Abstract

Small states play a critical role in the operation of the Global Wealth Chains, storing capital assets and funnelling financial flows. However, the knowledge of how such practices of financial transit emerge remains scant. Focussing on the 1990s as the formative decade of post-Soviet capitalism, the article focuses on the variegated financial internationalization in the Baltics, as Latvia developed a vibrant offshore banking sector, whereas Estonia pursued complete Westernization in bank ownership. Challenging the literature that relates the emergence of Baltic offshore finance with right-wing politics, and existing trade and cultural links with Russia, the article argues that the varieties of financial internationalization in the Baltics were due to ‘economic statecraft’ by the Central Banks (CBs). Drawing upon a survey of CB reports, parliamentary speeches, press archives, memoirs, and elite interviews, the article argues that the Baltic CBs’ path-setting decisions shaped the two distinct financial internationalization paths through three interventions: currency reforms, agenda setting, and banking regulation. Drawing on the literature on social embeddedness of CBs, the article attributes the differences in the two CB approaches to their informal alliances with broader society – domestic financiers in Latvia and the government in Estonia.

Keywords

Introduction

The past decade has demonstrated that small states can play a major role in the Global Wealth Chains, storing huge amounts of capital assets, funnelling illicit financial flows, and more generally, helping to engage in tax evasion, corruption, and money laundering (Sharman, 2017). The literature on Global Wealth Chains (GWCs) has it that global firms and individuals create and protect wealth by strategically planning links across multiple jurisdictions to control how assets are evaluated and governed (Seabrooke and Wigan, 2014, 2022). According to Bohle and Regan (2022), in the world of globally interconnected banking and finance, small states often carve out a specialist niche in the GWCs and thus play a disproportionate role relative to their size in serving the needs of global firms and wealthy individuals (Bohle and Regan, 2022). A prominent example is Ireland where global US firms – notably, in the pharma and tech sectors – are storing their intellectual property and capital assets (Bohle and Regan, 2022). Similar business models have been developed by Liechtenstein, Seychelles, and well as various tax havens in the British Commonwealth (Murphy, 2017; Palan et al., 2010; Shaxson, 2012).

Taking a European perspective, this article focuses on the under-researched Baltic states, which have served not as ‘treasure islands’ but as conduits of illicit wealth from the Commonwealth of Independent Countries (CIS) – mostly, Russia – to the West. The literature on Baltic banking has mostly focused on the role of foreign-owned banks, whose unrestricted lending to households fuelled large macroeconomic imbalances (Bohle and Greskovits, 2012; Grittersová, 2017; Pataccini, 2022). However, the dominant focus on financial internationalization to the EU periphery has come at the cost of underestimating the significance of financial internationalization from the EU periphery, where the Baltics have infamously facilitated illicit financial flows from the East (Pataccini, 2023).

Share of foreign bank ownership (%).

Source: Cull et al. (2017).

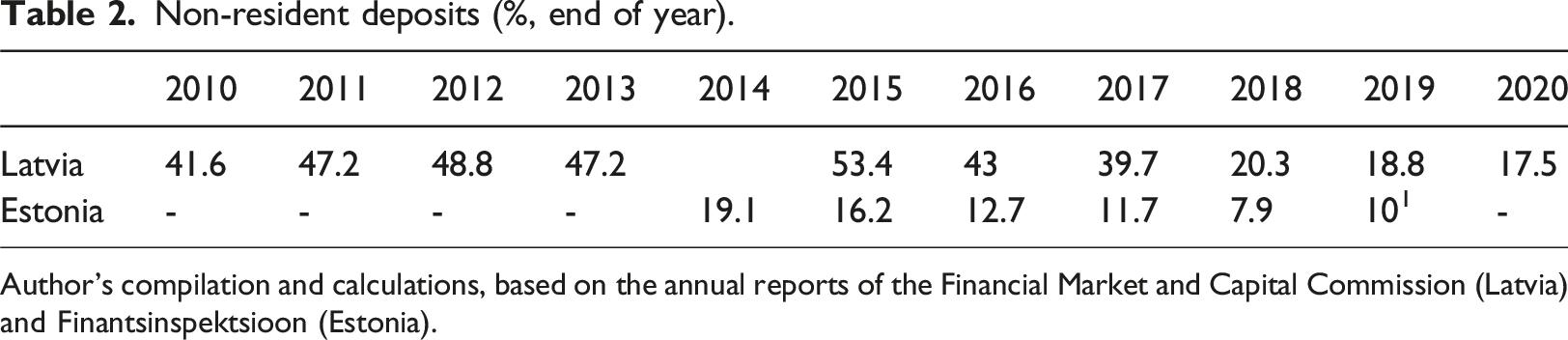

Non-resident deposits (%, end of year).

Author’s compilation and calculations, based on the annual reports of the Financial Market and Capital Commission (Latvia) and Finantsinspektsioon (Estonia).

Existing accounts of Baltic financialization tend to focus on right-wing coalitions shedding socialist legacies (Appel and Orenstein, 2018; Avlijaš, 2022; Bohle and Greskovits, 2012; Madariaga, 2020) and foreign financial capital embracing the opportunities in the single market (Becker et al., 2016; Pataccini, 2022). Meanwhile, the origins of entrepôt finance between East and West have mostly been linked to favourable geography, established trade (Hallagan, 1997b; Korhonen, 1996; Muižnieks, 2008) and cultural links with Russia (Berg and Oras, 2000; Sommers, 2018). However, none of these conditions can account for the distinct differences in outcomes between mostly similar Latvia and Estonia. Drawing on the recent literature on state developmentalism and industrial policy (Bulfone, 2022; Haffert, 2019; Haggard, 2018; Maggor, 2020; Naczyk, 2021) and the literature on ‘economic statecraft’ that explores how states boost domestic business capacities to compete against rival powers (Thurbon and Weiss, 2021; Weiss and Thurbon, 2021), this article analyses the role of Central Banks (CBs) in shaping the distinct financialization trajectories in the initial decade of post-socialist capitalism in the Baltics.

In line with the literature on ‘critical junctures’ (Capoccea, 2015: 147–148; Collier and Munck, 2022), it is argued that the CB interventions in (i) currency reforms, (ii) agenda setting, and (iii) financial regulation put the Baltic financial sectors on specific institutional paths, which then became entrenched over the following decades. First, besides the path-setting monetary reforms (Feldmann, 2001), the CBs stipulated the terms on which the new currency could be exchanged with the Russian rouble. The different approaches to the uncoupling from the Russian monetary system had far-reaching effects on the Baltic banking sectors. Second, and related, the CB governors articulated bold visions for financial development which then set the policy agendas for governments (Baumgartner, 2016). Third, during the first decade of post-socialist capitalism, CBs were the principal regulators of the financial and banking sectors (Juuse et al., 2019; Pataccini et al., 2019; Spendzharova, 2014), exerting substantial influence through both formal rules and strategic non-enforcement (Bowen and Galeotti, 2023; Dewey and Carlo, 2021).

Drawing on the literature on CB politicization and legitimacy (Johnson, 2006a, 2006b; McPhilemy and Moschella, 2019; Tucker, 2018), the article argues that the different approaches between the Latvian and Estonian CBs were due to their informal alliances with broader society – domestic financiers (Latvia) and government (Estonia). Based on an extensive survey of policy reports, parliamentary speeches, press archives, memoirs, and elite interviews analysed through the methodology of case studies and focused structured comparisons (George and Bennett, 2005), it shows that in Latvia, the CB’s vision of a financial hub between the East and the West embraced the existing practices of the Russia-oriented domestic banks. The BoL (Bank of Latvia) guaranteed lucrative profits to these domestic banks from exchanging non-convertible Russian rouble and supported them with favourable regulation. By contrast, the BoE (Bank of Estonia) – in close informal alliance with the Estonian government – rapidly uncoupled from Russia’s monetary system and sought full foreign banking ownership. To that end, the BoE kept exchanges of the Russian rouble strictly limited and effectively restricted illicit money inflows from Russia, thus nipping the domestic financial business with Russia in the bud.

The article is structured as follows. The theoretical framework discusses the two faces of financial internationalization in the Baltics as the main outcome of interest and develops a CB-focused framework conceptualizing the role of CBs and their informal alliances with society. The empirical section shows how the CB interventions regarding currency reforms, agenda setting, and banking regulation shaped the two distinct trajectories in Latvia and Estonia. I conclude by discussing the article’s main contributions and the long-term feasibility of the two distinct financial models.

Theoretical framework

Two faces of financial internationalization

The Baltic financial sectors are mostly known in the literature as cases of dependent financialization where, due to the extremely high foreign ownership, the key role is played by Scandinavian banks (Ban and Bohle, 2020; Bohle and Greskovits, 2012; Epstein, 2017). However, at a closer look, the Latvian and Estonian banking systems represent a striking diversity regarding ownership and specialization. In the formative decade of capitalism, the Estonian authorities put systematic efforts to upend the financial business with Russia and instead sought to increase banking standards by selling domestic banking operations to Western banks. Both the 1992 and 1998 banking crises led to significant consolidation of the financial sector, followed by a notable increase in Western ownership (Kraft, 2004; Sõrg et al., 2004; Spendzharova, 2014). By the late 2000s, Estonia had by far the highest levels of foreign banking ownership in the EU (98% in 2008) (Epstein, 2017). In contrast, Latvia pursued a mixed model where dominant Scandinavian banks serving Latvian residents operated in parallel with a vibrant sector of domestically owned banks serving illicit money from the East, most prominently, Russia (Pataccini, 2022, 2023). Table 1 shows the different proportions of domestic and foreign ownership in Latvian and Estonian banking. Table 2 shows the specialization in non-residential banking post-GFC.

In the 1990s, Russia’s rigged privatization processes and, particularly, the infamous ‘loans-for-shares programme’, meant a massive transfer of assets from the state to private individuals (Aslund, 2007). The Latvian domestic banks played a key role in providing short-term on-demand deposits to transit such newly created wealth to the international financial system through a network of Western correspondent banks, such as JP Morgan, Deutsche Bank, and Commerzbank (Aslund, 2017; Bohle and Regan, 2022). The path of non-resident banking was further consolidated in the following decades. After the 2008 financial crisis, Latvia doubled down on the strategy to attract wealth from the East through tax incentives, selling residence permits and loosening regulation to boost the economy (Eglītis et al., 2014). Between 2011 and 2015, the amount of non-residential deposits almost doubled (Jemberga and Puriņa, 2016; Pataccini, 2023). Remaining an open secret through the initial decades, the activities of Latvian domestic banks drew increased scrutiny from the international community in the aftermath of the GFC. The Latvian financial entrepôt was effectively upended after the bold intervention of the US Treasury, which observed ‘money laundering of an industrial scale’ and threatened to include Latvia in its ‘grey list’ (Aslund, 2017; Banka, 2023; Buckley, 2018; Eglitis, 2012; Moneyval, 2012).

Although the literature has increasingly appreciated the role of Latvian non-resident banking in global wealth management and financial value chains (Bohle and Regan, 2022; Pataccini, 2023), it has mostly remained silent on its origins in the formative decade of post-socialist capitalism, and why the two highly similar Baltic states opted for different paths, despite sharing most initial conditions. The Baltic penchant for unfettered markets has mostly been explained by right-wing governments embracing ethno-nationalist politics and the weakness of social actors (Appel and Orenstein, 2018; Avlijaš, 2022; Bohle and Greskovits, 2012; Madariaga, 2020), whereas the Baltic financialization has mostly been associated with the market-seeking strategies of the Scandinavian banks (Becker et al., 2016; Pataccini, 2022). Meanwhile, the literature on the origins of the Baltic states’ role in financial transit between the East and West has mostly focused on the role of geography, and commodities trade with Russia through the Baltic ports (Hallagan, 1997b; Korhonen, 1996; Muižnieks, 2008), as well as the role of Baltic Russian entrepreneurs (Berg and Oras, 2000; Sommers, 2018).

Yet, these shared conditions fall short of accounting for the Latvian and Estonian differences in financial internationalization. By bringing in the missing focus on the state, below I develop a framework that sees CBs as key players shaping the Baltic financial developments after the collapse of socialism.

Central banks and economic statecraft

Over the last decade, scholars have increasingly paid attention to how states can pursue a wide range of industrial and developmental policies to promote national businesses (Bulfone, 2022; Haffert, 2019; Haggard, 2018; Maggor, 2020; Naczyk, 2021). This article takes a step further and borrows from Weiss and Thurbon the concept of ‘economic statecraft’. Unlike industrial policy which encompasses any kind of state support aimed at economic activity regardless of objectives and drivers of motivation, economic statecraft presupposes specific state ambitions in a specific context of geo-economic pressures (Thurbon and Weiss, 2021; Weiss and Thurbon, 2021). Classic literature on economic statecraft has tended to focus on how powerful states can use economic policies, such as trade, investment, and economic sanctions, to achieve foreign policy objectives (Baldwin, 1985; Cohen, 2018; Drezner, 1999; Mulder, 2022). Following more recent scholarship, the article analyses how states engage in economic statecraft by boosting domestic business capacities ‘to fend off, outflank, or move in step with clearly defined rival powers’ (Thurbon and Weiss, 2021; Weiss and Thurbon, 2021). As such, the notion of ‘economic statecraft’ is highly relevant for the newly independent Baltic states which, facing a rivalry between themselves as well as the former socialist states, had to craft developmental strategies to find a new balance between economic growth and geopolitical security (Lamoreaux and Galbreath, 2008). However, unlike the well-known cases of ‘economic statecraft’, such as the United States, China, Japan, and South Korea (ibid.), where the central role is played by governments and special state agencies, in the context of the Baltic financial internationalization article extends the application of ‘economic statecraft’ to CBs. Below I lay out the three types of CB interventions – currency reforms, developmental agenda setting, and financial regulation – and specify how they shaped the financial international trajectories in the two Baltic cases.

First, currency reform was a central part of the shift from a planned to a market economy. Having proclaimed their political and economic independence from Moscow in 1990, the Baltic CBs had to take a range of decisions that addressed not only the immediate challenges regarding the means of payment but also shaped economic and financial development more broadly. According to the literature, the key decisions concerned the liberalization of capital accounts, opting for a pegged or a floating exchange rate and determining the money supply in the economy (Evens and Quirk, 1995; Prasad and Rajan, 2008; Sutela, 2001). Although often presented in a technocratic fashion, these policies were highly ‘political’, having variegated distributional implications for different domestic sectors (Frieden, 1991; Gabor, 2010; Johnson, 2006a, 2016).

The two Baltic states are known for their rapid liberalization of capital accounts and radical monetary reforms – a strict peg to the IMF’s SDRs in Latvia (1994) and a currency board in Estonia (1992) (Feldmann, 2001). However, the literature has so far overlooked the significance of timing and speed of uncoupling from the Russian monetary system and phasing out of the Russian rouble as an exchange currency. The BoL made the Latvian interim currency (Latvian rouble) a legal extension of the Russian rouble, which effectively subjected the Latvian monetary policy to Russia. The temporary arrangement (until 1993) created lucrative speculation opportunities for the local financiers, effectively laying the groundwork for Latvian offshore finance. By contrast, in Estonia, the rapid introduction of the currency board in 1992 – and hence the elimination of the Russian rouble as an exchange currency – effectively separated Estonia from the Russian monetary system and prevented the emergence of domestic financial intermediaries engaging in currency arbitrage.

Second, the path-setting currency reforms were closely related to the process of creating visions about nation-building and economic development (Abdelal, 2001; Dobbin, 2008). To be sure, the Baltic preference for financial services as an alternative to a state-led economy (Zysman, 1983) was by no means a foregone conclusion, considering that the three states – especially, Latvia – were the most industrialized parts of the Soviet Union (Bohle and Greskovits, 2012). However, in contrast to the Visegrad states which integrated their socialist industries into the global production chains (Ban and Adascalitei, 2022; Pula, 2018), the Baltic leaders from the outset perceived the socialist industrial legacy as a liability and saw their economic futures in various services, not least, finance (Ban and Bohle, 2020; Bohle, 2014, 2017). Yet, their ideas and strategies of financial internationalization were markedly different – a fully foreign-owned banking sector in Estonia and a split model with a domestically owned offshore sector in Latvia.

Accounting for the ideological underpinnings of these ‘initial choices’, the literature tends to focus on the Baltic states’ right-wing governments which married neoliberalism with ethno-nationalist narratives favouring the respective titular nations (Avlijaš, 2022; Bohle and Greskovits, 2012). However, much less attention in the literature has been paid to the CBs, whose idiosyncratic visions for financial internationalization set the political agendas (Baumgartner, 2016) and disproportionally influenced the making of the Baltic financial sectors. Complementing and advancing the literature on post-socialist CBs, I introduce two analytical propositions that better capture the dynamics in the Baltic cases. First, I distinguish between the generic policy blueprints that were sourced in a one-size-fits-all fashion from the international CB networks (Johnson, 2016) and the idiosyncratic and place-based financial development strategies that were articulated locally. Second, I argue that agenda setting on the part of the Baltic CBs has mostly been due to the agency of a few individual ‘central bankers’, rather than the newly created institutions which during the first capitalist decade were far from ‘settled’ (Swidler, 1986). Below I demonstrate how the bold visions of the respective CB leaders were key for the financialization developments.

The third key intervention on the part of CBs regards financial regulation. Most literature tends to see the Baltic economies as especially loosely regulated, whose liberal focus was cemented by their accession to the EU’s single market (Juuse et al., 2019; Pataccini, 2022; Pataccini et al., 2019; Spendzharova, 2014). However, this international focus tends to ignore the domestic dynamics and significant differences between states. First, it tends to overlook that during the formative decade of post-socialist capitalism, macroprudential regulation and supervision of financial actors were a direct responsibility of the national CBs (Bowen and Galeotti, 2023; Juuse and Kattel, 2014). It was the CB that granted banking licences, set accounting standards and regulated the financial sector, before these functions – as a result of EU accession conditionality – were delegated to independent financial regulators at the end of the 1990s (Eihmanis, 2019a; Pistor, 2012).

Against the backdrop of Europeanization when the Baltic states converged towards the EU standards as a requirement for EU membership and welcomed many foreign players (Grabbe, 2005; Juuse et al., 2019; Pataccini et al., 2019), domestic agency remained key regarding the niche banking activities of non-residents. Throughout the crises of the 1990s, it was in the non-resident sector where the contrast between Latvia and Estonia was the starkest. The BoE proactively adopted European rules and strictly restricted operations with illicit money from Russia (Juuse, 2015; Laar, 2002; Spendzharova, 2014). In contrast, the BoL was not only slower in adopting and enforcing the EU banking standards. Unlike the BoE, where each crisis led to stricter regulation and enforcement, the BoL responded to the series of banking crises in the 1990s by carving out a preferential regulatory regime for non-resident banks (Fleming et al., 1996), which then became consolidated over the following decades (Bowen and Galeotti, 2023; Eglītis et al., 2014; OECD, 2015).

Recognizing the limitations of hierarchical steering, I argue that the differences between the two CBs and their imprint on the Baltic financial developments were due to their informal alliances with financial and government elites, which are broadly defined by a shared preference over political objectives (a specific type of financial internationalization) and cooperation in achieving them. As famously argued by Peter Evans, industrial transformation depends not only on state autonomy but also on its ‘embeddedness’ in the broader society (Evans, 1995). In a similar vein, Weiss and Thurbon (2021) have shown that the state can advance its objectives by collaborating with private actors under ‘governed interdependence’ (Weiss and Thurbon, 2021). Recent literature finds that even independent and technocratic CBs are socially embedded institutions that seek legitimacy from the broader society (McPhilemy and Moschella, 2019; Tucker, 2018). In the post-socialist context, differentiated social support for CBs has been identified as a key factor in accounting for the uneven progress in implementing the macro-orthodoxy (Epstein and Johnson, 2010; Johnson, 2006b).

Building on these accounts, I argue that integration in the broader society was key for the newly independent central bankers in the Baltics who took path-setting decisions regarding post-socialist economic development. However, the key difference was whether the CBs were integrated into the national democratic processes or collaborated with private actors and entities in the domestic financial sector to pursue their developmental visions. In the case of Estonia, CBs’ economic and monetary decisions were aligned with the broadly shared political preference of rapid separation from the Soviet bloc. By contrast, in Latvia, the central bank’s links and collaboration with narrow financial interests resulted in a development strategy (of becoming a financial bridge) which was at odds with dominant ethno-nationalist politics of shedding Soviet legacies and integrating into the West (Eihmanis, 2019b). In the following empirical section, I show the role of such informal alliances in the three types of CB path-setting interventions.

Empirical analysis

Currency reforms

Although the Latvian and Estonian CBs shared the orthodox view that economic stability should be pursued by tight monetary policies and fast capital account liberalization (Bakker and Chapple, 2003; Feldmann, 2000; Prasad and Rajan, 2008), their approaches regarding the exchange of Russian roubles differed. When articulating and promoting the new model of financial transit between the East and the West, the BoL openly sided with the domestic banks. It granted the domestic banks the ‘exorbitant privilege’ of exchanging the Russian rouble for convertible currencies in unlimited amounts, thus turning these domestic financiers into core players of the emerging non-residential banking sector. By contrast, the BoE shared the government’s view regarding full financial internationalization to the West and therefore kept the convertibility of the Russian rouble strictly limited.

Peg to the Russian rouble in Latvia

The BoL became operational in 1990 as a branch of the Soviet Vnesekonombank, taking over currency exchange operations, which at the time were highly regulated across the Soviet Union due to exchange rate risks (Fleming et al., 1996; Fleming and Talley, 1996). However, the BoL leadership did not espouse the regulated approach of Moscow and instead opted for a radically unfettered approach. The BoL governor Repše saw unlimited foreign exchange from Russian roubles as part and parcel of the broader package of economic transition, where foreign exchange markets had to be fully liberalized even before setting up an independent CB (Repše, 1993). Unlike his Estonian counterpart, Repše deliberately rejected any CB role in providing currency exchange: ‘The BoL is unequivocally opposed to the monopolization of currency exchange. There is no serious basis for such an idea, as it is quite clear that closing of small currency exchange offices will increase black market operations’ (Lapsa and Saatčiane, 2008).

As a consequence of a decision by the BoL, as of January 1991, Latvia became the only post-Soviet state with unlimited convertibility between non-convertible Russian roubles and Western currencies (Laar, 2002). The BoL openly allied with the domestic entrepreneurs, delegating them the function of foreign exchange between convertible Western currencies and non-convertible Russian roubles. In April 1991, the BoL granted the first currency exchange licence in the former Soviet Union to Parex Bank, an established currency dealer facilitating a significant share of trade transactions from Russia and Ukraine. Riga was turned into the largest cash market in the former Soviet bloc, attracting huge amounts of rapidly inflating Russian roubles from all over the crumbling empire (Laar, 2002; Lainela and Sutela, 1994). As recalled by Valery Kargin, the co-founder of the Parex bank, the first and the largest player in the sector: ‘The process reached such a scale that sometimes we sent several cash-stuffed TU-134 aircraft a week to the Russian regions of Orenburg, Siberia, and don’t know where yet. We embarked the cash, and the plane took off with security men, cashiers and often the cash owners themselves’ (Kargins, 2005).

However, even if the massive financial inflows led to overheating of the Latvian economy – for example, in 1992, inflation reached almost a thousand percent – the Latvian CB continued to accept Russian roubles and converted them to ‘hard’ Western currencies. As argued by Governor Repše in June 1992: ‘We are ready to uncouple from the [Russian] rouble if … the Bank of Russia does not hold its ground [and devalue] … for now, there is no such threat. I hope that Russia will hold on’ (Saeima, 1992). However, the massive inflow of Russian roubles continued even after August 1992 when the BoL introduced differentiated exchange rates to accommodate for inflationary dynamics in the Russian rouble zone (Lainela and Sutela, 1994). It took as long as January 22, 1993, for the BoL to regain control of monetary policy by ‘cutting the naval string with the Soviet monetary system’, as retrospectively assessed by the BoL (Bitāns and Purviņš, 2005: 144–145). In February 1994, after an extended period of extremely tight monetary policy, the BoL decided to peg the Latvian currency to the IMF’s Special Drawing rights. Yet, the protracted integration into the Russian monetary system proved to be highly formative to Latvian non-residential banking. In 2005, the BoL acknowledged that Latvia’s emergence as an ‘important financial centre for international settlements of the former USSR republics…was facilitated by the liberal currency market and free currency convertibility’ (ibid. p. 152).

Rapid uncoupling from the Russian rouble in Estonia

In stark contrast with Latvia, the Estonian authorities preferred rapid separation from the Russian monetary system (Madariaga, 2017: 651–653; Raun, 2001: 24–25). An important role in shaping this determination was played by the Estonian 1992 banking crisis when Moscow froze foreign banking assets. This led to an emerging consensus between the BoE and the government that Estonia’s prosperity and growth could only be found by integration into the West (Fleming et al., 1996). As Ardo Hansson, a key architect of the Estonian monetary reforms and a subsequent BoE governor (2012–2019) told this author: ‘Losing that money in Russia, that was such a painful lesson, that you did not dare to go to that business again… I don’t know whether there was a fundamental vision [initially] other than a bias towards anything Western’ (Hansson, 2022).

Regarding integration into the Western economic system, the most consequential decision by the BoE was the introduction of a currency board which tied the Estonian kroon to a basket of Western currencies. If the Latvian rouble was initially a legal extension of the Russian rouble, the supply of Estonian kroon was strictly tied to the available Western currency reserves (Hansson and Sachs, 1994; Lainela and Sutela, 1994). Although viewed by the IMF as a step too far, the currency board served the Estonian authorities’ geo-economic objective to uncouple from Russia and, according to one insider, was a ‘realistic [solution], given our [limited] skills, education, and experience’ (Laar, 2002). Furthermore, the BoE’s swift introduction of the currency board was paired with the restrictions on the exchange of non-convertible Russian roubles, thus protecting the economy from a massive influx of Russian roubles from CIS and reducing the business opportunities for domestic bankers working with Russia. Estonia deliberately eschewed Latvia’s ‘very liberal’ approach with no limits on the exchange between the newly introduced currency and the Russian roubles (Laar, 2002, 2014). The BoE’s strict limits on the cash each Estonian resident could exchange effectively amounted to temporary capital controls. Ultimately, such restrictions directly stemmed from the hard constraint of the currency board, stipulating that new base money could be issued only with a corresponding increase in the convertible Western currencies (Fleming et al., 1996).

As Vahur Kraft, the CB governor between 1995 and 2005, explained to this author: ‘Only after some months, we liberated our capital control law, step by step. To a significant extent, such prudence was warranted by the currency board system, which imposed a hard constraint as to how much Estonian currency could be issued … There was a danger of speculative attacks against Estonian currency, and with capital controls, we avoided that’ (Kraft, 2022). This was confirmed to this author by Ardo Hansson: ‘When the banking [system] was set up in the rouble zone, your currency was … the base currency … and the risks came from dealing with Finish marks or dollars. However, the moment you did this rigid pegging to the DM, you drastically reduced all the risks looking at the West, and all the risks dealing with roubles suddenly accelerated. That alone encourages a lot of re-orientation’ (Hansson, 2022). In sum, the rapid introduction of a currency board against the backdrop of the 1992 banking crisis effectively helped the BoE to close off the economy to Russian roubles with far-reaching consequences on the development of the banking sector (Hirvensalo, 1994; Korhonen, 1996). During the 1990s, these interrelated decisions by the BoE effectively set Estonia on a markedly different financial development trajectory, nipping the emergence of domestically owned offshore finance in the bud.

Agenda setting

The contrasting approaches towards currency reforms and the Russian rouble were inspired by broader visions regarding financial and economic development put forward by the Baltic central bankers closely cooperating with their informal alliances in the domestic financial sector (Latvia) and government (Estonia). In the following section, I show how the BoL promoted the vision of Latvia as a financial hub between the East and West, whereas the BoE’s vision centred on rapid uncoupling from the Russian monetary system and complete Westernization of the banking sector.

Towards Latvia as a financial entrepôt

The idea of Latvia as a financial offshore was first put forward by the BoL governor Einars Repše (1991–2001). A physicist by training, Repše was a self-taught monetarist who believed in an open economy and conservative monetary policy leading to stable prices (Bohle and Greskovits, 2012). He explicitly aspired to turn Latvia into an international financial hub, modelled after Switzerland (Aslund, 2017; Bohle and Regan, 2022; Lainela and Sutela, 1994). Repše was closely allied with Ilmārs Rimšēvičs, his deputy governor (1992–2001) and successor (2001–2019) who executed and anchored the vision throughout the three post-socialist decades. As early as 1992, Rimšēvičs argued that ‘[i]f a financial system was created in Latvia that could serve both the East and the West, we would become another small Switzerland. That would be a huge achievement – this is how Latvia could rise’ (Latvijas Jaunatne, 1992). In their shared vision of Latvia as a financial bridge, the two central bankers openly allied with the domestic financial elites, building on the well-established practices of currency exchange in Riga in the 1980s (Kargins, 2005; Sommers, 2018; Sommers and Briskens, 2021). The BoL explicitly wanted to cultivate domestic financial capital, rather than attracting foreign investors. As Rimšēvičs argued at the time: ‘We must promote the development of the Latvian financial market in every possible way – but by relying on our forces. If we let foreign banks here, Latvian commercial banks could barely survive here’ (Latvijas Jaunatne, 1992).

In stark contrast with Estonia, the relations between the BoL and the Latvian governments remained tense throughout the 1990s. Although all post-transition governments of the 1990s espoused geopolitical neutrality to take advantage of the strategic location between the two geo-economic blocs (Austers, 2016: 212–218), the politicians remained hesitant about direct financial engagement with Russia. This was mostly due to prevailing ethnic nationalism, specifically, over such issues as the Soviet industrial and military legacy, citizenship, language, and rights of the Russian-speaking population more generally (EIHMANIS, 2019; Muižnieks, 2006). The dominance of such topics in the mainstream political agenda enabled the BoL to take a lead in the ‘quiet politics’ of financial governance (Culpepper, 2016), enabling it to proactively pursue its vision of non-residential financial services as a national development strategy (Aslund, 2017; Bohle and Regan, 2019).

However, when the Latvian economy was flooded with inflationary Russian currency as a result of the ‘no-limits’ convertibility of the Russian rouble (Bitāns and Purviņš, 2005: 144), the BoL’s approach, including the shadowing of the Russian rouble and favouritism towards the domestic financiers, was openly questioned by the Godmanis government (Saeima, 1992). The transcripts of the Latvian Supreme Council debates between June and October 1992 – the crucial period of the Latvian monetary reform – reveal fierce clashes between the CB governor Repše on the one hand, and Prime Minister Godmanis, who threatened to curtain the CB’s power by establishing a state development bank. According to Godmanis, such an institution would supposedly not only be more responsive to the credit needs of the economy but also take over the function of foreign exchange, which at the time had been fully delegated to private actors, such as Parex (ibid). In sum, in pursuing its vision of a financial entrepôt, the BoL directly built on the established business practices by domestic financiers, while keeping the elected government at arm’s length.

Towards foreign-owned banking in Estonia

In stark contrast to Latvia, in Estonia, the financial reform process was guided by the vision of increasing Western ownership, which then would help the economy as a whole. As a former BoE governor explained to this author, from the start the Estonian strategy was to attract foreign capital: ‘The BoE played a major role in that [process], first inviting international and multi-national institutions to the market, and later private banks came on their own’ (Kraft, 2022). Unlike Latvia, the Estonian monetary reform of 1992 was adopted by consensus between the BoE and the Laar government which closely cooperated both regarding the development of a strategic vision as well as its technical implementation. As recalled by Ardo Hansson, the BoE and government officials worked shoulder-to-shoulder, although the ‘technical capacity and expertise mostly came from the CB’: ‘At the time, I was an advisor to [the Prime Minister] Tiit Vähi, and it was purely about monetary reform, although the main work was more with [the governor of Eesti Pank] Siim Kallas. I was officially in Toompea, with the government, but the daily activities of preparing for the monetary reform were still at Eesti Pank’ (ERR, 2021). In an interview with this author, Hanson confirms: ‘It was quite consensual in the sense that it depended on few people who happened to get along reasonably well … everybody was pulling in the same direction’ (Hansson, 2022). Such unity was key to withstand the economic pressures and social grievances due to the rapid introduction of a currency board. As recalled by the then PM Laar, the societal pressures against the authorities included ‘attempts to topple the government using all kinds of methods … stand-off in the parliament … and demonstrations by incited pensioners in front of the parliament building’ (Laar, 2002). However, the BoE was able to withstand these pressures due to the shared consensus with the Laar government in power (Aslund, 2007; Bohle and Greskovits, 2012).

In addition, the Latvian and Estonian approaches markedly differed regarding their relationship with the domestically owned banks and their relationship with Russia. If the BoL openly cooperated with the established domestic financiers profiting from the exchange of Russian roubles, the Estonian authorities acted against such domestic financial interests. After the 1992 banking crisis (see above), PM Laar and the BoE governor Siim Kallas made it clear that the state would not bail out the collapsing banks which had engaged in high-risk operations, most notoriously, with Russia (Fleming et al., 1996; Laar, 2002; Madariaga, 2017). As noted by Prime Minister Laar, the state authorities pursued a ‘politically motivated resistance … against the influx of Russian capital’, stepping up regulatory standards and making financial transactions with the CIS countries increasingly difficult (Laar, 2002; Sõrg et al., 2004). Subsequently, the BoE significantly consolidated the banking sector, and the total number of banks in Estonia diminished from 43 in 1992 to 23 in 1993 (Lainela and Sutela, 1994). As demonstrated in the following section, the BoL then sought to improve the financial governance standards through rapidly increasing foreign ownership. According to a retrospective account by the Estonian Ministry of Foreign Affairs (2009): ‘With harsh measures, the government made it abundantly clear that Russia’s dirty money was not welcome in Estonia. After a few attempts, this was understood’ (Ministry of Foreign Affairs, 2009).

Financial regulation

As a broader trend in the ECE region, in the late 1990s, the Baltic states adopted European banking standards as part of EU accession conditionality, in line with the increasing share of financial internationalization to the West (Grabbe, 2005; Juuse et al., 2019; Pataccini et al., 2019; Pistor, 2012). However, unlike the BoE which imported higher regulatory standards through letting foreign financial capital, the BoL’s policy was aimed at retaining the regulatory perks to maintain Latvia’s advantage as a financial hub. Besides attracting foreign banking capital (initially, Estonian, then Scandinavian), the BoL cultivated a domestically owned banking sector that mostly worked with non-residents. In the 1990s, the BoL’s regulatory policy cemented the dominant role of Latvian domestic banks in the financial transit business from the East.

Selective regulation in Latvia

The 1992 Commercial Bank Law specified a few prudential regulations over six pages, providing full discretion to the BoL (Hansson and Tombak, 2011). In 1995, the BoL supervised as many as 79 licenced credit institutions, including 63 commercial banks. Many of them engaged in Ponzi schemes promising depositors an annual interest above 100%; others specialized in funnelling wealth from the CIS (Bank of Latvia, 1996; Bitāns and Purviņš, 2005; Hallagan, 1997a). The light-touch regulatory framework was hardly enforced, if at all. As early as the mid-1990s, the BoL noted that although the banking regulations were in line with EU directives, they ‘did not have the force of law’ (Bank of Latvia, 1996: 27).

The 1994–1995 banking crisis questioned Latvia’s increasingly financialized economic model and the regulatory framework behind it (Fleming et al., 1996; Fleming and Talley, 1996). The anger of domestic depositors over the lost savings – mostly in Banka Baltija, the then-largest domestic bank – put pressure on the political class and constituted a ‘to be or not to be’ moment for the Latvian offshore finance sector (Austrālijas latvietis, 1995; Saeima, 1995). The BoL was hard-pressed to step up the regulatory framework which endangered the very survival of Latvia as a financial hub. Illustrating how high the stakes were in the mid-1990s, a prominent Latvian economist argued that ‘the hope of becoming a second Switzerland’ could only be saved if the favourable geographic monetary and cultural preconditions were complemented with ‘appropriate banking legislation and supervisory framework … ensuring the two main factors: security and confidentiality’ (Krastiņš, 1995).

However, in line with its vision of a financial hub, the BoL openly sided with the established domestic financiers. Its regulatory policies favoured the domestically owned banks serving non-resident depositors in the CIS countries. While significantly stepping up regulation for the ‘core’ banks serving households and businesses, the BoL hardly changed the regulation for ‘non-core’ banks that exported their services abroad (Fleming et al., 1996). Out of 39 banks that were allowed to operate, only 14 were allowed to accept domestic deposits, whereas the other 25 banks specialized in serving clients from the CIS states (Bank of Latvia, 1996). The 1998 Russian crisis – when Moscow’s debt moratorium imposed significant losses on the Latvian domestic banks holding Russian government debt 2 – was another test for the BoL’s alliance with the domestic financial interests and its relations with Russia. Similar to the 1995 crisis, the BoL hesitated to act against the interests of domestic non-residential finance, which continued to grow in the following decades (Bowen and Galeotti, 2023; Pataccini, 2023).

Although the integration into the EU improved the regulatory standards overall (Bukovskis, 2022), the state authorities indirectly supported the sector through purposeful non-enforcement (Bowen and Galeotti, 2023; Dewey and Carlo, 2021). Having required establishing an independent financial regulator as part of the acquis (Eihmanis, 2019a), the EU constantly fell short of winding down the Latvian non-residential banking practices, including through the hard conditionality of the Balance-of-Payments programme and euro accession (Eglītis et al., 2014; OECD, 2015). It was only in the late-2010s as the United States leveraged its security guarantees vis-à-vis Latvia, when the Latvian authorities carried out comprehensive cleansing, effectively closing down the non-residential banking sector (Banka, 2023; Buckley, 2018; Meyer et al., 2018).

Conservative regulation in Estonia

From the early 1990s, the BoE pursued a more conservative regulatory policy than the BoL, demanding higher capital adequacy ratios and provisions against bad loans than required by international standards. After the 1992 banking crisis when Estonian assets were frozen by Moscow, the BoE became one of the ECE leaders in banking supervision and enforcement capabilities in line with the International Accounting Standards (IAS) (Bank of Estonia 1993, 1994, 1995, 1996; Kraft 2004). Bank supervision allowed the BoE to maintain a risk-averse supervisory approach throughout the 1990s (Spendzharova, 2014: 7–8). Throughout the 1990s, the BoE significantly increased the levels of foreign ownership, aiming to increase the governance standards and provide emergency financing in times of crisis (Hansson, 2022; Kraft, 2022; Spendzharova, 2014: 7). As the former CB governor Vahur Kraft (1995–2005) told this author, the BoE’s was deeply concerned that the Estonian domestic banks would fail and would have to be saved by the state. The BoE aimed to prevent such a scenario through increasing foreign ownership: ‘We at the CB had lots of meetings in international forums, at the IMF and the World Bank, EBRD where we invited foreign banks to Estonia. And the reason was better governance, clear ownership, and equity capital…This was a clear strategy’ (Kraft, 2022).

The 1998 Russian crisis and the debt moratorium further enforced the Estonian trajectory towards regulatory upgrading by attracting foreign financial capital. The consolidation of the domestic banking sector effectively upended Eesti Forekspank, the last major domestic outlet serving non-residents from Russia. After the takeover by the BoE, in 2000, the newly created Optiva Pank was sold to the Finish-based Sampo Bank and in 2007 acquired by Danske (Bruun & Hjejle, 2018). By the late 1990s, the Estonian banking sector was overwhelmingly foreign-owned, dominated by two Scandinavian banking groups – Foreningssparbanken (Swedbank) and Skandinavska Enskilda Banken (SEB) (Kraft, 2004; Sõrg et al., 2004).

Conclusions

The article has analysed the political origins of the variegated financial internationalization paths in the Baltics in the 1990s as the formative decade of Baltic capitalism. While Latvia strategically developed a domestic banking capacity to serve as a financial hub between the East and the West, Estonia made a systematic effort to eschew the financial business with Russia early on and, instead, pursued full financial integration in the West through increasing foreign ownership. Complementing the existing accounts that focus on right-wing ideology, underdeveloped social mobilization, and the legacies from the Soviet period, the article has pointed to the critical role of the path-setting decisions by the CBs which, drawing on their informal alliances with domestic financiers (Latvia) and government (Estonia), shaped the initial trajectories of financial development through currency reforms, agenda setting, and financial regulation.

Besides shedding light on the origins of the two financial internationalization trajectories, the article’s other contribution lies in showing the mechanisms of CB influence on the Baltic developmental policy after the collapse of socialism. It has demonstrated that the CBs played even more prominent roles than previously assumed, as the pet visions of CB governors shaped the Latvian and Estonian financial and economic developments for the decades to come. Although the article focuses on the Baltic states, its findings confirm the general scholarship associating the rise of offshore finance with national self-determination within crumbling empires (Murphy, 2017; Palan et al., 2010; Shaxson, 2012).

Retrospectively, the Estonian strategy of enforced Westernization has proven relatively more sustainable than the Latvian strategy of a bridge between the two geo-economic blocs. First, during the financial crisis, almost total foreign ownership allowed Estonia to push the banking adjustment costs onto the Scandinavian parent banks, whereas Latvia had to repeatedly rely on the domestic taxpayer and foreign creditors (Epstein, 2014). Second, the Latvian strategy of developing a vibrant offshore sector has imposed significant costs in terms of the uneven development of the real economy, widespread corruption, and damaged international reputation (Bohle and Regan, 2022; Meyer et al., 2018; O’Donnell and Gelzis, 2019). Nevertheless, the recent Baltic banking scandals have also shown that money laundering has been the prerogative not only of the domestic niche banks but has also been practised by Scandinavian household names, such as Swedbank, SEB, and Danske (Bruun & Hjejle, 2018; Milne, 2019; Ylönen et al., 2023). The Baltic experience thus serves as a welcome reminder of the contingency inherent in financial development (Collier and Munck, 2022), as well as of the bounded agency of small open economies located between competing geo-economic blocs.

Footnotes

Acknowledgements

I am grateful for the thorough comments from Raul Toomla and the participants at the Research Colloquium at the Skytte Institute of Political Studies, University of Tartu. Earlier versions of the paper were also presented at the 7th The Role of the State in Varieties of Capitalism Conference (SVOC) in Budapest, 29-30 November 2021, and the Society for the Advancement of Socio-Economics (SASE) conference in Amsterdam, 9-11 July 2022. Not least, I would like to express my gratitude for the helpful comments of three anonymous reviewers and the Guest Editors of the Special Issue.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.