Abstract

Financialisation is not a homogenous but a variegated process. However, the question along which categories this variegation happens is currently unanswered. We identify four variegation categories: financial sector structure, productive structures, the role of the state, and the growth model. We apply these categories to two seemingly similar emerging-economy contexts which have produced different financialisation experiences: Colombia and South Africa. Financialisation in South Africa is much more market-based, meaning it is led by the financial sector unfolding through financial markets and banks’ activities visible in their much larger size, activity, and international interconnectedness, than in Colombia. Hence, South African credit extension, bond markets, domestic pension funds, and stock market capitalisation are substantially larger than Colombia’s, while the Rand has experienced strong internationalisation since 2000. Nevertheless, there is evidence financialisation processes have been unfolding dynamically in both countries over the past two decades, reinforcing the view of variegated financialisation as a common tendency with significant heterogeneities across countries.

Keywords

Introduction

Financialisation has become a widely researched phenomenon across the social sciences since the term has been coined in the 1990s, capturing the changing nature of US capitalism. More recently, a consensus has been emerging among proponents of financialisation that the phenomenon needs to be understood as variegated, playing out differently across time and space without convergence of domestic experiences or institutions (Ward et al., 2019). Nevertheless, there is a tendency for financialisation studies focussing on poorer countries to either lump economies together under the heading of the ‘global South’ or portray the phenomenon as unique and country-specific, overlooking commonalities among these economies. Thus, there is a need for a more systematic discussion of variegation in the context of subordinate financialisation. The literature focussed on emerging economies (EEs) documents important commonalities countries exhibit in their specific financialisation manifestations. This can be seen in the shared traits of financialisation within this country group as opposed to the global North, generally reflecting the financial and productive subordination of EEs (Bonizzi et al., 2022). It can also be seen in the distinct commonalities of financialisation within and between different emerging world regions (Karwowski, 2022). Thus, we argue variegated financialisation in EEs can be understood as ‘commonality without convergence’ and put forward a systematic analytical toolkit which can help identify the distinct experience of the global South, while capturing those commonalities. 1

We understand variegated financialisation as process unfolding within common global trends, shaped and mediated by domestic determinants, resulting in variegated financialisation outcomes across countries. Empirically drawing on existing studies and theoretically inspired by comparative capitalism studies, we put forward four categories of variegation to capture crucial domestic determinants: (1) the financial structure, (2) productive structures, (3) the role of the state, and (4) the growth model. Our purpose is to provide an investigative framework that can be used as a guide to study variegated financialisation in an analytically coherent way, and inductively build an understanding of different forms and extents of financialisation.

To illustrate the relevance of our analytical schema, we apply these categories to compare two cases of financialisation in EEs: Colombia and South Africa. By choosing these two EEs, we are better able to distinguish between the commonalities of the global context they face, reflective of their productive and financial subordination, and their distinctive national differences. Both countries share similar experiences in terms of the process of financial liberalisation, and the dominance of an extractive sector that shapes domestic production especially through the presence of large conglomerates. We show that these commonalities lead to some similarities in financialisation outcomes as both countries have large financial sectors and receive sizeable cross-border financial flows.

Yet, there are important differences between the two countries which make them suitable case studies. From a regional perspective, Latin America – alongside Central Eastern Europe – exhibits some of the most severe signs of financialisation, while sub-Saharan Africa is the least financialised among the emerging world regions. Equally, comparative accounts place the two economies at opposite ends of the financialisation spectrum with South Africa being strongly financialised while Colombia showing more modest signs of financialisation (Karwowski, 2022). Hence, financialisation is much more pronounced in South Africa. Here, credit extension, bond markets, domestic pension funds, and stock market capitalisation are substantially larger than in Colombia, while the Rand has experienced strong internationalisation over the past two decades. Our categories of variegation can help us understand these differences in the two countries’ financialisation experience. We show that variegation emerges from the interaction of domestic institutions with international finance against the backdrop of the domestic growth model. In South Africa, financialisation is led by financial institutions’ activities and their international interconnectedness together with state entities who use finance in mediating industrial relations, highly compatible with consumption-led growth dependent on household debt. Thus, South Africa’s financialisation can be characterised as market-based, mass-based, and fuelled by corporate internationalisation. In Colombia on the other hand, the close relations between conglomerates and the financial sector have not led to mass-based financialisation. The less explicit usage of finance as a means to govern socio-economic inequalities reduced the role for developing capital markets instead, making financialisation a more elite-based and contained phenomenon.

The structure of the paper is as follows: In the next section, we discuss the evidence for variegated financialisation, while identifying some empirical measures typically used in the literature. Subsequently, we propose four categories of variegation (the financial structure, productive structures, the role of the state, and the growth model) which aim at capturing the country-level differences in empirical financialisation outcomes articulated, among other things, in the economic measures discussed in section 2. Our comparative analysis in section 3 captures the main common tendencies and variegation in the financialisation experiences of these two EEs, while section 4 operationalises the proposed categories to compare and understand the origins of the different financialised condition in Colombia and South Africa. Section 5 concludes.

Variegated financialisation: Evidence and empirics

The generally accepted working definition of financialisation is that it increases the ‘role of financial motives, financial markets, financial actors and financial institutions in the operations of the domestic and international economies’. Epstein (2005: 3). More specifically, this paper understands financialisation to represent a structural transformation of socio-economic processes in the contemporary historical phase of capitalism. This manifests itself globally in the growth of financial markets, their extension across and insertion into socio-economic processes, including those formerly untouched by finance. This transformation brings about a redistribution of income, the creation of new assets and markets, and the reshaping of the behaviour of market (infra-)structures, organisations, and individuals. Thus, financialisation represents a qualitative and quantitative transformation of the role finance holds at the global level.

At a more concrete level of abstraction, it is increasingly clear that financialisation is a complex process, manifesting itself in different forms across time and space. Economic geographers in particular have highlighted the importance of the multi-scalar spatialisation of financialisation (Engelen et al., 2010; French et al., 2011; Pike and Pollard, 2010). The concept of variegated financialisation has emerged to capture this diversity. The idea of variegation in financialisation has its origins in the concept of variegated capitalism (Peck and Theodore, 2007; Dixon, 2014; Jessop, 2014). Accordingly, capitalism should not be understood as one singular but rather as uneven multi-scalar process. Variety within capitalism therefore emerges through interdependence between various components of a (global) capitalist totality. Variegated financialisation similarly understands financialisation as a common global process within contemporary capitalism, but equally recognises that the concrete forms it takes are geographically and temporally specific. Financialisation unfolds in an uneven but interconnected world economy where domestic institutional specificities mediate change, producing observably different outcomes as a result (Engelen et al., 2010; Lai and Daniels, 2017; Ward et al., 2019).

The usefulness of variegated financialisation in highlighting ‘commonalities without convergence’ is especially clear for the analysis of EEs. Recent literature has developed concepts such as ‘dependent’ or ‘subordinate’ financialisation, which highlight how financialisation in EEs reflect their subordination in production and finance (Bonizzi et al., 2022; Akcay et al., 2022). These approaches stress the global processes that generate common pressures across EEs, thus shaping financialisation in similar ways. Yet differences between EEs remain visible. Therefore, it is important to distinguish between subordination as a structural characteristic of EEs and variegation due to local policies and institutions mediating a country’s position in global hierarchies of production, circulation, and finance. Notwithstanding the global dynamics of financialised capitalism, domestic determinants shaped by history, local institutions, and political constellations might well be more influential in defining the concrete reality of a country’s financialisation trajectory.

This ‘commonality without convergence’ of variegated financialisation can be clearly observed at the nation-state level (Karwowski et al., 2020). The nascent literature suggests that, while financialisation is multi-scalar and generates uneven patterns at different times and geographical levels, financialisation trajectories are shaped by productive and institutional structures, whose history is deeply embedded at the nation-state level and in the relations between world regions, not least through the role of the state itself. Of course, variegation also happens at the subnational level. Nevertheless, here we focus on the nation-state as the scale on which variegation can be measured and interpreted most evidently. To make sense of variegated financialisation, we can take inspiration from comparative capitalism studies (Jackson and Deeg, 2006), including the varieties of capitalism (VoC) approach (Hall and Soskice, 2001). VoC juxtaposes two broad types of capitalist systems, Anglo-Saxon liberal market economics (LME) and continental Western European coordinated market economies (CME), respectively. The former mainly rely on markets to coordinate production processes across the labour market, corporate governance as well as financial and welfare institutions, while the latter embrace nonmarket coordination through, for instance, trade unions or professional associations. The VoC approach understands domestic institutions to be functionally complementary. Hence, LMEs have sometimes simplistically been characterised as market-based financial systems where domestic corporations significantly tap into financial markets for funding, while corporations in bank-based CMEs were stylised as turning to bank loans. Empirically, there is little evidence for this simplification (Karwowski et al., 2020). Furthermore, the traditional distinction between bank and market financing has become outdated given the turn towards financial markets among big banks around the globe (Hardie et al., 2013).

While not without limitations (especially in the area of finance, see Dixon, 2011), the VoC approach has been successfully used as fruitful starting point for contributions on variegated financialisation: In one of the first attempts to highlight variegation, Engelen et al. (2010) compares the varying financialisation trajectories in the United States, Germany, and the Netherlands, explained by the different financial structures across these countries. Several works have emerged since, highlighting the variegated forms of financialisation across different countries (Lapavitsas and Powell, 2013; Aalbers, 2017; Brown et al., 2017; Ward et al., 2019; Bonizzi et al., 2021) including increasingly across EEs (Lai and Daniels, 2017; Karwowski, 2022). While the VoC approach has helped develop a variegated understanding of financialisation, the framework mainly focuses on productive and financial structures with a limited role for state actors and public institutions. Here, other related approaches such as regulation theory can serve as inspiration to highlight the important role of state policies and entities in financialisation (Boyer, 2005). More recently, research around comparative capitalism has turned to the study of growth models in an explicit attempt to incorporate aggregate demand into the framework which is mostly neglected by the VoC literature (Baccaro and Pontusson, 2016, Baccaro et al., 2022).

Against this background, we propose an empirical tool based on the macroeconomic aggregates, that is, the financial sector, non-financial companies (NFCs), households, the state, and the foreign sector, to identify commonalities and differences at the nation-state level (Karwowski et al., 2020; Ward et al., 2019). Using macroeconomic aggregates as analytical framework is not merely a descriptive tool but serves the purpose of distinguishing between the main sources of economic dynamics and change. In fact, once we surmount the strict focus on the nation-state, the remaining aggregates, that is, the financial sector, NFCs, households, and state institutions, constitute the main economic building blocks across geographical scales because behavioural patterns, logics and dynamics of change differ across these aggregates. Focussing on their analysis can help us understanding the empirics and theory behind socio-economic phenomena such as financialisation, showing how their quantitative and qualitative manifestations differ across economies. Furthermore, important aspects of comparative capitalism studies can be brought together using macroeconomic aggregates as organising framework. The strong focus among VoC approaches on productive and financial structures 2 can be mapped onto the analysis of the financial sector and non-financial corporations in aggregate and given the international character of much of modern production and finance also the foreign sector. Regulation theory additionally stresses the important role of the state.

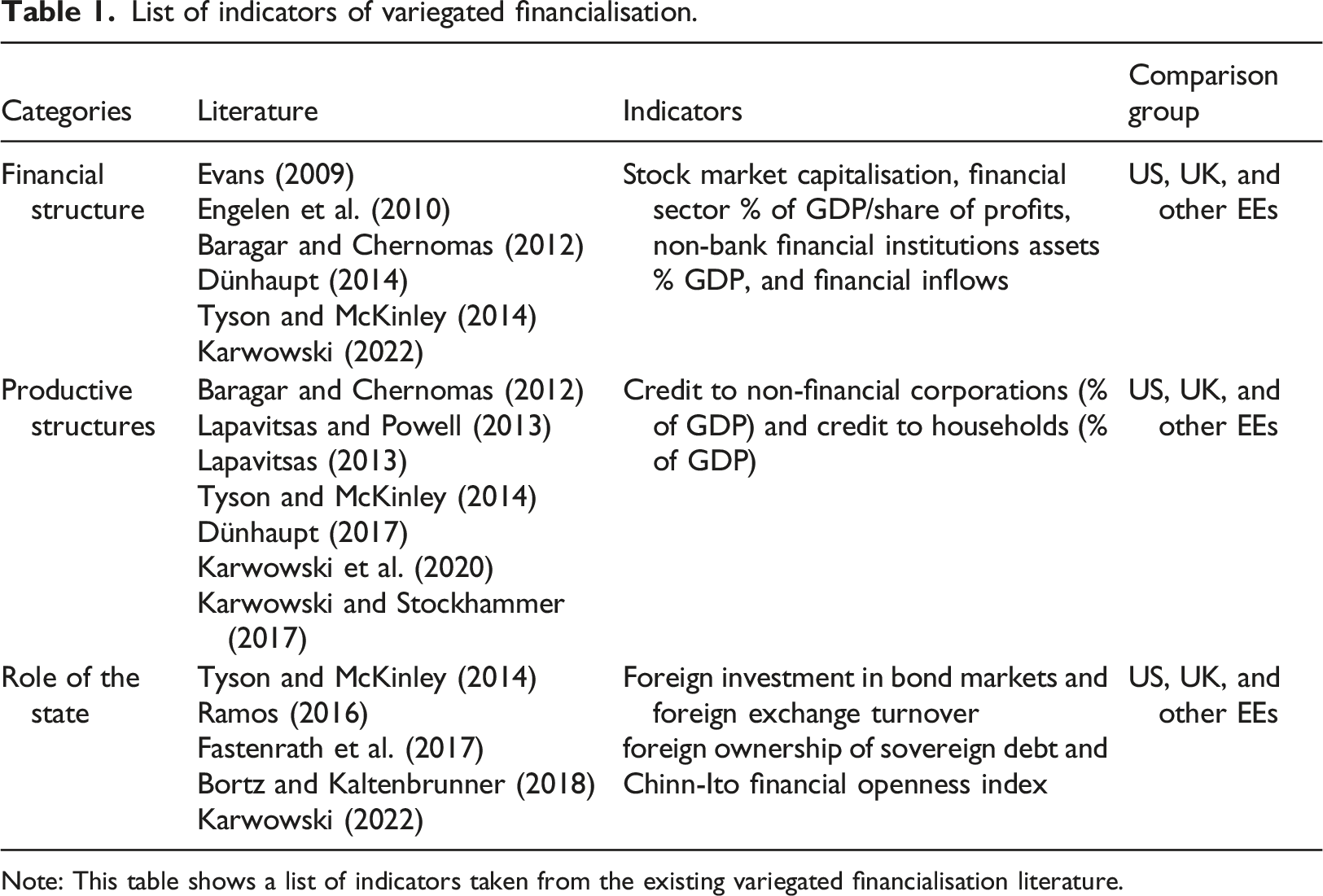

List of indicators of variegated financialisation.

Note: This table shows a list of indicators taken from the existing variegated financialisation literature.

Variegated financialisation thus offers a fertile conceptual starting point, linking the commonalities of financialisation with the diversity of its forms. However, existing studies on variegated financialisation either focus their analysis on a particular aspect of variegation, for instance, one specific sector or actor, or on cross-country comparisons which mainly describe rather than explain the diversity of its forms. What is missing from these accounts is a framework of analysis that can guide the empirical exploration of variegation. In what follows, we propose an investigative framework – though not necessarily exhaustive – for such an analysis by proposing four investigative categories which can help us better understand how the interaction between global drivers, that is, the common tendencies working through the international financial system, and domestic determinants lead to variegated outcome in financialisation. The proposed categories are not a deterministic matrix, but rather a systematic framework for investigation, which seeks to offer a comprehensive view of the factors that can determine distinct forms of financialisation across countries.

Investigative categories

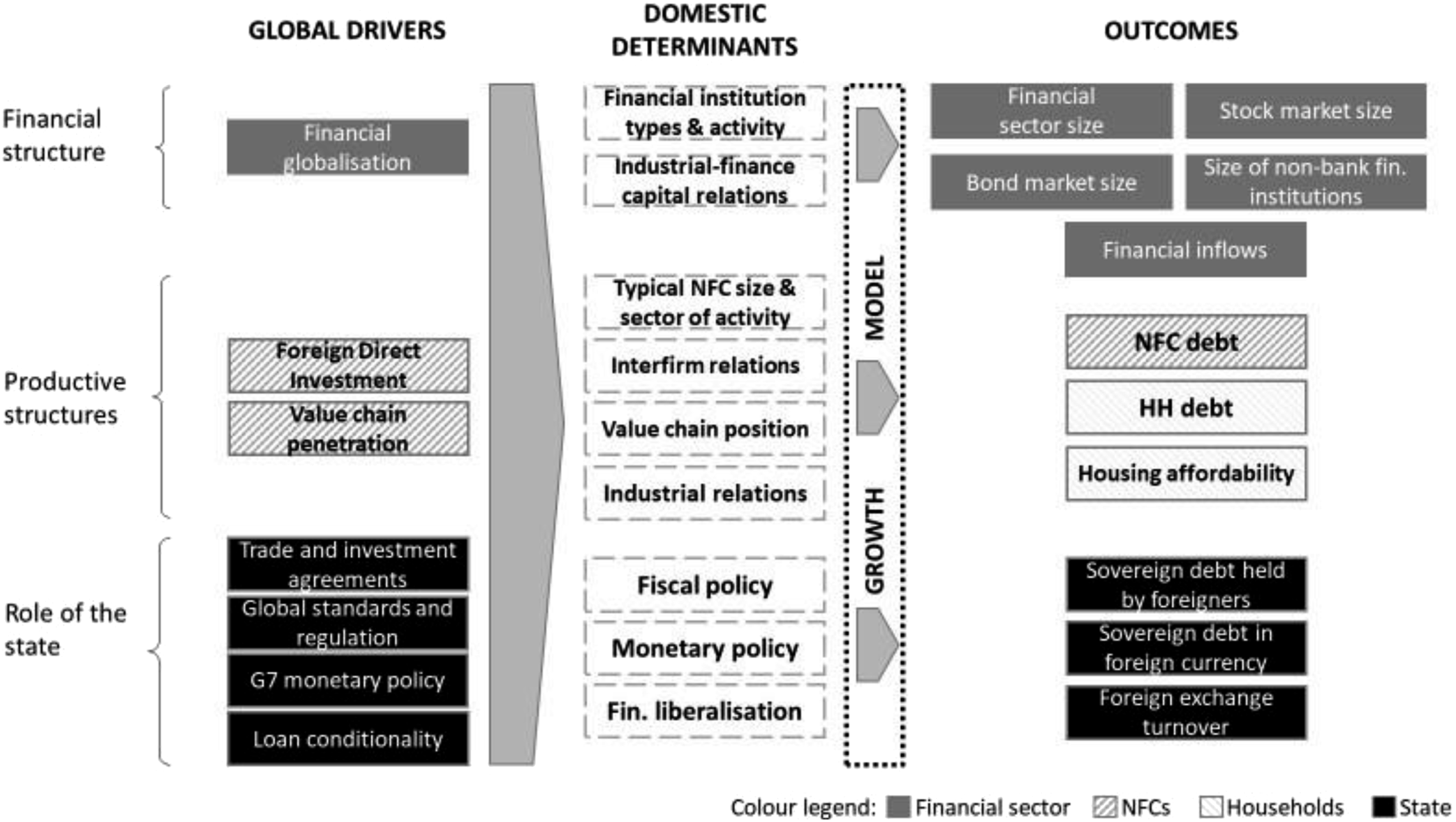

Financialisation is a global process which affects capitalism in its entirety. From the standpoint of EEs, this creates an essential context confronting national institutions. Domestic determinants are also very powerful drivers of variegated financialisation. The interaction of the pressures emerging from this global context with domestic determinants results in variegated outcomes at the national level

3

(see Figure 1). Categories of variegation.

Our framework is organised around the mentioned macro aggregates: the financial sector, NFCs, households, and the state, while keeping in mind the cross-cutting character of the foreign sector. Starting with the financial structure, the global logic of financialisation is towards greater cross-border financial integration and increased financial flows, a phenomenon referred to as financial globalisation, as well as a transition to market-based financial structures (Bonizzi et al., 2022). The interaction between global pressures, mainly originating from financial globalisation, with domestic financial sector determinants, in particular the types and activities of domestic financial institutions as well as the relations between industrial and financial capital, shape the size, and consequently influence of domestic financial markets. Variegated financialisation outcomes are then visible in varying sizes of the financial sector, the stock market, domestic banking, as well as non-bank financial institutions across countries (Engelen et al., 2010; Lapavitsas and Powell, 2013). Therefore, financialisation implies common processes of transformation for financial systems towards a greater centrality of market-based interactions and openness, but the pre-existing domestic financial structure will shape such a transformation resulting in a range of different outcomes, rather than converging to an ideal type of financial system. This is especially the case in many EEs, where domestic capital markets, while being transformed, often continue to be peripheral as source of financing.

The focus on financial structures captures the influence of the local finance industry, which is often inherently linked to the industry’s embeddedness in international circuits of finance. It is no coincidence that financialisation is most pronounced in the United States and the United Kingdom; each country hosting one of the major international financial centres: New York and London (Wójcik, 2013). While the emergence of the globally leading financial centres is shaped by history, their presence has driven and shaped local financialisation in the United States and the United Kingdom. A large and geographically concentrated financial sector is likely to wield substantial influence over domestic politics and policy formulation, pushing for deregulation (Nölke, 2020). For instance, the international position of London as financial hub and its direct competition with New York resulted in the emergence of the Eurodollar market during the 1950s in the United Kingdom since banking regulation was deliberately not applied to foreign currency transactions between non-resident lenders and borrowers (Fernandez and Hendrikse, 2020).

Financialisation can furthermore support or disrupt relations between what Marxist analysis defines as industrial and finance capital (Dumenil and Levy, 2001). The interests of finance capital might very well conflict with that of industrial corporations (Davis and Walsh, 2017). Full liberalisation of the financial account, for instance, can contribute to currency volatility, making domestic financial services more attractive and profitable (Gabor, 2012), while undermining the position of exporting businesses and allowing transnational corporations (TNCs), which are more equipped to navigate international financial markets, to enter at the expense of domestic capital.

However, a conflict resulting in the triumph of the former over the latter is not a necessary characteristic of financialisation. Domestic businesses can organise themselves and shape incipient forms of market-based finance to limit their disruptiveness, as shown by the creation of pension funds in Germany, where non-financial businesses and the traditional insurance sector were able to prevent the establishment of a widespread financialised pension system despite pressures from the financial industry (Röper, 2021). Hence, finance and domestic industrial capital interests may align in shaping financialisation trajectories. Indeed, in many instances, industrial elites have considerably expanded their investments into the financial sector which provides channels to store and transfer their wealth abroad (Fernandez et al., 2016).

Financialisation is not only caused by changes in the financial sector. Indeed, another crucial driver of variegated financialisation is the interaction of international and domestic productive structures, our second investigative category. At the international level, this mainly refers to foreign direct investment into and the value chain integration of domestic production, which embed countries into cross-border financial payments. Domestically, the size and sector of activity of NFCs, inter-firm relations, the position of domestic firms vis-à-vis the rest of the value chain, and industrial relations mediate these global tendencies. Variegated domestic outcomes of financialisation can especially be observed in NFC debt, levels of household indebtedness, and varying housing affordability across countries (Lapavitsas and Powell, 2013).

The focus on productive structures highlights how the heterogeneous characteristics and interactions between NFCs can exert significant influence on the process of financialisation. There is growing evidence that financialisation is actively embraced as an accumulation strategy by large corporations while smaller firms are merely exposed to some of its negative consequences such as higher levels of uncertainty. Countries where the local productive sector is characterised by smaller/low-value added corporations and without direct access to international markets are unlikely to engage in financial accumulation (Staritz et al., 2018). But once they are integrated into internationally operating value chains, they are exposed to financialisation, especially increased financial volatility and the need to generate returns to financial investors or powerful lead firms (Baud and Durand, 2011; Parker et al., 2018). However, existing coordinated or diversified oligopolistic inter-firm structures are not necessarily disrupted or replaced by market-based arrangements and can adapt to, shape, and contain the process of financialisation in different ways (Park and Doucette, 2016). For instance, the conditions that allow the German Mittelstand to thrive (including regional markets, localised consumption culture, and supportive regulation) seem to also restrain the pace, reach, and power of financialisation (Keenan, 2020). Certain sectors lend themselves more easily to a financialised business strategy than others. Industries in which intangible assets such as brand names, trademarks, patents, and copyrights play a major role tend to be more financialised (Orhangazi, 2019). Big pharma (Montalban and Sakinc, 2013), technology firms, the telecommunications sector (Massó and Bruna, 2020), and big international apparel and footwear companies (Soener, 2015) all fit this description. Listed corporations can then capitalise on these rights through stock markets, attracting financial investment, and, in return, generating shareholder value. Prospecting and mining rights can fulfil a similar function in the mining industry which can employ financialized business strategies to surmount the spatial embeddedness of its productive assets (Parker et al., 2018).

Another important aspect of productive structures is industrial relations. Important parts of the comparative capitalism literature (see, for instance, Thelen, 2010; Boyer, 2005) and political economy accounts of financialisation (Ashman et al., 2013) emphasise the importance of the capital/labour relationship to understand institutional change against the background of social conflict and the contestation of institutions as well as their (re)distributive functions. Financialisation is generally seen as redistributing power and value from labour to capital: it is associated with increasing labour flexibility and decreasing wage shares of national income (Kohler et al., 2019). It can therefore be expected that a strong union presence might contain financialisation, while the weakening of trade unions can facilitate the emergence of financialisation as seen in the United States (Witko, 2016). The strengthening link between NFCs and financial capital, in turn, has been documented to contribute towards declining union density across OECD countries since the 1970s (Kollmeyer and Peters, 2019), while eroding labour’s bargaining power (Darcillon, 2015). In some instances, financialisation has been observed to reinforce processes of labour subordination (Karacimen, 2015), and in others, it has increased the fragmentation of the working class through the reshaping of individual consciousness as risk-taking individuals (Langley, 2006). However, financialisation also takes place in economies characterised by collective bargaining, with trade unions shaping its particular forms rather than opposing it. For instance, in Northern Europe trade unions remain important actors through the management of private pension funds, whose logics do not always question the imperative of short-term financial profit (Anderson, 2019). The role of the state, through international and domestic institutions, represents another major area of interaction for global drivers and domestic determinants of financialisation, facilitating, fuelling, or hindering the phenomenon. The common logic of financialisation is towards greater openness, liberalising currency and financial markets, and opening them to foreign actors (Bortz and Kaltenbrunner, 2018). These pressures can come concretely through international trade and investment agreements, or loan conditionalities, more generally the setting of global standards and regulations and monetary policy of systematically important central banks. However, domestic institutions are crucial in mediating these forces as they translate international rules into domestic regulation and formulate national macroeconomic policies (Campbell, 2010).

There is a growing literature emerging on the financialisation of the state (Karwowski, 2019), which highlights how public policy and traditional state functions have been embedded in financial markets to different degrees according to countries’ domestic institutional setup and different public authorities’ interests. The two main policy areas here are monetary policy and fiscal policy, broadly conceived. 4 With respect to monetary policy, central bank activities (Gabor, 2012), such as provision of liquidity to financial institutions and markets (Braun et al., 2018), the overseeing of financial regulation (Braun and Gabor, 2020), and foreign exchange reserve accumulation in EEs (Kaltenbrunner and Painceira, 2018) emerge as key factors shaping particular forms of financialisation. These activities often result in the creation of hybrid public-private institutions, such as clearing houses and repo markets that act as the key infrastructure of financial markets (Braun and Gabor, 2020). Countries can maintain selective policy approaches to liberalisation as is visible, for instance, in China’s and India’s position vis-a-vis their peers among EEs as they adopt a much smaller degree of financial openness, keeping foreign financial inflows somewhat in check (Karwowski et al., 2020; Karwowski, 2022).

Financialisation can profoundly affect fiscal policy, which covers a large range of state functions since it contains state income, on the one hand, that is, taxation as well as sovereign debt, and expenditure, on the other, including, for instance, infrastructure provision and welfare policies. State authorities differ in the extent to which they promote rather than adapt to financialisation, with the size and composition of their spending and financing decisions. Increased involvement and use of financial markets might be a strategy for interventionist states in pursuing their domestic and international political objectives, through managing their sovereign debt or sovereign wealth funds, which gives rise to the concepts of state-led financialisation (Lai and Daniels, 2017) and the shareholder state (Wang, 2015). This is especially prominent in the case of China where the state has actively encouraged and directly shaped the development of capital markets, entrenching its control over domestic financial structures (Petry, 2020).

Our final investigative category is the growth model. The growth model brings together the interactions of global and domestic institutions, shaping local outcomes across the discussed macro aggregates, meaning financial structures, productive structures, and the state. As financialisation transforms socio-economic relations, it necessarily interacts with the specific national logic of capitalist accumulation and reproduction. A literature focussing on comparative growth models has emerged, which emphasises the role of aggregate demand as a driver of capital accumulation, based on Kaleckian and post-Keynesian theory (Stockhammer and Kohler, 2019). Analysing the ‘growth drivers’ of a growth model uncovers the key macroeconomic dynamics of a national economy. Here, finance-led growth is primarily driven by asset price inflation and debt – specifically household debt to finance consumption (Baccaro and Pontusson, 2016; Hein, 2019). Such growth models principally characterise Anglo-Saxon economies, which are therefore seen as more financialised, whereas other countries, such as Germany or Sweden, are characterised as export-led or wage-led (fuelling demand either externally or by domestic consumption financed by the aggregate wage bill) and therefore seen to be less financialised.

Our understanding of variegated financialisation implies that financialisation occurs across countries with different sources of growth, but growth models themselves act as a mediator of the financialisation form. Undoubtedly, in some countries, this takes the prominent form of debt-led consumption, but the absence or less systemic importance of such a phenomenon should not imply that these countries are somehow immune to financialisation. Even export-led economies, where household debt is not the primary driver of growth, will experience forms of financialisation. In Germany, export-led growth decreased domestic firms’ reliance on banks which in turn increased trading activities and lending to the financial sector and foreigners (Braun and Deeg, 2020). Furthermore, the global financial crisis has induced changes in growth models across major countries as international growth dynamics have changed (Kohler and Stockhammer, 2022). Given its more dynamic outlook, this final category complements the three preceding ones which due to their focus on specific domestic institutions are likely to capture slow and incremental change, while focussing more on supply-side issues around the production process. Growth models capture dynamic changes in aggregate demand and are therefore more than just their sum.

Figure 1 summarises the four proposed categories of variegation, mapping them onto the sectoral financialisation indicators identified in section 2. To summarise, we embrace the two analytical dimensions of financial and productive structures theoretically inspired by VoC and related approaches and empirically based on existing financialisation studies and their findings. Similar to VoC, we, for instance, stress inter-firm and industrial relations as important institutions shaping domestic outcomes and variegation. We complement these two categories by the role of the state especially important in Regulationist Theory and a country’s growth model introducing a more dynamic analytical dimension while acknowledging recent developments in comparative capitalism studies.

Two important qualifications must be made to the above scheme. Firstly, these categories are not meant to be analytically separate boxes but should be read as an indicative set of guiding principles to characterise variegated financialisation. It is their combination and the global/domestic interaction that mediates financialisation and produces its variegated forms. In fact, actors can start off mainly shaping local institutions (that is domestic determinants) and subsequently move into the international realm, becoming part of the international drivers of financialisation. 5 Thus, these two scales are porous and rather than self-contained. Therefore, the approach presented here is explicitly open to different methodological perspectives and does not seek to define ideal institutional set-ups that characterise specific varieties of capitalism. Institutions and power structures at the global, domestic, and class level can generate (at least temporarily) stable financialisation paths based on a particular combination of factors, but also dysfunctional arrangements, conflict, and eventually crises and breakdowns of institutional arrangements. Secondly, financialisation trajectories are also affected by even more contingent factors which are uneven in their distribution and path-dependent in their unfolding. Financialisation forms thus also depend on particular historical moments (like the fall of Soviet communism), which cannot solely be attributed to any of the above categories. Finally, our investigative framework is not meant as a specific theory of financialisation nor to draw definite unidirectional causal links. While we argue that the global context is essential in shaping financialisation in EEs, domestic institutions have an equally essential role. Our framework therefore does not imply that domestic or global factors are causally superior in determining financialisation. The next sections apply these analytical categories to compare the Colombian and the South African experiences of financialisation.

Comparing variegated financialisation in Colombia and South Africa

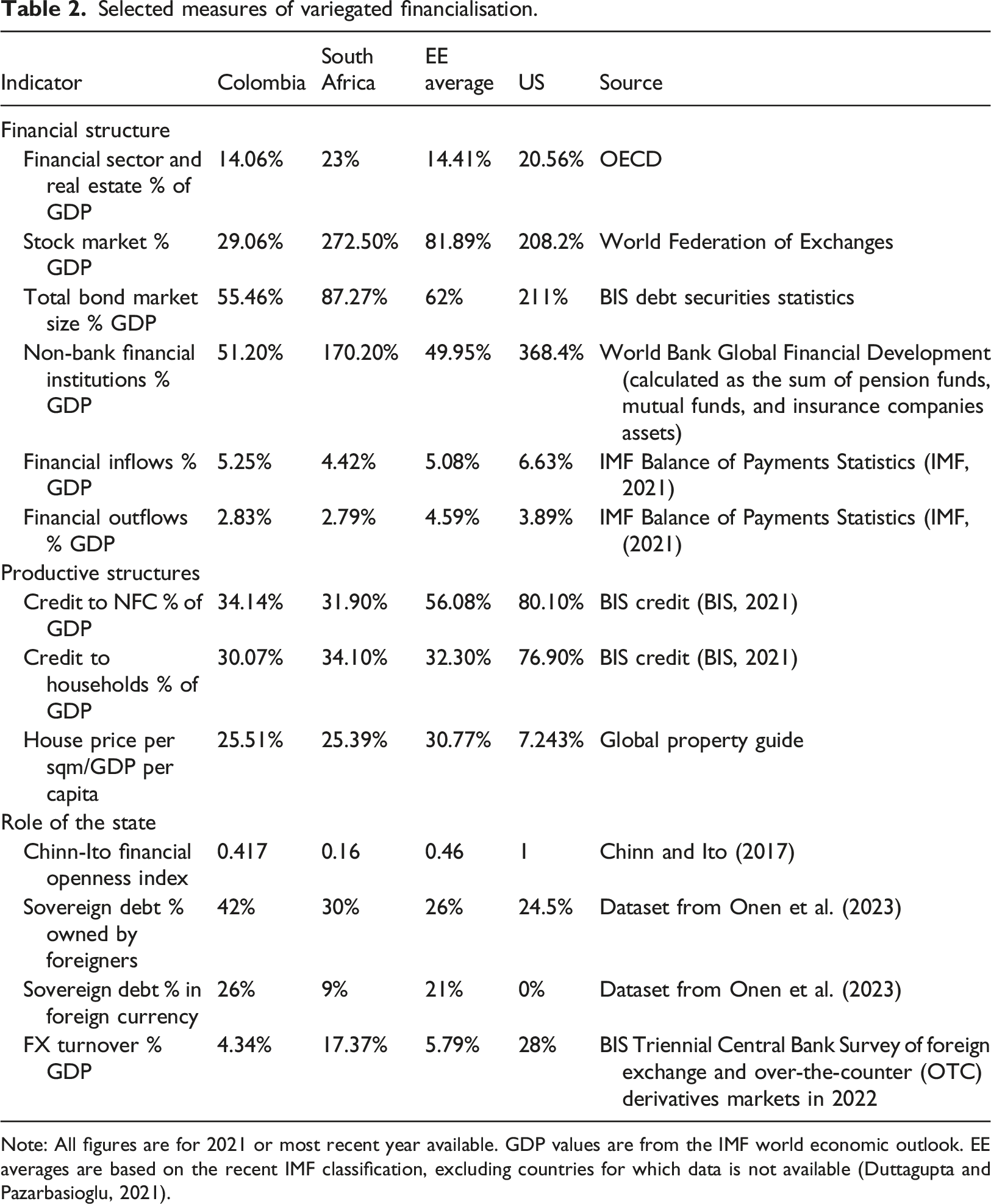

Selected measures of variegated financialisation.

Note: All figures are for 2021 or most recent year available. GDP values are from the IMF world economic outlook. EE averages are based on the recent IMF classification, excluding countries for which data is not available (Duttagupta and Pazarbasioglu, 2021).

In many other respects, the countries’ financialisation experiences look quite different, with South Africa generally displaying more highly financialised features. This makes the two countries useful comparators as they are significantly different cases among EEs which as a group are generally exposed to financialisation. The most striking difference is that financialisation in South Africa is much more market-based than in Colombia, with an overall larger weight of the financial sector within the economy, and a much more internationalised currency.

Over the past three decades, both countries have been recipients of significant financial inflows – worth just over 5% of GDP in both economies – and subject to financial outflows – worth around 3% of GDP – following a progressive liberalisation of the financial account more marked in Colombia than in South Africa as visible in Colombia’s stronger financial openness (see Chinn-Ito index in Table 1). In terms of composition of these cross-border flows, both countries have been significant recipient of FDI and portfolio flows. As a result, foreign investor participation in local capital markets has been high: foreigners own around 40% of the local government debt markets in Colombia and 30% in South Africa, compared to 26% across EEs and 25% in the United States.

However, the two countries exhibit varying degrees of and a different nature to their global financial integration, reflected in the very different levels of currency internationalisation – something that can be quantitatively seen in the size of foreign currency turnover for the South African Rand (17.37%) and the Colombian Peso (4.34%). The Rand has internationalised over the 2000s, with an increased volume of Rand-denominated financial instruments traded in international off-shore financial markets and over the counter also driven by large South African firms going global and listing abroad (Isaacs and Kaltenbrunner, 2018; Chabane et al., 2006), while the foreign exchange market in Colombia remains quite small. Despite growing foreign investor presence in Colombia, including in its local currency markets, foreign currency debt – rather than Peso-denominated liabilities – remains important making up around a quarter of all public debt in 2021 compared to only 9% in South Africa. This means that the Rand has increasingly been exposed to international investors who see it as an investment asset, influencing its movements through their transactions, more so than the Colombian Peso.

At the domestic level too, financial markets present some major differences. Johannesburg is an important regional financial centre and possesses one of the deepest stock markets when measured by capitalisation. While bank activity measured by domestic credit and indebtedness of the non-financial sector is similar and in line with EE averages there are striking differences when it comes to market-based finance. As of 2021, the Johannesburg Stock Exchange (JSE) was on average worth 2.72 the country’s GDP. This is significantly higher than the EE average of 81% and also the US figure at 208%. Equally, the South African bond market is sizeable at about 87% of GDP, and higher than the EE average of 62%. In comparison, Colombian capital markets remain quite small: the stock market totalled 29% of GDP, while bond markets were slightly larger (55%). These figures are lower than EE averages, and indeed there is evidence that the corporate bond markets remain peripheral to financing the real economy (Piñeros Castaño, 2016). Additionally, South Africa has a much larger non-bank financial industry whose assets exceed the country’s GDP (170%), compared to 51% of GDP in Colombia, and an average of 50% for EEs. Overall, the financial and real estate sector in South Africa has a considerably larger weigh in the economy at 23%, higher than in Colombia (14%), the average for EEs (14%) and even the United States (21%).

Based on these observations, the similarities between the two countries appear to stem to some extent from their EE ‘status’. Both are significant recipients of foreign portfolio and FDI flows. However, in South Africa, the process has a longer history and a deeper impact, quantitatively visible in the size of its capital and foreign exchange markets, and qualitatively shown by the importance of Johannesburg as a global financial centre. Financialisation in Colombia has seen more recent growth of domestic credit and non-bank financial institutions but has encountered more severe bottlenecks in terms of domestic capital market development and currency internationalisation. What can account for this differentiation?

Understanding variegated financialisation processes in Colombia and South Africa

The commonalities and variegation in South African and Colombian financialisation can be understood with reference to our investigative categories. Both countries have been affected by the same global forces which are root causes of financialisation and drive similarities in the phenomenon’s outcomes. Given the selection of our case study countries, the commonalities we observed are closely linked to these countries’ EE status. Financial globalisation, especially the increase in both FDI and portfolio flows, has gained pace markedly since the 1980s. This development affected rich countries first with EEs and developing countries only impacted a decade later (Prasad et al., 2003). International value chain integration strengthened also visibly starting in the 1990s, driven by the internationalisation of production processes (Cigna et al., 2022).

These developments were underpinned by changes in global policy. During the 1980s, the international policy discourse shifted away from government intervention as necessary policy tool to government interference as potential source of rent seeking, corruption and resource misallocation based on academic debates in rich countries starting in the 1970s (especially around ‘financial repression’, McKinnon, 1973). Consequently, strengthening of private sector financial institutions, financial liberalisation at home and integration into the international financial system, and global value chains became the prescribed policy by influential international organisations such as the World Bank and the IMF, promising accelerated growth (Levine and King, 1993; Levine, 2005). In reply, EEs and developing countries following rich economies have liberalised their financial sectors since the 1990s in the hope that this will spur growth (Rashid, 2013). Towards the end of the 1980s, a fundamental change in monetary policy across G7 countries started to emerge with the Greenspan put, shifting the United States and Japan towards loose monetary policy which subsequently intensified across the G7 with unconventional monetary policy embraced in response to the Global Financial Crisis (GFC). This made the international search for yield by financial investors more pressing, generating a push factor for international financial flows especially into EEs due to their structurally higher interest rates (Bonizzi, 2017).

Against this background, the role of the state can be clearly seen in the active liberalisation reforms that were implemented to ‘open up’ the economies of Colombia and South Africa to global markets. These included significant efforts of financial and trade liberalisation. In South Africa, the impulse for financial liberalisation and deregulation emerged as early as 1978, when a commission led by Gerhard de Kock, Senior Deputy Governor at the South Africa Reserve Bank (SARB) at the time, proposed the deregulation of domestic financial markets and the monetary system, and a roll-back of capital controls. From its inception the South African state had very close links to capitalist elites (Innes, 1984), partly explaining the early embracing of business-friendly reforms such as financial liberalisation without much external pressure through trade agreements or loan conditionality. Equally, policymakers were keen observers of academic and policy debates in rich countries, understanding South Africa as ‘developed’ economy (Keet, 2010). With the transition to democracy, the constitution enshrined the independence of the SARB from government and democratic oversight, 8 cementing the superiority of financial interests over societal goals such as growth and employment creation (Hickel, 2021). This paved the way for inflation targeting, which was introduced in 2000, fostering financialisation. SARB’s open market operations to drain ‘excess’ liquidity in adherence of the target create lucrative financial investment opportunities (Isaacs and Kaltenbrunner, 2018). In parallel, after a turbulent period in the 1980s, capital controls have been gradually removed in South Africa, albeit some oversight remains (IMF, 1997). In Colombia, the financial account has also become progressively more liberalised since the mid-1990s, opening to foreign transactions and portfolio investment, although unremunerated reserve requirements still exist to discourage short-term capital inflows (OECD, 2016). The new constitution of 1991 made Central Bank authority independent of government influence, restricted Central Bank lending to financial institutions and codified the goal of purchasing power stability, giving primacy to the objective of inflation control. The exchange rate regime, which had been a crawling peg since the 1960s, was partly liberalised by adding 15% bands in 1994, and eventually moved to floating in 1999, following pressures from external investors and the IMF amidst the currency crisis of 1999. The Central Bank of Colombia intervenes in foreign exchange markets to contain extreme movements of the Colombian Peso, but otherwise adheres to a standard inflation targeting regime (IMF, 2020). Thus, the combined global pressures of shifting policy and a built-up in international financial capital keen on new and lucrative financial investment translated into financial liberalisation in both economies. In South Africa domestic forces were a major driver, while Colombia experienced comparatively more pressure to open up from outside.

Another key commonality between the two countries is the dominance and concentration of conglomerates and their growing financial activities in domestic productive structure. Since the 20th century, the South African economy was dominated by five big conglomerates, combining mining and financial operations (the so-called mining-finance houses) and becoming more diversified over time (Innes, 1984). With the liberalisation of the country’s economy, conglomerates stepped back from productive long-term investment and manufacturing, as financial operations among South African NFCs have generally become more short-term focused and financially innovative (Karwowski, 2018). The largest among the former South African conglomerates, especially AngloAmerican, have assumed lead positions, while smaller ones have integrated further down, in international value chains. AngloAmerican moved its headquarters and primary listing to London in 1999, effectively becoming part of international productive structures as it diversified its geographical reach, today operating across the globe albeit with a focus on Africa (AngloAmerican, 2022). In Colombia, liberalisation disrupted previously dominant industries associated with import-substitution-industrialisation and coffee production, causing the domestic productive sector to become increasingly organised around large, diversified conglomerates (Misas-Arango, 2019). These groups have varying origins, but all benefitted from the processes of privatisation through acquisition of dominant stakes in key sectors, such as telecommunications, energy, media, infrastructure construction and finance, and acquiring considerable direct influence over policy-making (Rettberg, 2005; Misas-Arango, 2019). In parallel, the mining and extractive sector has become a key target for foreign corporations, often by establishing joint ventures with local actors, such as the state-owned company Ecopetrol. The dominance of the extractive industries in domestic production accelerated financialisation in Colombia and South Africa since mining corporations tend to favour internationalisation of their operations, while also requiring substantial (often foreign) funding. In South Africa, large domestic corporations pushed to move into the international sphere using the means of international stock markets, while in Colombia, dominant domestic and foreign capital established joint ventures, sidestepping those markets.

Similar levels of high concentration can also be seen in the countries’ financial structure. In South Africa, the oligopolistic power of four big banks has been a historical characteristic, further exacerbated by deregulation in the 1980s. Each of today’s big four used to be integrated into a mining-finance house, providing patient capital for productive operations. During the 1990s, conglomerates unbundled: for example, AngloAmerican shed its financial operations which today are part of the First Rand group, one of the big four banks – together with Absa, NedBank, and Liberty Life/Standard Bank – that dominate the domestic financial system. Once set free, these financial service operators were able to grow and increase profitability. In the early 2000s, these four owned three quarters of total banking assets (Falkena et al., 2002), increasing their share to 80% by 2014 (The Banking Association South Africa, 2014). The long-standing dominance of the domestic financial system by the big four banks and their close relationship with state institutions, especially the SARB, explain why foreign banks have not broken into the South African market more substantially. In Colombia, liberalisation and deregulation 9 enabled concentration of financial sector interest in the hands of domestic conglomerates, further exacerbated by foreign capital inflows (Giraldo, 2007: 201). A sizable 15% of FDI during the 1995–2019 period went to the financial sector (Banco Central De la República, 2020). Foreign banks entered the Colombian market in the 1990s, and over time, a few domestic conglomerates emerged as dominant players in the domestic financial markets (Guevara, 2015). Today, the three largest banks own over half of total banking assets (Superintendencia Financiera, 2019). A quarter of total banking assets is held by a single group, Bancolombia, owned in turn by the GEA group, one of the largest diversified conglomerates of the country; the Aval group, a major conglomerate mainly operating in finance, owns the second and fifth largest banks – Banco de Bogotá and Banco de Occidente, while Davivienda, the third largest bank, is owned by the Bolívar group, another financial conglomerate. Similar dominance and concentration exist in the pension fund sector: the two largest pension funds – Protección and Povernír – own three quarters of pension fund assets in Colombia and are owned respectively by the GEA and Aval groups.

Both countries have been subject to cyclical financial inflows, of a similar overall size over the past two decades. As a result, foreign investors have significantly increased their presence, especially in sovereign bond markets. Domestic conglomerates also received significant portfolio and FDI flows. Since the 1990s FDI boomed in Colombia: median net FDI from abroad increased from 0.73% of GDP in 1970–1994 to almost 4% between 1995 and 2019 (World Bank, 2021). Between 1995 and 2019, over 40% of total FDI flowed into oil and mining (Banco Central De la República, 2020), thus further indicating the strong presence of TNCs in these sectors. Foreign ownership of JSE-listed companies was negligible by the late 1980s, growing to 10% of JSE capitalisation by the early 2000 and to 30% a decade later (Mohamed, 2017).

However, the financial and productive structures in the two countries exhibit significant differences, which in turn are reflected in variegated financialisation forms, specifically in the development of capital markets. As discussed, the dominance of the mining conglomerates in South Africa has a long history, which has resulted in their close connections to domestic capital markets reflected in the JSE (Aghion et al., 2006). As the country was re-integrated into the global economy in 1994, large domestic conglomerates shifted their operational focus and stock market listings abroad but retained a presence in the country, for instance, through a secondary listing on the JSE (Chabane et al., 2006). As a result, foreign shareholders have become increasingly influential in the domestic economy, introducing pressures to generate shareholder value and focus on financial measures and profits (Bowman, 2018). Meanwhile the financial sector, now free from direct control of mining conglomerates, diversified, internationalising and moving into the African continent. Old Mutual, founded in 1845 and one of South Africa’s former mining-finance house, illustrates this internationalisation. The mutual insurance company was demutualised in 1999, moving its headquarters to London and listing at the stock exchanges in the United Kingdom, South Africa, Zimbabwe, Malawi, and Namibia. Today, the group has investors from around the globe, while running large operations in 13 African countries and China (Old Mutual, 2021). The shifting of large productive and financial corporations abroad promoted the internationalisation of the Rand as former South African conglomerates meet the need for Rands in their business operations through offshore trading in the currency (Isaacs and Kaltenbrunner, 2018). In Colombia, unlike in South Africa, ownership remains extremely concentrated and much less mediated through the stock exchange 10 with families and syndicates controlling the major conglomerates, which often include financial sector companies and major banks (OECD, 2016). This tight association between conglomerates and the financial sector paradoxically constitutes an obstacle to the rapid development of capital markets, since external financing is rarely required – especially for those conglomerates with access to foreign markets and FDI. The Colombian stock market remains therefore severely underdeveloped: since 2005, despite a mild growth in market capitalisation (from 35% to 41% of GDP), the number of listed companies and stock turnover declined, 11 and there have been only 44 equity offerings in total since 2000 (Pareja Otero, 2019) compared to over 500 in South Africa (PWC, 2019). Furthermore, aside from foreign investors, which are largely driven by global benchmarks, the market is dominated by institutional investors, which are mainly owned by conglomerates, and therefore trade is based on ‘insider’ information (Pedraza, 2018). As a result, there is very little role for dispersed ownership to apply conventional shareholder value pressures. This explains the significantly smaller size of the stock market and non-bank financial institutions in Colombia compared to South Africa.

Another key aspect in terms of variegation is the role industrial relations – and state intervention to mediate them – have had in shaping financialisation. In South Africa, the capital-labour conflict is central to understanding this process. Since mineral prices were fixed globally profits could only be raised by pushing down labour costs, incentivising mining capital to organise and lobby the government for measures that helped generate a domestic proletariat (Innes, 1984). Black trade unions, in turn, played a key part in bringing down the apartheid regime, and union membership remains strong. 12 Financialisation has often been used as policy tool to balance conflicting claims: early attempts to redistribute ownership over South African industry, notably Black Economic Empowerment (BEE), centred on financial markets. Under BEE, access to mining licences and government tenders is dependent on black shareholder involvement. 13 As a result, a very small number of black entrepreneurs, usually with strong personal links to the ANC, benefitted (Chabane et al., 2006). This embracing of financial markets by the ruling ANC party was the result of active campaigning by domestic capital since at least the late 1980s, which presented them as necessary part of the transition to democracy (Michie and Padayachee, 2019). In Colombia, by contrast, the capital-labour conflict is less central to the process of financialisation. The role of organised labour, historically weak, was further weakened by labour reforms and de-industrialisation after the ‘opening’ of the economy. While the new constitution expanded labour and social rights, labour markets were liberalised in terms of both wages and employment stability and welfare reforms established a significant private component of welfare provision (Giraldo, 2007). The welfare system has therefore been reformed towards individualised (and often privatised) provision, favouring the accumulation of wealth within financial markets. So, while in South Africa, financialisation had a concrete impact on a broad share of the population through, for instance (failed), redistribution efforts, and in Colombia, the efforts were much narrower in scope and size. This is reflected in the much larger size of non-bank financial institutions in South Africa, which were key intermediaries of policies such as BEE, while in Colombia, they mainly reflect the growth of a very unequal privatised pension system (Bonizzi et al., 2021). Therefore, financialisation can be characterised as mass-based in South Africa, while it is more elite-based in Colombia (Becker et al., 2010).

Finally, the different evolution of the two countries’ growth models can help explain differences in financialisation, especially when it comes to debt-to-GDP levels. While mineral exports were South Africa’s historical engine of growth, this has more recently shifted towards debt-led consumption. Since its peak in the early 1980s, mineral extraction has seen dramatically declining profits with the brief exception of the boom in the early 2000s. With South Africa’s re-integration in the global economy, large companies have further internationalised, in the attempt to shift the centre of their activity abroad, reducing production operations at home. This led to a decline in mining and manufacturing as an engine of growth towards financial services and domestic consumption. Today the overwhelming majority of South Africa’s GDP is generated through final consumption. Since 2000, the private sector consumed four fifth of the country’s GDP (World Bank, 2021). Significantly, consumption has been fuelled by debt. The large banks could benefit from and further fuel the house price boom in the country which saw real house prices inflate well above the levels in the United Kingdom and United States between 2003 and 2007 (BIS, 2017). The results were high levels of household indebtedness and poor housing affordability (see Table 1), two well-documented symptoms of financialisation. In Colombia, by contrast, the importance of mining exports has increased over time, but with a significant yet volatile role of debt in determining growth. In the 1990s, de-industrialisation led to a decline in exports, while liberalisation contributed to a debt-led spending boom ending in a financial crisis in 1999. From 2003 onwards, thanks to the global commodity price boom, the country experienced a sustained period of economic growth, which led to a trade surplus in goods. The significant FDI and portfolio inflows generated substantial payments to foreigners, particularly in the form of profit payments, forcing the current account into deficit despite a trade surplus, while the currency appreciated. The situation, a so-called ‘financial Dutch disease’, was dominant in Colombia until the collapse of commodity prices in 2015 (Botta et al., 2016). Aggregate demand in Colombia has therefore been closely linked to the dynamics of exports but is not strongly export-led. This produces a form of volatile financialisation: the commodity boom in Colombia in the 2000s resulted in declining corporate and government debt, but in the 1990s and since 2015, private indebtedness increased at a very fast pace. Housing markets and household debt have played instead a less important role, and, despite a steady rise (especially since 2010) remain at lower levels compared to South Africa.

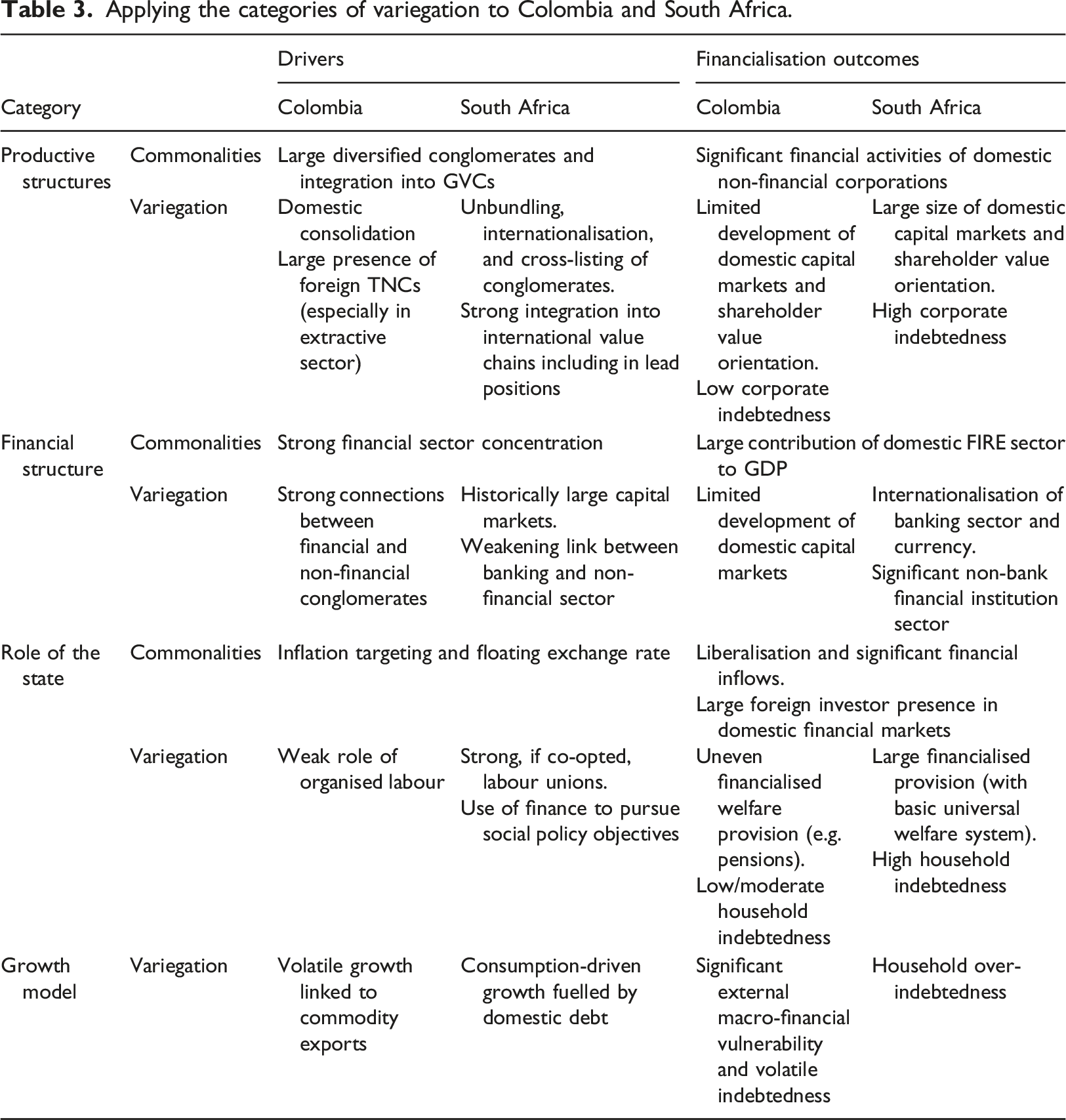

Applying the categories of variegation to Colombia and South Africa.

The powerful South African conglomerates have lobbied for policies that fuelled financialisation, entrenching the phenomenon through their internationalisation and the consequent exposure to shareholder demands (Freund, 2013). This accounts for the size and importance of the Rand internationally and Johannesburg as regional financial hub. The state supported, as part of its agenda to reform the post-apartheid economy, the interests and needs of powerful conglomerates. The resulting policies favoured the financialisation process, such as the growth of a concentrated financial sector and consequently a boom in household credit.

In Colombia, the financialisation process can be related to the power of domestic conglomerates but in a context characterised by more volatile economic and policy environment and a significantly smaller role for capital markets. A series of liberalisation policies in the 1990s reshaped the relations of power, favouring the rise of large, diversified conglomerates, and promoting forms of privatised and financialised welfare. These policies originated in a domestic push to reform the ISI structure but were also validated and reinforced after the currency crisis in 1999 through IMF conditionalities. Additionally, despite the power of domestic conglomerates, Colombia’s economy has exhibited a high dependence on the vagaries of global markets. A commodity export boom since the 2000s favoured a significant influx of foreign capital, particularly towards the extractive sector. Domestic capital markets therefore remained underdeveloped as conglomerates used them sparingly, having secured other sources of domestic and international financing. Instead financialisation grew slowly in various forms of privatised welfare, such as pension funds.

Conclusion

This article set out to systematically identify categories of variegation for financialisation in EEs as a consensus is emerging that there is commonality without convergence across these countries’ material experiences of the phenomenon. We have reviewed the emergent literature on variegated financialisation, identifying often used empirical dimensions. With this literature in mind, we proposed four categories of variegation – productive structures, financial structure, role of the state, and the growth model – which we can map onto these empirical observations. We illustrate how these four categories apply to two case study countries, namely, Colombia and South Africa. While both countries have large financial sectors and experience sizeable cross-border financial flows, the volume of outstanding credit and assets held by specific financial segments as well as the quality of their international financial integration vary widely. South African’s financialisation is strongly market-based, mass-based, and driven by domestic corporations’ internationalisation. Thus, bond markets, domestic pensions funds, and stock market capitalisation are substantially larger here than in Colombia. Financialisation has touched a large share of the population as financial markets and tools have been used for redistributive purposes. The Rand has experienced strong internationalisation over the past two decades since its use is fuelled by the internationalisation of formerly South African conglomerates whose move abroad weakened domestic production. While Colombia possesses smaller capital markets, financialisation processes have been unfolding dynamically but in a less pronounced and more elite-based manner in the country over the past two decades. These different experiences can be mainly explained analysing the influence of dominant corporate forces (productive structures) and financial sector actors (financial structure) lobbying for and taking advantage of liberalisation reforms (role of the state) in the two countries. In the short run, the interaction among these forces manifests itself in the growth model, yielding financialised and unstable paths in both economies.

Hence, the processes underlying these different financialisation outcomes are crucially shaped by local history as well as the constellation of domestical interest groups, the degree of their power and influence, at home and abroad. In many respects, the global drivers behind financialisation present new structural constraints for domestic agents and institutions who in the process of navigating these global structures shape domestic outcomes and in some cases also influence these global drivers themselves. Thus, the interests and agency of EE actors, sometimes overlooked in discussion of subordination and financialisation as a global process, are a crucial factor in explaining financialisation.

Our study is illustrative of the usefulness of our framework for the analysis of variegated financialisation across EEs. In principle, this framework can be modified for other contexts. In advanced economies ‘subordination’ might be less useful to characterise commonalities, but the relation between global and local factors remains crucial to understand financialisation in many rich countries, as studies on ‘extroverted financialisation’ in Europe show (Beck, 2021). Our four categories and related indicators would therefore need to be refined and adapted, but can form the basis for investigation of variegated financialisation more generally.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.