Abstract

This article compares Australian and UK approaches to regulating financial reporting from 1971 to 1985. Primary sources include accounting standards from both nations, alongside reports and commentaries from the bodies responsible for regulating financial accounting. This article finds that despite shared history and similar external pressures, the accounting professions in Australia and the UK diverged in their approaches to financial accounting regulation, with this divergence being manifested in both the content and enforcement of accounting standards. This divergence was found to have commenced from the release of the first accounting standards in the early 1970s. This study adds detail to the common categorisation of Australian and UK financial reporting found within the comparative international accounting literature and has relevance to contemporary practice, as many of the factors associated with these differences still exist today.

Introduction

In 1985, Nobes and Parker (1985: 58) stressed that ‘the issue that transcends all others in the affairs of the accounting professions in Britain and Australia in the past 15 to 20 years is that of accounting standards’. The UK's standards took the form of ‘Statements of Standard Accounting Practice’ (SSAPs) and were first released in 1971 by the Accounting Standards Steering Committee (ASSC), while ‘Australian Accounting Standards’ (AASs) were first released by the Australian Society of Accountants (ASA) and the Institute of Chartered Accountants (ICAA) in 1973. This article endeavours to answer the questions: What was the extent of difference between UK and Australian financial reporting regulation from the 1970s to the mid-1980s, and what factors in the context of financial reporting within these two nations can be linked to these differences? To answer these questions, this study draws on the content of accounting standards, reports from the bodies responsible for regulating financial accounting, as well as secondary sources. Given the interest in context, this article also identifies factors impacting on and running parallel to financial reporting in each country in the years either side of the period in focus (1971–1985).

There are several motivations for this topic of research. The first is to explore the detail underlying the ‘Anglo-American tradition’ (Nobes and Parker, 2020: 72), ‘practiced in the UK, and other countries where the UK has had a major colonial influence’, 1 where the main purpose of financial accounting is to provide useful information for participants in capital markets (Street and Shaughnessy, 1998: 180). Within comparative international accounting (CIA) research from the period (e.g., Doupnik and Salter, 1993; Frank, 1979; Nair and Frank, 1980, 1983; Nobes, 1983), 2 Australia and the UK were usually classified together. Despite this apparent similarity, in 1982, Robert Parker delivered an address to New South Wales (NSW) division of the ASA titled ‘Why Are Australian Accounting Standards Different?’ (Parker, 1982) which concluded that Australian accounting standards should be distinct from other countries due to it being ‘no longer appropriate to follow British standards and it is not appropriate simply to substitute the United States in Britain's former place’ (Parker, 1982: 429). The key motivation for this article, then, is to explore the historical record to shed light on the gap between the aforementioned classification studies (e.g., Nobes, 1983) and the glimpse of the comparative state of Australian and UK financial reporting alluded to in Parker's (1982) address. This gap points to the possibility that differences in accounting standards existed, which (a) may not have been pervasive enough to register within classification studies and (b) may have been relatively minor compared to differences in financial reporting between other countries, but nevertheless had ramifications for the preparation and analysis of financial reports in each country. By exploring the full extent of these differences alongside the contextual factors around them, this study answers calls for accounting histories to ‘challenge or overturn… beliefs’ (Parker, 2001: 63) and to ‘re-examine extant explanations’ (Stewart, 1992: 57). Specifically, this article aims to add nuance to the presumption that, based on various CIA classification studies, Australian and UK financial accounting systems were relatively homogenous, or at least appeared so when compared to the financial accounting practices of other nations.

A methodological contribution of this article relates to its longitudinal nature. The aforementioned classifications of comparative international financial reporting systems have provided static views of comparative practice and have relied on survey data, observations of actual practice, opinion, or characteristics like type of economic system, dominant forms of business organisation, commercial legal structure, language and culture to distinguish between different countries and to group families of nation states by frameworks of practices. These efforts have been criticised, however, for being based on questionable data and for producing incoherent taxonomies based on an elusive search for generalities (Roberts, 1995). By way of contrast, the position adopted in this article is that there was a progressive and dynamic divergence between the financial accounting systems of Australia and the UK, requiring a longitudinal analysis to fully capture the underlying nature and causes of the distinctions.

This research also complements single-country studies on the development of financial reporting, such as Carlson (1994) and Morris and Barbera (1990), who examined the development of financial reporting in Australia, and Napier (2010), who explored the UK. Also, by examining all accounting standards from 1971 to 1985 and the context of their development, this research contrasts with studies which have focused on specific accounting standards or principles such as MacArthur (1993) who compared the development of standards for pension funds in the USA and the UK, Horton and Macve (1994) who looked at accounting regulation related to life insurance in the UK and Burrows and Rowles (2010) who compared Australian and UK developments related to inflation accounting.

This study also engages with the accounting history literature by adding to the body of scholarly work on comparative international accounting history (CIAH) (Baker, 2014; Buhr, 2012; Carmona, 2006; Carnegie, 2014; Carnegie and Napier, 1996, 2002; Carnegie and Potter, 2000; Gomes, 2008; Maran and Leoni, 2019; Napier 2001; Walker, 2008). By engaging with the CIAH framework, this research serves to illustrate that ‘accounting in any country is not the outcome of invention within a single country or culture but rather the outcome of innovations in many places across centuries’ (Carnegie and Napier, 2002: 689).

This article is structured as follows. The first section explores the prior literature for the purpose of clarifying what is known and what remains unknown about the comparative states of Australian and UK financial accounting in the 1980s. The second section provides an outline of the CIAH framework as proposed by Carnegie and Napier (2002), how it relates to the context of this study and the sources used. The fourth section provides a narrative of the comparative history of UK and Australian approaches to financial reporting, beginning by exploring the historical context of standard setting before focusing on the years 1971–1985. The fifth section summarises the key events using the dimensions of the CIAH framework, responds to the research questions and provides some concluding thoughts on the relevance of the findings to contemporary practice and suggestions for future research.

Literature review

The purpose of this section is to outline what is known about the relative states of financial accounting regulation within Australia and the UK in the 1970s and 1980s and clarify the purpose of this research. Within the comparative international accounting literature of the period (including Doupnik and Salter, 1993; Frank, 1979; Nair and Frank, 1980, 1983; and Nobes, 1983), Australia and the UK financial reporting systems were usually classified together. 3 For example, Frank (1979) grouped Australia and the UK together (out of 46 nations) for both measurement and disclosure practices, while Nobes (1983: 12) classified Australia along with New Zealand and Ireland as countries that were ‘UK influenced’. Nobes (1983) also found that Australian and the UK financial reporting practices were the second-most similar (after Australia and New Zealand) out of a group of 14 countries based on nine factors. 4 The common classification has been attributed to colonial influence 5 – (see Nobes and Parker, 1985), the immigration of accountants from the UK to Australia (Carnegie and Parker, 1996; Carnegie et al., 2000, 2006; Goldberg, 1977, 1984) and the influence of the UK's accounting profession within Australia and other Commonwealth nations (see Chua and Poullaos, 2002 or Johnson and Caygill, 1971).

Countering these classification studies was a speech delivered by Robert Parker in 1982 (Parker, 1982) to the NSW division of the ASA titled ‘Why Are Australian Accounting Standards Different? Parker (1982) 6 stated that the focus of his attention was Australian differences with the standards of other countries, and referred to the work of Nobes (no date was provided) as stating that Australian financial accounting standards were most like New Zealand's and the UK's (these findings concur with Nobes, 1983) before calling for greater collaboration between Australian standard setters and those from Canada and New Zealand. Parker (1982) also provided some comparison between Australian and UK accounting standards as they were in 1982, stating that he first noticed differences in 1981 when he came to Australia to teach. Parker (1982) provided a table which compared the topics of Australian and UK standards from 1982 with a brief comment that there was scope for difference between standards of the same topic, such as inventories and tax effect accounting (Parker, 1982: 426), also noting that Australia lagged the UK on tax effect accounting but led the UK on accounting for extractive industries.

Parker (1982) also provided a brief outline of the history of Australian adoption of UK company law, and discussed the relative merits for Australia in simply adopting standards from the USA and Canada. Parker (1982) largely dismissed the relevance of International Accounting Standards Committee (IASC) standards for Australia, arguing that they were unknown to Australian accountants and were only relevant to multi-national companies. Parker's (1982) conclusion was that Australia was best served by developing its own accounting standards, and that these standards should adopt the best practices of the UK, the USA, New Zealand and Canada.

While Parker (1982) touches on similar issues to those addressed in this article, this research aims to build on Parker's (1982) findings in several ways. Firstly, Parker (1982) was principally concerned with the issue of the future direction of Australian accounting standards, with historical issues only provided for context. This article, by contrast, is fundamentally historical in focus and broader in scope, examining various aspects of financial reporting, including standards, conceptual framework development and shelved standards on inflation accounting.

Secondly, Parker (1982) delivered a speech to an audience comprised of members of the ASA, and at the time of writing, the text is only accessible via archives holding copies of the Australian Accountant from the 1980s. Given the audience and the nature of the address (a speech), Parker's (1982) comparison of UK and Australian accounting standards is relatively brief, essentially limited to a table comparing standards by topic. This article expands on this analysis by making the comparison in 1985 (during which time four new UK standards were released, along with 13 Australian standards), along with standard-by-standard examination of the approaches to development, structure, dates of release and provisions concerning disclosure and measurement (see Tables 1–4). This granular comparison is done to extend understandings beyond a binary notion of whether Australian standards were different, to instead substantiate the extent of difference. Thirdly, Parker (1982: 429) concludes by saying: Australian accounting standards are justifiably different from those in other countries because Australia is different from those other countries. It is no longer appropriate to follow British standards and it is not appropriate simply to substitute the United States in Britain's former place.

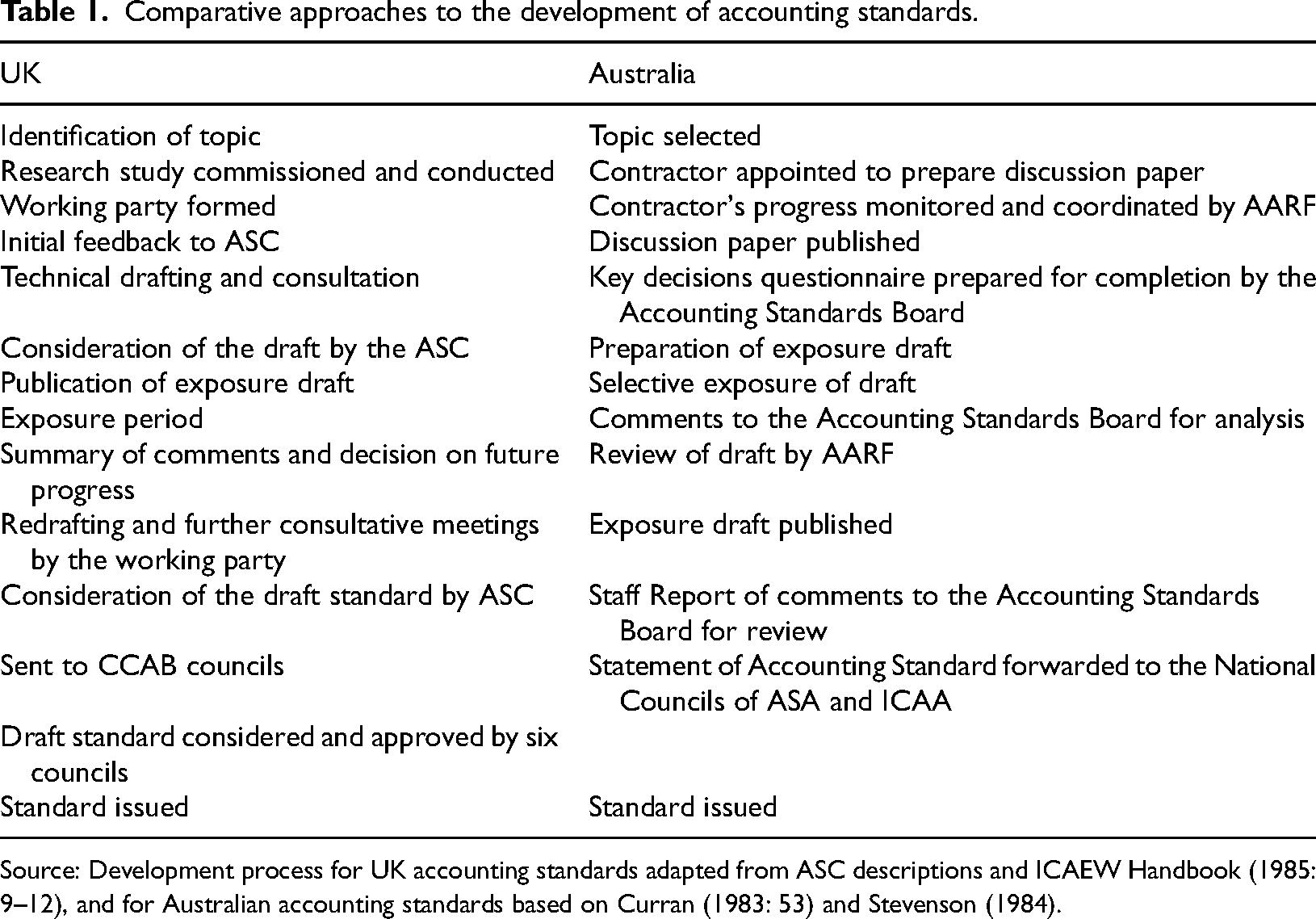

Comparative approaches to the development of accounting standards.

Source: Development process for UK accounting standards adapted from ASC descriptions and ICAEW Handbook (1985: 9–12), and for Australian accounting standards based on Curran (1983: 53) and Stevenson (1984).

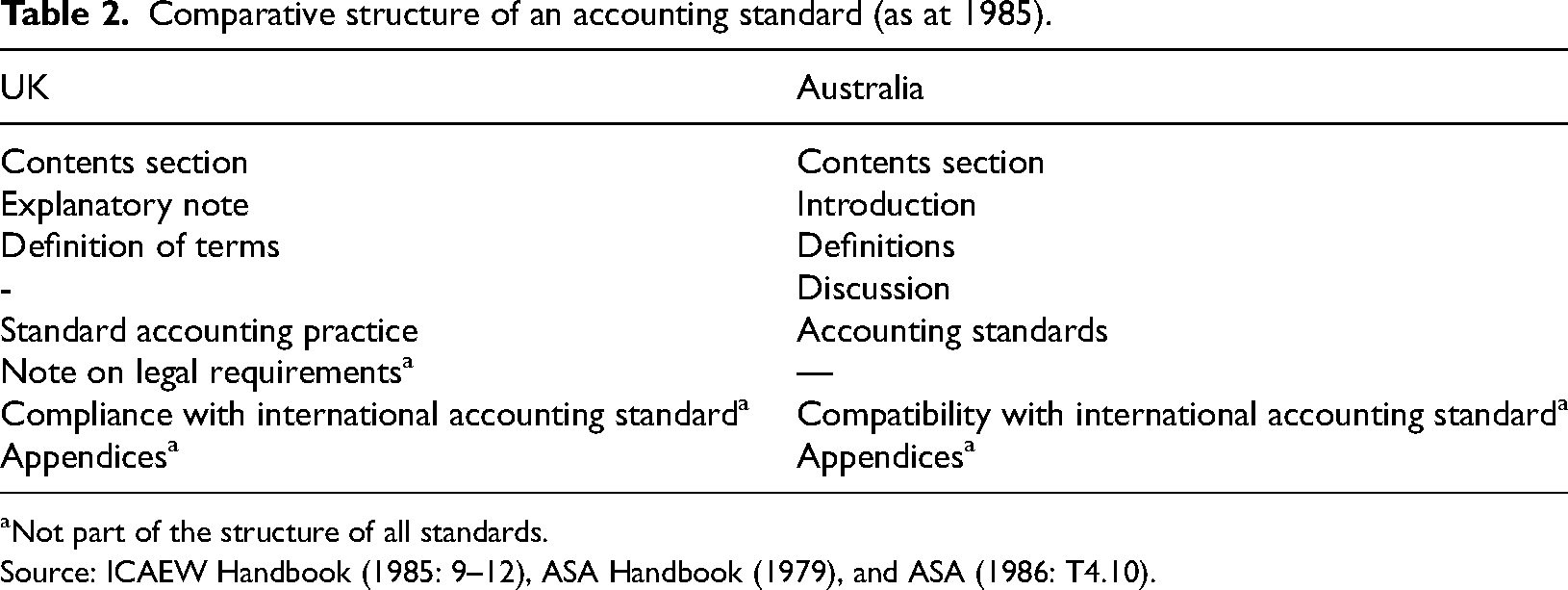

Comparative structure of an accounting standard (as at 1985).

Not part of the structure of all standards.

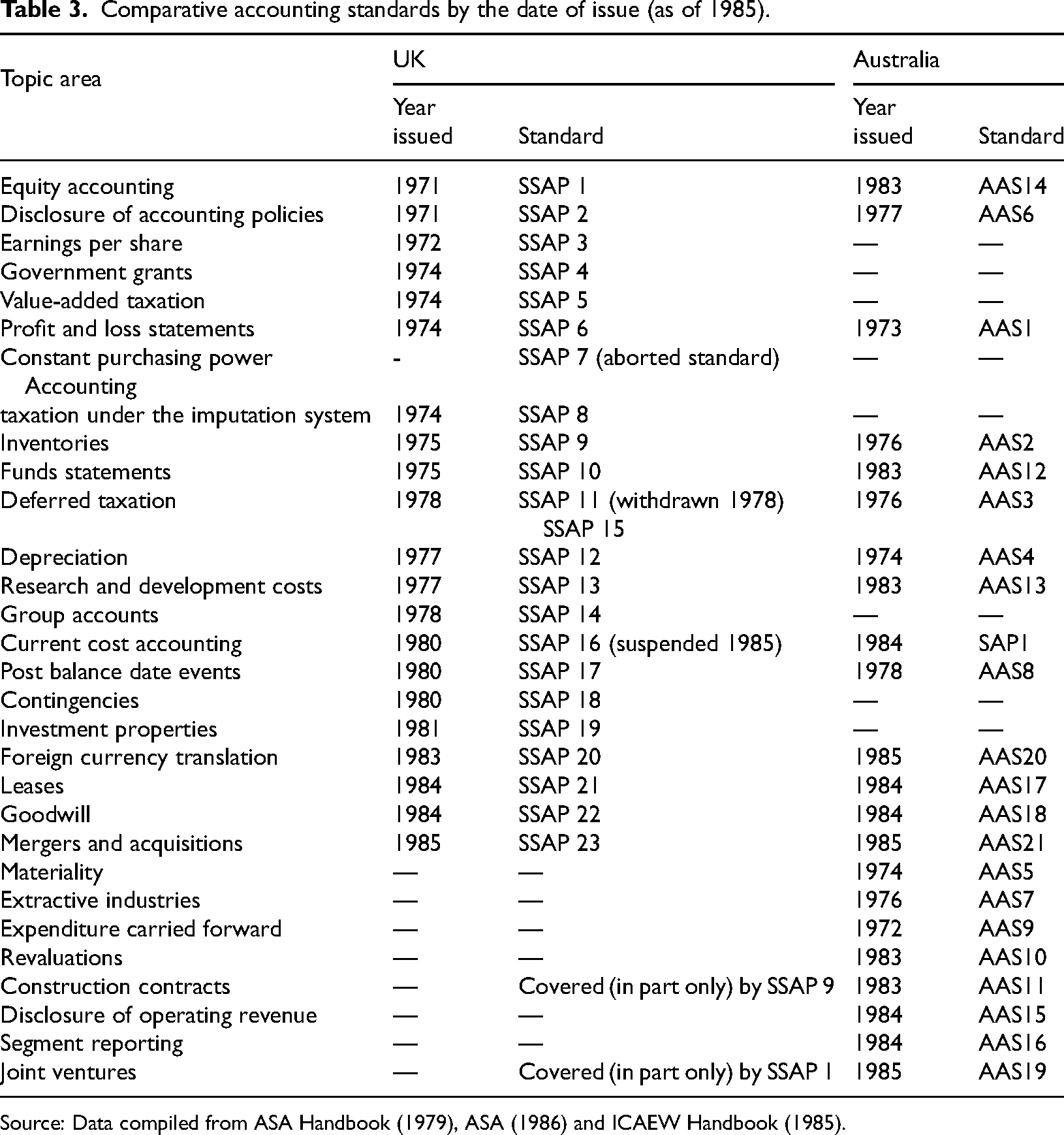

Comparative accounting standards by the date of issue (as of 1985).

Source: Data compiled from ASA Handbook (1979), ASA (1986) and ICAEW Handbook (1985).

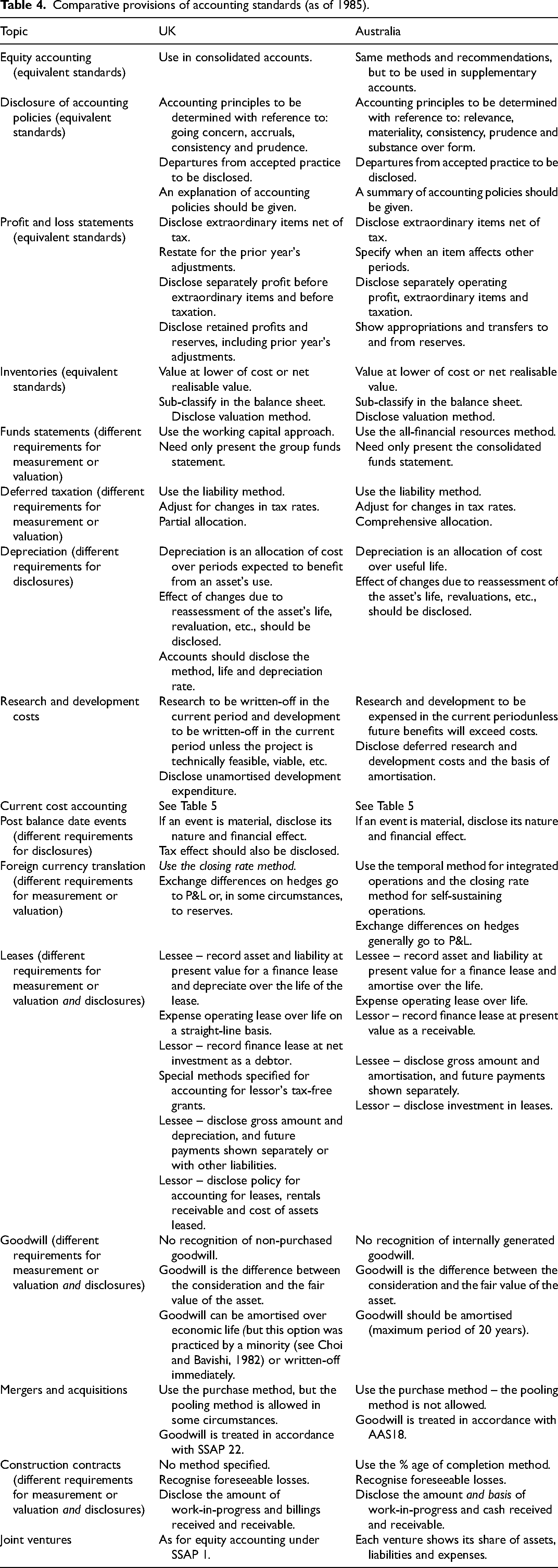

Comparative provisions of accounting standards (as of 1985).

As can be seen, this conclusion does not provide any elaborations on the nature of Australia's differences – it simply states Australia ‘is different’. This article aims to contribute to this understanding of Australia's differences by comparing the impact of inflation, corporate collapses, the state of the accounting professions and the role of Government in Australia with those of the UK.

In sum, while Parker (1982) found that UK and Australian standards were different, this article expands on this by exploring the full extent of the difference. In doing this, it adds to understandings of the comparative international accounting literature by fully elucidating what the common categorisation of countries such as Australia and the UK means for the detail of financial reporting. This article also builds on Parker (1982) by attempting to explain these differences by looking at the factors at work in the historical context of both Australia and the UK.

Comparative international accounting history

CIAH has been described by Carnegie and Napier (2002: 693–4) as ‘the transnational study of the advent, development and influence of accounting bodies, conventions, ideas, practices and rules’, with the aim being to ‘identify, explain and interpret differences and similarities between phenomena in different contexts’ (Carnegie, 2014: 1245). Maran and Leoni (2019: 13) refer to CIAH as ‘a rather flexible tool that can fit different contexts or objects of investigation’. CIAH's have examined a range of issues, including the evolution of cost accounting in France, Portugal and Spain (Carmona, 2006), the development of the auditing profession in the UK and France (Baker, 2014), the differences in approaches to earnings management in Italy and the USA (Leoni and Florio, 2015), the implementation of accrual accounting in five ‘Anglo-American’ countries (Buhr, 2012) and the development of financial reporting and corporate social responsibly (CSR) reporting (Tschopp and Huefner, 2015). To date, CIAH has not been used as a means of comparing financial accounting systems.

Carnegie and Napier (2002) identified seven dimensions of CIAH: period, places, people, propagation, practices, professions, and products. In relation to period, Carnegie and Napier (2002) noted two modes of analysis: synchronic (where accounting in different parts of the world is compared at a given point in time) and parallel (where a period is selected and accounting practices in different countries are compared over that period). This study can be classified as parallel, given its longitudinal nature. Carnegie and Napier (2002: 700) also noted that period selection ‘may impose unarticulated cultural assumptions as to key turning points in broader political, social and economic history’. In terms of articulating these ‘assumptions’, 1971 was selected as the opening year because this was when the first accounting standard was released in the UK, with Australia following in 1973. 1985 was chosen as the endpoint because in 1984, the Australian Accounting Standards Review Board (ASRB) began to review AASs for the purpose of providing statutory backing as per Australian companies’ legislation, 7 commencing its full mandate in 1985. By this time, the EEC's (European Economic Community) fourth directive on company law had been incorporated into the UK Companies Act (in 1981), resulting in significant changes to British company law and accounting practices (Bartlett and Jones, 1997). These two factors significantly modified the relationships between the profession and the state in differing manners and were thus deemed to provide an appropriate endpoint for this study.

It should be noted that events occurring in the years either side of the focal period are also examined to provide context. For example, factors leading to the regulatory arrangements that prevailed between 1971 and 1985 are outlined. It should also be noted that while standards were first introduced in the 1970s, the first major professional accounting principles were issued decades earlier. All told, factors dating back as far as 1853 (the origins of professional bodies) and as late as 2020 (the UK's departure from the EU) are mentioned.

Place within CIAH's is most often conceived of as being the nation state (Carnegie and Napier, 2002). The UK and Australia were selected for comparison because of the inconsistency between the numerous comparison studies (e.g., Doupnik and Salter, 1993; Nobes, 1983), which categorised Australia and the UK together, and Parker's (1982) address to the NSW branch of the ASA, which alluded to the existence of important differences.

Analysis of people can involve comparisons of who the accountants were at a particular point in time and who they served (Carnegie and Napier, 2002). The role of specific individuals is not the focus of this article 8 – instead, the analysis of people is encompassed within the role of groups – the accounting professional bodies from the UK and Australia – involved in regulating financial accounting, the motivations of these groups and their target audiences.

Through propagation, CIAH's explore how accounting ideas formed and spread, whether ideas originated from outside or within each country and the nature of the channels through which accounting ideas flowed (Carnegie and Napier, 2002). In the context of this article, Australia's inheritance of the UK legal system and the prevalence of corporate and related accounting failures are examined in terms of their roles in influencing the spread of financial accounting regulation in Australia and the UK.

According to Carnegie and Napier (2002), exploration of practices involves asking what counts as ‘accounting’, and for this study, the focus is on the regulation of financial accounting. This article, therefore, compares the accounting standards of the two nations (ASA, 1979 – updated to 1985 for Australia, and Institute of Chartered Accountants in England and Wales – ICAEW, 1985/6 for the UK) to substantiate the extent of divergence. This article also compares responses to the emergent regulatory issues and the inflation accounting conceptual framework development.

Analysis of professions encompasses the activities of groups of accountants and the importance of professional status for these activities (Carnegie and Napier, 2002). For this study, analysis of professions primarily involves comparison of the collaboration activities and attempts at integration/mergers of Australian and UK accounting professional bodies, with this providing context for analysis of the relative approaches to financial accounting regulation.

Lastly, the dimension of products refers to the things that the accounting produced in each country, including whether accounting fell under the gaze of regulators (Carnegie and Napier, 2002). The dimension of products involves a comparison of the eventual state of the financial accounting regulations in each country as they existed in 1985 in addition to some discussion of the periods following.

Primary sources, mainly originating from the professional and regulatory bodies of each country, form the basis of this study. ASA (1966), ASSC (1970) and ICAEW (1970) are reports from the accounting professions in Australia and the UK that provided elaborations on the rationale for the shift towards accounting standards. The comparison of accounting standards from 1985 was performed using ASA (1979 – updated to 1985), and ICAEW (1985/86) – the accounting standards for each country. Additional primary sources include the Report of the Inflation Accounting Committee (1975), Accounting Standards Committee (ASC) (1977) and Chambers et al. (1978), which outlined the UK Government's, the UK accounting professions’, and the New South Wales Governments’ plans for inflation accounting standards, respectively. Also examined were ASSC (1975), Barton (1982) and Department of Trade (1977a, 1977b), which addressed UK and Australian approaches to conceptual framework development. ASC (1981) was a report on the state and future of accounting standard setting in the UK, which covered a range of issues relevant to EEC membership, including the impact on conceptual frameworks and the future of standard setting. Lastly, a joint submission by the two Australian professional bodies on the development of the ASRB from 1982 was examined, as was the Australian Accounting Research Foundation (AARF) (1986), which was used as a source for analysis of Australia's use of non-mandatory guidance statements. While these primary sources form the basis of the study, secondary sources, primarily originating from the accounting literature, were also used to provide context around the evidence gathered from the primary sources.

Comparative history of UK and Australian approaches to financial reporting

Financial accounting regulation before the standards

Before the existence of codified accounting principles and standards, financial accounting regulation in both Australia and the UK was the remit of company law, which placed boundaries on the accounting profession through mandatory disclosure rules. Within the CIA literature, is has been noted that ‘colonizing countries usually bequeath their legal system… to their colonies’ (Nair and Frank, 1980: 438) and several authors have identified that UK company law spread to Australia through a process of adoption and transcription of British statutes (see Kavass and Baxt, 1970 or Parker, 1986a; Parker and Morris, 2001). According to Parker (1986a: 85), this spread of British company law to Australia held true until ‘the very end of the nineteenth century’, although Kavass and Baxt (1970: 8) and Parker and Morris (2001: 300) put this date later, arguing that in the 1950s 9 and 1960s, Australian companies’ acts still adopted British law. The influence of precedent from judicial decisions in the form of case law concerning accounting principles (Reid, 1988) was also important for accounting in both countries, given that the right of appeal to the British Privy Council remained open to Australian entities until 1986. 10

While company law set parameters for financial reporting, the regularity of corporate abuses in both countries provided motivation for both Australian and UK accounting professions to evaluate why and, codify how financial reports should be prepared (Edey and Panitpakdi, 1956; Zeff, 1972: 1). According to Parker (1986b: 81) the UK was ahead of Australia in this regard as the more mature professional bodies in the UK, unlike their developing Australian counterparts, recognised the need for increased disclosure regulation as early as the 1930s and 1940s. 11 The Royal Mail case of 1931 in the UK, ‘was followed by considerable questioning by accountants about the desirability of explicit, common professional standards’ (Birkett and Walker, 1971: 97). Other failures included the collapse of Rolls Razor Ltd in 1964 and the GEC-AEI takeover battle of 1967 (Rutherford, 1996; Zeff, 1972: 33). Similarly, Australia experienced several corporate failures including those of Cambridge Credit, HG Palmer and Westmex (Clarke and Dean, 2014), and ‘as in the UK, the Australian profession was held partly responsible in many quarters’ (Parker, 1986a: 86). The reaction by the Australian and UK accounting professions to these collapses was similar (ASA, 1966; Birkett and Walker, 1971), with Zeff (1973: 54) noting that ‘criticism in the financial press (in Australia), as in … England, has been a portent factor in accelerating the efforts of the accounting profession to review its professional standards’. Maintenance of the legitimacy of professional bodies was also cited by Carnegie and O'Connell (2012) as a key motivating factor.

The first ‘Recommendations on Accounting Principles’ were issued in the UK by the ICAEW in 1942 ‘to provide direction and guidance for their members within the general framework of the Companies Acts’ (Oldham, 1975: 61). In contrast to accounting standards however, they ‘were only persuasive and companies and auditors did not have to report whether or not they had been followed’ (Parker, 1986b: 81). In Australia, the two main professional bodies adopted, almost entirely, the UK's statements of accounting principles. This practice of wholesale adoption began in 1946 with the ICAA's initial promulgations retaining the substance and detail of pre-existing English recommendations (Zeff, 1973: 3), such that ‘in the 1940s (the) first attempt to provide members with guidance … reflected an almost total reliance on English precedent’ (Zeff, 1973: 23), to the extent that: if there was to be … [a pronouncement] they wanted a word-for-word transcription of the English one. The seven Australian recommendations issued in 1946 and 1948 followed the equivalent English ones very closely. (Parker, 1982: 427)

Australian releases were also titled ‘Recommendations on Accounting Principles’, and dealt with the treatment of taxation, disclosure of subsidiaries’ results in holding company accounts, accounting for reserves and provisions, and the form and content of the balance sheet (Levy, 1986: 43). While some nuance between Australian and UK principles had developed prior to the release of accounting standards (e.g., Australian balance sheet recommendations showed some departures from the UK recommendations), as late as 1967, the ICAA was still using ICAEW publications, such as the ‘Qualifications in Auditors Reports’ guidelines (Birkett and Walker, 1971).

While the primary driver of the development of accounting principles in the UK, and their spread to Australia, was the desire to improve financial reporting – ‘accounting rules were … codifications of what accountants regarded as best practice’ (Evans, 1974: 64) – the ad hoc nature of this approach, and subsequent press criticism for inadequate responses by the profession to reduce variation in financial reporting (Jones, 2011: 129) led the ICAEW in 1969 to issue a ‘Statement of Intent on Accounting Standards in the 1970's’ to set an agenda for future UK standard setting. Nobes and Parker (1985: 58) also stated that ‘the move to standard setting in both Britain and Australia occurred in response to what were widely regarded as damaging examples of misleading annual accounts and sustained hostile criticism of the profession, particularly by sections of the media’.

The subsequent findings of an ICAEW (1970) commissioned survey of annual reports for 1968–69 revealed continued variations in accounting treatments and disclosures, which reaffirmed the profession's commitment to its ‘Statement of Intent’, as supported by ICAEW President R.G. Leach's comments appearing in The Accountant (1970a, 1970b). The ASSC 12 was then established in 1970 by the ICAEW 13 following the issue of the ‘Statement of Intent’, which was established by the ICAEW. The ASSC wanted to narrow the variety in accounting practice, improve disclosure of accounting bases, and make explicit disclosure of ‘departures from established definitive Accounting Standards’ (Oldham, 1975: 61).

While no equivalent prospectus was devised in Australia, the solution to the problem of variation in financial reporting practices resulted in virtually the same general pattern as in the UK. The ICAA established an accounting principles committee in 1969, and in 1970, the ASA agreed to use the AARF to communicate with the ICAA for the purpose of releasing joint standards and working on future standards. This was manifested in the ASA's endorsement of ICAA pronouncements on profit and loss statements and depreciation in 1972 (Zeff, 1973). The consequence of this collaboration was that limits were placed upon the diversity of condoned practices and attempts were made to ensure the disclosure of accounting bases and any departures from established standards (Evans, 1974: 70). The first AAS's issued by the two professional bodies followed in 1973, and compliance with AAS's was required by members through the code of ethics (Howieson, 2017: 134).

UK entry into the European Economic Community

A key factor that impacted the UK's approaches to financial reporting regulation was its entry into the EEC. The UK applied to join the EEC in 1960 and was admitted as an observer in 1971, becoming a full member approximately 12 months later. The EEC (later to become the European Union [EU]) was a body for common markets, trade, and policies and was composed of nations such as France, West Germany, Italy, and the Netherlands.

The UK's entry into the EEC impacted upon trade relations, company law and financial accounting. 14 The most relevant EEC directive for accounting was the fourth directive on company law, which was incorporated into UK company law in 1981. The specific impact of the fourth directive, according to Bartlett and Jones (1997: 61), was that ‘mandatory disclosure (in the UK) increased sharply’. The fourth directive also prescribed formats for financial statements and the measurement of assets, making ‘explicit the primacy of historical cost valuation rules’ despite high rates of inflation in the 1970s and 1980s, reinforcing the stewardship function of accounting (Bromwich and Hopwood, 1983: xvi). Most EEC members apparently preferred existing norms and more traditional objectives of financial reporting.

The adoption of EEC directives ultimately led to conflict between the Government and the accounting profession in setting accounting standards for the UK. The UK Department of Trade took on the ‘role of guardian of the fourth directive’ (Bromwich and Hopwood, 1983: xvi-xvii) and provided resistance to the ASC (the successor to the ASSC). For example, the Department of Trade resisted an ASC exposure draft on foreign exchange because the fourth directive stressed the primacy of prudence and objectivity in accounts. Bromwich and Hopwood (1983: v) concluded that the effect of the EEC was to increase ‘continental European influences on British accounting and seem[s] likely to restrict the future freedom of standard setting in the UK’. By way of contrast, Australia had no regional affiliations impacting on corporate law, so Parker's (1982) comment that Australian standards were different can be complemented with the finding that UK financial accounting regulation was changing due to its membership of the EEC.

The state of the professions in Australia and the UK

In both Australia and the UK during the focal period, the setting of financial accounting standards was the purview of members of the professional bodies. The UK was the first country to establish an independent, non-state professional accounting association 15 in 1853 (Lee, 1995; Walker, 1988, 1995), with Australia following in 1886 with the Adelaide Society of Accountants (Carnegie et al., 2000). 16 In Australia, the two main bodies (ICAA and ASA) coordinated their standard-setting activities both through a Joint Standing Committee, which represented the executives of both bodies (Ryan, 1998) and through the AARF. By contrast, in the UK, there were five bodies (with another in Ireland) 17 which co-ordinated areas of common concern and interactions with the UK Government through the ‘Consultative Committee of Accountancy Bodies’ (CCAB), which was established in 1974 (Nobes and Parker, 1985: 50).

Many of the key standard-setting activities of the professional bodies in both nations thus involved collaboration between these separate bodies. Collaborative arrangements for standard development in Australia predated those in the UK, with collaboration between Australia's two main professional bodies leading to the establishment of the AARF – a joint body of the two main professional accounting bodies established initially as the Accounting Research Foundation (ARF) in 1965. The AARF's role was to undertake research and prepare and issue statements on accounting principles, and it encompassed two further standard-setting bodies, the Accounting Standards Board (AcSB – established in 1978), which addressed private sector standards, and the Public Sector Accounting Standards Board (PSASB). Linking back to the role of corporate collapses, Burrows (1996: 10–11) argued the AARF was a response by the profession to the ‘fragmented and contentious’ nature of accounting principles, the collapse of ‘supposedly profitable companies’ and the appearance of a ‘deficient’ and ‘incompetent profession’. Formal collaboration of the UK bodies for standard setting did not occur until the formation of the ASSC in 1970.

A consequence of these fragmented arrangements was that the merging of professional bodies was an ongoing project in both nations. The UK professions attempted professional integration in 1971 and failed, while unsuccessful endeavours were made in Australia in 1969, 1981–82 and again in 1998. In terms of standard setting, the consequence of the failed 1971 merger attempt for the UK was said by Nobes and Parker (1985: 50) to have been a ‘a rather uneasy co-ordination… through the CCAB’. Further failed merger attempts occurred in 1989, 1990, 1996, 2004, and 2005 (see Noguchi and Edwards, 2008). In assessing the failed merger attempts of the Australian professional bodies, Willmott (1986) and Velayutham and Rahman (2000) revealed a commonality with the UK in that sectional interests contributed to the failures – members of Chartered bodies in both nations exhibited a preference for protecting their status over unifying the profession.

The fragmented nature of the accounting professions in Australia and the UK is relevant to the political nature of the setting of accounting standards (see Gerboth, 1973; Solomons, 1978). In the UK, this political process took place among six bodies, with lobbyists needing to direct their attention to numerous bodies, stating their cases (Rutherford, 2007), with these bodies then needing to compromise. In Australia, with only two main professional bodies, consensus was more easily achieved.

Comparison of standards, conceptual frameworks and inflation accounting

This section compares the standards issued by the respective professional bodies of each country between the period of 1971 and 1985, substantiating just how ‘different’ (Parker, 1982) Australian standards were from those of the UK. The analysis of sources revealed that two other issues emerged during the period alongside standard development – attempts at developing a conceptual basis for accounting standards, and inflation accounting, and these issues are also analysed.

Points of contrast for standards emerge with the first choice of topic. The UK profession's first formal accounting standard, released in 1971, dealt with ‘Accounting for the Results of Associated Companies’ (SSAP 1). According to Leach and Stamp (1981: 6), this choice of issue was ‘highly controversial’, opened ‘entirely new ground’, and was motivated by the problem that ‘there was no established practice for providing for the proportionate share of losses or of profits…’ (for associated companies). Two years later (in 1973), the first AAS was released concerning the determination of profit and disclosures in Profit and Loss Statements (AAS1) (Walker, 1987). An Australian standard comparable to SSAP 1 was not produced until 12 years later (in 1983).

Table 1 offers a description of the practices underpinning the development of a standard in the UK and Australia, while Table 2 identifies the comparative structure of standards. Both tables illustrate that Australian and UK standards had many similarities, both in due process and configuration. There is, however, a notable difference in relation to structure, as UK standards required a ‘Note on Legal Requirements’ which detailed the various sections of company law that would be complied with if the standard was followed. This note was prompted by the UK's membership of the EEC. Another example of the consequences of the UK's membership of the EEC can be seen with SSAP 15, which specified the presentation of deferred taxation for each allowable balance sheet format, given that such formats had also become part of UK company law because of EEC membership. Many ‘Notes’ also discussed discrepant treatments for satisfying the differing statutory requirements of the UK and Ireland.

Table 3 compares the stated topics and release dates of SSAPs and AASs through to 1985. During the period under consideration, 21 AASs existed alongside 20 SSAPs (the ICAEW handbook from 1985/86 shows that there were 23 standards, but three of these were withdrawn between 1978 and 1985 18 ). Of note is that across the collective standards of the UK and Australia, 29 topics were identified, yet only 15 (52%) were common to both countries. Further, two of the UK standards appear twice. For instance, SSAP 1 concerned equity accounting and, in part, joint ventures, while there was an individual AAS standard for each topic. There were also variations between standards that ostensibly dealt with the same topic. SSAP 1, for example, caused revaluations in assets and earnings, while AAS 14 did not. Also, contrary to the established pattern of Australia adopting financial reporting systems from the UK, for the dates of issue (see Table 3) for the 15 common topics, in six instances (40% of cases), the promulgation of a standard in Australia pre-empted its UK equivalent.

Based on the presumption that accounting standards are generally set to address issues of importance, it becomes apparent that different conditions and characteristics within each country were flavouring the accounting standards. For example, the tax system in the UK was distinct, so standards on value-added tax and taxation under the imputation system had no relevance to Australia. Industrial differentiation in each nation also led to specific standards in Australia on construction contracts and extractive industries, and on accounting for government grants in the UK, as well as varying ideas and emphases on disclosures, giving rise to operating revenue and segment reporting standards in Australia, and earnings per share disclosures in the UK.

Table 4 provides more detail on these differences through an analysis of the specific provisions of recommendations within the 15 standards with common topics. Of these, only four standards (27%) used equivalent terms for both measurement requirements and provisions for related disclosures. These comparable standards were for profit and loss statements, inventories, disclosure of accounting policies, and equity accounting. In three of these cases, the UK standard was released earlier than the Australian standard. While there was only a variance of a few months in the dates of publication on profit and loss statements (December 1973 for Australia and April 1974 for the UK) and inventories (May 1975 in the UK and February 1976 in Australia), several years separated the release of the standards dealing with the other two areas.

Further differences between Australian and UK standards can be found with six of the 15 standards (40%) presenting different recommendations concerning disclosures and, most significantly, nine standards (60%) having differences regarding measurement methods. The most notable in this latter category are those on funds statements, research and development expenditure and, to a lesser extent, joint ventures, mergers and acquisitions, and construction contracts.

It is telling that when the detailed provisions of accounting standards are scrutinised, there is little relationship between the more fundamental measurement practices recommended in standards, given that only four genuinely comparable and equivalent standards existed. This would suggest that the common categorisation of Australia and the UK in terms of financial accounting practices – while no doubt being valid in relative terms (i.e., Australian and UK financial reporting was similar relative to other countries) – nevertheless overlooked significant differences that only a granular analysis of accounting standards can reveal.

Conceptual frameworks

Another target for the profession's efforts in regulating financial reporting in both countries between 1971 and 1985 was the development of conceptual frameworks. In the UK, despite the release of numerous SSAPs since 1971, a governmental Green Paper in 1977 on ‘The Future of Company Reports’ (Department of Trade, 1977a, 1977b), together with an earlier ASSC (1975) publication titled ‘The Corporate Report’, reignited concerns within the accounting profession about the need for conceptually driven accounting standards. The objectives of accounting were also shifting towards the inclusion of more decision-useful information, so work began on a conceptual framework that would provide the basis for accounting standards and include prescriptive qualitative characteristics of financial information. Developments in the UK preceded those in Australia, with the ASSC (1975) discussion paper identifying the qualitative characteristics of relevance, reliability, understandability, comparability, completeness and objectivity. ASSC (1975) was met with resistance from the business community, however, mainly due to its proposal for increased disclosure requirements (Peasnell, 1982).

Noting the resistance of the business community in the UK, Deputy Chairman of the National Companies and Securities Commission in Australia (Coleman, 1981: 536) stated that ‘the difficulty of forming a conceptual framework for such standards has been amply demonstrated in the United Kingdom’. The Commission was anxious that this should not be the Australian experience, too. Sponsored by the AARF but not released until several years after its UK counterpart, the Australian version of a draft framework (Barton, 1982) outlined the essential characteristics of relevance, reliability, understandability, and comparability. It was argued that three of the criteria in the UK listing would be met if information was relevant and reliable, such that completeness and objectivity were seen as inherent dimensions of reliability, while timeliness was a latent aspect of relevance.

With respect to both objectives and qualitative characteristics, Australia and the UK were closely aligned. 19 Nevertheless, conceptions about the pre-eminence of the decision-usefulness and associated qualitative criteria for accounting information were secondary to the legislative requirement in both the UK and Australia for adherence to the more ambiguously defined ‘true and fair view’, which was generally viewed as being conformance with generally accepted accounting principles (GAAP), and did not imply a target audience in the same way as the notion of ‘decision usefulness’ (see Cheung et al., 2010: 152–5). Consequently, standards issued by both countries fell well short of meeting many of these idealised attributes and failed to prevent further accounting scandals in each polity (see Carnegie and O’Connell, 2011; Gwilliam and Jackson, 2011). Decades later, the extent and success of the incorporation of such characteristics into accounting standards remained contentious (Cheung et al., 2010).

While the ASSC had commissioned research on a conceptual framework, it then instead wished to explore ‘whether a conceptual framework could be agreed upon which would be appropriate to the European Community, given the influence being exerted upon accounting practice by EEC directives’ (ASC, 1981: 33–41). Regardless of whether such an agreement was achievable, according to Peasnell (1982), the controversy around the draft conceptual framework within ‘The Corporate Report’ meant that the UK professions shelved further work on conceptual frameworks, instead choosing to focus on the development of inflation accounting standards. By way of contrast, according to Boymal (1986: 40), the Australian profession continued to ‘develop … projects which will result in a conceptual framework, useful to all standard setters to obtain consistency between various standards’. This ultimately resulted in the release of several exposure drafts, including EDs 42A, B, C and D in 1987 (Morris and Barbera, 1990).

Inflation accounting

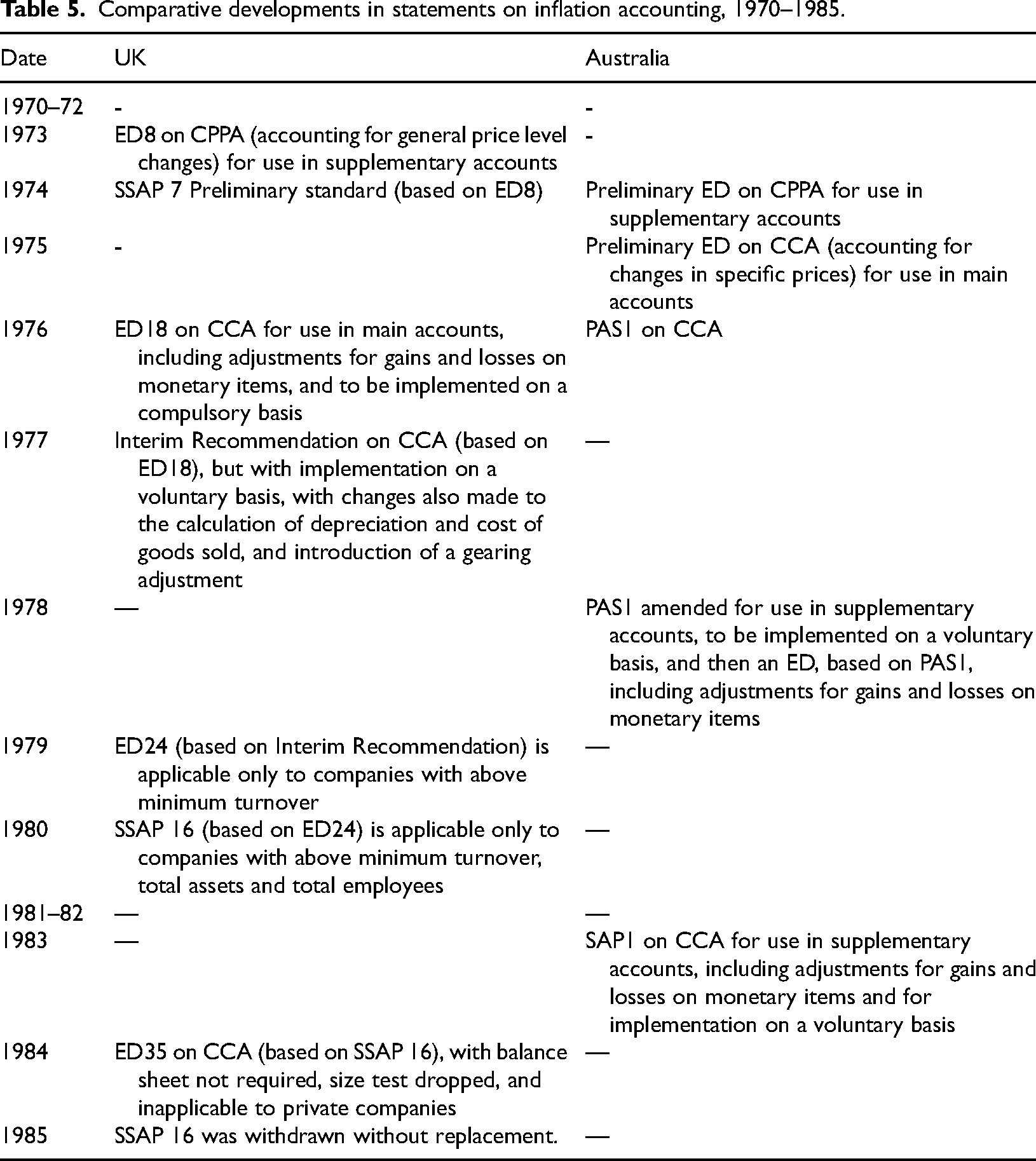

Another important issue between 1971 and 1985 that provided a catalyst for accounting standard development in the UK and Australia was the crisis caused by high rates of inflation. Both nations experienced high inflation in the 1970s to mid-1980s, with inflation reaching double digits in 1974 (16% in the UK and 15% in Australia) and in close correspondence thereafter, with the exceptions of 1975 (24% in the UK and 15% in Australia) and 1980 (18% in the UK and 10% in Australia). 20 While the development of standards and the recommendations of respective standards were distinctive, the outcome for each country ultimately was similar.

The various turnabouts by professional bodies in both nations, largely as a reaction to successive government and other committees of inquiry established to cope with inflation, are depicted in the timeline presented in Table 5. In the UK, the ASC opted for Constant Purchasing Power Accounting (CPPA). The UK Government's Sandilands Committee (Report of the Inflation Accounting Committee, 1975), however, favoured Current Cost Accounting (CCA) and, despite the profession's attempt to retain CPPA, Government acceptance of the report led to the publication of ED18. Subsequent developments saw the Hyde Committee (ASC, 1977) report its findings, and the issue of a new exposure draft – ED24, which ultimately became SSAP 16 in 1980 but was withdrawn in 1985 without replacement.

Comparative developments in statements on inflation accounting, 1970–1985.

In Australia, by way of contrast, the report of the Accounting Standards Review Committee (Chambers et al.,1978: 142) ‘… (lent) support to the CCA system’, and after two prior EDs, the Australian profession developed CCA pronouncements.

Mason (1978: 42) concluded that Australia ‘became the first … in the world to issue a standard, albeit a provisional one (PAS1 in 1978) – on a form of current value accounting’, but by ‘the end of 1983 it was decided that an accounting standard would not be issued, primarily because of strong opposition in the business sector’ (Nobes and Parker, 1985: 259). Parker (1986c: 48–9) argued that ‘with the absence of government intervention [CCA] failed through the inability of the profession to enforce it – Australia has had a similar experience to the UK’.

While the endpoint for the UK was the same as Australia, the UK professions differed as they had adopted an incrementalist mindset by designing and implementing inflation accounting principles using a ‘phasing in’ approach whereby the disclosure requirements would only initially apply to large organisations. Developments in Australia were more radical – for example, no size criterion was specified in relation to disclosures. Perhaps this was demonstrative of a stronger underlying conservatism in UK accounting thought and practice, and the primacy of historic cost in line with the EEC fourth directive. Consensus within the Australian profession appeared to have been more forthcoming than was the case in the UK, where the situation has been described as one of lost possibilities (see Rutherford, 2007).

Clarke (1982: xix) summed up the failure of the professions to introduce inflation accounting standards in both nations as being due to: pervading attitudes of inertia and compromise, in which the technical aspects of financial calculation in general and calculation of general purchasing power in particular were subordinated, and the increased complexity of the proposed adjustments improperly presented as technical refinement. As a consequence of those factors the professional prescriptions in every instance failed to achieve what was intended by them.

Approaches to the enforcement of accounting standards

Despite the introduction of accounting standards in the 1970s, the decades of pressure on the accounting professions in both nations around the issue of variation of accounting practice continued into the 1980s, although each nation ultimately approached the issue in contrasting ways. For Australia, the pressure on the profession ultimately resulted in the target for lobbying and the place for political negotiation shifting from the private to the public arena with the creation of the ASRB in 1984. The ASRB's development was directly linked to the corporate collapses and non-compliance with reporting requirements, which reached a peak in the early 1980s (Olsson, 1981: 546). Government involvement in standard setting was intended to address the issue of compliance by providing legal backing for accounting standards. The existence of standards alone had not alleviated the problems with variations in practice, with a survey by the NSW Corporate Affairs Commission in Australia exposing that 30 per cent of companies failed to comply with the provisions of the NSW Companies Act, 30 per cent did not comply with all relevant stock exchange listing requirements, and 80 per cent did not fully meet the provisions of accounting standards. Examination of Australian annual reports also suggested there were shortcomings resulting from ‘over-reliance on the statutory requirements as the major if not sole source of information to be disclosed’ and ‘preoccupation with the “stewardship” concept of an annual report’ at the expense of meeting the ‘informational needs’ of entities, shareholders, investors, employees, lenders and other parties (Olsson, 1981: 544–6).

By 1981, discussions were underway regarding the establishment of the ASRB, which was not intended to set standards itself, but would function to ‘review and either accept or reject proposed standards submitted to it by the profession (primarily through the AARF) and other interested persons and bodies’ (Cooke, 1981: 549). Prior to the formation of the ASRB, the profession in Australia had vigorously pursued the ideal of legal sanctions for non-compliance with AASs; however, ‘the Australian profession was … unhappy that it would … have to live with the ASRB superimposed above it’ (Standish, 1985: 115). Consequently, an alternative option was proposed by the two Australian professional bodies in their response to the government's proposal for the ASRB: the profession should administer the Board (see Australian Accountancy Profession, Joint Submission, 1982; Vincent, 1982: 19). This proposal was rejected, and the ASRB was established in 1984 by the Ministerial Council

21

for Companies and Securities in Australia, although it only began to carry out its full mandate in 1985. This change to the mechanism for endorsing standards was dramatic, and ‘the new system which has emerged in Australia is unique’ (Boymal, 1986: 36). The functions and powers bestowed upon the ASRB included: (a) determine priorities in consideration of proposed accounting standards referred to it; (b) review standards referred to it; (c) sponsor the development of standards; (d) seek expert advice as it deems necessary; (e) conduct public hearings into whether a proposed accounting standard should be approved; (f) invite public submissions into any aspect of its functions; (g) approve accounting standards. (Walker, 1987: 271)

While the full work of the ASRB is beyond the scope of this study, by October 1986, the Board had approved seven standards (AAS 6, 8, 12, 15, 16, 17 and 19). McGregor (1986: 50) commented that ‘while a number of amendments were made to the … approved Statements during the process of approval, none of these constituted a change of substance’ compared to the former standards of the joint professional bodies.

The goal for setting up such a body was to divorce the standards approval process from the standards setting process, given that the ASRB had the power to approve standards from bodies other than those representing accountants and that only two of the seven members originally on the Board needed to be accountants. While this was the goal, the outcome for standard setting in Australia was that the ASRB was captured by the profession (Walker, 1987). Consequently, the only major controversy between the ASRB and the profession in the mid-1980s was over the Board's significant variations to AAS 20 prior to approval in March 1987. The profession then gained an even greater hold over the ASRB as in late 1988, the ASRB and the ACSB of the AARF merged, increasing the number of members on the ASRB from seven to nine (McGregor, 1989: 87). The merger was described as a joint venture between the bodies representing the accounting profession and government and, according to Allen (1991: 61), ‘means the profession has effectively gained control of the ASRB and consequently of the standard setting process’. Lambert (1989: 18) went further in saying that the ASRB had an ‘inability to operate in an effective manner given the pressures placed on it by the profession’. By 1985 and into the 1990s, the accounting profession in Australia retained its hegemony, with standards developed by the profession being duly approved by the ASRB and the Ministerial Council having the force of law.

By way of contrast the professional bodies in the UK continued to release SSAPs which were not mentioned in companies legislation, even if it was ‘generally held that accounts prepared in accordance with SSAPs are presumptively true and fair and that statements not so prepared are less likely to be regarded by the courts as true or fair’ (Nobes and Parker, 1985: 65). In other words, while conformity with the requirements of SSAPs would presumably lead to true and fair accounts, the strict legal requirement to apply standards was less clear. This contrasted with the position in Australia, where standards had legislative backing once they had been approved by the ASRB. This matter of governmental role in standard setting and enforcement provides another key difference between Australian and UK financial accounting regulation in 1985.

Further to this, the influence of the EEC on the UK served to confine the power and autonomy that the UK professional bodies had enjoyed in the past. Indicative of this was that by the 1980s, the UK profession was focusing on the development of non-mandatory Statements of Recommended Practice (SORPs), with Parker (1986b: 82) saying that this change in focus was the result of a ‘lack of legitimacy and power (in enforcing accounting standards) … and compromise … (between numerous professional bodies)’. This is a significant conclusion that encapsulates the lack of clear legal backing for standards and the complex political nature of the standard-setting process in the UK. A similar initiative was taken in the form of ‘franked SORPs’, a subcategory of SORPs generally related to what the UK profession perceived to be topics of limited application (e.g., accounting in specific industries). Atchley (1983: 13) argued that the move to SORPs was a response by the profession to the ‘compliance climate’ whereby ‘lesser subjects’, would be dealt with through ‘non-mandatory recommendations with no disclosure requirements, irrespective of compliance’, all of which suggested a ‘future paucity of new accounting standards’. Watts (1981: 37), then Chairman of the ASC, felt that ‘with the absence of statutory or quasi-statutory mechanisms for enforcement (which would be contrary to our customs in the United Kingdom and Ireland), a sound means of supervision must be developed to support standards for at least a decade ahead’. A ‘sound means’ proved elusive, however, as the profession had turned to issuing SORPs in response to enforcement issues.

Given the ‘customs’ of the UK, it is not clear whether a body similar in nature to the ASRB would have been welcomed in the UK. Watts (1981) quote suggests that different social values and professional attitudes in the UK negated the profession's desires for a public regulatory body for accounting standards, leading Lafferty (cited in Leach and Stamp, 1981: 221) to interpret the stance such that, ‘the likelihood is that Britain will muddle through with the present system of setting and pretending to enforce accounting standards for another decade or two’.

Furthermore, the ASC (1981: 39-40) believed that ‘accounting standards should continue to be set in the private sector… not by government… The standards setting body should consist primarily of accountants’. Representing the views of the ASC, McKinnon et al. (1983: 115) concluded that ‘the essential characteristics of future accounting standards will be that … they deal only with matters of major and fundamental importance affecting the generality of companies and will therefore be few in number’. The ASC (1981: 13) also predicted a profession without any direct role in the development of standards, suggesting that ‘perhaps in the distant future it might prove practicable for EEC directives to contain all the necessary accounting requirements’.

Perhaps fulfilling these predictions, only two further SSAPs (SSAP 24 and SSAP 25) were released in the UK, with the ASC's other work on standards focusing on revisions to SSAPs 6, 9, 12, 13 and 22 and exposure drafts on intangibles, financial instruments, cash flow statements and goodwill, amongst others. In 1990, the Financial Reporting Council (FRC) was established, and the Accounting Standards Board (ASB) was introduced to replace the ASC. By 2000, the FRC had worked on revising existing standards, as well as releasing eight new standards. 22

Australia also began releasing a series of non-mandatory recommendations in the guise of Accounting Guidance Releases (AGRs) and issued AGR1 in 1985. Several AGRs were swiftly published to solve ‘problem[s] … not expected to affect significantly financial reporting in general, but … expected to be of significance to those reporting entities affected by the problem’ (Peirson, 1987: 1). In contrast however, AGRs were little more than ancillary and did ‘not establish new accounting concepts or standards and do not amend existing concepts or standards’ (AARF, 1986: 80) and dealt with issues of lesser substance than UK SORPs.

The ASRB ultimately evolved into the Australian Accounting Standards Board in 1991 and approved a range of existing AASs – 17 in all (AAS22 to AAS38) prior to 2000. 23 While it was initially believed that the ASRB would confine the power and autonomy of the accounting profession, this was not the case – the presence of a government body approving accounting standards and the shift of negotiation from the private to the public arena seemed to simplify the standard-setting process as there was a single target for lobbying.

Discussion and concluding remarks

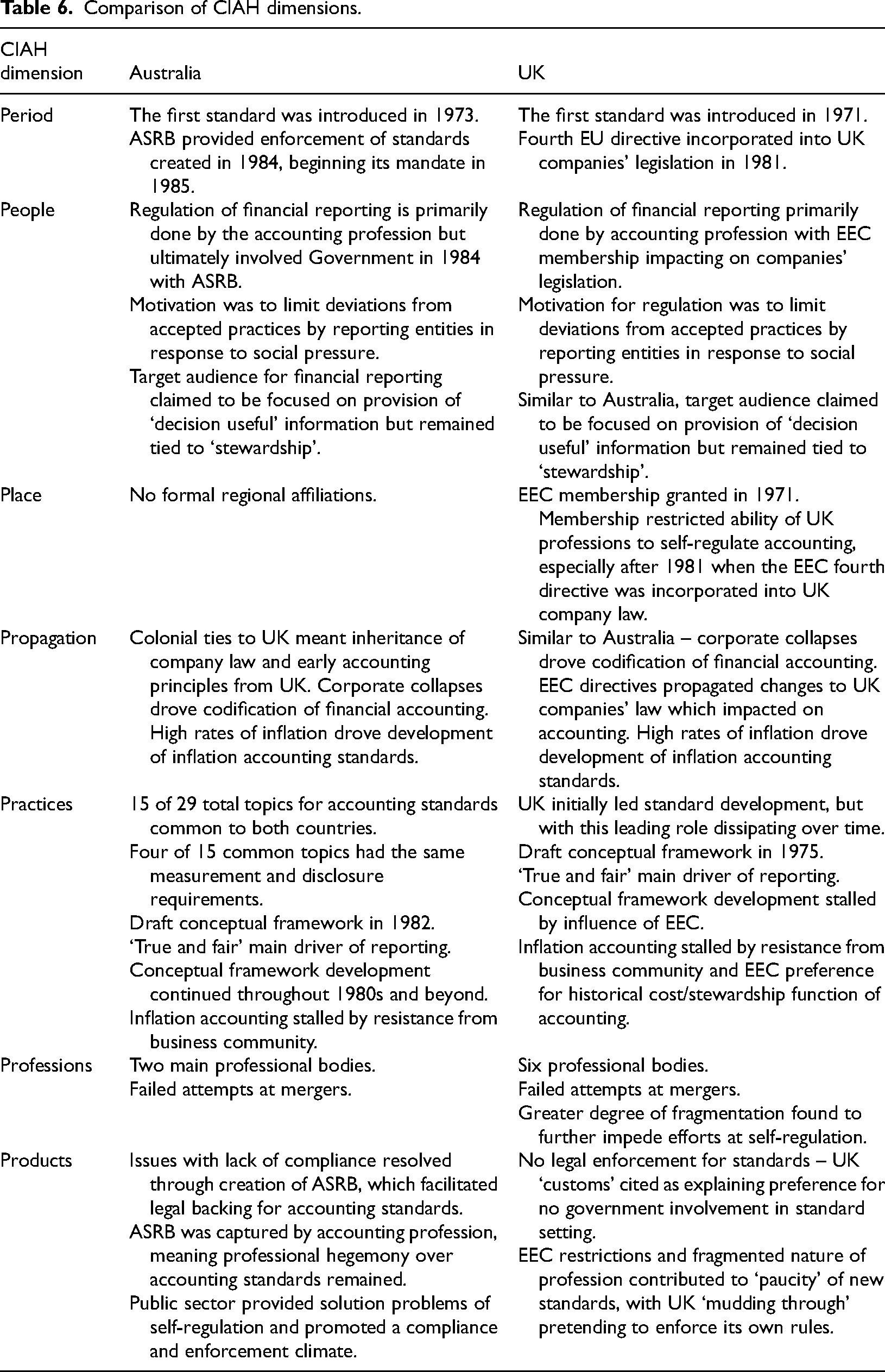

The primary aim of this article was to substantiate the extent of difference between Australian and UK approaches to financial accounting in the period 1971–1985, and to explore the factors driving these differences in the broader socio-political context of each country. A summary of the main findings of this article for each of the CIAH dimensions can be found in Table 6.

Comparison of CIAH dimensions.

In addressing the questions posed by this article: contrary to the comparative international accounting studies (e.g., Doupnik and Salter, 1993; Frank, 1979; Nair and Frank, 1980, 1983; Nobes, 1983), and despite the diffusion of legal systems, the interrelationships of the professions, the common need to respond to the long-term issues of variations in financial accounting practices, associated corporate collapses and high inflation, by 1985 UK and Australia approaches to financial reporting exhibited significant differences, with there being only four standards genuinely common to both nations. The impacts of evolving legal, political, social and economic forces in each country also resulted in significant variations in the specifics of accounting standards and approaches to their enforcement. The UK had more professional bodies, needed to harmonise its company law with those of European countries and had a culture which was not predisposed to having government involved in enforcing standards. At the same time, as per Parker (1982), Australian standards were different because Australia itself was different – it had no equivalent supranational entity with which it needed to conform, fewer professional bodies that needed to compromise, different industries, and it ultimately opted for legal enforcement through the ASRB to deal with the long-term issue of variation in financial reporting practice.

Post 1985, the UK continued its relationship with other European nations via the European Union (established in 1993 via expansion of the remit of the EEC) until 2016, when a referendum precipitated its eventual withdrawal in 2020. Australia established further, albeit less formal ties with its peers. For example, the USA came to be an increased source for accounting standards in Australia with Miller (1994: 340) arguing that USA was ‘the most important external influence on accounting and auditing in Australia’ and that Australia was subjected to an eclectic set of influences, while also being a source of influence itself, for example, through its role on the IASC. This was supported by Parker and Morris (2001: 300–301) who said that over the previous 20–30 years, ‘Australian accountants … [were also] moving away from the UK and towards the US at the same time that the UK [has] been increasingly influenced by its fellow member states of the EU’. The influence of the USA was also evident in relation to the development of conceptual frameworks during this time, as both nations borrowed heavily from work conducted in the USA by the Financial Accounting Standards Board (FASB).

Economically, Australia went on to enjoy greater financial security than the UK, faring better through corporate crashes and financial scandals and the global financial crisis, and outperforming the UK on most measures of national performance. In their continuing efforts to forge accounting standards, both nations worked closely on the IASC (often voting alike) before adopting International Financial Reporting Standards (IFRS) in 2005. In the UK, the move to IFRS was by de facto, through European Union adoption of the standards until 2020, when IFRS adoption was incorporated into UK law as part of the UK's withdrawal from the EU (Deloitte, 2024).

In terms of how these findings can be linked to contemporary practice, many of the identified factors causing divergence remain relevant today and still have the potential to impact on the effective regulation of financial reporting. While the UK Companies Act (2006) requires firms to adhere to the ‘true and fair’ requirements in section 393, UK accounting standards remain without the same force of law when compared to Australian standards, which have specific reference in section 297 of the Corporations Act (2001). The UK accounting profession is still fragmented, albeit with the CCAB now comprising five constituent bodies rather than six (ICAEW, 2024a, 2024b), while the Australian accounting profession is still dominated by two.

Also of relevance to contemporary financial reporting is the finding that two nations with a veneer of similarity in financial reporting systems diverged in terms of the detail of accounting standards and approaches to enforcement from the issue of the first accounting standards. This veneer of similarity between Australia and the UK remains an ongoing issue in the IFRS era, given that countries that ostensibly use IFRS still have scope for differences in practice due to the IASB having no powers over enforcement or interpretation, and it not keeping a track of the extent of compliance with IFRS within specific countries (see Camfferman and Zeff, 2018). An example of an ongoing difference between the UK and Australia in the context of the IFRS era is the mandatory application of IFRS to non-listed entities, with non-listed entities in the UK having the option to use UK GAAP, while in Australia, all reporting entities are required to adhere to the Australian Accounting Standards (which are IFRS compliant) (Deloitte, 2024). The finding of the long-term existence of divergence between two countries with historical and cultural ties as close as those shared by Australia and the UK can therefore temper expectations of eventual global standardisation of financial reporting.

While the primary purpose of this article was to explore the extent of similarity between Australian and UK financial accounting systems, it has also examined the interplay of the accounting profession and the state and the impacts of this interplay on the standardisation of financial accounting, given the prominent influences of the EEC and the ASRB. Thus, it has connected changing contextual factors with government intervention, political manoeuvring, lobbying, and declining faith in the accounting profession within the societal arena. This work therefore contributes not only to the literature on CIAH and accounting standards, but also to those which deal with histories of accounting's professional project, the quest for professional legitimacy and professional closure, such as Carnegie and Napier (2010), Carnegie and O’Connell (2012) and Sidhu et al. (2020).

An obvious limitation of this study is its reference to two countries. Scope therefore exists for further studies to examine the relationship between the UK and its numerous other former colonies, such as New Zealand, Canada or the United States (along with others). Further studies could also delve into the relationship between former colonies.