Abstract

The Papal States was a longstanding nation ruled by the Pope, the Head of the Roman Catholic Church. Its accountants included priests and laymen who were employed as bureaucrats. Despite an expectation that the finances would be carefully managed, this research from the mid-nineteenth century shows that incompetence and fraud dogged the Papal States’ latter years, contributing to it losing most of its territory in the Second War of Italian Independence from 1859, and its final demise in 1870. This prosopography of three men who held high bureaucratic positions, analyses their approach to accounting in the Papal States. It shows that waste and deficient accounting arose from individuals undertaking fraud and from organisational (and individual) incompetence. In doing so, it elucidates how the Papal States could be a ‘vehicle for fraud’, and in particular, how it was used as a shield to enable both fraud and incompetence to go unpunished.

Introduction

Through the centuries, the Papacy has often been criticised for corruption, nepotism, simony, and for its closeness to economic and political powers: financial mismanagement continues today (Kirchgaessner, 2016). Indeed, one of the main political triggers of the Protestant reformation was the carelessness with which the Roman Curia (the Papal States’ administration) managed its financial matters, traded in curial and political offices, and indulged in morally decadent behaviour. Thus, the Papacy was internally and externally criticised. Criticisms were lobbied against its accounting practices, with G. Belli, a popular author of dialect poems, being one who lavishly refers to the waste and thefts committed by the Papal Treasurers over the centuries (see Belli, 1998). Waste may arise from incompetence or fraud. We are encouraged to analyse the interaction between accounting and the society within which it is practised (Hopwood, 1976) therefore, our research questions are: what are the differences between fraud and incompetence, and did the Papal States encourage incompetence or was it used as a ‘vehicle for fraud’? In this article, we compare and contrast examples of incompetence and fraud, and how fraudsters used the Papal States as a vehicle (in the cases, as a shield) for fraud. An incompetent organisation enabled such fraudulent practices. We add to the small amount of literature on public/nonprofit sector fraud and present prosopographies of three senior Italian accounting bureaucrats.

Fraud has devastating effects leading to entity failure (Fremont-Smith and Kosaras, 2003; Gibelman and Gelman, 2004). Incompetence can also lead to failure, but it is often assumed that requirements for professional qualifications and experience will mean that an incompetent manager is replaced before an entity experiences financial failure. Nevertheless, the role of organisational incompetence in allowing failure is seldom explored. For this reason, the prosopography of three men holding senior accounting roles within the Papal States enables us to examine the link between fraud (including corruption) and organisational incompetence.

In general terms, the Papal States was one of the most long-lived political institutions in European history, with a crucial role due to the strength of Roman Catholicism and the Pope. It existed formally over eleven centuries (from 752 to 1870) until the unification of Italy; 1 at its demise its finances were in a parlous state. The Papal States was successful during a period when religion and state were inseparable (Cordery, 2019). It was overturned as society transitioned to the modern state and greater democracy. Yet, while the Papal States’ influence declined (Antonelli et al., 2021), the Roman Catholic Church (the Church) remained strong internationally. Other Papal States studies have considered the accounting practices of the pre-unification Italian states (Coronella et al., 2013), accounting reforms adopted by the Papal States between the end of the sixteenth and the beginning of the seventeenth century (Gatti and Poli, 2014), and the governability of the institutions operating in the Papal States’ territory (Coronella et al., 2013). Nevertheless, this longstanding institution has further aspects to add to our knowledge. The major justification for the existence of the Papal States was that a strong, wealthy and autonomous state could amass adequate means to perform its spiritual function, to extend the reach of Roman Catholicism (Chandler, 1909; Jemolo, 1963; Manning, 1862; Mori, 1967; Owen Legge, 1870; Torelli, 1870). Thus, close financial management and an accounting system should have been important to ensure financial stability and sustainability (as argued by Soll, 2015).

Certainly similar studies of religious entities at this time show the benefits of such control. For example, Heier (2016), who used data from the annual reports of the US Southern Baptist Convention, found regulation for internal controls, the imposition of audit (in 1885) and a keenness to be accountable financially to members. When fraud hit the Convention in the 1920s, further controls were introduced to reduce financial risk. In the Papal States case, Antonelli et al. (2021) show that the last leader of the Papal States (Pope Pius IX) authorised reforms to improve financial management through regular accounting, internal controls and audit. Yet those responsible for these systems (‘the accountants’) selectively chose what to make visible and flouted the reforms, with the result being that waste and extravagance abounded and the Papal States failed. This inconsistency in purpose suggests a need to further understand how the accountants could have diverted the reforms’ purpose; was it fraud or incompetence and how may they be differentiated? In this article, therefore, we analyse three influential accountants whose working lives intermingled within a 28-year period and who were indicative of those flouting the reforms. While other men may have presented themselves for study, commentators’ accusations against these particular three, their closeness to the Papal States’ finances and our desire to ascertain further details about the divergent accounting practice in the Papal States and interrelationships of upbringing, education and prior working experience, made these men ideal for such a study.

Our research aims to analyse accountants’ financial management in the final stage of the Papal States’ existence, as related to the papacies of Gregory XVI and Pius IX, that is, in the period 1831–1859. This period ends with the Second War of Italian Independence when the majority of the Papal States’ territory was lost, reducing Pope Pius IX’s temporal power, although his religious legitimacy remained. In analysing the political and social context within which these accountants worked (Carnegie and Napier, 1996; Hopwood, 1976; Walker, 2016), this research also develops the implications of incompetence and fraud for accounting and accounting history.

The research offers several contributions to the accounting history literature. First, it introduces three high-ranking individuals practising the craft of accounting and financial management within the Papal States. This is to respond to calls for more prosopographies, and for historical analysis of the public sector (e.g. Anderson and Walker, 2009; Carnegie and Edwards, 2001; Carnegie et al., 2003; Carnegie and Napier, 1996, 2012; Charle, 2015). Second, this research delineates between financial fraud and incompetence, as well as utilising the concept that organisations are ‘vehicles for fraud’. The focus on incompetence moves this research beyond the majority of other fraud studies, which Cooper et al. (2013) note are focused solely on the individual and the audit procedures that could detect and prevent fraud. Finally, the research brings to light (in English) a rich archive of Italian accounting that operated within a monarchy where democratic notions of public accountability were not present, enabling us to contextualise the fraud and incompetence, as recommended by Cooper et al. (2013).

First, we analyse literature on fraud and mismanagement (incompetence) in public/nonprofit organisations to develop a framework that can assist us to analyse the differences between fraud and incompetence and how the Papal States encouraged incompetence or was used as a ‘vehicle for fraud’. Second, we describe the methods followed, and the primary and secondary sources used to build the argument. The context of the Papal States between 1831 and 1859 is depicted briefly and extended through the biographies of the three senior accountants who led the body of public sector accountants within the Papal States. The discussion section shows the institutional weaknesses of the Papal State as a favourable milieu for incompetence and fraud. The conclusions and limitations of the article follow, along with areas for further research.

Fraud and incompetence in the public and private nonprofit sectors

The great majority of historical analyses of fraud and mismanagement (incompetence) has been undertaken in for-profit entities and typically relates to audit failure. Indeed, Agostini and Favero (2017), in their analysis of the fraud promulgated in the US company Sunbeam from 1996–2001, suggest that the auditor may become a scapegoat, despite work highlighting audit failures and the need for auditor independence (e.g. Heier and Leach-López, 2010, reporting on the fraud at the US-based Interstate Hosiery Mills between 1934–1937). Jones (2011) provides a summary of the main tactics fraudsters use, which are outlined later in this section.

Most prior research considers the role of fraud in corporate collapse, for example, Carnegie and O’Connell (2014) analyse accounting failure over 110 years and suggest that these corporate collapses are more likely to occur during economic downturns. While governance changes and new regulations attempting to eradicate fraud seem to repeat cyclically, Carnegie and O’Connell (2014) argue that accountants choose how to apply any new standards and, indeed Pontell (2005) notes that they may use company accounts as a ‘vehicle for fraud’. To understand these fraudulent individuals, Cooper et al. (2013) call for further contextualisation of their actions within the ‘moral mazes’ in which they work. This call mirrors those to analyse the vital role of accounting and accountants in shaping society (Hopwood, 1976; Walker, 2016).

In this section, we differentiate between fraud and incompetence to develop a framework for the paper’s analysis, with a specific focus on public/nonprofit organisations. This focus is unusual for the period being studied. While Soll (2015) acknowledges that the British parliament was accused of corruption in the early nineteenth century, Robb’s (1992) study of England from 1845–1929 suggests that the rise of for-profit companies in the nineteenth century was matched by a raft of fraudulent schemes. Furthermore, he noted that, ‘[m]any Victorians made no distinction between misadventure and malfeasance. Nineteenth-century England was a society which worshipped success and vilified failure’ (Robb, 1992: 27). It is this distinction between fraud and incompetence which we address, utilising an Italian case. Next, we define fraud, before turning to incompetence.

Fraud definitions vary among authors, nevertheless it is commonly agreed that fraud is private gain at public expense (Huberts, 1998). While Jones (2011) limits fraud to false accounting, Archambeault et al. (2015), divide fraud into . . . three components: asset misappropriation (e.g., theft of cash, fraudulent disbursements, misuse of assets), corruption (e.g., bribery, conflicts of interest), and FSF [financial statement fraud] (e.g., misstatement of assets, misstatement of revenues, improper valuations, improper disclosures). (p. 1196)

Fraud in the public and nonprofit sectors 2 is a perennial issue, and yet one that is not often reflected on historically (Fremont-Smith and Kosaras, 2003; Gibelman and Gelman, 2004), despite the damage it inflicts. 3 Wheeler and Rothman (1982) find that individuals acting inside organisations stand to make greater gains from fraud, as the organisational form provides a legitimacy and size that can make larger frauds plausible. This is what occurred in the US Southern Baptist Convention in 1927 and 1928 where one trusted treasurer falsified Bills of Exchange and another took out loans in the organisation’s name. Both men stole the funds for personal use (Heier, 2016).

The organisational form may also delay the discovery of fraud. Pontell (2005) draws on Wheeler and Rothman (1982) to state that insiders can use organisations as ‘vehicles for fraud’, enabling them to defraud greater amounts and to remain undetected for longer (Heier’s 2016 trusted treasurer stole US$900,000 in 1928). Thus, insiders can use the organisation either as a ‘sword’, to steal from other organisations, or as a ‘shield’ using the organisation’s ‘resources and legitimacy to avert detection and negative sanctions’ and neutralise internal and external controls (Pontell, 2005: 310).

Asset misappropriation and corruption involves individuals misappropriating organisational funds for personal benefit (Fremont-Smith and Kosaras, 2003; Heier, 2016; LeClair, 2019). Fraudsters are often charismatic leaders, well-placed insiders (Agostini and Favero, 2017; Gibelman and Gelman, 2004; Heier, 2016; Heier and Leach-López, 2010), or as Jones (2011) suggests, ‘overstrong individuals’. In addition to misdirected funds, managers and trustees of an entity can undertake fraud in the nonprofit and public sectors by paying excessive salaries and perks. LeClair (2019) describes these tactics as ‘soft corruption’, as higher salary and perks may be the only way to remunerate good staff in sectors where remuneration will not comprise dividends and share allocations (Fremont-Smith and Kosaras, 2003). Fraud can also be effected by nonprofit and public sector entities, when they breach their fiduciary duties.

Corruption may also consist of paying a sum of money in return for an unlawful privilege. In the Roman Catholic Church, this ‘simony’ occurred when individuals bought ecclesial or civilian offices or roles. Until the reign of Innocent XII (Pope reigned: 1691–1700), the role of the General Treasurer could be bought at a special rate that sometimes could even be as high as 100,000 scudi

4

(Bruscoli, 2007: 531). Despite the cost, the office was in great demand, as it could be used to extract public funds for personal use or to encourage other staff to do so on the perpetrator’s behalf. Even when the office was no longer ‘for sale’, the idea remained that those who took it could become rich or make other people rich. Indeed, Bossi (1912c) noted that this is the way some of the last Treasurers understood the situation; and the common people, who do not mince their words, felt a deep loathing for such prelates, seeing them as the main cause of the financial collapse of the Church. (p. 545)

This is an example of how an individual can make greater gains from acting inside an organisation and of using the organisation as a shield to enrich themselves (Pontell, 2005). It is also an example of how high-ranking individuals engage Papal State staff to encourage fraud.

The third type of fraud – FSF – has two roles; it may be used to mask fraud or be the prime vehicle through which fraud is undertaken. The Fremont-Smith and Kosaras (2003) state entity frauds include conflicts of interest, storing funds, and failing to keep proper records; matters that were exposed through audits. Jones (2011) takes a financial statement approach by arguing FSF can result from techniques to (1) increase income (e.g. premature recognition of sales or other receivables), (2) decrease expenses (e.g. through increasing provisions to smooth earnings in future years, capitalising payable expenses such as interest, reduce depreciation or bad debts), (3) increase assets (e.g. through techniques such as in 2, but also increase intangibles), and (4) decrease liabilities (e.g. off-balance sheet financing or reclassifying debt as equity). While the examples in Jones (2011) are from for-profit frauds, similar events could occur in the nonprofit and public sector. Melis (2011) provides specific Italian examples and notes that financial statements may be massaged to meet the needs of conflicting stakeholders’ demands.

The classic Cressey (1953) fraud triangle has been applied to reasons why individuals might undertake fraud, that is, because they have the opportunity, can make a rationale for it and feel under pressure to do it. A fraudster can perpetrate fraud by neutralising internal controls (thus, they need accounting skills), but there is no doubt that the fear of detection is a prime deterrent to future fraud (Pontell, 2005). Agency theory argues that information asymmetry raises the need for audit (external and internal) to expose fraud, particularly asset misappropriation (Fremont-Smith and Kosaras, 2003). Nevertheless, Dye (2007) and Jones (2011) note that fraud can often leave little documentary evidence, meaning auditors will find these issues hard to detect.

While there is little literature analysing and defining incompetence, de Bruin (2015) argues that incompetence can be worse than (fraudulent) greed because, to act ethically, a person must have both (an honest) motivation and competence. Thus, an individual’s poor motivation combined with incompetence can be as harmful as outright fraud. Incompetent organisational governance is a further factor in allowing wrongdoing to occur, by providing opportunities to an individual who is not monitored adequately (Gibelman and Gelman, 2004). Kauppi and Van Raaij (2015) suggest ‘honest incompetence’ when the principal is not fully competent to explain their goals clearly, or the agent cannot understand the goals. Poor decision-making and environmental disasters (‘bad luck’) also suggest organisational incompetence, with failures resulting from fraud, not mismanagement. In an analysis of local government fraud in the United States in the 1990s, Ziegenfuss (1996) found poor management practice, inadequate training, and a lack of responsibility for individual action. These failings could also suggest organisational incompetence.

Ott and Shafrits (1994) argue that incompetence is primarily an organisational issue and arises because an organisation is repeatedly unable or unwilling to learn from its environment, its failures, or its successes. Incompetence can be a systemic issue that is sustained by organisational culture, thus transcending the individual. Organisational incompetence is also a social construct which means that different stakeholders will judge an organisation’s competence differently and may result in them withdrawing their support (Ott and Shafrits, 1994). We now turn to the method by which we assessed fraud and incompetence in the Papal States.

Method and sources

This research is a prosopography which ‘focuses on presenting evidence for a group of actors on a range of characteristics such as social and family backgrounds, career paths, political and religious connections, and wealth accumulation’ (Carnegie and Napier, 1996: 22). While this method of collective biography was most commonly applied in ancient and medieval history, Charle (2015: 256) notes the more recent rise of micro-history to gain ‘intimate knowledge of small problem-related constituencies’. He recommends defining groups for study by relational characteristics, or the capacity of the individuals to impose their image on the majority of their members. This collective dimension enables a richer consideration of the societal inhabited by the group studied (Charle, 2015) and it is the ability to impose their image on staff that explains our choice of men to study. Prosopographies like this also enrich our knowledge of the value systems of historical actors (Carnegie and Napier, 1996).

In this prosopography, we outline the characteristics of three men who were ‘accountants’ in the general sense and appear indicative of the group that Antonelli et al. (2021) identified as having divergent aims to that of the Papal States. They had parallel careers, were connected to the same religious and institutional setting (the Roman Curia) and were, due to their roles, selected for the role of Cardinal. Two of these men (Tosti and Antonelli) were Ministers of Finance (from 1834–1847) and Galli worked under each of them, first as General Accountant (1826–1848) and then under Antonelli as Deputy Minister of Finance when Antonelli was Secretary of State. In this research, we compare and contrast the background characteristics of these three men’s lives and careers.

Prosopography is under-recognised in historical accounting research, and requires considerable archival sources (Anderson and Walker, 2009; Carnegie and Edwards, 2001; Carnegie et al., 2003; Carnegie and Napier, 1996, 2012). Indeed, of the numerous biographical studies across the accounting history literature, only four other recent papers are specifically prosopographies, with a further five being collective micro-historical biographies. We briefly review relevant nineteenth-century studies, which, except one, focus on the rise of the accounting profession during this period. Carnegie and Edwards (2001) consider the rise of the accountancy profession in Australia with an analysis of the social standing of the 45 founders of the Incorporated Institute of Accountants, Victoria (IIAV) in the period to 1886, with a later paper (Carnegie et al., 2003) analysing the role of these key actors as rival professional associations emerged in 1908. Similarly, Anderson and Walker (2009) analyse the social origins of the founders of the Institute of Chartered Accountants England and Wales (ICAEW) in 1880 finding that, unlike the Scottish founders of the Institute of Chartered Accountants in Scotland (ICAS) they were less likely to be highly born. Importantly, all three studies show that aspiring accountants were trained ‘on the job’ with few of these founders listing accountancy as their profession in earlier census material. These studies take a whole population (the founders), while we analyse three men who were indicative of those working as accountants in the Papal States. The final collective biography is therefore most related to our study, being of fraudsters. Lee (2015) analysed two brothers who he describes as ‘outliers’ in Victorian public accounting, but whose collective micro-history provides an alternative perspective of extant accountants. James and William Waddell ran an insolvency business in London and, due to lax regulation, they could undertake teeming and lading with creditor funds until a new Bankruptcy Act was passed in 1883 with more stringent rules. The Waddells were declared bankrupt in the same year and fled to the United States where they both ran successful accountancy firms, but did not join the profession. As they were at odds to what was expected, their behaviour could be described as similar to the men in this article who perpetrated fraud.

To address the challenges of prosopography, our article refers to several primary and secondary sources. The main primary source, regarding the financial, administrative, and juridical reports of the Papal States, comprises the documents of the Rome State Archive 5 which holds the public archives retained during papacies prior to and Rome’s annexation to Italy (1870). In the Rome State Archive, there are many files preserved in the Tesorierato Generale section including letters and documents concerned with the life and the activities of Cardinal Tosti and Cardinal Antonelli. The Archivium Apostolicum Vaticanum section labelled Segreteria di stato included the files related to Cardinal Antonelli, some of his correspondence, the acts and regulations signed by him. The Archive of the Salustri Galli families provides us with some documents related to the life of Angelo Galli. The third primary source is the Archivum Secretum Vaticanum, from October 2019 renamed as Archivum Apostolicum Vaticanum 6 kept at the Holy See.

The documents examined include the official collection of laws and acts for the period in question, financial regulations, state budgets and balance sheets, statistics and censuses, and other official documents such as those for the rates and the mints. Many documents from these archives have been reproduced in print, and are readily available. Accounting books, however, are less available and we photographically reproduced relevant documents. Secondary sources, contemporary to the events, include books and pamphlets by scholars, laics and clergymen who wrote essays and histories of Popes and cardinals. These include histories of the Papal State and its economic and accounting activities and biographies of the accountants we examine.

We now proceed to provide the context of the prosopographies and why they are important to elucidate distinctions between incompetence and fraud.

The nineteenth-century governance and accounting context of the Papal States

The Papal States was officially founded in 752, following various Carolingian donations (Duchesne, 2010; Fried, 2007), and continued to exist until 1870 when the army of Victor Emmanuel II invaded the region of Lazio and Rome (Mori, 1967), promulgating a decree ratifying the annexation of the conquered territories to the Kingdom of Italy (Riall, 1994; Tomassini, 2011). 7 Prior to 1859, it covered an area of about 40,000 square kilometres (including the current regions of Lazio, Umbria, Marche, Romagna and the northern part of Campania) and numbered a peak of 2,800,000 inhabitants in the mid-nineteenth century (Galli, 1840; Stato Pontificio, 1857). The Papal States was an absolute monarchy, where the Pope-king was elected in a conclave of Cardinals. This context is therefore unusual in that, rather than the separation of State and religion, they were one and the same.

The period investigated in this article is 28 years during the reign of two Popes: Gregory XVI 8 (1831–1846) and Pius IX 9 (1846–1870, although he ruled the Vatican/Holy See until his death in 1878). Relevant details of their reigns are provided through the prosopographies.

Accountants and accounting in nineteenth-century Italy and the Papal States

At least two pre-unification Italian States placed great importance on the training of public accountants. The Kingdom of Lombardy-Venetia initiated accountancy courses at the Universities of Padua (1839) and Pavia (1840). In the Kingdom of Naples, from 1857 to 1860, the General Treasury held a double-entry accountancy school to teach young people how to record coordinated transactions to meet civil-service requirements (Coronella et al., 2013). The Papal States had no accountancy school with accountancy taught on the job, maybe (but not necessarily) after attending a basic course. Until 1836, the Papal States required no training of any accountants in the public or private sector.

It was under Gregory XVI, on 6 July 1836, that Cardinal Lambruschini enforced the first regulation on the ‘accounting profession’ (Ordinazioni, 1836). Anyone seeking to work as a public sector accountant was required to complete a three-year internship at an accredited accountant and then to pass a state examination. The applicant must have studied theoretical arithmetic but required no other specific prior education. This regulation did not extend to the private sector until the Papal States were annexed to the Kingdom of Italy. 10 Accountants were in demand in the public sector; by 1848 the Ministry of Finance employed 2,017 laymen and three clerics. This was almost 40 per cent of the total number of employees of all the ministries (5,059 laymen and 243 clerics). The Ministry of Finance also consumed about 40 per cent of the total ministry funds (Stato Pontificio, 1849). The clergy may have not previously studied accounting (see our examples below); however, each lay employee was required to be of religious habits, impeccable political behaviour, be a national of the Papal States and have a certificate of study at least equivalent to the first year of secondary school (Friz, 1974; Ventrone, 1942). While we cannot now observe the training provided, Antonelli et al. (2021) find that accounting practices were antithetical to the Papal States’ regulations and that accountants could choose what to make visible, transferring funds from the Church to State and also allowing revenues from forbidden activities to underpin budgets.

In this article, we present three accountants from the final two papacies in the Papal States (those of Gregory XVI: 1831–1846 and Pius IX: 1846–1870). These men were: Cardinal Tosti, the General Treasurer 1834–1845, Angelo Galli, the General Accountant, 1826–1848, and Deputy Minister of Finance 1849–1854, and Cardinal Giacomo Antonelli, the Secretary of State 1848–1870 (see Table 1). Our analysis will show whether they felt pressure to be fraudulent and could make a rationale for it (as per Cressey, 1953), or whether poor accounting was caused by incompetence and sustained at an organisational level. As a final contextual matter, we outline briefly the governance in the Papal State.

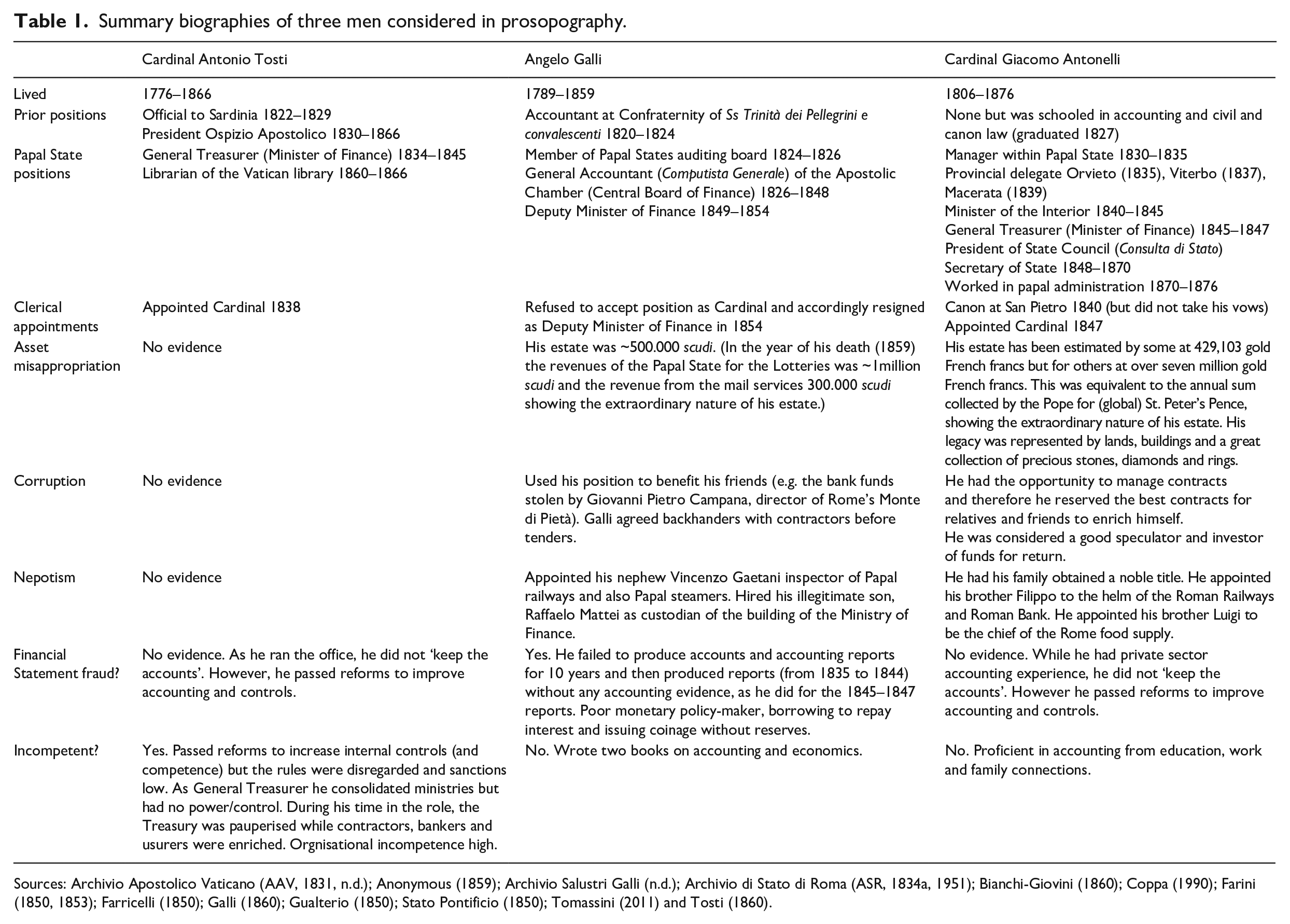

Summary biographies of three men considered in prosopography.

Sources: Archivio Apostolico Vaticano (AAV, 1831, n.d.); Anonymous (1859); Archivio Salustri Galli (n.d.); Archivio di Stato di Roma (ASR, 1834a, 1951); Bianchi-Giovini (1860); Coppa (1990); Farini (1850, 1853); Farricelli (1850); Galli (1860); Gualterio (1850); Stato Pontificio (1850); Tomassini (2011) and Tosti (1860).

Governance in the Papal State

Until 1847, the Papal States’ form of government was that of an absolute monarchy: there was no separation of powers; nor any parliament. The summit of the state administration consisted of the Secretariat of State (curia) comprising the following offices:

The ‘Cardinal Secretary of State’, who presided over internal and foreign affairs;

The ‘Cardinal Camerlengo’, which oversaw industry and commerce;

The ‘Cardinal Vicar’ who was entrusted with the customs police;

The ‘Cardinal President of the Congregation of Good Government’, whose ‘congregation’ was responsible for supervising the acts of local administrations.

These personalities were nominated and revoked by the pontiff, with whom they had a relationship of personal trust. They responded directly to the pontiff for all their acts.

Following reforms in 1847 the Council of Ministers, the High Council and the Council of Deputies were established. The Secretary of State also became President of the Council of Ministers and therefore was responsible for the state bureaucracy employing clerics and laymen (Stato Pontificio, 1849). The first government was formed by nine ministers, reduced to five in 1850 and then to four in 1853. In 1847, Pius IX also created the ‘Consulta’ (State Council), an institution that legally represented the provinces (Pope Pius IX 1847b). The Consulta was formed by a cardinal president, a prelate as vice president and 24 councillors appointed by province. Each province was allowed one councillor, Bologna two and Rome four.

In 1848, Pius IX allowed a constitution (Ara, 1966; Pope Pius IX, 1848), which instituted two legislative chambers and opened the political and administrative institutions to laymen (Pope Pius IX, 1847a, 1847c). Following the revolution, 11 a State Council was charged with drafting, under the direction of the government, the bills and the regulations of the new public administration. In 1849, the Pope and his absolute power was restored and the government offices were once again entrusted exclusively to clergy (with the sole exception of the Ministry of Arms). Nevertheless, the State Council comprised 15 members, of which only four were curial, and a Council of Deputies comprising 86 members which was completely lay (a combination of noblemen, university professors and lawyers) (Spada, 1869). The office of Prime Minister was, however, reserved for the Secretary of State which was held by the last of our three men, Cardinal Giacomo Antonelli, from 1848 until the end of Pius IX’s papacy. As noted, each of these men held accounting as well as governance roles. Thus, they had the ability to impose their beliefs on accounting to the other clerics and laymen bureaucrats (a reason to choose prosopographical subjects – see Charle, 2015), and we focus on whether their inconsistent actions suggest fraud or incompetence.

Cardinal Antonio Tosti – General Treasurer, 1834–1845

Antonio Tosti is an example from Gregory XVI’s Papacy of someone who was probably incompetent and certainly worked in an organisational environment of incompetence, owing to poor structures and a failure to learn from mistakes. Indeed, when Gregory XVI’s government concluded, the Vatican finances were in a parlous state, partly due to the huge cost of architectural and engineering works the Pope had instigated, and partly due to the many problems of controlling expenditure (Castellano, 1837; Galli, 1840).

Tosti was born in Rome on 4 October 1776; there is nothing to suggest he came from a merchant family, nor that he was trained in accounting in any way (given compulsory training was instigated two years after he became General Treasurer). There is little reference to his life before he was nominated Cardinal. On 25 April 1822, he was appointed ‘Official to Sardinia’ and resigned on 15 January 1829. In 1830, he became president of the ‘Ospizio Apostolico’, a shelter for the less fortunate. Under his control, this institution was reorganised as an arts and crafts school, which attracted poor men seeking education in arts, music and printing. Tosti reformed the school so that it became a reference point in both Roman and international arenas and epitomised social recovery of outcasts (Gasparoni, 1839). He continued as president for 35 years until his death, making efforts to better the school and maintain its supremacy.

Following serving as High Prelate of Pope Gregory XVI, he was elevated to Cardinal in the Concistory of 12 February 1838 (see Figure 1), being publicly appointed a year later (De Camillis, 1955). Following his work as General Treasurer, Tosti was appointed Librarian of the Vatican Library on the 13 January 1860 and he died in Rome on the 20 March 1866. 12 Records do not show if Tosti trained in accounting or administration. His only prior job with seemingly relevant skills is that of Official to Sardinia, in Turin (Lupano, 2015).

Tosti pre- and post-Cardinal days.

General Treasurer period: 1834–1845

In 1832, Gregory XVI reorganised the Treasury creating a supporting Board of Finance and Board of Tax, and making the bookkeeping department responsible directly to them on respective matters. Tosti was appointed General Treasurer (heading the Board of Finance/Minister of Finance) of the Papal State on 25 June 1834 (ASR, 1834a). He therefore became responsible for keeping the accounting records of all state administrations and compiling all budgets and balance sheets (Raccolta, 1834).

Antonio Tosti, after being appointed General Treasurer, wrote a broad report entitled ‘On the state of finance’, dated 16 July 1834, in which he described the organisation of the financial administration of the Papal State, the situation of finance and the deficit, denouncing the disorder of his ministry that was also due to the resistance of the offices to apply any accounting innovation (ASR, 1834b).

Reforms and the calls for reform were not new. For example, Pope Pius VII’s 1816 modernisations required a state budget to be drafted, and increased powers for the Treasury to examine and intervene in the case of excessive expenditure (Pope Pius VII, 1816). Yet, following the deficit from Gregory XVI’s payments for military to suppress uprisings in 1831, 13 public debt increased. This worsened the Papal States’ financial position, despite Gregory XVI selling state assets. 14 For this reason Gregory XVII appointed a special Commission, called ‘Particular Congregation for the deficiencies of the Treasury’, comprising three Cardinals, assisted by Tosti (General Treasurer) and the Secretary of the Treasurer, to ‘to take effective measures to remedy the deficiency of the Treasury’ (AAV, 1831).

Despite the impetus for Tosti to instigate reform, Angelo Galli (then General Accountant) and other senior officials of the State devised a division of the management and the responsibilities, so that the Ministry of Finance had 30 branches (subdivisions), including Authorities and Commissions (Bossi, 1914d). Before staff could discuss issues with Tosti as Minister of Finance, they had to inform and discuss matters with various managers, consuming an inordinate amount of time. When the General Accountant (Angelo Galli, see next section) did not produce accounts for Tosti for 10 years, Tosti had little power to force their production.

Nevertheless, Cardinal Tosti operationalised the Congregation of Review requirements for a single bookkeeping method to be used (Bernetti Card, 1834), and developed clear job descriptions for the General Treasury and for the totally renewed Computisteria Generale (the General Accounting Department) on December 15 1836, writing to General Accountant Angelo Galli, to ask him to attend to applying his reforms within the Offices (ASR, 1836). (Appendix 1 lists accounting regulation immediately prior and during the period Tosti managed the Papal accounting system.) Despite this, most state authorities ignored the new rules and produced cashbooks only (Rapporto sul bilancio generale del decennio dal 1835 al 1844 della Reverenda Camera Apostolica, Rome, 1847). Tosti failed to mandate close connections between the budgets and the actual accounts, and therefore, after the accounting departments’ managers had gained approval for their budgets, they could request more resources and/or report lower revenues. The efficacy of their requests was not checked and poor, inaccurate or even fraudulent work rendered the Papal States’ budgets unreliable. In a circular letter dated 18 January 1842, the Minister of the Interior, Cardinal Mario Mattei, wrote, The Congregazione di Revisione, which audits the public accounts and transactions, had to reveal to Our Holiness that, even though since the year 1835 it had given, on behalf of His Holiness, the most accurate instructions about the way and the time the interim budgets of the State revenues and expenses had to be presented; and despite having repeatedly reminded such authorities, not least by begging His Holiness to submit those who had been the cause for such delays to the same punishments that apply to those who breach the rules for the drawing up of the balance sheets, yet some of those authorities and some of those Ministries had not produced those interim budgets they should have submitted in May last year, in 1841, so that the general balance of the State revenues and expenses for the year 1842 could be drawn up in time. [. . .] as a consequence of which His Beatitude will take those measures He will deem fit against any disobedient person. (Raccolta, 1843: 5–6)

Instead of punishing poorly performing departments or staff, Tosti issued new rules on 24 January 1843 hard allowing him to delay submission of the combined balance sheets to the Congregazione di Revisione as late as 15 months after the closing of the relevant financial year (Raccolta, 1843). Yet, Tosti could not abide by these new rules as shown in the archival evidence. Bossi (1912b: 504) also notes ‘the proliferation of useless audits’. In frustration, Tosti, as General Treasurer, sought authorisation to stop paying the accountants’ salaries (Bossi, 1912a).

Cardinal Antonio Tosti was the General Treasurer for over a decade (1834 to 1845), and was known to be honest, but the evidence suggests he was incompetent and part of a system that failed to learn from its own mistakes. Historian Gualterio (1850) wrote of him: Cardinal Tosti, who for many years directed [the Ministry of Finance], was a man of natural intelligence, although of no economic study, and gifted with many and various expedients. He had a wonderful facility for preventing the imminent danger of bankruptcy, but by preventively using up all funds and all means, he increased the difficulties for the future. By filling a pit, he opened a chasm [. . .]. Thus the finances went from bad to worse, and theft increased greatly. (p. 173)

On the contrary, another observer believed Tosti was of ill-repute: Cardinal Tosti was famous for his dishonest management . . . Through robbery he became very opulent and he displayed unprecedented luxury and arrogance. Such lifestyle was demonstrated in his house by furniture, tapestries, carpets which were particularly refined; even the door handles were of amber. (Bianchi-Giovini, 1860: 22, 64)

Nevertheless, Farini (1850) concluded that Tosti was indeed incompetent and inexperienced, but so honest that he died poor. Therefore, while contemporaries disagreed over Tosti’s abilities, the Papal States’ system evidenced organisational incompetence and an inability to learn from unsuccessful reforms. Furthermore, ‘despite the financial ruin of the Roman State, the expenses, including luxury ones, increased by the day, and squandering, instead of decreasing, increased [. . .]’ (Gualterio, 1850: 172). Cesare Cantù (1858) concurred, The debt was far from being redeemed by the new taxes and other payments; so much the worse, because everyone squandered and the government’s luxury grew; and the Treasurer, Cardinal Tosti, could hardly dry up one well without having to dig another just to stay afloat. (p. 580)

Public debt rose despite Tosti’s attempt to fight the trend, and after 11 years as General Treasurer, he was replaced by Cardinal Giacomo Antonelli. Yet, Antonelli was unable to reverse the situation, as we show in the section after next. Tosti disliked Antonelli, as well as Angelo Galli, whom we present next.

Angelo Galli – General Accountant 1826–1848 of the Central Board of Finance and Deputy Minister of Finance 1849–1854

Angelo Galli served under both Gregory XVI and Pius IX. He was responsible for providing reports to the General Treasurer (Tosti) throughout Tosti’s time in that position. Working within an organisationally incompetent system, he was a poor monetary policy-maker but had good accounting skills. Nevertheless, Galli was accused of being an immoral and greedy man, active in fraudulent behaviour including contraband, corruption and nepotism. He ensured his nephew, Vincenzo Gaetani, was appointed inspector of the Papal steamers, and his illegitimate child, Raffaelo Mattei, was hired as guardian of the Ministry of Finance headquarters (Farini, 1853; Liverani, 1861; Tomassini, 2011).

Angelo Galli was born in Rome in February 1789 from a master mason and was the first-born of seven sons; hence, we can assume that he learnt business skills as he matured, despite no compulsory accountancy training being available until 1836. As shown in Table 1, in 1820 after a training period, he was appointed as accountant at the Confraternity of ‘Ss. Trinità dei pellegrini e convalescenti’ which enabled him to develop skills for working in public finance. Indeed, on 29 September 1824 hard he was elevated to the membership of a Papal States’ accounting board responsible for auditing military, post services and lottery accounts, and by June 1826 he was appointed as Computista Generale (General Accountant) of the Apostolic Chamber (the Central Board of Finance). He became the highest reference for technical accounting matters in the Papal State (Archivio Salustri Galli, n.d.; Ospizio della Ss, n.d.). The General Accounting Department concentrated the accounts of all of the State’s financial services and was in charge of keeping the books and producing the balance sheets. Accordingly, Galli ‘assisted’ Tosti in drafting the Papal States’ balance sheet for the period 1836–1844 during Pope Gregory XVI’s reign.

From 1826–1854, Galli was the only man who clearly had full access to the Papal States’ finances. When the ministries were established in the reform of 29 December 1847 (Pope Pius IX, 1847c), the Treasury (including Antonelli) and Galli’s Computisteria Generale were subsumed into the Ministry of Finance. During the interim government and the Roman Republic (24 November 1848 –3 July 1849), Galli relinquished his position to avoid allegations, however, a few days after the Pope’s return on 15 July 1849, he was appointed Deputy Minister of Finance. He resigned in November 1854, because he allegedly did not want to relinquish his lay status (to become a Cardinal) and because public-service directives were becoming too strict (D’Errico, 1998). His refused to take the vows of obedience; nevertheless, we are told that he wore the priest’s robe, and this led to misunderstandings (Tomassini, 2011).

Galli was an accomplished author (see examples in Figure 2), publishing an accounting work in two volumes entitled ‘Istituzioni di contabilità coi metodi teorico-pratici per eseguirne le operazioni’ (Pillars of accounting through a theoretical and pragmatic approach to run operations properly), printed in Rome in 1837 (Galli, 1837) and ‘Cenni economici e statistici sullo Stato Pontificio’ (Clues on statistics and economy in the Papal State), printed in Rome in 1840 (Galli, 1840). These works are deemed to have increased the Papal States’ knowledge on accounting and economics. Furthermore, Galli wrote ‘Sulla opportunità delle strade ferrate nello Stato Pontificio’ (On the economic aspects of a railway system to be developed in the Papal State) (Galli, 1846). He died in Rome on 23 July 1859.

Cover of Galli’s accounting and economics works.

General Accountant period: 1826–1848

Galli not only ran his administrative office in the Papal State, but he also developed many other initiatives. For instance, he was among the founders of the Insurance Company of the Pope, the first public company established in Rome. He was partner of the Roman Savings Bank, founded in 1833 (ASR, 1833–1834), along with many other financial institutions. He strongly advocated and dealt with the foundation of the Papal railway; supporting this latter project by a thorough study (see above and Figure 2). Galli also managed the re-arrangement of river navigation services on the Tever (D’Errico, 1998). He involved relatives and friends either in public procurement procedures or public positions within these activities, and provided special judicial help in return for payments. He also embezzled funds from his nephew who was his protégé (D’Errico, 1998; Tomassini, 2011).

Galli perpetrated financial statement fraud (FSF), as he failed to prepare reliable budgets and financial reports. Despite the specific accounting methods and numerous regulations laid down regarding accounting, budgets and balance sheets, while he was responsible for their preparation, the Papal States failed to produce their yearly balance sheets for 15 years (1835–1849). At the end of the first decade, a special committee was appointed to solve the problem and to track down missing accounting records. Although there were four other members, Angelo Galli chaired the committee 15 and he began the Committee’s report (dated 22 June 1845) by justifying himself and declaring himself uninvolved in the failure to draw up the records in an ‘ordinary’ way (Farini, 1853; Galli, 1860; Gualterio, 1850). In summary, the ledgers were last completed by the General Accounting Department in 1836 and afterward two annual books were kept, one for expenses and one for revenues, but these were ‘unusable’ and ‘dubious’ (Galli, 1860). Galli (1860) continued that, since 1837, no authorities within the Treasury Management had kept their statutory books and there had been no audits of even their cashbooks between 1836 and 1843, despite him being the General Accountant through this period. He concluded that the accounts of the administrative departments of the Regia Camera Apostolica were ‘total anarchy’, being compounded by the lack of sense in the underlying records (Galli, 1860). This further underlines the organisational incompetence during this period, which allowed FSF to be perpetrated.

The special committee assigned to solve the issue drew up a single balance sheet for the entire decade from January 1835 to December 1844, breaching the rule of annual balance sheets. They agreed to divide this concocted balance sheet by 10 to create annual accounts. After reviewing and approving the Committee’s report, Antonelli (by then the General Treasurer) wrote a letter (Antonelli, 1860) dated 12 July 1845, approving the Committee’s preliminary efforts and commissioning Galli alone to produce the balance sheet for the decade 1835–1844. It was not until late 1847 (18 months later) that Galli delivered his final report of revenues, expenses, deficits, liabilities and assets (Bossi, 1914c). In doing so, Galli confirmed the unreliability of the entries in the 1835–1844 balance sheet, stating that the assets and liabilities required adjustment and correction due to miscalculated payables and receivables and other information that had been missed (Bossi, 1914c). As he was unable to determine the actual deficit for each year, Galli estimated the entire decade. Unsurprisingly, his efforts were criticised. Farini (1850) writes, Galli, the general accountant of the Reverenda Camera, muddled the figures although pretending to have done it well, but he was just throwing dust in our eyes. (p. 144)

It was argued he did not have the requisite records, was not familiar with the facts and therefore misrepresented them, using false or even expressly made-up facts as valid (Tosti, 1860). Furthermore, despite Galli reporting to Tosti during this period, Galli was specifically blamed for the state of affairs: The Congregazione di Revisione repeatedly asked to have the state accounts while Cardinal Tosti was at the helm. The Accountant of the Camera Apostolica, Angelo Galli, was blamed by everyone for such an incredible, decade-long recalcitrance. (Gualterio, 1850: 173)

After Cardinal Tosti had been replaced as General Treasurer, he wrote a chronicle questioning Galli’s results, objecting in particular that the liabilities and deficits had been widely underestimated (Tosti, 1860).

16

Tosti (1860) disclaimed any involvement in Galli’s concoction of accounts, disagreeing with values reported for publicly owned buildings, government bond repayments, use of the reserve fund, the dates of the payment orders during the 10 years or before, and the earnings from real estate sales. He also highlighted the negative impacts from extraordinary events, such as the cholera epidemic in 1837 and the flood of the Po River which helped create the deficits. Yet Tosti (1860) continued to divert blame from himself, and onto Galli, arguing that the annual budget deficits could not be attributed to the General Treasurer (himself) because he could only consolidate the Ministerial budgets and did not have the power to negotiate the planned expenses. For him, Financial results were achieved by means of the control, supported by ‘demonstration accounts’, and not by a [complete] report . . . If accounts and reports were badly kept it was the fault of the bad execution of the accountants working in the peripheral departments, not of those belonging to the Camera Apostolica. (Tosti, 1860: 567–568, emphasis added)

Farricelli, a lawyer and expert of public finance, concurred with concerns about the falseness of the accounts, but also worried about the judiciousness of publishing the report, stating, I wonder whether it was cautious – Arcana Imperi evulgare – to publish the data in these times, when all enemies of the governments, and especially of the Papal State government, take every opportunity to slander them. (Farricelli, 1850: 7)

Both Farricelli (1850) and Tosti (1860) stated that instead of past results, future needs should be focused on, including ‘providing the State Finance with the resources necessary to face future needs and collect outstanding debts’ (Farricelli, 1850: 7). This was particularly because Galli stated that deficits ‘might increase considerably as some sums that are still recorded as State assets, are uncollectable’ (Galli, 1851: VII).

Deputy Minister of Finance period: 1849–1854

The evidence shows the outcomes of organisational incompetence, but also falsification of assets and liabilities which indicates Galli was likely to have been promulgating FSF. Despite this, on 15 July 1849, hard Galli was appointed Deputy Minister of Finance. He proceeded to breach the principle of annual reporting soon afterwards, when he drew up the balance sheet for the three years 1845–1847 and published it on 26 June 1852 (four and a half years late). Martinelli (1860) claims these figures were also untrue and reported that Galli acknowledged that the Pontiff was asked to issue orders of payment despite insufficient funds.

17

Rather than taking the blame, Galli argued that the lateness of the accounts was due to political unrest, the Roman Republic and the regulatory changes effected on the Pope’s return to Rome. Indeed, to transfer this blame onto constitutionalists and republicans, he separated the diciottimestre (the 18-month period of revolutionary upheavals from January 1848 to June 1849

18

) from the preceding three years (1845–1847). Bossi (1914c), albeit commenting six decades later, argued that rather than blaming external events, those who led the State should have taken the blame, as for years, the Congregazione di Revisione had in vain asked Galli to produce the balance sheets, but he failed to do so. In respect to Galli therefore, Roncalli (1884, Letter 12 July 1852) stated, The State Budget drawn by the pro-Minister of Finance [Angelo Galli] appears to be prepared not by a well-trained financier but by a murky accountant. In fact, the budget does not present any idea but only a tour of numbers, probably misstated or unfounded.

Farini (1853) agrees and provides an insight as to why he could stay in his post: Angelo Galli was a figure-muddler. Formerly an accountant at the Treasury office, with his abacus he had muddled things up so much that only he could read into them: treasurers and ministers had to resort to him only, as if he were the reader of inexplicable hieroglyphics. Good old Cardinal Tosti did not think much of him, but he kept him in office, because he had become a necessary tool; Antonelli, Tosti’s sly successor, could not do without him, even if he said he disliked him; Pius IX’s Council, which valued him for what he was worth, had to resort to him, otherwise it would get lost in the labyrinth of his figures. If he wanted to produce the 1847 balance sheet, Monsignor Morchini had to rely on the figures of those ten-year accounts, around which Galli had spent a lot of time and earned a lot of money, without accounting for it: Ministers, lay and republicans had to go to Galli if they wanted to have the details of those accounts that were his secret, his Kabbalah, his genius . . . he became the prince of the Pope’s finances, despite . . . that he had made a dishonest name for himself, once found guilty of smuggling, of lavishing privileges on his relatives, of mixing with contractors, of turning the fortunes of a miserable nephew, whose guardian he was, to his own advantage. (pp. 233–234)

Leti (1909: 56) also confirmed that Galli ‘muddled things up’, was a dishonest person, and his important office allowed him this freedom. Thus, he had both opportunity and apparently also provided a rationale for being fraudulent (as per Cressey, 1953) and used his organisational appointment to perpetrate (in this case) FSF. Despite the ‘figure-muddling’, Galli had constantly proven to be loyal to the Papacy, which could not do without him and could rely on his total discretion and loyalty. It is unsurprising that, in one of his financial reports Galli (1851), first lavishes praise on his own work as a public accountant and on his accounts, before blaming others for the financial difficulties. In this example, he blames understaffing and perhaps also a lack of training: The General Accounting Department of the Ministry of Finance has so diligently and accurately entered and re-organised all the accounting records of every Ministry and every management will find the boundary of its interests perfectly defined; and, as soon as such a department can complete its internal development, this gap will be filled by efforts that, though big, will go like clockwork. (Galli, 1851: 23–24)

Nevertheless, Bossi (1914b), the historian, lays the blame for the parlous state of the Papal States’ finances at Galli’s feet: With bad timing, a political shambles deeply affecting governance, poorly managed public finances, exceedingly scattered responsibilities, the underlying records of the balance sheets in full chaos, the Ministry of Finance crumbled just as any other Papal authority, rapidly waning into its inglorious ending. (p. 188)

This is further evidence of the organisational incompetence that allowed in this case, FSF and other fraud to take place.

As a Deputy Minister of Finance, Galli was also trusted to derive monetary policies and regulate the State Bank.

19

Yet, he took out new loans to pay interest on older loans creating a vicious cycle and, due to the availability of cash, fuelling more spending. In terms of monetary policy, Galli recalled the paper money issued during the Republican age,

20

as well as coining new copper coins which exceeded the necessary gold reserves and had to be recalled (Bossi, 1914e). Bossi (1914b: 186) noted, ‘This Minister of Finance was resource-less’. It is unsurprising that The economic ideas that Angelo Galli wrote about were censored by everyone for being against the basic elements of sound, good economy. Sadly, seeing the State’s finances managed by someone who proved to be so patently ignorant of the economic science was really painful. (Gualterio, 1850: 173)

He also encouraged others to enrich themselves at the Papal States’ expense. For instance, Angelo Galli repeatedly authorised Giovanni Pietro Campana, director of Rome’s Monte di Pietà, to ‘lend’ himself sums of money and not to repay them. Campana was eventually caught after he stole nearly one million scudi from the Bank between 1854 to 1857; he had previously hidden the deficiencies by borrowing money from Rothschilds, then the Papal bankers (Bossi, 1914e).

Galli was replaced as Treasurer by Mons. Ferretti, Comm. of the Holy Spirit. Mons. Ferretti refused to accept his appointment until Galli presented him with a report regarding his financial management (Roncalli, 1884, Letter 25 November 1854). While financial management was bad under Galli, our next accountant, Giacomo Antonelli ‘brought the State to total ruin’ (Bossi, 1912b: 504).

Cardinal Giacomo Antonelli – General Treasurer 1845–1847; Secretary of State 1848–1870

Giacomo Antonelli was very proficient in accounting and finance. He had some business ability and had benefitted from the chance to work with his brothers (especially Filippo), who were prominent figures in both policy and Rome’s economic sphere. Antonelli became powerful and was favoured by Pope Pius IX; however, he accumulated enormous wealth during his long mandate as Secretary of State. He was accused of corruption, including nepotism; for example, he appointed his brother Filippo to the helm of the Roman Railways and Banco di Roma and his brother Luigi to the position of chief of Rome’s food supply (Aubert, 1961; Tomassini, 2011). 21 Giacomo Antonelli had the opportunity to manage contracts and therefore he reserved the best contracts for relatives and friends (Bianchi-Giovini, 1861).

Giacomo Antonelli was born in Sonnino, southern Lazio, on 2 April 1806. He was born into a humble family which nevertheless rose through business ventures and later made its fortune from real estate speculation. As his father Domenico wished, Giacomo Antonelli attended the Collegio Romano School to pursue a career in the Papal Administration, studying humanities at the University of Rome where he took the ‘laurea inutroque’ (a civil and canon law degree) in 1827. In 1830, he joined the Prelatura iustitiae beginning his service as a manager for the Papal State (Soderini, 1929), as summarised below and in Table 1. He died in Rome on 6 November 1876, leaving a large fortune to his relatives and an alleged daughter, although they fought over the inheritance. 22

General Treasurer period: 1845–1847

Following his appointment as a manager in the Papal States in 1830, in 1835 Antonelli was appointed provincial delegate of the Pope at Orvieto, in 1837 at Viterbo and Macerata in 1839, gaining experience and refining his governance and management skills. In 1840, he was summoned back to Rome, replacing Cardinal Mario Mattei, as Minister of the Interior. Contemporaneously, he was appointed Canon at San Pietro, thus starting his path towards the Roman Curia. He took holy orders up to the diaconate, despite having no theological education, but did not take the vows and, for this reason, he did not became a priest (Coppa, 1990). On 5 January 1845, Pope Gregory XVI supported Antonelli to take over the leadership of the Ministry of Finance from Cardinal Antonio Tosti. He was appointed ‘pro tesoriere della Camera Apostolica’, that is Treasury deputy of the Apostolic Chamber and by 25 March 1845, he was appointed General Treasurer.

Antonelli was highly regarded by Pope Gregory XVI. Indeed, he was allowed to sit at the Pope’s bedside when he died on the 10 June 1846 (Falconi, 1983). However, Antonelli became even more powerful when Pope Pius IX was elected, as he served as the Pope’s expert in policy and finance matters. On 11 June 1847, at the age of 41, he was appointed cardinal of the Roman Church, despite not being a priest, but because he had managerial and accounting skills useful for the Papal States (Regoli, 2012) (see Figure 3). On 15 November 1847, he became President of the ‘Consulta di Stato’ (State Council).

Antonelli pre- and post-Cardinal.

Secretary of State period: 1848–1870 (1848–1859 covered here)

During the 1848 civil riots, Antonelli was elected State Secretary and then behaved as a Republican. Following the re-establishment of Papal power from 1849 he reverted and persecuted his political opponents. He introduced an authoritarian regime, thus strengthening Pope Pius IX’s conservative approach both for religious and political matters. He was appointed State Secretary again on 18 March 1852, continuing in this post until the end of the Papal States in 1870 and then, in the Papal administration until his death (Vetere, 1871).

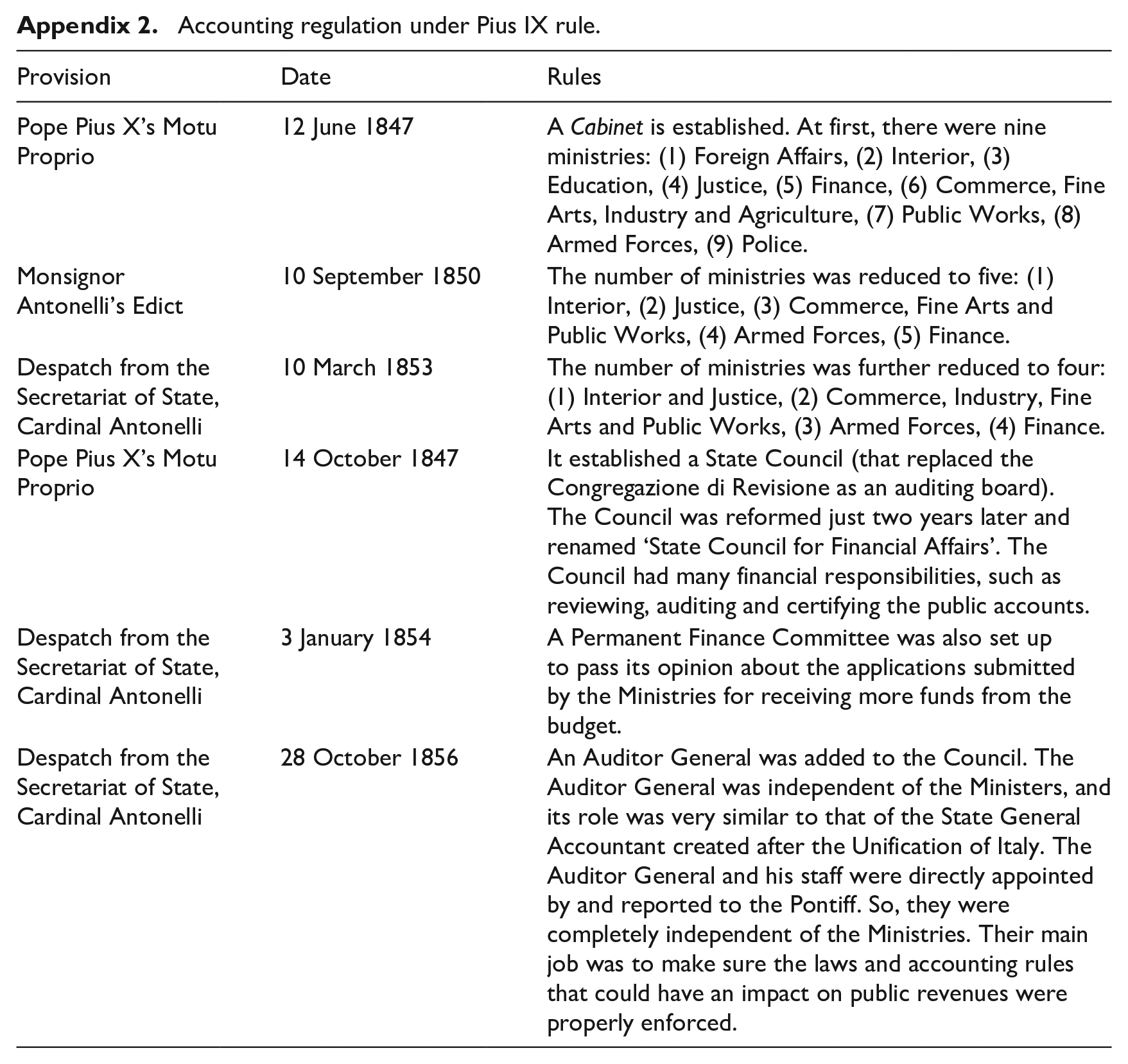

Despite backing the revolutionaries for a short time, as Secretary of State, Cardinal Antonelli played a pivotal role in the administrative and political reforms throughout the office of Pius IX up to the fall of the Papal States in 1870 (Anonymous, 1859; Coppa, 1990). He was responsible for all of the legislative regulations in terms of civil relations (Mombelli Castracane, 1987), the commercial code (Fortunati, 2011) and the penal code (Stato Pontificio, 1862) (except for motu proprio directly issued by the Pope). A complete list of such reforms is in Appendix 2.

Some argue that dishonesty and corruption were at their highest point during Antonelli’s time as Secretary of State. Cardinal Francesco Pentini (1863) notes, There were dismissals at the Mint in 1851 for thefts of metal; one of the dismissed workers was appointed lieutenant in the Financial Police. In 1854, a high-ranking officer, having learnt through his office that duties would suddenly increase very soon, told a shopkeeper, who purchased goods beforehand and repaid him for his favour; for this, he received 500 scudi. (p. 7)

Antonelli was able to use his position within the Papal States to perpetrate corruption and nepotism. Furthermore, he was apparently able to make a rationale for fraud (as per Cressey, 1953) and was unconstrained by bonding and monitoring activities which are called for in agency theory, such as audit and internal controls, even though he instigated them. Bossi (1914c) reminds us that Ritter von Schulte, a German theologian, wrote in his memoirs (Lebenserinnerungen drei Bände) in 1854: Finances are in a scary state. There are only big copper coins around, and such copper cannot be exchanged with silver . . . The Secretary of State, Cardinal [Antonelli], is assumedly to be blamed for this horrible economic situation, and I have heard that the cardinal had some colossal swindles hushed up. (p. 400)

Examples of monitoring that Antonelli implemented were Pope Pius IX’s 1850 auditing reforms, establishing the rules for the functions and related competences of the State Council which took the place of the Congregation of Review. It was required to undertake the following financial tasks:

(a) examine and review the balance sheets and accounts of the States and of public administration;

(b) vote on the budgets;

(c) provide final verdicts on the balance sheets;

(d) produce opinions in relation to the creation and the paying off of new debts, and the imposition, abolition and distribution of new taxes (Raccolta, 1851: 211–221).

Nevertheless, this reform (the State Council) was ineffective. Furthermore, Antonelli issued a dispatch (no.79690 dated 28 October 1856), entitled ‘Regulations for the general control established in the Papal States’ (Raccolta, 1857: 274–289), requiring a General Supervisor to join the Council. The General Supervisor was to be independent from the ministers and he and his colleagues were appointed directly by, and were answerable to, the Pope. They were to ensure laws and administrative regulations were enforced. In particular, they examined preventively all warrants for payment, declining those issued beyond the budget limits, hoping to keep spending within budget (Stato Pontificio, 1857). Nevertheless, despite the progressive reduction in the number of ministries, and therefore reduced expenses, and the implementation of new rules, including new managing and auditing boards, the Papal finances were always in an extremely precarious condition, and the State failed to make a surplus. Indeed, to fulfil its most urgent obligations, it was forced to continue borrowing money from banks (Ministero del Tesoro, 1961: 191). Antonelli continued in post until 1870, which is outside of the period for this article, but his fraudulent actions continued inside an incompetent organisation.

A summary of the three men and their (in)competence and fraudulent activities is provided in Table 1.

Discussion

This research sought to explicate the differences between fraud and incompetence and how the Papal States encouraged incompetence or was used as a ‘vehicle for fraud’ (Pontell, 2005) through a prosopographical study of three senior Italian accounting bureaucrats whose work lives overlapped during the reign of two Popes. They had the capacity to direct accountants (Charle, 2015) and thus appear indicative of the group that Antonelli et al. (2021) identified as having divergent aims to that of the Pope who sought good financial management (as argued for by Soll, 2015). Specifically, we analysed the financial management and accounting work of Tosti, Galli and Antonelli to provide relevant evidence of accountants and their integrity (or otherwise) within an incompetent organisation. We argue that they were not outliers (as per Lee, 2015) but that their backgrounds and careers provide an alternative perspective on the environment in which accountants’ behaviour was antithetical to that of the State (as shown by Antonelli et al., 2021). Classically, they shaped the society in which they worked (as per Hopwood, 1976).

Incompetence has both individual and organisational aspects. Tosti, our first ‘accountant’, was generally deemed incompetent although it is likely his motivations were honourable (as suggested by de Bruin, 2015) towards the Papal State, given his actions to keep it afloat. Despite accounting being important for the survival of the Papal State (Antonelli et al., 2021; Soll, 2015), Tosti allowed poor bookkeeping and failed to obtain accounts to enable management of the Papal States whose financial difficulties were clearly visible in 1846 (Montani, 1846), 1857 (Margotti, 1857) and upon its demise in 1870 (Antonelli et al., 2021). Practice was at odds to what was required in the Papal States but also in other Italian States, for example, the Kingdom of Sardinia and the Grand Duchy of Tuscany. In the latter State, if the administrators responsible for publishing the accounts were late, their salaries were stopped (Coronella et al., 2013). While the Papal States had a regime of similar fines, there is no record of them being levied, thus disempowering financial management. Despite an increasing number of rules, regulations and audits, the Papal States’ financial situation did not improve; for example, establishing the ‘Congregazione di Revisione’ in 1847 made no difference to practice, as that body’s requests of Angelo Galli to produce the accounts did not bear fruit (Gualterio, 1850).

Organisational incompetence derived from poor decision-making, disasters (such as uprisings) (Kauppi and Van Raaij, 2015), and an inability to learn from its mistakes (as suggested by Ott and Shafrits, 1994). Furthermore, in light of the lack of training for accountants until at least 1836 (and then only ‘on the job’), organisational incompetence was evident in the employment of Tosti and others with inadequate training (as noted by Ziegenfuss, 1996). Tosti was arguably incapable of understanding or carrying out the goals of the principal (the Curia) (Kauppi and Van Raaij, 2015). He was unable to manage Galli and to monitor subordinates to achieve the goals of the Papal States and died poor. In light of such organisational and individual incompetence, ambiguity and goal confusion arose from and reinforced poor decision-making and financial management. Evidence suggests this lack of training was a feature of the accounting bureaucrats, whether they were clerics or lay. While this was a feature of nineteenth-century accountancy (Anderson and Walker, 2009; Carnegie and Edwards, 2001; Carnegie et al., 2003), it was imperative for training to lift competency, and this did not appear to occur, especially with Tosti in charge.

In respect to fraud, the cases of Galli and Antonelli allow us to extend beyond Jones’ (2011) fraudulent false accounting, to include Archambeault et al.’s (2015) wider notions of asset misappropriation, corruption, and FSF (financial statement fraud) (see also Heier, 2016). Evidence of nepotism from the fraudulent activities of Galli and Antonelli should be added to this list. They used the Papal States as a ‘vehicle for fraud’ and, by acting inside the organisation, were able to make greater gains from fraud (as in Heier, 2016; Pontell, 2005; Wheeler and Rothman, 1982). The Papal States provided legitimacy and size that made larger frauds plausible, and potentially delayed the discovery of fraud. We did not examine the Papal States acting as a ‘sword’ to steal from others due to our focus on accountants rather than the organisation. We observe Galli and Antonelli using the organisation as a ‘shield’, as they hid fraud and diverted blame when they were exposed. They averted detection and negative sanctions (Pontell, 2005) perpetrating fraud by neutralising internal controls. Their actions speak of Papal States accountants’ values (Carnegie and Napier, 1996) and evidence (e.g. Belli, 1998) suggests accounting staff were encouraged to assist in fraudulent activities.

Some frauds leave little evidence and can be hard to detect (Dye, 2007; Jones, 2011). Due to our dependence on archival materials, and the lack of official enquiries on these sensitive issues, we are unable to assert that Galli or Antonelli defrauded the Papal States through asset misappropriation, although their positions (as well-placed insiders) does not rule it out (see: Agostini and Favero, 2017; Gibelman and Gelman, 2004; Heier, 2016; Heier and Leach-López, 2010). Anecdotal evidence (from secondary sources) suggests that many leaders in the Papal States availed themselves of numerous perks (asset misappropriation), argued by LeClair (2019) to be ‘soft corruption’. Furthermore, as shown in Table 1, both Galli and Antonelli left considerable legacies which were far in excess of that which a cardinal could have been expected to amass. This evidences asset misappropriation and Bossi (1914a, 1914d) notes that many scandals were hushed, so they avoided sanctions. This has similarities to Lee (2015) where the Waddell brothers were able to emigrate and thus evade sanctions for their frauds.

Archival sources also provide evidence that Galli and Antonelli perpetrated fraud of other types. Both men were offered the post of Cardinal with their accounting role, smoothing a path to the upper reaches of the Church in the absence of apparent religious merits (and strengthening their ability to use the organisation as a ‘shield’). This reveals the strategic importance afforded by the Papal States to those who managed the public accounts, despite the poor advice they may have provided. Both Popes during this period studied were more focused on spiritual matters, with the decision-making during Pope Gregory XVI’s reign being undertaken by successive Secretaries of State and Pope Pius IX placing complete reliance on Cardinal Antonelli. While Pius IX had accounting reforms passed in his name, Galli and Antonelli chose both what to make visible and which regulations the accountants should follow (Antonelli et al., 2021) (as also in Carnegie and O’Connell, 2014).

In respect of corruption, we find that Galli and Antonelli used their positions to enrich themselves, often through backhanders from contracts let to friends and relatives. They also utilised nepotism as a further form of fraud, by letting these contracts and by appointing their relatives to high level (lucrative) positions (e.g. Galli’s corruption through Giovanni Pietro Campana; Galli’s and Antonelli’s nepotism through sons and siblings). These are examples of how an individual can make greater gains from acting inside an organisation, using the organisation’s resources as a ‘shield’ and neutralising internal controls to defraud the organisation (Pontell, 2005; Wheeler and Rothman, 1982) and is an extension of Heier (2016) where the fraudsters extracted funds only.

We noted that Archambeault et al.’s (2015) FSF has two roles, either to mask fraud or to undertake fraud. We found Galli was instrumental in the lack of proper records (as per Fremont-Smith and Kosaras, 2003; see also Antonelli et al., 2021). He failed to abide by rules he developed for annual accounts and independent audit, producing financial statements that were seriously late and with figures that were incomplete and misleading. Rather than the creative accounting techniques explained by Melis (2011) in the Italian for-profit sector in the twentieth century, Galli refused to provide reporting at all, which may have had the same result. Certainly, the reports he eventually provided have the flavour of the Italian examples provided by Melis (2011) where entities massaged the financial statements to provide positive messages to stakeholders. Galli’s twisting of monetary policy (e.g. issuing currency beyond the reserves held) is another example of FSF.

Evidence shows Galli had the opportunity through his high position to undertake fraud; despite Tosti and others demanding financial statements, Galli failed to provide them, the lack of sanctions providing a rationale to undertake fraud. It is unclear whether he was under pressure to do so (as per Cressey, 1953). Antonelli’s position provided the opportunity to undertake fraud; he was also unconstrained by internal controls, making a rationale for fraud (as per Cressey, 1953). Although we have no evidence of the pressures these men may have been subject to, we find that they had opportunity and rationale (Cressey, 1953) to undertake fraud. We also note that the lack of internal controls and detection allowed fraud (Fremont-Smith and Kosaras, 2003; Pontell, 2005), in particular due to the high trust the Popes placed in them, especially Antonelli. These classic hallmarks of fraud typify the dynamic and socially constructed practice of accounting and (low levels of) social controls (Walker, 2016) that failed within this organisation, simultaneously Church and State.

Dye (2007) suggests that when incompetence and corruption exist, the public become weary and more tolerant, instead of attempting to change the status quo. In the case of the Papal States, as an absolute monarchy, no public accountability was expected or required. The Republican effort was quickly quashed, and therefore incompetence and fraud continued without public complaint. Specifically, the clergy-bureaucrats were disinterested in being transparent with their subjects and lenders about their asset management. Nevertheless, they were heavily criticised by the public (Bossi, 1914c; Farricelli, 1850). Such critique is surprising as, among the contemporary Italian States, only the Grand Duchy of Tuscany published its financial statements for citizens’ use (Coronella et al., 2013).

The Papal State required an adequate architecture of procedures, accounting books, balance sheets, accountants and auditors. However, while other historical research reveals that standards of efficiency, accountability and ethics imposed on accountants and accounting methods in religious organisations are much higher than those prevailing publicly and privately elsewhere (Baker, 2006; Barlev, 2006; Gallhofer and Haslam, 2004; Hagerman, 1980; McKernan and Kosmala, 2007; Moerman, 2006), in the specific case of the Papal States, such standards appear decidedly very low. This is despite the steady increases in monitoring, or at least the establishment of auditing authorities (see Appendices). The appointments and continuation of Tosti, Galli and Antonelli may be attributable to a lack of democratic scrutiny and sanctions. The collective biography enables an ‘alternative narrative’ (Charle, 2015; Lee, 2015) of accountants who incompetently or wittingly enabled the Papal States bureaucrats to disempower financial management and assisted its demise.

Conclusion