, ‘royal’ titles, ‘appointments’, ‘currency’, and ‘international business companies’ have no legal validity. (DFAT, 2013a: 10)

The Australian Government's reactions to the principality's activities can be likened to boundary work against the principality (Carlson, 2016; Gieryn, 1983; Gracia and Oats, 2012). The Australian Government and its departments and agencies – such as the Australia Post, the ATO and the DFAT – discredit the principality as private property and a thriving tourist attraction, somehow likened to international terrorism and drug running. Aligned with the goal of monopolisation, it is convenient for the Australian Government to brand the principality a micronation, which can be seen as a pejorative designation, suggesting that it is not a sovereign state and should not be taken seriously. Micronations are recurrently portrayed as illegitimate, and people engaged in micronational activity are often considered eccentric (Giuffre, 2015; Hayward, 2019a; Hobbs and Williams, 2021b; Ryan et al., 2006). For instance, foreign companies registered with the principality are termed tax avoidance schemes. The use of this term to dismiss the Companies House is evidence of boundary work since it relies on linguistic concepts that serve to separate Australian legal accounting practices from tax dodgers of the principality (Gracia and Oats, 2012). Accounting was mobilised in this fashion by the Australian Government to delegitimise the principality (Lemke, 2001; Miller, 1990).

Furthermore, the use of passports issued by the principality has been likened to ‘international terrorism and drug running’ by the Australian Minister for Foreign Affairs (Commonwealth, 1982: 2605). The dismissal of honours, foreign affairs, postage stamps, currency, and citizenship and the branding of these technologies as illegal schemes via ‘us’ and ‘them’ branding, with ‘them’ being derogatory, is evident boundary work against the newcomer (Brighenti, 2010; Bucher et al., 2016). Besides suppressing the micronation, the Australian Government use of boundary work towards the principality seems like a useful strategy for suppressing plural citizenship (i.e., people with affiliations to Australia and the principality), since the host state is investing time and effort into disenfranchising citizens of the principality by branding them as participants in illegal schemes (Esmark, 2016; Hartley, 2010).

Despite the Australian Government actively pursuing the Principality through its departments and agencies, it is interesting to note how the Western Australian Government and the Shire of Northampton seemed to turn a blind eye to the matter. On different occasions, local and state governments added the principality to maps and tourist guides and had the principality listed by the Heritage Council of Western Australia (Bicudo de Castro and Kober, 2018). The evidence suggests some leniency towards the principality by the Western Australian Government due to the benefits to the tourism industry, as exemplified in records from the Western Australia Parliament. The first example is an exchange in 1977 between two members of the parliament, Reginald John Tubby and John Edward Skidmore: Mr Tubby: Around the Greenough flats and through Walkaway we have the additional tourist attraction of historic buildings. Indeed, we even have the Hutt River Province in the electorate. Mr Skidmore: It is not in your electorate, according to Prince Leonard. Mr Tubby: Perhaps I should say that my electorate surrounds the Hutt River Province. In spite of the criticism directed at the Hutt River Province, I must say it is a great drawcard so far as tourists are concerned, even if it is a once-only type of tourist attraction. I have been invited to the Hutt River Province, but I have not been there as yet. I presume if I were to go there, I might even be knighted. (Western Australia, 1977: 361)

The second example is from 1981 when the Premier of Western Australia was questioned about a news article showing Prince Leonard being welcomed by a public servant: The cutting contains a photograph which purports to show Mr Leonard Casley meeting an officer of the Regional Administration Office. I understand the officer concerned was not present as a government officer – although he is from the Regional Administration Office – but as a member of the Kalgoorlie Tourist Bureau which, I believe, is promoting Mr Casley's visit. (Western Australia, 1981a: 1164)

It is worth noting that this is the same Premier of Western Australia, Sir Charles Court, who in 1975 branded Casley's claims as ‘stupidity’ and the principality as a ‘hoax’. It can be argued that the local and state governments benefited from the attention drawn to the principality via revenues raised from increased tourist activities, and the principality did not pose a direct threat to the state and local governments. 9 Consistent with the Australian Government, the Western Australian Government did not officially acknowledge the principality as a legitimate state, but, possibly owing to the economic benefit derived from the principality, they on occasion appeared to play along with the secession claim.

Postnationalism

The Australian Government deemed it necessary to assert its monopoly of sovereignty over the principality due to the advance of a post-national zeitgeist (Keating, 2018; Spiro, 2018). Postnationalism is the idea that, over the long term, state membership will cease to be relevant, since rights are increasingly invested in the individual and not in a legal relation between individuals and the state (Bloemraad, 2004). Elements of the transition depicted by postnationalism on how individuals are willing to decouple from sovereign states have been foretold by studies examining the neoliberal agenda (e.g., Lemke, 2001; Miller and Rose, 1990). The government refers to a continuum extending from the political government to forms of self-regulation. Within this continuum, the neoliberal agenda shifts responsibilities for social risks and for life in society into a domain for which the individual is responsible, implying a withdrawal of the state (Lemke, 2001; Womack, 2012). With the weakening of the benefits of being a member of a sovereign state, there has been increased demand for plural citizenship, fostering the rise of entities that emulate formal trappings of sovereign states (e.g., Bicudo de Castro and Hayward, 2021; Bicudo de Castro and Kober, 2019; Tiryakian, 2011). Bloemraad (2004) argues that the short-term result of globalisation will be increased claims of plural citizenship where it is permitted. Advanced technologies have provided greater interconnectedness and more choice, enabling people to choose which groups they perceive and recognise themselves as belonging to (Furnues, 2018; Hobbs et al., 2023). Therefore, neoliberalism and globalisation have encouraged the reactive creation of micronations with societal demand moving away from the uniformisation offered through globalisation itself. This societal demand propels the establishment of micronations that emulate the formal trappings of sovereign states, challenging the status quo of sovereign states.

Due to a postnationalist realpolitik (Bloemraad, 2004; Keating, 2018), the micronation of the Principality of Hutt River was a thorn in the side of the Australian Government. In the 2000s, the Australian Government started a legal battle over tax collection to constrain the principality's financial resources. Following the court case Casley v. Commissioner of Taxation [2007] HCATrans 590, where arguments regarding the principality not being part of Australia were classified as ‘fatuous, frivolous and vexatious’, the Deputy Commissioner of the Taxation v. Casley [2017] WASC 161 court case claimed approximately AUD three million in debt due and payable for income tax, interest, and penalties with respect to the income years ended 30 June 2006 to 30 June 2013. The principality's appeal against this claim was dismissed in Casley v. Deputy Commissioner of Taxation [2017] WASCA 196. Due to the substantial amount of money involved in the court case, the principality asked for public assistance and pro bono legal support. Again, there is evident boundary work due to the derogatory treatment the Australian Government provides the newcomer (i.e., the principality) by labelling the claims ‘fatuous, frivolous and vexatious’ and disenfranchising Casley (Brighenti, 2010; Bucher et al., 2016; Gracia and Oats, 2012) and setting the tone on how the Australian Government deals with secessionist states within its territory (Esmark, 2016). The Australian Government used accounting practices, which include tax collection, as an apparatus of power and subjectivising practice (Boden et al., 2010; Miller and Power, 2013; Sikka and Hampton, 2005). Thereby, accounting was used to terminate a social conflict enacted in the relation between a micronation and an established national government (Hopwood, 1987; Kurunmäki et al., 2011; Miller, 1990), evidencing how accounting has social and moral imperatives and is more than a technical practice (Carnegie et al., 2021; Twyford, 2023; Twyford and Abbas, 2023).

Since the principality was an unrecognised state, the ownership of the property and other assets belonging to the principality was under Casley's name. Under the Australian legal system, prior to the distribution of assets from a deceased estate, the trustee or executor must first pay all outstanding debts, including those owed to the ATO (Hobbs and Williams, 2021a). Thus, when Casley passed away in February 2019, in winding up his estate the trustee or executor was required to pay ATO AUD three million from the deceased's estate (Meachim, 2019). Therefore, the principality found itself in financial hardship, which ultimately led to its dissolution and placement of the property on the market, suggesting that the ATO delivered the coup de grâce to the principality by constraining its financial resources through a legal battle over tax collection. Accounting thus played a pivotal role in suppressing a micronation and contributing to the cohesiveness of the Commonwealth of Australia (Kurunmäki et al., 2011; Mennicken and Miller, 2012), contributing to the statement that accounting originates from social conflicts (Hopwood, 1987) and functions as a cohesive and influential mechanism for economic and social management (Carnegie and Napier, 1996, 2012). Finally, the suppression of the principality through accounting evidences the role of accounting as a subjectivising practice because it was used by the Australian Government to subdue the principality and assure a monopoly of sovereignty (Miller and Power, 2013).

By using accounting to suppress the principality, the Australian Government was able to handle the micronation in a subtler way than other sovereign states. For instance, Italy blew up the Republic of Rose Island in 1969 (Bezrucka, 2022), Tonga took over the Minerva Reefs in 1972, which were claimed by the Republic of Minerva (Hobbs and Williams, 2022), and Thailand seized and dismantled an Ocean Builders’ seastead in 2019 (Simpson, 2021). 10 The use of accounting by the host country avoided direct confrontation with the principality but was still an unfriendly response, as evidenced by the boundary work.

The demise of the principality sent a shockwave throughout the micronational community and led other micronations to start putting their books in order. The threat of potential legal issues and financial hardship led contemporary established micronations to undergo accounting reforms (Moussalli, 1996, 2008) and to register themselves as nonprofit entities. For example, the Grand Duchy of Westarctica has been registered as a nonprofit corporation in the United States, the Grand Duchy of Flandrensis has been registered as a nonprofit organisation in Belgium, and the Royal Republic of Ladonia has one nonprofit foundation in the United States and another in Sweden.

Conclusions

In this article, we examine how a sovereign state used accounting to suppress a micronation and assert its monopoly of sovereignty. Within the performance of micronationality, the micronation endeavoured to uphold itself as a tentative sovereign state. A qualitative approach to examine the performance of micronationality through albeit often rudimentary government practices and the host state's boundary work in dismissing any potential legitimacy for the micronation towards sovereignty was adopted.

We find evidence that the Principality of Hutt River adopted the formal trappings of a sovereign state; hence, the micronation adopted political rationalities and technologies to uphold its sovereignty, although it was not recognised by any other sovereign state. Despite this lack of international recognition, the micronation was able to persevere for 50 years due to the advance of a post-national zeitgeist, enduring a succession of challenges by the host state (i.e., the Commonwealth of Australia). Accounting was then mobilised by the host state to deliver the coup de grâce to the micronation by constraining its financial resources through a legal battle over tax collection; accounting was thus used by the host state to monopolise its sovereignty against a micronation. Accounting was utilised as an apparatus of power, being a territorialising activity and a subjectivising practice (Mennicken and Miller, 2012; Miller and O’Leary, 1987; Miller and Power, 2013). A limitation to our research is that, although sources were plentiful, including but not limited to more than 100 declassified diplomatic cables, there was no access to the micronation's accounting records. We hope that in the future more information regarding the defunct micronation will be released to the public.

The growing number of micronations is presented as a product of postnationalism propelled by globalisation and a neoliberal agenda, and, given the increasing trend of postnationalism, opportunities for plural citizenship in liberal societies will likely grow. Besides the Principality of Hutt River, recent examples include the Principality of Aigues-Mortes established in 2010, the Free Republic of Liberland established in 2015, and the Space Kingdom of Asgardia established in 2016. Hence, this article contributes to the accounting literature by broadening the perspective of accounting beyond its role in sovereign states to its role in the performance of micronationality. The micronation evidenced political rationalities and technologies, and the host state's reaction through boundary work demonstrates the increasing relevance of such entities competing with sovereign states and of the role of accounting in the advance of a post-national zeitgeist.

Footnotes

Acknowledgements

The authors are grateful to the joint editors and two anonymous reviewers for their valuable insights and helpful comments. Earlier versions of this article benefited from feedback from discussants and participants at the Accounting and Finance Association of Australia and New Zealand Conference (Brisbane, 2019) and the 9th Asia-Pacific Interdisciplinary Research in Accounting Conference (Auckland, 2019) and at a Deakin University Accounting Department brown bag session (2022), an Academy of Accounting Historians brown bag online session (2022), and a Victoria University of Wellington School of Accounting and Commercial Law seminar (2022). The authors also benefited from exchanges and suggestions from academics, such as Philip Hayward, Harry Hobbs, Isabelle Simpson, Sandra Petermann, Matthias Muskat, Robert Motum, Garry Carnegie and Damien Lambert. Open access publishing was facilitated by Deakin University, as part of the Sage – Deakin University agreement via the Council of Australian University Librarians.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Author note

This article is dedicated to Leonard George Casley (1925–2019), also known as HRH Prince Leonard, Sovereign of the Principality of Hutt River. It is not titles that make men illustrious, but men who make titles illustrious (Machiavelli, 1517, Ch. XXXVIII).

Notes

Appendix 1