Abstract

Irving Fisher's capital-income theory uses the discounted cash-flow model to explain prices, markets, and capitalism. How did his theory get into ‘fair-value’ accounting standards given that his framework was discredited in the post-1929 crisis aftermath? This article explores one of the possible causes, namely, the popularity of Fisher's theory in mainstream accounting and economic research albeit its lack of supportive evidence and logical consistency. Nonetheless, its history of ideas is far from straightforward. Although ‘decision-usefulness’ researchers (who inform standard setters) currently endorse Fisher's theory, they have seldom engaged with Fisher's writings. Alongside them, capital-income theorists, normative-theorists and mainstream-economists have been advocating Fisher's theory with a taken-for-granted-knowledge status, which often fails to cite its heritage. Furthermore, although ‘decision-usefulness’ researchers have historically claimed opposition to normative theories, this opposition is deceptive. Fisher's theory is undeniably normative. It favours shareholders/owners over other stakeholders. Moreover, various normative-theorists have accepted Fisher's theory for valuation purposes.

Keywords

Introduction

Cardao-Pito and Ferreira (2018a) have recently demonstrated an impressive similarity between Irving Fisher's writings (1906, 1907) on accounting and economics, and key ‘fair value’ accounting standards from the International Accounting Standards Board (IASB) and Financial Accounting Standards Board (FASB) 1 (see also Baker, 2018; Bryer, 2013b; Cardao-Pito, 2020; Cardao-Pito and Ferreira, 2018b; Markarian, 2018). Those findings relate accounting ideas and theories to economic thought, which is an ongoing effort (Baker, 2018; Bhimani, 1994; Bryer, 2012, 2013a, 2013b; Markarian, 2018; Mattessich, 2003; McSweeney, 2009; McWatters, 2018; Mouck, 1995; Oldroyd et al., 2015; Persson et al., 2018; Pucci and Skærbæk, 2020; Suzuki, 2003). Nevertheless, when Fisher is not altogether omitted, some papers and articles dispute his relevance for accounting research and practice, which we describe as the ‘Fisher's irrelevance hypothesis’ (see for instance Baker, 2018; Oldroyd et al., 2015).

Therefore, a question remains on how Fisher's capital-income theory ended up in fair value accounting regulations. As with other historical phenomena, there could be several reasons for Fisher's theory to have been inscribed in these regulations. This article explores one of those, namely, the acceptance and popularity that Fisher's capital-income theory has gained in mainstream accounting and economic research. It provides an exploratory history of ideas influenced by Fisher's theory. Due to length constraints, it devotes little space to other possible reasons or to a socio-economic history of this important phenomenon, which are tasks for future research to complete.

Fisher's (1906) novelty investigated in this article is his theory that the discounted cash flow model could be used to explain actual markets, prices, values and even capitalism. This model is often called by other names such as (net) present value or present worth. Before Fisher, this model never had such a prominent role (Bryer, 2013a, 2013b, 2021; Cardao-Pito, 2016, 2017a, 2017b, 2020, 2021a; Cardao-Pito and Ferreira, 2018a, 2018b; Mouck, 1992; Parker, 1968; Schumpeter, 1952, 1997) This ad-hoc model was used to estimate values for a few (financial) assets such as insurance premiums, loans, or bonds, and to particularly speculative assessments of investment value. There is no significant proof that discounted cash flow models could explain markets, prices, values or capitalism (Basilli and Zappia, 2012; Bougen and Young, 2012; Bryer, 2021; Callen, 2015; Cardao-Pito, 2012, 2016, 2021a; Cardao-Pito and Ferreira, 2018a, 2018b; Mouck, 1992; Shiller, 1981, 1984, 2005). Yet, Fisher's theory is widely popular in vast sections of accounting and economic research.

As described by Schumpeter in 1952, Fisher has given economists and accountants: opportunities to learn from accounting and actuarial practice and in turn to try to rationalize it from the standpoint of economic theory. Attempts to do both are of comparatively recent origin and the more important of them, though no doubt subconsciously, follow Fisher's example. (Schumpeter, 1952, 1997: 228)

In this citation, the actuarial practices are the discounted cash flow models used to estimate for instance insurance premiums or financial liabilities.

Nevertheless, Fisher's reputation was devastated by the post-1929 crisis. In the years to 1929, Fisher, who had advised presidents, achieved a stellar status as an economist and public intellectual. He was widely known and commended. Perhaps he could have been America's most famous economist (Allen, 1993; Dimand, 2013, 2019; Dimand and Geanakoplos, 2005; Economist, 2009). However, his reputation would soon be undermined. In addition to his theories collapsing in face of the evidence, there was of course the infamous statement on 15th October 1929 where Fisher had predicted that stock prices could never go below the high plateau they had settled upon, and they should be ‘a good deal higher than it is today within a few months’ (Galbraith, 1954: 116; see also Fox, 2009). Instead, a great crash ensued. Three years later, stock prices in America would have lost more than 90 per cent of their previous value, which added to the bankruptcy of thousands of banks, and had complex after-effects in many national economies (Fox, 2009; Michie, 2006). Fisher himself would become almost broke because of his investments. He was rescued by his sister-in-law's emergency loans, and Yale University buying his house. Later, Fisher could not even pay the rent established by his university, thus, moving on to a smaller house (Allen, 1993; Dimand, 2019; Markarian, 2018). These events hardly help in qualifying him as a thinker who understood markets, prices or capitalism. In the years after the post-1929 crisis, most economists would dismiss Fisher as ‘a nut with mathematical ability’ (as described in a letter from Calkins to Zeff in 1965, which was cited by Zeff, 2000: 22; see also Dimand, 2019). To a certain extent, this statement may be an exaggeration. Fisher would retain a few fringe followers, some of whom would decades later reach Nobel prize status in economics (Cardao-Pito, 2021a, see also below). Moreover, he remained influential at the American Economic Association where he was the President in 1918, and at research institutions he had helped to form such as the Econometric Society and Cowles Commission for Research in Economics, (Dimand, 2019, 2009). However, by the 1930s, few could predict that Fisher's idea would guide accounting norms and regulations.

Currently, Fisher is not widely recognised as an important contributor to accounting thought and practice. There are several researchers who advocate greater attention must be paid to him to promote a better understanding of accounting theory, regulations and practice (Bryer, 2013b; Cardao-Pito and Ferreira, 2018a, 2018b; Markarian, 2018; Mouck, 1995). For instance, Bryer (2013b: 603–604) argues that Fisher created a toxic theory of economics and accounting when he characterised ‘capital’ as the present value of expected cash flows and ‘income’ as interest. In this manner, Fisher disconnected accounting from actual transactions and events. Cardao-Pito (2016) and Cardao-Pito and Ferreira (2018a) explain that Fisher created this theory of capital and income to measure Adam Smith's reformulated concept of capital. To Smith, capital is no longer money invested or investable in business, but comprises elements that can be used to increase the wealth of investors in organisations: these elements can include machines, buildings but also human beings (Cannan, 1921; Cardao-Pito, 2016, 2020; Hodgson, 2014). Generally, Smith's reformulated definition of capital has been adopted by economics and sociology, but not by business circles (Cardao-Pito, 2016, 2020; Hodgson, 2014).

Nonetheless, Fisher's theory is indisputably normative: it privileges the interests of one group of organisations’ stakeholders, namely, shareholders/owners. By claiming that the value of the organisation is identical to the discounted future monetary flows paid to owners/shareholders, Fisher is indeed claiming that the purpose of organisations is to increase the monetary flows (wealth) to their owners/shareholders (Cardao-Pito, 2016, 2017a, 2017b, 2021b; Cardao-Pito and Ferreira, 2018a). Given the high proximity between Fisher's theory and fair value accounting, Cardao-Pito and Ferreira (2018a: 149) suggest that the latter could be considered as ‘the normative Fisherian phase of accounting’.

On the other hand, Oldroyd et al. (2015: 215) have disputed that Fisher is an important contributor to accounting thought because Fisher has been ‘omitted or mentioned only in passing by most works on accounting history’. Baker (2018) accepts their findings but does not explain how Fisher's theory has ended up in ‘fair value’ regulations. He suggests that the relation between Fisher and those regulations can still be a ‘coincidence’ (Baker, 2018: 192) or an ‘anomaly’ (Baker, 2018: 196). Given the magnitude of Cardao-Pito and Ferreira's (2018a) findings, however, the hypotheses of coincidence or anomaly are unlikely.

Without further evidence, Fisher's irrelevance hypothesis promoted in Baker (2018) and Oldroyd et al. (2015) would remain conceivable. This article, however, refutes the Fisher irrelevance hypothesis. Thus, it contributes to the literature by settling the dispute between those who claim that Fisher is highly relevant to the history of accounting thought (as in Bryer, 2013b; Cardao-Pito, 2020; Cardao-Pito and Ferreira, 2018a, 2018b; Markarian, 2018, Mouck, 1995), and those who think he is irrelevant for accounting thought (e.g. Baker, 2018; Oldroyd et al., 2015). The article shows that arguing for the irrelevance hypothesis is no longer viable. Rather, we must try to better understand Fisher's consequence for accounting thought. Although in the limited space of this article we could not identify every impact that Fisher's theory has had on accounting thought, we can identify several instances where Fisher's theory has been defended and promoted. Furthermore, we present a hypothetical history of ideas model regarding the pathway by which Fisher's theory reached accounting regulations. As we will see, the relation between Fisher's theory and accounting thought is rather complex, not least because many contemporary defenders of Fisher's framework may not be aware that they are promoting his ideas. Nonetheless, we will show that although accounting regulators and several financial accounting researchers invoke guidance from market imperatives (Bhimani, 2008; Mehrpouya and Salles-Djelic, 2019; Pucci and Skærbæk, 2020; Young, 2003, 2006; Young and Williams, 2010), they are instead guided by Fisher's fragile and feeble theory on prices, markets, and capitalism.

The article is organised as follows. The next section summarises Fisher's views that are inscribed in fair value accounting norms. The following section identifies several groups and events bearing on accounting thought that are to some extent connected to Fisher's views. The section after puts together the hypothetical exploratory model and discusses its limitations. The folllowing section discusses the possibility of existing political reasons for the prevalence of Fisher's theory in accounting research and regulations. The final section concludes the article.

Synthesis of Irving Fisher's capital-income theory in accounting norms

Undeniably, only a minor subgroup of assets and liabilities are targeted by fair value accounting standards (Baker, 2018; Cairns, 2006; Cardao-Pito, 2020; Nobes, 2015). This subgroup includes a few financial items, along with a few circumstances where fair value accounting is used for initial determination of cost, when no other workable alternatives are available. The current dominant accounting system is a mixture of historical costs and current market prices (Baker, 2018; Cairns, 2006; Cardao-Pito, 2020; Nobes, 2015, see below). However, given the support that fair value accounting has from accounting regulators and many research departments, a possibility exists that fair value accounting will expand further in future (Botzem and Quack, 2009; Cardao-Pito, 2020; Georgiou, 2018; Mora et al., 2019). Thus, a better understanding of this accounting phase is acutely needed.

Fair value accounting must be comprehended by relating its three levels (Cardao-Pito, 2020; Cardao-Pito and Ferreira, 2018a). Level one accepts market values, and level two comparable market values, if no direct market is available. Level three allows predictive models to identify market prices, when no direct or comparable markets are available. These models are based on discounted projections of future monetary flows. 2 Nonetheless, the third level does not only settle alternative models for accounting values without markets. It implies that if a market were to exist, it would operate as a large discounted future cash flow model processor. That is, discounted cash flow models could explain markets, price formation and even capitalism (Cardao-Pito, 2020; Cardao-Pito and Ferreira, 2018a). Hence, a specific theory can be found in fair value accounting, which distinguishes it from other moments in the history of economic and accounting thought where the market value argument in accounting was made with different motivations (Cardao-Pito, 2020; Ding et al., 2008; Georgiou and Jack, 2011; Richard, 2004, 2005, 2012). Fair value accounting must not be understood as requiring market values. Historical cost accounting systems can also accept market values, for instance the rule of the lower of market or cost value (Cardao-Pito, 2020, Nobes, 2015, Zeff, 2013).

We can thus find a specific theory of valuation in fair value accounting. What is more, Cardao-Pito and Ferreira demonstrate this very same theory in Fisher's writings (1906, 1907). Like Fisher, the IASB and FASB's fair value standards consider markets to be efficient processors of information. Moreover, they suppose that markets would be mega processors of discounted projections of (unpredictable) future cash flow to define their prices. In fact, Fisher's theory may have to some extent been more extreme than that of contemporary standard setters because he has advocated a concept of ‘psychic income’ (Fisher, 1906 in Chapter 10; see also: Cardao-Pito, 2021a; Chambers, 1971a; Frankel, 1952; Mouck, 1995), indicating that even forms of enjoyment or displeasure could be transformed into a monetary market price figure: ‘it is necessary to imagine an exchange, even when actual exchange is impossible’ (Fisher 1906: 177). Standard setters do not yet endorse Fisher's ‘psychic income’. However, fair value accounting does adopt Fisher's theoretical explanations for markets, prices and capitalism, which is indisputably normative because they align with shareholders/owners’ interests (Cardao-Pito, 2017a, 2017b; Cardao-Pito and Ferreira, 2018a, 2018b). What follows seeks to refute Fisher's irrelevance for the accounting thought hypothesis by highlighting systematic motives for Fisher's theory framing fair value accounting standards. We will identify research events and backgrounds where Fisher's theory has been highly influential in the last century. Understandably, we will see, it has not been unusual to find Fisher's framework being advocated without any reference to him.

When someone uses discounted cash flow models, his/her position is not, necessarily, Fisherian. In Fisher's time, the discounted cash flow model already had a few distinct applications such as the analysis of loan operations, ad-hoc investment appraisal for (complex) business endeavours, evaluation of insurance businesses, and investment debates in the political economy (Cardao-Pito, 2016; Cardao-Pito and Ferreira, 2018a, 2018b; Parker, 1968). Likewise, as explained above, the defence of market prices for accounting purposes does not make someone's position as necessarily Fisherian. On the other hand, many an individual who did not read any of Fisher's writings can be Fisherian by adopting his views. However, those who adopt Fisher's explanation for valuation, adopt likewise his theory regarding values, prices, markets, and capitalism (Bryer, 2021; Cardao-Pito, 2016, 2021a; Cardao-Pito and Ferreira, 2018a, 2018b).

As Fisher became much less popular after the post-1929 crisis, he also became much less cited. Yet, his ideas were frequently promoted. Thus, we need a test to identify those writers who endorse Fisher's theory even when they do not cite him (and in some cases do not know how Fisher is important to their own work). For this analysis, we follow Cardao-Pito and Ferreira (2018a, 2018b) in defining Fisher's theory as a normative theory for accounting and economics (see also Bryer, 2021: 15). Accordingly, we define writers and documents as Fisherian through Bryer's (2021: 3–4, 133) test, namely, in considering the present value (discounted cash flow model) as the implicit ideal measure of money value. It is with reference to this test that our analysis proceeds. Treated as a valuation ideal, Fisher's ideal of monetary value is claimed as superior to any other form of valuation, or explanation for prices, markets, and capitalism (Bryer, 2013b, 2016, 2021; Cardao-Pito, 2020, 2021a; Cardao-Pito and Ferreira, 2018a, 2018b; Whittington, 2017). However, evidence for this is clearly missing. Nonetheless, followers of Fisher's theory generally adopt his ideal of valuation as a truism, and without any discussion regarding its validity or lack of supporting evidence.

Popularity of Fisher's capital-income theory in mainstream accounting and economic research, despite his reputational problems after 1929

Initial capital-income-accounting theorists

Bryer (2021) shows that in the years just before the post-1929 great crisis, Fisher was quite influential in accounting. Furthermore, as suggested by Bryer, while Fisher cannot be indicated as the only cause of that crisis, his ideas and followers may have had something to do with it. Despite his difficult experiences in the post-1929 crisis, Fisher still maintained some of his previous influence. For instance, he kept on writing books and presenting papers at the American Economic Association or the Econometric Society (which he had founded and, at some point, presided over) (Allen, 1993; Bryer, 2013b; Dimand, 2019). Moreover, he received honourary degrees and career celebrations (Allen, 1993). Furthermore, he remained in touch with politicians and United States Presidents (Allen, 1993). His death in 1947 was headline news across America (Allen, 1993; Fisher, 1956).

Indisputable, however, Fisher's reputation as a public intellectual and economist was deeply affected by the post-1929 crisis (Allen, 1993; Bryer, 2013b; Dimand, 2007, 2019; Fox, 2009; Galbraith, 1977). Yet, several researchers working in the post-1929 crises’ aftermath persisted in developing Fisher's framework in accounting, albeit Fisher's fall from grace. We describe this group as initial capital-accounting theorists. Several other researchers would disagree with them by overtly’ claiming that Fisher's theory could have a damaging impact on accounting and economics (e.g. Frankel, 1952; Simmons, 1938).

John Canning has been identified as the first person to develop a conceptual framework for accounting valuation and measurement founded explicitly on Fisherian expectations of future cash flows discounted by a rate (Chambers, 1979; Whittington, 1980; Zeff, 1999: 90). Canning's work also confuses measurement with an ad-hoc valuation, as Fisher did before him. In his ‘The Economics of Accountancy’ Canning (1929: 161, 144–145, 170), pays a large tribute to Fisher, who would himself praise the book (Fisher, 1930b). Canning was an economist by training. He focused his work on accounting for a short 4-year period, curiously around, 1929–1933, thus, featuring three years after the 1929 crisis's inception. However, Canning's work in this period was based upon his PhD in economics at the Chicago University, which he begun before the crisis in 1920. His dissertation was submitted in 1928, thus before the crisis's inception (Zeff, 2000). Zeff (2000) describes Fisher as a mentor to Canning's doctoral studies. In the preface of his book, moreover, Canning declares his large debt to Fisher's ideas: ‘I need not declare my obligation to Professor Fisher for his influence of his writings upon my thought – that obligation appears throughout the whole book’ (Canning, 1929: iv; see also Zeff, 2000).

Nonetheless, Canning would have a strong influence on later accounting researchers (Chambers, 1979; Whittington, 1980; Zeff, 1999, 2000). Since Canning, similar Fisherian views have recurrently been referred to as the economists’ notion of accounting for elements such as income, assets, capital, and liabilities (Chambers, 1979; Whittington, 1980; Zeff, 1999, 2000). Yet, Canning did not describe Fisher's views as economists’ views. Instead, he chose Fisher as the economist whose work on the subject has been the most exhaustive, and whose book ‘The Nature of Capital and Income’ would be quite useful for accountants (Chambers, 1979).

Canning was not alone in his efforts. For instance, Lindhal (1933) and MacNeal (1939) (as stated in Zeff, 1982) also promoted the Fisherian agenda, while praising Fisher's writings. Likewise, while extensively citing both Fisher and Canning, Bonbright (1937) compared methodologies to appraise property value for legal purposes. He identified four major methods of valuing property, namely, (i) actual sales price, (ii) actual or original cost, (iii) replacement cost, and (iv) capitalisation of income. Clearly, he prefers method (iv), which is Fisher's theory of value (Bonbright, 1937). As noted by Barnes (1937: 160), who reviewed his book, in Bonbright's argument the practical difficulties at ‘estimating prospective income and selecting the rate of capitalization receive only passing attention’. Generally, this problem remains unresolved by contemporary followers of Fisher's theory.

Ronald Coase would be another important contributor to the Fisherian cause in accounting and economics. Coase would himself later be an influential economist who developed the prominent mainstream economic theory about the nature of the firm (Coase, 1937), and who would obtain a Nobel prize many years later in 1991. Like many posterior researchers, Coase did not always cite Fisher when using his ideas. Nonetheless to Coase, market, values and prices are based on expectations of future economic benefits. Thus, Coase's work is Fisherian according to the test devised above. Coase (1937) is also the key reference for Oliver Williamson's mainstream transaction costs theory. Likewise, Williamson would receive a Nobel prize many years later in 2009. Through a series of 12 papers published in The Accountant, and summarised in Coase (1938), Coase tried to persuade accountants to use discounted cash flow models (current values) instead of historical costs to report equity, assets and liabilities (Coase, 1938; Parker, 1968). Clearly, Coase advocates the Fisherian framework: ‘By this phrase (‘the value of an asset’) I mean the present value of the net receipts which it is estimated will be obtained from ownership of that asset (‘discounting them by a rate of interest’)’ (Coase, 1938: 5.14, 5.28). Although Coase's definition is akin to Fisher's valuation ideal, Coase does not cite Fisher, preferring the formulation that the expressed view is the ‘common property’ of economists of the London School of Economics (LSE) at the time (Coase, 1938: 5.2, see also Napier, 2011). Hence, here we have perhaps one of the first instances where Fisher's theory is promoted while Fisher is not cited.

Coase might have been referring to another economist at LSE: John Hicks (1939, 1946) who delivered a Fisher-inspired definition of income in his book ‘Value and Capital’, while failing to acknowledge Fisher. As defined by Hicks (1939, 1946: 173, 178–179): ‘Income No. I is thus the maximum amount which can be spent during a period if there is to be an expectation of maintaining intact the capital value of prospective receipts (in money terms).’ To Hicks, the value for capital should be found by this ex-ante computation for expected income discounted by some rate as in Fisher's valuation ideal: Any stream of values whatsoever has a capitalized value, which may now be regarded as a function of the rate of interest … we shall measure, not the rate of interest, but what may be called the discount ratio - the proportion in which a sum of money has to be reduced in order to discount it …. Corresponding to any particular level of income, we have a capital-value curve ... which shows the present value of the standard stream corresponding to that particular level of income (according to the definition of income we are using) at various discount ratios. (Hicks, 1939, 1946: 185, see also: 173–190)

According to Hicks, the income definition that is used to explain capital would have one supremely important property: As long as we confine our attention to income from property, and leave out of the account any increment or decrement in the value of prospects due to changes in people's own earning power, income ex-post (based on historical data) would not be a subjective affair, like other kinds of income; ‘it is almost completely objective’ (Hicks, 1939: 179). However, Hicks emphasised that income ex post ‘can have no relevance to present decisions’ (Hicks, 1939, 1946: 179), because, according to him, present decisions ought to be based on income ex ante. As shown above, the latter's value is computed through Fisherian discounted cash flow models.

Clearly, a similar definition for capital to that used by Hicks can be found in several of Fisher's works (Cardao-Pito and Ferreira, 2018a). Fisher also uses the discounted cash flow model to explain the value for capital, and its respective market price. Nonetheless, Hicks's lack of references to Fisher might have misled the FASB and IASB into attributing the concepts of capital-income based upon discounted projections of future benefits to Hicks (Bromwich et al., 2010; FASB/IASB, 2005). That is, unfairly, Hicks has come to be known as the founder of the capital-income view of accounting and economic value instead of Irving Fisher.

Normative accounting theorists

Normative theorists belonged to a time and movement trying to address major epistemological questions in accounting, such as its purpose, or how accounting affairs should be conducted. The expression ‘normative’ arises from their attempts to solve notable questions (Campfield, 1970; Chambers, 1976; Dyckman and Zeff, 2015; Edwards et al., 2013). This group had their heydays mostly in the decades after the Second World War, until positivists took over from them. Despite agreeing on questions, normative theorists have produced greatly divergent answers (Dyckman and Zeff, 2015; Edwards et al., 2013; Kabir, 2005).

Many researchers at that time were well informed about Fisher's conception of economic and accounting value. Though more of an economic persuasion, Parker and Harcourt's (1969) ‘Readings in the Concept and Measurement of Income’ devotes the first chapter to an extract from Fisher. Parker's (1968) notable historical perspective of the discounted cash flow model describes Fisher's application of this ad-hoc model into a valuation theory. Furthermore, it is not uncommon to find normative theorists studying Fisher (e.g. Chambers, 1971a; Ijiri, 1967).

However, several normative theorists legitimised Fisher's value theory, at least because they did not question its lack of serious supportive evidence or logical consistency. Thus, according to the test devised above, they were Fisherian in this respect. Normative theorists were convinced that accounting measurement must follow a sound normative theory. At this point, they were not persuaded that a normative theory could justify adopting Fisher's theory as the basis of accounting regulation. However, because accounting valuation was given centre stage, Fisher's theory gained notoriety as a possible framework for valuation in economics. Hence, this group was also influenced by Fisher's framework in the sense that these theorists accepted studying and discussing Fisher's framework as a valid theoretical alternative. They generally did not endorse Fisher's theory as an adequate normative theory for accounting practice and regulations. The application of Fisher's theory to financial statements received very serious criticism, including that Fisher's theory does not fit within accounting's double entry system, that his system could not produce coherent and balanced balance sheets, and his system fails to distinguish between measurement and valuation (Bryer, 2013b; Chambers, 1965, 1971a; Littleton, 1929, 1930, 1935). However, by embracing the Fisherian framework as a possible explanation for value and market prices, these researchers actively contributed to disseminating Fisher's theory on accounting.

The FASB and International Accounting Standards Committee (reformulated in 2001 into IASB) would only be created in 1973. Before that, the Securities and Exchange Commission (SEC) ruled accounting practices in the United States, though in 1938 it delegated its authority to set accounting standards to the American Institute of Accountants and the Committee on Accounting Procedure (Carey, 1969; Previts and Merino, 1998). In 1959, the American Institute of Certified Public Accountants (AICPA) created the Accounting Principles Board (APB), a forceful body that issued guidelines and rules on accounting principles. The APB was replaced by the FASB in 1973 (Previts and Merino, 1998). Nevertheless, the SEC was also a body formed in the post-1929 crisis aftermath to address and prevent future crises (Michie, 2006). As with other countries’ regulators at that time, the SEC systematically supported historical cost practices (Zeff, 1999, 2013). It regarded the departure from the objectivity of historical cost accounting as having the potential to deceive readers of financial statements (Zeff, 1999).

Several theorists have tried to develop normative principles and postulates that could explain the existing historical cost accounting practices (Ijiri, 1975; Littleton, 1953; Paton, 1922; Paton and Littleton, 1970; Sanders et al., 1938). On the other hand, normative theorists who tried to advance alternatives to historical cost practices generally made proposals based on normative principles and postulates, not on Fisherian economics. 3 However, normative accounting theorists have had an important role in advancing the Fisherian agenda because they accepted Fisher's discounted cash flow model as the valuation ideal (our test above). Their reservations were concerned with the discounted cash flow method being too subjective and impractical to be suitable for accounting measurement. For instance, Chambers’ (1965, 1966, 1968), several texts defend the view that accounting measurement issues must not be confused with valuation issues, which implies that Fisher's valuation ideal could eventually be suitable for valuation. Despite being a proponent of historical cost accounting systems, Ijiri clearly engaged with the mainstream economic approach to accounting (Ijiri, 1967; Ijiri and Noel, 1984). He was open to the idea that forecasts about the future could be published as a parallel accounting to traditional accounts, which implies the acceptance towards Fisher's valuation ideal to a certain extent (Ijiri, 1982, 1986, 1989; see also Fellingham, 2018; Fraser, 1993). He described a parallel accounting of ‘accounting for the future’ (Ijiri, 1982: 41). He also suggested: ‘Consider the power of a triple-entry system that insists on getting future events accounted for in a similar fashion (temporal triple-entry bookkeeping) or getting the reasons for changes in income accounted for (differential triple-entry bookkeeping)’ (Ijiri, 1982: 41). Ijiri described his motivation as directing ‘management's attention and sensitivity to factors at a level deeper than the level of wealth and income that has been traditionally dealt with by double-entry bookkeeping’ (Ijiri, 1986: 745). Certainly, Ijiri suggested that Fisher's valuation ideal is not entirely reliable and must be separated from cost-based bookkeeping. However, Ijiri accepted the Fisherian ideal as accounting for the future, which could be identified as an alignment with Fisher's theory. Perhaps Chambers and Ijiri were still trying to build fences against applications of the Fisherian valuation ideal in accounting practices, and, thus, trying to separate facts from forecasts in financial statements (Glover et al., 2005). Nonetheless, normative theorists like Chambers and Ijiri have, to great extent, helped legitimise Fisher's ideal for valuation purposes.

However, before long the distinction between accounting measurement and economic valuation, or between faithful and relevant information established by several normative theorists was about to be contested by the decision-usefulness researchers. Often, normative theorists did not have an effective strategy to advance their agenda (Edwards et al., 2013). Furthermore, they did not entirely understand the danger posed to their scholarship by decision-usefulness researchers trained at highly ranked schools, who they were keen to hire on the grounds of their elite academic status (Edwards et al., 2013). Yet, among other influences, decision-usefulness researchers built on the fact that various normative theorists had accepted Fisher's valuation ideal for explaining prices, markets, and capitalism.

Mainstream economics

Before we address ‘decision-usefulness’ accounting theory, we need to observe fundamental episodes in mainstream economics that may have influenced it. Currently, although it is quite common for papers published in high-profile accounting journals to reference mainstream/financial economics journals, the latter very rarely cite any journal in accounting (Bricker et al., 2003; Hussain et al., 2020; Pieters and Baumgartner, 2002). That is, mainstream accounting imports theories, models and concepts from mainstream economics literature. However, it rarely exports any new ideas back. Disappointingly, mainstream accounting research seems like a secondary division of economics.

Several mainstream economic landmarks have promoted Fisher's theory, and thus, may have greatly impacted accounting research. Fisher's view still is how mainstream economists think about capital and income (Concise Encyclopedia of Economics, n.d; Tobin, 2005). Friedman's (1966) highly influential ‘positive economics’ was later adapted into a ‘positive accounting theory’ by Watts and Zimmerman (1978, 1979; see also, Christenson, 1983; Milne, 2002; Whittington, 1987). Friedman (1994: 37) has no issue in supporting Schumpeter's (1951: 223) statement that Fisher has been ‘the greatest economist the United States has ever produced’. This is a similar position to Paul Samuelson, who described Fisher's thesis as ‘the best of all dissertations in economics’ (cited in Mirowski, 1991: 223). Friedman and Samuelson, who also gained Nobel prizes, likewise did not cite Fisher in most of their writings, seemingly taking his ideas for granted.

Among many other possible features, two mainstream economic features may have been of great relevance for accounting. The first is the reintroduction of Fisher's framework into financial economics by Modigliani and Miller (1958), who did not cite Fisher in this reintroduction (Cardao-Pito, 2021a). However, 30 years later, Miller (1988) admitted what was evident, namely, that his work with Modigliani had been based on Fisher's theory (see also Cardao-Pito, 2021a). Certainly, there were more writers at the time developing Fisherian ideas. Above we have seen the cases of Canning, Coase, Friedman and Samuelsen. Likewise, Hirschleifer (1958: 328) defended Fisher's theory of optimal investment decision while maintaining that ‘recent works on investment decisions … suffer from the neglect of Fisher's great contributions’. However, Modigliani and Miller would be the writers credited to have launched the corporate finance theory that has attributed several Nobel prizes in economics (Cardao-Pito, 2017a, 2017b, 2021a; Harris and Raviv, 1991; Myers, 2001; Pasinetti, 2012). Still, Modigliani and Miller had simply redecorated Fisher's framework as admitted by Miller (1988) himself (see also Cardao-Pito, 2021a).

Following this Fisherian lead, research papers, classes and didactic textbooks in financial economics/finance specifically define the value of a firm (or any organisation) as the set of future discounted cash flows payable to the owners of the firm's equity securities. This valuation procedure is generally called the ‘net present value’ or ‘net present worth’, an expression already used by Fisher (e.g. Brealey et al., 2010; Cardao-Pito, 2017a, 2017b; Damodaran, 2003; Ross, 2010). Every year, thousands of students at economics and business schools take courses where they are taught mainstream financial economics (Cardao-Pito, 2017a, 2017b; Fourcade and Khurana, 2013), conveying a theory that, as explained above, is biased towards organisations’ owners/shareholders. Undeniably, mainstream accounting theory is frequently linked to mainstream financial economic theory, as assumed by their major proponents: ‘This methodology (of economics, finance, and science generally) has been successful in accounting research and we feel no need to apologise for it. ‘Under this methodology, a theory is not discarded merely because of some inconsistent observations’ (Watts and Zimmerman, 1990: 150).

The second feature is the belief that efficient market prices are perfect recorders of all available information; that markets are capable of processing all information to identify organisation's future cash flows and discount rates, asset or liability, as in the efficient market hypothesis (Fama, 1970, 1990, 1998; Previts and Merino, 1998). When delivering his Nobel Prize lecture, Fama (2014: 1471) recognised Irving Fisher's contribution to an initial market efficiency hypothesis: I turn to bonds to study Irving Fisher's (market efficiency) hypothesis that rt + 1, the time t interest rate on a short-term bond that matures at t + 1, should contain the equilibrium expected real return, E(rt + 1), plus the best possible forecast of the inflation rate, E(πt + 1).

The expression (market efficiency) is from Fama (2014: 1471). However, in his initial writings proposing this hypothesis, Fama (1970, 1990, 1998) also did not cite Fisher. Curiously, when evidence against this hypothesis was being compiled by behavioural economic studies, Fama (1998, 2014) employed a similar defence to Fisher's (1930a), on the lines that we could not be sure whether markets are efficient, because this possibility cannot be tested as we could not be sure what the correct prices would be. Evidently, this is a lame excuse, as they claim to demonstrate that markets operate according to their descriptions.

Mainstream economists, the mainstream accounting researchers who follow them, and regulators who set standards, apparently all have an idealised view of the market, wherein markets are complete and always in perfect competitive equilibrium (Whittington, 2010). Mainstream economic and accounting theories therefore deny the possibility of market failure, even when diverse indicators reveal that a serious economic crisis has occurred (Cardao-Pito and Ferreira, 2018a, 2018b; McSweeney, 2009). Thus, rather than being empirical or realistic, regulators and mainstream economic theorists seem to rely on a set of beliefs that ignore the complexity of social structures and human actions (Callon, 1998; Cardao-Pito, 2012, 2016, 2021b; Granovetter, 1985; Polanyi, 1957).

Decision-usefulness researchers

Positivist decision-usefulness researchers currently dominate accounting research. These researchers have aimed to reorient accounting towards providing useful information to those taking decisions based upon (Fisherian) economic value, that is, speculative discounted projections of future cash flow models. Decision-usefulness researchers fully endorse Fisher's valuation ideal (using our test devised above to classify someone as Fisherian). Importantly, the decision-makers preferred by this group of researchers are investors of capital seeking to increase their wealth through future income. These potential shareholders/owners whose interests are preferred in Fisher's theory of value and prices are the same as those followed in mainstream economics.

There are several ironies in the decision-usefulness researchers’ contributions to accounting. Their initial proponents claimed to be reacting against normative accounting theories, which they have gone so far as to accuse of being non-scientific (Mattessich, 1995; Whitley, 1988). Following this, it would be impossible to define what must be the purpose of accounting and how should accounting be conducted. Nevertheless, what decision-usefulness researchers see as advanced quantitative tools from mainstream economics could, they argue, produce scientific research in accounting. Ironically, while stating to be seeking empirical regularities and being against normative theories, decision-usefulness researchers have reinforced Fisher's normative theory that gives precedence to shareholders/owners’ interests (Bryer, 2013a, 2013b, 2021; Cardao-Pito and Ferreira, 2018a). However, as shown earlier, various normative theorists have contributed to the prevalence of Fisher's theory in accounting because they accept Fisher's ideal as valid for valuation purposes. Thus, while decision-usefulness researchers are directly influenced by capital accounting theorists such as Canning, Coase or Hicks, and by mainstream economists like Modigliani, Miller and Fama, they also take advantage of various normative theorists’ acceptance of Fisher's valuation ideal.

The Study Group on Business Income, organised in 1948 by the American Institute of Accountants (they became AICPA after 1957) is perhaps foundational to the decision-usefulness movement. Various prominent members such as Alexander (1950), Bronfenbrenner (1950) and Fabricant (1950) assumed a Fisherian perspective. They took the view that to businessmen (decision makers), only the economic (i.e. Fisherian) concept of capital-income is relevant for conducting business affairs. This statement was based on their belief that accountants would want to avoid responsibility for subjective judgements because they were bounded by objectivity and conservatism. However, businessmen would later accept the need to make subjective judgements based on (Fisherian) economic value to make decisions, given that market prices would be explained by discounted cash flow-type models built on projections of future income.

These presuppositions, as described earlier, have no support in logic or empirical evidence. According to Bryer (2016), during this period business leaders of large organisations launched the ‘Free Enterprise Campaign’. This campaign was also based upon Fisher's theory, without however citing the discredited investor-economist As Fisher's normative theory is in favour of investors’ interests, business leaders used its arguments against other groups of stakeholders, and, specially, workers’ unions who later themselves accepted Fisher's view (Bryer, 2016). However, when the AICPA Study Group on Business Income was launched, Fisher's theory was again at the centre of another important normative dispute.

The framework developed by the AICPA study group would be refined into a theory of accounting for investors by Staubus (1961: 11 cited by Zeff, 2013). The study group suggested that the ‘purpose of accounting is to provide information which will be of assistance in making economic decisions’, which would be related to times and amounts of future cash receipts as a result of investment relations, as in the Fisherian view. Contemporaneously, Moonitz (1961) was strongly influenced by Fisher and Canning when he suggested a set of what he termed: Basic Postulates of Accounting (Most, 1977). His work was also published by the AICPA. Postulate A-1 and C-5 see the purpose of accounting quantification and disclosure as to assist ‘rational economic decisions’, as in the Fisherian framework. Postulate B-2 claims that accounting should be founded on market prices, which could be explained by expectations of future transactions as Fisher had suggested: ‘Accounting data are based on prices generated by past, present or future exchanges which have actually taken place or are expected to’ (Moonitz, 1961: 28).

Later, Sprouse and Moonitz (1962) suggested a framework to implement Moonitz's (1961) postulates for accounting. Certainly, they received antipathy from SEC and other researchers for departing from historical costs (Zeff, 1999, 2013). Sprouse and Moonitźs proposal suggested the use of replacement costs for inventories, plant and equipment, and discounted present values for cash and its equivalents. However, they were not completely certain as to what extent the Fisherian framework could be applied. Current values were restricted to claims about future cash flows that are certain (e.g. those of a financial bond), not speculative estimates for all accounting items: If the claims to money are uncertain as to time or amount of receipt, they should be recorded at their current market value. If the current market value is so uncertain as to be unreliable, these assets should be shown at cost. (Sprouse and Moonitz, 1962: 57)

Following these leads, Beaver (1968) suggested that accounting data evaluation must be according to the criterion of predictive ability (ability to predict events of interest to decision-makers), clearly aligned with Fisher's theory of value and market prices. This agenda was followed by several other studies at that epoch (e.g. Ball and Brown, 1968; Beaver, 1968; Gagnon, 1967; Gordon et al., 1966; Sterling, 1965). In fact, a committee of academics of the American Accounting Association (AAA) had already proposed redirecting the attention of accounting theory towards the ‘decision-usefulness’ of financial statements to owners/investors who need to make economic decisions (based upon future cash flows) (Zeff, 1999: 96; see also AAA, 1966, 1977).

The purpose of providing expedient information based upon Fisher's value for decision makers (who are or might be investors) was at the time in open conflict with the SEC and practitioners who preferred historical cost accounting to present value estimates. Likewise, this focus was not accepted by many normative theorists (e.g. Chambers, 1980, 1993; Ijiri, 2005). However, the decision-usefulness researchers’ reasoning alleges that normative accounting standards are impossible because they are dependent upon individual interests and beliefs (Demski, 1973). Hence, decision-usefulness researchers claim to eliminate normative objectives in understanding accounting's purpose or how accounting affairs should be conducted. Instead, this group suggest another purpose, namely, the ‘decision-usefulness’ of accounting information.

Years later, Watts and Zimmerman (1978, 1979) merely rebranded this already established research agenda as ‘positive accounting theory’ which had been in existence for decades. Nonetheless, Watts and Zimmerman certainly invoked a certain missionary spirit for this agenda. According to them, this research field's major purpose was to explain and predict corporate behaviour in order to prevent corporate lobbying over accounting regulations. Allegedly, normative accounting theories were developed from a ‘market’ of providing excuses for political/regulatory options, while attending to different interests and beliefs, rather than those of decision-usefulness positivists who went so far as to promise their research agenda would not be used to justify changes in accounting standards (Watts and Zimmerman, 1978, 1979). This suggests another irony, because this group had fundamental importance in promoting Fisher's normative theory that is currently inscribed upon fair value regulations.

A key strategy has been to make ad hominem attacks on proponents of theories not exclusively based on mainstream economics and, therefore, on mathematical/ quantitative methods of reasoning and utility functions. As the argument goes, only an accounting theory centred on self-interest (i.e. explained by utility functions based on Fisher's value concept, which are prevalent in mainstream economics) could provide a set of predictions consistent with observed phenomena. All other theories would allegedly be serving the vested interests of groups benefitting from regulatory change (Cardao-Pito, 2021c; Chabrak, 2012; Demski, 1973; Watts and Zimmerman, 1979).

For decision-usefulness researchers, price replica models generate discounted projections of eventual future cash flows as in Fisher's theory of value. Variations of the Ohlson model (Feltham and Ohlson, 1995, 1996; Ohlson, 1995, 1999, 2000), a discounted cash flow/net present value model, have been very influential in mainstream accounting. Thus, these models may have been influential on the norms set by accounting regulators. Decision-usefulness researchers consider projections of discounted cash flows to be accurate values, while declaring that several ‘value-relevant’ studies concluded that historical transaction (cost) accounting values are not relevant for market values (e.g. Barth et al., 2001; Barth and Landsman, 1995, 2010; Brown et al., 1999; Brown and Sivakumar, 2003; Collins et al., 1997; Holthausen, and Watts, 2001; Song et al., 2010; Venkatachalam, 1996). The prudence principle conventionally followed in accounting of anticipating the registration of losses but not uncertain future profits/income is even dubbed as ‘conservatism’, which must be explained though the light of Fisher's theory of value and prices (e.g. Hsieh et al., 2019; Watts, 2003a, 2003b) 4 . In these debates, likewise, Fisher's writings are not cited. These studies’ implicit conclusions are as follows: (i) historical accounting values are not market values; and (ii) because market values are ‘right’, historical accounting values are not value relevant. Therefore, such discussions are rhetorically constrained by Fisherian decision-usefulness accounting theory. These studies maintain that markets are efficient processors of all information, and that there are models based on discounted projections of future cash flows that can explain/predict market prices.

These same explanations, which had been suggested by Fisher many decades earlier, can be found in fair value accounting (Cardao-Pito and Ferreira, 2018a, 2018b). In the same manner that Fisher provided the normative theory that underlies fair value accounting standards (Bryer, 2021; Cardao-Pito and Ferreira, 2018a, 2018b), he provided the normative theory that underlies the writings from decision-usefulness researchers. Indeed, although Watts and Zimmerman explicitly promised that decision-usefulness research could not be used to justify accounting standard modifications, that promise was broken. Decision-usefulness theories following Irving Fisher are inscribed in ‘fair value’ accounting norms. Nevertheless, there is a lack of any systematic evidence that discounted cash flow models can accurately predict or explain market prices, and vice versa, or be adequate for accounting regulations (Basilli and Zappia, 2012; Bougen and Young, 2012; Bryer, 2021; Callen, 2015; Cardao-Pito, 2012, 2016, 2021a; Cardao-Pito and Ferreira, 2018a, 2018b; Mouck, 1992; Shiller, 1981, 1984, 2005).

Accounting journal rankings

Currently, the editorial boards of prominent journals are dominated by graduates of elite schools championing a mainstream economics-based positivist research paradigm. These individuals shape the agenda in accounting research (Lee, 1997; Williams et al., 2006). With a few notable exceptions, such as this journal and others, the Association of Business Schools (ABS) gives much higher rankings to journals based on decision-usefulness accounting theory compared to other publications, thereby further constraining the discussion of accounting issues (e.g. Andrew et al., 2020; Donleavy, 2022; Gerdin and Englund, 2019; Hussain et al., 2020; Rowlinson et al., 2015; Tourish and Willmott, 2015). This control over research resources has real effects on accounting scholars’ careers, who can be advised to adopt decision-usefulness perspectives or else not receive resources (e.g. Hopwood, 2008; Hussain, 2011; Hussain et al., 2020; Sangster, 2011). The refusal of decision-usefulness researchers to accept any other theoretical approach may be a factor in the dominance of Fisher's theory. By completely disregarding alternative theories and perspectives, mainstream researchers create an echo chamber environment in which their arguments go unchallenged.

Standard setters

Regulatory changes have resulted from a series of cross-border developments, which originated from a conjuncture of financial globalisation and a particular mix of international institutional configurations and capacities (Bhimani, 2008; Posner, 2010). Many national governments began to outsource (or privatise) the production of accounting norms to single private agencies (Bengtsson, 2011; Oehr and Zimmerman, 2012; Sunder, 2011), which have become very powerful. For instance, the IASB produces accounting norms that are used by all countries in the European Union, as well as Australia, Canada, Hong Kong, India, Japan, Russia, Singapore, South Africa, Taiwan, Turkey, and other countries. The FASB in the 2000s produced accounting norms for the United States and was collaborating with the IASB to produce common regulations. These major regulators may have been influenced by decision-usefulness accounting and economic research to change accounting regulations, with little debate outside specialised financial circles (Bromwich, 2007; Masocha and Weetman, 2007; Mehrpouya and Salles-Djelic, 2019; Mouck, 1992; Power, 2010; Pucci and Skærbæk, 2020; Ravencroft and Williams, 2009; Zhang et al., 2012).

The ascendency of the decision-usefulness agenda in regulatory bodies that set accounting standards, such as IASB and FASB, is rather well documented and need not be repeated here. It is currently reflected in the conceptual framework that defines regulators’ views about the purpose of accounting (Bhimani, 2008; Mehrpouya and Salles-Djelic, 2019; Pelger, 2016; Power, 2010; Ravencroft and Williams, 2009; Young, 2003; Young and Williams, 2008; Zeff, 2013, 1999).

Furthermore, it has been well documented that IASB and FASB's staff members have been continuously seeking to persuade corporations, practitioners, researchers, and other stakeholders that the regulators’ work is valuable, appropriate, useful, ‘right’, and supported by market imperatives (Bhimani, 2008; Young, 2003; Young and Williams, 2008). Undeniably, real-politic and the composition of Boards’ staff and members can materially affect the course of standard-setting projects (Pelger, 2016: 15).

Hypothetical explanatory history of ideas model and limitations

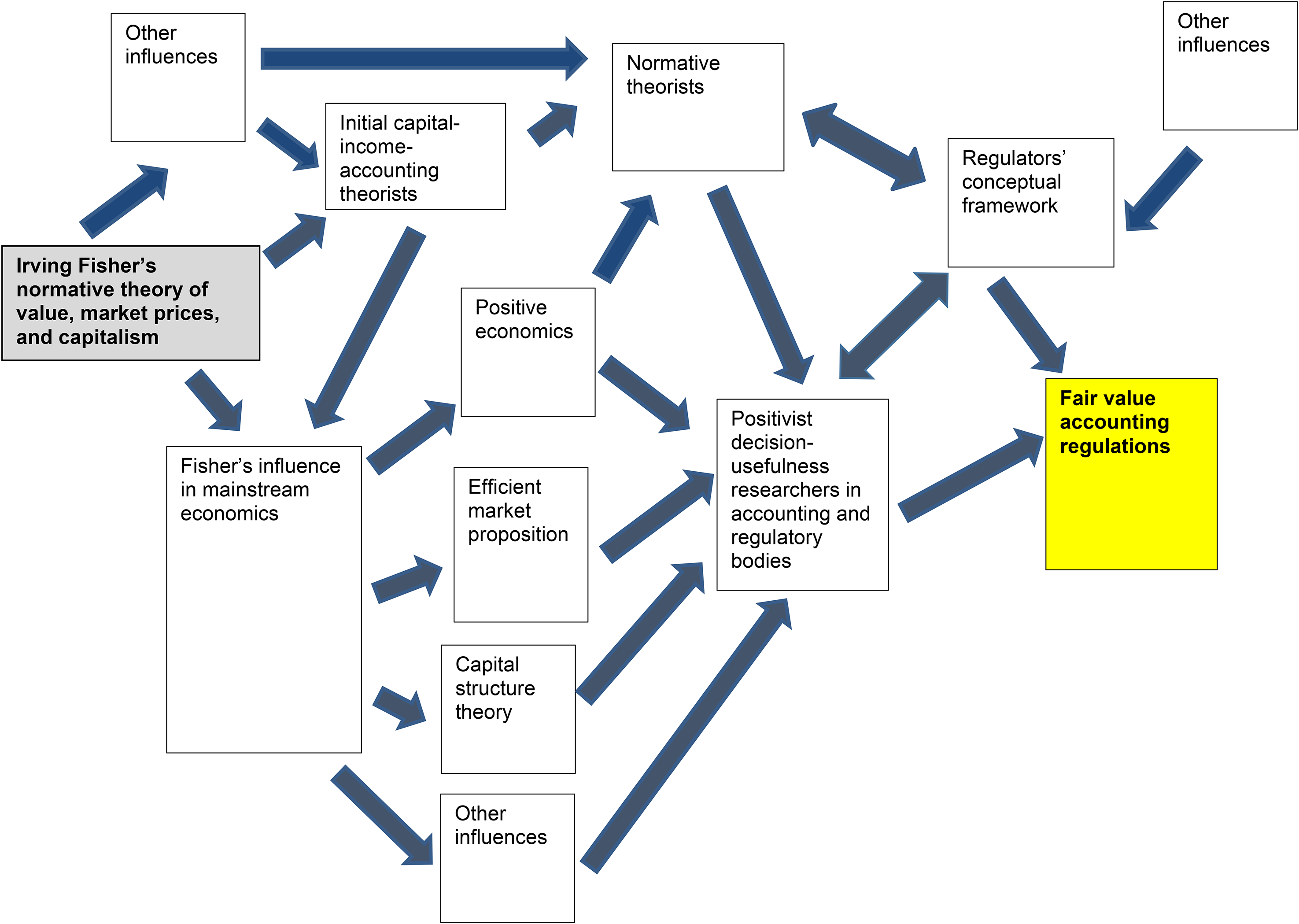

Using Bryer's (2021) test for identifying Fisherian researchers and their writings, we have highlighted key historic landmarks where we can be sure that Fisher's theory is being promoted and diffused. At this stage, we cannot identify all influences, key moments and events. Moreover, our study is focused on writings in English. Yet, even for the English-speaking world we cannot find more than one century of scholarship that contains ideas advanced by Fisher. Naturally, we are constrained by space limits. Furthermore, we cannot indicate the exact point where Fisher's authorship has ceased to be acknowledged, while his ideas have kept being embraced. Nonetheless, we hope to contribute to the curiosity of other researchers who may wish to further clarify these important themes. Figure 1 summarises this article with a hypothetical exploratory history of ideas that is a description of the lengthy, complex and sinuous path taken by Irving Fisher's theory to contemporary dominance in accounting theory, practice and regulations.

Hypothetical history of ideas model regarding the pathway followed by Irving Fisher's theory to reach fair value accounting regulations (Source: The Author).

As noted, there might be other factors and influences not accounted for in Figure 1. However, this figure contains elements that can be demonstrated, as exhibited above. Fisher had a direct influence on capital-income accounting theorists working in the 1920s and 1930s. Moreover, Fisher has had a great impact in areas of mainstream economics with direct bearing on financial accounting such as positive economics, the efficient market proposition and capital structure theory. Curiously, normative accounting theorists have played a perhaps unintended role in promoting Fisher's theory. While several normative accounting theorists were against the use of Fisher's ideal in accounting practices believing it was subjective and lacked practical applicability, they, nonetheless, accepted Fisher's ideal as valid for valuation purposes or ‘accounting for the future’ without rejecting it because of its limitations and lack of empirical support. The normative theorists were far from the current views that see Fisher's theory as a toxic theory of accounting and economics (Bryer, 2013a, 2013b, 2021; Cardao-Pito, 2020; Cardao-Pito and Ferreira, 2018a, 2018b). Nevertheless, various normative theorists have helped to legitimise Fisher's theory in accounting as a possible explanation for value, prices and capitalism. Positivist and decision-usefulness accounting theorists in accounting began from there. They in effect claimed instead that Fisher's theory was the only possible theory for accounting and economics. That is, Fisher's valuation ideal should not be limited to valuation instances, but fully applied to accounting practices, even though those claims are presented without any reference to Fisher's himself. Along the way, positivist and decision-usefulness have claimed to be against normative theories in accounting. Decision-usefulness researchers, however, claim to support not normative claims but ‘true and fair views’ of accounting, which is an absurd claim given that Fisher's theories currently underly accounting standards, norms and regulations (Cardao-Pito and Ferreira, 2018a, 2018b). Importantly, the prevalence of Fisher's theory has not been merely a scientific endeavour because it seems also to be related to the political control wielded by advocates for Fisher's theory on accounting departments, research rankings and accounting standard setters. Moreover, it might also have something to do with their intolerance regarding alternative explanations for accounting and economic phenomena.

Are there socio-political reasons for the prevalence of Fisher's theory in accounting?

As demonstrated above, Fisher's irrelevance hypothesis is no longer viable. Likewise, the näive view that using Fisher's valuation ideal merely provides a descriptive analysis of prices, markets and capitalism is no longer acceptable in either accounting or economics. Fisher's theory is undeniably normative because it prefers the interests of owners/shareholders over those of all other stakeholders. By inspecting textbooks in financial economics, Cardao-Pito (2017a: 369) was able to explain the three unproved rhetorical premises that constitute this normative theory: 1) The ‘correct’ equity/stock prices are equal to future cash flows that are payable to the organizations’ owners/shareholders. 2) The purpose of the firm and its managers is to maximize the value of the equity/share prices. 3) Hence, their purpose is to maximize the cash flows (wealth) payable to owners/shareholders.

Although none of these three conjectures have been clearly demonstrated or empirically supported, they ground the normative theory that underlies today's mainstream economics and accounting (Cardao-Pito and Ferreira, 2018a, 2018b).

Fisher's theory guides the project of transforming accounting into the language of investors/shareholders, ignoring the interests of all other stakeholders. For instance, workers, suppliers, customers, governments, communities and so forth. In fact, Fisher's theory is presented by its proponents as superior to any cost-based theory of value, which traditionally informed accounting. However, by advocating the elimination of concerns related to material costs, or to profit and loss accounts that articulate with balance sheets (Bryer, 2013a, 2013b), proponents of Fisher's accounting theory also undermine conversations about how owners/shareholders may capture the surplus value that results from the difference between revenues and costs.

Bryer (2013a, 2013b, 2021; see also Tobin, 2005; Weinstein, 1968) suggests that Fisher developed his theory in response to the economic theory that at his time appeared to most threaten the interests of investors/shareholders, namely, Marxism. In Marxism, investors/shareholders are often described as being part of the capitalist (or bourgeoisie) class. Indeed, the United States was developing fast and perhaps looking out for an economic ideology. The events of the Russia Revolution in 1917, subsequent creation of the Soviet Republics, the popularity of Marxism in countries such as Germany, and some non-negligible support back home in the United States, must have certainly impressed the economic and social United States elites. These events may help explain the support Fisher's theory has received from elites in the United States and other Western countries before the crisis of 1929. Fisher could have been considered as the economist who had provided an economic theory of accounting that could react not only against Marxism, but also other labour-based theories from Adam Smith and David Ricardo from which Marxism is derived (Cardao-Pito, 2020, 2021b). Undeniably, Fisher's theory puts accounting at the service of the investors/shareholders.

Furthermore, the aim of providing an answer to labour-based theories could certainly help explain why several mainstream economists, capital accounting theorists, decision-usefulness researchers, or the ‘Free Enterprise Campaign’ (Bryer, 2016) described above were so keen to return to Fisher's theory without citing Fisher. Although his reputation had been tainted, Fisher had formed an effective rhetorical defence against labour-based theories, and thus, claims that could be based upon the later. Indeed, most of the twentieth century was spent with a cold war among economic regimes, where the two major underlying economic theories of the two foremost regimes were mainstream economics partially derived from Fisher's ideas and Marxism (Bryer, 2013a, 2013b, 2021; Cardao-Pito, 2021a, 2021b).

Nonetheless, while Fisher's theory is still highly effective in defence of investors/shareholders’ interests, at some points, and to several decision-usefulness researchers, the rivalry to Marxism or other labour-based theories may have ceased to be a motivation to adopt Fisher's economic theory of accounting. In the same manner that many contemporary researchers do not know how Fisher was important for their own work, they may also not know the basics of Marxism. Moreover, they might have only a rough understanding of cost-based accounting systems, which is prejudiced by their education. Most contemporary decision-usefulness researchers have been trained in mainstream economics and mainstream accounting, which are heavily based on Fisher's theory. Furthermore, they can work their entire careers without any awareness of other economic theories. What is worse, they can confuse Fisher's theory with the economy and society.

One must also note that, in the last century, Fisher's theory of accounting and economics has been highly effective against Marxism and other labour-based theories. Yet, the theories and practices involving costs in accounting precede Karl Marx, David Ricardo, and Adam Smith by many centuries. Labour-based theories, such as Marxism, remain relevant today. However, we may have another option than that of simply returning to labour-based theories because it remains possible to try and create a new theory (Cardao-Pito, 2021b).

Conclusion

In this article, we have refuted the hypothesis of Fisher’s irrelevance for accounting thought, which has appeared in previous research. However, this refutation shows that there is still much to research and learn about Fisher's extraordinary impact on contemporary accounting. Mainstream accounting theory is not based upon market imperatives, or a theory with sustained insights about how markets function as implied by decision-usefulness researchers. Instead, mainstream accounting theory is based upon Irving Fisher's unproved and fragile theoretical framework. His capital-income theory advocates (without evidence) that discounted cash flow models can explain value, prices, markets and capitalism. Testing the theory requires identifying the theory.

Fisher's theory must not be assigned only to Irving Fisher. Rather, it must be identified among its many subsequent adopters and developers. Nonetheless, current leading advocates of Fisher's theory in accounting, namely, decision-usefulness researchers and standard setters, generally fail to acknowledge Fisher's influence. This strange situation may occur because those advocates have obtained Fisher's framework from secondary sources that also did not directly acknowledge him, such as initial capital-income-accounting theorists, normative accounting theorists, and mainstream economists. Of foremost significance seems to be the subalternity of mainstream accounting research in relation to mainstream economic research. This subalternity may be a key channel to diffuse the Fisherian framework in accounting. To a substantial extent, fair value accounting is a methodology that conforms to mainstream economic theory.

To substantiate our claim, we have demonstrated that key capital income theorists such as Canning, Coase and Hicks, and key mainstream economists such as Fama, Friedman, Modigliani and Miller, and Samuelsen, have also adopted Fisher's valuation ideal, and thus his theory about prices, markets, and capitalism. Furthermore, we have shown that various normative accounting theorists have a key role in promoting the Fisherian valuation ideal. Generally, normative accounting theorists tried to solve major questions in accounting with a special emphasis on accounting measurement. Yet, several of them have pursued a distinction between measurement and the (Fisherian) valuation followed in the separate discipline of economics. However, they have accepted Fisher's ideal for valuation purposes, which has contributed to legitimising Fisher's theory. Reacting against normative theorists, decision-usefulness positivists have claimed to be against normative theories. Accordingly, they would bring to accounting the advanced quantitative research tools from mainstream economics, where Fisher's theory was already dominant. However, their stance against normative theories is illusory. On one hand, they agreed with normative theorists that Fisher's ideal would be adequate for explaining valuation exercises. On the other hand, in practice, decision-usefulness positivists are the prime advocates of Fisher's theory of value, prices, markets, and capitalism, which is indisputably normative. Besides being inscribed in real accounting norms, it prefers the interests of one group of stakeholders, namely shareholders/owners.

While we have not completely explained why Fisher's ideas are inscribed in fair value accounting standards, the popularity of Fisher's theory in mainstream accounting and economic research must be included in the explanatory set. Our exploratory history of ideas sought to provide a helpful framework for future research willing to return to this important question about how Fisher's theory has become dominant in accounting theory, regulations and practice. Although the field is populated by Fisher's framework, the omission of his name is perhaps what is more impressive in his extraordinary influence in both accounting and economics. Furthermore, it remains unexplained why accounting and economics should adopt Fisher's normative conceptions of market, value, prices, markets, or capitalism. Likewise, it remains unexplained why so many studies and regulations use Fisher's theory without acknowledging him. Moreover, much is left to be done in terms of a socio-economic history of Fisher's theory in accounting and economics.

By identifying the origins of this highly influential theory, we may better address its dismal empirical and logical weaknesses. The taken-for-granted attitude in regard to mainstream Fisherian concepts is indeed dangerous and deleterious to the intertwined research projects of decision-usefulness accounting, and accounting derived from mainstream economics.

Footnotes

Acknowledgements

The author wishes to acknowledge the late João da Silva Ferreira, Carolyn Fowler (the Editor) and two anonymous referees for their comments and suggestions.

Funding

The author disclosed receipt of the following financial support for the research, authorship, and/or publication of this article. This work was supported by the ADVANCE Research Center at ISEG, and the Portuguese national funding agency for science, research and technology (FCT - Fundação para a Ciência e a Tecnologia, I.P) (grant number UIDB/04521/2020).