Abstract

This article aims to provide a historical perspective of neoliberalism and new public management practices in the Australian higher education system from the early 1980s to contemporary times. Drawing on historical and contemporary data sets and research articles, it evaluates historical changes in control systems and metrics applied to university teaching and research. From an audit culture framework, it examines the emerging rationales driving financially focused university governance. Organisational and individual audits of performance have become standard practice, couched in the conventional language of transparency, performance and accountability. Accounting-based performance measurement, control and audit are found to dominate university operations, fostering mass delivery of education, research outputs and knowledge commercialisation. Neoliberal performance management is shown to have dramatically altered accounting models and changed internal power relations, transforming university identities and roles into a commercialised corporate model pursuing a self-interested financial bottom line aided by a private sector performance control orientation.

Keywords

Introduction

The idea of a self-governing and independent public university system that safeguards its academic freedoms appears to belong to a bygone era (Guthrie et al., 2021). Instead, many of Australia's public universities have been transformed into academies of mass production for teaching local and international students (Guthrie et al., 2014; Parker et al., 2021).

The model of a public university as a corporate enterprise (Shore and Wright, 2004) emerged from the neoliberal higher education policies introduced in the late 1980s. These new market mechanisms focussed on universities as income-generating enterprises that would help reduce the federal government's burden to provide higher education funding (Guthrie and Lucas, 2022). Since then, the attention of senior university management, from university principals/vice-chancellors (VCs) down to an increasingly professionalised class of school deans and department heads, has been taken up with performance measurement for teaching and research, competitive quasi-market approaches to student recruitment, intense competition for research grant funding and changing expectations over what a university should contribute to society (Martin-Sardesai et al., 2020).

These changes are based on the accounting, auditing and accountability practices of new public management (NPM) (Guthrie et al., 1998). Consistent with neoliberalism, public universities have become increasingly focused on financial performance. Their organisational behaviour is now engineered through strategies, targets and elaborate measurement procedures (Parker, 2012). The techniques employed to achieve these ends – such as economic and accounting calculations and audit logic – are the same as those promoted by the Big Four accountancy firms (Shore et al., 2015). In aligning their behaviour with the Big Four, public universities have become champions of the NPM principles of efficiency, commensurability and accountability. However, critics rightly ask: Who benefits from these values? (Carnegie et al., 2021).

Over decades, various Australian governments have systematically restructured universities according to NPM principles and practices (Marginson, 1997a; Olssen and Peters, 2005). Within the Australian higher education system (AHES), the emphasis has been on the ability of universities to help create and disseminate knowledge; drive the knowledge economy by producing employable graduates; and undertake research that results in commercial innovations (Guthrie et al., 2017). Governments have shaped universities into politically and financially responsible authorities through regulatory legislation and budgetary policies. Furthermore, neoliberal techniques for controlling universities have facilitated governance at a distance while effectively intensifying central control by the government. Consequently, most universities today have highly centralised academic management systems. These forms of accountability arguably contradict the model of universities as autonomous democratic and cultural institutions (Carnegie and Napier, 2012).

In this article, we aim to provide a brief history of the impacts of neoliberalism on the AHES, paying particular attention to how NPM practices have influenced performance management systems (PMS) over the last four decades. This discussion on the changing landscape of higher education accountability practices and public policy has three objectives:

To identify various policy transformations in the AHES since the 1980s. To explore the intrusion of PMS practices into Australian public university operations nationally and locally. To reveal the implications of accountability-based performance measurement and control systems for Australian public universities on their contributions to civil society.

In pursuing these objectives, this article offers a national historical case study of the influence of neoliberal governmental philosophies and the implementation of NPM upon university identities, roles and associated internal performance management. Accounting and its influence on performance metrics will be considered in the context of the increasingly commercialised Australian university performance management and audit cultures exhibited over recent decades.

The rest of this article is structured as follows. The next section briefly outlines the methodological approach adopted in this article, while the following section provides background to the contemporary AHES. Then the literature on the neoliberal commodification of academic labour and the audit society is explored, while the next section contains a brief review of Australian policy since 1985, the four themes of the Dawkins reforms, the Hoare review and how assessments of research, teaching and students have been reconfigured. The subsequent section analyses the past four decades through the themes of accountability, audit and performance measurement systems. The final section provides conclusions and policy suggestions for the recent review of developing the Australian Universities Accord in 2023.

Methodological approach

In delivering this historical perspective, we have adopted an instrumentalist constructionist perspective where we reflect on contemporary events and interpret them through accounting for the past. By analysing the past, we seek relevant knowledge to inform the present (Hurst, 1981; Previts et al., 1990a). In particular, we seek to understand how past patterns of behaviour have shaped PMSs and accountability practices in the AHES (Previts et al., 1990a). The future implication of past change is also considered, as Demski (1985: 1972) argues, ‘Whenever we encounter a problem, it goes without saying that the problem has a past and, presumably, a future’. In addressing this, we take the attitude of historiographer John Tosh (1981), who sees historical research as making visible people, practices and outcomes. He challenges conventional wisdom and identifies past experiences and precedents that have led to the current policies and strategies. So, as argued by Previts et al. (1990b), we contend that reflections on the history of the AHES can provide valuable pointers to the ongoing trajectories of change.

Accordingly, we present a longitudinal narrative timeline account of the significant periods of change in the AHES since the 1980s, particularly identifying critical events, including the Dawkins AHES reforms, the Hoare review reforms to AHES, the Australian Research Council (ARC)'s reconfiguration of research assessment, and progressive changes to teaching and student assessment over the 40 years. Those major institutional changes are then revisited via thematic analysis of the underlying agendas and strategies involving the impact of NPM, the invasion of quality audits, the intensification of performance measurement, the orientation of teaching the student as a customer and the focus on commercial competition. This way, historical events are analytically connected to thematic reflections on current university system orientations and operations. In this way, accounts of the past are connected to reflections on current practice.

Nonetheless, we do not suggest that historical evidence will predict the future of the AHES. Instead, we believe that by contextualising the present and critiquing past events, we can identify patterns of change over time that might be useful for informing our decisions in the present and future (Carnegie and Napier, 1996; Parker, 1999). Carr (1987) argues that we seek connections between the past and the present to gain a better sense of the trajectory of change and pursue an enhanced appreciation of the future (Parker, 1997). From a postmodernist perspective, we share Jenkin's (2003) ambition of trying to render the previously opaque more transparent so that insights from the past can contribute to some hope of emancipating the present (Parker, 1997).

In presenting this historical reflection on the past and present trajectory of AHES change and focus at the macro levels of the national university experience, the study has employed governmental reports and prior published empirical and analytical studies from the accounting and higher education research literature. The latter covers both Australian and international published research, a significant proportion having been researched and published by the authors of this article.

In doing so, we acknowledge the exercise of reflexivity in our historical analyses and contemporary reflections as researchers with lengthy prior published research experience in this field of university commercialisation, accountingisation and performance management. As Haynes’ (2017) exposition on reflexivity in accounting research points out, our analyses and arguments concerning AHES historical changes and present trajectory bear the hallmarks of our positions as longstanding researchers into university governance, strategy and control and the analyses and findings of our research have been presented in the past, with respect both to Australian and international university trends. Our reflexivity acknowledgement must necessarily include accounting for our prior experience as researchers in this field and as academics in the university sector (in Australia and overseas) covering the past 40-year period (and more). This reflexivity has been exercised, mindful of our combined personal engagement in the university environment over these 40 years, occupying multiple roles from emerging to senior scholars, department headships, school deanships, research deanships, teaching program directors and more. Finally, such reflexivity also bears the imprint of our home discipline, accounting and the lens this brings to our historical examination.

Finally, this study's approach takes up Hopper's (1999) contention that accounting research can benefit from analysing and reflecting on the broad spectrum of published international research into specific issues to build on what otherwise can become a separate set of individual studies. Accordingly, this article analyses a considerable corpus of accumulated empirical and analytical studies, presenting a historically informed macro analysis connecting past and present.

The Australian higher education system

Comprising 37 public system universities and over 150 private higher education providers, the AHES is an economically and socially critical part of Australian society. On average, the AHES educates a diverse mix of 1.4 million national and international students yearly. In 2021, there was much doom and gloom from university management about the prospects for the higher education system. However, to the sector's combined financial report Finance 2021, released by the Australian Government Department of Education in March 2023, it is apparent that the talk of dark times ahead was nothing more than a smokescreen to drive down the terms and conditions of university employees and, more importantly, to make redundant over 50,000 staff.

The AHES in 2021 generated $5.3 billion as a net accrual accounting result from revenue of about $40 billion. The report reveals that combined payments by local and international students were $15.3 billion, whilst the government contribution for teaching and research was about $14 billion. Also, during 2021, there was a significant increase in cash and investments held by universities as of 31 December.

The report suggests that the sector fared well, with total cash and investments of $30.9 billion as of 31 December 2021, up $6 billion or 24.1 per cent from $25 billion in 2020. The universities ring-fence these assets and income from the university's operations, yet these funds have been built from operational revenue over decades. Only a tiny proportion of this $31 billion would be from foundations or charity gifts with special purposes attached to them.

However, this growth is primarily due to Higher Education Loan Program (HELP) loans, which domestic students repay in the future. It is estimated that outstanding student debt reached A$74.4 billion in mid-2022, up almost A$6 billion in a year and A$50 billion in a decade. With inflation at 8 per cent in 2023 and loans indexed to Consumer Price Index (CPI), these numbers will be higher.

In addition, the federal government-introduced fees for students in management, commerce, law and economics have risen by 27.7 per cent, in creative arts by 66.1 per cent, and in communications and humanities by an astonishing 113.1 per cent (Hurst, 2020). Furthermore, all this has occurred because of cost claims (Guthrie et al., 2020).

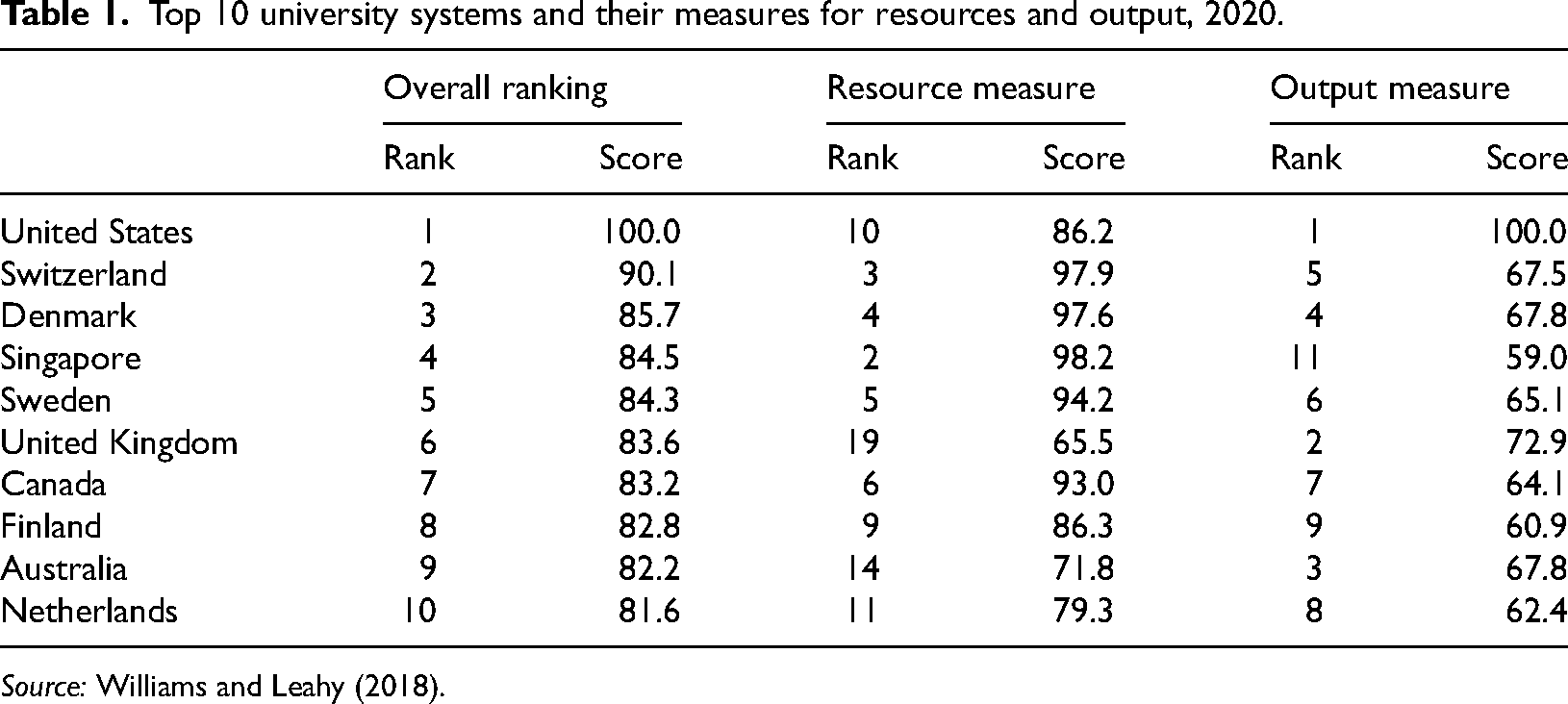

The Universitas 21 Reports provide an annual snapshot of higher education systems in 50 countries. Notably, these reports assess national higher education systems rather than individual universities. In 2020, Australia was ranked ninth worldwide and eighth the year before. However, Australia was one of only two countries in the top five for output that did not rank in the top 10 for resources – the other country being the United Kingdom. In this regard, Australia ranked 14th based on the resources available to its universities and alarmingly, Australia sits at 34 out of 50 countries in terms of government expenditure on tertiary education institutions as a percentage of Gross Domestic Product (GDP) (Table 1).

These impacts are due to the pervasive influence of neoliberal NPM practices and the operations model adopted by VCs in AHES over the past 40 years. Under these policies, undergraduate education has become far more narrowly focused on training students for immediate short-term employment and engagement with industry rather than laying the foundations for contributing to society over the long term. At the same time, a significant proportion of university teaching is now done by low-cost casuals (Guthrie and Lucas, 2022).

In short, AHES relies heavily on international students for income in contemporary times. It employs a highly casualised workforce to control costs and build flexibility into its labour force. Furthermore, it strategically focuses on student enrolment growth and international student fee revenues. However, even though this approach is unsustainable, it has become the default setting for political elites and university VCs (Hil et al., 2022; Lake et al., 2022).

Neoliberal commodification and audit

There are many definitions of neoliberalism, and its points of emphasis have changed over the decades. According to Brown (2015: 28), ‘Neoliberalism is most commonly understood as enacting an ensemble of economic policies in accord with its root principle of affirming free markets’. Indeed, it has been argued that market fundamentalism and self-interested economic competition have become the prevailing metaphors for social and cultural relations and institutions (Brown, 2015; Scharff, 2015).

When put into practice, neoliberalism aims to reduce the size of the public system and reassert political control by introducing NPM and new public financial management (Guthrie et al., 1997, 1998, 1999). In addition, it advocates an individualistic approach to accountability where citizens should be self-managing and self-enterprising rather than promoting collective responsibility (Morrish, 2017).

Neoliberal reforms have prompted various government-led public initiatives in higher education in Australia, the United Kingdom and internationally (Ferlie et al., 1996; Vodeb et al., 2022). From this foundation, governments have propelled higher education institutions towards a commodified redefinition of their identity and societal role. As a result, higher education responsibility has been detached from the public domain and re-attached to the market and private enterprise (Davies et al., 2006). Education is not seen as distinctive or unusual; it is treated as a product or service like any other, and its value is determined by the so-called marketplace (Parker et al., 2021). Nor have universities been exempt from the neoliberal ideal of personal responsibility. Thus, a culture of entrepreneurialism has been enforced, where surveillance mechanisms proliferate, financial accountability requirements constantly escalate and efficiency targets abound (Parker et al., 2021). By way of an aside, while these aspects may have proliferated in the AHES, Australian press articles in the 2020–22 period have begun to raise questions about university risk management and risk disclosures regarding their exposure and responses to such dramatic losses of international student revenues as occasioned by the pandemic and associated federal and state level Australian government responses and controls (Carnegie et al., 2020; Carnegie and Parker, 2021).

Nevertheless, over time, government funding for Australian higher education has, in real terms, been reduced. Parker (2011) referred to this as a clever sleight-of-hand, where the government reduces funding while imposing more interventionist performance controls over universities. For example, he identified that AHES student enrolments had risen from 393,734 in 1987 to 957,176 in 2005, while the proportion of higher education funding from the Commonwealth government fell from 85 per cent in 1987 to 41 per cent in 2003. Alongside developments such as this, there have been greater demands to account for how funding is used – accounts that rely on the elaborate neoliberal paraphernalia of auditing, accrual statements and other controls (Guthrie and Lucas, 2022). Within universities, the meaning of efficiency has shifted away from a generalised social and economic good towards a notional monetary value attached to designated products and practices. Thus, graduate students and published research have been redefined as primary products (Hil et al., 2022).

Moreover, this new university world of commodified products and services has become subject to monetised measurement and calculation. For instance, everything from the university to its teaching, research and graduate employment is ranked and rated. Furthermore, these rankings and ratings are primarily produced and controlled by external private companies like publishing houses and ranking organisations.

A culture of time charts, benchmarks, league tables and vision statements are now embedded in the models of academic production to the extent that, according to Halffman and Radder (2015: 896), what is at stake is the ‘very notion of knowledge itself’. These metrics undermine the professional autonomy of the academic and the values of independent critical inquiry. Moreover, they affect academic life and intellectual independence (By et al., 2013). Academic freedom is intrinsically linked to the notion of the university as a public good. It is central to higher education and affects all aspects of university work (Latif, 2014). Academic work is understood to be advanced through the ‘creativity … originality [and] freedom’ of academics (Henkel, 2005: 149–150). It is epitomised by an absence of interference and idealised in the freedom to pursue inquiry and publish findings (Finkin and Post, 2009; Liszka, 2008). Freedom to pursue one's research interests is a significant attraction for academics (Bexley et al., 2011). However, managerialism and an audit culture undermine these academic freedoms. They often erode the ability of academics to exercise their professional discretion and expertise in choosing areas of research they consider relevant, potentially significant or worth pursuing. Shore and Wright (2015) define audit culture as the process by which accounting and financial management are employed in the governance of people and organisations and the degree to which their measurement and ranking practices have been financialised, institutionalised and become all-pervasive – even in the routine language of organisational life. They point to such audit culture's social and cultural consequences as major issues.

The surveillance of academics by university audit culture and calculative practices has rightly become an object of study – and activism – mainly because of the increasing use of digital technologies to monitor and control employees. Measuring academic outputs, quantifying scholarly work and controlling culture have become so ingrained that auditing has become a central organising principle (Shore and Wright, 2015). Performance audits of the university and its employees are not just performance management and governance techniques; they are a mode of thinking. To argue that their activities are evidence-based, ranking organisations overproduce quasi-empirical language (Shore and Wright, 2015). Rating systems and league table comparisons have become popular. The scale to which performance indicators and audits have spread in contemporary times is extraordinary, and universities and society have embraced and endorsed them (Connell, 2022). Audits appear to be natural and benign solutions to performance management and governance (Shore et al., 2015). However, Power (1997) suggests that while audits and indicators may promote organisational transparency, they become opaque. Indicators become targets as institutions are reshaped according to the criteria and methods used to measure them. Hence, universities and academics alike are transformed into auditable entities that focus their energies on doing ‘what counts’ (Carnegie, 2023).

It is worth observing that Harvey (2005: 162) identifies another characteristic of neoliberal institutions as ‘the management and manipulation of crises’. Anyone who has worked in Australian universities since 1980 will recognise that their careers have unfolded in an era of constant crisis management, accompanied by urgent calls for ‘change’, ‘efficiency’ and ‘modernisation’ to forestall further turmoil (Sims, 2022; Tregear et al., 2022). Morrish (2017) argues that academics have gained nothing from pursuing corporatisation and that their silent acquiescence to the process has made them collaborators. Canaan (2010: 58) asks, ‘Why do we all just keep going along with it?’ suggesting that the answer is because the carrot of self-actualisation is dangled before academics while their compliance is ensured with the stick of internal regulations. Whatever the root cause, it is undeniable that, as governments have transformed universities into neoliberal institutions, academics have been hard-pressed to generate a collective position of resistance (Hil et al., 2022).

Post-1980s national higher education policy transformation in Australia

Our review of Australian national higher education policies since the 1980s highlights that the AHES has not been immune to neoliberal commodification and audit practice encroachments. Financial quantification, performance management, control and accountability have been central features in the policy changes implemented, and these tenets have been embedded in a series of reforms. The changes started with the Dawkins reforms of the late 1980s and subsequent policy and funding developments, as outlined in the following sub-sections.

The Dawkins reforms

John Dawkins, the then Labor Federal Minister for Education, was focused on clarifying the federal government’s responsibility for higher education institutions (Bay, 2011). Responding to the introduction of major neoliberal reforms in the 1980s under NPM, the AHES moved to quasi-market-based operations for teaching and awarding degrees (Guthrie and Neumann, 2007). The Dawkins changes then led to abolishing the then-binary higher education system (consisting of colleges of advanced education (CAEs) and universities) and establishing a unified national system for higher education. The Federal government's focus was also on developing budget management structures and a changeover by universities to an accrual audit and reporting system to emphasise efficiency (Guthrie and Parker, 1990).

In the binary system, universities were funded based on their teaching and research activity, and CAEs were funded according to their number of approved courses. However, introducing this unified national system required CAEs to amalgamate with existing public universities (Coaldrake and Stedman, 1999). The consequent demise of the binary system led to a reduction in the number of higher education institutions from 88 (19 universities and 69 colleges) to 36 universities by 1996 (HEC, 1988; Mahony, 1992, 1993).

The new system also required each university to have a standardised single governing body, one chief executive, one educational profile, one funding allocation, and one set of academic awards (Gamage, 1992; Marginson, 1997b). The system was based on the assumption that it would be easier for the government to govern the system under a unified approach (Bessant, 1996). The preference was for ‘strong, decisive implementation … [and] policies by institutional managers’ (Dawkins, 1988: 101). The reforms encouraged universities to adopt smaller governing bodies comparable to the boards common to private businesses. These ‘specialised management skills’ were essential to university management (Dawkins, 1988).

Another objective of the Dawkins policies was to prescribe a review of institutional management to ensure systems of accountability and performance measures were developed (Dawkins, 1987). The subsequent Dawkins (1988) White Paper foreshadowed the changing accounting mechanisms, performance indicators and audit practices for higher education funding arrangements and the university profiling process. In addition, research was to be funded increasingly through competitive grants with the ‘goal of maximising the research potential of the AHES and achieving a closer alignment with broader national objectives’ (Smith, 1989:1). Thus, the defined role of research within the AHES in the 1990s was reorganised, and research funding was to be allocated based on competitive principles.

The Hoare review

The Hoare Review (Hoare, 1995) was the next major reform in the AHES. This review recommended that universities adopt contemporary governance, managerial capacities and workplace practices. Performance measurement, centralised management and cost reductions were the core principles of managerialism translated into Australian public universities by the Hoare Review, thereby diminishing the scope for academic authority and collegial processes. In particular, the newly introduced professionalised organisational system of university governance, imported from the private system, offered a process that could break existing academic power structures. In this period, power struggles between academics and administrators emerged in response to the rise of managerialism, especially regarding finance and resource allocation (Lake et al., 2022; Ryan and Guthrie, 2009).

To cope with conflicting pressures, university VCs often opted for a new professional-managerial class to control operations and finances. Under managerialism, performance and performance management came to be seen more in quantified economic and financial terms than in qualitative social terms. Thus, during the 1990s, universities imported business accounting and management control techniques. These included establishing quasi-markets, fostering employee competition, marketising public system services and developing efficiency measures (Parker and Guthrie, 1998).

Reconfigured research assessment

Since its establishment in 1987, the role of the ARC has been to provide (along with other government agencies) both research funding and research policy advice to the AHES (Harman and Meek, 1988). However, the Australian Research Council Act 2001 transformed the ARC into an independent body. As a result, the ARC granted a broader range of advisory functions and full administrative responsibility for assessing grant applications (ARC, 2012). The ARC also became responsible for various research support schemes, moving research funding mechanisms away from indirect means (e.g., through the core funding of the AHES) to direct and competitive financing of individual research projects and researchers (ARC, 2016).

Over the ARC's history, different performance measures and indicators have recorded and measured research activities (Martin-Sardesai and Guthrie, 2018). This has included the Relative Funding Model, the Research Quantum, the Institutional Grants Scheme, and other models focused on formulae-driven, project-based funding and performance-based block research grants. 1 These changes have had significant impacts on university research and the manner of its accounting and financing. The ARC's declared priority research areas used to be determined by federal government guidelines (e.g., by Ministers). These guidelines dictated the distribution of the research quantum and the use of associated PMSs. Now the ARC announces its priority research areas and associated PMSs annually. These announcements directly impact how universities operate, with many adopting a corporate business focus on performance measures, audits and controls to secure ARC funding.

Reconfigured teaching and student assessment

Student evaluations of university teaching have a relatively recent history in Australia, notably triggered by the 1964 Martin report into Australian higher education. In 1969, there was a call by the increasingly organised National Union of Australian University Students for teaching and learning units and teaching abilities to be factored into academic tenure and promotion decisions (Darwin, 2016). Additionally, academics were required to hold compulsory teaching qualifications. These calls came in response to growing tertiary student dissatisfaction with teaching quality. Factoring teaching abilities into tenure and promotion decisions was a particularly controversial demand that attracted attention across universities. This issue was still not resolved by the early 1980s (Australian Vice-Chancellors’ Committee, 1981). However, the so-called Dawkins (1987) reforms to the AHES reorganised the university system and introduced student assessment of teaching as a staff performance metric. Hence, students evaluating teachers was effectively mandated by an accord between the Australian government and the reorganised Australian universities. This essentially transmogrified students into education consumers (Darwin, 2016).

The year 2000 saw the introduction of a quality assurance framework (Commonwealth of Australia, 2000). The framework included: external five-year cyclical quality audits by the Australian University Quality Agency; federal government monitoring of university performance across enrolments, student experience, academic outcomes and graduate employment; and accreditation compliance with a range of laws, regulations and the Australian Qualifications Framework. In 2008, the Bradley et al. (2008) review of higher education, however, found the system highly complex with an excess focus on quality assurance systems and processes rather than outcomes (Shah and Jarzabkowski, 2013; Shah et al., 2011b). As such, quality assurance policies for teaching and strategies driven by the government have been a continually evolving phenomenon in the AHES landscape – a phenomenon that involves ever-expanding bureaucracies and audits to secure performance-based funding in a period of funding declines and shortfalls (Shah et al., 2011a, 2011b).

From the 1980s onwards, government and university management's general focus has been graduation and completion rates. Now, four decades later, universities pursue various statistics and performance metrics. To name just a few, they chase local and international student loans, student liability status, trends and Commonwealth-supported places, enrolments in courses leading to professional registration, work-integrated learning, student satisfaction with teaching and university experience, student outcomes and employment, award course completions, attrition and completion rates, graduate salaries, jobs by industry and occupation and completions by the skills priority list, along with many others. PMS such as those that grade students’ experience of lecturers and study units now observably drill down from organisation-wide metrics to the individual academic. Such metrics are often presented as scorecards, some of which are made publicly available by the universities because management thinks highly rated academics will attract more students to their subjects.

What is observable is that government funding is not based on any of the above multiple metrics other than federally supported places, an input activity and capped university places, an input criterion. Today, in public universities, most local students pay a substantial part of their higher education costs through the Higher Education Contribution Scheme (HECS) loan scheme, and international students pay total fees plus whatever the university can charge extra (this can be in the tens of thousands per student). Experience shows that university management prices very highly the latter source of revenue as an alternative source of funding to the still limited funding supplied by the government. Reflecting their apparent perceptions of a university revenue dependence on their fees, students have often been observed to employ course evaluations as an avenue for highlighting their disappointments. These can take the form of unfair evaluations of courses and teaching in reaction to performance standards required and results expected or achieved by students in the latters’ attempt to attribute their own performance to ‘poor teaching’ rather than ‘poor learning’. In a commercialised university environment where the student has been transmogrified into fee-paying customer, students often appear to avoid accepting accountability for their own efforts and performance (Lama et al., 2015). In response, university management has been observed by staff as increasingly caving into the critiques levelled by students who are oftentimes being regarded as more reliable or dependable than academic staff. Such gaming has arguably become a significant feature of university culture and life, risking the undermining of the organisational culture of universities as learned institutions.

Accountability, audit and performance measurement systems

As seen above, the intrusive practices of accounting, audit, accountability and performance measurement in Australian public university operations have had far-reaching effects over time. In particular, four impacts are worth exploring: the imposition of managerialism, the audit explosion, national research assessment exercises and pre- and post-COVID-19 impacts. These areas have gained prominence not only because there has been an erosion of trust between the Australian government and public universities but also because various research and teaching assessment exercises have introduced a plethora of performance criteria and accountability rules. In response, public universities have imposed strategic monitoring of faculties, departments and individual academics. As a necessary condition of the managerial model, any semblance of collegial democracy has been weakened or already eliminated (Baum et al., 2022).

The onset of managerialism and new public management

The reforms of the 1980s are referred to as ‘managerialism’ in the public system accounting literature (Guthrie et al., 1990; Parker and Guthrie, 1993). They include five characteristics (Guthrie and English, 1997; Martin-Sardesai et al., 2019):

clear and consistent objectives that incorporate strategies, plans, performance agreements and individual programs; greater managerial autonomy through the delegation of ministerial authority and the devolution of managerial authority to senior management; performance evaluations through performance indicators at the national, organisational and individual programme levels; the introduction of accrual accounting statements for external accountability; and rewards and sanctions for senior public service managers.

This managerialist trend has gone hand-in-hand with the gradual commercialisation of Australian universities whose managements strive to comply with Australian government economic agendas and generate massive financial returns from overseas student recruitment. Thus, the core strategic values of most universities have evidenced a gradual shift towards market share, competitive positioning, financial returns, industry partnerships, vocational relevance and customer responsiveness (Parker, 2002). Image, brand and customer service have become a language and an ethos that increasingly permeates the university lexicon while, despite public protestations to the contrary, service to the public interest has been gradually replaced by priority service to government, industry, commerce and the university's own financial and growth objectives (Carnegie, 2022; Parker, 2011).

Supported by neoliberal political rationality, managerialism has become manifest in NPM practices. It has filtered its way into universities through the financial management improvement programme, an umbrella mechanism to implement managerial reforms throughout the Australian federal public system (Department of Finance, 1994). Managerialism has introduced a distinctive mode of governance into universities in Australia – one that is focused on financial and operational accountability. Neoliberal techniques allow the federal government to maintain governance at a distance while university management exerts control through highly centralised management processes (Marginson, 1995). Top-down management controls and performance measurement have influenced everything from university executive management to individual academics. These practices have positioned Australian academics as self-managing individuals, supposedly ‘free agents [that] are empowered to act on their behalf while “steered from a distance” by policy norms and rules of the game’ (Marginson, 1993: 63). They have become passive employees subject to top-down, authority-based management and intrusive individual performance controls. The multiple performance measures applied to academics were observed as early as two decades ago by Parker (2002) when he identified the neoliberal pressures for measurable individual performance outcomes. These, he argued, produced a self-focussed individualistic approach to academic work; academics began focussing their efforts on tasks that are measured and rewarded.

The audit explosion

Consistent with neoliberalism, the Dawkins Reforms of 1987, instituted by the federal Labor government, ushered in sweeping changes to Australia's higher education system that spanned management structures, pricing, the devolution of budgets, auditing mechanisms, reporting systems and more – all in the name of improving service delivery, efficiency and effectiveness (Guthrie and Parker, 1990). NPM emphasises accountability and efficiency through explicit quantitative performance measures and external audits, including performance reviews, staff appraisal systems, performance-related pay, quality audits, customer charters and quality standards (Parker et al., 2021).

There were three rounds of Quality Audits between 1993 and 1995, with the promise of additional funding as an incentive for institutions to conform with the government's priorities (Gallagher, 2003). From 1996 on, quality issues were incorporated into each institution's reporting obligations (Gallagher, 2003: 30). Power (1997) phrases this regime as ‘the audit explosion’. It is a regime that requires expert judgement about which ‘realities’ are to be selected for examination. It also narrows attention to only the auditable aspects of performance, excluding other aspects from view. At the same time, auditing has become a standard way of dealing with and absorbing various social problems (Power, 1997). Governments believe in transferring market properties to public services because they see NPM delivering benefits in the guise of efficiency – tightening accountability and social control. Power (1997) calls this the ‘audit society’.

The Australian government has employed PMS to steer the AHES towards teaching and research performance. Inherent within these systems is a requirement for universities to be more responsive to the strategic imperatives of the government. Their inception has taken the form of explicit teaching, research performance indicators and quality audits. Universities, in return, have been required to meet accountability demands in the form of performance reporting and quality audits by government agencies. These expectations have been monitored through performance targets and other accountability mechanisms, such as audited accrual financial statements, enterprise profiles and quality audits through the Australian Universities Quality Agency and Tertiary Education Quality and Standards Agency.

Research assessment exercises: An intensification of performance measurement

Coinciding with the emergence of global university ranking (GUR) systems (Harman, 2009), the Australian Government in 2006 announced that it would be establishing an assessment/audit of research output in the form of the research quality framework (RQF) (Martin-Sardesai et al., 2015). From its inception, the RQF was pilloried as ‘poorly designed, administratively expensive and relying on an impact measure that is unverifiable and ill-defined’ (Carr, 2008). Although a change in government in 2007 led to its cancellation, the new federal Labor government in 2008 announced a replacement for this national research assessment scheme called Excellence in Research for Australia (ERA). Enacted in 2010 across all Australian universities, the ERA is a quality assurance process that uses metrics (or other agreed-upon quality measures) appropriate to each research discipline. The AHES has engaged in subsequent ERA exercises in 2012, 2015 and 2018 (Martin-Sardesai et al., 2019).

Early on, the ERA focused on rating research and ranking journals and publishers. National and international rankings (or league tables) from these assessment exercises now play a role in managing universities (Martin-Sardesai et al., 2017c). However, what is less explicit is that implementing ERA 2010 produced a potent form of a governmental audit. Its outcomes (in the manner of ratings) have incentivised a strategic and operational response by the management of Australian public universities to enhance the quality (and quantity) of research consistent with ERA requirements. To this end, universities have instituted highly instrumental PMSs covering internal research, individual academics and disciplinary groups (Martin-Sardesai et al., 2017c).

In pursuing higher ERA scores for various disciplines, universities are manipulating these measurements and increasingly quantifying research outputs at both the individual and the departmental level and embedding those metrics into their PMSs (Martin-Sardesai et al., 2017a). The consequences include significant research pressures that constrain the freedom of academics to conduct research of their choice and the need to reconcile their research interests with the strategies of their universities (Martin-Sardesai et al., 2017b).

Such research measurement approaches also have induced some academics to prioritise research compared to other work. With scholarly productivity increasingly measured and audited through quantitative indicators based on PMS data such as publications and grants, academics have come under intense pressure to publish and win research grants while also focusing on their teaching responsibilities and workloads. This has increased academic workloads and stress (Martin-Sardesai et al., 2017c). The dynamics of these impacts on academics have been amply evidenced by Vesty et al.'s (2018) survey of Australian and New Zealand university accounting academics. Vesty et al. (2018) find that emotional exhaustion is common and that many academics are suffering from a risk of burnout due to high workloads, long working hours and a lack of personal recognition which produces significant levels of staff cynicism, fatigue and job dissatisfaction.

Teaching and student-as-customer assessment

As a result of 40 years of ‘metrifying’ teaching and research, these two spheres of education in the AHES have become oftentimes disconnected (Norton et al., 2013). While university management may promulgate the teaching–research nexus as a marketing strategy, the idea is now a myth (Krause, 2009; Mayson and Schapper, 2012). Education has been massified (Tight, 2019). This trend has been reinforced by large class sizes, customer-responsive packaging of the educational product and the large-scale casualisation of Australian university teaching (Parker, 2013; Shah et al., 2011a).

Several recent studies addressing scholarly work in academia have indicated significant changes in how individual teachers’ performance is evaluated (Grossi et al., 2020; Kallio et al., 2021). For instance, Grossi et al. (2020) find that universities and academic workers are affected by a range of pressures, including government regulations and control of the state (state pressure), the expectations of the professional norms and collegiality of the academic community (academic pressures), and the need to comply with international standards and market mechanisms (market pressures). This line of research exists at the intersection of two broader academic traditions. One addresses NPM and PMS (e.g., Parker, 2012; Steccolini et al., 2020); the other studies change in higher education organisations and the academic profession (e.g., Kallio et al., 2020; Martin-Sardesai et al., 2019).

The past decade has seen a particular consolidation of the last 40 years of performance management in the contemporary Australian university context. Performance-based funding has exacerbated the trend towards management's pursuit of prestige and marketability. Rather than prioritising quality teaching and research, universities now seek higher positions in the global league tables. There also appears to be obsessive compliance with the government's quality review cycles. The role of the student experience and course and lecturer evaluation metric as a performance management tool. This has only reinforced the deferential elevation of the student to the position of a fee-paying customer.

Furthermore, as we know, customers can, without foundation, threaten expertise, independence, quality and fitness for purpose – in the case of education, this means educator expertise, course quality and graduate employability (Darwin, 2016; Parker, 2002; Shah et al., 2011a; Shah and Sid Nair, 2012). Universities today are, arguably, too sensitive to student evaluations. What used to be a voluntary exercise is now compulsory. Shah and Nair (2012) explain the linkage between teaching scores and annual performance reviews for academic staff.

These recent historical trends have driven an intensely quantified performance measurement and management approach. Driving a compliance and marketability focus down from organisation-wide to individual academics has had profound implications for the autonomy of universities and their academics. It arguably carries questionable motivations, orientations and outcomes concerning course content standards, the quality and rigour of assessment, grading standards, actual student attainment levels and graduate suitability for employment (Shah and Jarzabkowski, 2013; Shah and Sid Nair, 2012).

A commercially competitive agenda

Returning to the GUR systems mentioned earlier, Carnegie (2022) points out that Australian universities have been beset with an accounting-based obsession with metrics and rankings-based performance. His analysis of the vision and mission statements of 37 Australian public universities reveals them as having arrived at a state of macro–micro contradiction. While their public declarations report their macro-contributions to local, regional, national and global societies, their internal micro-measurement metrics-driven management control sees them focused on pursuing Key Performance Indicators (KPIs) that will enhance their GURs. Carnegie (2022) argues that these micro-strategies focus on driving performance metrics for academic staff and producing outcomes that build brand profiles to increase revenue.

That naked commercial agenda is also revealed in Flemings’ (2021) analysis of how universities transformed after the onset of COVID-19. From reports published by several prominent consulting firms, he identifies that, since the 1980s, universities have increasingly engaged management consultants following the NPM spirit of commercialising the public sector. This involvement, he argues, has often been concealed by universities because they implement business strategies that are primarily unsuited to the unique missions of a public university. However, this commercial agenda has increasingly been ‘sold’ by consultants as a necessary response to the exigencies of the pandemic. University managers have seized the opportunity to downsize staffing, slash operating costs, curtail working conditions, casualise contract work and tighten performance targets. These are neoliberal philosophies that have been imported from the private sector. However, the recent pandemic has provided an excuse for these austerity measures to become entrenched in the university's fundamental mission. Such trends have been in ample evidence for over two decades (Parker, 2002, 2011, 2012, 2013, 2020). In substance, our public universities are now, effectively, ‘public’ organisations in name only (see, e.g., Carnegie, 2022). The institutional propensity for constantly aggressively chasing higher GURs increasingly makes their explicit mission and vision statements less believable, if not approaching irrelevance due, to the ‘loud noise’ emanating from GURs, not just in Australia.

Moreover, this commercially competitive agenda has grown over recent decades into a dominant strategic focus for Australian universities. To this end, they have proliferated their internal performance metrics, redoubled their controls and leveraged the results as marketing tools to appeal to target stakeholders. Wide now is the spectrum of metrics for reputational claims: marketplace rankings, learning and teaching indicators, research performance, community engagement, student numbers, graduate employment, publications statistics, facilities expenditure, and more. Performance ‘quality’ has become code for quantity, speed, growth, cost control and profits (Parker, 2013, 2020).

Conclusions

This study reveals a significant shift in AHES profile, focus and management since the 1980s. It shows evidence of the onset and pervasiveness of the NPM audit culture resulting from Neoliberal philosophies that, as in many Western countries, have consumed government and parliamentary thinking. During this period, Australian universities have experienced massive growth in student numbers (only recently interrupted by the COVID-19 pandemic) as they have been let loose by Australian governments to self-fund their operations and contribute to the national economy increasingly. As a result, the past 40 years have witnessed a significant transmogrification of university missions that, while ostensibly still proclaiming their societal role, have been refocused on their corporate financial success built on a neoliberal user pays approach to national and international student recruitment and associated revenues. Simultaneously they have been observed to placate government policy agendas by their fixation on graduate employment outcomes, alignment with ruling government policy objectives of the day, and winning recognition for their performance as contributors to the national economy.

Australian universities’ embracing NPM has transformed them from a former predominantly public sector entity to becoming broadly commercialised corporates or government-owned business entities. In so doing, their leadership and governance have changed to mimic their private sector corporate counterparts, a professionalised managerial class has overtaken their senior and middle-level leadership, and performance control and audit within the organisation have become the order of the day. Accounting and accountability have emerged as key players in facilitating this new university profile, role and audit culture embedded throughout higher education teaching, research and external engagement functions. The all too familiar accounting tools and processes of private sector performance measurement, management, control, reporting and audit now drive university strategies and have arguably reconditioned their core values.

The performance management and audit cultures have not only become central to university organisational level strategic thinking and behaviour, they have permeated the individual academic teaching and research staff levels. The latter has been increasingly subject to all-pervasive and intrusive performance surveillance, metrics measurement and individual rankings with which, in pursuit of job retention and career progression, they appear to have been willingly compliant.

What is noteworthy in this historical reflection has been the apparent success of governments while requiring universities to compete in the global marketplace in maintaining remote control of the AHES. This has been achieved despite the actual decline in government funding of the AHES. The recipe has been one of proliferating attention to global and national rankings, expanding arrays of metrics applied to teaching, research and engagement activities, as well as ever more intrusive ‘quality’ audits of teaching and research. Just as academics have become compliant with their employers’ expanding array of performance management metrics and controls, universities have similarly become compliant with governments’ NPM performance metrics. Given universities’ enthusiastic embracing of their now emerged commercialised corporate identity, they have accordingly adopted the proliferating metrics and rankings that have been applied in the AHES, frequently selecting those most favourable to their claimed marketplace image, brand and status ranking. Those metrics and rankings, however, reflect claimed ‘quality’ control tools and processes rather than actual practical impacts and risk reinforcing self-interested commercial outcomes focus rather than a contribution to the broader society. This raises the question of whether the post-1980s emergence of AHES performance management led the sector to mirror the commercial world stereotype: Australian Higher Education now appears to be all about the financial bottom line.

This transmogrification of Australian university identity and role over the past 40 years has had profound impacts both externally on its societal role and internally on the work and roles of its academics. They have been subject to increasingly intrusive performance measurement and control systems to which they appear to have reacted with almost universal compliance. Their internal goal displacement is reflected in their pursuit of satisfactory student teaching evaluation scores, volume and ranking of journal article publications and research grants demanded by their employers. Performance metrics have replaced original contributions to knowledge, societal critique and community engagement as their prime concerns.

In offering this historical case study and critique of performance management in the AHES, we pose fundamental questions for the future. Has university commercial and reputational self-interest permanently replaced its public interest role? Will the now predominant role of Australian university academics as production-line manufacturers of accountingised and measurable teaching and research products continue into the long term? Have we accounting academics been complicit in the creation and promotion of the very performance control and management systems that have contributed to the gradual erosion of academics’ and universities’ wider community service role? We contend that our historical analysis connecting past to present has revealed disturbing insights into the inner workings of the university system. What of the future? As historians, we must historiographically desist from offering predictions for the future trajectory. As Carson and Carson (1998) and Parker (1999) argued: …it is important to recognise that history's ability to predict is limited by the uniqueness of each event or chain of events and their surrounding circumstances which are unlikely to ever be exactly replicated at a later date. Hence history offers explanation rather than prediction, laying a basis for informing present and future decisions by way of illuminating precedents…. (Parker, 1999: 20)

Top 10 university systems and their measures for resources and output, 2020.

Source: Williams and Leahy (2018).

Footnotes

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.