Abstract

Literature on the financialisation of infrastructure gives limited attention to public banks. Since public banks are key state institutions to enable and shape financialisation, more research is needed to show how they mediate financialisation processes amidst evolving social, political and economic pressures. To address the gap in existing literature, this article develops a case study on the UK Infrastructure Bank to examine how the bank enables financialisation whilst maintaining credibility with the United Kingdom's neoliberal-nationalist regime. The findings show that the UKIB is a centralised, technocratic institution which deploys de-risking interventions to attract private investment, including guarantees, equity shares and debt financing. Yet, these interventions enable projects which offer limited public value, such as debt financing to fuel over-investment in fibre broadband markets, or equity investments in infrastructure funds which perpetuate the dominance of short-term, extractive investment logics. To maintain credibility with the neoliberal-nationalist regime, the UKIB's governance strengthens the central government's power over its activities, allowing it to shape the post-Brexit policy agenda and target investment to specific constituencies. While the UKIB boosts the profitability of infrastructure assets for private investors, it also exposes regions to extractive logics that undermine the potential public benefits. The findings show how public banks can be used to coordinate and bolster support for financialisation, yet, the use of de-risking interventions to catalyse financialisation is often at odds with generating long-term public value.

Introduction

Public infrastructure assets, ranging from toll roads and water utilities to solar farms, have become increasingly financialized as states seek to develop novel financial instruments and governance arrangements to transfer responsibility for financing, ownership and operational management to private investors (Carolini and Cruxên, 2020; Christophers, 2023; Gabor, 2021). The financialization of infrastructure assets entails the transformation of physical assets and the services they provide into a profitable financial asset, by reconfiguring ownership, legal and accounting arrangements to secure revenue streams, control costs and mitigate or delegate financial risks (Ashton et al., 2016; O’Neill, 2013, 2017). Since infrastructure assets provide essential public services and often operate as monopolies, they present investors with an opportunity to extract rents, particularly where they can increase barriers to competition (Christophers, 2020: 282). Investors can also take advantage of the reliable revenue streams generated from infrastructure services to raise debt and engineer financial returns for investors (Lorrain, 2008; Pryke and Allen, 2019). However, the extent of financialization is uneven across different geographies and infrastructure sectors: many attempts to financialize infrastructure assets fail, and states negotiate substantial financial constraints, uncertainties and risks to successfully negotiate deals (Deruytter and Derudder, 2019; Pike et al., 2017).

The role of public banks in enabling the financialization of infrastructures has received limited attention in academic literature. It is neither inevitable nor necessary that public banks accelerate financialization. They could potentially catalyze definancialization by allocating finance through democratic structures, towards pro-public goals such as reducing inequalities or facilitating just transitions to climate change (Marois, 2021: 154). Yet, recent studies show a growing tendency for public banks to adopt profit-oriented logics or deploy public resources to de-risk private investment. De-risking involves the provision of subsidies, or taking responsibility for certain project or asset risks through equity stakes or guarantees, to enhance financial returns for private investors (Gabor, 2021). For example, the European Union mobilized public banks after 2015, using de-risking interventions to raise market-based finance for small and medium enterprices (SMEs) and infrastructure projects, to offset the austerity budgets imposed after the Global Financial Crisis (Mertens and Thiemann, 2018). In Turkey, the influence of the Justice and Development Party government’s neoliberal agenda and pressure from international financial institutions drove municipally owned Ilbank from financing public water infrastructures towards profit-generating urban real estate development and de-risking private investment (Marois and Güngen, 2016). The Canada Infrastructure Bank de-risks private investment, targeting projects that secure state access to natural resources in Indigenous territories (Stanley, 2019).

Despite the tendency towards profit-oriented logics, public banks still pursue diverse goals and financing activities. In the early stages of the COVID-19 pandemic, public banks demonstrated diverse responses to the major economic and financial crisis precipitated by lockdown measures. Italy’s Cassa Depositi e Prestiti and Germany’s Kreditanstalt für Wiederaufbau (KfW) offered emergency loans and aid for SMEs or self-employed workers (Marois, 2020; Vandone et al., 2020), while publicly - owned commercial banks in China were directed by the country’s central bank to sacrifice their profit margins to extend loans to SMEs, defer loan payments and reduce fees (Yeung, 2020). In Mexico, the government increased social transfers delivered by the public development bank Banco del Bienestar, yet recipients were required to create accounts with private banks that charged excessively high interest rates to receive the transfers (Reis, 2020).

Public banks warrant closer analysis to understand why states are deploying these institutions to support the financialization of infrastructure, and how public banks are influencing the form and outcome of financialization processes. To address the gap in existing literature, this article develops a case study of the UK Infrastructure Bank (UKIB), a new public bank created to finance infrastructure development after the UK’s departure from the European Union and loss of access to European Investment Bank financing. The analysis draws on new theoretical contributions that recognize how public banks’ governance, design and operation are contingent on social, political and economic forces, rather than being pre-determined by public ownership (Marois and Güngen, 2016; Marois, 2022).

The UKIB offers a valuable case to show how public banks are shaped by evolving political, economic and social forces within class-divided societies. The UKIB is the latest in a series of infrastructure financing schemes introduced since the large-scale privatization of public infrastructures in Britain between 1979 and 1991: the Private Finance Initiative and Private Finance 2 (1992–2018), the UK Guarantees Scheme (2012–2021), the Green Investment Bank (2012–2017) and the Contracts for Difference scheme (2014–present). These schemes involved a range of financing interventions: the Private Finance Initiative introduced a new procurement approach with vertically integrated, long-term contracts tendered to investment consortia to raise private finance for public buildings and infrastructure projects. The UK Guarantees Scheme offered Treasury guarantees for privately financed infrastructure projects, negotiated on an ad hoc basis. The Green Investment Bank deployed equity and debt finance to mobilize private investment in infrastructure funds and projects which contributed to the UK’s Net Zero Agenda. The Contracts for Difference scheme aimed to encourage private investment in renewable energy, offering guaranteed prices for electricity generators over a fixed period, to give investors certainty on the financial viability of renewable energy investments.

The political shift towards neoliberal-nationalism since 2016 is critically important to understand the political, economic and social forces shaping the UKIB’s creation. Neoliberalism refers in broad terms to an ideological preference for markets and market mechanisms to organize the economy, over state planning (Berry, 2022; Davies et al., 2021). Yet, neoliberalism is a flexible concept and a wide variety of governing logics and strategies have been deployed over the past four decades to maintain a preference for markets and market mechanisms. 1 The UK’s neoliberal-nationalist regime emerged after 2016, fusing long-standing neoliberal ideas with strengthened nationalist imperatives. The 2016 Brexit referendum was pivotal to this political shift: the cross-party Vote Leave campaign appealed to voters in economically deprived regions with the populist slogan ‘take back control’, blaming deteriorating public services and economic decline on diversion of public resources to the EU budget, and immigration enabled by freedom of movement across the EU (Hay, 2020). 2 The campaign also politicized national identity, promoting an agenda to restore Britain as a global power while retreating from integration with a globalized world that was ‘no longer recognizably British’ (Virdee and McGeever, 2018). Although some of the highest vote shares to leave the EU came from electorates in the north of England, the referendum received 1.3 million more Leave votes from the London and South East region overall, indicating that concerns over regional economic decline did not fully explain the result (Taylor, 2019). The mobilization around national identity galvanized a cross-class alliance of ‘the excluded and the insulated’, comprising older, less-educated, mostly white voters living outside major cities (Willetts, 2021).

The Conservative government signalled a shift to interventionist policies immediately after the Brexit referendum, yet the broader transformation to neoliberal-nationalism emerged between 2017 and 2020. Alongside the adoption of explicitly nationalist rhetoric, and goals to restore Britain as a global commercial power, the process of delivering Brexit included reforms to communications, scrutiny and consent, which centralized power and authority to 10 Downing Street and the Cabinet Office (Ward and Ward, 2021).

Valluvan (2019: 136) defines the UK’s distinctly neoliberal form of nationalism according to three features: a particular set of anxieties about immigrants as less-productive and a potential drain on public services; the invocation of Empire through goals to restore Britain’s position as a global political and commercial power; and a ‘hierarchical understanding of ethno-racial place’ that induces anxieties about who belongs where by casting certain ethno-racial groups as alien and the cause of socio-political or security concerns. These features show how concerns about immigration, identity and Britain’s international role are framed in economistic terms, providing a neoliberal justification for nationalist policies. The UK’s regime also supports claims that neoliberal values are not only compatible with nationalist policies, but depend on them in many cases (Gallo, 2022; Harmes, 2012). Critically, the neoliberal-nationalist regime is not primarily concerned with material improvement: it generates political currency by appealing to senses of frustrated entitlement and white grievance, while treating material outcomes as secondary (Valluvan, 2022). This insight explains the symbolic nature of recent programmes such as the delivery of Brexit and the Levelling Up agenda, which were promoted by bullish communications campaigns on ‘getting things done’ while failing to deliver meaningful material improvements 3 (Ward and Ward, 2021).

The rapid rise of neoliberal-nationalism creates a valuable context to scrutinize how public banks are shaped by evolving political, economic and social forces within class-divided societies. The analysis of the UKIB responds to two research questions: 1. How does the UKIB influence the broader trajectory of infrastructure financing policies in the UK? 2. How does the UKIB’s deployment of the pro-market additionality model seek to maintain credibility amidst new forms of neoliberalism?

The first question positions the UKIB within the broader trajectory of infrastructure financing policies and schemes since the 1980s, to discern the novel aspects of the UKIB’s goals, strategies and activities. The second question examines the bank’s deployment of the pro-market additionality model to show how it sought to maintain credibility with the neoliberal-nationalist regime that emerged since after 2016.

The article is organized as follows. First, the theoretical approach is outlined, followed by the case study analysis across four sections which correspond to the dimensions of Marois’ (2022) dynamic theory of public banks. This is followed by a broader discussion of the UKIB case, positioning the findings within a broader range of public banks and reflecting on the implications for public banks’ role in the financialization of infrastructures. Finally, the conclusion summarizes the main findings and outlines an agenda for further research.

Approaching public banks as dynamic institutions

A public bank is a financial institution that operates under majority public ownership, according to a binding public mandate, or under the governance of public law or authorities (Marois, 2021: 11–12). This definition covers a wide range of institutions, however, the UKIB is a specific type of public bank insofar as it focuses solely on financing infrastructure investment and lends directly to infrastructure funds, large-scale projects or firms, or local authorities.

The case study analysis draws on Marois’ (2022) dynamic theory of public banks. The dynamic theory allows critical evaluation of how public banks are shaped by broader social, political and economic forces, challenging the orthodox and heterodox views which presume that public ownership of financial institutions pre-determines their function (Marois, 2022). Orthodox views treat public banks as inevitably subject to interference from political actors, special interests or lobby groups (Marcelin and Mathur, 2015: 529), while heterodox approaches presume that public banks are inherently aligned with social or public benefit, by virtue of their public ownership (Griffith-Jones and Ocampo, 2018: 3). Marois’ dynamic theory contends that public ownership does not impose any specific function and role on public banks. Rather, these institutions can act in both the public or private interest, and evolve over time to maintain credibility amidst shifting social and political and economic forces within class-divided society (Marois, 2021: 11).

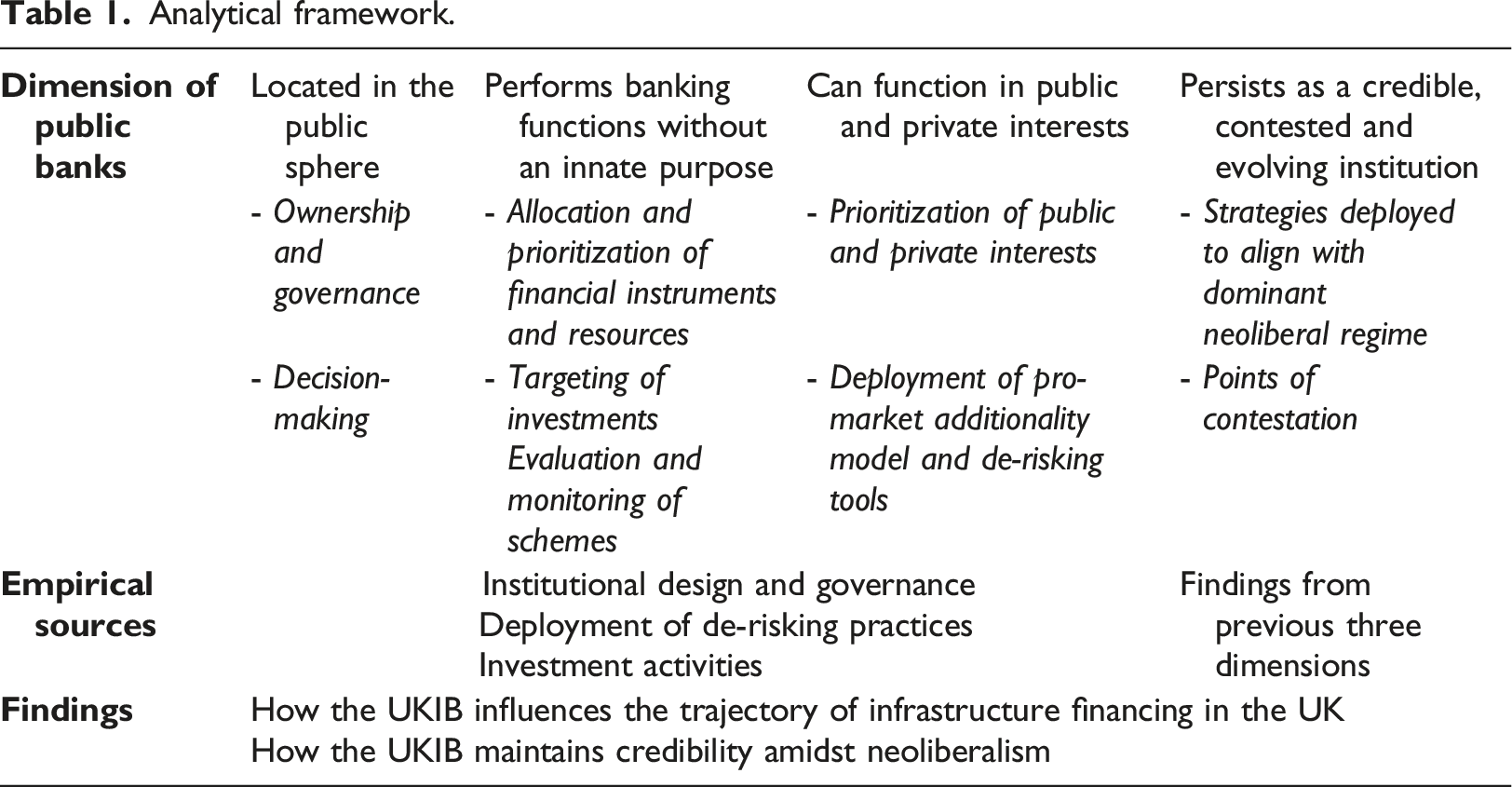

Marois’ (2022) theory outlines four dimensions of public banks as dynamic institutions, to analyze how they are shaped by conflicting social and political forces: 1. They are positioned in the public sphere by their specific form of ownership, governance and decision-making. 2. They perform financial intermediation and banking functions without an innate policy orientation or purpose. 3. They can function in public and private interests. 4. Their institutional persistence is contested and relies on their credibility amidst neoliberalism.

The dynamic theory also defines public banks as contested and evolving institutions which persist amidst neoliberalism by adapting their mandate and functions to maintain credibility with neoliberal regimes. To remain credible, public banks must maintain perceived social support within domestic political milieus, or they will inevitably be sold off, shut down, or fall into disuse (Ho, 2016: 1126; Marois, 2021: 79).

The strategies deployed by public banks to maintain credibility are important to explain their role in financialization (Marois, 2021: 13). In this context, Marois identifies a policy innovation known as pro-market additionality. Pro-market additionality draws on a ‘theoretically uncomfortable convergence of orthodox and heterodox thinking on the potential of public banks', claiming that the required level of infrastructure investment exceeds the capacity of public sector balance sheets (Marois, 2021: 70). This approach argues that public intervention should be limited to instances of market failure where markets are not sufficiently developed, or risks are not sufficiently mitigated, to attract private investment. In turn, the state is tasked with de-risking projects to ensure that projects are ‘bankable’ for private investors, instead of directly financing schemes that could not otherwise obtain commercial finance. Bankable is not a neutral term: it refers to a project’s ability to operate on a financially self-supporting basis and to generate a desirable profit for investors. Since infrastructure projects are characterized by public-good externalities, demand uncertainties and inherent challenges to monetizing the benefits or services generated, achieving bankability can take two forms: redesigning an asset to provide a premium service to a population that can afford to pay charges to use it (O’Neill, 2013), or alternatively, using state subsidies, investments or guarantees to generate a satisfactory financial return, or assume the risks that investors are not willing to accept. Thus, bankability implies that infrastructure projects either target an exclusive population with the purchasing power to pay for premium services and generate sufficient revenues, or they are publicly subsidized to ensure they return a profit to investors.

Gabor (2021) shows how de-risking and the production of bankable projects is a key feature of the emerging of the Wall Street Consensus paradigm for international development, which reconfigures policy settings and development strategies around the interests of private investors in the Global North. By restricting the role of public banks to de-risking investments for private capital, the pro-market additionality model subordinates public banks to private interests by presuming that the public interest will be adequately served by market-led solutions, despite empirical evidence on the trade-offs between financial returns and serving the public interest through privatized infrastructures (Bayliss et al., 2023; Pryke and Allen, 2019), or public-private partnerships which delegate responsibility for the construction, maintenance or service delivery to the private sector (Eurodad, 2018; Lorrain, 2008; Whiteside, 2020). Pro-market additionality has gained popularity as a model to address concurrent climate and financial crises while maintaining the primacy of private investors and market forces (Marois, 2021: 70). The deployment of this model is inevitably mediated by economic constraints and domestic political interests and coalitions. In turn, understanding specifically how pro-market additionality is deployed in terms of public banks’ policy goals, investment strategies and financial instruments, is vitally important to explain how public banks can enable financialization.

Analytical framework.

The UKIB’s location within the public sphere

Public banks are embedded within the public spheres of states by virtue of their ownership, the forms of accountability, control and influence that shape decision-making, power relations between public and private actors as well as individual or collective social forces (Marois, 2022: 362). This dimension of the analysis shows how the UKIB’s institutional design and governance place the bank under highly centralized control, albeit with public ownership and funding, with a technocratic approach to deal-making and limited scope for public input.

The UKIB is sponsored and funded by HM Treasury with delegated authority to make investment decisions (HM Treasury, 2021a: 3). Public ownership places the institution under government oversight with access to public funds, and control of the UKIB is heavily centralized to HM Treasury and the Chancellor of the Exchequer. Although the policy design asserts that UKIB will operate with a ‘high degree of operational independence’ (HM Treasury, 2021b: 5), HM Treasury and the Chancellor retain substantial influence and powers to guide and intervene in the bank’s activities. The Chancellor appoints the chair and non-executive directors (House of Lords, 2022). The Treasury Permanent Secretary acts as the bank’s Principal Accounting Officer, advising on the bank’s objectives and targets, monitoring its activities and raising concerns to the board for explanation and appropriate action (HM Treasury, 2021a: 9). Moreover, UKIB’s legislation gives HM Treasury authority to intervene to give ‘specific or general direction’ to the UKIB about how it delivers on its objectives, which the bank must adhere to (House of Lords, 2022: 3). Although local authorities can access debt finance from the UKIB, this function steers local authorities towards commercialized deals that can attract private investment, limiting their autonomy to pursue projects that best serve the public interest. Given the broad range of impacts resulting from major infrastructure programmes and the UKIB’s purpose to deliver on the Levelling Up agenda to rebalance disparities in economic prosperity across the country (HM Government, 2021: 10), the tightly centralized control of the UKIB raises concern about its capacity to genuinely empower UK regions and support long-term prosperity.

Alongside the centralized ownership and governance structure, the UKIB adopts a technocratic approach to decision-making with limited criteria and few formal roles for regional representatives, industry stakeholders, civil society groups and advocates for accessibility and inclusion, to influence decisions. Investment decisions are evaluated against the UKIB’s goals of contributing to achieving net zero greenhouse gas emissions by 2050, and the Levelling Up agenda to rebalance regional inequalities between the South East and other UK regions (Smith, 2022). Yet there are limited opportunities for public, local or regional input to influence how the UKIB seeks to achieve these goals. Instead, decision-making is controlled by bank officials, HM Treasury and the Chancellor, and there are no formal mechanisms to coordinate investments across cities and regions. The UKIB’s mandate indicates that they intend to work closely with a range of government departments and bodies, including local authorities (HM Treasury, 2021b: 14), yet the lack of formal responsibilities or powers for other public entities or stakeholders gives ultimate authority to the UKIB. Overall, this dimension of the UKIB shows how the bank is protected from public scrutiny and allows limited influence from regional and civil society representatives.

The UKIB’s allocation of finance for infrastructure investment

Public ownership does not pre-determine the purpose of financial intermediation and banking functions performed by public banks (Marois, 2022). Rather, these functions are influenced by broader economic, social and political forces or constraints within class-divided societies. The UKIB offers de-risking interventions on an ad hoc, negotiated basis for privately financed infrastructure projects, alongside a local authority lending and commercial advisory function that aims to institutionalize the financialization of infrastructure within local authorities. The de-risking strategy and heavy reliance on negotiated deals, instead of structured programmes to allocate finance, gives considerable power to private investors to set the terms and scope of investment.

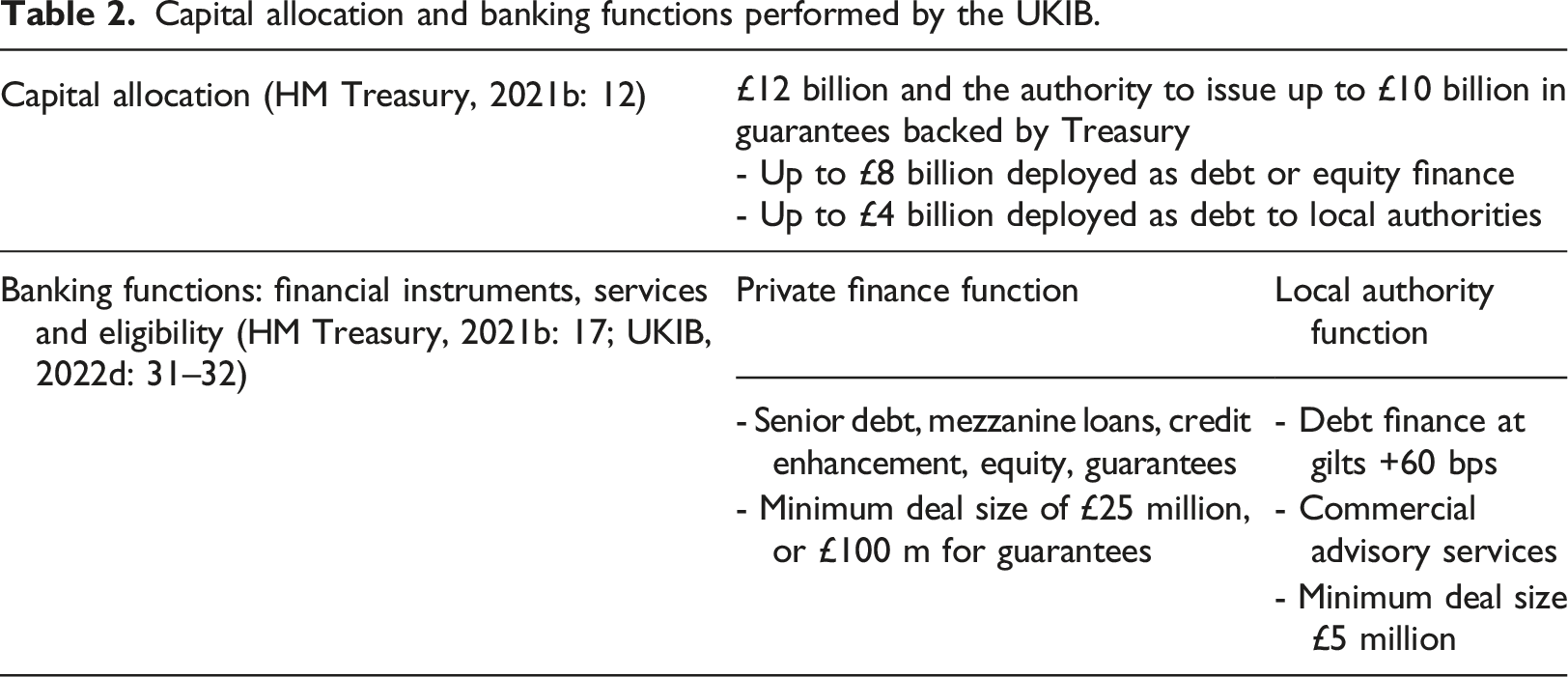

Capital allocation and banking functions performed by the UKIB.

Most of the bank’s capital is allocated to senior debt, mezzanine loans, credit enhancements, equity investment or guarantees to de-risk privately financed deals. The local authority function offers commercial advisory services and debt finance to address the lack of local authority expertise on structuring projects for private investment. The UKIB’s financial instruments reflect the bank’s focus on de-risking private investment. Although senior debt is intended for deals where the private market cannot provide sufficient capacity in terms of the volume of finance, all other debt, equity and guarantee instruments aim to de-risk private investment by take on a higher share of risk that, in turn, enhances the value of private investors’ equity or debt finance (HM Treasury, 2021b: 17).

The UKIB assesses deals on a case-by-case basis to develop tailored financing structures through negotiation with co-investors (UKIB, 2022d: 8). This approach is premised on the bank’s need to remain flexible and respond to market failures as they become evident (UKIB, 2022d: 31), yet the lack of structured schemes or allocation processes gives significant discretion to the bank and private investors alike, to select or prioritize certain types of investments or projects. Since private infrastructure investment is characterized by ‘relational investing’ where the flow of capital follows relational ties and networks (Knight and Sharma, 2016; Torrance, 2009), the UKIB’s approach will likely privilege investors with existing professional connections and financial sector expertise. Furthermore, the minimum deal size of £25 million for private finance, £100 million for guarantees and £5 million for local authority lending imply that de-risking interventions target an exclusive set of commercial banks, institutional investors, asset managers and private equity funds with the capacity to invest at this scale.

The UKIB invests according to four principles: to support regional and local economic growth; to tackle climate change by reducing carbon emissions; to invest in infrastructure assets, networks or new technologies; and to deliver a 2.5–4% return on equity across its portfolio (UKIB, 2022d: 9). These principles align with the bank’s mandate, yet the UKIB’s strategy does not robustly address well-documented trade-offs between goals for local and regional growth and carbon reduction (Hickel and Kallis, 2020). Although the strategy acknowledges the potential tension between local or regional growth and decarbonization, it only addresses this by qualifying that investments to support growth should not do ‘significant harm’ to the climate objective, without explaining how projects should negotiate this tension (UKIB, 2022d: 42).

UKIB-financed projects and investments are subject to a limited set of criteria to ensure they serve the public good. Projects are evaluated against three key performance indicators (KPIs): relative reduction in greenhouse gas emissions, number of jobs created and impacts on productivity in terms of gross value added per worker (UKIB, 2022d: 71). For these measures, there is ambiguity over the geographic scale of impacts on local growth, raising questions over whether investments generate new growth or displace jobs from other regions. The KPI for climate change focuses solely on carbon reduction, overlooking the imperative to integrate climate adaptation and resilience into projects. 4 Investments are also subject to additionality criteria to ensure they create a ‘real increase in social value that would not have occurred in the absence of the intervention’ (HM Treasury, 2022: 126). The UKIB adopts a broad definition of additionality, including financial and non-financial additionality (UKIB, 2022b). Evaluating additionality relies on professional judgements and commercially sensitive information, drawing on the detail of project fundraising, due diligence, engagement with market actors and stakeholders, market analysis, industry reports, subsidy analysis or sector benchmarks. While a judgement-based process may be adequate for private investors, this approach makes it difficult to scrutinize the UKIB's decisions objectively, and raises concerns over transparency and accountability for the UKIB’s use of public money. Overall, the UKIB deploys a range of de-risking tools to a relatively narrow scope of investors, since the reliance on negotiated deals and large minimum deal sizes privileges private equity and institutional investors. The limited criteria and conditionalities raise concern over the long-term public value of the bank’s investments, and how effectively it will deliver on its goals.

How the UKIB functions in public and private interests

The UKIB functions in both the public and private interests, across multiple mandates and investment activities. This section evaluates the UKIB’s investments 5 to show how they serve public and private interests, focusing on the Teesworks freeport development, co-lending for fibre broadband expansion, and equity fund investments. The narrative in the bank’s policy design defines all privately financed infrastructures as inherently beneficial for the public good, which in turn justifies the use of public money to de-risk private investment (HM Treasury, 2021b). Yet, closer examination of the bank’s activities shows how infrastructure investments pursue a limited scope of potential public benefits, or involve extractive practices that undermine the public good.

Teesworks deep-water quay

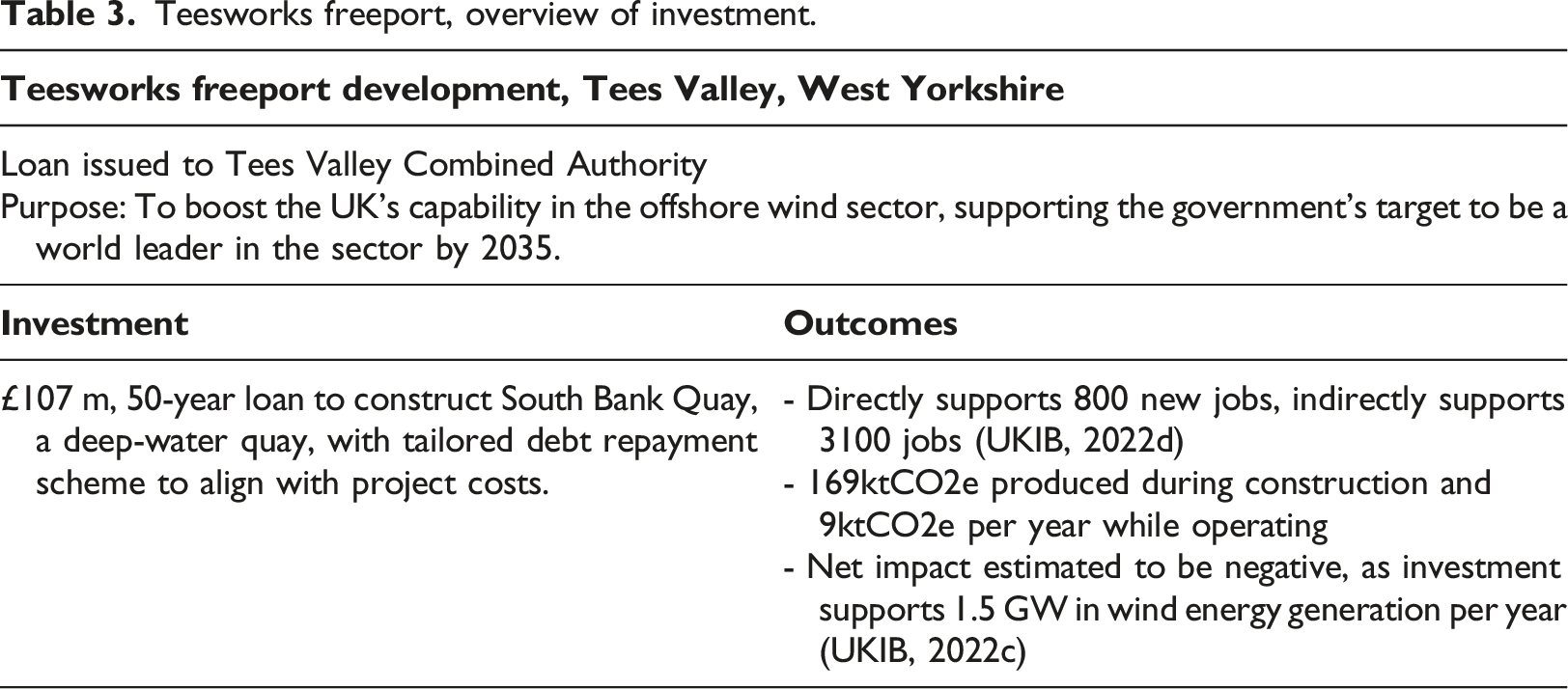

Teesworks freeport, overview of investment.

The UKIB offered concessional financing to Tees Valley Combined Authority to build the deep-water quay, de-risking the freeport by financing a key infrastructure asset to attract firms in the offshore wind sector. Although the scheme's goals to support green innovation, industrial development, jobs and energy security are relevant and worthwhile, Teesworks’ ownership arrangements mean that the anticipated industrial revival in Teesside will primarily benefit the freeport’s investors and land-owners. After South Tees Development Corporation (STDC) acquired the Teesworks site under compulsory purchase in 2020, ownership was transferred to Teesworks Limited, a joint venture 50% owned by local property developers (Metcalfe, 2022a). In October 2021, STDC transferred a 40% ownership share to the property developers on the premise that they would raise a further £200 million to complete land remediation, on top of the £270 million in grant funding already awarded by the government (Metcalfe, 2022b). The deep-water quay will substantially increase the value of the Teesworks site, yet the ownership arrangements mean that 90% of the land value uplift and ongoing revenue-generating potential will accrue to the site’s private owners. Meanwhile, the benefits for the broader public are limited to job creation, overlooking opportunities to hold land or infrastructure assets under public ownership to ensure sound governance and control, and capture long-term revenue streams for public investment or services. Although the government gave assurances that jobs created in freeports would not have inferior working conditions, the current passage of anti-strike legislation that has been deemed incompatible with the UK’s human rights obligations 6 suggests that the wider societal benefits of job creation are likely to be compromised, regardless.

Fibre broadband expansion

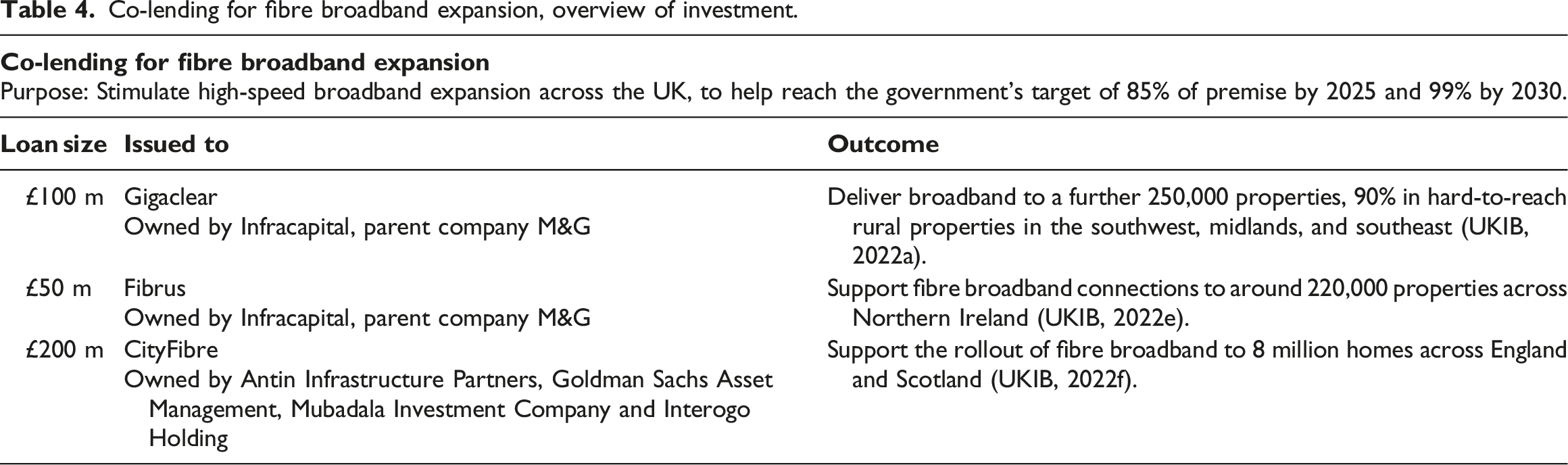

Co-lending for fibre broadband expansion, overview of investment.

Broadband upgrades are a key target for the Levelling Up agenda, supported by the government’s £5 billion Project Gigabit scheme. Yet the current market context shows that de-risking broadband investment carries the risk of fuelling speculative investment that is overbuilding broadband networks in some locations. The UK fibre broadband market is characterized by intense competition between large incumbent operators and a number of small firms known as ‘altnets’, including Gigaclear, Fibrus and CityFibre. All four of the altnets financed by the UKIB are backed by sovereign wealth funds, private equity or infrastructure fund investors. Most altnets are not yet profitable, as their long-term viability is predicated on capturing a larger market share through rapid network expansion (Gross, 2022a). Rapid growth has led to duplication in many areas and creates a substantial risk of an overbuilt network, re-creating speculative bubbles like those witnessed in the UK cable market in the 1990s, which eventually resulted in over-capacity and consolidation as firms failed (Fildes, 2018). Mergers and consolidation of altnets are anticipated (Gross, 2022b), yet lending from the UKIB continues to fuel speculative investment as firms seek to gain a larger market share. In late 2022, reports emerged that the government was considering a rescue scheme to bail out altnets as the unsustainable pace of market expansion and challenging macroeconomic conditions threatened their viability (Nimmo, 2022). This example shows how debt finance can fuel unsustainable market speculation for the benefit of private investors, while leaving the state responsible for intervening when speculative bubbles lead to failure and consolidation.

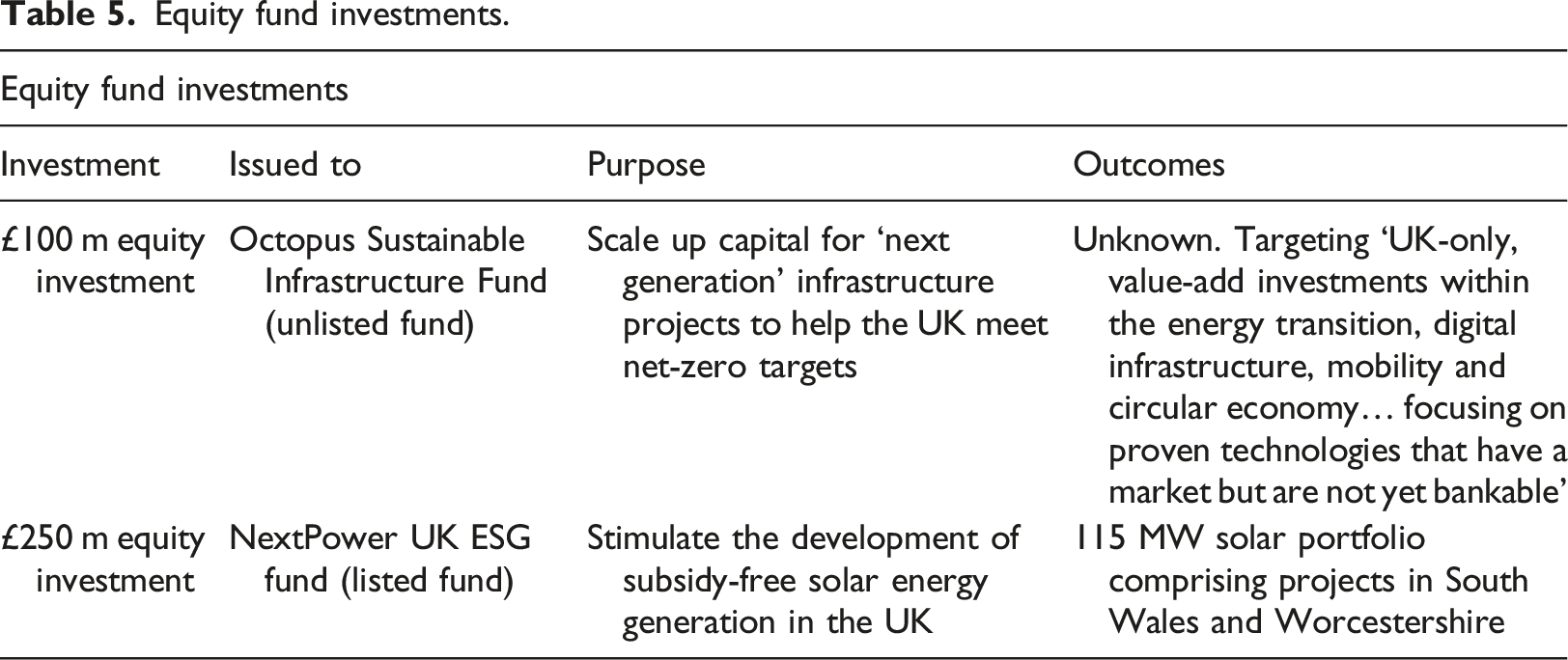

Infrastructure equity fund investments

Equity fund investments.

The structure and management of the two funds give limited transparency over where the UKIB’s capital is ultimately invested. The Octopus Sustainable Infrastructure Fund (OSIF) targets a range of sectors, focusing on technologies yet to reach commercial viability (Infrastructure Investor, 2022). OSIF has not yet deployed capital, and the broad scope of the fund’s mandate gives few clues to its potential deployment. The NextPower UK ESG fund (NPUK ESG) targets UK-based subsidy-free solar projects (NextEnergy Capital, 2022). The UKIB acts as a cornerstone investor to de-risk the fund by offering credibility and state-backed support, with equity investment of up to £250 million on a match-funding basis. NPUK ESG has only disclosed one investment, a 115 MW solar portfolio with projects in South Wales and Worcestershire. The goal to produce subsidy-free solar emerged in 2015 after fluctuations in subsidy schemes created volatility in the solar generation markets (Kay, 2015). NPUK ESG targets projects with Power Purchase Agreements (PPAs), specifically, facilities that will provide a direct and exclusive electricity supply to large corporates.

The UKIB’s fund investments raise concern over the accountability, transparency and ultimate public benefits generated, since these investment vehicles have been criticized for short-term investment horizons, high fees and misalignment with investors’ long-term objectives (Monk et al., 2018: 18). Where funds have disclosed their investments, such as the NPUK ESG fund, funds are used to target assets with PPAs that channel renewable energy supplies to large corporates through exclusive contracts. These contractual arrangements divert solar energy to the entities that can afford higher prices, undermining broad and affordable access to renewable energy.

Overall, the investments analyzed indicate that the UKIB’s focus on de-risking privileges the profitability of private investors, with few safeguards or criteria to ensure that investments support long-term public value creation.

How the UKIB persists as a credible, contested institution

The persistence of public banks depends on their ability to fulfil credible functions within class-divided, capitalist societies (Marois, 2021: 13). The UKIB maintains credibility with the neoliberal-nationalist regime by reinforcing power and control at the centre. The bank’s governance and decision-making processes give the central government discretion to influence priorities and project selection according to its political priorities, with limited transparency or scrutiny. Furthermore, the UKIB neutralizes potential threats that a public bank may pose to private investors with a broad set of de-risking strategies, using public capital to render investments ‘bankable’ for private investors instead of displacing private investment.

Centralized political power is a crucial feature of the neoliberal-nationalist agenda enabling the government to pursue its agenda to revive Britain’s commercial power and restore a sense of British superiority, with limited interference from subnational entities or civil society organizations. The government aims to achieve Levelling Up to rebalance regional disparities, yet subnational actors have limited resources and little formal influence over regional development. The UKIB’s governance arrangements and decision-making processes reinforce the centralization of the Levelling Up agenda, as local or regional authorities and non-government organizations have no formal role in the institution’s governance and decision-making. Although the UKIB’s investment strategy and decisions do not explicitly identify with the nationalist, imperialist rhetoric of the Levelling Up agenda, they nonetheless enable this agenda through the absence of robust criteria or conditionalities for UKIB investments, the ad hoc and opaque nature of negotiated deals, and the powers given to the central government, all empower the government to pursue its agenda with limited scrutiny or complication.

Adopting robust project evaluation approaches, such as those used by other public banks to ensure projects deliver on climate resilience, gender equity and democratic participation (CDC, 2022; KfW, 2023), could ensure that the UKIB’s investments make sound use of public money. In conjunction with the government’s powers to intervene directly in the bank’s activities, the lack of robust evaluation mean that the UKIB’s capital can be easily channelled for projects like Teesworks which explicitly seeks to maintain the local constituencies’ loyalty to the Conservative government (Taylor and Houchen, 2021) while generating controversy over the transfer of wealth generated to private investors (Metcalfe, 2022b).

Neoliberal policy regimes also require public banks to limit potential threats to private banking activities. The UKIB neutralizes perceived threats to private banks by offering a broad set of interventions which de-risk profits and aim to develop new markets to finance infrastructure investment. As shown in the previous section, UKIB lending for the Teesworks freeport and broadband infrastructure expansion, and equity investments in infrastructure funds, take on a greater share of risk to bolster returns for private investors. The limited conditionality applied to UKIB investments, and reliance on professional judgement to assess key criteria like additionality, gives the UKIB discretion to offer de-risking interventions with limited scrutiny or accountability.

Overall, the UKIB persists amidst the neoliberal-nationalist regime by enabling direct interventions from the central government, limiting scrutiny and broader participation in decision-making to empower the government to pursue its agenda, while reinforcing the state’s subservience to market actors for private investment and service provision.

Discussion: De-risking infrastructure under the neoliberal-nationalist state

To position the UKIB amidst the wider landscape of public banks, this section addresses the research questions: how the UKIB impacts the broader trajectory of infrastructure financing policies in Britain, and how the UKIB deploys the pro-market additionality model to maintain credibility with the neoliberal-nationalist regime.

First, the UKIB bolsters the British state’s commitment to privately financed infrastructure by consolidating the functions of previous schemes, reinforcing the decision to remove Value for Money (VfM) appraisals for privately financed deals, and introducing goals to reduce regional inequalities. The UKIB replicates functions from previous schemes: equity co-investment and debt finance from the Green Investment Bank, guarantees from the UK Guarantees Scheme, and the capacity to negotiate and broker privately-financed deals, similar to the Private Finance Initiative. 7 The bank’s investment principles institutionalize the shift away from VfM appraisals by framing private finance as an end in itself, instead of a way to deliver public projects more cost-effectively. It is also difficult to scrutinize the UKIB’s investments without transparent and objective criteria to justify de-risking an investment. The UKIB’s goal to reduce regional inequalities is novel, as previous financing schemes did not pursue a geographical focus. 8 Yet, examples such as the Teesworks investment show that the UKIB’s investments could undermine regional prosperity by exposing regions to the extractive logics of private investors, alongside the public benefits of spurring local job creation and infrastructure development.

The UKIB seeks to maintain credibility with the neoliberal-nationalist government by enabling the central government to exercise discretionary control over the bank’s strategy, goals and specific investment decisions. As outlined in the Introduction, the UK’s neoliberal-nationalist regime is characterized by centralized state power, the aim to revive Britain’s global power, anxieties over immigration and selective targeting of certain ethno-racial groups, and a reliance on symbolic policy agendas that appeal to those with a sense of frustrated entitlement or white grievance (over material improvement). The UKIB’s governance, institutional design and decision-making processes mean that it doesn’t need to overtly reproduce all features of the neoliberal-nationalist regime, to maintain credibility and empower the government’s agenda. Indeed, the UKIB does not adopt any of the nationalist, racially inflected or imperialist rhetoric promoted by the Brexit campaign and the Conservative government. Yet, the UKIB nonetheless empowers the government by ceding authority to direct the bank’s strategy and investment decisions, bypassing democratic decision-making processes and failing to implement robust investment criteria that might prevent the government from directing investment for political purposes.

In particular, the reliance on ad hoc, negotiated deals gives the central government and the UKIB considerable discretion to pursue deals that align with political agendas or the interests of private investors. In contrast to a structured programme to allocate finance according to transparent criteria and fair competition between applicants, the UKIB’s approach is very difficult to evaluate objectively. Since infrastructure investment by asset managers and infrastructure funds is dominated by relational investing (Torrance, 2009), there are challenges to ensuring the UKIB’s approach to allocating capital is conducted fairly and competitively. Additionally, poorly specified criteria for regional growth and decarbonization create ambiguity over the scale and robustness impacts, and whether they are generated or displaced from elsewhere. The limited financial capacity of the UKIB suggests that the institution’s symbolic importance outweighs the bank’s ability to deliver infrastructure projects that will improve material conditions across the country. The UKIB’s £22 billion financial capacity is only a small proportion of the government’s £650 billion infrastructure pipeline, and the level of capital deployed is around 20% of that provided by the EIB.

Amidst other public banks, the UKIB offers a wide range of de-risking interventions to a narrow group of investors, primarily asset managers and infrastructure funds with established professional networks and the capacity to participate in deals at a minimum value of £5 million–£100 million. By targeting asset managers or infrastructure funds, the UKIB channels public capital towards investors that aggressively pursue financialization as part of their investment model. 9 The findings show how UKIB investment fuels speculative investment in fibre broadband markets, boosts capital raising for equity funds with limited disclosure of investment portfolios, and supports schemes like the Teesworks freeport which are overtly politicized by the government as a way to maintain political control over red wall seats in the north of England. The UKIB’s investment activities reinforce the ‘substitutive state’, where the government interventions increasingly act to substitute market activity without mechanisms to correct or strategically shape market activities or outcomes (Berry, 2022).

The UKIB overlooks opportunities to deploy credit to a broader group of borrowers or investors, to accelerate decarbonization and reduce regional inequalities. As outlined in the introduction, public banks can lend directly to households, community groups, commercial firms and public authorities to smooth the costs of large investments. Similar to the model deployed by Germany’s KfW (Bach, 2020), the UKIB could offer loans for energy-efficiency retrofits to upgrade housing, commercial and public buildings, making a substantial impact on reducing carbon emissions, reducing household energy costs, improving resilience to heatwaves and creating jobs across regions. Public banks can also operate under collective ownership models that allow democratic participation in decision-making (Lopez-Franco et al., 2020), or with a series of regional branches which devolve investment decisions and empower communities and regions to shape their own strategies for economic development (Griffith-Jones and Rice, 2019).

Conclusion

The UKIB case shows how public banks can accelerate the financialization of infrastructures by channelling public capital to de-risk private investment. This function is determined by a public bank’s governance and ownership arrangements as well as its mandate and scope of investment activities. The UKIB’s investments influence the form and outcome of financialization processes by channelling public capital selectively, using a flexible set of de-risking interventions. Investment in altnets intensified competition in a market already experiencing rapid network expansion and duplication, while infrastructure fund investments add to the already-substantial volume of institutional investor capital seeking to invest in infrastructure. In both examples, de-risking boosted the financial returns of private investors, yet the long-term public value of the UKIB’s investment was unclear.

The case study shows how centralized, technocratic public banks can be instrumental to nationalist agendas. Under the UK’s neoliberal-nationalist regime, the imperative to maintain credibility resulted in a public bank under tight control of the central government, with a narrow set of ambiguous investment criteria which allow the bank to justify a broad range of investments. This approach creates risks to the bank’s credibility and legitimacy, since investment activities can be directed by the central government with minimal democratic participation or accountability.

The discrepancy between private investors’ returns and long-term public benefits generated by investments reflects how the UK’s neoliberal-nationalist regime relies on symbolic policies and the production of affective qualities, instead of delivering material improvements to living standards across the country. The UKIB’s investment in the Teesworks freeport exemplifies this: Teesworks is framed by the government as a revival of Britain’s commercial prowess based around a green industrial revolution, alluding to the region’s commercial success as ‘workshop of the world’ under the British Empire. Teesworks is also an explicit attempt to retain control of red wall constituencies, yet the benefits of the project for private investors and foreign-owned commercial firms far outweigh the public benefits for the region.

A closer focus on public banks opens new avenues for research on the financialization of public infrastructures, since they have the potential to accelerate financialization or alternatively, pursue definancialization strategies. Comparative research on public banks seeking to finance climate action and biodiversity preservation could examine how banks’ institutional design and investment activities can catalyze environmental change amidst pressures to develop green technologies and nature itself as distinct asset classes. Research on the epistemic communities shaping the design and operation of public banks, and pro-public alternatives to the pro-market additionality model, could also illustrate how public banks could be repurposed to act against, instead of enabling, financialization.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.