Abstract

The paper analyses the links between illicit financial flows, money laundering and dependent financialization using the Baltic states as exploratory case studies. Since the restoration of their independence, Estonia, Latvia and Lithuania have been involved in several massive money laundering scandals, with illicit funds flowing mainly from Russia, as well as other former Soviet Republics. Currently, these episodes have taken on a new dimension in light of the Russian invasion of Ukraine. Until recently, the prevailing narrative was that illicit financial flows and money laundering in the Baltic states resulted from a failure in the financial system’s ability to monitor and detect these operations. However, this paper argues that far from being a simple shortcoming, money laundering and illicit financial flows in the Baltic states are products of dependent financialization in two main ways: first, in the decade leading up to the global financial crisis, the overall economic performance and the returns of financial actors in these countries became dependent on foreign capital inflows. This dependency was key to enabling the arrival of illicit financial flows and money laundering from the post-Soviet space, especially after the crisis. Second, due to its comparative advantages and its subordinate position in the international financial system, the banking sector of the Baltic states was used as an intermediary in global financial networks of money laundering for funds from the former USSR, where it assumed most of the financial, legal and reputational risks. Finally, the research also points to the emergence of new risks.

Keywords

Introduction

Since the beginning of the post-socialist transition in the early 1990s, the banking system of the Baltic states has been involved in various Money Laundering (ML) scandals with illicit funds flowing mainly from Russia, as well as other former Soviet republics (Milne, 2019; OCCRP, 2017a; OCCRP, 2017b; OCCRP, 2019). More recently, these episodes have taken on a new dimension in light of the Russian attack on Ukraine, as the evidence suggests that through the years Moscow has used Illicit Financial Flows (IFFs) to achieve its foreign policy objectives (Owen et al., 2022).

Until recently, the prevailing narrative of the media, authorities and even scholars was that IFFs and ML in the Baltics were the product of a failure in the financial system’s ability to monitor and detect this type of operations, and this phenomenon was primarily associated with the domestic banking sector in Latvia (e.g. Ban and Bohle, 2020; Bowen and Galeotti, 2014). However, recent revelations have shown that IFFs and ML practices were widespread throughout the entire Baltic banking sector.

To date, ML and IFFs remain key blind spots in the literature on financialization, particularly in peripheral and semi-peripheral contexts, referred to as dependent financialization. Therefore, this paper intends to contribute to address this conceptual gap by analysing the case of the Baltic states. Furthermore, at an empirical level, the research sheds light on the mechanisms used by oligarchs from Russia and other former Soviet republics to hide their wealth and funnel illicit funds to promote their geopolitical interests in the run-up to the invasion of Ukraine. Finally, regarding the policy implications of the research, the case of the Baltic states helps to highlight the limits of the risk-based approach to combat ML and IFFs.

The paper argues that money laundering and illicit financial flows in the Baltic states are linked to dependent financialization in two main ways: first, in the years leading up to the Global Financial Crisis (GFC), the overall economic performance and the profitability of financial actors in these countries became dependent on foreign capital inflows. During this period, IFF and ML practices existed but they were mostly confined to Latvian and, to a lesser extent, Lithuanian domestic banks. However, the disruption of cross-border financial flows after the GFC prompted other Baltic financial, and even state, actors to actively seek ways to attract foreign capital as a means to restore profitability and economic stability. This situation was key in enabling IFFs and ML to spread to other sectors of the Baltic economies and their financial systems. Furthermore, it is important to mention that this process coincided with an increase in the supply of IFFs from Russia and other CIS countries as a consequence of the rise in oil export revenues (see Becker, 2019).

Second, due to its subordinate position in the international financial system, the banking sector of the Baltic states was used a necessary intermediary in Global Financial Networks (GFNs) of money laundering, tax evasion, embezzlement, etc. (Wójcik, 2018), where they occupied the weakest link. In other words, the oligarchs from the Commonwealth of Independent States (CIS) countries benefited from the dependence of the Baltic economies on foreign capital flows to use them as transit points for IFFs and ML, in order to disguise the origins of the funds and transfer them to the final destinations in tax havens and safe offshore and onshore jurisdictions. Importantly, these operations were only made possible by the role of financial actors of the core economies. However, due to their lower position in the GFNs, the Baltic banks bore most of the financial, legal and reputational risks.

To meet its objectives, the research applies process tracing (PT) methods. As defined by Beach (2022), PT is a qualitative research method intended to trace causal processes through case studies (see also Bennett and Checkel, 2015; Checkel, 2021). In this framework, the Baltic states are used as exploratory case studies to identify the links between IFF, ML and dependent financialization. It is argued that these countries possess two key characteristics that make them suitable for this purpose: first, in recent years these countries have been proven to be at the centre of several money laundering platforms; second, they present all the hallmarks of dependent financialization. Yet, while sharing a number of characteristics with many (semi-)peripheral economies around the world, the Baltic states also possess a number of features that make them ideal targets for ML and IFFs from the post-Soviet space, as they are former USSR republics, possess significant shares of Russian-speaking population, and currently they are EU and Eurozone members. Thus, taking these specificities into account, the study also aims to show how the analysis of the Baltic states can help conceptualize the exposure of (semi-)peripheral economies to ML and IFFs in the context of dependent financialization.

In empirical terms, the main challenge of the present research was the access and reliability of data, due to the elusive and obscure nature of ML and IFFs. In this regard, the paper has collected data from five main types of sources: first, investigative journalism (e.g. Organized Crime and Corruption Reporting Project – OCCRP); second, think tanks and specialized NGOs reports (e.g. Transparency international); third, publicly available documents from the actors involved (e.g. Danske Bank and Swedbank auditories); fourth data from international databases (e.g. BIS, FKTK, Tax Justice Network) and fifth, secondary academic sources.

The paper is structured as follows: the next section conceptualizes the features of dependent financialization in the Baltic states and identifies the gap in the literature. Section three addresses the empirical links between dependent financialization, IFFs and ML in the Baltic states, as well as the emergence of new risks. Finally, section four presents the main conclusions of the research.

Conceptualizing dependent financialization in the Baltic states

Since the end of the GFC, there has been growing interest in the variegated nature of financialization (Karwowski, 2020). In particular, several authors have pointed out its distinctive features in peripheral and semi-peripheral contexts (Bonizzi, 2013; Bonizzi et al., 2020; Karwowski and Stockhammer, 2017). This phenomenon has been referred to as ‘dependent’, ‘subordinate’ or ‘peripheral’ and in many studies, these terms have been used interchangeably (see Lapavitsas and Soydan, 2022). While it is considered that they can be used as synonyms, this paper will use ‘dependent financialization’, since it is believed that this is the term that best reflects the relationship between the peripheral and semi-peripheral economies with the core. Furthermore, this approach goes in line with recent developments in the financialization literature (e.g. Akçay and Güngen, 2022; Apaydin and Çoban, 2022; Dal Maso, 2022).

In broad terms, dependent financialization shows three main characteristics. First, the dependence of peripheral and semi-peripheral economies on various types of capital and financial flows from the core, which determine their financial variables and their overall economic performance, and make them prone to boom-bust cycles (Becker et al., 2010; Lapavitsas and Powell, 2013; Karwowski and Stockhammer, 2017; Kaltenbrunner and Painceira, 2018; Akcay and Güngen, 2022; Apaydin and Çoban, 2022). Second, dependent financialization is characterized by bank-based financial systems, dominated by foreign institutions and this feature is particularly marked in Eastern Europe (Becker and Jäger, 2012; Sokol, 2017; Dal Maso, 2022). Third, dependent financialization is characterized by the subordinate integration of (semi-)peripheral economies into the international financial system, including that they can only borrow and accumulate reserves in foreign currency and that they have to offer higher interest rates than the core to attract international capital (Bortz and Kaltenbrunner, 2017; Alami et al., 2022). This, in turn, often leads to extensive carry trading and currency mismatches (Fernandez and Aalbers, 2019; Pataccini, 2023).

Thus, dependent financialization can be characterized as a process by which peripheral and semi-peripheral economies become dependent on financial flows, financial conditions, financial decisions and financial actors from the core. This process is led by a series of external drivers that interact with local configurations, giving rise to country-specific formations and trajectories.

In the case of the Baltic states, the rise of dependent financialization was directly linked to the process of post-socialist transformation. After more than four and a half decades of forced annexation to the USSR, Estonia, Latvia and Lithuania recovered their independence in 1991 and began the transition to become market economies. In doing so, they followed the ‘shock therapy’ approach, characterized by the rapid implementation of radical neoliberal policies (Bohle and Greskovits, 2012). During the first half of the decade, the Baltic economies suffered deep transitional recessions and in 1998 they were hit again by the Russian financial crisis. In this framework, in the late 1990s, the Baltic banking sector underwent an intensive process of foreignization dominated by Scandinavian institutions. As a result, by 2005, foreign banks owned 58% of the total banking assets in Latvia, 92% in Lithuania and 100% in Estonia (Pataccini, 2020).

Foreign banks were the main drivers of dependent financialization in the Baltic states. Since their arrival, they substantially increased lending, particularly to households (Bohle, 2018). In absolute terms, in 2000–2007, the consolidated debt of the private sector increased by more than 5 times in Lithuania, 6 times in Estonia and 8 times in Latvia (Pataccini, 2022). For this, parent banks took debt in euros (EUR) on international capital markets at very low interest rates and lent them to Baltic subsidiaries through internal capital markets at higher rates (De Haas and Naaborg, 2006). These carry trade operations generated substantial profits both for the parent banks and the subsidiaries (Kattel, 2010).

During this period, Foreign Direct Investment (FDI) was another great source of growth. For example, in 2005, the year after the Baltic countries joined the EU, net FDI inflows into Estonia reached more than 20% of GDP. However, capital inflows fuelled an explosive boom-bust cycle and, due to the massive imbalances accumulated through the years, the GFC hit hard on the Baltic economies, with GDP contractions amounting to 17% in Lithuania, 20% in Estonia and 25% in Latvia (Kattel and Raudla, 2013).

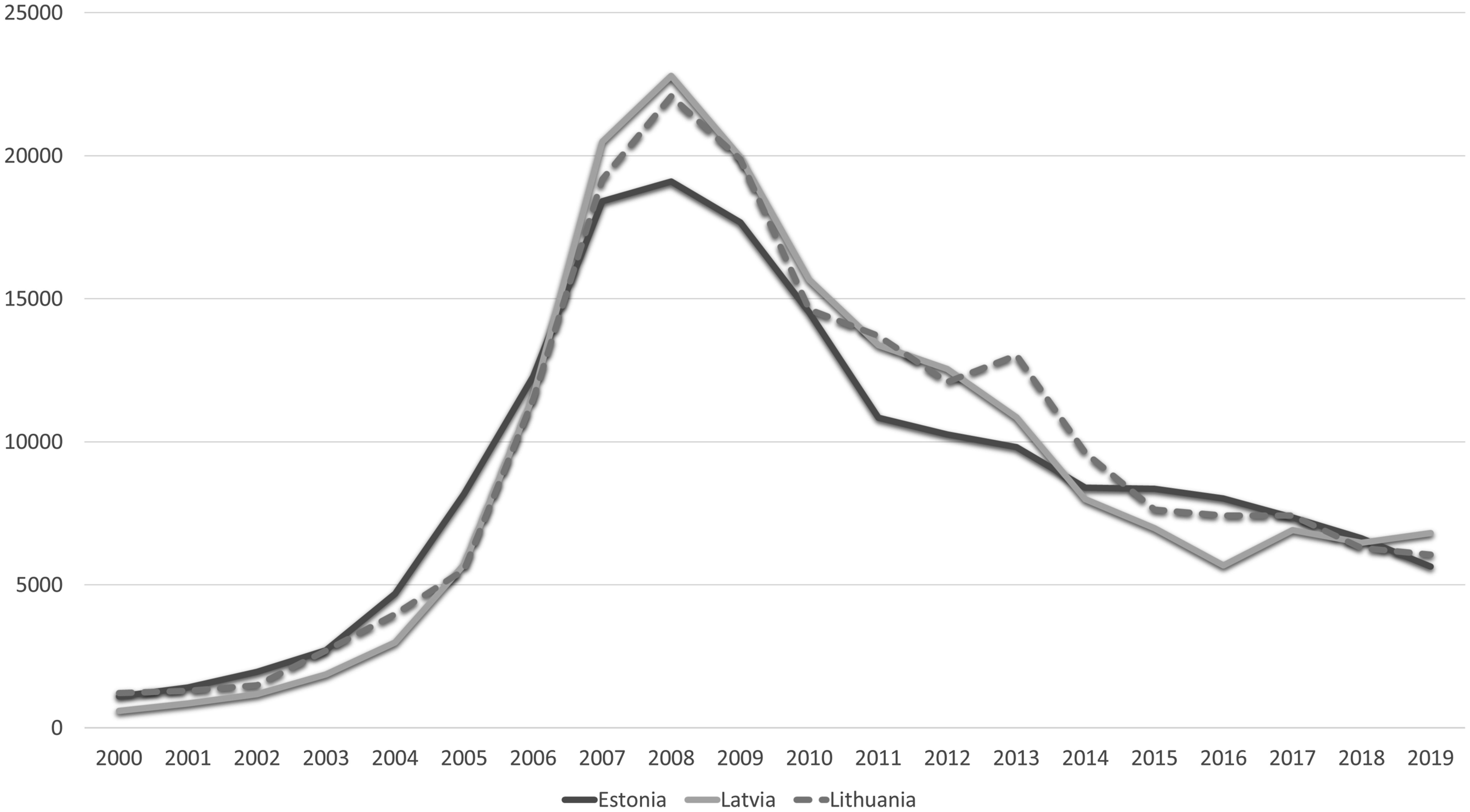

In the wake of the GFC, capital flows to the Baltics stopped almost completely and they even experienced capital outflows (Gros and Alcidi, 2015). This dynamic is linked to a global phenomenon defined by Milesi-Ferretti and Tille (2011) as the ‘Great Retrenchment’ in international capital flows. Essentially, it refers to the fact that after the crisis banks reduced cross-border operations, curtailed loans, and shed assets in their efforts to reduce risk exposure and restore their capital ratios (BIS, 2018). Notably, the Baltic states were the most affected economies in the world by this phenomenon. Between 2008 and 2019, foreign bank claims declined by more than 70% in all three countries (Figure 1). By comparison, cross-border bank claims in the EU decreased by 25% between the peak in 2008 and the bottom in 2016 (Emter et al., 2019). Evolution of foreign bank claims in the Baltic states, 2000–2019 (in millions of USD) Source: Bank for International Settlements - Locational Banking statistics (https://www.bis.org/statistics/bankstats.htm?m=2069).

In short, before the crisis, a substantial part of the banking business model and overall economic growth in the Baltic states depended on the inflow of foreign capital. Yet, after the GFC, the scenario changed drastically and the flows dried up almost completely. This situation created additional incentives for many Baltic financial and even state actors to seek various ways to attract foreign capital flows in order to stabilize the economy and restore profitability. In this way, the vulnerabilities and imbalances caused by dependent financialization in the Baltic states were key to enabling IFFs and ML from Russia and other CIS countries.

However, despite the growing interest on the features and dynamics of financialization in peripheral and semi-peripheral economies, to date significant research gaps remain. One of the main ones is that of IFFs and ML. Within the broad literature on financialization, the phenomenon of money laundering has been mentioned only tangentially. An eloquent example of this is that throughout ‘the Routledge International Handbook of Financialization’ (Mader et al., 2020), one of the cornerstones of financialization studies, money laundering is mentioned only once in relation to the potential activities of trusts (Harrington, 2020: 284). Instead, there have been a number of valuable contributions in relation to offshore financial centres, which have mostly addressed the issues of tax avoidance and evasion from the perspective of the core (e.g. Marshall, 2008; Wójcik, 2018; Fernandez and Hendrikse, 2020). In broad terms, these works show that the same offshore infrastructure that enables tax evasion is also used to channel IFFs and assist ML. In turn, some research has suggested that the proceedings from money laundering activities have served to fuel the financialization of housing (e.g. Fernandez et al., 2016) but these links are not explored deeper.

Regarding IFFs, Owen et al., (2022) refer to the Russian use of illicit financial flows to achieve geopolitical objectives as ‘financialization of foreign policy’. While this is perhaps the only work that connects those dots, it does not delve into the concept of financialization. In turn, other relevant contributions on this topic include Chayes (2015), who addressed the links between IFFs, state corruption and global security, and Prelec (2020), who delved into the role of Russian ‘corrosive capital’ in the Western Balkans. Similarly, the ‘transnational kleptocracy’ literature has examined how Western professional service providers have allowed post-Soviet elites to launder their ill-gotten money and whitewash their reputations (Cooley et al., 2018; Heathershaw et al., 2021; Aten, 2022).

In summary, while dependence on foreign capital flows, the dominance of foreign institutions over their financial sector, and their subordinate integration into the international financial system seem to make peripheral and semi-peripheral economies prone to funnelling IFFs and ML activities, these links have not been examined in depth. Therefore, the present work aims to contribute to addressing this gap by analysing the case of the Baltic states.

Illicit financial flows and money laundering in the Baltic states

The OECD refers to IFFs as ‘all cross-border financial transfers which contravene national or international laws’. In turn, ML is defined by UNDOC as ‘the conversion or transfer of property, knowing that such property is derived from any offense(s), for the purpose of concealing or disguising the illicit origin of the property […]’.1 These definitions show that while they are not the same, IFFs and ML are deeply intertwined and, due to their obscure nature, sometimes it is difficult to establish the differences. Therefore, this work will analyse both together.

To combat ML and IFFs, the Baltic states followed the so-called ‘Risk-Based Approach’ (RBA) (Greco, 2021). According to the Financial Action Task Force, a RBA ‘[…] means that countries, competent authorities, and banks identify, assess, and understand the money laundering and terrorist financing risk to which they are exposed, and take the appropriate mitigation measures in accordance with the level of risk’.2 In other words, the RBA requires banks and other financial institutions to assess any potential risk they may face and act accordingly. This means that if institutions fail or are lenient in identifying risks, they can be used for ML and IFFs.

Until recently, IFFs and ML in the Baltic sea region have been almost exclusively associated with the activities of Latvian domestic banks (e.g. Stack, 2015; Ban and Bohle, 2020). However, since the late 2010s, several money-laundering schemes were uncovered which involved not only the other Baltic countries but also the main foreign banks operating in the region. To date, the Baltic banking sector has been involved in at least three major ML schemes, referred to as ‘Laundromats’, linked to IFFs originating in Russia and other former USSR states: the Russian Laundromat, the Azerbaijani Laundromat and the Troika Laundromat. In brief, the Russian Laundromat is a money laundering scheme that operated between 2011 and 2014. It moved at least USD 20.8 billion out of Russia through a network of global banks and shell companies in 96 countries (OCCRP, 2017a). The Azerbaijani Laundromat is a complex money-laundering operation and slush fund that handled USD 2.9 billion from 2012 to 2014 through a network of European banks and shell companies. The money was primarily used to bribe European politicians in an attempt to help whitewash Azerbaijan’s international image (OCCRP, 2017b). The Troika Laundromat is a ML scheme that operated from 2006 to 2013, which allowed Russian oligarchs and politicians to secretly acquire shares in state-owned companies, buy real estate in Russia and abroad, purchase luxury yachts, and pay medical bills, among others. The scheme’s operator was Troika Dialog, once Russia’s largest private investment bank. Troika enabled the flow of USD 4.6 billion into the system and directed the flow of USD 4.8 billion out (OCCRP, 2019). Altogether, these schemes enabled oligarchs in the Former Soviet space to launder and move illicit funds for an estimated USD 30–80 billion derived from corruption, fraud and embezzlement, and use them for different purposes, including bribes, support to political allies abroad and destabilizing unfriendly regimes (Greco, 2021).

The systematic involvement of different components of the Baltic banking sector in IFF and ML platforms shows a structural tendency towards this type of activity. However, while there is a set of common factors, it is important to highlight that each country shows distinctive dynamics, resulting from its particular characteristics and the interaction of external forces of dependent financialization with domestic socio-economic configurations. Taking this into account, the research identifies three key aspects of dependent financialization that serve to explain the ML and IFFs episodes in the Baltic states: (a) dependence on foreign capital flows, (b) the fall in profitability of the banking sector after the GFC and (c) the subordinate position of the Baltic countries in the international financial system. Each of these aspects is analysed below based on a set of representative cases. Subsequently, the emergence of new risks is addressed.

The dependence on foreign capital: The case of Latvia

Since the restoration of independence, a significant portion of Latvia’s domestic banking sector specialized in providing offshore services to non-resident customers of Russia and other former Soviet republics (Ådahl, 2002). To a large extent, the development of this niche was supported by the state, as Einars Repše, president of the central bank from 1991 to 2001 and Prime Minister from 2002 to 2004 among other prominent positions, reportedly aimed to make Latvia the ‘Switzerland of the Baltics’ (Aslund, 2017).

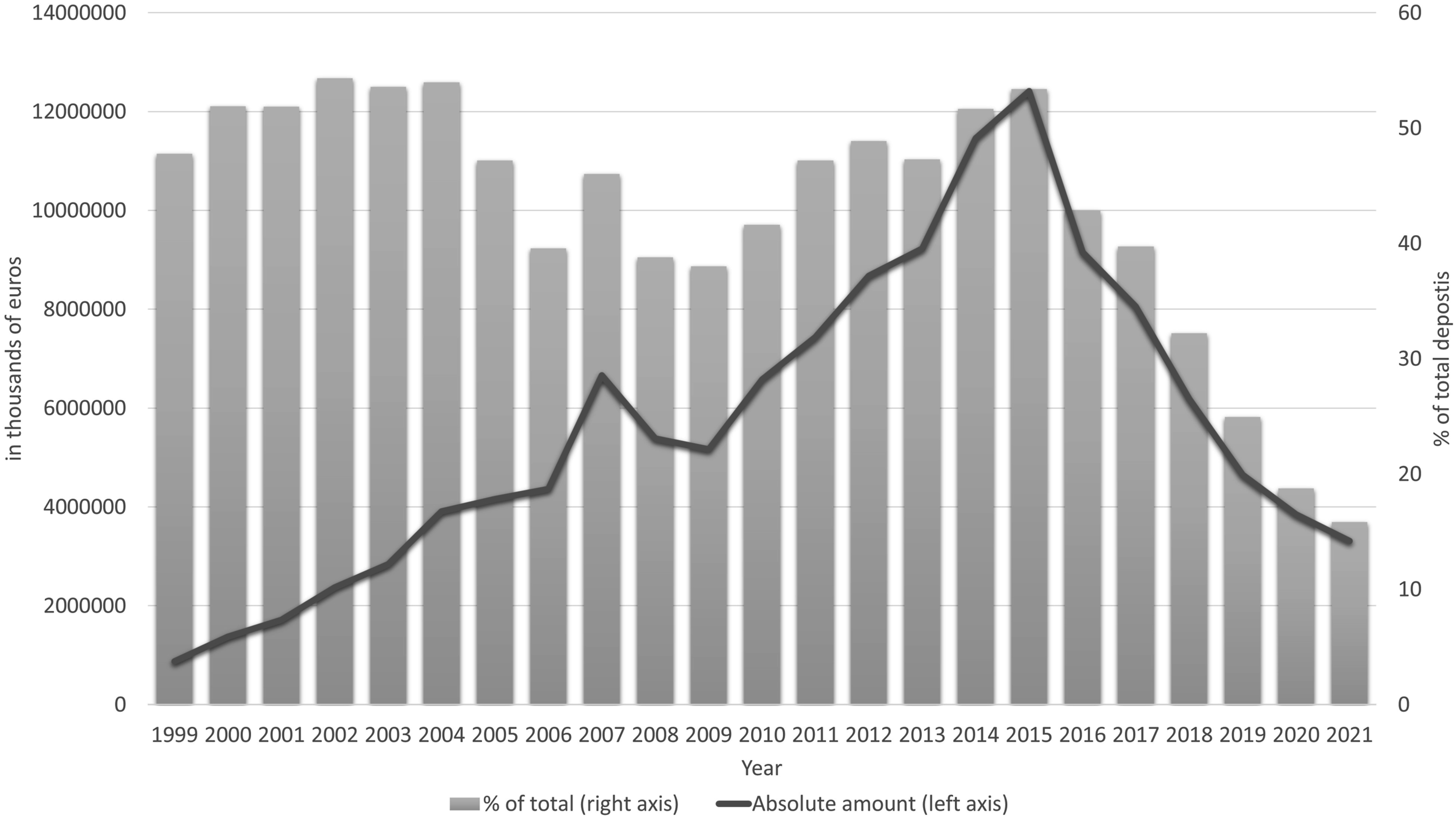

Therefore, since the early 1990s, Non-Resident Deposits (NRDs) played an important role in the Latvian economy, accounting for about half of the total deposits in the banking system (Ådahl, 2002). Even during the phase of foreignization in the late 1990s, Latvia retained a significant share of domestic banking institutions focused on services to non-residents (Roolaht and Varblane, 2009). Later on, as argued by Sommers (2009), finance-led growth in 2000–2007 was driven by two sources: on the one hand, foreign bank credit channelled through Scandinavian banks, and on the other hand, the rise of international energy and metal prices, which created vast fortunes for CIS oligarchs who used offshore centres like Latvia to launder and/or store their money.

However, when the GFC hit, the Latvian economy was extremely vulnerable, as more than 85% of NRDs were on-demand (OECD, 2016). The collapse of Lehman Brothers triggered massive capital outflows which seriously jeopardized not only the stability of the Latvian banking sector but also the balance of payments. In this framework, the country urgently necessitated capital inflows to stabilize the economy and promote recovery. To achieve this aim, in February 2009, the country agreed a bailout loan with the IMF, the EU and other international organizations, amounting almost 40% of Latvia’s GDP. However, following a radical austerity approach, the government used only part of that loan to stabilize the banking system (Lütz and Kranke, 2014). Instead, to promote economic growth, the Latvian government set out to obtain capital inflows in two ways: to attract Non-Resident Deposits in the banking sector and foreign direct investment.

To meet the first objective, Latvia aimed to exploit its comparative advantages to attract foreign capital from Russia and the CIS. In addition to its strategic location, historic ties and its large share of Russian-speaking population, since the early 1990s, Latvia had a highly liberalized capital account, while Latvian commercial banks had established correspondent banking relations with several US financial institutions, allowing them to offer clients the possibility of holding short-term deposits and carrying out international payments in US dollars (USD) (Ådahl, 2002). Moreover, during this period, several Latvian banks expanded their operations and advertised their services in Russia and other former Soviet republics, such as Ukraine, Kazakhstan, Azerbaijan, Armenia and Belarus (Bowen and Galeotti, 2014).

For its part, the implementation of the internal devaluation strategy during the GFC sent a clear message to non-resident depositors: the Latvian government was committed to securing the value of deposits and the non-resident banking business model. Additionally, Latvia’s strong commitment to adopting the euro helped make it even more attractive to non-resident depositors. As a result of this, after a significant decline in absolute terms between 2007 and 2009, NRDs started to increase, peaking at almost 55% of total deposits in the first quarter of 2015 (Figure 2). Evolution of Non-resident deposits in Latvia, 1999–2021 (total amount as of 31.12 of each year in millions of EUR and as % of total deposits) Source: Author´s own calculations based on FCMC statistics on credit institutions (https://www.fktk.lv/en/statistics/credit-institutions/).

In regard to the geographical origin of NRDs, IMF (IMF, 2013: 47) asserts that “As of end-September 2012, about 1/3 of NRDs were from EU countries, 12% from CIS countries (70% of them from Russia) and 55% from other non-EU jurisdictions. The latter, however, corresponds largely to offshore companies from jurisdictions such as the British Virgin Islands and Belize, whose ultimate beneficial owners are mostly CIS residents. Also, 58 and 25% of EU deposits are from the U.K. and Cyprus respectively, but the ultimate owners are mainly CIS residents. Overall, 80 to 90% of NRDs are estimated to come from CIS countries”.

In other words, Latvia, the IMF and the EU were well aware of the origins of NRDs in the Latvian banking system, but maintained a rather lenient approach.

Importantly, despite the inherent risks of the non-resident business model, Latvian regulators endorsed the provision of financial services to non-resident customers, claiming that it had positive effects for the Latvian economy, particularly, contributing to the stabilization of the balance of payments. This was clearly stated by the chairman of the Financial and Capital Market Commission (FCMC), Kristaps Zakulis: “The Latvian financial sector operates as the regional financial centre partially, dealing with the non-resident customer money flow. Latvia differs from other historical financial centres, such as Switzerland, Luxembourg or London, where the banks are focused on attracting the inflow of non-resident customer money for longer periods and maintaining the value of deposited funds. Whereas the Latvian banks mainly provide financial logistics services to non-resident customers, i.e. they are dealing with short-term incoming cash flows. This could be regarded as export of financial services that improves also the payment balance sheet (sic) in Latvia” (FCMC, 2012).

In line with this, during this period Latvian authorities have been reluctant to openly restrict the activities engaged in the provision of financial services to non-residents. An example of this is that in 2013 the FCMC applied a fine against one of the Latvian banks involved in the ‘Magnitsky Affair’. However, despite being demonstrated that the entire scheme laundered USD 230 million from Russia, of which at least USD 63 million passed through Latvian banks, the only action taken was a fine of USD 191,000, while the FCMC refused to identify the bank publicly (Bowen and Galeotti, 2014; RFE/RL, 2013).

On the other hand, in addition to non-resident deposits, Latvia also aimed to attract foreign investment. For this, it launched its ‘golden visa’ program in 2010. The programme granted 5 years temporary residency permit to foreign investors, based on the level of investment: for real estate the minimum required was 50,000 to 100,000 Latvian Lats (LVL) (equal to EUR 71,500–EUR 142,000) depending on location, and for buying Latvian equities LVL 25,000 (EUR 35,500) (Bowen and Galeotti, 2014). In the first year, Latvia received 289 applications. However, over the next years the number of applicants increased substantially: almost 2000 in 2011, 3000 in 2012, 4500 in 2013 and 5600 in 2014. More than two thirds of applicants were from Russia and altogether, almost 90% of the applications came from countries of the former Soviet Union. Yet, in the fourth quarter of 2014, Latvia introduced significant limitations to the program, in response to the Russian annexation of Crimea. For example, the minimum price requirement for a foreigner’s real property was raised from EUR 71,500 to EUR 250,000. As a consequence of that, the number of applicants declined significantly since 2015 and the programme underwent further restrictions after the Russian invasion of Ukraine, in 2022 (LSM, 2022a). Altogether, over the course of 10 years, 19,000 investors have received resident permits, spending EUR 1.55 billion in total, of which over 80% was allocated to the real estate sector and 10% to bank deposits, the remaining being distributed to share capital and government bonds (Jemberga, 2022).

Finally, regarding FDI inflows, during the GFC Latvia experienced divestments from its main investors (Sweden, Estonia, Denmark, Germany and Finland). However, as of 2010, FDI rebounded and reached a peak in 2015. All in all, FDI stocks during 2010–2015 increased by 66%. However, it is important to note that this boom was driven by a substantial increase in investments from five particular origins: the Russian Federation, the United Kingdom, the Netherlands, Cyprus and Luxembourg. In fact, during that period investments from these five countries accounted for almost 60% of total FDI in Latvia. While Russian FDI could be directly related to the benefits of the golden visa, the other four countries are widely recognized as major hubs for round-tripping (Makowski, 2020; see also Ledyaeva et al. (2015) on Russian capital round-tripping). In other words, in the years immediately after the crisis, Latvia became one of the preferred destinations for investments from the main centres linked to ML and IFFS. Yet, this wasn’t considered a problem by local and EU authorities at the time.

In short, since the restoration of independence, the Latvian economy became dependent on various types and sources of foreign capital inflows. However, the collapse of cross-border bank credit after the GFC left Latvia out in the cold. This situation was further aggravated by the radical austerity approach applied by the Latvian government to cope with the crisis. In this context, the country turned to non-resident deposits and golden investor visas to attract foreign capital and stabilize the economy. However, this strategy came at a high cost, as it provided full access to the Schengen area to various CIS citizens involved in dubious economic, financial and political activities, which later was considered to pose serious security risks, leading to the revocation of many of those resident permits (LSM, 2022b).

The fall in the profitability of the banking sector after the GFC

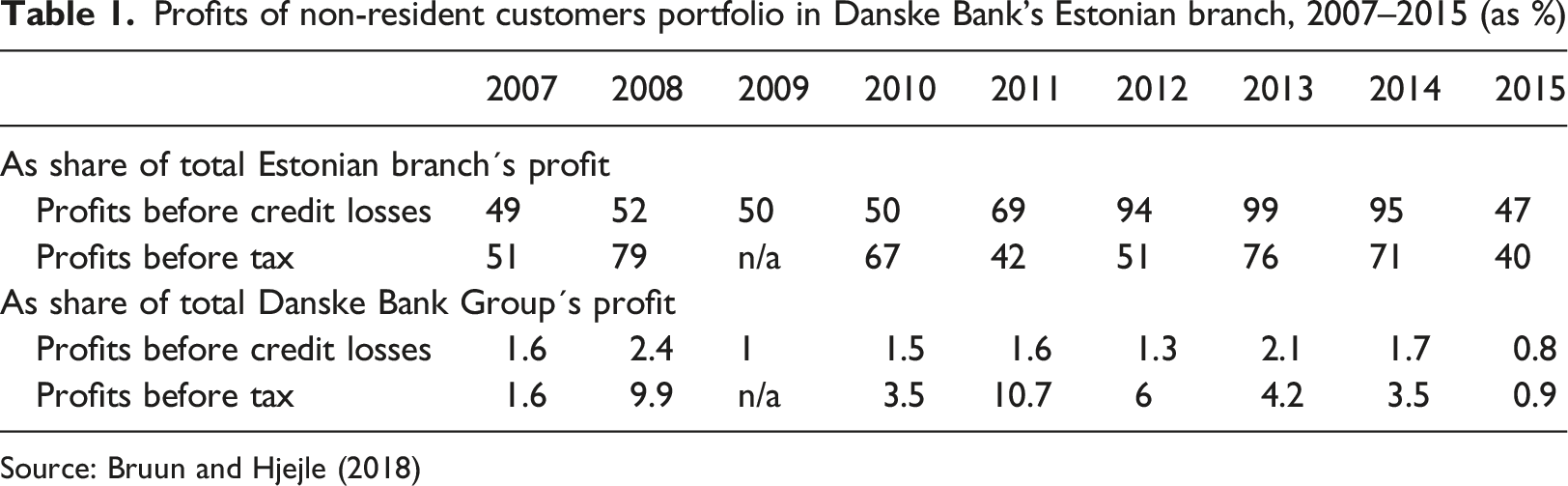

On 1 February 2007, the Danish ‘Danske Bank’ completed the acquisition of Finnish ‘AS Sampo Bank’ for USD 4.57 billion. This purchase included the branch in Tallinn. However, due to the effects of the crisis, the Estonian branch remained under its own management and largely independent from operations in Danske’s headquarters in Copenhagen (Coppola, 2018). Subsequently, in 2009, Thomas Borgen was appointed as Head of International Banking Activities of Danske, having the ultimate executive responsibility for the Estonian branch. In 2010, Borgen pointed out the goal of expanding the base of non-resident business in the Estonian branch due to its profitability. It consisted mainly of corporate entities from Russia, the UK and the British Virgin Islands (Bruun and Hjejle, 2018).

Profits of non-resident customers portfolio in Danske Bank’s Estonian branch, 2007–2015 (as %)

Source: Bruun and Hjejle (2018)

In 2014, Howard Wilkinson, a mid-tier executive at the Estonian branch, released a report about suspicious non-resident accounts moving large sums of money through the bank, often from rubles to USD (Milne and Winter, 2018). The whistleblowing report detailed suspicious operations by obvious shell companies and non-resident account holders, which had direct connections to individuals entrenched in money laundering schemes in Russia and other CIS countries (Kroft, 2019). Despite these concerns, the bank decided to not take any action, in order to avoid economic and reputational risks (Milne and Winter, 2018). Yet, in late 2015, Deutsche Bank and Bank of America cut Danske’s Estonian branch from its USD clearing services due to the large amounts of Russian money moving through its non-resident accounts (Bruun and Hjejle, 2018). Faced with this situation, Danske Bank executives tried to sell their Baltic operations. However, failing to do so, they dissolved the branch’s foreign banking division in 2016, approximately 2 years after Wilkinson’s whistleblower report and under considerable pressure from the Estonian regulators (Bruun and Hjejle, 2018).

However, in 2017, a team of journalists from the Danish newspaper Berlingske, OCCRP and other 15 media organizations across the world revealed that the Estonian branch of Danske was involved in the Azerbaijani Laundromat. In response to the these revelations, Danske Bank hired the Danish law firm Bruun & Hjejle to investigate anti-Money Laundering (AML) breaches in its Estonian branch. On 19 September 2018 Danske released the findings of the investigation from Bruun and Hjejle. The audit reported that during a period of over 9 years, the foreign banking division of Danske Estonia had carried out the largest money laundering scandal in Europe to date. Altogether, USD 236 billion of non-resident money passed through the Estonian branch, creating at least USD 225 million in profits (Bruun and Hjejle, 2018).

Yet, Danske was not the only foreign bank involved in this kind of activities in the Baltics. In 2020 an investigation by the Swedish broadcaster SVT revealed that between 2007 and 2015 a total of USD 5.8 billion of suspicious funds was transferred to around 50 accounts in Swedbank by companies with accounts in Danske Bank’s Baltic branches and mentioned in the Azerbaijani laundromat. This included USD 26 million linked to the Magnitsky affair. SVT also showed that Swedbank’s suspicious money also flowed through its Lithuanian branch, including an alleged USD 4.2 million bribe transferred for the ultimate benefit of Ukraine’s ex-president Viktor Yanukovych (SVT, 2019). The Swedbank exposé led to an independent inquiry commissioned by the bank and carried out by the law firm Clifford Chance. The final report, published in March 2020, found that the bank and its Baltic branches actively sought high-risk non-resident customers due to its profitability. As a result, it reportedly passed around USD 40 billion in high-risk transactions between 2014 and 2019, ignoring their AML duties (Clifford Chance, 2020). In response to these revelations, in March 2020, the Swedish Financial Supervisory Authority imposed a record fine of SEK 4 billion (approximately EUR 360 million) on Swedbank, and in June 2020, it also fined another bank, SEB with SEK 1 billion (EUR 96 million) for ‘deficiencies in its work to combat anti-money laundering in the Baltics’ (LSM, 2022c).

In summary, before the crisis, foreign banks' profits came mainly from carry trades and loans to households. However, in the wake of the fall in profitability caused by the ‘great retrenchment’, foreign banks also turned to non-resident business a way of absorbing the enormous losses caused by the crisis. This strategy was key to enabling IFF and ML through their Baltic subsidiaries.

c) The subordinate position of the Baltic countries in the international financial system: Correspondent bank relationships and shell companies

There are two key components to international money laundering schemes: the respondent-correspondent banking relationships and shell companies. On the one hand, the correspondent is a financial institution that provides banking services for the respondent in another country. In this way, through correspondent banking relationships, respondent banks can access financial services in different jurisdictions and provide cross-border payment services in different currencies to their customers (BIS, 2016). However, correspondent banks are not in direct contact with the origin or destination of the funds. Thus, respondent banks are responsible for the AML controls. On the other hand, shell companies are those that exist only on paper, with no significant assets or operations. Its main purpose is to facilitate tax evasion and money laundering, among other illicit activities (Greco, 2021). A fundamental aspect of shell companies is anonymity, as it allows individuals and organizations to carry out these operations without revealing their identity.

In the past, shell companies were primarily located in offshore jurisdictions. However, in recent years criminal networks gradually moved to using shell companies in reputable ‘onshore’ jurisdictions, such as the UK (Greco, 2021). According to Transparency International UK (TI-UK, 2017), there are three main reasons for this: first, incorporating a shell company in the UK is cheap and easy; second, UK companies offer a veil of legitimacy, especially compared to shell companies registered in traditional offshore locations, and third, until 2016, there was no requirement for UK companies to declare their beneficial owners, making them effectively anonymous. As a result of this, it is not surprising that the majority of shell companies used in the Laundromats involving the Baltic states were registered in the UK. For instance, the Russian Laundromat used 440 UK shell companies, 270 of them with accounts in Latvian banks and 122 with accounts in Estonian banks (OCCRP, 2017a). The Azerbaijani laundromat used mainly four UK Limited Partnerships with accounts in Estonia and Latvia (OCCRP, 2017b), and the Troika Laundromat used a platform of 75 UK companies, of which at least 35 had accounts in Lithuania (OCCRP, 2019).

In a nutshell, the mechanics of ML schemes through the Baltic banks were as follows: customers from the former Soviet Union, predominantly incorporated as shell companies in offshore and onshore jurisdictions, opened accounts in the Baltic banks (Stack, 2015). These banks acted as respondents and had extensive networks of correspondent banking around the world for clearing in USD, EUR and other currencies. Subsequently, the owners of the shell companies moved funds from their former Soviet Union-based businesses to their Baltic bank accounts, which then used their correspondent relations to transfer the funds into savings accounts in safe destinations or for the payment of various goods and services, including bribes, the financing of illicit activities abroad, etc. (Greco, 2018). As stated by Bowen and Galeotti (2014), due to their high money laundering risk rating, direct transfers from CIS countries to Western financial centres would have immediately drawn the attention of regulators. Yet, by transiting their capital through jurisdictions with lower risk ratings, better reputations, and soft AML controls, such as the Baltic states, the oligarchs from the former Soviet Union were able to avoid most of the scrutiny over their transactions.

These operations were enabled by Global Financial Networks (GFNs). These are defined as networks of financial and business service firms located in core countries which link financial centres, offshore jurisdictions and the rest of the world (Wójcik, 2018). In other words, money laundering operations in the Baltics required the involvement of financial actors in the core economies. Thereby, Deutsche Bank and Bank of America assisted the Estonian branch of Danske with wire transfers and currency exchanges while acting as an intermediary between different countries (Milne and Winter, 2018). In Latvia, Trasta Komercbanka, the bank that was at the centre of the Russian Laundromat investigations in 2014, received more than USD 13 billion in accounts belonging to shell companies, which were subsequently transferred to other shell companies and correspondent banks all over the world, including HSBC, Deutsche Bank, Bank of China, Bank of America, Danske Bank and Emirates NBD (OCCRP, 2017a).

In Lithuania, the banking sector was less developed than in its Baltic neighbours, but similar patterns can be observed. There, most of ML and IFF activities were concentrated in two institutions: Snoras and Ūkio. Since its origin, in 1992, Snoras was oriented towards Russia, making big investments in Russian government securities. In turn, by 2002, 44% of its loans were granted to companies registered in U.S. offshore zones and another substantial part of its loan portfolio was concentrated in Russia (Bogdanas, 2012). In 2003, just before the country’s accession to the EU, Russian businessman Vladimir Antonov became Snoras main shareholder. Over the following years, and specially in 2008–2011, Snoras and its subsidiaries in Latvia and Ukraine siphoned hundreds of millions of euros to offshore accounts, mainly in Belize and Cyprus, for which they used a correspondent bank account at Meinl Bank in Vienna (OCCRP, 2019a). For its part, Ūkio Bankas was the bank at the centre of the ‘Troika Laundromat’. Between 2006 and 2013, Ūkio moved more than USD 4.6 billion. However, since Lithuania had not adopted the euro yet, Ūkio needed correspondent accounts in European banks to handle euro-denominated transactions. In this way, the money passed through correspondent bank accounts in the EU core, such as the Austrian Raiffeisen or the German Commerzbank AG (OCCRP, 2019b). Notably, Ūkio also had direct ties with Russia, as it was owned by Armenian-Russian citizen Ruben Vardanyan. These episodes add to the involvement of the Lithuanian banking sector in the Magnitsky affair or the corruption scandal for the payment of bribes to the former Ukrainian president, Viktor Yanukovych, as previously mentioned.

In conclusion, the relationship of the Baltic respondent banks with the correspondent banks in the core economies was an essential part of the IFFs and ML platforms, as it allowed the funds to be converted into hard currency and safely deposited in onshore and offshore locations. In turn, within this scheme, AML responsibilities, as well as the legal and reputational risk, fell on the respondent banks, while the correspondent institutions allegedly had no responsibility with respect to the origin of the money. According to Stack (2015), this type of offshore banking model appears to be the opposite of ‘Swiss’ offshore banking, which specializes in secret savings accounts for non-residents. However, one could say that the models are actually complementary: Baltic banks are means of facilitating deposits in Swiss-type banks. Fundamentally, this shows that GFNs reproduce the asymmetric relationship of dependent financialization, in which the banks of the (semi-)peripheral countries assume most of the risks to ensure the safe transit of IFFs to tax havens and bank accounts in their final destinations.

The emergence of new risks

Since the public revelations of the money laundering scandals in the Baltics, many steps have been taken to reverse the situation. Starting in 2016, Latvia has intensified efforts to combat ML. As a result of that, already by 2018 NRD had decreased by 60% (OECD, 2019). In turn, the Estonian branch of Danske was forced to close in 2019 (Sorensen, 2019). The demise of Danske reduced the share of non-residents in banking in Estonia from 19.10% at the end of 2014 to around 7.91% at the end of 2018 (FI, 2019). Similarly, in the case of Lithuania, Snoras was nationalized in 2011 and Ukio’s licence was revoked in 2013, due to their poor assets quality (Mažylis and Unikaitė-Jakuntavičienė, 2014). These measures, along with others, have been fundamental to diminishing IFFs and ML risks in the Baltic banking sector. The regulatory improvements are reflected in their scores in the Financial Secrecy Index (FSI) elaborated by Tax Justice Network (TJN). The FSI is a ranking of jurisdictions most complicit in helping individuals to hide their finances from the rule of law (TJN, 2023). Starting from 2018, one can see an improvement in their scores and their rankings, particularly for Estonia and Latvia, meaning that Baltic states have become more transparent and therefore less prone to ML/IFF activities.

However, while those threats have been mitigated, new sources of risk are emerging. In particular, the ‘de-risking’ of the Baltic banking sector has coincided with a progressive shift of high-risk customers from the former USSR to new financial technologies (Greco, 2021; Sigalos, 2022; BBC, 2022; Chainalysis, 2023). This situation creates particular risks for Lithuania.

In 2016, the Lithuanian the Ministry of Finance launched the Fintech Strategy, aimed to promote development of the financial ecosystem by providing accommodative regulatory, tax, and policy environment, including enabling payment service providers and other non-bank financial institutions to use the central bank´s payment system CENTROlink for access to Single Euro Payments Area infrastructure (IMF, 2022). As a result of this strategy, the number of fintech companies in Lithuania boomed, reaching 263 in early 2023 (IL, 2023). In particular, the main area of specialization of the Lithuanian fintech hub is cross-border payments. Accordingly, the total value of transactions executed by electronic money institutions (EMIs) and payment institutions (PIs) increased from 7 billion EUR in 2017 to 317 billion EUR in 2022 (Idem).

However, most of the cross-border payments processed by the Lithuanian fintechs are not linked to the domestic market. The customer base of Lithuanian EMIs and PIs consists mostly of non-residents, in some cases making close to 100 percent of the total. The Lithuanian National Risk Assessment of Money Laundering and Terrorist Financing (NRA), conducted in 2019, notes that a large share of customers (up to 70 percent) is from offshore countries (NRA, 2020). Furthermore, since 2020, flows with offshore financial centres and some other higher-risk countries have increased at a faster rate than the overall flows (IMF, 2022).

These emerging business models pose high ML and IFF risks due to four main factors: first, customer onboarding and other business relationships of EMIs and PIs are conducted remotely, which is a traditional risk factor for ML/IFF; second, the majority of EMI and PI revenues come from services to legal entities (approximately 80%), which implies higher ML/IFF risks; third, some of the EMI and PI are specifically focused on serving higher-risk customers, such as virtual asset service providers, gaming platforms and military companies, among others; fourth, AML systems and EMI and PI controls are less effective than in the traditional banking sector, while the rapid growth of EMI and PI institutions makes it difficult for supervisors to conduct on-site inspections and external monitoring in a timely manner (IMF, 2022; NRA, 2020). Some clear examples of the emerging risks in the Lithuanian fintech sector is that in June 2021 the Bank of Lithuania (BoL) revoked the license of UAB Finolita Unio, linked to the Wirecard scandal, due to severe infringements of Anti-ML requirements (BoL, 2021). Finolita was used to steal and transfer more than €100 million from Wirecard prior to its collapse in June 2020 (O’Brien, 2022). Similarly, in February 2023, the BoL began investigating British fintech Railsr over alleged AML and anti-terrorist financing failures within its Lithuanian subsidiary (Pugh, 2022).

Most importantly, the challenges brought to the Lithuanian authorities by the monitoring of new financial technologies in relation to ML/IFF become particularly pressing in the context of the War in Ukraine. Evidence suggests that Russian financial actors could use cryptocurrency and other financial technologies to circumvent sanctions and finance the military operations (Cox, 2022; Chainalysis, 2023). This implies specific risks for Lithuania, where since 2019, the number of registered crypto exchanges has skyrocketed, reaching 760 by the end of 2022 (IL 2023).

In summary, after the GFC, the Lithuanian government opted for the expansion of the fintech sector to develop its financial sector, attract FDI and export financial services. Yet, this strategy has posed serious risks regarding the use of Lithuania as a transit point for IFFs and ML. In turn, these risks have been amplified by the Russian invasion of Ukraine and the potential for Russian financial actors to use new financial technologies to by-pass sanctions. While the BoL has tried to tighten regulations, many blind spots and vulnerabilities remain (Il, 2023).

Conclusions

The paper aimed to analyse the links between illicit financial flows, money laundering and dependent financialization using the Baltic states as exploratory case studies. Research shows that in the years prior to the GFC, the Baltic banks and economies became dependent on foreign capital flows. During this period, the IFFs and ML were concentrated in domestic institutions serving non-resident customers. However, the disruption of capital inflows caused by the crisis led other Baltic actors to actively seek new ways to attract foreign capital to restore profitability and economic stability. In doing so, these actors took accommodative approaches, which were key in spreading IFFs and ML practices to other sectors of the Baltic financial system. These opportunities were seized by the oligarchs of the post-Soviet countries who used the Baltic banks as transit points for IFFs and ML. In turn, these operations were made possible by the involvement of financial players from the core economies, while Baltic institutions bore most of the legal, financial and reputational risks.

Although the Baltic countries share a number of common aspects, it is also important to highlight their differences. In Latvia, the domestic banking sector was linked to licit and illicit capital flows from the post-Soviet space from its origins, and such a strategy was endorsed by the state. In Estonia, where domestic banking sector was practically non-existent, IFFs and ML were linked to foreign banks, especially after the GFC, with the aim of restoring profitability and absorbing losses caused by the crisis. For its part, in Lithuania, which had a smaller financial sector, IFFs and ML were mainly concentrated in domestic banks whose owners had direct ties to Russia. Above all, this scenario points to the specific characteristics that dependent financialization assumes in each particular context.

The research also shows that while the risks in the Baltic banking sector have been addressed, new risks are emerging. The development of the Fintech sector in Lithuania, increasingly specialized in electronic money institutions and payment institutions for non-residents, presents considerable threats, especially in the context of the Russian invasion of Ukraine.

Overall, the Baltic states possess a number of characteristics that made them ideal targets for illicit financial flows and money laundering from the post-Soviet space. However, the research suggests that the conditions of dependent financialization may make the banking sector of peripheral and semi-peripheral economies prone to this type of activities. As a concrete example, the same or similar mechanisms used by the oligarchs of the former USSR to hide their fortunes could be used by drug cartels in Latin America to disguise the income from their activities.

In regard to the policy implications of the research, it is shown that the Risk-Based Approach was significantly inefficient in the Baltics and enabled large money laundering schemes to operate for years. This calls for an urgent improvement of the criteria and approaches to prevent ML and IFFs, especially within the framework of the emerging Fintech sector, where a large part of the companies do not have experience, resources or incentives to conduct adequate controls.

Finally, the paper also outlines avenues for future research. On the one hand, it opens the way for the analysis of the links between IFFs and ML with (dependent) financialization in different contexts. On the other hand, to date, research on ML/IFF and growth models remains limited, pointing to a significant research gap in the field of comparative political economy. 1

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by European Regional Development Fund: [Grant Number 1.1.1.2/VIAA/3/19/491]; H2020 European Research Council: [Grant Number 683197].