Abstract

The objective of this article is to describe instances of charity accounting relating to a natural disaster in Sweden and to analyse the relationship between charity accounting and dimensions of moral conception prevailing in Sweden in the second half of the nineteenth century. Drawing on accounts of the Stockholm Relief Committee for Norrland, a temporary charity organisation established during the Swedish Famine of 1867–1869, the study shows that moral conceptions affected not only the distribution of relief but also what was accounted for. There are also indications that accounting was used to enhance the morality of the propertied class to act in the interest of those in need. In this way, the broader social implications of accounting history are considered, and previous conceptions of accounting as a one-sided technology exclusively favouring propertied interests and enhancing the morality of the poor are challenged.

Introduction

This article concerns a calamity resulting from ‘exogenous shocks’ in one of the Nordic countries: Sweden. Extreme climate events during a period of three years caused what came to be known as the Swedish Famine of 1867–1869 (henceforth: Swedish Famine), the last famine in Sweden of the ancient type (Nelson, 1988). Extreme weather brought about crop failure and obstructed the distribution of help especially to and within the northern parts of the country (Häger et al., 1978). Whereas the temperatures in the northern parts of Sweden in 1867 were well below the averages for that decade, the years 1867, 1868 and 1869 in the south-eastern parts of the country have been referred to as the wet year, the dry year and the hard year (Nelson, 1988; Västerbro, 2018). Sweden was not alone in experiencing famine in the nineteenth century. Finland was likewise struck during the same period (Häkkinen and Forsberg, 2015; Nelson, 1988) and valuable insights into accounting history have, for instance, also been gained in relation to the Irish Potato Famine (Funnell, 2001; O’Regan, 2010).

Many researchers have stressed the role played by accounting in society. Among other things, it has been shown ‘how individuals are controlled, restricted and in some cases enabled through the use of records and calculations’ (Napier, 2020: 34). Miller and O’Leary (1987), for instance, use Foucauldian concepts, such as the ‘calculable man’ to interpret standard costing as a means to construct the worker as a ‘governable person’. Research on natural disasters has highlighted the need to go beyond calculative and rational accountability and to focus on the potential social benefits provided by accounting (Baker, 2014; Lai et al., 2014; Sciulli, 2018). Similarly, accounting history research on poor relief in general and relief during famines in particular has described the role of accounting in constructing the social world. Walker (2004) outlines the social and behavioural consequences of calculative inscriptions of the poor during the early nineteenth century. Walker (2008: 454) argues that accounting was ‘a facilitative device in the stigmatisation of the poor in England and Wales’ and ‘the vast accounting apparatus constructed by the imperial government to support the task work system in Ireland in 1846–1847’ was investigated by O’Regan (2010: 428). A common theme, notable also in the work of Funnell (2001) and previous research on the Swedish Famine (Häger et al., 1978; Västerbro, 2018), is how underprivileged people experienced exercises of power by propertied interests. However, Ó hÓgartaigh et al. (2012: 242), who studied the pre-famine years of the Irish Poor Law 1838–1845, provide evidence that accounting did not ‘construct a social world or stigmatise the recipients of poor relief’. Rather, their case shows that accounting can be viewed as ‘contingent’ and reflecting a complex social undertaking. These contrasting findings leave room for further investigations.

Moreover, gaps in the literature on natural disasters and humanitarian relief interventions have been identified (Sargiacomo, 2014). Also, more specifically, according to Västerbro (2018), previous research on natural disasters in Sweden, especially the Swedish Famine, is relatively sparse. In terms of charity organisations, accounting historians have encouraged studies focusing on accounting and accountability (Gomes and Sargiacomo, 2013). Research on Swedish charity has mainly been conducted by political scientists and sociologists (Wijkström and Lundström, 2002). Other research contributions have been made by researchers in jurisprudence (e.g., Hessler, 1952) and in history (e.g., Jansson, 1985). In later years, scholars in the field of business administration have studied the organisation of the third sector (e.g., Ahrne, 1994; Sjöstrand, 1985; 2000). Concerning charity work during the Swedish Famine, valuable insight can be drawn from studies of Häger et al. (1978), Nelson (1988) and Västerbro (2018), but the case has yet to be scrutinised by accounting historians.

This article sheds light on accounts of relief sent to Norrland, the northernmost, largest and least populated part of Sweden, where the crop failures with subsequent hunger, misery and destitution became known as the Great Years of Want (Häger et al., 1978; Nelson, 1988). Thematic analysis was applied in focusing on the accounts of aid from private sources administered through the Stockholms undsättnings-kommitté för Norrland (Stockholm Relief Committee for Norrland), a charity organisation formed solely to collect and distribute aid to Norrland during the Swedish Famine. This article thus seeks to extend concerns beyond the traditional arenas of accounting (see Napier, 2020).

The objective is twofold: First, the article describes instances of charity accounting for a natural disaster in Sweden. Second, it analyses the relation between charity accounting and dimensions of moral conception prevailing in Sweden in the second half of the nineteenth century. In this way, the broader social implications of accounting history are considered (see Gaffikin, 2011).

This study contributes to both historical disaster research and historical charity research by adding an accounting perspective to a country previously overlooked in the international accounting history research on disasters and charity accounting (see Baskerville and Servalli, 2016; Sargiacomo et al., 2021). Also, this article adds to previous research on historical charity accounting (e.g., Funnell, 2001; Manetti et al., 2017) and related research on poor relief (Ó hÓgartaigh et al., 2012; Walker, 2004; 2008) by analysing the effects of nineteenth-century moral assumptions.

The article is structured as follows: The next section provides background information on the Swedish Famine and a theoretical lens for the study. I then describe the data sources and analysis used in this study and, in a subsequent section, the different ways that the Stockholm Relief Committee for Norrland (henceforth: Stockholm Relief Committee) accounted for its charity work. A discussion then centres on how the Committee's accounts relate to the moral notions prevailing at that time. In the last section, I present conclusions, limitations and suggestions for future research.

The Swedish Famine and the moral underpinnings of relief

The Swedish Famine of 1867–1869

The Swedish Famine struck during a period when Sweden was experiencing exceptional economic growth (Schön, 2010). A wave of reforms at both the state and municipal levels had increased the public sector's responsibility for infrastructure growth and enabled institutional change, including a modernised banking system. These components, together with a modernised steel industry, allowed for capital-intensive investments in railway construction, which spurred the demand for Swedish exports. However, a railway line through the northern parts of Sweden was built only after the Swedish Famine in the 1870s. Steam engines were increasingly incorporated into industrial production. This was apparent in the exponential growth of sawmills that started in the mid-1800s, especially in the far-flung and hitherto basically unexploited woodlands of northern Sweden. While exports of Sweden's natural resources, such as iron and wood, rose exponentially, agriculture remained the dominant sector and growth in industrial production was largely limited to rural areas. In the 1850s and 1860s, oats represented the most rapid growth in exports. The growth of industrial towns in Europe, especially in England, required local transport by means of horses that in turn were fed with oats – much of it imported from Sweden (Häger et al., 1978; Västerbro, 2018). Thus, regarding the country as a whole, food was available during the Swedish Famine, but – for various reasons – distribution was uneven.

As Sargiacomo et al. (2021) emphasise, natural disasters are interconnected. Funnell (2001: 204), for instance, notes that ‘[t]he Irish died in large numbers during the potato famine because they did not have the means to acquire legal entitlement to food, not because there was a complete absence of food’. Similarly, in the case of the Swedish Famine, although generally recognised as the triggering factor, not only extreme weather but also acts of men, such as political decisions and moral constraints are pointed out as causes of the crisis (Nelson, 1988; Västerbro, 2018).

The crop failures in Norrland in 1867 were a culmination of a series of bad years that aggravated the impact on people dependent on their harvests (Häger et al., 1978; Nelson, 1988; Västerbro, 2018). In terms of mortality, the Swedish Famine may not be regarded as a disaster or crisis (see Ó Gráda, 2007). But, as Nelson (1988) demonstrates, the effects of harvest failures on an individual level can take forms other than the extreme cases of death due to starvation. In fact, death is only the final stage in a long process of malnutrition and starvation. For instance, individuals may die of a disease, such as nerve fever or hunger fever, they may leave their homes to search for food or to beg, they may move away or emigrate, they may sell or lose their property or they may survive, albeit in miserable poverty. All these instances have been noted during the Great Years of Want. Both Häger et al. (1978) and Västerbro (2018) provide illustrations of desperate individuals. For instance, the secluded family from the Vilhelmina parish (Västerbotten province), who, after days of hunger and inability even to walk, boiled tarred leather shoes in order to extract nourishment. Nelson (1988) argues that in addition to the number of dead, other demographic numerical values, such as declining birth rates and marriage rates, can be taken into consideration as indicators of a crisis in times of hunger and want. Västerbro (2018) also reports on the rates of various crimes including thefts that tripled during the Swedish Famine and murders that doubled. 1 Indeed, there was large-scale suffering due to food scarcity in Sweden in the 1860s, which called for extraordinary and urgent measures.

Poor relief and charity in nineteenth-century Sweden

The organisation of famine work in Sweden in the 1860s was developed as early as in the first half of the nineteenth century and was related to the organisation of poor relief (Nelson, 1988). At this time, charity work was spurred by the growing number of people who neither had their own farmland nor permanent employment, as well as by an increasing crime rate (Qvarsell, 1993). A number of poor relief associations were founded in this ‘era of associations’; these complemented public social activities (Qvarsell, 1993; Wijkström and Lundström, 2002). At this time, the ‘third sector’ was inspired by international charity work, characterised by charity on a non-professional basis, often performed by middle and upper-class women who collaborated with the state and embraced Christian and liberal ideology (Wijkström and Lundström, 2002).

According to several researchers, the reformation that turned Sweden into a Lutheran Protestant state had far-reaching consequences both for the organisation of poor and sick relief and the way in which social responsibilities were politicised (Anderson, 2009; Koefoed, 2017; Wijkström and Lundström, 2002). The Swedish Church Law of 1686 declared that it was a Christian charitable duty to give to the poor. At the same time, the importance of daily work, which was the fulfilment of a holy vocation, and the idea that alms were not a way to reach salvation had a strong influence on Swedish people (Koefoed, 2017). At the beginning of the nineteenth century, this principle was formulated in a more secular way: those who were not themselves dependent on aid were obliged to give to the poor. The Poor Law of 1841 clarified that help was to be financed locally and be provided only to those who were not able to work or lacked other means of making a living (Qvarsell, 1993). Because relief was administrated locally by a committee of the poor, there were apparent differences in the extent of help provided.

The church and the committees of the poor held a rather negative view of the deprived at that time (Anderson, 2009; Koefoed, 2017). Generally, poverty was regarded as self-induced by irresponsibility and laziness. Also, poverty was seen as a will of God – nothing should be done to radically alter this situation. Poor people were divided into deserving and undeserving poor, indicating the justifiable burden that should be put on those who helped (Qvarsell, 1993). Similar ideas prevailed in other European countries. Funnell (2001: 195), for instance, notes that the Irish Poor Law required that ‘[t]he undeserving poor, that is those who were seen by the government to be poor because of their indolence and immorality, were to be identified and excluded from any assistance which did not involve work on their part’. Whereas Christian ideas related to poor relief have been foregrounded in the case of the Swedish Famine (Häger et al., 1978; Nelson, 1988; Västerbro, 2018), similar ideas emanate from economic doctrine (see Funnell, 2001; Ziliak, 1997).

In relation to charity work in Sweden and other Nordic countries during the nineteenth century, Taussi Sjöberg and Vammen (1995) highlight the polarisation of underprivileged people that rendered power and authority structures. While third-sector organisations aimed to circumscribe extreme social and economic differences, radical change in terms of social equality for all citizens was not on the agenda. Charity organisations adopted a mindset implying that help should not be regarded as an attractive alternative to work; the extent of help was thus limited to a minimum.

Distribution of relief during the Swedish Famine

Although the famine aid of concern here was outside the scope of the ordinary poor aid, concepts of the ‘moral man’ – as outlined in the previous section – strongly affected aid distribution (Nelson, 1988). Gifts of food had to be avoided as these were viewed as undermining moral well-being and paving the way for lassitude and depravation; loans, rather than alms were to be given. An emphasis on the importance of daily work led to a conviction that every effort was to be made to distribute aid through work carried out by aid recipients. Such work included building roads, clearing channels and improving harbours and canals. This resonates well with the ‘all should eat, all should work’ justification 2 of help that has been identified as a characteristic of the Lutheranism allegedly advocated in Sweden during the nineteenth century (Anderson, 2009).

Aid during the Swedish Famine came either from the government or from private sources (Nelson, 1988). Aid from the government was channelled to individuals through the provincial governments and/or landsting (county councils) and in turn, kommunalstämmor (local councils). Aid from private sources was mainly administrated through the Stockholm Relief Committee, which sent gifts – in cash and in kind from domestic and foreign sources – to provincial relief committees, which in turn distributed the aid to local relief committees. These local committees administered the distribution to the destitute. The Stockholm Relief Committee was founded by members of the Stockholm Stock Exchange, Frans Schartau, Samuel Godenius, Pehr Wikström and Carl Gustaf Hierzéel, when in September 1867 it became known that a harvest failure had occurred in the northern parts of the country (Schartau et al., 1869). They were wholesalers, local politicians and mill owners; one of them was also the founder of a well-known business school and a Member of Parliament, and another the founder of the Stock Exchange (Hagstedt, 2000–2002; Hildebrand, 1967–1969; Riksarkivet, n.d.). In addition to the Stockholm Relief Committee, some private aid was channelled via churches, groups and individuals.

Government aid included direct relief grants and loans, as well as grants and loans for public work programmes (Nelson, 1988; Västerbro, 2018). As far as possible, recipients of government aid were required to work or render services in exchange. Favoured government aid schemes in Norrland included land drainage, being one of many practical agricultural improvements encouraged to reduce the risk of crop failure and to increase production and employment. In Norrland, the building of roads was encouraged due to a lack of land communication. According to Hoppe (1945), public roads in Sweden's northernmost province nearly doubled in length in the 1860s.

Aid collected by the Stockholm Relief Committee was also linked to the requirements to work (Nelson, 1988; Västerbro, 2018). Nelson (1988) indicates that most of the help sent from Stockholm reached the major towns. However, relief had to pass through the hands of committees responsible for further distribution – the last barrier was not yet overcome. Obstacles included inaccessible roads and travel covering long distances, strict distribution criteria based on moral grounds and, according to newspaper reports, corruption in the distribution chain (Häger et al., 1978; Nelson, 1988; Västerbro, 2018). In the province Norrbotten, for instance, there were clear differences in the local criteria established for aid distribution (Nelson, 1988). In some parishes, the interests of the tax-paying property owners were favoured at the expense of the landless. Also, food was withheld, and flour was secretly mixed with large quantities of bark. Especially in the critical journal Fäderneslandet but also in other fora, complaints were often aired concerning the injustices of distribution (Nelson, 1988; Västerbro, 2018).

Modes of relief accounting in the nineteenth century

Previous accounting history research has highlighted the moral dimensions of accounts kept that related to relief both in pre-famine and famine years during the nineteenth century (e.g., Funnell, 2001; O’Regan, 2010; Walker, 2004; 2008). As noted, a common theme is how accounting served to marginalise the poor. Often, Foucault's studies of disciplinary power in institutional environments such as the asylum and the prison have served as a theoretical frame (Foucault, 1989, 1991). Techniques of hierarchical observation facilitate identifying and examining the exercise of power over individuals and the production of normalised behaviour. O’Regan (2010: 417), for instance, highlights how ‘the decision-making machinery of government came to depend on accounting technologies that made visible various aspects of relief operations at distant locales’ utilising an analysis of idleness, where poverty is made useful by ‘fixing it to the apparatus of production, at worst to lighten as much as possible the burden it imposes on the rest of society’ (Foucault, 1980: 167).

Of particular interest for the case presented in this article is ‘accounting publicity’ as addressed by Walker (2004), who relates accounting publicity to the surveillance of the poor. In conjunction with rapid population growth during the early nineteenth century in the case of England and Wales, physical identification in the form of badging was replaced by accounting publicity (Walker, 2004: 114): Rendering the pauper visible via inscription and the public disclosure of claimants’ identities through the medium of accounts was a component of the increasingly bureaucratised management of poverty. Surveillance thus shifted from symbolic labelling of the poor through dress (badging) on the corporeal subject to more calculable techniques.

He notes how alphabetical lists of paupers and amounts paid to them were displayed in public places such as the church vestry, the churchyard and local inns or printed in the local newspapers. Publicity was intended for both the giver and the receiver as a means of social control of the deserving poor, a confirmation of dependence and – as a basis for stigmatisation – an instrument of social discipline. Accounting publicity is thus described as ‘a symbol of the power of the parochial elite over the dependent local poor, a confirmation of social placement and difference’ (Walker, 2004: 124).

While most research on relief focuses on state accounts and the accounts of state-related organisations, Ó hÓgartaigh et al. (2012) reviewed the minute books of a union, the Castlebar Union, during the period prior to the Irish Potato Famine. Their conclusions deviate from previous research findings as the accounting apparatus surrounding the Irish Poor Law Act of 1837 is described as contingent, playing a different role in different contexts. In their case, accounting cannot be seen as a device to assist the preservation of the dominant interest, the propertied.

Charity accounting at the time of the Swedish Famine was a voluntary activity. Neither the state nor private organisations prescribed how charities should keep their accounts. Nevertheless, accountability was regarded as important during the Swedish Famine (Nelson, 1988). Concerning the possible relation between moral conceptions and charity accounting, the literature on poor relief and charity in Sweden during the nineteenth century stresses that Christian ideas prevailed (e.g., Nelson, 1988; Taussi Sjöberg and Vammen, 1995). As outlined above, those who were not themselves dependent on help were obliged to give to the poor. The poor were defined as those who were not able to work. During the Swedish Famine, this meant that a great proportion of the aid distributed to otherwise non-poor in Norrland was linked to requirements of work in public work schemes. Given these circumstances, it seems reasonable to assume that the moral conceptions of the time affected charity accounting during the Swedish Famine. Relevant questions are thus: Are moral conceptions concerning emergency relief manifest in the accounts of the Stockholm Relief Committee? If so, is the focus on the donors or the people in need?

Data sources and analysis

In order to pursue the research objective of this study, I analysed the accounts of the Stockholm Relief Committee, the most important administrator of aid from private sources during the Swedish Famine (Nelson, 1988). These accounts appeared as numerous announcements in different newspapers and as a printed final report. While the newspapers could be accessed digitally via the National Library of Sweden, the final report was studied at Stockholms stadsarkiv, the archive of the city of Stockholm, where the only copy is preserved. 3 To contextualise the accounts of the Stockholm Relief Committee, a thematic analysis was conducted taking into consideration how accounting practices made visible various aspects of the moral conceptions prevailing in Sweden and elsewhere.

The process of familiarisation, data coding, theme development and revision generated decisive patterns in the accounts provided by the Stockholm Relief Committee. During this process, the focus was directed towards ‘hierarchical observation’ (see Foucault, 1991) considering both donors (the propertied class) and people in need (underprivileged individuals). The thematic analysis enabled the identification and examination of the exercise of power over individuals within the various areas of the data sources, such as conditions for distributions, donations made and help distributed to the northern parts of Sweden.

The study also draws on data from reports of two of the provincial relief committees, the Norrbotten and the Westerbotten Relief Committees, in order to further contextualise the final report of the Stockholm Relief Committee. Further documents used were official statistical reports from the provinces Norrbotten, Västerbotten, Jämtland and Västernorrland. All data sources and their use in this study are shown in Table 1.

Data sources and their main content used for this study.

Empirical findings

This section describes the different ways in which the Stockholm Relief Committee accounted for its activities during the Swedish Famine. First, the accounts presented in newspapers are discussed, followed by a review of the Committee's final report.

Accounts of the Stockholm Relief Committee in newspapers

The Stockholm Relief Committee reached out to potential donors for emergency relief intended for the suffering inhabitants of Norrland through a number of announcements in different newspapers. 4 In this way, the Committee gave brief background information about the situation in the northernmost parts of Sweden, clarified conditions for the distribution of help and accounted for the help that had reached the Committee. In early announcements, it was assured that such accounts would be provided in due course.

Information about the situation in Norrland was limited to references to the harvest failures due to extreme weather conditions, which allegedly caused or might cause a famine. Concerning the distribution of help, a recurring message was that the railroad transport for aid in kind from donors in the whole country to the Committee in Stockholm was free and that sacks were promptly returned to the donors. Other recurring information was which steamboats were used to ship commodities to Norrland. The Committee also informed about government assistance.

The Committee's conditions for the distribution of help were clarified as follows. The distribution of aid had to balance two situations: creating conditions for the distressed to independently stave off hunger in the future, on the one hand, and protecting the victims of the hard years from the ‘pernicious influence of almsgiving’, 5 on the other hand. The solution was to require the provincial relief committees to distribute help among those in need not only in a fair way but also in return for work. Such work included the digging of drainage ditches, the construction of roads and the production of handicrafts. Only old, infirm or sick people and minors were exempted from the work requirement. In addition, the Stockholm Relief Committee required the provincial relief committees to account for the aid received by the Committee separately from aid received by other organisations or individuals. According to the Stockholm Relief Committee, these requirements corresponded both to the wishes of the Committee itself and to prompts made by numerous donors; it also corresponded to enlightened public opinion.

In some announcements, the Committee reported only the total of aid in cash or in kind that had been donated since the prior announcements in newspapers. In other announcements, the donors’ names and specified amounts were provided. Often the names of prominent individuals were emphasised; for instance, aid provided by consuls, barons and bank directors from foreign countries. A name that was repeated several times was that of Captain John Ericsson, a Swede living in New York who donated a considerable sum. 6

Also, charitable efforts in Sweden as well as in foreign countries were reported. For instance, the Uppsala choir and the orchestra of the Prussian music director visiting Hamburg gave benefit concerts. Also, book auctions were organised. Carl von Linné's personal notes were, for example, offered to charity. In terms of transport, many people volunteered, such as coachmen who made their horses and carriages available.

A kind of interim report was published as an appendix (two full pages) to the newspaper Aftonbladet in December 1867. The report provided an overview of aid in kind that was shipped to the provinces of Norrbotten, Westerbotten, Westernorrland, Jemtland and Dalarne. Also, an overview of aid in cash from Sweden and other countries, amounting to a total of 478,051.62 Rmt Rdr, 7 was provided. The Committee announced that a final report would be printed at a later date. Until then, foreign donations would receive extra attention and were reported in more detail. Thus, the aid, given in cash, of foreign individuals and organisations was listed country by country. In this report, the Committee also clarified the above-mentioned conditions for the distribution of help. The members of the Committee thanked all donors and assured them that their own work was conducted with zeal and care. After the publication of this report, announcements were basically limited to reports on additional aid sent to the Committee.

The final report of the Stockholm Relief Committee

The final report of the Stockholm Relief Committee (henceforth: final report) comprised 76 pages divided into an introduction, body and an appendix. However, double-entry bookkeeping was not utilised (Schartau et al., 1869), instead, the accounts are presented in a ‘cash-and-kind-flow’ style.

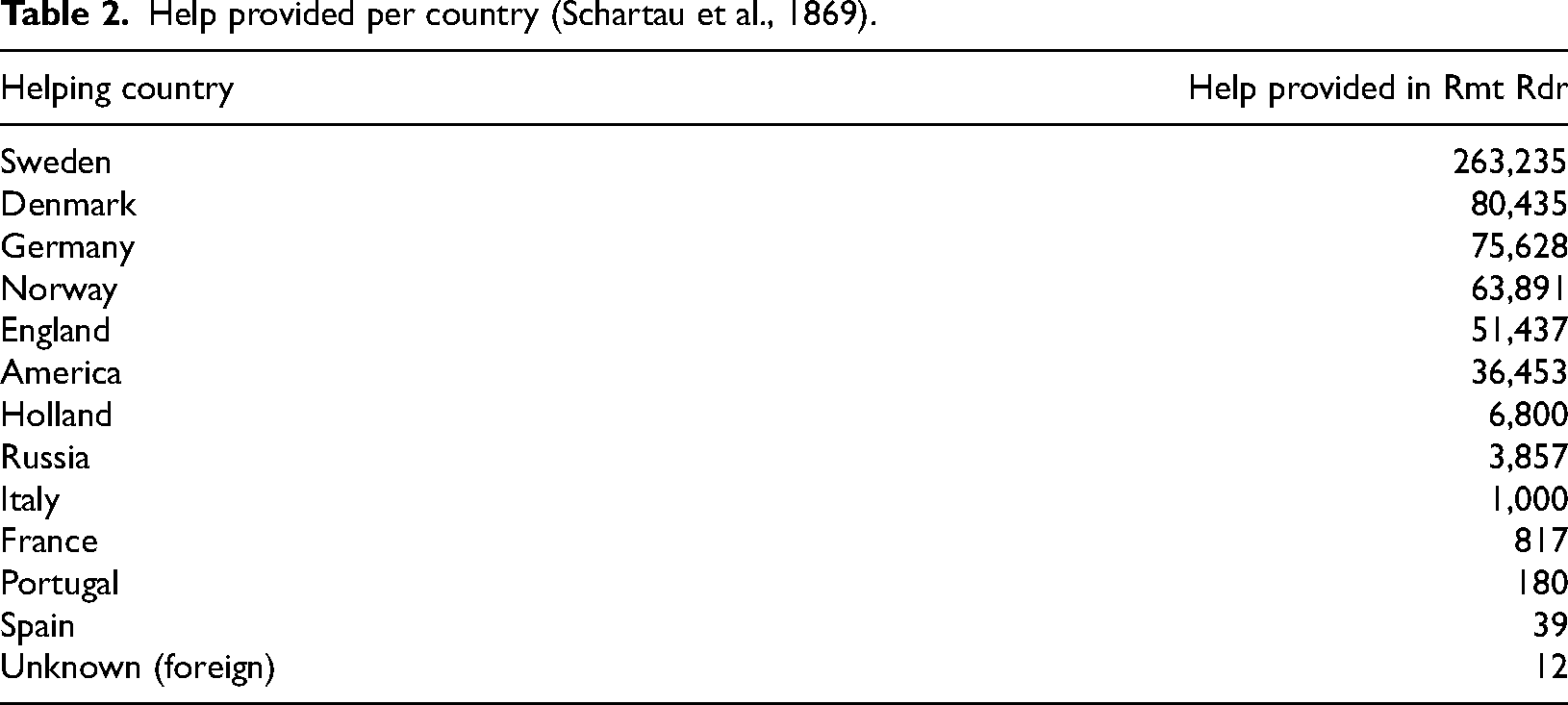

The report introduction not only gives background information as to when and why the Committee was formed but also reports that donors were reached via announcements in newspapers and that the accounts presented in the final report were kept by the chief accountant, Herman Osbeck on an honorary basis. Further, the introduction provides an overview of the income from the twelve aid-giving countries. Table 2 gives an overview of these countries and their aid provided in Rmt Rdr 8 (here in descending order).

Help provided per country (Schartau et al., 1869).

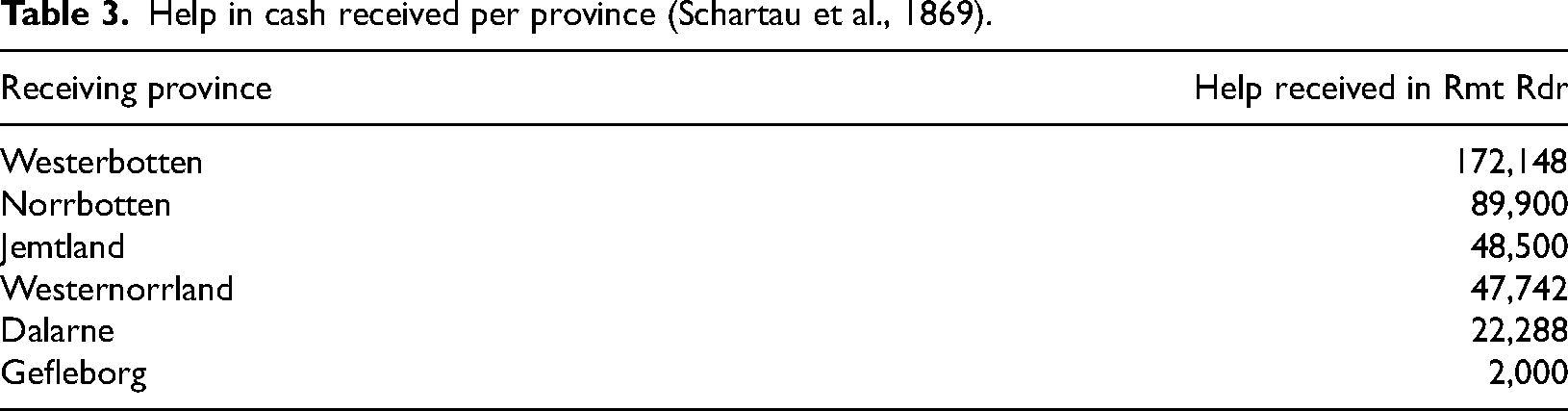

In total, the income from the various countries amounted to 583,789.15 Rmt Rdr, of which more than 50 per cent came from foreign countries. Also, an overview of the distribution of aid in cash and kind channelled to the provinces is given. Table 3 shows the aid provided in cash (here in descending order).

Help in cash received per province (Schartau et al., 1869).

In addition, a deposition in Sweden's national bank, Riksbanken (14,000 Rdr) and the cash balance (1838 Rdr), is shown. Before the names of the members of the Committee are listed, the report's introduction (page 5) concludes with the following words of gratitude: The Committee is fruitlessly and in vain searching for expressive words to interpret the deep gratitude of a population rescued from hunger and torment.

The main report section is divided into (1) the specified amounts of aid in cash that the Committee received from organisations and individuals in the different countries (pages 5–31), (2) the specified amounts of aid in cash that the Committee distributed to the provinces and compensations for goods and services that the Committee purchased from organisations and individuals (pages 31–35) and (3) the specified amounts of aid in kind that the Committee received from individuals and organisations (pages 36–75).

Part 1 opens with accounts of the aid provided by organisations and individuals from Sweden (pages 5–26). In alphabetical order, aid generated from different towns (pages 5–16) is first listed and then aid from different provinces (pages 17–26). For each town and province, the entries end with the total amount of all donations. Often, collections were organised by named individuals. Collections were also organised by organisations and church congregations. Individual donors are also named. In contrast to the few lines covering donations from other Swedish towns, the accounts for aid provided by organisations and individuals from Stockholm comprise approximately five pages. Aid from the Royals is presented first and separated from other Stockholm donors. Next in line are the members of the Committee, who each contributed 500 Rdr.

Part 1 continues with the specified aid provided by organisations and individuals from foreign countries (pages 26–31). Amounts and totals are given country by country. In addition, interest rates for the cash deposited in different banks are shown.

Part 2 first presents the specified amounts of aid in cash that the Committee distributed to the provinces of Norrbotten, Jemtland, Westernorrland, Westerbotten, Dalarne and Gefleborg (pages 31–33). For each province, the amounts received by diverse recipients – mainly not only the provincial relief committees but also individuals such as provincial governors – are shown together with the dates of distribution and the total for each province. Then follows a list of entries concerning payments for diverse goods and services including dates and specific amounts (pages 33–35). Goods included barley, flour, peas, hemp and rice, but not all entries show the type or amount of goods bought. Among services, the Committee accounted for shipping, storage and insurance costs. The various steamboats, such as Thor, Volontaire and Chapman, used for shipping to Norrland are also listed here.

The information concerning the specified amounts of aid in kind that the Committee received from individuals and organisations in part 3 of the final report is presented in a table (pages 36–75). Information includes dates for received goods, names of individuals and organisations, sometimes their local affiliation, the types and amounts of aid counted in sacks, barrels and mattor, 9 and sums. Barley was apparently the most important grain, followed by mixed grain and oats as well as rye.

There is no indication that an audit of the Committee's accounts and management was conducted. However, the following information is provided on the last page of the report (p. 76): The receipts of the individuals sending money and goods are available at the Committee's office to anyone who wishes to have insight into these receipts.

The final report also includes an appendix with a table showing aid in kind provided by donors and purchased by the Committee. The entries are ordered province by province and include dates, names of the boats used for shipping, destination, type and amount of aid in different units and totals.

Discussion

The above presentation of the different ways in which the Stockholm Relief Committee accounted for its charity activities during the Swedish Famine affords the opportunity to expand the discussion about the role of accounting in society during the nineteenth century, specifically with regard to accounting for natural disasters (see Sargiacomo, 2014; Sargiacomo et al., 2021). At first glance, the reports in the newspapers and the final report seem comprehensive. Both aid in cash and kind provided by individuals and organisations are recorded and aid sent to the different provinces is detailed. However, in order to understand the potential implications of moral conceptions of charity accounting, an analysis of what is not reported is also needed.

The announcements in the newspapers included direct prompts to provide help to those who suffered from crop failures in the northern parts of Sweden. The Stockholm Relief Committee focused on accounts of donors and donations. It is reasonable to assume that the prevailing convictions based on the Christian doctrine of giving at that time (see Koefoed, 2017; Qvarsell, 1993; Wijkström and Lundström, 2002) influenced decisions on what to report and thus, what to make public. The detailed presentations of donations were probably perceived as natural, given the notion that those who were not themselves dependent on aid were obliged to give to the poor. The publication of the names of generous people might also have been an indirect injunction, an allusion evoking moral duties. As Maltby and Rutterford (2016: 264), who studied charity investment during the nineteenth century, argue: ‘[…] public, charitable action was required in order to portray oneself as a concerned, morally aware individual’, or as Baskerville and Servalli (2016: 142) put it: ‘Benevolence is linked to reputation, social status and social mobility; so it may not only be altruism, but a move along the trajectory away from stigma and disgrace’. The fact that John Ericsson and other prominent individuals received considerable attention in the announcements also indicates that power and authority structures were exploited as well as maintained in charity work (see Taussi Sjöberg and Vammen, 1995). Thus, the Stockholm Relief Committee's accounting through announcements in newspapers represents a manifestation of social distancing or, as Walker (2004: 124) puts it, ‘a confirmation of social placement and difference’ – even though publicity was focused on donors rather than on those in need. The power of the ‘elite’ over the ‘dependent local poor’ was not obvious. Rather, from a Foucauldian perspective, the publication of donors and related donations can be seen as forms of surveillance in which moralisation and social control constitute means to exercise power over propertied interests.

Also in the final report, the focus is on the donors and donations rather than on those suffering from the crop failures. While 65 pages of the report are devoted to accounts of help given by individuals and organisations, only two pages present information on help received by the provinces in northern Sweden. Information is only given on output, that is, the products or services resulting from the Committee's activities. Outcome and impact, that is, to what extent the intended positive change was achieved and to what extent it was a result of the Committee's efforts, are not reported. For instance, the final report does not show how many people were saved from death due to starvation, or from death due to disease caused by malnutrition and starvation. It does not show how many people were saved from leaving their homes to search for food or to beg, from moving or emigrating or from selling their properties. It does not show how the help affected birth and marriage rates, and crimes, or how many people escaped from living in miserable poverty due to the help provided. Historical investigations, such as those conducted by Nelson (1988), prove that information was available to account for – if not for all, at least for some of – these matters. For instance, official statistical reports from the provinces inform about population, change of property ownership and poor relief (Almquist et al., 1871; Asplund et al., 1871; Bergman et al., 1871; Weidenhielm et al., 1871). In addition, reports from provincial doctors and the Sundhets-Collegii, responsible for state supervision of Swedish health care at that time, provide valuable information (see Nelson, 1988). Although attribution for the impact of charity on health status is always an issue, charity has the potential to counteract malnutrition and starvation.

Comparisons of the two types of reporting show that not all information provided in the newspapers is included in the final report. Most notably, the conditions for the distribution of aid outlined in the interim report are not reiterated in the final report. Furthermore, there is no information either in the newspapers or in the final report about what working in exchange for food actually accomplished among those who received help. Given that the interim report states that some donors requested that the afflicted should work in exchange for food and the prevailing moral ideas concerning relief at that time, it is surprising that neither the conditions for the distribution of aid nor the work accomplished in relation to the help was reported – not even in an aggregated manner.

As previous research has shown, ‘thousands and thousands of work receipts bear witness to the hard work in the winter cold’ (Västerbro, 2018: 137). Also, a review of the reports of the Norrbotten and the Westerbotten Relief Committees shows that such information – although in varying detail – is provided in these reports (Almquist et al., 1868; Bergman et al., 1869). According to instructions, the amount of monetary aid was not to exceed 10 per cent of the total private aid distributed in each district. Nelson (1988), who compiled the numbers regarding the forms of distributing work aid funds from voluntary contributions in Norrbotten, shows that the aid for ditch digging, roadbuilding and crafts amounted to between 12 per cent and 66.4 per cent in total. The distribution of monetary aid varied in the different parishes between 0.3 per cent and 32.5 per cent. In the final report of the Stockholm Relief Committee, there are no references to any of the reports from the provincial relief committees.

The concepts of the ‘moral man’ strongly affected the formulation of aid distribution regulations and the proposals for suitable schemes as evidenced in the interim report of the Stockholm Relief Committee and (to a varying degree) in the distribution of aid. Nevertheless, the final report of the temporary charity organisation excluded any such conceptions and related information. Whether this was a conscious choice is not apparent from the archival material. Perhaps the Stockholm Relief Committee wanted to highlight its charitable achievements as a private organisation disconnected from any forms of control and power exercised over those in need by the state (through provincial and local relief committees). Also, the communication from the provincial relief committees back to the Stockholm Relief Committee may have been deficient.

Whatever the reasons, despite the interconnection between the Stockholm Relief Committee and the provincial relief committees in the distribution chain of cash and kind, an accounting architecture for control was not established between the private charity organisation in Stockholm and the state-administrated provincial (and local) relief committees.

The announcements in the newspapers seem to have been intended – directly or indirectly – to encourage people to provide help, thereby enhancing the morality of the propertied class. The final report, on the other hand, seems to include information that was easy to access, but it was not necessarily crucial information for the donors. Thus, the report illustrates what Young (2006: 581) describes as ‘accounting is what accountants do’, rather than a means to exercise power over underprivileged people.

Conclusion

The objective of this article is to describe instances of charity accounting relating to a natural disaster in Sweden and to analyse the relation between charity accounting and dimensions of moral conception prevailing in Sweden in the second half of the nineteenth century. In pursuing this research objective, I reviewed the accounts of the Stockholm Relief Committee for Norrland, a temporary charity organisation and the most important administrator of aid from private sources during the Swedish Famine.

The study shows that charity accounting is not a neutral activity; it is informed by prevailing conceptions and can serve many functions. The accounts of the Stockholm Relief Committee seem to, directly and indirectly, have been used to sustain moral precepts concerning both those providing and receiving help. The accounts provide detailed information on the help given by individuals as well as organisations, supporting the prevailing idea that those who were not themselves dependent on aid were obliged to give to the poor. The accounts also clarify how the help was to be distributed to those in need. The conditions for distribution were in accordance with the conviction that aid should only be given in exchange for work. However, the reports do not specify the results of the help and how it was actually distributed. The accounts of the charity organisation thus do not reflect research findings from other contexts that suggest accounting publicity was related to the surveillance and social disciplining of the poor (e.g., Walker, 2004; 2008). Rather, in this case, there are indications that morality was enhanced by accounting publicity related to the donors, the propertied interest.

The analysis of the Stockholm Relief Committee's accounting shows that, even though an ‘accounting apparatus’ was enforced by the state-administrated provincial and local committees (Häger et al., 1978; Nelson, 1988; Västerbro, 2018), the accounting architecture for control over those in need was not extended to include the private charity organisation in Stockholm. Thus, the study adds to the accounting history literature about the role of accounting by ‘challenging recent conceptions of accounting as a technology that served propertied interests by primarily (if not exclusively) stigmatizing the poor’ (Ó hÓgartaigh et al., 2012: 244). A widespread use of measurement, classification and description for purposes of disciplining the unprivileged individual, as observed by Foucault (1991), is not evident in the accounts of the Stockholm Relief Committee.

Although this study on charity accounting during the Swedish Famine is a study of a particular context at a particular time, which largely rules out generalisations beyond these specifics, it provides valuable insights and prompts further research into the role of charity accounting in history, particularly during natural disasters.

Footnotes

Acknowledgements

The author would like to thank PhD Peter Olausson, Karlstad University, the three anonymous reviewers, and the guest editor for their insightful comments.

Declaration of conflicting interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.