Abstract

Although widely acknowledged as a foremost event of the Victorian age, accounting aspects of the Great Exhibition of 1851 have received limited attention. This article analyses accounting, control and audit at what was the first ‘universal’ Exhibition. Specific foci include the adoption of a cash-based accounting and financial reporting regimen, systems for protecting substantial volumes of cash and the nature of external and internal auditing. Insights are provided into the contemporary operation of these practices in a substantially unexplored setting. Visibility is also given to the role of the backstage personnel in the accounting and finance function, particularly the Financial Officer, who applied knowledge and skills drawn from the Commissariat Service. The latter analysis augments our understanding of the significance of the military in the development of accounting in nineteenth-century Britain. The study reflects on the research potential of exhibitions as a site for exploring diverse themes in accounting history.

Keywords

Introduction

Major international exhibitions are potentially significant sites for accounting history research. They constitute large-scale events, limited in time and space that give rise to distinctive accounting challenges and pose unique governance issues. As recognised by accounting researchers in modern-day contexts, exhibitions represent arenas in which diverse calculative practices may be operationalised and rendered visible (Ferry and Slack, 2022). Exhibitions also offer considerable scope for extending our knowledge of the role of accounting and accountants in the fields of culture and entertainment (Jeacle, 2012, 2021).

Despite their potential as research sites, exhibitions have received very limited attention in the accounting history literature. A rare exception is Fabre and Michaïlesco's (2010) investigation of the roles of accounting in the series of Universal Expositions convened in Paris from 1855 to 1900. The authors demonstrated how these exhibitions were a location for the application and adaptation of public accounting regimens; posed challenges in relation to financial planning, budgeting and the mobilisation of accounting expertise; and provided insights into the interface between accounting and the state in shifting political contexts. Fabre and Michaïlesco (2010: 88) also observed that the Paris expositions ‘generated a great deal of financial reports and numerous statistics, the nature of which changed over time’.

The focus of this article is on an event that predated the universal expositions in Paris studied by Fabre and Michaïlesco (2010). Here, we examine accounting, control and auditing at The Great Exhibition of the Works of Industry of All Nations, 1851. This was the first ‘universal’ exhibition. Several of its features were emulated at a host of subsequent cultural ‘mega events’ comprising international exhibitions, expositions universelles and world's fairs (Auerbach, 1999; Edwards, 2008; Findling and Kimberly, 1990; Gardner, 2018; Greenhalgh, 1988; Roche, 2000; Rydell, 1984). The Great Exhibition took place in Hyde Park, London. It was housed in the ‘Crystal Palace’, an iconic building measuring 563 metres long and 138 metres wide, hailed as a ‘milestone in modern construction’ (Shand, 1937: 66). Over 6 million people attended the event. There they saw 100,000 objects placed on display by 13,500 exhibitors. The Exhibition was considered a great undertaking, a symbol of British industrial progress and social inclusion. For contemporaries, this was a salient event of the Victorian age (Illustrated London News, 10.5.1851), one that heralded a new era of peace through international cooperation built on free trade.

Given its significance, the Great Exhibition has attracted the attention of generations of historians. Indeed, interest in this ‘monumental and monolithic event’ continues unabated (Auerbach, 1999: 1). Modern revisionist scholarship tends to depart from the self-congratulatory narratives produced immediately after 1851 and the superficial and triumphalist tone of histories published thereafter. Recognising that diverse aspects of the Great Exhibition are subject to multiple interpretations, more critical and penetrating analyses have been advocated in recent decades (Auerbach, 2008; Buzard, Childers and Gillooly, 2007; Cantor, 2013, Vol. 1: xv; Davis, 1999: ix-xi; Hoffenberg, 2001: xiii-xxiii; Purbrick, 2001; Shears, 2017: 1–11; Young, 2009: 6–15).

Scholars now recognise the Great Exhibition as ‘a protean event with numerous possible meanings’ (Auerbach, 1999: 2). It is understood as ‘a projection screen’ on which diverse aspects of the history of Victorian Britain are conveyed (Auerbach, 2008: ix). Such multiple agendas permit the inclusion of analyses beyond the heroic interventions of royalty and other luminaries, the magnificence of the building, the wonder of the exhibits and the institutional and cultural legacy of the event. To date accounting and those who practised it have not featured among these new agendas. In this article, an attempt is made to address this lacuna. In particular, our focus on accounting, control and auditing connects us to the activities of the Finance and Admissions Department of the Great Exhibition. This department, which was headed by a Financial Officer and overseen by a Finance Committee, has received limited attention in extant histories. There is thus an opportunity for the export of accounting history knowledge to inform and augment mainstream histories (Walker, 2005).

The article is structured as follows. In the next section, the sources and temporal scope of the study are explained. The establishment and personnel of the accounting and finance function at the Great Exhibition are then related. This is followed by an analysis of the management of expenditure and funds over the phases of the venture. Subsequent sections examine accounting and financial reporting, the nature of internal controls over cash disbursements and receipts, and auditing practices. The post-Exhibition history of the Finance and Admissions Department is thereafter briefly related. The concluding discussion summarises the findings, and the contributions of the study suggest further themes for investigation by accounting historians.

Sources and temporal scope

The study is based on a number of primary sources. Foremost among these were documents contained in the archives of the Royal Commission for the Exhibition of 1851 at Imperial College, London. The printed minutes of the meetings of the Commissioners (hereafter referred to as ‘Minutes’), which contained reports from the Finance Committee, were especially important. As well as providing insights into the work of the finance function they also disclosed monthly details of receipts, expenditure and cash balances. The archive also contains incoming correspondence to the President of the Royal Commission, Prince Albert. These documents, as well as the correspondence of Edgar A Bowring, Secretary to the Royal Commission, have recently been digitised as part of the Prince Albert Digitisation Project. 1 These collections were searched for material relating to accounting, auditing and internal control.

The 8-volume ‘Collection of Printed Documents and Forms used in Carrying on the Business of the Exhibition of 1851’ (hereafter Collection of Printed Documents) in the National Art Library, London, is a key source for analysing operational aspects of the Great Exhibition. It offers especially rich insights into administrative arrangements and control procedures. Henry Cole was a leading figure in the genesis and organisation of the Great Exhibition and was a key member of its Executive Committee. Cole's diaries were consulted in the same repository. They provided candid insights into discussions relating to financial statement disclosures and auditing issues. Parliamentary papers contained detailed descriptions of the Great Exhibition itself, especially the First Report of the Commissioners for the Exhibition of 1851 (hereafter First Report) as well as financial statements and a wealth of statistical tables relating to the event. Parliamentary papers were also useful for comprehending the strong connection between leading accounting functionaries at the Exhibition and the Commissary Department of the Treasury. The Report of the Committee Appointed to Inquire into the Existing Organization of the Commissariat Department (1858) (hereafter Report (1858)) was especially helpful in this regard.

Newspapers also offered voluminous commentaries on the Great Exhibition including, on occasion, its financial aspects. Digitised collections such as the British Newspaper Archive and The Times Digital Archive were searched for content on the specific subjects of the study. The closely defined temporal range of the focal event was conducive to the search for relevant material amidst the mass of reportage on the Great Exhibition in contemporary periodicals. Dilke's (1855) exhaustive printed Catalogue of a Collection of Works on The Exhibition of 1851 proved useful in identifying other potentially relevant material. The Great Exhibition has, of course, been the subject of substantial secondary literature, though, as stated above, accounting and those who performed it are seldom given sufficient attention.

Before proceeding to our analysis, a word about the temporal scope of the study. The Great Exhibition of 1851 represented the culmination of attempts by the Society for the Encouragement of Arts, Manufactures and Commerce (subsequently, the Royal Society of Arts) from the mid-1840s to establish periodic exhibitions of manufactures. The Society's early efforts met with mixed responses but from 1847 its annual exhibitions proved more successful, and planning began for a national exhibition in 1851. Following the involvement of Prince Albert, who was President of the Royal Society of Arts, a large-scale, more international exhibition was contemplated. It was decided to establish a Royal Commission for the purpose, chaired by the prince. The Royal Society of Arts was given responsibility for raising the estimated £75,000 needed to fund the event and in November 1849 a contract was signed with Messrs James and George Munday, builders. Messrs Munday would erect the exhibition building, assume the financial risks of the project, and in return receive a proportion of the profits of the venture. However, the public reaction to the notion of a private speculator earning substantial profits from a national project was unfavourable.

Consequently, when the Royal Commission for the Exhibition first convened in January 1850 it decided to terminate the contract with Messrs Munday and fund the event from voluntary subscriptions. The Great Exhibition was also to become a public event rather than the project of the Royal Society of Arts (Auerbach, 1999: 9–37; First Report, 1852: xv-xviii; Hobhouse, 2002: 1–17; Shears, 2017: 13–14). In the current study, attention is not devoted to this pre-history of the Exhibition. Rather, our investigation commences with the establishment of the Royal Commission on 3 January 1850 (Cantor, 2013, Vol. 1: 61–70; Shears, 2017: 24–31). It ends on 29 February 1852, the reporting date of the financial statements that were produced for the First Report to Parliament by the Royal Commissioners for the Great Exhibition. Shortly after this date, the Financial Officer also resigned and resumed his previous vocation.

Organisation of the accounting and finance function

The Royal Commissioners for the Great Exhibition gave early attention to accounting and financial arrangements. At their second meeting, a special committee was appointed to report on the steps necessary to control expenditure (Minutes, 18 January 1850). The latter issue was significant given that the Exhibition was to be a national venture funded by voluntary contributions. It was essential that potential subscribers could be confident that costs were properly managed and the accounts scrutinised (First Report, 1852: xvii). On receiving the report of the special committee, the Commissioners resolved to assume absolute control over expenditure, and to appoint Treasurers to receive subscriptions and donations and deposit them in an account at the Bank of England (Hobhouse, 2002: 15–16; Minutes, 24 January 1850). 2 A ‘Committee of Finance’ was also established. This would receive regular reports on expenditure. The Finance Committee was chaired by Lord Granville, Vice President of the Board of Trade and Paymaster General and deputy to Prince Albert.

In order to control expenditure, the special committee recommended the appointment of a Financial Officer on a fixed salary. This individual would prepare regular estimates of expenditure for authorisation by the Commissioners and sign all cheques. As to who might occupy this position the special committee suggested that an appropriate ‘person might be found among those employed by Government in the Commissary Department’ (Minutes, 24 January 1850), the branch of the army responsible for procurement and supply, then administered by the Treasury. A letter was accordingly sent to the Lords of the Treasury ‘requesting that the services of a Commissariat Officer on half-pay may be placed at the disposal of the Commission’. The Treasury recommended the appointment of Assistant-Commissary-General Frederick Stanley Carpenter (1817–1890), who was summoned to London by Sir Charles E. Trevelyan, Assistant Secretary to the Treasury and superintendent of the Commissariat Department (Minutes, 31 January 1850; First Report, 1852: xix; British Army Despatch, 22 February 1850; see Funnell, 2004). Carpenter took up his post in February 1850 (Minutes, 14 February 1850).

Carpenter receives practically no attention in histories of the Great Exhibition despite his undoubted contribution to its success. He was the only son of Digby T. Carpenter, a Captain in the 10th Regiment of Foot. In 1834, Carpenter was placed in the counting-house of the prominent Liverpool merchant and shipowner, Duncan Gibb. He entered the Commissariat service as a clerk in 1839 and was initially posted to Corfu (Bedfordshire Mercury, 21.6.1890; Report, 1858: 53). Following promotion to Deputy Assistant Commissary-General in 1842 (London Evening Standard, 8.1.1842), he was despatched to Hong Kong where he acted as a sub-accountant until the end of 1849 (British Army Despatch, 11.1.1850, 8.2.1850; Reports of the Committee appointed to inquire into Naval, Ordnance, and Commissariat Establishments and Expenditure in the Colonies, 1852: 40). On returning to the UK, Carpenter was placed on half pay and promoted to Assistant Commissary-General (London Evening Standard, 2.2.1850).

At the time of his appointment as Financial Officer to the Great Exhibition, Carpenter was by far the youngest of the officers in the Commissariat Service on half-pay (Report from the Select Committee on Army and Ordnance Expenditure, 1850: 1108). In giving evidence to the Select Committee on Army and Ordnance Expenditure in 1850, Sir Charles E. Trevelyan explained that while commissariat officers on half pay tended to be men of long service or impaired health, on occasion a small number were remitted to other ‘important situations in the public service’ beyond the department (Report from the Select Committee on Army and Ordnance Expenditure, 1850: 502). Indeed, ‘lately we lent a young officer to serve as financial officer under the Commission for the Exhibition of the Industry of all Nations’ (Report from the Select Committee on Army and Ordnance Expenditure, 1850: 502).

Why was a Commissariat Officer, and Carpenter in particular, appointed as Financial Officer to the Great Exhibition? According to Trevelyan, officers in the Commissariat ‘have to keep accounts and transact business of all kinds’ (Report, 1858: 4). They were experienced in dealing with contracts and supply and were aware of the importance of internal controls (Report, 1858: 129). Carpenter was undoubtedly experienced in accounting for procurement and processing the high volumes of cash likely to be received from attendees at the Great Exhibition. While in Hong Kong, he had been ‘in charge of the commissariat chest and cash accounts, with all the detail payments to army, navy, ordnance and advances for colonial services, together with the voluminous transactions arising therefrom; the annual expenditure being £157,305 6s. 3d.’ (Reports of the Committee appointed to inquire into Naval, Ordnance, and Commissariat Establishments and Expenditure in the Colonies, 1852: 40). Carpenter was thus a competent, recently promoted officer on half-pay with an appropriate skillset. At a time when respectability and patronage were also important to recruitment and careers in the Treasury and Commissariat Service (Report, 1858: 20–24, 55; Edwards, 2011), we might also note that Carpenter was a nephew of John Thomas Stanley, 1st Baron Stanley of Alderley, a Fellow of the Royal Society, and whose son, Lord Eddisbury, was Under-Secretary of State for Foreign Affairs.

As the opening of the Great Exhibition on 1 May 1851 approached, the responsibilities of the Financial Officer and his staff increased. In September 1850, it was proposed to establish functional sections (with relevant subdivisions), each headed by ‘men of ability and zeal’ (Reid to Phipps, 8 September 1850, RC/H/1/4/121). A new section for ‘Receipts of Money’ was proposed with Carpenter in charge. The complement of accounting and finance staff at the ‘arranging’ stage of the Exhibition consisted of the Financial Officer assisted by three clerks (First Report, 1852: 43). During the Exhibition, the Finance and Admissions Department was expanded and comprised the Financial Officer, a superintendent of money takers, three assistant superintendents of money takers, six clerks, two private doorkeepers, four collectors, 18 money takers, between five and 11 season ticket takers, 10 receivers of umbrellas and six porters and messengers (First Report, 1852: 46, 155). By 29 February 1852, remuneration of £3,528.9.10 had been paid to 58 persons in Carpenter's department (Minutes, 1 March 1852).

Managing expenditure and funds

At the end of February 1850, the Commissioners agreed on the responsibilities of the Finance Officer. He would provide monthly estimates of expenditure for the consideration and agreement of the Finance Committee. Once estimates were approved necessary amounts would be transferred from General Funds at the Bank of England to the ‘Special Account for Executive Services’. Carpenter would also prepare monthly accounts of actual expenditure and funds at the Bank for the Finance Committee. Further, he would ensure that spending was authorised and ‘exercise a vigilant control over the expenditure, in order that due economy may be observed in every item, and to suggest any arrangements for resorting to competition and contracting for services, if considered desirable’ (Minutes, 21 February 1850).

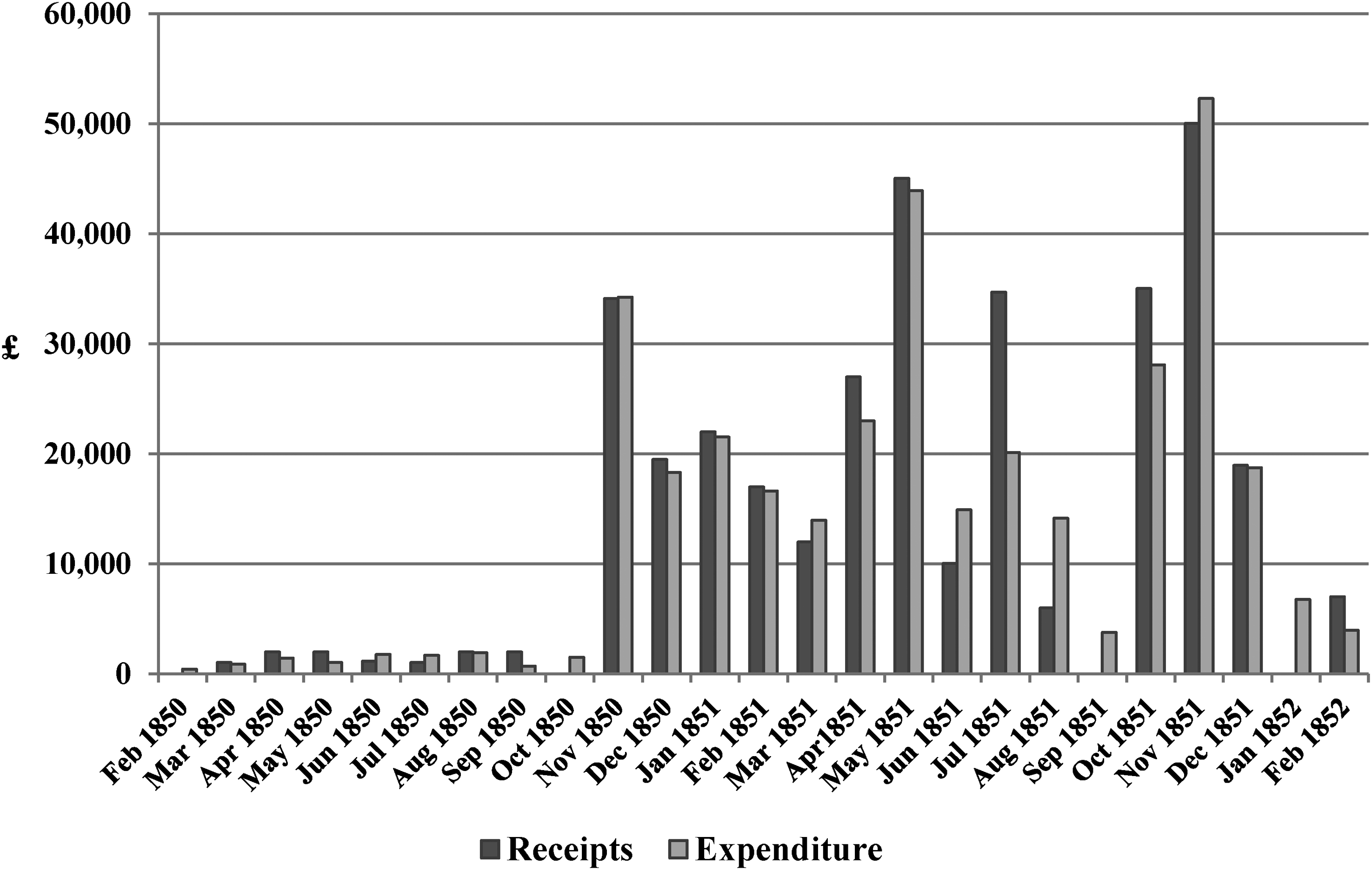

The evidence suggests that through the life course of the Great Exhibition, the Financial Officer successfully managed expenditure and cash resources. The data presented in Figure 1 indicates that Carpenter carefully matched monthly expenditure and receipts, especially in the period before the opening of the Exhibition in May 1851, when its revenue-generating capacity remained uncertain.

Monthly receipts and expenditure, 1850–52.

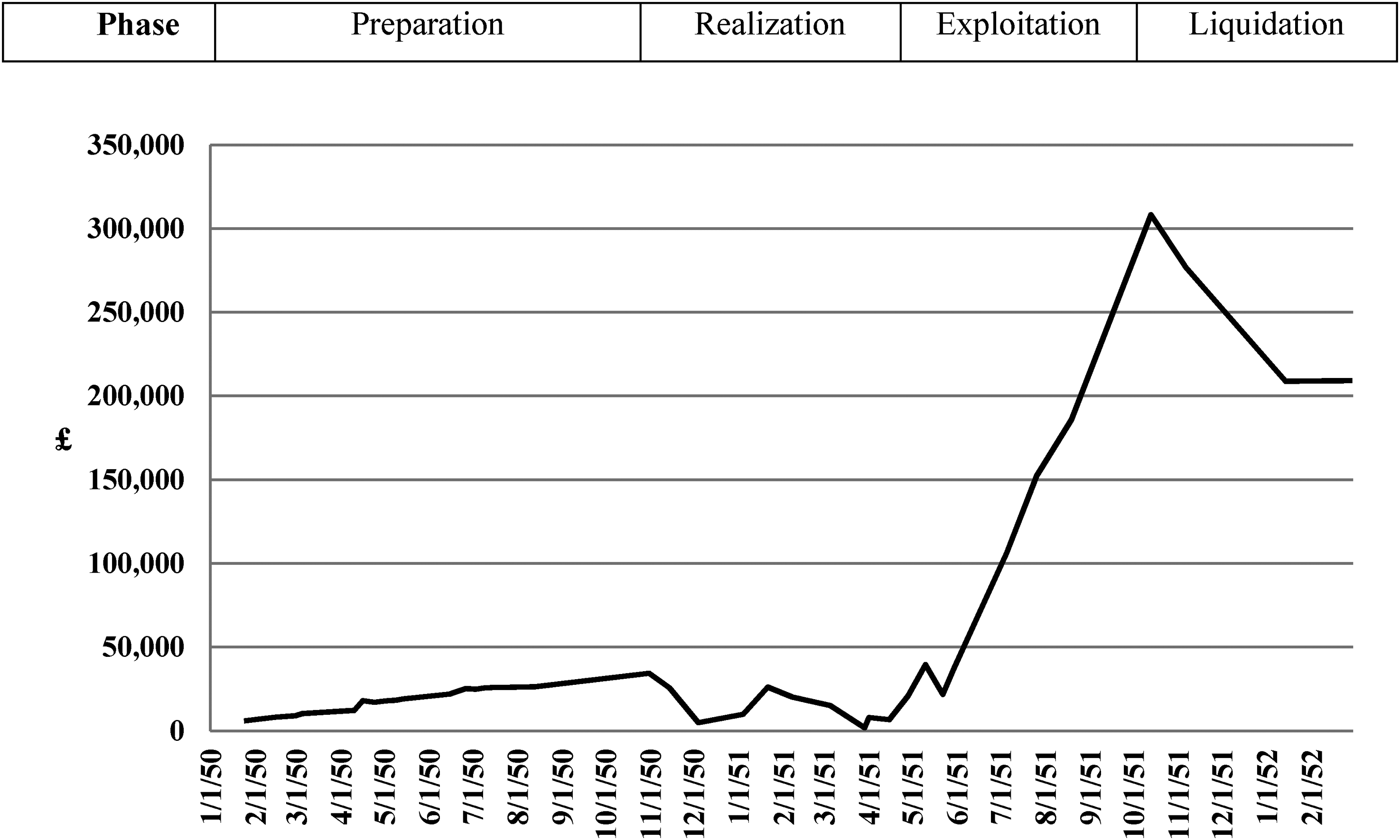

The management of funds focused on ensuring that there were sufficient liquid resources to meet payments, moving funds between bank accounts and investing surplus cash generated. As illustrated in Figure 2, Carpenter oversaw several phases of cash management during the focal period. These resonate with the four phases of exhibition projects identified by Fabre and Michaïlesco (2010), namely preparation, realization, exploitation and liquidation.

Balance at the Bank of England general account and exchequer bills, 1850–52.

The first phase was from February to November 1850 when receipts from subscriptions were used to maintain the operations of the Royal Commission and to prepare for and promote the Exhibition. In order to pay monthly expenses, Carpenter requested transfers in multiples of £1000 from the general account at the Bank of England to an account for ‘executive services’ opened with Messrs Coutts (First Report, 1852: xix; Minutes, 21 February 1850). By September 1850, these transfers totalled £11,000. Payments made during this period included salaries (especially the cost of engaging special commissioners to promote the Exhibition and the work of local committees), office rentals, printing and postage, as well as fees relating to the preparation of plans for the building. Cash inflows were primarily from subscriptions (Minutes, 9 May 1850; 21 June 1850).

During the second, realization phase, autumn of 1850 to the end of April 1851, the balance of available funds was comparatively low and required careful management. This was the period when the exhibition building was constructed and fitted out. During these months, the principal challenge was ensuring sufficient cash to pay numerous progress payments to the contractors. By 10 May 1851, these totalled £99,315 (Minutes, 12 May 1851). Employment costs also increased significantly during this stage of project realization. The cost of installing turnstiles, furnishings and other adornments to the building not provided by the contractors also had to be met. In spring 1851, these expenses were covered by receipts from season ticket sales (which totalled £20,344 by mid-April 1851, Grove to Carpenter, 14 April 1851, RC/A/1851/179) and the proceeds of the contracts awarded for supplying exhibition catalogues and providing refreshments.

The third, exploitation phase, May–October 1851, represents the period when the Great Exhibition was open and became a cash generator. These months witnessed rapidly increasing cash inflows as it became apparent that ‘The exhibition has been successful beyond expectation’ (Reid to Phipps, 31 July 1851, RC/H/1/7/140). By 30 June cash at bank, swelled by receipts from two million visits, stood at £114,643 (Minutes, 5 July 1851). The Finance Committee recommended that the Treasurers purchase £80,000 interest-bearing Exchequer Bills with the surfeit of cash . Final payments to contractors, the police and compensation to Messrs Munday relating to the termination of their contract, were easily paid from the ‘shower of silver’ collected at the doors. A further £65,000 of Exchequer Bills were purchased at the end of July (Minutes, 26 July 1851). Although a substantial volume of cash was taken over the summer, the Finance Committee and the Commissioners did not meet during the parliamentary recess. Further investments in Exchequer Bills were consequently not sanctioned until mid-October. As a meticulous rule-following commissariat officer of a ‘naturally retiring disposition’, Carpenter was neither empowered nor inclined to take the initiative in the absence of his superiors (Bedfordshire Mercury, 21.6.1890; Funnell, 1990).

The fourth, liquidation phase concerned the period after the close of the Great Exhibition in October 1851 to the end of February 1852, the financial reporting date. The Exhibition had proved enormously successful. Attention turned to distributing the surplus (Minutes, 13 October 1851). From October to December 1851 there were significant cash outflows (see Figure 2). These concerned payments relating to the award of prizes to exhibitors and photographing and removing exhibits. Payments were made to the building contractors, Fox and Henderson, for losses incurred under the construction contract. A substantial sum was also spent on gratuities to those deemed to have contributed to the success of the event. In early 1852, smaller payments were made for policing costs and in compensation for loss of earnings arising from the Exhibition.

Accounting and financial reporting

The Financial Officer at the Great Exhibition was responsible for accounting. This was performed on a cash basis. An emphasis on payments, receipts and available cash was the frame of reference for the discussions of the Finance Committee. The focus on receipts and especially expenses was consistent with the operational priority of assuring subscribers that strict economy would be pursued.

At the Great Exhibitions staged in Paris in 1853 state financing resulted in the imposition of public accounting systems (Fabre and Michaïlesco, 2010). Although the predecessor event in London in 1851 did not rely on monies voted by the state, the cash-based accounting regimen was redolent of that used in Victorian central government. Although there had been discussion of the merits or otherwise of introducing the mercantile system of double entry in central government during the second quarter of the nineteenth century (Edwards, 2011; Edwards, Coombs and Greener, 2002; Edwards and Greener, 2003), at the time of the Great Exhibition ‘the system of accounting in central government remained principally cash-based’ (Edwards, 2015). There continued to be an emphasis on ensuring that payments were valid and that delegated financial responsibilities had been properly discharged (Edwards, Coombs and Greener, 2002).

Cash-based accounting systems were pervasive in the department in which the Financial Officer of the Great Exhibition was principally employed – the Commissariat. A commissariat officer's attention was on cash and supply and the emphasis of the accounting regimen was on the comprehensive recording and vouching of all transactions. Commissariat accounting was characterised by punctiliousness – ensuring that ‘for every penny spent and every pound of supplies issued records had to be kept’ (Funnell, 1990: 325). Such attention to detail was encouraged by the fact that officers were deemed personally responsible for discrepancies in cash and stores (Funnell, 1990). The Commissaries’ accounts were produced on a receipts and payments basis and focused on amounts received into and disbursed from the military chests at overseas stations, as well as on the balance of the cash in the chest at the reporting date. 3 This resonated with accounting arrangements at the Great Exhibition. It was unlikely that a Commissariat officer would have the inclination to introduce more complex accounting arrangements (Report, 1858: 4, 29). Mercantile double-entry bookkeeping, for example, was not much used in the Commissariat service (Report, 1858: 26).

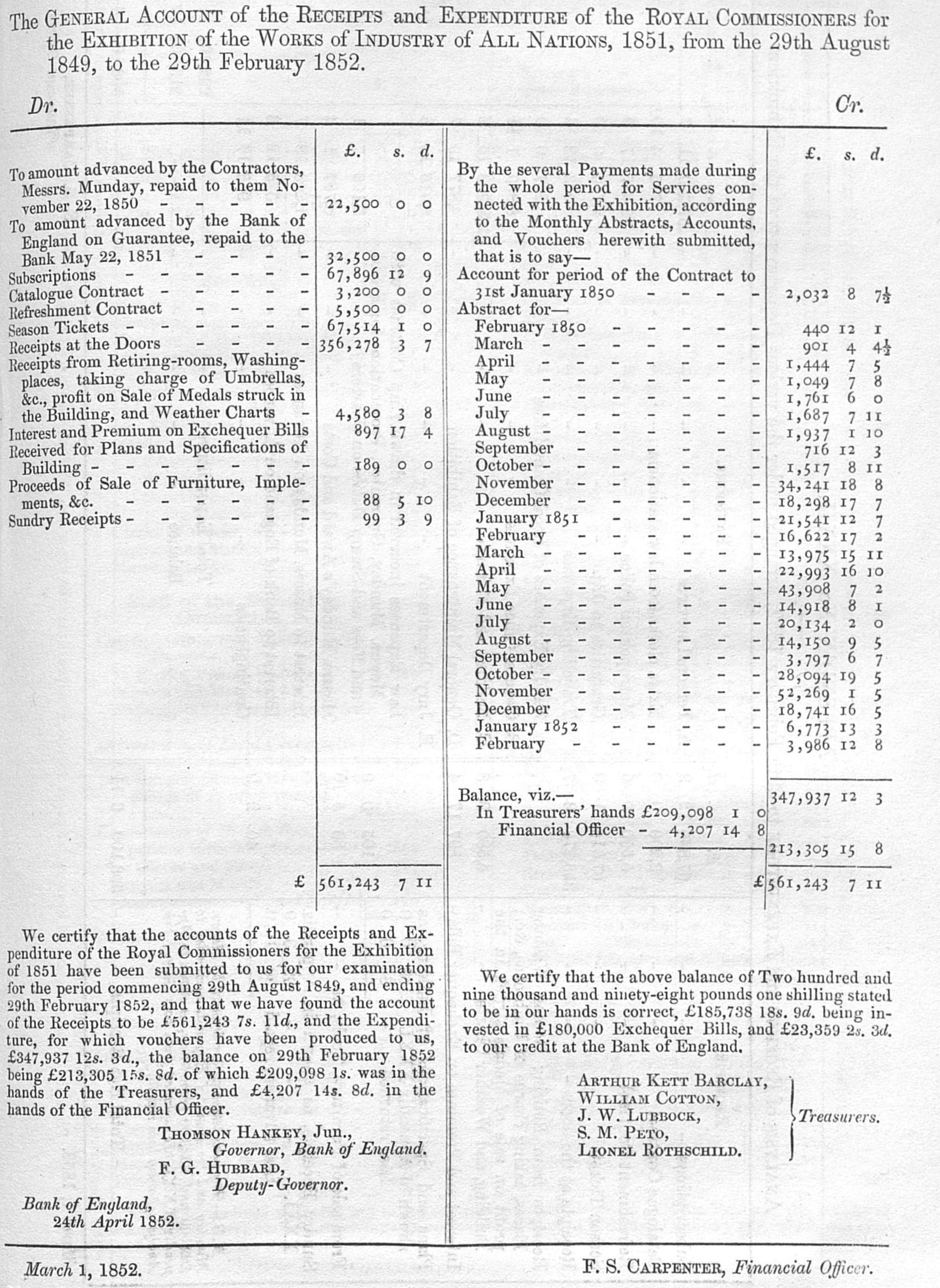

The Exhibition closed its doors in October 1851. By early 1852, with its success affirmed, the Commissioners turned their attention to preparing a report to the Crown (First Report, 1852: ix, xv). The Financial Officer submitted an analysis of receipts and expenditure which was to be included in the report (Minutes, 1 March 1852). Carpenter's financial statement related to the whole span of the exhibition project. His ‘General Account of Receipts and Expenditure’ for the period August 1849 to 29 February 1852 is reproduced in Figure 3.

General account of receipts and expenditure.

Although it was described as a ‘balance sheet of receipts and expenditure’ (First Report, 1852: l), this was not the ‘balance sheet’ of a profit-orientated business focused on assets, liabilities and return on capital. Rather, it represented an illustration of the cash-based accounting system operated by central government. Here, the term balance sheet was often deployed ‘to describe a variety of bilateral statements including those simply listing receipts on the left and payments on the right’ (Edwards, 2015). The format of Carpenter's ‘General Account’ was consistent with reporting practice at the Treasury, the government department that controlled the Commissariat. Although such financial statements could emanate from a double entry system for recording cash transactions, the existence of headings ‘Dr’ and ‘Cr’ does not imply that the accounts were prepared on that basis (Edwards, Coombs and Greener, 2002; Edwards and Greener, 2003).

The sources suggest that there was political sensitivity around the accounting period for the ‘General Account of Receipts and Expenditure’ (Figure 3). At the time of its composition, speculation was rife about the Commissioners’ intended use of the financial surplus generated by the Exhibition, which stood at £213,306. Financial reporting was initially perceived as akin to that of a finite venture where the accounts were left open until the cessation of the project (Luther, 2003). However, the financial statements produced in February 1852 were incomplete as they did not include the disposal of the surplus. Hence, it was not possible to ‘wind up’ the accounts. A note was, therefore, added to the report to the Crown to assure readers that further audited financial statements would be supplied (First Report, 1852: l). Prince Albert was particularly anxious that this commitment to providing full accounts from 1 March 1852 in a later report to the Crown would be honoured (Grey to Bowring, 13 May 1852, RC/H/1/B/39).

Another issue, again amidst speculation about the intended use of the surplus, relating to the reporting period arose from the fact that the end date of Carpenter's ‘General Account’ was 29 February 1852, but the report of the Royal Commissioners was dated 24 April. Several weeks’ receipts and payments were, therefore, unaccounted for and had not been audited. On 22 April 1852, the Secretary to the Commission expressed his fear that ‘if we leave out this month [March], people will say that a job has been done in it and that it is therefore omitted’ (Bowring to Grey, RC/H/1/B/29). It was, therefore, agreed that a note would be added in the Commissioners’ report about receipts and expenditure during March (First Report, 1852: li).

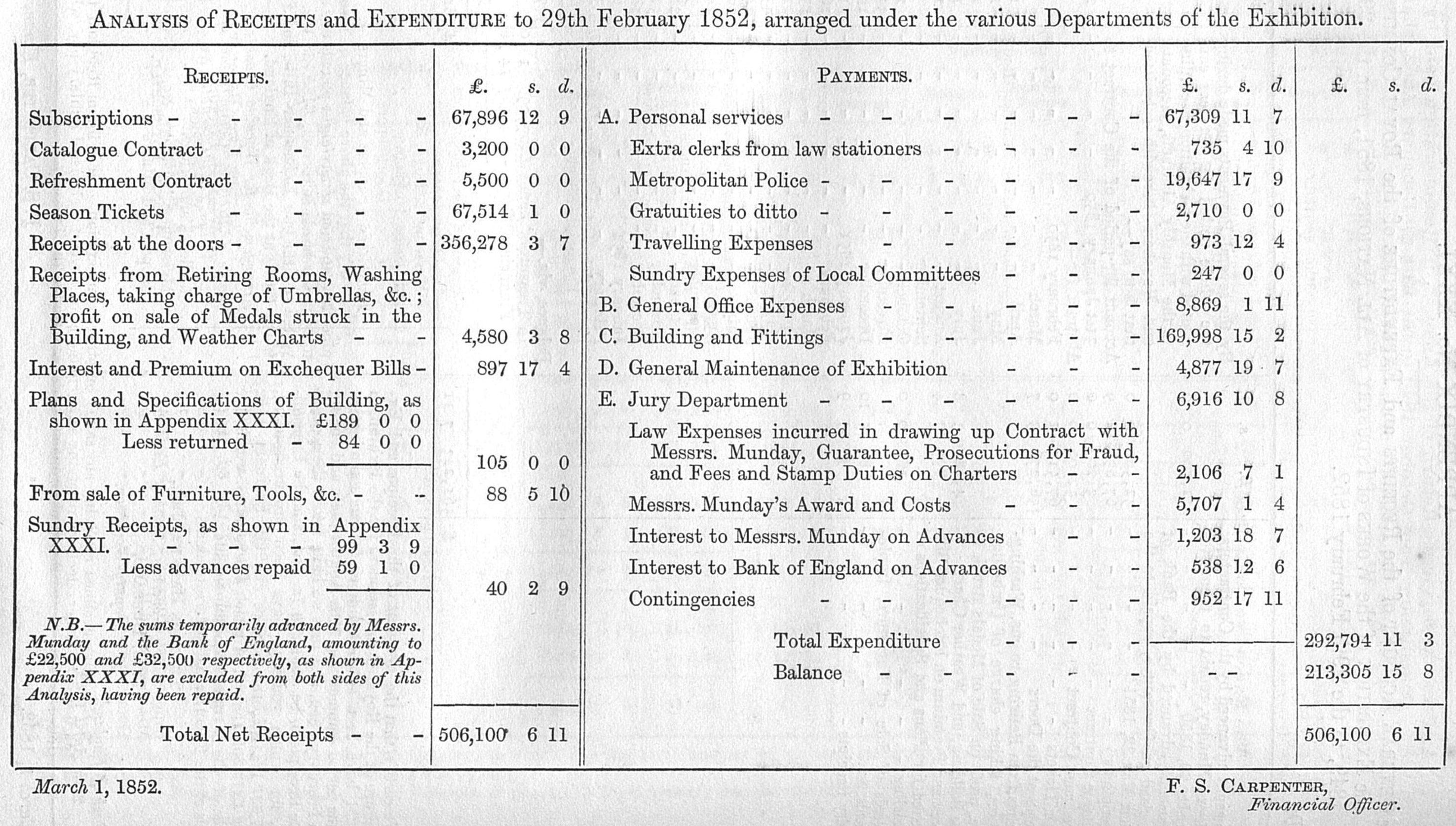

The ‘General Account’ was accompanied by an ‘Analysis of Receipts and Expenditure’ for the same reporting period (see Figure 4). The payments side of this analysis was supplemented by notes detailing major expense categories. These related to employment costs (personal services), office expenses, exhibition maintenance, expenses relating to the award of prizes and medals to exhibitors by 30 juries comprising ‘men of eminence in various branches of Arts and Science’ (jury department) (First Report, 1852: xxxviii-xxxix), and the most substantial outlay – the cost of constructing and fitting out the building (First Report, 1852: 155–156). The receipts side of the statement was supplemented by a daily analysis of the sources of revenue during the period of the Exhibition (First Report, 1852: 157–159). In relation to the most significant source of revenue, cash taken at the door, the Financial Officer also submitted a statement of daily losses arising from payment with light gold, defaced, foreign and spurious coin (First Report, 1852: 160–161). This is discussed further below.

Analysis of receipts and expenditure.

The form and content of the ‘Analysis of Receipts and Expenditure’ (Figure 4) and accompanying notes was the subject of much discussion among the Royal Commissioners for the Great Exhibition. There was political sensitivity surrounding specific disclosures in the context of a debate then raging about the future of the Exhibition building (Auerbach, 1999: 193–197; Colquhoun, 2006: 191–192; Davis, 1999: 209–210; Hobhouse, 2002: 77–80, 83–84). On 30 March 1852, the Prime Minister confirmed that the Crystal Palace would be removed from Hyde Park (Hansard: c.343). A strong opposition movement had formed, and numerous petitions were signed (Reports and Circulars Relating to the Preservation of the Crystal Palace, 1852). On 3 April 70,000 congregated at the Crystal Palace in a ‘great public demonstration’ of support for its preservation (Times, 5.4.1852).

In this context Henry Cole (who supported retaining the building) called for accounting transparency, emphasising ‘the necessity of publishing more fully than is now proposed the details of the Commission's expenditure’ (Cole to Grey, 20 April 1852, RC/H/1/B/26). Although Cole stated that there was ‘nothing to conceal’, non-disclosure of expenditure might provide ammunition to those seeking to prevent the demolition of the Crystal Palace. Cole observed an ‘ugly feeling towards the surplus’ and feared that the opposition movement might resort to violence (Cole to Grey, 20 April 1852, RC/H/1/B/26). The high public cost of maintaining the building was presented as a reason for its demolition. A Treasury Commission had recently estimated that the costs of keeping and maintaining the Crystal Palace as a winter garden would be £200,000 (Report of the Commissioners, 1852: vi). However, the preservation movement argued that the cost estimates had been inflated and could be offset by revenue from establishing the building as a permanent place of ‘public instruction and recreation’ (Reports and Circulars Relating to the Preservation of the Crystal Palace, 1852). Indeed, popular proposals, such as that of the building's designer, Joseph Paxton (1851: 15), to retain the Crystal Palace as a winter garden, had been accompanied by projections indicating annual expenditure of only £12,000.

There was also sensitivity around disclosures about remuneration, likely in the context of the substantial gratuities that the Commissioners decided to pay from the Exhibition surplus. The Great Exhibition was closed to the public on 11 October 1851. Two days later, the Finance Committee was remitted to consider the payment of additional remuneration to those in the executive service who had contributed to the event (Minutes, 13 October 1851: 2). Within five days, a list of potential recipients of gratuities was produced, totalling £32,500 (RC/H/1/8/115). Although the press was receptive to the ‘handsome recognition’ of those deemed to have secured the success of the Exhibition, amounts to individuals ranged considerably, from £5 to £5,000 (Times, 17.9.1851; 29 October 1851).

Henry Cole confided in his diary that at a Finance Committee meeting in January 1852, some members were ‘particularly averse to publishing the names and sums which each one received from the Commission’ (9 January 1852). Carpenter's initial draft of the ‘Analysis of Receipts and Expenditure’ was agreed on 1 March 1852 (Minutes). However, in April 1852, the Finance Committee discussed ‘the question of publishing a more detailed account of salaries and gratuities’ (Bowring to Grey, 22 April 1852, RC/H/1/B/29). Cole recorded in his diary that at the meeting Mr Labouchere ‘strongly backs the publication of the names of persons who received above £100’ (22 April 1852). The Commissioners requested that the Finance Committee revise the Analysis of Receipts ‘with a view to giving more detailed accounts of the sums expended, referring the amounts to services rather than to persons’ (Minutes, 24 April 1852). In the final published version of ‘Analysis of Receipts and Expenditure’ (Figure 4), payments were analysed by type rather than department. Employment costs were presented under the heading ‘Personal services’. The supporting analysis for this category did not identify whether remuneration was derived from salaries or gratuities, nor did it disclose amounts received by named individuals.

Internal controls

As we have seen, the Royal Commissioners were anxious to assure potential subscribers that the money raised was properly managed and applied. Attention was, therefore, given to establishing effective internal controls. These centred on the legitimacy of disbursements, protecting cash collected at the Exhibition, and ensuring that the accounting records accurately reflected the cash position.

In relation to cash disbursements controls took the form of establishing responsibility for payments, the segregation of duties and internal verification. The general account at the Bank of England was held in the names of the Treasurers. The account at Messrs Coutts & Co. to defray current expenses was held in the name of the Chairman of the Executive Committee of the Royal Commission and the Financial Officer (Minutes, 21 February 1850). All payments made by the Financial Officer from the latter account were subject to authorisation by the Finance Committee (First Report, 1852: l). The Financial Officer's requests to transfer funds between bank accounts to meet ‘executive expenses’ were also subject to the approval of the Finance Committee and ultimately the Commission (Minutes, 24 January 1850). Likewise, any requests for payments by the Finance Committee required the sanction of the Finance Officer. The Financial Officer prepared monthly estimates of expenditure for authorisation by the Finance Committee and the Commissioners. Any additional requests arising during the month also required such approval. The actual payments made by the Financial Officer, supported by vouchers, were presented to the Finance Committee on a monthly basis – a mode of internal verification invariably described as ‘auditing’ (First Report, 1852: xvii, 10; Collection of Printed Documents, Vol. 2, no. 152).

Considerable attention was also devoted to controls relating to the receipt of cash. This was not surprising given that cash is a vulnerable asset, its liquidity rendering it susceptible to misappropriation. The risk of accounting fraud and error was especially high in the context of the substantial volume of cash received in relation to the Great Exhibition. The Treasurers were given responsibility for the receipt of subscriptions from local committees and for paying them into the account at the Bank of England (Minutes, 25 January 1850). The Financial Officer frequently reported daily totals of receipts to the Finance Committee.

The principal control issue relating to cash receipts concerned the processing and security of a mass of coin collected from visitors to the Exhibition. A total of £356,808 was taken at the doors of the Crystal Palace. Procedures were necessary to collect and protect cash from an average of 37,610 persons per day (see Figure 5). From 2 May (when payment at the doors commenced) to 11 October 1851, no fewer than 5,265,429 visitors paid a daily entrance fee of one pound, five shillings, two shillings and six pence. or one shilling. This pricing structure was intended to raise sufficient revenue, encourage the attendance of all social classes and also allow those with sufficient means to avoid crowds (First Report, 1852: xlviii; RC/A/1851/22). Not surprisingly, 84.3 per cent of visitors attended on the 80 days when one shilling was charged (First Report, 1852: 90–91). During the first three days of the final week of the event, an average of 104,603 visitors paid one shilling at the door (First Report, 1852: 85–88; Short, 1966). The silver coin alone taken at the Exhibition weighed 35 tons (The Bucks Herald, 25.10.1851).

Entrance to the exhibition on shilling day.

The Financial Officer's experience as a Commissariat Officer was likely to have proved important to creating a control environment around cash. Commissariat Officers often had custody of large sums of public money and were experienced in establishing systems of checks (Report, 1858: 129). Ensuring the security of the coin contained in the military chest that was taken on a military campaign was an important responsibility (Report, 1858: 129, 136). Officers could find themselves in charge of a chest containing £100,000 in bills and specie at an overseas location. Consideration also needed to be given to securely transporting the chest in a horse-drawn carriage.

Controls over cash received were institutionalised in the architecture of the Crystal Palace. The application of the principle of ‘centralization of supervision’ was a key criterion in the design of the Exhibition building (Collection of Printed Documents, Vol. 2, no. 354; Vol. 8, Report of the Committee to Consider Matters Relating to the Building, 9 May 1850; Bennett, 1995: 59–88). In relation to cash from visitors, it was envisaged that the building would contain ‘Passages running behind the money-taker's boxes with glazed doors into them’.

This: ‘would enable each accountant to detect anything improper that might be going on, and to exchange balance checks, money, &c. at any moment. Telegraphic communication with each of the four pay places will permit orders to be given. Cash accounts, &c. to be issued, and returned, from and to the head Accountant as often as may be necessary’ (Report of the Committee to Consider Matters Relating to the Building, 9 May 1850, also Berlyn and Fowler, 1851: 9).

Further, multiple entrances were considered undesirable as this would result in dispersed rather than centralised money-taking and also require a larger complement of officers to supervise it (Berlyn and Fowler, 1851: 33). Contract drawings for the Crystal Palace incorporated the supervision of cash-receiving at three entrances (Collection of Printed Documents, Vol. 4). It was proposed to locate finance staff in offices to the side of the entrances where money was taken (Official Descriptive and Illustrated Catalogue of the Great Exhibition of the Works and Industry of all Nations, 1851 Vol. 1: 67).

Mechanical controls also featured. In March 1851, three alternative systems were considered for admitting the public to the Exhibition (RC/A/1851/105:1). Registering turnstiles were ultimately not only selected on grounds of economy and simplicity but also because they ‘give no room for fraud, except in the case of two children being forced through with one turn of the machine for which of course the Police and others must watch, and which could not occur often’ (RC/A/1851/105:1). The money taker could work the turnstile with his foot, his hands being free to process cash. Under the turnstile system, it was possible to admit more than 20,000 persons per hour with minimal supervision. 4

In April 1851, physical controls were also established to protect cash received at the doors. Following discussions between the Financial Officer, Thomas Baring MP of the Finance Committee and the Deputy Governor of the Bank of England, it was agreed that the Bank would receive all money taken at the Exhibition (Minutes, 2 April 1851; Bentley to Bowring, 9 April 1851, RC/A/1851/169). The Deputy Governor proposed the following: … a clerk should be sent from the Bank of England early every morning to bring down the silver received the previous day, which should be put up in Bags of £100 each, and placed in boxes of convenient size for carriage, locked before leaving the Exhibition, and opened by a key to be kept by the Cashiers at the Bank – it would be necessary of course to send a Clerk up expressly for this purpose, he would require safe conveyance, and it would be desirable to have a Porter for greater security (Minutes, 2 April 1851; Bentley to Bowring, 9 April 1851, RC/A/1851/169).

Also in April 1851, ‘Regulations for Money and Ticket Takers’ were produced. These documented responsibilities and internal verification controls (Collection of Printed Documents, Vol. 5, no. 679a). Responsibility for money-taking was to be affirmed by a roll call before the daily opening of the Exhibition. Having taken up his post, the employee was forbidden to leave without notifying the Superintendent of the Money Takers or the Superintendent of Police at the Exhibition entrance. Further, it was specified that ‘The Money and Ticket Takers will make up Money and shew their Books and Wheel at all such times and hours as the Financial Officer may appoint; and every way conform to his instructions’ (Collection of Printed Documents, Vol. 5, no. 679a). At the end of each day, the money takers made up their cash ready for collection by a person sent by the Financial Officer. The money taker was unable to leave his box until relieved by the signature of a visiting accountant.

When the Great Exhibition opened the controls relating to the mass of cash received by the money takers attracted press interest. Reports described how money porters gathered the cash from money takers and carried it to collectors for counting.

The cash was then taken: ‘to two tellers, who verified the sum, and handed it to the final custody of the chief financial officer, Mr F.G. Carpenter [sic], who locked each day's amount in his peculiar iron chests in the building till next morning, when in boxes, each holding £600, it was borne off in hackney-cab, in charge of a Bank of England clerk and a Bank porter’ (The Bucks Herald, 25.10.1851).

On 7 October 1851, 104,630 visitors paid one shilling at the door of the Exhibition.

On the following day, The Times (8.10.1851) observed: ‘Even the Bank of England begins to feel the flow of silver to its coffers from the glutted exchequer of the Royal Commissioners. Yesterday it was found necessary to have two cabs to convey to Threadneedle-street the accumulation of the previous day, and the weight of specie amounted to no less than 15cwt’.

Money takers were also subject to rules relating to all employees of the Exhibition. These included prosecution ‘with the utmost rigour of the law’ for embezzlement (Collection of Printed Documents, Vol. 5, no. 561). Limited references to suspicious behaviour by money takers suggest the effectiveness of the foregoing controls. The revelation contained in Lloyds Weekly London Newspaper on 17 August 1851 was an exception: We regret to hear that one of the more responsible of the persons employed as money-takers was noticed today by one of the sappers to place his hand in his pocket more frequently than, in the opinion of the latter, the circumstances of the case would fairly justify. This suspicion was communicated to one of the officials in attendance, and several of the detective officers were directed to watch; and they soon observed such a repetition of the acts as fully to warrant the suspicion previously formed. The subject will be more fully inquired into.

The press also disclosed that controls had to be relaxed when the number of visitors overwhelmed the money takers. On 6 October 1851, when 103,516 paid at the door, double the average attendance of the previous week, the system for admitting the public was unable to cope. It was reported that by opening time the human tide was such that the turnstiles were dispensed with, and visitors entered ‘without that check’ (The Windsor and Eton Express). For two hours, the money takers endured ‘a silver shower such as has seldom been witnessed’.

The Commissioners later reported that the arrangements: ‘for taking the money were found sufficient, except on about twenty occasions, when it was requisite to allow the general public to pass in by the season-ticket entrances, two persons being stationed at each to take the money. Such pressure seldom lasted more than half an hour’ (First Report, 1852: 29).

Despite such pressures, the Commissioners were confident that the system of checks ensured that its accounts of cash received at the door were ‘perfectly accurate’ (First Report, 1852: 80).

A particular concern of the Financial Officer, as an Assistant Commissary-General, was the risk of receiving bad coin. The Commissioner's decision to set a single daily entrance price and inform potential visitors that no change would be given at the door facilitated the scrutiny of money received from the many thousands admitted to the building. Carpenter produced a meticulous account showing the loss incurred each day from light gold and defaced, spurious and foreign coin (First Report, 1852: 160–161). He detailed the 12 Crowns, 260 Half-Crowns, 1,034 Shillings, 90 Sixpences and 3 Fourpences received in bad coin. Even though the rapid volume of persons could occasionally prevent the money takers from examining each coin received (The Bucks Herald, 25.10.1851), their vigilance was such that the total loss incurred from bad coin was only £529.17s.5d (First Report, 1852: li). This represented a mere 0.15 per cent of gross receipts taken at the door.

Admission to the Great Exhibition was not only by cash. Controls were also necessary in relation to season tickets. 25,605 season tickets (13,494 gentlemen's and 12,111 ladies’) were sold and generated total receipts of £67,514. 773,766 visitors (including the admission of staff and jurors) entered the Crystal Palace with them, an average of 5,473 per day (First Report, 1852: li, 85–91). As season tickets were non-transferable, verification procedures were necessary to prevent fraudulent use. It was, therefore, decided that season tickets would bear the autograph signature of the holder (Fuller to Granville, 22 January 1851, RC/A/1851/6). On arriving at the season ticket entrance, the signed ticket was shown to an inspector and its presenter was asked to write their signature in a book. The inspector then compared the signatures. If the signatures were not alike the Superintendent or the nearest Police Constable was sent for. Season ticket holders being of a superior class, money takers were reminded that ‘very great caution must be used on this subject and not acted upon without strong grounds for suspicion’ (Collection of Printed Documents Vol. 5, no. 679a). The signing-in of season ticket holders features in Figure 6. The knowledge that such checks were in place was considered a preventative to fraud (Belhouse to Reid, 22 January 1851, RC/A/1851/5).

Entrance to the exhibition on five shilling day.

The controls surrounding entrance by season ticket appeared to be effective. However, in September 1851, the Financial Officer reported that he had experienced ‘considerable difficulty’ when attempting to prepare accounts of season tickets issued at the Exhibition building (RC/A/1851/463). He discovered a deficiency of 4 gentlemen's and 17 ladies’ tickets. Although three of these season tickets had been issued by mistake, the remainder could not be traced or accounted for. Consistent with his priorities as a Commissariat Officer, Carpenter described to his superiors the detailed procedures he had followed to locate the deficiency, and more importantly, to identify the person(s) responsible for it. Despite exhaustive investigations, he failed in this endeavour. Carpenter suspected that the problem emanated from confusion in the days immediately before the Exhibition opened when the demand for season tickets was high, the issuance of temporary tickets, and the sale of season tickets by more than one vendor (RC/A/1851/463). Akin to his meticulous attention to the immaterial losses arising from ‘bad coin’ taken at the door, the deficiency in relation to season tickets represented no more than 0.07 per cent of total receipts from that source.

Auditing

As we have seen, the Royal Commissioners for the Great Exhibition made an early attempt to assure subscribers that the strictest economy would be practised and funds contributed would be carefully scrutinised. In addition to this monthly recurring ‘audit’ by the Finance Committee of the payments made by the Financial Officer, two specific audit tasks were performed. These comprised the verification of the financial statements and the examination of the accounts of the building contractors.

The limitations of auditing at the time of the Great Exhibition have been well-documented by accounting historians. Funnell (2004) has demonstrated the deficiencies of central government audit in Britain prior to major reforms in the 1860s (see also Edwards and Greener, 2003). Although more thorough ‘continuous audits’ were being instituted in some railway companies at the time of the Great Exhibition (Edwards and West, 2021), researchers of the history of corporate auditing have emphasised the limited scope of audit practice and the ambiguous role and questionable independence of auditors in Victorian Britain. They also demonstrate the limited performance of the audit function by professional accountants in general companies until the late nineteenth century (Anderson, Edwards and Matthews, 1996; Chandler and Edwards, 1996; Chandler, Edwards and Anderson, 1993; Lee, 1979; Maltby, 1999; Popp, 2000; Teo and Cobbin, 2005; Walker, 1998). Such limitations were apparent in external auditing at the Great Exhibition. Here, the accounts were formulated not for shareholders or suppliers of government finance but to meet the information needs of subscribers and the wider public.

The appointment of auditors not having been previously discussed, in February 1852 the Finance Committee decided to approach the Governor and Deputy Governor of the Bank of England to audit the accounts of the Commissioners (Minutes, 1 March 1852; First Report, 1852: 153). Although these members of the financial establishment no doubt lent authority and integrity to an audit opinion, the Bank of England was not strictly independent of the Royal Commission for the Exhibition. The principal bank account of the Commission was with the Bank as were its investments in Exchequer Bills. The Deputy Governor had been involved in arranging the collection and deposit at the Bank of £356,278 in cash taken at the doors of the Crystal Palace. A number of Bank of England clerks were also employed for this purpose by the Finance and Admission Department of the Exhibition (First Report, 1852: li, 155). Furthermore, Thomas Baring MP, one of the members of the Finance Committee, was a Director of the Bank of England. William Cotton, one of the Treasurers of the Royal Commission was also a director and former Governor of the Bank.

An audit of limited scope was also envisaged. One that appears to have been a superficial exercise, where the correctness of the headline balances in the financial statements was checked against the books of account and relevant vouchers. In February 1852, the Secretary to the Commissioners reported that although an independent audit was needed to satisfy the public it would be ‘a matter of form’, particularly as a member of the Finance Committee, Sir Alexander Spearman, had ‘already done everything’ (Bowring to Grey, 14 February 1852, RC/H/1/9/58). 5

Indeed, the examination of the financial statements did not unduly detain the Governor and Deputy Governor of the Bank of England. The audit of the accounts dated 29 February was completed by 1 March (Minutes, 1 March 1852). This was also an audit of the principal financial statement only. The audit report (see Figure 3) concerned the ‘General Account’, not the ‘Analysis of Receipts and Expenditure’ and its accompanying notes (Figure 4). The report stated that the auditors agreed with the total receipts as stated in the ‘General Account’ as well as the expenditure, for which vouchers had been supplied as well as the balance in the hands of the Treasurers and the Financial Officer. The face of the ‘General Account’ also contained a statement that the Treasurers to the Commission had certified the balance of cash in their hands.

The second significant audit task concerned internal investigations of the accounts of the contractors who built the Crystal Palace – Messrs Fox, Henderson & Co. On 16 October 1851, Fox and Henderson, who originally agreed to put up the building for £79,800 and had received numerous progress payments, wrote to Lord Granville, Chairman of the Finance Committee, to state ‘in plain terms’ that they had suffered ‘a deficiency of nearly £60,000… an amount which we shall be quite unable to bear’ (RC/A/1851/513). This deficiency had arisen from the rapid preparation of the original estimates for the building, the complexity of its design and the significant alterations made during its construction. Further, the need to meet the deadline for opening the Exhibition meant that it was impossible to control labour costs. Indeed, Fox and Henderson had proceeded ‘without regard to expense’ given that the venture represented a ‘great enterprise’. However, they hoped that by revealing the full facts, the liberality of the Commissioners might be forthcoming (RC/A/1851/463).

The letter from Fox and Henderson instigated two bouts of auditing. The Chair of the Finance Committee and Sir William Cubitt (who, as Chair of the Building Committee had hitherto scrutinised periodic statements of construction costs), assisted by Carpenter as Financial Officer, were remitted to investigate Fox and Henderson's accounts. The resultant report, dated 6 November 1851 (RC/A/1851/679), expressed the view that although the contractors had no claim to further remuneration under their contract, given the ‘ability and energy’ they had displayed in constructing the building as well as the ‘ample funds in the hands of the Royal Commissioners’, they ‘should be secured from pecuniary loss’. Having examined the 110 items in the accounts supplied by Fox and Henderson, it was calculated that the loss to the contractors was actually £50,000.

The Commissioners agreed that Fox, Henderson & Co should be secured against loss. They recognised ‘the unprecedented character of the undertaking, the shortness of time allowed for its completion, and the energy and liberality with which the contractors had laboured to meet the wishes of the Commission’ (First Report, 1852: xxx). They determined to pay an additional £35,000 on condition that the firm agreed to terms set by the Commission (Minutes, 6 November 1851). The remaining £15,000 would be contemplated on the satisfactory removal of the building and the restoration of the ground on which it had stood in Hyde Park. Fox and Henderson immediately agreed to these terms, which included the provision that £35,000 would be advanced subject to the verification and settlement of the accounts (RC/A/1853/217/2).

Among the Commissioners, Thomas Baring MP was particularly sceptical about Fox and Henderson's accounts and urged that they be ‘strictly’ and independently audited (Grey to Granville, 23 November 1851, RC/H/1/9/34; Henry Cole's Diary, 7 November 1851). Baring suspected that Fox and Henderson had made ‘special arrangements’ with supplying manufacturers and subcontractors such that actual payments were hidden (RC/A/1851/774). The audit would be performed by Joshua Field, an eminent engineer, who had sat on various committees relating to the Exhibition, and John Phipps and William Starie, Assistant Surveyors of Works in the Office of Works. Lord Granville expected that these appointments would ensure that ‘Mr Baring's anxieties will be laid at rest’ (Granville to Grey, 21 November 1851, RC/H/1/9/31; also RC/H/1/9/36).

The auditors presented their report (RC/H/1/9/36) on 1 December 1851 (RC/A/1851/820). Having examined the accounts and vouchers they were of the opinion ‘that the prices in the Bills of Messrs Fox and Henderson for castings and other works are at low prime cost prices, and that their charges for workmen's wages, salaries &c at the Park are fair’ (RC/A/1851/820). Further, the accounts relating to works executed by other tradesmen for Fox and Henderson were stated at prime cost and the prices were ‘generally low’ (RC/A/1851/820). The accounts had been correctly kept and trade discounts had been taken. Full explanations had been received from the firm during the investigation. Indeed, the auditors revealed that Fox and Henderson had understated their costs by £925. Despite this outcome, scepticism remained. Edgar A. Bowring was concerned that although Fox and Henderson's accounts were seemingly fair and the outcome of the investigation was ‘very satisfactory, as justifying the course taken by the Commission in the eyes of the public, it is of course quite impossible to get at the very bottom of the whole affair, as these may have been secret and sub-contracts the existence of which can never be found out’ (Bowring to Phipps, 4 December 1851, RC/H/1/9/38).

Although such apprehension persisted, the result of the audit left the Commission with no alternative but to compensate Fox and Henderson. £35,000 was accordingly remitted to them.

Aftermath

The Royal Commission for the Exhibition of 1851 was granted a supplemental charter on 2 December 1851 to prepare a scheme for the utilisation of the financial surplus generated by the event (First Report, 1852: xviii; Second Report, 1852: 5–8). A site in South Kensington was purchased on which national museums and educational institutions were built (Shears, 2017: 186–226; Hobhouse, 2002: chap 3). The Exhibition building was acquired by the Crystal Palace Company Ltd, removed from Hyde Park and rebuilt at Sydenham. It reopened in 1854 as a place of recreation and amusement. The Crystal Palace, a national symbol of the Victorian age, was destroyed by fire in 1936 (Auerbach, 1999: 200–213; Bird, 1976: 119–133, 144–152).

In spring 1852, the Finance Committee was requested to examine the future conduct of financial business given that Frederick S. Carpenter had ‘expressed his wish to re-join the active service of the Commissariat Department’ (Minutes, 24 April 1852). Carpenter was succeeded as Financial Officer by Captain Owen, who accepted the position without remuneration. Owen continued as Financial Officer until February 1855 when he proceeded ‘to the seat of [the Crimean] war in his capacity of an Officer of Engineers’ (Minutes, 28 February 1855). He was replaced by Henry R. Williams, Accountant to the Board of Trade, at a salary of £100 per annum.

Shortly after the Great Exhibition closed Frederick S. Carpenter was invited, along with a number of eminent personages, to what Henry Cole described as the ‘best dinner in England I have had’ at Baring's house (Henry Cole's Diary, 20 October 1851). Carpenter was reportedly ‘pleased’ to be rewarded for his services as Financial Officer with a gratuity of £1,200 – in addition to his salary of £363 (Carpenter to Granville, 28 October 1851, RC/A/1851/583; First Report, 1852: 155; Henry Cole's Diary, 24 October 1851). By comparison, luminaries such as the Secretaries to the Commission received £1,000 and the iconic civil engineer, Isambard Kingdom Brunel, a member of various Exhibition committees, was awarded a mere £500. Two clerks in the Finance Department received gratuities of £30 and £25 and two Bank of England clerks received £25 each (Report of Finance Committee, 23 October 1851, RC/A/1851/538). The level of additional remuneration to Carpenter and a number of his clerks represent a significant statement about the perceived contribution of the unheralded accounting and finance functionaries to the success of the Great Exhibition.

On returning to the Commissariat service in 1852 Carpenter was posted to Quebec (British Army Despatch, 11.6.1852). In April 1854, he was sent to Dublin but with British participation in the war with Russia he was immediately ordered to Varna, Bulgaria and subsequently to Crimea (British Army Despatch, 21.4.1854, 28.4.1854). Carpenter was one of 12 Assistant Commissaries-General who served in the Crimean War (Third Report from the Select Committee on the Army Before Sebastopol, 1854–55, Appendix 3: 362). In March 1855, following failures in transport and supply to the beleaguered British Army (Funnell, 1990), he was co-signatory of a letter of remonstrance to Lord Palmerston, the Prime Minister, who had implicated the limited energy, intelligence and zeal of the Commissariat service in the unsuccessful campaign (London Evening Standard, 10.4.1855). In 1856, Carpenter was promoted to Deputy-Commissary-General and subsequently served in London and Ireland (Saint James’s Chronicle, 17.1.1856). On retiring as Vice Controller in 1870, Carpenter became a partner in the bank of his father-in-law, Thomas Barnard & Co (Bedford Bank). He died in 1890 (Bedfordshire Mercury, 21.6.1890).

Conclusions

This article has sought to reveal the accounting, control and audit arrangements at the Great Exhibition of 1851 – the inaugurating event in ‘the age of exhibitions’ (Hoffenberg, 2001: xiii). It has attempted to contribute to the demystification of this ‘colossal and evanescent’ event in Victorian Britain by venturing beyond the architectural, cultural, social and political aspects that dominate the literature (Buzard, Childers and Gillooly, 2007: 1; Purbrick, 2001: 21). Akin to the findings of Fabre and Michaïlesco (2010), by analysing international exhibitions, we gain insights not only to the connections between accounting and the state but also to the accounting challenges posed by these singular, high-profile events, and how they were addressed by contemporaries.

Our analysis of the personnel of the Finance and Admissions Department reveals that the ‘triumph’ of the Exhibition depended not only on the interventions of ‘great men’ of the period but also on the efforts of its hidden actors (Shears, 2017: 119). Although the contribution of functionaries such as Frederick S. Carpenter was recognised by the Royal Commissioners in 1851, these actors have been largely invisible in subsequent histories of the Great Exhibition, especially when compared to illustrious personages such as Prince Albert, scientific visionaries such as Henry Cole, and architectural innovators such as Joseph Paxton (Bird, 1976: 3; Fay, 1951: 4, 26–41; Gibbs-Smith, 1950: 5).

The findings of the study suggest that the cash-based accounting arrangements at the Great Exhibition operated without controversy, at a time when there was much debate over the introduction of accruals-based accounting in government departments (Edwards, 2023). The nature of those arrangements was a consequence of the involvement of the Treasury and the appointment of an Assistant-Commissary-General as Financial Officer. The form and content of financial statements produced by Carpenter was consistent with the cash accounting systems prevalent in central government during the focal period. Issues arose as to appropriate reporting periods and the extent and nature of disclosures in the financial statements. Drafting changes were made with an eye to impacts on public opinion, especially as their compilation occurred amidst controversy about the future of the Crystal Palace. Providing assurances to the public also informed the appointment of auditors of the financial statements, even though the extent of the independence of those selected and the depth of their investigations were limited. The approach to external auditing was consistent with contemporary practice. Although more comprehensive internal and external audits of the accounts of the building contractors were performed, these did not completely allay suspicions that secret commercial arrangements laid undiscovered.

The control procedures established by the Finance Committee appear to have been effective in protecting cash assets. The experience of Frederick S. Carpenter as a commissariat officer with responsibility for the ‘military chest’ was put to good use at the Great Exhibition. A comprehensive control environment was created around cash received. This was evident in the application of a supervision principle akin to panopticism in the architecture of the building, the arrangements for admitting the public, and in codified processes for checking cash taken and transporting it to the Bank of England. Although internal controls could come under pressure on ‘one shilling days’, the Financial Officer's detailed accountings of bad coin and season tickets suggest that losses were immaterial.

The study affirms the significance of exhibitions as a site for accounting history research. In addition to exploring the interfaces between accounting, society and culture, the Great Exhibition, and potentially similar large-scale events, present opportunities to examine other accounting phenomena in an unconventional setting. The creation of exhibition buildings may generate evidence of accounting for large-scale construction contracts and their cost management. The erection of such buildings invariably demands the engagement of a substantial but temporary workforce where tight labour control and discipline are essential to meet deadlines. Calculative techniques may also be deployed in the determination, utilisation and division of exhibition space, such that accounting-based allocations may be implicated in the politics of display. Accounting information also features in pricing decisions concerning entry to exhibitions. Neither should we overlook the possibility that accounting-related artefacts might feature at universal exhibitions. At the Great Exhibition, for example, account books, ledgers, writing instruments, counting and calculating machines were displayed, offering insights into the state of the art in calculative technologies.

International exhibitions such as that held in London in 1851 are also conducted in the context of contemporary ideologies that impact on the commercial world. The Great Exhibition, for example, was associated with increasing international understanding through free trade and the pursuit of industrial and social progress (Geddes, 1887: 1). It unleashed debates about the need for more commercial education in Britain and encouraged movements to assimilate the mercantile laws of nations. These were utilised to justify national projects for combining the laws of insolvency in England and Scotland that posed a threat to leading accountants in Edinburgh and Glasgow. In response, in 1853, they formed protective organisations thus bringing the first accountancy bodies in the UK into existence (Walker, 1995). Our analysis of the work of the Financial Officer at the Great Exhibition also demonstrates the diverse arenas in which accounting practitioners could operate during the nineteenth century. Frederick S. Carpenter represents another example of the existence of career pathways in accounting beyond public practice that involves the military (Black and Edwards, 2016). The circumstances attending Carpenter's appointment also enhance our understanding of the military influence on the history of accounting practice.

Footnotes

Acknowledgements

Grateful thanks are due to the reviewers and editor for their valuable suggestions. Helpful comments were also received from attendees at the 14th National Conference of the Italian Accounting History Society. Particular thanks are due to Angela Kenny, Archivist at the Royal Commission for the Exhibition of 1851, for her insights into this article's subject and assistance in locating relevant source material.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.