Abstract

The literature on financialization tends to overemphasize the increasing size of the financial sector vis-á-vis the rest of the non-financial business sector, usually excluding from the analysis the inter-sectoral relationships between firms. Moreover, few studies have utilized the analytical tools of network theory and the notion of centrality, despite the fact that they conceptualize financialization as the rising centrality of the financial sector. This paper attempts to address these issues and explore the evolution of financialization in the US economy before and after the subprime crisis, investigating the changes in the position of the financial sector. Informed by financial geography and the framework of Global Financial Networks (GFN), we also shed light on the impacts of financialization on those advanced business services sectors that complement financial activity, such as accounting, law, business consulting, and other business services firms. Empirically, we estimate backward and forward inter-sectoral linkages, clustering coefficients, and measures of centrality, utilizing a long time-series of input–output tables at a highly disaggregated level, in order to study the inter-sectoral evolution of financialization in the US.

Introduction

Financialization—as a process that involves the increasing role of financial actors, markets, and motives in the economy—has become a central research theme for many social sciences, ranging from economics and political economy to economic geography, political science, and sociology. In general, the literature has been developed along three research paths (Van der Zwan, 2014). The first views financialization as a distinct regime of accumulation that characterizes capitalism after 1970s and the rise of neoliberalism (Aglietta, 1979; Arrighi, 1994; Boyer, 2000; Lapavitsas, 2009). The second focuses on the financialization of corporations, with emphasis on corporate governance (Froud et al., 2000; Lazonick and O’Sullivan, 2000; Stockhammer, 2004; Thompson, 2003, 2011), and the increasing role of financial profits over total profits in non-financial firms (Krippner, 2005; Tomaskovic-Devey and Lin, 2011). The third explores the financialization of everyday life, including consumption, real estate, and pension funds, affecting households (Martin, 2002), public institutions, as well as the provision of public goods and services, including housing and urban space (Fernandez and Aalbers, 2016; Halbert and Attuyer, 2016).

The above research paths have produced an extensive empirical and theoretical literature that has shed considerable light on the process of financialization, as well as its impacts on a wide variety of socio-economic actors and outcomes. However, despite the wealth of research on financialization, we argue in this paper, that there is a gap for studies that explore on the one hand, financialization present in the relationships between economic actors and sectors and on the other, the impacts of the process of financialization on those business services sectors that complement financial activity. Indeed, existing literature tends to overemphasize the increasing size of the financial sector vis-a-vis the rest of the non-financial business sector, usually excluding from the analysis the inter-sectoral relationships between firms. On this note, while the process of financialization is conceptualized as the rising centrality of the financial sector in a national economy, few studies have utilized the analytical tools of network theory and the notion of network centrality. Moreover, those approaches that highlight the links between financialization and residential and non-residential real estate markets and argue for a structural interdependence between the two, with the latter acting as an absorption sector for global capital, have failed to study the inter-sectoral nature of such a relationship.

To address these issues, we explore the evolution of financialization in the US economy before and after the subprime crisis, investigating the changes in the inter-sectoral position of the Financial and Advanced Business Services (FABS) complex. Informed by financial geography and the framework of Global Financial Networks (GFN), we define FABS as finance, insurance, and real estate, but also accounting, law, business consulting, and other business services firms (Haberly and Wójcik, 2022). In doing so, we investigate, not only how the centrality of the financial sector has changed over time but also how the process of financialization has altered the inter-sectoral relationships of the latter with the wider US economy, as well as the advanced business services sectors that complement financial activity. Putting emphasis on backward and forward inter-sectoral linkages, clustering coefficients, and measures of centrality, we also uncover the hidden complexities of financialization, better understand its impact on the structure of the US economy and explain the changing position of FABS and its components in the process.

Our contributions are theoretical, methodological, and empirical. Theoretically, we shed light on studying financialization in the US, combining elements from the literature of financialization and financial geography, as well as input–output analysis. In particular, informed by economic and financial geography and particularly the multidisciplinary GFN framework, we reconceptualize the process of financialization as a set of tighter relationships between finance, the rest of the economy, as well as a series of complementary and necessary business services sectors, like law, consulting, accounting, etc. (Haberly and Wójcik, 2022; Pažitka et al., 2021). Doing so, we are able to analyze the full scope of financialization, not only with respect to financial actors that are located in complementary occupations and sectors but also for the whole inter-sectoral structure of the US economy. Methodologically, we utilize the tools of input–output analysis and network theory, to explore the properties of the inter-sectoral structure of the US economy, with focus on the relative position of the FABS complex (Leontief, 1936; Miller and Blair, 2009).

Empirically, we provide evidence about the evolution of financialization in the US and the centrality of the FABS complex with respect to the rest of the US economy. To do so, we rely on input–output data from the US BLS (2021), at a highly disaggregated level of 205 industrial sectors, covering approximately 12 years before and 12 years after the collapse of Lehman Brothers, starting in 1997 and ending in 2020. Since the US subprime crisis, many economists and political commentators have anticipated a structural break in the process of financialization in the US, arguing that a new accumulation regime will emerge in the near future as the result of stricter regulation and the realization of political agendas that pledge to tame the excessive power of the financial sector (Griffiths, 2018; Lapavitsas and Mendieta-Muñoz, 2018, 2019). Others have left the question of the future of financialization open for further analysis, underlying the need for a multidisciplinary analysis (Ioannou and Wójcik, 2019). Our empirical analysis helps us improve on and contribute to this research.

Although financialization in the US economy has been primarily associated with the rising power of the financial sector, we show that this process is much more complex. Taking into account the industries that make the FABS complex, we observe that they have increased their centrality, as a whole, not only in the run up to the subprime crisis but also beyond. Within the financial sector, banking has declined in terms of its inter-sectoral linkages with the rest of the US economy after the subprime crisis, whereas the real estate sector has recovered and strengthened its position after a temporary decline during the subprime crisis. In line with the finance-real estate nexus literature (Fernandez and Aalbers, 2016; Halbert and Attuyer, 2016), we show that real estate is the most central sector of the FABS community and one of the most central key sectors of the US economy.

The rest of the paper is organized as follows: The Literature review section discusses the theoretical background and the literature on the recent developments in financialization. The Methodology and data section presents data and methods. The Empirical results section reports empirical results and the Discussion section discusses them. In the final section, we summarize our findings and contributions.

Literature review

Financialization can be defined as the “increasing role of financial motives, financial markets, financial actors and financial institutions in the operation of the domestic and international economies” (Epstein, 2005: 3). Despite the clarity of this definition, we still lack a widely accepted way to measure the extent of financialization in contemporary economies. As Krippner (2005: 175) notes the literature has not yet satisfactorily addressed the issue of “what constitutes the relevant evidence for financialization and how should this evidence be evaluated”. Although most studies investigate changes in employment or in the mix of goods and services produced, they ignore the fact that “the financial sector is not employment-intensive and its products do not show up in transparent ways in national economic statistics” (Krippner, 2005: 175). The solution proposed by Krippner is to trace financial actors and motives in the sources of profits generated in the US economy. To this end, she introduces two measurements of financialization for the US economy: the share of portfolio income as a source of revenue for non-financial firms, and the comparison between financial and non-financial profits of the corporate sector.

However, one could argue that these profit-based measures of financialization seem to ignore the multiple dimensions through which financialization unfolds, as well as the variety of financial and business actors that are involved in the process. Kotz (2011), for example, suggests to interpret Epstein’s definition of financialization, not only as the quantitative expansion of finance in the economy but also qualitatively, with respect to two possible changes: “(1) finance becomes more powerful in relation to the nonfinancial sector; (2) the link between finance and the non-financial sector becomes either tighter or looser” (Kotz, 2011: 4).

Similarly, Jayadev et al. (2018: 335) highlight the challenge of quantitatively measuring the size and scope of finance given the “extension in the range of social claims and obligations that take financial form”. Consider for example, the shifts from a tax-financed and public-serving model of education, healthcare, or housing to market-based and debt-financed models, in which debt claims can be assetized, securitized, and traded in financial markets. Such shifts result in a “recasting of social ties as financial claims” (Jayadev et al., 2018: 335) and the emergence of new sources of profits for the financial entities involved, but they also reconfigure the network of economic linkages that connects economic actors at the micro, and economic sectors at the meso level. Likewise, Aalbers (2019: 6) stresses that “finance has moved beyond its traditional intermediating functions” and “is not just the business of banking”. This is reflected in the rising importance of non-traditional financial actors such as non-bank lenders, private equity firms, pension and hedge funds, insurance carriers, as well as the army of business and financial services firms that complement and intersect with traditional financial services (Aalbers, 2019; Pažitka et al., 2021).

Engaging with an understanding of financialization as a process that involves both a quantitative increase and a qualitative transformation of the role finance plays in economic activity, helps us appreciate those studies that view financialization from a historical and institutional perspective. These approaches allow for a periodization of the phenomenon of financialization, identifying historical periods that are characterized by waves of acceleration/deceleration of the size and influence of finance in specific socio-economic historical contexts. Vercelli (2013), for example, identifies two periods of financialization—the first beginning in late 19th century and ending with the beginning of the Great Depression and the second starting in early 1970s with the collapse of the Bretton Woods regime—emphasizing various economic, political, and institutional factors that strengthened financial freedom and curbed financial oppression. Similarly, Fasianos et al. (2018: 35) explore the historical fluctuations of the process of financialization in the US, distinguishing between phases of financialization (1900–1933 and 1970s–2010) and de-financialization (1933–1940 and 1945–1970), highlighting a “plethora of empirical and qualitative indicators”, such as the size of the financial sector, the regulatory infrastructure, levels of indebtedness of households and businesses, capital mobility, and fiscal policy regimes.

A reasonable corollary emerging from the above is that financialization, as a process with its own history of ups and downs, might also come to halt and exhibit signs of slow growth, deceleration or even de-financialization in the future. The latter possibility has sparked the interest of political economists and policymakers, who in the aftermath of the US subprime crisis speculated about the prospect of financialization in advanced economies and whether a new global financial regime with the power of financial actors would be significantly tamed, is under way (Gabor, 2010; Ioannou and Wójcik, 2019; Kregel, 2010; Tymoigne and Wray, 2009; Wijburg, 2021). Lapavitsas and Mendieta-Muñoz (2018, 2019) attempted to empirically address the question of whether US financialization has come into a halt, after the subprime crisis. Analyzing the share of financial profits in total profits of the US economy, and the changing structure of the indebtedness of US households, businesses, and government, they conclude that the process of financialization has come actually to a halt. More specifically, they argue that financial profits after the subprime crisis have not recovered to their previous upward trend, whereas the level of debt and its composition has dramatically changed, with households and businesses decreasing their leverage, and the state providing unprecedented amounts of debt-financed liquidity.

What becomes clear from the above discussion is that financialization cannot be considered as a unidimensional and unidirectional process that only involves the increasing size of the financial sector or the quantitative expansion of financial assets and instruments. On the contrary, financialization, as a historical process, is a complex transformational procedure that progresses along and within the inter-sectoral structure of an economy, establishing financial dependencies and shaping the evolution of other sectors. In this paper, we draw inspiration from financial geography and the analytical framework of the GFN highlighting the multiplicity of actors involved—explicitly and implicitly—in the process of financialization.

The GFN is a multidisciplinary framework that integrates elements from economics, international political economy, economic history, law, and sociology, in addition to geography. The GFN is conceptualized as the network of actors and geographies that brings together national and supra-national governmental bodies, corporations concentrating on financial and non-financial business services (FABS), financial centers and offshore jurisdictions (Coe et al., 2014). FABS are defined as banks, insurance companies, asset management houses, financial services firms, but also the advanced business services firms, like consultancy companies, auditing and accounting firms, legal services firms, etc. The role of FABS in the GFN is considered equally important as the role played by traditional financial firms. For example, law firms provide credibility and trust into the financial system with the production of legal contracts, whereas accounting firms work on the accurate and fair depiction of financial values in corporate statements, supporting the confidence of market participants, shareholders, employees, and the state. Similarly, consultancy firms help “optimize, and maintain an alignment between, their [financial firms’] operational and financial strategies” (Haberly and Wójcik, 2022: 10). Likewise, business support and employment services firms, provide necessary back- and mid-office capabilities to financial firms, allowing them to reach global markets and distant financial centers (Urban et al., 2022). In other words, FABS act as the “master weavers” of the GFN, bringing together actors from the private and public sector.

Financial Centers (FC), cluster financial actors and financial markets, institutions, and infrastructures in one place, contributing to economies of scale, scope, and network enjoyed by FABS. Offshore jurisdictions (OJs) are territories that offer legal, regulatory, and fiscal flexibility to FABS actors (but also governments), with respect to the registration and booking of financial entities, contracts, and instruments. Finally, world governments (WG) are national and supra-national public institutions that regulate financial transactions and have the ability to exert extraterritorial authority over the production, circulation, and consumption of money (Haberly and Wójcik, 2022). Emerging research using the GFN concept investigates the financialization and globalization of financial and business services, and examines their rising power in the world economy (Wójcik, 2018).

In addition to the GFN, we also build on the literature that focuses on the financialization of the urban environment, putting particular emphasis on the linkages of financial markets and the real estate sector. Aalbers (2008) views financialization through the lens of Harvey’s notion of “capital switching,” according to which capital flows from low-yielding to high-yielding sectors of the economy (see also Harvey, 2006). For Aalbers (2008) housing, and the urban space in general, plays a crucial role in the process of financialization, not only with respect to the financial exploitation of social groups, like homeowners but also regarding the ability of global pools of capital to find profitable investment opportunities in local and globalized segments of the housing and real estate markets. In this way, real estate and financial markets “become entangled, they effectively become interdependent” Aalbers (2008: 151), with their inherent expansion-bust cycles being increasingly synchronized, at least in those countries with relatively advanced financial systems with secondary markets and developed mortgage markets. Focusing on the housing bubble in the US, Aalbers notes that the US financial system and the overall accumulation regime of the American economy, is structurally dependent on home equity and the easy and cheap access of households and corporations to credit, rendering the fluctuation in house prices decisive for the whole economy: “Home equity has become so entangled with the other parts of the economy, that problems in housing must affect other parts of the economy. A crisis in the mortgage market is therefore a crisis in the accumulation patterns of financialization and affects the economy at large. If a rise in home equity can keep the market going, a stagnation or decrease in home equity can result in a stagnation of other sectors of the economy and can depress economic growth” Aalbers (2008: 159).

Financial geographers have also charted developments in other parts of the US FABS complex. Focusing on investment banks, hedge funds, and securities companies, Wójcik and Cojoianu (2018) investigate the impacts of the subprime crisis between 2008 and 2016, finding that the securities industry has suffered significant losses in terms of employment. These were driven by a wave of mergers and acquisitions, offshoring to Asia, and labor-replacing technologies. Haberly et al. (2019: 179) explore the effects of technology and digital platforms in the structure of asset management industry, identifying that despite the tech-driven uproar, the “identity and geography of digital asset management platform providers has remained, to a rather counterintuitive extent, aligned with their identity as financial firms rather than as technology firms”. Literature on the effects of the subprime crisis on other parts of the FABS complex, such as law firms, consultancies, accounting, and auditing companies is scarce. Concentrating on the legal services industry in the US, Greenberg and McGovern (2012: 35) reflect upon three structural changes as the result of the financial crisis: the role of offshoring, temporary employment, and the increasing “use of contract attorneys for routine tasks, such as document review, due diligence, and contract management” as a strategic tool of law firms to control wage costs; the demand-side pressures from clients who negotiate for less costly fee arrangements; and the development of alternative legal financing schemes, like Third-Part Litigation Financing (TPLF) or the introduction to law firms of non-lawyer investors.

Although the above literature offers valuable insights into the process of financialization in the US economy, we are still missing an empirical analysis that sheds light on the evolution of the inter-sectoral linkages of the financial sector and its effects on those advanced business services sectors that complement financial activity (the ABS part of the FABS complex). This has important implications with respect to the understanding and exploration of financialization, as a complex and multifaceted process. The goal of this paper is to extend the respective scholarship and highlight the centrality of economic actors that belong to the FABS complex, as well as the articulation of the latter with other sectors of the US economy.

Methodology and data

In this paper, we combine input–output and network analysis to examine the inter-sectoral structure of the US economy and unveil the complexity of the relationships that the financial sector establishes within the FABS complex. Input–output analysis allows us to link the flow of goods and services with the various sectors of the economy and distinguish between their production and utilization. The basic aim of input–output analysis is to map and analyze the interdependence of the industrial structure of an economy, linking together the production processes of different economic sectors. A fundamental component of input–output analysis is the input–output table, which collects data about the value of goods and services used and produced in the production process of industries, as well as the transactions between industrial sectors, final users (final demand), and primary input providers (capital and labor).

A particular strand of the input–output literature has developed analytical tools for the analysis of the intersectoral linkages, which measure the relative importance of individual sectors in an economy, as well as the complexity of their interrelations with the other sectors. Commodities produced by one sector can be consumed by users representing final demand, but also demanded and used by other sectors as intermediate inputs. Consequently, the evolution of one sector generates direct and indirect effects for the input-producing and input-consuming sectors of the economy. These direct and indirect effects are captured with the measures of Backward (BL) and Forward (FL) linkages, respectively. In the Supplemental Material, we briefly introduce the fundamental concepts and mathematical formulations of the input–output analysis and describe the backward and forward linkages measures applied in the paper.

A rapidly growing literature located at the intersection of macroeconomics, input–output analysis and econophysics, draws insights and applies analytical tools from network theory, which conceptualizes the structure of an economy as a network of independent industrial sectors that are connected with each other, based on the properties of their input–output relations. Each industrial sector can be interpreted as a node (vertex) and the flows of economic activity between them as the links. In this paper, we focus on two important tools of the network theory: the clustering coefficient, and the node centrality. A clustering coefficient (CC) measures the degree to which the neighbors of a given node are linked to each other, whereas centrality measures the influence and importance of a certain node with respect to the position of the other nodes that make up a network (for more details see Supplemental Material).

Financial and advanced business services.

Source: Own Illustration. Data: BLS.

Notes: More information about the components of each sector is found in Supplemental Materials.

Empirical results

Linkages

The inter-sectoral linkages show a sector’s relationship with the rest of the economy, through its direct and indirect purchases and sales of inputs, captured by the Backward (BL) and Forward (FL) linkages. The sectors that have high backward and forward linkages will influence the national economy more, by stimulating output, incomes, and employment, expressed as a multiple of every unit rise of final demand. The knowledge of BL and FL distribution is important, since it allows us to have a better understanding of the basic structure of an economy and its inter-sectoral relationships, highlighting the inter-dependencies of sectors with their suppliers and buyers. The sectors that are strongly connected with other industries in a national economy, both in terms of their input demand and output supply, are called key sectors and are characterized by high backward and forward linkages. This implies that a unit increase in the output of key sectors will generate multiplicative economic activity to the rest of the economy. First, it will create higher demand for input goods and services which will be directed to the suppliers of the key sectors, and second, it will expand the input supply that is needed to support the production of higher output production.

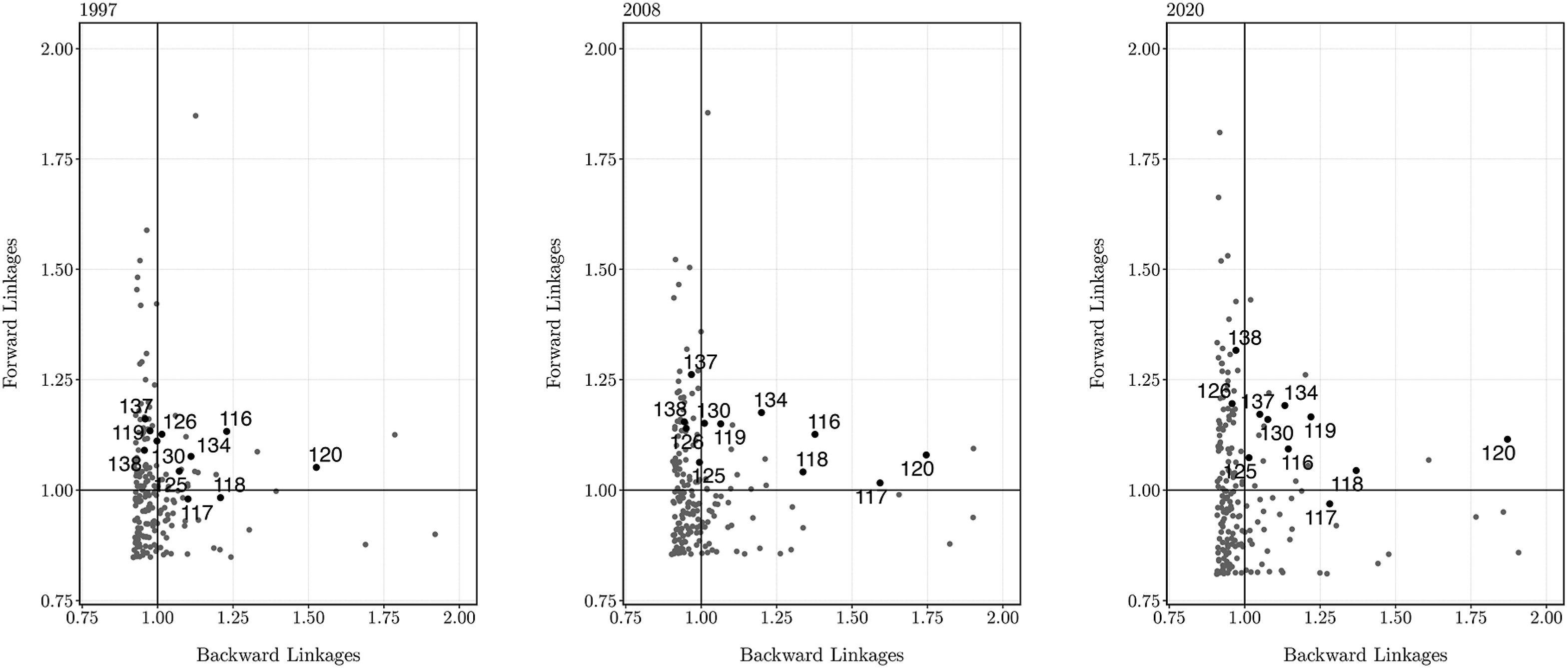

In Figure 1, we present the direct weighted BL and FL for the US economy, in 1997, 2008, and 2020, weighted by the shares of each sector in gross output, with the financial services and advanced business services sectors in black color. Comparing the three plots, we observe that in 1997 six out of eleven FABS sectors were identified as key sectors for the US economy, with securities (117) and insurance carriers (118) sectors being backward looking and insurance agencies (119), management of companies and enterprises (134) and employment services (137) being forward looking. By 2008, the first year of the financial crisis, seven FABS sectors were considered as key sectors, with legal services (125), accounting (126), employment (137), and business support services (138), becoming forward looking. By 2020, eight of the eleven FABS sectors were key sectors, with business support (138) and accounting (126) being forward looking and securities sector (117) backward looking. As such, over time we see a growing number of FABS sectors, that is both financial and ABS sectors, becoming key to the US economy. Weighted direct linkages of the FABS sector.

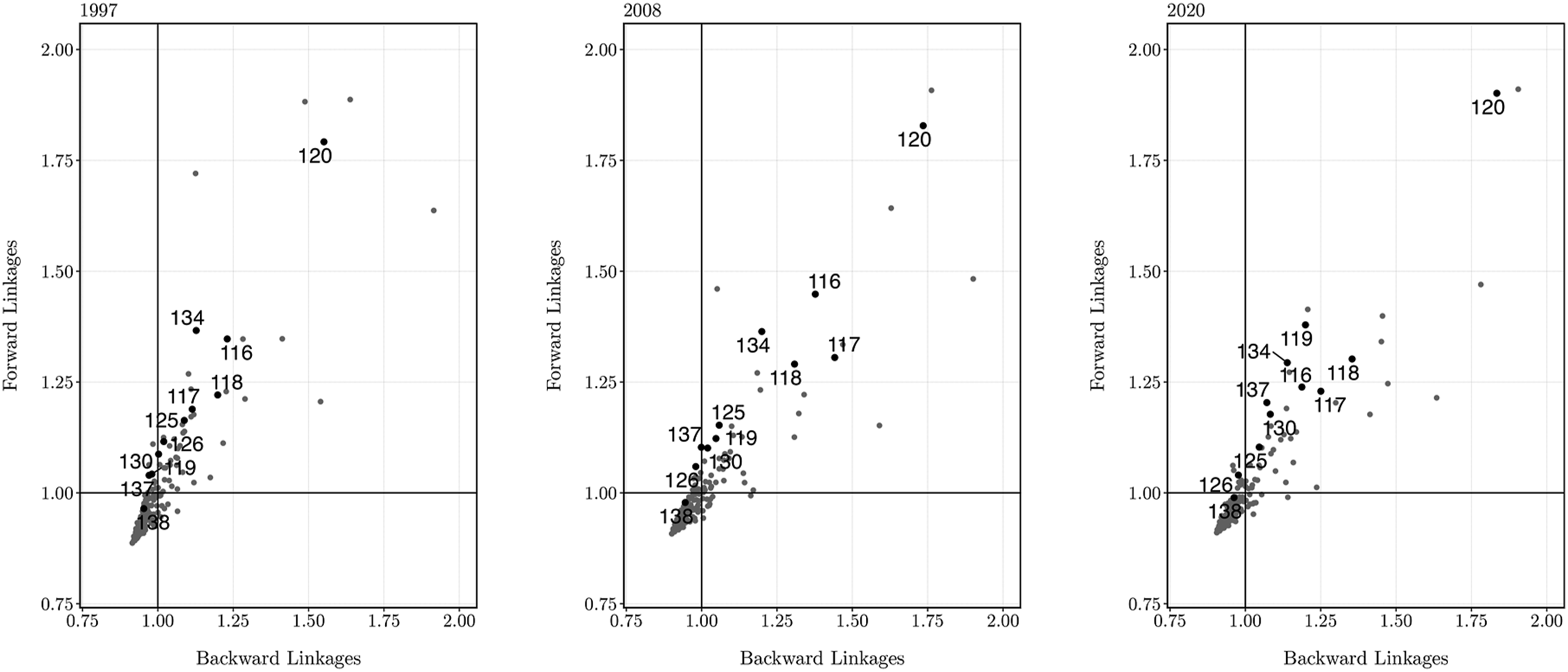

In Figure 2, we present the weighted total (direct and indirect) BL and FL for the US economy, in 1997, 2008, and 2020. The majority of the FABS sectors remain in the key sectors quadrant for the whole period, with business support services (138) standing as independent from backward and forward linkages sector, while employment services, securities, and insurance agencies, move between forward and key positions. Three interesting observations emerge from the analysis of direct and total linkages. First, the banking sector (116) exhibits a rise in linkages in the run up to the subprime crisis, after which it declined significantly, reflecting a decreasing importance for the US economy in terms of the direct and total backward and forward linkages. On the other hand, the insurance sector shows a moderate increase in its “key-ness,” whereas the real estate sector shows the most dramatic increase, becoming the most inter-sectorally connected part of FABS in the US economy. Weighted total linkages of the FABS sector.

Clusters

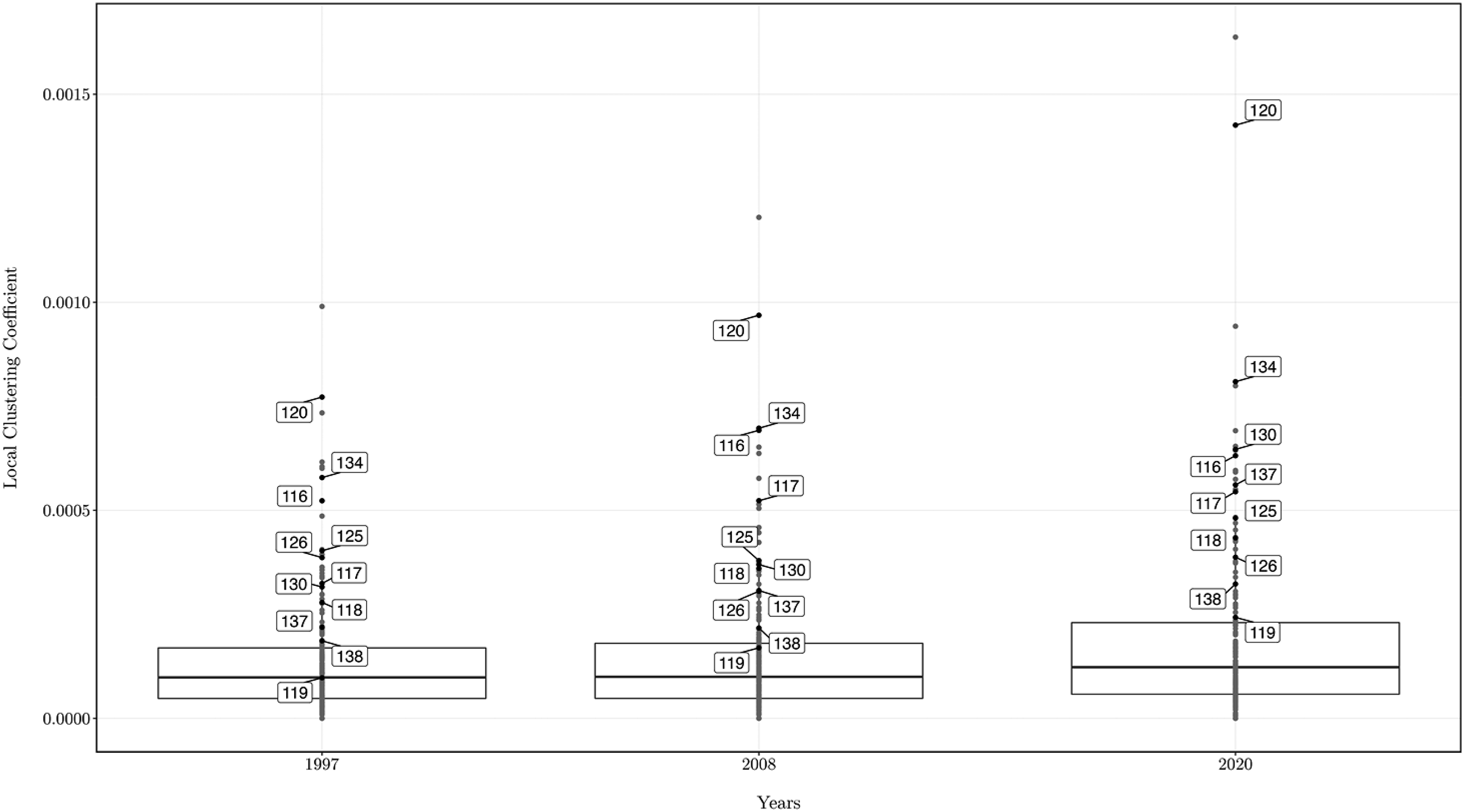

In Figure 3, we present the distribution of local clustering coefficients (CC) of the FABS sectors for 1997, 2008, and 2020, along with their first, second, and third quartiles. The clustering coefficient shows the ratio of links that are formed between each sector and its direct neighbors, divided by the number of links that could possibly exist between them. From the table, we see that all FABS sectors in 1997, with the exception of agencies, brokerages, and other insurance related activities (119), have a local clustering coefficient greater than the third quartile, meaning that they have values greater than the 75% of all sectors of the US economy. Distribution of local clustering coefficients of the FABS sectors.

By 2008, all FABS sectors increased their local CC significantly, except for legal services and accounting, the clustering coefficient of which declined. Meanwhile the CC of agencies and brokerages of insurance activities remained slightly lower than third quartile, despite an increase. By 2020 the legal and accounting subsectors recovered to their pre-crisis levels of CC, while all the other FABS sectors increased their clustering. The only exception from this trend was banking, the CC of which has not recovered to the pre-crisis level. These observations imply that the FABS sectors are part of densely interconnected neighborhoods or hubs of the US economy and with strong inter-sectoral relationships with the rest of the economy. The only sector that has reduced its interactions with the rest of the US economy since 2008 was banking, but it still had a CC higher than 75% of all sectors.

Centralities

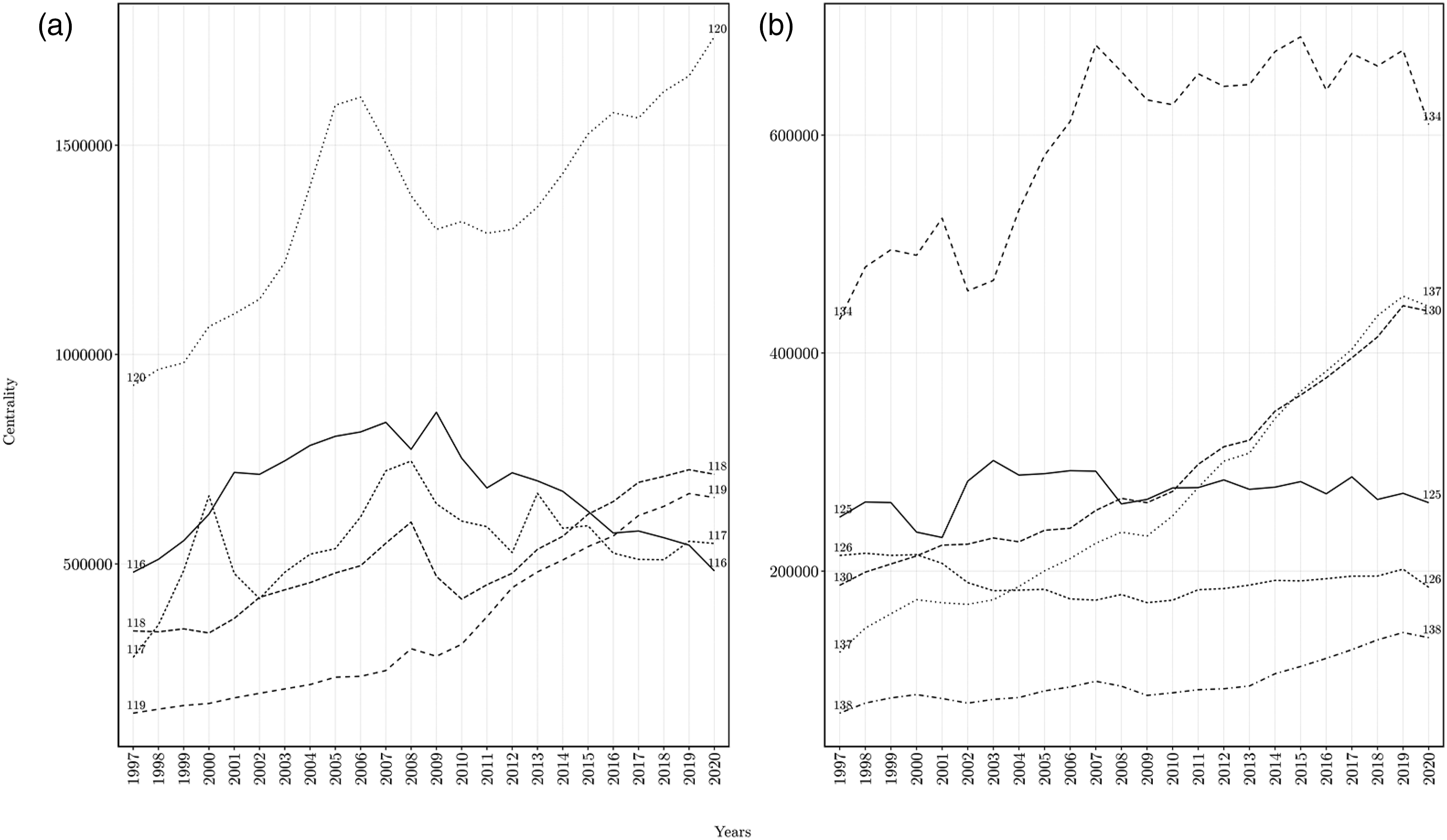

In Figure 4, we present the evolution of Strength Centralities of the US FABS complex. We find that the real estate sector (120) exhibits the highest strength centrality in the FABS complex, peaking in 2006, right before the Global Financial Crisis, falling considerably during the crisis and having a slow but steady recovery for the following 10 years. The strength centrality for credit intermediation (116)—excluding the securities, commodity contracts, fund, trusts, and other financial investments sector captured in (117)—has not yet recovered to the pre-crisis levels. From 1997 to 2009 (except for 2008), the financial sector showed a moderate increase in strength centrality. After 2009, we observe a sharp decrease in strength centrality until 2011, a small recovery for the next year (2012) and a slow but persistent reduction until 2020. The securities and funds sector (117) shows a remarkable volatility in its strength centrality scores, following the ups and downs of the capital markets. Strength centrality rises during the dot.com bubble of 2000, then falls until 2002, only to slowly recover and surpass the 2000 levels in 2008. Since the subprime crisis, the sector exhibits a falling strength centrality, with the important exception of 2013, when strength centrality of securities sector captured the world-wide rally in stock and securities markets. In that year, the Dow Jones, S&P-500, and Nasdaq, gained 26%, 29%, and 40%, respectively. For the insurance sector, we observe that insurance carriers (118) were hard hit by the subprime crisis in the period from 2008 to 2010, and only recovered to the pre-crisis levels in 2015. Total strength centralities of the FABS sector.

In contrast, the sub-sector of agencies, brokerages, and other insurance related activities (119) showed a remarkable resilience to the crisis, constantly increasing its strength centrality, at particularly high rates after the 2007–2009 financial crisis. Legal services (125), accounting, tax preparation, etc. (126), and business support services (138) have remained relatively constant in terms of their strength centrality for the whole period. On the other hand, consultancy (130) and employment (137) services, seem to exhibit a constant increase in strength centrality, even during and after the financial crisis. Lastly, the management of companies sector (134) has moderately increased its strength centrality, with the financial crisis slightly decreasing its centrality, which recovered to its pre-crisis levels in 2014.

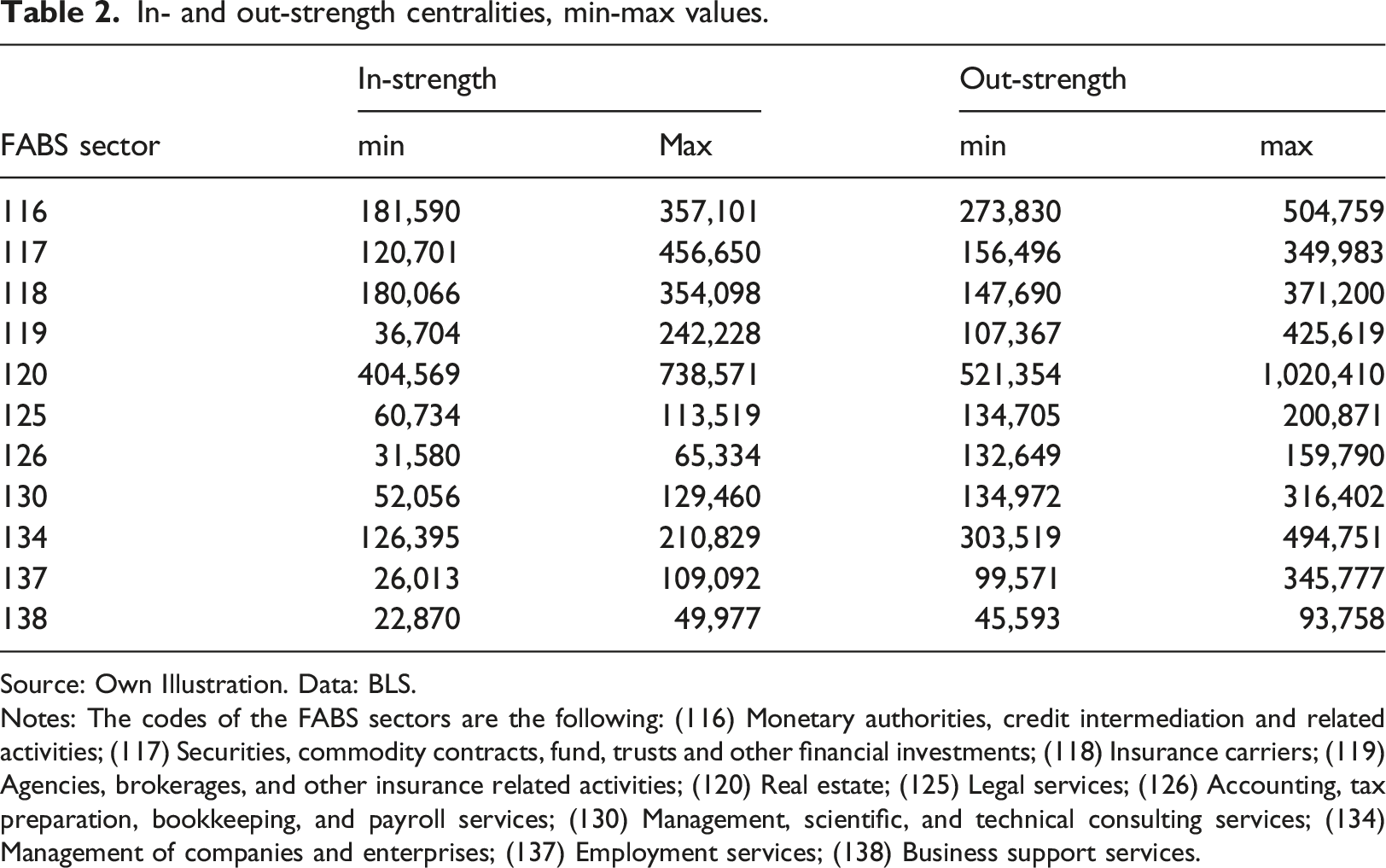

In- and out-strength centralities, min-max values.

Source: Own Illustration. Data: BLS.

Notes: The codes of the FABS sectors are the following: (116) Monetary authorities, credit intermediation and related activities; (117) Securities, commodity contracts, fund, trusts and other financial investments; (118) Insurance carriers; (119) Agencies, brokerages, and other insurance related activities; (120) Real estate; (125) Legal services; (126) Accounting, tax preparation, bookkeeping, and payroll services; (130) Management, scientific, and technical consulting services; (134) Management of companies and enterprises; (137) Employment services; (138) Business support services.

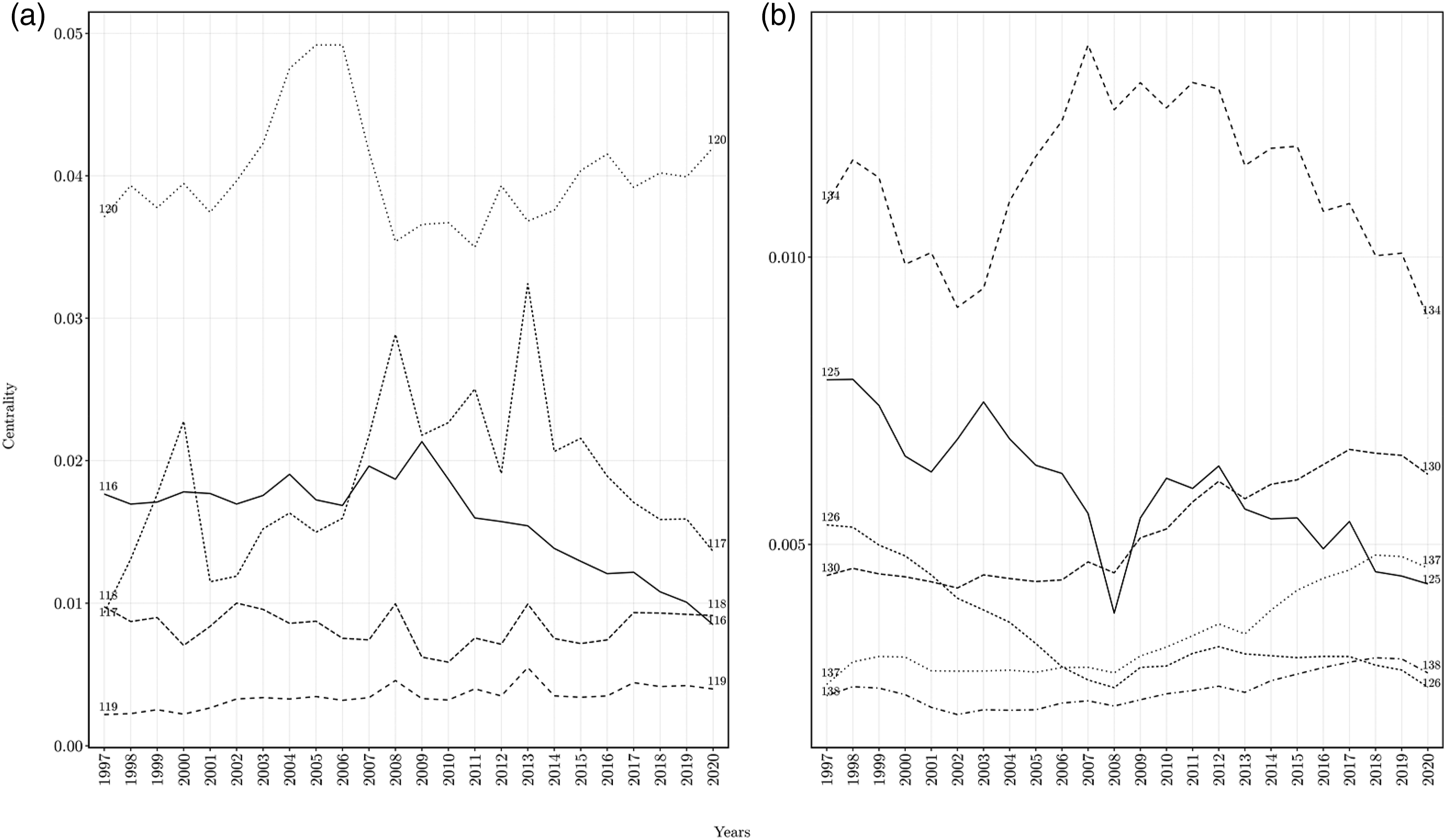

In Figure 5, we present the PageRank centralities of the FABS complex. PageRank captures not only the direct connections of a sector with its immediate buyers and suppliers but also the indirect linkages with the rest of the economy, while simultaneously removing the effects of mega-suppliers from the centrality scores. Four ABS sectors—employment services (137), legal services (125), business support services (138), and accounting services (126) —and one financial services sector—insurance agencies and brokerages (119), share similar, low, PageRank scores. Consulting services (130), as for Strength Centrality, exhibits a rising trend even after the crisis, whereas insurance carriers (118) and companies’ management (134) have not yet recovered to their pre-crisis levels. An interesting difference between Strength and PageRank centralities is the case of the financial sector, particularly financial intermediation (116) and securities (117). Whereas measuring only the first-order weighted links (strength), we observe that financial intermediation is more central than securities, and only in 2019 the latter surpasses the former, when we account for indirect linkages, we see that the securities sector has considerably higher PageRank centrality than financial intermediation since 2006. Although PageRank centrality of both sectors falls after the crisis (with the exception of the 2013 rally for 117), we might have empirical evidence of a rise in the relative power from traditional financial institutions and other financial entities, like investment funds, trusts etc. PageRank centralities of the FABS sector.

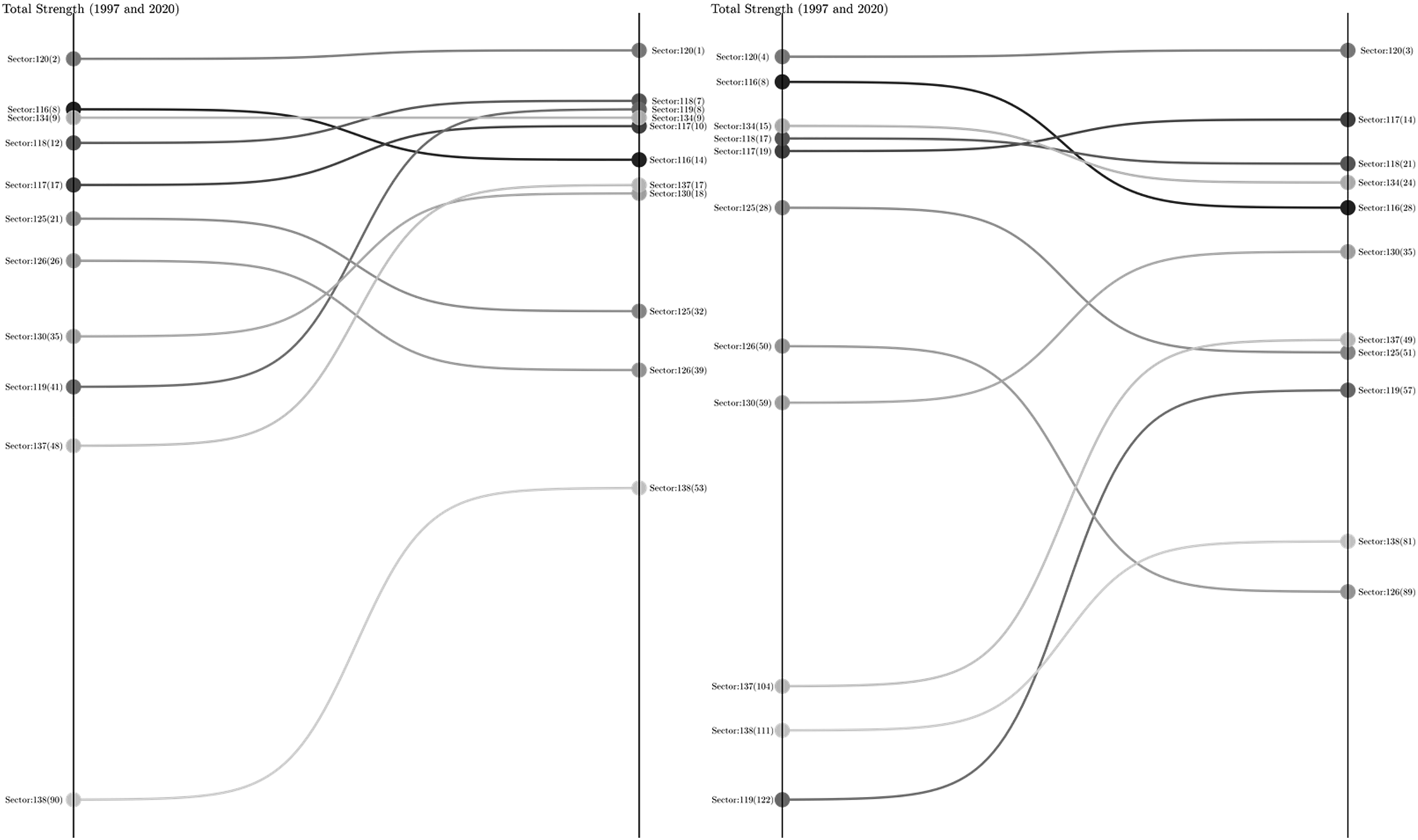

In Figure 6, we show the ranking of FABS sectors based on the two centrality measures. The real estate sector is the single most central sector in the US economy in 2020 by strength centrality and the third in terms of PageRank centrality. As for other FABS sectors, we observe a fall in the ranking of accounting, legal and banking sectors for both centrality measures, as well as for management and securities sectors for the PageRank. In contrast, business support services, employment services, insurance, and consultancy services have increased their rankings within the US economy. Ranking of FABS sectors by strength and PageRank centralities.

As a robustness exercise, we estimated the total strength and Page Rank centralities for the US economy, excluding the self-loops of each sector (i.e., the transactions of a sector with itself). This means that the main diagonal of the input–output tables that serve as the adjacency matrices of the US economic network, were set to zero, to exclude the impact of input purchases and sales within the same sector. The results are shown in the Supplemental Material demonstrating that the centrality scores share the same general patterns after controlling for the within-sector transaction for both total strength and Page Rank centralities, with the exception of agencies, brokerages, and other insurance related activities, the strength centrality of which falls significantly when we exclude self-loops. Moreover, in order to contextualize the magnitude of each component of the FABS complex and also be able to compare the relative importance of each sub-sector in the US economy, we show in Supplemental Materials, the share of each component of the FABS complex to total real output of the US economy.

Discussion

The core finding of our empirical analysis with respect to the impact of the subprime crisis on the pace of financialization with respect to the financial sector and the complementary business services, is its impressive resilience. Our results show that the FABS complex has increased its inter-sectoral importance in the US economy not only in the run up to the subprime crisis but also beyond. The majority of the FABS sectors can be classified as key sectors with above average backward and forward linkages. Meanwhile the distribution of the clustering coefficients implies a high likelihood to find well-connected sectors in the US economic network linked to one of the FABS sectors. Likewise, the evolution of the Strength and PageRank centrality measures sheds new light on the importance of the FABS sectors in the US economy.

Our results provide empirical support for the studies that conceptualize financialization as a phenomenon that extends beyond the mere increase in the size of the financial sector (Aalbers, 2019; Christophers, 2018; Jayadev et al., 2018). The fact that almost all FABS sectors have been identified as key sectors in the US economy and their centrality scores have increased in the aftermath of the financial crisis, sustains their arguments. Moreover, since our analysis covers 24 years, our findings complement the theoretical claims on the secular tendency of capitalist economies towards financialization, as the result of the rising importance of money circulation, financial innovations, and institutions (Vercelli, 2013). Moreover, the findings on the backward and forward linkages, the distribution of the clustering coefficients and the centralities of the FABS complex, come in stark contrast to the expectations that had been nurtured in the last decade from parts of the literature and political commentators (Lapavitsas and Mendieta-Muñoz, 2018). Although the banking sector has indeed reduced its importance in the US economy in terms of inter-sectoral linkages and centrality after the global financial crisis, the rest of the financial sector, along with the other complementary business services that comprise the FABS complex, have become significantly more important.

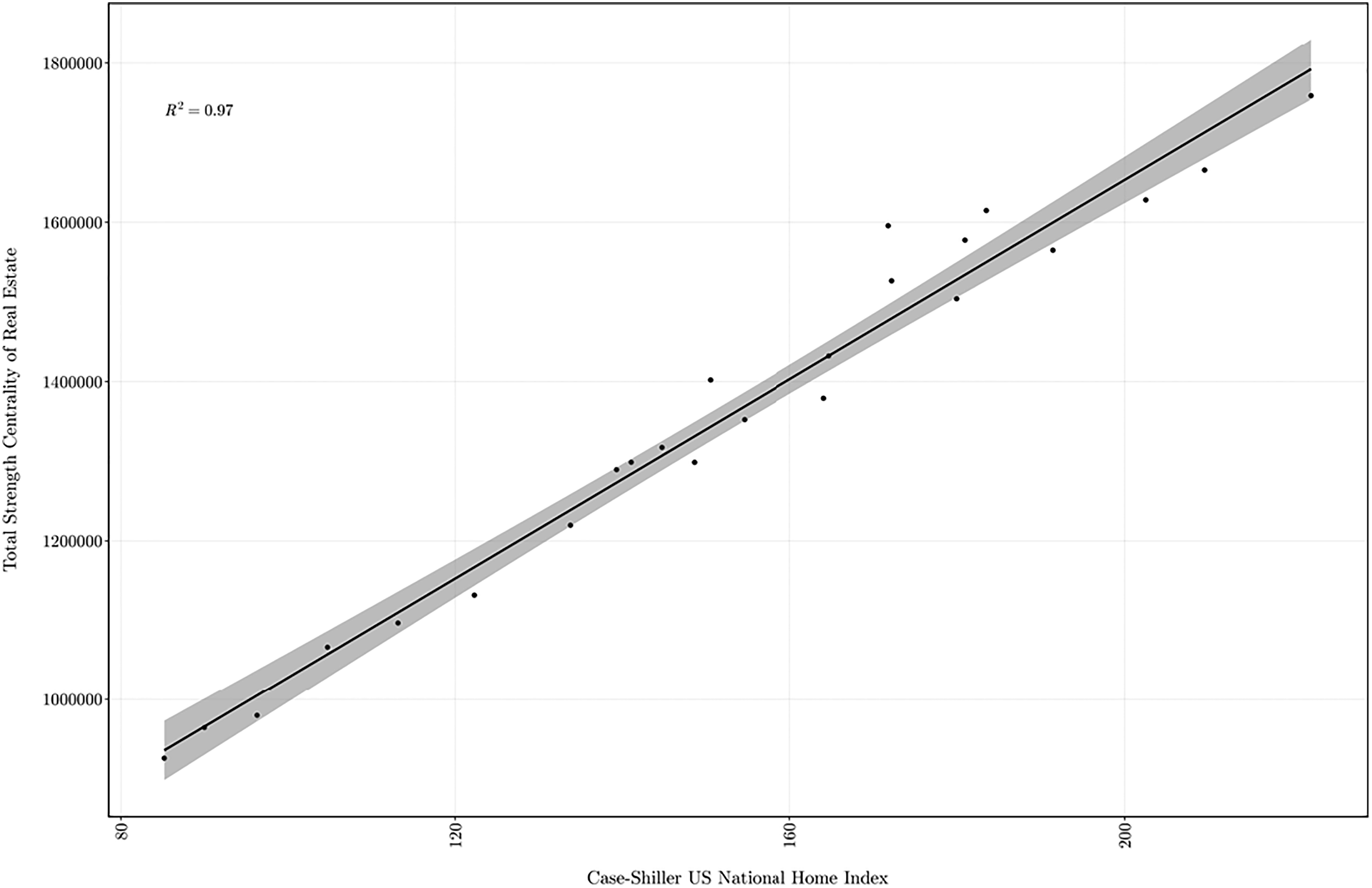

Furthermore, our main results demonstrate that the real estate sector has been an important and central sector of the US economy, a claim that has been indicated by the respective literature, as well (Aalbers, 2008; Fernandez et al., 2016; Fernandez and Aalbers, 2016). Aveline-Dubach (2020), for instance, reports that in 2017 the vast majority of the 50 largest private equity real estate firms in the world were headquartered in the US. With regard to real estate investment trusts (REITs), which are entities that hold financial securities dedicated to long-term property investments, the “US accounts for 64% of the REIT market capitalization globally (US$1069 billion in 2017) with 224 publicly-traded structures” Aveline-Dubach (2020: 398). The latter observation is also consistent with the empirical research on the centrality of economic sectors and the inter-sectoral linkages. Song et al. (2005, 2006) comparing the BL and FL of the real estate sectors for seven OECD countries from the early 1970s to 1998, confirm that the US, along with Australia, Denmark, France, and Japan, has one of the highest ratios in the group, indicating the important role that the sector plays in these economies. The dominance of the real estate sector in the US economy has been also reported by Xu et al. (2011) and McNerney et al. (2013). The above observation is not independent of the rising housing prices in the US. According to empirical research that investigates the correlation between housing prices and various variables that represent the performance of the real estate sector, there is a well-established positive empirical relationship between them (Highfield et al., 2015). In Figure 7, we show the very high correlation (R

2

= 0.97, ρ = 0.98) between the Case–Shiller National Home Index and the Total Strength centrality of the real estate sector. Scatterplot of total strength centrality of the real estate sector and Case–Shiller home index (1997–2020).

For the advanced business services sectors that belong to the FABS complex we observe that they have managed to also increase their inter-sectoral linkages and centralities, with the exception of legal and accounting services. This observation is in line with the impacts of the subprime crisis on the business model of the legal services industry in the US, identified by the literature (Greenberg and McGovern, 2012; Valentine, 2019). Valentine (2019) underlines that after the subprime crisis, law firms have increased the employment of temporary employees, counselors, and income partners, at the expense of legal associates and new graduates, whereas their revenue sources have become more sensitive to business cycle fluctuations, since the majority of their revenues come from commercial clients. 1 Moreover, the demand for legal services has changed considerably after the crisis, with businesses either demanding lower prices from law firms or outsourcing their needs to alternative service providers in low-cost locations Valentine (2019: 9). The securities sector seems less able to recover from the financial crisis, as the strength and PageRank centralities show, confirming analyses from the perspective of economic and financial geography that focus on remuneration and employment dynamics (Wójcik and Cojoianu, 2018).

The significant increase in the centrality (both direct and indirect) of the other FABS sectors is also noteworthy, with the business support services, employment services, insurance, and consultancy services having increased their rankings with respect to the rest of the US economy. Exploring the links between financialization and employment relations, Gospel and Pendleton (2003), Palpacuer et al. (2011), Appelbaum et al. (2013), and Clark (2016) report that beyond direct wage freezes and cuts, there is evidence that over the last decades the financialization of corporate governance is also associated with attempts to influence the broader institutional setting around labor markets and human resource management. These include union de-recognition, lobbying for the liberalization of employment relations, and even the breach of employment contracts. Such trends pave the way for the rise of workforce casualization, feeding the demand for the use of employment services. Katz and Krueger (2019), for example, analyzing survey data on the size of alternative work arrangements in the US—including temporary help agency workers, on-call workers, contract workers, and independent contractors and freelancers—compare 2005 and 2015 and report a significant 5% rise between 2007 and 2009, despite the great recession. Similarly, a BLS (2021) report records the persistent growth of the temporary help services industry in the US before and after the great recession, characterizing as a key feature of the US labor market.

The above trend of increased centrality of the employment and business support services in the US economy, cannot be viewed independently from the context of the internationalization and fragmentation of global production and the rise of outsourcing and offshoring. The latter, as corporate strategies for reducing production costs and re-focusing business activities from low-cost secondary processes to high-value core activities (Milberg and Winkler, 2013), have fueled the demand for advanced business and employment services. Especially, in an environment of high uncertainty, precipitated by the 2007/09 subprime crisis and more recently by the effects of the pandemic on the normal functioning of complex, geographically dispersed, supply chains, business services providers, and specialized consultancy firms are more relevant than before.

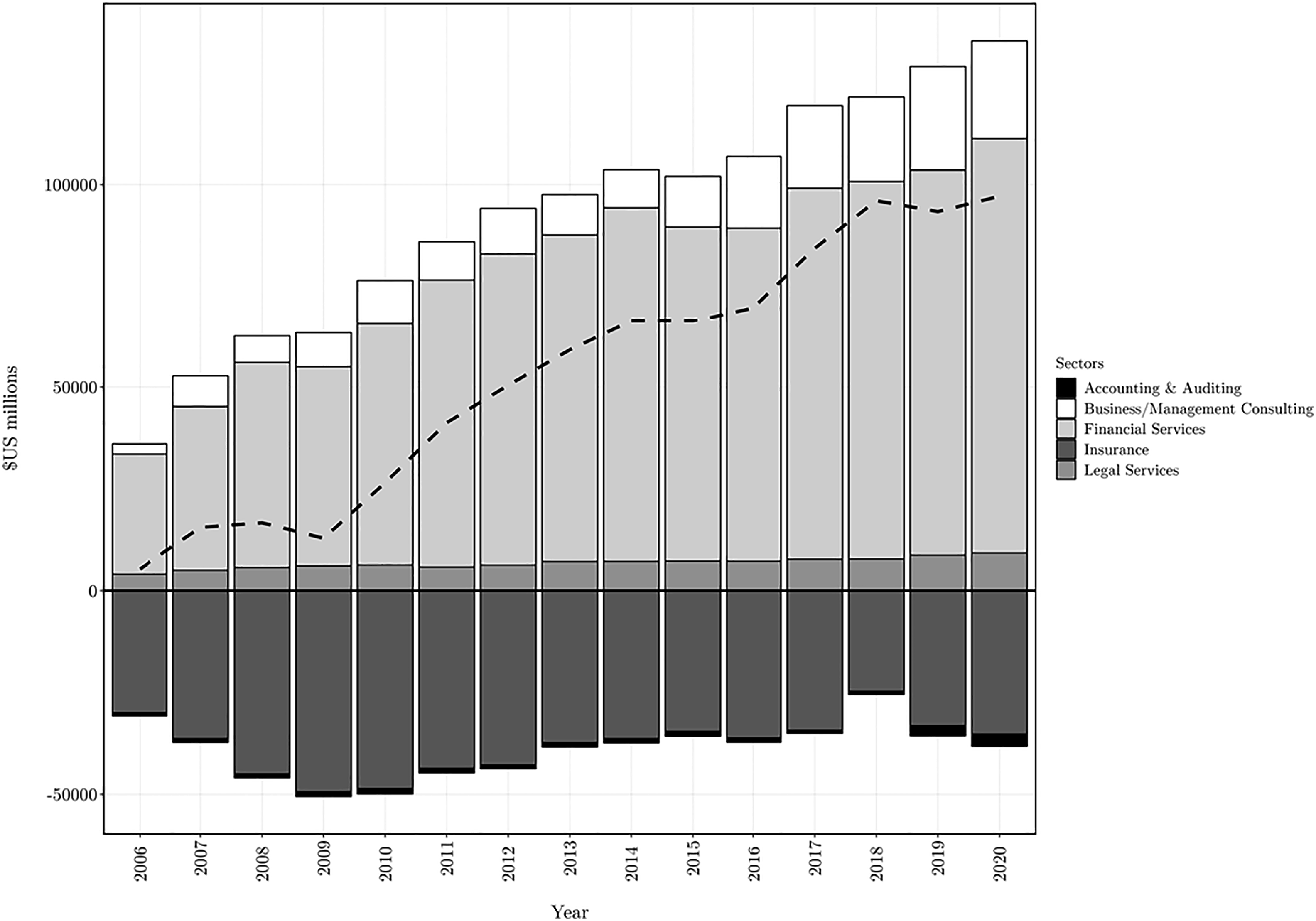

An obvious limitation of utilizing national input–output tables in our empirical analysis of financialization is that we need to abstract from the direct and indirect effects of international trade. At the level of analysis of this paper, we are not able to find comparable data on the US inter-sectoral trade of financial and other business services. Such an analysis, would require either the compilation of new data series or taking bold assumptions about the composition of imports and exports of US financial services, which nevertheless produce biased results (Patunru and Athukorala, 2021; Winkler and Milberg, 2012). In order to mitigate this limitation of our analysis, we provide in Figure 8, a gross picture of the relationship of US FABS sectors with the rest of the world. The US economy exhibits a trade deficit in insurance and accounting services, reaching a peak in 2010, which, however, is overcompensated by a high and continuously increasing trade surplus in financial services, business, and management consulting, as well as legal services. This observation demonstrates the importance of US financial actors in global financial markets and in the context of this paper can be perceived as a preliminary indication of the rising importance and influence of the US in global markets. Exports and imports of financial and business services, 2006–2020.

Conclusions

The purpose of this paper is to contribute to the literature on the financialization of the US economy, by presenting new empirical evidence about the multiplicity of the phenomenon and its presence in the inter-sectoral relationships between industries. Specifically, our focus has been on the evolution of the FABS complex, bringing together insights from financial geography, input–output analysis, and network theory.

Based on the review of the financialization literature, we have argued that it has understudied how financialization affects the inter-sectoral structure of the US economy, and how it has transformed the interdependencies of the financial sector with other economic sectors, and particularly with the business services sectors that complement financial activity. We address this limitation by investigating the relationships of the FABS complex with all other sectors of the economy, estimating backward/forward inter-sectoral linkages, clustering coefficients, and measures of centrality, utilizing a long time series of input–output tables from the BLS at a highly disaggregated level, with 205 × 205 dimensions. By doing so, we are able to unveil the multiplicity of the financialization processes, gain a better understanding about its effects for the overall structure of the US economy, and reflect upon various factors that have been proposed by the literature to explain the changing position of the FABS complex and its components.

The main findings of our study show that the process of financialization in the US has not been halted after the global financial crisis. Contrary to expectations about the advent of a new accumulation regime in which financial power will be significantly tamed by regulation, the centrality, and the backward and forward linkages of the FABS complex have significantly increased. Additionally, we were able to map the relative changes in the position of the FABS sectors with respect to the rest of the US economy and relate these results with the discussion about the driving forces behind financialization, whereas the banking sector, legal services, and accounting show signs of a relative decline in terms of their inter-sectoral linkages and centralities, other sectors of the FABS complex, including the real estate sector, consulting and employment services, business support services, insurance agencies, and to some extent the asset management and securities industry, have fully recovered from the crisis and even significantly increased their importance. This recovery applies also to real estate as one of the most central sectors of the US economy.

In summary, this study contributes to a more nuanced understanding of the nature and process of financialization. The complexity of the modern financial world characterized, among others, by a functional disaggregation of financial production, requires a careful and detailed mapping of those actors and FABS components that hold central positions in financial networks. Drawing inspiration from the analytical framework of the GFN, the results of this paper could be viewed as evidence for the presence of a stickiness of power, that is the ability of powerful financial actors to control the networks of information, standards, trust, and credibility that allow money and value to exist (Haberly and Wójcik, 2022). We see two directions for future research that deserve particular attention. The first could concentrate on a more in-depth analysis of specific segments of the FABS complex combining not sectoral input–output data with firm-level data on financial transactions that could be used to construct the input–output structure of those sectors with more dimensions. The second direction could shift the focus of the analysis to the global scale and utilize international multi-regional and multi-sectoral input–output tables, emphasizing geographical and functional position of financial actors in the globalized and financialized economy.

Supplemental Material

Supplemental Material - The multiple faces of financialization: Financial and business services in the US economy, 1997–2020

Supplemental Material for The multiple faces of financialization: Financial and business services in the US economy, 1997–2020 by Panagiotis Iliopoulos and Dariusz Wójcik in Competition & Change

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The authors have received funding from the European Research Council (ERC) under the European Union’s Horizon 2020 research and innovation programme (grant agreement number 681337). The article reflects only the authors’ views, and the ERC is not responsible for any use that may be made of the information it contains.

Supplemental Material

Supplemental material for this article is available online.

Note

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.