Abstract

The paper discusses the historical development of the debate on financialization supported by bibliometric analysis. There are several origins of the concept of financialisation in the 1990s, and in the early 2000s, this consolidates in a transdisciplinary project: an attempt to create a critical conversation across academic disciplines about the impact of finance on the economy and society. This was driven by the team of CRESC by organising workshops and special issues, involving critical business studies, constructivist approaches to the household and heterodox macroeconomics. This created the basis for the success of the concept and, since the global financial crisis, enabled an explosive rise in studies on financialisation. But with success also came a fragmentation of the debate and its disintegration along disciplinary lines. Thus, research on financialization today is published in more prestigious journals, but it has decoupled from the core financialisation debate of the 2000s.

Introduction

Financialisation has moved from a niche academic topic to a buzzword that can be found in major newspapers. First used in the 1990s, the term financialisation gained traction in the early 2000s and then became a popular topic in academic research, with several hundred papers on the topic now published every year. Today, the debate on financialization appears diverse and sprawling. The Routledge International Handbook of Financialization (Mader et al., 2022a; 2022b) features 43 contributions: The debate covers debates on corporate governance (what are the priorities of firms? In whose interest are firms run?), on how households deal with growing debt levels to speculation in commodity markets. It spans several disciplines, from economics, business studies, sociology to geography. Today, it is nearly impossible to survey the overall debate as it has grown both in terms of the sheer number of publications as well as in terms of the academic fields and thematic sub-debates. Van der Zwan (2014) is the last overall survey of the financialisation debate. Various survey papers cover particular areas of financialisation: Davis (2018) and Klinge et al. (2021) on corporate financialisation, Bobek et al. (2023) on the financialisation of households, Hein and Van Treeck (2024) on the financialisation of demand and growth regimes and Bonizzi (2013) on financialisation of emerging and developing countries. Palludeto and Felipini (2019) is one of the very few attempts to use bibliometric tools to identify clusters within the debate. The growth and fragmentation of the field is so rich in detail that it seems impossible to survey in its totality.

The contribution of the paper is that it proposes an interpretation of the evolution of the financialization debate backed by bibliometric analysis. In a nutshell, the argument is that there has been a dialectic movement from a transdisciplinary research program, which allows for the concept to become established in the academic discourse. When the Global Financial Crisis (GFC) hit and led to a boost in public as well as academic interest in critical analyses of finance, the financialisation debate received a boost and grew dramatically in size. The very success of the transdisciplinary early research program led to increasing recognition as well as to disciplinary fragmentation. A bibliometric analysis establishes stylised facts. It documents, first, an explosive rise of the literature since 2008. Second, financialisation analyses are now published in more prestigious journals. Third, it shows a change in the disciplinary landscape with heterodox economics declining and political science as well as mainstream economics rising. Fourth, the recent debate is decoupling from the foundational research on financialisation.

This paper distinguishes three periods: inception, consolidation and explosion. While there were several origins of the concept of financialisation in the 1990s, in the early 2000s this consolidates in a transdisciplinary agenda: an attempt to create a critical conversation across academic disciplines about the impact of finance. The trans-disciplinary conversation was driven by the team of the Centre for Research on Socio-Cultural Change (CRESC) at the University of Manchester, organising workshops, conferences and special issues; a second centre was the University of Massachusetts at Amherst, whose scholars provided a macroeconomic framing based on heterodox macroeconomics and explored in particular corporate financialisation. CRESC propagated a transdisciplinary research agenda that included critical business studies, constructivist approaches and post-Keynesian and regulationist macroeconomics (Ertürk et al., 2008b). This created the basis for the success of the concept in academia by generating the critical mass, and it enabled an explosive rise once the global financial crisis (GFC) broadened interest in issues of finance. With academic success also came a fragmentation of the debates on financialization and its disintegration along disciplinary lines. Once financialization gained enough visibility and prominence, research is increasingly situated in the debates of a given discipline. This can be interpreted as a decline of the original transdisciplinary financialisation project or its successful establishment within the organisation of academia.

The common ground of the debate had always been thin, but in the consolidation period two core features can be identified (see also Mader, Mertens and Van der Zwan 2020a; 2020b, p. 5). First, it was held together by a sense that the role of finance (in contemporary society) has changed; that finance is increasingly impacting areas (e.g. households) that had little exposure to it. As a consequence, the study of finance needed to go beyond its original disciplinary home as a subfield of economics. It needed to transcend traditional disciplinary boundaries and fuse economic and social analysis. Specifically, it needed to fuse heterodox economics and cultural political economy; and it needed a wide range of methods to appreciate changes at the level of agents as well as the changes at the systemic level. Second, the sentiment that financialization has had negative economic and social impacts. This highlighting of the ‘dark side of the growth of finance’ has been particularly important in the 1980s and 90s when in mainstream economics there was a strong positive view of financial deregulation, for example, McKinnon (1973) blamed financial repression for low growth in developing countries, Jensen and Meckling (1976) praised shareholder value orientation and Levine and Zervos (1998) argued that more finance was good for growth.

It is in particular the first leg of the debate (transdisciplinarity and anchoring in heterodox economics) that has been eroded over time, and this is in part an indication of its success. First, there has been a specialisation and fragmentation of the debate, which often proceeds along disciplinary lines. Recent contributions on financialization have become increasingly decoupled from what constituted its core in the first decade of the 2000s, and this has a strong disciplinary component, in particular a separation of economics and the social sciences. While most participants in the debate would readily agree on the need for a transdisciplinary approach, in practice the forces of disciplinary gravity exert an enormous pull. With the success of the concept it is becoming more widely used. A major change here is that mainstream economists (e.g. Jorda, Schularick and Taylor 2016) have since the Global Financial Crisis (GFC) also begun to use the term without relating to the financialization debate. A whole sub-stream of the financialization debate, the financialization of commodities (e.g. Ferrer et al., 2018; Tang and Xiong 2012), has hardly any relation to the core of the financialization debate but builds on debates in mainstream finance and economics.

The paper is structured as follows. The next sections follow a chronological order. Section 2 discusses the inception period. Section 3 covers the consolidation and the pivotal role of CRESC. Section 4 highlights some aspects of the explosion period of the debate. Section 5 provides bibliometric evidence for the changes in the debate. Section 6 discusses two interpretations of the evolution of the debate. Finally, section 7 concludes.

Inception

There are several possible origins of the term financialisation. Two notable works used it early on but had limited impact on the later debates. Giovanni Arrighi’s (1994) Long Twentieth Century is a wide-ranging historical analysis of hegemonic cycles since the Renaissance. It builds on world systems theory and argues that in the upswing of the cycle, the hegemon is leading in terms of production, innovation and competitiveness, whereas in the downswing phase of the cycle, the declining hegemon shifts from production to finance (thus financialisation). This is, first, because the hegemon finances investment and innovation in countries with more dynamic growth and, second, the growing military expenditures of a declining empire lead to public borrowing, which corresponds to a shift in private wealth accumulation. Arrighi (following Fernand Braudel) locates financialisation at the autumn of international hegemony. In contrast, later research on financialisation focused almost exclusively on developments in the late 20th century: the move from Fordism to neoliberalism. Another possible origin is Sweezy (1997), which, in a short three-page editorial, identifies the ‘financialisation of accumulation’ as a defining feature of the post-1975 period, next to slow growth and rising oligopolisation. Sweezy (1985) interpreted the ‘financial explosion’ (no use of the term financialisation yet) as a response of capital to the stagnation of monopoly capitalism. The financial sector, once deregulated, fosters growth as well as instability. Sweezy claims that financial crises would be responded to by government intervention but offers no systematic analysis of how financialisation impacts economic growth. Sweezy’s analysis did have an impact on Marxist research of financialisation, but little beyond.

The inception of the concept of financialisation in the sense it is used today is primarily due to the sustained efforts of a group of researchers at CRESC at the University of Manchester. 1 This group is significant not only in terms of its own research but also for organising workshops and editing special issues. This would provide the basis for a transdisciplinary research agenda, which brought together quantitatively oriented economists, critical business scholars and constructivist cultural political economists. 2

The Economy and Society 2000 special issue marks the end of the inception period; it brings into place many of the ingredients of the ensuing debate. The special issue has a paper by Froud et al. (2000b, p. 80) that analyzes ‘value-based management as part of a process of financialization’ and emphasises that ‘If the results are contradictory and disappointing, a persistent gap between expectations and outcomes can nevertheless drive management behaviours, which change the world’. This tension between ambitions and promises by managers and management consultants that often fail to deliver the intended outcomes, but still have profound economic and social effects, would remain a hallmark of their work in the following years. One of the most influential papers on shareholder value orientation for the financialisation debate is Lazonick and O’Sullivan (2000), who analyse shareholder value in the USA and coin the term of the shift from ‘retain and re-invest to distribute and downsize’. Three features of the special issue are noteworthy: First, the starting point is shareholder value orientation. The conduct and governance of firms is at the centre of the analysis, but there is also concern for their macroeconomic outcomes. However, a systematic analysis of households is yet absent. Second, the organisation of the special issue takes an internationally comparative approach and, in addition to the USA and UK, also analyzes changes in corporate governance in Germany and France. Third, there is a strong presence of the French Regulation School (Aglietta 2000; Boyer 2000), which tried to conceptualise the changes since the demise of Fordism and explore the possibilities of finance-led growth.

Consolidation

In the consolidation phase of the debate, which we date from 2000 (the first special issue in Economy and Society) to 2014 (the publication of van der Zwan’s survey), insights and arguments from the inception period began to be synthesised (though inception continued e.g. in the area of household financialisation). In this period, CRESC played a central role in shaping and establishing the debate on financialisation. They provided a platform for debate for scholars from different fields and sought to establish a common ground for the debate. This common ground included a temporary marriage (possibly an affair more than a marriage) between constructivist micro-level analysis and post-Keynesian and regulationist macro analysis. This common ground is tenuous, not fully agreed upon, but it did serve as a transdisciplinary, inclusive research agenda and it played a crucial role in establishing financialisation as a term in research across several academic disciplines.

The team at CRESC worked on shareholder value orientation and emphasised the discursive element, that is, the narrative and (ultimately unfulfilled) promises, of shareholder value orientation, but also analysed factual outcomes and encouraged quantitative research on its impact (Froud et al., 2000a). This was based on extensive case studies in the automotive sector (Froud et al. 2002, 2006). They also had a series of papers on how households were drawn into the system by what they call the coupon pool (Froud et al., 2001, 2002). Rising inequality and a change in pension systems mean that a larger share of savings goes into stock markets; consequently, share prices are rising. This reinforces shareholder value orientation. While the analytical framework has Keynesian elements (demand formation), its analysis of the financial sector is not Keynesian: demand for assets is out of savings, and there is no consideration of credit creation that might fuel asset demand.

The discussion of corporate financialisation took a quantitative turn. Stockhammer (2004) provided econometric evidence that shareholder value orientation (measured by rising financial income and payments by non-financial businesses) negatively impacted business investment and explained a substantial part of the slowdown of capital accumulation from the 1960s to the late 1990s. While this study used national data, the following literature (beginning with Orhangazi 2008) often uses firm-level data (e.g. Davis 2017; Rabinovich 2019; Tori and Onaran 2018).

Krippner (2005) is the most widely cited paper on financialisation. It defines financialisation ‘as a pattern of accumulation in which profits accrue primarily through financial channels rather than through trade and commodity production’ (p. 175). The paper is written in conversation with the post-industrialism literature (thus her classification contrasts developments in manufacturing, services and the financial, insurance and real estate sector. She shows that there is a substantial increase in (gross) financial income relative to cash flow since 1970 for non-financial corporations and that profits of the financial sector have risen relative to those of non-financial sectors. Krippner offers a very careful empirical analysis, but her analysis remains descriptive and does not attempt to identify causal impacts. She is focussed exclusively on (financial or non-financial) corporations and their profits, whereas households are absent.

The book Financialisation and the World Economy (Epstein 2005) is the result of another important institution for the financialisation debate: the University of Massachusetts at Amherst (UMass). Epstein’s introduction to the volume is widely cited, and his seminal definition of financialisation served as a common denominator for later research. However, the impact of the other contributions of this volume on the financialisation debate has been modest. A key difference to CRESC-led debates is that it is more centred in the analysis of the global financial system (the post-Bretton Woods system, Euro dollar markets) as well as on developing countries (e.g. the financial crisis in Turkey, papers on Mexico, Brazil, Argentina and Korea). Overall, there is a macroeconomic focus that does not fully match the transdisciplinary approach of CRESC.

While the above literature essentially focuses on economic outcomes and mechanisms, there was also a stream that analysed the impact of financialisation on culture and everyday practices. Two key authors in this approach are Randy Martin (2002) and Paul Langley (2008a), both of whom take a constructivist approach with a Foucauldian inspiration. Thus, discourses about finance, in particular the managing of risks and the spread of investment behaviour to what was considered the working classes, shapes perceptions of the world and identities. These identities, as Langley (2004) demonstrates for the shift to defined contributions investment schemes, clash with realities where poor households have limited capacity to deal with uncertainty. The changes in pension systems have shifted uncertainty from firms to households. The constructivist approach also has important implications for the analysis of the financial sector. McKenzie and Millo (2003) elaborate on how the establishment of Black Scholes equation for the evaluation of option values has transformed the behaviour of financial markets.

The 2008 Competition and Change special issue under the title ‘Questioning Finance’, together with Financialisation at Work, represents the climax of the CRESC approach to financialisation. It was prepared at a time when the Global Financial Crisis was already clearly on the horizon. An important difference from previous CRESC materials is that households and real estate play a more prominent role. Aalbers (2008) analyzes the financialisation of real estate markets and Langley (2008b) securitisation, consumer credit and self-discipline; both are heavy on social theory and do not engage with quantitative analysis. Several of the papers engage with the process of securitisation and changes within the financial sector (Langley, 2008a; 2008b; Aalbers 2008; Crotty 2008). Crotty, in particular, highlights that the risk taking in the financial sectors has increased dramatically. Stockhammer (2008) presents a (non-technical) macroeconomic analysis of financialisation arguing that the finance-dominated accumulation regime came with slow and volatile growth.

The CRESC book Financialisation at Work: Key Texts and Commentary (Ertürk et al., 2008a) provides a state of the art on financialisation (at the time) as well as some of the intellectual origins. It gives excerpts of seminal writings by Keynes on speculation and Berle and Means on the control of the corporation. It includes the papers on the defence of shareholder value orientation (by Jensen and by Fama) as well as critiques. It has both more quantitatively oriented as well as discourse-oriented papers on shareholder value orientation. It reprints some of the Economy and Society 2000 special issue, but quantitative analysis of shareholder value orientation is more developed, as are constructivist approaches. Two issues are noteworthy: The only coverage of households is from a constructivist perspective (Martin 2002), and international finance is not covered. The introduction to the book (Ertürk et al., 2008b) provides the clearest statement of the CRESC research agenda on financialisation. They delineate two axes: for/against financialisation, illustrated by the liberal collectivist approaches of the 1930s and the principal-agent approaches of the 1980s; and the political economy who analyse functional, quantitative relations in the economy and cultural economy approaches (which would later be labelled the financialisation of everyday life) which emphasise performativity. While Ertürk et al. clearly side with the sceptical view of financialisation, they argue that both heterodox economics and constructivist approaches are needed and need to be triangulated. Compared to later developments three features stand out: first, there is a commitment to a transdisciplinary project; second, there is recognition that both quantitative, heterodox economics analyses and constructivist, cultural analyses are needed; third, there is a sustained attempt to synthesize the partial insights into a macro analysis without imposing a systemic logic (for that they suggested ‘coupon capitalism’). Financialisation itself is regarded work in progress and shaped by multiple logics (Ertürk et al., 2008b, pp. 36f).

The focus of CRESC subsequently shifted towards the politics of the global financial crisis. Engelen et al. (2011) developed an analysis of the GFC as an elite debacle that emphasises that ‘finance is not only an economically unsafe and violently pro-cyclical sector but also part of a democracy that is not working’ (Engelen et al., 2011, p. 11). 3

We use Van der Zwan (2014)’s survey of the financialization literature, which has become a standard reference at the end of the consolidation phase. She follows Ertürk et al. (2008b) in identifying three streams (‘approaches’) in the debate: financialisation as a new regime of accumulation, financialisation of the modern corporations and financialisation of everyday life. Unlike Ertürk et al., she makes no strong call for synthesis or triangulation of these approaches and concludes her survey by identifying three contributions that relate to debates in sociology and politics (varieties of capitalism and welfare state regimes). Her essay thus sits between the transdisciplinary agenda and the disciplinary specialisation.

The section has emphasised the central role of CRESC and its activities to establish the term financialisation in the academic debate. The debate and its transdisciplinary agenda had to be deliberately (and institutionally) created. However, CRESC was not the only centre; rather, it was the most impactful one, which was supported by other centres, often in a symbiotic way. Two of these are noteworthy. First, the University of Massachusetts at Amherst (UMass) was another important centre. With Jim Crotty, Jerry Epstein and Bob Pollin, three leading (Marxist-informed) post-Keynesian scholars of finance were based there and encouraged and supported research on financialisation. Besides Epstein (2005), Stockhammer (2004), Orhangazi (2008) and Davis (2017) were based on dissertations written at UMass, and Krippner had first presented her 2005 paper at the conference that led to Epstein (2005). Research associated with UMass was more firmly on the economics side and was key in establishing debates on corporate financialisation. Second, several French researchers developed the notion of financialisation (Chesnais 1996). Boyer (2000) and Aglietta (2000), coming from French Regulation Theory, published their work in the Competition and Change special issue, based on previous work in French; Marxist contributions were collected in Dumenil and Levy (1997) and found their way via later English publication by Dumenil and Levy (e.g. 2001) into the Anglophone debate. They were informed, in particular, by David Harvey (2005)’s widely read Brief History of Neoliberalism, which contributed to the dissemination of the term financialisation.

Explosion and fragmentation: Maturation within academic disciplines or disintegration of a trans-disciplinary research program?

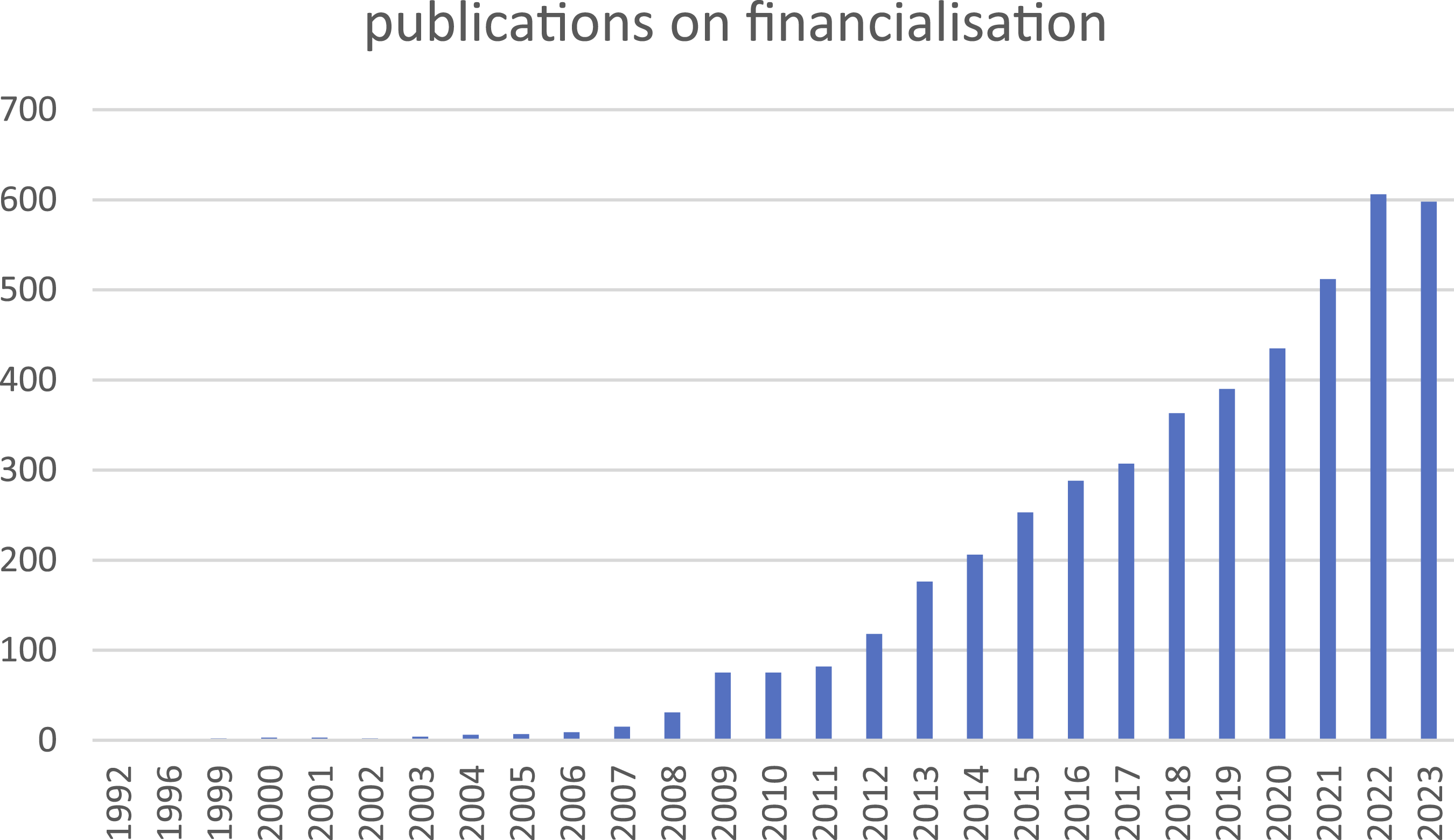

We date the explosion and fragmentation period from somewhere between 2008 and 2014. 2008 because financialisation research received a massive boost from the GFC, which stimulated interest in critical research on finance both by the general public (and policy makers) and by academics from various disciplines. By 2008, financialisation research was well positioned to meet this interest. 2014 (with van der Zwan’s survey) is the academic starting point. In this period, financialisation research takes off. While there were 31 journal publications on financialisation in 2008, in 2012 there were more than a hundred; since 2014 the number has exceeded 200 per year, and by 2021 more than 500 per year. It is hardly an exaggeration to call this an explosion. Figure 1 shows the number of articles, books and book chapters that have financialisation (or financialization) in the title, keywords or abstract. This is not only a growth in terms of the number of articles but also in terms of research topics and areas. This section will briefly comment on some developments in the subfields of the debate. A comprehensive review of each of these sub-debates is beyond the scope of this paper (or indeed of any one paper), but a brief if necessarily selective overview will help to illustrate the thematic growth of the debate. The following section will provide some bibliometric analysis. Publications on financialisation.

Beginning with those streams that began in the consolidation phase, the debate on corporate financialisation has grown. The field is relatively well established, and there are several reviews (Davis 2017; Klinge et al. 2021). Much of the debate is conducted with firm-level data and typically uses statistical methods. While early studies had focused on the USA (e.g. Orhangazi 2008), there is now work on a broader range of countries (Tori and Onaran 2018, 2022). This has confirmed some of the earlier findings, namely, the rise of financial assets by non-financial businesses, and that seems to come with a decline in physical investment. However, it also led to some qualifications, in particular the recognition that most of these financial assets are in low-yielding assets, which means that the switch from physical to financial accumulation is not due to the higher returns on financial assets (Fiebinger 2016; Rabinovich 2019). This is an area of debate that spans different disciplines and where communication across disciplines is functional, in part because of the shared quantitative methods (e.g. Akkemik and Ozen 2014; Soener 2015).

Since the GFC, there has been a rapid growth in heterodox economics research on financial instability and financial cycles, on shadow banking and securitisation and on central banking. However, much of that is done without explicit reference to financialisation. Rather, it seems that within economics, there are a handful of areas that refer to financialisation, whereas much of the research on finance does not. The macroeconomic modelling of financialisation began in the consolidation phase (Hein 2012; Onaran et al., 2011; Stockhammer 2005) and developed specialised literature that usually tries to synthesise different aspects of financialisation (shareholder value orientation, household financialisation, securitisation, sometimes financialisation of housing). This is strongly informed by post-Keynesian economics and often uses advanced modelling, including stock-flow consistent modelling or agent-based modelling (Caverzasi et al. 2019; Ricetti, Russo and Gallegatti 2016). It has informed the debate on growth models in comparative political economy (Baccaro et al. 2022), where heterodox economists as well as political economists are involved. However, this is something of an exception: much of the recent economics research on financialisation has limited transdisciplinary ambition.

The debate on the financialisation of households has also continued and expanded geographically. The focus of the literature shifts from investment and investors to borrowing and debtors, connecting with several longer-standing bodies of work, in particular in sociology. It shows a very different picture in that there is a stark divide between cultural political economists and quantitatively oriented economists. Bobek et al. (2023) offer a survey of the more cultural and constructivist side (see Zaloom and James 2023 for a survey in anthropology). This stands relatively unreconciled with the dynamic literature in economics, both on the heterodox and the mainstream side, on financial and housing wealth and household debt and their impact on economic growth and financial stability.

The relation of financialisation and income inequality has been a research topic from the beginning, initially with mostly descriptive methods, but since 2010 econometric literature (covering both economics and sociology) on the distributional impact of financialisation both in terms of the wage share and personal income distribution has developed (e.g. Dunhaupt 2017; Flaherty 2015; Huber et al. 2020; Kohler et al. 2019; Lin and Tomskovic-Devey 2013).

The financialisation of housing (or more generally, real estate) has become a distinct research field in urban studies and geography as well as in comparative political economy and, to a lesser extent, in economics. As will become clearer in the following section, urban studies and geography have proven a particularly fertile ground for financialisation studies (e.g. Aalbers 2016; Fernandez and Aalbers 2016). It has inspired work in comparative political economy (Fuller 2019; Kohl 2018; Schwartz and Seabrooke, 2009), but also features prominently in heterodox discussions of macroeconomic modelling (e.g. Caverzasi and Godin 2015), though much of it does not use the term.

Marxists have participated early on in the financialisation debates and Dumenil and Levy (2001) Harvey (2005) helped spread the notion of the rise of finance. Marxist debates have often operated within a value theoretic framing (e.g. Christophers and Fine, 2022), where the question whether finance is merely appropriating value produced by productive labour (Fine 2013) or whether there are new forms of financial appropriation (Lapavitsas 2009). Durand (2017) allows for dispossession and parasitism, but also innovative effects; Christophers (2018) emphasises monopoly profits. All of these share a focus on the origins of profits and thus on the corporate sector.

There had been an established field of the political economy of the international financial system, but many of the contributions only referred to financialisation after 2014. This happened in particular on debates on shadow banking and of central banking (e.g. Kessler and Wilhelm 2013; Walter and Wansleben 2020), but now much of the field of international political economy liberally uses the term (e.g. Beck 2022)

There is a growing stream of the literature on the financialisation of emerging and developing economies. This shows that insights from advanced economies do not necessarily carry over. Bonizzi (2013), in an early survey, emphasises that financialisation in emerging economies is often externally driven via capital flows. Bortz and Kaltenbrunner (2018) elaborate that in a monetary post-Keynesian framework of financial instability and currency hierarchy. Alami et al. (2023) synthesise dependency theory with elements of post-Keynesian finance and neo-Marxist treatment of global value chains, and emphasise the complementarity of real (production and trade) and financial subordination. Karwowski (2020) emphasises the variegation in the experiences of financialisation in the Global South. 4

A new development is the debate on the financialisation of commodities, which is mostly a debate within mainstream financial economics with hardly any relation to the financialisation debate (as discussed in the previous sections). It explores the question to what extent commodities (and thus commodity prices) have become a financial asset, the price of which depends on other financial assets. The contributions on this are highly technical analyses of the correlation of commodity prices with those of other financial assets. Contributions in this stream, for example, Tang and Xiong (2012) and Ferrer et al. (2018), do not refer at all to the financialisation debate (as discussed in sections 2 and 3). Only distantly related to this, there are a handful of papers that explore the commodity price dynamics from a genuine financialisation perspective (Ederer et al. 2016).

There is growing literature on the financialisation of food. Clapp and Isakson (2018) explore how different elements of food provisioning – from commodity trading and farmland tenure to risk management and food retailing – have been reconfigured for financial purposes. A central argument in her work is that financialization has created a new form of ‘distancing’ in the global food system by increasing the number and complexity of actors involved in agrifood commodity chains and by abstracting food from its physical form into highly complex agricultural commodity derivatives. Ouma (2020) investigates how farmland has been transformed into a financial asset class, particularly following the global financial crisis.

While commodity financialisation is one specific theme, it is indicative of a broader change: in the explosion phase of the financialisation debate, the term, which originally was synonymous with heterodox or critical approaches, is now also increasingly used by mainstream economists – but without any referencing of the financialisation literature. Within a mainstream economics framework, they take critical positions as regards the impact of financialisation on growth, inequality and financial instability; in other words, they formulate many of the insights of the financialisation debate. Prominent examples for this include particularly Jorda, Schularick and Taylor (2016) on financial cycles and Arcand et al. (2015) on evidence that ‘too much finance’ had negative growth effects, without using the term financialisation itself. However, the term is now also being used by the financial press (Wolf 2023).

To summarise, the explosion period of the financialisation debate saw a massive increase in academic research that refers to financialisation. The consolidation of the debate provided the basis for that, but the dynamism was due to the GFC and increased interest in finance. At the same time, the debate fragments. Instead of the three or four fields of debate that one could identify in the consolidation period, there is a proliferation of research fields now, across several different disciplines. While most of the financialisation debate is still clearly motivated by critical approaches, the concept is now also increasingly used by mainstream economics, without acknowledgement or referencing of the financialisation debate (heterodox economists will be familiar with this phenomenon). The academic success of the concept, so our hypothesis, comes with a price: a loss of the analytical core of the research program.

Bibliometric analysis

This section uses bibliographic data from Scopus to document changes in the debate on financialisation. Of particular interest is the question of which journals and disciplines financialisation is analysed in. The existing bibliometric literature on financialisation is thin. Engelen (2008), in a short section, identified Economy and Society (E&S), Review of International Political Economy (RIPE), Cambridge Journal of Economics (CJE) and Journal of Post Keynesian Economics (JPKE) as the leading journals of the financialisation debate; however, this is only partially consistent with Scopus data. Palludeto and Felipini (2019) offer a bibliometric analysis up to 2017. They report groupings based on co-referencing and co-citations and identify five clusters: on shareholder value orientation, macroeconomics, cultural aspects, geography and commodities and development (including food), the number of clusters being imposed by the researchers. They do not attempt to analyse changes over time. Short, the bibliometric study of the financialisation literature is an underexplored subject.

A number of conventions need to be clarified. First, the analysis is based on self-declaration, that is, whether authors use the term ‘financialisation’ in the title, abstract or keywords. Given that we argue that what debates use the term financialisation changes over time, this is a painful restriction. Second, ideally, we would like to trace changes over time, say, using annual data. However, this is not feasible as document as well as citation counts are extremely low to non-existent prior to 2000 (our first period), modest in our second period and high in our final period. Thus, we pragmatically split the period into up to 2014 and after 2014. This corresponds to our consolidation and explosion periods. Third, for consistency, the following analysis is based on journal articles published. 5

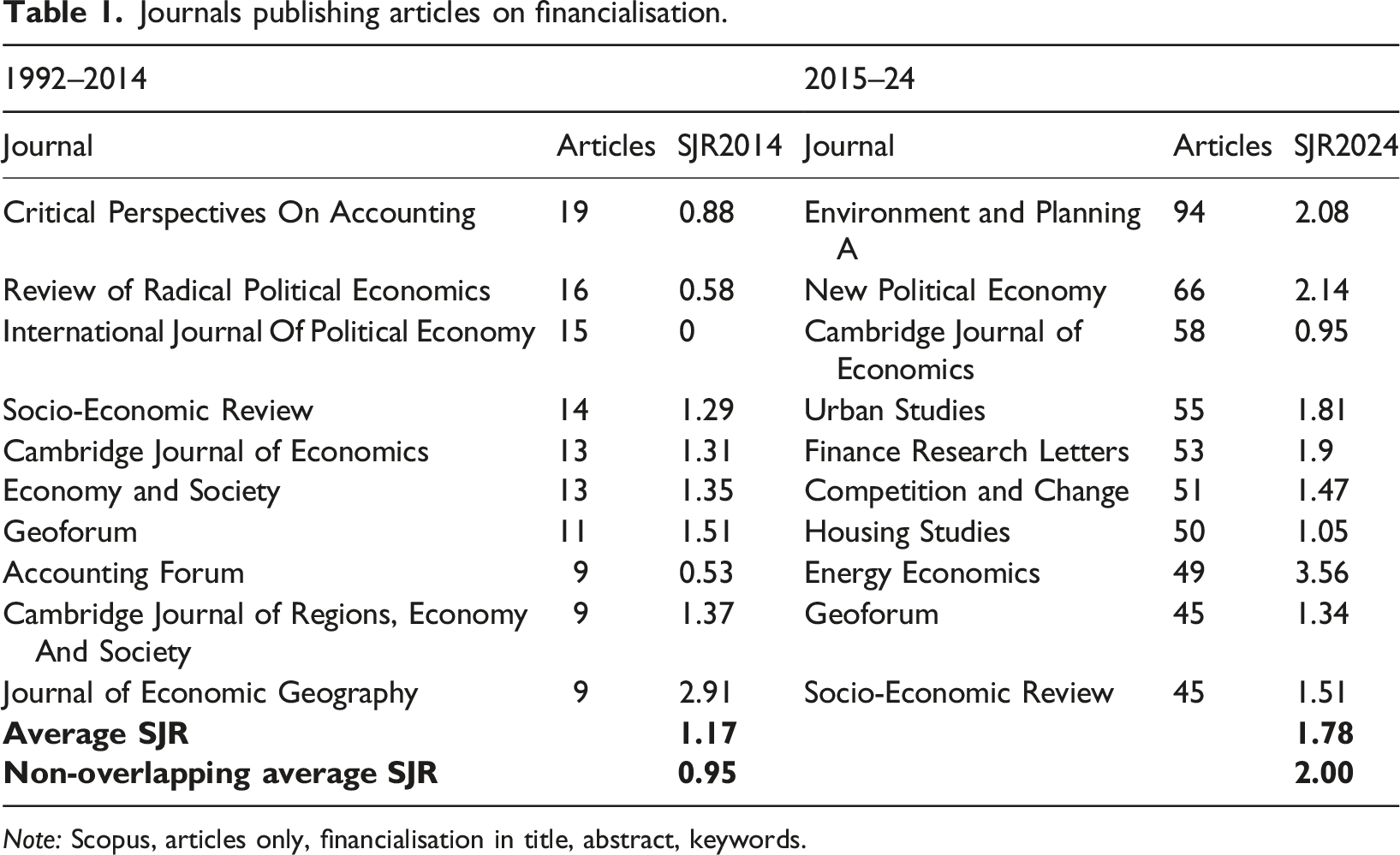

Journals publishing articles on financialisation.

Note: Scopus, articles only, financialisation in title, abstract, keywords.

To assess the prestige of the journals which publish financialisation articles, Table 1 reports the SJR (SCImago Journal Rank) index for each of the journals. The SJR is a recursively weighted citation index (Guerrero-Bote and Moja-Anegon 2012) and serves as an indicator of the reputation of a journal. The average SJR of the journals publishing articles on financialisation increased from 1.17 for the pre-2015 period to 1.78 for the 2014–25 period. The three journals (SER, CJE and Geoforum) that are listed for both periods experienced a decline in their (average) SJR. When we consider only the non-overlapping journals, the difference in (average) SJR values is even starker: 0.95 and 2.00, respectively, which is a very substantial difference. This illustrates that as the financialisation debate progresses, it has moved into more prestigious journals. I hypothesise that this move to more prestigious journals also corresponds to less transdisciplinarity. 8

Next, we look at the journals in which the most cited financialisation papers have been published. Table A1 in the Online Appendix presents a list of the journals that published the ten most cited articles on financialisation. For the first period, SER and CJE each have two of the most frequently cited articles, that is, there is some concentration of the debate; all other journals have only one. For the second period, there is no journal that published more than one of the ten most cited financialisation papers. In other words, the debate has spread out.

The financialisation of commodities papers feature highly in the citation counts. They are part of mainstream economics and investigate the co-movements of commodity prices with other financial indicators. They do not build on the core financialisation literature (see below).

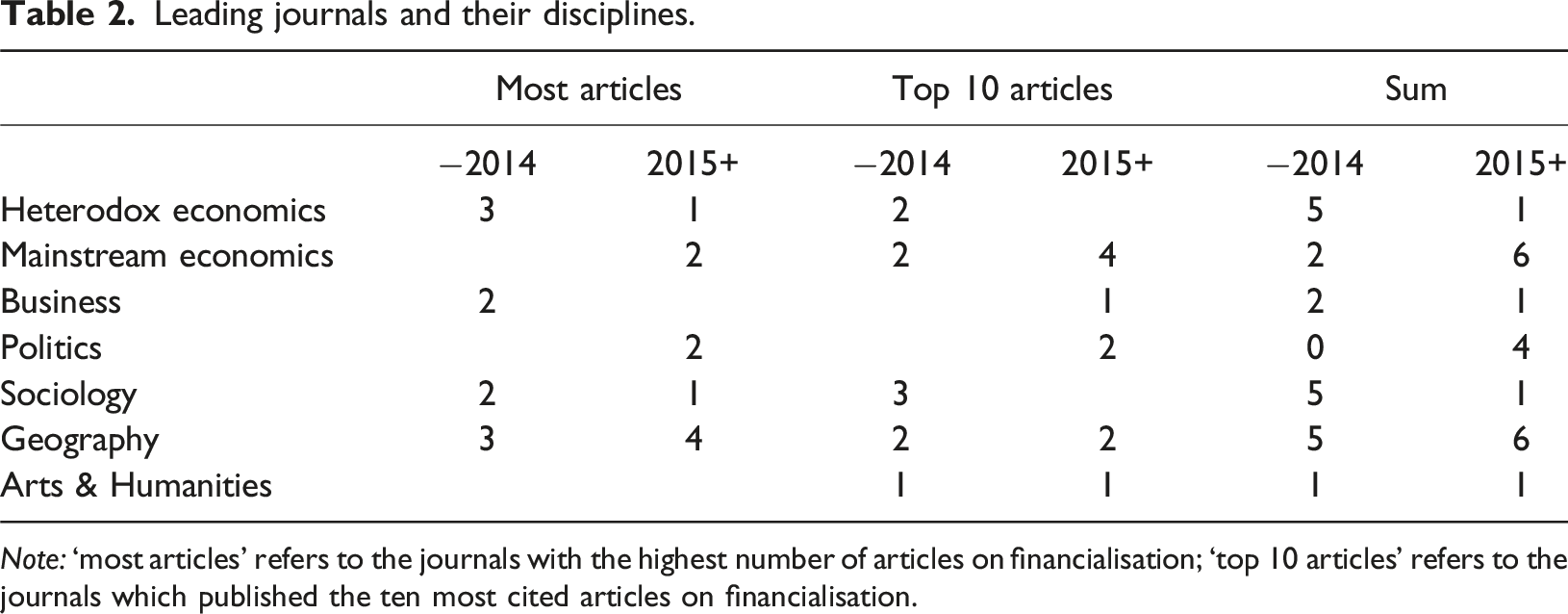

Leading journals and their disciplines.

Note: ‘most articles’ refers to the journals with the highest number of articles on financialisation; ‘top 10 articles’ refers to the journals which published the ten most cited articles on financialisation.

Finally, to assess the question of fragmentation and disintegration, we investigate the ten most cited papers on financialisation for the 2014–24 period to check whether and how much of the core financialisation literature they cite (Table A4 in the Online Appendix). We take as core financialisation literature the ten most cited papers from the pre-2014 period (excluding Tang and Xiong 2012) plus the papers in the Economy and Society and Competition and Change special issues. This definition of the core literature is admittedly somewhat arbitrary, but it is plausible enough to investigate the continuity in the debate. Among the ten most cited papers (for details see Table A3), seven do not have any reference to the core financialization literature. Among these are three commodity financialisation pieces. However, four papers in the social sciences and geography, that is, the majority, also do not cite a single one of the core references either, despite being closer to them in spirit. One paper (Birch 2017) cites one of the core references. Two (Christophers 2015; Fernandez and Aalbers 2016) cite several of the core; notably, these are authors who had already been involved in the debate in the previous decade.

The main findings of the bibliometric analysis are the following. First, there has been a meteoric increase in the articles on financialisation. Second, there has been a shift in the disciplinary composition of journals: a decline in heterodox economics journals, a rise in mainstream economics, a decline in sociology and rise in politics and a stable share of geography journals. Third, financialisation papers are now published in more prestigious journals than in the previous period. Fourth, post-2014 publications have decoupled from the debates of the previous period, with 70% of the ten most cited papers on financialisation not citing any of the previous core contributions. While this is partly due to mainstream economics using the term, it also holds for a majority of the papers from other fields. This is consistent with our argument that the debate has fragmented and lost its common core, while becoming more entrenched along disciplinary lines.

Interpreting the evolution of the financialisation debate

The overall development of the debate on financialisation can be given two quite different readings. The interpretation put forward in this paper tells a story of financialisation’s journey from the margins of academic discourse via a transdisciplinary research agenda to consolidation, and then to academic establishment and fragmentation along disciplinary lines. There have been two dialectics at work. First, a dialectic of growth based on transdisciplinarity, which establishes the critical mass for the debate. This enables financialisation analyses to move to more prestigious journals and establish the debate within existing academic disciplines, but also comes with a loss of (transdisciplinary) common ground, as recent research does not refer back to the original financialisation literature but identifies its contributions relative to the respective discipline. Academic careers are overwhelmingly made within academic disciplines and departments. Publishing in the leading journals of a field requires situating a contribution within that field. This plainly works against the original ambition of the financialization debate. A second dialectic is that between academic research and real-world developments. It was the global financial crisis that catapulted financialisation from a niche academic topic to a buzzword used in newspapers. The economic and social impact of the GFC and the prolonged stagnation afterwards were very real, and financialisation could address many of the questions this gave rise to because academic research had laid the analytical groundwork in the decade before. Something similar could have happened after the European Monetary System crisis, after the Asian Financial Crisis or the dot-com bubble, but it did not. Part of the reason will be the sheer severity of the crisis, but part of it is that by 2008 the financialisation debate was well placed to respond to the need for analysis by non-economists.

However, the main findings of this paper are also consistent with a different interpretation that regards the journey as one from transdisciplinary improvisation to disciplinary coherence(s). 10 The early research on financialization was driven by scholars who were at the margins of their own academic fields and disciplines. Transdisciplinarity thus was due to necessity, as within-discipline audiences were too small, rather than pro-active strategy. The fragmentation of the debate today is in part a result of the assertion of disciplinary norms – the integration of financialisation into normal science. Fragmentation and consolidation within academic disciplines and their respective norms are two sides of the same coin.

To some extent, the two interpretations are mirror images of each other that need not be in conflict even if they emphasise different aspects. After all, academic disciplines are a fact of modern academia, and it would be surprising if the financialisation debate had succeeded in overcoming disciplinary boundaries in a sustained fashion. It would have to create its own subfield of ‘financialisation studies’.

The question is what the costs of fragmentation along disciplinary lines and the loss of a transdisciplinary agenda are. Financialisation has economic as well as social and political effects. Separating these along academic disciplines undermines a holistic understanding of the phenomenon. If financialisation research is considered a political economy of finance, then it needs to encompass social and economic components. Moreover, there is a need to synthesise actor-level analysis with an investigation of how these behaviours articulate themselves at the system level, which imposes constraints or shapes options and opportunities for actors. There are two main issues. First, in practice, different disciplines use different standards of proof and methods. The biggest gap here is between economics, which routinely uses quantitative methods. Disciplinary coherence means a lack of consideration of insights based on methods not widely used in a discipline. In other words, there is a need for triangulation of findings across disciplines. Second, and closely related, is the need to synthesise the insights from different levels of analysis. In particular, the question of how actor-level changes, for example, in behaviours and goals, translate into macro outcomes. The separation of parts of the debate from heterodox macroeconomics means that the systemic economic effects cannot be satisfactorily analysed.

Conclusion

This paper has argued that the financialisation debate began as a transdisciplinary research project that drew on heterodox economics and cultural political economy: an attempt to create a critical conversation across academic disciplines about the social and economic impact of finance. This was due to the efforts of the team of CRESC by organising workshops and special issues. This transdisciplinary agenda provided the basis for the financialisation debate and received a boost with the GFC. It generated the critical mass for financialisation to take off as a subject of academic research and gain recognition within disciplines. With its success, however, also came fragmentation along academic disciplines and an erosion of the transdisciplinary project.

These trends clearly show in bibliometric analysis: financialisation research is now published in more prestigious journals, and there has been a decoupling of post-2014 research from the earlier financialisation debate. Only a part of this is due to the rise of mainstream economics research on financialisation (which does not relate to the core financialisation literature). It also holds for the majority of the most cited papers in the social sciences and geography. In particular, the separation of heterodox economics and social sciences (in the financialisation debate) is growing. Short, there has been a fragmentation of the debate and a disciplinary specialisation. One can conceive of this as a loss of the original transdisciplinary research ambition, but equally, one could argue that this is a normal sign of a maturing field, that is, an unavoidable price for success.

This paper has several implications for future research. First, it highlights the potential for further bibliometric analysis to enable an understanding of the development of the debate. Second, analyses of a field, say household financialisation, in different disciplines could shed light on how much the fragmentation of the debate has led to inconsistencies. Third, this paper has focused on the English-speaking debate. Thus, a more systematic analysis of French or Spanish debates would enrich our understanding.

However, the main implication for future research is more basic: one might think that financialisation, by its very subject nature, invites transdisciplinary approaches. It shapes the behaviour, objectives and aims of households and businesses, but it also impacts economic growth, income distribution and generates financial crises. A holistic analysis of financialisation thus clearly requires a multidisciplinary approach. However, given the incentives of contemporary academia, the transdisciplinary character of much of financialisation analyses cannot be taken for granted. Rather, transdisciplinarity emerged because scholars around CRESC propagated this research agenda and created an institutional platform via conferences and special issues for conversations that transcended academic fields. If the project of critical transdisciplinary debate on financialisation is to be continued, this will require purposeful efforts as it has to counteract the forces of disciplinary specialisation.

Supplemental material

Supplemental material - The financialisation debate: From transdisciplinary research program to disciplinary recognition and fragmentation

Supplemental material for The financialisation debate: From transdisciplinary research program to disciplinary recognition and fragmentation by Engelbert Stockhammer in Competition & Change

Footnotes

Acknowledgements

Earlier versions of this paper have been presented at EAEPE and FMM conferences and the RG IPE meetings at King’s College London. The author has benefited from discussions there and from comments by Jerry Epstein, Jakob Kapeller, Ewa Karwowski, Daniel Mertens, Joel Rabinovich, Karel Williams and three anonymous referees. The usual disclaimers apply.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Supplemental material

Supplemental material for this article is available online.