Abstract

The diversification and financial performance literature is ambiguous. To shed light on this relationship, quantitative and qualitative research was used to study the Canadian Pacific Railway (CPR) from 1883 to 2020. The CPR was selected because of its extensive archives and past range of diversification activities. Most of CPR's diversification investments were unrelated and unsuccessful. There is a statistically significant negative relationship between diversification and operating income/Tobin's Q. This negative relationship can become U-shaped or even positive by increasing operating income via reduced costs, improved conversion of inputs into outputs, and improved service to customers. The absence of diversification is not sufficient to significantly increase performance; satisfactory financial performance only comes from increasing operating income. These findings contribute to understanding the nuanced relationship between diversification and financial performance, highlighting the advantages of pureplay and the necessity for continuous financial performance improvement with related diversification and even pureplay.

Keywords

Introduction

The relationship between diversification and profitability remains ambiguous and inconclusive, as evidenced by various studies (Chang and Lee, 2016; Lang and Stultz, 1994; Somnath and Saptarshi, 2017). The existing literature fails to provide a definitive understanding of how diversification influences profitability positively, negatively or insignificantly. Despite this gap, a paradox emerges when considering CEOs’ strong inclinations to pursue diversification strategies. Although empirical evidence is lacking, it can be inferred that CEOs do not anticipate poor diversification outcomes. This puzzling desire among CEOs to diversify represents a second gap that warrants exploration.

Most research on this topic adopts a quantitative approach, primarily focusing on positive, negative or neutral correlations, thereby neglecting a detailed examination of the underlying process through which diversification impacts financial performance. To address this limitation, it is useful to study a firm where the diversification process can be observed both quantitatively and qualitatively. This enables an investigation into the discourses surrounding diversification investments. Furthermore, the selected firm should exhibit increased and decreased diversification variations, providing ample material for both qualitative and quantitative analyses.

North American railway firms present suitable subjects for research due to their historical engagement with diversification and their often more-than-a-century resilience in the face of unfavourable government rate regulation, multiple competitors, economic shifts and social transformations. In Canada, railways have navigated frontier conditions, transitioned to agricultural, industrial, and post-industrial economies and encountered challenges from automobiles, trucks, aeroplanes and pipelines.

The Canadian Pacific Railway (CPR), established in 1881, offers a comprehensive case study for understanding the full spectrum of diversification strategies, ranging from pureplay operations to sporadic, modest and extensive strategic diversification, before reverting to pureplay. Additionally, the CPR transitioned from extensive political rate regulation to market regulation. In contrast, the Canadian National Railway (CNR), the other Trans-Canada railway, has been under the ownership of the Canadian Federal Government until recently. The CPR, driven by a profit-oriented agenda for shareholders, provides a more appropriate context for examining the relationship between diversification and financial performance than the CNR, which was established to counterbalance the CPR's monopolistic control over Trans-Canada transportation (Stevens, 1973).

This study aims to analyse quantitative and qualitative evidence concerning the CPR's diversification strategies for much of the twentieth century before being completely discontinued in 2001. Our primary objective is to comprehend the motivations behind CPR's diversification actions and, consequently, the factors that triggered the sudden termination of diversification in 2001. Specifically, we seek to understand and assess the reciprocal impact between CPR's financial performance and its diversification efforts.

From an accounting history perspective, our motivation for this article stems from the opportunity to comprehensively study diversification efforts by examining financial and other relevant information within a rich and longitudinal context. By doing so, we gain a nuanced understanding of how railway financial performance influenced diversification's expansion and contraction. Our research contributes to the existing literature by shedding light on diversification's limited successes and numerous failures. Furthermore, our study enriches Canadian railway history, CPR's diversification history and the regulatory history of railways in Canada.

This research suggests that enhanced financial performance is achievable through pureplay expansion, and possibly with related diversification. These performance accomplishments require understanding operational systems, reducing costs and improving customer service. They contribute to reconciling the relationship between diversification and financial performance by providing insights into the factors influencing performance outcomes.

This article is organised into six sections. The present section serves as the introduction, providing an overview of the research objectives. The second section constitutes a literature review, which identifies gaps and develops research questions. Moreover, that section establishes the conceptual framework employed to assess the impact of diversification on financial performance. Moving forward, the third section describes the research site and methodology, elucidating the chosen approach for data collection and analyses. In the fourth section, the findings are presented and categorised by diversification strategy. Subsequently, the fifth section critically examines and discusses the extent to which the archival evidence aligns with or challenges our research questions. Finally, the sixth section encapsulates our key insights, our contributions to resolving the gaps in the literature, and some concluding remarks.

Literature review

Diversification and performance are the focus of this literature review. Diversification, as defined by Ramaswamy et al. (2017), entails a firm's entry into new products, markets or both, distinct from existing operations. Performance in financial terms is operating income as a percentage of revenue, which is the measure used by CPR.

The existing literature exhibits two notable gaps that warrant further investigation. First, there is a lack of clarity regarding the relationship between diversification and financial performance. Second, despite this uncertain relationship, CEOs often exhibit a propensity to engage in diversification investments. Through our longitudinal study encompassing both quantitative and qualitative research, we aim to enhance understanding of the unclear interplay between diversification and financial performance and shed light on the underlying motivations driving CEOs to pursue diversification investments. The literature review is divided into three parts, diversification and performance, expansion options and refinements for expansion/diversification.

Diversification and performance

The existing literature has extensively examined the effects of expansion through diversification; however, the findings have yielded inconclusive and ambiguous results, as highlighted by Lang and Stultz (1994), Chang and Lee (2016), and Somnath and Saptarshi (2017). Conversely, pureplay expansion, which is not diversification, focuses on existing products/services and markets. A commonly reached compromise is that the relationship between diversification and financial performance follows an inverted U-shaped pattern. Initially, they exhibit a positive association, but as diversification intensifies relative to revenue, the relationship plateaus before turning negative. Previous studies offer compelling evidence of a negative correlation between diversification and financial performance (Lang and Stultz, 1994: 1278). Notably, Lang and Stultz (1994) analyse a sample of firms from 1978 to 1990, considering diversification at a broad level without distinguishing between related and unrelated activities or comparing them against pureplay initiatives. Nevertheless, their analysis convincingly demonstrates the detrimental impact of diversification on firm value, as they find ‘no evidence that diversification benefits firms on average’ (Lang and Stultz, 1994: 1279). However, despite these findings, firms persist with diversification, implying that rationality and validity must underlie those actions.

Prior studies have explored diversification with various theoretical frameworks, including agency theory, market power theory, portfolio theory, regional diversification and transaction cost economics, as demonstrated by Palepu (1985), Varadarajan and Ramanujam (1987), Rowe and Wright (1997), and Villalonga (2004). Contrary to the findings of Lang and Stultz (1994), Somnath and Saptarshi (2017) argue in favour of a positive relationship between diversification and profitability. They contend that diversification can enhance performance by expanding a firm's customer base into new markets and industries. Similarly, Manral and Harrigan (2016) discover a positive association between diversification and financial performance when firms increase demand by offering complementary products and services.

Subsequent studies corroborate the negative relationship between diversification and financial performance. For instance, Chang and Lee (2016) examined productivity levels among a sample of firms from 2005 to 2012 and found a negative association between diversification and productivity. The authors said moderation could occur through process innovations. Moreover, Schommer et al. (2019) conducted a recent meta-study revealing that, starting from 1980, large firms reduced the extent of diversification in response to the acknowledged negative relationship between diversification and financial performance. The authors of the meta-study emphasised the importance of related diversification, as firms tended to compete in markets or offer products where they possessed competitive advantages in terms of knowledge.

An organisational perspective on managing diversification comes from Chandler's work (1962). He proposed that diversified firms adopt a multidivisional structure, with each business group separately operationally managed but financially coordinated at the corporate level. In contrast, pureplay firms typically adopt a monolithic structure focused on operational aspects. Chandler (1962) advocated for the multidivisional structure in diversified firms to ensure focused management of each business unit, although performance levels may or may not match those of pureplay monolithic structures. The adoption of the multidivisional structure institutionalised the ‘strategy of diversification’ (Chandler, 1962: 394), suggesting that the structure should follow the strategy and that the multidivisional structure should accompany diversification to enhance performance. In the 1960s and 1970s, the diversification (i.e., conglomerate) movement justified itself by embracing the multidivisional structure. However, by the 1980s, the superiority and even viability of extensive diversification with the multidivisional structure faced challenges. 1

As Berger and Ofek (1995) explain, diversification has both value-enhancing and value-decreasing effects, that is: The potential benefits of operating different lines of business within one firm include greater operating efficiency, less incentive to forego positive net present value projects, greater debt capacity, and lower taxes. The potential costs of diversification include the use of increased discretionary resources to undertake value-decreasing investments, cross-subsidies that allow poor segments to drain resources from better-performing segments, and misalignment of incentives between central and divisional managers. (Berger and Ofek, 1995: 40)

They extensively investigated the impact of diversification on performance, identifying multiple pathways through which diversification influences performance. Notably, one avenue for a positive relationship between diversification and performance lies in the concept of excess capacity. 2 Firms possessing unused resources can leverage these surplus capabilities to enhance financial performance. With that excess capacity, they are prepared to pursue expansion and diversification initiatives, as they can offer competitive prices when entering new markets or introducing new products. Consequently, firms with low opportunity costs 3 resulting from their excess capacity can undertake expansion and diversification endeavours at a lower cost than firms without spare capacity.

To further explore the notion of excess capacity in their study of a large New Zealand firm, Askarany and Spraakman (2020) adopted the ‘theory of excess capacity’ proposed by Paine (1936) and Cassels (1937). These researchers meticulously examined the firm's domestic and international capacity costs with 20 years of revenue and profitability data. When there was excess capacity, there was a positive correlation between diversification and financial performance.

The next sub-section shows how the literature explains the options – diversification or non-diversification – for creating performance with expansion.

Expansion options

A premise underlying our research is that firms have three options when pursuing expansion: pureplay, related diversification, and unrelated diversification. 4 Seen on a continuum, these options range from utilising existing products/services and markets (pureplay) to venturing into new products/services and markets (unrelated diversification). Occupying the middle ground on this continuum is related diversification. In this sub-section, we will examine the literature supporting each option. It is worth noting that the literature has proposed two approaches for characterising unrelated diversification: activity-based and market-based classifications. These classifications encompass strategies aimed at reducing the ‘unrelatedness’ of diversification.

Rowe and Wright (1997), Levinthal and Wu (2010), and Boschma (2017) identified two integrating options for enhancing financial performance. First, firms can focus on expanding among activity groups, that is, within an activity group (processing another product), between activity groups (packing to textiles), or between functions (wholesaling to manufacturing). Second, firms can pursue market diversification. An example of channel diversification would be the integration of online revenue into a physical store, effectively expanding the firm's reach. Retailers also employ this strategy with department stores expanding their operations by establishing discount stores. Another avenue for reducing unrelatedness is geographical diversification, whereby a firm expands its operations from local to national or international markets.

The existing literature widely acknowledges that expansion through pureplay rather than diversification tends to yield the highest levels of financial performance. The rationale behind this is that pureplay expansion within the same market(s) and with the same product(s)/service(s) leverages the existing knowledge possessed by managers, employees and systems (Palepu, 1985). This knowledge advantage enables the firm to improve its financial performance. In contrast, when pursuing diversification, the firm enters new and less familiar markets and/or introduces unfamiliar products/services, leading to reduced relevant knowledge among its managers, employees and systems. Consequently, the firm is likely to achieve lower levels of financial performance on these diversification investments. However, related diversification achieves higher financial performance than unrelated diversification. For the latter, neither the market nor the product/service is familiar.

The next sub-section will review suggestions from the literature for enhancing diversification performance.

Refinements

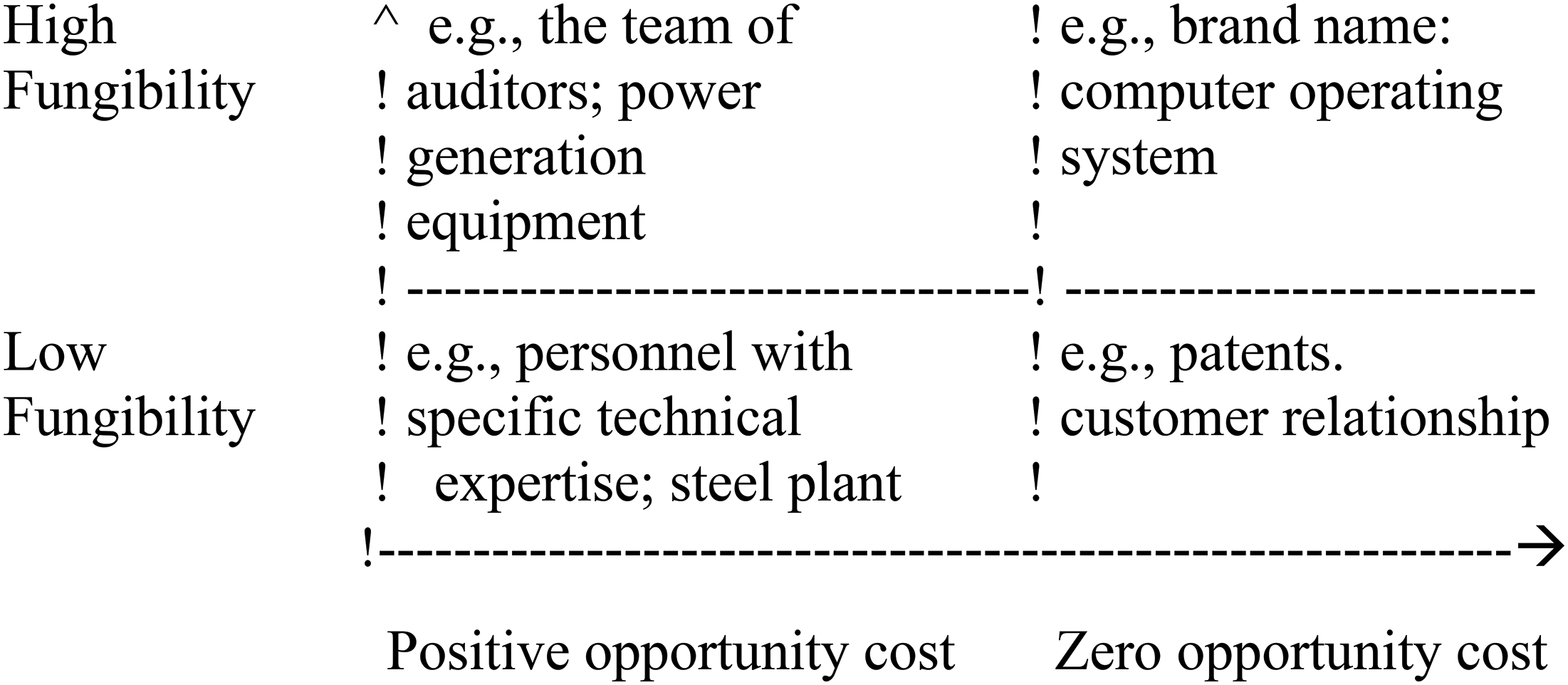

Levinthal and Wu (2010: 781–782), like Askarany and Spraakman (2020), adopt an organisational perspective, positing that within firms, most resources are utilised, particularly those based on human capital. Consequently, the ideal condition for diversification is low opportunity costs resulting from excess capacity. Rational decision-making necessitates that expansion with diversification only occurs when the anticipated returns from potential opportunities outweigh the associated costs. Drawing upon an extensive review of the existing literature, Levinthal and Wu (2010: 781–782) provide the following evaluation: the ‘fungibility of resources is the basis for the explanation as to why related diversification tends to outperform unrelated diversification and, in turn, why firms tend to pursue more related diversification’.

Levinthal and Wu (2010) describe these related diversification strategies as being influenced by fungibility and opportunity costs. Furthermore, they suggest that fungible but interchangeable resources such as brands, management skills, marketing skills and technology play a crucial role in facilitating profitable related diversification. Opportunity cost refers to the forgone return of the next best alternative when a particular choice is made. A low or zero opportunity cost is associated with excess capacity or unused debt. For instance, cash reserves in the bank represent a low opportunity cost, as there is minimal loss when those reserves are used for investments (see Figure 1).

Dimensions of relatedness.

The upper-right quadrant of Figure 1 represents the ideal starting point for diversification, characterised by high fungibility and low opportunity costs. In this scenario, resources such as brand names can be readily and without significant cost used for related diversification into familiar and easily accessible products and markets. Under these conditions, incremental financial performance is expected to be highly favourable. Conversely, the least favourable starting point is the bottom-left quadrant, where there is low fungibility and high opportunity costs. This indicates a lack of resources to create a competitive advantage, and the alternative use of existing resources is expensive. In such circumstances, incremental performance is anticipated to be unfavourable. This type of diversification involves entering significantly different and expensive product/service markets.

Despite the general relationship between diversification and financial performance outlined above, the literature review reveals a complex and nuanced association between those two variables at CPR. Accordingly, our research aims to address the following questions:

Why did the firm pursue diversification during specific strategic periods from 1883 to 2020? Why was diversification successful, or why did it fail to yield positive outcomes?

In exploring these research questions to understand what is missing, we consulted the relevant literature to guide our empirical analysis of diversification at the CPR throughout the 1883 to 2020 period.

Research site and methodology

CPR has been a significant contributor to nation-building. In 1867, following the establishment of Canada as a confederation of British North American colonies, the first Prime Minister committed to constructing a railway connecting all colonies, including British Columbia on the coast of the Pacific Ocean, within a decade. However, due to the immense financial and physical challenges associated with this ambitious railway project, it faced difficulties attracting investors, and thus completion did not occur in that first decade.

To gather relevant materials for our study, one member of our research team visited the CPR Archive in Montreal, Quebec, Canada. Our co-author received access to the archives on two separate occasions, during the fall of 2000 and the winter of 2001. These archives were within the historical CPR head office, known as Windsor Station.

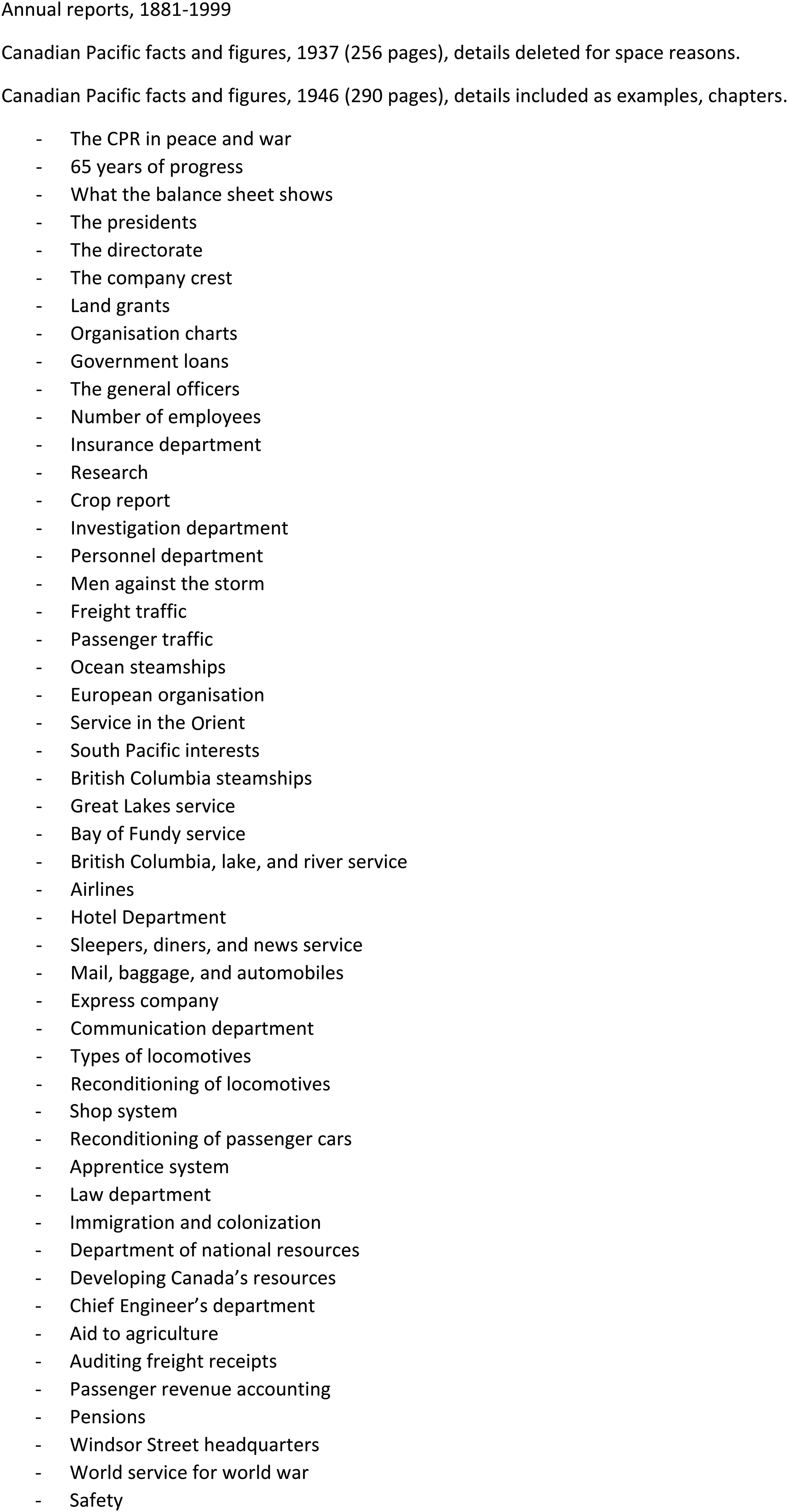

This archive contained a limited number of unclassified documents. Figure 2 shows the relevant and accessed materials. Annual reports existed from 1881, and there was substantial general summary information, such as the Canadian Pacific Facts and Figures for 1937 and 1946. For specific years, extra copies of annual reports were available, and in those cases, the archive personnel provided our co-author with original copies. Otherwise, our co-author requested copies of the original reports. Copies of reports for 2000 and onwards came from the CPR's investors' webpage.

CPR Archives, general contents accessed.

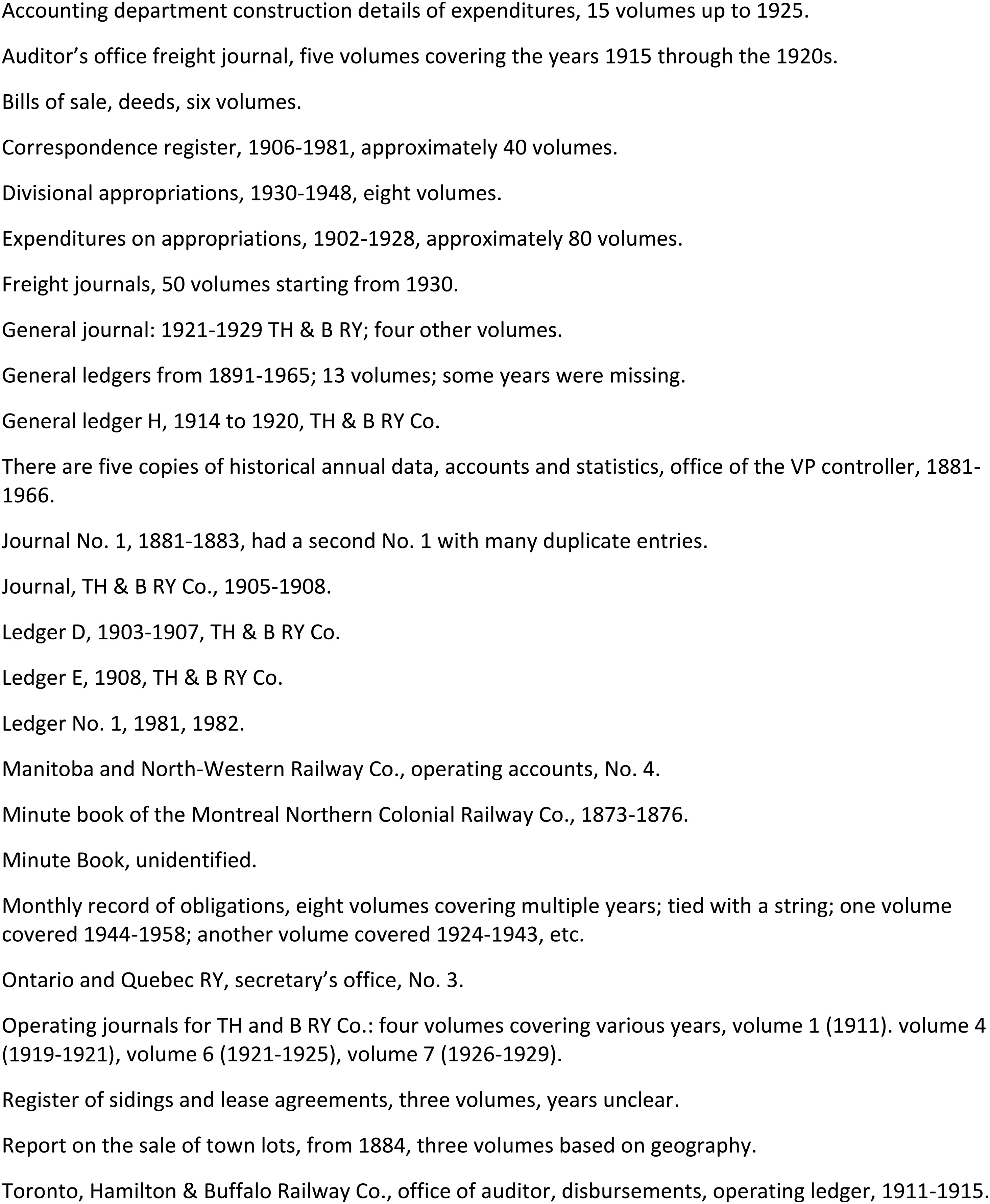

However, the accounting journals, ledgers and related documents of the CPR were not stored at the Windsor Station archive. Instead, they were stacked randomly on a large antique railway luggage cart in a temperature-controlled former art gallery blocks away from the archive. The first task undertaken was to compile a list of these documents, excluding stock and bond transfer books, which were present on the luggage cart. This alphabetical list, the only form of classification for these accounting documents, can be found in Figure 3 and was shared with CPR archive personnel.

CPR Archives, accounting contents.

To the surprise of our co-author, the luggage cart revealed multiple copies of a document titled ‘Historical Annual Data: Tables of Accounts and Statistics’. This report was compiled by the vice-president and controller's department, presenting annual report results in a consistent format from 1883 to 1966. The archive personnel at Windsor Station graciously provided us with one of the extra copies of the Historical Annual Data document. For the purposes of this article, the financial information was updated using annual reports from 1967 to 2020, which were readily available from the CPR archive or investors' webpage.

The Historical Annual Data document contained a crucial performance measure, namely, operating income as a percentage of revenue. This measure became our proxy for financial performance; it was calculated as the difference between revenue and operating costs divided by total revenue. Operating costs encompassed various components such as compensation and benefits, fuel, materials, equipment rents, depreciation, 5 amortisation, purchased services, and so on. Throughout the years 1883 to the 1980s, the CPR aimed to maximise operating income as a percentage of revenue or after 1980 to minimise the operating ratio, calculated as operating costs divided by revenue (CPR annual reports, various years). Currently, the firm prefers to evaluate its performance based on the operating ratio, as noted by Davies (2006: 70). It is important to note that operating income as a percentage of total revenue when added to operating costs as a percentage of total revenue, yields 100 per cent. In other words, maximising operating income is equivalent to minimising operating costs (or the operating ratio).

The quantitative data came from the CPR's Historical Annual Data document and subsequent annual reports, which align with the data utilised by CPR management. Historical stock market prices from 1890 to 1921 were obtained from Innis (1923: 284), while stock market prices from 1922 to 2020 came from CPR annual reports. 6 To provide a thorough understanding, qualitative analysis was employed to explore the intentions and actions of CPR executives concerning operating income as a percentage of revenue and diversification. The qualitative data came from the narrative sections of CPR annual reports from 1883 to 2020. In addition, CPR qualitative information and analyses came from reputable sources such as books, for example, Cruise and Griffiths (1988) and McDougall (1968), as well as articles, for example, Atkins (2021) and Fisher (1991). Qualitative and quantitative evidence would resolve the gaps.

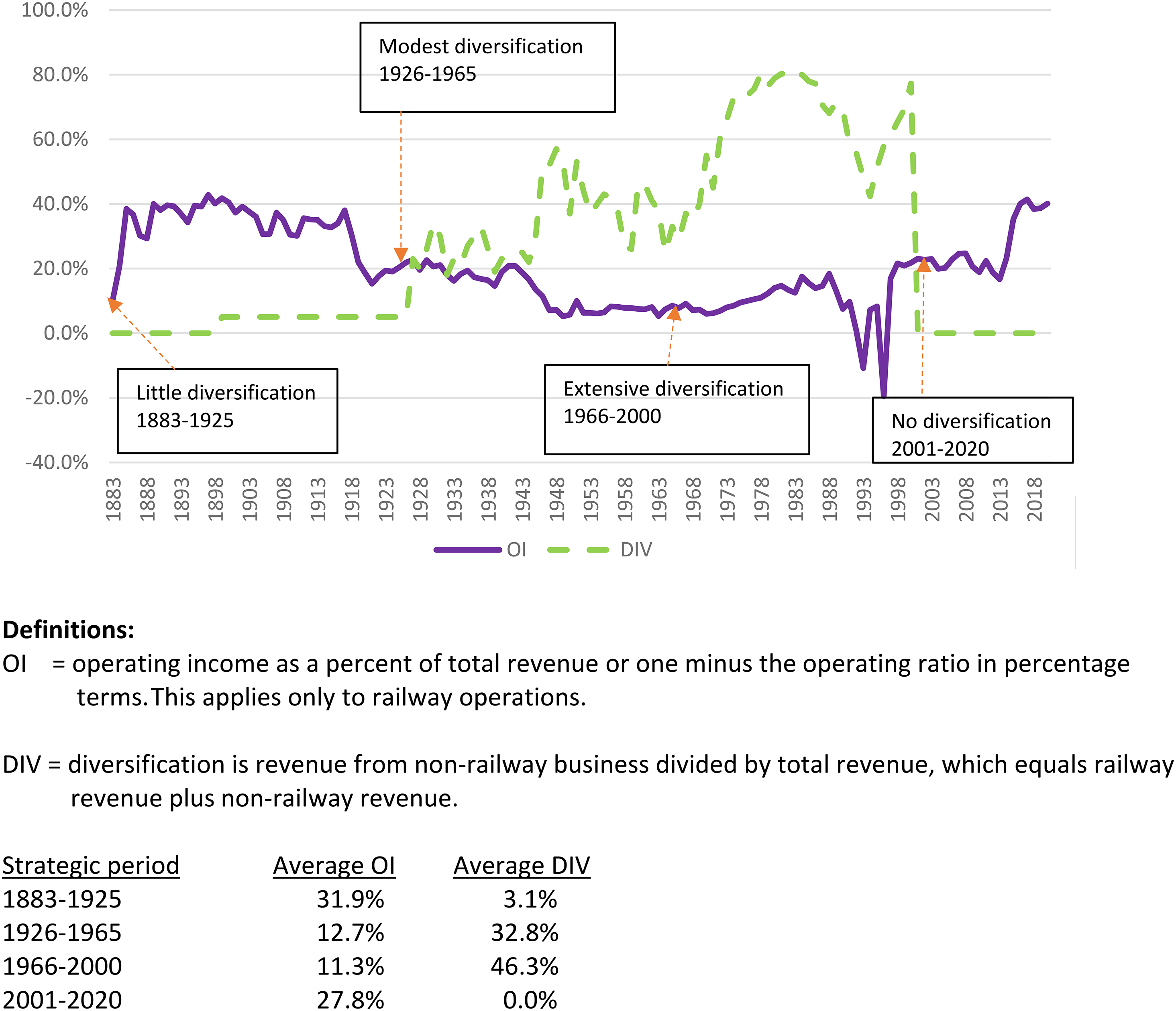

Figure 4 shows CPR's annual diversification rate, that is, revenue from non-railway business divided by the total or the sum of non-railway and railway revenue. The anticipated causal relationship between these two variables is that as operating income as a percentage of revenue declined, diversification increased. Based on the observed patterns of diversification, we inferred four diversification strategies employed by the CPR during the years 1883–2020:

- Little or irregular diversification strategy from 1883 to 1925, - Modest diversification strategy, 1926–1965, - Aggressive diversification strategy, 1966–2000, and - Pureplay or zero diversification strategy, 2001–2020.

Diversification (overall firm) and operating income as a percentage of railway revenue, 1883–2020.

Dividing 137 years into four strategic periods may appear arbitrary. Our analyses revealed the opposite. Specifically, the first period (1883–1925) exhibited minimal or no diversification as CPR focused on developing a profitable railway business. Conversely, the final period (2001–2020) intentionally excluded diversification. The classification of these end periods was not arbitrary but based on deliberate strategic decisions.

This approach left us with 1926 to 2000 to further divide into strategic periods. During this period, diversification progressively increased. In 1955, the CPR implemented a structural change by appointing three executives instead of one to distribute the management workload more effectively (Cruise and Griffiths, 1988: 403). This organisational shift, accompanied by an administrative lag, naturally created a visible dividing line in 1965, separating two distinct periods: modest diversification (1926–1965) and extensive diversification (1966–2000). This division by the percentage of revenue from diversification is the boundary between a lower percentage of non-railway/total revenue and a higher percentage of non-railway/total revenue, emphasising the changing diversification landscape between the second and third periods.

Findings

The findings in the following pages are in five sub-sections. The first explains the formation of the CPR. The next four chronologically describe CPR's diversification strategies regarding performance for the years: 1883–1925, 1926–1965, 1966–2000 and 2001–2020.

Formation

The (Dominion) Government of Canada had agreed to build a railway by 1880 that would link the colony of British Columbia on the Pacific Ocean with the province of Ontario in Central Canada. None of the existing railways were willing to expand from Ontario to British Columbia. A group of investors or syndicates headed by George Stephen and Donald Smith submitted a proposal to build the railway. The result of the Government of Canada accepting this proposal was the formation of the CPR and the building of the railway.

Then the Government of Canada on 21 October 1880, signed an agreement with the syndicate, led by George Stephen, along with Donald Smith and others to construct a railway from Ontario in central Canada (i.e., from the Canada Central Railway terminal near Lake Nipissing in northern Ontario) to the Pacific Ocean (i.e., to Port Moody near Vancouver, British Columbia) (Cruise and Griffiths, 1988: 88–89). The Canadian Parliament approved this agreement on 15 February 1881. In fulfilling its Trans-Canada obligation, the CPR also acquired existing railway lines in Eastern, Central, and Western Canada.

Among the three key syndicate members, George Stephen and Donald Smith had immigrated to Canada from Scotland many years earlier. Both had held executive positions at the Bank of Montreal, including the presidency. Stephen, as the head of the investment syndicate, became the first president of the CPR, while Smith, who lived longer, also served as the Governor of the Hudson's Bay Company and as the Canadian High Commissioner (ambassador) to the UK. The third senior syndicate member, James Hill, also self-made, achieved his wealth through railway construction and ownership in the United States. Together, these three individuals managed the syndicate, which remained active for 30 years (Cruise and Griffiths, 1988: 5).

Of the archival materials list in Figure 3, Ledger No. 1 covers the capital account for the period from February 1881 to June 1883. This account documents the investments made by the syndicate members. George Stephen, James Hill, R.B. Angus, and Donald Smith each invested $150,000, while Morton Rose and his son invested $222,300. Other notable investors included D. McIntyre and Co. ($142,500) and J.S. Kennedy and Co. ($135,000). In total, there were 43 investors.

Following its legal formation on 18 February 1881, the CPR immediately commenced the construction of the new railway (Cruise and Griffiths, 1988: 92). During the early to mid-1880s, the Canadian Government provided the CPR with a cash subsidy of $25 million and a land grant of 25 million acres for the construction of the western line. Additionally, the initial capitalisation of the private firm was $25 million, with shares valued at $100 each. To finance the construction, CPR sold shares at prices below par, and it was not until 1917 that share prices reached the par value of $100 (Cruise and Griffiths, 1988: 136, 151). The New York Stock Exchange listed CPR shares from 1883. 7

The financing of the CPR posed a significant challenge due to the inherent uncertainty of the undertaking. Moreover, the construction of the western railway presented formidable physical obstacles, especially in traversing the frontier and rugged terrain north of Lake Superior, as well as the Alberta-British Columbia mountains. The culmination of success came with the completion of the western mainline tracks on 7 November 1885.

As the CPR had its own construction firm, those profits were available to pay dividends on shares and interest on bonds during the construction phase, thereby mitigating the risk of bankruptcy (McDougall, 1966). By periodically receiving profits from their in-house construction firm, the CPR managed to maintain financial viability, recognising that railway revenues would not be forthcoming until after the completed railway facilitated the migration of settlers westward. Furthermore, there would be an additional delay until those settlers transitioned into farmers, cultivated crops, and sent grains and other produce east by the CPR railway. McDougall (1968: 47) referred to this predicament faced by the CPR as a ‘premature enterprise’. The Government of Canada ensured liquidity by compensating the CPR for the completed track.

The subsequent sections will examine each of the four CPR diversification strategies and their respective relationships with railway operating income as a percentage of revenue. As previously mentioned, Figure 4 presents a graphical representation of both diversification as a percentage of total revenue and railway operating income as a percentage of railway revenue for the study period.

Little or irregular diversification, 1883–1925

During this period, characterised by little diversification, the CPR witnessed the leadership of four presidents, each contributing uniquely to the firm's growth (Cruise and Griffiths, 1988). George Stephen played a crucial role in establishing and constructing the CPR with his financial acumen. William Van Horne demonstrated heroic abilities in spearheading the actual construction of the railway. Thomas Shaughnessy implemented administrative systems to ensure the ongoing functioning of the railway, while Edward Beatty ran the railway with the benefits of the contributions of his three predecessors.

Within this strategic period, the CPR primarily focused on serving the Canadian market, particularly Western Canada, with its core product or service being the railway itself. This encompassed the track infrastructure, locomotives, railway cars and the dedicated workforce. However, due to its status as a premature enterprise, the CPR had to engage in supplementary ventures such as hotels, ocean-bound ships and local express services to compensate for the temporary lack of necessary supporting infrastructure. An internal document titled ‘Canadian Facts and Figures, 1937’ provides insight into establishing and developing the CPR's ‘hotel system’ (CPR Archives, 8 Montreal). The CPR established four hotels in 1887 to cater to train passengers in regions with challenging railway grades that rendered dining cars impractical (i.e., they were too heavy) to include passenger cars. Subsequently, in 1887, the Banff Springs Hotel and the precursor to Chateau Lake Louise accommodated tourist travel. In the years leading up to 1930, CPR established hotels in Vancouver, Quebec City, Montreal, St Andrews, Victoria and Toronto. While these hotels were essential for the CPR's railway operations at the time, their necessity diminished as the market provided the required infrastructure, leading to a decline in the CPR's reliance on its own hotels.

To discern whether an investment was a diversification, the question asked was whether CPR's railway strategy could continue without it. If an investment was necessary for the continuation of the railway strategy, the study deemed it non-diversification. On the other hand, investments such as hotels, ocean-bound ships, local express services and other ventures, initially required by the railway strategy, eventually transitioned into diversification as the requisite infrastructure was developed by others. Specifically, from 1883 to 1925, many of these investments did not fall under the diversification category, but their classification shifted to diversification in subsequent years.

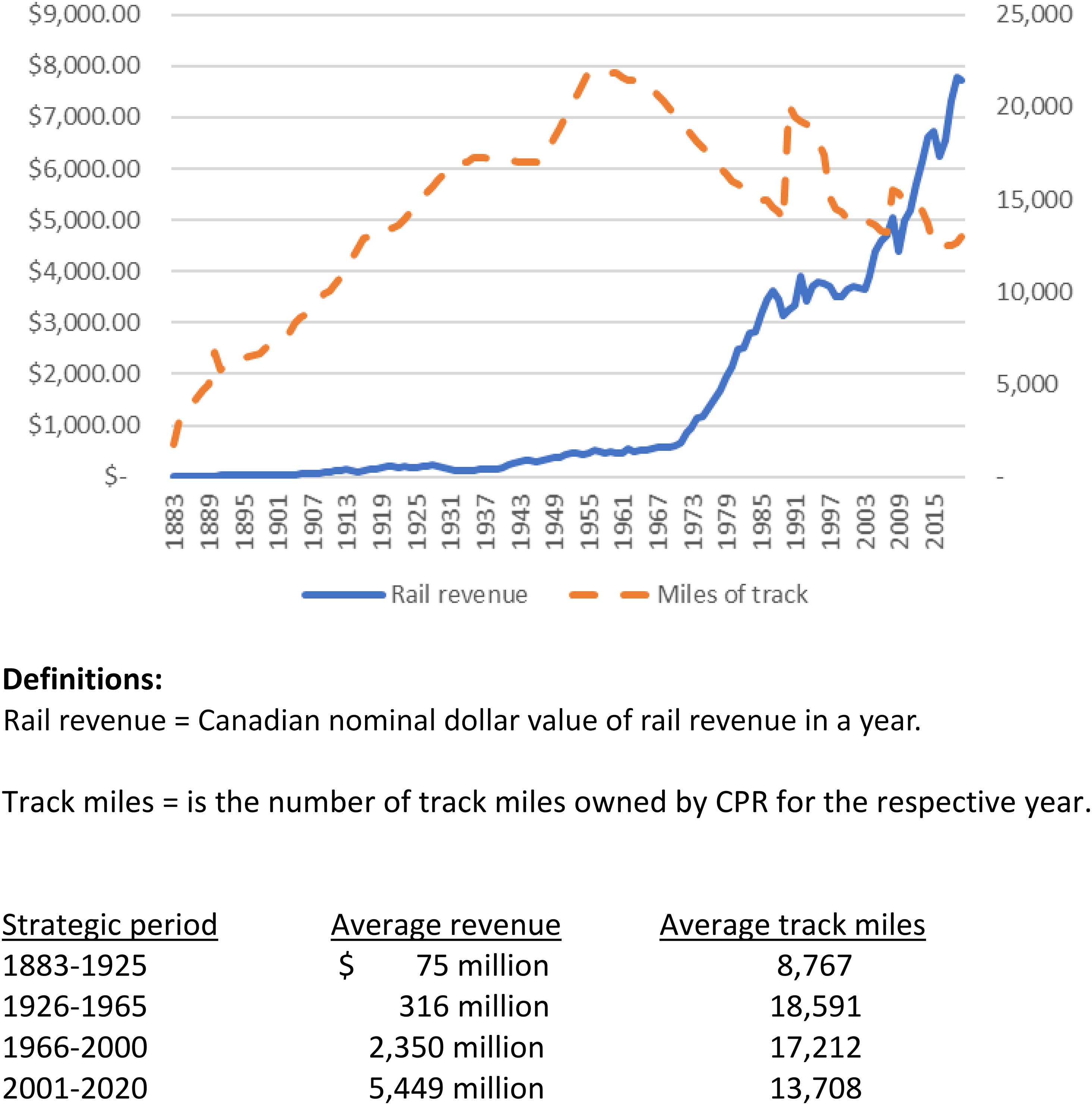

Figure 5 presents graphs illustrating total railway revenue and total miles of railway track from 1883 to 2020, segmented by strategic period. Rail mileage peaked in the mid-twentieth century while rail revenue had grown across the full period, even as rail mileage fell.

Rail revenue and miles of railway track.

For the years 1883 to 1925, the CPR transported various small-load shipments such as grain, flour, livestock, manufactured articles, lumber, firewood and passengers. The CPR experienced significant prosperity primarily due to its monopoly status, which remained unchallenged until some years after the CNR was created by the Government of Canada in 1917. It took upwards of a decade before CNR made a significant impact. The Canadian Northern, a competitor in certain regions of Canada, faced bankruptcy in 1917 and was subsequently acquired and renamed the CNR by the Federal Government (Cruise and Griffiths, 1988: 283). Through mergers with the Grand Trunk Railway and other acquisitions, the CNR encompassed 221 distinct railway lines and finally became a well-functioning railway in 1929 (Cruise and Griffiths, 1988: 330). The introduction of the CNR resulted in two parallel railways spanning Canada. Before the CNR, there were no alternative railways, water routes or roads that could compete with the CPR.

Freight rate regulation affected CPR's financial performance. These freight rate regulations posed a notable constraint on its monopolistic operations (Haritos and Elliott, 1983: 4). The Rail Clauses Consolidation Act of 1851 stipulated that the Government of Canada had to approve CPR freight rates. However, in 1888, this authority was transferred to the Railway Committee of the Government of Canada. While rate regulations initially did not affect CPR's operating income as a percentage of revenue, their impact became evident in subsequent strategic periods.

One significant rate regulation that had a profound impact on the CPR was the establishment of the Crowsnest Rate in 1897. The Government of Canada provided the CPR with a grant of $3.4 million for constructing a line through the border mountains of Alberta and British Columbia, known as the Crowsnest Pass (Friesen, 1987: 191). In exchange for this grant, the CPR agreed to future regulated freight rates, which came into effect in 1898 and 1899 (Rothstein, 1989). The CPR poorly negotiated this agreement, but politically astute western Canadian farmers were reluctant to allow the Government of Canada to revoke it. McDougall (1966: 54) concluded, based on an analysis of the Crowsnest Rate's impact on the CPR from 1899 to 1965, that the rates were mutually beneficial for both the CPR and the shippers. However, he noted that after 1965, the rates became outdated and harmed the CPR.

Then in 1886, the CPR entered into its first collective bargaining agreement (Fisher, 1991), signalling the challenging labour relations that persisted throughout most of the study period. While constructing the railway through the Crowsnest Pass, the CPR acquired the British Columbia Smelting and Refining Company in 1898 as part of a track acquisition. This acquisition, along with the merging of other properties, led to the formation of the Consolidated Mining and Smelting Company of Canada (Cominco) in 1906. This marked the CPR's initial but unplanned foray into industrial diversification, although Cominco operated independently from the CPR. However, in 1986, the CPR divested its ownership in Cominco (Cruise and Griffiths, 1988: 456).

In addition to Cominco, the CPR entered two other businesses based on land received from the Government of Canada as payment for constructing the railway across Western Canada. First, the CPR retained mineral rights on 25,000 acres of land, which allowed for the development of an oil and gas business. Over time, this business expanded and became known as PanCanadian Oil and Gas. Second, the CPR capitalised on the revenue and repurposing of railway land, thus entering the real estate business, and eventually establishing a separate entity called Marathon Realty. Initially, both the oil and gas and real estate businesses utilised land granted by the Government of Canada to the CPR. However, they gradually acquired their own land, with Marathon Realty starting in the 1970s (Cruise and Griffiths, 1988: 443) and PanCanadian Oil and Gas in the 1960s (CPR Annual Report, 1968). These businesses transitioned from being units of the CPR to becoming subsidiaries. By 1980, the overall firm owned 87 per cent of PanCanadian Oil and Gas and 100 per cent of Marathon Realty (CPR Annual Report, 1980). With the division of the overall firm into five market-based firms, PanCanadian Oil and Gas remained as one of the entities, while CPR sold Marathon Realty five years earlier (CPR Annual Report, 1996).

In 1888, the CPR obtained majority ownership of the Minneapolis Sault Ste. Marie and Atlantic Railway (CPR Annual Report, 1888). Around the same time, the CPR merged the following: Minneapolis and Pacific Railway; the Minneapolis and St Croix Railway; and the Aberdeen, Bismarck and Northwestern Railway. These merged lines became the Minneapolis, St Paul and Sault Ste. Marie Railway, commonly known as the Soo Line, continued to operate as a separate autonomous railway with its headquarters in Minneapolis, Minnesota. The CPR's acquisition of the Soo Line secured access for shipping freight to port destinations in the United States, with Chicago being one of the significant port access points.

As the period ended, the CPR had expanded its track network to encompass 14,648 miles, as depicted in Figure 5. Railway revenue experienced the highest annual growth rate during this period compared to other strategic periods analysed in this study. Furthermore, as demonstrated in Figure 4, this period proved to be the most profitable for CPR, with an average operating income rate of 31.9 per cent on total revenue.

The primary strategic focus of this period was on pureplay growth through the construction and expansion of the railway. The CPR's product/service, namely the railway, expanded into similar markets within Canada. The organisation operated under a monolithic or operational structure, indicating a centralised and streamlined approach. The CPR demonstrated a high level of knowledge about its products/services and the markets it served.

Moreover, the organisation possessed a considerable degree of fungibility in its capabilities, allowing for flexibility and adaptability. This enabled the CPR to effectively allocate resources, leveraging positive opportunity costs. As the railway network expanded, the CPR achieved economies of scale, decreasing average costs per mile. Operating income as a percentage of revenue remained high during this period as shown in Figure 4.

Modest diversification strategy, 1926–1965

For this strategic period, the leadership of the CPR was under various CEOs, including Beatty, who assumed the role of president in 1918, facing two significant challenges throughout his 25-year tenure. First, the CPR encountered increased competition from automobiles, trucks, aeroplanes and particularly from the CNR. Second, the railway had to navigate the adverse effects of the 1930s recession, which further compounded the difficulties faced by the firm.

Unfortunately, due to his unexpected death in 1943, Beatty's presidency was shortened. He did not leave an apparent successor, unlike his predecessors, resulting in a transitional phase marked by three ‘temporary’ presidents: D.C. Coleman, William Neal, and William Mather. It was not until 1955 that Norris Roy (Buck) Crump assumed the role of president, bringing stability to the leadership of the CPR. Buck Crump was from a similar mould as some previous CPR presidents, Like Stephen, Van Horne and Shaughnessy, Crump had humble origins, yet he was strong-willed, ambitious, opinionated, and intelligent. Any weaknesses were well sealed behind an air of invincibility. He had just the right amount of arrogance to set him apart from the general horde, yet his own labourer's roots and common-sense approach made him the most popular company president ever. At long last, Canadian Pacific again had a leader who could look the devil in the eye – and this one didn’t need a good day to make him blink. (Cruise and Griffiths, 1988: 375–376)

Crump's professional journey within the CPR began at the lowest levels, as noted, where he gained practical experience in various operations. While working for the CPR, he pursued his education, successfully completed high school and two university degrees from Purdue University (Cruise and Griffiths, 1988: 383–387). His second degree focused on ‘Internal Combustion Engines in the Railway Field’, a subject that propelled him to become a leading expert on diesel engines in North America. At the time, steam-powered engines fuelled by coal were the industry's standard.

The transition from steam to diesel-electric power presented CPR with its first major technological transition, which took place during the late 1950s and early 1960s. Subsequently, further technological advancements, such as the introduction of automated track maintenance equipment, reshaped railway operations and had implications for railway employment.

When Crump assumed the presidency in 1955, he inherited a financially troubled firm. The persistence of the 1897 Crowsnest Rate and growing competition posed significant obstacles to operating income as a percentage of revenue. Recognising the need for professional representation in legal matters and regulatory proceedings, Crump identified CPR lawyer Ian Sinclair, who was groomed and entrusted with the management of the non-transportation investments. Canadian Pacific Investments (CPI) was formed in 1962 when transportation and non-transportation businesses were separately managed. This move signalled a shift towards a more explicit diversification strategy, reflected by a distinct place in the organisational structure.

In response to railway performance weaknesses, diversification was pursued by acquiring additional hotels as unrelated diversification investments. Furthermore, the CPR expanded its diversification efforts by adding ships on the East Coast to extend its network to Europe, as well as on the West Coast, to serve China and Japan. With these diversification investments and CP Air, the overall firm positioned itself as a transportation firm rather than a railway business to justify certain diversified investments (CPR, various annual reports). These diversified investments operated as separate entities, detached from the railway operations, thereby constituting unrelated investments.

Rowe and Wright (1997), Levinthal and Wu (2010), and Boschma (2017) shed light on the period from 1926 to 1965 from two perspectives. First, pureplay expansion persisted by constructing additional branch lines, allowing the railway product/service to penetrate more local markets. Although the geographical markets varied to some extent, they shared similarities. Regarding organisational structure, the CPR continued to operate in a monolithic or operational fashion within the railway business. Second, on the other hand, the diversification investments were unrelated, particularly in mining, airlines, and hotels. These diversification ventures comprised separate entities that were unintegrated with the CPR and with one another, resembling a portfolio of investments. Despite attempts to position the overall firm under the umbrella of transportation, the various parts remained disconnected. Once again, the CPR pursued a strategy characterised by low fungibility and high opportunity costs, factors that were unlikely to yield successful diversification outcomes.

Extensive diversification strategy, 1966–2000

Sinclair became CEO in 1966; he became chair on Crump's resignation in 1972. The other three CEOs during this period were Burbidge, Stinson, and O'Brien. According to Cruise and Griffiths (1988: 450), Sinclair eventually retired ‘under his own conditions’. In his unique and distinctive manner, he appointed Fred Burbidge as CEO and chair but retained the roles of chair and CEO of Canadian Pacific Enterprises. Notably, Sinclair maintained his position as chair of the influential executive committee for the overall firm. With this formal power, Sinclair effectively diminished the authority of Burbidge, who would have assumed the CEO and chair positions. Nonetheless, Burbidge successfully abolished the Crowsnest Rate, a significant achievement.

William Stinson, appointed president in 1981, assumed the role of CEO in 1986. Unfortunately, the overall firm suffered a substantial financial loss during that year. To ensure survival, Stinson had to sell money-losing diversification investments to reduce debt, which he accomplished successfully. David O'Brien, the previous CEO of the highly profitable subsidiary PanCanadian Oil and Gas, became the CEO of the overall firm and concurrently assumed the roles of chair and president in 1995. With all three senior positions within the parent firm, O'Brien played a decisive leadership role in the 2001 division of the overall firm into five separate stock market-listed public firms.

An analysis of the annual reports during this period revealed two notable concerns. First, the regulator suppressed operating income by not allowing rate increases to compensate for cost escalations (CPR Annual Reports, multiple years from 1956 to 1967). Second, the CPR consistently acknowledged the diversification policy in the annual reports as to purpose (CPR Annual Reports, 1962–1964) and successes (CPR Annual Reports, 1970–1973). In reference to diversification, the CEO expressed enthusiasm, stating, ‘In this many-sided world of Canadian Pacific, there are almost endless opportunities’ (CPR Annual Report, 1966). However, in 1975, CPR modified this statement to emphasise that ‘the most favourable prospects for growth of the [firm]'s income are in the activities of the CP Investments Group’ (CPR Annual Report, 1976). Apparently, CPR believed success was dependent on diversification.

After years of lobbying by the CPR, the Government of Canada, in 1959, established the MacPherson Commission, formally known as the Royal Commission on Transportation (Haritos and Elliott, 1983: 5). The formation of the MacPherson Commission was a response to economic developments in the 1950s that had a profound impact on Canadian transportation, namely: the growth of the highway network allowed trucks to carry freight that had previously been captive to the railways and made private automobiles more convenient than trains for personal travel to many destinations; coal and petroleum traffic declined because of the cost advantages of pipelines; grain, petroleum and other bulk traffic moving from the west to the Atlantic Ocean were diverted at Thunder Bay to ships with the opening of the St Lawrence Seaway; and long-distance passenger travel switched from railway to faster and more convenient airlines.

The MacPherson Commission drew two significant conclusions that were relevant for the CPR. First, it recognised the existence of multiple suppliers in the transportation environment and stated that regulations based on monopoly were unnecessary for customer protection as competition could effectively control freight rates. Second, the Commission recommended the separation of national policy from transportation policy, that is, railways should receive compensation from public funds for providing public services that would not be economically viable under competitive conditions, such as maintaining unprofitable branch lines, passenger services and grain transportation.

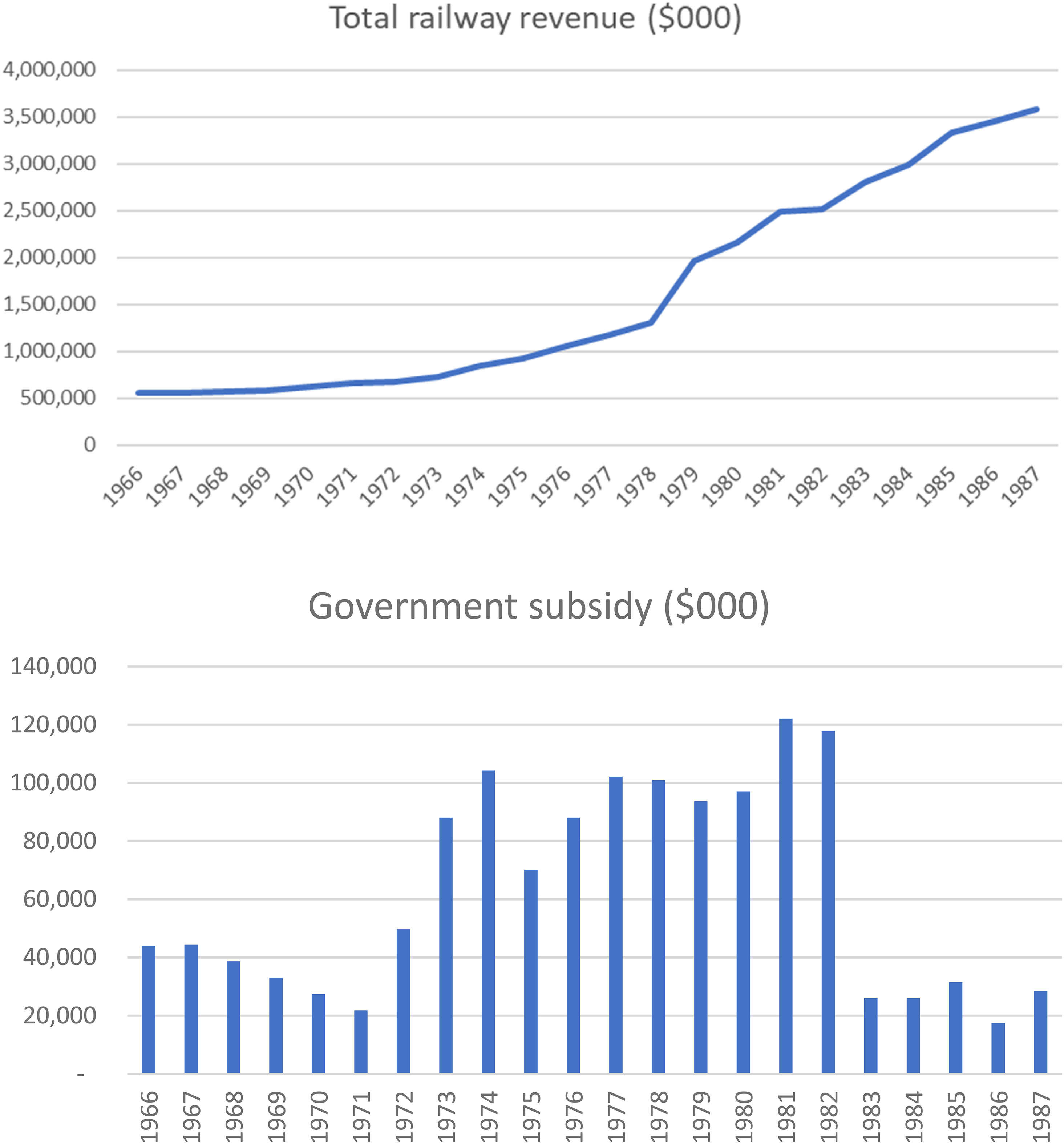

Despite these pivotal conclusions during the second strategic period, the CPR took no action until the third strategic period. As shown in Figure 6, the Government of Canada provided the CPR with substantial annual subsidies for the years 1966 to 1987.

Federal government subsidies provided to CPR.

At the beginning of this strategic period, regulated railway rates still exerted downward pressure on profitability. Partial implementation of the MacPherson Commission's recommendations occurred in 1984 with the replacement of the Crowsnest Rate with the Western Grain Transport Act (Swanson and Venema, 2006). Instead of the 1897 rate regulation system, railway freight rates were determined based on the railway's variable costs plus a 20 per cent markup to cover fixed costs. The Government of Canada abolished the Western Grain Transport Act in 1996, resulting in unregulated freight rates set by market competition (CPR Annual Report, 1996). Finally, after 35 years the Government of Canada implemented the recommendations made by the MacPherson Commission in 1961, leading to the cessation of freight rate regulations (Timur and Ponak, 2002). 9 Political power was eventually lost to economic rationale.

Bulk products dominated what CPR hauled in this period; this included grain, coal, sulphur, fertilisers, forest products, intermodal cargo and automobiles. Notably, this shift to bulk products led to multiple train cars travelling together or dedicated trains, particularly for commodities like coal and grain. CPR introduced profit centres to explicitly pursue profits (Cruise and Griffiths, 1988: 417). This marked a modest transition towards a divisional structure (Chandler, 1962). Subsequently, in 1976, CPR and CNR established a joint passenger service called VIA; the Government of Canada acquired VIA in 1978. VIA assumed responsibility for inter-city railway services for passengers, which CPR and CNR had considered unprofitable.

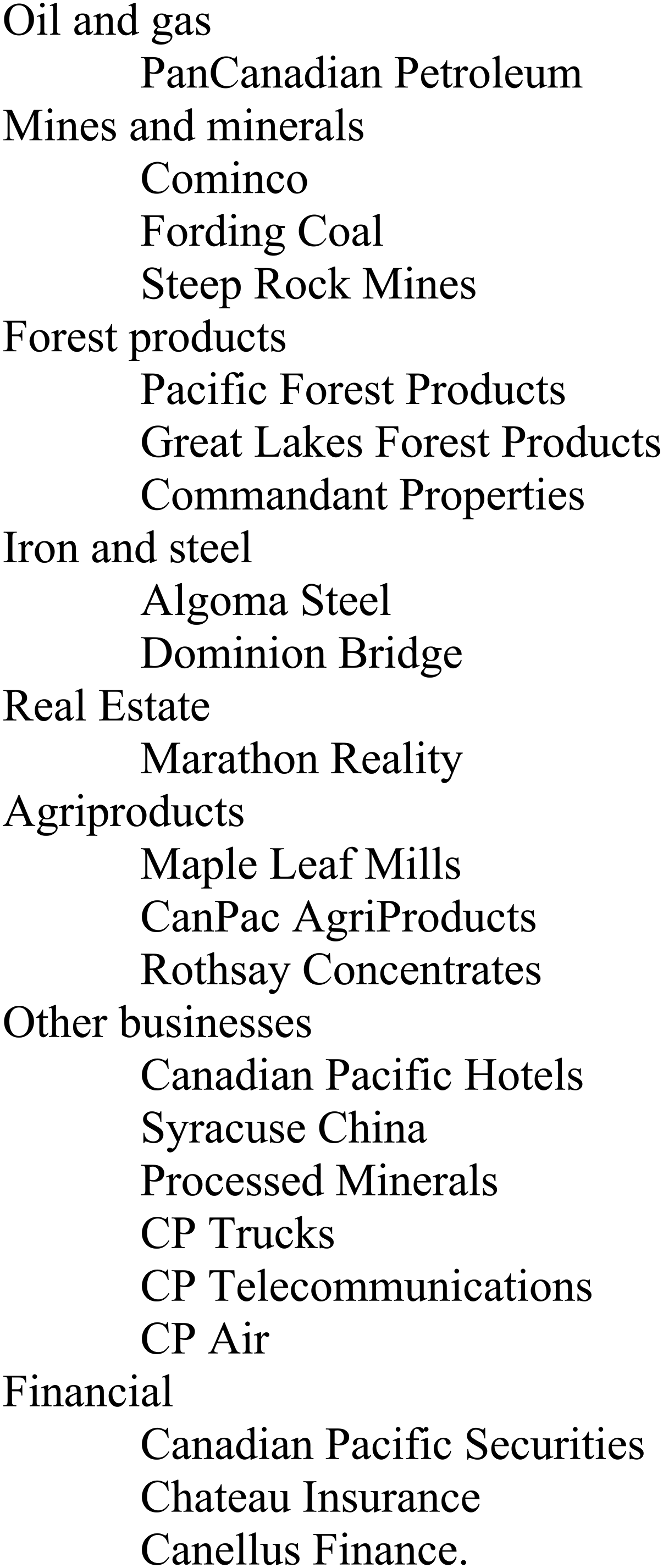

CPI exploded with diversification. It went from $277 million in fixed assets in 1965 to $8.9 billion in 1980 when it became Canadian Pacific Enterprises Limited (CPE). The annual report for 1980 listed as in Figure 7, a sizable number of – non-railway, autonomous and largely unrelated – diversification investments.

Canadian Pacific enterprises fully or partly owned.

In addition to the diversified businesses listed in Figure 7 and the core railway business, the parent firm also owned CP Ships, an unrelated investment. From 1966 to 2000, the total miles of track declined significantly, as indicated in Figure 5. Non-railway revenue accounted for about 77 per cent of total revenue by the end of the strategic period (i.e., in 2000), as shown in Figure 5. The operating income as a percentage of rail revenue averaged 11.3 per cent of revenue, representing the lowest average operating income as a percentage of revenue for any strategic period in the 137-year study (Figure 4).

Two interrelated strategic thrusts characterised this period. First, the pureplay railway business experienced a contraction, with a sharp decrease in total railway mileage as CPR abandoned uncompetitive branch lines. Second, unrelated diversification was unable to compensate for the operating income shortcomings of the railway sector.

Moreover, CPR had major challenges. The Canadian economy faced unfavourable conditions, which posed a threat to the diversification strategy. Specifically, between 1981 and 1985, Canada experienced a severe recession that adversely affected subsidiaries such as CP Air, CP Ships, Algoma Steel, and Canadian International Paper. In response to these challenges and anticipation of a substantial financial loss in 1986, further structural changes were implemented in 1985 to signify the concerns with the diversification strategy.

The apparent solution in the latter part of this diversification period from about 1986 to 2000 was the allocation of investments into divisions of ‘related’ investments (CPR Annual Report, 1986: 2–5). These divisions included transportation (with railway), energy, forest products, real estate and hotels, and telecommunications and manufacturing. Many of these diversification investments seemed to have been squeezed into their respective group. Senior management sought this structural change to enhance performance by reducing dependence on cyclical industries and strengthening the asset mix (CPR Annual Report, 1986: 7). The new structure placed emphasis on cost reduction and market positioning.

This structure served as an internal market for guiding the investments within each division (Chandler, 1962), However, the level of convergence among the investments within each division remained minimal. For instance, the transportation division encompassed unintegrated railway and trucking. Forest products had some potential convergence via trees with pulp, paper and lumber. Energy consisted of oil, gas and coal, which were separate from one another. Real estate exhibited minimal association with hotels, as their products or services were largely unrelated. Similarly, telecommunications and manufacturing did not appear to have a significant association. In other words, when comparing firms within each division, there were often few commonalities, resulting in little opportunity for integration to enhance operations and performance.

Under the new structure, management aimed to exert direct financial control rather than operational control. 10 The following quote extracted from an annual report (CPR Annual Report, 1984) highlights the ‘[achievements] among subsidiaries … including cost restraint programmes, reorganisations, rationalisations, and continued modernization and expansion of facilities’. While we acknowledge these direct management efforts, the level of anticipated success remains uncertain. Despite the group structure, the firms within these divisions operated independently. For instance, the annual report revealed that the firms within the mining and minerals division – Cominco Ltd, Fording Coal Ltd, Processed Minerals Inc. and Steep Rock Resources Inc. – were unintegrated despite their similar operating practices. As per the existing literature, CPR found unrelated portfolio investments to be an ineffective diversification tactic.

The Soo Line had represented a portfolio investment consisting of 7,600 miles of track across 12 mid-western states (CPR Annual Report, 1985). Approximately 102 years after its acquisition and following the subsequent acquisition of the minority interests, the Soo Line was eventually integrated into the CPR in the early 1990s. Similarly, in 1991, the CPR acquired and integrated the Northeast, Delaware, and Hudson Railway.

In an annual report, both the chair and the president/CEO contrasted diversification strategies employed in the 1960s and 1970s with those from the 1980s. They stated that expansion and diversification were the driving forces in the earlier years, while consolidation and improved productivity became the focus in the 1980s (CPR Annual Report, 1986). They encouraged the divestment of less-related investments and the acquisition of more-related investments. CPR justified this shift in strategy in a subsequent annual report. The [firm] has the management capabilities, the financial capacity, and the asset base to support both internal growth and strategic acquisitions in core businesses in Canada, the United States, and abroad. (CPR Annual Report, 1989)

The CPR further explained that strategy in the following annual report: With the consolidation and refocusing phase now mainly behind us, our strategy has shifted to strengthening our businesses, positioning them as the leading [firms] in their respective fields. Our [firms] are enhancing their competitiveness in terms of market position, productivity and cost control and are capitalizing on opportunities for selective expansion. (CPR Annual Report, 1990)

For this period, Nemeth and Warwick (1995) recognised CPR's difficulty with controlling railway costs: Both Canadian railways [CNR and CPR] have been cutting costs and are currently profitable. But their operating ratios, a critical industry yardstick that measures the operational expenses as a percentage of [revenue], are hovering in the 90 percent range. Most major American railroads boast stronger performances, with average operating ratios of 80 percent or lower. That is partly because the Canadian industry has had to maintain branch lines in low-traffic areas.

Implementation of the divisional structure yielded a positive outcome. This structural shift led to the elimination of additional tracks, as evidenced in Figure 5. Moreover, diversification increased to an average of 46.7 per cent of revenue compared to 32.8 per cent in the prior strategic period, also demonstrated in Figure 5. Unfortunately, the railway's average operating income fell to 11.3 per cent in the 1966–2000 period, compared to 12.7 per cent in the prior period. In its 1999 annual report, the CPR referred to itself as a ‘diversified operating firm active in transportation, energy and hotels’, although the present study argues that the holding firm structure had limited impact on the integration among businesses within the divisions.

Detailed operating income as a percentage of revenue underlying Figure 4 for (1) railway, (2) non-railway and (2) non-railway and non-PanCanadian Oil and Gas show key trends. This study needs to consider two additional factors, Government of Canada rate regulation ceased, thus allowing CPR to pass on costs, and PanCanadian Oil and Gas was an entirely separate highly profitable unrelated business. To include Pan Canadian Oil and Gas with non-railway diversification when considering whether to continue with the diversification strategy would not be appropriate. In the last seven years of the 1966 to 2000 extensive diversification period, the average operating income as a percentage of revenue was 8.0 per cent for the railway operation, compared to only 6.9 per cent for non-railway operations excluding Pan Canadian Oil and Gas. This was a significant change in relative profitability.

Regarding Figure 1, which explores the dimensions of relatedness, the CPR remained positioned in the bottom-left quadrant, indicating low fungibility and positive opportunity costs. Diversification continued as portfolio investments with an average cost of capital exceeding zero. Their primary objectives were to generate high returns or to sell the investment.

Amidst these challenges, several technological advancements emerged within the railway industry. For instance, in the mid to late 1980s, the introduction of hot box detectors, instruments used to remotely measure wheel-bearing temperature, marked a notable technological change. Additionally, in the 1990s, the CPR implemented various technological innovations such as E-billing systems, electronic data exchange (EDI), human resources information systems and automatic equipment identification.

Pureplay or zero diversification strategy, 2001–2020

In this strategic period, CPR witnessed the leadership of four CEOs: Ritchie, Green, Harrison and Creel. Robert Ritchie, who commenced his career with the firm as a research analyst for the non-railway side of the business in 1970, transitioned to the railway side in 1972 and held various positions within the firm before being named CEO in 1995. Fred Green, with a background in marketing, took over as CEO in 2006 after serving as the CPR's president and COO. However, Green resigned in 2012 to enable Harrison to assume the CEO position. E. Hunter Harrison, characterised as a railroader in the vein of notable figures like Van Horne, Shaughnessy, and Crump, had a remarkable career trajectory. Starting as a labourer in a railyard in the United States, Harrison steadily climbed the ranks to become CEO of another railway firm.

During his tenure as CEO at the CNR, the CPR's major competitor, Harrison garnered recognition for his adeptness in reducing costs. When he joined the CPR as CEO, he was granted substantial stock options due to his successful track record in cost reductions at other railways. At the CPR, Harrison concentrated on establishing a system that would enhance the efficiency and effectiveness of operations. Keith Creel, who joined the CPR in 2013 as part of Harrison's assembled team, ascended to the role of CEO in 2016 upon Harrison's departure. Since their initial meeting in 1996, Harrison had mentored and guided Creel's career development, emphasising operational and financial performance.

The diversification strategy of the CPR was ended in 2000, marking a return as a pureplay competitor (CPR Annual Report, 2001: 5). This strategic shift involved the breaking of the overall firm into five distinct entities, each listed on the stock market. Shareholders participated in this transformation by exchanging their shares in the original company for shares in the five newly created firms. The decision to pursue this breakup was met with significant attention, as reflected in the assessment published by the Canadian newsmagazine, Maclean's: Standfast, Craigellachie! Somewhere near that craggy mountain pass in British Columbia [Canada], where [on November 7, 1885] the last spike welded Canada together a century ago with a ribbon of steel, the ground is shifting. The mighty corporate empire is about to leave this mortal coil. By the end of this year, if corporate planners get their way and the stock markets don’t go kaflooey, Canadian Pacific Ltd – worth $18 billion and growing again suddenly – will transform itself from a gawky behemoth into five separate [firms], each with its own set of single-minded shareholders. (Sheppard, 2001) The [firms] will have a greater ability to develop independent strategies, pursue growth opportunities, use equity to facilitate growth, and design equity-based compensation programs targeted to their performance. (Dixon, 2001: 9)

In this transition to a pureplay strategy in 2001, the CEO of CPR acknowledged the significant challenge of shifting from the umbrella of a diversified conglomerate to direct accountability with the capital markets (CPR Annual Report, 2001: 5). New management implemented a comprehensive programme aimed at cost reduction (CPR Annual Report, 2001: 2) and increasing operating efficiencies. The adoption of a pureplay approach resulted in improved performance, as evidenced by the enhancement of operating income as a percentage of revenues as depicted in Figure 4. The pureplay strategy had the performance advantage expected.

The repertoire of goods transported by CPR during this period mirrored that of the previous strategic period, encompassing bulk commodities such as grain, coal, sulphur, fertilisers, forest products, intermodal shipments and automobiles. CPR's operations underwent significant transformations and workforce reductions through technological advancements since the introduction of diesel-electric engines in the 1960s. These technological innovations played a vital role in enhancing CPR's competitiveness (Timur and Ponak, 2002: 542). Over the years following the 1960s, CPR's management and unions jointly formulated protocols or rules for successful technology implementation, which became integral to the company's operations and continued growth (Timur and Ponak, 2002: 555). These protocols highlight the need for unions and management to maintain a ‘mature relationship’ characterised by strong contractual protections and adherence to business-like practices. This enabled the CPR to introduce innovative technology accompanied by fair compensation for employees in the event of job displacement. Consequently, during the 2001 to 2020 period, there existed a capacity for harmonious cooperation between the unions and CPR management.

CPR pursued a strategy of contracting out activities where it lacked world-class expertise. As part of this approach, CPR entered into a 10-year agreement with Consolidated Fastfrate to manage the less-than-truckload business through cross-docking operations (CPR Annual Report, 2001). Additionally, in the same year, ALSTOM was contracted to manage and operate CPR's large maintenance and overhaul shop in Calgary. The primary focus was jointly on cost reduction and maximising asset utilisation through an integrated operating plan known as Genesis. This operation emphasis centred on becoming a low-cost bulk carrier, enhancing efficiency and reliability as an intermodal service provider, and providing an appealing alternative to trucks for merchandise freight (CPR Annual Report, 2004). The key performance indicators for success during this strategic period were improved customer service and a reduced operating ratio.

In pursuing pureplay expansion, CPR extended its geographical reach farther into the US by acquiring the Dakota, Minnesota and Eastern Railways (CPR Annual Reports, 2007, 2008). This expansion was facilitated by reduced railway regulations in both Canada and the US. However, despite these strategic efforts, certain shareholders expressed dissatisfaction with CPR's performance. William Ackman of Pershing Square Capital Management initiated a proxy battle on 23 April 2012, arguing in a letter to shareholders that the existing CPR management was underperforming. Specifically, Ackman said: The incumbent board and management have failed shareholders, employees, and customers. Their failed stewardship of CP[R] and indifference to concerned shareholders make it clear that nothing less than a fundamental board restructuring and a new CEO will put CP[R] back on track. This is precisely what the seven Nominees for Management Change will accomplish if elected with a strong mandate for change.

11

Ackman's coup proved successful as he secured a position on the board of directors alongside seven new board members, while nine retired members exited (CPR Annual Reports, 2011, 2012). Concurrently, Ackman retained five senior officers while replacing seven others. Notably, his most significant appointment was Hunter Harrison as CEO and board member, roles that Harrison had previously held at the CNR 12 and other railways.

Despite experiencing modest annual revenue growth of only 2.9 per cent during the final strategic period, the pureplay strategy enabled CPR to achieve an operating income equivalent to 27.8 per cent of revenue. Furthermore, the operating ratio exhibited a favourable decline, reaching 72.2 per cent. Harrison, known for his expertise in enhancing operational efficiencies, employed his successful approach of Precision Scheduled Railroading, which entailed cost reduction, longer train operations, and significant workforce reductions, as seen in his previous endeavours with the Illinois Central Railway, CNR, and other US class 1 railways (Atkins, 2021: B1; Green, 2018). Atkins and Castaldo (2021: B1+) say Precision Scheduled Railroading improved overall performance. In 2017, Keith Creel, Harrison's protégé and the subsequent CPR CEO, further enhanced the organisation by nurturing relationships with customers, employees, union leaders, staff and shippers. Creel also implemented changes to the employee disciplinary system, addressing concerns raised by union members regarding the perceived harshness and arbitrariness of that system. Atkins and Castaldo (2021) note that Creel emphasised marketing tactics tailored to meet customer requirements. Together, Harrison-Creel successfully reduced the operating ratio and increased operating income as a percentage of revenue by implementing comprehensive cost-control measures, that is, 2016 was about next-level operational improvements, focusing on planning and execution, right down to the shipment level. We were relentless in pursuing and finding new ways to operate more efficiently, reduce costs, enhance service, and improve safety. (CPR Annual Report, 2016: 11)

Pureplay had a significant role in enhancing financial performance; however, additional emphasis on cost reductions and customer service improvements were essential in achieving the post-2012 favourable outcomes. Hence, we conclude that pureplay alone was insufficient to drive the desired improvements in financial performance.

The resulting improved customer service and reduced costs may appear to be inconsistent with one another, but that was not true. Harrison and Creel had, perhaps unintentionally, a two-step process, which was dependent on detailed scheduling and information for managing operations. First, Harrison as CEO dominated the cost reduction and efficiency improvements. Green (2018: 175) used annual report data for his explanation: At the end of 2016, the operating ratio was 58.6%, the best on record at the railroad – and down from more than 80 in 2012. Since 2012, average train length had increased from 5981 feet to 7217 feet. Average train speed had gone from 18.4 miles per hour in 2013 – Harrison's first full year – to 23.5 miles per hour in 2016. Average terminal dwell dropped from 7.5 h in 2012 to 6.7 h in 2016. Average train weight increased.… [All] of this was occurring with 12,082 employees versus the 19,999 at the end of 2012…

This first step was assisted by spending increases on information systems from $54 million in 2010 to $105 million in 2012 (CPR Annual Report, 2012: 102).

The second step, done by Creel, was making the rough edges of Harrison's efficiency change more amenable to employees and customers. Atkins and Castaldo (2021) said that Creel ‘softened the employee disciplinary system criticised by union members as harsh and arbitrary’ and ‘created the position of chief marketing officer – a position that Harrison never bothered with – and heralded a new focus on the companies that paid CP to move their goods’. Creel elaborated on the customer focus improvements: the CPR ‘gives … customers access to our fluid and reliable network as well as to the shortest routes to key markets’ (CPR Annual Report, 2017: 6).

Notably, in September 2021 (beyond the study period), the CPR and Kansas City Southern signed a merger agreement, establishing the first railway system connecting Canada, the US and Mexico. The resulting combined entity, named Canadian Pacific Kansas City, represents a pureplay market expansion (Berman, 2023: B7).

When evaluating this strategic period, the pureplay positioning enabled the CPR to operate in the top right quadrant of Figure 2, exhibiting high fungibility and low or zero opportunity cost. The authors deem this position to be the most desirable for achieving growth in performance. The high fungibility resulted from the CPR's efforts to improve the quality and reduce the cost of existing products and services offered to its current customers in existing markets. Additionally, the pursuit of operational cost reductions through system improvements incurred zero opportunity cost.

Analyses and discussion

We posed two questions for this study.

Why did the firm pursue diversification during specific strategic periods from 1883 to 2020? Why was diversification successful, or why did it fail to yield positive outcomes?

The answer to the first research question was: CPR pursued diversification in the middle two strategic periods, 1926 to 1965 and 1966 to 2000, to offset the significant decline in railway operating income as a percentage of railway revenue. Factors contributing to this decline included the loss of the CPR's monopoly, intensified competition and unfavourable freight rate regulations imposed by the Government of Canada. CPR intended diversification to mitigate the reduction in railway operating income. In contrast, the earlier strategic period, 1883 to 1925, exhibited railway operating income as a percentage of revenue at approximately twice the level of the subsequent periods (1926–1965 and 1966–2000), as shown in Figure 4.

As for the second research question, diversification was unsuccessful. Evidence for this conclusion is twofold. First, anecdotal evidence stems from the 2001 decision made to abandon diversification as a strategy and divide the overall firm into five separate stock market-influenced and listed firms. Management's conclusion at the time was that, overall, diversification had proven to be unsuccessful. Cominco and PanCanadian Oil and Gas were exceptions as they, operating with a significant degree of autonomy, achieved success under their own management teams and boards.

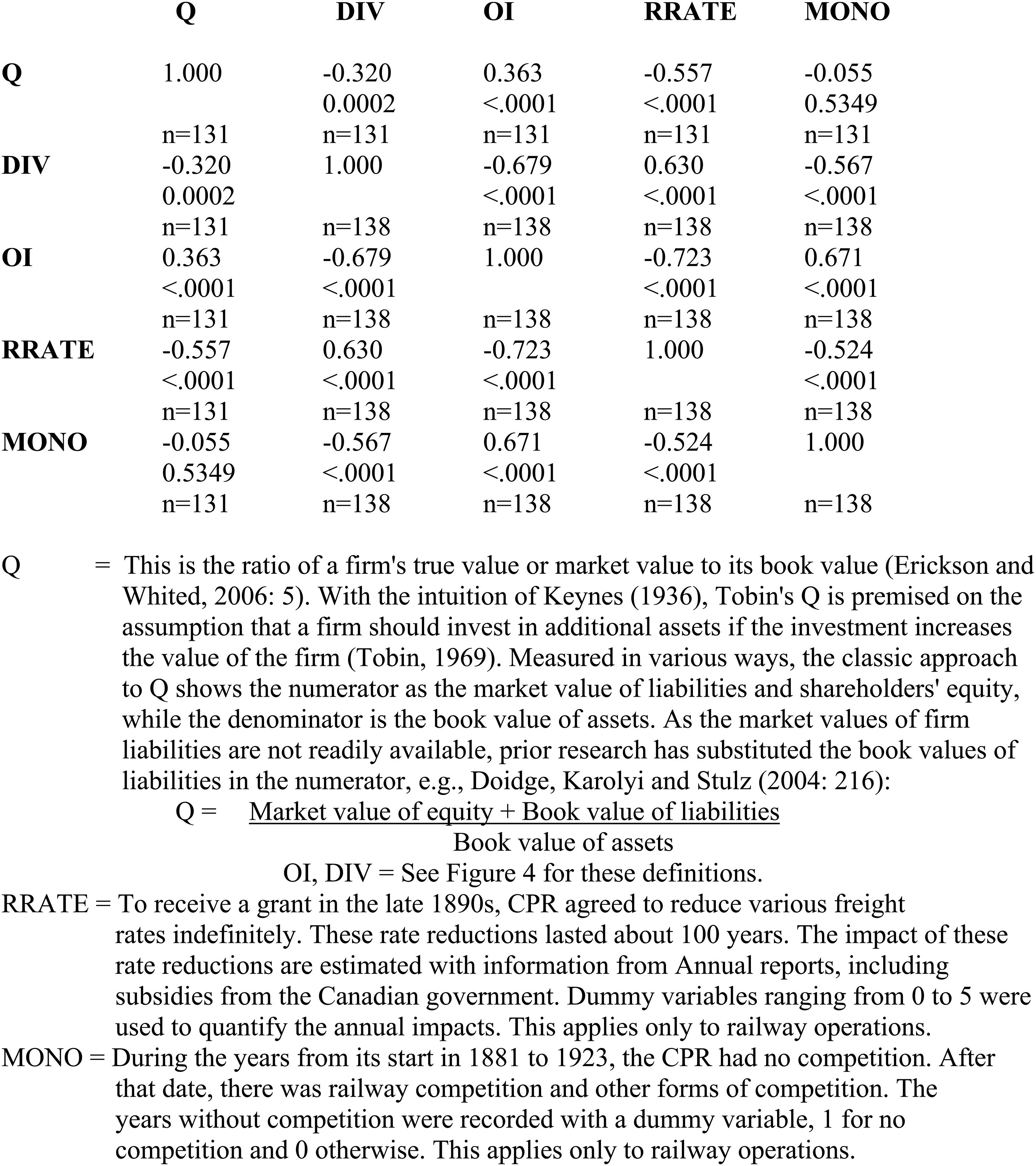

Quantitative data analyses provide additional insights, as reflected in the Pearson correlation coefficients presented in Figure 8, which explores the relationships between the railway's operating income as a percentage of revenue (OI), diversification (DIV), and other relevant variables. Over the entire study period, 1890–2020 13 , a statistically significant negative correlation (−0.677) was observed at the 0.0001 level between the railway's operating income as a percentage of railway revenue and the overall firm's diversification. 14 The message from the Pearson correlation coefficients is that diversification was increasingly pursued as railway operating income as a percentage of railway revenue decreased.

Pearson correlation coefficients, 1883 or 1890–2020.

Tobin's Q, the market's reaction – or evaluation – to CPR's diversification, is a ratio of the firm's market value of assets to its book value of assets (Erickson and Whited, 2006: 5). As expected, there was an adverse and statistically significant relationship between DIV and Q for 1890–2020, that is., the market reaction depicted with Q expressed an unfavourable assessment of diversification at the CPR. This finding is consistent with prior research (e.g., Lang and Stultz, 1994). Thus, quantitatively, based on the market's value as measured through Q, CPR's diversification strategies were unsuccessful.

Figure 8 also demonstrates that rate regulations (RRATE), which had a detrimental impact on profitability for nearly a century, exhibited a negative correlation with railway operating income as a percentage of revenue. Interestingly, regulation was positively correlated with diversification. This evidence suggests that CPR partly pursued diversification to offset the operating income losses caused by rate regulation. Additionally, the presence of a CPR monopoly (MONO) from 1883 to the early 1920s 15 exhibited a positive and statistically significant relationship with railway operating income as a percentage of railway revenue but a negative and statistically significant relationship with diversification.

As predicted by the literature depicted in Figure 1, the intended diversification strategies in the middle two periods were unsuccessful because they lacked any meaningful relationship with other investments or the railway to enhance operating income returns. Consequently, the study categorises CPR's diversification investments as portfolio investments. Referring to Figure 1, diversification investments did not benefit through high fungibility with the CPR or other diversification investments. Moreover, there were significant opportunity costs involved, as the overall firm raised external funds to finance diversification investments. Unfortunately, diversification focused on the less desirable bottom-left quadrant of Figure 1 instead of the desired top-right quadrant. Regrettably, the CPR's unfavourable diversification aligned with the literature's expectations.

Insights from the CPR's 2001–2020 period are noteworthy. Implementing the pureplay strategy led to improvements in railway operating income as a percentage of railway revenue, but Harrison and Creel achieved further enhancements. Harrison regarded the railway as a system for delivering services to customers. Green (2018: 51) described Harrison's Precision Scheduled Railroading as: service customers, control costs, utilize assets, don’t get anyone hurt, and recognize and develop people – and over time, he gained more confidence.… Freight trains ran on volume. Customarily, when the car was full, it would depart. Neither the railroad nor the customer knew when that would be. He said, we’re going to flip this very basic premise and run on schedule. By doing so, the railroad would utilize its assets at maximum efficiency and get rid of ones that it didn’t need, saving huge amounts of money.

Precision Scheduled Railroading emerged as a management technique to reduce costs and enhance customer service. In pursuit of greater profitability, Harrison focused on reducing the operating ratio through technological advancements, process restructuring and cost reduction, particularly in labour expenses. Harrison's deep understanding of railway systems played a pivotal role in improving operating income as a percentage of revenue.

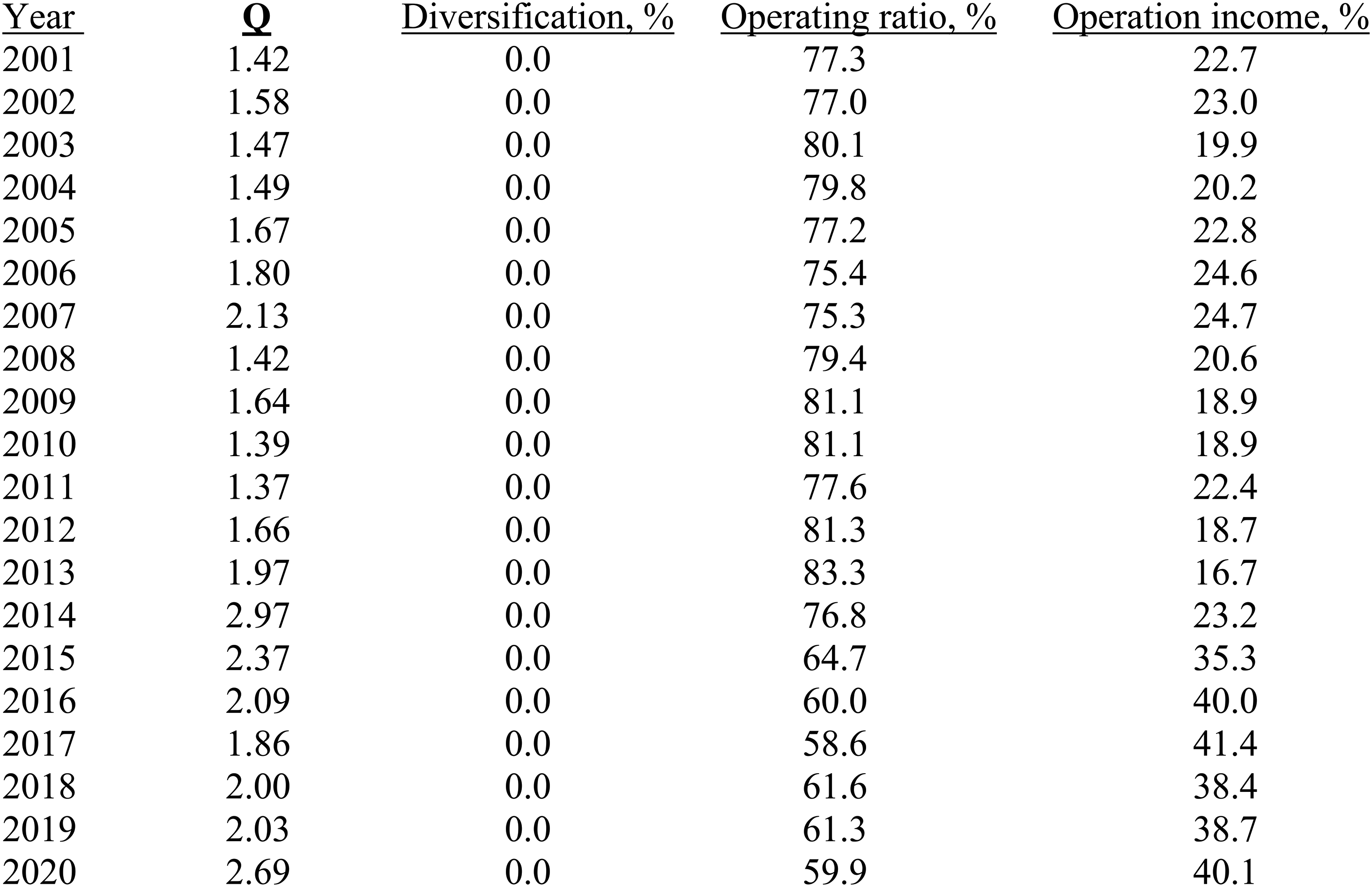

As indicated in Figure 9, during the 2001–2020 period with the implementation of the pureplay strategy, CPR witnessed a decline in operating expenses as a percentage of revenue in the first half of the period. However, these improvements fell short of the expectations set by Pershing Square Capital, the major shareholder that appointed Harrison as CEO for the CPR. Nevertheless, Harrison managed to further enhance railway operating income as a percentage of railway revenue, as demonstrated in Figure 9.