Abstract

Off-balance-sheet policies are an important but understudied phenomenon that emerged from a technical subtlety in the calculation of public debt statistics. Taking the case of an exemplary European off-balance-sheet policy, public–private partnerships (PPPs), this paper analyzes the technocratic processes that allow the emergence of such debt-neutral instruments. In the aftermath of the sovereign debt crisis, off-balance-sheet policies have become an important policy tool for Member States in the European Economic and Monetary Union, enabling them to strike a balance between the perceived ‘public investment gap’ and the mantra of fiscal consolidation. The case study shows how the lack of political solutions to Europe’s investment-consolidation conundrum leaves it to technical experts to find workable solutions within the existing rules. The off-balance-sheet status of PPPs came under threat in 2014 but was reaffirmed through a coordinated effort by two strange bedfellows: the European Investment Bank (EIB), a promoter of PPPs, and Eurostat, the European authority responsible for public debt and deficit indicators. I argue that Eurostat and the EIB have entered into strategic cooperation to increase each other’s room for manoeuvre, diffuse political pressure and avoid bureaucratic overload. This paper contributes to a better understanding of the role of technocrats and their expertise, which shape the mutual relations between fiscal constraints and financialized investment policies in the European investor states.

Introduction

How can policymakers boost long-term investment while pursuing fiscal consolidation? After the sovereign debt crisis, EU Member States grappled with an investment-consolidation conundrum as fiscal surveillance was tightened, but calls for public investments intensified. The city of Liège thought it had found a way to square the circle when it tendered a public–private partnership (PPP) for a new tram in 2013. Inspired by the London Underground PPP, the City Council wanted to design an ‘off-balance-sheet project’ that engaged a private company and reduced the negative repercussions for the public accounts. However, when the PPP contract was about to be signed, the Belgian National Statistical Institute had doubts about its off-balance-sheet treatment and consulted Eurostat, the European authority responsible for the calculation of public debt and deficit indicators (Eurostat, 2016e). After three rounds of consultation, Eurostat decided that the PPP should be recorded ‘on balance sheet’, which ultimately led Liege officials provisionally to abandon the project (Bechet, 2016).

Only a year later, a novel ‘Guide to the Statistical Treatment of PPPs’ (hereafter ‘the PPP Guide’) gave fresh impetus to the off-balance-sheet use of PPPs and the Liège City Council could finally sign a PPP contract with a consortium led by the French train-maker Alstom, which included 200 million euro financing from the European Investment Bank (EIB) earmarked via the ‘Investment Plan for Europe’ (hereafter ‘Juncker Plan’) (European Investment Bank, 2019). The Tram de Liège is an example of a new configuration of European economic governance, the European Investor State, in which public actors attract private investors and leverage public funds to stimulate economic growth without incurring new debt (Lepont & Thiemann, 2024). Moreover, the bumpy road to the Tram’s realization highlights two important but understudied features of the European Investor State: the role of off-balance-sheet policies and the technical expertise required to define them as such.

First, off-balance-sheet policies have become a publicly accepted solution to the investment-consolidation conundrum plaguing the EU since the sovereign debt crisis (Streeck 2014; Lepont & Thiemann, 2024, this issue). To support economic growth while consolidating public finances, the Commission chose the EIB as the Juncker Plan’s implementing partner, with extensive experience in public–private projects (Liebe and Howarth, 2020). Through financial instruments such as PPPs, private companies finance, build and manage core government functions, such as the provision of public infrastructure or services, while delaying or offsetting their impact on public finances, thus exploiting flexibility in fiscal rules (Gabor 2023; Streeck 2014). 1 While the proliferation of European PPPs peaked in 2007 (Bain, 2009; Cepparulo et al., 2023), it was only after the sovereign debt crisis that the Commission began to promote PPPs and other instruments to explore this flexibility within fiscal rules (European Commission, 2009, 2015; Schmidt, 2020).

Second, the central role of the PPP Guide in the Tram de Liège saga highlights the crucial involvement of technical experts in designing policies to be recorded off-balance-sheet (Savage, 2005). Specifically, statisticians hold the key role in determining whether PPPs can be deferred or offset in government accounts, as their off-balance-sheet status is determined by statistical rules within a limited circle of experts (Piron, 2020). This underscores the essential role of technical expertise in shaping and implementing policies related to off-balance-sheet accounting. Puzzlingly, the Guide was co-produced by two strange bedfellows: Eurostat and the EIB’s advisory hub for PPPs, the European PPP Expertise Centre (EPEC). 2 This leads me to my research question of why would statisticians, who prioritize the independent calculation of debts and deficits and interact only within their tightly knit expert community, ally themselves with an ardent supporter and financier of PPPs like the EIB?

Scholars who argue that European governance has taken an intergovernmental turn since the sovereign debt crisis would predict that Member States will put pressure on Luxembourg technocrats to find new avenues for off-balance-sheet public investment (Bickerton et al., 2015). But the analysis of the political process leading to the adoption of the PPP Guide shows that European technocrats, empowered by the reliance on their expertise, are carefully navigating these new hybrid institutional arrangements, using the room for manoeuvre they create to expand their toolbox and diffuse political pressure. Combining insights from theories of policy instrumentation, expertise in policymaking and the concept of usage, the paper argues that the complex and politically charged European multi-level governance system leads to the emergence of heterogeneous expert coalitions (Woll and Jacquot 2010), which shape the instrumentation of statistical decision-making processes (Lascoumes and Le Galès, 2007) and empower technocrats to navigate politically charged policies (Cross, 2013b; Dunlop and Radaelli, 2016).

Based on seven expert interviews, several background discussions and in-depth documentary analysis, complemented by primary and secondary literature, the empirical section traces the statistical classification of PPPs over the last 20 years. The reconstruction of the rules governing off-balance-sheet PPPs shows how the increasing drive for economic growth after the sovereign debt crisis puts a new emphasis on technical expertise and led to an unusual cooperation between Eurostat and the EIB’s EPEC, best explained by their mutually complementary expertise. Eurostat benefits from EPEC’s expertise in order to strengthen its authority over the statistical interpretation of Maastricht indicators by adding the perspective of practitioners. The EIB sees the cooperation with Eurostat as part of its toolbox to support a vibrant PPP market, aiming to become ‘a knowledge bank for PPP task forces’ (European Investment Bank 2010, 11), and its PPP advisory hub EPEC is the ideal technical body to cooperate with Eurostat without attaining to political pressure.

Scholars to date have highlighted the importance of institutions that design and finance off-balance-sheet instruments to work around fiscal constraints (Guter-Sandu and Murau, 2022; Mertens et al., 2021). Yet, we know relatively little about the actors and rules that make off-balance-sheet policies actually possible by enabling the design of policies that fall outside Europe’s sophisticated fiscal surveillance regime (but see de Vlieger and Tesche, 2021). Focusing on off-balance-sheet PPPs this paper shines a light on the strengthening of non-elected experts, such Zampino as Eurostat and other national government finance statisticians and development banks, in this evolving dynamic of new statecraft (Quinn, 2017).

By analysing the micro-processes and actors behind the design of off-balance-sheet instruments, this paper contributes, first, to the growing literature on changing statecraft after the crisis (Gabor, 2023; Prontera, 2018), highlighting the importance of off-balance-sheet policies in the EU, which have so far been understudied (but see Guter-Sandu and Murau, 2022) because scholars focus mainly on official accounts, such as the budgets or public debt indicators. Second, the detailed analysis of the strategic usage of statistical decision-making underlines the importance of technical experts for Europe’s fiscal governance and especially the public debt calculations in the European multi-level governance system (Sánchez-Cuenca, 2017; Tortola and Tarlea, 2021). Finally, the back and forth between PPPs and fiscal constraints shed light on the performative effect of (macroeconomic) indicators, as PPPs and the statistical rules evolve co-dependently (Desrosières, 2015).

The rest of the paper is organized as follows. The next section embeds the rise of off-balance-sheet policies in the broader changes in European public finances since the 1980s. The third section clarifies the technical underpinnings of off-balance-sheet policies and reviews the most recent policies in Europe. The fourth section outlines a framework to analyse statistics as instruments reflecting the power struggles among experts for their definition and introduces the concept of strategic usage of European debt and deficit calculations. The fifth section presents the empirical case of PPPs and shows that, while the off-balance-sheet status of PPPs is rooted in European government finance statistics since the early 2000s, only the strategic partnership between Eurostat and the EIB allowed PPPs to maintain their off-balance-sheet status after the sovereign debt crisis. In the conclusion, these findings are embedded in the current efforts to reform the European fiscal surveillance system and the broader developments of the EIS.

From European consolidation to investor state – The rise of off-balance-sheet policies

The rise of off-balance-sheet policies, and PPPs in particular, has occurred in the context of broader changes in public finances that have their roots in the 1980s, when governments faced increasing fiscal constraints (Brixi and Schick, 2002; Polackova, 1998). In this period, states began to cover expenditures increasingly ‘through borrowing rather than taxation’ (Streeck 2014, 72). Despite, or perhaps because of, these adjustments, rising debt levels led authorities to prioritize fiscal consolidation over other policy objectives, turning debtor states into consolidator states (Streeck, 2014). States became increasingly dependent on financial markets to ensure the marketability of their sovereign debt (Preunkert, 2017; Rommerskirchen, 2020). Moreover, financial logics were gradually incorporated in public services, transforming them into tradable assets, converting pension funds into funded schemes and inspiring the privatization of social or physical infrastructures (Karwowski and Centurion-Vicencio, 2018; Wang, 2020).

After the 2008–2012 debt crisis and amid a pronounced economic contraction, the mantra of fiscal consolidation was soon accompanied by the contradictory quest for economic growth and the consolidation states evolved into the European Investor State (Lepont & Thiemann, this issue). Caught in political impasse over fiscal rules, the European Commission continued to explore more ‘workable’ solutions to support public investment (Schmidt, 2020). Meanwhile, governments incorporated ‘new types of advanced financing’ for public infrastructures (Streeck 2014, 122–123) by ‘de-risking’ (Gabor, 2023) and assetizing public investments (Chiapello, 2017). In light of these new techniques, European statecraft evolved from ‘rowing’ the economy in a post-Keynesian world, towards ‘steering’ the economy by enrolling private actors and vehicles of off-balance-sheet policymaking (Bulfone, 2022). These efforts were streamlined in the Juncker Plan, which aimed to actively promote growth while leveraging European funds with private capital (European Investment Bank 2020). To this end, the Commission relied on European and national development banks, often convenient off-balance-sheet economic policy vehicles (Bulfone and Di Carlo, 2021; Mertens and Thiemann, 2019). As implementation partners development banks can draw on years of experience. For instance, the EIB has been promoting PPPs since the 1980s (Liebe and Howarth, 2020).

Scholars have extensively discussed the changes in European statecraft and the emergence of new forms of economic policy-making. However, one aspect of contemporary European economic policy that has been overlooked is the growing use of off-balance-sheet instruments. This is noteworthy, considering that discussions about their fiscal risks date back to the 1990s (Brixi and Schick, 2002; Polackova, 1998). In Europe, governments have used off-balance-sheet policies to comply with debt limits (Budina et al., 2007; Easterly, 1999) or as a backstop for fiscally constrained member states (Guter-Sandu and Murau, 2022). The social sciences’ neglect of the diffusion of off-balance-sheet policymaking might be explained by scholars’ focus on the ‘hard, naked facts’ of such traditional institutions as the budget or macroeconomic indicators (Schumpeter, 2012, p. 23), the very same indicators from which off-balance-sheet policies such as PPPs can be excluded by design. To analyse how this design has been fundamentally shaped by the rules and experts calculating public debt, the next section focuses on the technical aspects of recent off-balance-sheet policies in Europe.

A technical fix for a political problem – The redistributive and the marketable state

Off-balance-sheet policies emerge because Maastricht debt and deficit indicators are based on the general government sector, which includes only ‘redistributive’ policies that are financed by national income, while it excludes ‘marketable’ policies, which are profitable and thus considered part of the broader public sector (Irwin, 2015).

3

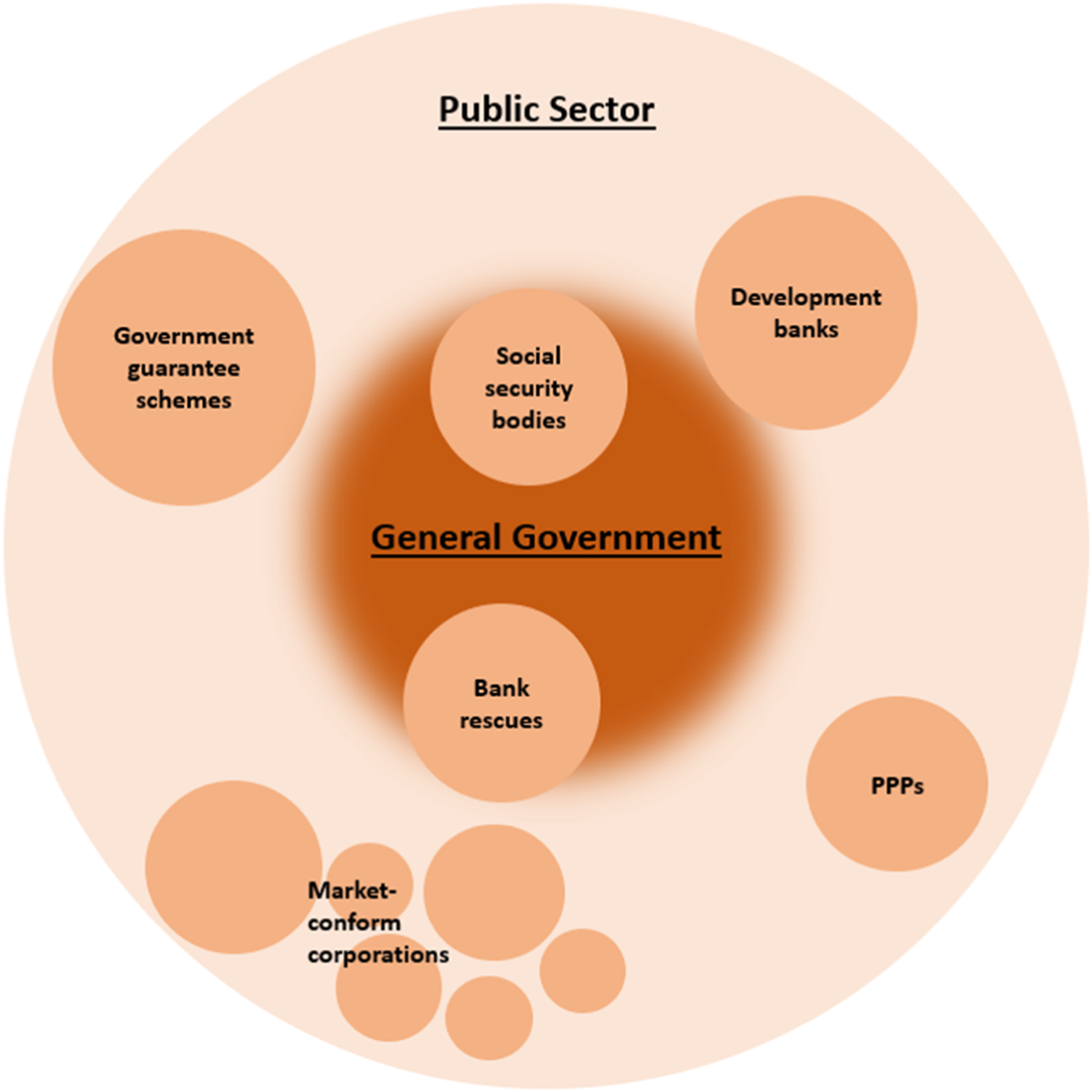

The distinction is not always straightforward as there are boundary institutions in which the state acts like a private investor prioritizing profitability but also including a redistributive logic. Figure 1 includes examples of borderline institutions that are categorized in some Member States inside and in others outside the general government sector. Borderline institutions of the general government sector (author’s elaboration).

To ensure the equal treatment of all Member States, Eurostat constantly fine-tunes the distinction between the ‘marketable’ and the ‘redistributive’ state by clarifying the statistical treatment of new borderline policies. For example, after the financial crisis governments suddenly incurred large liabilities as a result of banking bailouts and other financial interventions, and some governments tried to design their interventions off balance sheet (Gandrud and Hallerberg, 2016). More recently, the Italian and Greek governments set up securitization schemes for banks to off-load their bad assets without impacting government finances (Emmott and Georgiopoulos, 2019). In the meanwhile, development banks have become important industrial policy vehicles to distribute European financial instruments and support public investment debt neutrally (Bulfone and Di Carlo, 2021; Mertens et al., 2021).

The importance of off-balance-sheet policies has been further underlined in the aftermath of the COVID-19 crisis, when Member States and European authorities designed substantial parts of their policy measures off balance sheet, ‘in the form of direct state guaranteed loans, which are not reflected in the official debt statistics’ (Rodríguez-Vives and Giron, 2021). These guarantees amounted to 14% of GDP and thus far exceeded previous guarantee packages (Gardó et al., 2021). All of these off-balance-sheet policies are very distinct instruments, but they share the key feature that they expose the state to a financial logic which considerably increases the fiscal risks outside the democratic control of public finances (Bova et al., 2016). 4

Though PPPs might still appear small compared with these figures, they are analytically important as the archetypal case of a financial fix for chronic underinvestment. Crucially, off-balance-sheet PPPs are a truly European fix as EU statistical rules differ from international standards (Heald and Georgiou, 2011). It is in this sense that PPPs represent a further iteration of the underlying logic of the European Investor State, based on the idea of making public investment conditional on future returns, while blending public and private sources within the specific European governance framework (see Lepont & Thiemann, this issue). To understand how statistical rules for off-balance-sheet policies have evolved in Europe, we need to focus on the actors that have the authority and expertise to define them.

Empowering expertise in Europe’s multi-level fiscal governance

Statistical figures are policy instruments ‘marked by the play of power relations’ (Scott, 1998, p. 58). Therefore, an analysis of the specific rules that shape macroeconomic indicators must pay attention to the actors that shape the indicator biases and their struggles (Mügge, 2020). Historically, statisticians have often been subject to ‘manipulations or pressures by politicians to conceal or “massage” a particular statistic’ (Desrosières, 2013, p. 12). In response to these pressures, the statistical profession has tried to ensure its independence by focusing solely on holding up a mirror to economic reality (Morgenstern, 1977). Central to this independence is specific knowledge of the effects of statistics as political instruments (Lascoumes and Le Galès, 2007). This knowledge becomes authoritative when statisticians can agree on a methodology that allows them to act as ‘teachers to decision-makers’ (Dunlop, 2017, p. 215). This feature is particularly important for the politically pertinent European debt and deficit indicators which are the bases for economic sanctions and for the interference of the European Commission into national budgets (De Vlieger and Tesche, 2021).

European statisticians widely shield their work from political and legislative procedures by formulating solutions backed by an expert consensus (Savage, 2005; Schelkle, 2009). To defend their autonomy, statisticians abstain from passing rules that contradict existing ones, preferring to change their interpretations at most incrementally (De Vlieger and Tesche, 2021). The path-dependency of statistical rules works as a protective shield, defending statisticians’ prerogative over the statistical categorization of policies against the undesired influence of central bankers, economists and elected officials (Savage and Howarth, 2018). This then also empowers national statisticians in their decision-making processes because they can refer to rules that are ‘based on a well-reasoned consensus among those in the best position to know’ (Cross, 2013a, p. 147). However, European statisticians are restricted to a specific statistical nomenclature that passes the legislative procedure wherefore they can only work according to ‘established rules and procedures in the light of the evolving consensus among peers’ (Mabbett and Schelkle, 2016, p. 18).

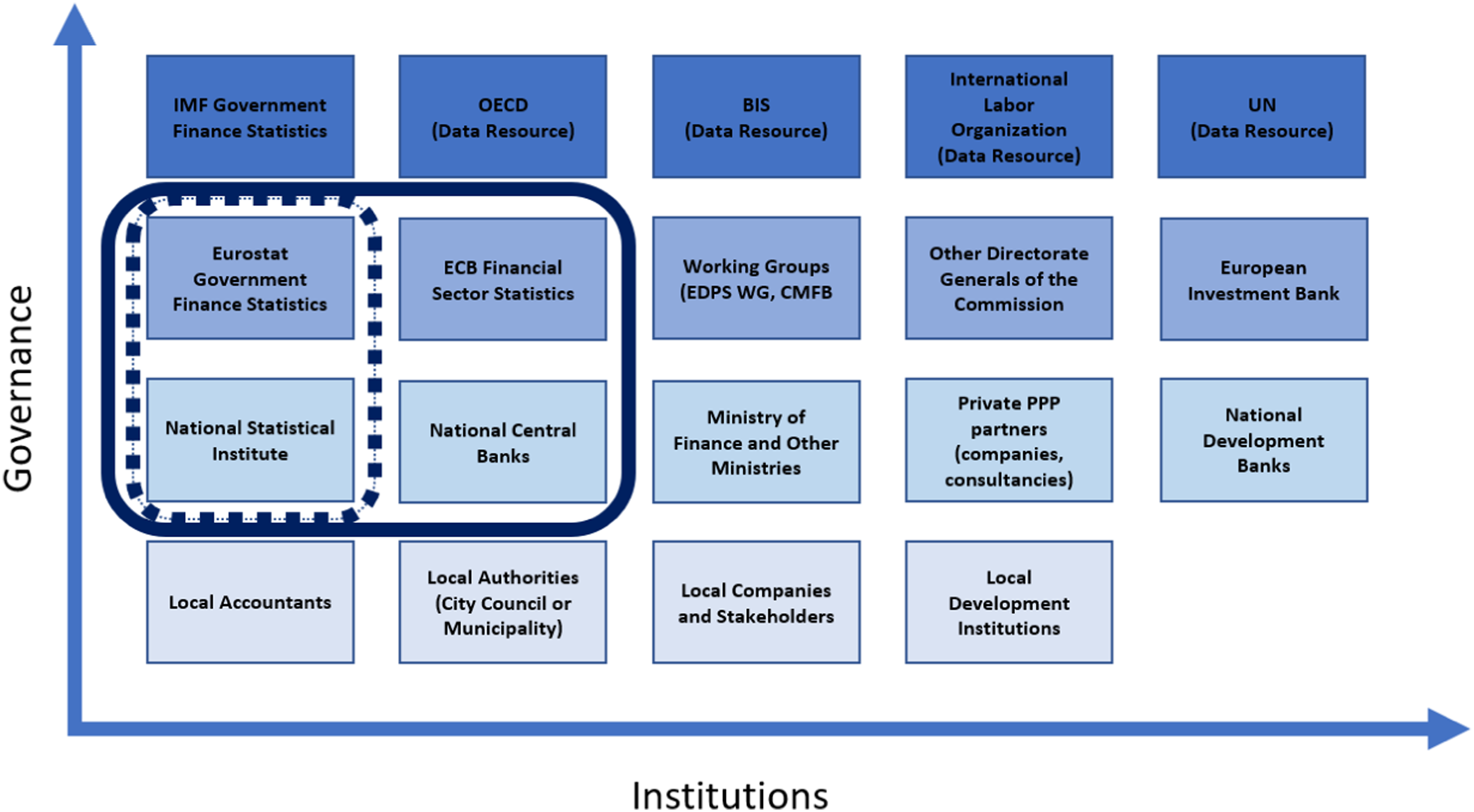

It is within this consensus that statisticians can try to 'use’ European governance. That is, statisticians might want to strategically steer the decision-making process in pursuit of a particular goal (Woll and Jacquot, 2010). In Europe, debt and deficit indicators are calculated by a handful of specialized national and European statisticians that, like many European technocrats, operate in ‘an increasingly complex web of interdependence’, which extends horizontally and vertically (Bache et al., 2016, p. 486). National statisticians collect and translate data, while Eurostat certifies or flags the submitted data (Savage and Howarth, 2018). Together, national statisticians and Eurostat have exclusive competence and authority over statistics and over the adaptation of existing rules to boundary institutions (small circle), while central banks and ministries of finance provide data and act as advisors (big circle), as Figure 2 exemplifies. Multi-level governance of the data collection and statistical classification of Maastricht debt and deficit for PPPs (author’s elaboration).

The various actors involved in this rule-making and adaptation process can form all kinds of coalitions that combine their interests and steer the discussions in a certain direction, helping them to increase their ‘access to the policy process or the number of political tools available’ (Woll and Jacquot, 2010, p. 116). The following analysis of the statistical rules for PPPs will show how national statisticians have strategically pursued a clarification of the PPP rules against the background of their limited capacity to analyse PPP contracts and increasing political demands for off-balance-sheet PPPs. Eurostat, in turn, forged a coalition with the EPEC not only to overcome its limited bureaucratic resources in its efforts to understand the PPP market but also to strengthen its legitimacy by adding a practitioner’s perspective while diffusing political pressure.

Public–private partnerships: once off balance sheet, always off balance sheet?

PPPs are popular off-balance-sheet instruments pioneered by the United Kingdom and Australia in the 1990s (Findeisen, 2022; Whiteside, 2020). In the wake of the financial crisis, European national governments and the European Commission agreed that PPPs are needed ‘to accelerate investments in response to the crisis, whilst needing to preserve budgetary discipline’ (European Commission, 2009, p. 2). The promotion of PPPs occurred despite the fact that some observers criticized PPPs as tools ‘to conceal public borrowing, while providing long-term state guarantees for profits to private companies’ (Hall, 2015, pp. 3–4). Comparative country analysis found a link between ‘high levels of government debt and governmental support for PPPs’ (Cepparulo et al., 2019; Verhoest et al., 2015, p. 134). Similar arguments have been made for the local level in Germany (Wigger and Zimmermann, 2020), Italy (Antellini Russo and Zampino, 2010, p. 21) and France (Buso et al., 2017, p. 21).

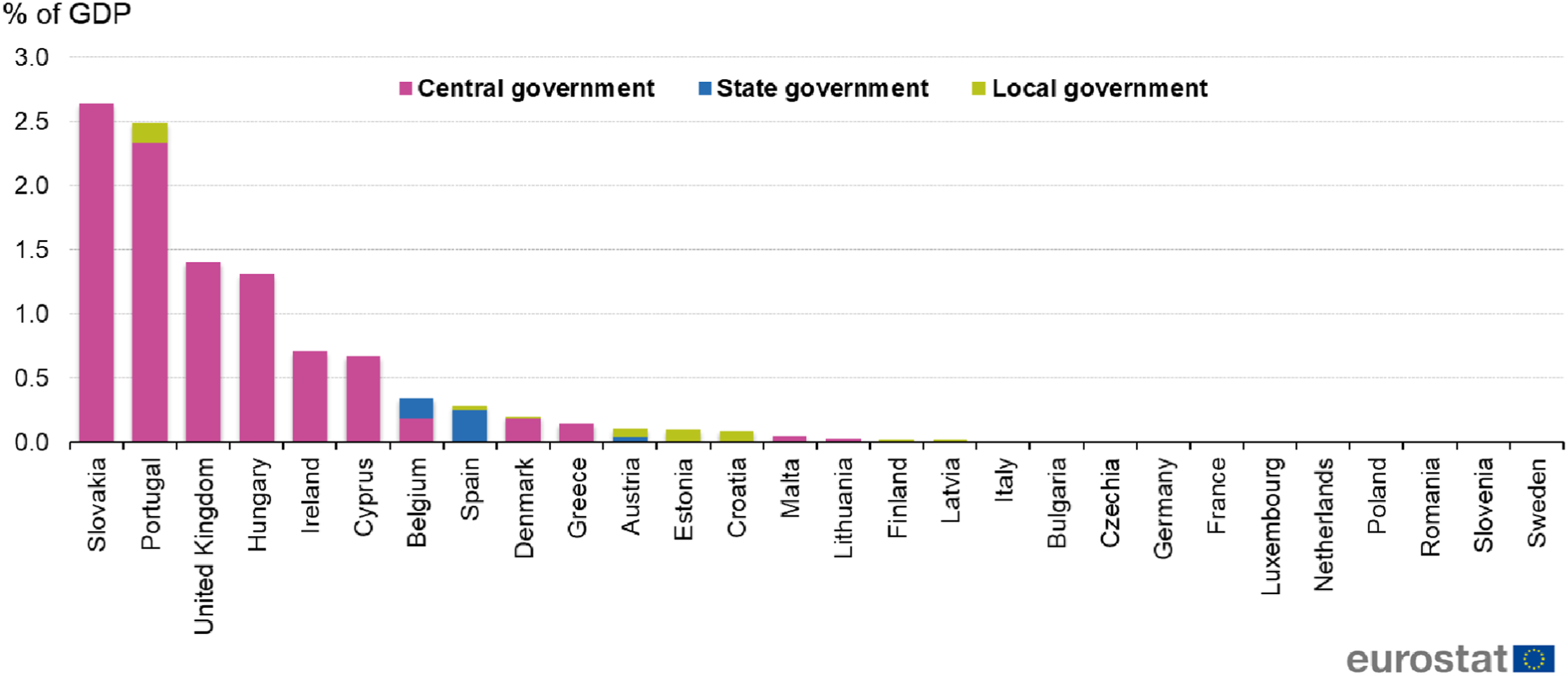

Figure 3 shows that the classification of PPPs varies across Europe. PPPs are reported on balance sheet in France and Germany, mainly off balance sheet in Belgium and partially off balance sheet in Spain (see Piron in this issue). European statistical rules have allowed for the design of off-balance-sheet PPPs since the early 2000s (Piron, 2020), thus creating an international precedent (Heald and Georgiou, 2011, p. 240). The EIB has been among the most active promoters of PPPs, and after the Eurozone crisis presented PPPs as a way of strengthening the European market (Liebe and Howarth, 2020). However, in 2013 the periodical change of the statistical nomenclature (ESA10) in coordination with the renewal of the international statistical rulebook called into question this renewed interest in Maastricht-neutral PPPs, almost jeopardizing their diffusion (Sousa 2020, Interview 3). European off-balance-sheet PPP liabilities as a percentage of GDP in 2018 (source: Eurostat).

Under considerable pressure from various stakeholders, including governments, European Commission officials, national statisticians and development institutions (Kelly 2016, Interviews 4 and 6), Eurostat and the EIB forged a strategic alliance and translated the rules into a guide for practitioners. The subsequent empirical analysis shows that Eurostat made effective use of the collaboration with EPEC to define streamlined bureaucratic processes while EPEC could strengthen its position as Europe’s PPP expert centre.

Laying the path for a European exception – The first statistical rules for PPPs

To understand the conflicts behind the off-balance-sheet treatment of PPPs in 2014 one needs to trace them back to their roots, in line with the path-dependence of statistical rules (Barta and Schelkle, 2015). In Europe, the first clarification of the statistical treatment of PPPs was issued by Eurostat in 2004. The statistical nomenclature applied back then, the ESA95, did not touch upon PPPs. This became a problem when in 2003 the European Commission announced the European Growth Initiative and promoted the use of PPPs to catalyse investment for growth-related infrastructure. Having been assigned an explicit mandate to promote the development of Trans-European Networks in transport, energy and telecommunications, the EIB quickly emerged as one of the main advocates of the diffusion of PPPs (Liebe and Howarth, 2020, p. 202). Staffed with UK-trained PPP experts, the EIB actively promoted the use of PPPs and their budget-neutral accounting (Liebe and Howarth, 2020; Piron, 2020).

In the early 2000s, the United Kingdom already had a vibrant PPP market. To promote this dynamic, the British Office for National Statistics had designed off-balance-sheet PPPs following the ‘risk and reward’ approach (Heald and Georgiou, 2011). In the absence of an international consensus on the statistical treatment of PPPs, European statisticians found this approach convincing and put it at the heart of the 2004 Guidance Note, which was adopted with a 26 to 1 majority (Eurostat, 2004; Savage, 2005, p. 175). The Guidance Note was written in Eurostat’s spirit of technical neutrality and refrained from making any political assessment, clarifying that it ‘does not examine the motives, rationale and efficiency of these partnerships’ (Eurostat, 2004, p. 1). Nevertheless, the Guidance Note continues to be influential as it paved the way for the design of off-balance-sheet PPPs in Europe (Interview 7). In 2004, the IMF remarked in this regard that Eurostat’s rules ‘could open the door to PPPs that are intended mainly to circumvent the [Stability and Growth Pact]’ (IMF quoted in Heald and Georgiou 2011, 241).

Eurostat’s initial treatment of PPPs was criticized as vague because it was formalistic and focused on risk distribution between public and private partners (Braekeleer and Braekeleer, 2014, p. 43; Mühlenkamp, 2014, p. 27). Even though the Guidance Note was based on the principle of ‘risk and reward’, as in other jurisdictions, assessment relied mainly on risk distribution. 5 There were several problems both with the ‘risk and reward’ approach in general and with Eurostat’s take on it in particular. Developed in business accounting for operating leases, the approach was soon found to allow malpractice because ‘financial commitments and risks are not indicated therein and misleading information about the assets and leverage of lessees is given’ (Mühlenkamp, 2014, p. 26). Looking back, a PPP specialist with decades of experience stated that, by allowing European PPPs to blossom in the early 2000s, the Guidance Note paved the way for the emergence of disputes around the off-balance-sheet treatment of PPPs which unfolded in 2014 (Interview 7). Indeed, a review of 15 PPP projects financed by the EIB in 2005 shows that all but one met Eurostat’s off-balance-sheet conditions (European Investment Bank, 2005, p. 10).

In the decade following the publication of the Guidance Note, international statisticians found that especially ‘under Eurostat’s criteria many government-funded PPP assets and related liabilities are recorded off government’s balance sheet’ (Budina et al., 2007; Funke et al., 2013, p. 15). Statisticians and accountants alike became aware that several projects were actually recorded ‘off-off’, meaning that neither the private nor the public partners recorded the assets (Kellaway, 2008). To fill the loophole, international accounting standards moved away from the ‘risk and reward’ approach, focusing instead on whether the public partner attempts to exert ‘control’ over the project. However, European statisticians stuck with their initial assessment, beginning to specify PPP rules only after 2010 (Piron, 2020, p. 81). This created a growing divergence between Eurostat’s classification and the prevalent international statistical rules, leaving national statisticians with little guidance on how to interpret the rules and allowing Eurostat to emerge as their only point of reference (DLA Piper, 2016).

Until the sovereign debt crisis, only a few countries had frequent recourse to the off-balance-sheet classification of PPPs, most prominently the United Kingdom and Belgium. Therefore, PPP projects did not have serious repercussions on Maastricht indicators (Interview 7, see also Budina et al. 2007). This changed after the crisis reduced the fiscal space for public investment, leading more countries, such as Greece and Poland, to explore the option of designing Maastricht-neutral public infrastructure PPP investments (Kania, 2011; Papadopoulos and Stamati, 2013). At the European level, the European Commission publicly supported the diffusion of PPPs (European Commission, 2009), bolstered by the Monti report, which identified the shortage of public investments as an obstacle to the completion of the single market and recommended facilitating ‘the combination of public-private partnerships with the use of structural funds’ (Monti, 2010, p. 66).

Central to the Commission’s promotion of PPPs was the EIB, which had developed expertise in the use of PPPs since the 1990s and, after the crisis, aimed to become ‘a knowledge bank for PPP task forces’ (European Investment Bank, 2010, p. 11; Liebe and Howarth, 2020). To this end, the Commission and the EIB founded an advisory hub in 2008, EPEC, for the promotion of PPPs ‘to address the tightening of bank credit conditions in most member states and pressure on public finances as a result of the crisis’ (EPEC, 2011; Liebe and Howarth, 2020, p. 201). In addition to financing PPPs, the EIB also became the central platform for national public sector actors to exchange and pool expertise and consult ministries or local authorities interested in designing a PPP (Liebe and Howarth 2020, 202; Interview 3).

Two sets of rules created an obstacle to the development of the European PPP market: procurement rules and statistical rules. The European Commission revised the public procurement rules accordingly in 2014, but it could not formally intervene in the statistical classification of PPPs. It was instead EPEC that focused its efforts on the clarification of PPPs’ statistical treatment (EPEC, 2010; Jenett, 2010, p. 15). In one of its first reports, EPEC discussed the potential adaptation of the control approach by Eurostat and remarked that this would ultimately lead to the (re-) classification of most PPPs on balance sheet. Furthermore, EPEC stated that it is unclear why an essentially definitional change should disadvantage PPPs if and when these promote infrastructure investments which are economically justified, affordable and good value for money for the public sector (EPEC, 2010, p. 27).

This lenient view of PPPs was opposed by the proponents of the control approach, who called for the harmonization of public accounting and statistics. As quoted in the same EPEC report, central banks argued that the control approach ‘would increase the transparency of future fiscal commitments by governments’ (EPEC, 2010, p. 27). For the EIB, however, the shift to the control approach endangered the deepening of the PPP market because it would put them on balance sheet, and PPPs were popular among Member States precisely because of their limited repercussions for Maastricht calculations (Interviews 6 and 7 [European Court of Auditors 2018, 47]).

For the EIB and EPEC the statistical classification of PPPs was not of primary importance, although they were aware that some Member States prefer PPPs to be off balance sheet. This was already remarked in a review of the EIB’s PPP projects in 2009, in which the majority of the 17 interviewees, all EIB PPP experts, highlighted PPPs’ political ‘fashionability’ and ‘the fact that some promoters continue to see PPPs primarily as off-balance sheet vehicles’ (Bain, 2009, p. iii). For the EIB officials, the ‘accounting distractions’ ultimately let governments prioritize the balance sheet treatment of PPPs over value-for-money concerns (Bain, 2009, p. v). 6 Notwithstanding the risks and concerns, the EIB strengthened its efforts to promote PPPs. After all, the EIB’s and EPEC’s priority was and is to remove any barriers to the EU PPP market. In 2012, however, all these efforts risked being jeopardized by the looming introduction of new statistical rules, ESA10, which gave rise to heated debates about the statistical categorization of PPPs among statisticians, who were caught between national political preferences and Eurostat’s statistical decisions and other interested parties, such as line ministers (i.e. health, transport or the economy) or Commissioners seeking to pursue Maastricht-neutral PPPs (Interviews 6 and 4).

A lack of understanding of PPPs? How changes in statistical rules inhibited off-balance-sheet PPPs

In 2013, the European statistical rulebook was revised to align with the international statistical nomenclature, which so far had not explicitly addressed the statistical classification of PPPs. Most notably, the ESA10 review led for the first time to the inclusion of a section on PPPs (Eurostat, 2016a, p. 3). These changes affected the classification of many PPPs. On one hand, statistical rules emphasized rewards, which led to the reassessment of those PPP projects in which governments held stakes in the private part of the contract or projects with conditionality clauses to limit the profits of private partners. On the other hand, the accounting criterion of control was applied in statistically unclear cases, which focused on governmental influences in private companies, namely, through holding stakes directly or indirectly (Eurostat, 2016a, p. 5).

These new criteria put several existing and planned projects under scrutiny by forcing the on-balance-sheet reclassification of PPPs. Besides the Tram in Liège, which was abandoned after its reclassification on balance sheet in 2015 (Bechet, 2016), also Scottish models for smaller PPPs were put on balance sheet after several years of investments, while the Welsh scheme barely avoided reclassification and the Polish government declared that it would cancel the procurement for major expressways if Eurostat reclassified the PPPs on balance sheet (Sousa, 2020). In this context, several PPP experts pointed out that they felt Eurostat lacked an understanding of the technicalities and intricacies of PPPs, 7 causing ‘problems for governments planning and procuring PPPs, particularly those for whom the debt and deficit impact is critical’ (Kennedy, 2016).

Besides these national projects, the European Commission had set up a plan to encourage investment in infrastructure – the so-called ‘Juncker plan’ – which implicitly promoted the use of PPPs. Or, as a senior economist at an investment bank puts it: The investment plan for Europe, better known as the Juncker Plan, is a paradigm for PPP: it aims to kickstart EU investment by mobilising financial resources more effectively, allowing the EIB to finance riskier but more innovative projects and getting rid of barriers to investment in the EU (Mestres Domènech, 2017).

Although not explicitly promoted in the Juncker Plan, PPPs are exemplary of the plans’ ambition to blend public and private investments in common projects. By 2018 PPPs worth nearly €4 billion had already been guaranteed as part of the plan while between 2015 and 2018 over 70% of European PPPs were financed through EFSI (Counter Balance, 2020). For the EIB, the classification of PPPs does not matter, but the EIB is aware that many Member States prefer Maastricht-neutral PPPs (Interviews 3 and 6). The combination of growing demand for off-balance-sheet PPPs by Member States and the promotion of PPPs through the EIB and national promotional banks created political momentum for a more favourable statistical treatment. Political actors argued that the new statistical rules made it impossible to tackle the shortage of infrastructural investment identified by the Juncker Plan and that there was need to ‘raise the matter at the highest political level’ (Kelly 2016; Interviews 4 and 5).

But the Commission and elected officials from the Member States are not allowed to interfere directly with Eurostat’s work (Interview 2). Therefore, it was statisticians from the Member States who, under increasing political pressure from their home government, asked Eurostat to clarify the statistical rules for the classification of PPPs (Eurostat, 2015; 2016d). For example, during Eurostat’s visit to Belgium, national statisticians pointed out that Belgian governments have the clear objective to record PPPs off balance sheet, which entails that governments might change their contracts until a recording off balance sheet is accepted (Eurostat, 2014, p. 44).

National politicians wanted clarity about the statistical categorization of their PPP projects, as Eurostat rules did not cover all contractual provisions in detail, leaving this task to national statisticians (Kelly, 2016; Sousa, 2020). In 2015, statisticians emphasized their difficulties in dealing with PPPs and suggested the creation of a dedicated expert group ‘in order to analyse existing contracts and clarify practical issues’ (Eurostat, 2016d, p. 32). Furthermore, companies, consultants and policymakers shared a growing interest in the standardization of PPP contracts to simplify the planning process (EPEC, 2017). 8

The politicization of PPPs affected government finance statisticians in two ways. First, the bureaucratic workload for the statistical classification of PPPs had increased considerably because PPP contracts entail multiple transactions and are written in legal jargon, making their statistical categorization complex and lengthy (Interviews 4, 5, 6 and 7). These struggles were aggravated by the new ESA10 rules, for which statisticians wanted new application guidelines adjusted to the European PPP contracts (Eurostat, 2015, p. 16). Second, Eurostat statisticians’ bureaucratic workload had increased because of the political promotion of PPPs by the Commission (European Commission, 2009), which in turn created requests for advice from National Statistical Institutes and criticism of ‘wrong’ classifications (Sousa, 2020). After all, Eurostat’s main concern is to strengthen the institutional capacity of National Statistical Institutes and empower their independent political decision-making (Interview 2), while the statistical community as a whole tries to champion the methodological work behind the ESA10 (Savage 2005).

The culmination of this political and professional pressure led Eurostat to investigate the treatment of PPP contracts more exhaustively (Interview 6). Subsequently, Eurostat created a working group among the most invested statisticians and tasked them with clarifying the statistical treatment of PPPs (Eurostat, 2015; 2016c). After two years the results were published as a chapter in the application guide for statisticians – which was by far the longest chapter – (Eurostat, 2016a, p. 1), as a detailed separate clarification note (Eurostat, 2016a) and for the first time as a translation of statistical rules into practitioner language, the PPP Guide, published jointly by Eurostat and EPEC (Eurostat & EIB, 2016). The Guide would prove crucial for the future development of the PPP market.

The strategic alliance of Eurostat and EPEC – A guide to PPP rescue

The 2016 PPP Guide was intended to complement the technical publications for statisticians and specifically addressed ‘stakeholders in Member States, PPP practitioners and non-specialists in national accounts’ (Eurostat, 2016a, p. 1). The PPP Guide looked at statistical rules ‘through a PPP lens’ in a language that was accessible to practitioners, while simplifying the analysis of contracts for statisticians (Eurostat & EIB, 2016). After several national actors had expressed concerns about the new statistical rules (Kelly, 2016; Sousa, 2020), EPEC’s expertise in the legal design of different national PPP markets and its financial resources were key in the effort to use the policy process to deflect political pressure (Interviews 3, 6 and 7). The Guide helped Eurostat to widen its room for manoeuvre by meeting the demands of policymakers and PPP practitioners. Furthermore, it simplified the statistical assessment of PPP contracts, thereby reducing the workload of national and European statisticians (Interviews 6 and 7).

The PPP Guide does not overrule previous rule clarifications provided by Eurostat but outlines the contractual implications for the statistical categorizations of PPPs very clearly (e.g. thresholds for risks and rewards, for control and specification of the forms of government participation that could trigger a re-classification of PPPs on balance sheet [CMS 2016]). The thresholds for risks and rewards emerged as negotiated compromises between EPEC and Eurostat based on evidence from different practices in Europe, which made it possible to identify the most common PPP contractual features (Eurostat & EIB, 2016, 9). Thus, the Guide meticulously describes the statistical aspects of the contractual features, which are summarized in a table at the end of the document, and implicitly provides codified instructions for the design of off-balance-sheet PPPs (Eurostat & EIB, 2016, 142–52).

The PPP Guide was received positively by political actors and statisticians alike, as it allegedly made Eurostat more predictable and consistent, and ‘paves the way for the procurement of additional infrastructure at a time when investment in infrastructure is being pushed’ (Sievwright, 2016). From the industry’s viewpoint, the Guide resolves the ‘nightmare’ created by the possibility of changes to the statistical categorization of PPP projects already under way (Interviews 3 and 7). To promote the new guide Eurostat and EPEC gave several presentations, which were welcomed by the PPP industry and statisticians (Oneto, 2018). The IMF even stated that its ‘departments might consider PPPs as a solution for investment’ (Eurostat, 2017, p. 8). Member States used the guide as a stylized model for standardized PPP contracts and emphasized that PPP rules should be left unchanged, explicitly pointing out ‘that politicians in their country liked the current PPP rules and may want to block any move towards control’, meaning a stricter assessment of asset control (Eurostat, 2020, p. 13).

In the broader context of statistical-rule development, Eurostat explained the rationale for investment in the PPP Guide as follows: PPPs have been an important subject in many MS, and the treatment of the PPPs in national accounts has raised a substantial interest by the Commission and other, including political, parties. In addition, the Investment Plan for Europe (Junker's plan) promotes investments in MS, while many of these investments will be carry out via PPPs. Therefore, apart from statistical issues, there are some communication aspects which need to be addressed (Eurostat, 2016c, p. 20).

All these efforts to clarify the statistical classification of PPPs can also be explained by the combined strategic interest of the EIB and Eurostat. For the EIB and EPEC, clarification was vital to ensure the roll-out of funds, and the issue of their statistical treatment was brought up during discussions with the working group about issues within European government finance statistics (Eurostat, 2015). Even though some Member State investments in the Juncker Plan can be excluded from Excessive Deficit Procedure (EDP) calculations, EPEC explained already in 2010 that for PPPs ‘a “carve out” from the application of the EDP for long-term infrastructure investment is one option, albeit one that could be both politically controversial and complex to implement’ (EPEC, 2010, p. 29).

Moreover, this recent clarification of statistical rules fits very well with Europe’s new goal of exploring how fiscal rules ‘could be applied more flexibly without changing them’ (European Commission, 2015, 2016). Later, in 2016, the Economic and Financial Committee (EFC)

9

circulated a questionnaire on ‘statistical issues in the context of the Stability and Growth Pact’, following which the Council encouraged ‘Eurostat and the EFC to further improve the governance of EDP statistical processes’ (Eurostat 2016e, 3). In response to this pressure, Eurostat stated that the PPP Guide is already a support for Member States (Eurostat, 2016d, p. 3). EPEC was also seemingly satisfied with the clarified statistical rules for PPPs, countering criticism by PPP practitioners of the hurdles posed by statistics, while warning of ‘an excessive focus on the off-balance-sheet treatment’ and the ‘affordability illusion’ that PPPs create (EPEC, 2016, p. 6). However, the ability to keep PPPs off balance sheet remains a key concern for governments. A 2018 report by the European Court of Auditors states that for governments’ investment decisions the possibility of recording PPPs as off-balance-sheet items was an important consideration. Five out of the 12 PPP projects assessed, with a total cost of €7.9 billion, were initially recorded off-balance-sheet (European Court of Auditors, 2018, p. 2).

In this context, the PPP Guide proved an ideal instrument for Eurostat and EPEC to square the circle between enforcing statistical rules for debt calculations and addressing previous allegations of opaque decision-making. While Eurostat used the guide to formulate practitioner-informed guidance without direct political interference, EPEC could strengthen its standing as the European PPP expert hub.

Conclusion

Off-balance-sheet policies are an important but understudied feature of public finance (Brixi and Schick, 2002; Polackova, 1998). This paper has analysed the political and technical struggles around an archetypical off-balance-sheet instrument, PPPs. After the sovereign debt crisis, PPPs were seen as an important policy tool to boost long-term investment while pursuing fiscal consolidation (European Commission, 2009; Monti, 2010) but for many governments they were only attractive due to their off-balance-sheet status. However, PPPs are not debt-neutral by definition but need to fulfil certain criteria defined by technical experts, and these criteria have changed with the tightening of fiscal rules after the sovereign debt crisis, putting the off-balance-sheet status of PPPs at risk. At the heart of this paper is the puzzling alliance between Eurostat and the EIB’s EPEC which led to the publication of a PPP Guide in 2016 that, by outlining the specific contractual features for PPPs’ off-balance-sheet status, prevented the categorization of all PPPs on balance sheet (Eurostat & EIB, 2016).

The case of the PPP guide is exemplary of the importance that technical experts have gained for economic policy-making in the European Investor State. As national and European actors seek to foster economic growth by enrolling private actors and leveraging public funds to keep debt off their balance sheet (Lepont & Thiemann, this issue), technocrats at EPEC and Eurostat become key to formulating workable solutions within the existing fiscal rules. Combining theoretical insights from the literature on multi-level dynamics in Europe, expertise and policy instruments, I argue that, in spite of limited bureaucratic resources and severe institutional constraints, Eurostat successfully forged a strategic collaboration with EPEC. For EPEC the collaboration supports the goal to remove barriers to the PPP market, as the foreword to the PPP Guide, co-signed by Commissioner Marianne Thyssen and EIB vice-president Jan Vapaavuori explicitly acknowledges (Eurostat & EIB, 2016, p. 3). The motivation of statisticians is more puzzling to grasp as they usually restrict their work to narrow statistical expert circles. However, the case study has shown that amid increased bureaucratic workload and growing political pressure for more clarity in PPPs’ statistical assessment, EPEC’s expertise helped statisticians to safeguard the independence of their assessment.

By emphasizing the interplay between policy support for off-balance-sheet instruments and the ensuing technical discussions, this paper contributes to three distinct strands of the literature. First, the analysis provides a comprehensive background to the technical subtleties that shape PPPs, thus complementing the sparse accounts of European off-balance-sheet instruments (Guter-Sandu and Murau, 2022) and their centrality for the new configuration of Europe’s multi-level public–private investment system. Second, the debt-neutrality of PPPs is a typical example of how technical experts shape ‘workable solutions’ for European policy impasses (Schmidt, 2020) and thus help the European Union to ‘fail forward’ (Jones et al., 2021). In this regard, the findings put emphasis on experts’ agency by expanding their (supranational) policy toolbox, rather than simply serving the interests of large Member States. Third, the analysis highlights a hitherto understudied performative dynamic of European debt and deficit indicators (Desrosières, 2015). Politicians can intentionally design off-balance-sheet policies, but if in doing so they challenge existing rules, experts have to adapt the rules to new policy designs, thus shaping fiscal constraints.

The PPP Guide provides guidance on the application of existing rules and is a typical case of incremental change in European debt indicators (Barta and Schelkle, 2015). Even though the resulting stimulus was not sufficient for the PPP market to recover its pre-crisis level of activity (Cepparulo et al. 2023), the market did pick up slightly in 2024. In any case, the cooperation between the EIB and Eurostat was so successful that they worked on another practitioner’s guide for green-transition PPPs and are currently revisiting the rules on concessions (Eurostat, 2019b, 20; Eurostat and European Investment Bank 2018). Thus, the cooperation between the EIB and Eurostat exemplifies how the consolidation-investment conundrum has forced the emergence of new alliances among technocratic actors to formulate ‘workable solutions’ (Schmidt 2020) in order to ‘coordinate an expansion of de facto fiscal space’ (Lepont & Thiemann, this issue, 9).

With the off-balance-sheet infrastructure already up and running, and the cleavage between fiscal prudence and fiscal constraints as relevant as ever, ‘the risk is that the European Commission will spend the next decade finding creative ways to bypass its own rules’ (Paolo Gentiloni, EU Commissioner for the Economy, cited in Fleming 2021). The recent surge in off-balance-sheet policies has highlighted once more the importance of debt-neutral policy instruments in the EU (Rodríguez-Vives and Giron, 2021) and the case of PPPs shows how, along with the off-balance-sheet institutions making these investments, European and national technical experts play a key role in this dynamic. More research is needed to explore the off-balance-sheet universe of the EU at both the national and European levels, and the instruments and actors at its heart.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.