Abstract

This paper contributes to Comparative Political Economy (CPE) by developing an analytical concept of corporate welfare. Corporate welfare—the transfer of public funds and benefits to corporate actors with weak or no conditionality—is a prominent form of state-business relations that CPE scholarship regularly overlooks and misinterprets. Such transfers should be understood as a structural privilege of business in a globalized post-Fordist capitalism, and an increasingly common strategy through which states attempt to steward national economic dynamism within a highly constrained range of policy options. However, without a well-developed concept of corporate welfare—premised upon the key criterion of conditionality—studies that identify a “return” of the state in industrial planning misrepresent these transfers to business as a reassertion of state influence and control, rather than a reflection of state weakness and subordination. The paper provides the analytical building blocks to properly conceptualize transfers to business, works out the core challenges for empirical research, and provides empirical illustrations of this burgeoning phenomenon from the fields of unconventional monetary policy, privatization, and urban political economy.

Keywords

Introduction

Since the Global Financial Crisis (GFC), it has become commonplace to diagnose the end of neoliberalism. Scholars and commentators see historical breaks with the neoliberal paradigm in multiple instances: the recent existential troubles of the liberal international order (Stiglitz, 2019), the global decline of faith in liberal democracy (Beckert, 2020; Peters, 2017), and the extensive public life-support measures for private capital that followed both the GFC and the coronavirus pandemic (Chwieroth and Walter, 2019; Streeck, 2016). Parallel to these claims lie diagnoses concerning the return of state-led forms of capitalist development. Alami and Dixon (2020), Dosi (2016), Wade (2012), and Rodrik (2010), to name a few, document a resurgence of interest in industrial planning among advanced economies, developing countries, and multinational organizations.

In addition to such diagnoses, prominent contributions to Comparative Political Economy (CPE) have recently rediscovered the role of the state and industrial policy in determining growth, developmental, and industrial outcomes (Bohle and Regan, 2021; Iversen and Soskice, 2019; Regan and Brazys, 2017). Despite their merits, we contend that these recent contributions suffer from an unqualified approach to analyzing the design and underlying logic of government transfers to business. In particular, it is difficult to substantiate arguments about state-business relations through evidence about state aid without also problematizing the conditions attached to these transfers (Maggor, 2021; Mazzucato, 2013). That is because unqualified figures about state aid to industry cannot distinguish between a return of dirigisme for green energy, advanced manufacturing, or digital industries, and a condition of state actors deploying public resources to prop up corporate balance sheets.

Public discourse does in fact contain a concept designed to situate public transfers to business within a broader political economy framework—the concept of corporate welfare. Its main problem is that it is notoriously ill-defined and pejoratively connotated. This paper is an attempt to resuscitate the concept, develop it in a more rigorous manner, and lay the analytic groundwork for its use in empirical research. It contends that a more sustained engagement with the concept of corporate welfare within the field of political economy will address the limitations and misrepresentations that stem from unqualified analyses of public transfers to business. In doing so, we provide a twofold contribution to the debate on the mutual power relationship between state and corporate actors (Culpepper, 2015).

First, we argue that the proliferation of unconditional forms of transfers of financial resources from state to business should be perceived as a sign of states’ structural weakness vis-à-vis corporate actors, rather than strength—even if it implies substantial state activity in the economy. In our view, this weakening dates back to the transition from Fordism to the post-Fordist production regime. In that transition, state actors replaced many of the instruments of direct intervention in the economy deployed in the post-war decades with more indirect industrial policy tools (Bulfone, 2022), such as granting largely unconditional investment aid to corporate recipients, in the hope that business prosperity as such would provide for more generalized economic and social prosperity. In this regard, we build on the recent literature that characterizes neoliberalism not as a policy of non-intervention, but as a policy of “active collusion” that emanates from structural state weakness (Berry, 2021; Hathaway, 2020, 325–30).

Second, we provide a conceptually coherent definition of corporate welfare that distinguishes the unconditional transfer of resources from states to large and small, domestic and foreign business actors from all other forms of state involvement in the economy. We contend that this distinction advances the current political economy debate concerning the nature of contemporary state-business power relations. It does so by delineating the boundaries between genuinely independent instances of economic activism by strong states, as opposed to structurally induced programs of financial assistance to segments of capital.

The remainder of the paper is organized as follows. The next section discusses the utility of resurrecting the concept of corporate welfare and integrates our contribution within wider debates on structural power and state-business interactions. The third section develops our definition of corporate welfare by discussing its key element—conditionality—and examines the relationship between corporate welfare and alternative forms of state involvement in the economy. In the fourth section we provide three empirical illustrations of the concept of corporate welfare, seeking to highlight its ubiquity and salience across countries and economic sectors. The conclusion recapitulates the argument and offers brief indications for future research.

Prior art and the need for concept recovery

Though it is commonplace to talk about corporate welfare in public discourse (Ford, 2020; James and MacLellan, 2015; Wilkes, 2015), the term evades conceptual specification and is rarely explored in its theoretical implications. Within public debate, it is commonly used as a pejorative to denote transfers from the public to the corporate sector that strike observers as particularly “undeserving.” Indeed, popular conceptions of corporate welfare have historically been used by left-wing parties and organizations as a means to illustrate how private firms systematically rely on public benefits to survive and enhance profits at the expense of the wider population (Bennett, 2017; Harrington, 1997; Nader, 2000). Perhaps unsurprisingly, these critiques find a mirror image on the political right, as conservatives complain about the rent-seeking of “crony capitalism” and wasteful state intervention under the rubric of corporate welfare (Holcombe, 2013).

Putting aside the charged contention of political malfeasance, the conceptual (and empirical) reality highlighted by both sides is that the state and private corporations are institutionally compelled into close coordination with one another as a functional means to accomplish the twin goals of economic growth and continued accumulation. This is, of course, a foundational insight within political science (e.g., Culpepper, 2015; Lindblom, 1982; Polanyi, [1944], 2001) as well as in anthropology and sociology (e.g., Polanyi, [1944], Streeck, 2014)—yet it is also one that usually lacks specificity given the tendency to pitch this analysis at a high level of abstraction (e.g., Block 1977; Cox 1987). This is a key reason why, as a discipline, political economy is perfectly situated to advance a meaningful exploration of corporate welfare and use it to investigate the character and regular interactions between political (state) and economic (business) elites.

Crucially, the issue of specifying and elaborating upon the variety of business-state relations is of particular relevance in the context of contemporary events such as the 2007–08 financial crash, the populist backlash against austerity and liberalized globalization, and rising inequality (Piketty, 2020; Streeck, 2016). Such developments have instigated a flood of academic investigations focused on economic elites (Davis and Williams, 2017; Savage and Williams, 2008), the structural power of business (Bell and Hindmoor, 2015; Culpepper, 2015; Woll, 2016), economic stagnation in advanced democracies (Storm, 2017), the hidden development capacities of the state (Block 2008; Kattel and Mazzucato, 2018), and the idiosyncratic strategies adopted by powerful social groups to promote economic dynamism (Baccaro and Pontusson, 2016; Iversen and Soskice, 2019). We consider the study of corporate welfare to be a unique angle into such debates, and an empirical perspective that manifests right at the intersection of these inquiries.

In particular, we see our present contribution as both complementary to and critical of these debates in political economy. The paper is complementary in that it fosters awareness of the ubiquity and proliferation of corporate welfare programs and illustrates how such programs endure as a primary mechanism for (elite) business and state actors to realize shared objectives (Molotch, 1976). The paper is critical, however, in that it explicitly foregrounds questions of power and democracy, rather than just matters of economic allocation and technocratic management. To the extent that corporate welfare programs are discussed or implicitly recognized, most of the aforementioned literatures interpret the practice of state transfers as relatively unproblematic in principle, and even desirable to the extent that it fosters further growth (Iversen and Soskice, 2019). The question of cui bono is one that is too often elided when the issue of state transfers, for the ostensible purpose of “economic development,” is broached by analysts. This is likely due to a concern with being associated with either a left or right normative and ideological critique. However, the cost of avoiding this question is the production of a distinctly sanitized depiction of public policy-making and social power relations.

Toward a restrictive definition of corporate welfare

While a range of authors analyze the multiple existing forms of state aid, Kevin Farnsworth has done the most work in advancing a robust concept of corporate welfare. 1 We share Farnsworth’s conviction that, given corporate welfare’s particular ubiquity, it is surprisingly undertheorized in the present literature. Moreover, we share in the desire to bring a wider swath of corporate state aid programs under a unified conceptual banner. This includes phenomena as diverse as state contracts, tax breaks, abatements and deferrals, loan guarantees, public grants and funding supports, cash subsidies, bailout programs, discount schemes, debt write-offs, public-private partnerships, and a whole host of other monetary or in-kind assistance to businesses.

However, when defining instances of corporate welfare, we distinguish our contribution in one important way from Farnsworth. In his primary text on the issue, Farnsworth consciously opts for an expansive definition of corporate welfare, stating that it is constituted simply as all “state provision that functions to meet some of the fundamental and supplementary needs of business and protect against various market-based risks.” Based upon this conception, Farnsworth indicates that, for example, Denmark commits more expenditure to business subsidies than it does to its defense, police, housing, and community programs combined. Moreover, similar commitments are common across the advanced democracies with approximately half of all governments annual spending going toward the purpose of “ensur[ing] that business can do business” (Farnsworth, 2012, 2–5).

Nevertheless, we argue that there is a fundamental political economy reason to adopt a more restrictive definition, premised upon the existence (or not) of conditionality—that is to say, whether or not states demand that firms behave in a certain manner in order to qualify for resource transfers. When they do, we contend that this should not be considered an instance of corporate welfare, given that states are able to impose their own logic of action in promoting economic growth. Such coercion can justifiably be considered a form of activism that signifies state strength, which is rooted in the capacity to align business behavior with its own developmental goals. By contrast, when state transfers are offered without conditions attached, this should be considered a manifestation of corporate welfare, whereby state weakness is reflected in the need to induce business to carry out its normal functions, but without controlling or directing the character of investment decisions.

Narrowing the criteria by which transfers should be designated as corporate welfare or not allows us to better specify the nature of state-business power relations at the present historical juncture. Farnsworth overlooks this distinction when he advances the claim that states have always played an active role in promoting capitalist markets through their different stages of development. But while it is true that states always play a participatory role, the extent and level of control over this participation is incredibly varied, and that contingent variation gives us crucial insights into the character of state-business power imbalances at any given historical moment (Cox, 1987). Thus, while Farnsworth correctly points out that globalization’s second wave since the 1980s has tilted the balance of power between states and business in favor of the latter, the focus on all-encompassing figures for corporate welfare makes it difficult to document precisely how state-business relations have changed in practice. Hence, we suggest shifting the focus away from comparisons of blanket transfers to business, and toward a more thoroughgoing analysis of the kinds of conditionalities involved.

Prominent scholars within the field of CPE have recently highlighted the importance of activist industrial policy in determining growth and development outcomes (Bohle and Regan, 2021; Iversen and Soskice, 2019; Regan and Brazys, 2017). These works share the underlying assumption that state activism should be perceived as a sign of state strength vis-a-vis corporate actors. According to Iversen and Soskice (2019), the “advanced capitalist democratic state” has actually become stronger with the transition to the knowledge economy. This is due to the fact that corporations depend upon the scarce skills of highly educated workforces in productive regional clusters. This dependence, in turn, makes investments immobile, and thus weakens the bargaining position of corporations vis-a-vis state actors. However, this claim is difficult to reconcile with the generous subsidies and tax benefits municipal authorities (especially in booming cities like New York or London) routinely award to corporate actors. 2 Although Iversen and Soskice do appear to recognize the importance of conditionality, they only vaguely refer to the need for states to impose product market competitiveness upon recalcitrant business actors.

Bohle and Regan (2021) have a more balanced view of the power relationship between the state and large corporate interests. Drawing on Culpepper (2015), they argue that the two are tied by a relationship of mutual dependence. On the one hand, in their interactions with state actors, large corporations can leverage their size, the availability of multiple investment options, and the promise to create relatively good employment opportunities for the local population. On the other hand, large corporations are weakened by the fact that, once they pick an investment location, these investments create sunk costs, thereby making businesses less mobile. Furthermore, according to Bohle and Regan, with the need to be globally competitive, MNEs depend upon state actors to provide them with a “competitive edge” (p. 81) in the form of tax benefits, subsidies, and other forms of financial transfer. As Bohle and Regan put it, “the mutual dependency that exists between the interests of large multinationals and the state is often considered a form of structural power, with the state in the inferior position. But this underestimates the extent to which … multinationals depend on governments to enact … favorable market reforms and grant [...] generous incentives” (p.99).

While we are sympathetic to this view of mutual dependence, we reject the notion that any and all transfers of financial resources from the state to corporate actors is a sign of state strength, as it may just as easily be a sign of state weakness and a direct consequence of the intensifying struggle to attract and retain FDI. Instead, more attention should be paid to instances in which state actors demonstrate their relative strength vis-a-vis corporate actors by making access to financial support contingent upon clear and strong conditionality requirements.

A renewed focus on conditionality would also open interesting pathways for comparative research trying to identify the coalitional (Maggor, 2021), power-based (Bulfone, 2020), or institutional factors that lead some countries, regions, or cities to establish and enforce stronger conditionality than others. This research agenda would build on Culpepper’s intuition that structural power is indeed a mutual relationship between corporate and state actors in which some corporate actors (but not others) are strengthened vis-a-vis some state actors (but not others) (Culpepper, 2015, 391). This comparative perspective also opens potentially fruitful avenues for a dialogue between mainstream CPE and critical political economy perspectives. While critical political economy highlights a common tendency toward forms of state intervention in the economy that are inherently favorable to business (Berry, 2021; Jessop, 2002), CPE scholars can detect variation in the extent of this subservience.

Corporate welfare as a form of structural power

Corporate welfare programs are, at their conceptual root, a particular manifestation of structural power (Culpepper, 2015; Farnsworth, 2012, 28; Hacker and Pierson, 2002). That is to say, they are a form of power derived not from the strategic or intentional activities of business, but rather through the operation of (global) market pressures that compel states into providing policies that privilege the interests of business. As such, our emphasis is not so much on the active engagement of corporations within policymaking, but rather on the strategic adaptation of state actors who face these geographic constraints and must nevertheless act as stewards of national growth.

The structural root of these programs might not be obvious at first glance, and there are several ways that one could construe corporate welfare as being a product of instrumental (i.e., strategic) business activity. For instance, specific firms can and do lobby for particular types of aid. Moreover, the precise structures and boundaries of this aid often involve the active policy input of corporations. Nevertheless, from the strategic perspective of governments and public officials, the underlying impetus for providing these forms of state aid in the first place is the increasing competitive pressure to attract or retain global business investments (Genschel and Schwarz, 2011; Jessop, 2002; Reurink and Garcia-Bernardo, 2021; Bulfone, 2022), and one simple way of achieving this is through direct handouts in order to incentivize investment within a specific territory. 3 Hence, while it might appear that the state is taking a proactive and commanding role in economic development by providing multiple forms of transfers (with colorful labels such as green growth, Industrie 4.0, or advanced manufacturing), we see the proliferation of such measures as a product of heightened market constraints and a growing subservience to the power and transnational scale of large corporations.

Recent developments within the literature on corporate structural power and state-business relations integrate with this understanding of the role of corporate welfare in national policy-making. Two analytic perspectives are especially related: infrastructural power and institutional power.

First, we consider the proliferation of corporate welfare as resulting from the infrastructural power dependence of the state on capital. According to Braun, business and state actors are increasingly involved in a “hybrid public-private partnership” with the key objective of buttressing economic growth (Braun and Hübner, 2018, 396). The direction of power runs from business to state, rather than vice-versa, by virtue of the governance method that is pursued in trying to achieve this objective: namely, a “market-based form of state agency” (Braun and Hübner, 2018, 400). As it relates to corporate welfare programs, state officials interpret themselves within a strategically constrained terrain of global competition, and thus (non-conditional) public transfers to corporations offer them a straightforward and powerful way of tweaking global-oriented market incentives and inducements in their favor. As noted previously, this is typically portrayed as an intelligent form of statecraft and a forceful “return” of state activism (Iversen and Soskice, 2019). In fact, however, the steering capacity of the state is reduced to an indirect reliance on private actors for the delivery of public goods and services that were previously under its direct control or influence. As examined below, the case studies of ECB monetary interventions, public service industry privatizations, and regional investment incentives serve as sharp illustrations of this transformed dynamic and the material benefits that flow to corporate actors as a result.

Second, corporate welfare, through its rapid spread across various domains of policy-making, is taking on the character of an institutionalized policy tool, thus becoming an increasingly entrenched source of business power (Busemeyer and Thelen, 2020). This is because corporate welfare transfers typically act as an incentive scheme whereby the state effectively “delegates” the provision of public good functions to private business actors. This can be seen not only in the obvious domain of public service privatizations, but also in state procurement contracts and public-private partnership agreements across social policy areas such as health, education, and welfare, where states “de-risk,” rather than direct, private investments (e.g., Busemeyer and Thelen, 2020, 458–73; Farnsworth, 2012). Daniela Gabor (2021) has also analyzed this phenomenon of private delegation norms and the rise of the “de-risking state.” By shielding private investors from risks, public actors in poor as well as rich countries increasingly try to mobilize private financial pools for development, infrastructure, and greening projects.

As noted by Busemeyer and Thelen, the over-time proliferation of corporate actors within these spheres of policy provision generates several feedback mechanisms that further entrench a power asymmetry between business and state actors. For example, states’ administrative and organizational systems begin to decay and drop out of use, making it more difficult and impractical for the state to genuinely “return” to service provision. In addition, the embedding of new collaborative relationships and private–public working arrangements will increase the political and economic transactions costs associated with efforts to change course. As such, the longer a corporate welfare program is maintained, the greater a state’s dependence on corporate provision is likely to be, and the less likely it is that a state will risk a disruption to key services (Busemeyer and Thelen, 2020, 455–57).

Both of these perspectives (infrastructural and institutional power) speak directly to the character of state-business relations when it comes to corporate welfare transfers, and are, to a greater or lesser extent, rooted in the state’s strategic—or perhaps pragmatic—response to an increase in the wider structural power of business in the post-Fordist era. As a means to facilitate the further empirical investigation of corporate welfare, the following section fleshes out the logic for proceeding with a more restrictive definition of the concept.

The centrality of conditionality

To address the difficulties in gathering reliable data on corporate welfare, and the inherent ambiguity of the concept, we develop here a “restrictive” definition of the phenomenon to include only transfers coming with no strings attached, or with weak conditionality.

Conditionality is key to distinguishing different types of transfers as it explicitly hints at a divergence in public and business interests, and the ways in which public transfers attempt to “carry” public interests against corporate inclinations (Maggor, 2021; Mazzucato, 2013). While it is straightforward to argue that instances in which corporate actors get a “free lunch” fall within our definition of corporate welfare, state actors often find it difficult to enforce previously agreed-upon conditions. When conditionality exists, it is therefore necessary to distinguish between its two dimensions: the formal content of the agreement and the concrete impact it has on the behavior of corporate actors.

For instance, public competitions for location decisions by Tesla and Amazon in the US (Goodman and Weise, 2019; Lecher, 2016), come with formal conditionalities for future funds invested, jobs created, and taxes paid. However, concluding on the basis of such formalized figures that these incentive schemes are particularly tough in international comparison would probably be wrong, as they are typically subject to ongoing renegotiation or dilution. It is therefore crucial to understand whether conditions effectively lead to a change in corporate behavior, thereby representing “costs” for the corporate beneficiaries agreeing to them. While gathering comparative data on formal conditionality is easier, the concrete impact of conditionality on business actors is more difficult to grasp.

While conditionality is regrettably rarely a concern within CPE scholarship, the topic was at the center of a stimulating academic debate among scholars focusing on the political economy of development. The work of Alice Amsden on performance standards provides particularly important insights in this regard (Amsden, 2001; Amsden and Hikino, 2000). Amsden argues that the successful industrial upgrading in countries like South Korea, Malaysia, or China depends on the capacity by domestic state elites to create control mechanisms to discipline corporate behavior. These control mechanisms revolve around the idea that subsidies or other forms of monetary advantages to corporate recipients need to be subject to monitorable, redistributive, and results-oriented performance standards (Amsden, 2001, 8). If corporate recipients failed to meet these performance standards, state actors would withdraw their financial support, and eventually take more radical measures like ownership repossessions. Performance standards could relate to a wide variety of goals including firm-level managerial practices, sectoral industrial policy goals, or broader national policy goals. Concretely, corporate recipients could be asked to meet “export targets, local content requirements, debt-equity ratio ceilings, national ownership floors, operating scale minima, investment time-table obligations, regional location criteria, and eventually product quality specifications and environmental rules” (Amsden, 2001, 25).

When performance standards were not established, or enforced, state officials ended up being captured by corporate interests. This in turn led to a massive transfer of financial resources from the public to the private sphere with negligible developmental and industrial outcomes (Chibber, 2009). We urge the CPE literature to share this concern for conditionality, as there is no reason to believe that it is only state actors in developing countries that face the risk of a socialization of losses and a privatization of risks when engaging in industrial or innovation policies (Block, 2008; Maggor, 2021; Mazzucato, 2013).

When approaching the issue of conditionality, CPE scholarship should first draw on the comprehensive overview of the goals and policy instruments deployed to enforce performance standards as identified in the literature on developmental regimes. The concrete impact of conditionality can then be explored by pursuing two empirical strategies, either together or separately. Large-n studies could focus on specific forms of state support to business actors, for example, banking bailouts or export grants, and gather comparable data on the presence and strictness of certain conditionality clauses. Existing literature usually focuses on comparisons of the presence or absence of specific clauses, such as equity requirements or dividend restrictions in bank bailouts (Woll, 2014). However, a major problem of studying conditionality is that the details of contractual arrangements are often agreed behind closed doors by regulators, technocrats, and other elite insiders. In fact, robust oversight mechanisms are likely to generate widespread discussion about the unusually generous conditions of these programs and their targeting of already hugely profitable corporations. Hence, there are strong incentives for governments to keep corporate welfare programs within the realm of “quiet politics” (Culpepper, 2010), making them difficult to qualify in legal terms. A creative strategy used by Weber and Schmitz is to use approval times by the European Commission as a proxy to infer the generosity of conditions in bank bailout packages during the Great Financial Crisis (Weber and Schmitz, 2011). While we have doubts about their assumption that the European Commission primarily polices “favorable” terms for business—rather than state influence on business, for example—the underlying logic of searching for “revealed conditionality” in legal experts’ assessments is highly promising.

Quantitative approaches can and should be complemented with qualitative in-depth studies covering specific instances of state support to large corporate actors that are relevant from an analytical point of view due to the large size of the disbursement or the strategic nature of the companies involved (Amsden, 2001). For instance, qualitative analyses of the annual reports of large corporate recipients could help in understanding whether the conditions agreed upon to obtain state resources effectively impacted corporate strategies. Connecting to the extensive literature on aid to industry in Urban Studies (Molotch, 1976), qualitative studies of transfers to business also help to shed light on the social coalitions that drive corporate welfare. Understanding the socio-political dynamics that motivate public transfers to business helps to specify the political economic character of corporate welfare.

Conceptual delimitation

While our restrictive definition is likely to produce a more conservative estimate of the “size” of corporate welfare, this is appropriate as a means to draw the boundaries between corporate welfare and other similar, but qualitatively different, transfers of public resources to private actors. As a matter of fact, state actors frequently rely on transfers to small and large, domestic and foreign business when conducting industrial policy, welfare policy, labor market policy, regional policy, or education policy. However, only when these transfers are unconditional do they fall within our category of corporate welfare. In this respect, corporate welfare does not constitute a separate sphere of state intervention that is different in nature from industrial or structural policy. Instead, state actors are increasingly conducting industrial or other structural policies through corporate welfare measures. To clarify this idea, we illustrate the relationship between corporate welfare and the form of state intervention that is, by its nature, the most conceptually proximate: industrial policy.

When studying industrial policy, scholars often rely on the distinction between vertical and horizontal measures. While vertical industrial policy aims at supporting a specific firm or sector by “picking winners” or “helping losers,” horizontal measures intervene on framework conditions that should, in principle, benefit all business actors. Examples of business-friendly horizontal interventions include investment in R&D and infrastructure, support to SMEs, or the deregulation of labor and product markets (Warwick, 2013).

At first glance, one might think that corporate welfare measures are a subset of vertical industrial policy benefiting selected corporate recipients. However, the distinction between vertical and horizontal measures provides limited analytical leverage for the study of corporate welfare. In fact, a principally horizontal tax exemption benefiting a set of companies irrespective of their sector of activity and coming with no strings attached would qualify as corporate welfare. On the other hand, not all vertical industrial policies necessarily fall within our definition of corporate welfare. For instance, corporate bailouts in which, in exchange for financial support, the state acquires a stake in a troubled credit institution to influence corporate policy, like the US government did in the first Chrysler bailout, would fall outside our conceptualization of corporate welfare. Hence, horizontal measures can sometimes signal a weakening of state actors’ control, while vertical measures can signal a strengthening, contingent on conditionality.

Corporate welfare should therefore be seen as a particular type (either vertical or horizontal) of industrial policy that is proliferating as a result of the structural power imbalance between state actors and corporate recipients (Bulfone, 2022). For this reason, we encourage industrial policy scholars observing a return of state activism to reserve the distinction between vertical and horizontal interventions for specific research questions, focusing instead on the content and impact of the conditionality attached to industrial policy measures (Maggor, 2021).

Empirical illustrations

In this section, we provide selected empirical illustrations of the ubiquity and form of corporate welfare measures. The vignettes cover different policy domains—monetary policy, industrial policy, and urban development—identifying state transfers to business actors that share the core features of our concept: namely, state transfer programs that are designed with weak or no conditionality. Taken together, the vignettes illustrate how corporate welfare is widespread across nations and economic sectors.

While some of the examples discussed are strikingly one-sided in favor of business, most take the form of state actors unconditionally benefitting business in order to achieve public policy goals. As such, our vignettes are intended more as a means to exemplify a style of public policy, rather than simply indicating net-benefits to business.

ECB monetary policy interventions

Monetary interventions have emerged as the most important policy tool for managing the eurozone’s persistent financial turmoil and sluggish economic performance over the last 15 years. These measures involve both conventional and (at the Zero Lower Bound) unconventional policy measures—in particular, the mass purchasing of government and private sector securities, including mortgage-backed securities and corporate bonds. For the ECB, this entailed the controversial move into official Quantitative Easing (QE) in March 2015—although, in the preceding years, it consistently deployed Long-Term Refinancing Operations (LTROs). Offering ultra-low-cost loans to private financial firms, these latter operations were effectively a “disguised” form of QE, masked by technical modifications to avoid unwanted political and legal controversy (Pisani-Ferry and Wolff, 2012).

The reasoning behind such unprecedented action is explicitly based upon a trickle-down/structural dependence logic—both the typical motivator, and root justification, for corporate welfare. The policy claim by central bankers is simple: in the absence of ECB largesse and the prevalence of scarcer credit, there will be slower economic growth, more failing companies, higher unemployment, reduced pension values, and, hence, a corresponding need for greater state retrenchment. Whatever the truth of this counterfactual is, however, the policy raises serious questions about accountability, transparency, legitimacy, and above all power relations and democracy (Braun, 2017). To this end, the rest of this section outlines how ECB interventions are consistently advanced on unconditional grounds and illustrates how the bias inherent to these transfers is reflective of the state’s growing structural weakness vis-à-vis globally operative financial firms.

From the very beginning of the financial crisis, the ECB overwhelmingly prioritized interventions with no strings attached. After the global credit crunch in late 2007, an almost unlimited supply of money was made available to the banking system without any compulsion to put that money to productive use through, for example, greening mandates, small business lending, or facilitating easier access to mortgages. In this manner, central bank outlays were extended on the basis of inducing key financial concerns to carry out their normal lending functions but stopped short of using the coercive capacity of the state to enforce this outcome.

More specifically, the ECB’s early interbank money market interventions offered unlimited liquidity to counterparties (“fixed rate full allotment”) along with extended maturities and an expansion of eligible collateral (Lenza et al., 2010). While this was certainly effective in unfreezing bank-to-bank credit markets, it paradoxically reduced the ability of the ECB to appropriately fine-tune the amount of liquidity generated within the eurozone and diminished its capacity to influence banks’ liquidity allocation preferences (Kaminska, 2011). Contrary, then, to what some might interpret as the powerful reassertion of state power, this intervention is more adequately conceived of as the deliberate relinquishment of state capacities, in a desperate bid to stave off panic within private financial markets.

Perhaps the clearest manifestation of unconditional corporate welfare was the two rounds of 3-year LTROs in 2011 and 2012. These operations provided over 1 trillion euros in liquidity (9% of eurozone GDP) to European banks at just 1% interest and, again, lower collateral requirements (Fontan, 2018, 175). From the perspective of banks, however, those generous terms did not necessarily outweigh the risk premium involved in passing on credit to highly indebted businesses and consumers. Thus, in the context of precarious macroeconomic conditions and the distinct threat of a euro area breakup, these loans were largely diverted to alternative investment purposes.

The most controversial alternative was a profitable eurozone “carry trade” involving the reinvestment of central bank loans into sovereign bonds, which offered a significantly higher rate of return. Hence, banks could recycle a 1% ECB-derived loan into, say, a 5% loan to peripheral states such as Italy, and pocket a lucrative 4% interest in the process. Such transactions not only underwrote easy profits for bank shareholders, but also allowed banks to reduce their capital requirements (due to the safety status of sovereign bonds) under new Basel rules (Thompson and Jenkins, 2013). Moreover, relaxed collateral requirements allowed lenders to utilize their most risky balance sheet assets—for example, corporate bonds, loans to faltering SMEs—as a means to access easy credit. Overall, then, these ECB interventions effectively functioned to shield financial institutions from past bad decisions, while removing much of the risk from new trading opportunities.

The poor revival of credit growth stemming from these policies put considerable pressure on the ECB to eventually pilot new “targeted” LTROs—in June 2014, March 2016, and March 2019. While still offering ultra-low interest rate loans, participants were this time compelled to pass on a certain proportion of those loans to non-financial productive sectors of the economy (though excluding mortgages) (Thompson and Atkins, 2014). As such, these latter ECB interventions appeared to signal a change in central bank policy with respect to conditionality. Two considerations, however, undermine that conclusion.

First, due to the extremely weak take-up of these loans (Hale and Jones, 2015), the ECB gradually loosened their criteria in order to increase the auction participation of banks and make the scheme viable. In early 2016, for instance, the ECB withdrew their stipulation that previously acquired funds must be returned if they had not been used for lending to the real economy (Fontan, 2018, 175–76). Unsurprisingly, then, while credit transmission to productive sectors continued to stagnate, banks selectively engaged with these operations for their own purposes.

Second, due to the eurozone’s persistent deflationary spiral, in 2015 the ECB’s flagship policy intervention moved decisively away from LTROs and into outright QE: a unilateral policy initiative explicitly designed with no strings attached and, through the propping up of real estate and stock market values, offering disproportionate benefits to asset rich financial institutions. 4

The logic of maintaining unconditional state transfers is nowhere more apparent than in the ECB’s unwillingness to effectively tackle the Too Big to Fail (TBTF) dilemma. This is because the imposition of mandatory obligations is perceived by central bankers as making systemically important banking firms less attractive to financial markets/investors and, thus, would only serve to undermine the wider policy goal of economic recovery and positive trickle-down effects that (putatively) result from implicit state subsidies. Moreover, there is a persistent fear on the part of European policymakers that burdensome regulatory demands (especially those that might restrict the activities of their national banking “champions”) is counterproductive to global competitiveness. This is a prime example of how banking “structural power” (Massoc, 2020) generates the economic conditions and policy incentives for corporate welfare provision. It is also important to recognize that this is not simply a function of “emergency” transfers required in the midst of crisis firefighting; the TBTF dilemma and its implications for state-business (state-finance) relations is one that long precedes the crisis period of 2008–2013 and persists to the present day.

According to the IMF’s (2014) Financial Stability Report, banking concentration increased within most member states during the post crisis era, with implicit public subsidies for banks being “much higher than before the crisis for [the] euro area”—ranging anywhere between 90 to 300 billion dollars per year (International Monetary Fund, 2014, 104–05, 14). A recent analysis (Ioannou et al., 2019) shows how this problem had not been addressed by 2017—at least 5 years after both the peak of the crisis and the launch of Banking Union initiatives. Over the course of a decade, the largest continental European banks—excluding Swiss banks—declined by only 10% (from 125% to 115%) in size since 2007, measured as a proportion of domestic GDP (Ioannou et al., 2019, 362). This is mirrored in the varying size of individual banks (measured by assets) over the same time-period. Hence, while firms such as Deutsche Bank, ING, and UniCredit witnessed a moderate decline, this was counteracted by increases in the asset size of other major players such as BNP Paribas, Société General, Credit Agricole, BPCE, Santander, and Nordea (Ioannou et al., 2019, 360–62).

Undoubtedly, the causal drivers of Europe’s persistent TBTF dilemma are manifold and much of the blame resides with national governments. Nevertheless, ECB policy also played a pivotal role in these developments, and it is difficult to identify an actor with a comparable influence on this matter across multiple policy measures.

As noted by several critics, the practically unlimited financing offered to banks through money market interventions, LTROs, and various forms of asset purchases, have functioned to prop up oversized and overleveraged firms. By flooding the market with liquidity, many of the major banks were not only protected from potential default (and market contagion) but could continually postpone the process of building up their own capital reserves and, over a prolonged period of time, gradually restructure non-performing loans. As pointed out in a recent review of QE by the Directorate-General for Internal Policies, the ECB’s ostensible tactic of “buying time” ultimately led to the “zombification” of uncompetitive banking outlets and the subsequent poor allocation of credit (Directorate-General for Internal Policies, 2017). This perspective resonates with the analysis of those from the political right who argue that corporate welfare interventions usually serve to delay much needed reforms and protect inefficient firms.

Ironically, this is precisely the reasoning advanced by the ECB when it came to the question of structural reforms within periphery member states. Leveraging identical “moral hazard” arguments, the ECB argued throughout various peaks of the crisis that unqualified central bank interventions would only facilitate government backsliding on reform commitments and delay the implementation of tough, but necessary, austerity choices (De Grauwe, 2013). However, this position is entirely at odds with its proactive and unconditional stance toward the banking system, and that discrepancy, as pointed out by Fontan, allows one to “define the scope of [the ECB’s] political choices … beyond economic and legal constraints” (Fontan, 2018, 163).

ECB policy toward Greece and Ireland illustrates the political nature of the ECB’s choice. In both countries, senior ECB figures pressured governments to forego imposing bondholder losses for fear that any default/restructuring would bring major banks from the core—in particular, German and French banks—to the brink of collapse. In Ireland, this came in the form of hostile communications between successive Irish finance ministers and Jean-Claude Trichet, as well as implicit blackmail with regards to the provision of Emergency Liquidity Assistance (Kalaitzake, 2018).

Within Greece, the ECB was the leading voice in bailout negotiations arguing against any form of debt write-down. As a result, between 2009 and 2012, approximately 100 billion euros of private banking debt migrated onto public balance sheets as maturing bonds were paid back in full, up front, and on time. Indeed, a considerable portion of this migration was also facilitated through the ECB’s emergency purchases of government debt on secondary markets (Kalaitzake, 2017). A similar prioritization of systemically important banks can be seen in relation to the ECB’s “strategic” involvement with the financial troubles of Italy and Spain (Henning, 2016).

Finally, several other ECB policy interventions indicate that protecting systemically important financial firms has been the bank’s primary focus. First, the ECB (in conjunction with the European Banking Authority) continued the practice of crafting extremely lax stress tests for major European banks. This was demonstrated most clearly by the dubious 2014 EU-wide financial assessment that artificially inflated bank capital levels, underplayed the importance of leverage ratios, and dismissed the credible scenario of eurozone deflation (Goldstein, 2014). Second, the ECB made a range of interventions in the area of financial regulation that corresponded precisely with the policy preferences of major banking firms. This included supporting delays for banks in meeting the Basel III provisions, along with defending the practice of internal risk weight modelling in international negotiations—effectively allowing Europe’s largest banks (who disproportionately use those models) greater flexibility over their capital reserve requirement levels (Bowman, 2017). Notably, this went against the objectives of US regulators who were willing to clamp down on a “self-regulatory” practice that was widely recognized as a contributor to dangerous overleveraging in the pre-crisis period. Nevertheless, given the competitive disadvantage faced by Europe’s beleaguered megabanks, the ECB acted to blunt those proposals globally and embarked upon their own regional review of risk modelling with a significantly extended (i.e., generous) timeline (Noonan, 2015).

In sum, the ECB has consistently taken action over the last 15 years to offer unconditional support to European financial firms and, in particular, TBTF banks upon which the region is structurally dependent for credit provision. Such interventions effectively amount to elaborate forms of state transfer that are, by dint of the ECB’s technocratic independence, substantially shielded from political contestation.

The marketization of public service industries in the European Union

The marketization of public service industries like telecommunications, electricity, oil production, and transportation provides a unique angle to observe the causal link between the retreat of the state from economic activity that followed the transition to the post-Fordist era and the diffusion of corporate welfare measures. In the post-war period, network industries across the EU were organized around monopolist providers. Depending on the sector of activity or country of provenience, these providers could either be state-controlled public corporations or departmental agencies of public administration.

Since the 1980s, the global diffusion of the regulatory state paradigm, coupled with the impact of a series of sectoral EU Directives, led to a profound restructuring of network industries (Majone, 1997). State-owned monopolists were first transformed into private law corporations and later sold to private investors. However, these privatized entities still provide services considered strategic for national security and economic prosperity. Since most governments across Europe deem it vital to have at least one strong domestic company in each of these sectors, they engage in industrial policy efforts to support them. These efforts typically involve measures that fall outside the scope of our definition of corporate welfare, such as the acquisition of stakes in strategic companies, or the use of golden share powers to influence managerial strategies (Bulfone, 2019, 2020). At the same time, however, governments also support domestic companies by awarding them unconditional subsidies or tax exemptions.

Among network industries, telecommunications stands out both for the important role historically played by the state and for the extent of its retreat. Until the late 1980s, communications services were provided by state-owned Postal, Telephone and Telegraph (PTT) monopolists (Bauer, 2010). PTTs were departmental agencies, part of the public administration whose employees had civil servant status (Clifton et al., 2011; Thatcher, 2007). Since the late 1980s, the PTT model was progressively abandoned as a result of the combined impact of international competition and of a series of EU sectoral Directives.

The restructuring of the telecommunications sector proceeded in two steps. First, PTTs were transformed into state-owned private law joint stock companies, with independent managers and own assets and liabilities (formal privatization or corporatization), then, their shares were sold, all or in part, to private investors (material privatization) (Obinger et al., 2016; Son and Zohlnhöfer, 2019). By the late 1990s, all EU-15 member states had transformed PTTs into private law companies, and by 2008 private investors held an absolute majority of the stakes in ten of the fifteen telecommunications incumbents (Bauer, 2010, 6). Privatization came hand in glove with market openings, leading to a wave of cross-border merger and acquisitions across the EU.

EU member states actively supported the foreign expansion of domestic incumbents (Bulfone, 2019, 2020; Clifton et al., 2010; Colli et al., 2014). Subsidies, tax exemptions, and other corporate welfare measures played a decisive role in this effort. For instance, in the early 2000s the French government offered France Telecom, which was at the time in a dire financial situation due to a misguided campaign of foreign expansion, a credit line in the form of a shareholder contract worth 9 billion euros at very favorable conditions (Colli et al., 2014).

Similarly, in 2002 the Spanish government passed a provision allowing for the amortization of the financial goodwill resulting from the acquisition by corporations established in Spain of 5% or more of the shares in a foreign company. 5 The fully privatized telecommunications incumbent Telefonica was among the main beneficiaries of the measure, saving over 40 million euros per year in taxes (El Pais, 2014). Other corporate recipients include global multinationals like the electricity producer Iberdrola and the bank Banco Santander. In 2018 the European Court of Justice found the goodwill amortization scheme to be incompatible with internal market rules due to its selective nature (Ernst and Young, 2018).

The licensing process that followed market liberalization gave EU governments another opportunity to favor domestic incumbents. In fact, member states typically opened their domestic market by awarding a limited number of licenses to provide telecommunications services on the national territory. While privatized incumbents were awarded the license for free, or at a discounted rate, their competitors had to participate in onerous auctions (Sancho, 2000).

Similar dynamics of state retreat followed by the proliferation of unconditional corporate welfare deals in favor of large corporate recipients characterize the electricity sector. For instance, it is customary for governments to award domestic electricity producers generous subsidies to pay back infrastructural investments that had become redundant after opening the domestic market to competition (the so-called stranded costs). The awarding of stranded costs to former monopolists is not necessarily an instance of corporate welfare. However, EU governments were often excessively generous in their calculations, effectively using stranded costs repayments to finance the internationalization of former incumbents. For instance, according to the Italian electricity regulator, the 2.3 billion euros the government awarded to the incumbent ENEL largely exceeded any infrastructural cost previously incurred (Rangoni, 2011). For its part, the Spanish government awarded no less than 11.6 billion euros in stranded costs to regional electricity producers (Toral, 2011, 100). As in the telecommunications sector, governments often made recourse to tax exemptions to support their national champions. For example, the French government awarded the state-owned electricity producer EDF tax breaks for a total of 1.37 billion euros, which were later deemed illegal by the Commission (European Commission, 2015).

To sum up, as a result of the restructuring of network industries, the state went from providing direct services to the population via departmental agencies, to awarding monetary advantages to private law (often privately-owned) companies that have replaced these services. These unconditional monetary transfers function to benefit above all large multinational corporations. In fact, due to the high level of sunk costs, network industries like telecommunications, electricity and oil production are characterized by highly concentrated markets (Colli et al., 2014), and are dominated by some of Europe’s largest multinationals. For instance, in 2019 these three sectors alone contained fourteen of the largest fifty European companies by revenue (Forbes Global 500).

Regional development policies

The third area illustrating the proliferation of unconditional transfers is the field of subnational economic development policies. Comparative Political Economy has looked at subnational dynamics mostly with respect to the small number of extremely successful economic agglomerations, such as in the Bay Area, Dublin, or Stuttgart (cf., Herrigel, 2000; Iversen and Soskice, 2019; Regan and Brazys, 2017).

On the one hand, this research focus mirrors the outsized economic importance of highly productive regions in post-Fordist capitalism (Storper et al., 2015). In terms of state-business relations, the centralized structure of the global knowledge economy has been quoted as a major reason for why economic globalization may not have caused a systematic disempowerment of states vis-a-vis mobile capital flows. As argued by Iversen and Soskice, highly innovative economic clusters hold significant sway over mobile capital as hubs for scarce high-skill labor (Iversen and Soskice, 2019).

On the other hand, focusing on the showcase regions of the knowledge economy risks overshadowing increasingly desperate attempts among ordinary regions to boost employment and local tax bases. Particularly in North America, states, counties, and cities have been locked into progressively cost-intensive contests over corporate investment decisions since the 1970s. As a result, capital investments today rarely happen without “incentives” and “support services” provided by various levels of government. These range from dedicated infrastructure investments and consulting and training services through to tax abatements and cash transfers. This section gives a brief overview of the field of local development policies in the United States and the European Union. We also briefly introduce attempts at urban, European, and global levels to police beggar-thy-neighbor policies. We argue that the politics of regional development policies play out around the question of the conditionalities attached to recruitment packages. Comparative perspectives on regional development policies should hence not solely focus on regions' nominal generosity, but on within-transfer conflicts over conditionality.

The empirical tracing of subnational development policies is riddled with methodological and data problems. It remains difficult to compare monetary to non-monetary government services for would-be investors, such as loan guarantees to fewer workplace safety or environmental regulations. Moreover, even in rich democracies, regional development and industrial recruiting policies are not fully transparent due to confidentiality requirements and obfuscation practices. This even holds true for member states of the European Union, which features an institutional regime policing important vertical instruments of state aid since the Treaty of Rome (Thomas, 2000).

Systematic data collection efforts—for example, for the United Kingdom (Farnsworth, 2012), for Germany (Laaser and Rosenschon, 2020), or for the United States (Good Jobs First, 2022)—often run into problems of delimitation when taking stock of public benefits for business. While public expenses for education and training or depreciation schedules in the tax code, for example, undoubtedly benefit domestic businesses, their classification as subsidies or corporate welfare risks overblowing quantitative estimates. By contrast, more restricted classificatory schemes may seem arbitrary and tend to make comparative analyses very difficult as different regions may operate with different sets of policy instruments.

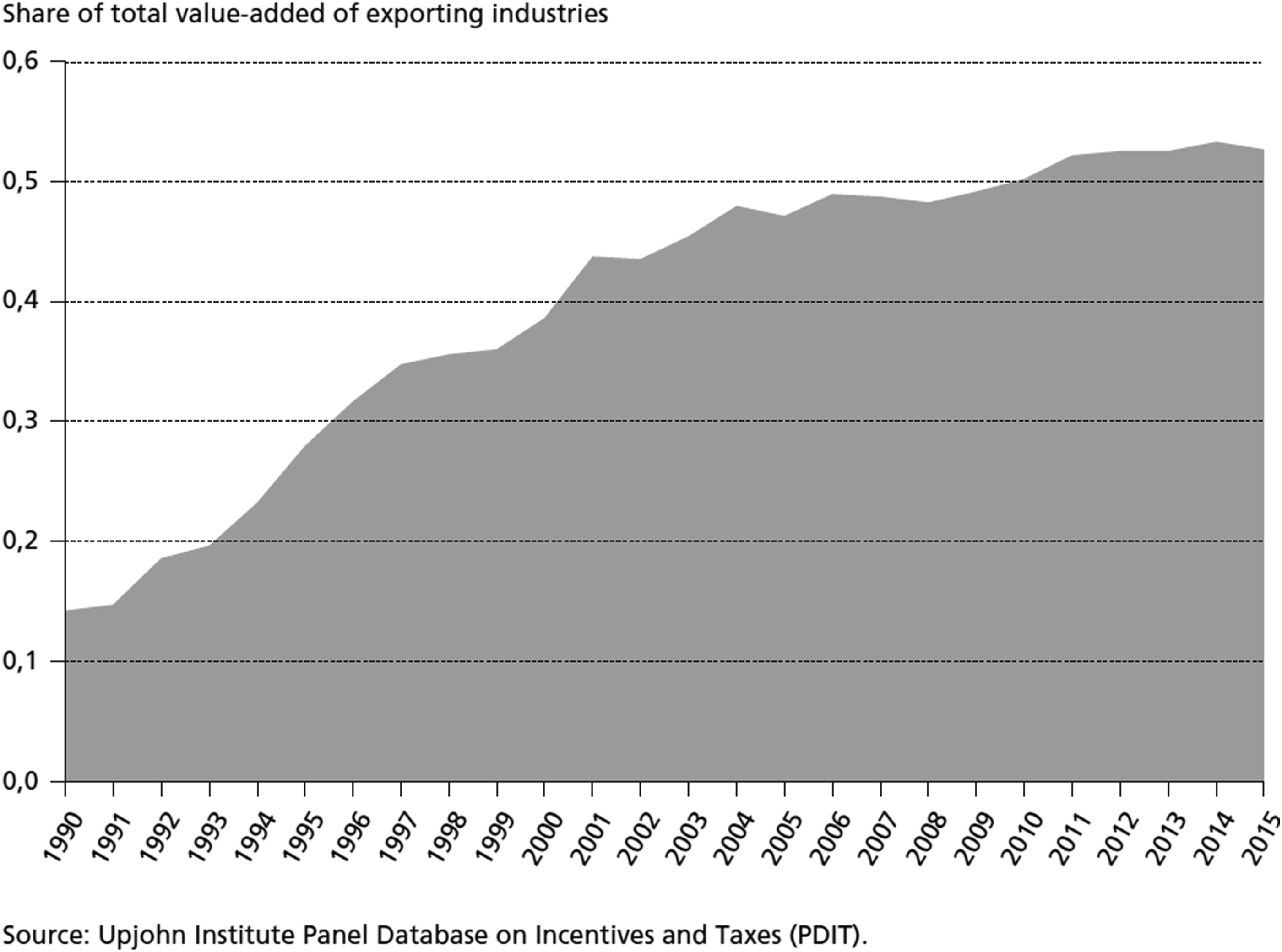

While beggar-thy-neighbor industrial recruitment policies have existed throughout the history of capitalism, regional governments have arguably professionalized the bidding for mobile capital in the post-Fordist era. Figure 1 charts the expansion of subnational incentives for investments by exporting industries in the United States since 1990 (excluding routine additional tax abatements and non-monetary services). Even such restricted classifications of subnational transfers to business as pure incentive payments show a significant rise. Estimates of the overall value of recruitment packages common in the late 1990s and 2000s routinely arrive at figures between 100,000 and 500,000 dollars per job created or retained (see the collection of examples from around the world in Oman, 2000). Incentives for exporting industries across the United States, 1990–2015.

As argued by Peter Eisinger, systematic attempts by regions to recruit footloose industries in the United States broadly emerged in the South during the Great Depression (Eisinger, 1989). These policies diffused and grew in scale and sophistication throughout the US since the 1970s. The erosion of the industrial dominance of the Northeast since the 1960s was accompanied by aggressive recruitment policies in Sunbelt states—now often called smokestack chasing. Southern local business and political elites developed elaborate strategies to improve their local “business climates” since the Great Depression – among them tax rebates and land provision, selective infrastructure projects, sponsoring of recreational and educational facilities, and suppression of labor organization (Perry and Watkins, 1977). At the latest since the late 1960s, most American states had similar economic development strategies in place—either to stop the bleeding or to gain a foothold in the competition for corporations’ plant location decisions.

Following Eisinger’s (Eisinger, 1989) work, instruments of smokestack chasing have been categorized into five types: various forms of tax abatements, debt financing programs, labor suppression, policies ameliorating specific geographical areas, and regulatory relief, particularly in environmental and workplace safety respects (Grant et al., 1995, 135). While there exists no quantitative data on program design, there is no systematic qualitative evidence that American incentive schemes were ever systematically tied to performance metrics, benchmarking regimes, or other forms of strong conditionality. Case studies and surveys of policy effects suggest very weak conditionality and resulting difficulties of local governments to stimulate durable industrial dynamics (Cowie, 1999; Peters and Fisher, 2004).

Industrial recruitment activities have been professionalized and amended and have grown in sophistication in the post-Fordist era. Changing instruments, mission statements, and institutional manifestations have given rise to extensive debate about “new generations” of local development policy. Already in the late 1980s, Eisinger (1989) suggested that smokestack chasing, what he called “supply side” policy, was a thing of the past. Under the somewhat misleading label of “demand-side” policy, Eisinger collected measures by which “government” would begin to play “an unaccustomed entrepreneurial role” (Eisinger, 1989, 227), many of which we today associate with twenty-first century industrial policies. According to Eisinger, governments’ attempts to establish sector-specific infrastructures, export support facilities, research and development centers, cluster structures, and venture capital financing grew out of frustration with the race to the bottom-dynamic of smokestack chasing. Importantly, these policies were available to—if not targeted at—small business and local entrepreneurial groups. Since the 1990s, scholars have emphasized a third wave of economic development policies in which states try to recruit and retain industry through brokerage and the supply of expertise and information, sometimes called network-based (Bradshaw and Blakely, 1999; Whitford and Schrank, 2009).

While the proliferation of more sophisticated policies has given rise to interpretations of the United States as developing new types of state capacity in guiding industrial development (Block, 2008; Iversen and Soskice, 2019), local beggar-thy-neighbor policy toolkits have remained in place, if not intensified. In fact, Southern-style local development transfers have since the 1990s become common across rich as well as developing countries (Oman, 2000). Viewed from a perspective focused on conditionality rather than blanket figures, notions of a new breed of developmental states in the knowledge economy should be treated with even more skepticism. While smokestack chasing policy repertoires undoubtedly constitute a dynamic in favor of investors’ interests, incentive packages usually include rudimentary ties to investors’ future behavior, such as jobs created or overall dollars invested. Regional governments’ recruitment strategies have also been an avenue for social movements and local activists to extract concessions and commitments from investors, for example in the form of Community Benefits Agreements (Lowe and Morton, 2008; Thomas, 1997). By contrast, many of the components of the new generation of policies—for example, in export assistance, research and development services, or loan underwriting and de-risking—put state agencies into the position of routine service providers without significant leverage to influence corporate decision-making.

Accompanying the proliferation of local recruitment policies, there have been a number of attempts to institutionally limit government transfers to investors. While most of these measures had some limiting effects on vertical development policies, they may at the same time have restrained states’ ability to influence investors’ decision-making and implement conditionality. On the transnational level, the 1994 Agreement on Trade-Related Investment Measures (TRIMs) tried to limit discriminatory industrial policy practices. At the same time, it made local content, technology transfer, licensing and other practices contestable. The General Agreement on Tariffs and Trade (GATT) includes commitments on limiting subsidies in agriculture and industry since the 1990s, while debate about subsidies in services through the General Agreement on Trade in Services (GATS) has to date not been concluded. The GATT/WTO framework focusses heavily on non-discrimination and trade distortions and arguably leaves ample space for governments to implement industrial recruitment policies—especially under the banners of science and technology, regional and environmental policy (Amsden and Hikino, 2000; Oman, 2000). Regulations regarding subsidies have also been part of most contemporary bilateral and regional trade agreements, as well as of individual countries' trade policies, such as the EU’s and US’ antidumping and antisubsidy rules. An exception to the largely futile attempts to limit competitive transfers to industry among governments may be constituted by the European Union. The EU’s state aid regime has been restructured significantly since the late 1990s. While it still contains significant loopholes, for example through the corporate tax code and regional aid, it has arguably worked as a roadblock restricting the further expansion of smokestack chasing since the late 1990s (Thomas, 2011).

Conclusion

We argue that an engagement with the concepts of corporate welfare and conditionality helps to make sense of a defining feature of contemporary capitalism: the weakening of state actors vis-a-vis corporate interests. We define corporate welfare as transfers from state actors to large, small, domestic, and foreign corporate recipients, coming without strings attached, or with weak conditionality. Such a restrictive definition, which departs from previous work, serves to specify the blurred boundaries between corporate welfare and other forms of state support to business actors that fall under the rubric of developmental industrial policy, cyclical interventions, or structural policies.

Corporate welfare without substantive conditionalities denies the state a capacity to enforce its own logic of action within the economy. It comes as a result of the state (often voluntarily) relinquishing its various tools of constructive economic intervention over recent decades, but also as a result of the competitive pressures wrought by intensified globalization and the transnational expansion of large corporations. As such, the state has become increasingly dependent on corporations to fulfill the primary goal of providing for prosperity and social stability and has less bargaining power to dictate the terms of these functions. While focused on the rich capitalist democracies of Europe and North America, the empirical illustrations spanned areas as diverse as unconventional monetary policy, the regulation of public service industries, and regional development policy serving to highlight the widespread diffusion of unconditional public transfers as a policy style across countries and sectors. While we described a trajectory of decreasing conditionality in post-Fordist capitalism, by no means do we want to suggest a unidirectional or uniform process. As mentioned in our empirical vignettes, public transfers to business can become sites of state reassertion, contestation, and politicization—as recently widely seen in attempts to attach greening mandates to pandemic relief programs.

Future research on corporate welfare should be developed in two directions. First, more systemic efforts must be made at integrating the concept of corporate welfare within current debates on structural power and state-business interactions. Future research should aim at understanding whether the large corporate giants that dominate contemporary capitalism (Philippon, 2019) are effectively the recipients of disproportionate corporate welfare privileges, and to what extent their preferences differ from those of other segments of business. Second, quantitative case studies should aim at improving the availability of data on conditionality. Our understanding of cross-regional, cross-sectoral, and historical regularities is extremely sparse and only concerted efforts at data collection can remedy this situation.

Nevertheless, measurement and data gathering problems do not negate the value of conceptualization—particularly as they can be solved in principle. Key concepts in political economy like liberalization, corporatism, or clientelism have been deployed to compare societies across time and space long before there were attempts to measure and quantify them. Furthermore, systemic data sources about government transfers to industry exist, albeit scarce in number (Bartik, 2017; Good Jobs First, 2022; Jakli, 1990, 172–92; Thomas, 2000). While often biased politically and of regularly unreliable quality, these constitute rare occasions in which actors try to “take stock” of transfers to industry, and vastly underexploited data sources that open many promising pathways for future research.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.