Abstract

Most foreign capital-led, export-oriented Eastern EU member states and the consumption-driven Southern European countries suffered a heavy blow during the Global Financial Crisis (GFC) in 2008–09. The GFC exposed the vulnerability of these economies to external shocks and raised the need for readjustment of their growth models through state intervention. While the rise of illiberal governments drove readjustment in the East, the main driver was externally fomented in the South. This article focuses on state aid, a particular instrument of industrial policy, which has been a main vehicle for growth model readjustment. We seek to explore whether the provision of state aid in the two European semi-peripheries contributes to long-term post-crisis recovery by promoting competitive investments in two Eastern (Hungary and Poland) and two Southern EU members (Portugal and Spain). Relying on the European Commission’s state aid database, we show that after 2013, in the consumption-driven South, governments aimed to strengthen supply through aid, while in the export-oriented East, they were more concerned about promoting exporting firms. The article thus reveals how state aid may preserve and reinforce existing growth models in the semi-periphery even if strategic aims and rhetoric target readjustment.

Introduction

The Global Financial Crisis (GFC) generated heated debates among political economists and those discussions mostly involved three related, yet separate streams of literature. First, the GFC revived debates on the role of the state in facilitating economic development and, in particular, the role of industrial policy in contributing to economic restructuring and upgrading (Bailey et al., 2015; Esteban et al., 2013). Second, the drivers of institutional stability and change in advanced capitalist economies gained renewed attention in the comparative political economy (CPE) literature, which was also reshaped with a new approach, the demand-focused growth model perspective (Baccaro and Pontusson, 2016; Blyth et al., 2022). Third, within the European context, economic convergence and divergence, core-periphery relations, and the consequences of the constraints and opportunities offered by the EU’s transnational regulatory framework on member states have gained increasing interest among scholars (Börzel et al., 2017; Börzel and Langbein, 2019; Bruszt and Langbein, 2020).

Although these streams of literature are closely related to each other, their synergies have not yet been realised. The CPE literature, including its recent extension, the growth model approach, downplays the role of the state in the adjustment and restructuring of the economy and nearly entirely neglects industrial policy as an important vehicle for the state to steer developmental outcomes (Bulfone, 2022). Part of the literature on industrial policy in advanced capitalist economies stresses the limitations to the use of direct policy instruments because of mounting pressures on state budgets (Zohlnhöfer et al., 2018). However, the last decade has also witnessed a burgeoning debate on how post-GFC industrial policy may serve the state to regain control over markets and shape economic restructuring (Clift and Woll, 2012; Mazzucato et al., 2015; Mertens and Thiemann, 2019). Much of the research on regulatory integration in the EU highlights the diverging economic trends between the core and periphery and emphasises the constraining character of the single market and Eurozone regulations on member states’ policy space (Ceron and Palermo, 2022; Magone et al., 2016; Volintiru et al., 2021). Contrary to these views, Bruszt and Langbein (2020) recently showed how the EU’s regulatory frameworks offered novel resources and opportunities for member states to manage developmental outcomes.

This paper aims to link the above literature by exploring how states in the European semi-periphery readjust their growth models and contribute to economic upgrading within the EU context of narrowing policy space. The paper thus aims to fill an important gap in the CPE literature about state activism, exposed by Bulfone (2022). By focusing on the EU’s Eastern and Southern semi-periphery, we explore how some of the most vulnerable members of the EU, which also face severe limitations to their current growth models, have utilised transnational regulatory opportunities to upgrade their economies in the post-GFC period. Both the EU’s Eastern and Southern members traditionally struggle to catch-up with the most advanced, core EU countries, and, recently, the engines of their economic growth have been depleted, although for different reasons. Both semi-peripheries thus face important economic challenges that need to be addressed: to focus on upgrading their economies and target greater domestic value capture. We concentrate on state aid, a key element of industrial policy and explore the high-tech and knowledge-intensive profile of both individual aid measures and schemes beyond 2013, the year when post-GFC recovery was mostly over in the two peripheries.

After they entered the EU in the 1980s, the consumption-oriented mixed-market economies in the South (Molina and Rhodes, 2007) could minimally narrow the economic gap with the most prosperous members, only to experience divergence in the post-GFC period. The lasting economic stagnation in the South has urged both policy-makers (see for instance Prodi, 2014) and scholars (Godinho and Mamede, 2016; Lucchese et al., 2016) to demand a profound reform of economic policies because existing measures proved largely ineffective in triggering growth and stimulating innovation. The economic decline of the South is often attributed to the incompatibility of their growth models with the EU’s single market and monetary integration, which seems to favour export-oriented growth models (Johnston and Matthijs, 2022; Pérez, 2019). This is because the monetary integration exposed the consumption-led, inflation-prone models to unsustainable imbalances in external trade and lending without offering any correctives (Johnston and Regan, 2016).

In contrast, the foreign direct investment (FDI)-dependent market economies in the East have experienced a relatively quick post-crisis recovery-as they had not been so seriously hit-and are incrementally converging towards the core. However, their GDP per head is still far below that of the most developed members and several observers suggest that the region’s main competitive advantages in the form of cheap, skilled labour have been exhausted (Galgóczi and Drahokoupil, 2017; Kalotay, 2017). Finding new sources of growth thus would be necessary (Sass, 2017). Key decision-makers also share a critical view on FDI-led development and urge for economic upgrading through greater state involvement (Morawiecki, 2016).

The success of economic upgrading depends on how well the state can promote local or transnational competitive businesses that participate at the higher ends of global value chains (Gereffi et al., 2005). Such economic upgrading may then translate into sustained economic development and higher living standards (Sen, 1999). Within the EU, the policy space for central governments to take individual developmental action is limited by the single market’s regulatory framework, particularly by competition policy rules, which constrain the scope of industrial policy. However, besides constraining central governments, EU regulations also redistribute resources and opportunities across member states, thereby broadening the space of manoeuvre for members that bear the sufficient institutional capacity to take advantage of them (Bruszt and Langbein, 2020). Hence, the ability of the (semi)peripheral members to recover from economic crises and upgrade their economies crucially depends on how well they can take advantage of the opportunities and resources offered by the EU’s transnational regulatory regime.

Our findings suggest that the two semi-peripheries took only limited steps to adjust their growth models towards high value-added activities. Both the sectoral and ownership structure of post-GFC state aid mostly follow prevailing structural economic characteristics exposing a mismatch between the stated objectives and the actual policy practices. The paper proceeds with the introduction of the research design, which is followed by a review of the literature on growth models, industrial policy and the relevant constraints and opportunities offered by European integration, in particular the EU’s state aid control. The empirical section explores the state aid grants and schemes adopted in the selected countries after 2013. The final section discusses the findings and concludes.

Research design and expectations

State aid in the form of direct grants, tax benefits, guarantees or soft loans is one of the most visible state interventions in the market. If it aims to foster employment, growth and export competitiveness 1 by targeting firms and sectors that are internationally competitive and active in high value-added segments, then it becomes an important vehicle for upgrading industrial policy (Bulfone, 2022). Our outcome variable is therefore the value-added of the supported firms and sectors in terms of technology and knowledge intensity. We seek to explore the differences between the two semi-peripheries regarding their post-GFC state aid practices, especially the difference in supporting low, medium and high value-added activities. In classifying those activities, we rely on the grouping prepared by Eurostat based on NACE two-digit level sectors (see annex).

Empirically, we focus on the post-GFC state aid practices in two Southern (Portugal and Spain) and two Eastern EU members (Hungary and Poland). While Portugal and Spain are typically considered consumption-driven economies (Johnston and Matthijs, 2022), Hungary and Poland are exemplary cases of FDI-led, export-oriented growth regimes (Ban and Adascalitei, 2022). The pairwise selection follows the logic of the ‘most similar systems’ design within the two distinct growth regimes. Hungary and Poland share similar dependent growth models with high exports, and they have so far remained outside the Eurozone, thus they face less strict fiscal constraints than the Southern members. In these two Central European countries, the traditional sources of competitiveness (cheap, skilled labour) no longer represent a competitive advantage while the quality of human capital, innovation and productivity lag behind the most advanced capitalist economies (Iammarino et al., 2019). Both Hungary and Poland have recently experienced an illiberal turn with economic nationalist governments trying to shift away from dependent growth by promoting domestically owned firms in selected, mostly inward-oriented sectors (Kozarzewski, 2021; Sebők and Simons, 2021). In this respect, domestic political and ideological motivations are the main drivers behind the readjustment of the Hungarian and Polish growth models.

Portugal and Spain represent similar cases among the Southern consumption-led economies. Both countries face declining growth, and experienced the same EU pressures for structural reforms involving a persistent push for readjustment towards an export-led model (Bulfone and Tassinari, 2021). Unlike in the case of Hungary and Poland, growth model readjustment in Spain and Portugal can be considered as externally fomented (Pérez and Matsaganis, 2019). At the same time, in both countries, central governments have traditionally been committed to the proactive support of the economy (Ban, 2016; Mamede et al., 2014). However, the Spanish and Portuguese fiscal space is heavily constrained by the Eurozone rules. Besides the different sizes of their economies, an important distinction between the two countries is that Spain did not need to resort to an IMF rescue package during the GFC (Meardi, 2014) and it has a more competitive profile in high-tech industries than Portugal, that is ‘overspecialized’ in low-tech segments (Godinho and Mamede, 2016).

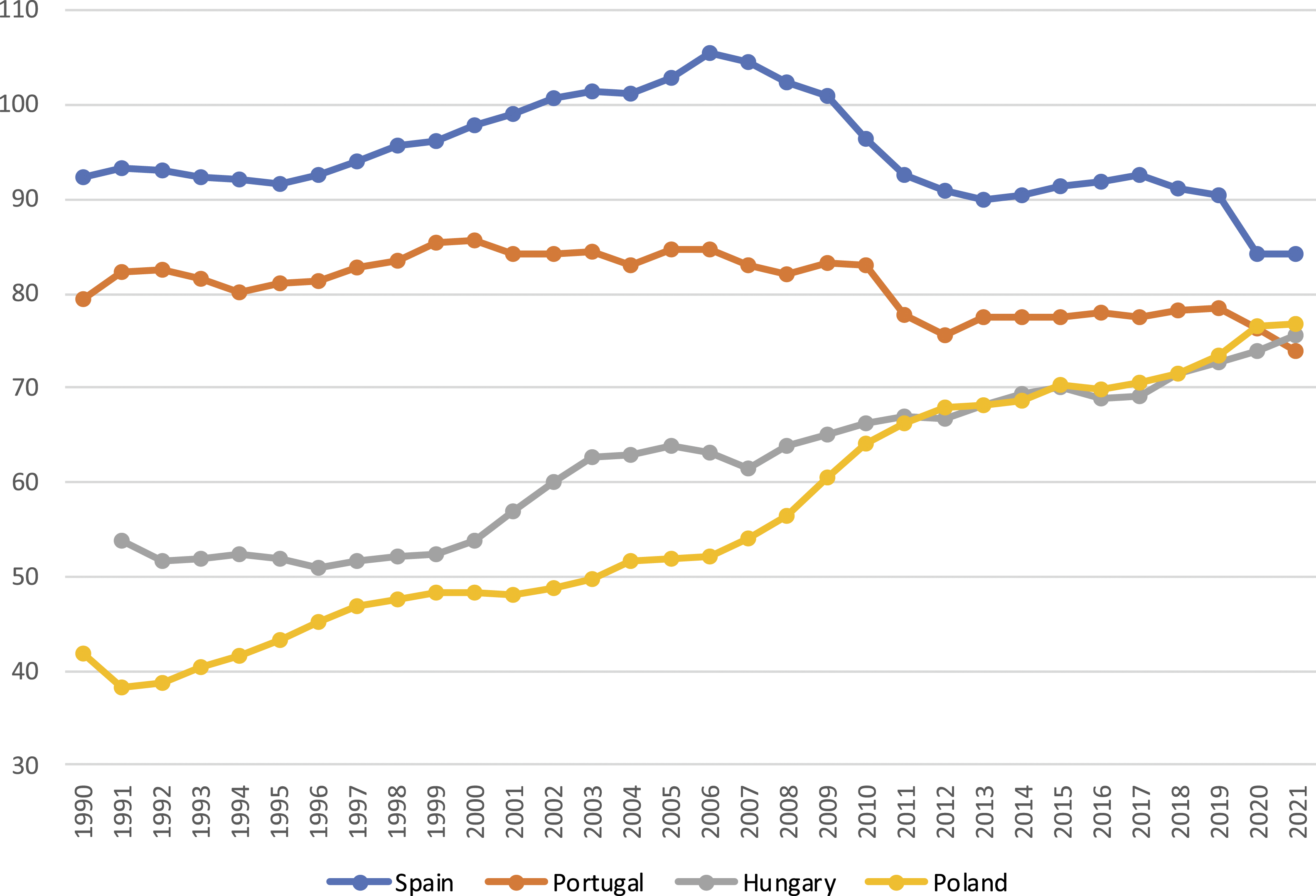

The four country cases also allow for a comparison of post-GFC state aid practices in semi-peripheral growth models exposed to different dynamics of internal and external pressures. While the FDI-dependent, export-oriented Hungarian and Polish economies have so far performed relatively well, the ruling right-wing, anti-liberal governments began to address their excessive dependence on foreign capital by resorting to economic nationalism and they became more selective towards FDI inflows (Bohle and Greskovits, 2019). Meanwhile, the prolonged crisis of the consumption-oriented Portuguese and Spanish growth regimes has triggered mounting external pressures for improving their export competitiveness and attracting more FDI (Johnston and Regan, 2018; Pérez and Matsaganis, 2019). The EU-imposed fiscal constraints and the economic decline drained the Southern members’ budgets, leaving limited tools for them to stimulate their economies (Scharpf, 2016) unlike in the relatively fast-growing non-eurozone economies in the East (Figure 1). Purchasing power adjusted GDP per capita as a percentage of EU27.Source: calculations from World Bank, World Development Indicators data.

The four cases, therefore, offer a controlled comparison of state aid practices, under different external and internal structural conditions. The illiberal Eastern governments aimed to engage in economic upgrading by promoting domestic ownership at the expense of FDI, although their competitiveness and growth performance are primarily tied to foreign-owned firms active in low value-added activities. This ‘illiberal readjustment’ of the Eastern growth model may therefore bear an inherent tension between structural economic conditions (FDI-dependence) and political ambitions (promotion of domestic businesses). Conversely, the Southern governments face an externally constrained fiscal space for state aid spending and an externally fomented readjustment towards an export-oriented growth model instead of the so far prevailing consumption-driven model. However, the forced turn towards exports is taking place in a context where historically influential domestic businesses traditionally promoted by the state (Etchemendy, 2004) suffer in those inward-oriented sectors that were previously pulling these economies such as construction and finance. Thus, the externally triggered readjustment in the South generates considerable mismatch between the goals of readjustment and the consumption-driven domestic political economy.

The above contradictions between stated policy objectives and structural economic constraints in both semi-peripheries raise whether the former or the latter will prevail in post-GFC state aid practices. Business power theory argues that business-state interactions are characterised by mutual dependency between the interests of the state and the dominant businesses (Culpepper, 2010). Applied to growth models, it follows that sectors and firms that are key to the success of national growth models enjoy greater access to and influence over governments (Blyth et al., 2022: p. 33), thus the state may consider incorporating their interests into specific policies.

We therefore expect that the Southerners would be inclined to distribute aid to the leading but in the post-GFC period ailing, less technology- and knowledge-intensive, domestically owned businesses and sectors rather than to the knowledge-intensive segments. At the same time, because of its more developed high-tech segments, Spain may be better suited for turning its economy more competitive and export-oriented than Portugal; thus, it is also more likely to channel aid to knowledge- and technology-intensive activities, thereby defying the prevailing structural constraints. Given that the Hungarian and Polish growth models rest on export-oriented, foreign-owned manufacturing firms, it follows that these regimes would target those companies with state aid. However, the illiberal turn accompanied by economic nationalism and the subsequent authoritarian tendencies in Hungary and Poland may allow for post-GFC state aid promoting the creation of national champions instead of foreign investors, thereby mirroring industrial policy practices implemented in the past by core EU members (Bulfone, 2022). Nevertheless, allocating fiscal subsidies to domestically owned sectors does not necessarily involve the promotion of technology and knowledge-intensive segments. Based on these considerations, we expect that neither the illiberal nor the externally fomented growth model readjustment through state aid will serve economic upgrading. Before exploring the post-GFC state aid patterns in the four countries, the next section offers a conceptual framework for the analysis.

Growth models, industrial policy and peripheral upgrading in the EU

The growth model perspective focuses on the demand-side drivers of economic growth and the underpinning business-state coalitions that create flexible yet stable varieties of growth regimes (Baccaro and Pontusson, 2016; Blyth et al., 2022). The growth model of the EU’s Southern periphery rests on domestic consumption, which was financed from cheap external credit flowing from the North to the South causing rising household and state debt (Johnston and Regan, 2018; Pérez, 2019). However, when the flow of cheap credit halted in 2008, the growth of the Southern countries slowed and soon they entered a deep recession arising from the unfolding sovereign debt crisis.

Before the crisis, Eurozone membership had facilitated the thriving of the consumption-oriented models based on fiscal expansion and foreign borrowing, but after the GFC this became unviable. The new, post-GFC rules of the European Monetary Union (EMU) required strong fiscal discipline from the members and delegated strengthened fiscal surveillance powers to the European Commission. The EU (together with the ECB and the IMF) echoed the demands of the creditors and urged the Southern members to conduct pro-cyclical fiscal consolidation involving austerity measures and structural reforms, including internal devaluation by adjusting wages downward (Pérez and Matsaganis, 2018, 2019). According to Vukov (2021), the Southern countries were affected by the toxic mixture of debt- and consumption-led growth suppressed by the increasing fiscal constraints of the EU’s economic governance regulations.

The growth model of the Eastern, FDI-led economies relies on the inflow of foreign direct investment, particularly in export-oriented complex manufacturing (Bohle and Greskovits, 2012). Typically, foreign investors take advantage of the availability of cheap, skilled labour in the region and keep high value-added activities in their home countries (Nölke and Vliegenthart, 2009). Because of the limited domestic innovation potential and high dependency on foreign capital, several scholars concluded that these FDI-led, export-oriented growth models have reached their limits (Galgóczi and Drahokoupil, 2017; Szent-Iványi, 2017) and without a major shift towards high value-added activities, the region may fall into the middle-income trap (Győrffy, 2022; Myant, 2018). In our view, the limits of this model are yet far, because the region continues to attract foreign capital. However, its limited upgrading potential is a relevant critique of this growth model.

Overall, both the East and the South are dependent on foreign capital. In the South, the decline in export competitiveness in the 1990s was compensated with an unsustainable boom in debt-driven consumption, which shifted economic activity towards finance, construction and real estate (Nölke, 2016). In the East, FDI reinforced the industrial base in the low value-added segments (Bohle and Greskovits, 2012). Consequently, both semi-peripheries face upgrading challenges and need a structural shift towards high value-added activities, which requires an active industrial policy from the state.

However, the comparative capitalism literature remained silent about industrial policy despite its increasing significance in the post-GFC context (Bulfone, 2022). After the crisis, the issue of industrial policy in the EU emerged as a debate between liberal solutions and developmentalist interventions calling for a more active involvement of the state in the economy. Scholars contend that neoliberal ideas have remained dominant in the EU (Schmidt and Thatcher, 2013) and the same old policies are applied without a considerable shift in industrial policy practices (Szalavetz, 2015). Yet, growing concerns about the failure of the market in addressing competitiveness, de-industrialisation, and rising inequality (AA Ambroziak, 2017; Bailey et al., 2011; Mazzucato et al., 2015) triggered EU institutions to argue for strengthened, better targeted and more integrated industrial policies (European Commission, 2010; European Council, 2019).

This leads to the discussion on how European integration influences development in the core and (semi)periphery and what policy space it allows the members for taking autonomous developmental actions. The literature shares the view that European integration has produced a differentiated impact on the East and the South with some convergence experienced primarily in metropolitan regions, but, after the crisis, this limited convergence has stopped or slowed down and the gap between the EU core and periphery have been rising (Rhodes et al., 2019). Some also argue that the EU has proved unable to address and manage its growing internal heterogeneity (Höpner and Schäfer, 2012), while its regulatory rules heavily constrain member states’ policy space (Clift and Woll, 2012; Jabko, 2006).

Bruszt and Langbein (2020) challenge this view of the EU as a ‘straightjacket’ on member states and argue that European regulations offer new opportunities and resources for members to shape their own developmental trajectories. For instance, EU state aid rules provide an opportunity to promote economic upgrading in the EU’s periphery because higher regional aid intensities are allowed in areas that are more backward relative to the EU average. In this respect, the Eastern and Southern members offer an excellent context to examine how the interaction between European rules and domestic developmental agency affect developmental outcomes in less advanced members.

Although the provision of state aid may be distortive in the EU’s single market (Botta, 2016), the EU Treaties allow for the granting of aid when the market fails to deliver certain economic, social or environmental objectives. In line with Bruszt and Langbein (2020), we thus argue that European state aid rules offer market-correcting legal tools to member states to the extent that those states comply with the EU’s fiscal regulations. This is the reason why Eurozone members, particularly those with a debt-driven, consumption-oriented growth model face greater limitations in state aid spending than export-oriented economies outside the eurozone.

The European Commission, which bears an exclusive mandate to determine legal and unlawful state aid, considers sectoral aid as the most distortive type, while endorses horizontal aid such as aid for training, SMEs, regional development, or R&D. By the end of the 1990s, the growing number of state aid cases undermined the Commission’s ability to focus on the most distortive aid measures (Doleys, 2013). Facing these limitations, the Commission responded by introducing the so-called general block exemptions regulations (GBER), which promote horizontal aid that does not require prior notification by the member states (Aydin, 2014). The scope of GBER kept expanding in the 2000s (Heimler, 2018), which involved the policy’s gradual decentralisation by dispersing more responsibility to the national administrations.

Moreover, the introduction and gradual extension of block exemptions redirected state aid from sectoral to horizontal grants (Volberding, 2021). This is because the block exemptions, which before the coronavirus pandemic constituted more than 90% of new aid measures (Colombo, 2019), pose a strong incentive for member states to spend on ‘good’, less distortive aid instead of sectoral support. The broadening scope of block exemptions has considerably increased central governments’ policy space and placed greater responsibility in their hands to comply with the state aid regulations. Adopting horizontal aid schemes under block exemptions instead of offering sectoral or individual aid to businesses involves looser Commission scrutiny. At the same time, block exemptions may also contribute to the fragmentation of the single market along core-periphery dimensions because wealthier members can distribute much greater amounts of aid than the less affluent ones. Because of their drained post-crisis public budget, the Southern countries’ fiscal capacity to take advantage of the increased policy space remains behind that of the ECE countries. Thus, the expansion of block exemptions may indirectly favour the growth model readjustment of the single market ‘compatible’ export-led ECE model rather than the consumption-led one.

Having established the conceptual framework of this study, the next section introduces the challenges that the four countries face in economic upgrading and their state aid practices in the post-GFC context.

Challenges to economic upgrading and post-crisis state aid practices in the two semi-peripheries

Comparison of the Eastern and Southern growth models.

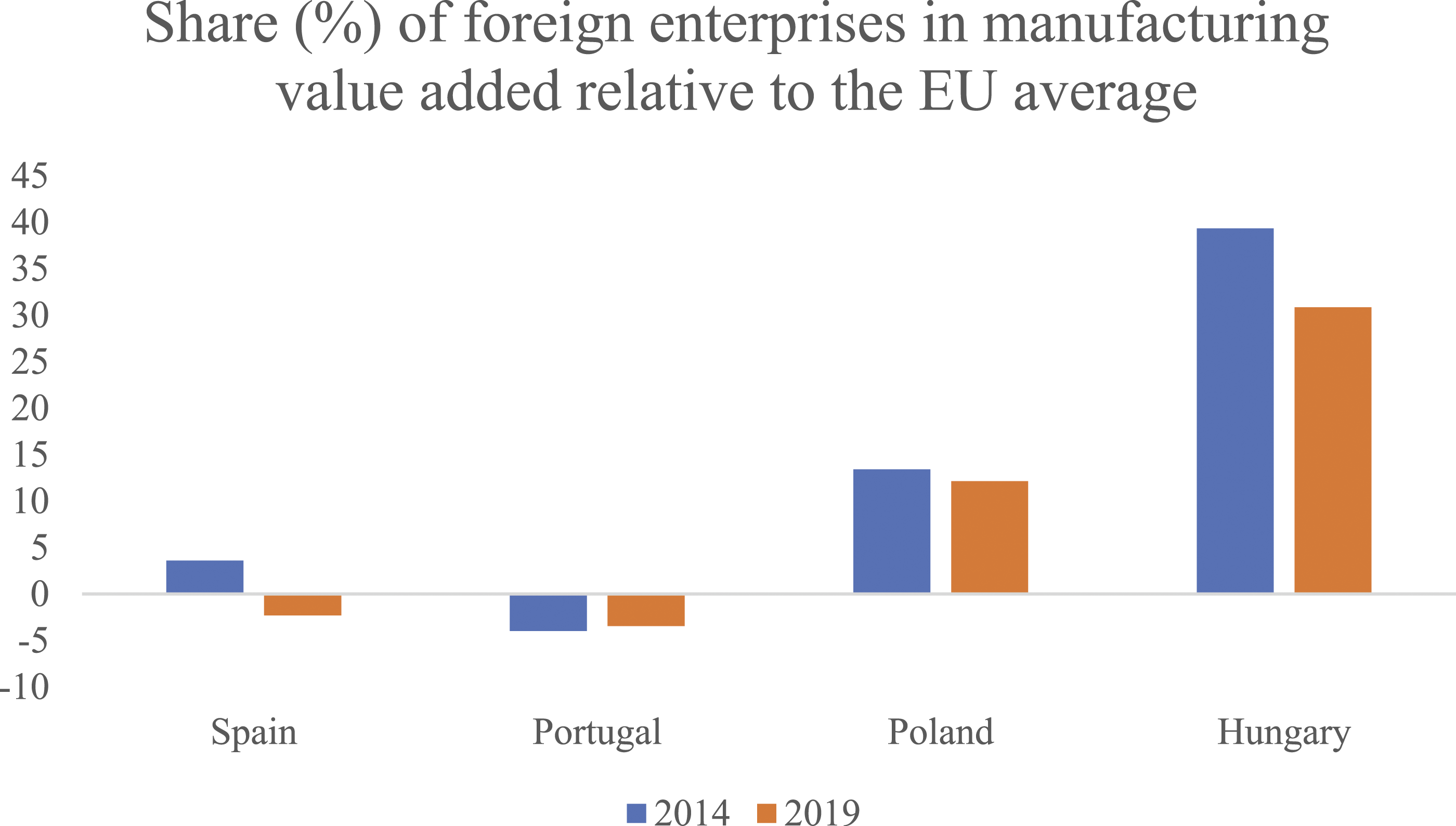

However, the industrial dynamics over the last two decades reveal sharp differences and diverging trends between the two semi-peripheries. The industrial sector in Poland and Hungary has a greater and growing economic role than in the Iberian countries that have experienced deindustrialisation, which began before the GFC (see Figure 2 and Table A in the annex). The industry value added, and manufacturing value added from GDP fell below the EU average in Portugal and Spain whereas they rose above the EU average in Hungary and Poland. Consistent with their growth model, the role of foreign enterprises in manufacturing value added increased far above the EU average in Hungary and Poland but remained below that in Portugal and Spain (Figure 3). The share of industrial employment and the share of manufacturing exports from total exports also declined below the EU average in the Southern countries, unlike in the East (Figure 2). These figures confirm that the Eastern growth models have become more industry-based and much more export competitive than the Southern ones. This is also why upgrading the Iberian industry has produced limited success so far (European Commission, 2020, Šćepanović, 2020). Developments in the industrial sector in the four countries relative to the EU-average.Note: EU average = 0. The bar charts reveal the percentage point difference between the national values and the EU average. * Industry including mining, construction, electricity, water, gas.Source: authors’ calculation based on World Bank, World Development Indicators, Eurostat small business (SBS) and foreign affiliates (fats) statistics. Share (%) of foreign enterprises in manufacturing value added relative to the EU average (2014 and 2019).Note. EU average = 0. The bar chart reveals the percentage point difference between the national values and the EU average.

The above dynamics are partly the consequence of the EU’s Eastern enlargement, which caused a shift in European manufacturing activity and production chains from the Southern EU members towards Central Europe. Poland and Hungary have become important members of the ‘Central European manufacturing core’ (Stehrer and Stöllinger, 2015) that has been formed with the leadership of Germany organising the region’s production networks and integrating them into the global value chains (GVCs) (Pavlínek, 2017). GVC participation in these countries is greater than in the Southern countries and their dependence on foreign capital and technologies has been persistent (Grodzicki and Geodecki, 2016; Kersan-Skabić, 2017). Ambroziak (2018) also revealed that a large part of Central European exports to Germany are intermediates and re-exported to other countries (to Asia for example), indicating that intra-GVC trade is really global. Although the Eastern growth models have contributed to the economic catch-up of these countries, the low domestic value capture limits the possibilities of upgrading (Szalavetz, 2017). Both Poland and Hungary function mostly at the bottom part of the so-called ‘smile curve’ that reflects functional specialisation in the low value-added segments (Stöllinger, 2021).

In the South, parallel to the decline in their industry, the domestically owned service sector has become dominant. While in Spain several giant domestic companies operate mostly in the banking, utilities, retail and construction sector, the Portuguese economy is characterised by a high share of labour-intensive, low-technology, low value-added, non-tradable and/or non-market activities (Mamede, 2017). Besides, the tourism sector has gained great significance in these countries: direct and indirect tourism contributed to 12.4% of the Spanish and 8.1% of the Portuguese GDP in 2019 according to OECD data.

Having introduced the main challenges to upgrading in the two semi-peripheries, the next paragraphs explore the patterns of post-GFC state aid including individual grants and aid schemes adopted in 2014–2021 to determine how (if at all) these policies contributed to growth model readjustment and upgrading.

To obtain data on state aid, we relied on the European Commission State Aid Scoreboard and State Aid Register. The former offers aggregate data on the composition of state aid spending including the main objectives of aid, while the latter provides a comprehensive record of all individual aid and state aid schemes. 2 Because of the block exemptions, the number of individual cases has significantly declined over the past decade and now aid schemes represent the bulk of aid. Even though the data on aid schemes do not indicate the individual beneficiaries (because they no longer need to be notified to the Commission), their objectives reveal the economic purpose they serve thus it is possible to judge if they promote technology- and knowledge-intensive activities in manufacturing and services. We classified aid by the sector of the recipients or, in the case of schemes, by the stated objectives, according to technology level and knowledge intensity (see annex). First, we introduce the aggregate data on state aid spending, and the post-GFC industrial policy approaches of the four countries to contrast them with our findings based on the classification of individual aid and aid schemes.

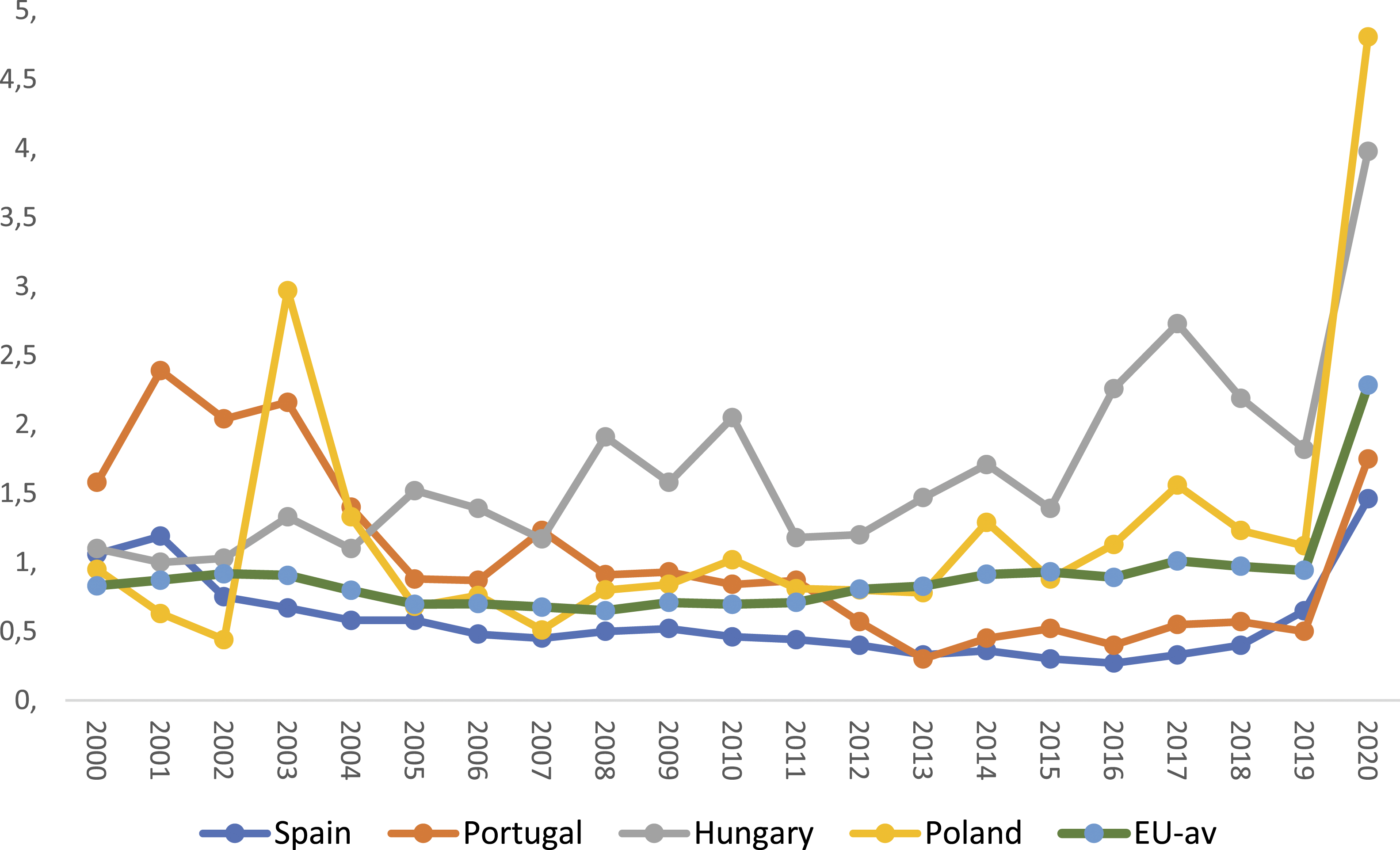

Regarding regular state aid compared to the GDP, as expected, Spanish and Portuguese figures were relatively low in Europe (below 0.5%) before the coronavirus crisis. At the same time, the Eastern countries demonstrated much higher shares (around 1–2%), mostly above the EU average before the pandemic (Figure 4). This is consistent with our expectations: the severely reduced fiscal space of the governments in the South did not allow them to initiate excessive spending on state aid, while in the East such constraints have been much less profound. Regular state aid (without financial sector aid) in percentage of the GDP.Source: State aid scoreboard data (European Commission).

The illiberal growth model readjustment in Hungary and Poland began when right-wing populist governments were elected (2010 in Hungary and 2015 in Poland). Both governments have harshly criticised the role of FDI in the domestic economies and, fuelled by economic nationalism, called for reindustrialisation and the promotion of domestic ownership at the expense of foreign firms (Varga, 2021). They motivated these moves with a developmentalist agenda, 3 aiming at improving competitiveness and upgrading the economy (Morawiecki, 2016). Both governments levied sectoral taxes on the financial and retail sector that disproportionately affected large foreign-owned businesses (Bohle and Greskovits, 2019; Vukov, 2020) and both of them launched an industrial strategy targeting high value-added industries and innovation (the Irinyi Plan in Hungary and the Strategy for Responsible Development in Poland).

However, the implementation of these plans proved to be less ambitious and more controversial. In Hungary, the government not only maintained but even increased state aid to the export-oriented, foreign-owned manufacturing sector and has been more concerned with extracting short-term rents to political cronies than promoting the competitiveness of domestic firms (Scheiring, 2021). Domestic ownership was, however, successfully promoted by the state in banking in both countries through the renationalization of several foreign-owned banks (Kozarzewski, 2021; Sebők and Simons, 2021). The Polish government also retained generous state aid for investments in foreign-dominated sectors such as automotive, aviation and biotechnology (Vukov, 2020), but paid greater attention to the promotion of high value-added activities, and took a more genuine developmentalist approach (Naczyk, 2022). Partly attributed to its generous state aid provisions, business services have become one of the fastest-growing economic segments in Poland, which, nevertheless, is mostly driven by foreign investors (Hashimoto and Wójcik, 2021).

Like the Eastern countries, the two Iberian states jumped on the post-GFC European bandwagon of reindustrialisation to stimulate their export sectors. In 2014, the Spanish Ministry of Industry published the ‘Agenda for strengthening the industrial sector’ and adopted an Industry Action Plan, which, however, remained ‘long on rhetoric but short on ambition’ (Garcia Calvo and Coulter, 2022: p. 204) mainly because of the government’s highly limited space for fiscal manoeuvre. The Spanish plan established six broad priority areas, but the measures rather aimed at streamlining processes and reducing costs instead of a general renovation, thus there was no break with institutional structures inherited from the past (Garcia Calvo and Coulter, 2022). In its new roadmap for industrial policy until 2030, the ministry admitted that the previous government plan was not successful, which is also reflected in the declining Spanish industrial performance demonstrated in Figure 2. Nevertheless, the new document does not bring any novel aspects to the policy as it still stresses the importance of the reindustrialisation of the economy and the spread of digital technologies.

In Portugal, the government targeted structural change and upgrading in the economy, similar to the Spanish ambitions. Knowing that future growth is highly dependent on generating value from exports, the Portuguese government reformed its direct business support programs and gave priority to the promotion of R&D, innovation and to sectors with high-tech content or growing international demand. Two-third of the direct support benefited the manufacturing sector, however, the majority of the subsidised businesses were active in low- and medium-tech manufacturing (Mamede, 2017) thus contributing little to economic upgrading. The post-crisis recovery of the Portuguese economy can be attributed to the strong growth in demand for tourism and the related real estate segment, however, without experiencing substantial productivity gains, which makes the economy fragile and exposed to external shocks such as the coronavirus crisis (Martins and Mamede, 2022).

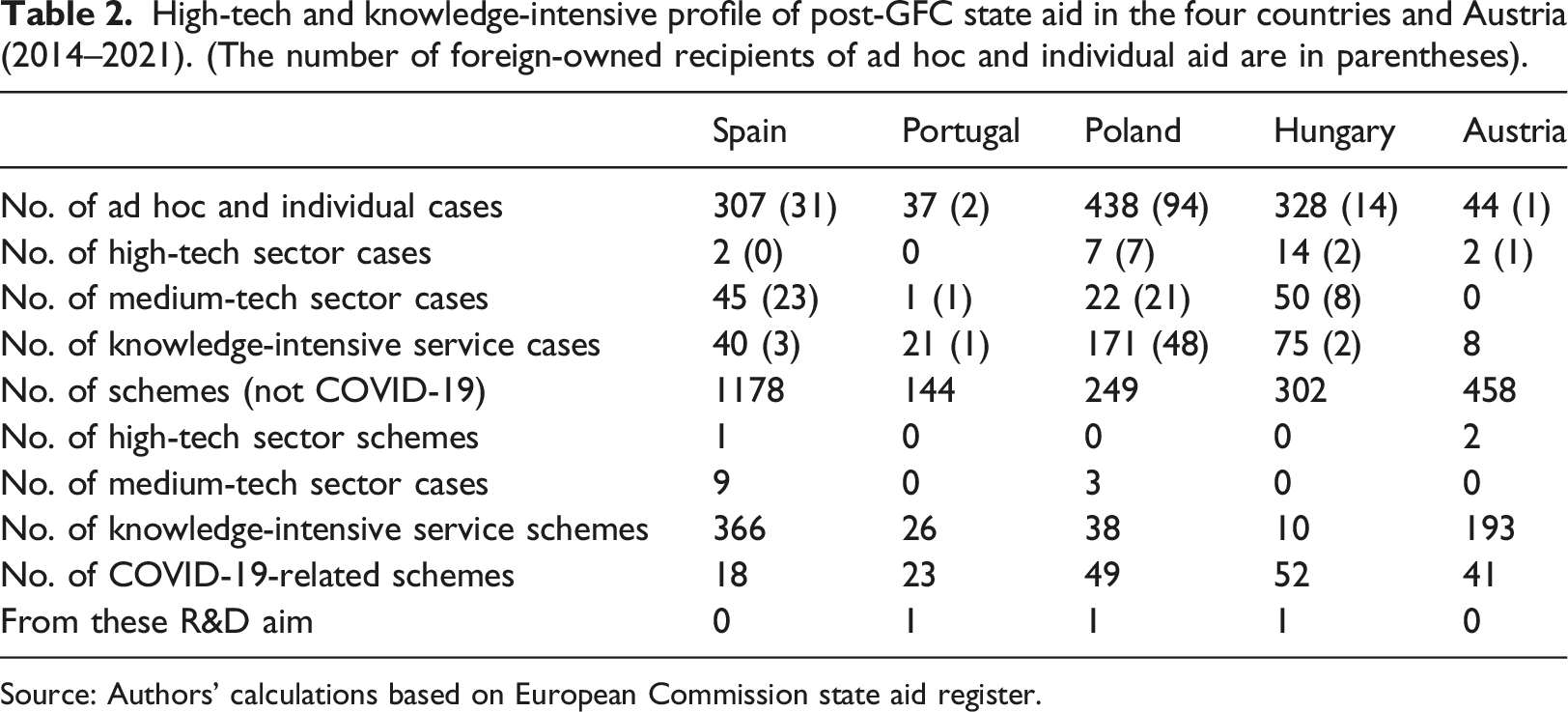

High-tech and knowledge-intensive profile of post-GFC state aid in the four countries and Austria (2014–2021). (The number of foreign-owned recipients of ad hoc and individual aid are in parentheses).

Source: Authors’ calculations based on European Commission state aid register.

The data on ad hoc and individual cases represent specific firms that have been recipients of state support. This type of aid has lost its former European significance because of the block exemptions, yet, except for Austria and Portugal, it has remained popular in the selected countries. Among the individual cases, medium, high-tech, and knowledge-intensive recipients are relatively few, even in Austria. Poland excels with the highest number of supported companies active in the knowledge-intensive segments. These Polish recipients were either foreign-owned companies offering business services, or domestic higher education institutions and academic research centres where the aid aimed to strengthen research infrastructure. In contrast, the Hungarian recipients of knowledge-intensive individual aid were almost exclusively domestic SMEs that received support for small-scale upgrading of their services. In Portugal and Spain, among the very few knowledge-intensive beneficiaries there were businesses involved in financial services, recreational and entertainment activities, sports, telecommunication and air transport.

The main recipients of aid granted to the medium-tech sectors were large foreign-owned investors active mostly in the automotive industry, such as Ford, Renault, Opel, Nissan, the PSA Group, Delphi and Michelin in Spain; Volkswagen and an aerospace manufacturer, Embraer in Portugal; Toyota, Mercedes-Benz and Samsung in Poland, to name a few. In Hungary, medium-tech grants mostly supported domestic firms. However, it would be misleading to conclude that the Hungarian government abandoned the promotion of foreign multinationals in the complex manufacturing segment because most of such aid to foreign companies is usually awarded through a dedicated scheme. 5

The ownership and sectoral composition of individual aid in the semi-periphery reflect the structural attributes of these economies. The foreign recipients were active in the medium-tech, export-oriented segments dominated by foreign companies. In the knowledge-intensive segments, Hungary and Poland were more active in granting individual aid than Spain and Portugal. Overall, except for the Polish promotion of domestic research infrastructure and foreign-owned companies in business services, the sectoral composition of individual aid does not reveal substantial shifts towards economic upgrading.

Most of the aid is distributed through aid schemes benefiting thousands of companies at the same time. One of the main limitations of our data is that the identity of the beneficiaries of the schemes is not available in the state aid register. Thus, it is not possible to determine the sectoral and ownership composition of the recipients, however, the schemes still reveal important differences between the export-led and the consumption-led countries and between the semi-periphery and the representative of the core, Austria. Nearly half of the Austrian state aid schemes targeted knowledge-intensive activities, almost exclusively promoting domestic research infrastructure and innovation, including support for digitalisation. This specific targeting of knowledge-intensive activities is missing in the semi-periphery, with the partial exception of Spain where one-third of all the schemes were dedicated to this purpose. The Spanish knowledge-intensive schemes support culture, heritage conservation, audio-visual works (108 schemes) and experimental development and industrial research (120 schemes), which suggests some notable steps towards economic upgrading, although, as mentioned, without changing so far the profile of the Spanish economy. In Portugal, most of the knowledge-intensive schemes (15 out of 26) were dedicated to financial services in the form of guarantee schemes, which is a sign of liquidity problems in this sector and, in this respect, are less forward-looking measures. Most of the Hungarian and Polish state aid schemes offer general, typically small-scale support to SMEs for human resource training and investments into production capacities without requiring high-tech or knowledge-intensive content.

Conclusion

The post-GFC period has seen the rejuvenation of industrial policy within and beyond the EU. While it may serve the development of modern, future-oriented, competitive economies, industrial policy may also become a vehicle to support nationalist and protectionist ideologies, or it can simply reinforce developmental trajectories that fail to upgrade the domestic economy. Besides the frequent calls for treating industrial policy more seriously, the effects of the crisis also questioned the past development models in the Southern and in the Eastern semi-peripheries of the EU. However, neither industrial policy nor challenges and opportunities posed by transnational regulatory integration feature prominently in the comparative capitalism literature. We therefore complemented this literature by focusing on how the two Iberian (Spain and Portugal) and two Eastern European (Hungary and Poland) governments used state aid grants and schemes in the post-GFC period to readjust their growth models by promoting more knowledge- and technology-intensive activities.

In both semi-peripheries, growth model readjustment has been burdened with several contradictions. In the East, excessive dependence on low value-added FDI has threatened with a middle-income trap, which the illiberal governments aimed to address by resorting to economic nationalism and the promotion of domestically owned businesses. In the South, the GFC and the subsequent strengthening of fiscal surveillance in the Eurozone have exposed the vulnerabilities of the consumption-led model and made it unviable in the long run. Adjusting the domestic growth models in the South towards export-orientation may therefore undermine the privileged position of the previous drivers of these economies, the domestically owned financial and real estate sectors.

The prevailing structural circumstances in both the East and the South therefore work against economic upgrading. By reviewing individual aid and state aid schemes in the two semi-peripheries, we found that proportional to their GDP, Poland and Hungary applied considerably more state aid than the Iberian countries, which were facing severe fiscal constraints throughout the observed period. Our inquiry also revealed that in both semi-peripheries foreign-owned businesses were the prime target of individual aid in the medium-tech segment, corresponding to the foreign domination in complex manufacturing. Individual aid showed a slight move towards upgrading only in Poland, as a notable share of the Polish recipients were active in knowledge-intensive services such as business consultancy, computer programming and engineering. This confirms that the Polish illiberal growth model readjustment is genuinely more developmentalist, than the much more clientelistic Hungarian approach (Naczyk, 2022; Scheiring, 2021).

The state aid schemes revealed a remarkable contrast with our control case from the European core, Austria. There the leading profile of the aid schemes supported research, innovation and digitalisation. Among the observed semi-peripheral countries, only Spain dedicated substantial attention to the support of knowledge-intensive activities. In the other three countries, the majority of the state aid schemes have mostly targeted investments of SMEs into human resources and production, or offered guarantees to the financial sector. Our findings thus bring further indirect evidence to the claim that industrial policies in the EU have so far been unable to narrow the technology gap between the core and the periphery (Pianta et al., 2020).

The structure of post-GFC and pre-pandemic state aid schemes and individual aid in the semi-periphery suggests that declared objectives and political rhetoric about economic upgrading fall far from the policy practice. Neither the illiberal growth model readjustment in the East nor the externally fomented in the South have matched the stated ambitions and, overall, they seem to have reinforced existing structural features of the domestic growth models instead of engaging in real readjustment. This may be the consequence of the structural constraints that the central governments face and the power of leading sectors and firms supportive of the original growth model. In any case, our findings suggest that the semi-peripheral countries have not fully taken advantage of the policy space offered to them by the loosening European state aid regulations. At the same time, our empirics also suggest that growth models may not be easily adjusted without a comprehensive set of policies closely involving the private actors.

While so far, the consumption-oriented Southern EU members have faced important fiscal constraints relative to the Eastern countries, the coronavirus turned the tide in this respect. The Southern countries are the prime beneficiaries of the EU’s generous Recovery and Resilience Facility (RFF), which considerably boosts their fiscal capacity in spending on structural transformation, including high value-added activities. In total, Portugal is set to receive 7.86% of its GDP from the grants and loans available through the RFF from 2021 until 2026, while the same figure for Spain is 5.77%. 6 In contrast, the Eastern states may have fallen into their own illiberal trap: although they are entitled to a comparably high support from the programme (6.16% of the Polish and 3.78% of the Hungarian GDP), because of their unresolved rule of law conflicts with the EU, as of February 2023, they have not received a single eurocent, while their public budgets have been exhausted due to the coronavirus crisis. Conversely, both in Portugal and Spain RFF pre-financing began in August 2021, thus the Iberian countries have managed to turbocharge their industrial policies with these EU grants and loans while Hungary and Poland have remained on standby.

Our findings on the post-GFC and pre-pandemic state aid are based on the patterns of the aid schemes and individual aid where the exploration of the recipients in terms of ownership and the economic sector was possible. In the case of schemes, data on the final beneficiaries is missing, which poses limitations to our inquiry. However, our empirics suggest that state aid policies face important structural economic constraints in the semi-peripheries arising from their prevailing growth models even if European policy space for pursuing autonomous industrial policy has considerably widened since the GFC. Further research into specific cases of business promotion needs to explore the mechanisms of how interactions between state and leading businesses may facilitate or hinder growth model readjustments in the semi-periphery.

Footnotes

Declaration of Conflicting Interests

The Author(s) declare(s) that there is no conflict of interest.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the National Research, Development and Innovation Office, Hungary; NKFI-135342. Gergő Medve-Bálint’s research has also been supported by the Bolyai Research Scholarship of the Hungarian Academy of Sciences.