Abstract

This article contributes to the literature on state capacity in financialized political economies by studying the market-based investment setting for the Thames Tideway Tunnel, a £4.2 billion sewer, built underneath central London to prevent raw sewage from spilling into the River Thames. Most analyses conclude that financial statecraft undermines state capacities, as it empowers finance and exposes states to uncontrollable risks. This article moves beyond these accounts by arguing that public policy officials engage with finance instrumentally, taking on risks to solve the governing challenges they face. It demonstrates that state action can build islands of state capacity with financial statecraft in fragmented policy environments. Based on expert interviews and documentary analysis, the article traces how the UK’s Ministry of the Environment experimented with a policy instrument and used investment capacities from different levels of government, to implement the Thames Tideway Tunnel through institutional equity investment and share risks in the privatized and financialized environmental sector. The paper concludes that under the current conjuncture, financial statecraft will play an important role in addressing the climate crisis. Therefore, further comparative research is required to explore its normative paradox.

Keywords

Introduction

In August 2015, the Thames Tideway Tunnel reached financial close. At costs of £4.2 billion, it is the largest and most complex capital undertaking to have ever been implemented in the UK’s environmental sector and was one of the first greenfield infrastructures involving deep tunneling works financed by institutional investors. The 25-kilometer storage and transfer tunnel is built underneath central London to prevent 40 million cubic meters of sewage from spilling into the River Thames every year. When the Secretary of State to the Department for Environment, Food, and Rural Affairs (Defra) decreed the project to bring UK territory into compliance with national and European environmental law, Kemble Water, the equity consortium owning Thames Water at the time and the monopoly provider of environmental services in England’s South East, refused to finance the policy. The treasury ruled out public financial support for what it considered to be a private-sector responsibility. Implementation was thus stalled. To break the deadlock, the Secretary offered a bargain to Thames Water’s shareholders. He would legislate a new policy instrument known as “Infrastructure Provider,” which allowed to set up a new company for financing the Thames Tideway Tunnel in capital markets and off the national accounts.

This article analyzes the implementation of the Thames Tideway Tunnel to contribute to the debate on state capacity in financialized political economies. Political economy has long shown that the transformation of capitalism undermines state capacity (Streeck, 2014) and makes state action dependent on capital markets (Schelkle and Bohle, 2021). In her seminal work, Gabor (2021, 2023) coined the notion of the “de-risking state” to capture how the co-evolution of state institutions and financial markets underpinned a new modality of financial statecraft, which consists in steering price signals and correcting market failures by designing risk-return profiles. She traced the roots to neoliberal ideation and its view of the market as a privileged vehicle for addressing economic concerns. The work of Mertens and Thiemann (2018) highlights that public financial institutions and instruments are cornerstones of de-risking. They analyze how the European Investment Bank used complex financial instruments and limited public funds to absorb investments risks and channel capital market investments into real assets and innovation. The authors conclude that this “hidden investment state” undermined state capacity by transferring authority over investment decisions to expert institutions and exposing public budgets to capital market volatility. From a different starting point, the assetization literature reaches similar conclusions (Birch and Muniesa, 2020, Chiapello, 2017). Studying public policy heads on, it probes how financial actors use financial instruments and expertise to transform collective goods and services into financial assets in contexts framed by the state. Economic geographers working on the UK traced how privatization enabled asset managers to reengineer London’s environmental infrastructure system into revenue streams and shareholder profits (Allen and Pryke, 2013, Bayliss et al., 2022).

The coevolution of state institutions and financial markets notwithstanding, in some instances of public policy, states have succeeded in implementing crucial policy objectives with market-based finance (Quinn, 2017). Germany, for example, relied on capital markets for rolling out one of the world’s most aspiring climate policies (Naqvi et al., 2018). The UK implemented the Thames Tideway Tunnel, the environmental policy studied in this paper, through institutional equity investment, despite opposition from Thames Water’s shareholders, the industry’s economic regulator, and the treasury’s refusal to get involved. Under what conditions are state actors in fragmented policy environments able to use market-based finance for the implementation of policies? How are market-based investment settings set up with investment state capacities? And whose projects are advanced with these state–finance entanglements? (Samman et al., 2022: p. 98)

This paper examines the Thames Tideway Tunnel as a case in which state action, through financial statecraft, builds an island of capacity within a fragmented policy environment. In this context, public officials experimented with a new policy instrument and directed financial innovation to solve the governing challenge they faced. To make this argument, the paper draws on economic sociology (Quinn, 2017; Wansleben, 2023) and uses insights from political sociology (Lascoumes and Le Galès, 2007), to analytically separate policy objectives from their instruments of implementation and analyze why, how, and with what results public officials set up market-based investment settings for the implementation of crucial policy objectives. It shows that in this case public policy officials engaged with finance instrumentally, and not on ideological grounds, taking risks and managing these to create new opportunities of governance. The paper contends that the choice, design, and layering of financial instruments are an important site of financial statecraft. Negotiating whose resources are mobilized and on what terms, and who shoulders what risks and costs, these processes enlist investment coalitions in the implementation of policies by aligning interests and determining the conditions of public support.

Empirically, the paper shows that Defra experimented with the Infrastructure Provider to align Thames Water’s shareholders with the implementation of the Thames Tideway Tunnel, sidestepping capacity constraints and avoiding blame for longstanding environmental policy failures. The Department then negotiated a national guarantee with the treasury that shared risks with investors to make the project sellable in merger and acquisition markets and the instrument compliant with European competition law. And to manage the vulnerabilities carried by this strategy, the Department secured a loan from the European Investment Bank that sourced the financial management capabilities of the financial institution. In its operationalized form, the multilevel investment setting mobilized £2.4 billion from institutional investors to implement the Thames Tideway Tunnel faster than alternative modes of delivery and at costs that meaningfully undercut the returns utility shareholders earned for routine investments.

This paper makes three contributions to the literature. First, it offers a detailed account of how a market-based investment setting is set up and framed with investment state capacities to implement a crucial policy (Mertens and Thiemann, 2018). Second, it shows how public policy officials can rely on financial statecraft to build islands of capacity in fragmented policy environments and share risks with investors (Gabor, 2023). This advances research on the role of the state financialization processes, shedding light on both its agency and problem-solving dimension. And third, the paper expands research on the politics and limits of financial statecraft from macroeconomic policy into public policy (Braun, 2018).

Methodologically, this paper builds on 31 interviews with public and infrastructure finance experts, regulators, and government officials responsible for the project and on documentary analysis. 1 It proceeds as follows. The first step develops the theoretical framework. It reviews the literature on state–finance relations and draws on economic and political sociology. The second section traces the history of the Thames Tideway Tunnel and shows that the policy and its implementation failure had their roots in the denationalization of its environmental sector and the transformation of the UK’s political economy. The third step studies how the choice of the Infrastructure Provider allowed Defra to align Thames Water’s shareholders and the industry’s economic regulator with the market-based implementation of the Thames Tideway Tunnel. The fourth step shows how the Department layered national and European financial instruments onto the Infrastructure Provider to make the Thames Tideway Tunnel sellable in merger and acquisition markets and share risks with investors. The discussion reflects on the findings’ generalizability and reviews the contributions to the literature. The conclusion identifies the normative paradox of financial statecraft as an important area for future research.

State financialization and financial statecraft

Political economists have long shown that the transformation of capitalism is driving state reconfigurations that undermine state capacity for future-oriented investments (Streeck, 2014). Beginning in the 1980s, European states re-regulated financial markets to borrow on capital markets and avoid politically costly decisions (Karwowski, 2019). Increasing public debt levels, coupled with the European integration process, however, forced member states to reconcile their policy offerings with fiscal consolidation. The Maastricht Treaty, the Fiscal Compact, and the so-called Six-Pack regulations (Verdun, 2015), together with European state aid provisions (Thatcher, 2013), institutionalized balanced budget requirements and disciplined state intervention. In his seminal work, Wolfgang Streeck (2017) theorized this process as the rise of the consolidation state, in which policymakers rely on private finance to offset spending constraints. In Britain, consolidation is firmly institutionalized. Since the Thatcher administration, the state has aspired to a public debt-to-GDP ratio of below 40% and relied first on privatizations and then on the Private Finance Initiative for public policy.

Financialization scholars have tied the rise of the consolidation state to public financial innovations (Schelkle and Bohle, 2021) and shown that state actors harness financial markets as a tool of statecraft (Wang, 2020). This notion captures an indirect mode of governance, by which policymakers induce financial market actors to realize policy goals. In a pioneering study, Lagna (2016) analyzed how the Italian government used derivates to comply with European Monetary Union criteria. Research on sovereign debt documented that states use debt management agencies and bond auctions to diversify their investor base and compete with other sovereigns for financing (Schwan et al., 2020, pp. 7–10). Most research concludes that financial statecraft ends up creating opportunities for the financial sector to reap profits, while simultaneously undermining redistributive capacities and democratic processes.

Gabor (2021, 2023) coined the term “de-risking state” to theorize how the development of market-based financial systems drives the emergence of a form of financial statecraft that is shaped and constrained by the interests of finance, albeit with variegated manifestations. This modality consists in steering price signals and addressing market failures. Policymakers design monetary, regulatory, and fiscal interventions to engineer risk-return profiles and investable policies. Gabor (2023) demonstrates how the de-risking state is anchored in the neoliberal vision of the market as a privileged vehicle of governance and the corresponding macro-institutional configuration of the state in market-based financial systems, specifically the division of labor between central banks, finance ministries, and capital markets. Expanding on Braun’s (2018) notion of the infrastructural power of finance, Gabor (2021) argues that the infrastructural entanglements between states and finance, which are characteristic of the de-risking state, facilitate the capture of state action by finance and prevent it from disciplining capital.

The work of Mertens and Thiemann (2018) highlights that public financial institutions and instruments are cornerstones of de-risking in Europe. The authors analyze how the European Investment Bank channeled market-based investments into real assets and innovations in the aftermath of the 2008 financial crisis by using complex financial instruments and limited public funds to absorb idiosyncratic financial risks. To them, this “hidden investment state” is emblematic of macroeconomic governance constraints in the EU, where the dominant role of monetary policy and the European Central Bank, coupled with the lack of fiscal capacity at the European level, leaves few governance options for policymakers but to rely on financial instruments and regulations (Braun et al., 2018). Mertens and Thiemann (2018) conclude that despite their policy expediency, investment states undermine state capacity by transferring authority over investment decisions to expert institutions and exposing the European budget to uncontrollable risks.

From a micro-perspective, the literature on assetization studies how financial actors use financial technologies and expertise to transform public policies into financial assets in contexts framed by the state (Birch and Muniesa, 2020, Chiapello, 2017). Economic geographers emphasize the spatial dimension of these processes, showing how financial actors employ securitization techniques and special purpose vehicles to mediate revenue extraction and intertwine spatially situated infrastructures with financial architectures and flows (O’Brien et al., 2019). Scholars working on the UK substantiated how the privatization of the environmental sector allowed the Macquarie-led Kemble consortium to buy the utility Thames Water and deploy financial engineering techniques to reconfigure cash flows derived from water bills into dividend payouts (Allen and Pryke, 2013). Bayliss (2017) showed that financial engineering was made possible by the sector’s selective regulatory regime. It created certainty by making the prices utilities could charge predictable but remained neutral vis-à-vis utilities’ capital structures. This allowed equity investors to realize high returns, and at the same time exhaust balance sheets and leave infrastructure and services underfunded (Bayliss et al., 2022). Loftus and March (2019) argued that equity investors pursued large-scale capital interventions, importantly the Thames Tideway Tunnel, to expand rent extraction within the environmental sector.

In sum, both political economy and assetization studies find that financial statecraft empowers the financial sector and re-centers state action on guaranteeing profits for investors. Political economy traces the co-evolution of state institutions and financial markets and shows how states’ ideological engagement with finance makes state capacity dependent on market-based finance. Focused on macroeconomic policy, however, the literature has not studied public policy and its implementation. As a result, it provides a one-sided account of the objectives state actors pursue with financial statecraft and fails to adequately consider its variation and multilevel dimension. Assetization studies focus on public policy and conceptualize the assetization process as a site where finance extracts profits and exerts its power over states. Yet, the literature reduces state action and capacity to mere framework conditions of financial action, ignoring the interdisciplinary insights that states and finance are intricately intertwined at an infrastructural level.

This paper foregrounds the flipside of financialization and financial statecraft (Samman et al., 2022: p. 98). It studies how public policy officials use market-based finance entrepreneurially, to implement public policies crucial for social and economic development. It demonstrates that in fragmented policy environments, public policy officials can build islands of state capacity through financial statecraft, experimenting and solving the governing challenges they confront. It argues that public officials engage with finance instrumentally, and not on ideological grounds, taking risks and managing these to create new opportunities for governance. This is not to deny the dark side of financial statecraft and absolve the problematic institutional configurations that undergird it from critique (Samman et al., 2022). The literature has forcefully demonstrated how these empower finance and subject states to massive and asymmetric risks, from which finance is the first to profit. However, financial risk-taking also offers opportunities, albeit ones that are uncertain and problematic. There is no inherent reason why this should not apply to state action as well (Mazzucato, 2013).

This paper draws on economic and political sociology to make this argument. Economic sociologists have shown that policy actors use public financial innovations to bypass political constraints and solve the governing problems they face. In her seminal study, Quinn (2017) demonstrated how the Johnson administration redesigned the US’ public housing financial intuitions, the so-called Government-Sponsored Enterprises, to leverage capital markets via securitization techniques and implement housing policy against the resistance from Republican law makers and politically engineered budget constraints. In a conceptual article, Wansleben (2023) shows how policymakers employ financial policy innovations to bypass fiscal and distributional conflicts and manage the recursive effects of financialization. By creating contingent liabilities, these move the political and economic costs of policy off-balance sheet and into the future, with their magnitude contingent on future events.

Following these lines, this paper separates public policy into its objectives and instruments of implementation (Lascoumes and Le Galès, 2007). It analyzes why, how, and with what results public officials use financial instruments to implement public policy through market-based finance and the mutually shaping effects of objectives and modes of implementation. In this way, it also accounts for the multilevel dimension of financial statecraft, which not only interweaves public and private sectors but also combines capacities from different levels of government. The paper explores why officials chose instruments and from what level, and how these instruments are configured and combined to frame and orchestrate collective action—a process referred to as instrumentation—to examine how policy is implemented with market-based finance, along with the distributional consequences and normative effects produced in implementation. The paper argues that the choice, design, and layering of financial instruments are an important site of statecraft. Negotiating whose resources are mobilized and on what terms, and who shoulders what risks and costs, these processes enlist investment coalitions in the implementation of policies by aligning interests and shaping the distributional consequences of public support.

The Thames Tideway Tunnel was undeliverable in the UK’s environmental sector

The Thames Tideway Tunnel was a hard test for state capacity. Defra elevated the Thames Tideway Tunnel to public policy to avoid blame for longstanding environmental policy failures in the Greater London Area. Yet, the Department’s implementation capacity was undermined by the denationalization of the UK’s environmental sector (Moran, 2003) and 30 years of New Public Management reforms (Whiteside, 2020). When Defra decreed the Thames Tideway Tunnel in response to legal proceedings lodged by the European Commission at the onset of the 2008 financial crisis, Thames Water’s shareholders refused to comply.

The denationalization of the UK’s environmental sector

In 1989, the Thatcher Administration had passed the Water Industry Act to privatize the environmental sector and avoid some of the massive spending required by European regulations (Moran, 2003). These included the Urban Waste Water Treatment Directive, transposed into British law in 1991 to mandate that all waste water produced in urban areas is collected and treated. Toward these ends, the Act migrated responsibility for environmental services to regional monopoly providers and created a three-partied regulatory regime under the auspices of Defra. Within this regime, utilities are funded from customer charges, their undertakings are financed by private investors, and they have a statutory obligation to deliver services in line with national and European regulations. And utilities are eligible for lending from the European Investment Bank. The Environment Agency oversees compliance with environmental regulations. The Drinking Water Inspectorate monitors drinking water quality. And Ofwat regulates the charges utilities levy. The economic regulator is obligated to set these at a level that safeguards the interests of customers and at the same time allows shareholders to recover their costs and earn reasonable returns. Utilities can appeal against regulatory decisions in front of the Competition and Markets Authority. 2

This regulatory regime allowed asset managers to invest in the UK’s environmental infrastructure systems and reconfigure revenue streams into financial assets (Bayliss, 2017, Bayliss et al., 2022). The regime determines shareholder reward over 5-year regulatory cycles. Utilities submit business plans at the beginning of each to detail how they will deliver services in line with regulatory requirements. Ofwat then takes a view on compliance and the costs shareholders are likely to incur based on several building blocks. To incentivize efficiencies, shareholders can keep the gain if they outperform regulatory assumptions. If they underperform, they must shoulder the pain. The most important building block is the Weighted Average Cost of Capital, with which Ofwat estimates the cost of financing for utilities. Toward these ends, the regulator assumes that utilities access investment-grade capital markets and that shareholders finance investments with around 60% of debt and 40% of equity. It then forecasts the market cost of debt and equity and calculates a weighted average of the financing costs shareholders should incur. It leaves it to shareholders to choose actual financing strategies if these don’t impair the utilities’ investment-grade credit ratings. These mechanics created ample room for financial engineering (Allen and Pryke, 2013). Not only was Ofwat underestimating the share of equity on utilities’ balance sheets and overestimating the real costs of debt to incentivize investments, but in guaranteeing customer charges, the regulator also stabilized the value of the bonds utilities issued, safeguarding capital market access for routine operations with financial structures that were far more leveraged than it assumed. Shareholders could fund investments with more debt relative to equity than nominally assumed and retain the savings as profits. And they could issue debt for dividend payouts as opposed to capital expenditures.

By the mid-2000s, equity funds had become major shareholders in the environmental sector and Thames Water’s room for financing non-routine undertakings began to narrow (Helm and Tindall, 2009). In October 2006, the Kemble consortium bought Thames Water for £4.8 billion. It refinanced equity stakes and issued debt to increase shareholders’ returns. By 2009, more than 75% of Thames Water’s liabilities consisted in debt, up from below 50% at the time of purchase. 3

As a result, Thames Water failed to develop infrastructure in line with the development of the Greater London Area. After decades of stagnation and between 1998 and 2015, the GDP produced by London's agglomeration economy grew by almost 250% to around £430 billion, which was equivalent to more than 20% of the national GDP.

4

The metropolis added more than 1 million inhabitants and surpassed its previous 1939 population peak of 8.6 million. As a result, the demand for environmental services surged in the Greater London Area, while the impact of climate change intensified runoffs into London’s sewer systems due to increasingly extreme weather events. More and more often the system hit capacity and by the end of the century, it discharged 20 million cubic meters of sewage into the River Thames every year.

5

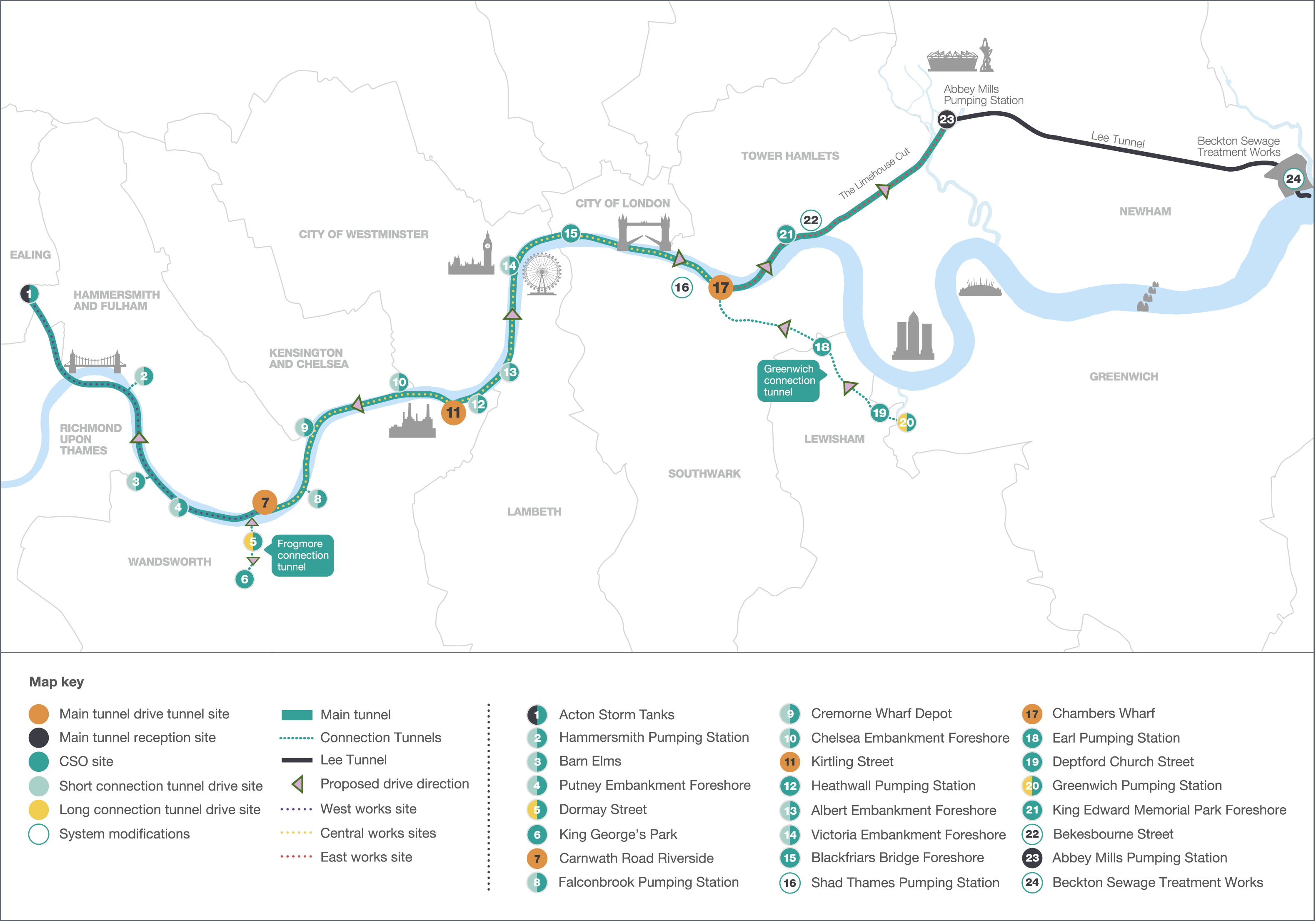

In April 2006, the European Commission issued a reasoned opinion that the UK was in breach of the Urban Waste Water Treatment Directive. In March 2007, the Secretary of State instructed Thames Water to build the Thames Tideway Tunnel and intercept the overflows. Figure 1 The route of the Thames Tideway Tunnel (source: Tideway).

The market-based environmental sector failed

The 2008 financial crisis laid bare the vulnerabilities the UK state had created in relying on market-based finance for infrastructure (Braun, 2018). As uncertainty mounted, the Kemble consortium decided to refuse the Thames Tideway Tunnel. Following the collapse of Lehman Brothers, capital markets for regulated industries shut for more than 4 weeks. The same month, Ofwat started its price review for the fifth regulatory cycle and downward adjustments of the Weighted Average Costs of Capital loomed large on shareholders’ horizons. Meanwhile, Kemble had calculated that it would have to invert Thames Water’s gearing from 75% to 25% and re-inject equity worth £3.5 billion to finance the Thames Tideway Tunnel. The project alone was expected to require investments worth £1 billion in equity and £2.5 billion in debt, the equivalent of half of Thames Water’s asset base. 6 The consortium concluded that it would not move forward on the Thames Tideway Tunnel and argue that Ofwat had no comparator against which to benchmark a determination of the appropriate costs and rewards. “And so to try to ascertain what the appropriate Average Cost of Capital would be for a scheme of the nature of the Thames Tideway Tunnel,” one of my interviewees remembers the objection, “I think everyone would be exercising judgments […] but from [Thames Water's] perspective [that the Costs would be set] at a level which represents an appropriate remuneration of [Thames Water's] risk, you can imagine that is going to be a very difficult process.” 7

Ofwat sided with Kemble as it feared making itself vulnerable to regulatory capture. 8 The Thames Tideway Tunnel was of a scale and complexity that was without precedence in the privatized environmental sector. As a result, Ofwat had no benchmark for assessing the level of reward that was adequate for investors in shouldering the construction risks. This exposed the regulator to the vulnerability of either overaccommodating Kemble’s claim that financing the Thames Tideway Tunnel justified massive rewards, or of seeing its determination challenged in front of the Competition and Markets Authority. And in an adverse scenario, it feared that an implementation failure could put Thames Water’s ability to deliver services into jeopardy. “What particularly concerned us,” one of my interviewees explained, “was that this was a large very risky, and very different project to anything else that had been done in the sector and if you were to put that within the existing company, and its existing business activities, to what extent would that topple, distort, the risks of the overall company?” 9

In May 2010, finally, the Coalition government, led by Prime Minister Cameron, came to power, and denied any form of public support for the Thames Tideway Tunnel. Its treasury oversaw one of the deepest periods of public sector austerity in the UK. 10 With cuts totaling more than 25% and £100 million annually (roughly £700 through to 2015), Defra had to absorb some of the severest retrenchments in relative terms. Beyond austerity, the Coalition launched an infrastructure policy aimed at creating investment settings that entice institutional investors to finance economic infrastructures in the UK. Most germane here, it reconfigured Partnership UK, a Public–Private Partnership set up under New Labour to roll out the Private Finance Initiative (cf. Whiteside, 2020), as expertise unit “Infrastructure UK” within treasury ranks, and tasked it with using regulatory powers and limited public funds to shape commensurate market conditions. 11 The treasury, however, considered the Thames Tideway Tunnel un-eligible for these capacities. In its view, the project concerned a private industry and was environmental in scope rather than economic. 12 Dissatisfied with the UK’s compliance efforts, the European Commission submitted its opinion that the UK was in breach of the Urban Waste Water Treatment Directive to the European Court of Justice in October 2009.

Experimenting with financial innovation: The Choice and design of the Infrastructure Provider

This section shows that Defra chose the Infrastructure Provider to avoid blame for longstanding environmental policy failures in the Greater London Area (Lascoumes and Le Galès, 2007). The choice allowed Defra to align Thames Water’s shareholders and the industry’s economic regulator with the Thames Tideway Tunnel and harness market-based finance for implementing the policy (Quinn, 2017). It induced Thames Water to hire a team of infrastructure experts, who collaborated with Ofwat to design the Infrastructure Provider in ways that emulated the asset characteristics of operational utilities and could harness institutional equity investments for expediting the implementation of the Thames Tideway Tunnel (Birch and Muniesa, 2020). The section demonstrates that Defra relied on financial statecraft to solve a crucial governing challenge under adverse conditions, along with the politics and hybridity of assetization work, which is shaped by both state and financial interests and negotiated in public-private collaborations.

The Infrastructure Provider aligned Thames Water’s shareholders and the industry’s economic regulator

The Secretary of State found himself between a rock and a hard place when the threat of European fines became real. He faced opposition from Kemble and his authority was undermined by austerity and objections from the economic regulator, along with the treasury’s refusal of support. To break this deadlock, the Secretary bargained with Thames Water’s shareholders. He would designate the Thames Tideway Tunnel as Infrastructure Provider to allow for the setup of a new company for financing the Thames Tideway Tunnel and the formal release of shareholders from their statutory obligations toward the national decree. In exchange for the designation, Thames Water would have to operationalize the Infrastructure Provider in ways that expedited the environmental service delivery and avoided any draw on the national balance sheet. And to further hedge against Defra’s vulnerability, the Secretary made clear that if the Infrastructure Provider strategy failed, he would argue in front of the Competition and Markets Authority that Kemble was deliberately obstructive and Ofwat was therefore empowered to commence enforcement action regardless of the technicalities of financial reward. 13 In April 2010, Defra had amended the Water Industry Act to allow for the procurement of special purpose companies within regional monopolies of service referred to as Infrastructure Providers. 14 But the Act left the instrument and its mechanics unspecified.

Kemble accepted to protect the value of its equity investment and disambiguate its responsibilities. In May, the consortium hired some of the UK’s most high-profile infrastructure experts to operationalize the Infrastructure Provider strategy. 15 Among them was Michael Gerard, appointed Managing Director for the Thames Tideway Tunnel, who had made his career as director of the treasury’s infrastructure task force and as Chief Executive Officer of Partnership UK. 16 Trusted in both worlds, he created a linkage between the treasury and the investment community.

Defining the Infrastructure Provider

The team began with an appraisal of options for procuring a special purpose company that would transform the Thames Tideway Tunnel into a proposition for capital market investors (Birch and Muniesa, 2020). 17 An important instrument it considered was the Private Finance Initiative. With it, the Thames Tideway Tunnel would have been financed, built, and operated by a special purpose vehicle formed by engineering companies and investors at a price the consortium fixed in its winning bid. The consortium would have had to raise up to £5 billion for the massive and complex construction works that were expected to take 7 years. Private Finance Initiatives, however, had hitherto remained below £1.5 billion in value, and construction took on average 3 years. The team reasoned that only very few companies would be able to realize such an undertaking and that they would require very high rewards for the risks. Based on this, the team expected Ofwat to find a Private Finance Initiative incompatible with its regulatory duties as rewards would be paid by Thames Water’s customers. To make matters worse, a Private Finance Initiative would be framed by the European procurement directive, which mandated a 24-month bidding window. The team concluded that this was a time span between the call for tender and contract award that Thames Water’s shareholders did not have. 18

The appraisal highlighted the limits of market-based finance in delivering infrastructure for the UK (O’Brien, O’Neill and Pike, 2019). Like the privatizations, the Private Finance Initiative was created in the 1990s to use private finance for reconciling collective services with fiscal consolidation. To keep the Initiative off the national accounts, the treasury had standardized the allocation of risks to the private sector, forcing bidders to absorb uncontrollable risks. As a result, Private Finance Initiatives were high-risk high-reward investment propositions. Only large engineering companies had the capacity to bid even for relatively straightforward policies such as hospitals or schools and to manage the specified risks. In the virtual absence of competition, they had an easy game to top up their bidding prices with “risk premia.” 19 And the Initiative simply failed to implement more complex policies as investors shunned the risks. The treasury, indeed, had had to subsidize financing costs with so-called “PFI credits” to incentivize the use of the Initiative. Costs further escalated when the 2008 financial crisis hit and capital market conditions deteriorated. In 2010, around the time the team was appraising, the Coalition government abolished PFI credits as part of its fiscal consolidation efforts. In 2018, the treasury discontinued the Private Financial Initiative as it “found the model to be inflexible and overly complex” and “a source of significant fiscal risk to the government.” 20

But the appraisal also hammered home with the team the contours of the Infrastructure Provider strategy. If the design blended the commercial principles of the Private Finance Initiative with the regulatory regime of the environmental sector, it could make possible what under real-world conditions seemed impossible. If it procured a special purpose vehicle, the Thames Tideway Tunnel could be financed off Thames Water’s balance sheet and the national accounts. This would further remove the regulatory vulnerability by delegating the determination of the Weighted Average Cost of Capital to investors as part of their bid offer. And if the design adapted the established regulatory mechanics of the environment sector to the construction works of the Thames Tideway Tunnel, the Infrastructure Provider could emulate the risk-reward characteristics of an operational utility and become financeable in merger and acquisition markets. This would not just tap into the low-risk low-reward financing provided by institutional investors. But equally important to the team, it would also cut the procurement timeline for the Thames Tideway Tunnel in half. Tenders in merger and acquisition markets typically close within 12 months and are not subject to the European procurement directive.

Designing the Infrastructure Provider

Thames Water’s team collaborated closely with Ofwat to adapt the regulatory mechanics of the Water Industry Act in ways that mitigated the specificities of the Thames Tideway Tunnel and were acceptable to the regulator. 21 The Infrastructure Provider would charge from the day of financial close onwards, 7 years before the Thames Tideway Tunnel was expected to deliver services, and its revenues would remain exempt from regulatory review until the completion of the construction work. Investments would be rewarded at the “Bid-Weighted Average Costs of Capital” committed to by investors in their winning bid. As 7 years was an unusually long time for investors, the “financing cost adjustment” mechanic further linked returns dynamically to fluctuations in capital markets. And to mitigate the risk customers would find the charges objectionable, the Infrastructure Provider billed Thames Water, which would then recover the money from its customer base, as opposed to charging for the project separately. One of the architects of the instrument explained, “we started with an ordinary company license and then thought about how do you adapt that license to deal with the specifics of the tunnel and the risk the tunnel faces.” 22

To reconcile these enhancements with Ofwat’s regulatory duties, the team limited their duration to the construction works period and capped the gearing ratio for the Infrastructure Provider at 70%. The Infrastructure Provider would be allowed to recover expenditures without regulatory interference only up to the target costs of £2.65 billion, a volume referred to as “P50”-cost. Investors would share every pound below or above that figure equally with customers as returns or costs. If expenditures were to exceed P50 by more than 30%, a point referred to as the “Threshold Outturn,” the instrument would re-subject all expenditures beyond that threshold to Ofwat’s reviews. And regardless of costs, once construction would be completed, the Infrastructure Provider would be subjected to the established regulatory regime, like any other utility, but would have to fulfil the gearing requirement.

23

One of the architects explained the logic of design: So you saw the regulatory, or perceived, uncertainty around the application of the regulatory mechanics, you diminished them to a point which was still acceptable to the regulator but also presented an opportunity to the private sector to take a sharper view on what that risk represents, but at the same time get over a potential red line, when it came to the financiability of the scheme.

24

With the risk-reward characteristics defined (Birch and Muniesa, 2020), the team innovated vis-à-vis conventional procurement to make the Infrastructure Provider sellable in merger and acquisition markets. It planned to unbundle the Infrastructure Provider into two separate suits of contracts. It would tender the first suit dedicated to the construction works and subject to the 24-month window requirement, 12 months ahead of the second, which invited bids for the ownership of the Infrastructure Provider. In this way, it could expedite the implementation of the Thames Tideway Tunnel by 12 months and present the winning investors with a pre-selected group of engineering companies. A conventional approach would have proceeded sequentially. First select shareholders. And then let shareholders procure the construction works. One of my interviewees explained, “we needed investors who had loads of money and wanted to effectively deploy that quickly.” 25

While politically expedient, the Infrastructure Provider strategy escalated risks to a level merger and acquisition markets failed to take. In October 2011, the team took a draft version of the instrument to Moody’s to get an indication as to whether it was on track for an investment-grade rating. While the rating agency was satisfied with the adaptation of the regulatory mechanics, it remarked that the remote, yet conceivable, scenario of “if I did knock down London Bridge, and then Tower Bridge, and then I hit the tube network and flooded it” 26 was unaccounted for and motivated a sub-investment-grade credit rating. If this scenario remained undefined, capital markets would classify the Infrastructure Provider as a “venture capital asset,” and not as a corporate equity asset. 27

An island of capacity: Orchestrating a multilevel public investment infrastructure

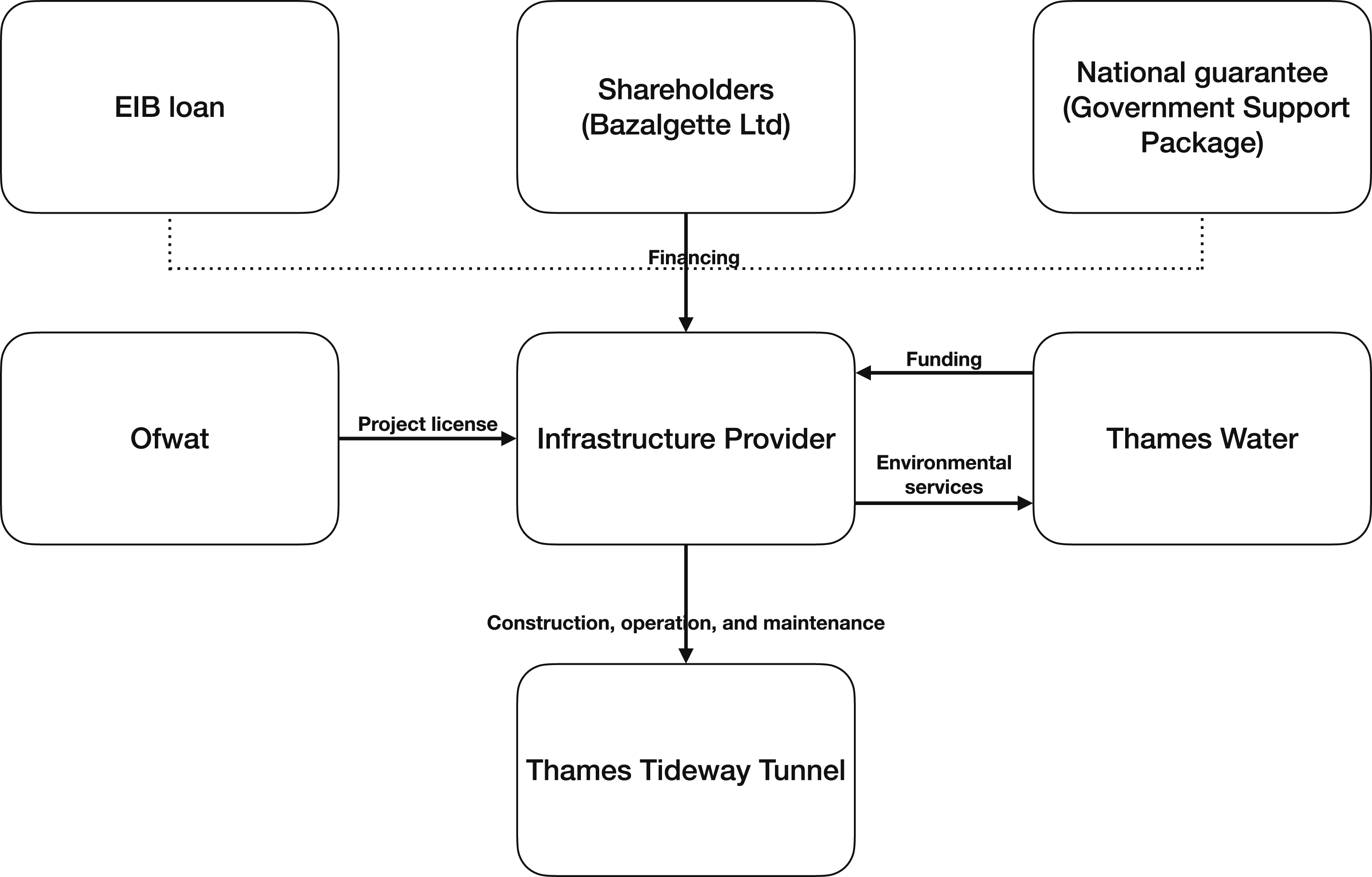

This section analyzes how Defra layered investment capacities from different levels of government onto the Infrastructure Provider to enlist an investment coalition in the implementation of the Thames Tideway Tunnel (Mertens and Thiemann, 2018). This infrastructure interwove Defra’s budget with the Thames Tideway Tunnel in contingent ways to share uncontrollable risks with investors and make the Infrastructure Provider sellable in merger and acquisition markets, all the while ensuring the compliance of support with European competition law (Thatcher, 2013). And at the same time, the infrastructure sidestepped Defra’s eroded capabilities, sourcing the financial management expertise of the European Investment Bank for managing the risks of this entrepreneurial strategy (Wansleben, 2023). Thus, the analysis demonstrates that albeit leaving the UK state with uncontrollable risks (Gabor, 2021), Defra’s financial bricolage created an island of capacity because it pursued a crucial policy and orchestrated investment capacities from the national and European levels to share risks between public and private sectors. Figure 2 illustrates the final architecture of the Infrastructure Provider. The Infrastructure Provider (source: the author’s own creation).

National financial instrument: Interweaving private and public sectors

Following the rating agency’s verdict, the Secretary of State to Defra used the Infrastructure Provider to reframe the Thames Tideway Tunnel and align the treasury with providing public financial support. In a written statement read to Parliament on 03 November 2011, Defra maintained that if backed by contingent government support, the Infrastructure Provider would operationalize the Coalition government’s flagship infrastructure policy as it would channel institutional equity investment into the construction of nationally strategic infrastructure. In two policy documents, the Coalition government had specified its strategy for “use[ing] limited public funds wisely and unlock[ing] every possible source of private sector investment” for UK infrastructure.

28

Defra stated: The Government believe that the private sector can and should finance this project but accept that there are some risks that are not likely to be borne by the private sector at an acceptable cost. It is willing in principle to provide contingent financial support for exceptional project risks where this offers best value for money for customers.

29

Shortly thereafter, the treasury instructed Infrastructure UK to support the development of the Infrastructure Provider. Until this day, it had ruled out any support,

30

as one of my interviewees vividly recollected: Here you got a privatized sector, so [Defra] comes to the [treasury] and says I want to give a government guarantee to Thames Water, what is [the treasury’s] response here? Actually [it is] what the fuck, I privatized this whole sector 20 years ago and now they are coming to me—the public—to actually fund and help them out?

31

Another one of my interviewees conceded, “[the Thames Tideway Tunnel] was a project where the government got drawn into because it became clear that the regulated utility, i.e., Thames Water, was not going to be in a position to fund and finance it in an as effective and efficient way as it could have been, and therefore the risk was a massive increase in costs to the customers.” 32 Someone else explained Defra’s tactics, “you get over the line by saying I am not giving a full guarantee, all I am doing is promoting ‘value for money’, and I am promoting ‘value for money’ because actually it will get a better pricing.” 33

Infrastructure UK designed the guarantee to allocate uncontrollable risks to Defra (Gabor, 2021), but at the same time share risks with investors to receive state aid clearance from the European Commission. By design, it left de-risking incomplete. In the words of a senior official, “every project of this nature faces pressures from the market, state aid, balance sheet treatment, and value for money, and you have to satisfy all four.” 34 Toward these ends, the unit defined four scenarios for financial assistance and set a fee the Infrastructure Provider would be charged for these enhancements. In the scenario defined by the “Supplemental Compensation Deed,” Defra covered the costs of a catastrophic construction event that insurance markets failed to underwrite at reasonable costs. In the scenario defined by the “Market Disruption Facility Agreement Deed,” Defra would lend to the Infrastructure Provider if a market event worse than the 2008 financial crisis happened. In the scenario defined by the “Contingent Equity Support Deed,” Defra allowed shareholders to cap their equity stake at £1.4 billion in the event costs overran beyond the “Threshold Outturn.” Shareholders could then choose to request Defra to take over. In the adjacent scenario defined by the “Discontinuation Deed,” Defra could choose not to step in and compensate senior debt only. Finally, in the scenario defined by the “Special Administration Deed,” Defra would consent to the appointment of a Special Administrator in the event the Infrastructure Provider entered special administration. The Department reserved the right to buy the asset at a price of its own choosing if restructuring failed.

None of the stakeholders expected any call on government support. It “would be an extraordinary set of circumstances” one of interviewees detailed, “but just having it there as a safety blanket, or a comfort blanket, in the background, it then enables everybody to say, or to give an answer to, a what-if scenario, and therefore that allows the banks, bondholders, and people like that, to price it at a very low level.” 35

EU financial instrument: Sourcing expertise

With the Government Support Package taking contours, the Secretary of State capitalized on the European investment state (Mertens and Thiemann, 2018) to source the financial management expertise of the European Investment Bank for the entrepreneurial strategy. In the aftermath of the financial crisis, the European Commission had launched a series of policy measures aimed at reviving economic growth and addressing the climate crisis by increasing market-based investments in European political economies. Complementing the Capital Market Union (Braun et al., 2018), it launched the Investment Plan for Europe in 2014, which massively increased the lending capacity of the European Investment Bank, including for higher-risk projects. If Defra secured a loan from this facility, the Secretary reasoned, it could delegate a substantive share of the financial management entailed by the guarantee, as the multilateral lender would subject the Infrastructure Provider procurement to “full technical, legal, and financial due diligence.”

As policy responsible department, Defra was liable for managing the guarantee. But financial management would not just overwhelm the Department’s eroded administrative capacities, making it vulnerable to capture from investors. 36 Any call on support was also likely to exceed the Department's budget, which annually was around half the value of the Thames Tideway Tunnel. Building up capability, however, would be time-consuming and eat into its budget—resources Defra did not have. One of the investors later marveled at the EIB’s involvement, as he deemed it unnecessary from a financial perspective: “I think on some projects [EIB investment] is absolutely necessary, but I would say for Thames Tideway we would actually get the money without the EIB.” 37 Defra explained in the Outline Business Case submitted to the treasury to gain final approval for the guarantee, “[we] delegate some or all of that [financial management] role if e.g. the EIB comes in and undertakes its detailed credit analysis.” 38 In November 2014, the European Investment Bank confirmed that it would lend up to £1 billion to the Infrastructure Provider.

Investment infrastructure: Bypassing constraints and harnessing finance

The operationalization of the guarantee offers a window onto how public financial experts can design investment infrastructures to bypass constraints and harness market-based finance for policy. When Infrastructure UK confirmed the Government Support Package in June 2014, it triggered a formal state aid review from the European Commission. The competent DG Competition considered “the [Government Support Package] and the [Infrastructure Provider] charge benefitting the [Thames Tideway Tunnel] project to constitute State aid.” 39 But Infrastructure UK had designed the instrument so that it afforded “just enough” support to make the project financeable and that it responded only to cost overruns that exceeded the Threshold Outturn. 40 Further, while under EU law the charge levied for the Thames Tideway Tunnel was accountable as a tax and not as an off-balance sheet service charge, Thames Water’s team had devised the instrument in line with the logic of the UK’s environmental sector that the costs of investment are spread across regional customer bases. 41 In negotiations with the European Commission, Infrastructure UK agreed to adjust the fees charged for the guarantee and to cap the value up until Defra would provide support and argued that the Infrastructure Provider maintained “current and established billing practice” in the environmental sector. On 12 August 2015, the EU cleared the UK of state aid. 42 One of my interviewees explained, “[the clearance] was expected, and with all of these things […] it is never perfect, but it is good enough.” 43

The hybrid and multilevel investment setting enlisted institutional investors for the implementation of the Thames Tideway Tunnel and averting European infraction fines at costs that were politically acceptable. On 14 July 2015, Thames Water selected “Bazalgette Limited,” the institutional investor consortium, as the preferred bidder based on an 2.497% Weighted Average Cost Capital bid. This commitment was more than 1% lower than the industry-wide regulatory determination of 3.85% for operational utilities, which Ofwat had adjusted downward from 5.1% in April of the same year. On 24 August 2015, Bazalgette selected three engineering consortia for the construction works, which all had submitted bids at the lower end of cost estimates. Subsequently, Thames Water revised the estimate for how much the Thames Tideway Tunnel would increase average water bills down from £80 annually to below £25.

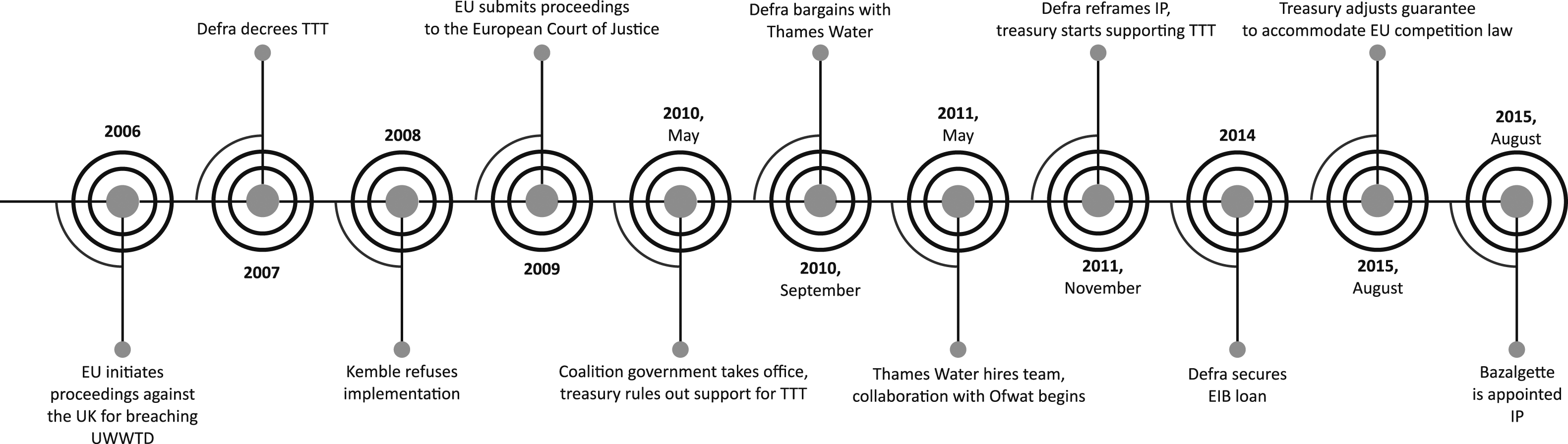

44

Figure 3 provides an overview of the key events in the policy's implementation. Timeline for the implementation of the Thames Tideway Tunnel (source: the author’s own creation).

Discussion

The Thames Tideway Tunnel is a paradigmatic case of public policy implementation in a fragmented policy environment. As such it offers a window into the mechanisms of state capacity in European political economies, as their policy spheres are increasingly marked by denationalization trends. Along with financial market re-regulation and austerity, the British state pioneered market-based modes of collective service delivery. It privatized the environmental sector in part to avoid government spending required by EU membership. This created privately owned regional monopolies, which under the auspices of Defra and the supervision of three regulators rely on market-based investors for national and European policy. In lockstep, the British state slashed the budget for environmental policy, making Defra one of the weakest departments within its hierarchies. Research shows that as a result of the transformation of capitalism and the European integration process, EU member states have migrated authority sideward, upward, and downward (Le Galès and King, 2017) and institutionalized consolidation policies along with policy reliance on market-based finance (Schwan et al., 2020, Wansleben, 2023). At the same time, the emergence of the climate crisis generated significant investment needs that alongside other challenges overwhelm existing state capacities. The crises since 2008, and the national and supranational responses these triggered, intensified these dynamics (Armingeon et al., 2022, Schelkle and Bohle, 2021). The European Union and its member states created new instruments and budget lines to fortify their investment states. And at least nominally, they doubled down on their climate ambitions. Because of this convergence trend, this paper argues the theoretical implications derived from the analysis of the Thames Tideway Tunnel are generalizable to fragmented policy environments in Europe’s political economies.

This paper makes three contributions to the literature. First, it develops an in-depth case study of how policy elites set up a market-based investment setting with investment state capacities (Mertens and Thiemann, 2018). It highlights the complex state–finance entanglements underpinning assetization work (Birch and Muniesa, 2020) and the multilevel and political dimension of investment capacities.

Second, this paper advances the debate on state capacity in financialized political economies (Schelkle and Bohle, 2021; Gabor, 2023) by studying how public policy officials use financial statecraft to overcome the governing challenges they face. By analytically separating public policy into its objectives and instruments of implementation (Lascoumes and Le Galès, 2007), it demonstrated that public policy officials engaged with finance instrumentally and not on ideological grounds (Quinn, 2017). Their financial bricolage can build islands of state capacity in fragmented policy environments when it pursues crucial policy objectives and combines investment capacities from different levels. Put in a nutshell, states, as endogenous market participants, can overcome adverse conditions and create new opportunities for governance by shaping market conditions, despite the inherent uncertainties and challenges involved (Wansleben, 2023).

Defra decreed the Thames Tideway Tunnel to avoid blame for longstanding environmental policy failures in the Greater London Area. But the Department’s implementation capacity was undermined by the regulatory regime for the environmental sector, the treasury’s austerity policy, and Thames Water’s refusal to risk shareholder value in financing the massive undertaking. Defra chose the Infrastructure Provider to bypass these constraints. This choice aligned Thames Water’s shareholders and the industry’s economic regulator with designing the Infrastructure Providers to finance the Thames Tideway Tunnel in capital markets and off the national accounts. An expert team hired by Thames Water collaborated closely with Ofwat to blend the regulatory mechanics of the environmental sector with the commercial principles of the Private Finance Initiative and engineer a risk-return profile that emulated an operational utility but capped financial gearing. To safeguard the success of this strategy, Defra reframed the Infrastructure Provider as in the strategic national interest to convince the treasury to layer a guarantee onto the investment setting. Interweaving the Department’s budget with the Infrastructure Provider, the instrument made the project financeable for institutional investors and so harnessed the procurement timeline of merger and acquisition markets for expediting the implementation of the Thames Tideway Tunnel. While the guarantee de-risked, de-risking remained incomplete. While it allocated uncontrollable risks to Defra, it left some risks with investors so that it would sit off-balance sheet and receive state aid clearance from the European Commission. And because the responsibility for the instrument remained with Defra, the Department secured a loan from the European Investment Bank to source the financial management expertise from the multilateral institution for its entrepreneurial strategy.

Defra’s financial bricolage, in short, built an island of state capacity within the boundary conditions defined by the UK’s environmental sector and its macroeconomic regime. Experimenting with financial innovation and orchestrating investment capacities from different levels of government, Defra mobilized £2.4 billion from institutional investors for avoiding blame and redressing longstanding environmental policy failures in the Greater London Area. It required investors to accept risks and induced these to commit to returns that were 1% lower than those earned by the shareholders of operational utilities. As a result, customer bills in the Greater London Area increased significantly less relative to what they would have if investors had been rewarded at the level Ofwat allowed for in the sector at the time of instrument design. And they increased only by a fraction if compared to alternative market-based modes of delivery, importantly the Private Finance Initiative.

Third, this paper sheds light on the unstable institutional foundations underpinning financial statecraft and the iterative state interventions these require to avoid policy failures. This analysis expands research on the politics and limits of market-based financial systems from macroeconomic policy into public policy (Braun, 2018). The paper shows that since the 1990s, British state elites have engineered and stabilised significant parts of infrastructure and service delivery as state-finance hybrids. This finding problematizes dualistic accounts of state–finance relations, in which state action is a mere framework condition for financial action (Allen and Pryke, 2013, Bayliss et al., 2022).

Following the successive rounds of privatizations, New Labour legislated the Private Finance Initiative, which overseen by Partnership UK, delegated the implementation of public policies to the private sector. Both instruments used market-based investments for off-balance sheet policy making, and both tapped into lending from the European Investment Bank to better the terms of financing. Both instruments, however, failed to steer investments commensurate with the development of the UK’s political economy and exposed collective services to the dynamics of market-based finance. The regulatory regime for the environmental sector delivered services at an efficient price, but also created an opportunity for shareholders to raise debt for dividend payouts instead of capital development. And to avoid balance sheet implications, the Private Finance Initiative allocated risks to the private sector so comprehensively that it only implemented routine investments and these at such a high cost that the treasury had to subsidize them. The 2008 financial crisis crystallized these vulnerabilities. Alongside emergency measures, the Coalition government responded by nationalizing Partnership UK and re-instituting it as public expertise unit Infrastructure UK, which it tasked with operationalizing financial instruments that unlock capital market investment. Defra aligned the treasury with deploying these capacities to support the Infrastructure Provider, designed to overcome the limits of both the regulatory regime for the environmental sector and the Private Finance Initiative. Today, the instrument is further trialed in major projects delivery, such as the new nuclear power plant at Sizewell. In January 2020, the UK withdrew from the EU, cutting its investment state off from the European level. In June 2021, the UK launched the UK Infrastructure Bank. A couple of months later, the COVID-19 pandemic hit, putting major strains on cash flows in market-based infrastructure. In March 2022, Ofwat agreed to amend the Infrastructure Provider’s license to share the fallout with equity investors.

Conclusion

Now at its conclusion, this paper highlights the normative paradox of financial statecraft in modern political economies (Woll, 2017). On the one hand, the literature powerfully demonstrates that financial statecraft creates vast opportunities for finance, erodes democratic processes, and leads states to shoulder asymmetric risks. The analysis developed here further shows that investors, in their role as financiers of collective goods and services, can pass on the costs of external shocks and financial market volatility to governments and their citizens, along with those associated with strategic planning, all the while cashing in on the opportunities.

On the other hand, this paper illustrates that in many countries and contexts, financial statecraft will need to play a role in addressing the climate crisis. As such, it cannot and should not be reduced to a captured process where state actors pursue policies solely in the interest of finance. Addressing the climate crisis urgently requires massive investments and a profound restructuring of modern political economies. This transformation hinges on strong and proactive state intervention, even as state capacities have been weakened by decades of neoliberal reforms, financialization, and cascading crisis events. However, the (re)building of public institutional capacities able to meet the investment needs alongside those of other pressing societal challenges will be a lengthy and uncertain process, if achievable at all. For Europe alone, the European Commission estimates that an additional €3.5 trillion must be invested between 2021 and 2030 relative to current levels to fulfill the block’s obligations under the Paris Accords. 45 Thus, we need more and comparative research to understand financial statecraft as a problem-solving strategy under adverse conditions. This research should further specify the administrative features and strategies that enable financial statecraft to implement crucial policies, share risks with investors, and tie conditionalities to public support.

Footnotes

Acknowledgements

This paper benefited immensely from comments made by Leon Wansleben. I am grateful to Matthias Thiemann and Patrick Le Galès for their suggestions and insights. I am thankful to Cornelia Woll for her remarks, which helped me develop the framework for the analysis. Lastly, I gratefully acknowledge the constructive remarks made by the two anonymous reviewers and the editors. All errors are mine.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Notes

Appendix

The ID abstracts as follows: Finance groups interviewees that worked in finance outside of UK public finance, for example, equity investors but also the EIB; Private positions in corporations such as Thames Water; Central and urban, positions in government and regulators, including Defra, the treasury, and Ofwat; Other, positions in advisory. 1. Urban.London.05/04/16. 2. Finance.London.07/04/16. 3. Finance.London.11/04/16. 4. Urban.London.14/04/16. 5. Finance.London.25/04/16. 6. Private.London.28/04/16. 7. Central.London.03/05/16. 8. Central.London.05/05/16. 9. Private.London.10/06/16. 10. Central.London.12/05/16. 11. Private.London.16/05/16. 12. Central.London.16/06/16. 13. Other.London.21/06/16. 14. Private.London.30/06/16. 15. Central.London.05/07/16. 16. Central.London.06/07/16. 17. Central.London.14/07/16. 18. Central.London.19/07/16. 19. Central.London.22/07/16. 20. Private.London.22/07/16. 21. Private.London.26/07/16. 22. Central.London.11/08/16. 23. Finance.London.12/08/16. 24. Urban.London.16/08/16. 25. Central.London.17/08/16. 26. Other.London.22/08/16. 27. Private.London.23/08/16. 28. Other.London.24/08/16. 29. Central.London.26/08/16. 30. Central.London.06/09/16. 31. Urban.London.06/09/16.