Abstract

This study examines the centrality of ethics within editorials published in the Canadian Institute of Chartered Accountants’ professional journal, CA Magazine, over the 1912 to 2010 period. Starting from the twin assumptions that editorials speak about appropriate professional behavior using a variety of words such as ‘ethics,’ ‘conduct,’ and ‘codes,’ and that appropriate professional behavior is situational, we use topic modeling techniques to identify these dimensions of ethical discourse. We then use social network analysis methods to map the position and centrality of ethics within the editorials across time. The results show that enunciations about appropriate professional conduct are broader than simply enunciations using the word ‘ethics’. The results also highlight that ethical utterances become more central, not less central, over time.

This study examines the centrality and historical trajectory of ethical utterances within professional narratives. Starting from Bakhtin’s (2013) notion of a speech genre and prior research on ethical narratives (Preuss and Dawson, 2009; Statler and Oliver, 2016), we examine how utterances about ethics are part of a larger professional narrative that centres around norms of conduct, norms of competence and the role of education in producing a technically competent and ethical professional practitioner. Our data consist of 43,060 sentences from the editorials published between 1912 and 2010 in the Canadian Institute of Chartered Accountants’ (CICA's) professional journal, CA Magazine. The provided analysis shows how ethical utterances are positioned vis-à-vis other speech genres as well as how the centrality of the ethics speech genre increases over time.

The Canadian public accounting profession pre-dates the American profession: the Quebec provincial association was founded in 1879 and was the first formal accounting association in Canada and the United States (Murphy, 1993). The national umbrella association, which was initially known as the Dominion Association of Chartered Accountants and later the Canadian Association of Chartered Accountants (CICA), launched the CA Magazine in 1911 with the aim of unifying a geographically dispersed membership. As Creighton (1984: 69) notes, the magazine provided the Canadian public accounting profession ‘with a vehicle for expressing its views, educating its members, and influencing the development of accounting thought in Canada.’ The readership for the CA Magazine grew steadily over the next century as the CICA membership continued to grow. The CA Magazine editorials chronicle this membership and readership growth: there were 2,000 members in 1932, 6,800 in 1947, 15,000 in 1959, 45,000 in 1979, and 55,000 in 1995. During 2010, the CICA announced the start of formal merger discussions with the industry-based Certified Management Accountants of Canada, and the rival Certified General Accountants of Canada (Richardson and Kilfoyle, 2012). These merger discussions were completed by 2014 and a new umbrella designation, the CPA, was adopted. In keeping with these institutional changes, in 2014 CA Magazine changed its name and broadened its focus: being ‘built around the diverse talents, skills and perspectives’ of the new membership (CPA Canada, 2021). The current study stops in 2010, which was the year in which the merger discussions were announced.

The analysis makes three contributions to our understanding of the history of professional accounting association ethics. First, the analysis shows the usefulness of viewing ethics as a speech genre that consists of a common subject matter and way of speaking about norms of conduct. This view emphasizes that ethical utterances are a type of narrative and that conduct enunciations are broader than simply enunciations using the word ‘ethics.’ The idea that ethics is a narrative is not surprising since professional associations, given the multiplicity of settings in which practitioners work, require multiple ways of articulating the importance of ‘appropriate’ conduct. As prior research notes (cf. Litschka et al., 2011), ethics is relational and situational in that it involves appropriate ways of relating to and interacting with other groups of people in specific types of situations. Within the accounting profession, these other groups include clients, students, other members and the professional association itself (cf. Abbott, 1983), whereas the situations include auditing as well as consulting services.

Second, the study illustrates the importance of examining the intra-textual aspects of ethical utterances. Prior research suggests that norms of conduct and competence are central to professionalization processes and that education both ensures adequate levels of technical competence and inculcates norms of conduct: including helping future members; first, recognize who will be impacted by professional accounting work and, second, adjusting the level of competence to ensure that sufficient competence is exercised given the foreseen users (Gaa, 1994). Individually, utterances about ethics, competence and education help communicate this information but this communication is always a semiotic process that involves the intra-textual positioning of ethics vis-à-vis utterances about competence and education. Furthermore, the illocutionary force of the ethics speech genre depends on the centrality of the genre within the broader professional narrative. The provided analysis illustrates how the ethics speech genre is positioned within the professional narrative and how this positioning (and centrality) changes over time. Consistent with the analyses of Gorman and Sandefur (2011: 287) and Larson (2018: 36), our study highlights that ethical utterances do not diminish in importance but rather become more central over time as the scope and complexity of professional work increases.

Finally, the analysis complements recent research by Ferri et al. (2018, 2021), illustrating the usefulness of computer-assisted machine-learning-based approaches to the study of accounting history. Computer-assisted approaches are becoming increasingly popular because these methods help to both organize and systematically analyze large-scale corpuses of data (cf. Dyer, Lang and Stice-Lawrence, 2017; Loughran and McDonald, 2011; Neu et al., 2020; Suddaby, Saxton and Gunz, 2015). The current study uses a Latent Dirichlet Allocation (LDA) topic modeling algorithm (cf. DiMaggio, Nag and Blei, 2013) to identify the individual speech genres that are part of a larger professional narrative and then utilizes computer-assisted social network analysis techniques to consider the positioning and centrality of the speech genres. This two-fold approach provides a systematic way to identify and analyze the ethical components of large-scale corpuses of textual communication.

Theoretical frame

Our starting point for thinking about ethics is Bakhtin’s (2013) linguistic work on speech genres. Bakhtin's work is useful because it stresses the importance of examining both the composition and trajectory of communication streams. For example, Bakhtin emphasizes the ways that narratives are constructed via inter-textual and intra-textual work involving speech genres and, at the same time, enjoins us to examine how the positioning and centrality of genres change over time. According to Bakhtin, such textual work is fundamental to communication in that it both brings the external environment into the speech genre and, in turn, aggregates upward thereby contributing to the drift and mutation of (professional) narratives. The remainder of this section outlines how Bakhtin's speech genre perspective is relevant to the current study.

For Bakhtin, utterances are the basic building block of communication. Utterances refer to strings of words that have a subject matter, mode of expression, and a definitive beginning and ending. Utterances are communicated by a social actor but, at the same time, an utterance belongs to and draws upon a pre-existing speech genre. Social actors grow up using a variety of speech genres in their communication activities and, thus, have a familiarity that allows them to construct an utterance that gives the appearance of being placed into a speech genre (Bakhtin, 2013: 78–79). It also results in the utterance answering, at some level, what preceded it within the communication stream as well as having the utterance speak to and be answerable by future conversation participants. The result of these communication processes is a stream of ‘similar’ utterances that share a common subject matter, group of words, and stylistic form.

While utterances are the building blocks of communication and a specific manifestation of a speech genre, they are but one strand of a larger (professional) narrative. Bakhtin (2013), for example, notes that a communication stream, like the CA Magazine editorials that we examine, consists of multiple distinct yet overlapping speech genres (p. 62). It is the amalgam of these genres, and the ways that they play off each other, that helps to construct a professional narrative (p. 73). Bakhtin, and the linguistically oriented researchers that have followed him, use the term intertextuality to refer to the inter-textual and intra-textual ways that different speech genres are enlisted, juxtaposed and modified in the processes of communication (cf. Briggs and Bauman, 1992: 132).

Prior research on the professions suggests that enunciations about norms of competence, norms of conduct and education are fundamental to professionalization processes since the maintenance of professional privilege depends on convincing influential stakeholders that a professional association provides socially relevant cognitive expertise that will be exercised in an ethical manner (Chandler, 2017; De George, 1990; Gaa, 1994; Sonnerfeldt and Loft, 2018; West, 1996). More specifically, it is the ethical exercise of socially relevant expertise that allows professional accounting associations to both act, and claim to act, ‘for the public interest’ (cf. Dellaportas and Davenport, 2008). As Roberts notes, ‘public-interest objectives are to protect society by safeguarding the economic interests of clients and third parties, delineate client-profession relations, and orient the profession towards social responsibility’ (2010: 103).

This said, researchers such as Abbott (1983) emphasize that enunciations about norms of conduct must be viewed as something broader than simply communications that invoke the word ‘ethics’. While universal abstract words such as ethics, moral, duty, virtue, etc. both mean something to the speaker and communicate something to the audience, ethics is more fine-grained in that it is relationship-based as well as situational. Abbott notes that norms of appropriate professional conduct are centered around a series of social relationships and a series of different situations. Social relationships include relationships to the public, to clients, to the profession, to other members, and to students, whereas the different types of situations include auditing and consulting settings. Abbott's research encourages us to assume that discussions about appropriate professional behavior will both use multiple words to discuss appropriate behavior and will include situational words. We return to these twin assumptions in the subsequent methods section.

The view that ethics are simultaneously situational and relational is consistent with previous ethics-focused research (Chandler, 2017: 181; Sonnerfeldt and Loft, 2018: 522). Litschka et al. (2011: 475) note that managers, when confronted with an ethical dilemma, must first classify the situation before choosing an appropriate ethical decision-making basis (see also Hauser, 2006). Furthermore, the complexity of different situations and the uncertainty regarding the potential outcomes associated with different choices complicates both the classification of situations and the decision as to what constitutes appropriate conduct (Statler and Oliver, 2016: 93). Because of this, Statler and Oliver suggest that ethical narratives are used to help contextualize rule-based, ‘abstract’ ethical codes and to elaborate on the distinctions among situations (2016: 93). Indeed, the editorials in the CA Magazine that we subsequently analyze can be read as a professional narrative that attempts to make sense of what technical competence and appropriate behavior means in different professional accounting contexts. Following from the aforementioned previous research, we assume that the word ethics, by itself, provides little information about to whom one needs to act ethically, the types of behaviors that count as ethical in different situations, and the challenges to ethical behavior.

The notion of intra-textuality is the second aspect that we borrow from Bakhtin (2013: 117–118). At any moment in time, utterances about norms of conduct are intra-textual in that they co-exist with and are positioned vis-à-vis other utterances within an editorial. Of particular interest is the positioning of ethical utterances in relation to utterances about competence and education. As mentioned previously, competence and conduct are fundamentally inter-related in that professionals are expected to exercise technical competence in an ethically acceptable fashion. However, enunciations about education are equally important in that such utterances explain not only how students and members are expected to achieve these technical and ethical competencies but also what technically competent and ethically appropriate behavior looks like in different settings (Gaa, 1994). These two characteristics contribute, we think, to the continuing, vibrant academic conversation regarding whether the teaching of norms of competence and conduct is best accomplished by courses that integrate the technical and the ethical (Martinov-Bennie and Mladenovic, 2015; Molyneaux, 2004;) or by having a stand-alone ethics course (Dellaportas, 2006).

Like Bakhtin, prior ethics-focused research foregrounds the importance of intra-textual work. Preuss and Dawson (2009), for example, propose that texts should be viewed as forms of narrative that need to be read both horizontally and vertically. According to the authors, a horizontal reading ‘will look at the surface meaning of a narrative, where the analysis is concerned with the structural features of the narrative’ (p. 136). A vertical reading, in turn, ‘examines the plural meanings of the text and thus takes a more philosophical approach to the analysis’ (p. 140). Preuss and Dawson’s (2009) research is useful to the current study in that it both draws attention to the importance of examining the construction of ethical utterances and provides a concrete example of such an analysis. 1

Bakhtin's suggestion that speech genres are somewhat stable yet constantly changing is the final conceptual piece that we enlist. Bakhtin suggests that the dynamics of stability and change is connected to the micro-level intra-textual work of social actors and to events in the external environment that impact on the speaking habits of these social actors. External events have the potential to introduce new topics of conversation (i.e. speech genres) as well as to shift pre-existing ones (cf. Bonilla and Rosa, 2015). Consequently, the positioning and centrality of individual speech genres within a broader discursive narrative may drift and/or radically change over time.

Previous research on the professions (cf. Preston et al., 1997: 511; Murphy and Quinn, 2018: 94) suggests that these processes of drift and change may impact on professional narratives; however, there is some uncertainty as to whether this will increase or decrease the centrality of ethical utterances. Over the past century, public accountancy has become more commercial, with accounting associations actively seeking out new business opportunities that include the offering of new services as well as more technical versions of already existing services (Carnegie and Napier, 2010; Murphy and Quinn, 2018: 94). This expansion of jurisdiction has been accompanied by changes in the organization of professional firms and in the modes of partner remuneration to more firmly emphasize new business development (Cooper et al., 1998). With these changes in mind, researchers like Hanlon (1997) imply that commercialization decreases the prevalence of enunciations about ethics as accountancy becomes more a business and less a profession whereas others like Larson (2018) suggest that an expansion of jurisdiction changes how professional associations ‘produce the professional producer’ but that this does not necessarily result in norms of conduct becoming less important. Rather, as we noted previously, the prevalence and centrality of ethical utterances may actually increase as professional associations attempt to communicate to an increasingly diverse membership the increasingly complex nature of ethical behavior. Stated differently, it is the expansion of the sites of professional work and the differences as to what counts as appropriate professional behavior in these different sites that potentially increases the centrality of ethical utterances within professional narratives.

The study that follows draws upon Bakhtin's speech genre approach to study the positioning of ethical utterances within broader professional narratives. The suggestion that ethical discourse is broader than enunciations that directly use the word ‘ethics’ motivates us to view ethics as a type of speech genre that consists of patterns of speaking about norms of appropriate professional conduct and to attempt to identify these patterns of speaking. Second, it encourages us to explicitly consider how an ethics speech genre is positioned vis-à-vis other speech genres, especially speech genres about competence and education, since it is this intra-textual work that ultimately impacts on the salience and centrality of ethical utterances. Finally, a speech genre perspective enjoins us to examine how the positioning and centrality of ethical utterances change over time in response to changes in the external environment.

Our approach to studying the composition and centrality of ethical utterances is similar yet different from previous ethics-focused research. Like Preston et al. (1997) as well as Preuss and Dawson (2009), we are interested in reading ethical utterances horizontally and better understanding how such utterances are positioned. What differs in the current study is our focus on also reading these utterances across time and better understanding how centrality changes over time. The quantity of data that we examine—43,060 sentences over a 98-year period—encourages us to enlist a series of computer-assisted techniques to understand and analyze the composition and positioning of ethical utterances. While our approach cannot provide the same depth of detail as previous case-based studies (cf. Murphy and Quinn, 2018; Preston et al., 1997; Sonnerfeldt and Loft, 2018), it contributes to our understandings by making visible the patterns of intra-textuality as well as how the positioning of different speech genres changes over time.

Data

Editorials contained in the CA Magazine between 1912 and 2010 are our primary data. As mentioned in the introduction, 1912 was the first full year in which the CA Magazine was published. The magazine—with its structure of a lead editorial and then a series of articles— allowed the association to both provide timely information for public accountants and to communicate with government bureaucrats and security regulators (cf. CA Magazine March, 1983). The editorials convey the accounting association's public perspective on the important external and internal events of the day. They are more readable (i.e. less technical), timelier (they require less production lead time), and shorter than the regular articles. It is these characteristics that encouraged us to focus on the editorials rather than the technical articles contained in the magazine. We stopped our data gathering and analysis in 2010 because, as mentioned in the introduction, the CICA started a merger process involving two other accounting associations, one of which was an industry-based management accounting association. Our focus on editorials is consistent with prior qualitative research on the Canadian (cf. Everett et al., 2018; Neu, 2001; Neu et al., 2003) and American (Roberts, 2010) accounting professions.

We gathered the editorials by reviewing the physical or digital copies of the CA Magazine. Editorials were photocopied and then typed and/or scanned. Scanned editorials were processed with optical character recognition software and then reviewed for accuracy. The open-source statistical package R was then used to collate the editorials and to prepare the corpus of editorials for textual analysis. These gathering and initial processing steps resulted in a corpus of 980 editorials spanning the 1912 to 2010 period.

Consistent with prior research (cf. Sonnerfeldt and Loft, 2018: 525), we adopted a periodization approach. Given that we have 98 years of editorials, we wanted to divide the data into four periods of approximately 22 to 26 years. The four periods that we consider in the subsequent analysis satisfy both criteria. Period 1 (1912–1938) was a period of gradual growth for the Canadian public accountancy profession that was interrupted by the start of the Second World War (Creighton, 1984; Murphy, 1993). Period 2 (1939–1964) was a period of wartime changes and postwar growth (Simmons and Neu, 1996). Period 3 (1965–1985) was bookended by the failure of the financial institution Atlantic Acceptance Corporation in 1965 and the CCB and Northlands Bank in 1985. Period 4 (1986–2010) is the period that precedes the aforementioned mergers with other accounting associations. While our choice of periods is consistent with the aforementioned historical research on the Canadian public accounting profession, we do not attempt to directly assess the appropriateness of the chosen periods. Rather, we assume that the use of inappropriate periods would mitigate against finding differences across periods.

Method and results

Phase 1: Topic modeling method

Phase 1 of our research uses an LDA topic modeling technique to identify the latent thematic speech topics that exist within the corpus of editorials. LDA-based topic models are useful to the current study for four reasons (see also Ferri et al., 2018: 174–175). First, LDA makes visible latent themes within the corpus of texts that would have been difficult to identify without the use of computer-assisted techniques. Second, the LDA-generated topics highlight the narrative structure of the individual speech genres: including the groups of social actors (i.e. students, members, and regulators) that are involved in the speech genre story, and whether the ethical setting is specific or general. Third, the topic models are reproducible by other researchers in that the models rely on relatively standardized algorithms that are publicly available in the open-source statistical software R. Finally, LDA deals with empirical noise by locating extraneous words (and even scanning errors) into one or more unrelated themes (DiMaggio et al., 2013: 576). While this means that some topics will not be conceptually significant, this form of culling has certain advantages when dealing with large text corpuses. It is for these four reasons that we enlist a topic modeling approach. This approach has been used within previous accounting history (Ferri et al., 2018), ethics (Neu et al., 2020), and accounting (Bao and Datta, 2014; Dyer et al., 2017) research.

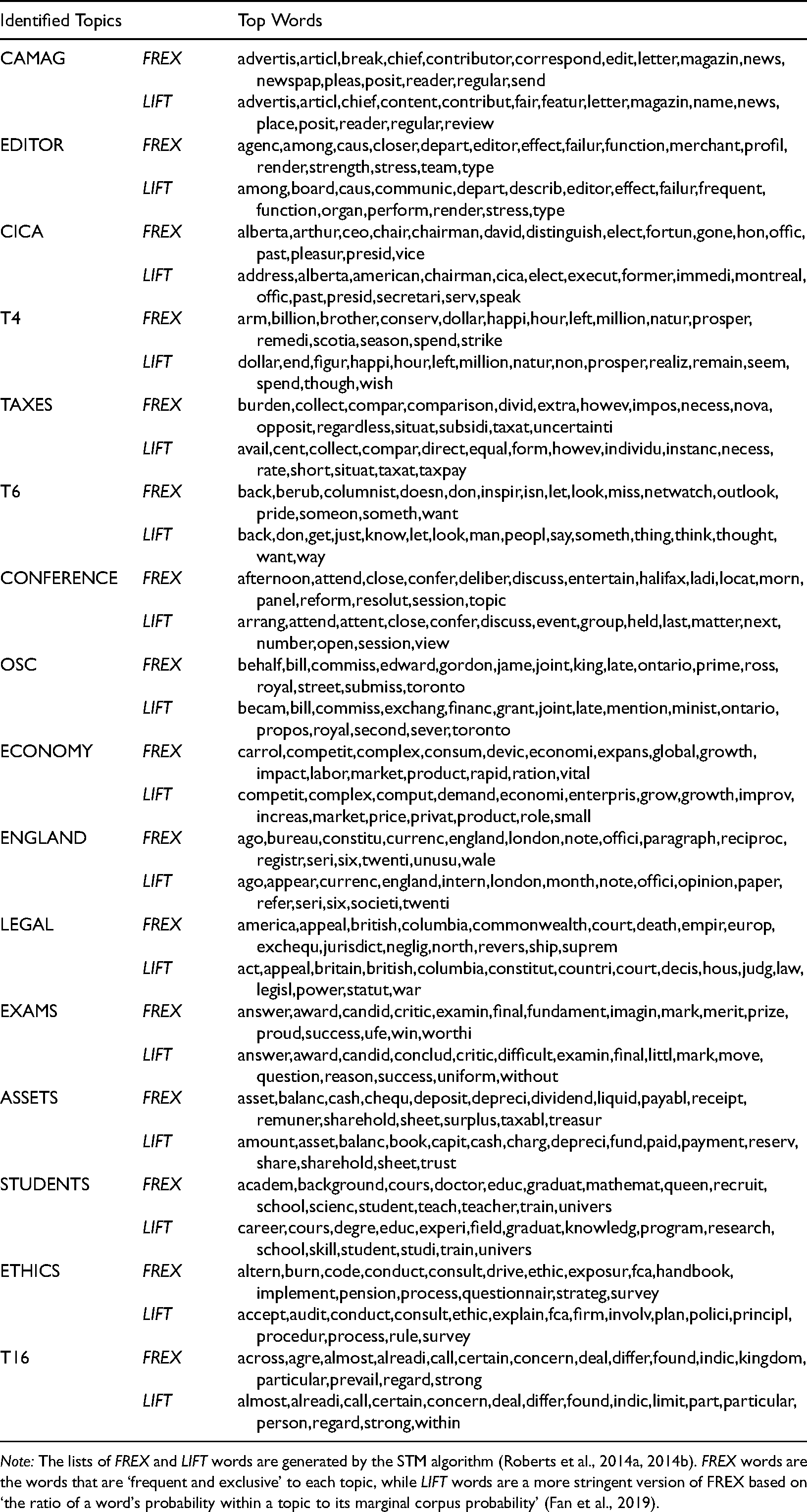

LDA topic modeling approaches adopt a Bayesian probabilistic perspective to discover the co-occurrences of word groupings. 2 The algorithms trade-off the assignment of words to a small number of topics against a small number of words that discriminate among topics (DiMaggio et al., 2013: 578). As a starting point for identifying the topics that were present in each editorial, we used R to partition each editorial into its component sentences. The LDA-based structured topic model (STM) algorithms of Roberts et al. (2014a, 2014b) that are available in R were then used to identify the topics. 3 The STM algorithm generates a listing of frequent and exclusive (FREX) words for each topic as well as a set of LIFT words, which is an even more stringent version of frequent and exclusive words (cf. Taddy, 2013; Fan et al., 2019). 4

The research decision to partition the editorials into sentences assumes that sentences are an empirical proxy for Bakhtin's notion of an utterance: that is, the basic unit of speech communication. 5 The partitioning into sentences provides us with a fine-grained way to identify the subcomponents of speech communication. Furthermore, it allows us in Phase 2 to identify the centrality of an ethics speech genre by assigning a dominant theme to each sentence and to then determine the grouping of dominant themes that are present in each editorial. The partitioning of the editorials into sentences resulted in a corpus of 43,060 sentences.

LDA topic modeling algorithms generate the best division of words given a specified number of topics. Therefore, it is necessary to utilize a series of LDA diagnostic tests to identify a range of acceptable solutions (cf. Roberts et al., 2014a, 2014b). The diagnostic test results contained in the Appendix indicate that the optimal number of topics falls somewhere between 15 and 20 topics. Our review of the discursive themes for each of these five topic models indicated that there was minimal variation in the key discursive themes across topic models but that the k = 16 topic model represented the best trade-off among the different diagnostic results. 6 Our use of LDA diagnostic test plus researcher interpretation as to which model is ‘best’ from within a group of acceptable models is consistent with the approach of Ferri et al. (2018: 178).

Phase 1: Results

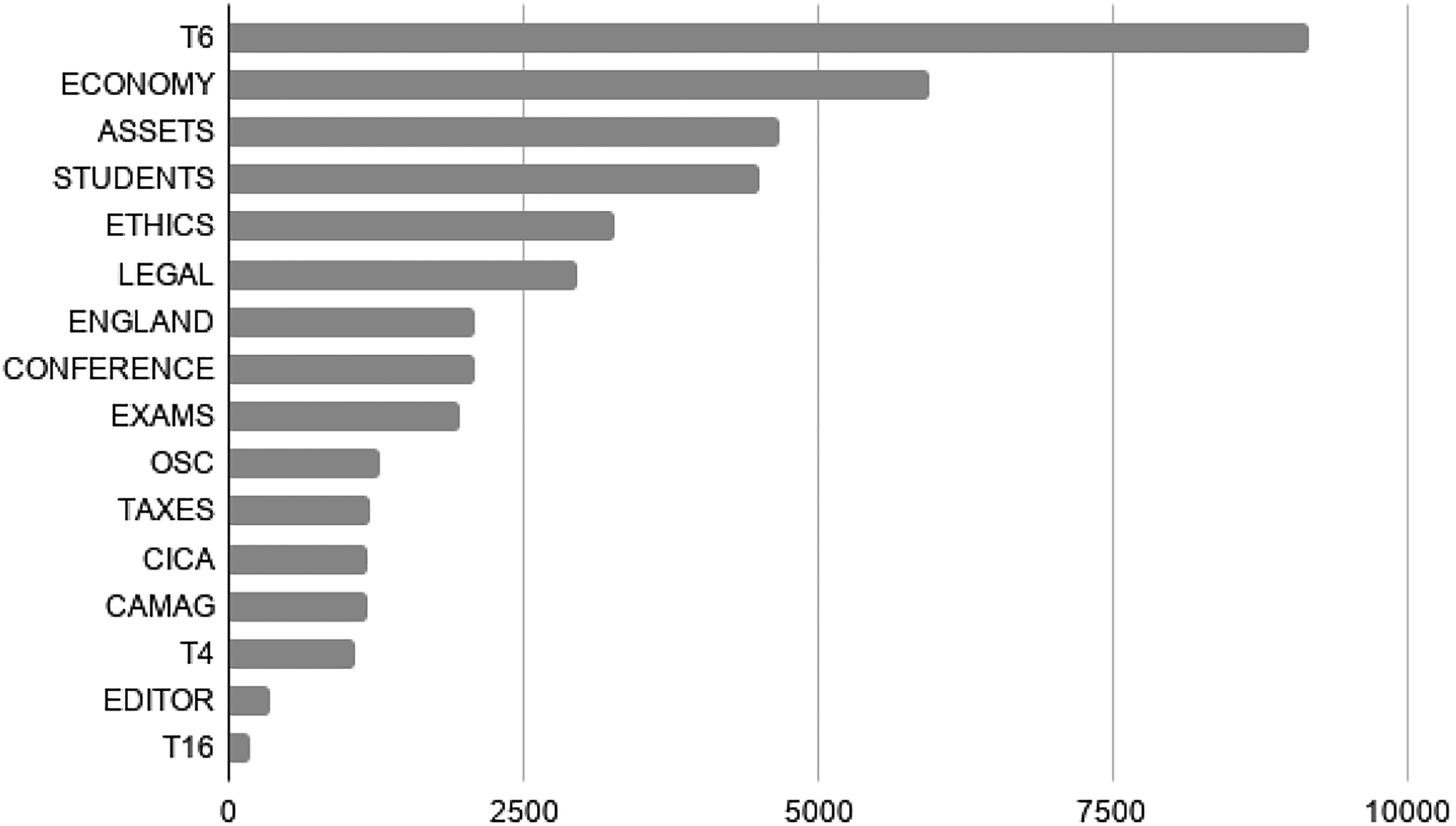

Table 1 summarizes the frequent and exclusive (FREX) words and LIFT words associated with the identified themes whereas Figure 1 illustrates the prevalence of the different topics. In both Table 1 and Figure 1, the authors have added the topic labels.

Frequency of Top topics

Latent Dirichlet Allocation (LDA) topic modeling results for corpus of the CA Magazine editorials.

Note: The lists of FREX and LIFT words are generated by the STM algorithm (Roberts et al., 2014a, 2014b). FREX words are the words that are ‘frequent and exclusive’ to each topic, while LIFT words are a more stringent version of FREX based on ‘the ratio of a word's probability within a topic to its marginal corpus probability’ (Fan et al., 2019).

The provided results contain three topics pertaining to ethics and education that are labeled as ETHICS, STUDENTS, and EXAMS. There is also an ASSET topic which relates to the technical bases for valuing assets and to the information that is communicated on the balance sheet. These four topics are of primary interest in that our theoretical framing suggested that utterances about norms of conduct, competence, and education would be a salient component of professional narratives. In addition to these four topics, there are also topics about the ECONOMY, TAXES, the CICA, the OSC, LEGAL issues and the CA Magazine itself (CAMAG and EDITOR). In total, there are 13 topics that we have labeled (because they appear to have a conceptual theme) and three unlabeled, miscellaneous topics.

Figure 1 illustrates the prevalence of the different topics. Consistent with our preconceptions, the topics of ETHICS, ASSETS, and STUDENTS are three of the most prevalent topics. These topics can be viewed as linchpin topics that connect the external and internal dynamics of the profession (Klegon, 1978). Puxty et al. (1987), for example, suggest that accounting associations have a corporatist bargain with the state where accounting associations, in return for quasi-monopoly privileges, agree to produce technically competent and ethical practitioners. Utterances about these topics are both directed inward (helping to socialize current/future members) and directed outward (helping to satisfy government regulators and forestall challenges from rival occupational groups). From this vantage point, it is not surprising that there were also a group of topics that were focused on the external environment (ECONOMY and TAXES) and the regulatory environment (OSC and LEGAL). The second phase of our research examines these connections in more detail.

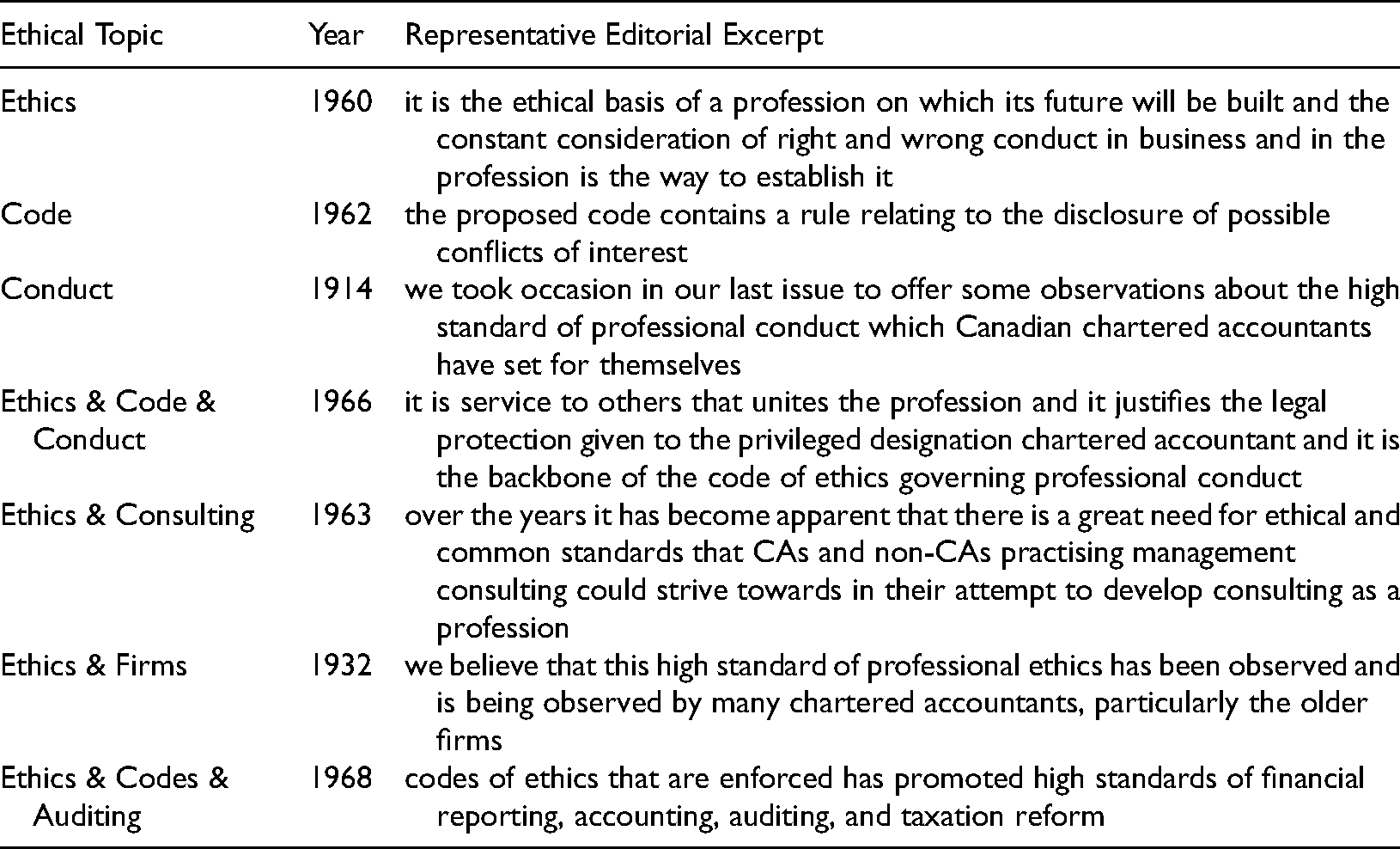

A closer examination of the ETHICS topic draws attention to the narrative structure of the speech genre. First, consistent with our preconceptions, the notion of ethics itself is referred to in multiple ways via references to ethics, rules, codes, principles, regulations, and conduct. Second, the speech genre acknowledges two concrete types of ethical situations in that the words ethics/rules/codes/principles co-occur with both the auditing setting and the consulting setting (audit is both a FREX and LIFT word whereas consult is a LIFT word). It is these multiple ways of speaking ‘about ethics’ and the addition of situational words that move ethics from being something abstract and general to something that refers to the behaviors of specific social actors in specific situations. Table 2 provides the reader with some examples taken from the editorials.

Speaking about ethics – example excerpts.

The topic modeling results contribute to our understanding of professional narratives in at least two ways. The results provide us with a complete set of the speech genres that were present within the professional narrative over the first 98 years. While previous research on the Canadian profession (Creighton, 1984; Everett et al., 2018; Neu et al., 2003) and other accounting professions (cf. Murphy and Quinn, 2018; Preston et al., 1997) provided a partial list of discursive topics, the identification of a complete listing provides a starting point for examining the positioning and centrality of the ethics speech genre at different moments in time. Furthermore, the topic modeling method complements prior ethics-focused accounting research by foregrounding the narrative components of the ethics speech genre. The ethics speech genre has a narrative structure (Dawson, 2005; Preuss and Dawson, 2009; Statler and Oliver, 2016) that consists of somewhat abstract ethical concepts such as ethics and principles, ethical tools such as codified rules (Statler and Oliver, 2016), social actors that need to behave ethically (Farias et al., 2021; Karakas and Sarigollu, 2013; Winkler, 2011), and settings/situations in which ethics must be practiced (Litschka et al., 2011; McNichols and Zimmerer, 1985). It is this narrative structure that makes ethics into something that can be practiced (cf. Wang et al., 2016: 76) thereby turning ethics into something specific rather than abstract. The topic modeling approach allowed us to identify, map out, and document the narrative structure across 98 years in ways that would have been almost impossible without the use of topic-modeling techniques.

Phase 2: Network centrality method

The second research phase uses social network analysis methods to examine the positioning and centrality of the topics identified in phase 1 across time. Social network analysis methods convert co-occurrences of different speech genres within an editorial into edges and nodes. The nodes in this case are the individual speech genres whereas the edges are the connections among the different nodes. For example, if an editorial contained a sentence where the dominant topic was ETHICS and another sentence with STUDENTS as the dominant topic, ETHICS and STUDENTS would be nodes and ETHICS–STUDENTS would be an edge. Social network analysis methods calculate the edges that are present within each editorial and assign a value of 1 (zero otherwise) to the edge. These edges are then used to calculate the existing network. The subsequent network analyses use the FREX values from the topic modeling presented in the previous section to generate the node and edge information. Prior accounting, ethics, and social science research (cf. Chapman, 1998; Richardson, 2009, 2017) have used social network analysis techniques.

Social network analysis methods are both visual and quantitative. For example, the igraph function in R generates graphical representations of the connections among the speech genres. More central nodes appear in the center of the graph and the distance between nodes depicts how close the different nodes are within the network. At the same time, social network modules in R also generate quantitative measures for the different forms of centrality. More specifically, the Centiserver (Jalili et al., 2015), CINNA (Ashtiani et al., 2019), and Keyplayer (An and Liu, 2016) modules allow us to calculate three types of centrality: that, following from Freeman (1978/1979), are referred to as degree, closeness, and betweenness centrality.

Degree centrality is the first type of centrality. It measures the number of direct connections that a node has to other nodes and assumes that more central nodes have more direct connections to other nodes. In the words of Freeman (1978/1979: 219), central nodes are ‘in the thick of things’ (see also Iacobucci et al., 2017: 76). We use eigenvector values as our measure of degree centrality. Eigenvector values tell us ‘the extent that someone knows everybody who is anybody’ (Borgatti and Everett, 2006: 471).

Closeness centrality is the second type of centrality and it measures the shortest path between the different network nodes, with the assumption that the more central nodes are those with shorter distances to other nodes. Central nodes are those that can directly reach other nodes and/or reach them via short geodesics (Iacobucci et al., 2017: 77). We use the Lin measure, which is calculated as ‘the inverse of the average distance (where) the smaller the value, the more central is the node’ (Borgatti and Everett, 2006). Like all closeness measures, Lin centrality is based on the length of the path rather than the volume of direct connections.

Betweenness centrality is the final type and it measures what happens to the network if a node is removed (Borgatti, 2003). Iacobucci et al., note that ‘unlike degree's measure of connections or closeness's measure of the distance between (nodes), betweenness identifies how often a particular (node) serves as a connection between other (nodes) in the network’ (2017: 78). Stated differently, betweenness centrality highlights what is the ‘glue’ that holds the network together. Betweenness is not about being popular or providing the shortest path to get somewhere but rather about being the node that ensures that the network is not fragmented. We use the fragmentation measure from the keyplayer module to calculate betweenness centrality. Each of these three measures draw attention to salient characteristics of the network of professional discourses.

Phase 2: Results

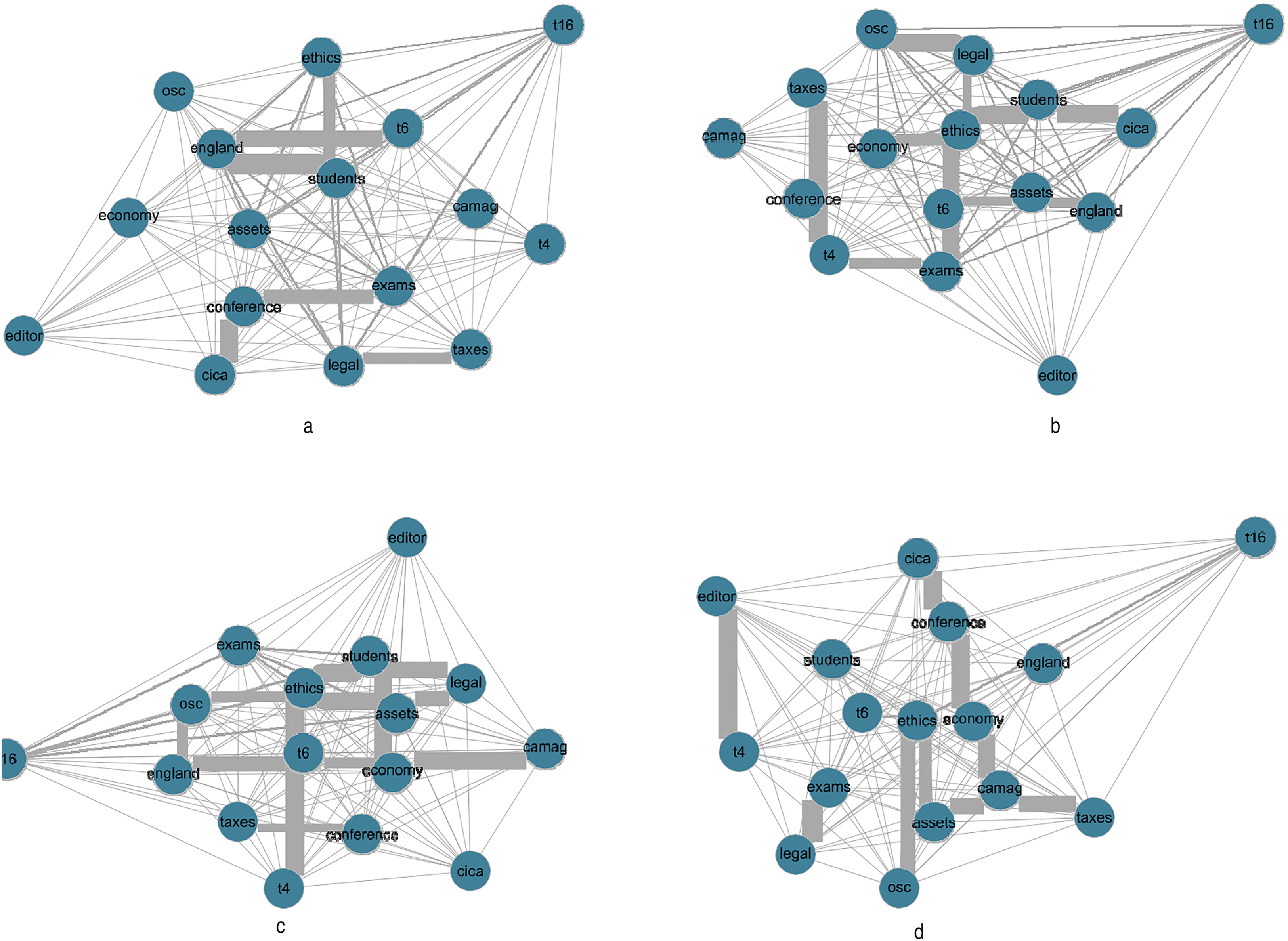

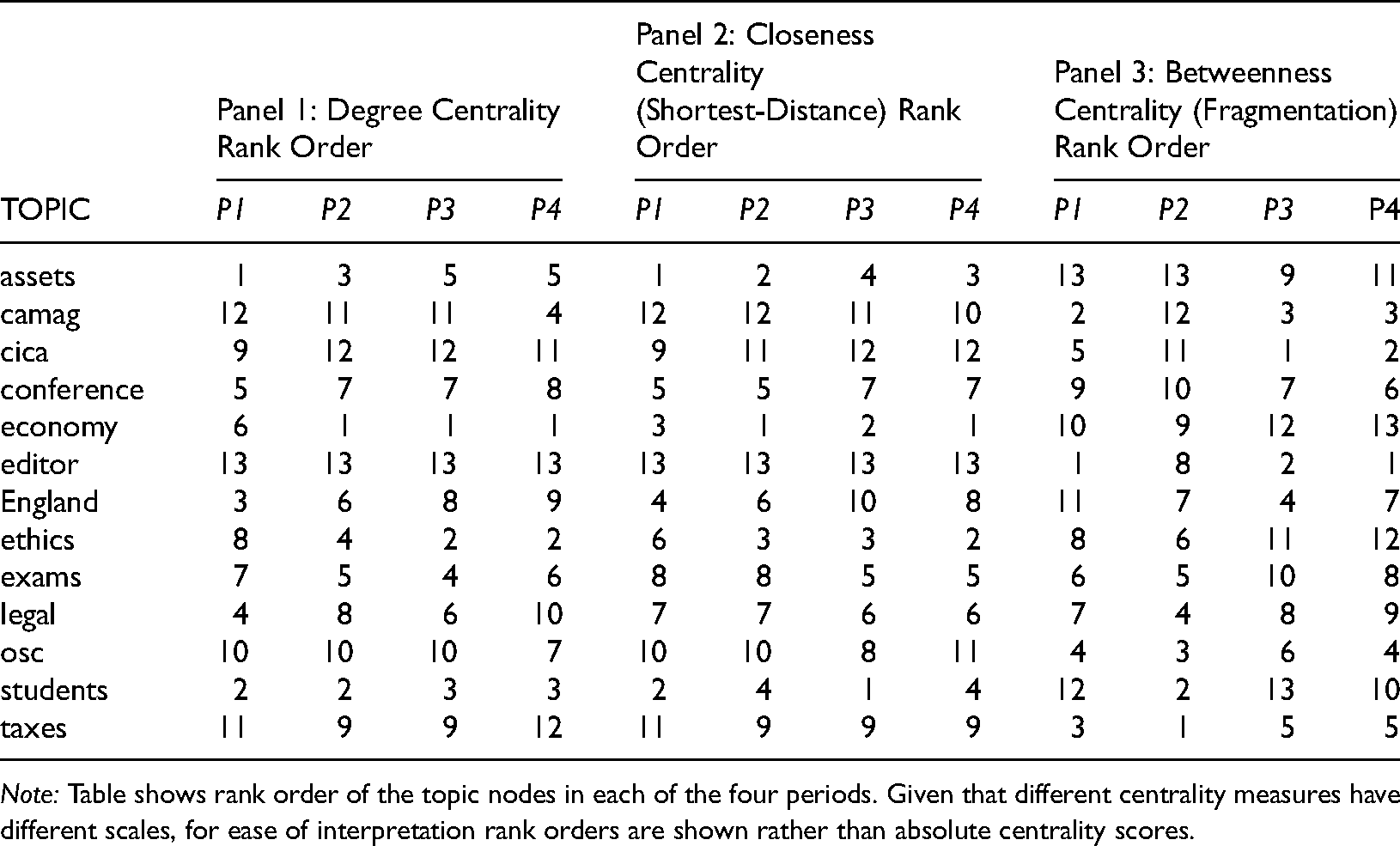

Figures 2(a) to (d) presents the graphical results whereas Panels 1–3 in Table 3 report the rank order results for these three centrality measures. For ease of interpretation, Table 3 contains rank order numbers instead of absolute centrality numbers. Similarly, the results in Table 3 exclude the non-labeled topics (T4, T6, and T16).

Sociograms of Topics Covered in CA Magazine over Four Time Periods: (a) Period 1 Topical Network, (b) Period 2 Topical Network, (c) Period 3 Topical Network, (d) Period 4 Topical Network.

Rank ordering for three centrality measures of topical nodes across four time periods.

Note: Table shows rank order of the topic nodes in each of the four periods. Given that different centrality measures have different scales, for ease of interpretation rank orders are shown rather than absolute centrality scores.

Figures 2(a) to (d) illustrate how the enunciations of the Canadian accounting profession evolve and congeal over time. In period 1, the network is quite dispersed with ASSETS and ENGLAND closer to the center and with a large peripheral ring. Included in this peripheral ring are ETHICS, STUDENTS, and EXAMS. The degree and closeness results from Panels 1 and 2 in Table 3 place ASSETS at the center and ETHICS in a middle centrality position (6 out of 13 and 8 out of 13, respectively).

In period 2, ECONOMY and ETHICS begin to drift toward the center as other topics such as EDITOR become more peripheral. The degree and closeness centrality results confirm this with ECONOMY becoming the most central node and ETHICS becoming more important. Although the graph implies that ASSETS is less central than previously, this shift is not that large as it still is the third most important node in terms of degree centrality and second most important in terms of closeness centrality.

Period 3 sees little change from period 2. ECONOMY continues to be the most important degree centrality node, but STUDENTS offers a shorter path to all other nodes in terms of closeness centrality. ETHICS, meanwhile, is second and third, respectively. Finally, period 4 sees ECONOMY and ETHICS being the two most important nodes in terms of both degree and closeness centralities.

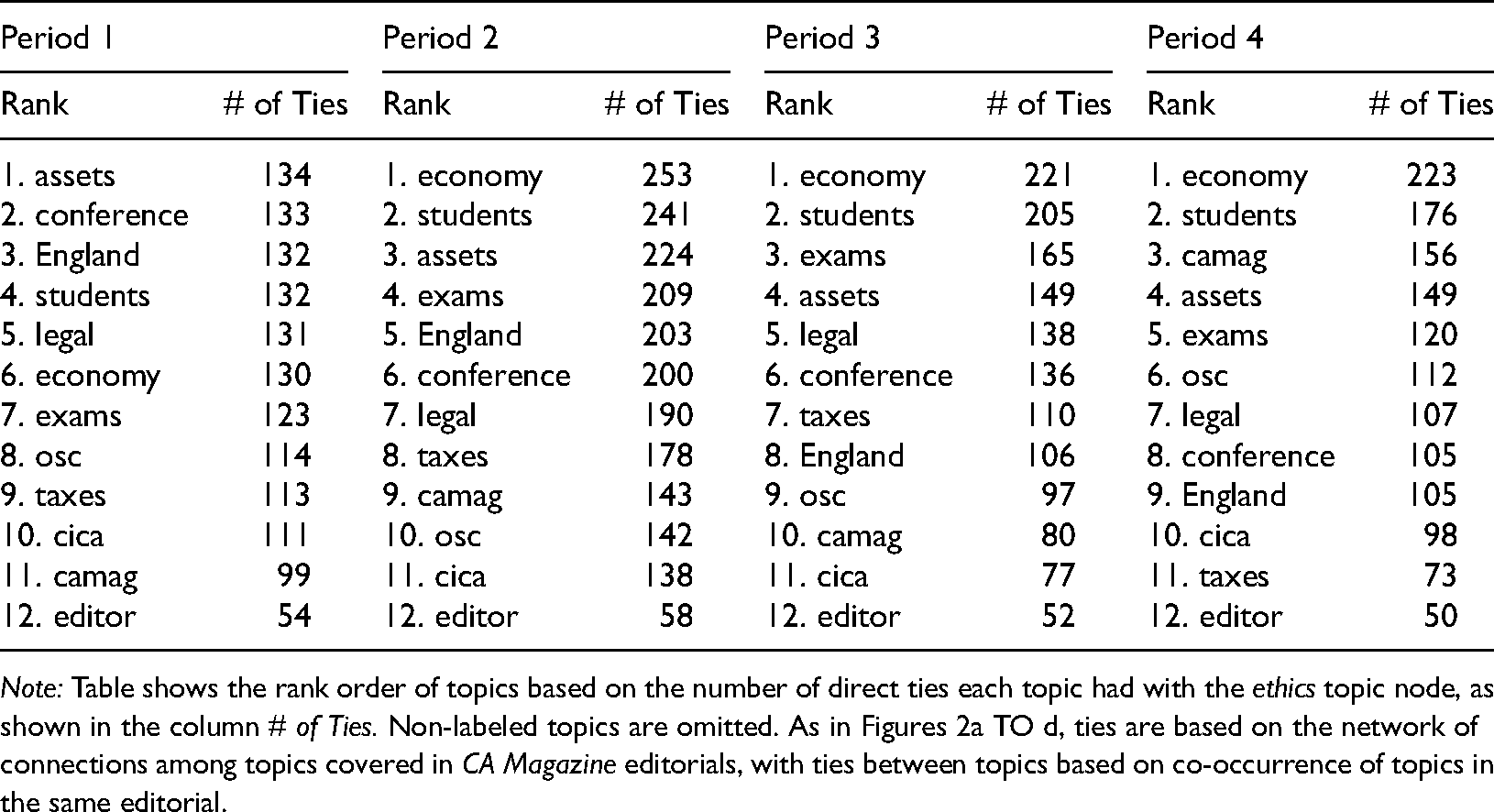

In addition to the aggregate results presented in Figures 2(a) to (d) and Table 3, we moved down a level of analysis to consider the positioning of ETHICS vis-à-vis other individual nodes. More specifically, we conducted an ego analysis that utilized R algorithms to calculate the number of direct ties that ETHICS had to the other nodes in each of the periods. Table 4 summarizes the top nodes based on the magnitude of the number of direct ties.

Rank ordering of topic nodes based on number of connections to ethics, by period.

Note: Table shows the rank order of topics based on the number of direct ties each topic had with the ethics topic node, as shown in the column # of Ties. Non-labeled topics are omitted. As in Figures 2a TO d, ties are based on the network of connections among topics covered in CA Magazine editorials, with ties between topics based on co-occurrence of topics in the same editorial.

The results show that, in all four periods, ETHICS has the most direct ties to ECONOMY, STUDENTS, and ASSETS with ECONOMY being the most tied node in periods 2 to 4. The finding that STUDENTS and ASSETS are tied to ETHICS is consistent with our theoretical framing and the idea that norms of conduct, norms of competence, and education are inter-connected.

Similarly, the connection to ECONOMY is consistent with suggestions that the economy is the context for public accounting work (Hanlon, 1997).

The provided results foreground three salient aspects of the professional narrative. First, the results challenge the notion that the early 1900s were the golden age for professional ethics and that ethics became less important over time. The degree and closeness centrality results indicate that, during the formative years of the Canadian public accounting profession (1912–1938), ETHICS was a middle-range topic but certainly not the topic with the most direct connections to other topics. Over time, however, ETHICS increased in importance to become the second most central topic by period 4. By period 4, ETHICS was directly connected to and knew ‘everybody who was anybody’ (Borgatti and Everett, 2006).

Second, the network is mostly cohesive and quite stable in that the removal of any single node does not disrupt the core. The fragmentation (betweenness centrality) results in Panel 3 of Table 3 indicate that the four topics that comprise the discursive core in periods 2 to 4 in Panels 1 and 2 are not the most central in terms of betweenness centrality. These four nodes have multiple connections to each other and thus are not irreplaceable in the sense that the network would collapse if one of the topics was removed. Rather, it is the EDITOR and the CICA that would fragment the network the most if removed. However, as Figure 2(a) to (d) show, the removal of these two nodes would only disrupt the peripheral ring—rather than the central core—of the network.

Finally, the results highlight how a discursive core emerges in period 2 and remains mostly stable across subsequent periods. This core consists of enunciations about the external economic environment (the ECONOMY), norms of competence (ASSETS), norms of conduct (ETHICS), and education (STUDENTS). This discursive core is not surprising since: the focus of public accountancy is economic activity; a primary technical competence relates to measuring economic values; and the education of prospective members contributes to both technical competence and appropriate ethical behaviors. For these reasons, it is not surprising that ETHICS, ASSETS, STUDENTS, and ECONOMY are directly connected to each other as well as being core components within the professional accounting narrative.

Altogether, the network centrality results illustrate and map the structure of CA Magazine editorials at different moments in time and across time. This mapping is descriptive in that the network analysis techniques attempt to show the positioning of individual nodes vis-à-vis other nodes. Indeed, it is this ability to both map the relationships among nodes and to identify central nodes that is the main strength of this method. Furthermore, in the absence of this form of quantitative data analysis, it is simply not possible to identify and understand the positioning of ethics and other discursive themes within professional accounting association discourse. From this vantage point, the ability to map, and hence describe, the structure of discourse and how the structure of discourse changes over time is the key strength of this method.

Discussion

Starting from 43,000+ editorial sentences contained in the CA Magazine between 1912 and 2010, we considered the centrality of ethical utterances within the professional accounting narrative. Consistent with previous research on the sociology of the professions, the results show that ETHICS, ASSETS, STUDENTS, and ECONOMY were components of the professional narrative. These four topics both pointed to the domain of public accounting work (the ECONOMY) and the role of education in producing technically competent and ethical accounting practitioners. The analysis also highlighted the centrality of ethical utterances and the ways that the topics of ETHICS and the ECONOMY become more central over time.

The provided analyses contribute to our understanding of the history of professional accounting association ethics. First, the analysis identifies the components of the professional narrative. Prior research has suggested that discourses about conduct and competence are salient but the current study, to our knowledge, is the first to systematically use topic modeling techniques to identify the individual components. Like Ferri et al. (2018: 174), topic modeling methods allowed us to systematically analyze a large historical data set—a data set consisting of 43,060 sentences—and to identify the components of the professional narrative: something that would be almost impossible to do without topic modeling.

Second, our topic modeling approach identified the structure of ethical utterances. More specifically, the ETHICS topic contained rules, codes, principles, regulations, and conduct as well as the recognition of different situations within which ethics is practiced (auditing and consulting). This finding that ethical utterances have a narrative structure complements and extends Statler and Oliver’s (2016) as well as Preuss and Dawson’s (2009) research on ethical narratives.

Third, social network analysis methods foregrounded the intra-textual ways that the professional narrative is constructed, especially the ways that the ETHICS topic is positioned vis-à-vis ASSETS, STUDENTS, and ECONOMY. Like Preuss and Dawson (2009), the results highlight the importance of reading textual materials horizontally and in positioning ethical utterances in relation to other utterances. As our results imply, the illocutionary force of ethical utterances, depends, in part, on the packaging of ethical utterances: especially the other topics that are enlisted into the conversation. As Briggs and Bauman note, it is these forms of strategic packaging that make communication forceful (1992: 149).

Finally, the social network analysis shows that the topic of ETHICS has become more, not less, central over time. This result is consistent with the idea that expanding professional jurisdictions require more, not less, ethical discourse in that the increasing number of domains within which professional accounting work occurs and the increasing complexity of accounting work requires professional associations to communicate differently about ethics. As the results highlight, ETHICS along with ECONOMY became more central components over time. These findings are somewhat reassuring in that a publicly interested orientation appears to be alive and well within the Canadian public accounting profession. Publicly interested does not deny that accounting expertise involves providing value-added services to clients; rather, as Roberts notes, it involves providing such services in ways that are socially responsible (2010: 103).

The current study complements and extends prior qualitative, historical research on the accounting professions. Previous historical research on accounting associations, especially research that attempts to examine the complicated historical trajectory of professional discourses over long periods of time, must either simplify the data or enlist computerized techniques to organize and analyze the data (cf. Preston et al., 1997; Everett et al., 2018). Such qualitative analyses do contribute to our understanding of professional discourse, but there is always the risk that some underlying, latent sets of connections will be missed (cf. DiMaggio et al., 2013). Like Ferri et al. (2018, 2021), we believe that computer-assisted topic modeling techniques as well as social network methods can enhance our understandings of accounting history.

Although the current study contributes to our understanding of professional ethical discourse, additional research has the potential to complement and extend the provided results. For example, we focused on the editorials contained in the CA Magazine, but the magazine also contains longer articles that are commissioned and/or selected by the editor. Additional research that examines the speech genres contained in the editorials vis-à-vis the articles would be useful. Similarly, the post-2010, post-merger period witnessed both a change in membership demographics and the emergence of social media. Additional research on the positioning of ethics within the new association as well as within this new communication medium has the potential to foreground the changing nature and positioning of ethical discourse. These topics, when juxtaposed against the past, will better help us to understand the history of the present.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the University of Calgary Haskayne Research Grant (Grant no. RT758558).